Trading Strategies Generated Pathwise

by Functions of Market Weights

††thanks: Research supported in part by the National Science Foundation under grant NSF-DMS-14-05210.

Abstract

Almost twenty years ago, E.R. Fernholz introduced portfolio generating functions which can be used to construct a variety of portfolios, solely in the terms of the individual companies’ market weights. I. Karatzas and J. Ruf developed recently another methodology for the functional construction of portfolios, which leads to very simple conditions for strong relative arbitrage with respect to the market. In this paper, both of these notions of functional portfolio generation are generalized in a pathwise, probability-free setting; portfolio generating functions, possibly less smooth than twice-differentiable, involve the current market weights, as well as additional bounded-variation functions related to the market weights. This generalization leads to a wider class of functionally-generated portfolios than was heretofore possible, to novel methods for dealing with the “size” and “momentum” effects, and to improved conditions for outperforming the market portfolio over suitable time-horizons.

Keywords and Phrases: Stochastic portfolio theory, pathwise Itô formula, pathwise Tanaka formula, trading strategies, functional generation, regular functions, strong relative arbitrage, size effect, momentum effect.

1 Introduction

The concept of ‘functionally generated portfolios’ was introduced by Fernholz, (1999, 2002) and has been one of the essential components of stochastic portfolio theory; see Fernholz and Karatzas, (2009) for an overview. Portfolios generated by appropriate functions of the individual companies’ market weights have wealth dynamics which can be expressed solely in terms of these weights, and do not involve any stochastic integration. Constructing such portfolios does not require any statistical estimation of parameters, or any optimization. Completely observable quantities such as the current values of ‘market weights’, whose temporal evolution is modeled in terms of continuous semimartingales, are the only ingredients needed for building these portfolios. Once this structure has been discerned, the mathematics underpinning its construction involves just a simple application of Itô’s rule. Then the goal is to construct such portfolios that outperform a reference portfolio, for example, the market portfolio, under appropriate structural conditions.

Karatzas and Ruf, (2017) recently found a new way for the functional generation of trading strategies, which they call ‘additive generation’, as opposed to Fernholz’s ‘multiplicative generation’, of portfolios. This new methodology weakens the assumptions on the market model: asset prices and market weights are continuous semimartingales, and trading strategies are constructed from ‘regular’ functions of the semimartingales without the help of stochastic calculus. Trading strategies generated in this additive manner require simpler conditions for strong relative arbitrage with respect to the market over appropriate time horizons; see also Fernholz et al., (2018).

Along a different, but related, development, Föllmer, (1981) showed almost 40 years ago that certain aspects of Itô calculus can be developed ‘path by path’, without any probability structure. Once a given function admits the pathwise property of quadratic variation/covariation along a given nested sequence of partitions over a fixed time interval of finite length, this new type of Itô’s change of variable formula can be proven by an application of Taylor expansion in a surprisingly simple way. Then Wuermli, (1980) introduced in this same setting the concept of local times and the corresponding pathwise Tanaka formula, in a pathwise sense. This allows the change of variable formula to be applied to less regular functions, by involving appropriately defined pathwise local times. These concepts of local times have been further developed recently; see Perkowski and Prömel, (2015), Davis et al., (2018), and Cont and Perkowski, (2018).

In this paper, we generalize both additive and multiplicative functional generation of trading strategies in several ways. First, we use pathwise Itô calculus to show that one can construct trading strategies, generated additively or multiplicatively from a given function, depending on the market weights and in a manner completely devoid of probability considerations. The only analytic structure we impose is that the market weights admit continuous covariations in a pathwise sense. Secondly, we admit generating functions that depend on an additional argument of finite variation. Introducing new arguments, other than the market weights, gives extra flexibility in constructing portfolios; see Strong, (2014), Schied et al., (2018), Ruf and Xie, (2018). We present various types of additional such arguments, to the effect that a variety of new trading strategies can be generated from a function depending on them; these strategies yield new sufficient conditions for strong relative arbitrage with respect to the market portfolio. Then, we show how to apply the pathwise Tanaka formula to construct portfolios from generating functions rougher than heretofore possible. In order to use the Itô formula, a function needs to be at least twice-differentiable, whereas the Tanaka formula requires less smooth functions, namely, absolutely continuous. Thus, usage of the Tanaka formula broadens the class of portfolio-generating functions very considerably.

We also present new sufficient conditions for strong relative arbitrage via additively and multiplicatively generated trading strategies. The existing sufficient condition in Karatzas and Ruf, (2017) requires the generating function to be ‘Lyapunov’, or the corresponding ‘Gamma function’ to be nondecreasing. By contrast, the new sufficient conditions in this paper depend on the intrinsic nondecreasing structure of the generating function itself. This new condition shows that trading strategies outperforming the market portfolio can be generated from a much richer collection of functions depending on the market weights and on an additional argument of finite variation. We provide some interesting examples of such trading strategies, and empirical analysis of them.

Preview : Section 2 presents the elements of the pathwise Itô calculus that will be needed for our purposes. Section 3 defines trading strategies and regular functions, then discusses how to generate trading strategies from regular functions in ways both additive and multiplicative. Section 4 gives sufficient conditions for such trading strategies to generate strong relative arbitrage with respect to the market. Section 5 shows methods of generating trading strategies in a similar manner as in Section 3, but from less smoother functions with help of relevant notion of local time and Tanaka formula. Section 6 gives some examples of trading strategies generated from entropic functions and corresponding sufficient conditions for strong arbitrage. Section 7 contains empirical results of portfolios discussed in Section 6. Finally, Section 8 concludes.

2 Pathwise Itô calculus

In what follows, we let be a -valued continuous function, representing a -dimensional vector of assets whose values change over time. Each component is defined on , for a fixed , and stands for the value of the th asset at time .

We require the components of to admit continuous covariations in the pathwise sense with respect to a given, refining sequence of partitions of . The sequence is such that each partition is of the form for , as well as , and the mesh size decreases to zero as . We fix such a sequence of partitions for the remainder of the paper.

Here and below, the notation means that and are consecutive points in the partition , i.e., , . Also, when we write and simultaneously, we set when is the biggest index satisfying . With this notation, we present the notion of the pathwise quadratic covariation of along , as follows.

Definition 2.1.

A continuous function is said to have a pathwise quadratic covariation along a given nested sequence of partitions of , if the limit of the sequence

| (2.1) |

exists for any as and the resulting mapping, denoted by , is real-valued and continuous for every . We call the pathwise quadratic covariation of and , and define the pathwise quadratic variation of by as usual.

We stress that the existence of pathwise covariations and quadratic variations for the components of depends heavily on the choice of the nested, or “refining” sequence of partitions. Example 5.3.2 in Cont, (2016), and the arguments following, illustrate this fact. We note also that the existence of pathwise covariations and quadratic variations is required for Itô’s formula to hold in a pathwise sense.

Next, we state the original one-dimensional pathwise Itô formula, introduced by Föllmer, (1981).

Theorem 2.2 (Pathwise Itô formula for paths with quadratic variation, Föllmer, (1981)).

Fix a continuous function which admits the quadratic variation along the given nested sequence of partitions of . Then for every function , the pathwise change of variable formula

| (2.2) |

holds for . Here, the Föllmer-Itô integral is defined as the pointwise limit

| (2.3) |

and the last integral of the right-hand side of (2.2) is Lebesgue-Stieltjes integral.

We will need also the pathwise Itô formula in a higher-dimensional setting than Theorem 2.2, and with an extra ‘input’ as additional argument. For this purpose, we let be an additional vector function of finite variation and consider a -dimensional function of time . We say that a given function is in , if it is -times continuously differentiable with respect to the first components and -times continuously differentiable to the last components. We also denote by the th partial derivative, and by the th partial derivative of .

We now present the following version of the pathwise Itô formula involving both and . The proof is given in the Appendix, and the idea of proof is the same as that of Föllmer’s original Theorem.

Theorem 2.3 (Multidimensional pathwise Itô formula).

Fix a -dimensional continuous function having pathwise quadratic covariations along a given sequence of partitions of , and an -dimensional continuous function of finite variation defined on . Then for every , the pathwise change of variable formula

| (2.4) |

holds for . Here the Föllmer-Itô integral is defined as the pointwise limit

| (2.5) |

whereas the other integrals of the right-hand side of (2.4) are Lebesgue-Stieltjes integrals.

3 Trading strategies generated in pathwise sense

As in the previous section, we consider a -valued, continuous function which admits continuous covariations with respect to a refining sequence of partitions of ; we also let be an additional vector function of finite variation. For the purposes of this section, the components of will denote the value processes of tradable assets, and eventually stand for the market weights in an equity market. At the same time, the components of will model the evolution of an observable, but non-tradable, quantity related to these market weights.

For a subset of a Euclidean space, we denote by the space of continuous -valued functions defined on ; whereas stands for the space of those functions in which are of bounded variation. With this notation, we have the following definition of trading strategy with respect to the pair , in the manner of Karatzas and Ruf, (2017).

Definition 3.1 (Trading strategies).

For the pair of a -dimensional function and an -dimensional function , suppose that is a -dimensional function with representation

| (3.1) |

Here, is a vector of functions, for which we can define an integral with respect to ; we write , to express this. We shall say that is a trading strategy with respect to , if it is ‘self-financed’ in the sense that

| (3.2) |

holds. In (3.2) and in what follows,

| (3.3) |

denotes the value process of the strategy at time .

The interpretation is that stands for the “number of shares” invested in asset at time . If is the price of this asset, then is the dollar amount invested in asset at time , and the total value of investment across all assets. “Self-financing” means that there are neither infusions nor withdrawals of capital: gains are re-invested, losses have to be absorbed. We shall write instead of whenever the integrator is fixed and apparent from the context.

The preceding pathwise Itô formula in Theorem 2.3 suggests that integrands of the special form , for some function , play a very important role for integrators that admit finite quadratic covariations , along an appropriate nested sequence of partitions. This gives rise to the following definition.

Definition 3.2 (Admissible trading strategy).

Let be a -dimensional function in , and an -dimensional function in . A -dimensional trading strategy in is called admissible trading strategy for the pair , if there exists a function in the space , such that (3.1) holds for ; that is,

| (3.4) |

If is an admissible trading strategy for , the last integral of (3.2) above is interpreted as a pathwise Föllmer-Itô integral in the context of Theorem 2.3. In an what follows, we will define a regular function for the pair , consisting of a -dimensional continuous function , and an -dimensional function in .

Definition 3.3 (Regular function).

We say that a function in is regular for the pair , consisting of a -dimensional continuous function and of a function , if the continuous function

| (3.5) |

has finite variation on compact intervals of .

Remark 3.4.

In order to define a pathwise Föllmer-Itô integral and be able to use the pathwise Itô calculus, we need a sufficiently smooth (in general, at least ) function , and an integrand which can be cast in the form of a derivative of this function in the manner of (3.4). Thus, thanks to the above definition, we can always apply the pathwise Itô formula (Theorem 2.3) to the function as in Definition 3.3 above, and obtain another expression for the so-called “Gamma function” in (3.5); namely,

| (3.6) |

Here we recall that and are, respectively, the first-order th partial derivative and the second-order th partial derivative of at .

The difference in Definition 3.3 here, with Definition 3.1 of Karatzas and Ruf, (2017), should be noted and stressed. In Karatzas and Ruf, (2017), the integrand need not be the form of ‘gradient’ of a regular function . Here, the special structure of (3.4) for the integrand is necessary; this is the “price one has to pay” for being able to work in a pathwise, probability-free setting, without having to invoke the theory of rough paths.

3.1 Trading strategies depending on the market weights

We place ourselves from now onward in a frictionless equity market with a fixed number of companies. We also consider a vector of continuous functions , where represents the capitalization of the company at time . Here we take and allow to vanish at some time , for all ; but we assume also that the total capitalization does not vanish at any time .

With these ingredients, we define another vector of continuous functions that consists of the companies’ relative market weights

| (3.7) |

We also assume that the components of admit finite quadratic covariations , along a given, fixed, nested sequence of partitions of , in the manner discussed at the start of Section 2. In what follows, we will consider only regular functions of the form which depend on the vector of market weights and on some additional function . Examples of such functions appear in (4.3), (4.4).

3.2 Additively generated trading strategies

We would like now to introduce an additively-generated trading strategy, starting from a regular function in the pathwise sense. For this, we will need a result from Karatzas and Ruf, (2017). For any given function which is regular for the pair , where is the vector of market weights and an appropriate function in , we consider the vector with components

| (3.8) |

as in (3.4) of the Definition 3.2, and the vector of functions with components

| (3.9) |

Here,

| (3.10) |

is the “defect of self-financibility” at time of the integrand in (3.8), the “value” of the strategy at time in the manner of (3.3), and

| (3.11) |

the “defect of balance” at time for the regular function . By analogy with Proposition 2.3 of Karatzas and Ruf, (2017), the vector of (3.9), (3.8) defines a trading strategy with respect to .

Definition 3.5 (Additive generation).

Proposition 3.6.

Proof.

The proof is exactly the same as that of Proposition 4.3 of Karatzas and Ruf, (2017), if we change , there, into , in our present context. ∎

The decomposition (3.12) suggests, that we can think of in (3.5), (3.6), as expressing the “cumulative earnings” of the strategy of (3.9), around the “baseline” .

Remark 3.7.

- (i)

- (ii)

3.3 Multiplicatively generated trading strategies

Next, we introduce the notion of multiplicatively generated trading strategy. We suppose that a function is regular as in Definition 3.3 for the pair , where is the vector of market weights and is some additional function in , and that the scalar function is locally bounded. This holds, for example, if is bounded away from zero. We consider the vector function defined by

| (3.17) |

in the notation of (3.5), (3.8) for . The integral here is well-defined, as is assumed to be locally bounded. Moreover, we have , since from Definition 3.1, and the exponential term is again a locally bounded function. As before, we turn this into a trading strategy by setting

| (3.18) |

in the manner of (3.9), and with , defined as in (3.10) and (3.11).

Definition 3.8 (Multiplicative generation).

Proposition 3.9.

Consider the trading strategy , generated as in (3.18) by a given function which is regular for . This pair consists of the vector of market weights, and of a suitable function such that is locally bounded.

The value generated by this strategy is given by

| (3.19) |

in the notation of (3.5). This strategy can be represented for in the form

| (3.20) |

Proof.

We follow the argument in Proposition 4.8 of Karatzas and Ruf, (2017), using the pathwise Itô formula instead of the standard Itô formula for semimartingales. With the notation

in (3.19), the pathwise Itô formula (Theorem 2.3) yields

Here, the second equality uses the expression in (3.6), and the last equality relies on Proposition 2.3 of Karatzas and Ruf, (2017). Since (3.19) holds at time zero, it follows that (3.19) holds at any time . The justification for (3.20) is exactly the same as that of Proposition 4.8 in Karatzas and Ruf, (2017). ∎

Remark 3.10.

- (i)

- (ii)

4 Sufficient conditions for strong relative arbitrage

We consider the vector of market weights as in (3.7). For a given trading strategy with respect to the market weights , let us recall the value process from Definition 3.1. For some fixed , we say that is strong relative arbitrage with respect to the market over the time-horizon , if we have

| (4.1) |

along with

| (4.2) |

Remark 4.1.

The notion of strong relative arbitrage defined above does not depend on any probability measure, and is slightly stricter than the existing definition of strong relative arbitrage. The classical definition involves an underlying filtered probability space, and posits that the market weights should be continuous, adapted stochastic processes on this space. Also, there are two types of classical arbitrage; relative arbitrage and ‘strong’ relative arbitrage as in Definition 4.1 of Fernholz et al., (2018). In this old definition, an underlying probability measure is essential in defining this ‘weak’ version of relative arbitrage. However, if we posit that be strong relative arbitrage when (4.2) holds for ‘every’ realization of , instead of ‘almost sure’ realization of , the notion of strong relative arbitrage can be established without referring to any probability structure. Since we constructed trading strategies in a pathwise, probability-free setting, the ‘strong’ version of relative arbitrage is here a more appropriate concept of arbitrage, and we adopt the above strict definition from now on.

The value process of a trading strategy generated functionally, either additively or multiplicatively, admits a quite simple representation in terms of the generating function and the derived Gamma function as in (3.12) and (3.19). This simple representation provides in turn nice sufficient conditions for strong relative arbitrage with respect to the market; for example, as in Theorem 5.1 and Theorem 5.2 of Karatzas and Ruf, (2017). In this section, we find such conditions on trading strategies generated by a regular function , which depends not only on the vector of market weights , but also on an additional finite-variation process related to . We also give new sufficient conditions leading to strong relative arbitrage for both additively and multiplicatively generated trading strategies, which is different from Theorem 5.1 and Theorem 5.2 of Karatzas and Ruf, (2017).

Until now, we have not specified the -dimensional function , so it is time to consider some plausible candidates for this function of finite variation. A first suitable candidate would be the -dimensional vector

| (4.3) |

of quadratic variation of market weights. We can also think about a more general candidate; namely, the -valued covariation process of market weights. Here, is the notation for symmetric positive matrices, and we will use double bracket to distinguish this -dimensional vector from (4.3): namely,

| (4.4) |

The advantage of choosing as in (4.4), is that we can match the integrators of the two integrals in (3.6), and the resulting expression for can then be cast as one integral.

There are many other functions of finite variation which can be candidates for the process . We list some examples below:

-

1.

The moving average of defined by

-

2.

The running maximum of the market weights with the components , and the running minimum of the market weights with the components for .

-

3.

The ‘pathwise local time’ of at the origin, for , which is defined in Section 5. We call this process the “collision local time” of order (the number of particles involved in the collison), for the ranked market weights

Since the vectors , and , defined above, are -dimensional, holds for these choices of . For the choice of -dimensional vector with the components , the dimension of is . Empirical results using the moving average can be found in Section 3 of Schied et al., (2018). The collision local times always appear when we deal with function of ranked market weights, as in Example 3.9 of Karatzas and Ruf, (2017).

We first consider conditions leading to strong relative arbitrage with respect to the market with general as the third input of generating function . Then we present some examples of with specific finite variation function chosen from among the above candidates, and continue with empirical results regarding these examples.

4.1 Additively generated strong relative arbitrage

We start with a condition leading to additively generated strong arbitrage, which is similar to Theorem 5.1 of Karatzas and Ruf, (2017).

Theorem 4.2 (Additively generated strong relative arbitrage when is nondecreasing).

Fix a function which is regular for the pair , and such that the function in (3.5) or (3.6) is nondecreasing. Here, is the vector of market weights and is some -dimensional function in , as before.

For some real number , suppose that

| (4.5) |

holds. Then the trading strategy , additively generated by the regular function as in Definition 3.5, is strong arbitrage relative to the market over every time horizon with .

Proof.

Since is nondecreasing, we obtain for every from (3.12). We also have for all . The last equality holds because . ∎

Remark 4.3.

If we choose as in (4.4), then from (3.6), the function is nondecreasing when

is nondecreasing. Here, denotes the first-order partial derivative operator with respect to the th entry of . Also, we substitute from (4.4), (3.6) into (4.5) to obtain the more explicit form

| (4.6) |

of the condition (4.5) for strong relative arbitrage. Thus, unlike the situation of Theorem 3.7 in Karatzas and Ruf, (2017), we can have a nondecreasing and a chance for effecting strong relative arbitrage, even without the ‘concavity’ of in .

Remark 4.4.

Let us assume that the arguments and are ‘additively separated’ in the function . By this we mean, that there exist two regular functions and with the property that depends only on and depends on , and such that

| (4.7) |

holds. Then, we get and . Substituting these expressions into (3.6), we obtain

| (4.8) |

and, from (3.12) of Proposition 3.6, the relative value process of the additively generated trading strategy by can be expressed as

| (4.9) |

After substituting (4.8), (4.9) into (4.2) and rearranging terms in such a manner that the left-hand side contains only terms involving , the strong arbitrage condition (4.2) takes the form

| (4.10) |

where

When we apply the pathwise Itô formula of Theorem 2.3 to the function , the right-hand side of the above expression vanishes. Hence, the requirement (4.10) becomes

and we are in very similar situation as in Theorem 5.1 of Karatzas and Ruf, (2017).

To be more precise, if takes non-negative values and is a ‘Lyapunov function’ for the vector of market weights, in the sense that is nondecreasing, then the requirement ensures strong relative arbitrage over every time-horizon with as in Theorem 5.1 of Karatzas and Ruf, (2017). Thus, in this ‘separated’ case, we cannot achieve more than the result in Theorem 5.1 of Karatzas and Ruf, (2017), as all terms on the right-hand side of (4.10) that involve vanish. This is because when we generate additively the trading strategy in (3.9) from a regular function , only the partial derivatives of with respect to the market weights in (3.8) are involved in , and this makes the term in (4.7) meaningless in generating . Therefore, to be able to find new sufficient conditions for strong relative arbitrage, we need forms of more sophisticated than (4.7). All the examples of we develop in this paper from now onwards, are of those more elaborate forms.

From (3.12), the value at time of the additively generated trading strategy with respect to the market, has two additive components, and . In Theorem 4.2, we derived the strong arbitrage condition from the “nondecreasing property” of , but there is no reason to differentiate between and . If the mapping is nondecreasing, it is possible derive a strong arbitrage condition like Theorem 4.2, switching the role of and . However, it is difficult to find functions which are monotone in , because must depend on the market weights and these fluctuate all the time. Thus, we have to ‘extract a nondecreasing structure’ from the generating function , and use this nondecreasing structure instead of to derive a new strong arbitrage condition. This is done as follows.

Theorem 4.5 (Additively generated strong relative arbitrage when admits a lower bound).

Fix a regular function for the pair , where is the vector of market weights and is an -dimensional function in , such that the following conditions are satisfied:

- (i)

-

(ii)

there exists a function satisfying for all and the mapping is nondecreasing;

-

(iii)

holds by some constant .

For some real number , suppose that

| (4.11) |

holds. Then the additively generated strategy of Definition 3.5 is strong arbitrage relative to the market over every time horizon with .

Proof.

In Theorem 4.5, the function can be seen as the ‘extracted nondecreasing structure’ of . This result states that the generating function can lead to strong arbitrage relative to the market without necessarily being “Lyapunov”, as in Theorem 5.1 of Karatzas and Ruf, (2017). There can be strong relative arbitrage even if is nonincreasing. This is intuitively plausible already on the basis of the representation (3.12) when grows faster than decays. Some applications of Theorem 4.5 will appear in Section 6 (Example 6.4 and Example 6.6).

4.2 Multiplicatively generated strong relative arbitrage

In this subsection, in order to simplify the arguments, we assume that the regular function takes only nonnegative values and satisfies . This normalization can be achieved by replacing by if , or by if . Though we shall not use in later sections the following result, which comes from Theorem 5.2 of Karatzas and Ruf, (2017), we state here for completeness.

Theorem 4.6 (Multiplicatively generated strong relative arbitrage).

Let us fix a regular function for the pair with the market weights and some -dimensional function . For some real number , suppose that there exists an satisfying

| (4.12) |

Then, there exists a constant such that the trading strategy , multiplicatively generated by the regular function

as in Definition 3.8, is strong arbitrage relative to the market over the time-horizon ; as well as over every time-horizon with , if is nondecreasing.

In Theorem 4.6, we had to construct the “shifted” function , which was useful but also rather extraneous. However, for functions which are bounded from below and above, we have the following novel condition leading to multiplicatively generated strong arbitrage.

Theorem 4.7 (Multiplicatively generated strong relative arbitrage when is nondecreasing).

Let us fix a function which is regular for the pair with the market weights and some -dimensional function , and satisfies the following conditions:

-

(i)

is bounded away from zero and infinity, i.e., there exist positive constants such that ;

-

(ii)

is nondecreasing.

For some real number , suppose that

| (4.13) |

holds. Then, the multiplicatively generated strategy of Definition 3.8 is strong arbitrage relative to the market over every time-horizon with .

Proof.

Remark 4.8.

Since the market weights , and the continuous function are bounded on the compact interval , a regular function depending on the pair is also bounded. Thus, the condition (i) in Theorem 4.7 just requires that the lower bound should be strictly bigger than . Also, in (4.13), finding tighter bounds , of yields smaller satisfying the arbitrage condition (4.13). See Remark 6.2 for further discussion regarding the bounds on in the case of specific entropy function.

The conditions of Theorem 4.7 resemble those of Theorem 4.2. We also have the following formulation, which is similar to Theorem 4.5.

Theorem 4.9 (Multiplicatively generated strong relative arbitrage when is nonincreasing).

Fix a regular function for the pair , where is the vector of market weights and an -dimensional function in , such that the following conditions hold:

-

(i)

there exists a function satisfying for all , and the mapping is nondecreasing;

-

(ii)

is nonincreasing and holds by some positive constant .

For some real number , suppose that

| (4.14) |

holds. Then the multiplicatively generated strategy of Definition 3.8 is strong arbitrage relative to the market over every time horizon with .

Proof.

The following example provides a condition for strong relative arbitrage more general than Example 5.5 of Karatzas and Ruf, (2017), by involving an additional function into the generating function . We specifically use , the vector consisting of the running maxima of the market weights

Example 4.10 (Quadratic function).

For fixed constant and , consider the following function

This is the same as in Example 5.5 of Karatzas and Ruf, (2017) except for the last term. Note that takes values in the interval . After some straightforward computation of partial derivatives, we have

for , and using these expressions along with (3.6), we obtain

As is nondecreasing and , the integral term is always non-negative and nondecreasing in , which makes nondecreasing and non-negative. Also, using the property that the nondecreasing process is flat off the set , we have

thus also

Since , let us consider the case from now on. Using the same argument as in the proof of Theorem 4.2, the condition

| (4.15) |

where

yields a strategy which is strong relative arbitrage with respect to the market on . If we compare the condition (4.15) with the condition

| (4.16) |

that is, (5.4) of Example 5.5 in Karatzas and Ruf, (2017), there is a trade-off between the left- and the right-hand sides. The presence of the extra nondecreasing term in (4.15), guarantees that its left-hand side grows faster than the left-hand side of (4.16), as increases; but we also have a bigger constant on the right-hand side of (4.15), namely,

Thus, by choosing the value of wisely, we can obtain bounds for the times for which there is strong relative arbitrage with respect to the market over , better than those of Example 5.5 in Karatzas and Ruf, (2017).

5 Tanaka’s formula for constructing trading strategies

In the previous sections, we used the pathwise Itô formula (Theorem 2.3), instead of the usual Itô formula for semimartingales, to construct trading strategies in a pathwise manner. In this section, we generalize Stochastic Portfolio Theory (SPT) in a different direction: we apply the pathwise Tanaka formula (Generalized Itô’s formula) with appropriately defined local time, in building up trading strategies. The Itô formula requires the existence of a second derivative, whereas the Tanaka formula is applicable to ‘weakly differentiable’ functions; this broadens the class of functions from which we generate trading strategies. First, we develop some definitions and notation, and introduce the pathwise Tanaka formula. Then, we construct trading strategies generated additively and multiplicatively, and in a manner similar to that of Section 3, but from generating functions less smooth than those used there. Finally, relevant strong relative arbitrage conditions and some examples follow.

5.1 Pathwise local time and Tanaka formula

We fix a refining sequence of partitions of the interval , whose mesh size goes to zero as , as in the introduction of Section 2. We also consider an -valued continuous function defined on the compact interval , thought of here as representing a value of an individual asset which fluctuates over time. With these ingredients, we present the measure-theoretic notion of quadratic variation of along .

Definition 5.1.

A continuous function is said to have finite quadratic variation along a given sequence of partitions of , if the mesh size

| (5.1) |

goes to zero and the sequence of measures

converges vaguely to a locally finite measure without atoms as , where denotes the Dirac measure at . We write for the collection of all continuous functions having quadratic variation along . We call for , the quadratic variation of .

For a sequence of measures on , vague convergence is equivalent to the pointwise convergence of their cumulative distribution functions at all continuity points of the limiting function. If the limiting distribution function is continuous, the convergence is uniform. Thus we are led to the following result.

Lemma 5.2.

Let be a function in . The function belongs to if, and only if, there exists a continuous function such that for every ,

| (5.2) |

If this property holds, the convergence in (5.2) is uniform.

From this Lemma, the quadratic variation of in Definition 5.1 coincides with that of in Definition 2.1. However, there is a notion of quadratic ‘covariation’ between different components , of a -dimensional vector in (2.1), whereas in Definition 5.1 is defined in terms of the individual function .

Remark 5.3.

The assumption in Definition 5.1 that the mesh size in (5.1) goes to zero as , imposed on the sequence of partitions, is actually stronger than the usual assumption on the sequence of partitions in other works involving the pathwise local time. For example, in Perkowski and Prömel, (2015), Davis et al., (2018), Cont and Perkowski, (2018), the authors define the ‘oscillation’ of the function along the partition as

| (5.3) |

and require as instead of the mesh size going to zero. This is because it is enough to work with Lebesgue partitions generated by when defining the pathwise local time and deriving the pathwise Tanaka formula. Since the function is uniformly continuous on the compact interval , the decrease to zero of the mesh size does imply that the oscillation of also shrinks to zero.

One reason for the stronger condition on used here, is to follow our original definition of pathwise quadratic covariation/variation in Definition 2.1. Another reason is that we are going to involve an additional (vector of) continuous function when generating trading strategies, and the oscillation of also has to shrink to zero along the sequence of partitions . In other words, by using the ‘mesh’ assumption instead of the ‘oscillation’, we can get rid of such ‘dependence’ of the sequence of partitions on both and .

The very first definition of the pathwise local time was introduced in the unpublished diploma thesis of Wuermli, (1980). This original local time is called “-local time” of a path along a sequence of partitions . Using this notion of local time, Wuermli showed the following equation (5.7) for , where is the Sobolev space of functions two times weakly differentiable in . Since then, many versions of pathwise Tanaka formulas (generalized Itô formulas) and different definitions of local times have been introduced and studied; these vary according to the regularity of the path , the function , and the notion of “convergence for local time”. Weaker convergence in defining a local time requires more regularity on the part of the function , for the Tanaka formula (5.7) to hold. Some of these versions are stated in Section 2 of Perkowski and Prömel, (2015) for continuous paths with quadratic variation. Similar results for rougher paths (with finite -th variation, ) can be found in Section 3 of Cont and Perkowski, (2018). Among these, we present here the following version of local time and Tanaka’s formula, which we consider most appropriate in our setting.

With the notation

| (5.4) |

we have the following definition of continuous local time.

Definition 5.4 (Continuous local time).

We say that the continuous function has a continuous local time along the given nested sequence of partitions , if , the ‘discrete local times’

| (5.5) |

converge uniformly to a continuous limit as for every fixed , and the resulting mapping is jointly continuous. We call this limit continuous local time of along , and write for the collection of all functions in having a continuous local time along the given nested sequence of partitions .

The existence of continuous local time for typical price paths is shown in Theorem 3.5 of Perkowski and Prömel, (2015). In order to simplify notation, we shall write or simply , whenever the context is unambiguous. With the definition of continuous local time, we state the following version of the pathwise Tanaka formula. The proof is given in the Appendix.

Theorem 5.5 (Pathwise Tanaka formula for paths with finite quadratic variation).

Let and be absolutely continuous with right-continuous Radon-Nikodým derivative of finite variation. Then, the one-dimensional Föllmer-Itô integral

| (5.6) |

exists, and we have the generalized change of variable formula

| (5.7) |

If belongs to the space , we obtain from this

by comparing the last terms of (2.4) and (5.7). Furthermore, by setting for any continuous function and by the fact that the indicator function for any Borel set can be approximated by continuous functions, we also have the “occupation density formula”

We state now pathwise versions of classical Tanaka-Meyer formulas as a corollary to Theorem 5.5.

Corollary 5.6.

For a function , the pathwise Tanaka-Meyer formulas

| (5.8) |

| (5.9) |

and

| (5.10) |

hold for all with the notation Here, the integral terms represent pointwise limits as (5.6).

5.2 Construction of additively generated trading strategies

Now we recall the pair in Section 3, where the vector represents market weights defined in (3.7), and is an auxiliary function in . We assume that and have the same dimension . Also, in this section, we assume that each component is a continuous function with finite quadratic variation in the sense of Definition 5.1, and belonging to , i.e., admitting a continuous local time, for every . Then, we set

| (5.11) |

and assume that each is also in . For any functions , satisfying the conditions in Theorem 5.5, we define the generating function for the pair as

| (5.12) |

We can only consider such generating function of the form (5.12), because there is no ‘multidimensional Tanaka formula’ that can be applied to directly. However, we can apply instead Theorem 5.5 to each components , and sum up to obtain

| (5.13) | ||||

where we denote

| (5.14) |

as in (3.8). Here, we recall from Theorem 5.5 that each is the RCLL derivative of , and a function of bounded variation. Furthermore, the Föllmer-Itô integral in (5.13), defined via the recipe (5.6), can be decomposed as

| (5.15) | ||||

| (5.16) | ||||

| (5.17) |

because the last limit (5.17) exists as . Thus, the limit (5.16) also exists, and we denote the two limits (5.16) and (5.17) as , , respectively. For the generating function in (5.12), we define the Gamma function as in (3.5), namely

| (5.18) |

The last equation is from (5.13), and we note that is of bounded variation again. We proceed now in the manner of (3.9)-(3.11), to construct the additively generated trading strategy.

Definition 5.7 (Additive generation).

We also have the following result, which can be proved by analogy with Proposition 3.6. Note that the Gamma function below takes the form of (5.18), not of (3.6).

Proposition 5.8.

The sufficient conditions for strong relative arbitrage effected by additively generated trading strategies, presented in Section 4.1, can be applied in a similar manner to the strategies of Definition 5.7.

Concave functions such as and , when used to generate trading strategies, produce nondecreasing Gamma functions as in (3.5); this is because these functions have negative semidefinite Hessians , which play the role of the integrand of the last integral in (3.6). Such concavity is known to lead to “diversity-weighted” investment strategies, as explained in Definition 3.4.1 of Fernholz, (2002). However, these concave functions had to be in to apply Itô’s rule. Now, we can use concave but not differentiable functions, while still being able to generate portfolio with the help of Tanaka formula. Typical examples are and .

Example 5.9 (On the “size effect”).

Consider a constant and a function

where and is the dimension of the market weight vector . Note that satisfies the conditions in Theorem 5.5. Then, for the pair with , we have in (5.11), and set for to obtain the generating function in (5.12) as

| (5.23) |

which is nonnegative by construction. Here, plays the role of threshold on the market weights: we only include in our generating function those stocks whose market weights exceed the threshold level . From (5.14) and (5.18),

| (5.24) |

and

| (5.25) |

Note that this Gamma function is nondecreasing, and increases whenever a market weight hits the threshold .

The trading strategy , additively generated as (5.19), can be represented by Proposition 5.8 as

| (5.26) |

with the value

Since the Gamma function in (5.25) is nondecreasing, we can use the strong arbitrage condition in Theorem 4.2: Strong relative arbitrage with respect to the market exists over every time horizon with , satisfying

In the expression of in (5.26), the sum is a universal term, same for all indices . Thus, invests one currency unit less to this universal baseline amount for those ‘big-capitalization stocks’, whose market weights exceed the threshold . Therefore, we can interpret the strategy of (5.26) as generating strong arbitrage relative to the market by investing more money to ‘small-capitalization stocks’. This is in broad agreement with previous results in Stochastic Portfolio Theory, to the effect that “tilting” in favor of small capitalization stocks, as opposed to their larger brethren, can lead to superior results.

Example 5.10 (On the “momentum effect”).

In Example 5.9, we compared the individual market weights with a fixed constant , to determine whether to include them in the generating function or not. Now, we extend this idea by comparing current market weights with past market weights. To be specific, we want our trading strategy to depend on the difference between and for some fixed .

In order to do this, first we fix the time interval and enlarge the domain of each from to . This extension of domain can be done easily because even before we start investing to our trading strategy at time , there must be past stock prices and past market weights. We simply attach these past data to the left of the timeline, so as to extend its domain.

Furthermore, since the evolution of is as rough as its original path , we need somehow to make it smoother. Thus, we take the moving average of market weights between very small time interval for some small satisfying , and use this moving average instead of . Therefore, we introduce the function of finite variation

| (5.27) |

for each ; this is a good estimate of for some very small constant and fixed, and also a function of finite variation.

Now, we consider the function

where is again the dimension of the market weight vector . Then, for the pair with defined as in (5.27), we introduce the following nonnegative generating function

This generating function includes those stocks whose current market weight is bigger than or equal to its (estimate of) past market weight . It is also very similar to that of (5.23) with the difference that the threshold is replaced by the stock-specific level , capturing in this way the “momentum effect”.

In this manner, we compute the quantities of (5.14), (5.18) as

| (5.28) |

where we recall the continuous local time of at the origin, as in Definition 5.4. Here, in the integral expression above, the integrand is a quantity observable at time , whereas the integrator represents the increment of moving average of between time interval which is also observable value at time . Therefore, this integral can be computed at any time between and , even though the integrand and the integrator are from different times. The last term in (5.28) is nondecreasing, but the integral term is generally not monotone, as the finite variation integrator in general fluctuates.

The trading strategy , additively generated in the manner of (5.19), can be represented by Proposition 5.8 as

| (5.29) |

and its value is given as

Since the Gamma function of (5.28) is no longer monotone, it is hard to formulate appropriate conditions for strong relative arbitrage in this context. We note, however, that the strategy in (5.29) invests one unit of currency less in stocks whose current market weight is bigger than or equal to its (estimate of) past value.

5.3 Construction of multiplicatively generated trading strategies

We now recall the definitions (5.11)-(5.18) from the earlier subsection, and we further assume that is locally bounded as in Section 3.3. Then, we consider the vector with components

| (5.30) |

in the notation (5.14), and we have the following definition as Definition 3.8.

Definition 5.11 (Multiplicative generation).

For the trading strategy of (5.31), we have the similar formula for its value as in Proposition 3.9, but the difference here is that our generating function can be a lot less smooth than before; namely, of the form (5.12) with absolutely continuous . The proof requires additional attention and computation, as there is no ‘product rule’ that can be applied to such less regular functions.

Proposition 5.12.

Proof.

We denote the exponential

We recall the notation (5.11), (5.12) and consider the following telescoping expansion over the refining sequence of partitions:

| (5.34) | |||

| (5.35) |

Then, we can further expand the last double sum (5.35) as

| (5.36) | |||

| (5.37) | |||

| (5.38) |

where the first equation is from (A.7), and the last follows from (5.11) and (5.5).

Next, we show that the sum of (5.34), (5.37), and (5.38) vanishes as . First, since the mesh size goes to zero as , the limit of the sum (5.34) is a Lebesgue-Stieltjes integral

because is bounded on the compact interval for each . From (5.18), the change of variable formula for Lebesgue-Stieltjes integral gives

| (5.39) |

where

We apply the change of variable formula once again to obtain

and this is just the negative value of limit of the sum (5.37). On the other hand, the last integral of (5.39) can be expressed as the limit of the sum

which coincides with the limit of the sum (5.38). Therefore, the claim that the limits of the sums (5.34), (5.37), and (5.38) are equal to zero, is proven; whereas, the remainder term on the right-hand side of (5.34), (5.35) is the sum (5.36), whose limit we denote as

from (5.12), and (5.30). Finally, we obtain

where the last equation follows from the fact with the construction (5.31). The result (5.32) then follows from the self-financibility of and the relationship

The equation (5.33) can be justified in the same manner as Proposition 3.9. ∎

Example 5.13 (On the “size effect”, revisited).

Recall the generating function of (5.23) in Example 5.9, and add a very small constant to have

with the same as in (5.24) and the same Gamma function as in (5.25). The reason for inserting the constant is to ensure the positivity of regardless of the choice of , so that is locally bounded.

The trading strategy , multiplicatively generated by this as in Definition 5.11, can be represented by Proposition 5.12 as

| (5.40) |

and its value is given as

where

From Theorem 4.7, strong relative arbitrage with respect to the market exists over every time horizon with , satisfying

because satisfies the bounds .

In the same manner as in Example 5.9, the strategy in (5.40) invests unit of currency less than the ‘universal baseline amount’, namely , for those ‘big-capitalization stocks’, whose market weight exceeds the threshold , at time . Because is nondecreasing, the strategy keeps investing less and less money to those ‘big-capitalization stocks’ as time goes by, and the “size effect” increases gradually.

6 Examples of entropic functions

In this section, we present some examples of trading strategies additively and multiplicatively generated from variants of the ‘entropy function’, and the corresponding conditions for strong relative arbitrage introduced in Section 4. Empirical results regarding these examples will be presented in the next section.

Consider the Gibbs entropy function

| (6.1) |

with values in (0, ). Being nonnegative, twice-differentiable and concave, this function is one of the most frequently used functions in stochastic portfolio theory. See Fernholz, (2002); Fernholz and Karatzas, (2009); Karatzas and Ruf, (2017) for its usage in generating portfolios, and also Ruf and Xie, (2018), Schied et al., (2018) for some variants of portfolios generated by this function.

Example 6.1 (Entropy function).

In order to compare the trading strategy generated by the original entropy function, with those generated from variants of functions related to it, we first derive and summarize the trading strategy additively/multiplicatively generated by the original entropy function. Consider the “shifted entropy”

| (6.2) |

for some given real constant , where the last equality uses the fact . This quantity coincides with the original entropy in (6.1) when ; the reason for inserting the additive constant will be explained in the following remark. From (3.6), (3.13), and (3.20), the additively generated trading strategy , and the multiplicatively generated trading strategy from this entropy function, can be represented as

| (6.3) |

| (6.4) |

where

| (6.5) |

is nondecreasing in . The values of these trading strategies are given via (3.12) and (3.19). Note that in (6.3) and in (6.4) have relatively simple forms, because in (6.2) is ‘almost balanced’, in the sense that

holds; compare this equation with (3.14), and also compare (6.3), (6.4) with (3.15) and (3.21). Then, the condition (4.5) for additively generated strong arbitrage in Theorem 4.2 is given as

| (6.6) |

whereas the condition (4.13) for multiplicatively generated strong arbitrage in Theorem 4.7 is

| (6.7) |

Here, the constants , are the lower and upper bounds on , which appear in the boundedness condition (i) of Theorem 4.7. We discuss these bounds on in the Remark 6.2 below.

Remark 6.2.

The construction of trading strategies described in the previous sections does not require any optimization or statistical estimation of parameters. However, we can improve the relative performance of trading strategies with respect to the market by introducing a parameter or a set of parameters in the generating function . Though the original entropy function is as in (6.2) with , we purposely inserted a constant inside the logarithm. To achieve strong relative arbitrage faster, or to find the smallest such satisfying (6.6), or more generally (4.5), it helps to be able to make the ‘threshold’ value on the right-hand side of the inequality smaller, while keeping the ‘growth rate’ of fixed.

It is in this spirit, that we placed the parameter in (6.2); inserting such constant inside the would make the initial value smaller by the amount , compared to the case , while it does not affect , as subtracting a constant from does not change any derivatives of with respect to the market weights. However, if is so large that holds at some time , then has a negative value. Theoretically, has the minimum value of only when one of the market weights, say , is equal to , and all the other weights for vanish, which does not happen in the real world. Empirically, the value of is always bounded away from zero, and we can guarantee this condition theoretically by imposing a weak condition on the market weights. For example, restricting the maximum value of the market weights, say

| (6.8) |

yields an additional condition on the market weights, namely; there must be an index such that

| (6.9) |

for any , thanks to the identity . Then, the value of should be bigger than , and is bounded away from at all times. Finding a suitable value of , while maintaining bounded away from (and bigger than some positive constant ) should be statistically done and it depends on , the number of stocks. It is quite straightforward that is bounded from above by some constant , as the function has the maximum value . Empirical estimation of such can be found in the next section.

Making the initial value of small while keeping the growth rate of is also beneficial for calculating the ‘excess return rate’ of trading strategies with respect to the market. The excess return rate of the trading strategy at time can be defined as

| (6.10) |

and from (3.12), this can be represented as

in the case of additively generated trading strategy. Thus, if we somehow make the value , the denominator of above fraction, smaller, while keeping the value of in the numerator, we can obtain larger excess return rates for the trading strategy . In the following examples, we use this trick to decrease the initial value of generating function by inserting an appropriate constant whenever possible.

The following two examples use for the component two “polar opposite” functions of finite variation; the running maximum

| (6.11) |

and the running minimum

| (6.12) |

of the market weights.

Example 6.3 (Entropy function with running maximum).

Consider an entropic function of the type

| (6.13) |

with the notation of the vector function . As before, is a constant as in Remark 6.2, and the initial value is the same as in Example 6.1. We then easily obtain the derivatives as

for . From (3.6), we also have

| (6.14) |

where we used the fact that the increment is positive only when . As the function of (6.13) is linear in , the second order partial derivatives with respect to of vanish, and the nondecreasing structure of comes solely from . Also from (3.12), and (3.13), the trading strategy generated additively from this function in (6.13), is expressed as

| (6.15) |

and the value of this trading strategy is given as

The strong arbitrage condition (4.5) in Theorem 4.2 takes the form

On the other hand, from (3.19), and (3.20), the trading strategy generated multiplicatively by the function in (6.13), is given as

| (6.16) |

and the associated value is

where

The strong arbitrage condition (4.13) in Theorem 4.7 takes the form

Here are again lower and upper bounds on , and these bounds depend on the parameter and the condition imposed on the market weights, as described in Remark 6.2. Empirical results regarding this example can be found in the next section.

The Gamma function which represents the “cumulative earnings” of the next example is nonincreasing, but surprisingly, the empirical value and of trading strategies grow asymptotically in the long run as the value of grows, as indicated in the empirical results of the next section. Thus, in this case, it is more appropriate to apply Theorem 4.5 and Theorem 4.9 regarding the strong arbitrage condition.

Example 6.4 (Entropy function with running minimum).

Consider the function

| (6.17) |

with the notation of the vector function in (6.12). As before, is a constant and the initial value is the same as previous examples. Then, similarly as before, we have

for . Also from (3.6), we obtain

| (6.18) |

which is nonpositive and nonincreasing function of .

We first consider the trading strategy additively generated from this function which is expressed as

| (6.19) |

by (3.13). Note that admits the lower bound

| (6.20) |

because the function is decreasing in the interval and, thus, the quantity is positive provided that

holds. By (3.12), the value of this trading strategy is given as

| (6.21) |

While , the last term on the right-hand side of (6.21), is nonincreasing, the second term asymptotically increases as the mapping is nondecreasing. Actually, as we can see in the next section, the value of this trading strategy grows in the long run. We can apply Theorem 4.5, rather than Theorem 4.2, to find a strong arbitrage condition, because in this example is not nondecreasing.

In order to apply Theorem 4.5, we first need to show that holds. From (6.20), we obtain

holds for all . The last inequality follows from the fact that the function is decreasing in the interval . Then, we also obtain

because is just the weighted arithmetic average of with weights with . Thus, in (6.21) admits the lower bound

for any , and is guaranteed when

| (6.22) |

holds. Regarding the second condition of Theorem 4.5, we have

| (6.23) |

where we used the fact ; now the mapping is nonincreasing, so is nondecreasing in . Finally, the last condition of Theorem 4.5 follows easily from (6.18), as

| (6.24) |

Thus, Theorem 4.5 shows that the additively generated strategy in (6.19) is strong arbitrage relative to the market over every time horizon with , satisfying the condition

Remark 6.5.

In Remark 6.2, we need to find a suitable value for satisfying an inequality, for instance, for all in Example 6.1, to make the function nonnegative. This inequality usually depends on the values , which are not observable at time . Thus, we need to impose some condition on the market weights or statistically analyze historical market data to find an appropriate value for before we construct the trading strategy.

However, in Example 6.4, due to its unique structure, we can analytically find a suitable value of without any statistical estimation at time . Indeed, from (6.23), we have that

holds; and setting

| (6.26) |

guarantees the condition for all . Note that this can be calculated from absolutely observable values at time . Actually, satisfying (6.22) also guarantees the nonnegativity condition of because holds due to the nonpositivity of . Of course, one can perform a statistical estimation of using past market data, to obtain a better value of while satisfying both and .

The next example provides yet another application of Theorem 4.5.

Example 6.6 (Iterated entropy function with running minimum).

In this example, we first fix a positive constant such that the following condition on the initial market weights holds;

| (6.27) |

Here, is the exponential constant. As the initial market weights are observable before we construct a trading strategy, we can find and fix such value of at the moment we start investing in our trading strategy. For example, if no single stock takes more than of total capitalization at time , we can set , as . Then, we consider a function

| (6.28) |

with the notation of the vector function . As in Remark 6.5, we can pre-determine the value of the constant , without any statistical estimation, because of the series of inequalities

| (6.29) | ||||

The first inequality uses the fact that is decreasing function and the second inequality is from the equation . The last inequality holds because is increasing in the interval and

| (6.30) |

holds from the assumption (6.27). Note that defined in (6.29) is a nondecreasing in as the mappings and are nonincreasing. Then, the choice

| (6.31) |

which is completely observable value at time , guarantees that is always nonnegative. Next, after some computation, we obtain the partial derivatives

| (6.32) | |||

for . We note that holds again because the mapping is increasing from to in the interval . From (3.6) and the fact that the increment is positive only when , we obtain

| (6.33) |

which is nonincreasing function of , because holds by the equation (6.30). This function admits the lower bound

| (6.34) |

with the notation

Here, represents the logarithmic integral function. Note that the function has negative value and is decreasing from to in the interval . The last inequality holds because the inequality

| (6.35) |

is satisfied for all with the condition (6.30). We also note that defined in (6.34) satisfies from the same inequality (6.35). On the other hand, by (3.13), the trading strategy additively generated from this function is expressed as

| (6.36) |

Finally, by (3.12), the value of this trading strategy is given as

| (6.37) |

and is estimated as

from (6.29) and (6.34). Thus, the choice

| (6.38) |

guarantees and also satisfies (6.31). We emphasize here again that defined as in (6.38) depends only on the initial market weights , thus no statistical estimation of is required. Using the same technique as in (6.29), in (6.36) is greater or equal to

which is by (6.38). Thus, this trading strategy is ‘long-only’, i.e., for all .

As we showed above that all conditions of Theorem 4.5 are satisfied, the additively generated strategy in (6.36) is strong arbitrage relative to the market over every time horizon with , satisfying the condition

with in (6.34).

7 Empirical results

We present some empirical results regarding the behavior of additively-generated portfolios in the Section 6, using historical market data. We first analyze the value function of these portfolios with respect to the market by decomposing it with generating function and corresponding Gamma function in (3.12). Especially, we show that all value functions of portfolios in Section 6 outperform the market portfolio. Then, we present that the different choice of the parameter , explained in Remark 6.2, indeed significantly influences the performance of portfolios.

7.1 Data description and notation

In order to simulate a perfect ‘closed market’, we construct a “universe” with stocks which had been continuously traded during consecutive trading days between 2000 January 1st and 2017 December 31st. These stocks were chosen from those listed at least once among the constituents of the S&P 1500 index in this period, and did not undergo mergers, acquisitions, bankruptcies, etc.

Remark 7.1.

This selection of stocks is somewhat biased, in the sense that we are looking ahead into the future at time by blocking out those stocks which will go bankrupt in the future. However, the reason for this biased selection is to keep the number of stocks constant all the time which is the essential assumption of our ‘closed’ market model. If we compose our portfolio from stocks included in S&P 1500 index at the beginning, remove one stock whenever it goes bankrupt, or take in a new stock whenever it is newly added to the index, the number of stocks in our portfolio fluctuates over time and the generating function would be discontinuous whenever changes.

One possible solution to this problem is to consider an ‘open market’. We first fix the value of , say at the beginning, keep track of price dynamics of all stocks in the market (which should be composed of more than stocks, say stocks with ), rank them by the order of their market capitalization, and construct our portfolio using the top stocks among stocks. In this way we can keep the same number of companies all the time, but considering ranked market weights always involves a ‘leakage’ issue. As explained in Chapter 4.2, 4.3 of Fernholz, (2002) and Example 6.2 of Karatzas and Ruf, (2017), this refers to the loss incurred when we have to sell a stock that has been relegated from top capitalization index to the lower capitalization index. Even worse, as we want to invest only in the top companies among companies in this open market, our trading strategy should satisfy the equations for whenever the -th company fails to be included in the top companies at time . However, we do not know how to construct such trading strategy yet.

Thus, it is not easy to make a perfect empirical model, and we decided to select stocks in a biased manner which fits better to our theoretic model described in the previous sections.

We obtained daily closing prices and total number of shares of these stocks from the CRSP and Compustat data sets. The data can be found here; https://wrds-web.wharton.upenn.edu/wrds/. We used R and C++ to program our portfolios.

As we used daily data for days, we discretized the time horizon as . For , we summarize our notations here;

-

1.

: the capitalization (daily closing price multiplied by total number of shares) of th stock at the end of day .

-

2.

: the total capitalization of stocks at the end of day . This quantity also represents dollar value of the market portfolio at the end of day with the initial wealth .

-

3.

: the th market weight at the end of day .

-

4.

: the additively generated portfolio weight of the th stock at the end of day which can be computed using the equation (3.16). Note that holds.

-

5.

: the total value of the portfolio at the end of day . Then, represents the amount of money invested by our portfolio in th stock at the end of day .

As the capitalization of th stock at the beginning of day should be equal to , the capitalization of the same stock at the end of the last trading day , we also deduce that , , , and represent the total capitalization, th market weight, th additively generated portfolio weight, and the money value of portfolio at the beginning of day , respectively.

The transaction, or rebalancing, of our portfolio on day , is made at the beginning of the day , using the market weights at the end of the last trading day. We compute from via (3.16), and re-distribute the generated value according to the these weights . Then, the monetary value of portfolio at the end of day can be calculated as

In order to compare the performance of our portfolios with the market portfolio, we set our initial wealth as and compare the evolutions of and . Once the initial amount invested in our portfolio is determined, the monetary value of the portfolio can be obtained recursively by the above equation. However, can be defined with the trading strategy in (3.9) or (3.13);

| (7.1) |

Then, the value with respect to the market, defined as in (3.3) or represented as in (3.12), has another representation as the ratio between the money value of our portfolio and total market capitalization;

and the expression ‘value of trading strategy (or portfolio) with respect to the market’ makes sense. Furthermore, the excess return rate of the portfolio defined in (6.10) can be represented as

and the expression ‘excess return rate with respect to the market’ also makes sense. Here, because we set . In the last part of following subsection, we show the evolutions of of several portfolios to compare their performance.

7.2 Empirical results

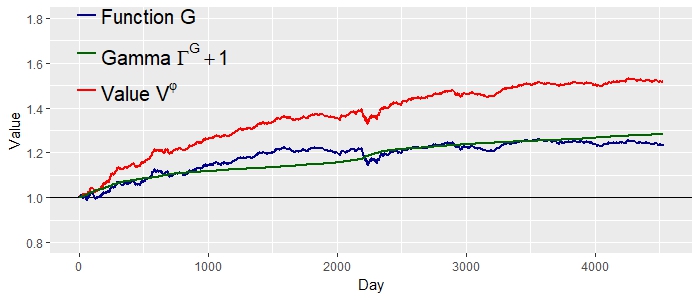

We first decompose the value functions of trading strategies additively generated from the functions in entropic examples (Example 6.1, 6.3, 6.4, and 6.6) into the generating function and the corresponding Gamma function . For easy comparison, we normalized all generating functions so that holds, and shifted up the Gamma functions by in Figure 1.

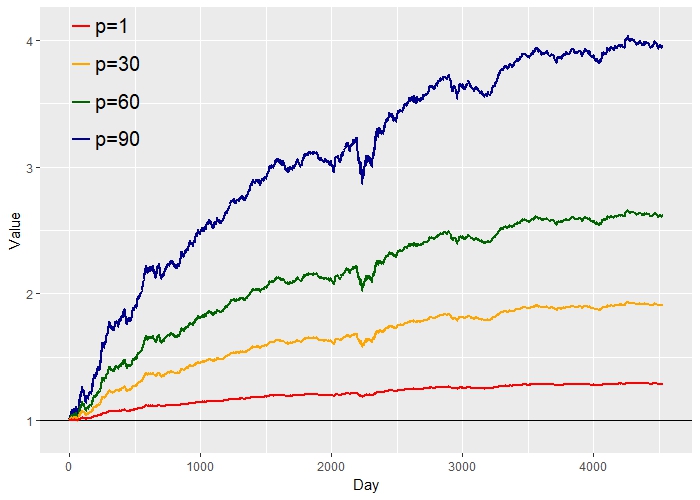

Figure 1 confirms that all trading strategies additively generated in Section 6 outperform the market as the values (red lines in the figure) gradually increase. In sub-figures (a) and (b), the growth of the value comes from the growth of the Gamma function. In contrast, even though the Gamma function decreases, the value of trading strategy grows as the function increases substantially in sub-figures (c) and (d). In the sub-figure (d), we set the parameter as it is the largest integer satisfying the equation (6.27); initial market weights data give us and holds. We chose the same parameter (See Remark 6.2) in all sub-figures for fair comparison, but this is a very sloppy choice of the parameter for (a), (b), and (c). If we chose the value of using statistical estimation elaborately in each examples, the performance of portfolio would be improved, as Figure 2 represents in the case of Example 6.1.

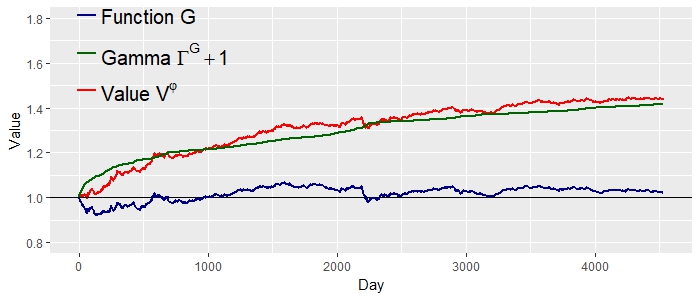

Figure 2 shows the values of additively generated portfolios in Example 6.1 with different choices of the parameter . We can verify that trading strategy with bigger value of performs better as described in Remark 6.2. From the data, the Gibbs entropy of market weights ranged from to during 4528 days. Thus, is a safe estimation of the parameter which guarantees the non-negativity of the function in (6.2) as holds.

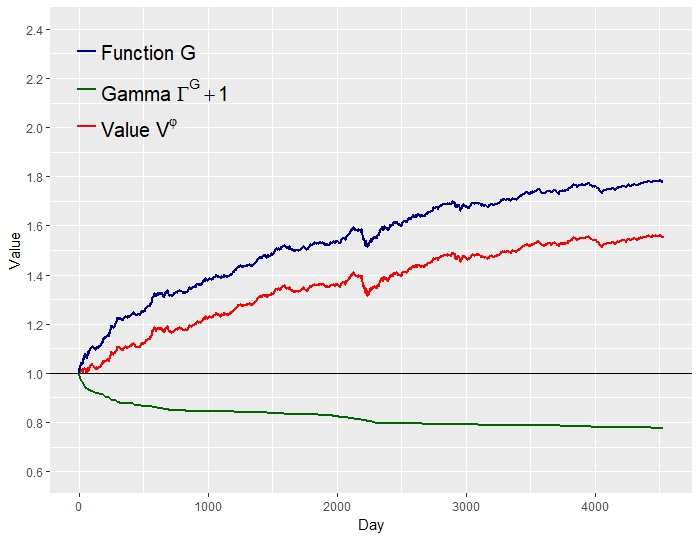

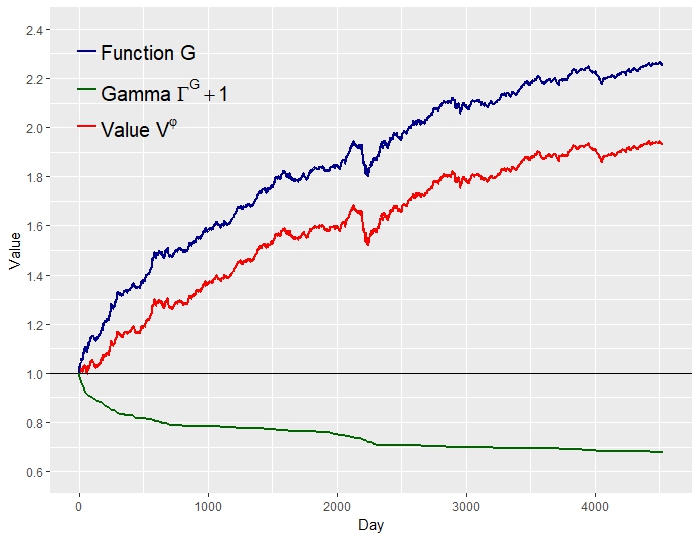

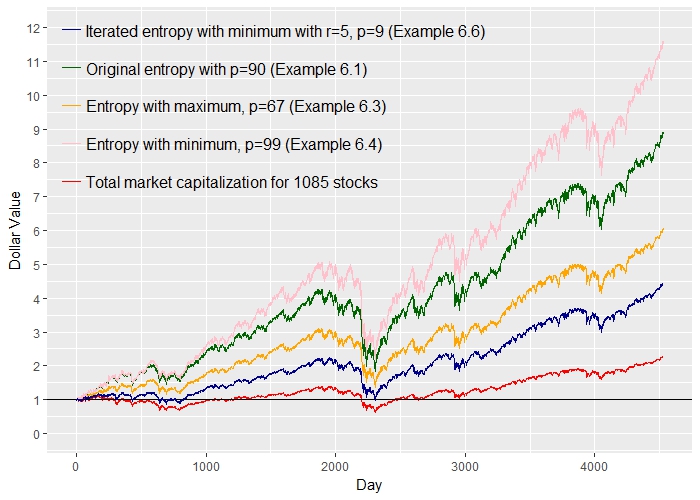

Finally, ‘dollar values’ of portfolios from four examples of Section 6, which are defined as in (7.1), along with the total market value of stocks from the start of 2000 to the end of 2017, are illustrated in Figure 3. Dollar values are normalized by replacing by . In Figure 3, while the market capitalization had been approximately doubled during years, the dollar values of all other portfolios had been grown more than times. Parameters are appropriately chosen using statistical estimation in each portfolio.

8 Conclusion

Karatzas and Ruf, (2017) introduced an alternative “additive” way of functional generation of trading strategies and compared it to the original “multiplicative” way of E.R. Fernholz. This new approach weakens the assumption on the asset prices from Itô processes to continuous semimartingales, characterizes the class of functions called “Lyapunov functions” which generate trading strategies leading to strong arbitrage with respect to the market, and gives a very simple sufficient condition for strong arbitrage. The present paper takes more generalized approaches to these two ways of functional generation. The results of this paper can be summarized as follows:

-

1.

We show how to generate both additively and multiplicatively, trading strategies without any probabilistic assumptions on the market model. This is done by using the celebrated pathwise Itô calculus, and the only analytic assumption we impose is that the market weights admit continuous covariations in a pathwise sense. In the practical sense, we do not have to care about this analytic assumption because market weights data are given as the form of discrete time-series and such data always admit pathwise covariations.

-

2.

We extend the class of functions which generate trading strategies by introducing an additional argument of finite variation other than market weights as the input. Inserting this argument in the generating function gives extra flexibility in portfolio construction and this has been dealt with in other literatures. However, we present some new examples of such extra argument which gives us simple sufficient condition leading to strong arbitrage relative to the market.

-

3.

We also extend the class of functions which generate additive and multiplicative strong relative arbitrage by giving new sufficient conditions. The new conditions allow the function not be “Lyapunov”, or concave with respect to the market weights, in order to generate strong relative arbitrage or to outperform the market portfolio in the long run. We also present empirical results of portfolios which indeed outperform the market.

-

4.

We further extend the class of portfolio-generating-functions from twice-differentiable to less smoother, namely absolutely continuous, functions with help of the pathwise Tanaka formula. Using Tanaka formula involves the concept of local times and this yields new interesting types of portfolios and corresponding strong arbitrage conditions.

While this paper generalizes the functional generation of portfolios in several respects, we suggest some new questions. First, this paper assumes a ‘closed market’, in other words, the number of stocks is fixed. In this respect, it fails to represent or resemble the real market. As explained in Remark 7.1, an ‘open market’ models the real world better, but nothing seems to be known on how to construct trading strategies in this open market. Secondly, the market weights in this paper should have finite second variation along a sequence of time partitions; can something be said, along the lives of Cont and Perkowski, (2018), regarding price dynamics, or market weights, with finite -th variation for ?

Appendix A Proofs

Proof of Theorem 2.3.

Using the telescoping sum representation, we obtain

| (A.1) | ||||

| (A.2) |

The Taylor expansion, applied to the components of the function in the sum (A.1), gives

| (A.3) | |||

where the last remainder term is bounded by

for some function with the property . Since is continuous and of bounded variation, the last double sum of the right-hand side of (A.3) goes to zero as and the sum (A.1) converges to the Lebesgue-Stieltjes integral

as . On the other hand, again by the Taylor expansion applied to the components of the function in the sum (A.2), we obtain

| (A.4) | |||

| (A.5) | |||

| (A.6) |

where the last remainder term (A.6) is bounded by

for some function with the property . Again, by the continuity of and by the fact that admits the pathwise quadratic covariation in the sense of (2.1), the double sum (A.6) approaches zero as . The sum (A.5) converges to the Lebesgue-Stieltjes integral

again by the existence of the pathwise quadratic covariation of . As all the other terms converge, the remaining sum (A.4) should converge to some limit, which we call ‘Föllmer-Itô integral’ as in (2.5). ∎

Proof of Theorem 5.5.

For any two real numbers and , by applying the integration by parts formula with the notation (5.4), we have the equation

| (A.7) |

Thus, using the telescoping sum

for the sequence of partitions of , the above equality becomes

| (A.8) | ||||

thanks to the definition (5.5). The last integral on the right-hand side of (A.8) converges to the last integral of (5.7), since converges uniformly to , and the result follows. ∎

References

- Cont, (2016) Cont, R. (2016). Functional Itô calculus and functional Kolmogorov equations. In Stochastic Integration by Parts and Functional Itô Calculus, pages 115–201. CRM Barcelona, Birkhäuser Basel.

- Cont and Perkowski, (2018) Cont, R. and Perkowski, N. (2018). Pathwise integration and change of variable formulas for continuous paths with arbitrary regularity. Preprint, arXiv:1803.09269v2, To appear in Transactions of the AMS.

- Davis et al., (2018) Davis, M., Obłój, J., and Siorpaes, P. (2018). Pathwise stochastic calculus with local times. Ann. Inst. H. Poincaré Probab. Statist., 54(1):1–21.

- Fernholz, (2002) Fernholz, E. R. (2002). Stochastic Portfolio Theory, volume 48 of Applications of Mathematics (New York). Springer-Verlag, New York. Stochastic Modelling and Applied Probability.

- Fernholz et al., (2018) Fernholz, E. R., Karatzas, I., and Ruf, J. (2018). Volatility and arbitrage. Ann. Appl. Probab., 28(1):378–417.

- Fernholz, (1999) Fernholz, R. (1999). Portfolio generating functions. In Avellaneda, M., editor, Quantitative Analysis in Financial Markets. World Scientific.

- Fernholz and Karatzas, (2009) Fernholz, R. and Karatzas, I. (2009). Stochastic Portfolio Theory: an overview. In Bensoussan, A., editor, Handbook of Numerical Analysis, volume Mathematical Modeling and Numerical Methods in Finance. Elsevier.