Online Inference with Multi-modal

Likelihood Functions

Abstract

Let be a sequence of i.i.d. observations and be a parametric model. We introduce a new online algorithm for computing a sequence which is shown to converge almost surely to at rate , with a user specified parameter. This convergence result is obtained under standard conditions on the statistical model and, most notably, we allow the mapping to be multi-modal. However, the computational cost to process each observation grows exponentially with the dimension of , which makes the proposed approach applicable to low or moderate dimensional problems only. We also derive a version of the estimator which is well suited to Student-t linear regression models. The corresponding estimator of the regression coefficients is robust to the presence of outliers, as shown by experiments on simulated and real data, and thus, as a by-product of this work, we obtain a new online and adaptive robust estimation method for linear regression models.

1 Introduction

Let be a sequence of i.i.d. observations that take values in the measurable space and are defined on the probability space with associated expectation operator . Let , where , be a collection of probability density functions on w.r.t. some -finite measure . Assuming that we can compute at a finite cost for all and that is well-defined, we consider the problem of learning the parameter value online as new observations arrive, at a (nearly) optimal rate.

To our knowledge, the only class of algorithms able to achieve this goal for a broad range of models is that of stochastic approximation (SA) methods. Given a non-negative sequence of learning rates and an initial value , the standard SA algorithm amounts to computing

| (1) |

Under suitable conditions on , the estimator converges in -probability to at the optimal rate (see e.g. Toulis et al.,, 2017, and references therein). However, for this convergence result to hold, it is necessary to impose strong conditions on the mapping (see e.g. Lei et al.,, 2019, for a recent convergence result of SA methods). In particular, if this mapping is multi-modal, convergence to from an arbitrary starting value cannot be guaranteed.

We introduce an online algorithm for computing an estimator which, under standard assumptions on the statistical model , converges -a.s. to at rate in the sense that

| (2) |

where is a user specified parameter. Notably, we establish (2) without assuming the uni-modality of the mapping and by allowing to be unbounded. The fact that the rate in (2) is slower than the usual rate is expected; for a non-compact parameter space, standard statistical estimators, such as the maximum likelihood estimator or the Bayesian posterior mean, are known to converge to at rate only in -probability (see e.g. van der Vaart,, 1998, Chapters 5 and 10).

Our strategy for computing is to couple two different algorithms, namely one algorithm whose goal is to search across all the different modes of the function and one algorithm whose goal is to find the extremum within a given mode. At each iteration these two algorithms process a new observation and, by a careful design of their interactions, they are -a.s. able to learn the parameter value at rate .

The exploration within a given mode of the objective function relies on Bayes updates. This allows the algorithm to be derivative free, and thus to be applicable to non-differentiable problems. However, this comes with a cost. In gradient based optimization methods, such as SA, the gradient gives the direction of search (see the update (1) of SA). Without this directional information, the only possibility to find is to explore, at each iteration, all the directions of the parameter space. Consequently, the computational complexity of computing grows exponentially with the dimension of .

To be more precise, for all the algorithm we introduce below requires operations to process , with and where the integer is a tuning parameter of the algorithm. It is worth mentioning at this stage that our main result guarantees that the convergence property (2) holds only if for some problem specific and unknown integer . The numerical experiments in Section 4 suggest that this constraint on is not an artefact of our proof but is needed for (2) to hold. The experiments also suggest that the inequality is sharp, and thus in some problems the condition seems enough for (2) to hold.

An important application of online learning algorithms is to facilitate the inference in large datasets, where the number of observations is such that each of them can only be read a small number of times for practical considerations (see e.g. O’Callaghan et al.,, 2002; Toulis and Airoldi,, 2015). When used in this context, an important property of the proposed algorithm is that the operations needed to compute can be made trivially parallel, except for specific time instances when communication between computers is required. As we shall see, these time instants are exponentially far apart, so that the total parallel complexity to compute is . For this reason, in the offline setting the algorithm introduced in this work is applicable for large values of and thus, recalling the constraint , for problems with moderate values of .

We demonstrate the applicability of our approach to a moderate dimensional problem () in Section 4.4, where we consider parameter inference in the Student-t linear regression model. We derive a version of the algorithm which is well suited to this model, and apply it to both simulated and real data. The resulting regression coefficient estimator is robust to the presence of outliers and therefore, as a by-product of this work, we obtain a new approach to robust online linear regression, which is known to be a difficult problem (Pesme and Flammarion,, 2020).

The remainder of this paper is organized as follows. In Section 1.1 we introduce the notions of perturbed Bayesian inference and perturbed posterior distributions (PPDs) that are the cornerstones of constructing the algorithm for computing the estimator , as explained in Section 1.2. In Section 2 we formally introduce the estimator and establish sufficient conditions for (2) to hold. In Section 3 we discuss the elements of the proposed algorithm that need to be chosen by the user, and make some practical recommendations. In Section 4 we propose some numerical experiments and Section 5 concludes.

Unless otherwise mentioned, we assume henceforth that and that for all . These two conditions ensure that all the quantities introduced below are well-defined, but they are not needed for the proposed method to be applicable or for the theoretical results to be valid.

1.1 From Bayesian inference to perturbed Bayesian inference

We let denote the set of probability measures on and, for all , we let be the random mapping defined by

Let be a prior distribution for and be the corresponding sequence of posterior distributions, defined by the recursion

| (3) |

Under mild conditions on and on the sequence converges to at the optimal rate, in the sense that for any we have (see e.g. Kleijn and van der Vaart,, 2012, Theorems 3.1 and 3.3)

| (4) |

where denotes the Euclidean norm and .

From (3)–(4), we conclude that Bayesian inference is theoretically well suited for efficient online parameter estimation, since can be computed recursively from only and it concentrates to the target value at the optimal rate. However, often in practice, the recursion (3) cannot be used to learn , as computing is generally intractable.

We propose a practical alternative to Bayesian inference which we dub perturbed Bayesian inference. It is based on the observation that, for any distribution with a finite support of size , we can compute in operations since, denoting by the support of ,

However, if we consider a prior distribution with a finite support of size , then, for all , the corresponding posterior distribution will typically have zero mass on , the reason being that the support of is a subset of the support of which, usually, does not contain .

In order to account for not belonging to the support of we introduce a support updating schedule , which is a set of time instants when a new support is generated by means of support updating functions . For all , is a random function that takes as an input a distribution on with a finite support and returns as output a uniform distribution with a support of the same size.

Then, for a given triplet , the corresponding sequence of perturbed posterior distributions is defined by the recursion

| (5) |

from which we see that if , then is computed from by a conventional Bayes update , while for , the Bayes update is preceded by a support update using .

Henceforth we restrict our attention to support updating functions such that the time and space complexity of computing is bounded by , where is the support size of and where is independent of . Under this condition, can be computed in an online fashion, which enables these PPDs to be used in practice to learn on the fly.

1.2 From perturbed Bayesian inference to the estimator

The key step to define the proposed estimator is to find conditions on which ensure that, for any prior distribution with support of size , the sequence of PPDs associated to the triplet concentrates -a.s. on at rate , in the sense that

| (6) |

for any , and where is a parameter that enters in the definition of the support updating functions .

2 The estimator

As explained in Section 1.2, the main step to define the proposed estimator is to construct a pair such that the resulting sequence of PPDs, defined in (5), has the convergence property (6) when its support size is large enough.

The key feature of the considered support updating functions is that they contain information about which, informally speaking, is used to generate the new supports of the PPDs in the regions of that are likely to contain this target parameter value. More precisely, for every information about is brought in the support updating function through the -th element of another sequence of PPDs, with support size and characterised by the triplet . The functions have a simple algorithmic description and the corresponding subsequence of PPDs is proven to concentrate on . However, as we shall see, this subsequence concentrates on at a slow and dimension dependent rate, and can therefore not be used to efficiently learn . To avoid confusion, below we will refer to as the auxiliary PPDs and to as the main PPDs.

For reasons that will be clear in the following, the support size of the main PPDs, the support size of the auxiliary PPDs and the support updating schedule are such that

| (8) |

with a strictly increasing sequence in .

The rest of this section is organized as follows. We start in Section 2.1 by detailing the construction of the auxiliary PPDs. Notably, we define the support updating mappings and explain why these PPDs should not be directly used to estimate . In Section 2.2 we use the auxiliary PPDs to construct the support updating mappings , and we give the precise definition of the support updating schedule . This completes the definition of the sequence which, together with (7), also completes the definition of the sequence whose algorithmic definition is given in Section 2.3 (Algorithm 3). The convergence result (2) for the estimator is established in Section 2.4 and in Section 2.5 we briefly discuss a more general version of the proposed algorithm. The assumptions for the convergence results of Section 2.4 are gathered in Section 2.6. Sections 2.1-2.2 are quite technical and can be skipped in a first reading.

Below we let be the open ball of size around w.r.t. , the maximum norm on , and denotes the Student’s t-distribution with mean and scale matrix . For integers we will often use the notation and .

2.1 The auxiliary PPDs

Given a sequence in such that , we consider the problem of choosing a support updating schedule and support updating functions such that

| (9) |

where, for all , . In other words, we require that, -a.s., the mode of belongs to the ball for large enough. We focus here on the sequence for reasons that will be clear in Section 2.2.

In this work we consider the following three steps to establish (9), which will guide our construction of and definition of . In a first step we want to prove that, -a.s., for infinitely many the distribution has positive mass on the ball of size around , that is

| (10) |

In a second step, we want to use (10) to show that infinitely often. Next, we note that if this latter result is verified then (9) holds if the event occurs finitely many times, -a.s. Establishing that this is indeed the case notably requires to establish that

| (11) |

which is therefore the last step we want to go through in order to show (9).

2.1.1 Support updating schedule

Choosing a sequence so that (10)–(11) hold amounts to solving a balancing problem. Indeed, on the one hand, the number of support updates should be large enough to ensure a proper exploration of the entire parameter space , that is for (10) to hold. On the other hand, the support updates should be infrequent enough to enable the convergence property (4) of Bayes updates to operate between two successive updates of the support, that is for (11) to hold. Since both (10) and (11) depends on our definition of , given in Section 2.2, logically depends on this sequence.

2.1.2 Support updating mappings

We now turn to the construction of the functions that are used to update the support of the auxiliary PPDs. Recalling that we write as in (8), for every we let be such that the uniform distribution has support , where

| (12) |

with the Algorithms L_Exp (for Local Exploration) and G_Exp (for Global Exploration) given in Algorithms 1 and 2, respectively.

With this construction of the elements of the new support belong -a.s. to the ball of size around , and each of the hypercubes of equal size that partition this ball contains at least one element of this set. This partitioning of is needed to ensure that if then the next estimate can be such that . Since will be taken so that for all (see (15)), it follows that the first elements of the new support are generated in a way that enables (11) to hold.

The last elements of the new support, generated by mean of Algorithm G_Exp, aim at exploring the different modes of the mapping , and in particular at allowing (10) to hold for some suitable choices of . It turns out that sampling from a heavy tails Student’s t-distribution with bounded (random) mean is enough to achieve this goal. The rationale for sampling in this way is to guarantee that, as , the probability of the event does not converge to zero too quickly. Informally speaking, controlling the speed at which ensures that, for every , the support updating mapping allows to explore sufficiently well the entire set .

2.1.3 Limitation of the auxiliary PPDs

It should be clear that, for the support updating functions defined above, as the quantity cannot be guaranteed to converge to zero faster than the rate at which . Unfortunately, as we will now argue, condition (9) can only hold if at a slow and dimension dependent rate, so that the estimator can only have poor statistical properties.

Given our definition of the support updating functions a natural way to ensure (10) is to show that, -a.s., for infinitely many the Student’s t random variate belongs to the set . Assuming that in Algorithm 2 we have for all , it follows by the first and the second Borel-Cantelli lemmas that this is the case if and only if

| (13) |

Under the specific version of Algorithm 2 that we are considering, it is easily checked that there exists a finite constant such that

For the sake of the argument let for all and some . Then, for any we have

showing that for (13) to hold we must have . Hence, as increases must decrease, for any choice of support updating schedule .

2.2 The main PPDs

We now describe how we use the auxiliary PPDs introduced in Section 2.1 to define the support updating functions in such a way that the convergence property (6) may hold.

For every the support of the uniform distribution is generated using Algorithm L_Exp (Algorithm 1), with input parameters and that depend on , the mode of the auxiliary PPD . Notice that the support of is therefore -a.s. included in the ball whose radius and center are functions of .

In our construction of we centre the support of the distribution at the location when . The rational for doing this is the trivial implication

from which it follows that if then is closer to than , whenever the event occurs. The effectiveness of this mechanism by which guides the support of towards depends crucially on the probability of this latter event, which needs to converge to one sufficiently quickly as . Our computations show that this is the case if, for some parameter , the support updating schedule is such that

| (14) |

while, for some parameter , the sequence is defined by

| (15) |

Then, by construction, it follows that for large enough and with high probability , we have when . Based on this information, when this latter event occurs we logically let , so that the support of belongs precisely to the ball .

Notice that the support of and the first points of the support of are therefore generated exactly the same way each time we have . Given the poor statistical properties of mentioned in Section 2.1.3, it should be clear that the convergence result (6) cannot hold if the event occurs infinitely often. For this reason, the support updating schedule and the sequence defined in (14) and (15) are also chosen to ensure that, -a.s. surely, we have for large enough.

We now turn to the situation where . In this case, we let while the radius of the new support is such that if we have for all then . Together with the fact that, -a.s., we have for large enough, this enables the convergence result (2) for to hold.

For completeness, we finish this subsection with an explicit definition of in the case . This is done by setting, for some parameter ,

| (16) |

where is as in (15), and where, for all , denotes the cumulative number of support updates since (and including) the last support updating time at which we have .

2.3 Algorithm summary

# Initialisation

# Main loop over the observations

# Support update Yes/No

# Apply mapping (update the support of the auxiliary PPD)

# Apply mapping (update the support of the main PPD)

# Determine the next support updating time

Bayes updates

#(auxiliary PPD)

#(main PPD)

Compute

Below the sequence is as defined in (16) and Algorithms L_Exp and G_Exp correspond to Algorithm 1 and 2, respectively.

The construction of the estimator , explained in (7) and in Sections 2.1-2.2, is summarized in Algorithm 3.

The lines with non-bold numbers can be used to recursively compute the sequence of auxiliary PPDs, associated to the triplet where is as defined in (14) and where is the empirical distribution associated to the starting values . Indeed, letting ,

where and are as defined in Algorithm 3. Notice that for all the support of the uniform distribution is generated on Lines 10–11 of the algorithm.

For reasons explained at the beginning of this Section 2, for every the auxiliary PPD is used in the definition of the support updating mapping , as can be observed on Lines 14-18 of Algorithm 3 where the support of the uniform distribution is computed. Letting be the empirical distribution associated to the starting values , the sequence of PPDs associated to the triplet is given by

| (17) |

with and as defined in Algorithm 3.

Remark 1.

If we are only interested in computing for some fixed number of observations then, unless , we can omit Line 27 of Algorithm 3. By doing so, the operations performed by Algorithm 3 at time become trivially parallel and, since the difference increases exponentially fast with (see (14)), it follows that the parallel complexity to compute only is .

2.4 Convergence results

The proof of Theorem 1 and of Corollary 1 below are provided in the Supplementary Material. In Theorem 1 the notation means that are such that for all .

The following result shows that the sequence of PPDs, defined by Algorithm 3 as in (17), is indeed such that the convergence result (6) holds, provided that the support size is sufficiently large.

Theorem 1.

Note that since and , condition (18) requires that .

Remark 2.

The condition ensures that, if at support updating time it holds true that for a then, -a.s., the new support L_Exp contains at least one element in the ball .

The requirement can be removed, but in this case we only managed to show that the conclusion of the theorem holds for (see Remark 2). In practice, except in some very particular situations, for all the components of and of will all be random variables on , in which case this condition on will be fulfilled.

The following result, which is a direct consequence of Theorem 1, establishes that the estimator converges -a.s to at the announced rate.

Corollary 1.

Under the assumptions of Theorem 1, we have

2.5 Extensions

In the Supplementary Material we show that the convergence results of Section 2.4 hold for a class of support updating mappings much larger than the one considered here (the support updating schedule being unchanged). Notably, the broader class of support updating mappings considered in the Supplementary Material is such that, instead of comparing with as on Line 14 of Algorithm 3, the estimator is compared to

| (19) |

with a parameter, such that and such that . Remark that we recover Line 14 of Algorithm 3 when . Informally speaking, the goal of setting in (19) is to reduce the probability that, due to the randomness of the observations, the generation of the new support forces to move towards a lower mode of the mapping . In particular, as shown in the Supplementary Material, taking ensures that the probability of this undesirable event remains small as and increase, which allows us to derive a version of Theorem 1 and of Corollary 1 uniform in and . However, the definition of the random variables and used in (19) is quite involved and, in practice, we find that taking does not bring any significant improvements compared to the simpler case considered in Algorithm 3.

2.6 Assumptions on the model

The theoretical results of Section 2.4 rely on Assumptions A1-A5 introduced below. Assumptions A1-A2 are borrowed from Kleijn and van der Vaart, (2012). Assumption A3 contains some of the classical conditions to prove the asymptotic normality of the maximum likelihood estimator (van der Vaart,, 1998, Section 5.6, p.67) while Assumption A4 is a standard requirement to establish the consistency of this estimator (van der Vaart,, 1998, Theorem 5.7, page 45). Conditions under which Assumption A5 holds are given in Kleijn and van der Vaart, (2012, Lemma 2.2).

Assumption A1.

There exist an open neighbourhood of and a measurable function such that, for all ,

We assume that for all and that for some we have .

Assumption A2.

For every there exists a sequence of measurable functions , with , such that

where, for and , we denote by the measure on defined by for all .

Assumption A3.

For every the function is three times continuously differentiable on some neighbourhood of , with first derivative and second derivative , and there exists a measurable function such that, for all ,

| (20) |

We assume that , the matrix is invertible and the matrix is negative definite.

Assumption A4.

for all .

Assumption A5.

where, for every , is defined by , , with a closed ball containing a neighbourhood of .

3 Discussion

In this section we discuss the role of the key ingredients of Algorithm 3 that need to be chosen by the user, and make some practical recommendations regarding their choice.

3.1 The Algorithm G_Exp

When the function has several modes the finite sample behaviour of may depend heavily on the precise definition of Algorithm G_Exp (Algorithm 2), whose role is to guarantee some global exploration of the entire parameter space . Indeed, at every support updating time , the ability of to escape from a local mode of the mapping to start exploring a higher mode will typically depend exclusively on the distribution used within Algorithm G_Exp. If this distribution is poorly chosen then may be stuck in the same local mode while processing a large number of observations.

An important feature of the proposed approach is that we have a lot of flexibility to build this distribution , since it can be any distribution on whose definition does not depend on the future observations . As illustrated in Sections 4.2–4.3, for small dimensional problems (for , say) a simple random search approach (see e.g. Algorithm 5) usually enables to quickly reach a small neighbourhood of , with a reasonable computational budget. However, in practice, even for moderate values of reaching quickly the global mode of the objective function will typically require that the problem at hand has some special structure that we can exploit to define . This approach to construct an efficient problem specific Algorithm G_Exp is illustrated with the dimensional example of Section 4.4.

In addition to be used to explore new regions of the parameter space, some of the last elements of the support of , the auxiliary PPD, can be used to keep track of the most promising values of encountered so far, as we now explain. To this aim let and assume that is located in the global mode of the mapping . Then, due to the randomness of the observations, at support updating time there is a positive probability that the support of the main PPD leaves this mode. If this event occurs, we can facilitate the return of to the global mode at a subsequent date by including the parameter value in the support of the auxiliary PPD. However, at any time we do not know if, and when, the mode has been reached, and a practical version of the idea we just described is to use some elements of the support of the auxiliary PPD to store the modes of the objective function that have been the most recently visited by the algorithm. This idea is implemented for the numerical experiments of Section 4 (see Algorithm 5), where we explain how the quantities generated by Algorithm 3 can be used to guess when leaves a particular mode of the function to start exploring a new one.

3.2 The Algorithm L_Exp and the parameter

It is worth noting that, alone, the support points generated by mean of Algorithm L_Exp, used to locally explore , can perform some global exploration of the parameter space, since the definition (15) of and (16) of are such that while . In other words, the successive local explorations of performed on Lines 11 and 15/17 of Algorithm 3 may allow the support of the two sequences of PPDs to traverse an arbitrarily long distance. In particular, if the function has a single mode we expect these local explorations to be sufficient to gradually guide towards . As illustrated in Section 4.4, for some (multi-modal) problems we can indeed rely on this exploration mechanism to design a computationally cheap version of Algorithm G_Exp which enables to quickly reach a small neighbourhood of .

Given the condition (18) on imposed by the convergence results of Section 2.4, a natural ideal is to let with the integer as large as possible, given the available computational budget. However, having larger than the lower bound given in (18) may improve the finite sample performance of the estimator , since increasing allows the random point set L_Exp to perform a finer exploration of the ball . For instance, in practice it may be useful to take in order to perform a finer exploration of along some specific directions of interest, which can be specified through the distribution used within Algorithm L_Exp. As illustrated with the example of Section 4.4, this approach can be applied in some problems to improve the finite sample estimation of some components of .

3.3 The parameter

The parameter is an important parameter of the algorithm, since its value influences both the speed at which the time between two support updates converges to (see (14)) and , the lower bound (18) on required by Corollary 1 to ensure that converges to at rate , a.s.

More precisely, increasing reduces and thus enables the conclusion of Corollary 1 to hold for a smaller value of . In addition, increasing may improve the finite sample properties of . Indeed, as gets larger the support updates become more frequent, which may reduce the number of iterations needed by the algorithm to reach a small neighbourhood of (see Section 4.4 for an example). On the other hand, due to the computational cost caused by the support updates, Algorithm 3 becomes slower as we increase .

However, if we are only interested in the value of associated to a fixed number of observations, for reasons explained in Remark 1 we observed that increasing has only a moderate impact on the running time of the algorithm. Consequently, for offline estimation problems it is often computationally feasible to choose a value for this parameter which is close to one. For instance, in all the experiments of Section 4 we take .

3.4 The parameters and

The parameter appears in the logarithmic term of the convergence rate of given in Corollary 1 and therefore it is sensible to set it close to 0, e.g. . Parameter influences the rate at which (see (15)). Noting that at the support updating time we have , it follows that decreases very slowly with the number of observations that we process, for every . For this reason, in practice we observed that this parameter has little influence on the behaviour of . As a default approach, we suggest to make this rate as fast as possible by setting close to its admissible lower bound, e.g. .

3.5 Scaling of the components of

In some applications it may be useful to rescale some components of to ensure that, for a finite sample size , the resulting distribution provides a good approximation of the distribution we aim at estimating.

To explain this point precisely we let and assume that the model is well-specified, so that . In addition, instead of estimating in the model we consider the alternative but equivalent model , with . Remark that is the target parameter value in this alternative model. To simplify the presentation we focus below on the subsequence for estimating .

Let and assume that at support updating time the new support is generated in (that is, assume that in Algorithm 3). Assume also that . Then, all what Algorithm L_Exp ensures is that the new support contains at least one element in the ball , and thus that the estimate may belong to this set. Simple computations show that for some constant , and consequently, under the above assumptions, at support updating time the support update can at best ensure that at time it is possible to have

| (21) |

However, in term of statistical learning, an error of size may or may not be large, depending on the problem at hand. To clarify this point, for every we let be the Kullback-Leibler (KL) divergence between the distributions and , and assume that there exist constants and such that for all while for all .

Then, since the implication (21) holds only if , it follows that, in this example, as long as is such that there is no guarantee that seeing more observations will allow to reduce the KL divergence between the estimated distribution and the target distribution . Notice that as increases the condition holds for smaller values of , which enables the above implication to hold for smaller sample sizes. However, if is too large then the mapping will vary slowly with and, informally speaking, the modes of this function that we aim at maximizing will be far apart. In this case, an important number of support updates may be needed for to reach a small neighbourhood of the target parameter value .

To sum up, both when is too small and too large, a large sample size may be required to guarantee that the estimated distribution is close to the target distribution , in the sense of the KL divergence. In practice, we observe that it is usually a sign that is too small when multiple runs of Algorithm 3 return very different values for . This observation was expected since, as argued above, if is too small then the sample size may not be large enough to enable to estimate well the distribution , in which case several parameter values may provide an equally good (or poor) approximation of this latter distribution.

Following a similar argument as above, when it may be worth rescaling some components of , that is to consider the alternative model for some well-chosen constants , instead of estimating in the original model . This strategy will be adopted for the real data example of Section 4.4.4.

4 Numerical experiments

The main objective of the examples below is threefold. First, it is to illustrate on a simple example the ability of the sequence to explore different modes of the objective function and to concentrate on the highest one at rate (Section 4.2). Second, it is to illustrate the result of Corollary 1, and notably to confirm that there exists a problem specific lower bound on that needs to be reached to enable to converge towards at rate . Lastly, it is to demonstrate the usefulness of the proposed approach to tackle challenging estimation problems (Sections 4.3-4.4).

Throughout this section we let and , for reasons explained in Sections 3.3-3.4. In addition, we let in (14), so that the first support update occurs after 5 observations, while .

4.1 Implementation of Algorithm 3 for the examples of Sections 4.2–4.3

For these two examples we let for some integers , and such that , and we consider the version of Algorithms L_Exp and G_Exp given in Algorithms 4 and 5, respectively. In Algorithm 5 the notation is used to denote the cardinality of the finite set defined on Line 3.

It is worth noting that in Algorithm 5 the exploration of the whole parameter space relies entirely on random draws from a Student’s t-distribution. In addition, this algorithm is such that elements of the new support , generated at support updating time , are used to store the value of at the last values of for which we had . If then the support is completed using random draws from the distribution. For reasons explained in Section 3.1, this implementation of Algorithm G_Exp aims at keeping track of the modes of the objective function that have been the most recently visited by the estimator , with each support updating time such that being interpreted as a mode switching time.

Notice that we only consider the case where is such that since the algorithm is used only for such values of . Obvious convention is used when and when

4.2 An illustrative example

We let

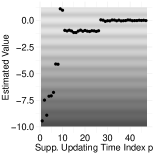

where , is the density of the distribution, and where for all . We generate observations from , with . Note that for all we expect to be approximatively a local maximizer of the objective function (see Figure 11(a) for a visual confirmation of this assertion). For this example we run Algorithm 3 with , , with the Algorithms L_Exp and G_Exp as defined in Algorithms 4-5 for , and by letting the initial values and be random draws from the distribution. We stress that this implementation of Algorithm 3 is not designed to learn efficiently but to generate a sequence that, visually, illustrates well the ability of the proposed estimator to visit several modes of the objective function before concentrating on at the fast rate .

Figure 11(a) shows the value of for obtained from a single run of Algorithm 3, where is the number of support updates needed to process the observations. Given the chosen initial values of the algorithm, when is small we see that is negative and far away from . However, as increases, the value of increases and, in particular, the 8th support update (performed at time ) enables to jump from the mode to the mode . Thanks to 10th support update (performed at time ), the estimate leaves this local mode and start exploring the mode . We then see that 16 support updates, representing about 1 400 iterations of Algorithm 3, are needed for to escape this mode and to eventually reach the global mode located at . Afterwards, remains in this global mode and concentrates on at rate , as shown in Figure 11(b) where the value of for is reported. Remark that the results in Figure 11(b) suggest that, for this example, the conclusion of Corollary 1 holds for .

4.3 Hyperbolastic growth model H1

We let be a sequence of -valued random variables and assume that, for all and , the conditional distribution of given belongs to where, for all , denotes the density of the distribution with the hyperbolastic function of type I, defined by

The function , introduced by Tabatabai et al., (2005), has proved to be useful e.g. to model the growth of some tumours (Eby et al.,, 2010) or to model the long term behaviour of the US healthcare expenditure (Guemmegne et al.,, 2014).

We simulate observations as follows:

where the function on the interval is represented in Figure 22(a). Notice that for this example we have and for all .

To assess the difficulty of estimating in this model we first use the SA algorithm (1) to learn this parameter value from the initial observations. To this aim we generate starting values at random from the distribution and, for each of them, we compute for every the quantity

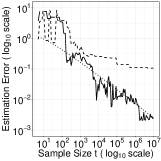

where is the log-likelihood function of the sample and where and are computed using (1) with learning rate . Theoretical results for the SA algorithm (1) with learning rate of this form can be found e.g. in Polyak and Juditsky, (1992); Shamir and Zhang, (2013). Finally, for each starting value we retain as an estimate of the element that maximizes the likelihood function of the sample, that is which is such that we have for all .

The resulting values of are presented in Figure 22(b), where a close look at these simulation results reveals that the estimation error is larger than one for 97.22% of the considered starting values and larger than 10 for 27.72% of them. This shows that learning in this model with SA is challenging, which may be due to the fact that the mapping has several local maxima.

We now consider Algorithm 3 with the default instance of Algorithms L_Exp and G_Exp given in Algorithms 4-5. For this example we let , with , and we let the initial values and be random draws from the distribution. Notice that the initial values of Algorithm 3 are generated in the same way as those used above for the SA algorithm (1). Lastly, we set in (14) and (16).

To assess the ability of to quickly reach a small neighbourhood of we consider 100 independent runs of Algorithm 3 using the first observations only. The corresponding values of , obtained with , are given in Figure 22(b). For a close look at the simulation results show that the estimation error is smaller than one in 91 out of 100 runs of the algorithm, and that its median value is about 0.39. When the sample size is increased to we see from Figure 22(b) that the estimation error is smaller than 0.1 in all cases but one, where it is approximatively equal to 26. This large value of obtained after observations confirms that finding the global maximum of the function is a difficult problem, as already suggested by the results obtained with the SA algorithm.

To illustrate the convergence property (2) of the estimator we report, in Figure 22(c), the estimation error for obtained from a single run of Algorithm 3. Contrary to what we observed in the previous example, for the estimator does not appear to converge to at rate . By contrast, for the estimation error decreases at the rate predicted by Corollary 1. As suggested by Corollary 1, these results confirm that there exists a problem specific lower bound on that needs to be reached for to converge towards at rate .

4.4 Student-t linear regression model

In this example we consider a sequence of real-valued random variables and a sequence of -valued random variables, and let for all . We let and assume that, for all and , the conditional distribution of given belongs to where, for all ,

| (22) |

The Student-t linear regression model (22) is useful to model data that exhibits a heavy tail behaviour. In addition, estimators of the regression coefficient based on (22) have usually the advantage to be less sensitive to outliers than the ordinary least square (OLS) estimator (Lange et al.,, 1989). The degree of robustness depends on the parameter , with smaller implying more robustness, whose estimation is known to be a difficult problem. For instance, Fernández and Steel, (1999) show that the likelihood function may tend to infinity as while, in a Bayesian setting, the posterior distribution may be improper if the prior distribution for is improper. These observations have motivated the development of specific methods for parameter inference in (22), see e.g. He et al., (2020) and references therein.

4.4.1 Algorithm specification

The dimension of that we will consider in what follows is too large for the default instance of Algorithm G_Exp proposed in Algorithm 5 to enable to reach quickly the highest mode of the mapping at a reasonable computational cost (i.e. for a reasonable value of ).

However, as we now explain, we can exploit the particular structure of the problem at hand to define a version of Algorithm G_Exp which is suitable to Student-t linear regression models. To do so remark first that the tails of the distribution depend only on the parameters and while, for a fixed , the mean of this distribution depends only on the parameter . Hence, we can expect the estimated value of to be not too sensitive to that of , and vice versa. This informal reasoning suggests that a small neighbourhood of can be found by exploring the 2-dimensional space to reach a small ball around and by exploring the -dimensional space to find a small neighbourhood of . Typically, in real life applications the number of covariates is too large to explore the whole space at a reasonable computational budget. However, noting that for a fixed value of the function is uni-modal, we can expect that the successive local explorations of performed by Algorithm L_Exp are enough to reach a small neighbourhood of (see the discussion of Section 3.2). This argument suggests that an efficient exploration of the whole space by Algorithm G_Exp is not needed to enable to be close to for moderate values of .

Following the above reasoning, the version of Algorithm G_Exp that we consider in this example amounts to replacing Line 5 of Algorithm 5 by the following line 4’:

4’: Let and be such that and write . Then, let

-

•

Let

-

•

For , let

where denotes the first points of the nested scrambled Sobol sequence in .

We recall the reader that if are the first points of the nested scrambled Sobol sequence in then for all and, -a.s., the point set covers the square more evenly than a sample of i.i.d. random draws from the distribution (see e.g. Dick and Pillichshammer,, 2010, for a formal definition of the nested scrambled Sobol sequence).

To complete the specification of Algorithm 3 we propose a version of Algorithm L_Exp that performs a particularly fine local exploration of along the components of , with the goal of improving the finite sample behaviour of the estimator . To this aim we let for some and the proposed version of Algorithm L_Exp amounts to adding the following line 14 in Algorithm 4:

12: Writing with , let

4.4.2 Simulated data without outliers

We simulate observations as follows:

where is a random draw from the Wishart distribution with degrees of freedom and scale matrix , and where with a random draw from the distribution. Notice that in this example there are parameters to estimate.

As for the previous example, to assess the difficulty of the estimation problem we first consider learning using the SA algorithm (1) from the initial observations. More precisely, we generate initial values by sampling from , the distribution we will use to generate the initial values of Algorithm 3 (see Section 4.4.1). Then, for each starting value we compute the estimate of , as defined in Section 4.3.

The resulting values of are presented in Figure 33(a). The estimation error is larger than one for of the considered staring values, and larger than 10 for 85.6% of them. In particular, a closer look at the simulation results reveals that in most cases (i.e. for 89.67% of the considered staring values) using as an estimate of yields to an overestimation of both and of . This observation is not surprising since, the tails of the distribution becoming thinner as decreases and as increases, a smaller value of can be, to some extend, compensated by a lower value of . From these results we conclude that, for this model, learning with SA is a challenging problem, probably because the function has several local maxima.

We now consider the version of Algorithm 3 introduced in Section 4.4.1, with and . To assess the ability of to reach a small neighbourhood of for a moderate sample size we consider 50 independent runs of Algorithm 3 with and using, as for the experiments with the SA algorithm, the first observations only. The resulting values of are given in Figure 33(a). For the estimation error is smaller than 1.03 in all the experiments, and its mean value is about 0.46. As explained in Section 3.3, decreasing reduces the number of support updates performed to process a given number of observations, and can therefore increase the time needed for to reach a small neighbourhood of . This phenomenon is illustrated with the results of Figure 33(a), where we observe that the estimation error tends to be much larger with than with . In particular, in this problem reducing from 0.95 to 0.9 increases the median value of from 0.48 to 1.45. To sum-up, these results suggest that the version of Algorithms L_Exp and G_Exp proposed in Section 4.4.1, together with frequent support updates (i.e. with ), enable to efficiently guide towards .

Figure 33(b) shows the value of for , obtained from a single run of Algorithm 3. We observe that until time the estimation error is approximately constant and larger than , suggesting that is initially stuck in a local mode of the function . Around time , the value of drops to about , which may indicate that a higher mode of the objective function has been found. However, at time , the estimate goes back to the mode , because at this sample size the number of observations processed between two support updates is not large enough to distinguish for sure which of the two modes or is the highest. However, quickly returns to the mode and never visits again the mode . Instead, the value of decreases quickly between time and time (from approximately 1 to 0.23). The value of then remains approximately constant up to time before decreasing at rate , suggesting that for this example the conclusion of Corollary 1 holds for . Lastly, it is worth mentioning that the additional local exploration of along the components of , performed by the version of Algorithm L_Exp that we consider for this model, successfully allowed to learn particularly well . Indeed, the value of is a bout 9 times smaller than that of , where the factor is used to make the two estimation errors comparable.

4.4.3 Simulated data with outliers

It is well-known that the MLE of in the model (22) is less sensitive to the presence of outliers than the OLS estimator (see e.g. Lange et al.,, 1989), where as mentioned above the degree of robustness to outliers depends on (the smaller is the more robust the MLE for is). Hence, the joint estimation of by maximum likelihood provides an adaptive robust procedure to estimate , in the sense that the appropriate degree of robustness is learnt from the data (Lange et al.,, 1989).

To investigate if the proposed approach can be used as an adaptive robust procedure to estimate we now introduce outliers in the dataset used Section 4.4.2 by replacing, for each and with probability 0.02, the sixth component of by a random draw from the distribution. We then consider 50 independent runs of Algorithm 3 (implemented as in Section 4.4.2) using the first observations only, and for each value of we compute the distance . These 50 estimation errors are then compared with , the estimation error obtained with the OLS estimator.

The results are presented in Figure 33(c), from which we observe that is much less sensitive to the outliers than the OLS estimator. Notably, the maximum value of over the 50 runs of Algorithm 3 is only 0.69, and is therefore approximately 8.7 times smaller than the estimation error obtained with the OLS estimator. The 50 corresponding estimates of belong all to the interval . Recalling that , this shows that, as for the maximum likelihood estimation method, the robustness of the proposed approach to estimate in presence of outliers goes together with an underestimation of .

4.4.4 Airbnb data

We end this section with a real data application of the proposed online algorithm for parameter inference in Student-t linear regression models. To this aim we consider data on airbnb rental transactions in the city of New York for the period March 2018–December 2018111The data can be downloaded here: http://insideairbnb.com/get-the-data.html, resulting in a sample of observations. We let be the log-rental prices and, after data preprocessing and a variables selection step, for all we let where a vector of seven features, listed in Table 1. The scaling factors appearing in the definition of these features are introduced for the reasons explained in Section 3.5 and have simply be chosen so that the OLS estimate of each regression coefficient belongs to the interval . For this real data example, where , Algorithm 3 is implemented as in Section 4.4.1, with and , and the observations are randomly permuted before proceeding to the estimation of .

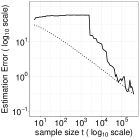

Figure 3(d) shows the values of obtained from 50 runs of Algorithm 3. We observe that the estimated parameter values are quite similar across the different runs of Algorithm 3, although some variability is observed. Notice that all the values of fall in the interval . By comparison, the OLS estimate of is provided in Table 1. The main difference between and the values of reported in Figure 3(d) concerns the estimation of the parameter , associated to the number of bedrooms available in the accommodation (see also Table 1, where the component-wise median is reported). Indeed, while the OLS estimate of is positive, 34 out of the 50 runs of Algorithm 3 produced a negative estimated value for this parameter. We note that, based on its OLS estimate, is the second least significant parameter of the model (although it is significant at the 1% level), and learning its value on the fly may therefore be challenging. It is also worth mentioning that if a negative value for is judged as being not realistic then we can easily facilitate the estimation of this parameter by restricting the parameter space in such a way that for all .

To assess the convergence of the 50th run of Algorithm 3 we report, in Figure 3(f), the value of for . The results in this plot show that around time the estimate jumps to a new region of the parameter space and start converging to the parameter value . For large values of the quantity decreases to zero at the predicted rate, which indicates that the sequence is converging to a specific parameter value.

| Without outliers | With outliers | |||

|---|---|---|---|---|

| Intercept | 2.25 | 2.18 | 2.25 | 2.12 |

| (Min. numb. of nights)/1000 | 1.49 | 1.50 | 1.38 | 1.06 |

| (Numb. of reviews)/1000 | -1.44 | -1.24 | -1.41 | -1.43 |

| (Score location)/10 | 1.21 | 1.37 | 1.15 | 1.49 |

| (Numb. of amenities)/1000 | 6.26 | 3.50 | 8.82 | 1.52 |

| (Host duration)/1000 | 0.06 | 0.03 | 0.05 | 0.04 |

| (Numb. of persons)/10 | 2.23 | 2.54 | 1.03 | 2.06 |

| (Numb. of bedrooms)/100 | 2.98 | -2.02 | 23.65 | 4.57 |

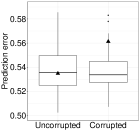

To compare further the estimates produced by Algorithm 3 with the OLS estimator we consider the observations of January 2019 as a test set, and compute for each estimates of the average prediction error . The 50 values of , as well as the value of , are given in Figure 3(f). We observe that the median value of coincides almost exactly with the OLS prediction error , and that the distribution of is nearly symmetric around its median.

It is worth mentioning that if there are no outliers in the data then we expect the OLS estimator to have good statistical properties and, in particular, to outperform the online estimator . If the above results tend to confirm this assertion they also show that, in absence of outliers, compared to in a satisfactory way.

We now corrupt the dataset by replacing, for every and with probability 0.02, the 7th component of by a random draw from the distribution, where 0.1 and 2 are, respectively, the smallest and the largest observed value for this covariate. From Table 1, where the value of is reported, we observe that this corruption of the dataset has decreased the estimated value of and increased that . The former effect was expected, since the corruption of the data has globally increased the value of the 7th component of . Informally speaking, and being regression coefficients associated to two highly correlated features, namely the number of persons the accommodation can host and the number of bedrooms available, the OLS estimator has increased the estimated value of to compensate the decrease in that of . In Table 1 we also report the component-wise median of , computed from 50 independent runs of Algorithm 3. We observe that, as for the OLS estimator, the estimated value of has decreased and that of has increased. However, the changes in the estimated regression coefficients are much smaller than for the OLS estimator. The corresponding values of , as well as the value of , are given in Figure 3(f). From this plot we see that the presence of outliers has increased the OLS prediction error from 0.53 to 0.56. By contrast, corrupting the observations has only slightly increased the prediction error of . In particular, if with the original dataset we have for exactly half of the 50 values of , with the corrupted dataset this is the case in only 4 out of the 50 runs of Algorithm 3. Lastly, we note that, as in Section 4.4.3, the presence of outliers tends to reduce the estimated value of . For instance, the mean (resp. median) value of has decreased from 9.98 to 5.71 (resp. from 9.77 to 5.29) with the corruption of the data.

The results in Table 1 and in Figure 3(f) provide a real data confirmation of the robustness properties of the estimator that was observed in Section 4.4.3. Studying further the robustness properties of this estimator, or comparing its performance with that of alternative robust estimation methods, is however beyond the scope the paper.

5 Conclusion

A natural idea to make the proposed approach scalable w.r.t. the dimension of the parameter space is to replace the local exploration of performed by Algorithm L_Exp by a random variable evolving according to SA steps, as in (1). To understand why this idea cannot be readily applied within the proposed algorithm let for every and consider a pure online setting where each observation is read only once. Then, since the value of changes after each observation, for every the only available approximation of is the estimate based on a single observation. Consequently, it is unclear how the mode around which evolves can be compared with those discovered by Algorithm G_Exp, whose objective is to find the highest mode of the objective function . Future research should aim at addressing this problem, with the goal of constructing an online procedure for multi-modal models whose computational requirement to estimate at rate grows linearly with .

As a final comment we stress that, as the dimension of increases, ensuring that the global mode is reached with a given probability after iterations will generally require a computational effort that grows exponentially fast. Consequently, even for moderate values of , efficient online learning with a multi-modal likelihood function is a realistic goal only for models having a particular structure, which can be exploited to facilitate the search of the highest mode of the mapping .

References

- Dick and Pillichshammer, (2010) Dick, J. and Pillichshammer, F. (2010). Digital Nets and Sequences: Discrepancy Theory and Quasi-Monte Carlo Integration. Cambridge University Press.

- Eby et al., (2010) Eby, W. M., Tabatabai, M. A., and Bursac, Z. (2010). Hyperbolastic modeling of tumor growth with a combined treatment of iodoacetate and dimethylsulphoxide. BMC cancer, 10(1):509.

- Fernández and Steel, (1999) Fernández, C. and Steel, M. F. (1999). Multivariate student-t regression models: Pitfalls and inference. Biometrika, 86(1):153–167.

- Guemmegne et al., (2014) Guemmegne, J., Kengwoung-Keumo, J., Tabatabai, M., and Singh, K. (2014). Modeling the dynamics of the us healthcare expenditure using a hyperbolastic function. Advances and applications in statistics, 42(2):95.

- He et al., (2020) He, D., Sun, D., and He, L. (2020). Objective bayesian analysis for the student- linear regression. Bayesian Analysis.

- Kleijn and van der Vaart, (2012) Kleijn, B. and van der Vaart, A. (2012). The Bernstein-von-Mises theorem under misspecification. Electronic Journal of Statistics, 6:354–381.

- Lange et al., (1989) Lange, K. L., Little, R. J., and Taylor, J. M. (1989). Robust statistical modeling using the t distribution. Journal of the American Statistical Association, 84(408):881–896.

- Lei et al., (2019) Lei, Y., Hu, T., Li, G., and Tang, K. (2019). Stochastic gradient descent for nonconvex learning without bounded gradient assumptions. IEEE Transactions on Neural Networks and Learning Systems.

- O’Callaghan et al., (2002) O’Callaghan, L., Mishra, N., Meyerson, A., Guha, S., and Motwani, R. (2002). Streaming-data algorithms for high-quality clustering. In Data Engineering, 2002. Proceedings. 18th International Conference on, pages 685–694. IEEE.

- Pesme and Flammarion, (2020) Pesme, S. and Flammarion, N. (2020). Online robust regression via sgd on the l1 loss. arXiv preprint arXiv:2007.00399.

- Polyak and Juditsky, (1992) Polyak, B. T. and Juditsky, A. B. (1992). Acceleration of stochastic approximation by averaging. SIAM journal on control and optimization, 30(4):838–855.

- Shamir and Zhang, (2013) Shamir, O. and Zhang, T. (2013). Stochastic gradient descent for non-smooth optimization: Convergence results and optimal averaging schemes. In International conference on machine learning, pages 71–79.

- Tabatabai et al., (2005) Tabatabai, M., Williams, D. K., and Bursac, Z. (2005). Hyperbolastic growth models: theory and application. Theoretical Biology and Medical Modelling, 2(1):14.

- Toulis and Airoldi, (2015) Toulis, P. and Airoldi, E. M. (2015). Scalable estimation strategies based on stochastic approximations: classical results and new insights. Statistics and computing, 25(4):781–795.

- Toulis et al., (2017) Toulis, P., Airoldi, E. M., et al. (2017). Asymptotic and finite-sample properties of estimators based on stochastic gradients. The Annals of Statistics, 45(4):1694–1727.

- van der Vaart, (1998) van der Vaart, A. W. (1998). Asymptotic statistics, volume 3 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge.

See pages - of supplement.pdf