Pricing of debt and equity in a financial network with comonotonic endowments

Abstract

In this paper we present formulas for the valuation of debt and equity of firms in a financial network under comonotonic endowments. We demonstrate that the comonotonic setting provides a lower bound and Jensen’s inequality provides an upper bound to the price of debt under Eisenberg-Noe financial networks with bankruptcy costs. Such financial networks encode the interconnection of firms through debt claims. The proposed pricing formulas consider the realized, endogenous, recovery rate on debt claims. We endogenously construct the comonotonic endowment setting from a equity maximizing standpoint with capital transfers. We conclude by, numerically, comparing the network valuation problem with two single firm baseline heuristics which can, respectively, approximate the price of debt and equity.

1 Introduction

Valuation adjustments, especially credit valuation adjustment [CVA], have become an important part of derivative valuation by any bank since the 2007-2009 financial crisis. CVA proposes an adjustment to the “traditional” price of a derivative, as in the seminal paper of Merton (1974), to account for counterparty risk of the instrument. However, CVA does not take into account the full network of interconnections that exist within a financial system. As evidenced by the 2007-2009 financial crisis, considering the risk of a single firm alone can cause gross misspecification in firm health. In this work, we will focus on interconnections through correlated assets as well as interbank debt claims. These interconnections effectively link the balance sheets of different banks and make the value of a firm dependent on the performance of other firms. These shared connections might open up avenues for shared prosperity but also introduce potential channels for contagion. These avenues of contagion become particularly significant during a financial crisis where the default of one firm might cause the failure in other firms. This effect is also referred to as cascading defaults.

The rest of the paper is organized as follows. A review of relevant literature is provided in Section 1.1. Detailed motivation for the comonotonic endowment setting, which is central to this work, is provided in Section 1.2. The primary innovations of this paper are highlighted in Section 1.3. In Section 2 we provide a description of our mathematical setting and necessary background on the Eisenberg-Noe framework. Section 3 considers network clearing when firms have comonotonic endowments. We provide the expectation of the equilibrium payments, equity, and wealth. Further, we prove that these expected values can provide upper and lower bounds for the general random endowment setting of, e.g., Gouriéroux et al. (2012); Barucca et al. (2020) in Section 4. Section 5 considers simple comparative statics of the provided valuations with respect to the different system parameters under a lognormal setting for clear comparisons to Merton (1974). Section 6 concludes. All proofs can be found in Online Appendix J.

1.1 Literature review

Since the 2007-2009 financial crisis there have been significant efforts to study the effects of interconnection within the financial system, with particular emphasis on modeling and quantifying systemic risk. One of the primary approaches for modeling systemic risk is fundamentally network-based. The seminal paper Eisenberg and Noe (2001) models these financial dependencies as a directed graph. In this approach, firms must meet their full liabilities by transferring their assets, otherwise they are deemed insolvent and are unable to pay out in full. This inability to make the full payment can, in turn, make other banks default, thus resulting in cascading failures. This interdependency of realized (clearing) payments is modeled as a fixed point problem. Eisenberg and Noe (2001) prove the existence and uniqueness of the clearing payments and provides an elegant algorithm for the computation of the same. This baseline setting of Eisenberg-Noe has been extended in many directions to account for more realistic situations. Interconnections through cross-holdings have been considered in Suzuki (2002); Gouriéroux et al. (2012, 2013). Realistic default mechanisms in the form of bankruptcy cost has been studied in Elsinger (2009); Rogers and Veraart (2013); Glasserman and Young (2015); Weber and Weske (2017); Capponi et al. (2016); Veraart (2020). Central banks and regulatory bodies have incorporated these network models into their stress tests of the financial system (see, e.g., Anand et al. (2014); Hałaj and Kok (2015); Elsinger et al. (2013); Upper (2011); Gai et al. (2011)). As such, valuing claims that take the full network effects into account is imperative so that the true risk of the claims are also taken into account. And, in fact, Siebenbrunner and Sigmund (2018) concludes, empirically, that at present financial contagion is not priced into interbank markets; as such, the focus of this work is on a network valuation adjustment scheme [NVA] to determine what prices should be if markets were to accurately price such contagion. The NVA approach is closely related to the work of Cossin and Schellhorn (2007) which constructs a network of obligations with infinite maturity and in which debts are refinanced at time of default. In this work we construct a tractable NVA approach specifically in an Eisenberg-Noe framework.

The NVA approach in an Eisenberg-Noe framework was, to our knowledge, first considered in Gouriéroux et al. (2012) and extended to more general clearing mechanisms in Barucca et al. (2020). We wish to note that the general methodology of NVA in the Eisenberg-Noe framework, as studied in Gouriéroux et al. (2012), requires partitioning the endowment space into possible default scenarios in a system with banks. Therefore computing the expectation suffers from the curse of dimensionality and is typically computationally intractable for realistic systems. In fact, a common thread of the existing literature is that explicit, analytical solutions are considered only for cases with either no direct interconnection between firms or where the number of firms in the system is very low. Further complications arise if we consider bankruptcy costs along the lines of Rogers and Veraart (2013). Without bankruptcy costs, the default scenarios result in the partition of the bank endowment space into mutually exclusive and convex regions. However, in the presence of bankruptcy costs, these partitioned regions are not, in general, convex. We refer the reader to Online Appendix B for elucidation of this point. Providing any analytical solution in this case becomes very challenging even in small systems (as has been highlighted in past works such as Suzuki (2002)). Hence a numerical approach has been generally followed, i.e., via Monte Carlo simulations.

1.2 Motivation for comonotonic endowments

We note, first, that the problem of finding the expectation of the clearing wealths and payments under (integrable and nonnegative) random endowments was considered in Gouriéroux et al. (2012) in the case of no bankruptcy costs () but with cross-ownership. We replicate those results and extend them to consider the case with bankruptcy costs in Online Appendix B. However, in this work we focus on a financial system in which banks hold comonotonic endowments; this is used directly in Section 3 and as bounds for the general setting in Section 4. Briefly, a random vector is called comonotonic if it is equal in distribution to for some random variable and nondecreasing function ; this is formalized in Section 2.2. There are three complementary motivating justifications for the comonotonic endowment setting fundamental to this work: theoretical, empirical, and computational.

-

(i)

Portfolio optimization: First, as is standard in the literature, if all firms are portfolio optimizers and do not take any other firm’s investments into account, the chosen endowments will all be countermonotonic to the pricing kernel (see, e.g., Peleg and Yaari (1975)). Formally, we wish to consider the risk-sharing equilibrium problem of Bühlmann (1980, 1984); this problem, under a finite probability space, is equivalent to the Arrow-Debreu equilibrium Arrow and Debreu (1954) (see, e.g., Anthropelos and Kardaras (2017); Bichuch and Feinstein (2020)). Let denote a probability space describing the financial market of utility maximizing agents. Agent has some initial (uniformly bounded random) endowment which she can trade with the other agents so as to maximize her own expected utility . A Bühlmann equilibrium is a pair so that

-

(a)

utility maximizing: for every agent , and

-

(b)

market clearing: .

As proven in Lemma 3 of Tsanakas and Christofides (2006), any equilibrium vector of portfolio holdings will be comonotonic. The details of this argument can be found in Online Appendix I. In fact, Tsanakas and Christofides (2006) proves the comonotonicity of the portfolio holdings even with (potentially heterogeneous) distortions on the probability measure which can account for, e.g., ambiguity aversion of the economic agents.

-

(a)

-

(ii)

Empirical correlations: The empirical evidence shows that the bank assets exhibit a very high degree of rank correlation. The Spearman correlations of the daily returns (adjusted for dividends and stock splits) for five U.S. banks (JP Morgan Chase and Co, Goldman Sachs Group, Bank of America Corporation, Morgan Stanley, and Citigroup Inc.) are shown in Table 1 from January 1, 2015 to December 31, 2020. This notion of a homophilic financial system is reported in US and German banking systems by Elliott et al. (2021): “Banks often have similar real exposures to their financial counterparties.”

Name Ticker JPM GS BAC MS C JP Morgan Chase and Co JPM 1.00 0.82 0.88 0.85 0.87 Goldman Sachs GS 0.82 1.00 0.81 0.86 0.81 Bank of America Corporation BAC 0.88 0.81 1.00 0.84 0.87 Morgan Stanley MS 0.85 0.86 0.84 1.00 0.83 Citigroup Inc C 0.87 0.81 0.87 0.83 1.00 Table 1: Spearman correlations of the daily returns for five large U.S. institutions. -

(iii)

Computational and analytical tractability: The general random endowment setting with , as considered in Gouriéroux et al. (2012), requires computing the measure of regions in . This would typically require Monte Carlo simulation and suffer greatly from the curse of dimensionality. The comonotonic framework, in contrast, requires computing the measure of only intervals in ; this is tractable both computationally and analytically. As such, the comonotonic framework allows for resilience and stability analysis as considered in Acemoglu et al. (2015). That work restricts the network topologies to those constructed from ring and completely connected networks with i.i.d. Bernoulli shocks; by considering comonotonic endowments instead, we are able to analytically study resilience and stability for general network topologies and more general shock types. In particular, in Section 4, we will demonstrate that we are able to provide lower and upper bounds on the expectation of the system behavior under any random endowment using the comonotonic setting. This is considered in the special case of a common, systematic, shock with idiosyncratic shocks in Online Appendix G. By focusing on the comonotonic framework, we are able to take advantage of the tractable analytical results with at most intervals for consideration.

1.3 Primary contributions

In light of the aforementioned analytical and computational limitations to NVA in the current literature, and with the highlighted motivations in Section 1.2, we define and study the price of debt and equity under comonotonic endowments. Within this work, we broadly equate prices with expectations. That is, up to discounting, the expected payments of a total obligation is viewed as the price of debt and the expected equity is viewed as the price of equity. This is made explicit in Section 5 with the use of discounting and a risk-neutral measure . The primary contributions of this paper are as follows:

-

(i)

We formulate an analytical formulation for NVA under the comonotonic endowment setting in Section 3. In this setting, the default regions can be characterized by at most intervals on and become tractable analytically. This tractability extends to the case where bankruptcy costs are considered; this is in contrast to prior considerations of NVA, such as Gouriéroux et al. (2012), in which nonconvex regions need to be evaluated (see Online Appendix B). Thus the comonotonic setting allows us to explore the network effects from an analytical perspective.

-

(ii)

Under the comonotonic framework, we are able to provide bounds on the expectation of the system behavior under any general random endowment. The lower bound assumes particular importance from a stress-testing perspective and for assessing systemic risk in a financial network. While it may appear contradictory that banks would choose the riskiest scenario (as considered in the portfolio optimization motivation above and revisited specifically under the Eisenberg-Noe network setting in Corollary 4.6) the upside benefits for individual bank and sector equities outweigh, for the institutions themselves, the downside systemic risks for the system. The upper bound, by conditioning on a systematic factor, also follows a comonotonic endowment setting and thus the computational improvements can be applied for that bound as well.

-

(iii)

We provide special consideration to the analytical bounds for the setting in which the shocks to the banking sector can be decomposed into a systematic component felt (heterogeneously) by all firms and an idiosyncratic component. The lower bound, in particular, can be used to perform stress-testing and assess the health of the system. In doing so, we are able to quantify the effects of diversity of investment strategies on pricing and, therefore, also systemic risk. By deconstructing the returns of any bank into the systematic or market component and the idiosyncratic component, we can recover the tradeoffs between systematic risk and idiosyncratic risks on systemic risk. This so-called diversity versus diversification problem is well-studied in the price-mediated contagion literature; we refer the interested reader to, e.g., Capponi and Weber (2021); Detering et al. (2020).

-

(iv)

From an application standpoint, we wish to note the comparison of the NVA setting to that taken in the single-firm setting by Merton (1974) (see, also, Online Appendix F). Numerical case studies are presented to study the comparative statics for the performance of the system with respect to important system parameters and highlight the difference with respect to Merton (1974). These illustrative exercises permit us to study the extent to which interbank networks impact prices through direct comparison to equivalent balance sheets without the network contagion effects. In fact, we construct two baseline heuristic balance sheets without financial networks in Section 5 which approximate the network effects on the price of debt and equity.

Though not undertaken in this work, our results allow for consideration of financial networks as in Acemoglu et al. (2015) to compare the health and stability of various network topologies to random shocks. In contrast to Acemoglu et al. (2015), this setting allows for the formulation of stability results under any network topology and not only the two stylized networks (ring and completely connected) undertaken in that work. We wish to highlight that, though the comonotonic setting may appear restrictive for this purpose, Acemoglu et al. (2015) imposes i.i.d. shocks to symmetric systems in order to obtain analytical results. As far as the authors are aware, one other work has analytically studied the stability and resilience of general network topologies; that work, Amini and Feinstein (2021), is based on the results presented herein in order to solve the optimal network compression problem under systematic shocks.

2 Setting

We begin with some simple notation that will be consistent for the entirety of this paper. Let for some positive integer , then

, and . Further, to ease notation, we will denote to be the -dimensional compact interval for . Similarly, we will consider if and only if . We will also make wide use of the vectors for . This vector is defined so that has a 1 in its element and 0 in all other elements.

2.1 Financial networks

Throughout this paper we will consider a network of financial institutions. Often we will consider an additional node , which encompasses the entirety of the financial system outside of the banks; this node will also be referred to as society or the societal node. We refer to Feinstein et al. (2017); Glasserman and Young (2015) for further discussion of the meaning and concepts behind the societal node.

In this paper, we consider obligations with a single maturity date, as considered in Eisenberg and Noe (2001). Any bank may have obligations to any other firm or society . We will assume that no firm has any obligations to itself, i.e., for all firms , and the society node has no liabilities at all, i.e., for all firms . Thus the total liabilities for bank is given by and relative liabilities from bank to bank is given by if and arbitrary otherwise; for simplicity, in the case that , we will let for all . Note that, for any firm , we recover the property that . Throughout this work we will consider the square matrix ; the relative liabilities from firm to the societal node can be defined as being . On the other side of the balance sheet, all firms are assumed to begin with some endowments for all .

The central question explored in the network models is the determination of the firm wealths after network clearing. Let the clearing wealths be given by . In this paper to determine the clearing wealths, we assume the following stylized rules, in adherence to the standard literature, i.e. Eisenberg and Noe (2001); Rogers and Veraart (2013):

-

(i)

Limited liabilities: the total payment made by any firm will never exceed the total assets available to the bank.

-

(ii)

Priority of debt claims: the shareholders of a firm receive no value unless all its debts are paid in full.

-

(iii)

All debts are of the same seniority: in case a bank defaults, debts are paid out in proportion to the size of the nominal claims.

Throughout this work we consider a system with some exogenous recovery rates in case of default, i.e. the model proposed in Rogers and Veraart (2013). This means if bank has negative wealth then it is defaulting and its assets are reduced with recovery rates on its external assets and on its interbank assets.

We will briefly define this setting mathematically, the details can be found in Eisenberg and Noe (2001); Rogers and Veraart (2013) and are replicated for our discussion in Online Appendix A. With the rules set, we formalize the clearing process in wealths to describe this system as

| (1) |

As such, the clearing procedure implies: if bank has nonnegative wealth then it is solvent and its wealth is equal to its total assets minus its total liabilities; if bank has negative wealth then it is defaulting and its assets are reduced by the recovery rates . From Rogers and Veraart (2013), we immediately recover a greatest and least clearing solution to within the lattice . We note that with (i.e. under no bankruptcy costs) we recover the model of Eisenberg and Noe (2001); if additionally all firms have obligations to the societal node (i.e. with for all firms ), then there exists a unique clearing solution in this setting.

Assumption 2.1.

For the remainder of this paper we will assume that all firms have obligations to the societal node (i.e. with for all firms ).

Throughout this work we will focus on the greatest clearing wealths solution . We choose this equilibrium as all firms and regulators, if given the choice, would prefer these clearing wealths to all others as no firm can improve on their performance beyond that given by . We wish to note that if the least clearing wealths were desired instead, all subsequent results of this paper would follow comparably.

Definition 2.2.

Define the mapping so that is the maximal clearing wealth solution under endowments . Further, define and to be the associated payments and equity.

2.2 Comonotonicity

For the remainder of this paper, we will consider a probability space . Denote by all measurable random variables. Further, denote by those random variables that have finite absolute expectation, i.e. if is measurable and . We will denote by those random variables that are almost surely nonnegative.

As highlighted in Section 1.2, within this work we will focus on comonotonic random vectors.

Definition 2.3 (Definition 4 of Dhaene et al. (2002)).

is comonotonic if it has comonotonic support, i.e. either or for any the smallest Borel set such that .

Rather than using the formal definition of comonotonicity given above, we will focus on a widely utilized equivalent formulation which comes from, e.g., Proposition 7.18 of McNeil et al. (2015).

Proposition 2.4 (Proposition 7.18 of McNeil et al. (2015)).

is comonotonic if and only if (i.e. equal in distribution) for some random variable and nondecreasing.

3 Expectations of debt and equity under comonotonic endowments

Consider the motivation expressed in Section 1.2 for a financial system with comonotonic endowments. With the justification that banks would choose comonotonic endowments in theory as well as the data to support this being (approximately) accurate, a general endowment space is not necessary for understanding systemic risk and financial contagion. As such, in this section we will consider comonotonic endowments. We will present herein the expectations and probability distributions under general comonotonic endowments. We wish to emphasize that in this paper, we consider a single maturity model along the lines of Eisenberg and Noe (2001); Rogers and Veraart (2013), i.e. the network is formed and fixed at time and all claims mature (and solvency is determined) at time .

Though all results of this section are presented as the expectation of clearing solutions under the probability measure , we consider these as pricing formulas. That is, up to discounting, we view the term as the price of debt and as the price of equity for bank with system endowments . In Section 5, we explicitly consider a market model with risk-neutral measure under which prices can be given. Throughout this work we, additionally, consider an effective interest rate as an equivalent measure for the price of debt; this interest rate for bank , under some pricing measure , is such that with risk-free rate and network maturity .

Definition 3.1.

Consider a financial network with maturity and a market with risk-free rate and prices determined by the probability measure . Define the effective interest rate on firm ’s debt by:

| (2) |

For bank , we can define as the risk premium along the lines of Merton (1974). Note that either the effective interest rate or the risk premium is often taken as the measure of the price of debt due to the monotonic relation between the expectation and the interest rate (see, e.g., Merton (1974)).

Assumption 3.2.

Throughout this section we will restrict our consideration to comonotonic nonnegative random vectors of endowments that are equal in distribution to for some nonnegative random variable and nondecreasing map .

3.1 Piecewise linear formulation of clearing wealths

From the fictitious default algorithm of Rogers and Veraart (2013) (see Corollary A.4) we are able to give a linear construction for the clearing vector provided the defaulting set is known. This is given by the following construction. We compare this linear structure to the directional derivative proposed in Liu and Staum (2010) and the “network multipliers” from Chen et al. (2016) when considering only the model of Eisenberg and Noe (2001), i.e. with full recovery (). For the remainder of this paper we will use the following definitions:

| (3) | ||||

| (4) |

for denoting the set of defaulting institutions as in the fictitious default algorithm. Thus

for any endowment by construction.

Remark 3.3.

The results of this work can be compared to those from Gouriéroux et al. (2012) with cross-ownership of equity. In that setting the ownership of equity is denoted by where bank owns of bank ’s equity. Under the assumption that no firm has sold off all of its equity to other firms within the financial system, we consider only the case that . Though Gouriéroux et al. (2012) does not consider bankruptcy costs, we allow for these within our generalized framework through the use of the recovery rates as presented above. That is, the clearing wealths satisfy

for every bank . We can replicate all results of this section – the formulations of the expected debt payments and equity values under comonotonic endowments – for the setting of Gouriéroux et al. (2012) with bankruptcy costs by simply redefining as:

without any other modification. The comonotonic cases that we consider in this work would solve the curse of dimensionality issues that exists in the work of Gouriéroux et al. (2012). We wish to highlight that, though the comonotonic endowment setting presented in this section can be approached with equity cross-ownership, the bounds presented in Section 4 do not hold for this more general setting.

3.2 Defaulting regions

For any random endowment satisfying Assumption 3.2, we can now consider the defaulting regions, i.e. the regions in which different combinations of banks are deemed to be defaulting on a portion of their liabilities. In fact, under the comonotonic setup considered herein, all such regions in the -space must be convex intervals in . This is in contrast to a general endowment space in which the regions need not be convex if the recovery rate is strictly less than 1 (); we refer to Gouriéroux et al. (2012) and Online Appendix B for more on this analysis. Thus, with the comonotonicity assumption we can uniquely define the regions of under which different firms default, which we will do so with the vector . Notably, this construction of the defaulting regions is fully characterized by the monotonic map defining the comonotonic endowments without consideration for the underlying random variable.

Definition 3.4.

Fix some random endowments satisfying Assumption 3.2. Define so that is the minimal value such that firm is solvent, i.e.

A discussion on the computation of is provided within Online Appendix C. The values of have a clear financial meaning if the construction is considered to be a single factor model. This is expanded upon in Remark 4.3. Specifically, the value is, in some sense, indicative of the financial stability of bank .

Assumption 3.5.

Without loss of generality we will assume for the remainder of this paper (except where explicitly mentioned otherwise) that the banks are placed in descending order of , i.e. so that . Additionally, define and .

3.3 Price of debt and equity

Immediately with the construction of minimal values for which each firm is solvent (as defined in Section 3.2 and with computation provided in Online Appendix C), we are able to deduce formulations for the defaulting probabilities for each bank as well as the expectations of the wealth, payments, and equity for each firm; such a construction of minimal threshold prices can only exist in the comonotonic setting assumed herein. As such, and in contrast to the general formulation in Gouriéroux et al. (2012) which requires a partition of the endowment space into defaulting regions, the formulations given in the below theorem require only a partition into intervals due to comonotonicity. Further, as demonstrated in Lemma 4.1 below, in the setting of Rogers and Veraart (2013), this formulation provides a tractable bound on the general expectations given in, e.g., Gouriéroux et al. (2012); Barucca et al. (2020) for large networks.

Theorem 3.6.

These expectation formulas implicitly encode the network and clearing model of Rogers and Veraart (2013) in two key points: (i) through the piecewise linear constructions for and (ii) through the minimal solvency prices . With these components encoding the network, the various expectations are found by conditioning on all possible default sets; in this comonotonic framework that requires partitioning the -space into intervals with endpoints determined by . In Online Appendix G, we make these formulas more explicit in a lognormal setting akin to that taken by Merton (1974) (summarized in Online Appendix F) for a single firm only.

4 Comonotonic pricing bounds

In this section we will utilize comonotonic endowments to consider upper and lower bounds on the pricing of debt with general random endowments. We wish to note that in the following the threshold values for the comonotonic versions (see Definition 3.4) may not have a physical interpretation. In the special case that a single factor model is considered, the regains a clear meaning with regards to this factor analysis. This is expanded upon in Remark 4.3 below and considered explicitly in Online Appendix G.

4.1 General upper and lower bounds for wealth and payments

We now wish to consider how the formulas above for the expectations of wealth and debt under comonotonic endowments can provide a bound for the more general random endowments. As previously mentioned, the expectations of debt and equity were studied in Gouriéroux et al. (2012); Barucca et al. (2020), but the formulations required suffer from the curse of dimensionality. More generally, if the correlations between firm endowments is unknown, the following lemma is useful from a stress-test viewpoint as we find that the comonotonic case is a lower bound on the health of the system. We wish to note that these bounds are to be considered mathematically and not as a statement on portfolio rebalancing. In Online Appendix E, we demonstrate that these bounds can be binding.

Lemma 4.1.

Let and be its comonotonic copula, i.e., for uniform random variable on the support and marginal distributions for respectively.111For non-continuous distributions we define as in McNeil et al. (2015). Further, let be the set of sub--algebras such that is a comonotonic projection of . Then

for any bank . The bound on wealth holds, also, for the societal node where the relative liabilities owed to society are fixed by , i.e. such that the societal wealth is explicitly defined by .

Remark 4.2.

As discussed previously in, e.g., Remark 3.7, we view the expectation as the price of debt (up to modification by discounting). Thus, we can view the bounds on the expectation provided in Lemma 4.1 as a bound on the price of debt. Similarly, due to the monotonic relationship between the effective interest rate and the price of debt, we can determine that

for every bank utilizing the notation from Lemma 4.1.

The conditional upper bounds with endowments for some sub--algebra in Lemma 4.1 are comonotonic. This means that each possible objective value over which we are optimizing is computationally tractable via the formulations in Theorem 3.6. Though we present this upper bound as the infimum over all such comonotonic projections, in practice it can be challenging to determine the set of all appropriate sub--algebras. As presented in Lemma 4.1, the trivial -algebra is always an element of which provides a bound to this infimum. In Remark 4.3 we consider another specific, financially meaningful, choice of sub--algebra when considering a single factor model.

We wish to briefly discuss some intuition surrounding Lemma 4.1 before continuing. When banks have interbank relationships, these assets serve as a method for diversification. However, if banks are all subject to a common shock, this diversification, in effect, disappears and the interconnectedness becomes irrelevant from a risk perspective. From a computational standpoint, we construct upper bounds for the expected wealths and payments via the comonotonic setting as well, and thus this is not only useful from a worst-case scenario.

Remark 4.3.

For simplicity of exposition, consider the full recovery setting of Eisenberg and Noe (2001). Consider a single factor model for endowments that allows for errors or idiosyncratic terms in which every firm is long the factor: where and are as in Assumption 3.2 and is independent from ( need not be monotonic in ). The conditional upper bound considered in Lemma 4.1 implies and for all banks (i.e., with ). We wish to note that this upper bound is again with respect to comonotonic endowments and, thus, can be computed via the formulations in Theorem 3.6. Such a setting is of particular interest when is a “systematic factor” and defines idiosyncratic risks; we refer the interested reader to Online Appendix G for a detailed example of this setting.

Remark 4.4.

The lower bound discussed in this section assumes particular importance from a stress-testing perspective and for assessing systemic risk in a financial network. This can be used to construct measures of stability and resilience as discussed in Acemoglu et al. (2015). However, the results of stability and resilience discussed in Acemoglu et al. (2015) are only proven for ring and completely connected network. In contrast our comonotonic setting allows for these results to be extended (analytically) to any general network topology. These bounds can, furthermore, be applied to both scalar systemic risk measures (Chen et al. (2013); Kromer et al. (2016)) and set-valued ones (Feinstein et al. (2017); Ararat and Rudloff (2020)) via the robust representation; this is detailed in Online Appendix D.

4.2 Price bounds for the market capitalization

Intriguingly, though the payments and wealth attain their worst-case under comonotonic endowments and best case under expected endowments, the equity of the different firms in the financial system typically is higher under the comonotonic endowments than other correlation structures and lower under the expected endowments. (We wish to note that the societal node would exhibit the same bounding properties as given in Lemma 4.1 since its equity is equal to its wealth by construction.) In fact, as proven in Corollary 4.5 below, the total market capitalization of the financial sector is bounded in the reverse order from those given in Lemma 4.1.

Corollary 4.5.

Consider the notation and setting of Theorem 4.1. Then the total expected equity of the financial sector is bounded from above and below by the comonotonic endowment setting, i.e.,

In fact, as in, e.g., Acharya (2009); Elliott et al. (2021), these market capitalization bounds allow us to consider the portfolio choice problem endogenously in our network framework with full recovery , i.e., that of Eisenberg and Noe (2001).222As the upper bound for market capitalization is considered with full recovery, the below results are only guaranteed to hold in that setting. We undertake this in order to reiterate (a different) portfolio optimization motivation of the comonotonic endowment framework. In order to study this problem, consider banks who seek to maximize their own expected equity in the worst-case subject to some budget and regulatory constraints , i.e., bank seeks to solve the minimax problem relative to all other institutions

| (5) |

We will assume that is law-invariant for every bank , i.e., if and (equal in distribution) then as well. Consider the setting in which banks can coordinate and jointly strategize to maximize the total equity of the coalition whose market capitalization is then shared, i.e., coalition seeks to optimize the modified minimax problem

The below corollary proves that the grand coalition will invest comonotonically and is stable against individual defections and, thus, the banks would endogenously strategize to invest in the comonotonic endowment space.

Corollary 4.6.

Consider a financial system with full recovery (i.e., ) in which all banks are equity maximizers according to (5) in which they can coordinate investment strategies. The Shapley value

of the grand coalition is an imputation, i.e., it is an efficient equity sharing arrangement () which is individually rational ( for every bank ) so that no bank will unilaterally choose to leave the grand coalition under this arrangement. Furthermore, all banks in the grand coalition will invest comonotonically.

As a result of this corollary, though we consider general space of random endowments to be bounded by comonotonic endowments, the comonotonic setting can arise endogenously in an Eisenberg-Noe framework due to a simple equity maximization principle.

5 Comparative statics

In this section we provide the comparative statics for the performance of the system with respect to important system parameters through numerical examples. In these numerical examples we will assume a lognormal setting as expressed in Assumption 5.1.

Assumption 5.1.

Let bank endowments be given by for vector of holdings and such that the risky investment has lognormal payout with risk-free rate , volatility , and maturity where is some standard normal random variable. To simplify the setting further, we will assume and throughout this section.

Assumption 5.1 presents a simplified setting of Online Appendix G (under the risk-neutral measure) such that the comonotonic condition with the additional restriction that for all firms and risk-free rate . We utilize these illustrative numerical examples to emphasize the impacts of default contagion through the interbank network by comparing the prices formulated in this work to those in Merton (1974) without interbank liabilities (see, also, Online Appendix F). We note that the comonotonic construction from the prior sections would allow us to consider more complicated underlying market models, e.g. a jump diffusion model; this would be accomplished by considering the appropriate distribution of at maturity . But for simplicity and due to its use in the seminal work by Merton, we will restrict ourselves to the lognormal setting.

As mentioned above, in the following numerical examples we wish to compare the pricing of debt and equity with network adjustments to the formulation of Merton (1974), which is presented also in Online Appendix F. In particular, we wish to study two simple baseline heuristics in the single bank Merton setting which we numerically find approximate the prices of debt and equity (respectively) in markets with high recovery rates.

-

(i)

Risky approximation for debt: Assume all interbank assets – reduced by the recovery rate in some way (herein we choose to consider ) – are fully invested in risky assets (i.e. exhibiting the lognormal distribution and not capped by the total obligations). In particular, as demonstrated below, this setting provides an approximation for the price of debt of the firms for high recovery rates. Heuristically, due to the comonotonicity assumption utilized in this work, the default of the banks occur under overlapping market conditions with payments comonotonic to the risky asset. Therefore, taking these ideas to the extreme, any bank is defaulting only if all others are as well with those banks paying out proportionally to their obligations and to the (low) asset value; if the (future) asset value is high then these interbank payments are valued comparably, which results in full payments and no defaults.

-

(ii)

Risk-free approximation for equity: Assume all interbank assets are paid off in full in units of the risk-free asset. In particular, as demonstrated below, this setting provides an (upper) approximation for the market capitalization of the firms. Heuristically, due to the comonotonicity assumption utilized in this work, the solvency of the banks occur under overlapping market conditions. Therefore, taking this idea to the extreme, any bank has positive equity only in the cases in which all other banks pay their liabilities in full.

Notably, these heuristics have the added advantage in that they can be computed under only aggregate network information (i.e., knowing the total interbank assets) without granular network information. As expressed in the network reconstruction literature (see, e.g., Upper and Worms (2004); Gandy and Veraart (2017)) and seen in Section 5.2, though total interbank assets and liabilities are known, granular information on the interbank obligations is often unavailable. As such, these heuristics take on a larger importance as they can approximate the network valuation adjustments without requiring the exact network construction.

5.1 Two bank system

Consider the financial system with 2 banks and an additional societal node as depicted in Figure 1. This two bank system with an additional societal node is such that bank owes units to bank and to the societal node and bank owes units to both bank and the societal node. Additionally, for simplicity and where otherwise we are not varying that parameter, we consider the risky asset to have volatility and the claims to have maturity at time . Further, recall that the risk-free rate is assumed to be . We consider this simple, illustrative, example so as to demonstrate the effects of the financial network (in comparison to the same system in two baseline systems without interbank debt as in Merton (1974)). For a clear comparison we will take this system without bankruptcy costs ()333Except where otherwise noted, the choice of bankruptcy costs do not alter any conclusions within this case study. and with a common risky asset exhibiting a lognormal distribution at maturity. Specifically, we will consider the same comparative statics on the effective interest rate as undertaken by Merton (1974), i.e. by varying the debt-firm value ratios and the maturity of the debt claims. We omit a consideration of varied volatility as the conclusions from that study are directly comparable to that of modifying the maturity of the debt claims. We wish to note that since we have assumed , the risk premium utilized by Merton (1974) is equivalent to the effective interest rate herein. We wish to highlight two key insights from this case study. First, we wish to study the impacts that network effects have on the price of debt and equity. This comparison with the single firm setting of Merton (1974) demonstrates that qualitative conclusions no longer hold in general once the network effects and systemic risk are taken into account; namely the debt-firm value ratio does not uniquely define the price of debt and equity (Section 5.1.1) nor does it define the shape of the term structure, i.e., the dependence of the effective interest rate on maturity (Section 5.1.2). Second, we consider the performance of our aforementioned baseline heuristics to demonstrate their relevance in estimating the price of debt and equity.

5.1.1 Impact of debt-firm value ratio

First we will consider the impact of the debt-firm value ratios on the effective interest rate and thus the price of debt for each firm. In Merton (1974) in which no firm holds any interbank assets (), it was shown that an individual firm’s debt-firm value ratio can completely determine its own interest rate . However, herein we consider explicitly the effects of the interbank assets. In our case, we can vary by either:

-

(i)

altering the liabilities and keeping investments constant, i.e.

given the desired debt-firm value ratio constrained by ; or

-

(ii)

altering the assets and keeping liabilities constant, i.e.

given the desired debt-firm value ratio so that .

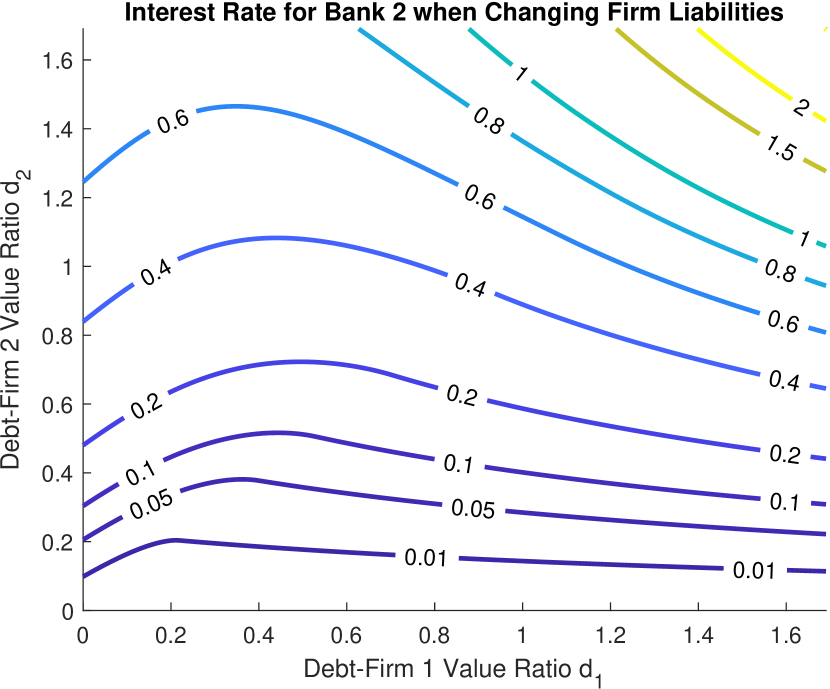

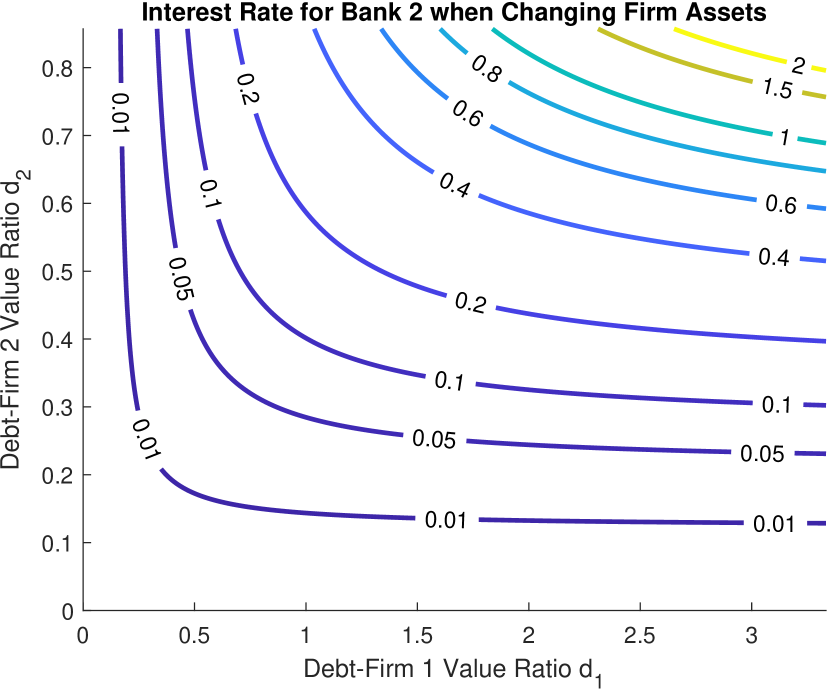

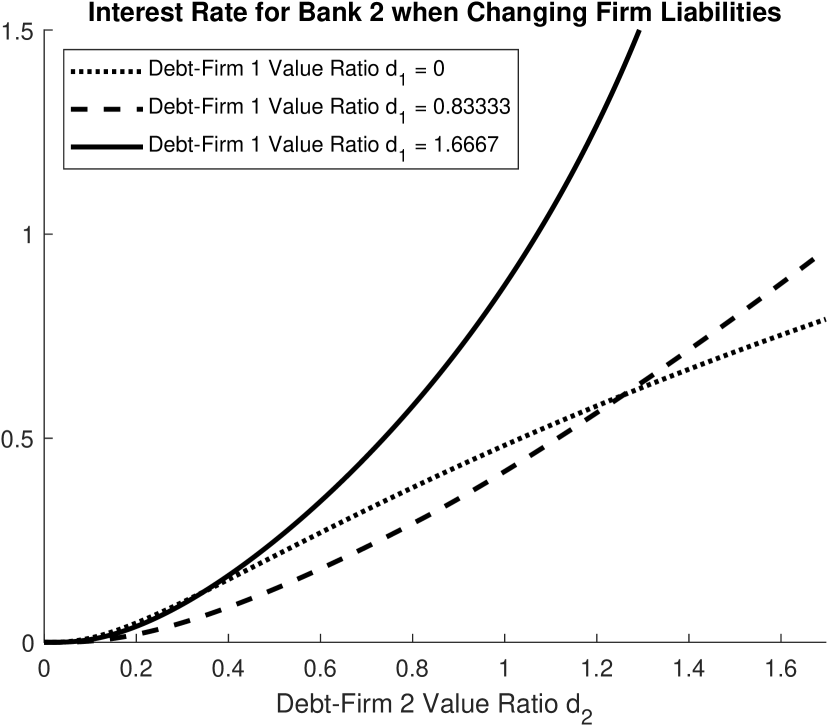

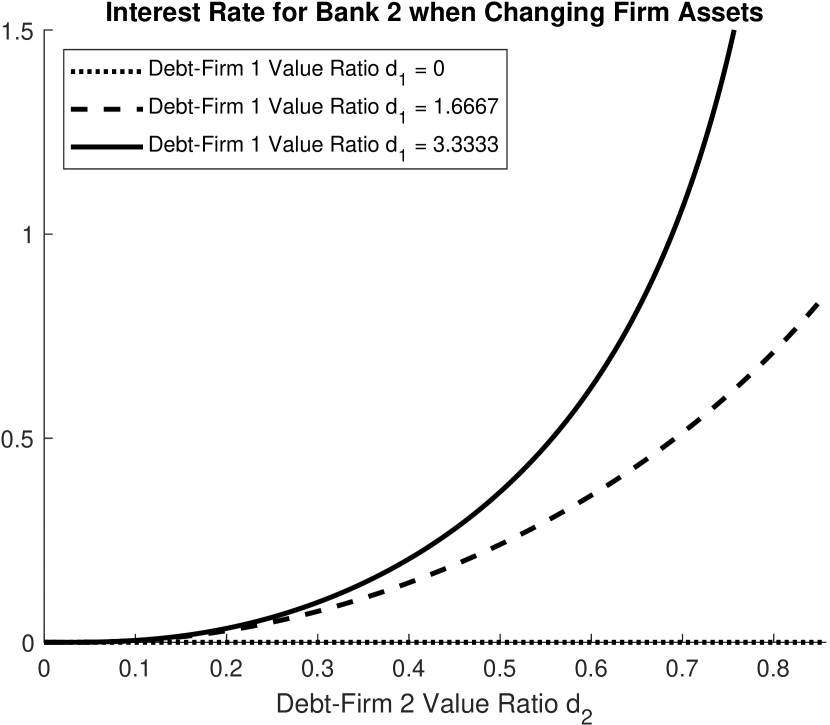

The distinction between the two approaches to varying is important because we find that the manner in which the debt-firm value ratio is modified can greatly affect the price of debt as measured by the effective interest rate. The contour plots of the interest rate of bank 2 with respect to debt-firm 1 value ratio and debt-firm 2 value ratio are shown in Figure 2(a) and Figure 2(b) for varying the debt-firm values by altering liabilities and altering assets respectively. To provide further clarity on how the individual debt-firm values affect each other, we consider three slices of this data, by fixing the level of and varying through either altering the liabilities or the assets in Figure 2(c) and Figure 2(d) respectively. Notably, if firm 1 has a lower debt-firm value ratio constructed through the change in assets, then firm 2 consistently has a lower effective interest rate for any debt-firm ratio chosen. However, there is no such monotonicity when the debt-firm value ratios are constructed through changes in the liabilities.

5.1.2 Impact of maturity

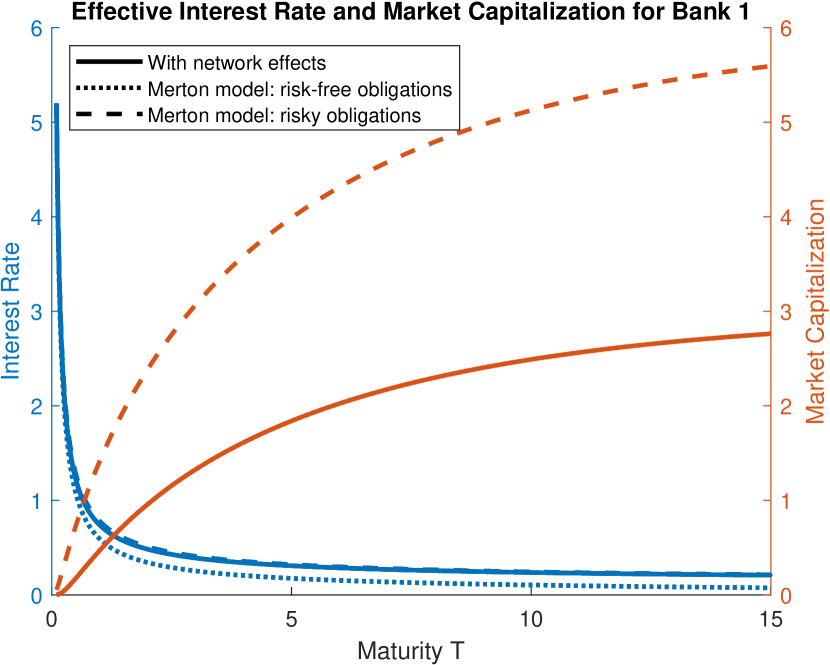

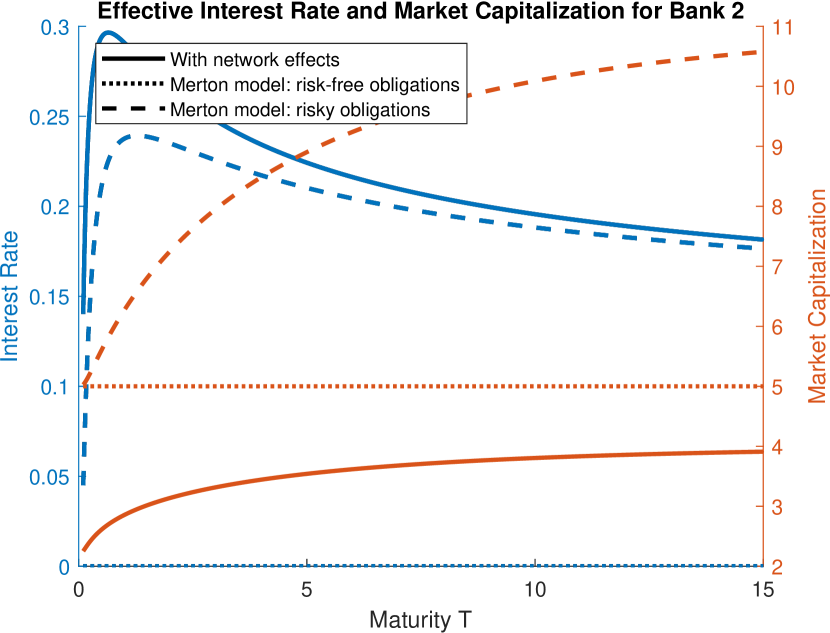

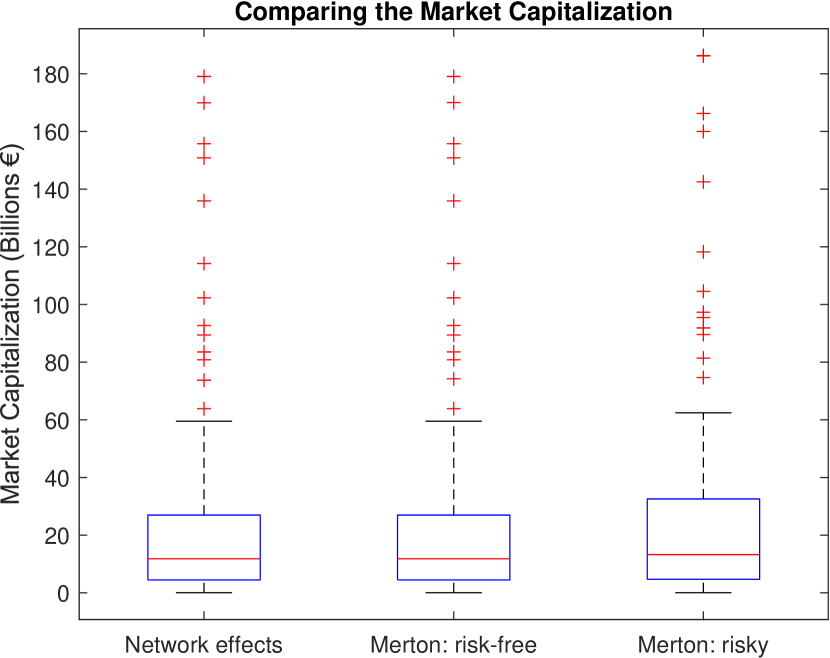

Second we will consider the impact of the maturity for the claims on the effective interest rate (and thus the price of debt) and the market capitalization for each firm. In this consideration we wish to compare the network effects with the two baseline models without a network presented above. Due to the risk of the interbank assets in a network, it is clear that the effective interest rate would be higher and market capitalization lower when including the network effects than when all interbank assets are treated as in baseline model (ii). As depicted in Figure 3(a), firm 1 has similar effective interest rate in all three scenarios, though the market capitalization is nearly double when interbank assets are treated as the market asset (baseline model (i)). Firm 2, as depicted in Figure 3(b), has orders of magnitude higher effective interest rates under the network effects than if they had no counterparty risk and noticeably higher effective interest rate when full network effects are taken into account than if interbank assets are treated no differently than other risky assets (i.e. following the market model). As expected due to their added risks, the network effects greatly reduce the market capitalization compared to the two single-firm scenarios considered herein. Notably, the results found herein match the heuristic expectations we have for our 2 baseline models; however, and as depicted in Figure 6 for the next case study, these heuristics lose much of their predictive power for low recovery rates .

We wish to conclude by considering the shapes of the interest rates as a function of the maturity of the claims under network effects. In Merton (1974) the hyperbolic shape of firm 1’s effective interest rate would only occur if its debt-firm value ratio was greater than or equal to 1; similarly the shape exhibited by firm 2’s effective interest rate would only occur if its debt-firm value ratio was strictly less than 1. However, as discussed above, the debt-firm value ratio does not have as unique a property under network effects as it did in Merton (1974) without counterparty risk. Thus we find that the change in shape need not (and in this numerical example, does not) occur at the individual debt-firm value ratios of 1.

5.2 European banking system

We will now consider a larger financial network consisting of banks. This large network provides clear reasoning for considering the comonotonic approach taken within this paper. As previously discussed, with 87 banks, there are potential combinations of defaulting banks . As such, the general framework for considering expected payments from Gouriéroux et al. (2012) would be computationally intractable. However, the comonotonic framework presented herein (and which, under the setting of Eisenberg and Noe (2001), provides a worst-case for the general setting as discussed in Section 4.1) is computationally tractable as only defaulting regions need to be considered. As such, we wish to use this case study to highlight the computational tractability of the comonotonic setting as well as the performance of our baseline heuristics on a larger, more realistic, network.

For this example, we will consider these 87 banks to come from the 2011 European Banking Authority EU-wide stress tests.444Due to complications with the calibration methodology, we only consider 87 of the 90 institutions. DE029, LU45, and SI058 were not included in this analysis. This dataset has been used in multiple prior empirical case studies (e.g. Gandy and Veraart (2017); Chen et al. (2016)) of financial contagion in interbank networks. To calibrate this system, we will take the same approach from Feinstein (2019) which is provided in Online Appendix H. We note, however, that though we are calibrating the financial network to a real dataset, the marginal distribution for bank endowments are not calibrated and as such this example is for illustrative purposes only. We believe that there would be significant value in a further, detailed, case study to empirically determine the marginal distributions of the bank endowments and, with that result, consider yield rates and bond prices to compare with the realized prices in the market. This is, however, beyond the scope of the current example. In fact, the primary purpose of using this dataset in this example, as opposed to a large fictional network, is to demonstrate the order of magnitude that the effective interest rates (i.e., the price of debt) can achieve (in comparison to the values presented in the prior case studies on the 2 bank system).

In order to complete our model, we need to consider the remaining parameters of the system. First, as all economic data pulled from the EBA EU-wide stress test dataset are already in a consistent unit (millions of euros), we will consider the (risk-neutral) value of the market portfolio to be (million euros). Further, during the period over which this data was collected, central banks were setting a low interest rate environment. Therefore we estimate that the risk-free interest rate is (as is assumed throughout this section). Additionally, as this is data from a single year’s stress test, we will consider maturity on all debt claims to be (year). Finally, the volatility of the risky asset is estimated to be from comparisons to annualized historical volatility of European markets in 2011.

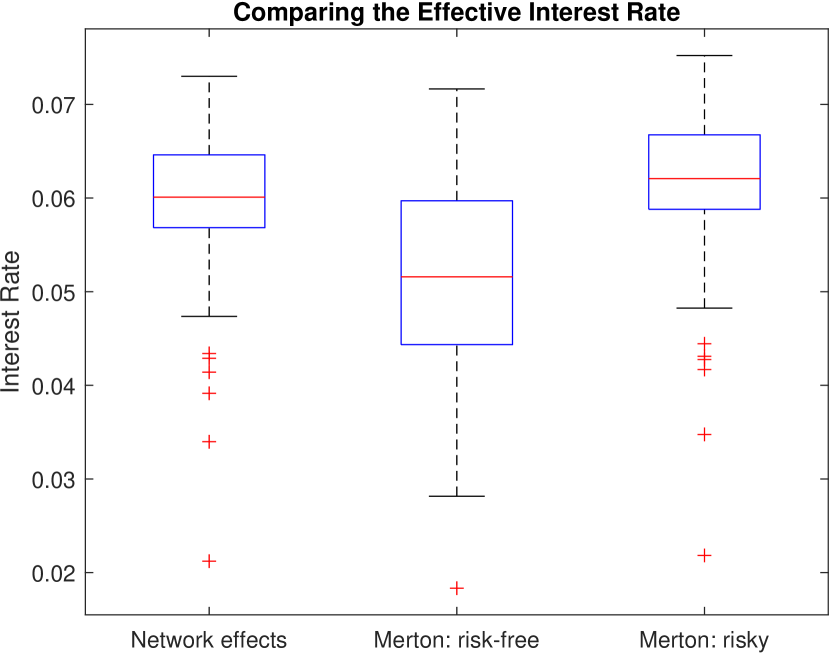

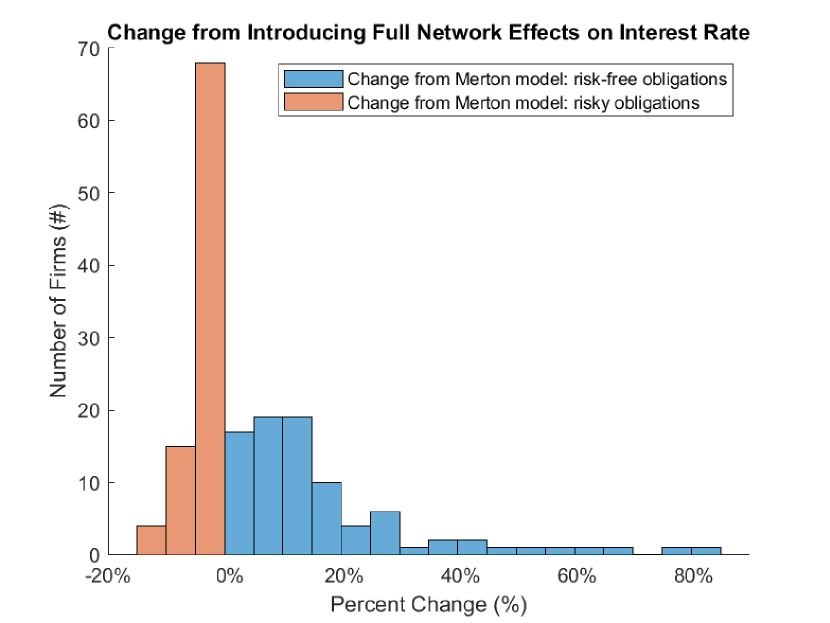

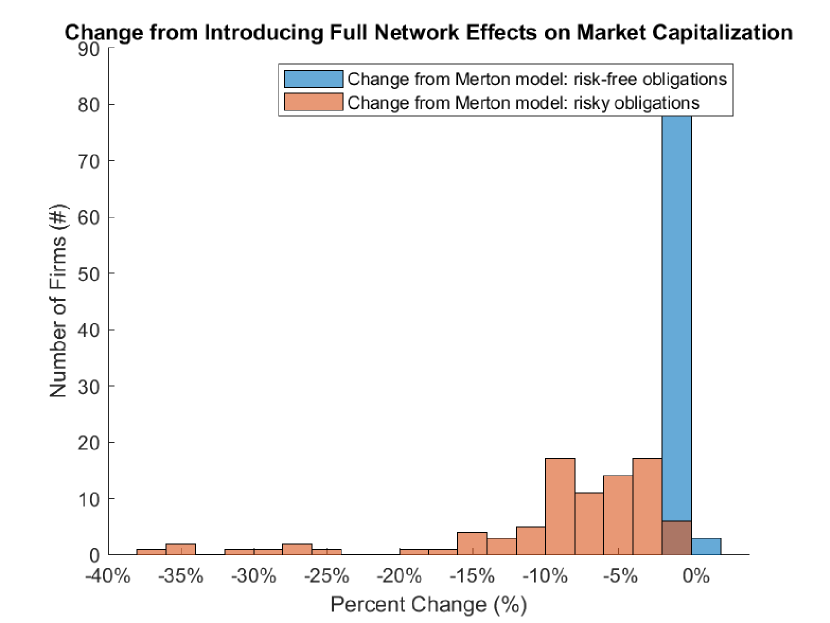

First, we wish to consider the impact of the full network effects on the effective interest rates and market capitalization in the setting without bankruptcy costs (). For this analysis we consider the same two baseline heuristic models as presented above. The data for these comparisons are provided in Figures 4 and 5 respectively. We note that, as with our intuition and as in Section 5.1 above, the price of debt with full network effects is generally comparable to the single firm effect case with all interbank assets treated as the risky asset. In fact, the interest rate of debt with full network effects is lower than if all interbank assets are treated as the risky asset, but significantly higher than when interbank assets are treated as the risk-free asset. In contrast, and again matching our intuition and comparable to that in Section 5.1 above, the market capitalization for firms is strikingly similar between the full network effects and the single firm effects with interbank assets treated as the risk-free asset. The single firm effects with interbank assets treated as the risky asset can differ by a large degree from the network effects for the market capitalization of the individual firms.

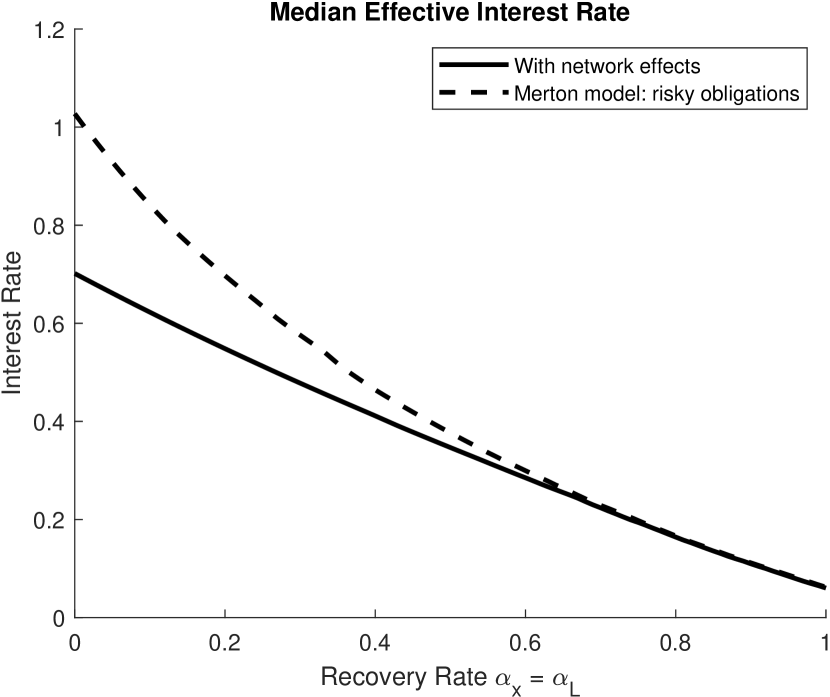

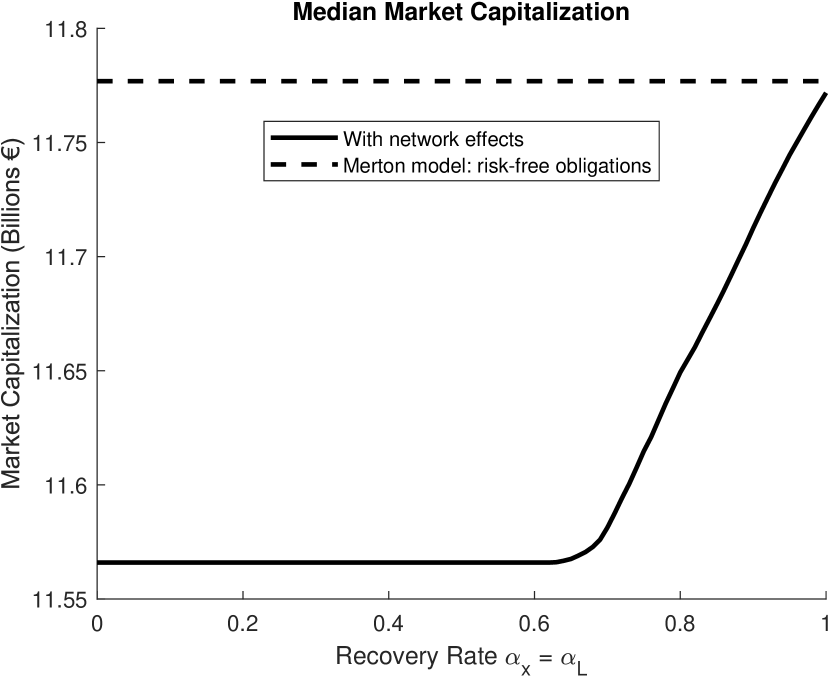

Second, though above we consider the setting without bankruptcy costs, we now wish to consider how the price of debt and equity are affected by the bankruptcy costs. Analytically, we can conclude before any simulations, that the effective interest rates will decrease and the market capitalization will increase with the recovery rates and . For the purposes of this case study we restrict ourselves to the special case that as in Veraart (2020) and only plot the relevant baseline model for debt (with interbank assets treated as risky assets) and equity (with interbank assets treated as risk-free assets). Figure 6 depicts the median effective interest rate and market capitalization for the 87 banks under consideration; this demonstrates that the heuristics are reasonable at high values of , but lose their predictive power if . Thus, if bankruptcy costs exist, considering the interbank assets as either the risk-free or risky asset can cause mispricing of risk.

6 Conclusion

In this work we present formulas for considering pricing of debt and equity of firms in a financial network under comonotonic endowments. This methodology extends considerations of CVA for valuation adjustment so that the whole financial network of counterparties is accounted for. Additionally, the comonotonic framework is theoretically justified, though this is only approximated in market data; under these approximations, we provide upper and lower bound for the price of debt in the Eisenberg-Noe framework. This is particularly valuable as financial networks are of specific interest in performing stress tests and studying systemic risk.

The models considered herein are simple compared to many modern processes considered for pricing financial instruments. Though updating the stochastic model of the risky asset would be of interest, herein we will only propose a few extensions for more complete financial network models. First, we propose utilizing an extension of the Eisenberg-Noe framework in which obligations are neither zero-coupon nor have the same maturities. Such an underlying financial network has been proposed in Capponi and Chen (2015); Kusnetsov and Veraart (2019); Banerjee et al. (2021). In particular, Banerjee et al. (2021) already proposes a setting with stochastic endowments. We believe using mark-to-market pricing of debt and market capitalization would allow for more realistic determination of default times over an exogenous deficit level. Second, as during systemic crises the failure of banks and drop in asset prices are inexplicably linked, we believe that including more complicated fire sale dynamics into this system would be of interest. In particular, we highlight Amini et al. (2016); Feinstein (2017); Feinstein and El-Masri (2017); Cont and Wagalath (2013, 2016) as possible underlying models for use in pricing with price impact dynamics. Finally, as highlighted in many empirical works such as Hałaj and Kok (2013, 2015); Elsinger et al. (2013); Anand et al. (2018), the network is typically unknown and needs to be estimated from partial information. Thus sensitivity analysis of pricing under misspecification of the network would be of interest. In the static, deterministic, setting of Eisenberg and Noe (2001) this was studied by Feinstein et al. (2018).

References

- Aase [1993] Knut K Aase. Equilibrium in a reinsurance syndicate; existence, uniqueness and characterization. ASTIN Bulletin: The Journal of the IAA, 23(2):185–211, 1993.

- Acemoglu et al. [2015] Daron Acemoglu, Asuman Ozdaglar, and Alireza Tahbaz-Salehi. Systemic risk and stability in financial networks. American Economic Review, 105(2):564–608, 2015.

- Acharya [2009] Viral V Acharya. A theory of systemic risk and design of prudential bank regulation. Journal of financial stability, 5(3):224–255, 2009.

- Amini and Feinstein [2021] Hamed Amini and Zachary Feinstein. Optimal network compression. 2021. Working paper.

- Amini et al. [2016] Hamed Amini, Damir Filipović, and Andreea Minca. Uniqueness of equilibrium in a payment system with liquidation costs. Operations Research Letters, 44(1):1–5, 2016.

- Anand et al. [2014] Kartik Anand, Guillaume Bédard-Pagé, and Virginie Traclet. Stress testing the Canadian banking system: A system-wide approach. Bank of Canada Financial Stability Review, 2014.

- Anand et al. [2018] Kartik Anand, Iman van Lelyveld, Ádám Banai, Soeren Friedrich, Rodney Garratt, Grzegorz Hałaj, Jose Fique, Ib Hansen, Serafín Martínez Jaramillo, Hwayun Lee, José Luis Molina-Borboa, Stefano Nobili, Sriram Rajan, Dilyara Salakhova, Thiago Christiano Silva, Laura Silvestri, and Sergio Rubens Stancato de Souza. The missing links: A global study on uncovering financial network structures from partial data. Journal of Financial Stability, 35:107–119, 2018.

- Anthropelos and Kardaras [2017] Michail Anthropelos and Constantinos Kardaras. Equilibrium in risk-sharing games. Finance and Stochastics, 21(3):815–865, 2017.

- Ararat and Rudloff [2020] Çağin Ararat and Birgit Rudloff. Dual representations for systemic risk measures. Mathematics and Financial Economics, 14:139–174, 2020.

- Arrow and Debreu [1954] Kenneth J Arrow and Gerard Debreu. Existence of an equilibrium for a competitive economy. Econometrica, 22(3):265–290, 1954.

- Banerjee and Feinstein [2019] Tathagata Banerjee and Zachary Feinstein. Impact of contingent payments on systemic risk in financial networks. Mathematics and Financial Economics, 13(4):617–636, 2019.

- Banerjee et al. [2021] Tathagata Banerjee, Alex Bernstein, and Zachary Feinstein. Dynamic clearing and contagion in financial networks. 2021. Working paper.

- Barucca et al. [2020] Paolo Barucca, Marco Bardoscia, Fabio Caccioli, Marco D’Errico, Gabriele Visentin, Guido Caldarelli, and Stefano Battiston. Network valuation in financial systems. Mathematical Finance, 30(4):1181–1204, 2020.

- Ben-Tal and Teboulle [2007] Aharon Ben-Tal and Marc Teboulle. An old-new concept of convex risk measures: The optimized certainty equivalent. Mathematical Finance, 17(3):449–476, 2007.

- Bichuch and Feinstein [2020] Maxim Bichuch and Zachary Feinstein. Endogenous inverse demand functions. 2020. Working paper.

- Borch [1960] Karl Borch. The safety loading of reinsurance premiums. Scandinavian Actuarial Journal, 1960(3-4):163–184, 1960.

- Borch [1962] Karl Borch. Equilibrium in a reinsurance market. Econometrica, 30(3):424–444, 1962.

- Bühlmann [1980] Hans Bühlmann. An economic premium principle. ASTIN Bulletin: The Journal of the IAA, 11(1):52–60, 1980.

- Bühlmann [1984] Hans Bühlmann. The general economic premium principle. ASTIN Bulletin: The Journal of the IAA, 14(1):13–21, 1984.

- Capponi and Chen [2015] Agostino Capponi and Peng-Chu Chen. Systemic risk mitigation in financial networks. Journal of Economic Dynamics and Control, 58:152–166, 2015.

- Capponi and Weber [2021] Agostino Capponi and Marko Weber. Systemic portfolio diversification. 2021. Working paper.

- Capponi et al. [2016] Agostino Capponi, Peng-Chu Chen, and David D. Yao. Liability concentration and systemic losses in financial networks. Operations Research, 64(5):1121–1134, 2016.

- Chen et al. [2013] Chen Chen, Garud Iyengar, and Ciamac C. Moallemi. An axiomatic approach to systemic risk. Management Science, 59(6):1373–1388, 2013.

- Chen et al. [2016] Nan Chen, Xin Liu, and David D. Yao. An optimization view of financial systemic risk modeling: The network effect and the market liquidity effect. Operations Research, 64(5), 2016.

- Cont and Wagalath [2013] Rama Cont and Lakshithe Wagalath. Running for the exit: distressed selling and endogenous correlation in financial markets. Mathematical Finance, 23(4):718–741, 2013.

- Cont and Wagalath [2016] Rama Cont and Lakshithe Wagalath. Fire sale forensics: measuring endogenous risk. Mathematical Finance, 26(4):835–866, 2016.

- Cossin and Schellhorn [2007] Didier Cossin and Henry Schellhorn. Credit risk in a network economy. Management Science, 53(10):1604–1617, 2007.

- Detering et al. [2020] Nils Detering, Thilo Meyer-Brandis, Konstantinos Panagiotou, and Daniel Ritter. Suffocating fire sales. 2020. Working paper.

- Dhaene et al. [2002] Jan Dhaene, Michel Denuit, Marc J Goovaerts, Rob Kaas, and David Vyncke. The concept of comonotonicity in actuarial science and finance: theory. Insurance: Mathematics and Economics, 31(1):3–33, 2002.

- Driessen [2013] T.S.H. Driessen. Cooperative Games, Solutions and Applications. Theory and Decision Library C. Springer Netherlands, 2013. ISBN 9789401577878.

- Dunkel and Weber [2010] Jörn Dunkel and Stefan Weber. Stochastic root finding and efficient estimation of convex risk measures. Operations Research, 58(5):1505–1521, 2010.

- Eisenberg and Noe [2001] Larry Eisenberg and Thomas H. Noe. Systemic risk in financial systems. Management Science, 47(2):236–249, 2001.

- Elliott et al. [2021] Matthew Elliott, Co-Pierre Georg, and Jonathon Hazell. Systemic risk shifting in financial networks. Journal of Economic Theory, 191:105157, 2021.

- Elsinger [2009] Helmut Elsinger. Financial networks, cross holdings, and limited liability. Österreichische Nationalbank (Austrian Central Bank), 156, 2009.

- Elsinger et al. [2013] Helmut Elsinger, Alfred Lehar, and Martin Summer. Network models and systemic risk assessment. In Handbook on Systemic Risk, pages 287–305. Cambridge University Press, 2013.

- Feinstein [2017] Zachary Feinstein. Financial contagion and asset liquidation strategies. Operations Research Letters, 45(2):109–114, 2017.

- Feinstein [2019] Zachary Feinstein. Obligations with physical delivery in a multi-layered financial network. SIAM Journal on Financial Mathematics, 10(4):877–906, 2019.

- Feinstein and El-Masri [2017] Zachary Feinstein and Fatena El-Masri. The effects of leverage requirements and fire sales on financial contagion via asset liquidation strategies in financial networks. Statistics and Risk Modeling, 34(3-4):113–139, 2017.

- Feinstein et al. [2017] Zachary Feinstein, Birgit Rudloff, and Stefan Weber. Measures of systemic risk. SIAM Journal on Financial Mathematics, 8(1):672–708, 2017.

- Feinstein et al. [2018] Zachary Feinstein, Weijie Pang, Birgit Rudloff, Eric Schaanning, Stephan Sturm, and Mackenzie Wildman. Sensitivity of the Eisenberg and Noe clearing vector to individual interbank liabilities. SIAM Journal on Financial Mathematics, 9(4):1286–1325, 2018.

- Föllmer and Schied [2004] Hans Föllmer and Alexander Schied. Stochastic finance – An introduction in discrete time. Graduate Textbook Series. De Gruyter, Berlin, 2nd edition, 2004.

- Gai et al. [2011] Prasanna Gai, Andrew Haldane, and Sujit Kapadia. Complexity, concentration and contagion. Journal of Monetary Economics, 58(5):453–470, 2011.

- Gandy and Veraart [2017] Axel Gandy and Luitgard A.M. Veraart. A Bayesian methodology for systemic risk assessment in financial networks. Management Science, 63(12):4428–4446, 2017.

- Glasserman and Young [2015] Paul Glasserman and H. Peyton Young. How likely is contagion in financial networks? Journal of Banking and Finance, 50:383–399, 2015.

- Gouriéroux et al. [2012] Christian Gouriéroux, Jean-Cyprian Héam, and Alain Monfort. Bilateral exposures and systemic solvency risk. Canadian Journal of Economics, 45(4):1273–1309, 2012.

- Gouriéroux et al. [2013] Christian Gouriéroux, Jean-Cyprian Héam, and Alain Monfort. Liquidation equilibrium with seniority and hidden CDO. Journal of Banking and Finance, 37(12):5261–5274, 2013.

- Hałaj and Kok [2013] Grzegorz Hałaj and Christoffer Kok. Assessing interbank contagion using simulated networks. Computational Management Science, 10(2-3):157–186, 2013.

- Hałaj and Kok [2015] Grzegorz Hałaj and Christoffer Kok. Modelling the emergence of the interbank networks. Quantitative Finance, 15(4):653–671, 2015.

- Hamm et al. [2013] Anna-Maria Hamm, Thomas Salfeld, and Stefan Weber. Stochastic root finding for optimized certainty equivalents. Proceedings of the 2013 Winter Simulation Conference, pages 922–932, 2013.

- Kromer et al. [2016] Eduard Kromer, Ludger Overbeck, and Katrin Zilch. Systemic risk measures on general probability spaces. Mathematical Methods of Operations Research, 84(2):323–357, 2016.

- Kusnetsov and Veraart [2019] Michael Kusnetsov and Luitgard A.M. Veraart. Interbank clearing in financial networks with multiple maturities. SIAM Journal on Financial Mathematics, 10(1):37–67, 2019.

- Lintner [1965] John Lintner. The valuation of risk assets and the selection of risky investments in stock portfolios and capital budgets. The Review of Economics and Statistics, 47(1):13–37, 1965. ISSN 00346535, 15309142.

- Liu and Staum [2010] Ming Liu and Jeremy Staum. Sensitivity analysis of the Eisenberg-Noe model of contagion. Operations Research Letters, 35(5):489–491, 2010.

- McNeil et al. [2015] Alexander J. McNeil, Rüdiger Frey, and Paul Embrechts. Quantitative risk management: Concepts, techniques, and tools. Princeton University Press, 2015.

- Merton [1974] Robert C. Merton. On the pricing of corporate debt: the risk structure of interest rates. The Journal of Finance, 29(2):449–470, 1974.

- Milgrom and Roberts [1994] Paul Milgrom and John Roberts. Comparing equilibria. American Economic Review, 84(3):441–459, 1994.

- Peleg and Yaari [1975] Bezalel Peleg and Menahem E. Yaari. A price characterization of efficient random variables. Econometrica, 43(2):283–292, 1975.

- Rogers and Veraart [2013] Leonard C.G. Rogers and Luitgard A.M. Veraart. Failure and rescue in an interbank network. Management Science, 59(4):882–898, 2013.

- Shaked and Shanthikumar [2007] Moshe Shaked and J. George Shanthikumar. Stochastic Orders. Springer Series in Statistics. Springer, 2007.

- Sharpe [1964] William F Sharpe. Capital asset prices: A theory of market equilibrium under conditions of risk. The journal of finance, 19(3):425–442, 1964.

- Siebenbrunner and Sigmund [2018] Christoph Siebenbrunner and Michael Sigmund. Do interbank markets price systemic risk? 2018. Working paper.

- Suzuki [2002] Teruyoshi Suzuki. Valuing corporate debt: the effect of cross-holdings of stock and debt. Journal of Operations Research, 45(2):123–144, 2002.

- Tsanakas and Christofides [2006] Andreas Tsanakas and Nicos Christofides. Risk exchange with distorted probabilities. ASTIN Bulletin, 36(1):219–243, 2006.

- Upper [2011] Christian Upper. Simulation methods to assess the danger of contagion in interbank markets. Journal of Financial Stability, 7(3):111–125, 2011.

- Upper and Worms [2004] Christian Upper and Andreas Worms. Estimating bilateral exposures in the German interbank market: Is there a danger of contagion? European Economic Review, 48(4):827–849, 2004.

- Veraart [2020] Luitgard A.M. Veraart. Distress and default contagion in financial networks. Mathematical Finance, 30(3):705–737, 2020.

- Weber and Weske [2017] Stefan Weber and Kerstin Weske. The joint impact of bankruptcy costs, fire sales and cross-holdings on systemic risk in financial networks. Probability, Uncertainty and Quantitative Risk, 2(1):9, 2017.

This appendix is organized as follows. First, in Appendix A, we provide details on the network clearing problem of Eisenberg and Noe [2001], Rogers and Veraart [2013]. Then, in Appendix B, we provide comments on computing the expectation of, e.g., the clearing wealths under general random endowments. In particular, we study the partitioning of the endowment space by the set of defaulting banks. In Appendix C, we provide an algorithm for computing the threshold prices introduced in Section 3.2 to partition -space by the set of defaulting banks under the comonotonicity assumption. This algorithm allows for efficient construction of the these threshold prices. We then consider systemic risk measures in Appendix D in which we generalize the results of Lemma 4.1 to find that bounds on these objects can similarly be provided by the comonotonic endowment setting. In Appendix E we return to the pure expectation setting presented in the main body of this work to provide simple examples demonstrating that the upper and lower bounds provided in Lemma 4.1 can be binding. This is followed by a summary of the Merton model for pricing debt and equity in Appendix F. The lognormal setting of the Merton model is then considered in a CAPM setting with idiosyncratic risks and placed in a financial network in Appendix G. Following this, we briefly describe the calibration of the interbank network for Section 5.2 in Appendix H. In Appendix I, we review details on the risk sharing problem presented in Section 1.2. Finally, the proofs of the results within the main body of this paper are provided in Appendix J.

Appendix A Details of financial networks

In this section we wish to give a formalized construction of all the details of the financial networks considered in this paper. We begin with the setting proposed in Section 2.1.

First, we wish to formalize the clearing process in wealths to describe this system. We refer to Veraart [2020], Barucca et al. [2020], Banerjee et al. [2021], Banerjee and Feinstein [2019] for detailed discussion of the clearing wealths and their relation to the more typical clearing payments from Eisenberg and Noe [2001], Rogers and Veraart [2013]. As in Banerjee et al. [2021], we can define the payments and equity from the wealths as and respectively. The clearing process is defined for all firms as

| (6) | ||||

As such, the clearing procedure implies: if bank has nonnegative wealth then it is solvent and its wealth is equal to its total assets minus its total liabilities; if bank has negative wealth then it is defaulting and its assets are reduced by the recovery rates . We note that with (i.e. under no bankruptcy costs) we recover the model of Eisenberg and Noe [2001].

We will now consider existence and uniqueness results on the clearing wealth . In general, we can get existence by applying Tarski’s fixed point theorem.

Proposition A.1.

There exists a greatest and least clearing solution to for and any finite clearing solution falls within the lattice .

Proof.

First note that is nondecreasing in wealths . Now we will prove that for any .

-

•

For any bank : by construction.

-

•

By monotonicity of the clearing procedure we recover .

The proof is completed by an application of Tarski’s fixed point theorem on the lattice . ∎

In general, however, the clearing wealth is not unique. In the special case without bankruptcy costs (), this reduces to the network described in Eisenberg and Noe [2001]. In that setting we can get uniqueness under very mild assumptions.

Corollary A.2.

Consider a setting with no bankruptcy costs () and all firms have obligations to the societal node (i.e. with for all firms ), then there exists a unique clearing solution .

Proof.

Proposition A.3.

Proof.

By Proposition A.1, and thus as well. Similarly to the proof of Proposition A.1, we can apply Tarski’s fixed point theorem to (1) on the lattice . Let be the greatest real-valued fixed point of and assume with for some bank . Then it must follow that , which implies . However this is a contradiction to being the greatest clearing solution to . ∎

We can compute the maximal clearing solution, as discussed in the previous proposition, through an application of the fictitious default algorithm as described in Rogers and Veraart [2013].

Corollary A.4.

The following algorithm converges to the maximal clearing solution :

-

(i)

Initialize , , and .

-

(ii)

Iterate and define .

-

(iii)

If then and terminate.

-

(iv)

Define to be the diagonal matrix with main diagonal defined by and

-

(v)

Go to step (ii).

Proof.

Before continuing, we wish to recall a notion of monotonicity for fixed points from Milgrom and Roberts [1994] which we regularly revisit within these appendices.

Theorem A.5 (Theorem 3 of Milgrom and Roberts [1994]).

Let be a complete lattice, a partially ordered set, and . Suppose is monotone nondecreasing. Let and . Then:

-

(i)

and are the least and greatest fixed points of ,

-

(ii)

and are nondecreasing, and

-

(iii)

if for all , is strictly increasing in then and are strictly increasing.

For the remainder of this section we use the notation introduced in Definition 2.2.

Proposition A.6.

The greatest clearing wealth mapping , and thus also the payment and equity mappings and , is nondecreasing in the endowments .

Proof.

The monotonicity of the clearing wealths in the endowments follow from Theorem A.5. The results for the payments and equity follow directly from the definition of those mappings from the clearing wealths. ∎

Proposition A.7.

Consider the setting of Eisenberg and Noe [2001], i.e. . The greatest clearing wealth mapping and the payment mapping are concave and submodular555 is submodular if for any . is supermodular if is submodular. in the endowments .

Proof.

We first note that, under the setting of Eisenberg and Noe [2001], we can consider this system as a fixed point in the payments with . Thus if is concave (submodular) so is .

-

(i)

Concavity of the clearing payment vector is given by Lemma 5 of Eisenberg and Noe [2001].

-

(ii)

To prove submodularity of the clearing payment vector , consider that the payment function is the pointwise limit of the mappings defined iteratively as:

As by construction (where convergence follows from the monotonicity and boundedness of the arguments ), if is submodular for all then the same must be true for the clearing payments . Trivially is submodular. Now by induction assume that is submodular. Take and ; there are three cases that must be considered:

-

(a)

If then by construction.

-

(b)

If then and by monotonicity (Proposition A.6); thus .

-

(c)

If and then and . Therefore we find

-

(a)

∎

Proposition A.8.

For any and any bank :

The bound on wealth holds, also, for the societal node where the relative liabilities owed to society are fixed by , i.e. such that the societal wealth is explicitly defined by .

Proof.

Note that, if the result holds for the clearing wealths, then it must also hold for the clearing payments as all bounds are given with respect to the same total obligations .

-

(i)

Consider the proposed upper bound. Consider with explicit consideration for the recovery rates . By construction, is (jointly) nondecreasing. Therefore, by Theorem A.5, it must follow that the (maximal) clearing wealths are nondecreasing as a function of the recovery rates as well and the upper bound is proven.

-

(ii)

Consider the proposed lower bound with fixed . Consider be the modification of the clearing equation so that

Notably, by construction of the clearing wealths, is the maximal fixed point of and is the maximal fixed point of . Additionally, by construction, is (jointly) nondecreasing. Therefore, by Theorem A.5, it must follow that the lower bound holds.

The bounds for the societal node follow directly from the those for the payments . ∎

Proposition A.9.

Define the random endowments . The greatest clearing wealths , and thus also the payments and equities and , is a measurable vector.

Proof.

First, we wish to recall the piecewise linear formulation of the clearing wealths as provided in Section 3.1; in particular, recall as defined in (3) and (4) respectively. For any we note that where provides the set of endowments that leads to the defaults encoded in , i.e., is defined as:

That is, is constructed as the intersection of a finite number of closed and open halfspaces as well as an additional condition that . This additional condition is the one that guarantees that does not provide a “better” (i.e. fewer defaulting banks) clearing wealth vector than the maximal clearing solution . By the use of Tarski’s fixed point theorem in the proof of Proposition A.1, we are able to guarantee that this construction of is, in fact, disjoint. As is the summation over a finite set, measurability of the clearing wealths follows. ∎

Appendix B Expectations under random endowments

In this section we wish to consider a partition of the endowment space into regions so that the defaulting set is constant in the subsets. This problem was considered in great detail in Gouriéroux et al. [2012] for the setting without bankruptcy costs, i.e. , and with cross-ownership. Herein we will present a quick extension that allows for bankruptcy costs, i.e. for any . Notably, when the partitions need not be convex sets, while they are convex polyhedrons in a system without bankruptcy costs as given in Gouriéroux et al. [2012]. In the below, we will consider the piecewise linear formulation of the clearing wealths as provided in Section 3.1; if cross-ownership is desired then we refer to Remark 3.3 for the modifications necessary to the mappings and .

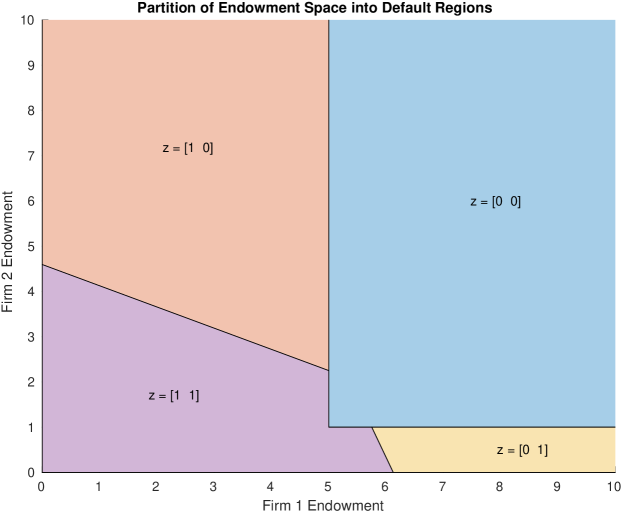

To consider the partitions, fix to denote the defaulting banks. By construction, the resulting wealths given endowments are provided by . For an endowment vector to be consistent with the defaulting set , it would need to be such that if and only if . That is, the set of endowments that generate the defaulting set is given by the system of inequalities:

However, except in the special case that there are no bankruptcy costs (), these regions need not be disjoint. If an endowment has two clearing wealth vectors , then it must be that where . If then, by construction of , it must follow that . In particular, we are interested in the maximal clearing wealth, thus we can construct the partition from the least to greatest number of defaults by considering the set of endowments that lead to by as provided in the Proof of Proposition A.9. That is, is defined as:

In Figure 7 we provide an image of the partitioning of the endowment space for a small network with 2 banks plus a societal node. We note that the societal node in this image can never default, this is due to it having no liabilities and thus always a nonnegative wealth.

Lastly, we wish to consider the particular case without bankruptcy costs () as provided by Gouriéroux et al. [2012]. Due to the uniqueness of the clearing wealths (Corollary A.2) in this case we obtain only a single consistent default set for every endowment and thus do not need to take a secondary intersection as in the case with bankruptcy costs. Further, in this case, those banks with 0 wealth can be considered equivalently both solvent and defaulting; thus the set of endowments that produce can be considered as the finite intersection of closed halfspaces only, i.e. the convex polyhedron: