A Stochastic Control Approach to

Managed Futures Portfolios

Abstract

We study a stochastic control approach to managed futures portfolios. Building on the Schwartz (1997) stochastic convenience yield model for commodity prices, we formulate a utility maximization problem for dynamically trading a single-maturity futures or multiple futures contracts over a finite horizon. By analyzing the associated Hamilton-Jacobi-Bellman (HJB) equation, we solve the investor’s utility maximization problem explicitly and derive the optimal dynamic trading strategies in closed form. We provide numerical examples and illustrate the optimal trading strategies using WTI crude oil futures data.

Keywords: commodity futures, dynamic portfolios, trading strategies, utility maximization

JEL Classification: C61, D53, G11, G13

Mathematics Subject Classification (2010): 91G20, 91G80

1 Introduction

Managed futures funds constitute a significant segment in the universe of alternative assets. These investments are managed by professional investment individuals or management companies known as Commodity Trading Advisors (CTAs), and typically involve trading futures on commodities, currencies, interest rates, and other assets. Regulated and monitored by both government agencies such as the U.S. Commodity Futures Trading Commission and the National Futures Association, this class of assets has grown to over US$350 billion in 2017.111Source: BarclayHedge (https://www.barclayhedge.com). One appeal of managed-futures strategies is their potential to produce uncorrelated and superior returns, as well as different risk-return profiles, compared to the equity market (Gregoriou et al., 2010; Elaut et al., 2016). While the types of securities traded and strategies are conceivably diverse among managed futures funds, details of the employed strategies are often unknown. Hurst et al. (2013) suggest that momentum-based strategies can help explain the returns of these funds.

In this paper, we analyze a stochastic dynamic control approach for portfolio optimization in which the commodity price dynamics and investor’s risk preference are incorporated. The commodity futures used in our model have the same spot asset but different maturities. Futures with the same spot asset share the same sources of risk. We apply a no-arbitrage approach to construct futures prices from a stochastic spot model. Specifically, we adopt the well-known two-factor model by Schwartz (1997), which also takes into account the stochastic convenience yield in commodity prices. We determine the optimal futures trading strategies by solving the associated Hamilton-Jacobi-Bellman (HJB) equations in closed form. The explicit formulae of our strategies allow for financial interpretations and instant implementation. Moreover, our optimal strategies are explicit functions of the prices of the futures included in the portfolio, but do not require the continuous monitoring of the spot price or stochastic convenience yield. Related to the strategies, we also discuss the corresponding wealth process and certainty equivalent from futures trading. We provide some numerical examples and illustrate the optimal trading strategies using WTI crude oil futures data.

There is a host of research on the pricing of futures, but relatively few studies apply dynamic stochastic control methods to optimize futures portfolios. Among them, Bichuch and Shreve (2013) consider trading a pair of futures but use the arithmetic Brownian motion. In a recent study, Angoshtari and Leung (2018) study the problem of dynamically trading the price spread between a futures contract and its spot asset under a stochastic basis model. They model the basis process by a scaled Brownian bridge, and solve a utility maximization problem to derive the optimal trading strategies. These two related studies do not account for the well-observed no-arbitrage price relationships and term-structure in the futures market. They motivate us to consider a stochastic spot model that can generate no-arbitrage futures prices and effectively capture their joint price evolutions. In our companion paper Leung and Yan (2018), we focus on dynamic pairs trading of VIX futures under a Central Tendency Ornstein-Uhlenbeck no-arbitrage pricing model. All these studies propose a stochastic control approach to futures trading. In contrast, Leung et al. (2016) introduce an optimal stopping approach to determine the optimal timing to open or close a futures position under three single-factor mean-reverting spot models. Futures portfolios are also often used to track the spot price movements, and we refer to Leung and Ward (2015, 2018) for examples using gold and VIX futures.

The paper is structured as follows. We describe the futures pricing model and corresponding price dynamics in Section 2. Then in Section 3, we discuss our portfolio optimization problems and provide the solutions in closed form. We also examine the investor’s trading wealth process and certainty equivalence. In Section 4, we provide illustrative numerical results from our model. Concluding remarks are provided in Section 5.

2 Futures Price Dynamics

Let us denote the commodity spot price process by . Under the Schwartz (1997) model, the spot price is driven by a stochastic instantaneous convenience yield, denoted by here. This convenience yield, which was originally used in the context of commodity futures, reflects the value of direct access minus the cost of carry and can be interpreted as the“dividend yield” for holding the physical asset. It is the “flow of services accruing to the holder of the spot commodity but not to the owner of the futures contract” as explained in Schwartz (1997).

For the spot asset, we consider its log price, denoted by . Under the Schwartz (1997) model, it satisfies the system of stochastic differential equations (SDEs) under the physical probability measure :

| (1) | |||||

| (2) | |||||

| (3) |

Here, and are two standard Brownian motions under with instantaneous correlation . The stochastic convenience yield follows the Ornstein-Uhlenbeck model, which is mean-reverting with a constant equilibrium level , volatility , and speed of mean-reversion equal to . We require that and .

The investor’s portfolio optimization problem will be formulated under the physical measure , but in order to price the commodity futures we need to work with the risk-neutral pricing measure . To this end, we assume a constant interest rate , and apply a change of measure from to . The -dynamics of the correlated Brownian motions () are given by

| (4) | |||||

| (5) |

Consequently, the risk-neutral log spot price evolves according to

where we have defined the risk-neutral equilibrium level for the convenience yield by

It is adjusted by the ratio of the market price of risk associated with and the speed of mean reversion . With a constant , the convenience yield again follows the Ornstein-Uhlenbeck model under measure but with a different equilibrium level compared to that under measure .

We consider a commodity market that consists of traded futures contracts with maturities . Let

be the price of the -futures at time , which is a function of time , current log spot price , and convenience yield . For any , the price function satisfies the PDE

| (6) |

for , where we have compressed the dependence of on . The terminal condition is for . As is well known (see Schwartz (1997); Cortazar and Naranjo (2006)), the futures price admits the exponential affine form:

| (7) |

for some functions and that depend only on time and not the state variables. The functions and are found from the ODEs

| (8) | |||

| (9) |

for , with terminal conditions and . The ODEs (8) and (9) admit the following explicit solutions:

| (10) | |||||

| (11) |

Applying Ito’s formula to (7), the -futures price evolves according to the SDE

| (12) |

under the physical measure , where the drift is given by

| (13) | |||||

| (14) |

The last equality follows from (8) and (11). As a consequence, the drift of is independent of and , meaning that the investor’s value function (see (22) or (34)) will also be independent of and . This turns out to be a crucial feature that greatly simplifies the investor’s portfolio optimization problem and ultimately leads to an explicit solution.

To facilitate presentation, let us rewrite the linear combination of and in (12) as

where is a standard Brownian motion and

| (15) |

is the instantaneous volatility coefficient.

Under this model, futures prices are not independent and admit a specific correlation structure. For example, consider the and contracts. The SDE for the respective futures price is

| (16) |

The two Brownian motions, and , are correlated with

where

| (17) |

is the instantaneous correlation that depends not only on the spot model parameters but also the two futures price functions through and .

3 Utility Maximization Problem

We now present the mathematical formulation for the futures portfolio optimization problem. To begin, we discuss the case where the investor trades only futures with the same maturity in Section 3.1. Then, we extend the analysis to optimize a portfolio with two different futures in Section 3.2. We will also investigate in Section 3.3 the value of trading using the notion of certainty equivalent.

3.1 Single-Maturity Futures Portfolio

Suppose that the investor trades only futures of a single maturity for some chosen . The trading horizon, denoted by , must be equal to or shorter than the chosen maturity , so we require .

We will let denote the number of -futures contracts held in the portfolio. The investor can choose the size of the position in the -futures, and the position can be long or short at anytime. For brevity, we may write .

Without loss of generality, we arbitrarily set in our presentation of the optimization problem and solution. The investor is assumed to trade only the futures contract and not other risky or risk-free assets. The dynamic portfolio consists of units of -futures at time . The self-financing condition means that the wealth process satisfies

| (18) |

Applying the futures price equations (7) and (12), we can express the system of SDEs for the wealth process and futures price as

| (19) |

| (20) |

A control is said to be admissible if is real-valued progressively measurable, and is such that the system of SDE (19) admits a unique solution and the integrability condition is satisfied. We denote by the set of admissible strategies in this case given an initial investment time .

The investor’s risk preference is described by the exponential utility function

| (21) |

where is the constant risk aversion parameter. For a given trading horizon, , the investor seeks an admissible strategy that maximizes the expected utility of terminal wealth at time by solving the optimization problem

| (22) |

We note that the value function is only a function of time , current wealth , and current futures price , and does not depend on the current spot price or convenience yield.

To facilitate presentation, we define the following partial derivatives

We expect the value function to solve the HJB equation

| (25) | ||||

for , with terminal condition for . Performing the optimization in (27), we can express the optimal control as

| (26) |

Substituting this into (27), we obtain the nonlinear PDE

| (27) |

Next, we conjecture that depends on and only, and apply the transformation

| (28) |

for some function to be determined. By direct substitution and computation, we obtain the ODE

| (29) |

subject to =0. In turn, we obtain by integration

Applying (28) to (26), we obtain the optimal strategy

| (30) |

Using (11), (14), and (15), the optimal strategy in the single-contract case is explicitly given by

| (31) |

We observe from (31) that is inversely proportional to and . This means that a higher risk aversion will reduce the size of the investor’s position. A higher futures price will also have the same effect. However, the total cash amount invested in the futures, i.e. , does not vary with the futures price, and is in fact a deterministic function of time. Note that the investor’s position is independent of the equilibrium level of the convenience yield or , but it depends on the speed of mean reversion , volatility , and market price of risk of the convenience yield.

3.2 Trading Futures of Two Different Maturities

We now consider the utility maximization problem involving a pair of futures with different maturities. Without loss of generality, let and be the two maturities of the futures in the portfolio. The trading horizon satisfies . The investor continuously trades only the two futures over time. The trading wealth satisfies the self-financing condition

| (32) |

where , , denote the number of -futures held. If it is negative, the corresponding futures position is short. For notational simplicity, we may write Writing the trading wealth and two futures prices together in terms of two fundamental sources of randomness , we get

| (33) |

A pair of controls is said to be admissible if it is real-valued progressively measurable, and such that the system of SDE (33) admits a unique solution and the integrability condition , for , is satisfied. We denote by the set of admissible controls with an initial time of investment . Next, we define the value function of the investor’s portfolio optimization problem. The investor seeks an admissible strategy that maximizes the expected utility from wealth at time , that is,

| (34) |

3.2.1 HJB Equation and Closed-Form Solution

To facilitate presentation, we define the following partial derivatives

We determine the value function by solving the HJB equation

| (36) | ||||

| (38) | ||||

| (39) |

for , along with the terminal condition

Next, we apply the transformation

| (40) |

with and . Substituting (40) into (39), we obtain the linear PDE for :

| (41) |

with =0. We have defined the partial derivatives

and suppressed the dependence on , in , , and to simplify the notation.

We can solve this linear PDE of by using the ansatz

to deduce that

From this, we deduce that is in fact a function of only, independent of and , and satisfies the first-order differential equation

Solving this and applying (14), (15), and (17), we obtain a closed-form expression for . Precisely,

| (42) |

Applying (42) to (40), the value function is given by

| (43) |

Interestingly, as in the single-futures case, the value function is independent of the speed of mean reversion and equilibrium level of the convenience yield process. Intuitively, it suggests that the optimal strategy effectively removes the stochasticity of the convenience yield in the investor’s maximum expected utility. This feature is evident again later in the characterization of the optimal wealth process. Moreover, the value function does not depend on the current futures prices . The simplicity of the value function is unexpected, especially since there are two stochastic factors and two futures in the trading problem. Nevertheless, it does not mean that the corresponding trading strategies are trivial. In fact, the strategies depend not only on other model parameters but also the futures prices, as we will discuss next.

By applying (40) and (42) to (39), we obtain the optimal trading strategies

| (44) | ||||

| (45) |

In this case with two futures, for either , the corresponding optimal strategy is a function of , but does not depend on the price of the other futures , for . Also note that if is zero, then the two-futures strategy reduces to the single-futures strategy, as in (30), which is given explicitly by (31).

We recall (14), (15), and (17), and express the optimal strategies explicitly in terms of model parameters. Precisely,

| (46) |

| (47) |

Thus we see that the optimal controls and do not depend on the current spot price or convenience yield , and is also independent on the equilibrium of the convenience yield . For practical applications, this independence removes the burden to estimate or continuously monitor the spot price or convenience yield. Nevertheless, the optimal controls do depend on all the other parameters, namely . Lastly, we notice from (44) that, when (see (17)) equals zero, in this two-futures case is identical to from the single-futures case (see (30)).

Remark 1

Naturally, one can consider trading futures with more than two maturities. However, in such case under the Schwartz two-factor model, there is an infinite number of solutions to the corresponding utility maximization problem and the additional futures are redundant, as we show in Appendix A.

3.2.2 Optimal Wealth Process

To derive the optimal wealth process, we substitute the optimal futures positions, and , into the wealth equation (32) and get

where we have defined

| (48) |

and

| (49) | |||||

Note that both and are constant. This implies that the wealth process, under the optimal trading strategy, is an arithmetic Brownian motion with constant drift and volatility. Moreover, these two constants do not depend on the speed of mean reversion and equilibrium level of the convenience yield process. This is why the value function is also independent of these two parameters. The financial intuition is that the optimal strategy suggests trading in a way that removes the randomness stemmed from the convenience yield process. As a special case, when and , the measure is identical to . This will lead to , and in turn a constant wealth, with .

3.3 Certainty Equivalent

Next, we consider the certainty equivalent associated with the trading opportunity in the futures. The certainty equivalent is the cash amount that derives the same utility as the value function. First, we consider the single-futures case. Recall from (21) and (28) that the investor’s utility and value functions are both of exponential form. Therefore, the certainty equivalent is given by

| (50) |

Here, the superscript refers to the futures with maturity in the portfolio. From (50), we observe that the certainty equivalent is the sum of the investor’s wealth and the time-deterministic component , which is positive and inversely proportional to the risk aversion parameter . All else being equal, a more risk averse investor has a lower certainty equivalent, valuing the futures trading opportunity less. Interestingly, the certainty equivalent does not depend on the current futures prices but it does depend on the model parameters that appear in the futures price dynamics.

Similarly, the certainty equivalent from dynamically trading two futures with different maturities is given by

| (51) |

Since the certainty equivalents in both the single-futures and two-futures cases have the same linear dependence on wealth , we will for simplicity set in our numerical examples to compare across these cases. To this end, we denote and .

4 Numerical Implementation

We now examine our model through a number of numerical examples using simulated and empirical data. For our examples, we will use the estimated parameters values found in Ewald et al. (2018). They are displayed here in Table 1. The drift parameter of the spot price was not given in Ewald et al. (2018), so we set for our examples. We use federal funds rate as a proxy for the instantaneous interest rate which, during the calibration period, hovered around .222Data from www.macrotrends.net. The default value for the risk aversion coefficient is unless noted otherwise.

μ κ η ¯η ρ λ r 0.010 0.800 0.450 0.500 0.750 0.050 0.001

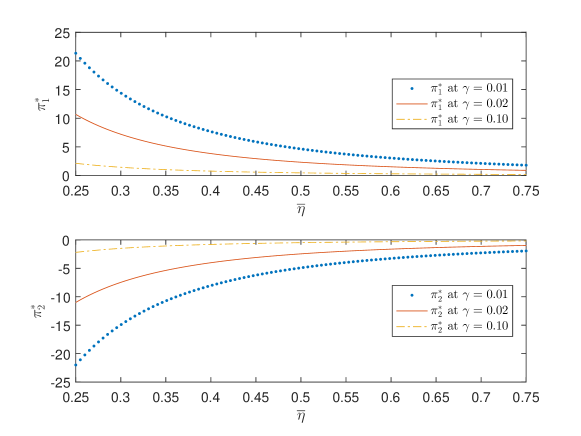

In Figure 1, we show the dependence of the optimal positions, and , respectively in the -futures and -futures in the two-futures case on the volatility parameter of the convenience yield process, for three different risk aversion levels. Observe that at all three levels of is positive and decreasing in while is negative and increasing in . With the parameters given in Table 1, we are long the -futures and short the -futures . When we rearrange the formulae (46) and (47) for and , respectively, and collect terms involving , we see that for both , the optimal strategies are of the form , which means that the absolute value of the each strategy decreases as increases, with other variables held constant. The practical consequence is that the number of contracts held, on both the long and short sides, are decreasing as the volatility of the stochastic convenience yield process increases. This is in line with a risk-averse trader’s intuition that less exposures on both legs of the traded pair should be preferred, if the volatility of the stochastic convenience yield is high. Furthermore, the positions increase in size (more positive for and more negative for ) as risk aversion decreases. This is obvious given the inverse relationship between and as seen in Eq (44) and (45).

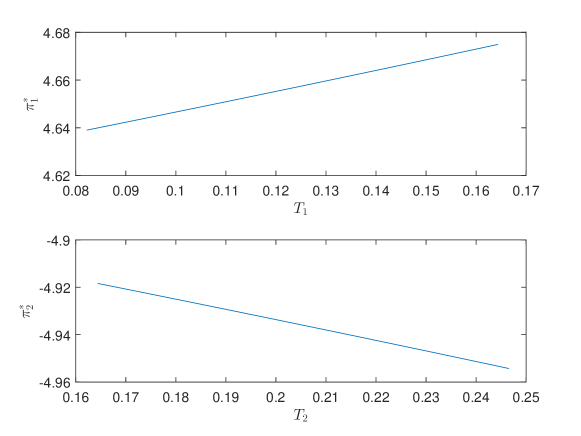

Figure 2 illustrates how the optimal futures positions, and , vary with respect to maturity. First of all, the two positions are of different signs and their sizes are very close. As maturity or lengthens, the size of the corresponding futures position increases, with becoming more positive and more negative. However, the change is very small as the scale on the y-axis shows, so one can interpret this as the positions are not very sensitive to the futures maturities.

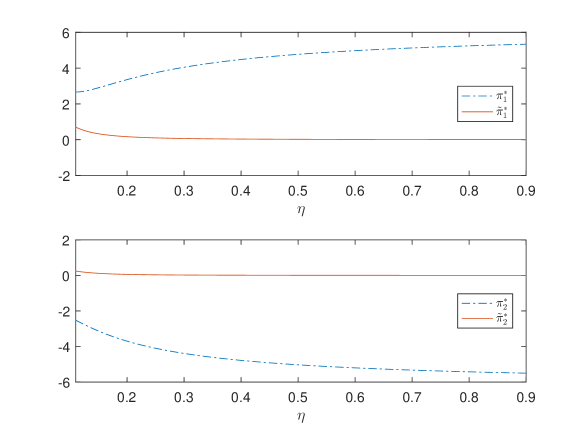

In Figure 3 we compare the optimal trading strategies, and for two futures to the optimal strategy for trading a single futures. We plot the strategies as functions of , the volatility of the spot price, using same set of parameters as in Table 1. When trading a single contract, the corresponding optimal strategy, and , are both very small near zero. However, it can be seen that they do increase slightly in size when becomes small, as volatility decreases.

This is in contrast to the two-contract case where the optimal strategies are and . Both increase, in opposite directions, as increases. This shows that despite the increase in risk as increases, paired positions in and , of opposite signs, will increase as volatility of the spot process increases.

It is also interesting to note the size of the positions in the single contract cases as compared to the pair-trading case. When we are constrained to trade only single contracts, that is when the admissible set is as opposed to , the position is much smaller. Under the current model, the presence of multiple contracts of different maturities significantly increases trade volume and allows the trader to take much bigger hedged trades.

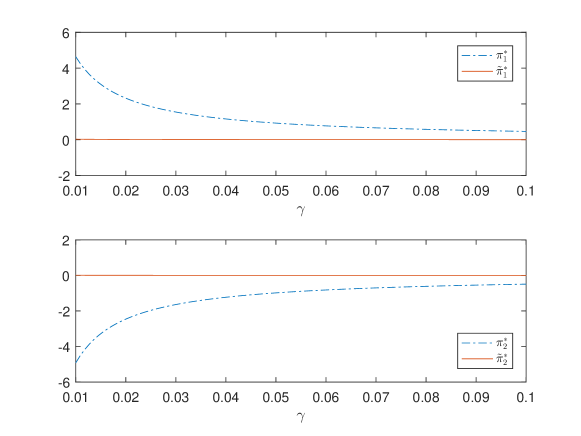

In Figure 4 we plot the optimal strategies as functions of , the risk aversion coefficient. Obviously, given the inverse relationship between and as seen in Eq (44) and (45), as well as between and as seen in Eq (30), the optimal positions are expected to decrease in magnitude. What is interesting to note is the insensitivity of with respect to , in comparison to . This means that in the single futures case, the position will be small regardless of the level of risk aversion.

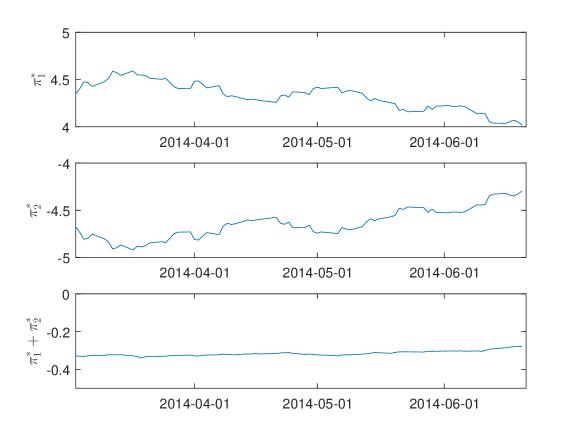

Having analyzed the parameter dependence of the optimal strategies in details, now we turn to their path behavior based on historical data. We consider the June 2014 and July 2014 WTI crude oil futures. We show the empirical optimal positions over the period March 2014 to June 2014. This period is chosen to correspond to the post-calibration period of Ewald et al. (2018). Applying our the explicit formulae for the strategies, we compute , , and based on the daily settlement prices of these contracts as well as the parameters in Table 1. As shown in Figure 5, the optimal strategy is positive throughout this period, corresponding to a long position in the front-month contract, and the opposite holds for . Taken together, the sum of both positions is negligibly small, corresponding to a net neutral position. Overall, the positions changed little when the parameters and are kept fixed. The only variables that change are and , of which we have already seen the relative insensitivity in Figure 2.

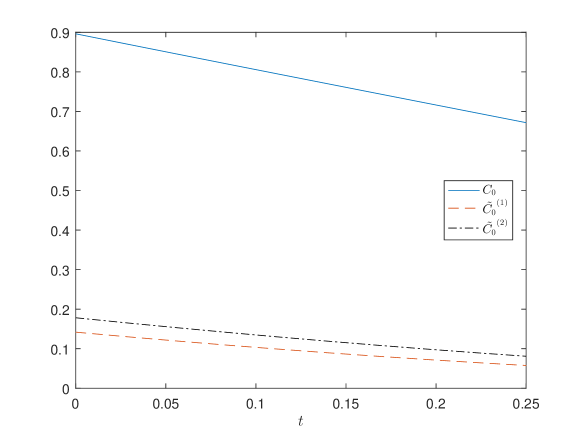

We now turn our attention to the certainty equivalents. With reference to Section 3.3, we plot in Figure 6 the following certainty equivalents: in the single-futures case with -futures traded, in the single-futures case with -futures traded, and in the two-futures case with -futures and futures traded. Their numerical values are given in Table 2.

C_0(0) ~C^(1)_0(0) ~C^(2)_0(0) 0.8962 0.1418 0.1782

We observe from Figure 6 that the certainty equivalent for trading two contracts simultaneously is significantly greater than that derived from trading only a single contract regardless of the choice of maturity. In fact, the certainty equivalent is much larger than the sum of the two certainty equivalents and . This makes sense since the single-contract case can be viewed as two-contracts case but with one strategy constrained at zero. Effectively, the single-contract case is restricting the admissible set from to , thus reducing the maximum expected utility as well as the certainty equivalent. Our result confirms the intuition that more choices of trading instruments are preferable to fewer.

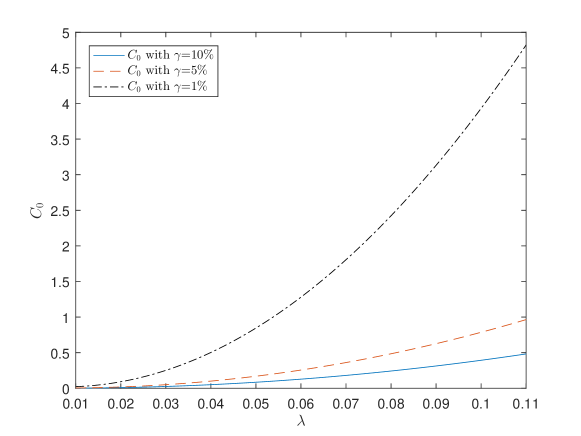

Lastly, we examine the behavior of at different risk aversion levels with focus on its sensitivity with respect to the market price of risk . In Figure 7, we see that the certainty equivalent at time 0, , is increasing and quadratic in , and tends to infinity as increases. This holds for all three values of shown, but a lower risk aversion suggests that the certainty equivalent is higher and faster growing in .

5 Conclusions

We have analyzed the problem of dynamically trading two futures contracts with the same underlying. Under a two-factor mean-reverting model for the spot price, we derive the futures price dynamics and solve the portfolio optimization problem in closed form and give explicit optimal trading strategies. By studying the associated Hamilton-Jacobi-Bellman equation, we solve the utility maximization explicitly and provide the optimal trading strategies in closed form. In addition to the analytic properties of our solutions, we also apply our results to commodity futures trading and present numerical examples to illustrate the optimal holdings.

There are several natural directions for future research on managed futures. First, additional factors and sources of risks can be incorporated in the spot model, including random jumps, stochastic volatility, and stochastic interest rate. Nevertheless, more complex models typically mean that the value function and optimal trading strategies are not available in closed form and thus require numerical approximations. In reality, futures are typically traded with leverage, and margin requirement is a core issue. Incorporating this feature to futures portfolio optimization may not be straightforward, but will certainly have practical implications.

Appendix A Appendix

A.1 Portfolio with Three Futures Contracts

Let us consider a dynamic portfolio of three futures contracts with different maturities and . In this case, the wealth and futures prices follow the system of SDEs

| (52) |

The HJB equation associated with the value function is

| (54) | ||||

| (56) | ||||

where we suppress the dependence on in and , for .

To solve for the optimal strategies (), we impose the first-order conditions. To facilitate the presentation, we define the constants

This leads to the following system of equations

| (57) |

which is singular as verified by computation.

References

- Angoshtari and Leung (2018) Angoshtari, B. and Leung, T. (2018). Optimal dynamic basis trading. working paper.

- Bichuch and Shreve (2013) Bichuch, M. and Shreve, S. (2013). Utility maximization trading two futures with transaction costs. SIAM Journal of Financial Mathematics, 4(1):26–85.

- Cortazar and Naranjo (2006) Cortazar, G. and Naranjo, L. (2006). An N-factor Gaussian model of oil futures prices. Journal of Futures Markets, 26(3):243–268.

- Elaut et al. (2016) Elaut, G., Erdos s, P., and Sjodin, J. (2016). An analysis of the risk-return characteristics of serially correlated managed futures. Journal of Futures Markets, 36(10):992–1013.

- Ewald et al. (2018) Ewald, C.-O., Zhang, A., and Zong, Z. (2018). On the calibration of the Schwartz two-factor model to WTI crude oil options and the extended Kalman filter. Annals of Operations Research.

- Gregoriou et al. (2010) Gregoriou, G. N., Hubner, G., and Kooli, M. (2010). Performance and persistence of Commodity Trading Advisors: Further evidence. Journal of Futures Markets, 30(8):725–752.

- Hurst et al. (2013) Hurst, B., Ooi, Y. H., and Pedersen, L. H. (2013). Demystifying managed futures. Journal of Investment Management, 11(3):42–58.

- Leung et al. (2016) Leung, T., Li, J., Li, X., and Wang, Z. (2016). Speculative futures trading under mean reversion. Asia-Pacific Financial Markets, 23(4):281–304.

- Leung and Ward (2015) Leung, T. and Ward, B. (2015). The golden target: Analyzing the tracking performance of leveraged gold ETFs. Studies in Economics and Finance, 32(3).

- Leung and Ward (2018) Leung, T. and Ward, B. (2018). Dynamic index tracking and risk exposure control using derivatives. Applied Mathematical Finance, 25(2):180–212.

- Leung and Yan (2018) Leung, T. and Yan, R. (2018). Optimal dynamic pairs trading of futures under a two-factor mean-reverting model. Journal of Financial Engineering, 5(3):1850027.

- Schwartz (1997) Schwartz, E. (1997). The stochastic behavior of commodity prices: Implications for valuation an hedging. Journal of Finance, 52(3):923–973.