Solving Nonlinear and High-Dimensional Partial Differential Equations via Deep Learning

TEAM One

Ali Al-Aradi, University of Toronto

Adolfo Correia, Instituto de Matemática Pura e Aplicada

Danilo Naiff, Universidade Federal do Rio de Janeiro

Gabriel Jardim, Fundação Getulio Vargas

Supervisor:

Yuri Saporito, Fundação Getulio Vargas

EMAp, Fundação Getulio Vargas, Rio de Janeiro, Brazil

Chapter 1 Introduction

In this work we present a methodology for numerically solving a wide class of partial differential equations (PDEs) and PDE systems using deep neural networks. The PDEs we consider are related to various applications in quantitative finance including option pricing, optimal investment and the study of mean field games and systemic risk. The numerical method is based on the Deep Galerkin Method (DGM) described in Sirignano and Spiliopoulos (2018) with modifications made depending on the application of interest.

The main idea behind DGM is to represent the unknown function of interest using a deep neural network. Noting that the function must satisfy a known PDE, the network is trained by minimizing losses related to the differential operator, the initial/terminal conditions and the boundary conditions given in the initial value and/or boundary problem. The training data for the neural network consists of different possible inputs to the function and is obtained by sampling randomly from the region on which the PDE is defined. One of the key features of this approach is the fact that, unlike other commonly used numerical approaches such as finite difference methods, it is mesh-free. As such, it does not suffer (as much as other numerical methods) from the curse of dimensionality associated with high-dimensional PDEs and PDE systems.

The main goals of this paper are to:

-

1.

Present a brief overview of PDEs and how they arise in quantitative finance along with numerical methods for solving them.

-

2.

Present a brief overview of deep learning; in particular, the notion of neural networks, along with an exposition of how they are trained and used.

-

3.

Discuss the theoretical foundations of DGM, with a focus on the justification of why this method is expected to perform well.

-

4.

Elucidate the features, capabilities and limitations of DGM by analyzing aspects of its implementation for a number of different PDEs and PDE systems.

We present the results in a manner that highlights our own learning process, where we show our failures and the steps we took to remedy any issues we faced. The main messages can be distilled into three main points:

-

1.

Sampling method matters: DGM is based on random sampling; where and how the sampled random points used for training are chosen are the single most important factor in determining the accuracy of the method.

-

2.

Prior knowledge matters: similar to other numerical methods, having information about the solution that can guide the implementation dramatically improves the results.

-

3.

Training time matters: neural networks sometimes need more time than we afford them and better results can be obtained simply by letting the algorithm run longer.

Chapter 2 An Introduction to Partial Differential Equations

Overview

Partial differential equations (PDE) are ubiquitous in many areas of science, engineering, economics and finance. They are often used to describe natural phenomena and model multidimensional dynamical systems. In the context of finance, finding solutions to PDEs is crucial for problems of derivative pricing, optimal investment, optimal execution, mean field games and many more. In this section, we discuss some introductory aspects of partial differential equations and motivate their importance in quantitative finance with a number of examples.

In short, PDEs describe a relation between a multivariable function and its partial derivatives. There is a great deal of variety in the types of PDEs that one can encounter both in terms of form and complexity. They can vary in order; they may be linear or nonlinear; they can involve various types of initial/terminal conditions and boundary conditions. In some cases, we can encounter systems of coupled PDEs where multiple functions are connected to one another through their partial derivatives. In other cases, we find free boundary problems or variational inequalities where both the function and its domain are unknown and both must be solved for simultaneously.

To express some of the ideas in the last paragraph mathematically, let us provide some definitions. A -th order partial differential equation is an expression of the form:

where is the collection of all partial derivatives of order and is the unknown function we wish to solve for.

PDEs can take one of the following forms:

-

1.

Linear PDE: derivative coefficients and source term do not depend on any derivatives:

-

2.

Semi-linear PDE: coefficients of highest order derivatives do not depend on lower order derivatives:

-

3.

Quasi-linear PDE: linear in highest order derivative with coefficients that depend on lower order derivatives:

-

4.

Fully nonlinear PDE: depends nonlinearly on the highest order derivatives.

A system of partial differential equations is a collection of several PDEs involving multiple unknown functions:

where .

Generally speaking, the PDE forms above are listed in order of increasing difficulty. Furthermore:

-

•

Higher-order PDEs are more difficult to solve than lower-order PDEs;

-

•

Systems of PDEs are more difficult to solve than single PDEs;

-

•

PDEs increase in difficulty with more state variables.

In certain cases, we require the unknown function to be equal to some known function on the boundary of its domain . Such a condition is known as a boundary condition (or an initial/terminal condition when dealing with a time dimension). This will be true of the form of the PDEs that we will investigate in Chapter 5.

Next, we present a number of examples to demonstrate the prevalence of PDEs in financial applications. Further discussion of the basics of PDEs (and more advanced topics) such as well-posedness, existence and uniqueness of solutions, classical and weak solutions and regularity can be found in Evans (2010).

The Black-Scholes Partial Differential Equation

One of the most well-known results in quantitative finance is the Black-Scholes Equation and the associated Black-Scholes PDE discussed in the seminal work of Black and Scholes (1973). Though they are used to solve for the price of various financial derivatives, for illustrative purposes we begin with a simple variant of this equation relevant for pricing a European-style contingent claim.

European-Style Derivatives

European-style contingent claims are financial instruments written on a source of uncertainty with a payoff that depends on the level of the underlying at a predetermined maturity date. We assume a simple market model known as the Black-Scholes model wherein a risky asset follows a geometric Brownian motion (GBM) with constant drift and volatility parameters and where the short rate of interest is constant. That is, the dynamics of the price processes for a risky asset and a riskless bank account under the “real-world” probability measure are given by:

where is a -Brownian motion.

We are interested in pricing a claim written on the asset with payoff function and with an expiration date . Then, assuming that the claim’s price function - which determines the value of the claim at time when the underlying asset is at the level - is sufficiently smooth, it can be shown by dynamic hedging and no-arbitrage arguments that must satisfy the Black-Scholes PDE:

This simple model and the corresponding PDE can extend in several ways, e.g.

-

•

incorporating additional sources of uncertainty;

-

•

including non-traded processes as underlying sources of uncertainty;

-

•

allowing for richer asset price dynamics, e.g. jumps, stochastic volatility;

-

•

pricing more complex payoffs functions, e.g. path-dependent payoffs.

American-Style Derivatives

In contrast to European-style contingent claims, American-style derivatives allow the option holder to exercise the derivative prior to the maturity date and receive the payoff immediately based on the prevailing value of the underlying. This can be described as an optimal stopping problem (more on this topic in Section 2.4).

To describe the problem of pricing an American option, let be the set of admissible stopping times in at which the option holder can exercise, and let be the risk-neutral measure. Then the price of an American-style contingent claim is given by:

Using dynamic programming arguments it can be shown that optimal stopping problems admit a dynamic programming equation. In this case, the solution of this equation yields the price of the American option. Assuming the same market model as the previous section, it can be shown that the price function for the American-style option with payoff function - assuming sufficient smoothness - satisfies the variational inequality:

where is a differential operator.

The last equation has a simple interpretation. Of the two terms in the curly brackets, one will be equal to zero while the other will be negative. The first term is equal to zero when , i.e. when the option value is greater than the intrinsic (early exercise) value, the option is not exercised early and the price function satisfies the usual Black-Scholes PDE. When the second term is equal to zero we have that , in other words the option value is equal to the exercise value (i.e. the option is exercised). As such, the region where is referred to as the continuation region and the curve where is called the exercise boundary. Notice that it is not possible to have since both terms are bounded above by 0.

It is also worth noting that this variational inequality can be written as follows:

where we drop the explicit dependence on for brevity. The free boundary set in this problem is which must be determined alongside the unknown price function . The set is referred to as the exercise boundary; once the price of the underlying asset hits the boundary, the investor’s optimal action is to exercise the option immediately.

The Fokker-Planck Equation

We now turn out attention to another application of PDEs in the context of stochastic processes. Suppose we have an Itô process on with time-independent drift and diffusion coefficients:

and assume that the initial point is a random vector with distribution given by a probability density function . A natural question to ask is: “what is the probability that the process is in a given region at time ?” This quantity can be computed as an integral of the probability density function of the random vector , denoted by :

The Fokker-Planck equation is a partial differential equation that can be shown to satisfy:

where and are first and second order partial differentiation operators with respect to and and , respectively. Under certain conditions on the initial distribution , the above PDE admits a unique solution. Furthermore, the solution satisfies the property that is positive and integrates to 1, which is required of a probability density function.

As an example consider an Ornstein-Uhlenbeck (OU) process with a random starting point distributed according to an independent normal random variable with mean 0 and variance . That is, satisfies the stochastic differential equation (SDE):

where and are constants representing the mean reversion level and rate. Then the probability density function for the location of the process at time satisfies the PDE:

Since the OU process with a fixed starting point is a Gaussian process, using a normally distributed random starting point amounts to combining the conditional distribution process with its (conjugate) prior, implying that is normally distributed. We omit the derivation of the exact form of in this case.

Stochastic Optimal Control and Optimal Stopping

Two classes of problems that heavily feature PDEs are stochastic optimal control and optimal stopping problems. In this section we give a brief overview of these problems along with some examples. For a thorough overview, see Touzi (2012), Pham (2009) or Cartea et al. (2015).

In stochastic control problems, a controller attempts to maximize a measure of success - referred to as a performance criteria - which depends on the path of some stochastic process by taking actions (choosing controls) that influence the dynamics of the process. In optimal stopping problems, the performance criteria depends on a stopping time chosen by the agent; the early exercise of American options discussed earlier in this chapter is an example of such a problem.

To discuss these in concrete terms let be a controlled Itô process satisfying the stochastic differential equation:

where is a control process chosen by the controller from an admissible set . Notice that the drift and volatility of the process are influenced by the controller’s actions. For a given control, the agent’s performance criteria is:

The key to solving optimal control problems and finding the optimal control lies in the dynamic programming principle (DPP) which involves embedding the original optimization problem into a larger class of problems indexed by time, with the original problem corresponding to . This requires us to define:

where . The value function is the value of the performance criteria when the agent adopts the optimal control:

Assuming enough regularity, the value function can be shown to satisfy a dynamic programming equation (DPE) also called a Hamilton-Jacobi-Bellman (HJB) equation. This is a PDE that can be viewed as an infinitesimal version of the DPP. The HJB equation is given by:

where the differential operator is the infinitesimal generator of the controlled process - an analogue of derivatives for stochastic processes - given by:

Broadly speaking, the optimal control is obtained as follows:

-

1.

Solve the first order condition (inner optimization) to obtain the optimal control in terms of the derivatives of the value function, i.e. in feedback form;

-

2.

Substitute the optimal control back into the HJB equation, usually yielding a highly nonlinear PDE and solve the PDE for the unknown value function;

-

3.

Use the value function to derive an explicit expression for the optimal control.

For optimal stopping problems, the optimization problem can be written as:

where is the set of admissible stopping times. Similar to the optimal control problem, we can derive a DPE for optimal stopping problem in the form of a variational inequality assuming sufficient regularity in the value function . Namely,

The interpretation of this equation was discussed in Section 2.2.2 for American-style derivatives where we discussed how the equation can be viewed as a free boundary problem.

It is possible to extend the problems discussed in this section in many directions by considering multidimensional processes, infinite horizons (for running rewards), incorporating jumps and combining optimal control and stopping in a single problem. This will lead to more complex forms of the corresponding dynamic programming equation.

Next, we discuss a number of examples of HJB equations that arise in the context of problems in quantitative finance.

The Merton Problem

In the Merton problem, an agent chooses the proportion of their wealth that they wish to invest in a risky asset and a risk-free asset through time. They seek to maximize the expected utility of terminal wealth at the end of their investment horizon; see Merton (1969) for the investment-consumption problem and Merton (1971) for extensions in a number of directions. Once again, we assume the Black-Scholes market model:

The wealth process of a portfolio that invests a proportion of wealth in the risky asset and the remainder in the risk-free asset satisfies the following SDE:

The investor is faced with the following optimal stochastic control problem:

where is the set of admissible strategies and is the investor’s utility function. The value function is given by:

which satisfies the following HJB equation:

If we assume an exponential utility function with risk preference parameter , that is , then the value function and the optimal control can be obtained in closed-form:

where is the market price of risk.

Optimal Execution with Price Impact

Stochastic optimal control, and hence PDEs in the form of HJB equations, feature prominently in the algorithmic trading literature, such as in the classical work of Almgren and Chriss (2001) and more recently Cartea and Jaimungal (2015) and Cartea and Jaimungal (2016) to name a few. Here we discuss a simple algorithmic trading problem with an investor that wishes to liquidate an inventory of shares but is subject to price impact effects when trading too quickly. The challenge then involves balancing this effect with the possibility of experiencing a negative market move when trading too slowly.

We begin by describing the dynamics of the main processes underlying the model. The agent can control their (liquidation) trading rate which in turn affects their inventory level via:

Note that negative values of indicate that the agent is buying shares. The price of the underlying asset is modeled as a Brownian motion that experiences a permanent price impact due to the agent’s trading activity in the form of a linear increase in the drift term:

By selling too quickly the agent applies increasing downward pressure (linearly with factor ) on the asset price which is unfavorable to a liquidating agent. Furthermore, placing larger orders also comes at the cost of increased temporary price impact. This is modeled by noting that the cashflow from a particular transaction is based on the execution price which is linearly related to the fundamental price (with a factor of ):

The cash process evolves according to:

With the model in place we can consider the agent’s performance criteria, which consists of maximizing their terminal cash and penalties for excess inventory levels both at the terminal date and throughout the liquidation horizon. The performance criteria is

where and are preference parameters that control the level of penalty for the terminal and running inventories respectively. The value function satisfies the HJB equation:

Using a carefully chosen ansatz we can solve for the value function and optimal control:

For other optimal execution problems the interested reader is referred to Chapter 6 of Cartea et al. (2015).

Systemic Risk

Yet another application of PDEs in optimal control is the topic of Carmona et al. (2015). The focus in that paper is on systemic risk - the study of instability in the entire market rather than a single entity - where a number of banks are borrowing and lending with the central bank with the target of being at or around the average monetary reserve level across the economy. Once a characterization of optimal behavior is obtained, questions surrounding the stability of the system and the possibility of multiple defaults can be addressed. This is an example of a stochastic game, with multiple players determining their preferred course of action based on the actions of others. The object in stochastic games is usually the determination of Nash equilibria or sets of strategies where no player has an incentive to change their action.

The main processes underlying this problem are the log-monetary reserves of each bank denoted and assumed to satisfy the SDE:

where are Brownian motions correlated through a common noise process, is the average log-reserve level and is the rate at which bank borrows from or lends to the central bank.

The interdependence of reserves appears in a number of places: first, the drift contains a mean reversion term that draws each bank’s reserve level to the average with a mean reversion rate ; second, the noise terms are driven partially by a common noise process.

The agent’s control in this problem is the borrowing/lending rate . Their aim is to remain close to the average reserve level at all times over some fixed horizon. Thus, they penalize any deviations from this (stochastic) average level in the interim and at the end of the horizon. They also penalize borrowing and lending from the central bank at high rates as well as borrowing (resp. lending) when their own reserve level is above (resp. below) the average level. Formally, the performance criterion is given by:

where the running penalties are:

and the terminal penalty is:

where and represent the investor’s preferences with respect to the various penalties. Notice that the performance criteria for each agent depends on the strategies and reserve levels of all the agents including themselves. Although the paper discusses multiple approaches to solving the problem (Pontryagin stochastic maximum principle and an alternative forward-backward SDE approach), we focus on the HJB approach as this leads to a system of nonlinear PDEs. Using the dynamic programming principle, the HJB equation for agent is:

Remarkably, this system of PDEs can be solved in closed-form to obtain the value function and the optimal control for each agent:

Mean Field Games

The final application of PDEs that we will consider is that of mean field games (MFGs). In financial contexts, MFGs are concerned with modeling the behavior of a large number of small interacting market participants. In a sense, it can be viewed as a limiting form of the Nash equilibria for finite-player stochastic game (such as the interbank borrowing/lending problem from the previous section) as the number of participants tends to infinity. Though it may appear that this would make the problem more complicated, it is often the case that this simplifies the underlying control problem. This is because in MFGs, agents need not concern themselves with the actions of every other agent, but rather they pay attention only to the aggregate behavior of the other agents (the mean field). It is also possible in some cases to use the limiting solution to obtain approximations for Nash equilibria of finite player games when direct computation of this quantity is infeasible. The term ‘’mean field” originates from mean field theory in physics which, similar to the financial context, studies systems composed of large numbers of particles where individual particles have negligible impact on the system. A mean field game typically consists of:

-

1.

An HJB equation describing the optimal control problem of an individual;

-

2.

A Fokker-Planck equation which governs the dynamics of the aggregate behavior of all agents.

Much of the pioneering work in MFGs is due to Huang et al. (2006) and Lasry and Lions (2007), but the focus of our exposition will be on a more recent work by Cardaliaguet and Lehalle (2017). Building on the optimal execution problem discussed earlier in this chapter, Cardaliaguet and Lehalle (2017) propose extensions in a number of directions. First, traders are assumed to be part of a mean field game and the price of the underlying asset is impacted permanently, not only by the actions of the agent, but by the aggregate behavior of all agents acting in an optimal manner. In addition to this aggregate permanent impact, an individual trader faces the usual temporary impact effects of trading too quickly. The other extension is to allow for varying preferences among the traders in the economy. That is, traders may have different tolerance levels for the size of their inventories both throughout the investment horizon and at its end. Intuitively, this framework can be thought of as the agents attempting to “trade optimally within the crowd.”

Proceeding to the mathematical description of the problem, we have the following dynamics for the various agents’ inventory and cash processes (indexed by a superscript ):

An important deviation from the previous case is the fact that the permanent price impact is due to the net sum of the trading rates of all agents, denoted by :

Also, the value function associated with the optimal control problem for agent is given by:

Notice that each agent has a different value of and demonstrating their differing preferences. As a consequence, an agent can be represented by their preferences . The HJB equation associated with the agents’ control problem is:

This can be simplified using an ansatz to:

Notice that the PDE above requires agents to know the net trading flow of the mean field , but that this quantity itself depends on the value function of each agent which we have yet to solve for. To resolve this issue we first write the optimal control of each agent in feedback form:

Next, we assume that the distribution of inventories and preferences of agents is captured by a density function . With this, the net flow is simply given by the aggregation of all agents’ optimal actions:

In order to compute the quantity at different points in time we need to understand the evolution of the density through time. This is just an application of the Fokker-Planck equation, as is a density that depends on a stochastic process (the inventory level). If we assume that the initial density of inventories and preferences is , we can write the Fokker-Planck equation as:

The full system for the MFG in the problem of Cardaliaguet and Lehalle (2017) involves the combined HJB and Fokker-Planck equations with the appropriate initial and terminal conditions:

Assuming identical preferences allows us to find a closed-form solution to this PDE system. The form of the solution is fairly involved so we refer the interested reader to the details in Cardaliaguet and Lehalle (2017).

Chapter 3 Numerical Methods for PDEs

Although it is possible to obtain closed-form solutions to PDEs, more often we must resort to numerical methods for arriving at a solution. In this chapter we discuss some of the approaches taken to solve PDEs numerically. We also touch on some of the difficulties that may arise in these approaches involving stability and computational cost, especially in higher dimensions. This is by no means a comprehensive overview of the topic to which a vast amount of literature is dedicated. Further details can be found in Burden et al. (2001), Achdou and Pironneau (2005) and Brandimarte (2013).

Finite Difference Method

It is often the case that differential equations cannot be solved analytically, so one must resort to numerical methods to solve them. One of the most popular numerical methods is the finite difference method. As its name suggests, the main idea behind this method is to approximate the differential operators with difference operators and apply them to a discretized version of the unknown function in the differential equation.

Euler’s Method

Arguably, the simplest finite difference method is Euler’s method for ordinary differential equations (ODEs). Suppose we have the following initial value problem

for which we are trying to solve for the function . By the Taylor series expansion, we can write

for any infinitely differentiable real-valued function . If is small enough, and if the derivatives of satisfy some regularity conditions, then terms of order and higher are negligible and we can make the approximation

As a side note, notice that we can rewrite this equation as

which closely resembles the definition of a derivative;

Returning to the original problem, note that we know the exact value of , namely , so that we can write

At this point, it is helpful to introduce the notation for the discretization scheme typically used for finite difference methods. Let be the sequence of values assumed by the time variable, such that and , and let be the sequence of approximations of such that . The expression above can be rewritten as

which allows us to find an approximation for the value of

given the value of . Using Euler’s method, we can find numerical approximations for for any value of .

Explicit versus implicit schemes

In the previous section, we developed Euler’s method for a simple initial value problem. Suppose one has the slightly different problem where the source term is now a function of both and .

A similar argument as before will now lead us to the expression for

where is explicitly written as a sum of terms that depend only on time . Schemes such as this are called explicit. Had we used the approximation

instead, we would arrive at the slightly different expression for

where the term appears in both sides of the equation and

no explicit formula for is possible in general. Schemes

such as this are called implicit. In the general case, each step in

time in an implicit method requires solving the expression above for

using a root finding technique such as Newton’s method

or other fixed point iteration methods.

Despite being easier to compute, explicit methods are generally known to be numerically unstable for a large range of equations (especially so-called stiff problems), making them unusable for most practical situations. Implicit methods, on the other hand, are typically both more computationally intensive and more numerically stable, which makes them more commonly used. An important measure of numerical stability for finite difference methods is A-stability, where one tests the stability of the method for the (linear) test equation , with . While the implicit Euler method is stable for all values of and , the explicit Euler method is stable only if , which may require using a small value for if the absolute value of is high. Of course, all other things being equal, a small value for is undesirable since it means a finer grid is required, which in turn makes the numerical method more computationally expensive.

Finite difference methods for PDEs

In the previous section, we focused our discussion on methods for numerically solving ODEs. However, finite difference methods can be used to solve PDEs as well and the concepts presented above can also be applied in PDEs solving methods. Consider the boundary problem for the heat equation in one spatial dimension, which describes the dynamics of heat transfer in a rod of length :

We could approximate the differential operators in the equation above using a forward difference operator for the partial derivative in time and a second-order central difference operator for the partial derivative in space. Using the notation , with and , we can rewrite the equation above as a system of linear equations

where and , assuming we are using

the same number of discrete points on both dimensions. In this two

dimensional example, the points form a

two dimensional grid of size . For a -dimensional

problem, a -dimensional grid with

size would be required. In practice, the exponential growth of the grid in the number of dimensions rapidly makes the method unmanageable,

even for . This is an important shortcoming of finite difference methods in general.

The scheme developed above is known as the forward difference method

or FTCS (forward in time, central in space). It is easy to verify

that this scheme is explicit in time, since we can write the

terms as a linear combination of previously computed

terms. The number of operations necessary to advance each step in

time with this method should be . Unfortunately,

this scheme is also known to be unstable if and do not satisfy

the inequality .

Alternatively, we could apply the Backward Difference method or BTCS (backward in time, central in space) using the following equations:

This scheme is implicit in time since it is not possible to write the terms as a function of just the previously computed terms. In fact, each step in time requires solving system of linear equations of size . The number of operations necessary to advance each step in time with this method is when using methods such as Gaussian elimination to solve the linear system. On the other hand, this scheme is also known to be unconditionally stable, independently of the values for and .

Higher order methods

All numerical methods for solving PDEs have errors due to many sources

of inaccuracies. For instance, rounding error is related to the

floating point representation of real numbers. Another important category

of error is truncation error, which can be understood as the error

due to the Taylor series expansion truncation. Finite difference methods

are usually classified by their respective truncation errors.

All finite methods discussed so far are low order methods. For instance,

the Euler’s methods (both explicit and implicit varieties) are first-order

methods, which means that the global truncation error is proportional

to , the discretization granularity. However,

a number of alternative methods have lower truncation errors.

For example, the Runge-Kutta 4th-order method, with a global truncation

error proportional to , is widely used, being the most known

method of a family of finite difference methods, which cover even

14th-order methods. Many Runge-Kutta methods are specially suited

for solving stiff problems.

Galerkin methods

In finite difference methods, we approximate the continuous differential

operator by a discrete difference operator in order to obtain a numerical

approximation of the function that satisfies the PDE. The function’s

domain (or a portion of it) must also be discretized so that numerical

approximations for the value of the solution can be computed at the

points of the so defined spatial-temporal grid. Furthermore, the value

of the function on off-grid points can also be approximated by techniques

such as interpolation.

Galerkin methods take an alternative approach: given a finite

set of basis functions on the same domain, the goal is to find a linear

combination of the basis functions that approximates the solution

of the PDE on the domain of interest. This problem translates

into a variational problem where one is trying to find maxima or minima

of functionals.

More precisely, suppose we are trying to solve the equation for , where and are members of spaces of functions and respectively and that is a (possibly non-linear) functional. Suppose also that and form linearly independent bases for and . According to the Galerkin method, an approximation for could be given by

where the coefficients satisfy the equations

for .111https://www.encyclopediaofmath.org/index.php/Galerkin_method

Since the inner products above usually involve non-trivial integrals,

one should carefully choose the bases to ensure the equations are more manageable.

Finite Element Methods

Finite element methods can be understood as a special case of

Galerkin methods. Notice that in the general case presented above,

the approximation may not be well-posed, in the sense that

the system of equations for may have no solution or

it may have multiple solutions depending on the value of . Additionally,

depending on the choice of and , may

not converge to as . Nevertheless, one could

discretize the domain in small enough regions (called elements) so

that the approximation is locally satisfactory in each region. Adding

boundary consistency constraints for each region intersection (as

well as for the outer boundary conditions given by the problem definition)

and solving for the whole domain of interest, one can come up with

a globally fair numerical approximation for the solution to the PDE.

In practice, the domain is typically divided in triangles or quadrilaterals

(two-dimensional case), tetrahedra (three-dimensional case) or more

general geometrical shapes in higher dimensions in a process known

as triangulation. Typical choices for and

are such that the inner product equations above reduce to a system of

algebraic equations for steady state problems or a system of ODEs in the case

of time-dependent problems. If the PDE is linear, those systems will

be linear as well, and they can be solved using methods such as Gaussian

elimination or iterative methods such as Jacobi or Gauss-Seidel. If

the PDE is not linear, one may need to solve systems of nonlinear

equations, which are generally more computationally expensive. One of the major advantages of the finite element methods over finite difference methods, is that finite elements can effortlessly handle complex boundary geometries, which typically arise in physical

or engineering problems, whereas this may be very difficult to achieve with finite difference

algorithms.

Monte Carlo Methods

One of the more fascinating aspects of PDEs is how they are intimately related to stochastic processes. This is best exemplified by the Feynman-Kac theorem, which can be viewed in two ways:

-

•

It provides a solution to a certain class of linear PDEs, written in terms of an expectation involving a related stochastic process;

-

•

It gives a means by which certain expectations can be computed by solving an associated PDE.

For our purposes, we are interested in the first of these two perspectives.

The theorem is stated as follows: the solution to the partial differential equation

admits a stochastic representation given by

where and the process satisfies the SDE:

where is a standard Brownian motion under the probability measure . This representation suggests the use of Monte Carlo methods to solve for unknown function . Monte Carlo methods are a class of numerical techniques based on simulating random variables used to solve a range of problems, such as numerical integration and optimization.

Returning to the theorem, let us now discuss its statement:

-

•

When confronted with a PDE of the form above, we can define a (fictitious) process with drift and volatility given by the processes and , respectively.

-

•

Thinking of as a “discount factor,” we then consider the conditional expectation of the discounted terminal condition and the running term given that the value of at time is equal to a known value, . Clearly, this conditional expectation is a function of and ; for every value of and we have some conditional expectation value.

-

•

This function (the conditional expectation as a function of and ) is precisely the solution to the PDE we started with and can be estimated via Monte Carlo simulation of the process .

A class of Monte Carlo methods have also been developed for nonlinear PDEs, but this is beyond the scope of this work.

Chapter 4 An Introduction to Deep Learning

The tremendous strides made in computing power and the explosive growth in data collection and availability in recent decades has coincided with an increased interest in the field of machine learning (ML). This has been reinforced by the success of machine learning in a wide range of applications ranging from image and speech recognition, medical diagnostics, email filtering, fraud detection and many more.

As the name suggests, the term machine learning refers to computer algorithms that learn from data. The term “learn” can have several meanings depending on the context, but the the common theme is the following: a computer is faced with a task and an associated performance measure, and its goal is to improve its performance in this task with experience which comes in the form of examples and data.

ML naturally divides into two main branches. Supervised learning refers to the case where the data points include a label or target and tasks involve predicting these labels/targets (i.e. classification and regression). Unsupervised learning refers to the case where the dataset does not include such labels and the task involves learning a useful structure that relates the various variables of the input data (e.g. clustering, density estimation). Other branches of ML, including semi-supervised and reinforcement learning, also receive a great deal of research attention at present. For further details the reader is referred to Bishop (2006) or Goodfellow et al. (2016).

An important concept in machine learning is that of generalization which is related to the notions of underfitting and overfitting. In many ML applications, the goal is to be able to make meaningful statements concerning data that the algorithm has not encountered - that is, to generalize the model to unseen examples. It is possible to calibrate an assumed model “too well” to the training data in the sense that the model gives misguided predictions for new data points; this is known as overfitting. The opposite case is underfitting, where the model is not fit sufficiently well on the input data and consequently does not generalize to test data. Striking a balance in the trade-off between underfitting and overfitting, which itself can be viewed as a tradeoff between bias and variance, is crucial to the success of a ML algorithm.

On the theoretical side, there are a number of interesting results related to ML. For example, for certain tasks and hypothesized models it may be possible to obtain the minimal sample size to ensure that the training error is a faithful representation of the generalization error with high confidence (this is known as Probably Approximately Correct (PAC) learnability). Another result is the no-free-lunch theorem, which implies that there is no universal learner, i.e. that every learner has a task on which it fails even though another algorithm can successfully learn the same task. For an excellent exposition of the theoretical aspects of machine learning the reader is referred to Shalev-Shwartz and Ben-David (2014).

Neural Networks and Deep Learning

Neural networks are machine learning models that have received a great deal of attention in recent years due to their success in a number of different applications. The typical way of motivating the approach behind neural network models is to compare the way they operate to the human brain. The building blocks of the brain (and neural networks) are basic computing devices called neurons that are connected to one another by a complex communication network. The communication links cause the activation of a neuron to activate other neurons it is connected to. From the perspective of learning, training a neural network can be thought of as determining which neurons “fire” together.

Mathematically, a neural network can be defined as a directed graph with vertices representing neurons and edges representing links. The input to each neuron is a function of a weighted sum of the output of all neurons that are connected to its incoming edges. There are many variants of neural networks which differ in architecture (how the neurons are connected); see Figure LABEL:fig:NN_arch. The simplest of these forms is the feedforward neural network, which is also referred to as a multilayer perceptron (MLP).

MLPs can be represented by a directed acyclic graph and as such can be seen as feeding information forward. Usually, networks of this sort are described in terms of layers which are chained together to create the output function, where a layer is a collection of neurons that can be thought of as a unit of computation. In the simplest case, there is a single input layer and a single output layer. In this case, output (represented by the th neuron in the output layer), is connected to the input vector via a biased weighted sum and an activation function :

It is also possible to incorporate additional hidden layers between the input and output layers. For example, with one hidden layer the output would become:

where are nonlinear activation functions for each layer and the bracketed superscripts refer to the layer in question. We can visualize an extension of this the process as a simple application of the chain rule, e.g.

Here, each layer of the network is represented by a function , incorporating the weighted sums of previous inputs and activations to connected outputs. The number of layers in the graph is referred to as the depth of the neural network and the number of neurons in a layer represents the width of that particular layer; see Figure 4.2.

The term “deep” neural network and deep learning refer to the use of neural networks with many hidden layers in ML problems. One of the advantages of adding hidden layers is that depth can exponentially reduce the computational cost in some applications and exponentially decrease the amount of training data needed to learn some functions. This is due to the fact that some functions can be represented by smaller deep networks compared to wide shallow networks. This decrease in model size leads to improved statistical efficiency.

It is easy to imagine the tremendous amount of flexibility and complexity that can be achieved by varying the structure of the neural network. One can vary the depth or width of the network, or have varying activation functions for each layer or even each neuron. This flexibility can be used to achieve very strong results but can lead to opacity that prevents us from understanding why any strong results are being achieved.

Next, we turn to the question of how the parameters of the neural network are estimated. To this end, we must first define a loss function, , which will determine the performance of a given parameter set for the neural network consisting of the weights and bias terms in each layer. The goal is to find the parameter set that minimizes our loss function. The challenge is that the highly nonlinear nature of neural networks can lead to non-convexities in the loss function. Non-convex optimization problems are non-trivial and often we cannot guarantee that a candidate solution is a global optimizer.

Stochastic Gradient Descent

The most commonly used approach for estimating the parameters of a neural network is based on gradient descent which is a simple methodology for optimizing a function. Given a function , we wish to determine the value of that achieves the minimum value of . To do this, we begin with an initial guess and compute the gradient of at this point. This gives the direction in which the largest increase in the function occurs. To minimize the function we move in the opposite direction, i.e. we iterate according to:

where is the step size known as the learning rate, which can be constant or decaying in . The algorithm converges to a critical point when the gradient is equal to zero, though it should be noted that this is not necessarily a global minimum. In the context of neural networks, we would compute the derivatives of the loss functional with respect to the parameter set (more on this in the next section) and follow the procedure outlined above.

One difficulty with the use of gradient descent to train neural networks is the computational cost associated with the procedure when training sets are large. This necessitates the use of an extension of this algorithm known as stochastic gradient descent (SGD). When the loss function we are minimizing is additive, it can be written as:

where is the size of the training set and is the per-example loss function. The approach in SGD is to view the gradient as an expectation and approximate it with a random subset of the training set called a mini-batch. That is, for a fixed mini-batch of size the gradient is estimated as:

This is followed by taking the usual step in the opposite direction (steepest descent).

Backpropagation

The stochastic gradient descent optimization approach described in the previous section requires repeated computation of the gradients of a highly nonlinear function. Backpropagation provides a computationally efficient means by which this can be achieved. It is based on recursively applying the chain rule and on defining computational graphs to understand which computations can be run in parallel.

As we have seen in previous sections, a feedforward neural network can be thought of as receiving an input and computing an output by evaluating a function defined by a sequence of compositions of simple functions. These simple functions can be viewed as operations between nodes in the neural network graph. With this in mind,

the derivative of with respect to can be computed analytically by

repeated applications of the chain rule, given enough information about the

operations between nodes. The backpropagation algorithm traverses the graph, repeatedly computing the chain rule until the derivative of the output with respect to is represented symbolically via a second computational graph; see Figure 4.3.

The two main approaches for computing the derivatives in the computational graph is to input a numerical value then compute the derivatives at this value, returning a number as done in PyTorch (pytorch.org), or to compute the derivatives of a symbolic variable, then store the derivative operations into new nodes added to the graph for later use as done in TensorFlow (tensorflow.org). The advantage of the latter approach is that higher-order derivatives can be computed from this extended graph by running backpropagation again.

The backpropagation algorithm takes at most operations

for a graph with nodes, storing at most new nodes. In practice,

most feedforward neural networks are designed in a chain-like way, which in turn reduces

the number of operations and new storages to , making derivatives calculations

a relatively cheap operation.

Summary

In summary, training neural networks is broadly composed of three ingredients:

-

1.

Defining the architecture of the neural network and a loss function, also known as the hyperparameters of the model;

-

2.

Finding the loss minimizer using stochastic gradient descent;

-

3.

Using backpropagation to compute the derivatives of the loss function.

This is presented in more mathematical detail in Figure 4.4.

-

1.

Define the architecture of the neural network by setting its depth (number

of layers), width (number of neurons in each layer) and activation functions -

2.

Define a loss functional , mini-batch size and learning rate

-

3.

Minimize the loss functional to determine the optimal :

-

(a)

Initialize the parameter set,

-

(b)

Randomly sample a mini-batch of training examples

-

(c)

Compute the loss functional for the sampled mini-batch

-

(d)

Compute the gradient using backpropagation

-

(e)

Use the estimated gradient to update based on SGD:

-

(f)

Repeat steps (b)-(e) until is small.

-

(a)

The Universal Approximation Theorem

An important theoretical result that sheds some light on why neural networks perform well is the universal approximation theorem, see Cybenko (1989) and Hornik (1991). In simple terms, this result states that any continuous function defined on a compact subset of can be approximated arbitrarily well by a feedforward network with a single hidden layer.

Mathematically, the statement of the theorem is as follows: let be a nonconstant, bounded, monotonically-increasing continuous function and let denote the -dimensional unit hypercube. Then, given any and any function defined on , there exists such that the approximation function:

satisfies for all .

A remarkable aspect of this result is the fact that the activation function is independent of the function we wish to approximate! However, it should be noted that the theorem makes no statement on the number of neurons needed in the hidden layer to achieve the desired approximation error, nor whether the estimation of the parameters of this network is even feasible.

Other Topics

Adaptive Momentum

Recall that the stochastic gradient descent algorithm is parametrized by a learning rate which determines the step size in the direction of steepest descent given by the gradient vector. In practice, this value should decrease along successive iterations of the SGD algorithm for the network to be properly trained. For a network’s parameter set to be properly optimized, an appropriately chosen learning rate schedule is in order, as it ensures that the excess error is decreasing in each iteration. Furthermore, this learning rate schedule can depend on the nature of the problem at hand.

For the reasons discussed in the last paragraph, a number of different algorithms have been developed to find some heuristic capable of guiding the selection of an effective sequence of learning rate parameters. Inspired by physics, many of these algorithms interpret the gradient as a velocity vector, that is, the direction and speed at which the parameters move through the parameter space. Momentum algorithms, for example, calculate the next velocity as a weighted sum of the gradient from the last iteration and the newly calculated one. This helps minimize instabilities caused by the high sensitivity of the loss function with respect to some directions of the parameter space, at the cost of introducing two new parameters, namely a decay factor, and an initialization parameter . Assuming these sensitivities are axis-dependent, we can apply different learning rate schedules to each direction and adapt them throughout the training session.

The work of Kingma and Ba (2014) combines the ideas discussed in this section in a single framework referred to as Adaptative Momentum (Adam). The main idea is to increase/decrease the learning rates based on the past magnitudes of the partial derivatives for a particular direction. Adam is regarded as being robust to its hyperparameter values.

The Vanishing Gradient Problem

In our analysis of neural networks, we have established that the addition of layers to a network’s architecture can potentially lead to great increases in its performance: increasing the number of layers allows the network to better approximate increasingly more complicated functions in a more efficient manner. In a sense, the success of deep learning in current ML applications can be attributed to this notion.

However, this improvement in power can be counterbalanced by the Vanishing Gradient Problem: due to the the way gradients are calculated by backpropagation, the deeper a network is the smaller its loss function’s derivative with respect to weights in early layers becomes. At the limit, depending on the activation function, the gradient can underflow in a manner that causes weights to not update correctly.

Intuitively, imagine we have a deep feedforward neural network consisting of layers. At every iteration, each of the network’s weights receives an update that is proportional to the gradient of the error function with respect to the current weights. As these gradients are calculated using the chain rule through backpropagation, the further back a layer is, the more it is multiplied by an already small gradient.

Long-Short Term Memory and Recurrent Neural Networks

Applications with time or positioning dependencies, such as speech recognition and natural language processing, where each layer of the network handles one time/positional step, are particularly prone to the vanishing gradient problem. In particular, the vanishing gradient might mask long term dependencies between observation points far apart in time/space.

Colloquially, we could say that the neural network is not able to accurately remember important information from past layers. One way of overcoming this difficulty is to incorporate a notion of memory for the network, training it to learn which inputs from past layers should flow through the current layer and pass on to the next, i.e. how much information should be “remembered” or “forgotten.” This is the intuition behind long-short term memory (LSTM) networks, introduced by Hochreiter and Schmidhuber (1997).

LSTM networks are a class of recurrent neural networks (RNNs) that consists of layers called LSTM units. Each layer is composed of a memory cell, an input gate, an output gate and a forget gate which regulates the flow of information from one layer to another and allows the network to learn the optimal remembering/forgetting mechanism. Mathematically, some fraction of the gradients from past layers are able to pass through the current layer directly to the next. The magnitude of the gradient that passes through the layer unchanged (relative to the portion that is transformed) as well as the discarded portion, is also learned by the network. This embeds the memory aspect in the architecture of the LSTM allowing it to circumvent the vanishing gradient problem and learn long-term dependencies; refer to Figure 4.5 for a visual representation of a single LSTM unit.

Inspired by the effectiveness of LSTM networks and given the rising importance of deep architectures in modern ML, Srivastava et al. (2015) devised a network that allows gradients from past layers to flow through the current layer. Highway networks use the architecture of LSTMs for problems where the data is not sequential. By adding an “information highway,” which allows gradients from early layers to flow unscathed through intermediate layers to the end of the network, the authors are able to train incredibly deep networks, with depth as high as a 100 layers without vanishing gradient issues.

Chapter 5 The Deep Galerkin Method

Introduction

We now turn our attention to the application of neural networks to finding solutions to PDEs.

As discussed in Chapter 3, numerical methods that are based on grids can fail when the dimensionality of the problem becomes too large. In fact, the number of points in the mesh grows exponentially in the number of dimensions which can lead to computational intractability. Furthermore, even if we were to assume that the computational cost was manageable, ensuring that the grid is set up in a way to ensure stability of the finite difference approach can be cumbersome.

With this motivation, Sirignano and Spiliopoulos (2018) propose a mesh-free method for solving PDEs using neural networks. The Deep Galerkin Method (DGM) approximates the solution to the PDE of interest with a deep neural network. With this parameterization, a loss function is set up to penalize the fitted function’s deviations from the desired differential operator and boundary conditions. The approach takes advantage of computational graphs and the backpropagation algorithm discussed in the previous chapter to efficiently compute the differential operator while the boundary conditions are straightforward to evaluate. For the training data, the network uses points randomly sampled from the region where the function is defined and the optimization is performed using stochastic gradient descent.

The main insight of this approach lies in the fact that the training data consists of randomly sampled points in the function’s domain. By sampling mini-batches from different parts of the domain and processing these small batches sequentially, the neural network “learns” the function without the computational bottleneck present with grid-based methods. This circumvents the curse of dimensionality which is encountered with the latter approach.

Mathematical Details

The form of the PDEs of interest are generally described as follows: let be an unknown function of time and space defined on the region where , and assume that satisfies the PDE:

The goal is to approximate with an approximating function given by a deep neural network with parameter set . The loss functional for the associated training problem consists of three parts:

-

1.

A measure of how well the approximation satisfies the differential operator:

Note: parameterizing as a neural network means that the differential operator can be computed easily using backpropagation.

-

2.

A measure of how well the approximation satisfies the boundary condition:

-

3.

A measure of how well the approximation satisfies the initial condition:

In all three terms above the error is measured in terms of -norm, i.e. using with being a density defined on the region . Combining the three terms above gives us the cost functional associated with training the neural network:

The next step is to minimize the loss functional using stochastic gradient descent. More specifically, we apply the algorithm defined in Figure 5.1. The description given in Figure 5.1 should be thought of as a general outline as the algorithm should be modified according to the particular nature of the PDE being considered.

-

1.

Initialize the parameter set and the learning rate .

-

2.

Generate random samples from the domain’s interior and time/spatial boundaries, i.e.

-

•

Generate from according to

-

•

Generate from according to

-

•

Generate from , according to

-

•

-

3.

Calculate the loss functional for the current mini-batch (the randomly sampled points ):

-

•

Compute

-

•

Compute

-

•

Compute

-

•

Compute

-

•

-

4.

Take a descent step at the random point with Adam-based learning rates:

-

5.

Repeat steps (2)-(4) until is small.

It is important to notice that the problem described here is strictly an optimization problem. This is unlike typical machine learning applications where we are concerned with issues of underfitting, overfitting and generalization. Typically, arriving at a parameter set where the loss function is equal to zero would not be desirable as it suggests some form of overfitting. However, in this context a neural network that achieves this is the goal as it would be the solution to the PDE at hand. The only case where generalization becomes relevant is when we are unable to sample points everywhere within the region where the function is defined, e.g. for functions defined on unbounded domains. In this case, we would be interested in examining how well the function satisfies the PDE in those unsampled regions. The results in the next chapter suggest that this generalization is often very poor.

A Neural Network Approximation Theorem

Theoretical motivation for using neural networks to approximate solutions to PDEs is given as an elegant result in Sirignano and Spiliopoulos (2018) which is similar in spirit to the Universal Approximation Theorem. More specifically, it is shown that deep neural network approximators converge to the solution of a class of quasilinear parabolic PDEs as the number of hidden layers tends to infinity. To state the result in more precise mathematical terms, define the following:

-

•

, the loss functional measuring the neural network’s fit to the differential operator and boundary/initial/terminal conditions;

-

•

, the class of neural networks with hidden units;

-

•

, the best -layer neural network approximation to the PDE solution.

The main result is the convergence of the neural network approximators to the true PDE solution:

Further details, conditions, statement of the theorem and proofs are found in Section 7 of Sirignano and Spiliopoulos (2018). It is should be noted that, similar to the Universal Approximation Theorem, this result does not prescribe a way of designing or estimating the neural network successfully.

Implementation Details

The architecture adopted by Sirignano and Spiliopoulos (2018) is similar to that of LSTMs and Highway Networks described in the previous chapter. It consists of three layers, which we refer to as DGM layers: an input layer, a hidden layer and an output layer, though this can be easily extended to allow for additional hidden layers.

From a bird’s-eye perspective, each DGM layer takes as an input the original mini-batch inputs (in our case this is the set of randomly sampled time-space points) and the output of the previous DGM layer. This process culminates with a vector-valued output which consists of the neural network approximation of the desired function evaluated at the mini-batch points. See Figure 5.2 for a visualization of the overall architecture.

Within a DGM layer, the mini-batch inputs along with the output of the previous layer are transformed through a series of operations that closely resemble those in Highway Networks. Below, we present the architecture in the equations along with a visual representation of a single DGM layer in Figure 5.3:

where denotes Hadamard (element-wise) multiplication, is the total number of layers, is an activation function and the , and terms with various superscripts are the model parameters.

Similar to the intuition for LSTMs, each layer produces weights based on the last layer, determining how much of the information gets passed to the next layer. In Sirignano and Spiliopoulos (2018) the authors also argue that including repeated element-wise multiplication of nonlinear functions helps capture “sharp turn” features present in more complicated functions. Note that at every iteration the original input enters into the calculations of every intermediate step, thus decreasing the probability of vanishing gradients of the output function with respect to .

Compared to a Multilayer Perceptron (MLP), the number of parameters in each hidden layer of the DGM network is roughly eight times bigger than the same number in an usual dense layer. Since each DGM network layer has 8 weight matrices and 4 bias vectors while the MLP network only has one weight matrix and one bias vector (assuming the matrix/vector sizes are similar to each other). Thus, the DGM architecture, unlike a deep MLP, is able to handle issues of vanishing gradients, while being flexible enough to model complex functions.

Remark on Hessian implementation: second-order differential equations call for the computation of second derivatives. In principle, given a deep neural network , the computation of higher-order derivatives by automatic differentiation is possible. However, given for , the computation of those derivatives becomes computationally costly, due to the quadratic number of second derivative terms and the memory-inefficient manner in which the algorithm computes this quantity for larger mini-batches. For this reason, we implement a finite difference method for computing the Hessian along the lines of the methods discussed in Chapter 3. In particular, for each of the sample points , we compute the value of the neural net and its gradients at the points and , for each canonical vector , where is the step size, and estimate the Hessian by central finite differences, resulting in a precision of order . The resulting matrix is then symmetrized by the transformation .

Chapter 6 Implementation of the Deep Galerkin Method

In this chapter we apply the Deep Galerkin Method to solve various PDEs that arise in financial contexts, as discussed in Chapter 2. The application of neural networks to the problem of numerically solving PDEs (and other problems) requires a great deal of experimentation and implementation decisions. Even with the basic strategy of using the DGM method, there are already numerous decisions to make, including:

-

•

the network architecture;

-

•

the size of the neural network to use to achieve a good balance between execution time and accuracy;

-

•

the choice of activation functions and other hyperparameters;

-

•

the random sampling strategy, selection of optimization and numerical (e.g. differentiation and integration) algorithms, training intensity;

-

•

programming environment.

In light of this, our approach was to begin with simple and more manageable PDEs and then, as stumbling blocks are gradually surpassed, move on to more challenging ones. We present the results of applying DGM to the following problems:

-

1.

European Call Options:

We begin with the Black-Scholes PDE, a linear PDE which has a simple analytical solution and is a workhorse model in finance. This also creates the basic setup for the remaining problems. -

2.

American Put Options:

Next, we tackle American options, whose main challenge is the free boundary problem, which needs to be found as part of the solution of the problem. This requires us to adapt the algorithm (particularly, the loss function) to handle this particular detail of the problem. -

3.

The Fokker-Plank Equation:

Subsequently, we address the Fokker-Planck equation, whose solution is a probability density function that has special constraints (such as being positive on its domain and integrating to one) that need to met by the method. -

4.

Stochastic Optimal Control Problems:

For even more demanding challenges, we focus on HJB equations, which can be highly nonlinear. In particular, we consider two optimal control problems: the Merton problem and the optimal execution problem. -

5.

Systemic Risk:

The systemic risk problem allows us to apply the method to a multidimensional system of HJB equations, which involves multiple variables and equations with a high degree of nonlinearity. -

6.

Mean Field Games:

Lastly, we close our work with mean field games, which are formulated in terms of conversant HJB and Fokker-Planck equations.

The variety of problems we manage to successfully apply the method to attests to the power and flexibility of the DGM approach.

How this chapter is organized

Each section in this chapter highlights one of the case studies mentioned in the list above. We begin with the statement of the PDE and its analytical solution and proceed to present (possibly several) attempted numerical solutions based on the DGM approach. The presentation is done in such a way as to highlight the experiential aspect of our implementation. As such the first solution we present is by no means the best, and the hope is to demonstrate the learning process surrounding the DGM and how our solutions improve along the way. Each example is intended to highlight a different challenge faced - usually associated with the difficulty of the problem, which is generally increasing in examples - and a proverbial “moral of the story.”

An important caveat is that, in some cases, we don’t tackle the full problem in the sense that the PDEs that are given at the start of each section are not always in their primal form. The reason for this is that the PDEs may be too complex to implement in the DGM framework directly. This is especially true with HJB equations which involve an optimization step as part of the first order condition. In these cases we resort to to simplified versions of the PDEs obtained using simplifying ansatzes, but we emphasize that even these can be of significant difficulty.

Remark (a note on implementation):

in all the upcoming examples we use the same network architecture used by Sirignano and Spiliopoulos (2018) presented in Chapter 5, initializing the weights with Xavier initialization. The network was trained for a number of iterations (epochs) which may vary by example, with random re-sampling of points for the interior and terminal conditions every 10 iterations. We also experimented with regular dense feedforward neural networks and managed to have some success fitting the first problem (European options) but we found them to be less likely to fit more irregular functions and more unstable to hyperparameters changes as well.

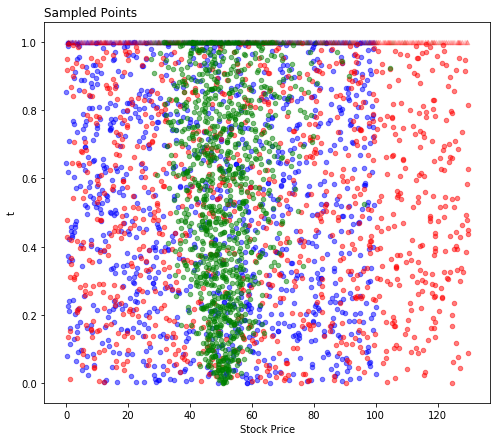

European Call Options

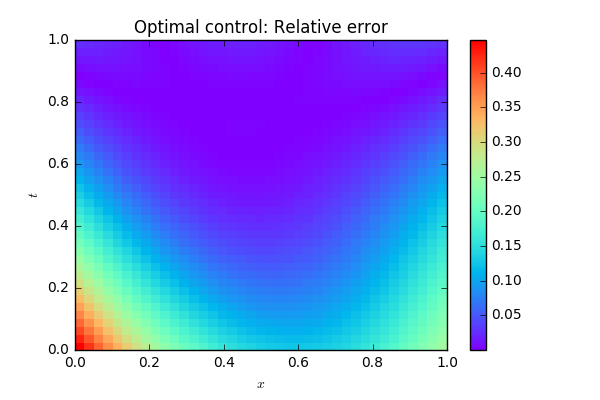

As a first example of the DGM approach, we trained the network to learn the value of a European call option. For our experiment, we used the interest rate , the volatility , the initial stock price , the maturity time and the option’s strike price . In Figure 6.2 we present the true and estimated option values at different times to maturity.

First, we sampled uniformly on the time domain and according to a lognormal distribution on the space domain as this is the exact distribution that the stock prices follow in this model. We also sampled uniformly at the terminal time point. However, we found that this did not yield good results for the estimated function. These sampled points and fits can be seen in the green dots and lines in Figure 6.1 and Figure 6.2.

Since the issues seemed to appear at regions that were not well-sampled we returned to the approach of Sirignano and Spiliopoulos (2018) and sampled uniformly in the region of interest . This improved the fit, as can be seen in the blue lines of Figure 6.2, however, there were still issues on the right end of the plots with the fitted solution dipping too early.

Finally, we sampled uniformly beyond the region of interest on to show the DGM network points that lie to the right of the region of interest. This produced the best fit, as can be seen by the red lines in Figure 6.2.

Another point worth noting is that the errors are smaller for times that are closer to maturity. This reason for this behavior could be due to the fact that the estimation process is “drawing information” from the terminal condition. Since this term is both explicitly penalized and heavily sampled from, this causes the estimated function to behave well in this region. As we move away from this time point, this stabilizing effect diminishes leading to increased errors.

Moral: sampling methodology matter!

American Put Options

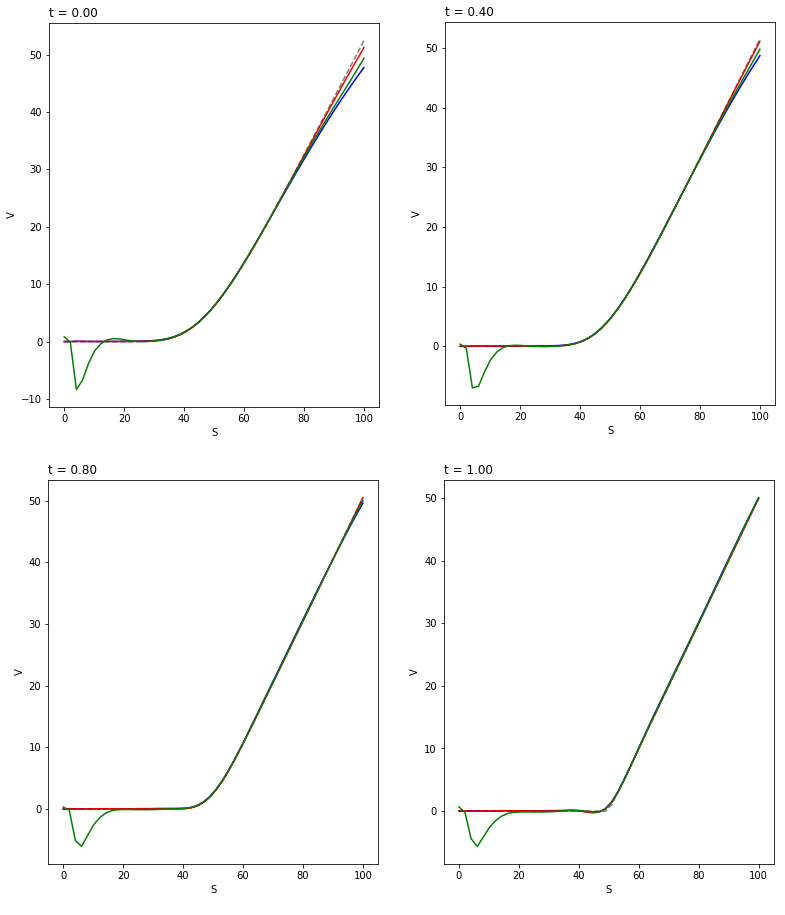

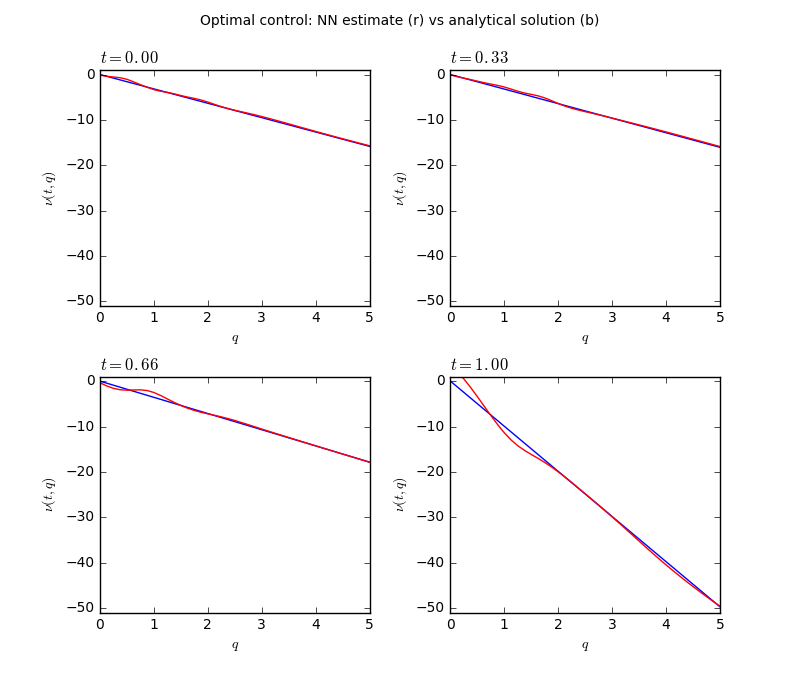

In order to further test the capabilities of DGM nets, we trained the network to learn the value of American-style put options. This is a step towards increased complexity, compared to the European variant, as the American option PDE formulation includes a free boundary condition. We utilize the same parameters as the European call option case: , , , and .

In our first attempt, we trained the network using the method prescribed by Sirignano and Spiliopoulos (2018). The approach for solving free boundary problems there is to sample uniformly over the region of interest ( in our case), and accept/reject training examples for that particular batch of points, depending on whether or not they are inside or outside the boundary region implied by the last iteration of training. This approach was able to correctly recover option values.

As an alternative approach, we used a different formulation of the loss function that takes into account the free boundary condition instead of the acceptance/rejection methodology. In particular, we applied a loss to all points that violated the condition via:

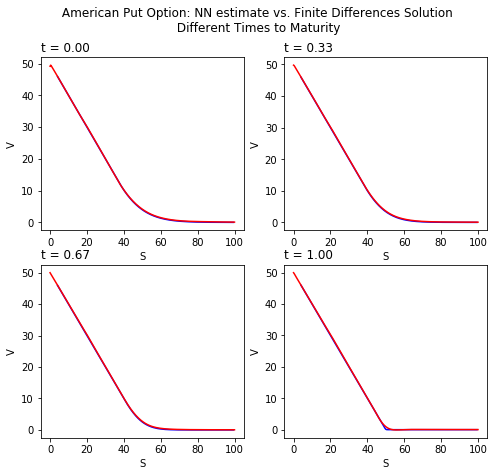

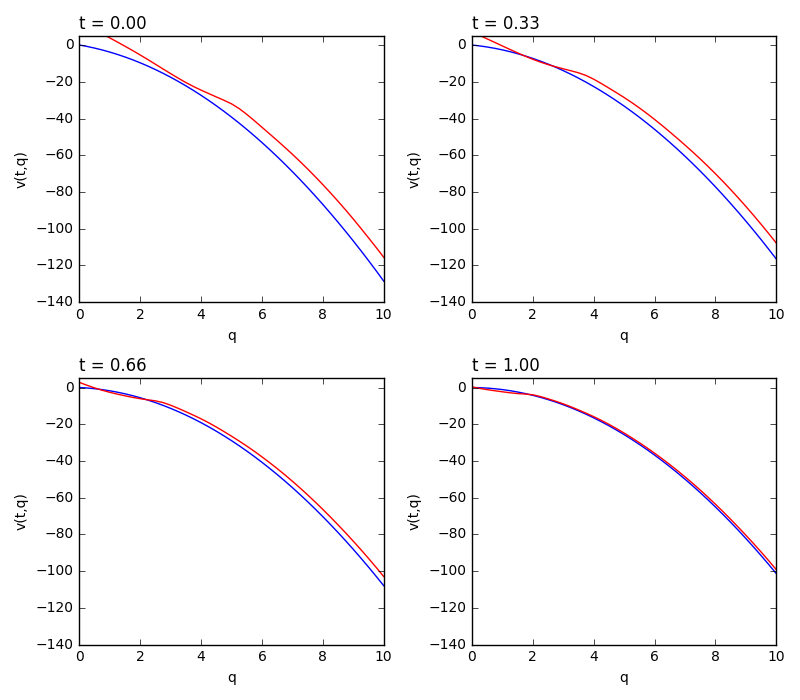

Figure 6.3 compares the DGM fitted option prices obtained using the alternative inequality loss for different maturities compared to the finite difference method approach. The figure shows that we are successful at replicating the option prices with this loss function.

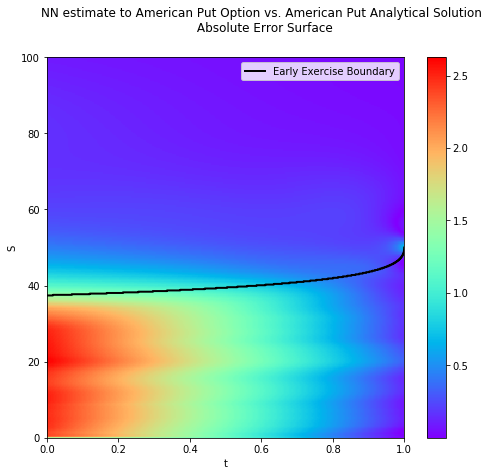

Figure 6.4

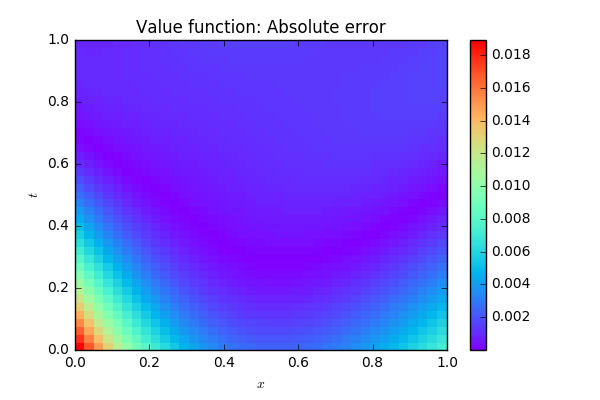

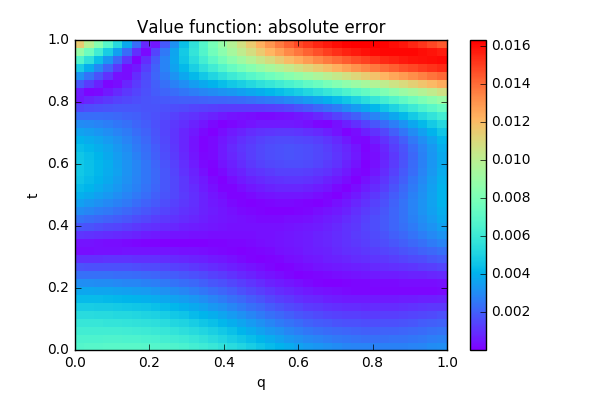

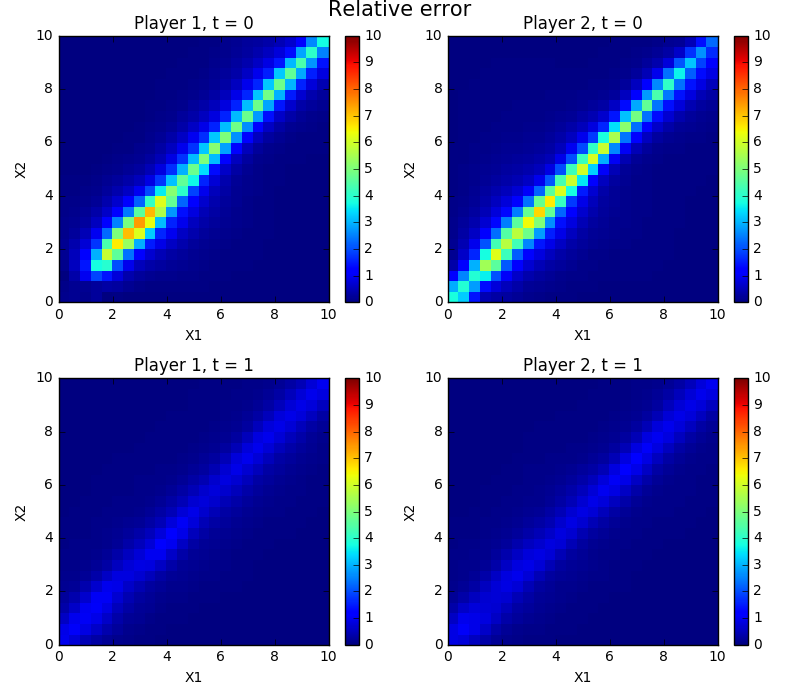

depicts the absolute error between the estimated put option values and the analytical prices for corresponding European puts given by the Black-Scholes formula. Since the two should be equal in the continuation region, this can be a way of indirectly obtaining the early exercise boundary. The black line is the boundary obtained by the finite difference method and we see that is it closely matched by our implied exercise boundary. The decrease in the difference between the two option prices below the boundary as time passes reflects the deterioration of the early exercise optionality in the American option.

Moral: loss functions matter!

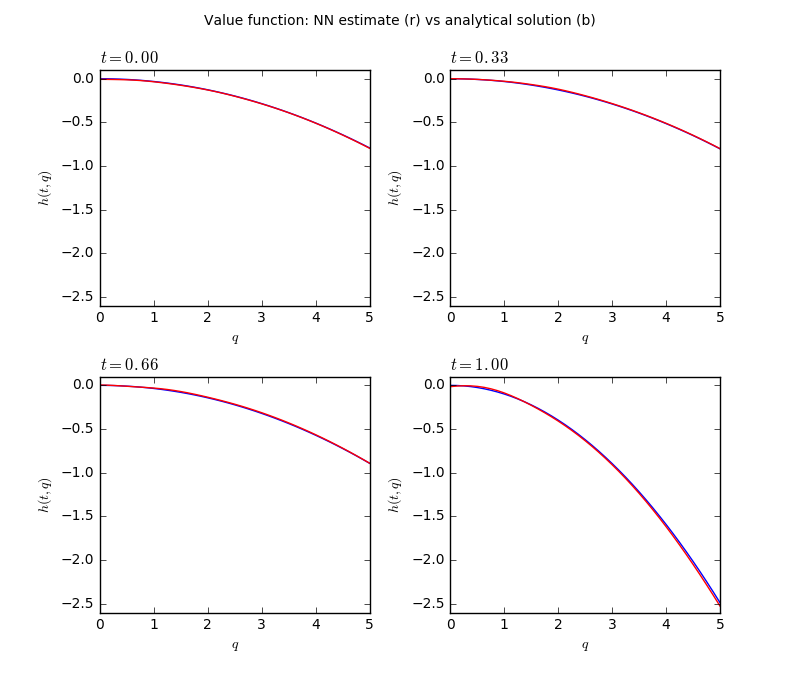

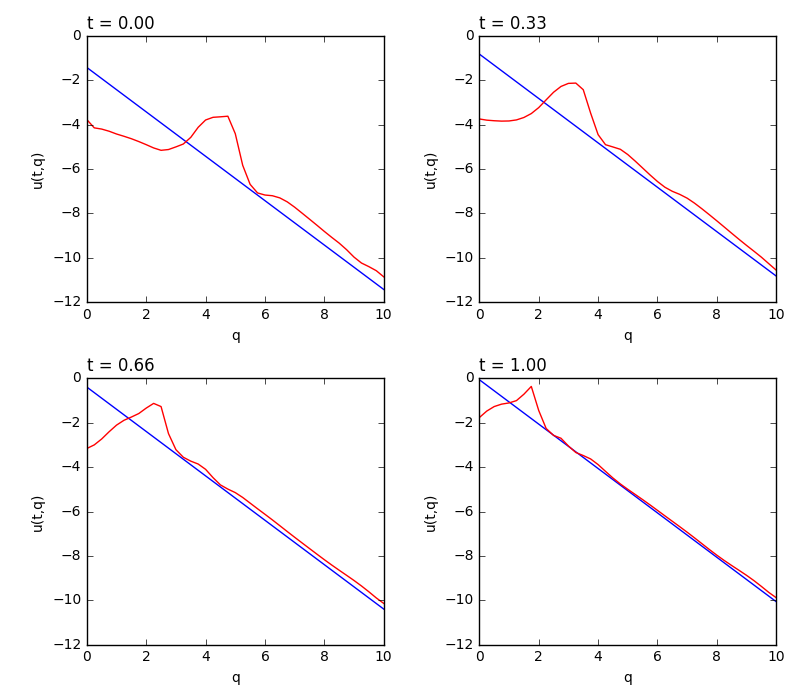

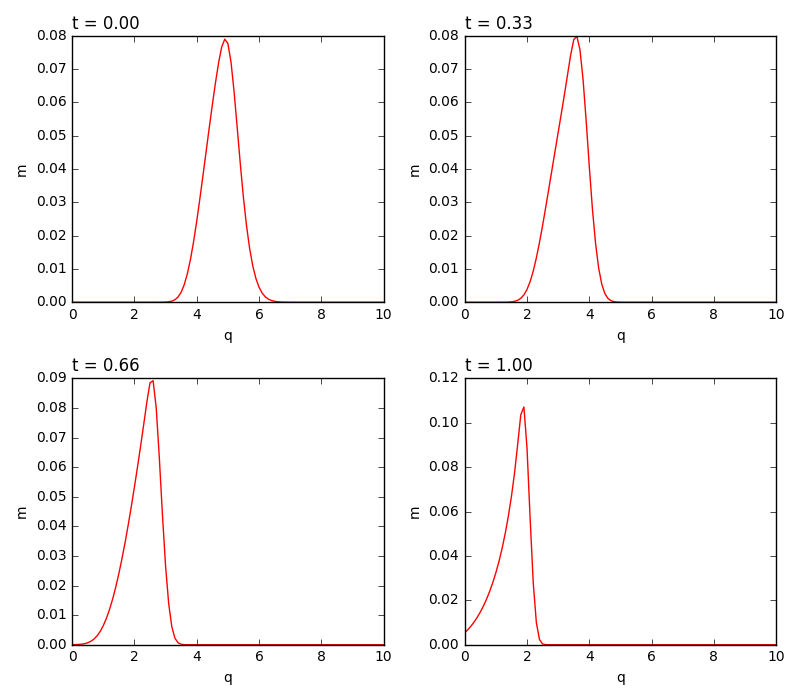

Fokker-Planck Equations

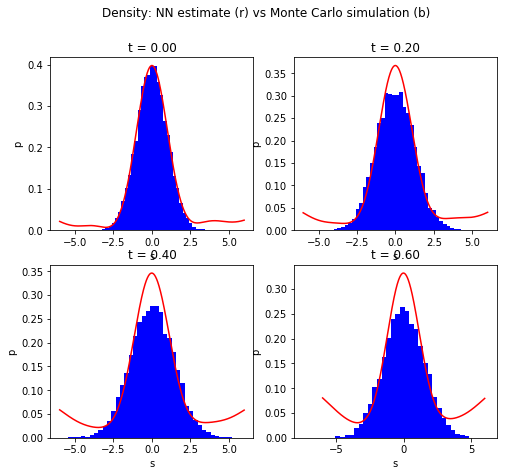

The Fokker-Planck equation introduces a new difficulty in the form of a constraint on the solution. We applied the DGM method to the Fokker-Planck equation for the Ornstein–Uhlenbeck mean-reverting process. If the process begins at a fixed point , i.e. its initial distribution is a Dirac delta at , then the solution for this PDE is known to have the normal distribution

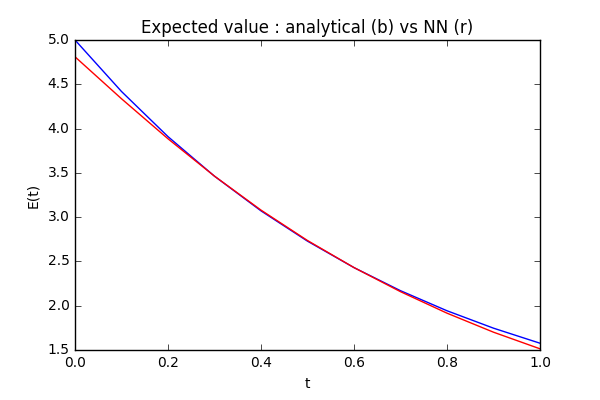

Since it is not possible to directly represent the initial delta numerically, one would have to approximate it, e.g. with a normal distribution with mean and a small variance. In the case where the starting point is Gaussian, we use Monte Carlo simulation to determine the distribution at every point in time, but we note that the distribution should be Gaussian since we are essentially using a conjugate prior.

For the DGM algorithm, we used loss function terms for the differential

equation itself, the initial condition and added a penalty to reflect the non-negativity constraint. Though we intended to include another term to force the integral of the solution to equal one, this

proved to be too computationally expensive, since an integral must be numerically evaluated at each step of the network training phase. For the parameters , , , , Figure 6.5 shows the density estimate as a function of position at different time points compared to the simulated distribution. As can be seen from these figures, the fitted distributions had issues around the tails and with the overall height of the fitted curve, i.e. the fitted densities did not integrate to 1. The neural network estimate, while correctly approximating the initial condition, is not able to conserve probability mass and the Gaussian bell shape across time.

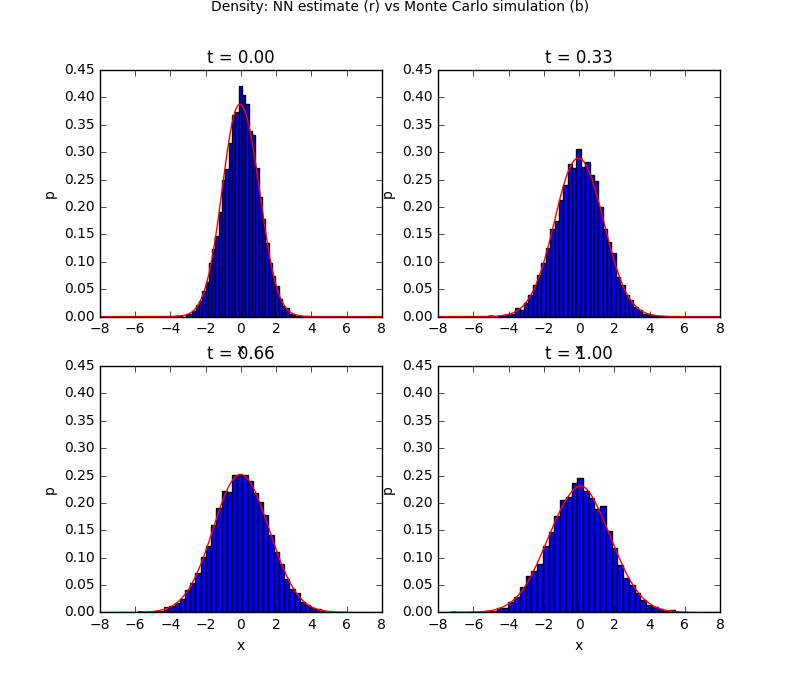

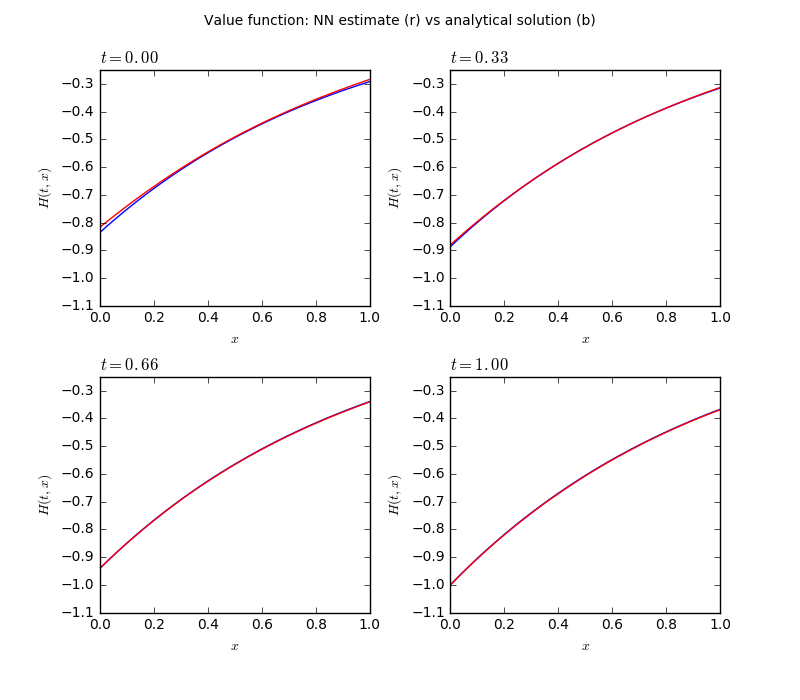

To improve on the results, we apply a change of variables:

where is a normalizing constant. This amounts to fitting an exponentiated normalized neural network guaranteed to remain positive and integrate to unity. This approach provides an alternative PDE to be solved by the DGM method:

Notice that the new equation is a non-linear PDE dependent on a integral term. To handle the integral term and avoid the costly operation of numerically integrating at each step, we first uniformly sample from and from , then, for each , we use importance sampling to approximate the expectation term by

where