Distributionally Robust Optimization with

Confidence

Bands for Probability Density Functions

Abstract

Distributionally robust optimization (DRO) has been introduced for solving stochastic programs where the distribution of the random parameters is unknown and must be estimated by samples from that distribution. A key element of DRO is the construction of the ambiguity set, which is a set of distributions that covers the true distribution with a high probability. Assuming that the true distribution has a probability density function, we propose a class of ambiguity sets based on confidence bands of the true density function. The use of the confidence band enables us to take the prior knowledge of the shape of the underlying density function into consideration (e.g., unimodality or monotonicity). Using the confidence band constructed by density estimation techniques as the ambiguity set, we establish the convergence of the optimal value of DRO to that of the stochastic program as the sample size increases. However, the resulting DRO problem is computationally intractable, as it involves functional decision variables as well as infinitely many constraints. To address this challenge, using the duality theory, we reformulate it into a finite-dimensional stochastic program, which is amenable to a stochastic subgradient scheme as a solution method. We compare our approach with existing state-of-the-art DRO methods on the newsvendor problem and the portfolio management problem, and the numerical results showcase the advantage of our approach.

Keywords: Distributionally robust optimization; first-order method; confidence band; data-driven ambiguity sets

1 Introduction

The goal of stochastic programming (SP) is to minimize the expectation of an objective function that depends on both decision variables and some random parameters. Assuming that the random parameters follow a distribution denoted by , a stochastic program can be formulated as follows:

| (1) |

where is the vector of decision variables, is the feasible set, is the vector of random variables taking values in with the distribution , and is the objective function. SP has been actively studied for several decades: see [5], [41] and references thereafter. Suppose is absolutely continuous and thus has a probability density function with respect to the Lebesgue measure. In other words, we have such that for any Borel set . We can further write (1) as follows:

| (2) |

Despite of their popularity, (2) is often challenging to solve since the distribution or the density of is rarely known in real-life applications. When a set of historical observations of is collected, one may solve the approximation of (1) by replacing with an estimated distribution from the dataset, e.g., the empirical distribution. However, due to the approximation error, the decision obtained from the approximate problem may be of inferior quality and thus may have an undesirable out-of-sample performance; see [2, 13, 29]. An alternative approach for solving (2) with an unknown distribution is distributionally robust optimization (DRO), in which one constructs an ambiguity set consisting of all distributions that are likely to be and then minimizes the expectation of the objective function over the worst-case distribution from the ambiguity set. In particular, letting be the ambiguity set, we can formulate DRO as follows:

| (3) |

Scarf first proposed this model for a newsvendor problem [39], and it has been extensively studied over the past in operations research and operations management community since then.

The ambiguity sets constructed by most of the aforementioned approaches contain distributions that are not absolutely continuous. In fact, as shown in many of the works, the worst-case distribution in their ambiguity set corresponding to the optimal decision of (3) is discrete. However, in some applications, the vector of random parameter is known to be absolutely continuous (e.g., when models the price of electricity or the return of securities). In this case, by solving (3) with these ambiguity sets, one may obtain a solution that is hedging against a discrete distribution that will never be the true distribution. This phenomenon potentially leads to over-conservative decisions in the DRO problems.

In this paper, we consider the situation where is absolutely continuous and propose a family of ambiguity sets consisting of only absolutely continuous distributions, or equivalently, distributions with density functions. With such an ambiguity set, the DRO model corresponding to (2) is given as:

| (4) |

Thus, the worst-case distribution corresponding to the optimal solution of (4) will be absolutely continuous.

We note that the ambiguity set of density functions has also been considered by [30] and [8]. While their ambiguity sets contain only polynomial density functions, our approach does not require for similar restrictions. We also note that the ambiguity set considered in [30] utilizes the kernel density estimation, as does one of our ambiguity sets. While their method must specify the Legendre polynomial series density estimator, our method allows for using a broader family of kernel density estimations. Moreover, our ambiguity set is constructed with data samples and fully utilizes shape information of the density function (e.g., unimodality or monotonicity), while the ambiguity set constructed in [8] is not based on a data-driven approach. Indeed, their ambiguity set is constructed using other prior knowledge on (e.g., moment information).

Other works closely related to our method include [25, 27]. Li and Jiang consider an ambiguity set with moment and generalized unimodal constraints [27]. Lam imposes convexity constraints on the tail of the density function [25]. The main difference between our approach and theirs is that our methods use the shape information on and a dataset generated by to construct the ambiguity set, while theirs does not use data samples and directly impose shape information as constraints in their optimization problems.

In the rest of the paper, we first propose the generic DRO in Section 2, followed by the construction of our data-driven ambiguity sets by using density estimation techniques from the statistics literature. In particular, we will present two classes of ambiguity sets and showcase their convergence to the true density function and further prove the convergence of the optimal value of (4) to the optimal objective value of the SP in (2) as the sample size increases to infinity; see detail in Section 3. The setting of our ambiguity set gives rise to a challenging problem to solve, as the resulting optimization problem (4) involves functional decision variables (i.e., the density ) and infinitely many constraints. In Section 4, taking the exploitation of the special structure of our ambiguity set, we show that (4) can be reformulated into a finite-dimensional convex stochastic program, which is amenable to an efficient stochastic first-order method approach as the solution method. Finally, we validate our approach with a newsvendor problem and a portfolio management problem in Section 5. The numerical results demonstrate that our approach can generate decisions with superior out-of-sample performances, especially when the number of observations is limited.

1.1 Literature review

In the existing literature, different approaches have been utilized to construct ambiguity sets. We briefly review some popular approaches as follows:

-

•

A moment-based ambiguity set is often constructed to consist of all distributions that share common marginal or cross moments; see [4, 6, 7, 9, 8, 11, 12, 16, 17, 27, 31, 43, 46, 47]. DRO problems with moment-based ambiguity sets in the format of (4) can usually be reformulated into tractable conic programs, e.g., second-order cone programming problems or semidefinite programming problems. However, the constructed ambiguity sets are not guaranteed to converge to the true distribution , as the size of the historical observations increases to infinity, although the estimations of the moments of the random variables are guaranteed to converge to their true values.

-

•

A distance-based ambiguity set is constructed by using some distance function to measure the distance between two distributions in the probability space. In fact, such an ambiguity set can be considered as a ball centered at a reference distribution, e.g., the empirical distribution, in the space of probability distributions. The distance functions considered in the literature include Kullback-Leibler divergence [20, 22], -divergence[1, 10, 24], Prohorov metric [12], empirical Burg-entropy divergence balls [25], and Wasserstein metric [34, 45, 13, 15, 14]. Many distance-based ambiguity sets have both asymptotic and finite-sample convergences. However, there is evidence that the resulting DRO problems have the tendency to be more challenging to solve compared to their counterparts with moment-based ambiguity sets; see [13].

-

•

More recently, hypothesis-test-based ambiguity sets have been proposed; see [2, 3]. Based on a hypothesis test, e.g., -test, -test, etc., and a confidence level, these approaches construct ambiguity sets consisting of the distributions that pass the hypothesis test with a given set of historical data. The methods that we use in this paper belong to this category.

- •

1.2 Notation and terminology

Let denote the Euclidean projection operator on to the set , i.e., Let be the indicator function that equals one when and zero when . Unless stated otherwise, the terms “almost every”, “measurable”, and “integrable” are defined with respect to the Lebesgue sense. For an extended-real valued function on , let be its epigraph, be its domain, be its subdifferential, and be its any subgradient. We call a multifunction if it maps a point in to a subset of . A multifunction is closed valued if is a closed subset of for every and is measurable if, for every closed set , the set is measurable. We define . A mapping is called a measurable (integrable) selection of if it is measurable (integrable) and for every . We use to represent the set .

2 Data-Driven Distributionally Robust Optimization

In this paper, we consider an ambiguity set that consists of the density functions whose value is between two known non-negative functions. To construct such a set, we assume that there exists a set of independent realizations of the random variable (i.e., samples from ) denoted by

Then, for a given , we construct two functions and based on , , and some prior knowledge on (e.g., its shape property) such that

| (5) |

We call the pair the confidence bands for the density functions at a confidence level of and is called the significance level. We will introduce two methods to construct such a ambiguity set in Section 3.

Using , we can construct an ambiguity set that contains with a confidence level of . More specifically, let be the space of all non-negative Lebesgue-measurable functions on . We consider the following ambiguity set:

| (7) |

which satisfies according to (5).

With , we can specify the distributionally robust optimization problem in (4) as

| (8) |

Immediately, we have the following result for the optimal value of (8).

Proposition 1.

Suppose the minimal objective value of (8) is finite and achieved at . Let . We have

Proof.

Proof. Whenever , we have . By the construction of the ambiguity set , we have ∎

3 Data-Driven Ambiguity Sets

In this section, we present two existing methods from the statistics literature to construct a confidence band for a density function based on observed data. The first method is applicable to only univariate distributions while the second one is applicable to multivariate distributions. Although we only described two confidence bands as the specific instances for constructing the ambiguity set in (7), the optimization method we propose in Section 4 can be applied to DRO with any ambiguity set in the form of (7) with other constructions of confidence bands.

3.1 Shape-restricted confidence bands

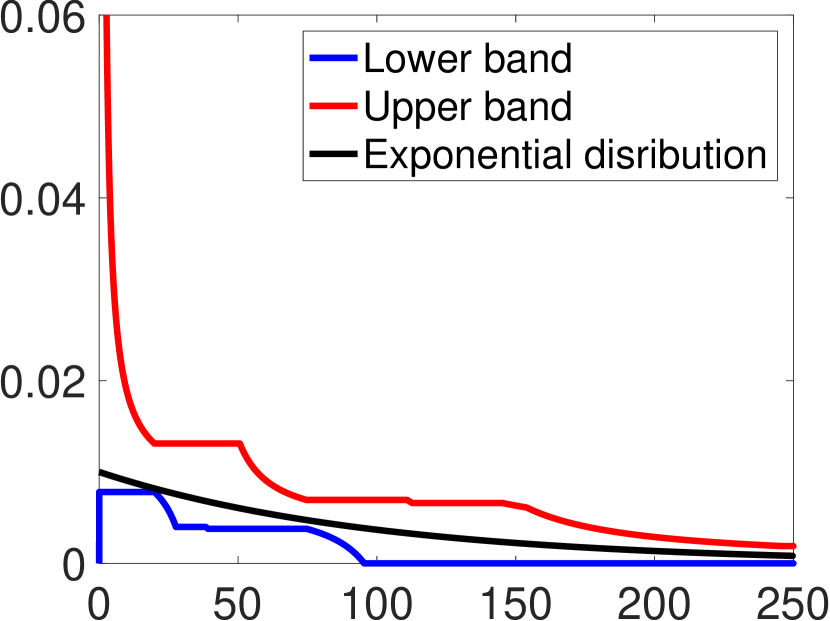

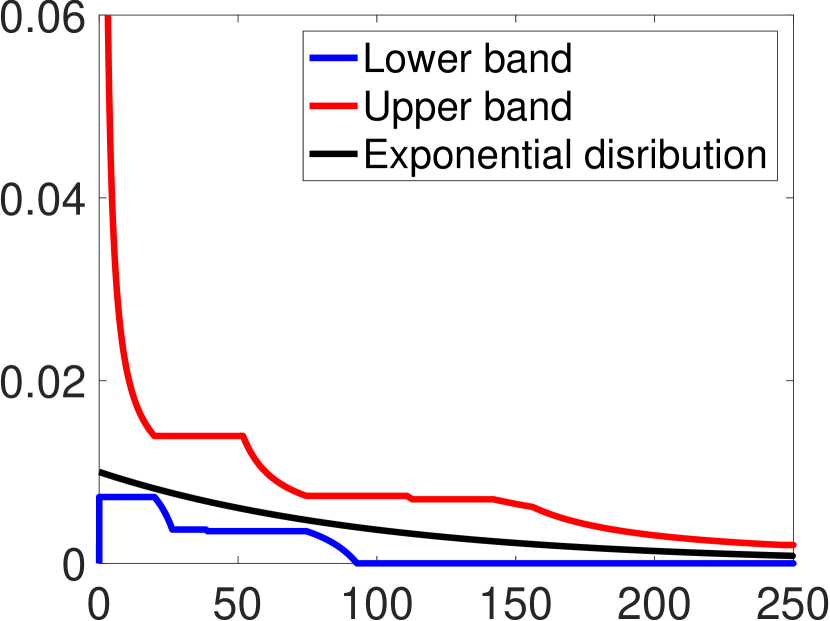

In this subsection, we present the method by [19] to construct a confidence band for with a confidence level of and use it to build an ambiguity set like (7). Although this method only applies to a univariate density function, it is able to incorporate some shape information about (e.g., unimodality and monotonicity) into the construction of the ambiguity set which improves the theoretical convergence rate of the set to the true density .

We need the following assumptions in this subsection.

Assumption 1 (For shape-restricted confidence bands.).

We assume:

-

A1.

(the support of ) is connected and contained in with known and satisfying .

-

A2.

is unimodal with a known mode , meaning that is monotonically increasing on and decreasing on .

-

A3.

There exists a known constant such that for any .

In Assumption 1 [A1.], we assume that and are finite for the simplicity of the notations in the derivation below. In fact, our results can be generalized when and . Moreover, for most applications, a conservative estimation of the range of is usually available, which can be directly used as . We also note that Assumption 1 [A2.] also covers the case where is known to be monotonically increasing () or decreasing (). In some real applications, the unimodality or monotonicity of a random parameter is a well-known fact and thus should be incorporated into the problem formulation. Note that the method by [19] can also used to construct a confidence band even when the mode is only known to be in an interval .

First, let be the order statistics of constructed from satisfying . We choose a group size satisfying and define and . Then we partition the sorted sequence into groups with the first groups of size and the th group (if ) of size . We then define for and for if . Let be the cumulative density function of . It is well-known that (citation?) the random variable has the same distribution as

| (9) |

where represents a gamma random variable with a shape parameter and a rate parameter . Let and be two constants that satisfy

Both and can be estimated to arbitrary precision by sampling according to (9). Let be the set of all density functions on with mode at , i.e.

and

Then, by the definitions of and , we have

Given the property above, can be used as an uncertainty set in (8). However, this uncertainty set may be too large to ensure a good solution from solving (8). Therefore, we need to further refine it using the prior knowledge about the shape of given in Assumption 1. Next, we show how to construct a shape-constrained confidence band using the technique from in [19].

Given any , let () be the number of distinct elements in the set and be the smallest element in this set. Then, we consider the following two sets of non-negative step functions on defined as

| (13) |

| (16) |

where denotes the indicator function. Both and consist of piecewise constant density functions on with break points on but with different continuous properties (i.e., left-continuity or right-continuity) on these break points. Then, the confidence band for given by [19] is a pair of functions defined as

| (17) |

Here, the superscript “SR” refers to “shape restricted”. By its definition, the value of function () equals the smallest (largest) value at of all density functions which have the form in (13) ((16)) and satisfy for all . Then, our shape-restricted uncertainty set are defined as

| (19) |

The following theorem is given by [19].

Theorem 1.

.

We then describe the method for compute and for any . Given , recall that denotes the smallest element in . Let and be the indexes in such that and . Using these indexes, we define a polyhedron

| (24) |

According to (13), (16) and (17), for any , and can be computed respectively by solving the following linear programs

| (25) |

Note that the first line of constraints in (24) is because is the mode of any in and . The second line of the constraints in (24) corresponds to the condition when is the step function in (13) and (16). The third line requires that must a density function while the last line requires is non-negative and no more than according the prior information of .

We summary this procedure by [19] for constructing a confidence band for a unimodal density function in Algorithm 1.

It is worthwhile to note that if the density is monotone, for example, non-decreasing, we have and the first line of the constraints in (24) becomes . Note also that, in the original work [19], no upper bound for is needed to construct this uncertainty set . In this paper, we require knowing so that we can include a constraint in (24), this modification does not change the statistical property of (i.e., Theorem 1) once we assume . We need the constraint only to ensure and which are needed in our theoretical analysis.

[19] established the convergence rate of the constructed confidence band in the following proposition.111The original Corollary 7.2 [19] was stated a little differently form from Proposition 2. In fact, the conclusion there replaces in (26) by and equality in (26) by . Their results were obtained by choosing the parameter appearing in the proof of Corollary 7.2 [19]. However, the same proof works for Proposition 2 and thus implies (26) if we choose .

Proposition 2 (Corollary 7.2 [19]).

Let but . Suppose is -Holder continuous for constants and , i.e., for any and . Suppose for a constant and sufficiently large . We have

| (26) |

According to the lower bound in [23], the convergence rate in (26) attains the minimax rate and thus is optimal (upto a constant factor) for the confidence band for a unimodal density. It is also worthwhile to note that the rate of convergence from Kolmogorov-Smirnov distance is slower as compared to this approach. As shown in [18], the confidence band formed by the Kolmogorov-Smirnov distance is only , which is slower than the rate of in Proposition 2 when .

Proposition 2 shows the pointwise convergence of the confidence band to the true distribution . In the next theorem, we show that, under additional assumption, we can characterize the convergence in probability of define in (8) to in (2).

Theorem 2.

Suppose is -Holder continuous for constants and , i.e., for any and . Moreover, suppose . For any and , there exists an such that for any , we have

and

Proof.

Proof. See Appendix Proof of Theorem 2. ∎

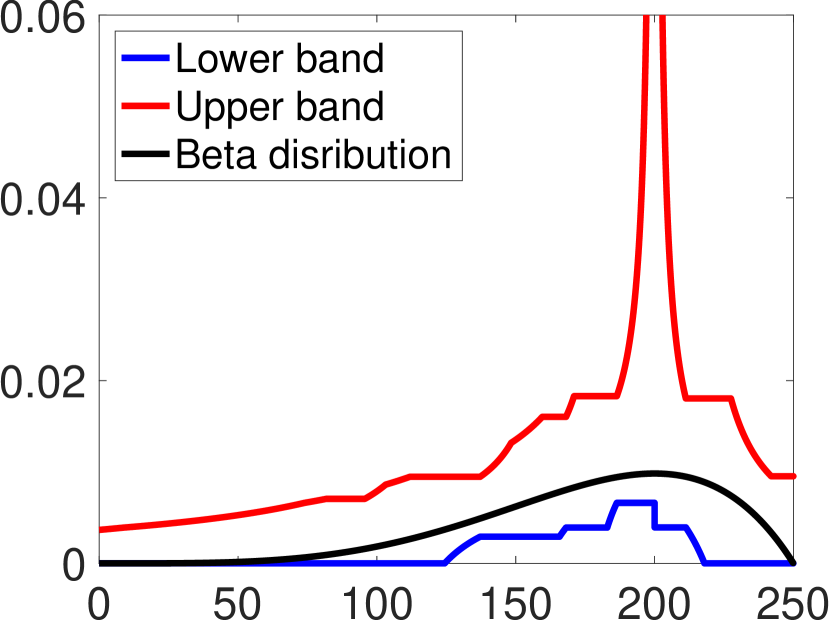

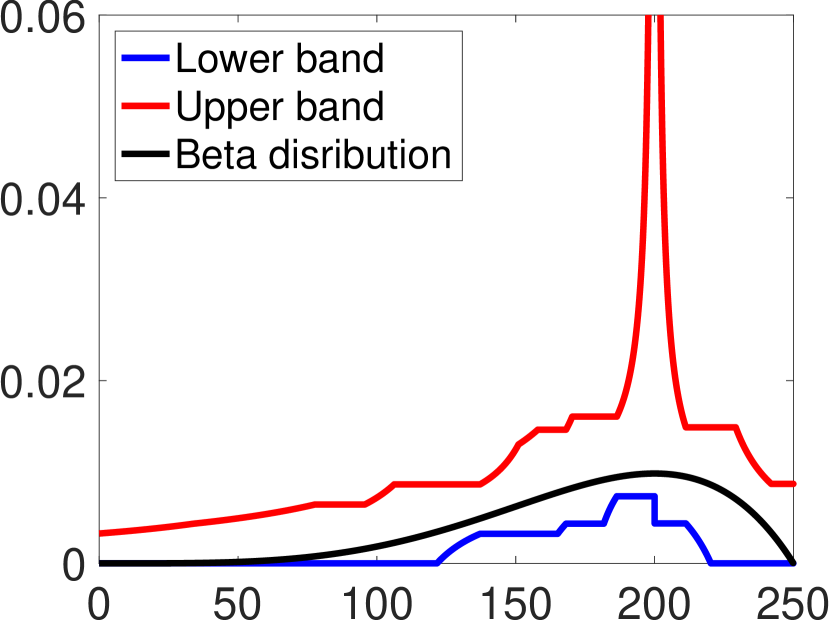

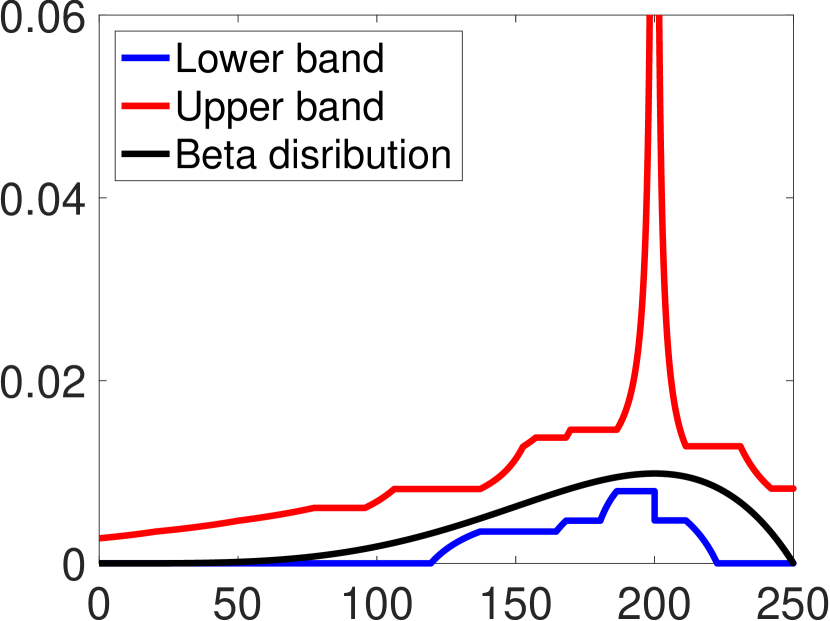

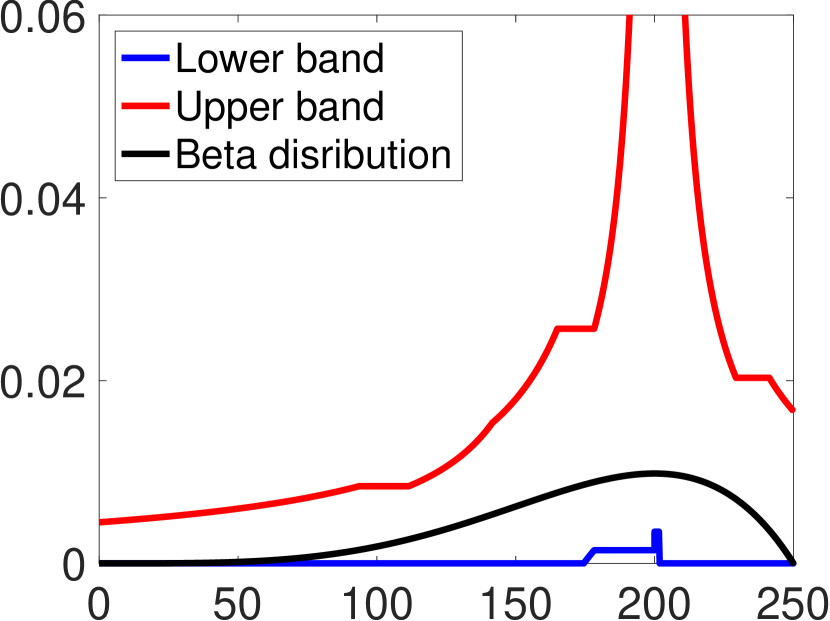

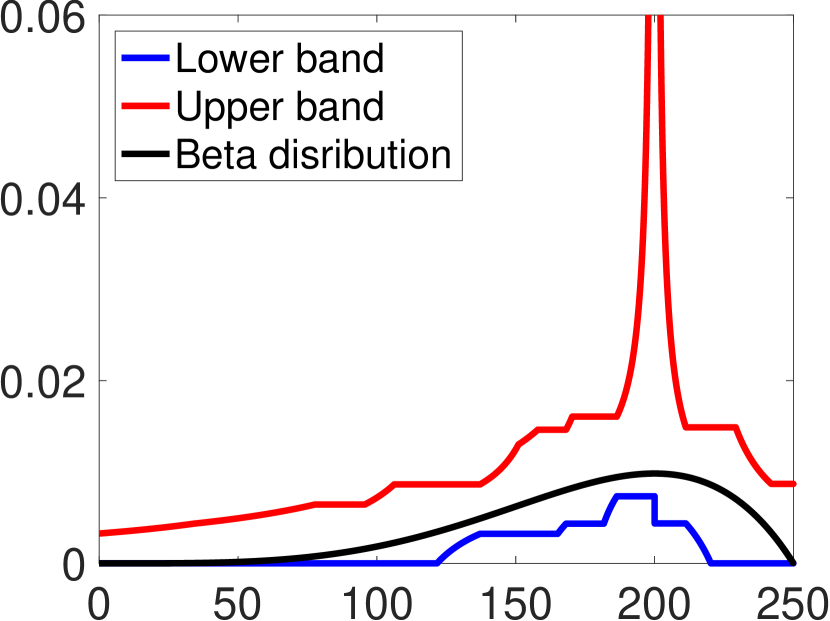

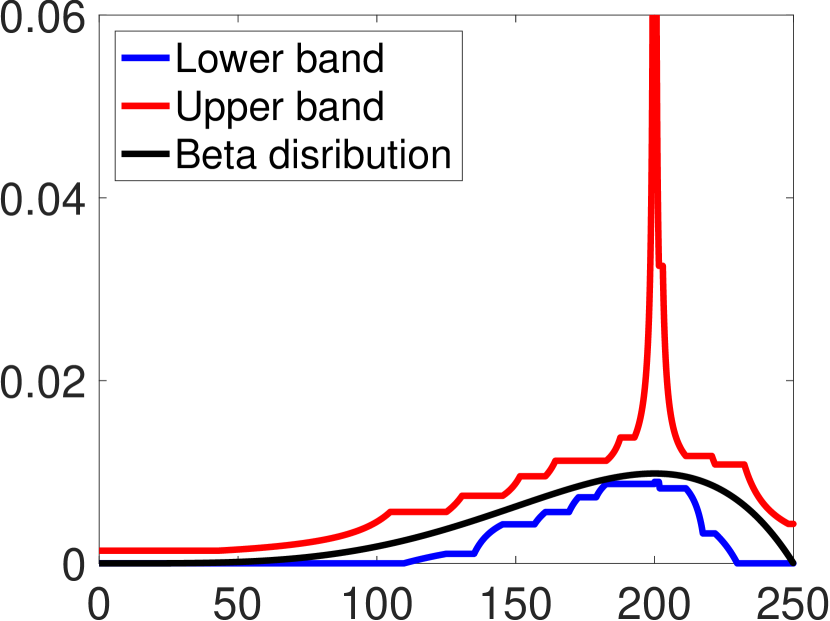

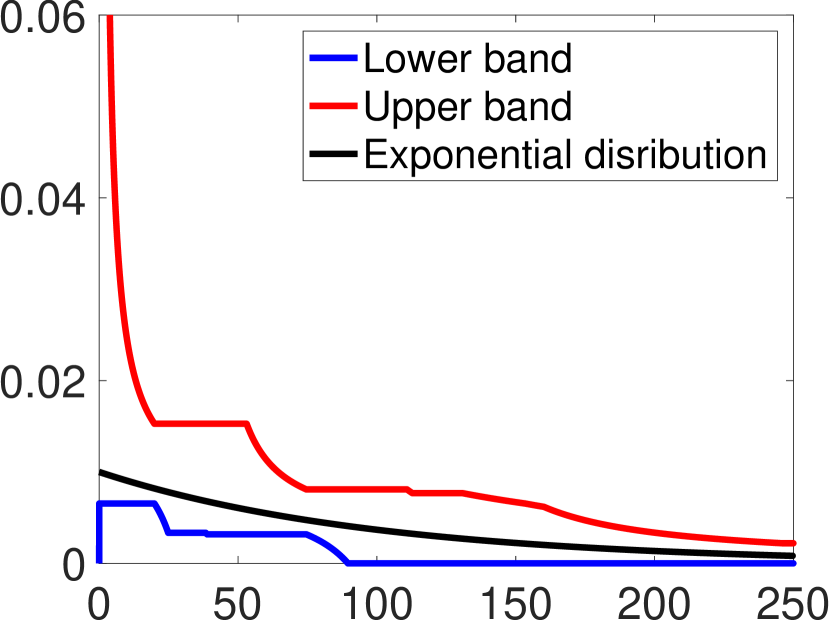

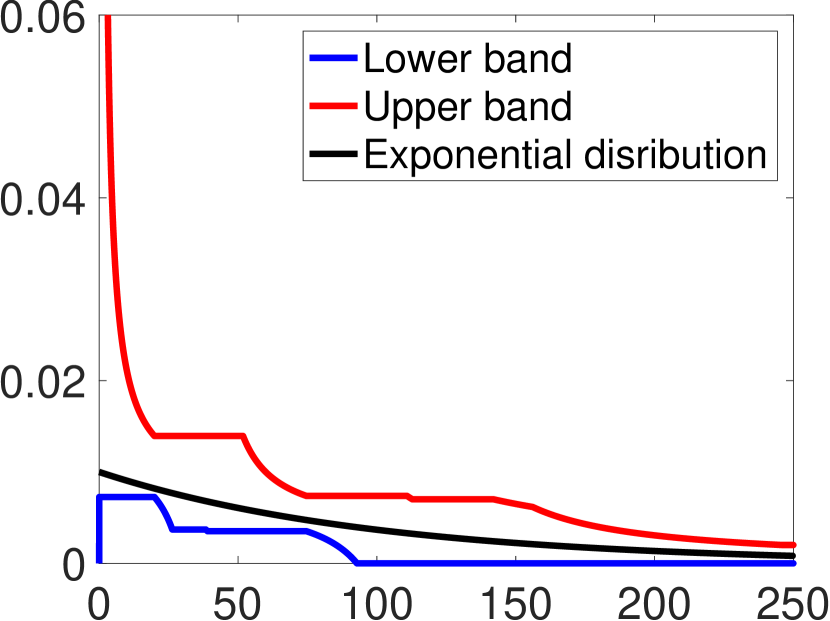

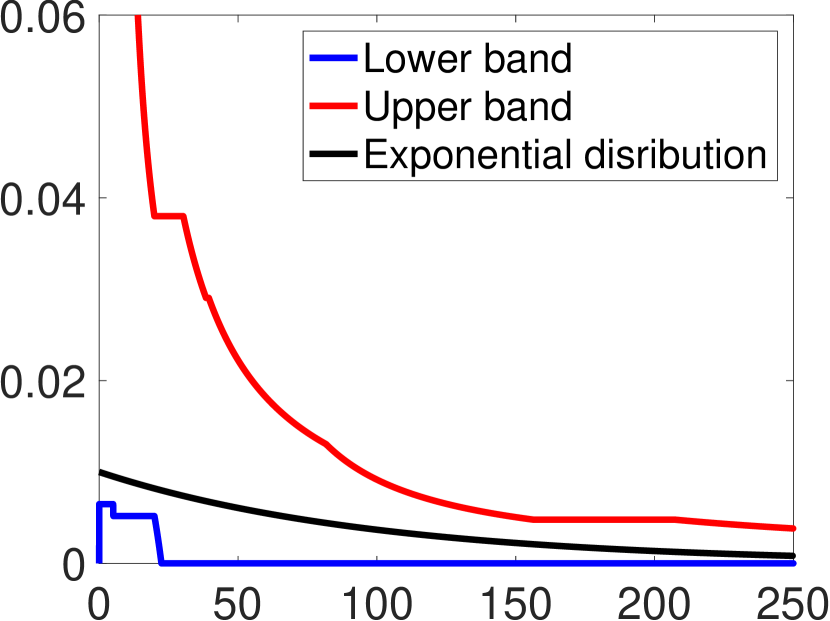

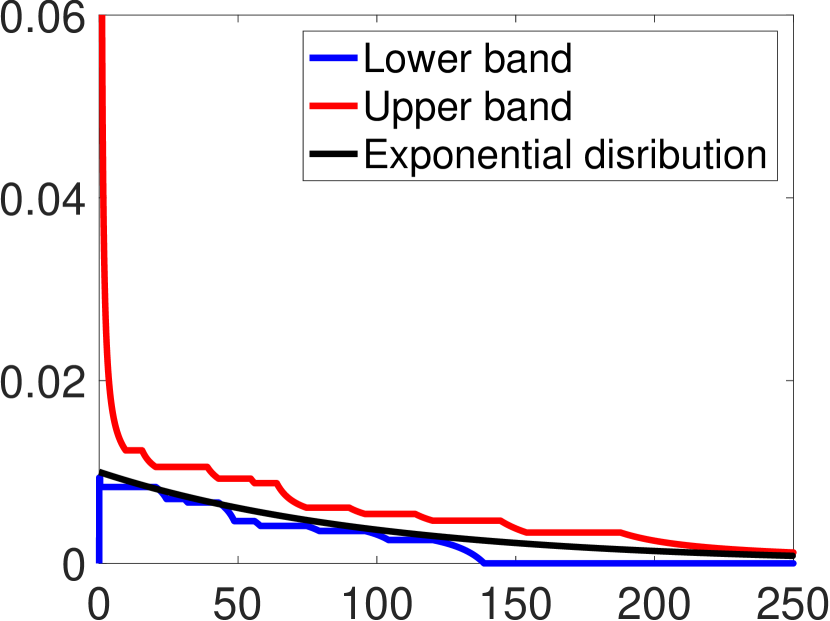

Finally, illustrations of this method are given in Figure 1(f) for a beta distribution and in Figure 2(f) for a truncated exponential distribution. (What exact parameters?)

3.2 Kernel-desnsity-estimation confidence bands

The shape-restricted confidence bands described in the previous section can only be applied to univariate density function. In this subsection, we describea method to construct confidence bands for multivariate density function based on the classical kernel density estimation (KDE) [38, 33]. This method requires a kernel function which is a mapping satisfying . The commonly use kernel functions include uniform kernel and Guassian kernel . Let be a bandwidth parameter. Recall that is i.i.d. samples drawn from . The KDE of based on , and is

| (27) |

The convergence of to the true density have been studied for a long time (see e.g. [42]) with most of existing works focusing the asymptotic convergence property. Recently, the finite-sample non-asymptotic convergence property of KDE is characterized by [36] and [21]. The confidence band we construct based on KDE utilize the non-asymptotic convergence bound by [21].

We need the following assumptions in this subsection.

Assumption 2 (For KDE confidence bands.).

We assume:

-

A1.

There exists a constant such that for any .

-

A2.

There exists a non-increasing function such that .

-

A3.

There exists , and such that for , .

A2 and A3 of Assumption 2 hold if is one of the popular kernel densities (up to scaling) in , including the two mentioned above as well as Exponential, Tricube, triangular, and Epanechnikov kernels. Under these assumptions, the following finite-sample convergence result is established by [21].

Proposition 3.

Based on the convergence property in Proposition 3, with , we construct the KDE confidence band of a significance level of for as follows

| (28) |

where

| (29) |

The corresponding uncertainty set is

| (31) |

The following property is a direct consequence of Proposition 3.

Theorem 3.

.

We summary this procedure for constructing a KDE confidence band in Algorithm 2.

Theorem 4.

Suppose is -Holder continuous for constants and , i.e., for any and . Moreover, suppose and . For any and , there exists an such that for any , we have

and

Proof.

Proof. See Appendix Proof of Theorem 4. ∎

4 An Numerical Method for DRO

In this section, we discuss a numerical scheme for solving the DRO problem in (8) with an ambiguity set in the form of (7). Here, the ambiguity can be one of the two ambiguity sets and introduced in Section 3 as long as Assumption 1 or 2 is satisfied. However, our numerical methods can be applied to a general ambiguity set like (7) as long as the following assumptions are satisfied. We make the following assumption regarding to :

Assumption 3 (On ambiguity set ).

-

a.

.

-

b.

.

Note that, under Assumption 1, satisfies Assumption 3 because for an upper bound of according to its definition (25) and the constraints in (24). Under Assumption 2, with the appropriate bandwidth (See Theorem 3), we have with a high probability.

We define as the optimal value of the inner maximization problem of (7), i.e.,

| (32) |

By Assumption 3, for every ,

| (33) |

Note that (32) is a continuous linear program which are formulated with continuously many decision variable (or a functional decision variable) and continuously many constraints. In general, (32) cannot be reformulated as a convex optimization problem of finite dimension and solved by off-the-shelf optimization techniques as in most of the works in distributionally robust optimization. In this section, we propose a stochastic subgradient descent (SGD) method for solving (32) and present its convergence rate.

The dual problem of (32) is given as follows:

| (34) |

Weak duality always hold between (32) and (34). Furthermore, by the result of [40], strong duality holds between (32) and (34). Since , it is easy to eliminate and in (34) and write it equivalently as:

| (35) |

where and . Thus, we have

| (36) |

In general, the two integrals appearing in (36) do not have an analytical form, raising a challenging for finding the optimal solution. In this section, we provide a stochastic gradient (SGD) method for solving (36) by approximating these integrals with random samples of . To apply gradient-based algorithm like SGD, we need to be able to compute the subgradient of in (36) with respect to both and . For doing that, we assume there exists a measurable mapping such that for any and , where is the subdifferential of with respect to . Then, under mild regularity conditions, the subgradients of with respect to and are, respectively,

| (37) | |||||

| (38) |

where is an indicator function. Then, we can use Monte Carlo method to approximate the integral in the subgradients above.

In particular, let be a set that contains the support of and . Note that such a set always exists because is assumed to be compact. We denote the volume of the box as and assume it can be computed. In fact, we can choose to be a box so that is the product of the lengths of all edges. Suppose is sampled from a uniform distribution on . We can show that (37) is the expectation of and (38) is the expectation of . Hence, we can use these two as the stochastic subgradient of . Although the algorithm converges with any number of samples, we can apply the mini-batch techniques by generating i.i.d. samples from the uniform distribution on and constructing such a stochastic subgradient using each sample and then take the average of all samples. This mini-batch approach reduces the approximation noise of the Monte Carlo method and accelerate the algorithm in practice.

Based on this idea, we proposed the SGD method for (36) in Algorithm 3. Note that and are the mini-batch stochastic subgradients of with respect to and , respectively, with a batch size of . The convergence analysis of Algorithm 3 is standard and well-known (see e.g. [32]) so we present the theorem below but omit its proof.

Theorem 5.

Suppose there exists a constant such that . Algorithm 3 ensures

| (39) | |||||

5 Computational Results

In this section, we validate our approach on two examples: a single-item newsvendor problem and a portfolio selection problem. Particularly, for the newsvendor example, we compare our approach with that in [2], which applies hypothesis tests to construct ambiguity sets, and for the portfolio selection example, we compare our approach with that in [13], which applies the Wasserstein metric to construct ambiguity sets. We implement Algorithm 3 in MATLAB (R2014a) version 8.3.0.532. The linear programs from the approaches in the literature are solved by CPLEX 12.4 on an Intel Core i3 2.93 GHz Windows computer with 4GB of RAM and the mathematical models are implemented by using the modeling language YALMIP [28] in MATLAB (R2014a) version 8.3.0.532.

5.1 Single-item newsvendor

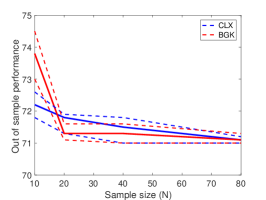

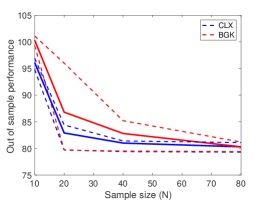

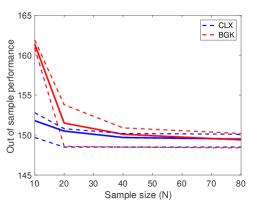

We consider a classic single-item newsvendor problem in which we assume the demand of an item follows a continuous distribution with a bounded support set with and a bounded density function. An order of units must be placed before demand occurs. After the demand occurs, each unit of unmet demand incurs a shortage cost denoted by and each unit of surplus inventory incurs a holding cost denoted by . Hence, the cost function is defined as , which represents the cost of mismatch between supply and demand. In a classical newsvendor problem, the goal is to determine the order size to minimize the expected cost. When the demand’s distribution is unknown, a corresponding DRO approach can be considered. Assuming a set of historical demand data is available, we construct an ambiguity set in the form of (7), or more specifically, in (19) and solve the DRO (8). We compare the optimal order obtained with the one found by the DRO model in [2] where the ambiguity set is built using Kolmogorov-Smirnov test.

In our numerical experiments, we choose and and consider three different ground true distributions for the demand:

-

1.

A truncated normal distribution created by truncating a normal distribution with mean and standard deviation on .

-

2.

A beta distribution rescaled onto with parameters and .

-

3.

A truncated exponential distribution created by truncating an exponential distribution with mean on .

For each distribution, we consider eight different sample sizes, i.e., . For each size, we randomly generate a dataset by i.i.d. sampling from the demand distribution. Using , we apply our approach and the method by [2] to construct the ambiguity sets and then solve the corresponding DRO problems to obtain an order size from each approach. To evaluate the out-of-sample performance of , we sample another i.i.d. dataset with from the true distribution and calculate the sample average approximation of the expected cost, i.e., with from each approach. We repeat this procedure 100 times to show the mean and variation of the out-of-sample performance.

When constructing the ambiguity set in our method, we need to provide a significance level and a group size (see Algorithm 1). Although a theoretical value of is suggested in Proposition 2, it involves quantities which are hard to estimate (e.g. and ). When we construct , we set and select from based on the holdout validation method. The value significance level is chosen from based on the same validation method. In particular, we randomly partition into and with and . Given a combination of and , we first construct using and , and then we solve using Algorithm 3. Then, we select the combination of and with the largest . For each of the 100 independent trial, we repeat this process to select and . Note that the entire procedure is simulating how a decision maker select in practice when only is available. For a fair comparison, we also apply the same validation scheme to choose the significance level used in the method by [2].

We denote our approach by CLX and the method in [2] by BGK. Figure 3 illustrates the performances of CLX and BGK for each of the three distributions of demand. For each sample size , we plot the percentile, the mean, and percentile of the out-of-sample performances in the 100 trials. The blue lines show the results from CLX, while the red lines show the results from BGK. Figure 3 indicates that CLX has a better out-of-sample performances than BGK when the sample size is small. As the sample size increases, the performances of both approaches become similar as the ambiguity sets in both approaches converge to the true deman distribution.

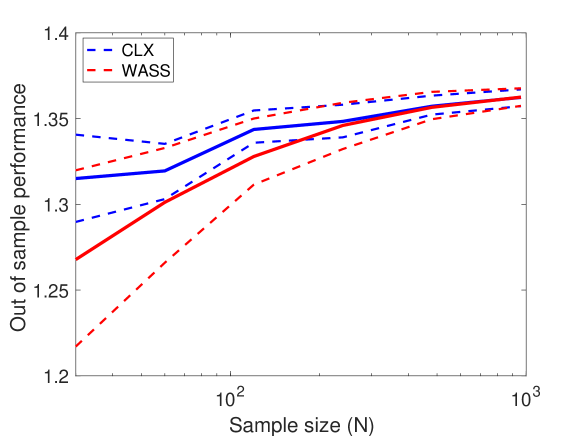

5.2 Portofolio management

In this example, we consider the classical portfolio selection problem consisting of assets in which the investor must divide the total budget to fractions with and , and invest of the budget in the security. We assume that the security has a random future return . The return from each unit of budget is thus . We assume that the investor is risk-averse and measures the investment risk by the conditional value at risk (CVaR) of the return ; see [37]. Suppose the joint distribution of the return has a density function . The CVaR at level of the return of a portfolio with respect to a probability distribution is defined as

which represents the average of the worst portfolio losses (negative return) under distribution . When is known, we consider the case where the investor wants to minimize a weighted sum of the mean and the CVaR of the portfolio loss , which is formulated as the following stochastic optimization:

where indicates the investor’s risk-aversion level, , and

If the joint distribution of is unknown but a collection of historical data return is collected, the investor can construct a data-driven ambiguity set of and solve the DRO problem corresponding to the stochastic optimization problem above. We construct the ambiguity set in (31) and solve the DRO (8) to construct an portfolio. Then, we compare our solution with the one obtained by the DRO model in [13] where the ambiguity set is constructed using Wasserstein metric.

Following the numerical experiments by [13], we consider assets with decomposable returns for where is a systematic risk factor shared by all assets and is an unsystematic risk factor associated with specific assets. By the construction, assets with higher indices promise higher mean returns at a higher risk. We set and in our all experiments. We consider different sample sizes, i.e., . For each size, we randomly generate a dataset by i.i.d. sampling returns from the aforementioned distribution of . Using , we apply our approach and the method by [13] to construct the ambiguity sets and then solve the DRO to obtain an portfolio from each approach. To evaluate the out-of-sample performance of , we sample another i.i.d. dataset with from the true distribution and calculate the sample average approximation of the expected cost, i.e., with from each approach. We repeat this procedure 100 times to show the mean and variation of the out-of-sample performance.

When constructing , we choose wiht being the boxcar kernel, namely, if and otherwise. Here, is a normalization constant that ensures . Similar to , the construction of in our method requires some quantities which are hard to estimate (e.g. and ). Therefore, we construct using and in the form (28) with the parameters and selected by the holdout validation method rather than their theoretical values in (29) and Proposition 3. In particular, we set (see Proposition 3) and then select from and from . We randomly partition into and with and . Given a combination of and , we first construct using and , and then solve using Algorithm 3. Then, we select the combination of and with the largest . For each of the 100 independent trial, we repeat this process to select and . For a fair comparison, we also apply the same validation scheme to choose the radius of the Wasserstein ball used to construct the ambiguity set in [13].

We denote our approach by CLX and the method in [13] by WASS and plot the numerical results in Figure 4.

In particular, for each of the datasets in each sample-size scenario, we evaluate the solutions from both CLX and Wasserstein by testing their out-of-sample performances over the large dataset. We then plot the percentile, the mean, and of the out-of-sample performances of both approaches over the sample-size scenarios. In figure 4, the blue lines show the results from CLX, while the red lines show the results from Wasserstein. Figure 4 indicates that both approaches converge to the true expectation with the increase in sample size.

6 Conclusions

In this paper, we proposed data-driven approaches to construct ambiguity sets that consist of continuous probability density functions. The ambiguity sets enjoy both finite and asymptotic convergences. The resulting distributionally robust optimization problem has infinite many variables and constraints. We then proposed a stochastic gradient decent method to solve the optimization problems. Numerical experiments in newsvendor problem and portfolio selection problem verify the effectiveness of our approach.

Appendix

Proof of Theorem 2

For , we define a subset of as We first analyze the approximation error between , and at a given point . We assume first and the proof for is similar. For simplicity of notations, we use and to represent and in this proof.

There exists an index such that . Since and is -Holder continuous, for a sufficiently large sample size , we will further have (as is close enough to ) and . Note that is monotonically decreasing over . By the definitions of and as in (25) and the constraints in (24), we must have and , which implies

| (40) |

Using the monotonicity of , we can show that

| (41) | |||||

| (42) |

Applying (41) and (42) to (40), we obtain

| (43) | |||||

According to equation (98) and (101) with () in [19], we have

| (44) |

and

| (45) |

for any and any (not necessarily ). Recall that so that . We apply (44) and (45) to (43) to achieve

| (46) |

Let represent the Lebesgue measure on . We then choose to be small enough such that . Consider a fixed , we have

which, according to (46), implies

Similarly, we can also show that

Therefore, for any and , there exists an such tha,t for any ,

Then, we have proof the first conclusion. The second conclusion can be easily implied from the first conclusion.

Proof of Theorem 4

Acknowledgements

The authors would like to thank Aditya Guntuboyina for referring us to the papers about confidence band constructions.

References

- [1] Aharon Ben-Tal, Dick Den Hertog, Anja De Waegenaere, Bertrand Melenberg, and Gijs Rennen. Robust solutions of optimization problems affected by uncertain probabilities. Management Science, 59(2):341–357, 2013.

- [2] Dimitris Bertsimas, Vishal Gupta, and Nathan Kallus. Robust sample average approximation. Mathematical Programming, pages 1–66, 2014.

- [3] Dimitris Bertsimas, Vishal Gupta, and Nathan Kallus. Data-driven robust optimization. Mathematical Programming, 167(2):235–292, 2018.

- [4] Dimitris Bertsimas and Ioana Popescu. Optimal inequalities in probability theory: A convex optimization approach. SIAM Journal on Optimization, 15(3):780–804, 2005.

- [5] John R Birge and Francois Louveaux. Introduction to stochastic programming. Springer Science & Business Media, 2011.

- [6] Giuseppe Carlo Calafiore and Laurent El Ghaoui. On distributionally robust chance-constrained linear programs. Journal of Optimization Theory and Applications, 130(1):1–22, 2006.

- [7] Zhi Chen, Melvyn Sim, and Huan Xu. Distributionally robust optimization with infinitely constrained ambiguity sets. Working Paper, 2016.

- [8] Etienne de Klerk, Daniel Kuhn, and Krzysztof Postek. Distributionally robust optimization with polynomial densities: theory, models and algorithms. arXiv preprint arXiv:1805.03588, 2018.

- [9] Erick Delage and Yinyu Ye. Distributionally robust optimization under moment uncertainty with application to data-driven problems. Operations research, 58(3):595–612, 2010.

- [10] John Duchi, Peter Glynn, and Hongseok Namkoong. Statistics of robust optimization: a generalized empirical likelihood approach. arXiv preprint arXiv:1610.03425, 2016.

- [11] Jitka Dupačová. The minimax approach to stochastic programming and an illustrative application. Stochastics: An International Journal of Probability and Stochastic Processes, 20(1):73–88, 1987.

- [12] E Erdoğan and Garud Iyengar. Ambiguous chance constrained problems and robust optimization. Mathematical Programming, 107(1-2):37–61, 2006.

- [13] Peyman Mohajerin Esfahani and Daniel Kuhn. Data-driven distributionally robust optimization using the wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming, 171(1-2):115–166, 2018.

- [14] Rui Gao, Xi Chen, and Anton J. Kleywegt. Wasserstein distributional robustness and regularization in statistical learning. ArXiv preprint arXiv:1712.06050, 2017.

- [15] Rui Gao and Anton J Kleywegt. Distributionally robust stochastic optimization with wasserstein distance. arXiv preprint arXiv:1604.02199, 2016.

- [16] Laurent El Ghaoui, Maksim Oks, and Francois Oustry. Worst-case value-at-risk and robust portfolio optimization: A conic programming approach. Operations research, 51(4):543–556, 2003.

- [17] Grani A. Hanasusanto, Daniel Kuhn, Stein W. Wallace, and Steve Zymler. Distributionally robust multi-item newsvendor problems with multimodal demand distributions. Mathematical Programming, 152(1):1–32, 2015.

- [18] J. A. Hartigan and P. M. Hartigan. The dip test of unimodality. The Annals of Statistics, 13(1):70–84, 1985.

- [19] Nicolas W. Hengartner and Philip B. Stark. Finite-sample confidence envelopes for shape-restricted densities. The Annals of Statistics, 23(2):525–550, 1995.

- [20] Zhaolin Hu and L Jeff Hong. Kullback-leibler divergence constrained distributionally robust optimization. Available at Optimization Online, 2013.

- [21] Heinrich Jiang. Uniform convergence rates for kernel density estimation. In International Conference on Machine Learning, pages 1694–1703, 2017.

- [22] Ruiwei Jiang and Yongpei Guan. Data-driven chance constrained stochastic program. Mathematical Programming, pages 1–37, 2015.

- [23] R. Z. Khas’minskii. A lower bound on the risks of non-parametric estimates of densities in the uniform metric. Theory of Probability and Its Applications, 23(4):794–798, 1976.

- [24] Diego Klabjan, David Simchi-Levi, and Miao Song. Robust stochastic lot-sizing by means of histograms. Production and Operations Management, 22(3):691–710, 2013.

- [25] Henry Lam and Clementine Mottet. Tail analysis without parametric models: A worst-case perspective. Operations Research, 65(6):1696–1711, 2017.

- [26] Henry Lam and Enlu Zhou. Recovering best statistical guarantees via the empirical divergence-based distributionally robust optimization. Operations Research, page To appear., 2018.

- [27] Bowen Li, Ruiwei Jiang, , and Johanna L. Mathieu. Ambiguous risk constraints with moment and unimodality information. Mathematical Programming, page To appear., 2018.

- [28] Johan Lofberg. Yalmip: A toolbox for modeling and optimization in matlab. In Computer Aided Control Systems Design, 2004 IEEE International Symposium on, pages 284–289. IEEE, 2004.

- [29] Wai-Kei Mak, David P Morton, and R Kevin Wood. Monte carlo bounding techniques for determining solution quality in stochastic programs. Operations research letters, 24(1-2):47–56, 1999.

- [30] Martin Mevissen, Emanuele Ragnoli, and Jia Yuan Yu. Data-driven distributionally robust polynomial optimization. In Advances in Neural Information Processing Systems, pages 37–45, 2013.

- [31] Karthik Natarajan and Chung Piaw Teo. On reduced semidefinite programs for second order moment bounds with applications. Mathematical Programming, 161(1):487–518, 2017.

- [32] Arkadi Nemirovski, Anatoli Juditsky, Guanghui Lan, and Alexander Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM Journal on optimization, 19(4):1574–1609, 2009.

- [33] Emanuel Parzen. On estimation of a probability density function and mode. The annals of mathematical statistics, 33(3):1065–1076, 1962.

- [34] Georg Pflug and David Wozabal. Ambiguity in portfolio selection. Quantitative Finance, 7(4):435–442, 2007.

- [35] Pengyu Qian, Zizhuo Wang, and Zaiwen Wen. A composite risk measure framework for decision making under uncertainty. Journal of the Operations Research Society of China, pages 1–26, 2018.

- [36] Alessandro Rinaldo, Larry Wasserman, et al. Generalized density clustering. The Annals of Statistics, 38(5):2678–2722, 2010.

- [37] R Tyrrell Rockafellar and Stanislav Uryasev. Optimization of conditional value-at-risk. Journal of risk, 2:21–42, 2000.

- [38] Murray Rosenblatt. Remarks on some nonparametric estimates of a density function. The Annals of Mathematical Statistics, pages 832–837, 1956.

- [39] Herbert Scarf, KJ Arrow, and S Karlin. A min-max solution of an inventory problem. Studies in the mathematical theory of inventory and production, 10:201–209, 1958.

- [40] Alexander Shapiro. On duality theory of conic linear problems. In Semi-infinite programming, pages 135–165. Springer, 2001.

- [41] Alexander Shapiro, Darinka Dentcheva, and Andrzej Ruszczynski. Lectures on stochastic programming: modeling and theory, volume 16. SIAM, 2014.

- [42] Alexandre B Tsybakov. Introduction to nonparametric estimation. revised and extended from the 2004 french original. translated by vladimir zaiats, 2009.

- [43] Lieven Vandenberghe, Stephen Boyd, and Katherine Comanor. Generalized chebyshev bounds via semidefinite programming. SIAM review, 49(1):52–64, 2007.

- [44] Zizhuo Wang, Peter W Glynn, and Yinyu Ye. Likelihood robust optimization for data-driven problems. Computational Management Science, 13(2):241–261, 2016.

- [45] Wolfram Wiesemann, Daniel Kuhn, and Melvyn Sim. Distributionally robust convex optimization. Operations Research, 62(6):1358–1376, 2014.

- [46] Steve Zymler, Daniel Kuhn, and Berç Rustem. Distributionally robust joint chance constraints with second-order moment information. Mathematical Programming, 137(1-2):167–198, 2013.

- [47] Steve Zymler, Daniel Kuhn, and Berç Rustem. Worst-case value at risk of nonlinear portfolios. Management Science, 59(1):172–188, 2013.