Fuzzy Profit Shifting: A Model for Optimal Tax-induced Transfer Pricing with Fuzzy Arm’s Length Parameter

Abstract

This paper proposes a model of optimal tax-induced transfer pricing with a fuzzy arm’s length parameter. Fuzzy numbers provide a suitable structure for modelling the ambiguity that is intrinsic to the arm’s length parameter. For the usual conditions regarding the anti-shifting mechanisms, the optimal transfer price becomes a maximising -cut of the fuzzy arm’s length parameter. Nonetheless, we show that it is profitable for firms to choose any maximising transfer price if the probability of tax audit is sufficiently low, even if the chosen price is considered a completely non-arm’s length price by tax authorities. In this case, we derive the necessary and sufficient conditions to prevent this extreme shifting strategy.

Keywords: fuzzy profit shifting, transfer pricing, tax evasion, tax enforcement, tax penalty.

JEL Classification: F23, H26, K34

1 Introduction

Tax literature frequently draws attention to the ambiguity between a tolerant tax avoidance behaviour vs. tax evasion. This ambiguity is especially relevant on the analysis of profit shifting strategies, where multinational enterprises – MNE carry intra-firm transactions between related parties from different jurisdictions, so to adjust the transfer prices in order to reallocate taxable profits from high-tax to low-tax locations111Existing studies provide relevant evidences of profit shifting by means of direct transfer pricing adjustments Davies \BOthers. (\APACyear2018); Cristea \BBA Nguyen (\APACyear2016); Bernard \BOthers. (\APACyear2006); Overesch (\APACyear2006); Bartelsman \BBA Beetsma (\APACyear2003); Clausing (\APACyear2003); Swenson (\APACyear2001).. Anti-shifting rules require that the transfer prices comply with the so called arm’s length principle OECD (\APACyear2017), which states that intra-firm prices must be consistent with ones that would have been established with independent unrelated parties. If the arm’s length condition is not satisfied, tax authorities require the payment of taxes over the shifted profits, and a tax penalty usually applies.

The arm’s length condition is a fuzzy concept, since independent prices are influenced by legitimate differences in transactions’ conditions Becker \BOthers. (\APACyear2017); Eden (\APACyear2001); OECD (\APACyear2017). It means that transfer prices are not attained to a unique true arm’s length price, but rather to a range of observable parameter prices with different degrees of appropriateness with respect to the arm’s length condition. In the case of a tax audit, the tax authority has to assess if the transfer prices applied by the MNE satisfy the arm’s length condition, or if the deviations from the core of the arm’s length range represent evidences of profit shifting. This is no more than an ambiguous decision to be taken by the tax authority, thus it implies in additional uncertainties for the MNE.

This paper derives a model for optimal tax-induced transfer pricing subjected to a fuzzy arm’s length parameter. We apply fuzzy numbers, which were first proposed by Zadeh \BOthers. (\APACyear1965) and developed further by several researchers Zimmermann (\APACyear1991); Klir \BBA Yuan (\APACyear1995); Verdegay (\APACyear1982), thus to model the impact of the uncertainty that is intrinsic to the arm’s length parameter over the profit-maximisation strategy. Our model follows the concealment costs approach that is traditional in profit shifting literature Allingham \BBA Sandmo (\APACyear1972); Kant (\APACyear1988); Hines Jr \BBA Rice (\APACyear1994), however we design it in a generalised tax condition, which allows for the maximisation analysis without constraints on the shifting direction. The model takes the arm’s length parameter as a fuzzy number, therefore the maximisation object is also a fuzzy object.

Baseline analysis shows that the solution of the fuzzy maximisation object under usual conditions is a -cut of the fuzzy arm’s length parameter, and any adjustments on the transfer price up to the optimal level provide a profit-shifting gain for the MNE. Nonetheless, we show that the MNE may completely disregard the arm’s length parameter if the probability of tax audits is sufficiently low. It means that it is profitable to choose any maximising transfer price if the MNE has low chances of being audited, even if the maximising transfer price is considered a completely non-arm’s length price. In this sense, we derive the necessary and sufficient conditions to prevent this extreme shifting case.

The remaining of this paper is structured as follows. Section 2 presents the basic notions of fuzzy sets and fuzzy numbers. Section 3 derives the general model. Section 4 solves the fuzzy maximisation object, presents the sensitivity analyses, and derives the impact of a general tax enforcement effect regarding the country-level anti-shifting variables. Section 5 draws some concluding comments.

2 Basics on Fuzzy Sets

Fuzzy sets were first introduced by seminal paper of Zadeh \BOthers. (\APACyear1965) and generalise the classical notion of crisp sets. Fuzzy sets are a collection of elements in a universe where the boundary of the set is not clearly defined. The ambiguity associated with the bounds of the fuzzy set in a universe is represented by a membership function defined as , , for measures the grade of membership of element in . If the grade of membership is 0, then the element does not belong to . If the grade of membership is 1, then the element completely belongs to . If the grade of membership is within the interval [0,1], then the element only partially belongs to . The fuzzy set is therefore characterised by the pair . Two fuzzy sets and are considered equal iff .

Let be a fuzzy set and define a continuous interval . The ordinary crisp set associated with any is called -cut of the fuzzy set and is defined as . We can use -cuts to represent intervals on fuzzy sets as

The sets , refer to a decreasing succession of subsets continua; , , Klir \BBA Yuan (\APACyear1995).

Theorem.

(Representation Theorem - Klir \BBA Yuan (\APACyear1995); Zimmermann (\APACyear1991); Verdegay (\APACyear1982)222Klir \BBA Yuan (\APACyear1995) analyse this theorem in a set of three Decomposition Theorems for representation of fuzzy sets by means of their -cuts.) For a fuzzy set and its -cuts , , we have

If the membership function is defined as the characteristic function of the set

the membership function of the fuzzy set can be expressed as the characteristic function of its -cuts as

A fuzzy set is convex iff its -cuts are convex. Equivalently, is convex iff , , . A fuzzy set is normalised iff .

A fuzzy number is a special case of a fuzzy set on the real line that is both convex and normalized. Its membership function is piecewise continuous and is called its mode. Since fuzzy sets are completely defined by their corresponding membership functions, we refer to a fuzzy number as the set as well as the membership function hereinafter. For a sequence of real numbers , the fuzzy number satisfies the following:

-

a.

for each ;

-

b.

is non-decreasing in and non-increasing in ;

-

c.

for each ;

where is the mode of the fuzzy number, is the interval on the lower side of the mode with width , and is the interval on the upper side of the mode with width . A fuzzy number is of the -type if it can be parametrised by shape functions and on the lower and upper sides of the mode respectively333Literature commonly refer to the left and right sides of the mode , i.e. though the origin of the term -type with shape functions and .. A plane fuzzy number satisfies , , i.e. its mode is a non-empty interval with more than one element Klir \BBA Yuan (\APACyear1995); Zimmermann (\APACyear1991). A fuzzy number is called a trapezoidal fuzzy number iff it takes the form

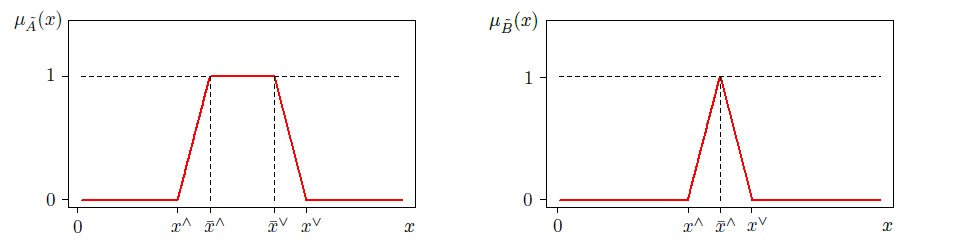

A fuzzy number is called a triangular fuzzy number iff it takes the form

Figure 1 shows examples of trapezoidal and triangular fuzzy numbers. It is clear that a trapezoidal fuzzy number is an instance of plane fuzzy number, and a triangular fuzzy number refers to a trapezoidal fuzzy number with .

3 The Model

In this section, we derive a model to analyse the optimal tax-induced transfer pricing. We first set the baseline net profit function for the MNE, then we derive the specification of the fuzzy profit shifting optimisation.

3.1 Baseline Profit Design

Consider a vertically integrated MNE with two divisions, the parent company located in Country 1 and a wholly owned subsidiary located in Country 2, . Both divisions444For simplification, we apply subscript for the reference of both countries and to each MNE’s divisions hereinafter. produce outputs under costs , bringing revenues based on domestic sales . Parent firm also exports a portion of its output to subsidiary in Country 2, regarding a single type of product, charging a transfer price established by means of exclusive self-discretion of MNE’s central management. We set and , thus intra-firm output depends on the market demand for final product in Country 2. The pre-tax profits of both divisions are

Country 1 applies the source principle on taxation of foreign profits, and we assume no incremental operational cost on transferring internal output to division 2, i.e. . For an income tax rate in each country, MNE’s global net profits are . Profit shifting incentives arise when tax rates between divisions are different, , and total net profit increases when MNE is able to choose a specific transfer price so profits are transferred from the high-tax country to the low-tax country. The condition implies the following two cases:

| (1) |

In the LTP case, the MNE has incentives to shift profits from division 1 to division 2 by choosing a low transfer price , thus harming tax revenues in Country 1. In the HTP case, MNE chooses a high price so to shift profits to the opposite direction, thus harming Country 2.

3.2 Fuzzifying the Arm’s Lenght Price

Assume that both countries impose a non-negligible and non-deductible tax penalty if profit shifting is detected, which is computed as a portion of the amount of evaded taxes. It means that the tax penalty is imposed if the harmed Country observes that the transfer price is different from a parameter price established under arm’s length conditions555The transfer pricing guidelines prepared by OECD (\APACyear2017) have become the main criterion adopted by most countries worldwide for evaluation of intra-firm prices. The guidelines are built on the basis of the arm’s length principle as the fundamentals for tax-compliant transfer pricing. and this price gap results in the outflow of taxable profits from Country . The parameter of an arm’s length price is a fuzzy concept, since independent prices vary according to legitimate differences in transactions’ conditions. Therefore, countries rather observe a fuzzy set of parameter prices , all of which have different degrees of appropriateness with respect to the arm’s length principle666In this line, anti-shifting rules usually establish an arm’s length range of appropriate transfer prices. The arm’s length range is usually set as an interquartile range within the complete set of comparable prices OECD (\APACyear2017)..

Define the fuzzy set of arm’s length prices , , , where is the universe of all observable independent prices, universe is convex, and is the membership function of the fuzzy set . For a sequence of independent prices , the fuzzy set satisfies the usual conditions

| (2) |

| (3) |

| (4) |

The mode of the fuzzy set satisfies , which provides the interval of prices that completely satisfy the arm’s length principle, for . Hence, the choice of any strict parameter price must lie within the interval of prices that define the mode of the fuzzy set , i.e. . Eq. 2 defines the limiting interval out of which any price is considered a completely non-arm’s length price.

Under these conditions, the fuzzy set becomes a fuzzy number of the -type. Call the fuzzy arm’s length price. We define a standard membership function of the fuzzy number as follows:

| (5) |

with both functions and monotone continuous. In Eq. 5, we allow for the fuzzy arm’s length price to be asymmetric. This asymmetry may be due to a difference in the widths and on the lower and upper sides of the fuzzy number respectively, as well as for differences in grades of membership denoted by functions and . In effect, the asymmetry in the fuzzy arm’s length price is useful to describe how Countries 1 and 2 differ in their tolerance for a transfer price farther from the parameter price .

For the LTP case in Eq. 1, Country 1 is less tolerant with respect to a low transfer price close to , while it accepts prices near or higher than the parameter price . Therefore, Country 1 is only concerned with the lower side of the fuzzy arm’s length price . The opposite occurs for the HTP case in Eq. 1, since Country 2 is only concerned with the higher side of . If we divide the fuzzy arm’s length price into two membership sections with respect to lower side and upper side , we obtain two fuzzy numbers and satisfying the additional conditions:

| (6) |

| (7) |

| (8) |

It is clear that the fuzzy numbers and refer to the fuzzy arm’s length prices taken into account by Countries 1 and 2 respectively777It is also clear that the fuzzy numbers and are of the -type and -type respectively.. We indicate the standard form of the fuzzy arm’s length prices satisfying conditions in Eq. 6-8 as , . The mode of the fuzzy numbers satisfies the standard condition . The bound of the mode of the fuzzy numbers is defined in standard form888The bound of the mode of the fuzzy number can be defined as with deviation . as . Hence, both profit shifting cases in Eq. 1 imply LTP , HTP .

3.3 Tax Audits and Tax Penalties

Both countries perform tax audits in order to prevent the profit shifting. In the universe of all taxpayers, we assume that countries are not able to continuously observe all MNE in absolute completeness, but they have to ex ante select which MNE are going to be audited. In special, both countries have no prior knowledge about the existence of intra-firm transactions , though this knowledge depends on an initial pick. Following Levaggi \BBA Menoncin (\APACyear2013), we set the audit selection in Country as a Poisson process with intensity rate homogeneous through the total period determined in the legal statute of limitations. Rate refers to the tax audit intensity in Country . If the MNE is selected, Country will observe , thus triggering a chance for tax penalty .

If the number of tax audits performed by Country is , the probability of exact tax audits is . Furthermore, the cumulative probability of Country to perform up to audits, is computed as

| (9) |

where is the gamma function and is the upper gamma function999Derivation of Eq. 9 in Appendix.. Remark that no penalisation will be imposed if there is no tax audit, . Moreover, even with an estimate of the number of tax audits , the MNE can be selected under any number different from . In summary, MNE has a chance of being selected for tax audit if Country performs at least one audit. Therefore, the total probability of tax audit for the MNE is

| (10) |

In the case of audit selection, Country observes the intra-firm transactions and compares the transfer price with the arm’s length parameter . If the harmed Country concludes that the MNE is shifting taxable profits away, the MNE is required to pay the amount of evaded taxes plus a penalty levied over this amount. In this case, tax penalty is computed as , where is the sign function and tax rates are non-negative, . Observe that the total tax penalty is non-negative for both LTP and HTP cases101010Total tax penalty is non-negative since the signs of both the tax differential and the price gap carry information about the shifting direction; HTP implies , , while LTP implies , ..

Nonetheless, the assessment of the transfer price by Country is based on the fuzzy arm’s length parameter , . Formally, this assessment is made by taking the fuzzy number and setting the equality . The result is a fuzzy price gap , where is the bound of the mode of the fuzzy number . The fuzzy price gap is defined such as to satisfy the condition . For the harmed Country , profit shifting may exist iff , i.e. iff the fuzzy price gap pushes the transfer price away from the mode of , . In this case, the original tax penalty turns into a fuzzy tax penalty in the following standard form:

| (11) |

It means that the harmed Country has the task to assess if the price gap is a tolerable variance under the fuzzy arm’s length conditions or if it is an evidence of profit shifting.

4 Optimal Transfer Pricing

The MNE aims choose a transfer price so to maximise global net profits , however it faces the chance of tax penalisation if the harmed Country finds out the existence of intra-firm transactions and decides that it represents a profit shifting strategy. In this line, assuming that the optimal transfer price implies , the MNE has a maximisation object specified as follows:

| (12) |

Since the expected tax penalty is a fuzzy number, objective function in Eq. 12 becomes a fuzzy objective, and profit maximisation must take into account the fuzziness of the price gap .

Conditions in Eq. 6-8 show that the standard-form fuzzy arm’s length price represents a one-to-one and onto correspondence with respect to the closed interval of interest . Therefore, we solve Eq. 12 by applying the procedure for fuzzy optimisation developed in the classical work of Verdegay (\APACyear1982).

For the membership function , , the corresponding -cuts are . From the representation theorem for fuzzy sets, Eq. 12 is expressed in the following parametric form:

| (13) |

with , where , is the inverse function of the membership function . Simply stated, if the solution of Eq. 13 is , then the solution of Eq. 12 is the fuzzy set . Hence, profit maximisation in Eq. 12 resumes to find the optimal -cut defined by at the membership grade .

Based on the general Stone-Weierstrass approximation, assume that the standard-form shape function in Eq. 5 can be defined as a simple power function

| (14) |

with as a regularised parameter for the tolerance of Country regarding fuzziness in the arm’s length price, e.g. a slacken tax assessment by Country implies , while a tighten tax assessment implies . Eq. 14 provides a smooth variation in membership grade as transfer price gets farther from the bound of the mode . For the interval of interest , parametric optimisation in Eq. 13 then becomes

| (15) |

Now we have the expected net profits specified completely in terms of the transfer price111111Parametric form in Eq. 15 is possible since the arm’s length parameters are exogenous with respect to and . . Differentiating Eq. 15 with respect to and solving, we obtain the solution

| (16) |

with as the absolute value function121212The following property is applied: for any real number , satisfies . Eq. 16 shows that the optimal transfer price is represented as a maximising -cut of the fuzzy arm’s length price defined as , i.e. the optimal price gap is a share of the price difference . This -cut is represented by a share function over the interval , which is measured as the magnitude of the profit shifting incentive adjusted by the marginal expected penalisation effect . The slope of this share is the same as of the shape function in Eq. 14 by means of the exponent . It also has an adjustment equal to , which derives from the endogenous specification of the fuzzy arm’s length price in terms of within the expected tax penalty in Eq. 15131313More specifically, the transfer price affects both the transfer price gap and the membership relation specified by the shape function in Eq. 14, for the combined marginal effect on becomes . On the other hand, the transfer price affects marginally the net profits in a direct way. The total effect on the expected net profits is equal to . Moreover, the amount of intra-firm output does not affect the optimal transfer price in the model, i.e. it refers to the application of the pure comparable uncontrolled price – CUP method141414Literature indicates that profit shifting detection is more effective if tax audits focus on the amount of intra-firm transfers rather than on transfer prices only Nielsen \BOthers. (\APACyear2014). Nonetheless, anti-shifting rules require the application of the arm’s length principle solely for the establishment of transfer prices , i.e. there are no current requirements for an ”arm’s length quantity” – say ””, and tax authorities bear no arguments against any intra-firm output as long as the transfer price is equal to the arm’s length price, . Eq. 16 reflects this condition. OECD (\APACyear2017). Sufficient joint conditions for non-zero optimal are , and .

Recall that the two profit shifting cases in Eq. 1 imply LTP , HTP . Total gains from profit shifting are obtained by substituting the optimal transfer price on the expected net profits and comparing it with the net profits under the arm’s length condition . We find

| (17) |

which is always positive for both LTP and HTP cases.

Proposition 1.

Satisfying sufficient joint conditions for non-zero price gap, , and , tax-induced variations in transfer prices always increase the expected net profits up to the optimal price gap

Proof.

Expected net profits with respect to the optimal transfer price and to the bound of the mode of the arm’s length condition are equal to

The difference is equal to

which is positive for both LTP and HTP cases derived in Eq. 1 as we have

∎

We state a relevant condition for the audit intensity derived from Eq. 16:

Proposition 2.

The optimal transfer price is a -cut of the fuzzy arm’s length price only if the audit intensity satisfies the condition

Proof.

For the optimal transfer price to be an optimal -cut equal to , specification in Eq. 16 requires the condition

which implies . With respect to the domain of all variables within Eq. 16, we observe that the only case where the condition is violated is when the audit intensity is sufficiently small, such that

for some value . The necessary condition implies

If this condition is not satisfied, the optimal transfer price as specified in Eq. 16 outbounds the interval of interest, , thus the solution of Eq. 16 is no more a -cut of the fuzzy arm’s length price . ∎

Proposition 2 shows that the optimal transfer price as specified in Eq. 16 outbounds the interval of interest, if the audit intensity is sufficiently weak. In this special case, the MNE can further increase the gains from profit shifting by disregarding the bounds of the fuzzy arm’s length price when determining the transfer price . It therefore implies:

Corollary 1.

If the audit intensity does not satisfy the condition in Proposition 2, maximisation object in Eq. 12 has no general solution in terms of an optimal transfer price .

Proof.

Assume that the solution of Eq. 16 provides the inequality , so the condition in Proposition 2 is violated. Therefore, Eq. 5-8 imply that the optimal transfer price has a membership grade equal to zero, , so is considered a completely non-arm’s length price. In this case, it is clear that the initial maximisation object in Eq. 12 takes the form of a crisp linear function of in the first place, with no constraints, which is equal to

with first derivative equal to

and second derivative equal to zero. The critical point at provides the same conditions as in Eq. 1, for we have

Therefore, any changes in the transfer price towards the profit shifting direction increases the expected net profits with no upper bound, for both LTP ans HTP cases. ∎

Corollary 1 simply shows that the MNE has full incentives to shift profits away from the high tax Country if the tax authority is lax. For a sufficiently weak audit intensity , the expected tax penalty becomes extremely low and linear with respect to the transfer price – see Proposition 2. In this case, it becomes profitable for the MNE to choose any tax-induced transfer price , even if is considered a completely non-arm’s length price.

4.1 Sensitivity Analyses

Initially state the following:

Corollary 2.

Under the optimality conditions regarding the price gap , increase in intra-firm outputs always increases the total amount of profit shifting.

Proof.

Marginal changes in intra-firm output intensify the profit shifting amount, however intra-firm transfers depends on the product demand in Country 2, . Assume that the demand in division 2 is not changed, but the MNE has flexibility to vary the application of internal output to provide revenues in division 2. Hence, the MNE can run a second optimisation stage to choose the optimal intra-firm output . Differentiating the second-stage objective with respect to intra-firm output , subjected to the constraint , we obtain

| (18) |

with conditions , , , where is the Lagrangian multiplier function. If the constraint is not binding, , we have . In Eq. 18, the exogenous effect of the intra-firm transaction follows the direction of the profit shifting incentive – LTP implies and HTP implies , , . However, the effect of the optimal price gap is always positive, , – see the Corollary 2 . Equality of net marginal costs occurs only in the extreme LTP case where the effect of the optimal price gap completely neutralises the exogenous arm’s length effect, i.e. iff . Hence, at the optimal intra-firm output , the generalised condition is attained in most of cases.

In special, Eq. 18 indicates that different tax rates disturb the effect of the -elasticity of substitution between costs and over the expected net profits . The effect is equal to , , where is the -elasticity of substitution151515Formally, the effect of the -elasticity is equal to where is the -elasticity between the arm’s length parameter and , and is the -elasticity between and . Eq. 16 implies both , , therefore we have , . between and .

With respect to the profit shifting incentive , , it is clear that the optimal transfer price is affected by changes in tax rate . Differentiating Eq. 16 with respect to , we obtain the following standard-form equations161616Derivation of Eq. 19-20 in Appendix.:

| (19) |

| (20) |

First, Eq. 19 shows that the variation follows the profit shifting direction.

Proposition 3.

Variation in the optimal transfer price with respect to marginal changes in the tax rate of the harmed Country follows the direction of the profit shifting incentive , such that . Variation is equal zero iff .

As it is intuitively conjectured, Proposition 3 shows that marginal increments in the tax rate of the harmed Country widens the optimal price gap thus to shift more profits away from Country , since it represents an increase in the profit shifting incentive. Reductions in tax rate cause the reverse effect. On the other hand, for marginal changes in tax rate , of the non-harmed Country , variation takes the opposite direction, e.g. a marginal increase in shrinks the optimal price gap and reduces the gains from profit shifting171717For changes in , , we have the condition . For the limiting case where the tax rate of the non-harmed Country is zero, , changes in the tax rate do not affect the optimal price gap . The general condition for Eq. 19 to be linear occurs at the arm’s length tolerance parameter equal to

with , where is the Lambert product log function181818Lambert product log function is defined as the following: for an exponential function , the inverse function is such as it satisfies the condition , where is called the Lambert product log function. It is applied for a general power function , as ..

Furthermore, Eq. 20 describes the slope of changes in the optimal transfer price as the tax rate changes. Under the scope of both LTP and HTP cases, Eq. 20 shows that the slope of the variation is opposite to the profit shifting direction; the slope of is strictly increasing for the LTP case and strictly decreasing for the HTP case.

Proposition 4.

The slope of the variation is opposite to the profit shifting direction, such that .

Proof.

First, the multiplier at the right hand side of Eq. 20 equal to

is defined as the second-order -semi-elasticity of the optimal transfer price , thus Eq. 20 is equal to Eq. 19 multiplied by . We notice that , , is always negative for both LTP and HTP cases. Proposition 3 shows that , therefore it implies

If , , the tax differential tends to zero, , so Eq. 20 diverges for any as follows:

where , which implies

The slope of is equal to zero only in the special case where , , i.e. it does not fit either LTP or HTP cases. Therefore, both LTP and HTP cases strictly satisfy the condition . ∎

Eq. 20 shows that the variation is elastic if the tax differential is narrow, since it implies that the initial shifting incentive is weak and the maximising price gap is rather small – see Eq. 16. In this case, small marginal changes in produce large marginal impacts on the optimal transfer price . On the other hand, a large profit shifting incentive implies that the initial price gap is already wide, and further marginal changes in the tax rate produce a weaker impact. Variation becomes inelastic as the tax rate approaches the boundary , .

Corollary 3.

Unitary -elasticity of the optimal price gap occurs at the equality

such that the arm’s length tolerance parameter scales the impact of the difference within Eq. 19.

Proof.

In overall, Eq. 19-20 show that the variation converges if the general conditions , are satisfied. The general convergence at individually increasing tax rates , are obtained as follows:

We also have . Nonetheless, in the limiting case of the tightest tax assessment , we obtain a special convergence for equal to

from which we obtain

Otherwise, variation diverges as follows:

With respect to the other country-level variables related with the audit intensity , tax penalty and the arm’s length tolerance parameter , specification of the optimal price gap in Eq. 16 shows an elaborate effect. Variation of the optimal price gap with respect to each individual country-level variable is equal to:

| (21) |

| (22) |

| (23) |

First regarding Eq. 21-22, both clearly present a negative effect on the optimal price gap for the complete interval of interest , which is consistent with the intuitive premise, e.g. a marginal increase in the audit intensity or in the penalty rate increases the expected tax penalty , thus it shortens the optimal price gap ; a decrease in or produces the opposite effect.

For the Eq. 23, on the other hand, the effect is not necessarily negative on the full interval , for all . In the general case, the variation represents a non-positive effect over the optimal transfer price iff it satisfies the inequality

otherwise, the effect follows the profit shifting direction. This positive effect is counter-intuitive at first, for we expect that changes in the arm’s length tolerance parameter to produce only effects that are opposite to the shifting incentive. Nonetheless, notice that the specification of the fuzzy arm’s length price in terms of produces a marginal adjustment effect on the gains from profit shifting equal to – see Eq. 16. It means that the effect of marginal changes in the tolerance parameter must be negative and must outburst the marginal effect of , in order to produce a negative effect on . This last outcome191919More specifically, marginal changes in the tolerance parameter produce a positive effect on iff Eq. 16 implies the inequality . In this case, the optimal transfer price is increasing at , although it implies beforehand that is not a -cut of the fuzzy arm’s length price – see Corollary 1. is specially due to the specification of in terms of within Eq. 15.

4.2 Modelling a General Tax Enforcement Effect

While Eq. 21-23 show how marginal changes in individual anti-shifting variables affect the optimal transfer price , the influence of a general enforcing behaviour from the harmed Country may be reflected simultaneously in more than one variable. In special, it is safe to assume that the audit intensity and the arm’s length tolerance parameter are both related with some common measure of tax enforcement applied by Country .

Let be a regularised tax enforcement measure for the Country , such that the arm’s length tolerance parameter is a monotone order-preserving function , for a weak tax enforcement implies , while strong tax enforcement implies . Moreover, assume that the tax audit intensity varies with respect to tax enforcement , thus the audit intensity becomes a non-homogeneous Poisson rate function with respect to the tax enforcement, . Assume that is continuous. Hence, if the number of tax audits performed by Country is and the tax enforcement level implies , , then the probability of exact audits is

with the non-homogeneous Poisson intensity parameter equal to

| (24) |

Eq. 24 derives from the non-homogeneous Poisson condition

which says that the incremental probability of one additional tax audit by Country is approximate to a linear relation between the rate function at and the variation in tax enforcement . The total probability of tax audit for the MNE derives directly from Eq. 10 and Eq. 24 and is equal to

Specification of the audit rate function is not a straight task. In general, existing studies suggest that higher tax enforcement implies in more frequent audits, although the increments on the number of tax audits vary through the enforcement range Alm (\APACyear2012), so we assume that the audit rate is clearly non-decreasing as the tax enforcement increases.

To simplify the analysis, define a general function , is monotone continuous for , and it satisfies , . Under adequate conditions202020Derivation of the conditions for Eq. 25 in Appendix. regarding the audit rate function and the tax enforcement , we argue that the the audit probability can be parametrised with respect to the variable as

| (25) |

so we are able to define the optimal transfer price in Eq. 16 in terms of the tax enforcement variable , equal to

From now on, simplify the notation of both general functions as and . On the bounded domain , both functions , have the same limiting values on the boundaries, and , which are equal to

by definition, regardless of their slopes. Since functions , are continuous on the complete domain, , we observe that any monotonic map implies . Therefore, it implies the following:

Proposition 5.

For the optimal transfer price parametrised with respect to the tax enforcement variable , the maximising prices at the boundaries of the domain, and are equal to

Proof.

For any marginal change in the tax enforcement , variation in depends on the effect of both , , which is equal to . For the upper bound , we clearly have

For the lower bound , we derive the following:

Since we also have the condition with respect to the other country-level variables, we finally conclude that . ∎

Proposition 5 confirms that the maximising transfer prices at the boundaries of the tax enforcement domain, and are both -cuts of the fuzzy arm’s length price . Nonetheless, for marginal changes within the domain interval , the effect over the optimal transfer price depends on how functions , vary. Differentiating with respect to , we obtain the following standard-form equations:

| (26) |

For Eq. 26, we observe again that the variation is not necessarily negative for all – compare it with Eq. 23. A negative variation such that requires the following necessary condition for the functions , :

Proposition 6.

Variation in the optimal transfer price with respect to marginal changes in the tax enforcement is opposite to the profit shifting incentive , such that , iff the functions , satisfy the condition

Proof.

For simplification, assume initially the equalities , . For the Eq. 26 to have a negative effect, such that , it requires the necessary condition

for the complete domain . Rearranging, we obtain the inequality

At the critical point , we clearly have

Now, for any small perturbation on function such that we have , the necessary condition is equal to

The inequality is satisfied for any non-negative value . On the other hand, if the perturbation is negative such that , we arrive at a contradiction – the right hand side of the inequality becomes the larger term. Hence, it implies

At last, this necessary condition is clearly maintained if we drop the simplifications , ; for both LTP and HTP cases, , , , we have the inequality

which also implies . ∎

Proposition 5 shows that the optimal transfer price at the lowest enforcement level, is equal to the least tolerable arm’s length price , e.g. for the lowest tax enforcement, the MNE may choose the transfer price equal to , which is the farthest from the mode . Moreover, Proposition 6 presents the necessary condition for the variation to produce an effect opposite to the profit shifting incentive, through the complete domain . Hence, it implies the following:

Corollary 4.

From Corollary 4, it means that the inequality is also a necessary condition for the optimal transfer price to be a -cut of the fuzzy arm’s length price . Otherwise, we may have a tax enforcement level such that .

Now, we derive a sufficient condition for the optimal transfer price to be a -cut of the fuzzy arm’s length price for the complete domain .

Proposition 7.

If the functions , satisfy the condition for the complete domain , the optimal transfer price is a -cut of the fuzzy arm’s length price .

Proof.

Corollary 4 derives the necessary condition for the optimal transfer price to be a -cut of the fuzzy arm’s length price with respect to the complete domain . First, we are sure that the necessary condition attains the equality at the lower bound of the domain, , for we have

But we also have that , so all terms converge to zero at the very initial point :

However, as the tax enforcement increases, , this equality is not maintained, since it implies . Besides, as the tax enforcement reaches the upper bound of the domain, , we have , thus it implies . Combining these two cases, we derive two possible inequalities:

It shows that if we have , we still need to confirm that the necessary condition is satisfied. On the other hand, if we have , the necessary condition in Corollary 4 is automatically satisfied. Therefore, the condition is a sufficient condition for the optimal transfer price is a -cut of the fuzzy arm’s length price .

∎

Remark that functions , refer to the arm’s length tolerance parameter and the probability of tax audit respectively. Proposition 7 thus indicates that the optimal transfer price is certainly a -cut of the fuzzy arm’s length price if the audit probability is greater than the arm’s length tolerance parameter, for the complete domain . Otherwise, we still need to confirm that the necessary condition is satisfied.

5 Discussion and Conclusion

This paper presents a model for optimal tax-induced transfer pricing under fuzzy arm’s length parameter. The fuzzy arm’s length price follows the structure of a fuzzy number Zadeh \BOthers. (\APACyear1965) by means of a concave shape function with smooth membership grading, which varies with respect to the arm’s length tolerance parameter of tax authorities. Under usual conditions, the optimal transfer price becomes a maximising -cut of the fuzzy arm’s length price, while it still satisfies the conventional assumptions of convex concealment costs and increasing profit-shifting incentives at an increasing tax differentials.

At first, we show that the MNE always obtains a gain from profit shifting up to the optimal transfer price, regardless of the shifting direction, and this gain is obtained at any levels of tax penalty, audit probability and arm’s length tolerance. Gains from profit shifting are intensified by adjusting the intra-firm outputs at a second maximisation stage. Moreover, the MNE may obtain exceeding gains by extrapolating the fuzzy arm’s length parameter if the probability of tax audits is sufficiently low. This extreme case is prevented specially by increasing the audit intensity or intensifying the other anti-shifting mechanisms on the harmed country.

These analyses offer some interesting insights on how the ambiguity of the arm’s length parameter may affect the profit shifting strategy of firms. First and foremost, the fuzziness of the arm’s length parameter can be used by firms to achieve their profit shifting goals, since this fuzziness is the condition that implies the gains from profit shifting. For any questioning by the tax authority, the transfer price may be more or less sustained based on arguments about the conditions of the comparable transactions. Moreover, even if the tax authority observes all intra-firm transactions in a full-audit mode, the ambiguity of what can considered an appropriate transfer price is not eliminated. It means that the uncertainty is not attributed only to the probability of being audited, but also on the tolerance level of the tax auditor. And this uncertainty can be beneficial for firms focusing on a profit shifting strategy. At last, anti-shifting rules impose the arm’s length criterion for the transfer prices, but no requirements are currently imposed for the level of internal outputs. In this sense, any change in the arm’s length tolerance of tax authorities might be offset by adjustments in internal outputs if the MNE has some operational flexibility, so the final amount of shifted profits remains the same.

Appendix

Derivation of Eq. 9

For a variable as any point within a continuum of occurrences at a constant average rate , the time of the -th occurrence is a random variable that follows a gamma distribution and has a cumulative probability as . The gamma function is defined as

and the upper gamma function is defined as

Since we have discrete events as , the upper gamma function can be expressed as the series expansion

The second multiplier at the right hand side of the above equation represents the cumulative chance of events to occur at intensity up to moment , where is a Poisson random variable212121The relation indicates that changes in occurrence rate produce an inverse impact on the distribution; a random gamma-distributed variable has mean and variance .. In addition, the gamma function satisfy the property for discrete variables , which implies the equality . Hence, assuming the occurrence rate is obtained for a period up to , thus , these conditions allow us to derive the cumulative probability distribution of events as

which is presented in Equation 9. Poisson cumulative distribution function expressed by means of gamma function is defined for all positive real numbers and provides continuity condition for the analysis.

Derivation of Eq. 19-20

For all real numbers , is equal to , with as the absolute value function and as the sign function satisfying

For , we have , which implies . Differentiating with respect to for both LTP and HTP cases provides

Under these properties, differentiating Eq. 16 with respect to provides the following standard form:

For , simplify the constant multiplier at the right hand side of Eq. 19. Standard form in Eq. 20 is derived as follows:

From the -semi-elasticity of the optimal price gap equal to , the second-order -semi-elasticity of is defined as

which is the multiplier at the right hand side of Eq. 20.

Derivation of Eq. 25

The homogeneous audit intensity can be any positive real number, thus the range of the corresponding non-homogeneous audit rate function is unbounded above. Since we have a bounded domain , therefore the rate function must indeed be unbounded above222222Of course, the condition for the function to be unbounded above necessarily arises from our restriction of the domain of to the bounded interval ., i.e. under the definition of non-uniformly continuous functions, it implies

From the general function as defined in Section 4.2, let the audit rate function follow a negative semi-elasticity design232323For a differentiable function , , is bounded, the negative semi-elasticity equal to is unbounded above at the zeros . Two classical examples are the functions and , which are unbounded above on the bounded domains and respectively. Both examples are defined as the negative semi-elasticities of the functions and as follows: , such that is unbounded above at the zeros, . Hence, it implies the following differential form:

Integrating on the full domain , we obtain a parametric representation of the audit intensity in terms of equal to

which satisfies the unboundedness condition. Therefore, the total probability of tax audit becomes .

Derivation of Eq. 26

To simplify the analysis, we adopt in this section the prime notation for the first and second derivatives as follows: for the differentiable function , the first and second derivatives regarding the variable are respectively equal to , .

Differentiating the optimal transfer price with respect to the variable as parametrisation in Section 4.2, we obtain the following standard form:

References

- Allingham \BBA Sandmo (\APACyear1972) \APACinsertmetastarsandmo1972{APACrefauthors}Allingham, M\BPBIG.\BCBT \BBA Sandmo, A. \APACrefYearMonthDay1972. \BBOQ\APACrefatitleIncome tax evasion: A theoretical analysis Income tax evasion: A theoretical analysis.\BBCQ \APACjournalVolNumPages13-4323–338. \PrintBackRefs\CurrentBib

- Alm (\APACyear2012) \APACinsertmetastaralm2012{APACrefauthors}Alm, J. \APACrefYearMonthDay2012. \BBOQ\APACrefatitleMeasuring, explaining, and controlling tax evasion: lessons from theory, experiments, and field studies Measuring, explaining, and controlling tax evasion: lessons from theory, experiments, and field studies.\BBCQ \APACjournalVolNumPagesInternational Tax and Public Finance19154–77. \PrintBackRefs\CurrentBib

- Bartelsman \BBA Beetsma (\APACyear2003) \APACinsertmetastarbartelsman2003{APACrefauthors}Bartelsman, E\BPBIJ.\BCBT \BBA Beetsma, R\BPBIM. \APACrefYearMonthDay2003. \BBOQ\APACrefatitleWhy pay more? Corporate tax avoidance through transfer pricing in OECD countries Why pay more? corporate tax avoidance through transfer pricing in oecd countries.\BBCQ \APACjournalVolNumPagesJournal of Public Economics879-102225–2252. \PrintBackRefs\CurrentBib

- Becker \BOthers. (\APACyear2017) \APACinsertmetastarbecker2017{APACrefauthors}Becker, J., Davies, R\BPBIB.\BCBL \BBA Jakobs, G. \APACrefYearMonthDay2017. \BBOQ\APACrefatitleThe economics of advance pricing agreements The economics of advance pricing agreements.\BBCQ \APACjournalVolNumPagesJournal of Economic Behavior & Organization134255–268. \PrintBackRefs\CurrentBib

- Bernard \BOthers. (\APACyear2006) \APACinsertmetastarbernard2006{APACrefauthors}Bernard, A\BPBIB., Jensen, J\BPBIB.\BCBL \BBA Schott, P\BPBIK. \APACrefYearMonthDay2006. \APACrefbtitleTransfer pricing by US-based multinational firms Transfer pricing by us-based multinational firms \APACbVolEdTR\BTR. \APACaddressInstitutionNational Bureau of Economic Research (No. w12493). \PrintBackRefs\CurrentBib

- Clausing (\APACyear2003) \APACinsertmetastarclausing2003{APACrefauthors}Clausing, K\BPBIA. \APACrefYearMonthDay2003. \BBOQ\APACrefatitleTax-motivated transfer pricing and US intrafirm trade prices Tax-motivated transfer pricing and us intrafirm trade prices.\BBCQ \APACjournalVolNumPagesJournal of Public Economics879-102207–2223. \PrintBackRefs\CurrentBib

- Cristea \BBA Nguyen (\APACyear2016) \APACinsertmetastarcristea2016{APACrefauthors}Cristea, A\BPBID.\BCBT \BBA Nguyen, D\BPBIX. \APACrefYearMonthDay2016. \BBOQ\APACrefatitleTransfer pricing by multinational firms: New evidence from foreign firm ownerships Transfer pricing by multinational firms: New evidence from foreign firm ownerships.\BBCQ \APACjournalVolNumPagesAmerican Economic Journal: Economic Policy83170–202. \PrintBackRefs\CurrentBib

- Davies \BOthers. (\APACyear2018) \APACinsertmetastardavies2018{APACrefauthors}Davies, R\BPBIB., Martin, J., Parenti, M.\BCBL \BBA Toubal, F. \APACrefYearMonthDay2018. \BBOQ\APACrefatitleKnocking on tax haven’s door: Multinational firms and transfer pricing Knocking on tax haven’s door: Multinational firms and transfer pricing.\BBCQ \APACjournalVolNumPagesReview of Economics and Statistics1001120–134. \PrintBackRefs\CurrentBib

- Eden (\APACyear2001) \APACinsertmetastareden2001{APACrefauthors}Eden, L. \APACrefYearMonthDay2001. \BBOQ\APACrefatitleTaxes, transfer pricing, and the multinational enterprise Taxes, transfer pricing, and the multinational enterprise.\BBCQ \APACjournalVolNumPagesThe Oxford Handbook in International Business, Oxford University Press: Oxford591–619. \PrintBackRefs\CurrentBib

- Hines Jr \BBA Rice (\APACyear1994) \APACinsertmetastarhines1994{APACrefauthors}Hines Jr, J\BPBIR.\BCBT \BBA Rice, E\BPBIM. \APACrefYearMonthDay1994. \BBOQ\APACrefatitleFiscal paradise: Foreign tax havens and American business Fiscal paradise: Foreign tax havens and american business.\BBCQ \APACjournalVolNumPagesThe Quarterly Journal of Economics1091149–182. \PrintBackRefs\CurrentBib

- Kant (\APACyear1988) \APACinsertmetastarkant1988{APACrefauthors}Kant, C. \APACrefYearMonthDay1988. \BBOQ\APACrefatitleEndogenous transfer pricing and the effects of uncertain regulation Endogenous transfer pricing and the effects of uncertain regulation.\BBCQ \APACjournalVolNumPagesJournal of International Economics241-2147–157. \PrintBackRefs\CurrentBib

- Klir \BBA Yuan (\APACyear1995) \APACinsertmetastarklir1995{APACrefauthors}Klir, G.\BCBT \BBA Yuan, B. \APACrefYear1995. \APACrefbtitleFuzzy sets and fuzzy logic Fuzzy sets and fuzzy logic (\BVOL 4). \APACaddressPublisherPrentice hall New Jersey. \PrintBackRefs\CurrentBib

- Levaggi \BBA Menoncin (\APACyear2013) \APACinsertmetastarlevaggi2013{APACrefauthors}Levaggi, R.\BCBT \BBA Menoncin, F. \APACrefYearMonthDay2013. \BBOQ\APACrefatitleOptimal dynamic tax evasion Optimal dynamic tax evasion.\BBCQ \APACjournalVolNumPagesJournal of Economic Dynamics and Control37112157–2167. \PrintBackRefs\CurrentBib

- Nielsen \BOthers. (\APACyear2014) \APACinsertmetastarnielsen2014{APACrefauthors}Nielsen, S., Schindler, D.\BCBL \BBA Schjelderup, G. \APACrefYearMonthDay2014. \APACrefbtitleAbusive transfer pricing and economic activity Abusive transfer pricing and economic activity \APACbVolEdTR\BTR. \APACaddressInstitutionCESifo Working Paper No. 4975. \PrintBackRefs\CurrentBib

- OECD (\APACyear2017) \APACinsertmetastaroecd2017{APACrefauthors}OECD. \APACrefYear2017. \APACrefbtitleOECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations 2017 Oecd transfer pricing guidelines for multinational enterprises and tax administrations 2017. {APACrefURL} \urlhttps://www.oecd-ilibrary.org/content/publication/tpg-2017-en {APACrefDOI} \doihttps://doi.org/https://doi.org/10.1787/tpg-2017-en \PrintBackRefs\CurrentBib

- Overesch (\APACyear2006) \APACinsertmetastaroveresch2006{APACrefauthors}Overesch, M. \APACrefYearMonthDay2006. \APACrefbtitleTransfer pricing of intrafirm sales as a profit shifting channel-Evidence from German firm data Transfer pricing of intrafirm sales as a profit shifting channel-evidence from german firm data \APACbVolEdTR\BTR. \APACaddressInstitutionZEW Discussion Papers No. 06-84. \PrintBackRefs\CurrentBib

- Swenson (\APACyear2001) \APACinsertmetastarswenson2001{APACrefauthors}Swenson, D\BPBIL. \APACrefYearMonthDay2001. \BBOQ\APACrefatitleTax reforms and evidence of transfer pricing Tax reforms and evidence of transfer pricing.\BBCQ \APACjournalVolNumPagesNational Tax Journal7–25. \PrintBackRefs\CurrentBib

- Verdegay (\APACyear1982) \APACinsertmetastarverdegay1982{APACrefauthors}Verdegay, J\BPBIL. \APACrefYearMonthDay1982. \BBOQ\APACrefatitleFuzzy mathematical programming Fuzzy mathematical programming.\BBCQ \APACjournalVolNumPagesFuzzy information and decision processes231237. \PrintBackRefs\CurrentBib

- Zadeh \BOthers. (\APACyear1965) \APACinsertmetastarzadeh1965{APACrefauthors}Zadeh, L\BPBIA.\BCBT \BOthersPeriod. \APACrefYearMonthDay1965. \BBOQ\APACrefatitleFuzzy sets Fuzzy sets.\BBCQ \APACjournalVolNumPagesInformation and control83338–353. \PrintBackRefs\CurrentBib

- Zimmermann (\APACyear1991) \APACinsertmetastarzimmermann1991{APACrefauthors}Zimmermann, H\BHBIJ. \APACrefYear1991. \APACrefbtitleFuzzy Set Theory – and Its Applications Fuzzy set theory – and its applications. \APACaddressPublisherKluwer Academic Publishers, 2nd, revised edition. \PrintBackRefs\CurrentBib