High-performance stock index trading: making effective use of a deep long short-term memory network

Abstract

We present a deep long short-term memory (LSTM)-based neural network for predicting asset prices, together with a successful trading strategy for generating profits based on the model’s predictions. Our work is motivated by the fact that the effectiveness of any prediction model is inherently coupled to the trading strategy it is used with, and vise versa. This highlights the difficulty in developing models and strategies which are jointly optimal, but also points to avenues of investigation which are broader than prevailing approaches. Our LSTM model is structurally simple and generates predictions based on price observations over a modest number of past trading days. The model’s architecture is tuned to promote profitability, as opposed to accuracy, under a strategy that does not trade simply based on whether the price is predicted to rise or fall, but rather takes advantage of the distribution of predicted returns, and the fact that a prediction’s position within that distribution carries useful information about the expected profitability of a trade. The proposed model and trading strategy were tested on the SP , Dow Jones Industrial Average (DJIA), NASDAQ and Russel stock indices, and achieved cumulative returns of , , and , respectively, over -, far outperforming the benchmark buy-and-hold strategy as well as other recent efforts.

keywords:

Finance , LSTM , Deep Learning , Stock Prediction , Automatic trading1 Introduction

Equity prediction lies at the core of the investment management profession and has also attracted significant attention from academia. One of the open questions has been whether (and how) one can forecast the behavior of stocks and then act accordingly to generate “excess returns”, i.e., profit in excess of those generated by the market itself (Fama and French, 1993). Towards that end, significant effort has been put into predicting the price of major U.S. stock indices such as the S&P 500 or the Dow Jones Industrial Average (DJIA) (Huck, 2009, 2010; Sethi et al., 2014; Krauss et al., 2017; Bao et al., 2017) as well as that of individual stocks, using techniques ranging from early linear models (Fama and French, 2004) to machine learning and neural network-based approaches (Sermpinis et al., 2013; Deng et al., 2017; Minh et al., 2018). There are two components which are generally part of the overall discussion on “intelligent” or automatic trading: a predictive model whose purpose is to anticipate an asset’s future price, and a trading strategy which uses the model’s predictions to generate profit. Developing a scheme with consistently superior performance is difficult, in part because of the “joint” nature of the goal: profits ultimately depend both on the prediction model as well as the trading strategy it is being used with, and changing either of the two affects the final outcome. Thus, in principle, these two components should be designed and optimized together, a challenge which currently appears to be out of reach, due to the seemingly endless variety of possible models and trading strategies. Instead, most of the relevant research (to be reviewed shortly) has focused on schemes that do quite well by improving on specific aspects of the overall prediction/trading process.

One approach has been to aim for a prediction model which is “as good as possible” at guessing the “next” price of an asset, and then use that guess to inform trading decisions (Bao et al., 2017; Baek and Kim, 2018; Zhou et al., 2019). This is frequently done by means of a so-called directional \sayup-down trading strategy which buys the asset when the predicted price is higher than the current price and sells if it is lower. While this approach can be effective, it is based on an implicit assumption that better short-term price predictions lead to higher profitability. This is not true in general: prediction accuracy is typically measured with a symmetric loss function (e.g., mean absolute error) which is indifferent to the sign of the prediction error, and yet that sign may be quite important when trading. In fact, it is possible for one model to lead to trades which are always profitable while another, having better predictive accuracy, to record only losses222Consider for example the four-day price series , and two possible predictions of its last three samples, and , both generated on the first day, when the price was 101. has a mean absolute error of 5 when measured against the last three samples of , while ’s error is 3. However, is always correct on the direction of the price movement of , i.e., its predictions are always higher (resp.lower) than the previous price of when the price will indeed rise (resp. fall) in the next sample, while is always wrong.. An alternative is to forgo predictions of the asset price itself and instead consider a directional model which predicts, with as high an accuracy as possible, whether the price will rise or fall compared to its current level, essentially acting as a binary classifier (Fischer and Krauss, 2018; Zhong and Enke, 2017; Chiang et al., 2016). Then, the trading strategy is again to simply buy or sell the asset based on the model’s “recommendation”. This approach is “self-consistent” from the point of view that the model’s predictions are judged against in the same setting as the trading strategy, i.e., being correct on the direction of price movement.

While one can of course consider many possible variations on trading strategies and accompanying models, there are two key points to be recognized. First, prediction models should be viewed and evaluated in the context of the trading strategies they are used with (Leitch and Tanner, 1991). Thus, prediction accuracy should not monopolize our focus: large(r) prediction errors do not necessarily preclude a model from being profitable under the “right” trading strategy, just like low errors do not by themselves guarantee profitability. Second, because the joint model/strategy optimum appears to be elusive, one may try to improve overall profitability by adapting the trading strategy to to make “fuller” use of the information contained within the model’s predictions; that information may generally be much more than whether the price will rise or fall in the next time step.

This paper’s contribution is to build on the ideas outlined in the previous paragraph by proposing a novel model-strategy pair which together are effective in generating profits with reasonable trading risk, and compare favorably to standard benchmarks as well as recent works. Our model consists of a deep long short-term memory (LSTM)-based neural network which is to predict an asset’s price based on a rolling window of past price data. Structurally, the network will be simple so that it can be trained and updated fast, making it suitable for intra-day trading, if desired. A key feature will be that the network’s output layer will have access to the entire evolution of the network’s hidden states as the input layer is “exposed” to a sequence of past prices. This will allow us to achieve a predictive accuracy similar to that of more complex models, while keeping our architecture “small” in terms of structure and data required. Our LSTM network will initially be trained to achieve low price prediction errors, as opposed to high profitability which is our ultimate goal. We will bring profitability into the fold in two ways: a) the network’s hyper-parameters will be selected to maximize profit (instead of accuracy, as is typically done in the literature (Zhong and Enke, 2017; Zhou et al., 2019)) in conjunction with b) a novel event-based333We will use the term “event” in the sense of probability theory (e.g., a sample of a random variable falling within a specified interval on the real line), as opposed to finance where it commonly refers to “external” events (corporate filings, legal actions, etc.). trading strategy which seeks to take advantage of the information available not in any single price prediction, but in the entire distribution of predicted returns. In broad terms, our strategy will not act simply on whether the predicted price is higher or lower compared to its current value, but will instead make decisions based on the expected profitability of a possible trade, conditioned on the prediction’s relative position within the aforementioned distribution. As we will see, such a strategy can be optimized in some ways and will lead to significant gains.

We will test our proposed approach on major U.S. stock indices, namely the S&P 500 (including dividends), the Dow Jones Industrial Average (DJIA), the NASDAQ and the Russel 2000 (R), over an almost 8-year long period (October 2010 - May 2018). These indices attract significant attention from market practitioners, both in terms of strategy benchmarking and for monitoring market performance. They will also serve as a common ground for comparison with other studies. When it comes to discussing the performance of our approach, we will provide the “standard” annualized and cumulative profits attained, but also additional metrics that relate to trading risk, which are very much of interest when assessing any investment but are often missing from similar studies. Moreover, our relatively long testing period will allow us to draw safer conclusions as to our scheme’s profitability over time.

The remainder of the paper is organized as follows. Section 2 discusses relevant literature, including details on profitability and overall performance. In Section 3 we present our proposed prediction model and trading strategy, as well as a class of capital allocation policies which are optimal for our trading strategy. Section 4 discusses model training and allocation policy selection. The profitability and overall performance of our model and strategy, as well as comparisons with recent works and “naive” benchmark approaches of interest, are discussed in Section 5.

2 Literature Review

We can identify two significant clusters in the literature which are most relevant to this work. One contains studies in which prediction and profitability evaluation are “disconnected” in the sense discussed in the previous Section: a model is trained to predict the value of an asset, but that prediction is then used with a \saydirectional trading strategy. Studies that fall within this category include Bao et al. (2017) who described a three-step process (de-noising of the stock price series, stacked auto-encoders, and a recurrent neural network using LSTM cells) achieving strong results, including a sum of daily returns whose yearly average was approximately and for the SP and DJIA, respectively, over the period -. Baek and Kim (2018) explored the role of limited data when training neural networks and the resulting deterioration in prediction accuracy, and introduced a modular architecture consisting of two LSTM networks. Using a trading day window and the SP as their underlying asset the authors reported low prediction errors (e.g., a 12.058 mean absolute error) and a cumulative return444Cumulative return (CR) is the product of the sequence of gross returns over a given time period, minus unity, i.e., for a stock or other asset whose value is over trading days ., beating the benchmark buy-and-hold555A standard benchmark for gauging the performance of a trading strategy over a given time period, is the so-called buy-and-hold (BnH) portfolio which is formed simply by buying the asset on the first day of the period under consideration, and selling it on the last day. strategy () over the period from to (we will conventionally use the U.S. format, for reporting dates throughout).

Several studies have applied feed-forward or convolutional neural networks (CNN) to financial time-series. A recent example is Zhou et al. (2019), which introduced the notion of empirical mode decomposition and a factorization machine-based neural network to predict the future stock price trend. For the SP, using a one-year test period (the year ), the authors reported , , and for the mean absolute, root mean squared and mean percentage errors, respectively. Combining their predictions with a long-short666 A Long-Short trading strategy is one in which in addition to buying, one is also allowed to sell short (borrowd) assets. trading strategy on the same index, they reported an average annualized return777Annualized return (AR) is the per-year geometric average of returns over a given time period, minus unity, i.e., , for an asset whose value is over trading days , where 252 is the nominal number of trading days in a calendar year. of and a Sharpe ratio888The Sharpe ratio (SR) is a measure of reward-to-risk performance, defined as the difference between AR and the federal funds rate (which is considered to be the \sayrisk-free rate, essentially at zero following the financial crisis of ), divided by the annualized volatility (AV) of the returns. AV is the standard deviation of returns over a given time period, multiplied by the square root of the number of trading days in a year (conventionally ). of . Another interesting CNN-based approach is that of Sezer and Ozbayoglu (2018) in which price time-series are transformed into -D images which are then fed into a trading model to produce a “buy”, “sell” or “hold” recommendation. Trading on well-known exchange-traded funds (ETFs) as well as the constituents of the DJIA, that approach could yield an annualized return of for the ETF portfolio and for the DJIA constituents portfolio, over -. Finally, Krauss et al. (2017) is an example of using a portfolio of stocks to outperform an index, as opposed to trading the index itself. That work tested several machine learning models, including deep neural networks, gradient-boosted trees and random forests in order to perform statistical arbitrage on the S&P using daily predictions from to . Before transaction costs, the authors reported mean daily excess returns of for their ensemble model during -, however returns were negative during that period’s last five years (-).

A second important cluster of works contains studies in which the loss function used to train the prediction model is “consistent” with the trading strategy, e.g., the model predicts the direction of the price movement - but not the numerical value of the price - which is then used with a directional trading strategy. Sethi et al. (2014) presented a neural network which used only two features to predict the direction (up or down) of next-day price movement for the largest stocks (in terms of market capitalization) in the S&P index. Those stocks were then combined into a portfolio in order to \saybeat the index itself. Using data from - and assuming a cost of per transaction, that approach achieved a annualized return. Recently, Fischer and Krauss (2018) also studied the daily direction of the SP constituents between , comparing various machine learning techniques. Their approach was to use a single feature, namely the standardized one day return over the past trading year, in order to predict the direction of the constituent stocks, and ultimately the probability for each stock to out-/under-perform the cross-sectional median. The authors reported mean daily returns of and a Sharpe Ratio of , which indicates low risk / high reward prior to transaction costs. However, the returns were not consistent throughout the testing period, and were close to zero during its last 5 years. Chiang et al. (2016) proposed a neural network for forecasting stock price movement, using a binary output to indicate buy/hold or sell trading suggestions. The authors applied a denoising process to the input time-series before feeding it to the neural network. Their model, applied to a variety of ETFs over a 1-year period -, achieved a strong cumulative return of in the case of SPY999SPY is an Exchange Traded Fund (ETF) which tracks the S&P500 index., before transaction costs, and even higher returns when short-selling was allowed. That approach also provides a good example of how very few trades ( in one year) can yield good performance when trading individual assets.

The work in (Zhong and Enke, 2017) also studied the daily direction of the SP index using input features and various dimensionality reduction techniques. The study period covered -. The best model in that study reached a accuracy, however the accuracy of a “naive” or other baseline strategy over the same period was not reported. Using a trading strategy which either bought the SP or invested in a one-month T-bill resulted in a mean daily return of with a standard deviation of over their test period of days ending on . Finally, an interesting attempt at event-driven stock market prediction using CNNs is Ding et al. (2015). The model proposed therein also produces a binary output, (i.e., the stock price is predicted to increase or decrease). Using a directional trading strategy over a test period from -, that approach was applied to 15 stocks in the SP, with a reported mean cumulative return of .

It is important to note that several of the works cited here report average returns (Bao et al., 2017; Zhong and Enke, 2017) but no annualized or cumulative returns. Unfortunately, the arithmetic average of returns is not informative as to actual capital growth / profitability, because it cannot be used to infer annual or cumulative return101010For example, if we invest 1 euro in an asset which achieves consecutive returns of -99%, 100%, and 100%, our investment would be worth just 4 cents, i.e., a cumulative return of -96%, while the average return would be approximately 33%.. Also, as one might expect, it is difficult to declare a single “winner” among the different approaches: not all authors report the same profitability metrics, and the evaluation periods vary; even when comparing against the same asset and testing period, one cannot safely draw conclusions if the testing period is rather short (e.g., a single year, as in Chiang et al. (2016); Zhou et al. (2019); Zhong and Enke (2017); Ding et al. (2015)). Finally, there is also a significant number of works on the use of machine learning methods and neural networks in particular, where the goal is exclusively accurate price prediction, with no discussion of further use of that prediction, be it for trading or any other purpose. Representative papers include Rather et al. (2015); Chong et al. (2017); Gu et al. (2018). The volume of research in this category is substantial but we will not delve deeper here because prediction accuracy by itself is not the focus of this work.

3 Proposed model and trading strategy

We proceed to describe a LSTM neural network which will be used to predict stock or index prices, followed by a trading strategy that attempts to take advantage of the model’s predictions - despite their inaccuracies - in a way which will be made precise shortly.

3.1 Network Architecture

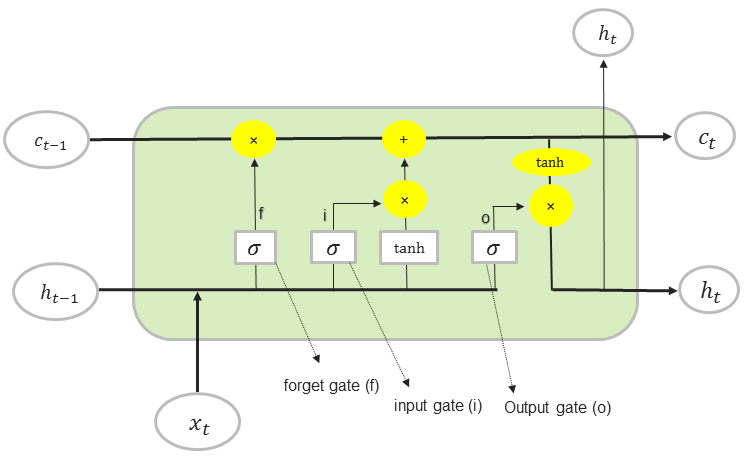

Our proposed network follows the popular LSTM architecture (Hochreiter and Schmidhuber, 1997), commonly used in recurrent neural network applications (Russakovsky et al., 2015; Silver et al., 2017; Wu et al., 2016; Foster et al., 2018). The basic LSTM cell, shown in Fig. 1,

receives at each time a batch of length- input vectors, (where is batch size and is the number of input features), and utilizes a number of multiplicative gates in order to control information flow through the network. In addition to the usual hidden state, , of size , where is the number of hidden units, the LSTM cell includes an “internal” or “memory” state, , also of size in our case. The three gates, input (), output () and forget (), which have feed-forward and recurrent connections, receive the input , and previous hidden state , to produce

| (1) | ||||

| (2) | ||||

| (3) |

where is the sigmoid function111111 applied element-wise, the bias terms are of size , and and are weight matrices with dimensions and , respectively. From the input, output and forget terms, ( - all of size ), the next instances of the hidden and memory states are computed as:

| (4) | ||||

| (5) | ||||

| (6) |

where denotes element-wise multiplication. The input gate controls which elements of the internal state we are going to update, while the forget gate determines which elements of the internal state () will be “eliminated”. In the case of deep networks with multiple LSTM layers, the hidden states generated by each layer are used as inputs to the next layer described by another instance of Eqs. (1)-(6), where the input terms in Eqs. (1)-(4) are replaced with the corresponding hidden states of the previous layer.

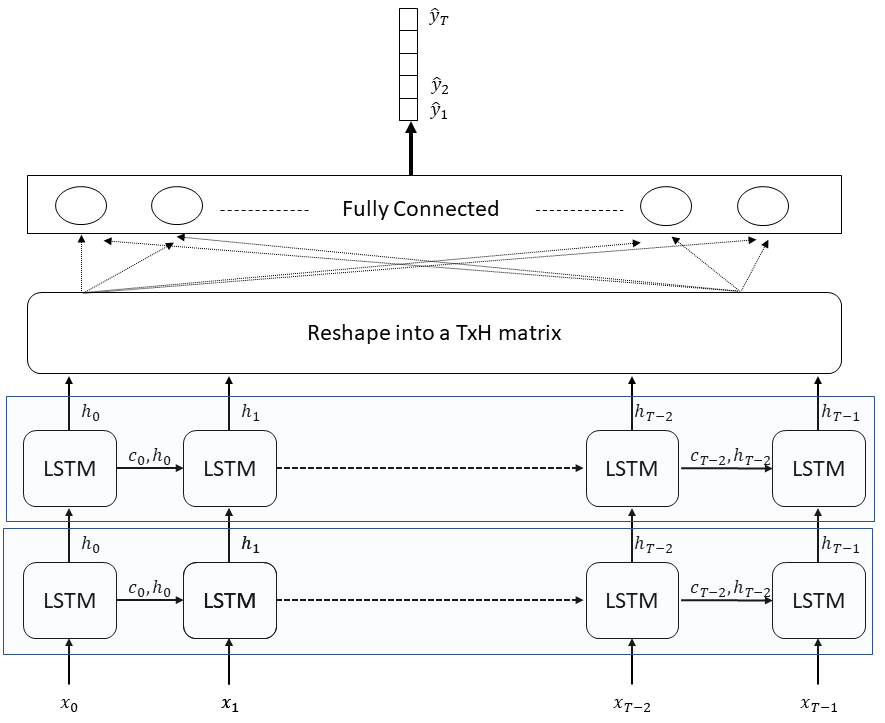

The un-rolled architecture of our network is depicted in Fig. 2.

Operationally, the network receives a sequence of numerical vectors (or batches thereof) , where is a fixed “time window” size (for our purposes will be measured in trading days), and produces a scalar output sequence of which in our context will represent the predicted price of a stock or other asset. We note that for each time , the quantity of interest in the output sequence is its last element, (i.e., the predicted price for the “next” time period), while the previous elements, , correspond to “predictions” for the prices , which are already known at time . Although the inclusion of these output elements may seem superfluous, opting for sequence-to-sequence training will make for better predictive accuracy as well as profitability, as we will see further on. The input vectors are fed into an LSTM cell sequentially, resulting in the sequence of hidden state vectors . These are in turn used as inputs to the next LSTM layer. The hidden state vectors generated by the last LSTM layer (Fig. 2 depicts only two LSTM layers although one can introduce additional ones) are fed through a linear fully-connected layer to produce the output sequence. In short, we have

| (7) |

where is , and O is the output dimension. The term contains the predicted output vectors , stacked in size- batches for each time within our size- window, is the similarly-stacked matrix of the hidden state vectors produced by the last LSTM layer (each batch contributing rows), and , are the weight matrix and bias vectors, sized and , respectively. For our purposes, the feature vectors, , will include an asset’s daily adjusted close price, , opening price, , intra-day low, , intra-day high, , closing price, , and the previous day’s adjusted close, , all obtained online (YahooFinance, 2018), i.e.,

The particular choices of the remaining network parameters (e.g., number of hidden states, , and window size, ), will be discussed in Sec. 4.3.

There are two design choices that we would like to highlight with respect to the network architecture. One has to do with the use of the entire sequence of hidden states, , produced by the last LSTM layer, when it comes to computing outputs. More typically, one could simply let the hidden state evolve while the input sequence is “fed in”, and use only its “last” value, , to compute the prediction . Doing so, however, essentially implies an expectation that all of the “useful” information present in the sequence will be encoded into the last hidden state. On the other hand, utilizing the entire hidden state sequence will allow us to look for information in the time-evolution of the hidden state within the rolling window, which will be prove to be beneficial, as we will see shortly. A second important design choice is the handling of the hidden state vectors by reshaping them into a matrix, to be fed into a single fully-connected linear activation layer as per Eq. 7. By doing so, we avoid having to use one fully-connected layer per time step, , which would introduce “copies” of Eq. 7 for handling each of the separately, resulting in a total of weights to be adjusted. Using a single dense layer as outlined above requires only + weights, a significantly lower number as the window size, , grows. This choice will allow us to train with a very small batch size, which will directly lead to short training times while exploiting information in the time history of the hidden states, and will also make our approach applicable in multi-asset settings or when frequent training is required e.g., in intraday trading.

3.2 Trading Strategy and Allocation

As we have mentioned in Sec. 2, it is common to make trading decisions based on a prediction model’s directional accuracy, even when the model was trained to attain low mean squared or absolute errors. That is, the decision to buy or sell is determined by whether the model predicts an upwards or downwards movement of the asset price over the next time interval. Here, we depart from prior approaches by taking advantage of the fact that it is possible to be nearly “agnostic” about an event occurring, i.e., the direction (up/down) of an asset’s price movement, and yet to be able to glean significant information about the profitability of a trade when conditioning on particular events. In our case the events will have to do with the relative location of predictions within their own distribution.

To make matters precise, we begin by defining the notions of allocation policy and trading strategy:

Definition 1 (Allocation policy).

Let be a prediction model that produces at each time an estimate, , of an asset’s future value , the latter resulting from some underlying stochastic process. Let be the model’s one-step predicted returns at time , and their distribution. An -bin allocation policy is a pair , where is a vector of percentiles of in increasing order, and a vector of allocations in units of the asset (e.g., number of shares to purchase), where the element denotes sale of all units of the asset held.

Definition 2 (Trading strategy).

Given a prediction model, , the current asset price, , and an -bin allocation policy , our proposed trading strategy consists of the following steps, executed at each time :

-

1.

Query for the asset’s predicted return in the next time step, .

-

2.

Let

-

3.

If and we are currently not holding any of the asset, buy units of the asset. If and we are already holding some of the asset, or if , do nothing.

-

4.

If , sell any and all units of the asset held.

In our case, the model will be the LSTM network described in the previous Section. Intuitively, the percentiles in partition the real line into “bins”, and the trading strategy is to buy units of the asset whenever the predicted return lies in bin and we do not already own the asset. For simplicity, we will consider allocation policies in which and , i.e, we always sell all of our asset if the predicted return for the next trading day is negative, that being the only event on which we sell. Of course, one can envision variations of the above strategy, including negative allocation values corresponding to “short sales” (i.e., selling an amount of the asset under the obligation to buy it back at a later time, with the expectation that its value will have declined), assigning the “sell signal”, , to more than one bins as determined by , using time-varying values of depending on the available cash in our portfolio, or measuring the allocations in monetary amounts as opposed to units of the asset. Some of these options are worth exploring in their own right, but we will limit ourselves to the setting previously described because of space considerations.

Remark: We note that the proposed trading policy can be viewed as a generalization of the classical directional “up-down” trading strategy. If we set , i.e., we use only one separating point, and , then there will be only two bins, one for positive predicted returns (in which case we buy 1 unit of the asset), and one for negative predicted returns (in which case we sell), which is exactly how the directional strategy works.

3.2.1 Optimizing the allocation policy

Armed with the above definitions, we can now consider the question of what allocation policy is optimal for a given prediction model while following the trading strategy of Def. 2. We will be buying some units of the asset, , when our model’s predicted return lies in bin , and will then hold those units until the predicted return falls within bin . Over time, this process generates a set of holding intervals, , where denotes the time of the -th buy transaction while the predicted return was in bin , and the time of the following sell transaction (i.e., the first time following that the predicted return falls within bin 1). It should be clear from Def. 2 that the intervals will be non-overlapping (because we never execute a buy when already holding the asset) and that their union will be the entire set of times during which we hold a nonzero amount of the asset.

Our allocation policy risks a monetary amount of to purchase units of the asset at each time . The net profit generated from the at-risk amount at the end of the holding interval (i.e., after a single buy-sell cycle) is therefore

| (8) |

Over time, there will be a number of instances, , that the asset was purchased while at bin and the total net profit after buy-sell transactions will then be

| (9) |

resulting in an expected net profit of

| (10) |

The expectation terms in Eq. 10 represent the expected sum of differences in asset price over each bin’s holding intervals, that is, the expected total rise (or fall) in asset price conditioned on buying when the expected return falls within each particular bin and following the proposed trading strategy. It is clear from Eq. 10 that the expected total profit will be maximized with respect to the allocations if each is set to zero whenever the associated expectation term is negative, and to as large a value as possible when the expected price difference is positive. Assuming an practical upper limit, , to the number of asset units we are able or willing to buy each time, the optimal allocation values are thus

| (11) |

In practice, the expectations terms in Eq. 11 will be approximated empirically from in-sample data, therefore their sign could be wrongly estimated, especially when they happen to lie close to zero. For this reason, one may wish to slightly alter Eq. 11 so that we buy when the expected sum of price differences is greater than some small threshold , to reduce the chance of “betting on loosing bins”. Finally, we note that we are taking to be constant (across time and across the bins ) for the sake of simplicity, although other choices are possible as we have previously mentioned.

4 Model training and allocation policy selection

As we have seen, the specification of the optimal allocation and trading strategy described in the previous Section, requires the (empirical) distribution of the predicted returns which are generated by our LSTM model. That is, we need a trained model in order to obtain concrete values for the percentiles in and the “bins” they induce, as well as the estimated sums of price differences per bin that will determine the allocations, , in Eq. 11. A step-by-step summary of our approach is as follows:

-

1.

Train and test the LSTM network over a rolling window of size , where for each trading day, , in the period from 1/1/2005-1/1/2008, the network’s weights are first adjusted using price data from the immediate past, (i.e., input , and output target ); then, the network is given as input and asked to predict the price sequence once step ahead, , from which we keep the next day’s adjusted closing price, , and calculate the predicted return, .

-

2.

Use the distribution of the predicted returns generated by the rolling-window process to determine the vector of cutoff points, . These points could be chosen to have constant values, or to correspond to specific percentiles of , or in any other consistent manner.

-

3.

For each bin determined by , use the history of input data and corresponding model predictions over 1/1/2005-1/1/2008 to determine the buy and sell events that would have resulted by having followed the trading strategy of Def. 2. Compute the asset price differences for each buy-sell cycle and sum over each bin, , in which the corresponding buy transactions took place (Eq. 10). Set the allocations to their optimal values as per Eq. 11.

-

4.

Given the allocation policy, , test the profitability of the trading strategy and all variants of our LSTM model with respect to a range of hyper-parameters, over a subsequent time period, -, again training the network daily based on input data from the previous trading days before predicting the next day’s price. Select the hyper-parameter values which yield the most profitable – as opposed to most accurate – model.

-

5.

Apply the selected model to a new data sample (1/4/2010-5/1/2018) and evaluate its profitability121212Profitability will simply be , where is the net profit, as calculated in (9) and is the initial capital invested. We will use the term out-of-sample (instead of testing) when referring to this period, in order to avoid confusion with the rolling training-testing procedure used to make predictions. Similarly, the period 1/1/2005-12/31/2009 used to construct the initial allocation policy and perform hyper-parameter selection will be referred to as in-sample.

We go on to discuss important details and practical considerations for each of these steps.

4.1 LSTM training

In contrast to other studies, e.g., (Bao et al., 2017), which make use of a more traditional training - validation - testing framework, we found that a rolling training-testing window approach was better suited to our setting, where at each time, , the network is trained using data from the immediate past and then asked to predict “tomorrow’s” price (at time ). By updating the model weights at each step, using the most recent information before making a prediction, we avoid “lag” or “time disconnection” between the training and testing data (as would be the case, for example if our training data was “far” into the past compared to the time in which we are asked to make a prediction) and allow the model to better “react” to changing regimes in the price sequence as time progresses, leading to it being more profitable as we shall see. As we noted in Sec. 3.1, we used a sequence-to-sequence training schema because it led to significantly higher cumulative returns compared to sequence-to-value training. We speculate that asking the network to predict sequences of the asset price over a time interval, combined with the use of all hidden vectors produced in that interval, allows the network to learn possible latent \saymicro-structure within the price sequence (e.g., trend or other short-term characteristics), thus facilitating the training process.

The network was trained using back-propagation through time (BPTT), with the ADAM optimizer, implemented in python 3 and Tensorflow v1.8. Network weights were initialized from a uniform distribution (using the Glorot-Xavier uniform method) and LSTM cell states were initialized to zero values. We applied exponential decay to our learning rate, and trained for iterations. The number of iterations was chosen to avoid over-fitting by observing both the training and testing errors, using a mean-squared loss function. It is important to note that the rolling window training process, as described above, used a batch size of (i.e., the network was trained each time on a single -sized window of the data, ). Our numerical experiments showed that for our proposed architecture, larger batch sizes did not increase the ultimate profitability of the model and trading strategy, and sometimes even led to lower performance131313For example, training with a batch size of on the S&P index resulted in twice the mean average percent error and a lower cumulative return compared to training with a batch size of 1, with full details on trading performance to be given in Section 5.. Depending on the choice hyperparameters (listed in Section 4.3), the time required to compute one rolling window step was between and seconds on an modestly equipped computer (Intel i7 CPU and GB of RAM).

4.2 Allocation policy selection

The overall number and values of the allocation policy’s cutoff points () were determined after numerical experimentation to ensure that all of the bins defined by included an adequate population of samples and were sufficient in number to allow us to discern differences in the profits realized by the trading strategy when executing a buy in different bins. We found that an effective approach, in terms of ultimate profitability, was to select the cutoff points in using percentiles of the distribution of the absolute expected returns, Thus, the cutoff was set to zero (so that as per Def. 2 we sell any holdings if our model’s predicted return is negative), and another six cutoff points, , were chosen to correspond to the first six deciles (, , , , , and points) of the distribution of absolute predicted returns, splitting the set of predicted returns into eight bins. For each bin, , we could then use historical predicted and actual prices to calculate the sum of price differences (as per in Eq. 11) and determine the optimal allocation . We emphasize that the above choices with respect to were the result of experimentation, and that the elements in could in principle be optimized; however, doing so is not trivial, and we will not pursue it here because of space considerations.

In practice, it is be advantageous to allow the allocation policy to adapt to new data rather than be fixed for a significant amount of time, because the distributions of the predicted and realized returns are unlikely to be stationary. As the model makes a new prediction each day, we have a chance to add the new data to the distribution of predicted returns and adjust the cutoff points in . In the same vein, as the trading strategy generates new buy-sell decisions, we may re-calculate the allocations . There are many options here, such as to accumulate the new information on returns and trading decisions as in a growing window that stretches to the earliest available data, or to again use a rolling window so that as each day new data is added to the distribution, “old” data is removed.

With the above in mind, we chose to update the percentiles in at every time step, using a growing window of data that began 120 time steps prior to our first out-of-sample prediction. For example, in order to making a prediction for - the first day of our out-of-sample period - the model’s predicted returns between - were included in the empirical distribution used to calculate . This was done in order to avoid the problem of initially having no data (e.g., on the first day of our out-of-sample period) from which to calculate the . The 120 step “bootstrap” period was selected after experimenting with several alternatives, including using more or less of the initial history of predicted returns, or using a fixed-size rolling window to determine how much of the “past” should be used. With respect to the allocations, , when computing the per-bin sums of price differences in Eq. 11, we found that it was best in practice (i.e., increased profitability) to include all of the available history of buy-sell events and corresponding price differences, up to the beginning of our data sample (). Moving forward, as buy and sell decisions were made at each time step, the resulting price differences were included in the sums of Eq. 11 and the allocations were updated, if necessary. An instance of the set of bins, corresponding cutoff points and sums of price differences for each bin (computed for use on the first trading day of the out-of-sample period, ) are listed in Table 1. For example, if the predicted return for for the SP falls within the - bin (or, equivalently in the interval ), we do not buy any of the asset (corresponding allocation set to zero) because if we did, the expected price difference in the asset would be negative at the time we sell the asset.

| SP | DJIA | NASDAQ | R | |||||

|---|---|---|---|---|---|---|---|---|

| Bin (deciles) | ||||||||

| 1: SELL | - | - | - | - | ||||

| 2: - | ||||||||

| 3: - | ||||||||

| 4: - | ||||||||

| 5: - | ||||||||

| 6: - | ||||||||

| 7: - | ||||||||

| 8: - | - | - | - | - | ||||

As previously discussed, it is optimal to buy units only when the predicted return falls within a bin whose realized sum of price differences is positive. In practice, the choice of is usually subject to budget constraints or investment mandates which limit the maximum number of units to purchase. This maximum could also be tied to the risk profile of the investor. In our study, was set to the maximum number of units one could buy with their available capital at the start of the trading period. For example, at the beginning of our out-of-sample period, 1/04/2010, the price of the S&P 500 index was , and therefore if our initial capital was we would set . On a practical note, however, because stock indices are not directly tradeable, one can instead trade one of the available Exchange Traded Funds (ETFs) which track the index and are considered one of the most accessible and cheapest options for investing in indices. Therefore, in order to apply our approach to the S&P, we could choose to trade SPY, a popular ETF which tracks that index, and – based on the aforementioned initial capital and SPY price of on 1/04/2010 – set . In the experiments detailed in the next Section, we will choose to trade four well-known ETFs, namely SPY for the S&P, DIA for the DJIA, IWM for the R and ONEQ for the NASDAQ.

4.3 Hyper Parameter Tuning

A grid-search approach was used to select the parameters of our neural network, namely the number of LSTM layers, number of units per LSTM layer (), the dropout parameter (dropout was applied only on the input of a given neuron), and the length of the input sequence. Because our ultimate goal is profitability, this meant evaluating the cumulative returns of our model under each combination of parameters, in order to identify the most profitable variant (which could be different depending on the stock or stock index under consideration). For each choice of hyper-parameters listed in Table 2, we carried out the rolling training-testing procedure described above, over the period 1/1/2005-1/1/2008, and calculated an initial allocation strategy .

| Parameters | Range |

|---|---|

| Nr. of LSTM layers | |

| Nr. of units () | |

| Input sequence length () | |

| Dropout | ,, |

Following that, we used data from 1/2/2008-12/31/2009, to calculate the profit realized by applying our trading strategy (while the allocation policy evolved each trading day, as described in the previous Section). This subsequent period, containing trading days, contained a sufficient number of rolling windows and corresponding predictions from which to compare performance for each choice of hyper-parameters. In addition, it encompasses the global financial crisis of 2009 and is long enough to capture various market cycles. The model parameters leading to the highest cumulative return for each of the four stock indices of interest were thus identified and are listed in Table 3.

| Parameters | S&P 500 | DJIA | NASDAQ | R |

|---|---|---|---|---|

| Nr. of LSTM layers | ||||

| Nr. of units () | ||||

| Input sequence length () | ||||

| Dropout |

On a small 6-machine, 96-CPU, 96Gb RAM computing cluster, the entire grid search process was easily parallelized. For smaller network configurations, e.g., input sequences of length , using layers and neurons, the process described above took a few () hours to complete, while configurations with length- input sequences required up to days.

5 Results

Having settled on a choice of hyper-parameters, we tested the performance (annualized returns and other measures of interest) of the resulting model(s) and associated trading strategy on our out-of-sample period, -, which we had set aside for this purpose. Summarizing the procedure outlined in the previous Section, for each trading day, , within this period, we updated the LSTM network’s weights by training it on the time window of input data from with a target output of , and then computed the prediction, , of the next day’s closing price, using input data over the window ,…,. Next, we determined the predicted return, , and the bin, , (based on the percentiles in ) within which it lies. We then bought or sold the amount of asset units (or corresponding ETF in case of an index) prescribed by the allocation policy (i.e., buy units if and we did not already own the asset, and sell all of our units if ) If a buy was executed, we recorded the index of the bin, , and the asset price at that time. When that asset was later sold, the profit obtained from that transaction (i.e., sell price minus buying price) was added to the sum of price differences term in Eq. 11, and we recalculated the corresponding allocation if the update caused a change in the sign of the sum. Finally, we included to the growing set of previous predicted returns and adjusted the decile points in to account for their new distribution, thus completing our update of the allocation policy, .

We proceed with the main results concerning i) the prediction accuracy, and ii) the profitability of our proposed scheme over the out-of-sample period, for each of the stock indices studied. We will also discuss comparisons against recent efforts, as well as “naive” prediction approaches and trading strategies.

5.1 Error metrics and prediction performance

Although our central goal is to achieve good trading performance, we will nevertheless begin by evaluating our proposed LSTM model using some of the metrics often cited in studies involving prediction accuracy including mean directional accuracy141414, where the indicator function returns if is positive, zero otherwise, and are the realized and predicted prices for time , respectively, is the length of the out-the-sample sequence. (MDA) which in less formal terms measures how accurate a model is at predicting the correct direction (up/down) of stock price movement, mean squared error151515. (MSE), mean absolute error161616. (MAE), mean absolute percentage Error171717. (MAPE) and correlation coefficient181818, where and are the averages of the actual () and predicted () price sequences, respectively. (). Table 4 shows the predictive performance of the proposed LSTM model for each of the four stock indices, for the same out-of- sample period (-).

| Metrics | SP | DJIA | NASDAQ | R |

|---|---|---|---|---|

| MDA | ||||

| MAPE | ||||

| MAE | ||||

| MSE | ||||

Overall, our model achieves a MAPE below and a MDA narrowly above , for all indices. However, applying the Pesaran-Timmermann (PT) to the predicted vs. actual direction of price movements did not confirm that the LSTM model accurately predicts price movement direction in a statistically significant manner. The test statistics and corresponding p-values were (PT=-3.61, p=0.999), (PT=-1.84, p=0.9674), (PT=-0.64, p=0.7378), and (PT=-2.03, p=0.9789), for the SP, DIJA, NASDAQ and R2000 indices, respectively. The fact that our LSTM model does not provide a significant advantage in predicting next-day price movement direction implies that our model may not be effective when used with the day-to-day directional \sayup-down strategy often used in the literature. It does not, however, preclude us from being able to produce significant profits under other trading strategies, such as the one proposed in Sec. 3.2 which does not require directional accuracy on the part of the model.

When compared against other recent studies, e.g., Bao et al. (2017), our model has significantly lower MAPE for SP and DIJA (see Table 5), while the coefficient is better in both cases (using the same test period as in Bao et al. (2017)).

| SP | DIJA | |||

|---|---|---|---|---|

| Metics | Bao et al. (2017) | LSTM | Bao et al. (2017) | LSTM |

| MAPE | ||||

| 0.946 | 0.949 | |||

| SP | NASDAQ | |||

|---|---|---|---|---|

| Metrics | Zhou et al. (2019) | LSTM | Zhou et al. (2019) | LSTM |

| MAPE | ||||

| MAE | ||||

| RMSE | ||||

for the same out-of-sample period used in that work, our model performs comes in very close for the SP and performs better for NASDAQ with respect to MAE and RMSE. Finally, Table 7 compares with Baek and Kim (2018), where our model outperforms in all three statistics (MAPE, MAE, MSE).

| SP | ||

|---|---|---|

| Metrics | Baek and Kim (2018) | LSTM |

| MAPE | ||

| MAE | ||

| MSE | ||

We note that our model relies on a relatively simple architecture with no pre-processing layers, making it simple to implement and fast to train. This is to be contrasted with more elaborate designs, such as the three-layered approach of Bao et al. (2017) passing data through a wavelet transformation and autoencoder neural network before reaching the LSTM model, or the “dual” LSTM models of Baek and Kim (2018). Despite its simplicity, our model’s predictive performance is similar to that of more complex approaches, and compares favorably to studies with long out-of-sample periods (Bao et al. (2017), Baek and Kim (2018)).

We emphasize the fact that the comparisons and discussion of the model’s predictive performance - although encouraging - are given here mainly for the sake of providing a fuller picture, and that good predictive performance will mean little unless our model also performs favorably in terms of profitability (to be discussed shortly). In fact, there is an important point of caution to keep in mind regarding predictive accuracy, and it has to do with the proper context when citing MAPE, MAE and MSE values. Specifically, when it comes to asset prices, daily changes are usually small on a relative basis, and thus a MAPE of less than , for example, is neither unusual nor surprising. In fact, a naive model which “predicts” that tomorrow’s price will simply be equal to today’s (i.e., ), applied to the SP, would typically yield very low error metrics, e.g., MAPE = , MAE=, MSE= over our out-of-sample period, or a MAPE of for the period examined in Baek and Kim (2018) (to be compared with a MAPE of reported in that work). Of course, this naive model is completely useless from the point of view of trading because it does not allow us to make any decision on whether to buy or sell, highlighting the fact that models with similar prediction accuracy can have vastly different profitability, while favorable MAPE, MAE, and MSE scores do not by themselves guarantee success in trading. When the ultimate goal is profitability, the prediction model should be evaluated in the context of a specific trading strategy, and one may achieve high(er) returns by looking beyond average errors, as the trading and allocation strategies of Section 3.2 do.

5.2 Profitability

We now turn our attention to the profitability of our proposed LSTM model and trading strategy. The results presented below are labeled according to the stock indices studied, however – as noted in Sec. 4.2 – all trading is done using their corresponding tracking ETFs, namely SPY for the S&P500, DIA for the DJIA, IWM for the R2000 and ONEQ for the NASDAQ, since the indices themselves are not tradeable. The cumulative returns we obtained when trading over 1/04/2010-5/1/2018 (listed in Table 8),

| Profitability Measures | ||||||

|---|---|---|---|---|---|---|

| CR | AR | AV | SR | DD | ||

| SP | LSTM | |||||

| BnH | ||||||

| DJIA | LSTM | |||||

| BnH | ||||||

| NASDAQ | LSTM | |||||

| BnH | ||||||

| R | LSTM | |||||

| BnH | ||||||

significantly outperformed the benchmark buy-and-hold strategy ( vs , vs , vs , and vs for the S&P500, DJIA, NASDAQ and R2000 indices, respectively); the same was true on an annualized basis. A sample comparison illustrating the time history of capital growth using our approach vs buy-and-hold is shown in Figure 3.

Our superior performance over the buy and hold strategy, comes at the cost of a higher standard deviation of returns achieved ( vs , vs , vs , vs for the SP, DJIA, NASDAQ and R, respectively), leading to lower corresponding Sharpe ratios (except for the SP) compared to buy-and-hold. Draw-down, a measure of investment risk defined as the largest peak-to-trough decline during the investment’s life-cycle, was also affected, with our model having larger negative peak-to-trough returns versus buy-and-hold ( vs , vs , vs , vs for the S&P5, DJIA, NASDAQ and R2000, respectively). This is expected, given that we are comparing a semi-active trading strategy against the “passive” buy-and-hold strategy that executes only a single buy; however, the draw-down is not excessive, and our trading strategy is able to more than make up for it as is evident from its superior annualized and cumulative returns. Finally, our trading strategy executed , , , and trades for the S&P, DJI, NASDAQ, and R, respectively, over the trading days in the out-of-sample period. On average, this corresponds to approximately one transaction per week (ranging from once per four trading days for the R, to once per six days for the DJI). We note that the returns cited above ignore transaction costs. We have chosen to do this because our strategy trades only one asset, does not take short positions where costs have a larger impact, and trades sparingly as noted above. Moreover, transaction costs for institution-class investors are minimal, ranging from to basis points per trade regardless of the transaction amount, while retail investors can nowadays trade without cost through online brokers191919Examples of brokers that offer free retail trades include RobinHood (https://robinhood.com), and Vanguard (https://investor.vanguard.com/investing/transaction-fees-commissions/etfs).

5.2.1 Comparisons with recent works

Besides the benchmark buy-and-hold strategy, the results given in the previous Section indicate that our proposed model outperforms those in several recent works which attempt to beat the major stock indices used here, most often the S&P500. A direct comparison to Baek and Kim (2018) (also trading the SP over a long out-of-sample period, -), shows that our approach outperforms by a significant margin in terms of cumulative return ( vs ). Next to Sezer and Ozbayoglu (2018), which employed deep convolutional neural networks instead of LSTMs, our model achieved an annualized return of compared to the reported in that work when trading the same tracking EFT as we have (SPY), or when using a portfolio of ETFs, over the period of -. Other studies with relatively long out-of-sample periods, include Krauss et al. (2017) and Fischer and Krauss (2018); compared to those, our model yields a significantly greater cumulative return ( vs and , respectively, over their out-of-sample period, -) and, as a result, a higher positive Sharpe ratio ( vs negative for the other two works), noting however that those works traded a portfolio of stocks derived from the S&P500 and not the index (or ETF) itself. Finally, we note that our results are not directly comparable with those in works who report high average or summed returns (e.g., Bao et al. (2017) and others) from which unfortunately one cannot deduce annualized returns or other “standard” measures of trading performance, as we have explained in Section 2.

The works cited thus far reported performance over multi-year periods. Direct comparisons between different approaches over short evaluation periods must be made cautiously because superior performance over any short period does not necessarily imply sustainable long-term results, making it difficult to say which method is better. Having said that however, compared to the model from Zhou et al. (2019) for the SP, using the same out-of-sample period (the year ), our approach attained a higher cumulative return of vs . Finally, in comparison with Chiang et al. (2016) during their out of sample period (the year ) our approach also performs strongly ( vs. when using their long-only trading strategy).

5.2.2 Attributing the overall performance

As we have previously stated, altering either the trading strategy or the prediction model will affect the overall scheme’s profitability. This brings up the question of “how much” of the performance attained is due to the proposed LSTM architecture versus the trading and allocation strategy which we have outlined. This is difficult to answer fully, partly because it requires rating the performance of many alternative prediction models when paired with our proposed trading strategy, as well as different trading strategies to be used with our proposed LSTM model. Here, we will opt to gain some insight by examining the performance of a simple autoregressive integrated moving average (ARIMA) predictor model under our proposed trading strategy, as well as the performance of our LSTM network under the classic directional “up-down”strategy whose variants are used frequently throughout the literature (Bao et al., 2017; Baek and Kim, 2018; Zhou et al., 2019). Of course the ARIMA model lacks sophistication, but its purpose here will be to serve as a “canonical” baseline case only.

To proceed with our analysis, we fitted an model to the daily (adjusted close) price sequence of each stock index under consideration, where , and are the orders of the autoregressive, difference, and moving average terms, respectively. In each case, the model was fitted to the price data of the in-sample period ( - ), and the optimal values of the , , and , were determined by searching over the integers (up to a maximum of order 3) and selecting the model with the lowest AIC and BIC. The selected models were then examined to ensure that their coefficients were statistically significant at the level. The resulting model orders were: for the SP, for the DJIA, for the NASDAQ, and for the R index. The model coefficients are not listed here for the sake of brevity.

In terms of MAPE, MAE and MSE, the predictive performance of the ARIMA models was close to but generally slightly worse than that of our proposed LSTM model (see Table 9, where for convenience we have also inlcuded the LSTM-based error metrics from Table 4).

| SP | DJIA | NASDAQ | R2000 | |||||

|---|---|---|---|---|---|---|---|---|

| Metrics | LSTM | LSTM | LSTM | LSTM | ||||

| MDA | ||||||||

| MAPE | ||||||||

| MAE | ||||||||

| MSE | ||||||||

A Diebold-Mariano (DM) test was performed to determine whether the LSTM price forecasts were more or less accurate than those of the ARIMA model(s). Under the null hypothesis that the ARIMA forecast was more accurate than that of the LSTM-based model, the test statistics and corresponding p-values for the SP, DJIA, NASDAQ and R2000 were (DM =, p-value=), (DM =, p-value=), (DM=, p-value=), and (DM=, p-value=), respectively. This indicates that at confidence level the LSTM model was a better (one-step) predictor than the ARIMA model only in the cases of the SP and the R but of course, as we have alluded to earlier, profits – rather than statistical measures of accuracy – should be used to evaluate stock market forecasts (Leitch and Tanner, 1991).

Turning to the central issue of profitability, we can elucidate the effect of the proposed trading strategy alone, by examining the performance “boost” it gives the LSTM and ARIMA models, compared to when those same models are paired with the directional \sayup-down trading strategy where each trading day we buy if the predicted price is greater than the current price, and sell if it is lower. The profitability (cumulative returns) of each model-strategy combination is shown in Table 10, for each of the four stock indices.

| Trading Strategies | |||

|---|---|---|---|

| Proposed | \sayUp-Down | ||

| SP | LSTM | ||

| BnH: | |||

| DJIA | LSTM | ||

| BnH: | |||

| NASDAQ | LSTM | ||

| BnH: | |||

| R | LSTM | ||

| BnH: | |||

Unsurprisingly, the linear ARIMA model was well behind the LSTM model in terms of cumulative returns; its returns also had roughly twice the annualized standard deviation202020under the proposed trading strategy, AV for ARIMA vs LSTM was vs , vs , vs , and vs , for the S&P, DJIA, NASDAQ and R, respectively.. Two things are worth observing, however. First, our proposed trading and asset allocation policy leads to a significant boost in cumulative returns with both models, sometimes allowing even the (simplistic) ARIMA model to outperform the buy-and-hold strategy (S&P, NASDAQ). Second, when using the “up-down” strategy, the LSTM model significantly outperforms the ARIMA model for all stock indices, despite the fact that the two models were similar in terms of accuracy, as previously discussed; in that case, however, the LSTM-based returns were much weaker relative to the buy-and-hold approach (or indeed to the studies mentioned in Section 5.2.1). The fact that the LSTM model can perform strongly (Section 5.2) but not when used with a strategy other than the one proposed here, highlights the fact that it is fruitful to treat the design of the prediction model and trading strategy as a joint problem, despite the difficulty involved.

6 Conclusions and future work

Motivated by the complexity involved in designing effective models for stock price prediction together with accompanying trading strategies, as well as the prevalence of “directional” approaches, we presented a simple LSTM-based model for predicting asset prices, together with a strategy that takes advantage of the model’s predictions in order to make profitable trades. Our approach is not focused solely on constructing a more precise or more directionally accurate (in terms of whether the price will rise or fall) model; instead, we exploit the distribution of the model’s predicted returns, and the fact that the “location” of a prediction within that distribution carries information about the expected profitability of a trade to be executed based on that prediction. The trading policy we described departs from the oft-used directional \sayup/down strategy, allowing us to harness more of the information contained within the model’s predictions, even then that model is relatively simple.

Our proposed model architecture consists of a simple yet effective deep LSTM neural network, which uses a small number of features related to an asset’s price over a relatively small number of time steps in the past (ranging from 11 to 22), in order to predict the price in the next time period. Novel aspects of our approach include: i) the use of the entire history of the LSTM cell’s hidden states as inputs to the output layer, as the network is exposed to an input sequence, ii) a trading strategy that takes advantage of useful information that becomes available on the profitability of a trade once we condition on the predicted return’s position within its own distribution, and iii) selecting the network’s hyper-parameters to identify the most profitable model variant (in conjunction with the trading strategy used), instead of the one with lowest prediction error, recognizing the fact that predictive accuracy alone does not guarantee profitability. Our design choices with respect to the LSTM network allowed us to “economize” on the architecture of the prediction model, using 2-3 LSTM layers, input sequences of 11-22 time-steps, and 32-128 neurons, depending on the stock index studied. Our model is frugal in terms of training data and fast in terms of training-testing times (updating the model and trading strategy requires between and seconds on a typical desktop computer), and is thus also suitable for intra-day or multi-stock/index prediction applications.

The performance of our proposed model and trading strategy was tested on four major US stock indices, namely the S&P500, the DJIA, the NASDAQ and the Russel 2000 over the period -. To the best of our knowledge, besides “beating” the indices themselves, our model and trading strategy outperform those proposed in several recent works using multi-year testing periods, in terms of the cumulative or annualized returns attained while also doing well in terms of volatility and draw-down. With respect to works that used short (e.g. single-year) testing periods, our scheme outperformed some in their chosen comparison periods, or could achieve lower vs. higher returns if the time period was shifted, keeping in mind that it is difficult to reach safe conclusions when comparing over any one short time interval. Based on the overall profitability results and rather long testing period used in this work, we feel that our approach shows significant promise.

Opportunities for future work include further experimentation with more sophisticated allocation and trading strategies, the possible inclusion of short sales, as well as the use of a variable portion of the time history of the LSTM hidden states when making predictions, to see where the optimum lies. Also, it would be of interest to optimize the manner in which the percentiles of the predicted return distribution are chosen when forming our allocation strategy, in order to maximize profitability and reduce risk. Finally one could in principle use the proposed distribution-based trading strategy with any other model that outputs price predictions, and it would be interesting to see what performance gains, if any, could be achieved.

References

References

- Baek and Kim (2018) Baek, Y. and Kim, H. Y. (2018). ModAugNet: A new forecasting framework for stock market index value with an overfitting prevention LSTM module and a prediction LSTM module. Expert Systems with Applications, 113:457–480.

- Bao et al. (2017) Bao, W., Yue, J., and Rao, Y. (2017). A deep learning framework for financial time series using stacked autoencoders and long-short term memory. PLoS ONE, 12(7): e0180944.

- Chiang et al. (2016) Chiang, W.-C., Enke, D., Wu, T., and Wang, R. (2016). An adaptive stock index trading decision support system. Expert Systems with Applications, 59(C):195–207.

- Chong et al. (2017) Chong, E., Han, C., and Park, F. C. (2017). Deep learning networks for stock market analysis and prediction: methodology, data representations, and case studies. Expert Systems with Applications, 83(C):187–205.

- Deng et al. (2017) Deng, Y., Bao, F., Kong, Y., Ren, Z., and Dai, Q. (2017). Deep direct reinforcement learning for financial signal representation and trading. IEEE Transactions on Neural Networks and Learning Systems, 28(3):653–664.

- Ding et al. (2015) Ding, X., Zhang, Y., Liu, T., and Duan, J. (2015). Deep learning for event-driven stock prediction. In Proceedings of the 24th International Conference on Artificial Intelligence, IJCAI’15, pages 2327–2333. AAAI Press.

- Fama and French (1993) Fama, E. F. and French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of Financial Economics, 33(1):3–56.

- Fama and French (2004) Fama, E. F. and French, K. R. (2004). The capital asset pricing model: Theory and evidence. Journal of Economic Perspectives, 18(3):25–46.

- Fischer and Krauss (2018) Fischer, T. and Krauss, C. (2018). Deep learning with long short-term memory networks for financial market predictions. European Journal of Operational Research, 270(2):654–669.

- Foster et al. (2018) Foster, G., Vaswani, A., Uszkoreit, J., Macherey, W., Kaiser, L., Firat, O., Jones, L., Shazeer, N., Wu, Y., Bapna, A., Johnson, M., Schuster, M., Chen, Z., Hughes, M., Parmar, N., and Chen, M. X. (2018). The best of both worlds: Combining recent advances in neural machine translation. In Proceedings of the 56th Annual Meeting of the Association for Computational Linguistics, ACL 2018, Melbourne, Australia, July 15-20, 2018, Volume 1: Long Papers, pages 76–86.

- Gu et al. (2018) Gu, S., Kelly, B. T., and Xiu, D. (2018). Empirical asset pricing via machine learning. Paper in Swiss Finance Institute Research Paper No. 18-71.

- Hochreiter and Schmidhuber (1997) Hochreiter, S. and Schmidhuber, J. (1997). Long short-term memory. Neural computation, 9(8):1735–1780.

- Huck (2009) Huck, N. (2009). Pairs selection and outranking: An application to the S&P 100 index. European Journal of Operational Research, 196(2):819–825.

- Huck (2010) Huck, N. (2010). Pairs trading and outranking: The multi-step-ahead forecasting case. European Journal of Operational Research, 207(3):1702–1716.

- Krauss et al. (2017) Krauss, C., Do, X. A., and Huck, N. (2017). Deep neural networks, gradient-boosted trees, random forests: Statistical arbitrage on the S&P 500. European Journal of Operational Research, 259(2):689–702.

- Leitch and Tanner (1991) Leitch, G. and Tanner, J. E. (1991). Economic forecast evaluation: Profits versus the conventional error measures. American Economic Review, 81(3):580–90.

- Minh et al. (2018) Minh, D. L., Sadeghi-Niaraki, A., Huy, H. D., Min, K., and Moon, H. (2018). Deep learning approach for short-term stock trends prediction based on two-stream gated recurrent unit network. IEEE Access, 6:55392–55404.

- Olah (2018) Olah, C. (2018). Understanding LSTM Networks, August 17 (2015). http://colah.github.io/posts/2015-08-Understanding-LSTMs/[Accessed: 1st May 2018].

- Rather et al. (2015) Rather, A. M., Agarwal, A., and Sastry, V. (2015). Recurrent neural network and a hybrid model for prediction of stock returns. Expert Systems with Applications, 42(6):3234–3241.

- Russakovsky et al. (2015) Russakovsky, O., Deng, J., Su, H., Krause, J., Satheesh, S., Ma, S., Huang, Z., Karpathy, A., Khosla, A., Bernstein, M., Berg, A. C., and Fei-Fei, L. (2015). ImageNet Large Scale Visual Recognition Challenge. International Journal of Computer Vision (IJCV), 115(3):211–252.

- Sermpinis et al. (2013) Sermpinis, G., Theofilatos, K., Karathanasopoulos, A., Georgopoulos, E. F., and Dunis, C. (2013). Forecasting foreign exchange rates with adaptive neural networks using radial-basis functions and Particle Swarm Optimization. European Journal of Operational Research, 225(3):528–540.

- Sethi et al. (2014) Sethi, M., Treleaven, P., and Rollin, S. D. B. (2014). Beating the S&P 500 index — a successful neural network approach. In 2014 International Joint Conference on Neural Networks (IJCNN), pages 3074–3077.

- Sezer and Ozbayoglu (2018) Sezer, O. and Ozbayoglu, M. (2018). Algorithmic financial trading with deep convolutional neural networks: Time series to image conversion approach. Applied Soft Computing, 70:525–538.

- Silver et al. (2017) Silver, D., Schrittwieser, J., Simonyan, K., Antonoglou, I., Huang, A., Guez, A., Hubert, T., Baker, L., Lai, M., Bolton, A., Chen, Y., Lillicrap, T., Hui, F., Sifre, L., van den Driessche, G., Graepel, T., and Hassabis, D. (2017). Mastering the game of Go without human knowledge. Nature, 550:354–359.

- Wu et al. (2016) Wu, Y., Schuster, M., Chen, Z., Le, Q. V., Norouzi, M., Macherey, W., Krikun, M., Cao, Y., Gao, Q., Macherey, K., Klingner, J., Shah, A., Johnson, M., Liu, X., Kaiser, L., Gouws, S., Kato, Y., Kudo, T., Kazawa, H., Stevens, K., Kurian, G., Patil, N., Wang, W., Young, C., Smith, J., Riesa, J., Rudnick, A., Vinyals, O., Corrado, G., Hughes, M., and Dean, J. (2016). Google’s neural machine translation system: Bridging the gap between human and machine translation. CoRR, abs/1609.08144.

- YahooFinance (2018) YahooFinance (2018). Yahoo Finance, Symbol Lookup (2018). https://finance.yahoo.com/quote/[Accessed: 1st May 2018].

- Zhong and Enke (2017) Zhong, X. and Enke, D. (2017). Forecasting daily stock market return using dimensionality reduction. Expert Systems with Applications, 67:126–139.

- Zhou et al. (2019) Zhou, F., Zhou, H., Yang, Z., and Yang, L. (2019). EMD2FNN: A strategy combining empirical mode decomposition and factorization machine based neural network for stock market trend prediction. Expert Systems with Applications, 115:136–151.