1. Introduction

Despite its undoubtedly significant historical and theoretical value, the classical Black-Scholes model does not explain numerous empirical phenomena that can be observed on real-life markets, such as implied volatility smile and skew. In order to overcome this issue, [17] and, later, [15] introduced stochastic volatility models that emerged into an essential subject of research activity in financial modeling nowadays.

To illustrate the range of existing models (without trying to list all possible references), we recall the approaches of [1], [4], [5], [8], [11], [18], [20], [29], and so on.

A separate class of stochastic volatility models are those based on fractional Brownian motion. They allow to reflect the so-called “memory phenomenon” of the market (for more detail on market models with memory see, for instance, [3, 12, 31]). In this context, we should also mention [7, 9, 10] and [6].

In the present paper, we consider option pricing in a framework of the fractional modification of the Heston-type model, namely a financial market with a finite maturity time that is composed of two assets:

(i) a risk-free bond (or bank account) , the dynamics of which is characterized by the formula

| (1) |

|

|

|

where represents the risk-free interest rate;

(ii) a risky asset , the evolution in time of which is given by the system of stochastic differential equations

| (2) |

|

|

|

| (3) |

|

|

|

with non-random initial values , where the process is a standard Wiener process, , are constants, : is a function that satisfies some regularity properties and is a fractional Brownian motion with the Hurst index , which corresponds to the “long memory” case. and are assumed to be correlated.

The process was extensively studied in [26, 27] and, for the case , in [25]. Note that, according to [28], the process exists, is unique and has continuous paths until the first moment of zero hitting. Moreover, in Theorem 2 of [26] it was shown that in case of and such process is strictly positive and never hits zero, therefore exists, is unique and continuous on the entire .

Such choice of the volatility process can be explained by the fact that can be interpreted as the square root of the fractional version of Cox-Ingersoll-Ross process. Indeed, according to [26], Theorem 1, the process satisfies the stochastic differential equation of the form

|

|

|

until the first moment of zero hitting, where the integral is considered as the pathwise limit of the sums

|

|

|

as the mesh of the partition tends to zero.

Note that, due to Kolmogorov theorem, fractional Brownian motion has a modification with Hölder continuous paths up to order . Hence, from the form of the equation (3), the process also has a modification with trajectories that are Hölder-continuous up to order . Therefore, in case of , the sum of Hölder exponents of the integrator and integrand in the integral

|

|

|

exceeds 1 and, due to [32], the corresponding integral exists as the pathwise limit of Riemann-Stieltjes integral sums.

It should be also mentioned that for the case , the process can hit zero and it is not clear whether the solution exists on the entire (see [27] for more detail). Therefore, we will concentrate on the case . For more information on markets with rough volatility see, for example, [14] or [19].

An analogue of the model (2), (3) was considered in [6] with fractional Ornstein-Uhlenbeck process instead of . However, Ornstein-Uhlenbeck process can take negative values with positive probability which is a notable drawback for a stochastic volatility model.

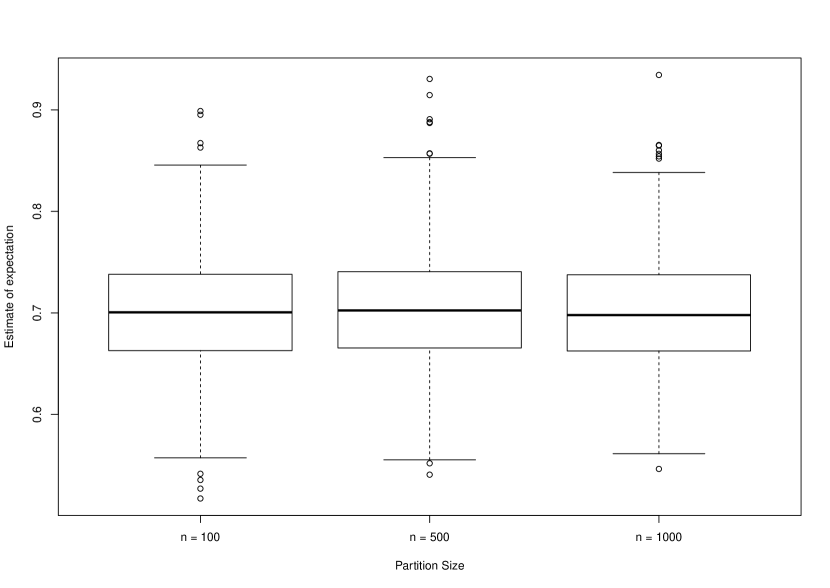

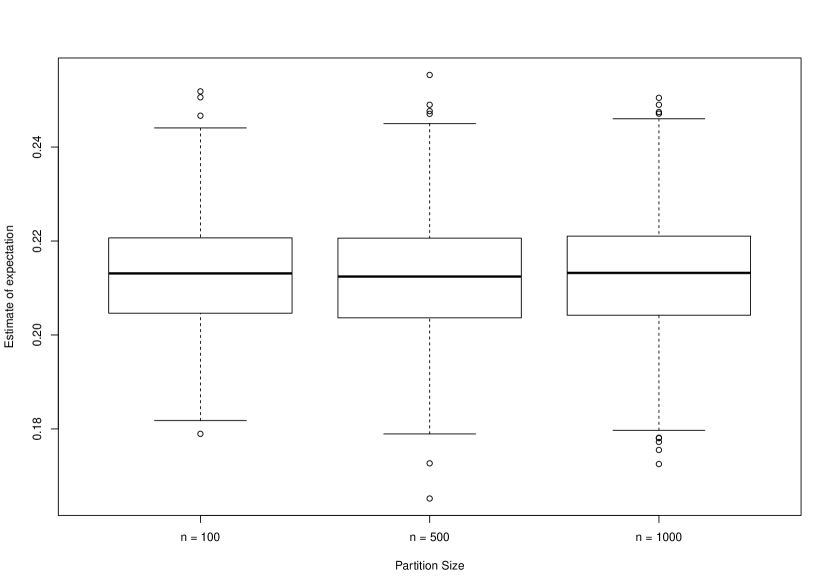

Note that it is impossible to calculate (with being a payoff function) for option pricing analytically, so numerical methods should be used. Therefore it is required to provide a decent discretization scheme for and prove the convergence

| (4) |

|

|

|

where is a discretized version of the process . Moreover, we allow to have discontinuities of the first kind which can cause errors in straightforward Monte-Carlo estimation of the expectation, so we provide an alternative formula with smooth functional under the expectation. In such framework, we also give the rate of convergence (4).

It should be mentioned that the market with risky asset defined by (2)–(3) is arbitrage-free, incomplete but admits minimal martingale measure (see Section 3). However, the expectations calculated with respect to the minimal martingale and objective measures differ only by non-random coefficient, therefore, for simplicity, we concentrate on expectation with respect to the objective measure. In order to model the volatility , we use the inverse Euler approximation scheme studied in [16].

The paper is organized as follows. In Section 2, we describe main assumptions concerning relation between the Wiener process and the fractional Brownian motion as well as volatility function and payoff function . In Section 3 several important properties of both price and volatility processes are presented and the arbitrage-free property is discussed. In Section 4 we apply the Malliavin calculus techniques, following [1] and [6], to obtain the formula for option price that does not contain discontinuities (which are allowed for the payoff function ). In Section 5, we study the rate of convergence of Monte-Carlo estimation of the option price based on inverse Euler approximation scheme for fractional CIR process presented in [16]. In Section 6, we give results of numerical simulations for different payoff functions . Section 7 contains the proofs of all results of the paper. Appendix A is devoted to several well-known results from the Malliavin calculus used in this paper.

7. Proofs

Proof of Theorem 3.3. Denote and let be fixed. By applying the chain rule, we obtain:

| (20) |

|

|

|

|

|

|

|

|

It is clear from (3) that the process has trajectories that are -Hölder-continuous for any , so the process

|

|

|

also has Hölder-continuous trajectories up to the order . Therefore, the sum of Hölder exponents of the integrator and integrand in the integral w.r.t. fractional Brownian motion in (20) exceeds 1. In this case this integral is the pathwise limit of Riemann-Stieltjes integral sums (see, for example, [32]), coincides with the pathwise Stratonovich integral and, by applying Theorem A.1, we can rewrite (20) as follows:

| (21) |

|

|

|

|

|

|

|

|

|

|

|

|

where is the Malliavin derivative operator w.r.t. and is the corresponding Skorokhod integral.

Note that

|

|

|

|

|

|

|

|

|

|

|

|

From this, it is easy to verify that

|

|

|

so

| (22) |

|

|

|

|

|

|

|

|

Taking into account (21) and (22), we can rewrite (20) in the following form:

| (23) |

|

|

|

|

|

|

|

|

|

|

|

|

where .

Note that

| (24) |

|

|

|

It is easy to verify that

|

|

|

|

|

|

|

|

|

|

|

|

so

|

|

|

Hence, if , i.e. when ,

|

|

|

and

| (25) |

|

|

|

Moreover,

| (26) |

|

|

|

Therefore, taking into account upper bounds (24), (25) and (26), it is obvious from (23) that

|

|

|

|

|

|

|

|

or

|

|

|

|

|

|

|

|

Since the expectation of the Skorokhod integral is zero, by letting we obtain that

| (27) |

|

|

|

Finiteness of the right-hand side of (27) follows from Theorem 3.1.

Proof of Theorem 3.4. From (3), Hölder’s and Jensen’s inequalities it is clear that

| (28) |

|

|

|

where

|

|

|

Note that form of follows from the fact that (see, for example, [30])

From Theorem 3.1 it is obvious that

| (29) |

|

|

|

Finally, from Theorem 3.3,

| (30) |

|

|

|

where .

The statement of the Theorem now follows from (28), (29) and (30) as well as the fact that from condition it is easy to verify that for any :

|

|

|

Proof of Theorem 3.5. 1. From Theorem 3.1, for all :

|

|

|

and, due to [13], for all and :

|

|

|

Hence,

|

|

|

2. In order to show that the representation (8) indeed holds, it is sufficient to prove that the integrals and are well-defined, while the form of the representation can be obtained straightforwardly.

Note that (see, for example, [24]) for all

|

|

|

so, due to item from Assumption 2 and Theorem 3.1,

|

|

|

and the integral is well-defined.

Now consider the integral . As

| (31) |

|

|

|

it is sufficient to check two conditions:

|

|

|

Using Theorem 3.1 and Assumption 2, , it is easy to verify that

| (32) |

|

|

|

Moreover, from (7), for any :

| (33) |

|

|

|

|

|

|

|

|

hence, for all , by putting , we obtain the Novikov’s condition for the process , .

Consequently,

| (34) |

|

|

|

and so

| (35) |

|

|

|

due to (33).

Therefore, from (31), (32) and (35),

|

|

|

and so the integral is well-defined.

Proof of Theorem 3.6. The proof is similar to the proof of Theorem 4 in [6].

Proof of Lemma 4.1. Item can be found in [6]. In particular, in follows from independence of and .

Applying stochastic derivative operator to both parts of the integral form of (3), we get

| (36) |

|

|

|

|

|

|

|

|

|

|

|

|

Application of the chain rule with the function can be justified by the same argument as in Remark 10 of [6], since is locally Lipschitz on .

According to [26], Theorem 2, does not hit zero a.s. Therefore is well defined a.s., and (36)

means that for a fixed , the process

defined by satisfies a random linear integral equation of the form

| (37) |

|

|

|

This is a Volterra equation, and its solution is given by

| (38) |

|

|

|

Note that is differentiable in the first argument ( is well defined for ), so (38) can be checked by

substituting in (37) and taking derivatives of both sides.

Both derivatives in are obtained by direct differentiation following the Malliavin derivative rules, see e.g. [23], Proposition 3.4. Since is independent of ,

|

|

|

To find , we note that

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proof of Theorem 4.1. The result can be obtained by following the proof of Lemma 11 in [6], taking into account Lemma 4.1 and relation (35).

Proof of Theorem 5.2. First, note that for any fixed and :

| (39) |

|

|

|

By continuing calculations above recurrently and taking into account that , it is easy to see that there is such constant that

|

|

|

Moreover, for any fixed there is such constant that

|

|

|

Let us prove that there is such (which does not depend on ) that

|

|

|

From calculations above, it will be enough to show that, for some ,

|

|

|

Let be fixed. Consider the last moment of staying above level , i.e.

|

|

|

Let us prove that for any point of the partition , , the following inequality holds:

| (40) |

|

|

|

|

|

|

|

|

In order to do that, we will separately consider cases and .

Step 1. Assume that . Then, due to representation (16),

|

|

|

Note that for all :

|

|

|

Moreover, from Jensen’s inequality,

|

|

|

Finally,

|

|

|

Hence, for all :

|

|

|

Step 2. Assume that , i.e. there are points of partition on the interval . From definition of , and for all points of the partition such that :

|

|

|

Let be fixed and denote

|

|

|

It is obvious that and , and

| (41) |

|

|

|

In addition, if ,

|

|

|

and if ,

|

|

|

From definition of , for all points of the partition it holds that , so

|

|

|

Furthermore,

|

|

|

and

|

|

|

Hence,

| (42) |

|

|

|

Finally, from (41) and (42),

|

|

|

Therefore, (40) indeed holds for any point of the partition.

Step 3. As ,

|

|

|

therefore, as, due to (40),

|

|

|

we have

|

|

|

Using the discrete version of the Grönwall’s lemma, we obtain:

|

|

|

i.e., taking into account that the right-hand side does not depend on and remarks in the beginning of the proof, there is such that

| (43) |

|

|

|

Now the claim of the Theorem follows from the fact that the right-hand side of (43) does not depend on and that (see, for example, [24])

|

|

|

Proof of Corollary 5.1. From (43) it follows that there is such that

|

|

|

The rest of the proof is similar to Theorem 3.5, 1.

Proof of Theorem 5.3. We shall proceed as in proof of Lemma 14, [6].

Using Hölder’s inequality, we write:

|

|

|

From Assumption 2 (iii), Jensen’s inequality and Theorem 5.1,

|

|

|

|

|

|

|

|

|

|

|

|

Moreover, Assumption 2, (ii) and (iii), implies that

|

|

|

From Theorem 5.1,

|

|

|

and, from Theorems 3.1 and 5.2,

|

|

|

Therefore, taking into account bounds above, there is such constant that

|

|

|

Now, let us prove (19). Taking into account Assumption 2 (i),

|

|

|

so, from Assumption 2 (iii),

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Proof of Lemma 5.1. It is clear that

| (44) |

|

|

|

Now we shall estimate the right-hand side of (44) term by term.

|

|

|

From Assumption 3 (i), both and are of polynomial growth, therefore, due to (35),

|

|

|

Furthermore, using sequentially the inequalities

|

|

|

and Hölder’s inequality, we obtain that

|

|

|

Next, from (34) and Remark 5.3 it follows that

|

|

|

so, using this together with Hölder and Burkholder-Davis-Gundy inequalities, we continue the chain as follows:

|

|

|

By applying Assumption 2, (ii) and (iii),

|

|

|

and

|

|

|

From Theorems 3.1 and 5.2,

|

|

|

and, according from Theorem 5.1,

|

|

|

hence

| (45) |

|

|

|

Now, let us move to the second term of the right-hand side of (44).

|

|

|

Due to Remark 5.3,

|

|

|

and, from Assumption 3 (i),

|

|

|

According to (35) and Remark 5.3,

|

|

|

so

|

|

|

To get the final result, we can proceed just as in the upper bound for the first term in the right-hand side of (44). Thus

| (46) |

|

|

|

Relations (45) and (46) together with (44) complete the proof.

Proof of Theorem 5.4. According to Theorem 4.1,

|

|

|

According to Theorem 3.5, Assumption 3 (i) and the Cauchy-Schwartz inequality, . Next,

|

|

|

The proof now follows from Theorem 5.3 and Lemma 5.1.