Online Primal-Dual Mirror Descent under Stochastic Constraints

Abstract

We consider online convex optimization with stochastic constraints where the objective functions are arbitrarily time-varying and the constraint functions are independent and identically distributed (i.i.d.) over time. Both the objective and constraint functions are revealed after the decision is made at each time slot. The best known expected regret for solving such a problem is , with a coefficient that is polynomial in the dimension of the decision variable and relies on the Slater condition (i.e. the existence of interior point assumption), which is restrictive and in particular precludes treating equality constraints. In this paper, we show that such Slater condition is in fact not needed. We propose a new primal-dual mirror descent algorithm and show that one can attain regret and constraint violation under a much weaker Lagrange multiplier assumption, allowing general equality constraints and significantly relaxing the previous Slater conditions. Along the way, for the case where decisions are contained in a probability simplex, we reduce the coefficient to have only a logarithmic dependence on the decision variable dimension. Such a dependence has long been known in the literature on mirror descent but seems new in this new constrained online learning scenario.

1 Introduction

We consider an online convex optimization (OCO) problem with a sequence of arbitrarily varying convex objective functions which are revealed per slot after the decision is made, and is a closed bounded convex set. For a fixed time horizon , define the regret of a sequence of decisions as

The goal of OCO is to choose the decision sequence so that the regret grows sublinearly with respect to . OCO is a classical problem and has been considered in a number of previous works such as (Cesa-Bianchi et al., 1996; Gordon, 1999; Zinkevich, 2003; Hazan, 2016). In particular, it is known that for differentiable functions , the projected gradient descent algorithm achieves an regret which is also worst case optimal. When the set is a probability simplex, the mirror descent algorithm further achieves an “almost dimension free” logarithmic dependency on the dimension .

The framework considered in this paper builds upon the previous OCO model by incorporating a sequence of time varying constraint functions , which are also revealed at each time slot after the decision is made. The goal of this constrained OCO is to choose the decision sequence so that both the regret and constraint violations grow sublinearly in (i.e. ) with respect to the best fixed decision in hindsight solving the following convex program:

| (1) |

The constrained OCO was first considered in the work (Mannor et al., 2009) where the authors (somewhat surprisingly) show via a counterexample that even with only one constraint, it is not always possible to achieve the aforementioned goal if we allow both objective and constraint functions to vary arbitrarily. Such an impossibility result implies that if one wants to obtain meaningful results on constrained OCO, then more assumptions have to be posed.

The works (Mahdavi et al., 2012; Jenatton et al., 2016; Titov et al., 2018) consider the scenario where the constraint functions are fixed (i.e. do not depend on the time index ) and propose primal-dual type methods whose analyses give regret and constraint violation, where is an algorithm parameter. This bound is improved in the work (Yu and Neely, 2016) where the authors show an regret bound and finite constraint violations (i.e. constraint violation) via Slater condition (i.e. There exists a such that ). A more recent work (Yuan and Lamperski, 2018) shows that one can get logarithm regret and constraint violations if one assumes instead that all objective functions are strongly convex.

Constrained OCO with stochastic constraints, where and are i.i.d., is considered in the works such as (Yu et al., 2017; Chen and Giannakis, 2019; Liakopoulos et al., 2019), where a primal-dual proximal gradient algorithm is proposed and expected regret and constraint violations are shown under the Slater condition (i.e. there exists a such that ). Without Slater condition, the best known result is again regret and constraint violation as is shown in (Yi et al., 2019). Also, to the best of our knowledge, previous bounds in constrained online learning fail to recover the “almost dimension free” phenomenon for the probability simplex decision set ubiquitous in unconstrained scenarios. In this paper, we make steps towards removing the Slater condition while maintaining the worst case optimal regret, constraint violations, and sharpening the dimension dependency on decision variables.

Slater condition is assumed in the classical analysis of optimization algorithms for constrained convex programs such as the dual subgradient algorithm (Nedić and Ozdaglar, 2009) and the interior point method (Boyd and Vandenberghe, 2004). A key implication of Slater condition, which is adopted in the convergence rate analysis in (Nedić and Ozdaglar, 2009), is that it implies the existence and boundedness of Lagrange multipliers. However, the reverse implication is in general untrue, as one can show that for many equality constrained convex programs, Lagrange multipliers do exist and are bounded (Bertsekas, 1999). This makes “Slater condition free” analysis an important topic in optimization theory and motivates series of improved primal-dual type algorithms and analysis for constrained convex programs with competitive convergence rate under the existence of Lagrange multipliers assumption (Neely, 2014; Yurtsever et al., 2015; Deng et al., 2017; Yu and Neely, 2017).

Replacing the Slater condition with Lagrangian type assumptions in online problems is highly non-trivial and does not follow from that of constrained convex programs. A key issue is that the objective function varies arbitrarily per slot, and so the definition of Lagrange multiplier is not clear. A simple attempt is to look at in-hindsight problems such as (1) and see if the Lagrange multiplier of this problem helps with the regret analysis. However, since problem (1) sums the objectives across the horizon, it hardly gives any insight on the per slot dynamics for any practical algorithm considered. If we instead look at the per slot constrained problem, then, one might be able to conduct analysis and obtain per-slot multipliers, but it is not clear how to piece together the analysis for different slots.

1.1 Contributions

In this paper, we consider the stochastic constrained online learning problem and propose a new primal-dual online mirror descent framework, which simultaneously weakens the assumptions and improves the dimension factors in the previously known online proximal gradient type algorithms. We introduce a new sequential existence of Lagrange multipliers condition, which is shown to be strictly weaker than the Slater condition, allows for equality constraints and bridges the aforementioned dilemma between on-hindsight problem and per slot problem. We then show via a new analysis that under such an assumption, the proposed algorithm enjoys a matching expected regret and constraint violations. For the case when decisions are contained in a probability simplex, we reduce the dimension dependency to have only a logarithmic factor. Conceptually, our analysis seems to be distinctive from the previous known methods in the sense that we look at the cumulative objectives over a specifically chosen time period (of length ), and consider the following static constrained program starting from any time slot : We demonstrate that the existence and boundedness of Lagrange multipliers for this problem provides certain weak error bound conditions for the dual function sufficient to bound the size of the dual variable process, leading to the desired results.

1.2 Notation

For any vector , means is entrywise nonnegative, zero and nonpositive, respectively. The notation denotes entrywise application of the function . The notation stands for the positive orthant of . For any set , let be its interior. The norms , and . For any convex function , we use to denote any one of the subgradients at and use to denote the set of all subgradients at . For any function which is convex on the first argument , denotes the subgradient of on while fixing . For any closed set and any point , the distance of to is defined as .

2 Problem Formulation and Algorithms

2.1 Basic definitions

Let be a general norm in . Define the dual norm on any as . Consider a convex set (potentially be itself) with a non-empty interior, i.e. . Let be a function that is continuously differentiable in the interior of . Let be a compact convex subset containing the origin and , which is non-empty. Define the Bregman divergence function generated from as follows:

The following is a key property of the Bregman divergence:

Lemma 1 (Pushback)

Let be a convex function. Fix , . Suppose and , then, for any ,

Remark 2

For the case where is a linear function and is convex, such a pushback result can be found, for example, in (Nemirovski et al., 2009). For results with being on domain , the proof can be found in (Tseng, 2005). Our result generalizes previous results to arbitrary set . It is proved in the Supplement (Section 7.1)

We say is a distance generating function if for any , is a continuously differentiable and strongly convex with modulus with respect to the primal norm , i.e. It is easy to see if is a distance generating function, then, the corresponding satisfies

| (2) |

Note that behaves asymmetrically on and over potentially different domains, which results from the (possible) non-differentiability of the distance generating function on the boundary of . One such example is the KL divergence.

-

1.

The set is a probability simplex, , the function is the entropy function, and for any two distributions , is the well-known Kullback-Leibler (KL) divergence. Furthermore, by Pinsker’s inequality, it is strongly convex with respect to with the strongly convex modulus . The dual norm in this space is .

-

2.

The set is in the Euclidean space , and , which is strongly convex with respect to , , and the dual norm is also .

2.2 Problem formulation

In this section, we set up the basic formulation of stochastic constrained online optimization. Let and be two processes, where can be arbitrarily time varying (might be chosen based on the system history) and are i.i.d. realizations of a random variable with a possibly unknown distribution. Let , be deterministic functions which are convex in the first component given the second component. Furthermore, let be sequences of i.i.d. random vectors in . Throughout the paper, we assume are jointly independent for all with system history up to time as . For any fixed , we write , , and , . We further define the vectorized notations , , and . It is also worth noting that our algorithms and analysis also apply to the special case where are also i.i.d. for which we have .

Define the benchmarking decision in-hindsight as a solution to the following static convex program:

| (3) |

where is a vector of constants. At the beginning of each time slot , none of the objective function , constraint function or random vector is known. The decision maker is supposed to choose a vector first before observing these quantities. The goal is to make sequential (possibly randomized) decisions so that both the expected regret, defined as , and expected constraint violations, define as and , grow sublinearly with respect to the time horzon . Throughout this paper, we make the following boundedness assumption:

Assumption 1 (Boundedness of objectives and constraint functions)

-

1.

Objective functions and constraint functions have bounded subgradients on , i.e. there exist absolute constants and such that , , for all , all , and all .

-

2.

There exist absolute constants such that , for all , and , for all .

-

3.

The Bregman divergence is generated from a distance generating and bounded on the set , i.e. there exists a constant such that .

2.3 Primal-dual online mirror descent

We are now in a position to introduce our new online mirror descent (Algorithm 1) for the stochastic constrained online learning. The algorithm computes the next decision by a proximal mirror map using , and , and control the constraint violations via dual multipliers and .

Let be some trade-off parameters. Let be sequences of dual multipliers such that . Let .

For t = 0 to :

-

1.

Choose as a solution to the following problem:

(4) -

2.

Update each dual multiplier via

(5) (6) -

3.

Observe the objective function and constraint functions .

End for.

2.4 Sequential Existence of Lagrange Multipliers (SELM)

In this section, we introduce our Lagrange multiplier condition. A detailed comparison between such a condition and other constraint qualification conditions is delayed to the Supplementary (Section 7.2). We start by defining a partial average function starting from any time slot as: . Consider the following optimization problem:

| (7) |

where are defined in Section 2.2. Denote the solution to this program as . Define the Lagrangian dual function of (7) as

| (8) |

where and are dual variables. For simplicity of notations, we always enforce them to be row vectors. Now, we are ready to state our condition:

Assumption 2 (Sequential existence of Lagrange multipliers (SELM))

For any time slot and any time period , the set of primal optimal solution to (7) is non-empty. Furthermore the set of dual optimal solution, which is , is non-empty and bounded. Any vector in is called a Lagrange multiplier associated with (7). Furthermore, there exists an absolute constant such that for any and , the dual optimal set defined above satisfies .

Remark 3

Note first that SELM reduces to the known existence and boundedness of Lagrange multipliers assumption adopted in optimization theory when the objectives are also i.i.d. functions. In Section 7.2 of the Supplement, we show that SELM is equivalent to certain constraint qualification conditions and strictly weaker than the Slater conditions. In particular, we obtain the following simplifications in special cases: (1) Lemma 15 shows that Slater condition implies SELM. (2) Corollary 24 implies that when the interior of is non-empty and there are only equality constraints, the linear independence of is equivalent to SELM. (3) Lemma 18 implies that when is a probability simplex there are only equality constraints, the linear independence of is equivalent to SELM.

The motivation for SELM is as follows: whenever Lagrange multipliers exist and are bounded, we automatically get that the dual function deviates according to a certain curve related to the distance from the set of Lagrange multipliers, namely, the weak error bound condition (EBC).

Definition 4 (Weak error bound condition (EBC))

Let be a concave function over , where is closed and convex. Suppose is non-empty. The function satisfies the weak EBC if there exists constants such that for any satisfying ,

Note that in Definition 4, is a closed convex set. This follows from the fact that is a convex function and thus all sub level sets are closed and convex. The following lemma shows SELM implies weak EBC:

Lemma 5

In the Supplement (Section 7.2.3), we will compare this weak EBC with the classical EBC in optimization theory and show that classical EBC implies weak EBC with explicit constants.

3 Main results

In this section, we present our main result of online primal-dual mirror descent.

Theorem 6

Let be a solution to the in-hindsight optimization problem (3). Suppose Assumption 1 and 2 hold. Let be absolute constants such that and for all obtained in Lemma 5 over and . If we choose in Algorithm 1, then the expected regret and constraint violations satisfy:

where are constants depending linearly on and independent of .

3.1 Proof of regret bound

In this section, we present the proof of regret bound in Theorem 6. The proofs of technical lemmas are delayed to the Supplement (Section 7.4.1). We start with the following key bound of a drift-plus-penalty (DPP) expression:

Lemma 7

Define the drift . Consider the following “drift-plus-penalty” (DPP) expression at time : . Let where is in (2), then, for any ,

| (9) |

This lemma is proved via the property of Bregman divergence (Lemma 1). Now, for the DPP expression on the left hand side, we also have the following lower bound:

Lemma 8

Our Algorithm 1 ensures

| (10) |

Substituting this bound in to (9), taking which is the solution to the in-hindsight problem (3), and taking conditional expectations from both sides, we readily get:

| (11) |

Note that

where, in both inequalities, the first step follows from the fact that are i.i.d. and depend on , and the second step follows from being a solution to the in-hindsight optimization problem (3), thus, must be feasible, i.e. , . Thus, taking the full expectation from both sides of (11) gives

Taking a telescoping sum on both sides from 0 to and dividing both sides by ,

where we use the fact that since and , . Substituting , and yields the desired result with .

3.2 Proof of constraint violations

In this section, we present the proof of constraint violations in Theorem 6. The proofs of technical lemmas are delayed to the Supplement (Section 7.4.2-7.4.5). First, it is enough to bound dual multipliers via the following lemma:

To bound and , we have the following lemma:

Lemma 10

Define constant Then, for any integer , we have the step drift satisfies

| (12) |

where the dual function is defined in (8).

This bound establishes the relation between dual multipliers and the dual function. Next, in view of (10), we would like to show that is small. This is done via Lemma 5 that whenever is far away from the optimal set , which is nonempty and bounded by Assumption 2, becomes negative. In fact one can prove the following lemma:

Lemma 11

Substituting the above lemma into (10) and using a known stochastic drift lemma, one can prove the following bound by setting , :

Lemma 12

The quantity satisfies the following conditions:

| (13) |

where and are absolute constants.

4 The probability simplex case

In this section, we deal with the probability simplex case where the decision set is a -dimensional probability simplex with huge . While Algorithm 1 can be applied to solve such problems by choosing to be , due to the dependencies on the , the constant factors in Theorem 6 linearly depend on . For mirror descent over a probability simplex, to improve the dimension dependence, people usually choose the Bregman divergence distance to be the KL divergence. However, KL divergence fundamentally violates the third assumption in Assumption 1. We now present an alternative algorithm in Algorithm 2 and shows that it can achieve sublinear regret and constraint violations that logarithmically depends on .

Compared to Algorithm 1, Algorithm 2 uses the K-L divergence as the particular Bregman divergence and introduces a probability mixing step , which pushes the update away from the boundary, at each round. Furthermore, it is known that the problem (14) admits a closed form solution known as the exponential gradient update (Hazan, 2016). More specifically, define

Then, the update can simply be written as

We have the following performance bound on this algorithm whose proof is similar to Theorem 6 and delayed to the Supplement (Section 7.5):

Theorem 13

Suppose the first two in Assumption 1 (using and ) and Assumption 2 hold. Let be absolute constants such that and for all obtained in Lemma 5 over and . Choose , in Algorithm 2. The expected regret and constraint violations satisfy:

where are absolute constants depending linearly on and independent of or . (Note that in Assumption 1 are independent of when .)

5 Simulation experiments

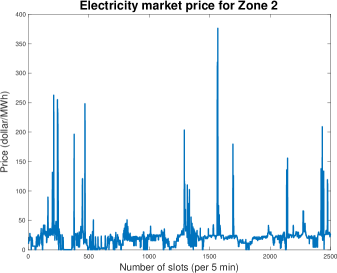

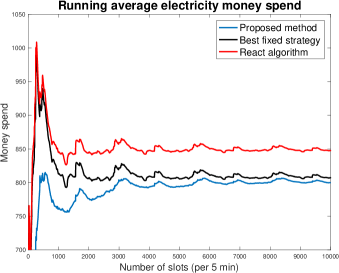

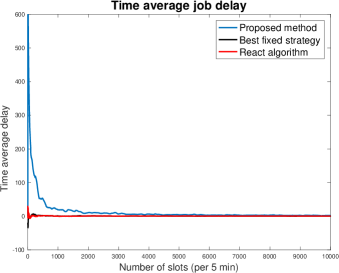

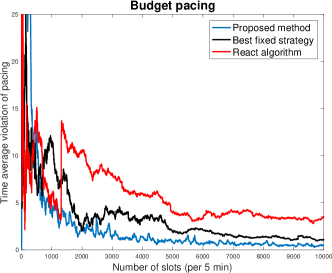

We consider the problem of cost minimization under budget pacing constraints in data center service scheduling. More specifically, consider a geographically distributed data center consists of 5 server clusters serving one stream of incoming jobs arriving at a central controller. Each cluster contains 10 servers. The jobs are directed to different clusters for processing by controller with different per unit electricity costs. In the simulation, we use electricity market price (EMP) data traces from 5 zones of New York ISO open access pricing data (http://www.nyiso.com/). For example, Fig 1(a) depicts the per 5 min EMP data of zone DUNWOD between 05/01/2017 and 05/10/2017. The number of incoming jobs per 5 min is , which is assumed to be poisson distributed with mean equals 1000. each server can choose a power allocation option . This option determines the following over the 5 min slot: (1) The electricity money spend of server : , where is the per unit EMP of the zone server belongs to. (2) The number of jobs served which follows a Pareto distribution (a.k.a. power law, see (Gandhi et al., 2012)) of mean . (3) Internal budget consumptions , where follows a Pareto distribution of mean 5 units. In a typical online service system such as ads service, budget is a measure of internal resources (Agarwal et al., 2014). The goal is to minimize the total average electricity cost over slots, i.e. , subject to the following two requirements: (1) The service rate supports the arrival rate: , which is a convex inequality constraint. (2) The internal budget consumption is well-paced, i.e. each cluster consumes a fixed ratio of the total consumed budget in expectation. More specifically, in the simulation, let be index sets of 5 clusters, then, it is required that and , where . In Fig 1, we compare our proposed algorithm with the best fixed solution in hindsight choosing the best fixed power allocation knowing all the data, and a benchmark Reac algorithm (Gandhi et al., 2012). The Reac algorithm is adapted to our pacing scenario by estimating the number of jobs in the next slot via the average of past 10 slots and assign the load according to the pacing ratio. For cluster 4 and cluster 5 (which take up a total ratio of 0.60), the Reac algorithm evenly distribute the workload between the two. Our algorithm achieves a similar electricity money spend with the best fixed solution which is better than Reac, while keeping the average number of unserved job low and achieving a fast budget pacing.

6 Conclusions

This paper proposes a new primal-dual online mirror descent framework for stochastic constrained online learning problem. We introduce a new sequential existence of Lagrange multipliers condition, which is shown to be strictly weaker than the Slater condition, and prove that the proposed algorithm enjoys a expected regret and constraint violations. We also obtain an almost dimension free result in the special case when the decision set is a probability simplex.

Acknowledgments

This work is supported in part by grant NSF CCF-1718477.

References

- Agarwal et al. (2014) Deepak Agarwal, Souvik Ghosh, Kai Wei, and Siyu You. Budget pacing for targeted online advertisements at linkedin. In Proceedings of the 20th ACM SIGKDD international conference on Knowledge discovery and data mining, pages 1613–1619. ACM, 2014.

- Bertsekas (1999) Dimitri P Bertsekas. Nonlinear programming. Athena scientific Belmont, 1999.

- Boyd and Vandenberghe (2004) Stephen Boyd and Lieven Vandenberghe. Convex optimization. Cambridge university press, 2004.

- Cesa-Bianchi et al. (1996) Nicolò Cesa-Bianchi, Philip M Long, and Manfred K Warmuth. Worst-case quadratic loss bounds for prediction using linear functions and gradient descent. IEEE Transactions on Neural Networks, 7(3):604–619, 1996.

- Chen and Giannakis (2019) Tianyi Chen and Georgios B Giannakis. Bandit convex optimization for scalable and dynamic iot management. IEEE Internet of Things Journal, 6(1):1276–1286, 2019.

- Deng et al. (2017) Wei Deng, Ming-Jun Lai, Zhimin Peng, and Wotao Yin. Parallel multi-block admm with o (1/k) convergence. Journal of Scientific Computing, 71(2):712–736, 2017.

- Gandhi et al. (2012) Anshul Gandhi, Mor Harchol-Balter, and Michael A Kozuch. Are sleep states effective in data centers? In 2012 International Green Computing Conference (IGCC), pages 1–10. IEEE, 2012.

- Gauvin (1977) Jacques Gauvin. A necessary and sufficient regularity condition to have bounded multipliers in nonconvex programming. Mathematical Programming, 12(1):136–138, 1977.

- Gordon (1999) Geoffrey J Gordon. Regret bounds for prediction problems. In Proceeding of Conference on Learning Theory (COLT), 1999.

- Hazan (2016) Elad Hazan. Introduction to online convex optimization. Foundations and Trends in Optimization, 2(3–4):157–325, 2016.

- Jenatton et al. (2016) Rodolphe Jenatton, Jim Huang, and Cédric Archambeau. Adaptive algorithms for online convex optimization with long-term constraints. In Proceedings of International Conference on Machine Learning (ICML), 2016.

- Liakopoulos et al. (2019) Nikolaos Liakopoulos, Apostolos Destounis, Georgios Paschos, Thrasyvoulos Spyropoulos, and Panayotis Mertikopoulos. Cautious regret minimization: Online optimization with long-term budget constraints. In Kamalika Chaudhuri and Ruslan Salakhutdinov, editors, Proceedings of the 36th International Conference on Machine Learning, volume 97 of Proceedings of Machine Learning Research, pages 3944–3952, Long Beach, California, USA, 09–15 Jun 2019. PMLR. URL http://proceedings.mlr.press/v97/liakopoulos19a.html.

- Mahdavi et al. (2012) Mehrdad Mahdavi, Rong Jin, and Tianbao Yang. Trading regret for efficiency: online convex optimization with long term constraints. Journal of Machine Learning Research, 13(1):2503–2528, 2012.

- Mannor et al. (2009) Shie Mannor, John N Tsitsiklis, and Jia Yuan Yu. Online learning with sample path constraints. Journal of Machine Learning Research, 10:569–590, March 2009.

- Nedić and Ozdaglar (2009) Angelia Nedić and Asuman Ozdaglar. Approximate primal solutions and rate analysis for dual subgradient methods. SIAM Journal on Optimization, 19(4):1757–1780, 2009.

- Neely (2014) Michael J Neely. A simple convergence time analysis of drift-plus-penalty for stochastic optimization and convex programs. arXiv preprint arXiv:1412.0791, 2014.

- Nemirovski et al. (2009) Arkadi Nemirovski, Anatoli Juditsky, Guanghui Lan, and Alexander Shapiro. Robust stochastic approximation approach to stochastic programming. SIAM Journal on optimization, 19(4):1574–1609, 2009.

- Nguyen et al. (1980) V Hien Nguyen, J-J Strodiot, and Robert Mifflin. On conditions to have bounded multipliers in locally lipschitz programming. Mathematical Programming, 18(1):100–106, 1980.

- Titov et al. (2018) Alexander A Titov, Fedor S Stonyakin, Alexander V Gasnikov, and Mohammad S Alkousa. Mirror descent and constrained online optimization problems. In International Conference on Optimization and Applications, pages 64–78. Springer, 2018.

- Tseng (2005) Paul Tseng. On accelerated proximal gradient methods for convex-concave optimization. MIT Technical Report, 2005.

- Tseng (2010) Paul Tseng. Approximation accuracy, gradient methods, and error bound for structured convex optimization. Mathematical Programming, 125(2):263–295, 2010.

- Wei et al. (2018) Xiaohan Wei, Hao Yu, Qing Ling, and Michael Neely. Solving non-smooth constrained programs with lower complexity than : A primal-dual homotopy smoothing approach. In Advances in Neural Information Processing Systems, pages 3999–4009, 2018.

- Xu et al. (2017) Yi Xu, Mingrui Liu, Qihang Lin, and Tianbao Yang. Admm without a fixed penalty parameter: Faster convergence with new adaptive penalization. In Advances in Neural Information Processing Systems, pages 1267–1277, 2017.

- Yang and Lin (2015) Tianbao Yang and Qihang Lin. Rsg: Beating subgradient method without smoothness and strong convexity. arXiv preprint arXiv:1512.03107, 2015.

- Yi et al. (2019) Xinlei Yi, Xiuxian Li, Lihua Xie, and Karl H Johansson. Distributed online convex optimization with time-varying coupled inequality constraints. arXiv preprint arXiv:1903.04277, 2019.

- Yu and Neely (2016) Hao Yu and Michael J Neely. A low complexity algorithm with regret and finite constraint violations for online convex optimization with long term constraints. arXiv preprint arXiv:1604.02218, 2016.

- Yu and Neely (2017) Hao Yu and Michael J Neely. A simple parallel algorithm with an convergence rate for general convex programs. SIAM Journal on Optimization, 27(2):759–783, 2017.

- Yu et al. (2017) Hao Yu, Michael Neely, and Xiaohan Wei. Online convex optimization with stochastic constraints. In Advances in Neural Information Processing Systems, pages 1428–1438, 2017.

- Yuan and Lamperski (2018) Jianjun Yuan and Andrew Lamperski. Online convex optimization for cumulative constraints. In Advances in Neural Information Processing Systems, pages 6140–6149, 2018.

- Yurtsever et al. (2015) Alp Yurtsever, Quoc Tran Dinh, and Volkan Cevher. A universal primal-dual convex optimization framework. In Advances in Neural Information Processing Systems, pages 3150–3158, 2015.

- Zinkevich (2003) Martin Zinkevich. Online convex programming and generalized infinitesimal gradient ascent. In Proceedings of International Conference on Machine Learning (ICML), 2003.

7 Supplement

7.1 The pushback property of Bregman divergences

In this section, we prove the following key property of the Bregman divergence:

Lemma 14

Let be a convex function. Fix , . Suppose and , then, for any ,

Proof [Proof of Lemma 14] First of all, we recall the following known facts about convex functions and their subgradients whose proofs can be found, for example, in (Bertsekas, 1999):

-

•

The set is non-empty for any .

-

•

For any bounded subset , the union is bounded.

By definition of Bregman divergence, we have for any ,

and

Now, we claim the following optimality condition:

Claim 1: For any , there exists a such that following holds:

Proof [Proof of Claim 1] Fix a constant . Since is a convex set, it follows . Thus, by the fact that is a minimizer:

where the first equality follows from the fact that is continuously differentially on the first argument at with representing a high order term such that , and the second equality follows from the definition of Bregman divergence. Canceling the common term and rearranging the terms give

| (15) |

Since is convex and , we have for any .

Substituting this bound into (15) gives

| (16) |

To this point, consider any sequence such that . By the aforementioned property of subgradient, we have the union is bounded. Thus, the sequence is bounded, and there exists a subsequence such that . On the other hand, by definition of subgradient, we have for any ,

Taking the limit gives

where we use the fact that a convex function must be continuous on the interior point of . This implies that

. Substituting into (16) and taking the limit finish the proof.

Thus, by Claim 1, we have there exists a ,

where third equality follows from adding and subtracting ,

the first inequality follows from the aforementioned optimality condition and the last inequality follows from convexity that . Rearranging the terms yields the desired result.

7.2 SELM and constraint qualifications

7.2.1 Slater condition implies SELM

The SELM assumption is actually implied by the Slater condition. More specifically, Slater condition considers the scenario where there is no equality constraint and there exists a such that . First of all, it is well-known that the Slater condition is sufficient for the existence of a dual optimal solution (see, for example, (Bertsekas, 1999)). Furthermore, the following lemma, which is essentially the same as Lemma 1 of (Nedić and Ozdaglar, 2009), implies that the set of dual optimal solutions is also bounded:

Lemma 15

Consider the convex program (7) without equality constraints , and define the Lagrange dual function . Suppose there exists such that for some positive constant . Then, the level set is bounded for any nonnegative . Furthermore, we have .

Note that since is bounded by some constant as stated in Assumption 1. Taking for any optimal dual solution , and notice that , , the above lemma readily implies . Thus, Slater condition implies the existence of Lagrange multiplier condition.

7.2.2 SELM is equivalent to Mangasarian-Fromovitz constraint qualification (MFCQ)

In this section, we show SELM is able to handle general equality constraints and thus strictly weaker than the Slater condition. In 1977, J. Gauvin (Gauvin, 1977) observed that for any constrained convex program, where both the objective and constraint functions are continuously differentiable, the Mangasarian-Fromovitz constraint qualification (MFCQ) condition is in fact equivalent to the boundedness of the set of Lagrange multipliers.111In fact, MFCQ does not require convexity of the constrained programs. Thus, the result in (Gauvin, 1977) even applies to non-convex programs. More specifically, MFCQ is defined as follows:

Definition 16 (Mangasarian-Fromovitz constraint qualification (MFCQ))

Consider a convex program:

| (17) |

It satisfies MFCQ if (a) The vectors are linearly independent. (b) For a solution to the above program, there exists some such that , where .

Theorem 17 ((Gauvin, 1977))

Note that compared to (17) our program (7) has an extra set constraint . The good news is that for the case where is a probability simplex, i.e. it can be written explicitly as , applying Theorem 17, we have the following lemma whose proof is delayed to Section 7.6:

Lemma 18

Consider the optimization problem (7) for any time slot and any time period where is the probability simplex. Suppose (a) The vectors are linearly independent. (b) There exists a solution to (7), denoted as , and a vector such that , where . Then, the set of Lagrange multipliers , where is defined in (8), is non-empty and bounded.

Remark 19

For general scenarios where is just an arbitrary abstract convex set, we have the following definition of generalized MFCQ following (Nguyen et al., 1980). First, we have the definitions of normal cones and tangent cones:

Definition 20 (Normal cone)

Consider any set , the normal cone of at any is

Note that normal cone at is the subgradient of the indicator function of , namely . To see this, consider any , then, we have is a subgradient of at if

Note that if , then , otherwise, . Thus, .

Definition 21 (Tangent cone)

Consider any set , the tangent cone of at any is

and .

Definition 22 (Generalized MFCQ)

Consider a convex program:

| (18) |

It satisfies the generalized MFCQ if (a) The vectors are linearly independent. (b) For a solution to the above program, there exists some such that and any subgradient , where and denotes the interior of .

Note that this definition requires the interior of to be non-empty, which does not work for the case where is a probability simplex. This is why we have a separate lemma (Lemma 18). When assuming the interior of is non-empty, we have the following theorem:

Theorem 23 ((Nguyen et al., 1980))

Applying the above theorem to (7) with , we readily get the equivalence condition for the existence and boundedness of Lagrange multipliers for (7) as follows

Corollary 24

Consider the optimization problem (7) for any time slot and any time period where has an nonempty interior. Suppose (a) The vectors are linearly independent. (b) There exists a solution to (7), denoted as , and a vector such that , where . Then, the set of Lagrange multipliers , where is defined in (8), is non-empty and bounded.

7.2.3 SELM implies weak EBC

In this section, we prove a key property of SELM, namely Lemma 5, which says SELM implies a weak EBC condition. We restate the lemma as follows, and for simplicity, we omit the subscript on the set for simplicity:

Lemma 25

Proof [Proof of Lemma 25]

Since is bounded, there must exist such that . Define . Then, since the set is closed, there exists some constant such that . Now, consider any such that , and choose such that

| (19) |

i.e. .

Choose . Note that . Let . The next claim shows that .

Claim 1: .

Proof It is easy to verify that . To prove this claim, it suffices to show that

To see this, suppose on the contrary, there exists such that attains the above minimum, then, by the strong convexity of the square norm function and convexity of the set , the solution is unique, and it follows

where the strict inequality follows from the aforementioned strong convexity and the last equality follows from the fact that

. However, this implies is of smaller distance to contradicting (19).

By the concavity of , we have,

| (20) |

This further implies that

Recalling the definition of and that by Claim 1, we have

Recalling that and , we have

and we finish the proof.

7.3 On the relation between weak EBC and classical EBC

Recall that the classical EBC, which has been shown to accelerate the convergence rate solving unconstrained and constrained programs (Tseng, 2010; Yang and Lin, 2015; Xu et al., 2017; Wei et al., 2018), is stated as follows:

Definition 26

Let be a convex function over . Suppose is non-empty. The function is said to satisfy the error bound condition (EBC) with parameters and if for any , the -sublevel set defined as ,

| (21) |

where is a positive constant possibly depending on . In particular, when , is said to be locally quadratic and when , it is said to be locally linear.

The following lemma shows that if the dual function further satisfies classical EBC, then, we can show that weak EBC holds with computable constants .

Lemma 27

The proof of this lemma is delayed to Section 7.6.

7.4 Supporting lemmas in proof of Theorem 6

Throughout the section, we let be the system history up to time , which includes , , and .

7.4.1 Proof of lemmas in Section 3.1

On the other hand, define

Using the updating rule (5), (6) and Holder’s inequality that , we have

where the inequality for follows from

via Assumption 1(3) that and . The first inequality in the bound on follows from the fact that if , then, the equality is attained and if , , then, while . The third line follows from . Thus, we have

| (23) |

where the last inequality follows from Assumption 1(1). To this point, we consider the following “drift-plus-penalty” term, i.e.

where the first inequality follows from (23). Now, by (22), we have for any ,

7.4.2 Proof of Lemma 9

We start with a supporting lemma:

Proof [Proof of Lemma 28] We prove the first inequality and the second inequality is proved in the same way. Note that by (5), we have

Taking a telescoping sum from both sides from to ,

This implies

since the right hand side is nonnegative. Thus, we have

where the second inequality follows from Assumption 1.

Proof [Proof of Lemma 9] It is enough to bound the difference . For this, we start from the relation (22) by taking ,

By the fact that

We get

By strong convexity (2), we have

Thus, it follows,

Solving the above quadratic inequality yields

Taking the expectation from both sides and subtracting this bound into Lemma 28 result in

One can prove the bound on with exactly the same computation and we omit the proof.

7.4.3 Proof of Lemma 10

For simplicity of notations, let constant be the minimum over all ’s and let be the maximum over all ’s in Lemma 5 with and . We start with the following supporting lemma:

Lemma 29

Consider the slots drift for some positive integer , then we have

| (24) |

Proof [Proof of Lemma 29] We start from equation (9). Substituting (10), we have

Take the summation from both sides between to for some to be determined later, we obtain

| (25) |

| (26) |

where the second from the last inequality follows from , and the last inequality follows from Assumption 1. Similarly, we can show that

| (27) |

Substituting the above two bounds into (25), using the fact that and , recalling that yields the desired result.

Proof [Proof of Lemma 10] Thus, taking a conditional expectation from both sides conditioned on , we get

| (28) |

where we use the following two facts: (1) . (2) and are independent of system history and thus the conditional expectation equals the expectation.

Note that by definition, , and according to the notation in (7),

Furthermore,

Substituting these three relations into (28), we get

| (29) |

The main idea here, as is mentioned in the proof outline, is to realize that

where is the Lagrangian dual function defined in (8) with dual variables

. This implies if we choose in (7.4.3) as one of the solutions to the above problem, then, we can transform the bound (7.4.3) to (10) and we finish the proof.

7.4.4 Proof of Lemma 11

Proof [Proof of Lemma 11] Now, we take and by SELM (Assumption 2), there exists a solution to the maximization problem

Let be one of the solutions to this problem. Recall that we define to be the minimum over all ’s and define to be the maximum over all ’s in Lemma 5 with and . If , then, by Lemma 5 we have

where the first inequality follows from Lemma 5, the second inequality follows from choosing as the solution to the following problem

and using weak duality (in fact, by Lemma 18, we know KKT conditions hold for this problem and strong duality holds). The third inequality follows from triangle inequality and the boundedness of Lagrange multipliers .

On the other hand, if , then, one has

where we choose to be a point in closest to , the first inequality follows from

and the second inequality follows from weak duality. Overall, we finish the proof.

7.4.5 Proof of Lemma 12

| (30) |

This bound is the key to our analysis. Intuitively, it says if is very large at certain time slot , then, becomes very small. Since is nonnegative, this means cannot be too large to start with. To transform this intuition into a uniform bound on over all time slots, we invoke the following drift lemma:

Lemma 30 (Lemma 5 of (Yu et al., 2017))

Let be a discrete time stochastic process adapted to a filtration with and . Suppose there exist integer , real constants , and such that

| (31) | ||||

| (34) |

hold for all . Then,

To apply this lemma, we set and we need to check condition (31) and (34), for which we prove the following lemma:

Proof [Proof of Lemma 12] For condition (31), we have

On the other hand, for condition (34) we start from (7.4.5). Suppose

then, (7.4.5) can be rewritten as

which implies

Taking square root from both sides and by Jensen’s inequality, we have

Overall, by Lemma 30, we obtain

Taking and and recalling the definition of yields:

where and are absolute constants.

7.5 Proof of Theorem 13

In this section, we present the proof for Theorem 13. The proof takes into account the fact that is the probability simplex and the effect of pull-away operation . Note that in this probability simplex case, we have , which will be used to replace the frequently used relation in the proof for general cases. Note further that when is the probability simplex and is chosen to be K-L divergence, we do not have a uniform bound such that . Fortunately, our analysis does not need such a uniform bound but instead uses a bound on where is in the form of specified in Algorithm 2.

The following lemma bounds the difference between and :

Lemma 31

Consider any , and let , for some , then, it follows

Furthermore,

Proof [Proof of Lemma 31]

where the first inequality follows from the concavity of function. Furthermore, for the second inequality, we have

7.5.1 Regret bound

First of all, by the same proof as that of Lemma 7 one can show the following:

| (35) |

Furthermore, similar to that of Lemma 8, we have

| (36) |

Substituting (36) into (35) gives

| (37) |

Using Lemma 31, we get

The rest follows from the same argument as that of Section 3.1 after (11) and we omit the details for brevity.

7.5.2 Constraint violations

Similar as before, we start with the following lemma:

Proof [Proof of Lemma 32] Using Lemma 28, it is enough to bound the difference . For this, applying Lemma 1 by setting , , and with

we have

| (38) |

Taking in (38) gives,

By the fact that

We get

By Pinsker’s inequality, we have

Thus, it follows,

Solving the above quadratic inequality

which implies

Taking the expectation from both sides and subtracting this bound into Lemma 28 results in

One can prove the bound on with exactly the same computation and we omit the proof.

Now, by Lemma 32 it is enough to bound and , for which we have the following lemma:

Lemma 33

Consider the slots drift for some positive integer , then we have

| (39) |

where

Proof [Proof of Lemma 33] First of all, summing both sides of (37) from to gives

| (40) |

By Lemma 31, one has

and

Thus, substituting these two bounds into (40) gives

| (41) |

Furthermore, following the steps to obtain (26) and (27) by invoking , we have

and . Substituting these three bounds into (41) and recalling that

gives the final bound.

Using the previous bound, one can prove the following lemma:

Lemma 34

If we take in Algorithm 2, then the quantity satisfies the following conditions:

| (42) |

where and are absolute constants independent of or .

Taking and recalling the definition of yields

where and .

7.6 Proof of other supporting lemmas

Proof [Proof of Lemma 18] We expand the simplex constraints in (7) explicitly and the full dual function writes

Let . By the assumption of lemma 18 and Theorem 17 we have the solution set of vectors of the following equations (KKT conditions) is non-empty and bounded:

| (43) | |||

It is easy to verify that and we have zero duality gap, i.e. . Our goal is to show that the set , defined in the statement of the lemma, is equal to the set .

First of all, for any , we have . Since we have zero duality gap and one always has , it follows . Thus, not only do we have a zero duality gap of , we also have being the solution point to the dual maximization problem , showing that is non-empty and .

For the other direction, we pick any and consider the following optimization problem:

| (44) |

By zero duality gap, the solution to this optimization problem is equal to . Thus must be one of the solution points of (44) such that the complementary slackness is satisfied.222Suppose on the contrary for some index , then, this means

taking gives smaller value of the objective than , contradicting the fact that the minimum is . Furthermore, it is obvious that MFCQ is also satisfied for (44) (we only need to check the simplex constraints satisfy MFCQ, which is obvious). Thus, by Theorem 17, we have there exists such that the stationary condition (43) is satisfied, and . Combining with the previous complementary slackness , we arrive at the conclusion that . This implies

.

Overall, we have the set is also bounded and we finish the proof.

Proof [Proof of Lemma 27] First of all, note that by the EBC, for any , one has , thus, for those such that , . We then recall the following result:

Lemma 35 (Yang and Lin (2015))

Consider any convex function such that the minimal set is non-empty. Then, for any and any ,

where , and is the -sublevel set defined in Lemma 27.

Applying this lemma to our scenario, we define and take function to be and consider the -superlevel set . By lemma (35), we readily have

On the other hand,

Now, we claim that . Indeed, suppose on the contrary, , then, by the continuity of the function , there exists and such that , i.e. , and , contradicting the definition that .

Thus, we have

Overall, we have

and we finish the proof.