Asymptotic Theory of -Statistics and Integrable Empirical Processes

Abstract

This paper develops asymptotic theory of integrals of empirical quantile functions with respect to random weight functions, which is an extension of classical -statistics. They appear when sample trimming or Winsorization is applied to asymptotically linear estimators. The key idea is to consider empirical processes in the spaces appropriate for integration. First, we characterize weak convergence of empirical distribution functions and random weight functions in the space of bounded integrable functions. Second, we establish the delta method for empirical quantile functions as integrable functions. Third, we derive the delta method for -statistics. Finally, we prove weak convergence of their bootstrap processes, showing validity of nonparametric bootstrap.

keywords:

[class=MSC]keywords:

journalname \startlocaldefs \endlocaldefs

T1The previous version was circulated with the title “Switching to the New Norm: From Heuristics to Formal Tests using Integrable Empirical Processes.”

1 Introduction

We derive the asymptotic distribution of the statistics of the form

where is a known continuously differentiable function, an empirical quantile function of a random variable , and a random Lipschitz function that depends on . This is a generalization of the classical -statistics [9, 13, 14, 15] to allow for integration with respect to random processes .111[13] allows integration on a random interval but not with respect to a random process.

This type of statistics appears, for example, when sample trimming or Winsorization is applied to asymptotically linear estimators. Let us collectively call sample trimming and Winsorization sample adjustments. If sample adjustments are made conditional on the values of , is a nonrandom function and it falls within the framework of classical -statistics. If sample adjustments are made on variables other than , becomes random and it affects the asymptotic distribution of the -statistics. In economics, this occurs as the parameters of interest (what -statistics estimate) often differ from the variables whose outliers we are concerned. In such cases, dependence of can be difficult to handle directly.

This paper gives both high-level and low-level conditions for weak convergence of the -statistics, derives the asymptotic distribution formula, and verifies validity of nonparametric bootstrap. The innovation of this paper lies in considering empirical processes in the space of integrable functions. The literature on empirical processes has largely focused on uniform convergence irrespective of the intended statistical application. As -statistics are integrals of empirical processes, we (partly) renounce uniform convergence and instead require integrability, which buys us substantial benefits in dealing with -statistics.222In applying the empirical process theory to -statistics, Van der Vaart [16, Chapter 22] states that “[this approach] is preferable in that it applies to more general statistics, but it…does not cover the simplest -statistic: the sample mean.” Our empirical process theory overcomes this problem.

Our theoretical development is summarized as follows. By integration by parts, we expect

First, we consider and as elements in the space of bounded integrable functions with respect to appropriate measures and derive conditions for weak convergence therein (Section 3). Second, we establish the functional delta method for the “inverse map,” , from the space of bounded integrable functions to the space of integrable functions, which shows weak convergence of as an integrable process (Section 4).333This paper is presumably the first to show weak convergence of (possibly unbounded) empirical quantile processes in on the untruncated domain . Third, we develop the functional delta method for the map, , from the spaces of integrable and bounded integrable functions to a Euclidean space, establishing weak convergence of -statistics (Section 5). Finally, we develop conditions for nonparametric bootstrap for the processes and -statistics (Section 6).

The theory of this paper was originally motivated by the following problem of formalizing outlier robustness analyses in economics.

Example 1 (Outlier Robustness Analysis).

Applied researchers often want to examine whether a small portion of outliers affect the regression outcomes [1, 2, 3, 4, 7]. The common heuristic practice in economics is to compare two estimators and , where is estimated with the full sample and with the sample that excludes outliers, against the standard error of . However, since and share largely overlapping samples, their difference tends to be small simply because of their strong positive correlation. To account for this, it is more appropriate to compare the difference to its own variance, as opposed to the marginal variance of . This calls for the joint distribution of and .

Consider linear regression with . The ordinary least squares (OLS) estimator of is , so its asymptotic distribution depends on that of the average of . However, is usually not the quantity whose outliers are of natural concern, but rather, [2], [1, 5], or [3] is. Then, conditional on the value of , the probability that the observation is deemed as an outlier is probabilistic.

Suppose we remove the 2% tail observations of and . Let be if and , and otherwise.444Winsorization can also be accommodated by appropriately defining . The outlier-removed estimator is . Through the quantile transform, we can write

where is the empirical quantile function of and a random weight function whose derivative is for for the empirical distribution function of . Then is random for each fixed value of , which affects the asymptotic distribution of the integrals.

In Section .6, we revisit the outlier robustness analysis in [3].

The rest of the paper is organized as follows. Section 2 defines the setup. Section 3 develops the theory of weak convergence of bounded integrable processes. Section 4 establishes Hadamard differentiability of the inverse map. Section 5 shows Hadamard differentiability of the -statistics. Section 6 verifies validity of nonparametric bootstrap. Section 7 contains proofs. Appendix contains supporting lemmas and an empirical application.

2 The Setup

Let be i.i.d. scalar random variables and be possibly random weights whose distribution is bounded but can depend on all of . Consider a statistic of the form where is a continuously differentiable function, is an order statistic such that , and is ordered according to the order of . Let and , , be the empirical quantile function of and the random weight function. With these,

Denote by the empirical distribution function of and define the inverse of a nondecreasing function by . Then, equals .

The aim of this paper is to derive the joint distribution of finitely many such quantities for possibly different , , and . For this, we proceed in four steps:

-

i.

Give conditions for convergence of and to Gaussian processes as bounded integrable processes.

-

ii.

Show convergence of to a Gaussian process as an integrable process via a functional delta method from to .

-

iii.

Show convergence of -statistics via a functional delta method from to .

-

iv.

Show bootstrap convergence for and .

3 Convergence of Bounded Integrable Processes

Define the space of bounded integrable functions as follows.

Definition.

Let be a measure space where is an arbitrary set, a -field on , and a -finite signed measure on . Let be the space of bounded and -integrable functions with the norm

where represents integration with respect to the total variation measure.

For sums of i.i.d. random variables such as , it is straightforward to prove weak convergence in by the combination of classical central limit theorems (CLTs) [17].

Proposition 3.1.

Let be a -finite Borel measure on . For a probability distribution on such that , the empirical process converges weakly in to a Gaussian process with mean zero and covariance function .

Remark.

For an increasing function , is equivalent to [6]. Moreover, if has a th moment for some , we have .

For processes not given as sums of i.i.d. variables such as , we need direct conditions for weak convergence. As in classical literature, we characterize weak convergence in by asymptotic tightness plus marginal convergence. Following [17], we consider a net indexed by an arbitrary directed set, rather than a sequence indexed by natural numbers. We also allow the sample space to be different for each element in a net, . Finally, we allow each element in the net to be not necessarily measurable. When we write for a map , is understood to be an element of and we regard as a map from to indexed by ; when we explicitly use in the discussion, we write .

Theorem 3.2.

Let be arbitrary. Then, converges weakly to a tight limit if and only if is asymptotically tight and marginals converge weakly for every finite subset of . If is asymptotically tight and its marginals converge weakly to the marginals of a stochastic process , then there is a version of with sample paths in and .

Weak convergence of marginals can be established by classical results such as CLTs in Euclidean spaces. The question is asymptotic tightness. We characterize this with uniform equicontinuity and equiintegrability.

Definition.

For a -measurable semimetric on ,555We call a semimetric -measurable if every open set induced is measurable with respect to . the net is asymptotically uniformly -equicontinuous and -equiintegrable in probability if for every there exists such that

The following result characterizes asymptotic tightness in .

Theorem 3.3.

The following are equivalent.

-

i.

A net is asymptotically tight.

-

ii.

is asymptotically tight in for every , is asymptotically tight in , and for every there exists a finite -measurable partition such that

(3.1) -

iii.

is asymptotically tight in for every and there exists a -measurable semimetric on such that is totally bounded and is asymptotically uniformly -equicontinuous and -equiintegrable in probability.

Remark.

The condition “” allows for the point masses in and plateaus in . In (3.1), this corresponds to “.”

Now we turn to conditions for . The following is a special case of suitable for .

Definition.

Let be an integrable increasing function and let be the space of functions with the norm

Let be the subset of Lipschitz functions with Lipschitz constants bounded by .

The following lemma gives a low-level condition for to converge in . Roughly, if is integrable, then in the uniform norm for some implies in .

Lemma 3.4.

Let be an increasing function in for some . If for a net of processes there exists such that for every there exists satisfying

then there exists a semimetric on such that is totally bounded, is asymptotically uniformly -equicontinuous in probability, and is asymptotically -equiintegrable in probability.

This implies that sample adjustments based on fixed quantiles satisfy the condition. For example, let be i.i.d. continuous random variables and be their subset selected by some (possibly random) criterion. Then, if the empirical process of the subset converges weakly uniformly to a smooth distribution, then converges weakly in .

Proposition 3.5.

Let be independent uniformly distributed random variables on and random variables bounded by whose distribution can depend on and . Define and Let and assume that exists and is Lipschitz differentiable. If and converges weakly jointly in , then for

we have converge weakly in for every increasing function for every .

4 Convergence of Quantile Processes as Integrable Processes

For a smooth function for which has sufficient moments, we establish weak convergence of to a Gaussian process. If is identity, the (unweighted) empirical quantile process converges weakly in on the entire domain , without truncating the tails, even if is an unbounded function. Interestingly, this point has been overlooked in the literature, which mostly concerned uniform convergence of either bounded or weighted quantile processes [8, 10, 11, 12, 15].

In particular, we show differentiability of the inverse map as a functional from to . Note that in terms of and in terms of . Therefore, the appropriate space for is the following special case of while the space for is a standard .

Definition.

Let be a nondecreasing continuously differentiable function. Let be the space of Borel-measurable functions with limits and the norm

where . Denote by the subset of of monotone cadlag functions with and .

Definition.

Let be the space of ladcag functions with the norm

Theorem 4.1 (Inverse map).

Let be a continuously differentiable function and a distribution function on (an interval of) that has at most finitely many jumps and is otherwise continuously differentiable with strictly positive density . Then, the map , , is Hadamard differentiable at tangentially to the set of all continuous functions in . The derivative is given by

The main conclusion of this section is summarized as follows.

Proposition 4.2.

Let be a continuously differentiable function. For a distribution function on (an interval of) that has at most finitely many jumps and is otherwise continuously differentiable with strictly positive density such that , the process converges weakly in to a Gaussian process with mean zero and covariance .

5 Convergence of -statistics

We seek conditions under which the integral of a stochastic process with respect to another stochastic process converges weakly. This is an extension of Wilcoxon statistics [17, Section 3.9.4.1] that allows unbounded integrands.

Theorem 5.1 (Wilcoxon statistic).

For each fixed , the maps and , and are Hadamard differentiable at every uniformly over . The derivative maps are and where is defined via integration by parts if is of unbounded variation.

Now we are ready to give the main conclusion of this paper.

Proposition 5.2 (-statistic).

Let be continuously differentiable functions and be a distribution function on (a rectangular of) with marginal distributions that have at most finitely many jumps and are otherwise continuously differentiable with strictly positive marginal densities such that and , , have th moments for some . Along with i.i.d. random variables and , let and be random variables bounded by whose distribution can depend on , , and such that the empirical distributions of , , , and converge uniformly jointly to continuously differentiable functions. Then,

where and converge weakly in to a normal vector with mean zero and (co)variance

where and . If has no jumps, this equals

where and . If and are known, this can be consistently estimated by its sample analogue

where and .

6 Convergence of Bootstrap Processes

We establish validity of nonparametric bootstrap, viz., conditional weak convergence of the bootstrap processes. The bootstrap process for is given by

where is the number of times is drawn in the bootstrap sample. We show that converges weakly to the same limit as conditional on . As in [17, Chapter 3.6], we proceed as follows: since sums up to , it is slightly dependent on each other; we replace with independent Poisson random variables by showing equivalence of weak convergence of and of the multiplier process (Lemma 7.7); then, we prove unconditional convergence of (randomness comes from both and ) by symmetrization (Lemma 7.8); finally, we show convergence of conditional on (randomness only comes from ) by discretizing (Lemma 6.1). We observe that many proofs in [17, Chapters 2.9, 3.6, and A.1] carry over to , so we will not reproduce the entire argument but prove steps that require modification.

In addition, we establish conditional weak convergence of the bootstrap process for . We restrict attention to sample adjustments by quantiles and write its bootstrap process in terms of empirical processes (Lemma 6.2).

The following shows conditional convergence of as in [17, Theorem 2.9.6]. Other lemmas are given in Section 7.4.

Lemma 6.1.

Let be i.i.d. random variables with mean , variance , and , independent of . For a probability distribution on such that , the process satisfies in outer probability, and the sequence is asymptotically measurable.

These results show that nonparametric bootstrap works for and . We also show validity for by representing as a function of “” and “” in Proposition 3.5.

Lemma 6.2.

Let be independent uniformly distributed random variables on and be i.i.d. random variables with mean , variance , and , independent of . Define the bootstrap empirical process of by and let be the indicator of whether is above the -quantile of the bootstrap sample, that is, . Define Then, for and ,

in outer probability, and and are asymptotically measurable.

Altogether, nonparametric bootstrap works for -statistics when sample adjustment is based on empirical quantiles.

Proposition 6.3 (Validity of nonparametric bootstrap).

In addition to assumptions in LABEL:{EkaRgpsiHieiNgk4NFP}, assume that represents sample adjustments based on a finite number of fixed quantiles.666The assumption on convergence must be extended to jointly over all processes. Then, the joint distribution of can be consistently estimated by nonparametric bootstrap.

7 Proofs

7.1 Convergence of Bounded Integrable Processes

Proof of Proposition 3.1.

Marginal convergence is trivial. By [17, Example 2.5.4], converges weakly in . In light of [17, Proposition 2.1.11] and Lemma .10, it suffices to show that for , (i) and (ii) (ii) follows since . Let and . Note that (ii) implies that has variance. Writing , we find The second term is a finite constant if (ii) holds. Thus, (i) holds if , which is the case if has variance. Thus, converges weakly in . ∎

Lemma 7.1.

If is asymptotically tight, it is asymptotically measurable if and only if is asymptotically measurable for every .

Lemma 7.2.

If and are tight Borel measurable maps into , then and are equal in law if and only if every marginal of and is equal in law.

Proofs of Lemmas 7.1 and 7.2.

These claims are not corollaries of [17, Lemmas 1.5.2 and 1.5.3] since is bigger than and , but they follow by the same logic. ∎

Proof of Theorem 3.2.

Necessity is immediate. We prove sufficiency. If is asymptotically tight and its marginals converge weakly, then is asymptotically measurable by Lemma 7.1. By Prohorov’s theorem [17, Theorem 1.3.9], is relatively compact. Take any subnet in that is convergent. Its limit point is unique by Lemma 7.2 and the assumption that every marginal converges weakly. Thus, converges weakly. The last statement is another consequence of Prohorov’s theorem. ∎

Proof of Theorem 3.3.

(ii) (i). Fix . Pick one from each . Then, with inner probability at least . Since the maximum of finitely many tight nets of real variables is tight and is assumed to be tight, it follows that the net is asymptotically tight in .

Fix and take . Let satisfy . Taking in (3.1) as , we obtain for each a measurable partition (suppressing dependence on ). For each , enumerate all of the finitely many values such that

Since is not necessarily finite on the whole , on some partition the only choice of may be . Let be the finite exhaustion of all functions in that are constant on each and take values on

Let be the union of closed balls of radius around each . Then, since , the three conditions and imply that . This holds for each .

Let , which is closed, totally bounded, and therefore compact. Moreover, we argue that for every there exists with . Suppose not. Then there is a sequence not in , but with for every . This has a subsequence contained in only one of the closed balls constituting , and a further subsequence contained in only one of the balls constituting , and so on. The diagonal sequence of such subsequences would eventually be contained in a ball of radius for every . Therefore, it is Cauchy and its limit should be in , which is a contradiction to the supposition for every .

Thus, if is not in , it is not in for some . Therefore,

Hence, we obtain , as asserted.

(i) (iii). If is asymptotically tight, then so is each coordinate projection. Therefore, is asymptotically tight in for every .

Let be a sequence of compact sets such that for every . Define a semimetric on induced by by Observe that and that is measurable with respect to .777 is not necessarily complete with respect to . Now for every , define a semimetric on by We argue that is totally bounded. For , cover by finitely many balls of radius centered at . Consider the partition of into cubes of edge length . For each cube, if there exists such that the following -tuple is in the cube,

then pick one such . Since is finite for every (i.e., the diameter of measured by each is finite), this gives finitely many points . Notice that the balls cover , that is, is in the ball around for which and are in the same cube; this follows because can be bounded by The first term is the error of approximating and by and ; the second is the distance of and measured by .

Define the semimetric by We show that is still totally bounded. For take such that . Since is totally bounded in , we may cover with finitely many -balls of radius . Denote by the centers of such a cover. Since is nested, we have . Since we also have , for every there exists such that . Therefore, is totally bounded.

By definition we have for every and . And if for , then for every pair . Hence, we conclude Therefore, for ,

(iii) (ii). For , take as given. Since is totally bounded, it can be covered with finitely many balls of radius ; let be their centers. Disjointify the balls to obtain . If , then separate the partition into and .

There are three types of components in the partition: (a) singleton components (mass points) of , (b) components with , and (c) components with . The size of (a) is controlled by construction, so we control (b) and (c). Clearly,

| (7.1) |

Denote by the index for which . Now we argue that can be arbitrarily small (with inner probability at least ) for sufficiently small . By construction, .888This follows because given that . Thus, . Since is totally bounded, is bounded by with inner probability at least (proving asymptotic tightness of ), and hence the previous integral must be arbitrarily small for small . Now we turn to (c). Let be such that

| (7.2) |

For each with , construct a further partition of it with this . Note that defines another finite partition of . If there exists such that , then by construction . The contrapositive of this is also true. Thus, observing we may assume at the cost of one more . Then, we also have since . For the partition of , further construct a nested finite partition . Now

with inner probability at least . This, (7.1), and (7.2) yield the result. ∎

Proof of Lemma 3.4.

We first work on the case . Define We show that is totally bounded with respect to . Observe that Lemma .9 (v) and imply as . Therefore, integrating by parts,

Since and for every , in particular for , this integral is finite by Hölder’s inequality. This means the diameter of is finite, so is totally bounded.

Note that is eventually smaller than near and , so that for every there exists such that

This shows uniform equicontinuity. Next, for every ,

Therefore,

By assumption, this can be however small by the choice of . Conclude that is asymptotically -equiintegrable in probability.

Finally, for , replace every by . Then the result follows since . ∎

Proof of Proposition 3.5.

Assume without loss of generality . Define . Let and be the continuous linear interpolations of and , that is, for , and and for , and . Observe that . By Lemma 7.3 it suffices to show that and converge weakly jointly in . Note that and for . Thus, converges weakly in if and only if does, and they share the same limit. The same is true for and .

The classical results imply that converges weakly in to a Brownian bridge and for every [10]. By Lemmas 3.4 and 3.3, it follows that converges weakly in . By assumption converges weakly in jointly with , and since , conclude that converges weakly in jointly with . ∎

Lemma 7.3 (Inverse composition map).

Let contain the identity map . Let be the subset of such that every satisfies for every , the range of contains , and is differentiable and Lipschitz. Let be the subset of of uniformly continuous functions. Then, the map , , is Hadamard differentiable at for tangentially to . The derivative is given by for

Proof.

For and , denote and . By assumption we have for every . Therefore, is monotone and bounded by the identity map up to a constant. This implies and ; it follows that is in .

Let and in and . We want to show as . That follows by applying [17, Lemma 3.9.27] to as elements in . Thus, it remains to show . In the assumed inequality, substitute by to find that Therefore, the following inequality holds pointwise: For , write as For any fixed the middle term vanishes as since . It remains to show that the first term can be arbitrarily small since then by symmetry the third term is also ignorable. Using the above inequality, write Since and , this integral can be arbitrarily small by the choice of , as desired. ∎

7.2 Convergence of Quantile Processes as Integrable Processes

If is an identity, we denote and by and , and by .

We first establish differentiability of the inverse map for distribution functions with finite first moments.

Lemma 7.4 (Inverse map).

Let be a distribution function on (an interval of) that has at most finitely many jumps and is otherwise continuously differentiable with strictly positive density . Then, the inverse map , , is Hadamard differentiable at tangentially to the set of all continuous functions in . The derivative is

Proof of Lemma 7.4.

Take in and . We want to show as . Let be a point of jump of . For small , split the integral as

Observe that the second integral is bounded by

The first term of this equals and can be arbitrarily small by the choice of . If is small enough that there is no other jump in , by Fubini’s theorem, which can be, again, arbitrarily small. Similarly for the last integral. Therefore, we ignore finitely many jumps of so that everywhere.

For there exists such that and . Write

By [17, Theorem 3.9.23 (i)], the integrand vanishes uniformly on . As the first integral is bounded by it vanishes as . Now turn to the second integral. The triangle inequality bounds it by Since and are nondecreasing, by Fubini’s theorem,

The first term goes to and the second term can be arbitrarily small by the choice of . Finally, by the change of variables, which can be arbitrarily small. Likewise, the integral from to converges to . This completes the proof. ∎

Now we allow transformations of locally bounded variation. A function of locally bounded variation admits decomposition into the difference of two monotone functions. Then, we exploit the relationship for a monotone and use the chain rule.

Proof of Theorem 4.1.

Since is of locally bounded variation, write where and are increasing. Moreover, and can be chosen to be continuously differentiable and strictly increasing, and for their corresponding Lebesgue-Stieltjes measures and , belongs to both and . Since the derivative formula is linear in , it suffices to show the claim for and separately. Now observe that is in (or ) if and only if is in (or ). The assertion then follows by [17, Lemma 3.9.3] applied to Lemmas 7.4 and 7.5. ∎

Lemma 7.5.

Let be a strictly increasing continuous function and be the associated Lebesgue-Stieltjes measure. Then, the map , , is uniformly Fréchet differentiable with rate function .999A map is uniformly Fréchet differentiable with rate function if there exists a continuous linear map such that uniformly over as and is monotone with . The derivative is given by .

Proof of Lemma 7.5.

Observe that . Therefore, . ∎

Proof of Proposition 4.2.

This follows from Propositions 3.1 and 4.1. ∎

7.3 Convergence of -statistics

Proof of Theorem 5.1.

The derivative map is linear by construction; it is also continuous since which vanishes as and . Let and such that is in and is in . Observe

The first term vanishes since As is integrable, for every there exists a small number such that This gives

Let . Since is ladcag on , there exists a partition such that varies less than on each interval . Let be the piecewise constant function that equals on each interval . Then

The first term is arbitrarily small by the choice of , and the second and third terms are collectively bounded by , which converges to regardless of the choice of .

The proof for is basically the same. ∎

Proof of Proposition 5.2.

Weak convergence follows from Propositions 4.2, 3.5 and 5.1. The derivative formulas give us

Consistency of the sample analogue estimator follows from uniform convergence of and and Lemma 7.6. ∎

Lemma 7.6.

Let be a ladcag increasing function. For a probability measure on such that , , we have

where the suprema are each taken over , , and .

Proof of Lemma 7.6.

We assume without loss of generality. In view of [17, Theorem 2.4.1], the first two claims follow if

have finite bracketing numbers with respect to . For take such that for each and consider the brackets .101010If has a probability mass at , then for small take, instead of , for appropriately chosen . This partition is finite by Lemma .9 and . For take such that for each and consider the brackets for every pair .111111Again, if has a mass, similar adjustments are needed. This partition is finite by .

For the third claim, observe that Then the claim follows by the first two claims and the triangle inequality, 121212Measurability of the sup on the LHS follows by the continuity of Lebesgue integrals.

For the last claim, observe that Lemma .9 and the preceding claim imply that for there exists such that with probability tending to . By the triangle inequality, Then the assertion follows by the Glivenko-Cantelli theorem. ∎

7.4 Validity of Nonparametric Bootstrap

We start with the key lemma in Poissonization, the counterpart of [17, Lemma 3.6.16].

Lemma 7.7.

For each , let be an exchangeable nonnegative random vector independent of such that and converges to zero in probability. Let be a probability distribution on such that . Then, for every , as ,

Proof of Lemma 7.7.

Assume without loss of generality that is a positive measure and let for and for . Since [17, Lemma 3.6.7] goes through with , the proof of this lemma is almost identical to [17, Lemma 3.6.16]. Essentially, the only part that requires modification is boundedness of (). Note that Therefore, Find that which converges almost surely to . ∎

Given this, we infer as in [17, Theorem 3.6.1] that conditional weak convergence of follows from conditional weak convergence of . For the latter, we first need to show unconditional convergence of in our norm. The following is a modification of [17, Theorem 2.9.2].

Lemma 7.8.

Let be i.i.d. random variables with mean zero, variance , and , independent of . For a probability distribution on such that has a th moment for and some , the process converges weakly to a tight limit process in if and only if does. In that case, they share the same limit processes.

Proof of Lemma 7.8.

Marginal convergence and asymptotic equicontinuity of follow from Proposition 3.1 and [17, Theorem 2.9.2]. It remains to show the equivalence of asymptotic equiintegrability of and .

Note that the proofs of [17, Lemmas 2.3.1, 2.3.6, and 2.9.1 and Propositions A.1.4 and A.1.5] do not depend on the specificity of the norm , but they continue to hold with . Given this, [17, Lemma 2.3.11] also holds with (and ). Finally, rewriting the proof of [17, Theorem 2.9.2] in terms of yields the proof of this lemma. ∎

Proof of Lemma 6.1.

By Lemma 7.8, is asymptotically measurable. Define a semimetric on by For , be such that , , and . Define by

Define analogously. By the continuity and integrability of the limit process , we have in almost surely as . Therefore, as Second, by [17, Lemma 2.9.5], as for almost every sequence and fixed . Since and take only on a finite number of values and their tail values are zero, one can replace the supremum over with a supremum over . Observe that is separable with respect to the topology of uniform convergence on compact sets; this supremum is effectively over a countable set, hence measurable. Third, This implies that its outer expectation is bounded by , which vanishes as by the modified [17, Lemma 2.9.1] as discussed in Lemma 7.8. ∎

Proof of Lemma 6.2.

Proof of Proposition 6.3.

With the remark below Lemma 7.7, the proposition follows from Lemmas 6.1 and 6.2 and [17, Theorem 3.9.11]. ∎

Appendix

.5 Supporting Lemmas

Lemma .9.

Proof.

(i) (iv). For , Since the left-hand side (LHS) is finite, one may take large enough that is arbitrarily small, which then bounds the two nonnegative terms. Hence as .

(iii) (iv). Suppose that is integrable but does not vanish as , that is, there exist a constant and a sequence such that . Since , one may take a subsequence such that By monotonicity of , a contradiction. Hence vanishes. Similarly , as .

Lemma .10.

Let and be metrics on . Then, converges weakly in and in to a limit that is tight in and in if and only if converges weakly in to a limit that is tight in .

Proof.

When we consider in metrics , , and , we denote them respectively by , , and . Sufficiency is trivial. Necessity is nontrivial since is bigger than and in [17, Definition 1.3.3]. Note that the algebra generated by separates points of . Therefore, in light of [17, Lemma 1.3.13], it suffices to show that tightness in and in implies tightness in .

Fix . Let and be sets compact under and respectively such that and . Then, . Now we show is totally bounded under . Take and to be finitely many points such that --balls of cover and --balls of cover . Then choose a total of at most points from each intersection of a -ball and an -ball, , and consider --balls around them. Since every point in belongs to at least one intersection of a -ball and an -ball, these balls cover by the triangle inequality. Therefore, is totally bounded, so its closure in is compact in . Since , is tight in . ∎

.6 Application to Outlier Robustness Analysis

We construct a statistical test of outlier robustness analysis. Recall our setup from Example 1 and consider the null hypothesis for fixed . We assume that is a scalar while can be a vector, in which case is the Mahalanobis distance between and , that is, where is either an identity, the covariance matrix of , or some other positive definite symmetric matrix. The natural test statistic to use is ( may be estimated consistently). Let be the size of the test. Our results imply that the variance of the difference can be estimated either by the analytic formula or by the bootstrap. Note that if , the null hypothesis is composite. The critical value satisfies for . If is a scalar, it reduces to for .

We reinvestigate the outlier robustness analysis in [3]. They tackle the long-standing question of whether and how democracy affects economic growth. They find that after 25 years from permanent democratization, GDP per capita is about 20% higher than without democratization, and check robustness of their results to outliers of the error term. We revisit their fixed effects regressions and conduct the outlier robustness tests proposed above.

The first-stage equation is

where is the instrumental variable (IV) constructed from the democracy indicators of nearby countries that share similar political history to country . The panel data is unbalanced; each country has a varying number of observations. Let be the year of country ’s first appearance in the sample and be the number of observations country has. Then, ’s time array spans .

In addition to regression coefficients, [3] report three parameters. The long-run effect of democracy, , represents the impact on of the transition from non-democracy to permanent democracy for every . The effect of transition to democracy after 25 years, where and , represents the impact on of the transition from to for . Persistence of the GDP process, , represents how persistently a unit change in remains.

To check robustness to outliers, [3] carry out same regression excluding observations that have large residuals. For notational convenience, let

Outliers are defined by , where is the estimated homoskedastic standard error of ,131313The purpose of is normalization. [3] do use heteroskedasticity-robust standard errors for inference. and, for the IV model, also by , where This means that they are concerned with whether tail observations of the GDP might have disproportionate effects on estimates. Defining outliers based on , not , even if they are interested in the effects of outliers of the GDP, is reasonable since sample selection based on does not affect the true parameters under some conditions while selection on certainly does.

Let be the vector of empirical distribution functions of and the vector of marginal empirical quantile functions of . Note that, with , the full-sample and outlier-removed OLS estimators are

where is the vector of measures whose th element assigns density

Assume that has smooth cdfs with th moments for some and has a well-defined limit. Then, our results imply that the joint distribution of and converges and can be estimated by nonparametric bootstrap. Similar arguments apply also to the IV estimators.

In a simple case where and are independent of covariates, outlier removal will not change the true coefficients. So, it seems sensible to set , the most conservative choice. Thus, we test the hypothesis .

We carry out nonparametric bootstrap across . All fixed effects are replaced by dummy variables. Each draw of country adds observations to the bootstrap sample; equivalently, we treat each sum, , , and , as one observation in order to exploit the i.i.d. structure. Bootstrap runs for 10,000 iterations, in each of which we draw 175 countries for OLS and 174 for IV with replacement.

| Estimate | -value for | ||||||||||||

| OLS | IV | OLS | IV | ||||||||||

| Notation | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | |||||

| Democracy | 0.79 | 0.56 | 1.15 | 0.66 | 0.15 | 0.32 | 0.20 | 0.41 | |||||

| (0.23) | (0.20) | (0.59) | (0.44) | ||||||||||

| log GDP first lag | 1.24 | 1.23 | 1.24 | 1.23 | 0.60 | 0.74 | 0.70 | 0.82 | |||||

| (0.04) | (0.02) | (0.04) | (0.03) | ||||||||||

| log GDP second lag | 0.21 | 0.20 | 0.21 | 0.20 | 0.75 | 0.85 | 0.84 | 0.91 | |||||

| (0.05) | (0.03) | (0.05) | (0.04) | ||||||||||

| log GDP third lag | 0.03 | 0.03 | 0.03 | 0.03 | 0.97 | 0.98 | 0.89 | 0.93 | |||||

| (0.03) | (0.02) | (0.03) | (0.03) | ||||||||||

| log GDP fourth lag | 0.04 | 0.03 | 0.04 | 0.03 | 0.26 | 0.45 | 0.28 | 0.46 | |||||

| (0.02) | (0.01) | (0.02) | (0.02) | ||||||||||

| Long-run effect of democracy | 21.24 | 19.32 | 31.52 | 22.63 | 0.72 | 0.79 | 0.46 | 0.63 | |||||

| (7.32) | (8.54) | (18.49) | (18.14) | ||||||||||

| Effect of democracy after 25 years | 16.90 | 13.00 | 24.87 | 15.47 | 0.29 | 0.46 | 0.27 | 0.49 | |||||

| (5.32) | (5.02) | (13.53) | (10.82) | ||||||||||

| Persistence of GDP process | 0.96 | 0.97 | 0.96 | 0.00 | 0.12 | 0.00 | 0.20 | ||||||

| (0.01) | 0.00 | (0.01) | 0.00 | ||||||||||

| Number of observations | 6,336 | 6,044 | 6,309 | 5,579 | |||||||||

| Number of countries | 175 | 175 | 174 | 174 | |||||||||

| Average number of years | 36.2 | 34.5 | 36.3 | 32.1 | |||||||||

* (1,3) Baseline estimates; (2) Estimates with ; (4) Estimates with and ; (5,7) -values of the formal tests that use the standard errors of ; (6,8) “-values” of the heuristic tests that use the marginal standard errors of . Some numbers in Columns (1,2) differ from [3] since we use our own bootstrap to compute standard errors.

Most of our reexamination reconfirms robustness to outliers even though we set . The exception is persistence of the GDP process, of which we reject the hypothesis of no change. Table 1 lists the estimates and the -values for our tests. Column 1 is the baseline OLS estimates and column 2 is OLS excluding . Column 3 is the baseline IV estimates and column 4 is IV excluding observations satisfying either or . Columns 5 to 8 illustrate the utility of our formal tests of outlier robustness. Column 5 gives the -values of the hypotheses that the two OLS coefficients are identical, using the standard error of the difference of two estimators estimated by bootstrap. Column 6 gives the “-values” of the same hypotheses, but heuristically using the standard error of the marginal distribution of the baseline OLS estimates. Columns 7 and 8 are the corresponding -values for IV coefficients. The identity of persistence of the GDP process is rejected in formal tests while accepted in heuristic tests at 5%. We note that the magnitudes of persistence are very close (0.96 and 0.97), so if we allow bias of, say, , the hypothesis will not be rejected.

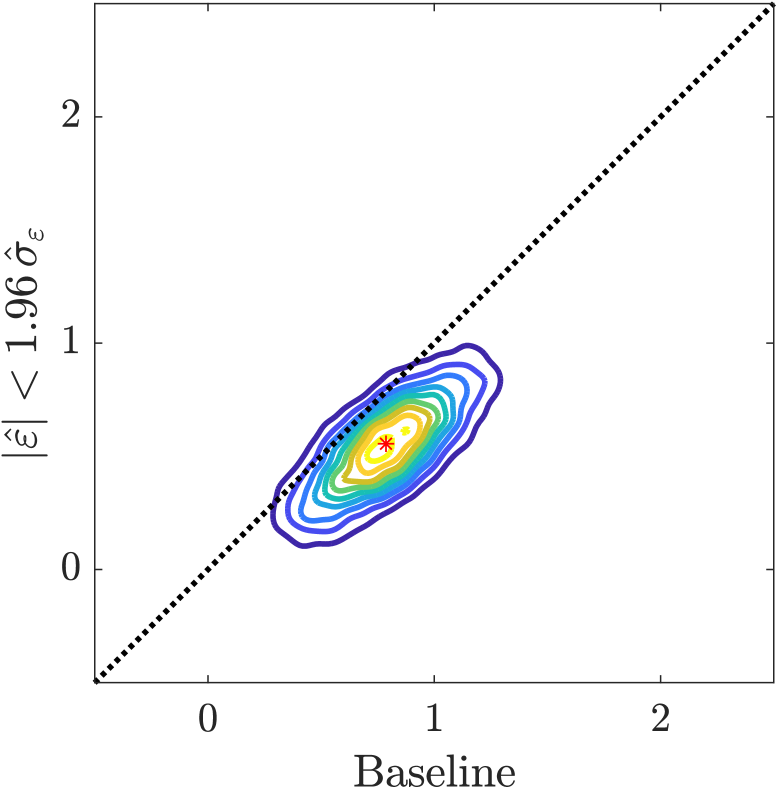

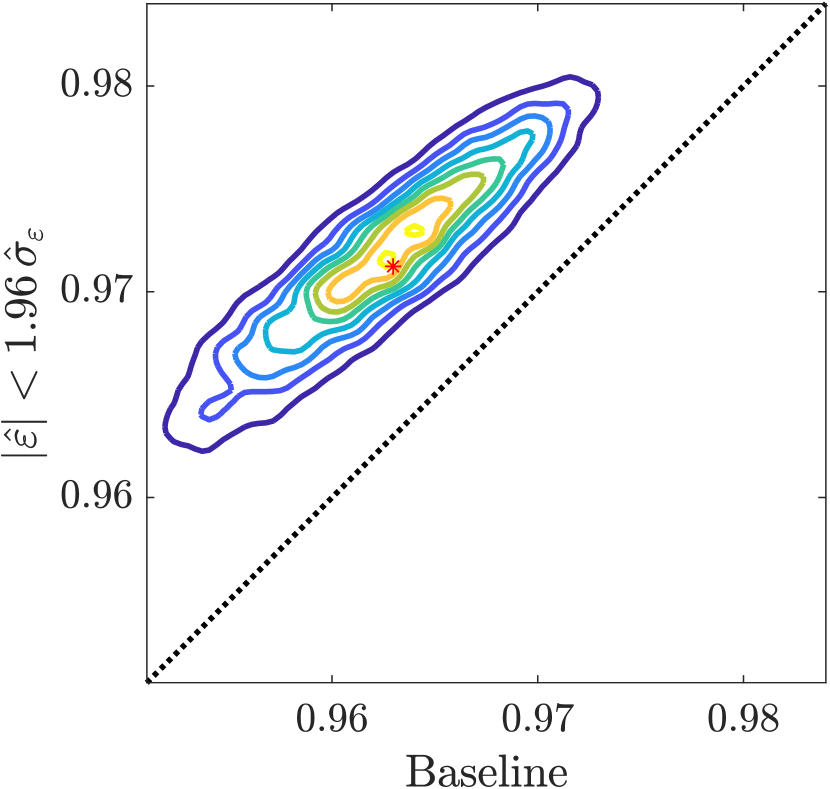

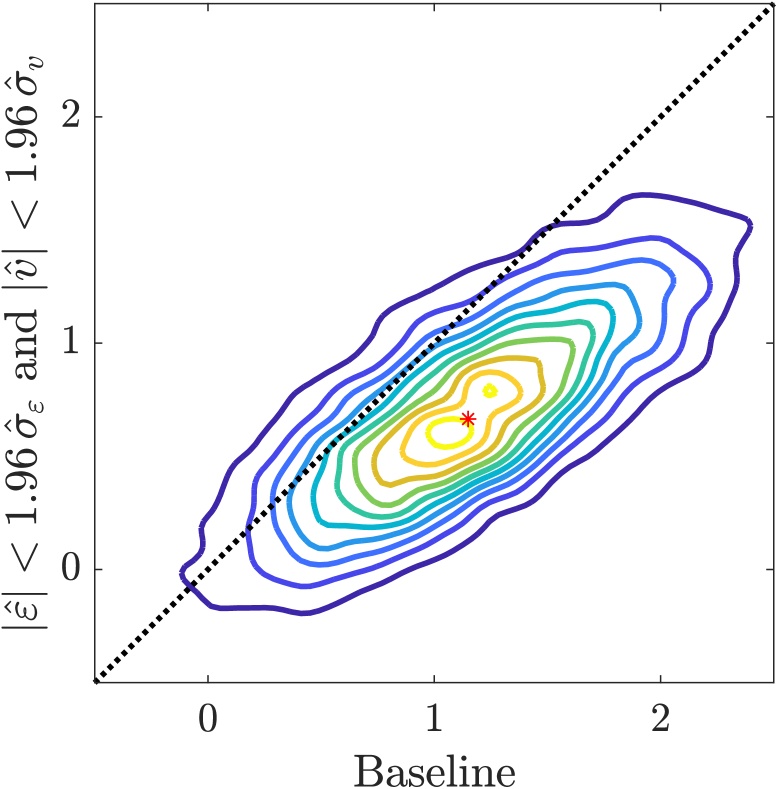

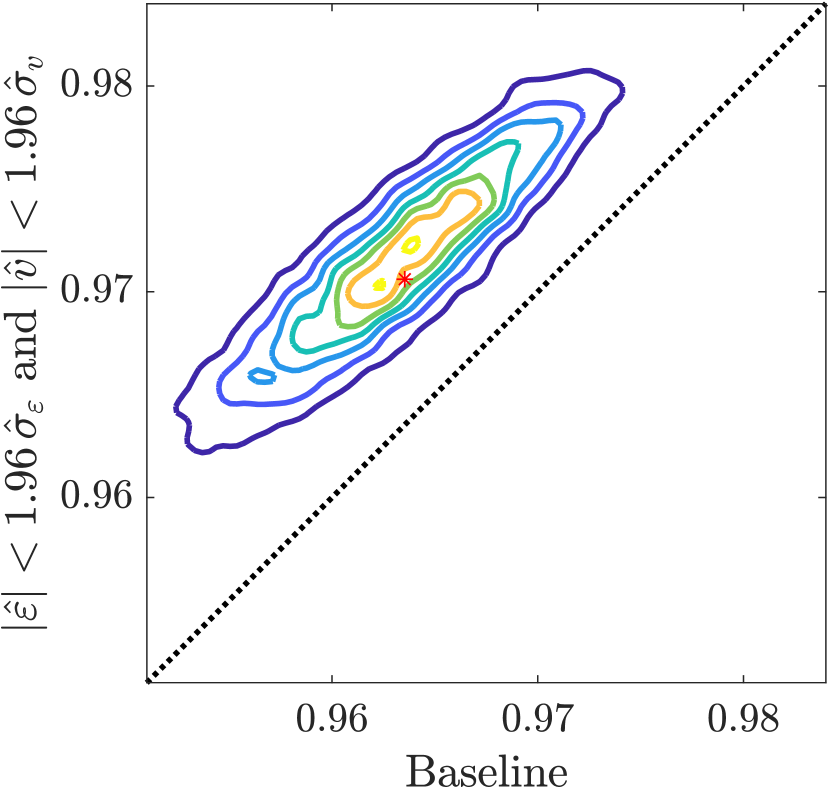

Positive correlation of baseline and outlier-removed estimators is visualized by the bootstrap distributions. Figures 1(a) and 1(b) illustrate the joint distributions of baseline and outlier-removed OLS estimators, and . Figures 1(c) and 1(d) are the corresponding figures for IV. The contour plots are based on the kernel density estimators of the bootstrap distributions. The estimators are positively correlated as anticipated by the fact that they share much of the samples. Graphically, the tests examine if the red stars (estimators) are close to the 45 degree lines (black dotted lines).

Acknowledgements

I thank Anna Mikusheva, Elena Manresa, Kengo Kato, Rachael Meager, Matthew Masten, Abhijit Banerjee, Daron Acemoglu, Isaiah Andrews, Hideatsu Tsukahara, Hidehiko Ichimura, Victor Chernozhukov, Jerry Hausman, Whitney Newey, Alberto Abadie, Joshua Angrist, and Brendan K. Beare for helpful comments. Daron Acemoglu and Pascual Restrepo kindly shared data and codes of their paper. This work is supported by the Richard N. Rosett Faculty Fellowship and the Liew Family Faculty Fellowship at the University of Chicago Booth School of Business.

References

- [1] {barticle}[author] \bauthor\bsnmAcemoglu, \bfnmDaron\binitsD., \bauthor\bsnmJohnson, \bfnmSimon\binitsS., \bauthor\bsnmKermani, \bfnmAmir\binitsA., \bauthor\bsnmKwak, \bfnmJames\binitsJ. and \bauthor\bsnmMitton, \bfnmTodd\binitsT. (\byear2016). \btitleThe Value of Connections in Turbulent Times: Evidence from the United States. \bjournalJ. Financ. Econ. \bvolume121 \bpages368–391. \endbibitem

- [2] {barticle}[author] \bauthor\bsnmAcemoglu, \bfnmDaron\binitsD., \bauthor\bsnmJohnson, \bfnmSimon\binitsS. and \bauthor\bsnmRobinson, \bfnmJames A.\binitsJ. A. (\byear2001). \btitleThe Colonial Origins of Comparative Development: An Empirical Investigation. \bjournalAmer. Econ. Rev. \bvolume91 \bpages1369–1401. \endbibitem

- [3] {barticle}[author] \bauthor\bsnmAcemoglu, \bfnmDaron\binitsD., \bauthor\bsnmNaidu, \bfnmSuresh\binitsS., \bauthor\bsnmRestrepo, \bfnmPascual\binitsP. and \bauthor\bsnmRobinson, \bfnmJames A.\binitsJ. A. (\byear2019). \btitleDemocracy Does Cause Growth. \bjournalJ. Pol. Econ. \bvolume127 \bpages47–100. \endbibitem

- [4] {barticle}[author] \bauthor\bsnmAgarwal, \bfnmNikhil\binitsN., \bauthor\bsnmBanternghansa, \bfnmChanont\binitsC. and \bauthor\bsnmBui, \bfnmLinda T. M.\binitsL. T. M. (\byear2010). \btitleToxic Exposure in America: Estimating Fetal and Infant Health Outcomes from 14 Years of TRI Reporting. \bjournalJ. Health Econ. \bvolume29 \bpages557–574. \endbibitem

- [5] {bunpublished}[author] \bauthor\bsnmBanerjee, \bfnmAbhijit\binitsA., \bauthor\bsnmDuflo, \bfnmEsther\binitsE. and \bauthor\bsnmHornbeck, \bfnmRichard\binitsR. (\byear2014). \btitle(Measured) Profit is Not Welfare: Evidence from an Experiment on Bundling Microcredit and Insurance. \bnoteCEPR Discussion Papers 10146. \endbibitem

- [6] {barticle}[author] \bauthor\bparticledel \bsnmBarrio, \bfnmEustasio\binitsE., \bauthor\bsnmGiné, \bfnmEvarist\binitsE. and \bauthor\bsnmMatrán, \bfnmCarlos\binitsC. (\byear1999). \btitleCentral Limit Theorems for the Wasserstein Distance between the Empirical and the True Distributions. \bjournalAnn. Probab. \bvolume27 \bpages1009–1071. \endbibitem

- [7] {barticle}[author] \bauthor\bsnmFabrizio, \bfnmKira R.\binitsK. R., \bauthor\bsnmRose, \bfnmNancy L.\binitsN. L. and \bauthor\bsnmWolfram, \bfnmCatherine D.\binitsC. D. (\byear2007). \btitleDo Markets Reduce Costs? Assessing the Impact of Regulatory Restructuring on US Electric Generation Efficiency. \bjournalAmer. Econ. Rev. \bvolume97 \bpages1250–1277. \endbibitem

- [8] {bbook}[author] \bauthor\bsnmKoul, \bfnmHira Lal\binitsH. L. (\byear2002). \btitleWeighted Empirical Processes in Dynamic Nonlinear Models, \beditionSecond ed. \bpublisherSpringer, \baddressNew York. \endbibitem

- [9] {barticle}[author] \bauthor\bsnmMason, \bfnmDavid M.\binitsD. M. and \bauthor\bsnmShorack, \bfnmGalen R.\binitsG. R. (\byear1992). \btitleNecessary and Sufficient Conditions for Asymptotic Normality of -Statistics. \bjournalAnn. Probab. \bvolume20 \bpages1779–1804. \endbibitem

- [10] {bbook}[author] \bauthor\bsnmCsörgő, \bfnmMiklós\binitsM. and \bauthor\bsnmHorváth, \bfnmLajos\binitsL. (\byear1993). \btitleWeighted Approximations in Probability and Statistics. \bpublisherJohn Wiley & Sons Ltd, \baddressChichester. \endbibitem

- [11] {barticle}[author] \bauthor\bsnmCsörgő, \bfnmMiklós\binitsM., \bauthor\bsnmHorváth, \bfnmLajos\binitsL. and \bauthor\bsnmShao, \bfnmQi-Man\binitsQ.-M. (\byear1993). \btitleConvergence of Integrals of Uniform Empirical and Quantile Processes. \bjournalStochastic Processes and their Applications \bvolume45 \bpages283–294. \endbibitem

- [12] {barticle}[author] \bauthor\bsnmCsörgő, \bfnmMiklós\binitsM., \bauthor\bsnmCsörgő, \bfnmSándor\binitsS., \bauthor\bsnmHorváth, \bfnmLajos\binitsL. and \bauthor\bsnmMason, \bfnmDavid M.\binitsD. M. (\byear1986). \btitleWeighted Empirical and Quantile Processes. \bjournalAnn. Probab. \bvolume14 \bpages31–85. \endbibitem

- [13] {barticle}[author] \bauthor\bsnmShorack, \bfnmGalen R.\binitsG. R. (\byear1997). \btitleUniform CLT, WLLN, LIL and Bootstrapping in a Data Analytic Approach to Trimmed -Statistics. \bjournalJ. Statist. Plann. Inference \bvolume60 \bpages1–44. \endbibitem

- [14] {bbook}[author] \bauthor\bsnmShorack, \bfnmGalen R.\binitsG. R. (\byear2017). \btitleProbability for Statisticians, \beditionSecond ed. \bpublisherSpringer-Verlag, \baddressNew York. \endbibitem

- [15] {bbook}[author] \bauthor\bsnmShorack, \bfnmGalen R.\binitsG. R. and \bauthor\bsnmWellner, \bfnmJon A.\binitsJ. A. (\byear1986). \btitleEmpirical Processes with Applications to Statistics. \bpublisherJohn Wiley & Sons, Inc., \baddressNew York. \endbibitem

- [16] {bbook}[author] \bauthor\bparticlevan der \bsnmVaart, \bfnmAad W.\binitsA. W. (\byear1998). \btitleAsymptotic Statistics. \bpublisherCambridge University Press, \baddressCambridge. \endbibitem

- [17] {bbook}[author] \bauthor\bparticlevan der \bsnmVaart, \bfnmAad W.\binitsA. W. and \bauthor\bsnmWellner, \bfnmJon A.\binitsJ. A. (\byear1996). \btitleWeak Convergence and Empirical Processes: With Applications to Statistics. \bpublisherSpringer, \baddressNew York. \endbibitem