Portfolio Optimization with Expectile and Omega Functions

Abstract.

This paper proves equivalences of portfolio optimization problems with negative expectile and omega ratio. We derive subgradients for the negative expectile as a function of the portfolio from a known dual representation of expectile and general theory about subgradients of risk measures. We also give an elementary derivation of the gradient of negative expectile under some assumptions and provide an example where negative expectile is demonstrably not differentiable. We conducted a case study and solved portfolio optimization problems with negative expectile objective and constraint.

©2019 IEEE. Personal use of this material is permitted. Permission from IEEE must be obtained for all other uses, in any current or future media, including reprinting/republishing this material for advertising or promotional purposes, creating new collective works, for resale or redistribution to servers or lists, or reuse of any copyrighted component of this work in other works.

1. Introduction

In this paper, portfolio optimization is the task of maximizing the expected return of a portfolio subject to the risk of the portfolio not exceeding a prespecified level. Formally, let be a vector containing random variables representing the returns of financial instruments. Let . The random return of the portfolio is given by . The decision variable represents position being invested in the -th instrument. Let us denote the risk measure of interest by . We investigate two single-stage stochastic optimization problems,

where is a convex set of feasible portfolios.

This paper considers two closely related risk measures, negative expectile and omega. Expectiles are asymmetric generalizations of expected value introduced by \citeNnewey1987asymmetric and defined by (3). When , negative level- expectiles satisfy the conditions of a coherent risk measure in the sense of \shortciteNartzner1999coherent. Section 4 of this paper shows that for the level- negative expectile is strictly expectation bounded (i.e. averse) as defined by \shortciteNrockafellar2006generalized. Moreover, negative expectile is elicitable, that is there exists a consistent way of comparing the quality of procedures that predict its value [\citeauthoryearZiegelZiegel2016]. Indeed, \shortciteNBellini2019 have suggested a procedure for testing the accuracy of an expectile forecasting model. A conditional version of expectile naturally generalizing conditional expectation has also been developed \shortciteBELLINI2018117.

In addition to this list of desirable theoretical properties, \citeNbellini2017risk offer the following intuitive motivation for the use of negative expectile as a measure of risk for portfolio optimization. Value at risk is a commonly used risk measure and can be given by (1) employing the concept of acceptance sets. The same reformulation can be given to negative expectile as in (2).

| (1) | |||

| (2) |

So if VaR represents the smallest amount we need to add to the random return such that the probability of a gain is times greater than the probability of a loss, then negative expectile represents the smallest amount we need to add such that the expected gains are times greater than the expected losses.

Property (2) of the negative expectile has a clear relationship to the ratio of expected over-performance to expected under-performance relative to a constant benchmark . This quantity is denoted and was introduced by \citeNkeating2002universal,

Choosing portfolio weights to maximize omega is a non-convex problem \shortcitekane2009optimizing. \shortciteNmausser2006optimising reduce the omega maximization problem to a linear programming problem in the case that the optimal portfolio has an expected return exceeding the benchmark. The case study “Omega Portfolio Rebalancing” [\citeauthoryearOmega Case StudyOmega Case Study] reduces omega optimization to maximization of expected return with a convex constraint on a partial moment. This case study posted data for a test problem (provided by a mutual fund) and codes in Text, MATLAB, and R formats. In other work, \shortciteNkapsos2014optimizing show that the omega maximization problem can be reformulated equivalently as a quasi-convex optimization problem. Section 3 shows equivalence of expectile and omega portfolio optimization problems. The relation of expectile to omega has also been explored by \shortciteNBellini2018 where they define a stochastic order based on expectile and show its equivalence to the same inequality holding for omega at every benchmark.

jakobsons2016 provides three linear programming formulations for portfolio optimization with an expectile objective when asset returns have a finite, discrete distribution. In the case of a large number of scenarios, convex programming has a significant advantage compared to linear programming. While the set of constraints for linear programming may grow infeasibly large, the convex formulation need only compute a subgradient. To this end, we deduce a formula for subgradients of negative expectile in Section 4 by combining a known dual representation of expectile \shortcitebellini2014generalized and general theory about subgradients of risk measures \shortciterockafellar2006optimality. Section 6 provides numerical results with Portfolio Safeguard subroutines calculating negative expectile and subgradient in order to solve portfolio optimization problems with a convex programming approach. Section 5 provides an elementary derivation of the gradient of negative expectile as a function of the portfolio and ends with an example where the negative expectile is demonstrably not differentiable.

2. Background

This paper considers a general probability space , unless specified otherwise. In some application-focused derivations, it is noted that the space is assumed to be finite. Inequalities between random variables are meant almost surely. Expectiles are generalizations of expected value introduced by \citeNnewey1987asymmetric. Let belong to the space of random variables with finite second moment. The level- expectile of is denoted and defined according to (3), where and .

| (4) |

We take this as an alternative definition of expectile that extends to , the space of random variables with finite first moment. For calculating expectiles, it is enough to assume the existence of the first moment. We make use of the following lemma throughout the paper.

Lemma 1.

If , then is strictly decreasing in .

Proof.

If , then which implies and . If both inequalities are equalities then

This is a contradiction, so either or , from which the result follows since . ∎

We define for some fixed . \shortciteNbellini2014generalized have shown that for , satisfies the following axioms of a coherent risk measure.

-

(1)

for all and constants ,

-

(2)

, and for all and ,

-

(3)

for all ,

-

(4)

when almost surely.

In this paper, we consider , where is a vector containing random variables representing the returns of financial instruments and the decision variable represents position being invested in the -th instrument. We denote by a convex set of feasible portfolios. Section 6 presents the Case Study with

Let us denote and . We are interested in the following portfolio optimization problems,

3. Portfolio Optimization Problems with Expectile and Omega Functions

This section shows that the portfolio optimization problems with expectile and omega functions are equivalent and generate the same optimal portfolios. Expectile and omega are inverse functions in the sense of Proposition 2; see also in \shortciteBellini2018.

In this section, we restrict our attention to because in this case is a coherent, strictly expectation bounded risk measure. When , we define .

Proposition 2.

Suppose . Then

Proof.

Define .

Constraints for expectile and omega are equivalent in the following sense.

Proposition 3.

Suppose , then

Proof.

Define . We begin by showing the first set includes in the second one. If , then by translation invariance, . Suppose and . If is infinite, then . If is finite, then

Note that whether is finite or infinite,

Let be a feasible set of random variables and . Consider the following optimization problems in the space of random variables with omega and negative expectile constraints.

The following corollary shows that problems and with expectile and omega constraints are equivalent.

Corollary 4.

Suppose , and there exists such that . Then the problems and are equivalent, i.e. their optimal solution sets and objective values coincide.

Proof.

implies that , which in turn implies . By Proposition 3, implies . Hence, for both optimization problems in question, the optimal objective value is strictly larger than and replacing with does not affect the optimal solution sets or objective values. The corollary now follows directly from Proposition 3. ∎

Further we prove two propositions showing the relation of the following optimization problems and with percentile and omega objectives.

Proposition 5.

Let and be an optimal solution of the optimization problem . If is non-constant, then is an optimal solution of the optimization problem .

Proof.

Define . is non-constant and so by Proposition 2, . Suppose by contradiction that there exists such that and .

If is infinite, then . This implies by the first order condition of expectiles (4) that , contradicting the optimality of as a solution of .

We now assume and introduce the following notation,

Note that by assumption and consequently . By Proposition 2, we have and . The first order condition of level- expectile implies

Substituting for gives

| (6) |

Equation (6) implies the following equation (7), since and .

| (7) |

Applying the first order condition for level- expectile gives the next equation (8).

| (8) |

Together, (7) and (8) imply that , which contradicts the optimality of as a solution of . ∎

Proposition 6.

Let be an optimal solution of the optimization problem . If is finite, then is an optimal solution of the optimization problem .

Proof.

Define and suppose by contradiction there exists such that and . The first order condition of level- expectile (4) gives (9), which implies (10) since .

| (9) | ||||

| (10) |

By Proposition 2, we have that , which implies

| (11) |

Equation (11) in turn implies the following equation (12), which is a contradiction to the optimality of as a solution of .

| (12) |

Corollary 4 and Propositions 5, 6 show that the same set of solutions (efficient frontier) can be generated by varying parameters in problems , , , .

Corollary 4 is valid for optimal portfolios found with the problems and .

Corollary 7.

If and there exists such that , then problems and are equivalent, i.e., their optimal solution sets and objective values coincide.

Corollary 8.

Let and be an optimal solution of the optimization problem . If is non-constant, then is an optimal solution of the optimization problem .

Corollary 9.

Let be an optimal solution of the optimization problem . If is finite, then is an optimal solution of the optimization problem .

4. Subgradient of

The function is convex in for . This section presents a formula for subgradients of the convex function when . The subgradient formula can be used for implementation of the convex programming algorithms for minimization of .

Lemma 10.

Suppose . Then for all non-constant , i.e. is strictly expectation bounded as defined in \shortciteNrockafellar2006generalized.

Proof.

Since , we have

Since is non-constant, and are positive. Moreover, the assumption that implies

The expression is non-increasing in and equals when . Hence, which implies . ∎

bellini2014generalized provide the following dual representation of .

Because is strictly expectation bounded, is a deviation measure in the sense of \shortciteNrockafellar2006generalized. Applying Proposition 1 of \shortciteNrockafellar2006optimality to leads to

The following proposition is modified from \shortciteNbellini2014generalized. Let us denote

Proposition 11 (\shortciteNPbellini2014generalized).

For all ,

is an element of .

Proof.

First note that , so to show it suffices to show .

The numerator of the second term in the penultimate step is because of the first order condition of expectile (4). ∎

In Section 6, we solve portfolio optimization problems with a constraint on . The following lemma furnishes a map from the subdifferential of to that of . We note that these optimization problems could alternatively be solved with convex programming approaches using the subdifferential of and the theory of \shortciteNrockafellar2006optimality.

Lemma 12.

If , then .

Proof.

The following proposition provides a collection of subgradients for .

Proposition 13.

The following is a subgradient of at for every ,

5. Derivative of for Discrete Distribution

In this section and in the following Case Study in Section 6 we assume that the random vector follows a discrete distribution. We derive subgradient formula for in this special case. These results are used for the implementation of optimization algorithms.

5.1. Notation

Let be a random vector with finitely many outcomes with corresponding probabilities . For any define , , and as follows.

The following proposition provides a collection of subgradients for .

Proposition 14.

The following is a subgradient of at for every .

Proof.

Apply Proposition 13. ∎

5.2. Partial Derivative of when

This section again derives the gradient formula for discrete distributions without using Proposition 14. This is done for illustrative purposes to show that the result can be obtained directly without using the sophisticated dual representation concept. In the following, we use the fact that can be defined as the unique solution to .

Proposition 15.

Suppose . Then there exists an open neighborhood of such that for every ,

Proof.

By assumption, , and by the definition of , we have

After rearrangement, we have

Note that is convex and thus continuous. Choose open neighborhoods of and of such that

-

(1)

for every ,

-

(2)

for every ,

-

(3)

for every .

Let be an element of .

Hence, . ∎

Corollary 16.

Suppose . Then

Note that need not be differentiable when . As an example, suppose and is uniformly distributed over . Let and . One can easily check that . However, while , so doesn’t exist at .

6. Case Study

The codes, data, and solution results for the first case study are available at “Portfolio Optimization with Expectiles” [\citeauthoryearExpectiles Case StudyExpectiles Case Study]. We solved the problem in a MATLAB environment using the Portfolio Safeguard (PSG) optimization software. PSG has both linear and convex programming algorithms. Convex programming is preferable for the cases with a large number of scenarios.

First, we consider the following single-stage stochastic optimization problem.

Here is a discrete, uniform random vector with outcomes and . An optimal solution for each in a given range was computed by supplying PSG with subroutines calculating the value and a subgradient of at any decision vector .

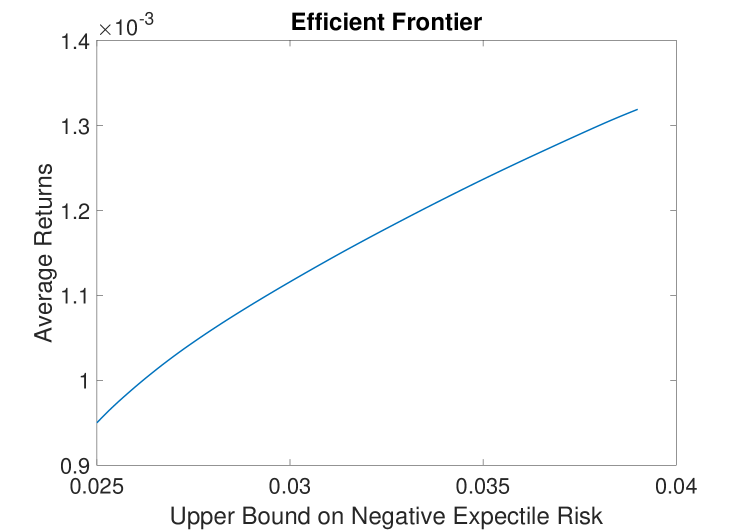

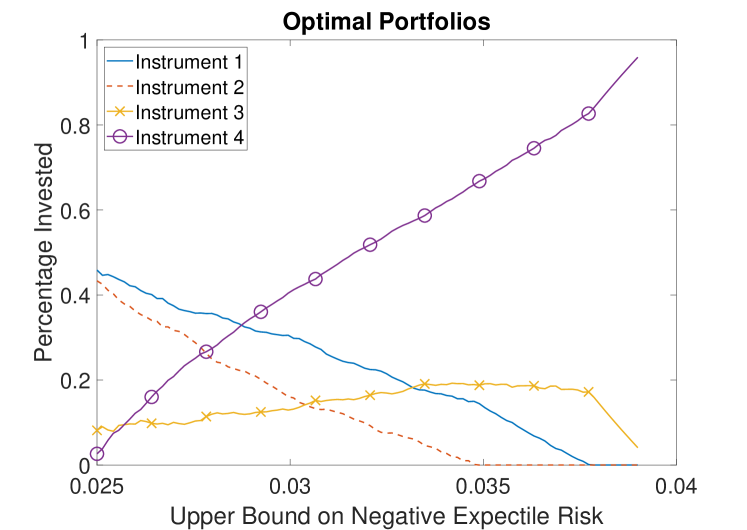

Figure 1 shows that when the upper bound on negative expectile risk is small, the optimal portfolio is a roughly even mixture of and . However, as the constraint is loosened, the portfolio gradually shifts to being concentrated in . This indicates that has the highest expected returns, while also carrying the most risk.

We also consider the problem of minimizing risk with expected returns bounded from below.

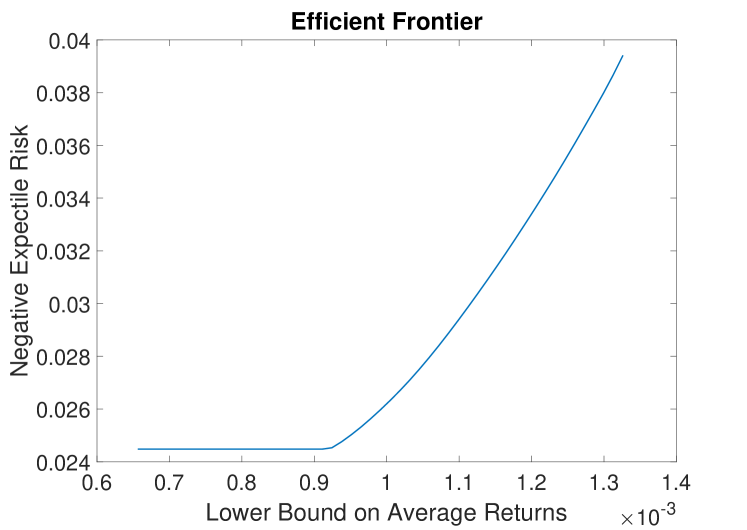

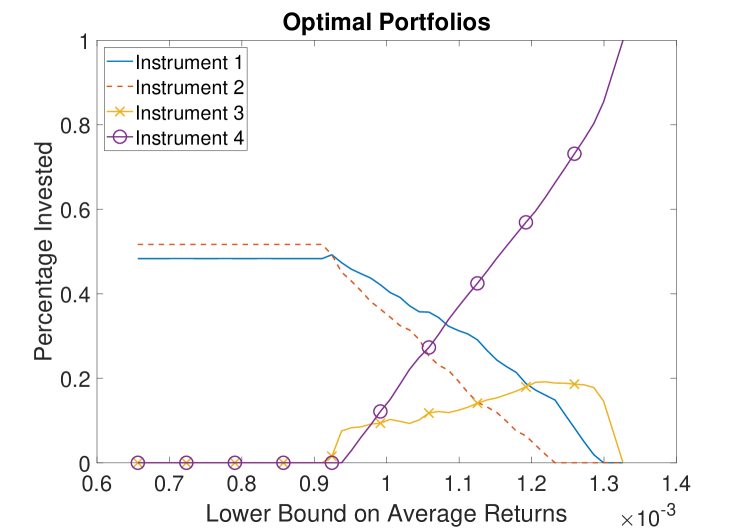

The efficient frontier in Figure 2 shows that until we require an average return of more than , the negative expectile risk of the optimal portfolio is constant. This suggests that in practice a lower bound greater than may be reasonable. Figure 2 shows that when the constraint on average return is small, the optimal portfolio is an even mix of and . However, as the constraint on average return increases, the portfolio shifts to the riskier .

Lastly, we compare our results with those from the case study “Basic CVaR Optimization Problem, Beyond Black-Litterman” [\citeauthoryearCVaR Case StudyCVaR Case Study] which uses the same data.

The optimal solution is given by , which has an average return of and . The optimal solution with the same expected return constraint but minimizing negative expectile is given by , which has an average return of and .

We also conducted experiments using data from the case study “Omega Portfolio Rebalancing” [\citeauthoryearOmega Case StudyOmega Case Study]. The first experiment is a numerical test of Corollary 8. We set such that and solved for values of between and . For each and its corresponding optimal portfolio , we then solved and obtained an optimal portfolio . According to Corollary 8, if , an optimal solution of is also optimal for as long as is non-constant. Indeed, this result is supported by the experiment because for each , the portfolios and were essentially equal. The largest difference in the percentage invested in any instrument between and was over all tested. We repeated the experiment with the dataset with scenarios from the previous case study and obtained similar results. We remark that the linear programming formulation of omega maximization due to \shortciteNmausser2006optimising took approximately seconds with this larger dataset while omega maximization with the convex programming approach afforded by PSG took approximately seconds.

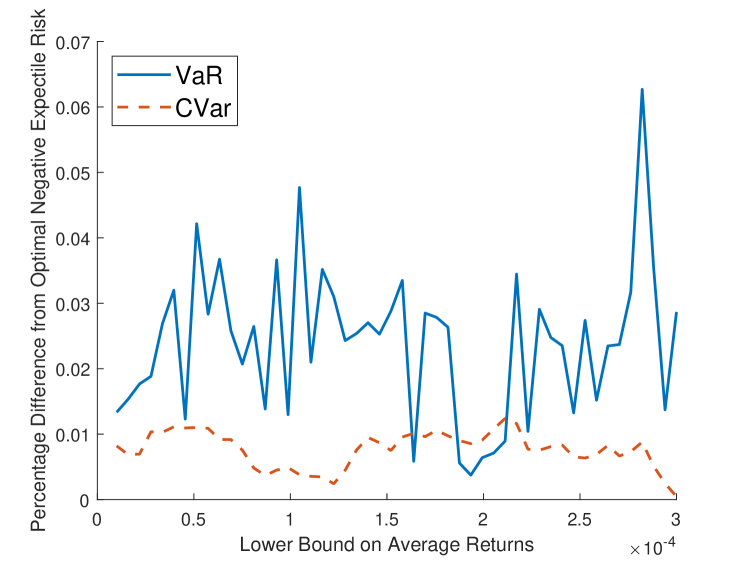

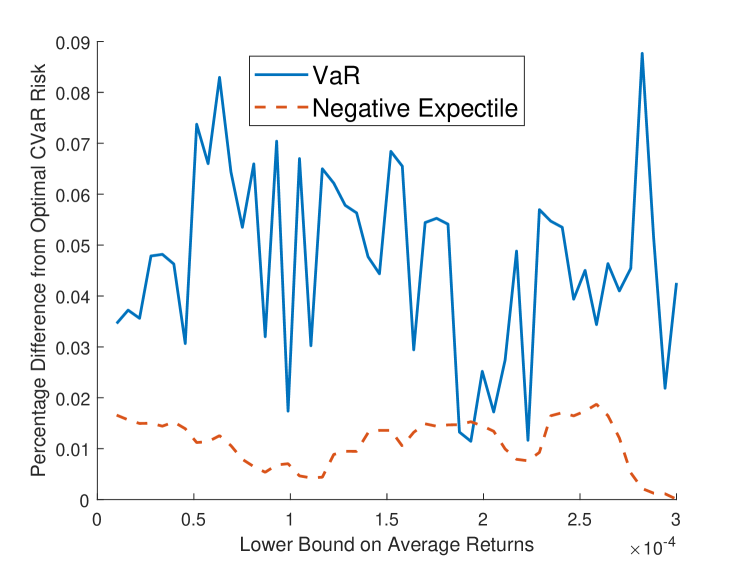

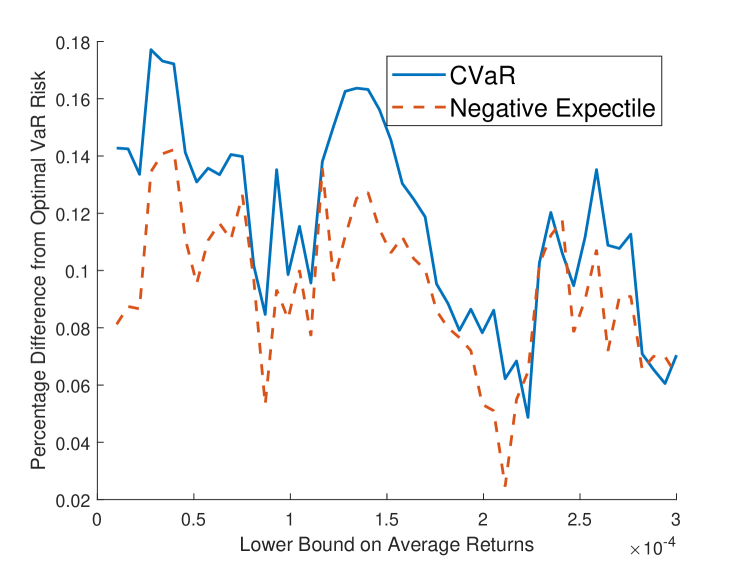

We also used this data to compare negative expectile to CVaR and VaR. For a range of values of between and , we solved the following optimization problems for and .

For each , we obtained an optimal solution for each risk measure and computed the value of this solution with respect to the other two risk measures. Figure 3 plots the relative differences. For example, the first plot shows the negative expectile risk of the optimal VaR and CVaR portfolios for a range of values of . The plots show that the CVaR of the optimal expectile solution and the negative expectile of the optimal CVaR solution are both nearly optimal while the VaRs of the optimal CVaR and expectile solutions are considerably larger. Hence, this experiment suggests that CVaR and negative expectile may be more similar to each other than either is to VaR.

7. Conclusion

This paper considered the optimization problems of maximizing a portfolio’s expected returns with an upper bound constraint on negative expectile risk or minimizing a portfolio’s negative expectile risk with a lower bound constraint on expected returns. We proved equivalences between both of these problems and omega ratio optimization problems in Section 3 by using the inverse relationship between expectile and the omega ratio described in Proposition 2. In order to solve expectile portfolio optimization problems using convex programming in Section 6, we derived a subgradient for , the negative level- expectile risk of a portfolio . This was done in Section 4 by applying the theory of \shortciteNrockafellar2006optimality to the dual representation of negative expectile due to \shortciteNbellini2014generalized and again in Section 5 by an elementary argument. In Section 6, we also conducted a numerical test of an equivalence between expectile and omega ratio optimization and performed a comparison of negative expectile to two other popular risk measures, VaR and CVaR.

References

- [\citeauthoryearArtzner, Delbaen, Eber, and HeathArtzner et al.1999] Artzner, P., F. Delbaen, J.-M. Eber, and D. Heath (1999). Coherent measures of risk. Mathematical Finance 9(3), 203–228.

- [\citeauthoryearBellini and BernardinoBellini and Bernardino2017] Bellini, F. and E. D. Bernardino (2017). Risk management with expectiles. The European Journal of Finance 23(6), 487–506.

- [\citeauthoryearBellini, Bignozzi, and PuccettiBellini et al.2018] Bellini, F., V. Bignozzi, and G. Puccetti (2018). Conditional expectiles, time consistency and mixture convexity properties. Insurance: Mathematics and Economics 82, 117 – 123.

- [\citeauthoryearBellini, Klar, and MüllerBellini et al.2018] Bellini, F., B. Klar, and A. Müller (2018). Expectiles, omega ratios and stochastic ordering. Methodology and Computing in Applied Probability 20(3), 855–873.

- [\citeauthoryearBellini, Klar, Müller, and GianinBellini et al.2014] Bellini, F., B. Klar, A. Müller, and E. R. Gianin (2014). Generalized quantiles as risk measures. Insurance: Mathematics and Economics 54, 41 – 48.

- [\citeauthoryearBellini, Negri, and PyatkovaBellini et al.2019] Bellini, F., I. Negri, and M. Pyatkova (2019). Backtesting VaR and expectiles with realized scores. Statistical Methods & Applications 28(1), 119–142.

- [\citeauthoryearCVaR Case StudyCVaR Case Study] CVaR Case Study. Case study: Basic CVaR optimization problem, beyond Black-Litterman. https://www.ise.ufl.edu/uryasev/research/testproblems/financial_engineering/basic-cvar-optimization-problem-beyond-black-litterman/. Accessed:2019-6-28.

- [\citeauthoryearExpectiles Case StudyExpectiles Case Study] Expectiles Case Study. Case study: Portfolio optimization with expectiles. https://www.ise.ufl.edu/uryasev/research/testproblems/financial_engineering/case-study-portfolio-optimization-with-expectiles/. Accessed:2019-6-28.

- [\citeauthoryearJakobsonsJakobsons2016] Jakobsons, E. (2016). Scenario aggregation method for portfolio expectile optimization. Statistics & Risk Modeling 33.

- [\citeauthoryearKane, Bartholomew-Biggs, Cross, and DewarKane et al.2009] Kane, S. J., M. C. Bartholomew-Biggs, M. Cross, and M. Dewar (2009). Optimizing omega. Journal of Global Optimization 45(1), 153–167.

- [\citeauthoryearKapsos, Zymler, Christofides, and RustemKapsos et al.2014] Kapsos, M., S. Zymler, N. Christofides, and B. Rustem (2014). Optimizing the omega ratio using linear programming. The Journal of Computational Finance 17(4), 49–57.

- [\citeauthoryearKeating and ShadwickKeating and Shadwick2002] Keating, C. and W. Shadwick (2002). A universal performance measure. Journal of Performance Measurement 6.

- [\citeauthoryearMausser, Saunders, and SecoMausser et al.2006] Mausser, H., D. Saunders, and L. Seco (2006). Optimising omega. Risk 19(11), 88.

- [\citeauthoryearNewey and PowellNewey and Powell1987] Newey, W. K. and J. L. Powell (1987). Asymmetric least squares estimation and testing. Econometrica 55(4), 819–847.

- [\citeauthoryearOmega Case StudyOmega Case Study] Omega Case Study. Case study: Omega portfolio rebalancing. https://www.ise.ufl.edu/uryasev/research/testproblems/financial_engineering/omega-portfolio-rebalancing/. Accessed:2019-6-28.

- [\citeauthoryearRockafellar, Uryasev, and ZabarankinRockafellar et al.2006a] Rockafellar, R. T., S. Uryasev, and M. Zabarankin (2006a). Generalized deviations in risk analysis. Finance and Stochastics 10(1), 51–74.

- [\citeauthoryearRockafellar, Uryasev, and ZabarankinRockafellar et al.2006b] Rockafellar, R. T., S. Uryasev, and M. Zabarankin (2006b). Optimality conditions in portfolio analysis with general deviation measures. Mathematical Programming 108(2), 515–540.

- [\citeauthoryearZiegelZiegel2016] Ziegel, J. F. (2016). Coherence and elicitability. Mathematical Finance 26(4), 901–918.