Soft robust solutions to possibilistic optimization problems

Abstract

This paper discusses a class of uncertain optimization problems, in which unknown parameters are modeled by fuzzy intervals. The membership functions of the fuzzy intervals are interpreted as possibility distributions for the values of the uncertain parameters. It is shown how the known concepts of robustness and light robustness, for the traditional interval uncertainty representation of the parameters, can be generalized to choose solutions that optimize against plausible parameter realizations under the assumed model of uncertainty in the possibilistic setting. Furthermore, these solutions can be computed efficiently for a wide class of problems, in particular for linear programming problems with fuzzy parameters in constraints and objective function. Thus the problems under consideration are not much computationally harder than their deterministic counterparts. In this paper a theoretical framework is presented and results of some computational tests are shown.

Keywords: fuzzy optimization; possibility theory; robust optimization; fuzzy intervals

1 Introduction

In this paper we investigate the following optimization problem with uncertain parameters:

| (1) |

In formulation (1), is an -vector of decision variables, is an -matrix of imprecise constraint coefficients and is an -vector of objective function coefficients. The meaning of and the relation depends on the model of uncertainty assumed and it will follow from the context. For simplicity of presentation, we first assume that the vector of the objective function coefficients is precisely known. We will show later, in Section 6, that the approach proposed in this paper can be easily extended to the case of uncertain objective function coefficients . An -vector of right hand sides is also assumed to be precisely known. It does not cause loss of generality, as we can always add artificial variables and include uncertain right hand sides in matrix (see, e.g., [3]). We will denote by the th imprecise constraint in (1), where , , is the th row of (throughout the paper we will use the notation ). Set is a bounded subset of , where is the set of nonnegative reals. For example, if is a bounded polyhedron, then we get an uncertain linear programming problem. If ( is a finite set), then (1) becomes an uncertain combinatorial optimization problem. For a particular realization of the constraint coefficients (called scenario), we get a deterministic counterpart of , which is a traditional optimization problem.

A typical method of solving (1) consists in replacing the imprecise constraints with some crisp equivalents and solving the resulting mathematical programming problem (see, e.g., [1, 13, 24, 26, 32, 35, 38]). The method of constructing such a problem depends on the interpretation of the imprecise parameters, which in turn, depends on the information available. In many cases the resulting model is harder to solve than the deterministic counterpart of (1).

If , , are vectors of random variables with known probability distributions, then stochastic optimization framework can be used (see, e.g., [24]). Namely, we can replace the imprecise constraints in (1) with chance constraints of the form

where is a given risk (significance) level. In practice, however, it is often difficult or even impossible to provide the parameter distributions. Furthermore, the resulting problem with chance constraints can be hard to solve [24].

If the probabilistic information about the parameters is not available, then robust optimization framework can be applied (see, e.g., [1], [2]). Suppose we only know that , where is a given uncertainty (scenario) set, containing all possible realizations (scenarios) of the uncertain constraint coefficients. Using the robust framework, problem (1) is then expressed as:

| (2) |

Solutions to (2) (if they exist), called strictly robust, can be very conservative, as we require that the constraints are satisfied for all possible realizations of the parameters (see [39]). Several methods of relaxing the strict robustness have been proposed in the existing literature. One of the most common was introduced in [4], where it is assumed for each constraint, that only a subset of the imprecise parameters can take their worst values. Then, each constraint is satisfied with a reasonable probability. We will describe this idea in more detail in Section 2.

Another method of softening (2) is to relax the right hand sides of the constraints, which leads to the concept of light robustness, originally proposed in [14] and further discussed in [36]. In typical situations, where everything goes smoothly without any disturbances, the constraint coefficients will take some nominal values , where is the nominal value of uncertain coefficient . A robust solution should be feasible in the nominal scenario and also not too far from optimality under this scenario. This can be modeled by adding the crisp constraints and , where is the optimal objective value of (1) under the nominal scenario and is a fixed tolerance. Finally, the constraints should be satisfied for all scenarios with some possible tolerances (deviations). The goal is now to minimize a distance of the deviations to the zero-vector. The light-robustness counterpart of (1) takes then the following form [14, 36]:

| (3) |

where denotes a given norm and is a vector of -decision variables, slack variables, that take strictly positive values if the corresponding constraints are violated.

In the classical stochastic approach a full probabilistic information about the problem parameters is available, while in the traditional robust approach we may only know the supports of the distributions of the random parameters. Many problems arising in practice are located between these two boundary cases. Namely, a partial information about parameter distributions, such as their mean (nominal) values and variances, is available. We can then seek solutions that hedge against the worst probability distributions which may appear. This leads to various robust distributionally models discussed, see for instance [8, 17]. Another method of modeling incomplete probabilistic information involves fuzzy sets with their possibilistic interpretation. Namely, we can assume that , , are vectors of fuzzy quantities with specified possibility distributions. Possibility distribution can be seen as an estimation (upper bound) on the unknown probability distribution and some methods of constructing it from the available data can be found in [9, 12]. We can now utilize this additional possibilistic information to improve the solution robustness, by using possibility and necessity measures. For example, we can replace the imprecise constraints of (1) with fuzzy chance constraints of the form

where and are possibility and necessity measures, respectively (see, e.g., [21, 28, 32]). For a deeper discussion on various approaches used in fuzzy optimization we refer the reader to [20, 22, 29, 26, 34, 33, 38].

The aim of this paper is to extend the robust concepts proposed in [4, 14, 36] to the fuzzy case in the possibilistic setting. As in [4], we will assume that for each uncertain parameter (matrix coefficient) an interval of possible values is provided, which is symmetric around its nominal value . This value is usually chosen as the most likely one. Indeed, in practice, knowledge about uncertainty of a parameter is usually expressed as a possible deviation () from , which means that the actual parameter will take some value within the interval , but it is not possible at present to predict which one. In consequence, it induces a simple interval uncertainty representation (see, e.g., [25]). In our approach a possibility distribution within this interval can also be prescribed. This possibility distribution can be seen as an upper bound on the unknown probability distribution (see, e.g., [9, 11]). Now, some parameter values within this interval are more plausible than others, which extends and refines the traditional interval uncertainty representation. Following [4], we make a reasonable assumption that in practical situations it is unlikely that all parameters will deviate from their nominal values at the same time. Accordingly, we specify at most how many coefficients in each constraint can deviate from their nominal values. Then, following [14, 36], we provide an acceptable increase in the cost of a solution found. In order to choose a robust solution, we propose two necessity measure based criteria. Using the first criterion we seek a solution, called a best necessarily feasible, for which we are sure with the highest degree that it is protected against the worst parameter realizations. The second criterion, called a best necessary soft feasibility, is a relaxation of the previous one and is similar in spirit to the idea of light robustness (see model (3)). It is worth pointing out that both criteria will lead to computationally tractable problems for some important special cases of (1).

The following natural assumption will be needed throughout the paper.

Assumption 1.

Set is a nonempty bounded subset of and there exists , feasible to , where is a matrix of the nominal constraint coefficient values.

The above assumption ensures that all the programs (models) proposed in this paper are bounded and feasible, when the parameters are precise.

This paper is organized as follows. In Section 2 we recall the concepts of robustness and light robustness proposed in [14, 4, 36]. In Section 3 we apply possibility theory to model the uncertain problem parameters. We introduce a possibilistic model of uncertainty and provide its interpretation. In Section 4 we propose a concept of choosing a solution, which extends the traditional robust approach to the fuzzy (possibilistic) case. In Section 5 we further generalize the concept from Section 4 by using the idea similar to light robustness. In Section 6 we show how the uncertain objective function can be considered in our model. In Section 7 we provide an algorithm for solving the problem and identify special cases which can be solved in polynomial time. Finally, in Section 8 we show results of some experiments, which suggest that taking additional information about the uncertain parameters into account may lead to solutions with a better quality over a set of plausible parameter realizations.

2 Robust and light robust solutions under interval uncertainty

In this section we briefly recall the robust and light robust approaches proposed in [4, 36, 14]. Consider the th imprecise constraint . Suppose that , , is a random variable, symmetrically distributed around its nominal value . The true distribution of is unknown and the value of is only known to belong to the support of , where is the maximal deviation of the parameter from its nominal (expected) value . Let be the Cartesian product of the supports, i.e.

| (4) |

and be an integer parameter in , called protection level, which specifies the maximal number of coefficients in the constraint, whose values can be different from their nominal ones. Accordingly, define

| (5) |

where is a realization (scenario) of the th constraint coefficients - a state of the world. Therefore, we will consider all scenarios which are in . Using the robust approach (2), we can rewrite the imprecise constraint as

| (6) |

From (4) and (5) and the fact that , it follows that (6) can be equivalently expressed as

| (7) |

where is the vector of nominal constraint coefficient values. Making use of the linear programming duality, the inequality (7) can be equivalently represented as the following system of linear constraints [4] (we include the transformation for completeness in Appendix A):

| (8) |

where and are dual variables (see Appendix A). Applying (8) to each constraint we get the following robust counterpart of problem (1) that is consistent with the approach proposed in [4]:

| (9) |

The protection levels , , allow decision makers to control the conservatism of the model by changing the value of , from to . If , then only the nominal constraint is considered and the uncertainty is ignored. On the other hand, when , all the coefficient , , can take their worst-case values. In this case the model becomes the highly conservative problem (2). It is worth pointing out that the existence of a feasible solution to (9) depends on . Obviously, by Assumption 1, (9) is feasible if for every and it may be infeasible for some larger , i.e. when the maximum increase in the left hand side of the th constraint (see (6)) for is greater than the right hand side. An optimal solution to (9) for some , , prescribed is a robust choice. Indeed, for this solution we are sure that each constraint , , is protected against all scenarios in which at most constraint coefficients take values different from their nominal ones - we call such constraints -protected. However, it is still assumed that a subset of the coefficients will take the largest values in the corresponding supports. The probability of occurrence of the extreme values can be much less than other values within the supports. Model (9) does not take any additional information about the coefficients distributions into account. In the next sections we will extend (9) to the case, in which possibility distributions for the coefficients are specified.

Under the model of uncertainty assumed in this section, the light robust counterpart of problem (1) (see also (3)) takes the following form [36, 14]:

| (10) |

where and are dual variables (see Appendix A), is a slack variable that takes positive value if the th constraint is violated, is the optimal objective value of the deterministic counterpart under the nominal scenario , is a fixed tolerance controlling the price of robustness, i.e. an increase in the cost of a solution computed with respect to , and is a given norm (for instance or ). The variables , , in (10) and Assumption 1 guarantee feasibility and boundedness of (10). Model (10) is more flexible than (9). It allows us to fix a tradeoff between the robustness of a solution and its price (modeled by the parameter ). However, similarly to model (9), only the information contained in the supports of the uncertain parameters is exploited.

3 Possibilistic model of uncertainty

Possibility theory provides a framework of dealing with incomplete information. Its key feature is using two dual set functions, called possibility and necessity measures. A detailed description of possibility theory can be found in book [12]. We now briefly describe (following [9, 11]) its main components, together with the interpretation assumed in this paper. The primitive object of possibility theory is a possibility distribution, which assigns to each element in universal set a degree of possibility . Function reflects the more or less plausible values of unknown quantity taking values in . The possibility degree of an event is then

Accordingly, the degree of necessity of an event is

| (11) |

where is the complement of . The necessity measure satisfies the minitivity axiom, i.e. for any two events

| (12) |

There are several interpretations of the possibility and necessity measures. In this paper (see, e.g., [11]) we assume that possibility measure encodes the family of probability measures such that or, equivalently, . Hence possibility distribution can be seen as an estimation (upper bound) on the unknown probability distribution, and for each event , .

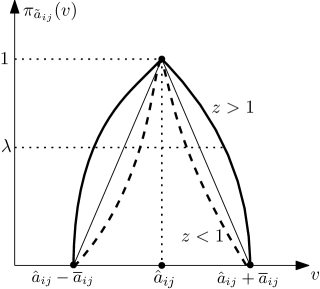

Consider uncertain parameter in matrix . In the approach described in Section 2, we only know the support of . However, in real applications more information about can be provided, which can be utilized to improve the quality of the computed solution. In our model we assume that is a fuzzy interval, whose membership function is continuous, symmetrically distributed around the nominal value and with the support equal to (see Figure 1). The membership function of fuzzy interval is interpreted as a possibility distribution for .

Recall that the set , , is called a -cut of and contains all values of whose possibility of occurrence is at least . We will assume that is the support of . The sets , , form a nested family of closed intervals with centers equal to the nominal value . The bound is a continuous, strictly decreasing function in , such that . For example, if is a symmetric triangular fuzzy interval, then . One can, however, use also generalized nonlinear functions , , to better reflect the uncertainty (see Figure 1). Namely, the smaller is the value of the less uncertainty is associated with . For large , tends to a closed interval. Before we proceed, let us state some additional remarks about the model of uncertainty assumed. In the following, for simplicity of presentation, we use the same value of to model the possibility distributions of all imprecise parameters (see Figure 1). However, the solution method proposed in the next part of the paper can be easily applied to the case in which the values of are different. Namely, for . Hence the shapes of the possibility distributions for the parameters can be different, which is reasonable in applications. Also the assumption that the possibility distributions are symmetric, which has been made to be consistent with the interpretation provided in [4], can be relaxed. We will use this assumption only in simulation tests, performed to compare our approach to the models proposed in [4, 14, 36].

Applying (11) and the continuity of yield

Hence and the probability that the value of falls within is at least . Let be scenario describing a realization of (a state of the world) in the th imprecise constraint . The degree of possibility that scenario will occur is provided by the following joint possibility distribution on the set of all possible scenarios, induced by possibility distributions , (see, e.g., [10]):

| (13) |

We can now compute the set of all scenarios whose possibility of occurrence is at least in the following way:

| (14) | |||||

and . Now , , so the probability that will fall within is at least .

4 A robust approach to possibilistic optimization problems

In this section we generalize the approach proposed in [4] (see Section 2) to the fuzzy case. We will use the possibilistic interpretation of the uncertain parameters, described in Section 3, and give a possibilistic counterpart of problem (1).

Consider imprecise constraint , in which vector has a possibility distribution described as (13). As in Section 2, we provide a protection level , which is an integer in and bounds the number of components in whose realization values are different from their nominal ones. We can now compute the possibility of the event that the constraint will be -protected for a given solution ( is called -feasible):

| (15) |

where is defined as (5). Applying the duality between the possibility and necessity measures gives the degree of necessity that a solution is -feasible (see (11)):

| (16) |

Observe that the quantity

is the possibility of the event that the constraint is not protected, i.e. it can be violated under the assumption that at most components of are different from their nominal values. Hence , , if and only if for all coefficient scenarios such that and , the inequality holds. Using (14), we get the following proposition:

Proposition 1.

For each , if and only if

| (17) |

We can now provide the following probabilistic interpretation of our model. If the inequality holds, then the constraint is -protected with probability at least . Observe that (17) is a parametrized version, with respect to , of (6). Hence, it can be replaced with the system of constraints (8) in which is replaced with (see also Appendix A).

Let be the optimal objective value of the deterministic counterpart of problem (1) under the nominal scenario and be a given tolerance parameter. Consider the crisp constraint

| (18) |

which ensures that the cost of solution must be of some predefined distance from the optimal cost . The parameter controls the price of robustness of our model (see [4]). Namely, the greater is the value of the more relaxed is the optimality of the solution.

Now, given tolerance , we wish to compute a solution, which satisfies all the constraints with the highest necessity degree. Namely, we focus on the following optimization problem:

| (19) |

An optimal solution to Nec is called a best necessarily feasible solution. Indeed, it is a reasonable choice, because with the highest degree we are sure that it is -feasible for every and the maximum increase in its cost above is not greater than . Using the minitivity axiom (see (12)), we can rewrite (19) as follows:

which in turn, by using standard techniques, can be expressed as follows:

| (20) |

By Proposition 1, we can rewrite (20) as

| (21) |

Finally, applying (8), we can represent Nec as the following mathematical programming problem:

| (22) |

where . If is an optimal solution to (22), then is a best necessarily feasible solution with . Note that model (22) is feasible and bounded by Assumption 1 (it is feasible for ). It is nonlinear due to the terms . A method of solving it will be shown in Section 7.

5 A soft robust approach to possibilistic optimization problems

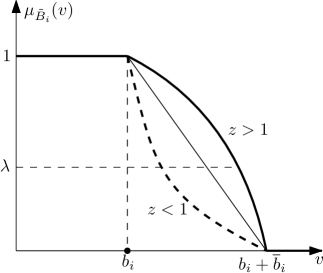

In this section we propose a more general and flexible concept for choosing a robust solution to problem (1). Consider again the uncertain constraint , where has a possibility distribution being as in (13). Solution is feasible for scenario if the crisp constraint is satisfied. Following the idea of light robustness [14, 36] (see also (3)), we relax the concept of feasibility by allowing some violation of the constraint. We assume that should now satisfy a flexible constraint under scenario , which is of the form , where is a fuzzy set in with membership function . The value of is the extent to which satisfies the flexible constraint. If for and for , then the flexible constraint reduces to the crisp one. In order to model the right hand side of the flexible constraint, we will use fuzzy set , shown in Figure 2. Namely, is nonincreasing, for and for , where is a parameter denoting the maximal allowed constraint violation. Let

be the pseudoinverse of . We get , where is nonincreasing function of such that . We will define . One can choose, for example, for some (see Figure 2). Notice that the larger is the value of the larger tolerance for the constraint violation is allowed.

We can now compute the possibility of the event that the soft constraint will be -protected for a given solution , i.e. the degree of possibility that is -soft feasible:

| (23) |

Notice that in (23) we jointly consider the uncertainty (induced by the uncertain coefficients in ) and flexibility of the th constraint (see [10]). Accordingly, the degree of necessity that a solution is -soft feasible is defined as follows:

| (24) | |||

Thus , , if and only if for all scenarios such that and , the inequality holds. This inequality is equivalent to Hence, (14) leads to the following proposition:

Proposition 2.

For each , if and only if

| (25) |

where .

We can now provide the following probabilistic interpretation of our model. If the inequality holds, then the th constraint is -protected with the tolerance , with probability at least .

In the approach described in Section 4 we required that , where is the optimal objective value of the deterministic counterpart under the nominal scenario and is the assumed tolerance. We can replace this crisp constraint with a flexible constraint of the form , where is a fuzzy set shown in Figure 2, with the pseudoinverse , where the interpretation of and is the same as in Section 4. Now, expresses a preference (satisfaction) about the deviation of from (less deviations are more preferred). We can define the necessity degree that the flexible constraint is satisfied as follows:

| (26) |

The following proposition is analogous to Proposition 2:

Proposition 3.

For each , if and only if

| (27) |

where .

Note that we can control the flexibility of the constraint by changing the parameter . If , then the computed solution must be optimal under the nominal scenario. On the other hand, if is large, then the constraint tends to the crisp constraint , which was used in the model discussed in Section 4.

We can now extend model (19) by considering the following optimization problem:

| (28) |

An optimal solution to (28) is called a best necessary soft feasible. Such a solution maximizes the necessity degree that it is -soft feasible for every and its cost falls within fuzzy cost . Using the minitivity axiom, Proposition 2 and 3, and applying the same reasoning as in Section 4, we can represent as follows:

| (29) |

where , , . If is an optimal solution to (29), then is a best necessarily soft feasible solution with . Such a solution exists, since by Assumption 1 model (29) is feasible and bounded. Note that it is nonlinear. We will show a method of solving (29) in Section 7. One can also optionally add to (29), along the lines of [14, 36], the crisp constraints

| (30) |

ensuring the feasibility of the solution in the nominal scenario.

5.1 Illustrative example

Consider the following uncertain problem (1):

| (31) |

where , , are symmetric triangular fuzzy intervals with supports , respectively. An optimal solution to the nominal problem, i.e. the one with , is with . The robustness of this solution is weak as the constraint violation is highly probable (it is worth pointing out that an increase of any coefficient above its nominal value results in solution infeasibility.) Let us fix the protection level , so the values of at most two coefficients in the constraint can differ from their nominal ones. If we use the robust model (9) for the supports of the fuzzy intervals, namely , then we get an optimal solution with the objective value . Notice that the possibilistic information for is not taken into account. This solution is more protected against the constraint violation, but one can observe a large deterioration () in the optimal objective value, so has a large price of robustness.

Let us now investigate the effect of taking the complete possibilistic information about into account. We compute a best necessarily feasible solution to (31) by solving the corresponding model (22) with . We can now control the price of robustness of the solution by changing the tolerance , used in the constraint . In Figure 3, the optimal objective value of (22), i.e. the degree of -feasibility, depending on the ratio is shown. If , then we require that the solution computed must be optimal for the nominal scenario. In this case, the best necessarily feasible solution is and its degree of necessary -feasibility is 0. On the other hand, if we fix (the ratio ), the best necessarily feasible solution computed is the same as the optimal robust solution to (9) for (recall that the optimal objective value of (9) is ). The degree of necessary -feasibility of this solution equals 1. It can be reasonable to choose some intermediate value of . For example, if (the ratio ), then we get solution with the degree of necessary -feasibility equal to 0.44.

Let us now compute a best necessarily soft feasible solution to (31) by solving (29). Assume that the maximum accepted magnitude of the constraint violation equals , i.e. it is at most of its nominal value equal to 6. The crisp right hand side in (31) is thus replaced with fuzzy set with . We also replace the crisp constraint with the flexible constraint , where is a fuzzy set with the pseudoinverse . As in the previous model, and is a parameter denoting the maximum accepted tolerance, controlling the price of robustness of the solution computed.

Let us first investigate the deterioration of the objective function for various (see Figure 4). Let be an optimal solution to (22) or (29) for a fixed and consider the ratio . Observe that for (22) the ratio increases linearly with . This is due to the constraint , which is tight at . Different behavior can be observed if is an optimal solution to (29). In general, the ratio can be smaller, due to the constraint , which is tight at and . Hence, model (29) returns solutions with smaller price of robustness.

In Figure 3 the optimal objective values of (22) and (29) are compared. For smaller ratios the objective value of (29) is greater. This is the effect of relaxation of the constraint which dominates the preference imposed on the objective value. The situation reverses for larger ratios , where the preference about the objective value is relaxed. Then a solution computed has a smaller price of robustness but also is less protected against the constraint violation.

In order to test the quality of the obtained solutions, one can perform a simulation, i.e. test the feasibility of the model for a sample of scenarios drawn according to the joint possibility distribution for . Such a simulation for larger instances will be done in Section 8.

6 Treating the uncertain objective function

In this section we will show how the model discussed in Section 5 can be extended to handle the uncertainty in the objective function into account. Suppose that the vector of objective function coefficients in (1), denoted now by , is imprecise. Many approaches have been proposed in the literature to deal with imprecise objective function . In the fuzzy setting, the problem is often reduced to minimizing , where is a real-valued ranking function [5, 6, 15, 32]. In another approach, a fuzzy goal is associated with the imprecise objective function and one can maximize , which is interpreted as the necessity degree of achieving the goal . This concept can be softened [23, 19] by maximizing , where is a fuzzy set whose membership function describes a possibility distribution of the maximum regret of (the maximum distance to the optimality of ).

In this section we will propose a method of dealing with uncertain vector , which is analogous to the concept described in the previous sections for the uncertain constraints. We will apply an approach, commonly used in robust and stochastic optimization (see, e.g., [4]), which consists in representing the imprecise objective function as imprecise constraint and minimizing , where is an additional variable that reflects possible realizations of objective function values. Therefore, we now study the following problem:

| (32) |

Observe that (32) has deterministic objective function and one additional imprecise constraint of the form . Hence, it is of the form (1) and for deterministic it is equivalent to (1). We can now treat this new constraint just in the same way as the remaining imprecise constraints.

In order to define , we will use the possibilistic model of uncertainty, described in Section 3. Namely, , , are fuzzy intervals with membership functions , symmetrically distributed around the nominal values and with the supports . We will use to denote the -cut of , where for a fixed (see Figure 1). If is scenario describing a realization of the uncertain objective function coefficients, then after applying the same reasoning as previously (see (13)), we can compute

Then and . Now , , so the probability that will fall within is at least .

Let us define a protection level , being an integer in . Then

Let us introduce fuzzy set (see Figure 2) with pseudoinverse . Accordingly, we can define

| (33) |

The following proposition is analogous to Proposition 2:

Proposition 4.

For each , if and only if

| (34) |

where .

Let be the optimal objective value of the deterministic counterpart of (32) under the nominal scenario . The flexible constraint , considered in Section 5, becomes then , where is defined in the same way as in Section 5. We can now extend Soft-Nec (see (28)), by using the necessity degree of conjunction of the events:

to the following optimization problem:

| (35) |

Taking Proposition 4 into account and applying the same reasoning as in Section 5, we can represent Soft-Nec as the following mathematical programming problem:

| (36) |

Observe that the variable can be eliminated from (36), which yields:

| (37) |

where , , and . If is an optimal solution to (37), then is a best necessarily soft feasible solution with . Note that by Assumption 1 model (37) is feasible and bounded. It is nonlinear and a method of solving it will be shown in Section 7. Model (37) generalizes (22) and (29). Indeed, if there is no uncertainty in the objective, then , , and for each . Then the first two constraints of (37) reduce to , which yields (29). Fixing further large in and for all leads to (22).

7 Solving the problem

The problems arising in practice are often of large-scale. It is thus important to construct efficient algorithms to solve them. In this section we show that the complexity of solving the uncertain problem under consideration is essentially the same as the complexity of solving its deterministic counterpart. For a brief introduction to computational complexity theory, we refer the reader to [7, Chapter 34].

Let us focus on solving (see (35)). We will study the most general model (37), in which an uncertain objective function is taken into account. For a fixed value of , all the constraints in (37) (possibly, except for the ones describing ) become linear. Let be the set of feasible solutions to (37) for a fixed value of . Since all the functions , , , are nonincreasing, we get if . Consequently, (37) can be solved by computing the smallest value for which is nonempty. This can be done by applying a binary search in the interval (see Algorithm 1).

The running time of Algorithm 1 depends of the complexity of the problem which must be solved in Steps 1 and 1, i.e. checking the feasibility of (37) for a fixed . In Step 1 the feasibility of (37) is implicitly checked for . Indeed, it is easily seen that this task can be reduced to solving the deterministic counterpart of problem (1) under the nominal scenario , since such solution computed, whose existence follows from Assumption 1, is always feasible to (37) for . Thus the computational complexity of Steps 1 and 1 depends on the structure of the set . If the feasibility can be checked in time, where is the size of (37), then Algorithm 1 runs in time, because the feasibility must be tested at most times. If is polynomial in size , then Algorithm 1 runs in polynomial time and Soft-Nec can be solved in polynomial time with a fixed accuracy . In the next section we will identify some important special cases of problem (1) for which this is the case.

7.1 Tractable problems

If is a polyhedron in , then (1) is an uncertain linear programming problem. In this case (37), for a fixed , is a system of linear constraints over , whose feasibility can be tested in polynomial time (see, e.g., [37]). In consequence, Soft-Nec can be then solved in polynomial time with a fixed accuracy .

If the integrality assumptions on some variables are imposed or , then checking the feasibility of (22), for a fixed , is NP-hard in general (see, e.g., [16]). We now describe a special case of such a problem, which can be solved efficiently. Consider the following combinatorial optimization problem with uncertain costs:

| (38) |

Using (37), we can express (38) as follows:

| (39) |

where . Using similar relation as the one between (6) and (8), we can equivalently express (39) as

| (40) |

where and were defined in Section 6. If is an optimal solution to (40), then is a best necessarily soft feasible solution with . A method of solving (40) is based on a binary search in the interval of possible values of . In order to test the feasibility of (40) of a fixed , we can first solve the problem

| (41) |

and check then if the optimal objective value of (41) is not greater than . To solve (41) we can use the algorithm proposed in [27, Theorem 1]. It consists of solving deterministic counterparts of problem (38) in time, where is the time required to solve one deterministic problem. The algorithm for solving (40) is an adaptation of Algorithm 1 (it is enough to solve deterministic problem under the nominal costs in Step 1 and apply the algorithm proposed in [27, Theorem 1] in Step 1). Its overall running time is now , where is a given accuracy and . Therefore, the algorithm is polynomial under the assumption that solving the deterministic counterpart of problem (38) can be done in polynomial time. This is true for such problems as: shortest path, minimum spanning tree, minimum assignment, etc. (see, e.g., [7, 31]).

8 Computational experiments

In this section we show the results of some computational tests. Our goal is to compare the soft robust approach in the possibilistic setting, proposed in Section 5, to the concept of light robustness presented in [14, 36]. We examine uncertain linear programming problem of the following form:

| (42) |

We assume that the objective function is deterministic (only the constraints are uncertain). An instance of the problem (42) is generated as follows:

-

1.

the number of variables and the number of constraints ;

-

2.

each cost , , is a random integer, uniformly distributed in the interval ;

-

3.

the nominal value of the constraint coefficient is a random integer, uniformly distributed in the interval and the bound is set to , where is a random number uniformly distributed in the interval ;

-

4.

we fix for each .

We set the protection levels for each . In the light robustness concept (see model (3)) we use the norm. In the soft robust approach (see model (29)) we assume the tolerance for the constraint violation, i.e. for each . For the membership functions of all fuzzy sets we fix , so their membership functions are piecewise linear. In particular, the uncertain coefficients are triangular fuzzy intervals. Let be the optimal objective value of the deterministic counterpart of (42) under the nominal scenario . We will choose for .

Let be a solution to (42), obtained by solving the model (29). We will compute the distance of to the optimum under the nominal scenario as follows:

The value of is the price of robustness of . In order to evaluate the a posteriori quality of we use the following Monte Carlo simulation. For each coefficient , independently, we generate its value (realization) as follows. First we choose uniformly at random and then uniformly at random the realization . Observe that realizations closer to are more probable. This gives us a scenario , which provides a deterministic counterpart of (42). For this deterministic problem we compute the magnitude of the constraint violation of , i.e. the value , where . After generating a set of random scenarios, we computed the fraction of the scenarios under which is infeasible, i.e.

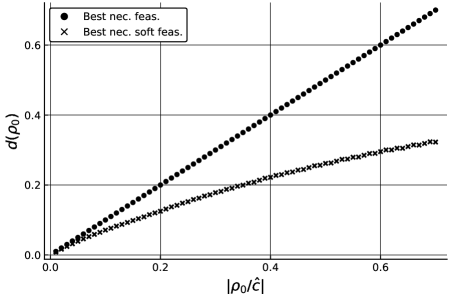

and the average magnitude of the constraint violation

The quantities , and can be seen as a posteriori evaluation of the quality of .

The experiments were performed as follows. For each we generated 100 instances as shown in points 1-4. For each instance we fixed and computed an optimal light robust solution , by solving (10), and a best necessarily soft feasible solution , by solving (29). For solving the models (10) and (29) we used IBM ILOG CPLEX 12.9 optimizer [18] and the modeling package JuMP [30] embedded in the programming language Julia. We computed the average qualities of the solutions. Namely, the average qualities of optimal light robust solutions are

The value of can be interpreted as the fraction of 100 000 deterministic counterparts for which an optimal light robust solution was infeasible (at least one constraint was violated) for a fixed . Accordingly, the value of is the average magnitude of the infeasibility. The quantities , and for the set of best necessarily soft feasible solutions are computed in the same way.

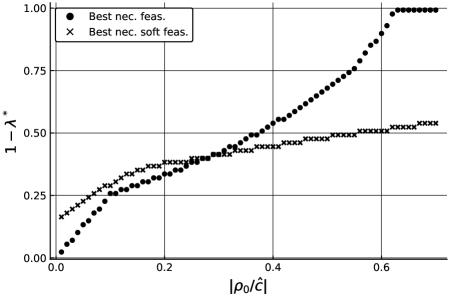

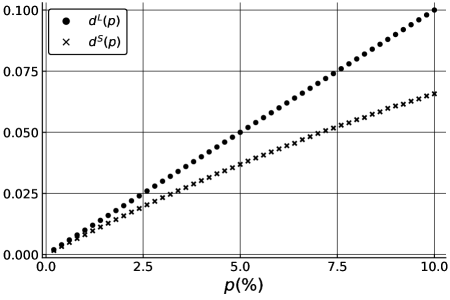

Figure 5 shows the average prices of robustness of the computed solutions for various ratios . One can observe that have smaller prices of robustness than . Furthermore, the difference between the prices becomes greater for larger . This observation can be explained as follows. In model (10) we use the constraint , which is tight at the optimum. So, the figure of is linear. In contrast, in the model (29) we use the flexible constraint, which yields . Because, , the cost of the solutions can be closer to .

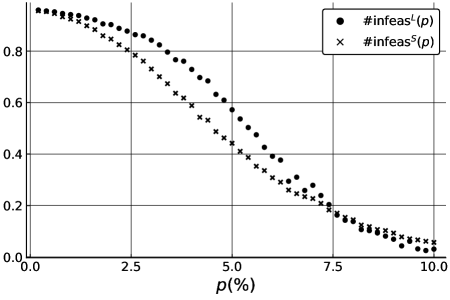

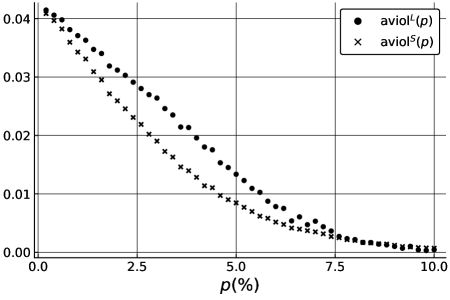

Figures 6 and 7 show the fractions of infeasible solutions and the average magnitude of constraints violations for both tested approaches. If , then both and must be optimal under (their prices of robustness equal 0). In this case they robustness is very weak, i.e. almost all deterministic counterparts are infeasible. Increasing (equivalently, the tolerance ), we can improve the robustness of both and . For almost all deterministic counterparts are feasible. However, the average price of robustness of is 0.1 whereas the average price of robustness of is about 0.06. For the solutions are more robust than , have smaller average magnitude of the constraints violation and also have a smaller price of robustness. We can thus conclude that taking the possibilistic information into account can improve the quality of the obtained solutions.

9 Conclusions

In this paper we have proposed a new concept of choosing a solution in uncertain optimization problems, in which unknown parameters are modeled by fuzzy intervals whose membership functions are regarded as possibility distributions for their values. In the traditional robust approach the values of uncertain parameters are only known to belong to a given uncertainty set . We then seek a solution which behaves reasonably under the worst parameter realizations in . This traditional robust approach has some well-known drawbacks. It does not take any additional information connected with into account. Furthermore, it is often considered to be too pessimistic (conservative) as the probability of occurrence of bad scenarios may be small. Our approach overcome these drawbacks. By specifying the possibility distribution in , as an upper bound on the unknown probability distribution, we provide additional information which can be utilized to improve the quality of computed solutions. Furthermore, following the idea of light robustness, we allow decision makers to control the price of robustness of the solutions. It is important that the proposed model can be solved in polynomial time if the underlying deterministic counterpart is polynomially solvable. In particular, this is true for uncertain linear programming problems and some uncertain combinatorial optimization problems (shortest path, minimum spanning tree, minimum assignment, etc.)

Acknowledgements

This work was supported by the National Science Centre, Poland, grant 2017/25/B/ST6/00486.

References

- [1] A. Ben-Tal, L. El Ghaoui, and A. Nemirovski. Robust optimization. Princeton Series in Applied Mathematics. Princeton University Press, Princeton, NJ, 2009.

- [2] A. Ben-Tal and A. Nemirovski. Robust solutions of uncertain linear programs. Operation Research Letters, 25:1–13, 1999.

- [3] D. Bertsimas and M. Sim. Robust discrete optimization and network flows. Mathematical Programming, 98:49–71, 2003.

- [4] D. Bertsimas and M. Sim. The price of robustness. Operations research, 52:35–53, 2004.

- [5] J. M. Cadenas and J. L. Verdegay. Using ranking functions in multiobjective fuzzy linear programming. Fuzzy Sets and Systems, 111:47–53, 2000.

- [6] S. Chanas and P. Zieliński. On the equivalence of two optimization methods for fuzzy linear programming problems. European Journal of Operational Research, 121:56–63, 2000.

- [7] T. Cormen, C. Leiserson, R. Rivest, and C. Stein. Introduction to Algorithms. The MIT Press, 2009.

- [8] E. Delage and Y. Ye. Distributionally robust optimization under moment uncertainty with application to data-deriven problems. Operations Research, 58:595–612, 2010.

- [9] D. Dubois. Possibility theory and statistical reasoning. Computational Statistics and Data Analysis, 51:47–69, 2006.

- [10] D. Dubois, H. Fargier, and P. Fortemps. Fuzzy scheduling: Modelling flexible constraints vs. coping with incomplete knowledge. European Journal of Operational Research, 147:231–252, 2003.

- [11] D. Dubois, L. Foulloy, G. Mauris, and H. Prade. Probability-possibility transformations, triangular fuzzy sets and probabilistic inequalities. Reliable Computing, 10:273–297, 2004.

- [12] D. Dubois and H. Prade. Possibility theory: an approach to computerized processing of uncertainty. Plenum Press, New York, 1988.

- [13] A. Ebrahimnejad and J. L. Verdegay. A survey on models and methods for solving fuzzy linear programming problems. In Fuzzy Logic in Its 50th Year - New Developments, Directions and Challenges, pages 327–368. Springer-Verlag, 2016.

- [14] M. Fischetti and M. Monaci. Light Robustness. In Robust and Online Large-Scale Optimization: Models and Techniques for Transportation Systems, pages 61–84. Springer-Verlag, 2009.

- [15] P. Fortemps and M. Roubens. Ranking and defuzzification methods based on area compensation. Fuzzy Sets and Systems, 82:319–330, 1996.

- [16] M. R. Garey and D. S. Johnson. Computers and Intractability. A Guide to the Theory of NP-Completeness. W. H. Freeman and Company, 1979.

- [17] J. Goh and M. Sim. Distributionally robust optimization and its tractable approximations. Operations Research, 58:902–917, 2010.

- [18] IBM ILOG CPLEX Optimization Studio. CPLEX User’s manual. https://www.ibm.com.

- [19] M. Inuiguchi. Robust-Soft Solutions in Linear Optimization Problems with Fuzzy Parameters. In Robustness Analysis in Decision Aiding, Optimization, and Analytics, pages 171–190. Springer-Verlag, 2016.

- [20] M. Inuiguchi, H. Ichihashi, and Y. Kume. Some properties of extended fuzzy preference relations using modalities. Information Sciences, 61:187–209, 1992.

- [21] M. Inuiguchi and J. Ramík. Possibilistic linear programming: a brief review of fuzzy mathematical programming and a comparison with stochastic programming in portfolio selection problem. Fuzzy Sets and Systems, 111:3–28, 2000.

- [22] M. Inuiguchi, J. Ramík, T. Tanino, and M. Vlach. Satisficing solutions and duality in interval and fuzzy linear programming. Fuzzy Sets and Systems, 135:151–177, 2003.

- [23] M. Inuiguchi and M. Sakawa. Robust optimization under softness in a fuzzy linear programming problem. International Journal of Approximate Reasonning, 18:21–34, 1998.

- [24] P. Kall and J. Mayer. Stochastic linear programming. Models, theory and computation. Springer, 2005.

- [25] P. Kouvelis and G. Yu. Robust Discrete Optimization and its Applications. Kluwer Academic Publishers, 1997.

- [26] Y.-J. Lai and C.-L. Hwang. Fuzzy Mathematical Programming. Springer-Verlag, 1992.

- [27] T. Lee and C. Kwon. A short note on the robust combinatorial optimization problems with cardinality constrained uncertainty. 4OR, 12:373–378, 2014.

- [28] B. Liu. Fuzzy random chance-constrained programming. IEEE Transactions on Fuzzy Systems, 9:713–720, 2001.

- [29] W. A. Lodwick and J. Kacprzyk, editors. Fuzzy Optimization - Recent Advances and Applications, volume 254 of Studies in Fuzziness and Soft Computing. Springer-Verlag, 2010.

- [30] M. Lubin and I. Dunning. Computing in operations research using julia. INFORMS Journal on Computing, 27:238–248, 2015.

- [31] C. H. Papadimitriou and K. Steiglitz. Combinatorial optimization: algorithms and complexity. Dover Publications Inc., 1998.

- [32] M. S. Pishvaee, J. Razmin, and S. A. Torabi. Robust possibilistic programming for socially responsible supply chain network design: A new approach. Fuzzy Sets and Systems, 206:1–20, 2012.

- [33] J. Ramík. Duality in fuzzy linear programming with possibility and necessity relations. Fuzzy Sets Systems, 157:1283–1302, 2006.

- [34] J. Ramík and M. Vlach. Generalized concavity in fuzzy optimization and decision analysis. Kluwer Academic Publishers, 2002.

- [35] M. Sakawa. Fuzzy Sets and Interactive Multiobjective Optimization. Plenum Press, 1993.

- [36] A. Schöbel. Generalized light robustness and the trade-off between robustness and nominal quality. Mathematical Methods of Operations Research, 80:161–191, 2014.

- [37] A. Schrijver. Theory of linear and integer programming. Wiley and Sons, 1986.

- [38] R. Słowiński and J. Teghem, editors. Stochastic Versus Fuzzy Approaches to Multiobjective Mathematical Programming under Uncertainty. Kluwer Academic Publishers, 1990.

- [39] A. L. Soyster. Convex Programming with Set-Inclusive Constraints and Applications to Inexact Linear Programming. Operations Research, 21:1154–1157, 1973.

Appendix A Appendix

In this appendix we show the transformation from (7) to (8) originally obtained in [4]. Fix and consider the th constraint (7). Since the first term in (7) is fixed, we focus on the following optimization problem over the set of constraint coefficient realizations , namely

| (43) |

Problem (43) can be formulated by the following linear programming problem:

| (44) |

Indeed, the constraint matrix of problem (44) is unimodular and each vertex solution is such that (see, e.g., [31]). Hence these decision variables express the selection of subset . Since , an optimal solution consists of variables at . The dual of problem (44) is as follows (the dual variables corresponding to the constraints in (44) are in the brackets):

| (45) |

Clearly problem (44) (problem (43)) is feasible and bounded for all integer in . By strong duality (see, e.g., [31]), problem (45) is feasible and bounded as well. At optimality the values of their objective functions are equal. Replacing (43) by (45) in (7), we have