Existence, uniqueness, and approximation of solutions of jump-diffusion SDEs with discontinuous drift

Abstract

In this paper we study jump-diffusion stochastic differential equations (SDEs) with a discontinuous drift coefficient and a possibly degenerate diffusion coefficient.

Such SDEs appear in applications such as optimal control problems in energy markets.

We prove existence and uniqueness of strong solutions. In addition we study the strong convergence order of the Euler-Maruyama scheme and recover the optimal rate .

Keywords: jump-diffusion stochastic differential equation, discontinuous drift, existence and uniqueness, Euler-Maruyama scheme, strong convergence rate

Mathematics Subject Classification (2010): 60H10, 65C30, 65C20, 65L20

1 Introduction

We consider a time-homogeneous jump-diffusion stochastic differential equation (SDE)

| (1) |

where , are measurable functions, , is a standard Brownian motion and is a Poisson process with Borel measurable and bounded intensity on the filtered probability space that satisfies the usual conditions.

Furthermore, let , define the equidistant time grid with for all and denote for all , . The time-continuous Euler-Maruyama (EM) scheme is given by and

| (2) |

In case the coefficients , , and are Lipschitz, it is well known that SDE (1) admits a unique strong solution which can be approximated with the EM scheme at strong convergence order .

In this work we allow to be discontinuous in a finite number of points. This is relevant for example for modelling energy prices, where jumps in the paths are a stylised fact, see, e.g., [1]. Control actions on energy markets often lead to discontinuities in the drift of the controlled process, cf., e.g., [39, 40].

We study existence and uniqueness of solutions to SDE (1) as well as numerical approximations of this solution.

In the jump-free case, SDEs with discontinuous drift have been studied intensively in recent years. For existence and uniqueness results see the classical papers [45, 42, 43, 44], as well as newer results, where boundedness of the coefficients and non-degeneracy of the diffusion coefficient is no longer needed, see [24, 39, 21, 22]. For approximation results see [12, 13, 14, 21, 30, 22, 31, 32, 33]. In the scalar case the best known results are -order of the EM scheme, see [27] and -order of a transformation-based Milstein-type scheme, see [26]. In the multidimensional setting the best known results are -order of the EM scheme, see [23] and -order of an adaptive EM scheme, see [29]. In the special case of additive noise the best known results are -order assuming piecewise Sobolev-Slobodeckij-type regularity of order for the drift, see [28] and [3], where they prove -order for the case where the drift is only bounded and (i.e. the case ). A lower error bound of order for the pointwise -error is proven in [15]. Lower bounds will be also studied in a forthcoming paper by Müller-Gronbach and Yaroslavtseva.

In the case of presence of jumps in the driving process, to the best of our knowledge there are no results available for SDEs with discontinuous drift so far. In the case of continuous coefficients however, the number of publications is still growing. This is due to the already mentioned fact that jumps often arise in models for energy markets, financial markets, or physical phenomena, see for example [34, 41]. The research directions cover for example classical Itô-Taylor approximations as in [8, 9, 34], construction of Runge-Kutta methods as in [2, 34], approximation of jump-diffusion SDEs under nonstandard assumptions as in [4, 6, 5, 16, 17, 18], multilevel Monte Carlo methods for weak approximation as in [7], and asymptotically optimal approximations of solutions of such SDEs as in [20, 36, 37, 38].

The current paper consists of two main contributions: the first existence and uniqueness result for jump-diffusion SDEs with discontinuous drift and consequently the first approximation result for solutions to such SDEs. We obtain the optimal -order for the EM scheme.

2 Preliminaries

In the following we denote by the Lipschitz constant of a generic function , we define with , and we denote by the compensated Poisson process, that is for all . Note that is a square integrable -martingale.

In order to define assumptions on the drift coefficient, we recall the following definition.

Definition 2.1 ([22, Definition 2.1]).

Let be an interval and let . We say a function is piecewise Lipschitz, if there are finitely many points such that is Lipschitz on each of the intervals , and .

Assumption 2.1.

We assume the following on the coefficients of (1):

-

(ass-)

The drift coefficient is piecewise Lipschitz with discontinuities in the points .

-

(ass-)

The diffusion coefficient is Lipschitz and for all , .

-

(ass-)

The jump coefficient is Lipschitz.

Lemma 2.2.

Let Assumptions 2.1 hold. Then , , and satisfy a linear growth condition, that is there exist constants such that

Proof.

We have that . Setting we get . The analog estimate holds for . For we have that there exists an with . With this . Setting we get . In the same way for there exists with . In the compact interval , is bounded by a constant . Setting proves the lemma. ∎

The transform

We will apply a transform from [22] that has the property that the process formally defined by satisfies an SDE with Lipschitz coefficients and therefore has a solution by classical results, see [35, p. 255, Theorem 6].

The function is chosen so that it impacts the coefficients of the SDE (1) only locally around the points of discontinuity of the drift. This behaviour is ensured by incorporating a bump function into , which is defined by

| (3) |

With this the transform is defined by

| (4) |

with

Note that is chosen such that for all , , so that has a global inverse . The transformation and its inverse are Lipschitz and the function , that is it is continuously differentiable with bounded derivative. Furthermore, is piecewise Lipschitz, since it is differentiable on with bounded derivative, see [22, Lemma 3.8]. Hence, is Lipschitz, since it is piecewise Lipschitz and continuous, see [21, Lemma 2.2]. These properties are proven in [22].

Finally, note that the choice of is not unique. In fact, it suffices to ensure existence of a function satisfying these properties.

3 Existence and uniqueness result

We are going to prove our first main result.

Proof.

Since is Lipschitz, we may apply the Meyer-Itô formula, which follows from [35, p. 221, Theorem 71], to and get

| (5) |

where for all ,

| (6) | ||||

| (7) | ||||

| (8) |

In [22] it is shown that and are Lipschitz. The jump coefficient is Lipschitz due to the global Lipschitz continuity of and . Hence, the SDE for , that is (5) with initial condition , has a unique global strong solution by [35, p. 255, Theorem 6].

Now observe that is absolutely continuous since it is Lipschitz. Moreover, , and by (8) we have

| (9) |

This implies that

| (10) |

Therefore, again by using Meyer-Itô formula

∎

4 Convergence of the Euler-Maruyama method

Our convergence proof is based on a transformation trick from [21, 23] in combination with ideas from [27] for the estimation of discontinuity crossing probabilities. By extending both to the case of presence of jumps and proving an occupation time result for the EM process, this leads to the optimal convergence order .

4.1 Preparatory lemmas

In this section we present several lemmas, cf. the results for the jump-free case in [27], which we need for the proof of the main result of Section 4.

Lemma 4.1.

Let Assumptions 2.1 hold and let . There exist a constant such that for all ,

and such that for all , ,

Proof.

There exists a constant such that for all ,

Furthermore there exists a constant such that

| (11) |

and by [6, Inequality (3.20)],

| (12) |

This and the linear growth of , , and imply the existence of a constant such that

Since it follows that

| (13) |

We also have for that there exists a constant such that

| (14) | ||||

The Burkholder-Davis-Gundy inequality, Doob’s maximal inequality for cádlág martingales, [25, Lemma 2.1], and the linear growth condition on , ensure the existence of constants such that

| (15) |

and since ,

| (16) |

Since is of at most linear growth, an analogous estimate for the Lebesgue integral holds. Hence,

| (17) |

By (13) we now obtain that

| (18) |

Equation (17) also yields

Since (18) holds and the function is Borel measurable (as a nondecreasing mapping), Gronwall’s Lemma yields the first assertion.

For the second statement note that for all , , there exists a constant so that it holds

| (19) |

The Hölder inequality, the Burkholder-Davis-Gundy inequality, [25, Lemma 2.1], and the linear growth condition of the coefficients together with the first assertion yield the statement. ∎

Note that we consider the -error and not the -error as in the jump-free case in [27], since due to (12) we will not get a better estimate for anyhow, cf. [6, Remark 3.14]. For later use we define .

4.1.1 Estimation of the occupation time of the Euler-Maruyama process

In this subsection we need to make the dependence on the initial value explicit in the notation. For all denote by the unique strong solution of (1) with initial condition and by the solution of the time-continuous version of the Euler-Maruyama scheme (2) starting at . Note that from the proof of Lemma 4.1 it follows that there exists such that for all , , , ,

| (20) |

| (21) |

Lemma 4.2.

Let Assumptions 2.1 hold. Then there exists such that for all , , , it holds

| (22) |

Proof.

By [41, Lemma 158] we have for all that

where is the local time of the semi-martingale in . Since , we get

| (23) | ||||

By Lemma 2.2 there exists such that

| (24) | ||||

and

| (25) | ||||

By (20) there exists such that

and

Together with (24) respectively (25) this gives that there exist constants such that

respectively

Combining these estimates with (23) shows

| (26) |

Note that the continuous martingale part of the semi-martingale (2) starting at is given by

| (27) |

and its predictable quadratic variation is

| (28) |

Therefore, by [41, Lemma 159], we have for all , that

| (29) | ||||

Since is Lipschitz and of at most linear growth,

Hence, by the Cauchy-Schwarz inequality, (20), and (21) there exists such that

Thus we have for all ,

| (30) |

From the continuity of and by the assumption that , we get that there exist such that

| (31) |

Combining this with (29) and (30) we get that there exists such that for all ,

For it trivially holds that

Choosing closes the proof.

∎

4.1.2 Estimation of the discontinuity crossing probability

Note that as in [4] from now on we write instead of . This is vindicated by the continuity of the compensators of and .

Let for all , ,

Lemma 4.3.

Let Assumptions 2.1 hold. Let with . There exists a constant such that for all , sufficiently small,

Proof.

For treating the Gaussian part we adopt arguments from [27, Proof of Lemma 5].

If , then for all , it holds that

So in this case, the assertion of the lemma holds for all .

Now let and let

Observe that are standard normally distributed, is Poisson distributed with parameter , are independent, is independent of since , and is independent of .

Let and let be sufficiently small such that

| (32) |

Then note that the following inclusion similar to [27, (20)] holds:

| (33) | ||||

In fact, with the additional condition , we are back to the jump-free case studied in [27]. The proof of (33) hence works exactly as the one for [27, (20)], which is a part of [27, Proof of Lemma 5].

Using (33) we obtain

| (34) | ||||

For the first term on the right hand side of (34), we use the fact that the sum of standard normally distributed random variables is normally distributed with mean 0 and variance 2.

| (35) | ||||

For the first term on the right hand side of (34) we use a standard Gaussian tail estimate.

| (36) | ||||

Lemma 4.4.

Let Assumptions 2.1 hold. Let . There exists a constant such that for all , sufficiently small,

Proof.

We follow the first part of [27, Proof of Lemma 6]. For ,

Therefore we may assume and hence . With this

| (37) | ||||

Let be such that . For it holds that and hence . Hence we may apply Lemma 4.3 and obtain that there exists a constant such that

Substituting gives

The Markov property yields

| (38) | ||||

Lemma 4.2 ensures that there exists such that

Combining this with (38) gives

∎

Lemma 4.5.

Let Assumptions 2.1 hold. There exists a constant such that for all ,

Proposition 4.6.

Let Assumptions 2.1 hold. There exists a constant such that for all , sufficiently small,

4.2 Main result

Theorem 4.7.

Let Assumptions 2.1 hold. Then there exists a constant such that for all sufficiently small,

Proof.

Let be as in (4) and be as in (5). Since is Lipschitz,

| (40) | ||||

| (41) |

and by the triangle inequality,

| (42) | ||||

| (43) |

There exists a constant such that

| (44) |

Hence our task is to estimate the second term in (42). For all let

and let for all , and . By the Meyer-Itô formula, which follows from [35, p. 221, Theorem 71], we obtain

This yields that

Using

we get

| (45) |

with

The Cauchy-Schwarz inequality yields

and the Burkholder-Davis-Gundy inequality, see, e.g., [19, Lemma 3.7], yields

Finally, since we get by Doob’s maximum inequality, Itô’s isometry, and the Cauchy-Schwarz inequality that

and analogously

Next, using that are Lipschitz, we get that

| (46) | ||||

The linear growth condition on , the Lipschitz continuity of , and the fact that is -measurable give

Let . Since and are independent of , is -measurable, and by the linear growth condition on , , and we get for ,

| (47) | ||||

This and Lemma 4.1 yield

| (48) | ||||

The Lipschitz continuity of establishes

By Lemma 4.1,

| (49) | ||||

| (50) |

For estimating first note that

| (51) | ||||

Analog to the estimate of above we obtain for the first term in (51),

| (52) | ||||

| (53) |

The second term in (51) will be analysed in the way introduced in [27], but adapted to our setup. It is essential that we have not applied the Cauchy-Schwarz inequality to the second term in (51) for recovering the optimal convergence rate . For this we define for all the sets

that is the set of all which lie on different sides of a point of discontinuity of the drift. So for we have that a Lipschitz condition is satisfied by . So for

| (54) | ||||

we can estimate the second term similar to above, that is

| (55) | ||||

For the first term in (54), observe that for all , ,

and hence

This and Lemma 4.1 yield for the first term in (54),

| (56) | ||||

Proposition 4.6 yields that

| (57) |

Combining (51) with (52), (54), (55), (56), and (57) we get

| (58) | ||||

Combining (45) with the estimates (46), (48), (49), and (58) shows that there exist constants such that

Applying Gronwall’s inequality yields for all ,

Combining this with (40), (42), and (44) finally yields

This closes the proof. ∎

4.3 Numerical examples

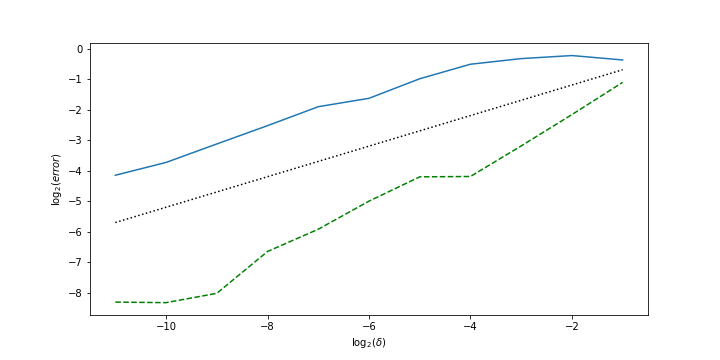

Finally, we do a numerical test to check whether the obtained convergence order can actually be observed. We choose the following coefficients:

Example 1.

Example 2.

and we set the parameter and the initial value . In Example 1 the drift is outward trending – away from the discontinuity. In Example 2 the drift points towards the discontinuity. Note that both examples satisfy Assumption 2.1. The -error is estimated by

where is an approximation of with step size ; the mean is taken over sample paths . Figure 1 shows plotted over for both examples. For Example 1 we observe that the slope of the estimated error is approximately the same as the slope of , which shows that the theoretical convergence order is attained. For Example 2 we observe that the slope seems to be even steeper than the slope of . The same behaviour has been observed and discussed in [11] in the Brownian additive noise case. This shows that numerical tests have to be interpreted carefully in the case of a discontinuous drift coefficient and knowing the theoretical rates is even more important.

Acknowledgements

M. Szölgyenyi is supported by the AXA Research Fund grant “Numerical Methods for Stochastic Differential Equations with Irregular Coefficients with Applications in Risk Theory and Mathematical Finance”.

P. Przybyłowicz is supported by the National Science Centre, Poland, under project

2017/25/B/ST1/00945.

References

- Benth et al. [2014] F. E. Benth, C. Klüppelberg, G. Müller, and L. Vos. Futures pricing in electricity markets based on stable CARMA spot models. Ener. Econom., 44:392–406, 2014.

- Buckwar and Riedler [2011] E. Buckwar and M. G. Riedler. Runge-Kutta methods for jump-diffusion differential equations. J. Comput. and Appl. Math., 236:1155–1182, 2011.

- Dareiotis and Gerencsér [2018] K. Dareiotis and M. Gerencsér. On the regularisation of the noise for the Euler-Maruyama scheme with irregular drift. 2018. arXiv:1812.04583.

- Dareiotis et al. [2016] K. Dareiotis, C. Kumar, and S. Sabanis. On tamed Euler approximations of SDEs driven by Lévy noise with applications to delay equations. SIAM J. Numer. Anal., 54:1840–1872, 2016.

- Deng et al. [2019a] S. Deng, C. Fei, W. Fei, and X. Mao. Generalized Ait-Sahalia-type interest rate model with Poisson jumps and convergence of the numerical approximation. Physica A: Stat. Mech. and its Appl., 533:122057, 2019a.

- Deng et al. [2019b] S. Deng, W. Fei, W. Liu, and X. Mao. The truncated EM method for stochastic differential equations with Poisson jumps. J. Comp. and Appl. Math., 355:232–257, 2019b.

- Dereich and Heidenreich [2011] S. Dereich and F. Heidenreich. Multilevel Monte Carlo algorithm for Lévy driven stochastic differential equations. Stoch. Proc. and their Appl., 121:1565–1587, 2011.

- Gardoń [2004] A. Gardoń. The order of approximations for solutions of Itô-type stochastic differential equations with jumps. Stoch. Anal. Appl., 22:679–699, 2004.

- Gardoń [2006] A. Gardoń. The order approximation for solutions of jump-diffusion equations. Stoch. Anal. Appl., 24:1147–1168, 2006.

- Göttlich et al. [2019a] S. Göttlich, K. Lux, and A. Neuenkirch. The Euler scheme for stochastic differential equations with discontinuous drift coefficient: A numerical study of the convergence rate. Adv. in Diff. Eq., 429:1–21, 2019a.

- Göttlich et al. [2019b] S. Göttlich, K. Lux, and A. Neuenkirch. The Euler scheme for stochastic differential equations with discontinuous drift coefficient: A numerical study of the convergence rate. Adv. in Diff. Eq., 429:1–21, 2019b.

- Gyöngy [1998] I. Gyöngy. A Note on Euler’s Approximation. Potent. Anal., 8:205–216, 1998.

- Halidias and Kloeden [2006] N. Halidias and P. E. Kloeden. A note on strong solutions of stochastic differential equations with a discontinuous drift coefficient. J. Appl. Math. and Stoch. Anal., 2006:1–6, 2006.

- Halidias and Kloeden [2008] N. Halidias and P. E. Kloeden. A note on the Euler–Maruyama scheme for stochastic differential equations with a discontinuous monotone drift coefficient. BIT Numer. Math., 48(1):51–59, 2008.

- Hefter et al. [2019] M. Hefter, A. Herzwurm, and T. Müller-Gronbach. Lower error bounds for strong approximation of scalar SDEs with non-Lipschitzian coefficients. Ann. Appl. Probab., 29:178–216, 2019.

- Higham and Kloeden [2005] D.J. Higham and P.E. Kloeden. Numerical methods for nonlinear stochastic differential equations with jumps. Numer. Math., 101:101–119, 2005.

- Higham and Kloeden [2006] D.J. Higham and P.E. Kloeden. Convergence and stability of implicit methods for jump-diffusion systems. Int. J. Numer. Anal. Mod., 3:125–140, 2006.

- Higham and Kloeden [2007] D.J. Higham and P.E. Kloeden. Strong convergence rates for backward Euler on a class of nonlinear jump-diffusion problems. J. Comp. and Appl. Math., 205:949–956, 2007.

- Hutzenthaler et al. [2012] M. Hutzenthaler, A. Jentzen, and P. E. Kloeden. Strong convergence of an explicit numerical method for SDEs with nonglobally Lipschitz continuous coefficients. Ann. Appl. Probab., 22:1611–1641, 2012.

- Kałuża and Przybyłowicz [2018] A. Kałuża and P. Przybyłowicz. Optimal global approximation of jump-diffusion SDEs via path-independent step-size control. Appl. Numer. Math., 128:24–42, 2018.

- Leobacher and Szölgyenyi [2016] G. Leobacher and M. Szölgyenyi. A numerical method for SDEs with discontinuous drift. BIT Numer. Math., 56:151–162, 2016.

- Leobacher and Szölgyenyi [2017] G. Leobacher and M. Szölgyenyi. A strong order 1/2 method for multidimensional SDEs with discontinuous drift. Ann. Appl. Probab., 27:2383–2418, 2017.

- Leobacher and Szölgyenyi [2018] G. Leobacher and M. Szölgyenyi. Convergence of the Euler-Maruyama method for multidimensional SDEs with discontinuous drift and degenerate diffusion coefficient. Numer. Math., 138:219–239, 2018.

- Leobacher et al. [2015] G. Leobacher, M. Szölgyenyi, and S. Thonhauser. On the existence of solutions of a class of SDEs with discontinuous drift and singular diffusion. Elect. Comm. in Probab., 20:1–14, 2015.

- Maghsoodi [1996] Y. Maghsoodi. Mean square efficient numerical solution of jump-diffusion stochastic differential equations. Ind. J. Stat., 58:25–47, 1996.

- Müller-Gronbach and Yaroslavtseva [2019] T. Müller-Gronbach and L. Yaroslavtseva. A strong order 3/4 method for SDEs with discontinuous drift coefficient. 2019. arXiv:1904.09178.

- Müller-Gronbach and Yaroslavtseva [2020] T. Müller-Gronbach and L. Yaroslavtseva. On the performance of the Euler-Maruyama scheme for SDEs with discontinuous drift coefficient. Ann. Inst. H. Poincaré Probab. Statist., 56:1162–1178, 2020.

- Neuenkirch and Szölgyenyi [2019] A. Neuenkirch and M. Szölgyenyi. The Euler-Maruyama scheme for SDEs with irregular drift: convergence rates via reduction to a quadrature problem. 2019. to appear in IMA J. Numer. Anal.

- Neuenkirch et al. [2019] A. Neuenkirch, M. Szölgyenyi, and L. Szpruch. An adaptive Euler-Maruyama scheme for stochastic differential equations with discontinuous drift and its convergence analysis. SIAM J. Numer. Anal., 57:378–403, 2019.

- Ngo and Taguchi [2016] H. L. Ngo and D. Taguchi. Strong rate of convergence for the Euler-Maruyama approximation of stochastic differential equations with irregular coefficients. Math. Comp., 85:1793–1819, 2016.

- Ngo and Taguchi [2017a] H. L. Ngo and D. Taguchi. On the Euler-Maruyama approximation for one-dimensional stochastic differential equations with irregular coefficients. IMA J. Numer. Anal., 37:1864–1883, 2017a.

- Ngo and Taguchi [2017b] H. L. Ngo and D. Taguchi. Strong convergence for the Euler-Maruyama approximation of stochastic differential equations with discontinuous coefficients. Stat. & Probab. Lett., 125:55–63, 2017b.

- Pamen and Taguchi [2017] O. M. Pamen and D. Taguchi. Strong rate of convergence for the Euler-Maruyama approximation of SDEs with Hölder continuous drift coefficient. Stoch. Proc. Appl., 127:2542–2559, 2017.

- Platen and Bruti-Liberati [2010] E. Platen and N. Bruti-Liberati. Numerical Solution of Stochastic Differential Equations with Jumps in Finance. Springer Verlag, Berlin, Heidelberg, 2010.

- Protter [2005] P. Protter. Stochastic Integration and Differential Equations. Springer, Berlin-Heidelberg, 2005.

- Przybyłowicz [2016] P. Przybyłowicz. Optimal global approximation of stochastic differential equations with additive Poisson noise. Numer. Alg., 73:323–348, 2016.

- Przybyłowicz [2019a] P. Przybyłowicz. Optimal sampling design for global approximation of jump diffusion stochastic differential equations. Stochastics: Int. J. Probab. Stoch. Proc., 91:235–264, 2019a.

- Przybyłowicz [2019b] P. Przybyłowicz. Efficient approximate solution of jump-diffusion SDEs via path-dependent adaptive step-size control. J. Comp. and Appl. Math., 350:396–411, 2019b.

- Shardin and Szölgyenyi [2016] A. A. Shardin and M. Szölgyenyi. Optimal control of an energy storage facility under a changing economic environment and partial information. Int. J. Theoret. Appl. Fin., 19:1–27, 2016.

- Shardin and Wunderlich [2017] A. A. Shardin and R. Wunderlich. Partially observable stochastic optimal control problems for an energy storage. Stochastics: Int. J. Probab. Stoch. Proc., 89:280–310, 2017.

- Situ [2006] R. Situ. Theory of Stochastic Differential Equations with Jumps and Applications: Mathematical and Analytical Techniques with Applications to Engineering. Springer Science & Business Media, 2006.

- Veretennikov [1981] A. Yu. Veretennikov. On strong solutions and explicit formulas for solutions of stochastic integral equations. Math. USSR Sbor., 39:387–403, 1981.

- Veretennikov [1982] A. Yu. Veretennikov. On the criteria for existence of a strong solution of a stochastic equation. Theory Probab. Appl., 27:441–449, 1982.

- Veretennikov [1984] A. Yu. Veretennikov. On stochastic equations with degenerate diffusion with respect to some of the variables. Math. USSR Izvestiya, 22:173–180, 1984.

- Zvonkin [1974] A. K. Zvonkin. A transformation of the phase space of a diffusion process that removes the drift. Math. USSR Sbor., 22:129–149, 1974.

Paweł Przybyłowicz 🖂

Faculty of Applied Mathematics, AGH University of Science and Technology, Al. Mickiewicza 30, 30-059 Krakow, Poland

pprzybyl@agh.edu.pl

Michaela Szölgyenyi

Department of Statistics, University of Klagenfurt, Universitätsstraße 65-67, 9020 Klagenfurt, Austria

michaela.szoelgyenyi@aau.at