Centralizing-Unitizing Standardized High-Dimensional Directional Statistics and Its Applications in Finance

Abstract

Cross-sectional “Information Coefficient” (IC) is a widely and deeply accepted measure in portfolio management. The paper gives an insight into IC in view of high-dimensional directional statistics: IC is a linear operator on the components of a centralizing-unitizing standardized random vector of next-period cross-sectional returns. Our primary research first clearly defines IC with the high-dimensional directional statistics, discussing its first two moments. We derive the closed-form expressions of the directional statistics’ covariance matrix and IC’s variance in a homoscedastic condition. Also, we solve the optimization of IC’s maximum expectation and minimum variance. Simulation intuitively characterizes the standardized directional statistics and IC’s p.d.f.. The empirical analysis of the Chinese stock market uncovers interesting facts about the standardized vectors of cross-sectional returns and helps obtain the time series of the measure in the real market. The paper discovers a potential application of directional statistics in finance, proves explicit results of the projected normal distribution, and reveals IC’s nature.

keywords:

high-dimension, directional statistics, cross-sectional returns, Information Coefficient, projected distribution, portfolio optimization1 Introduction

Directional statistics concerns a population of unit multivariates in norm, or, equivalently, on a unit hypersphere. In some application scenarios of high-dimensional statistics, people usually standardize the multivariate data by centralizing and unitizing the data taken from general like . Such centralizing-unitizing standardized multivariate data is a particular direction statistic orthogonal to the vector whose elements are all . The dimension is often higher than and even more than , particularly in finance. There is little literature about the probabilistic characteristics and statistical inference of direction statistics on a high-dimensional sphere, let alone such centralizing-unitizing standardized multivariate concerned in the paper.

This paper’s original idea is motivated by questions raised in the industry: “For a running strategy, what kind of time series can be considered an invalid strategy? Is there a feasible statistical inference method of data?” is the abbreviation of Information Coefficient of the predicted and actual return values. The first and fundamental thing is to define in a probabilistic theoretical viewpoint and to reveal the probabilistic and statistical properties. In a probabilistic view, we define as a linear operator on a centralizing-unitizing standardized multivariate. The measures the similarity between the series of the predicted and actual values, like a metric function. In active portfolio management, can be regarded as the weighted sum of the standardization of next-period cross-sectional returns. In the rest of this paper, we denote by , where is a random vector on , is the standardization of on a hypersphere, and is the predicted values and the weights. The precise definition is in (10) of Section 2. The time series of is an interesting topic in academia and industry. Coggin and Hunter [1983] thought that it originated from sample errors, and used “meta-analysis” to correct it. After that, Qian and Hua [2004] re-distinguished the definition of raw and risk-adjusted , regarding ’s volatility as “strategy risk”. Ye [2008] also investigated the impact of ’s variation on the performance of investment specifically. Ding and Martin [2017] systematically developed a stationary econometric model of for mean-variance portfolios. The dynamic modeling of realized is an essential and lasting issue in financial investment research.

Since a pioneer work of Fisher [1953], directional statistics has flourished to a certain degree. Mardia [1972], Mardia and Jupp [2000], and Ley and Verdebout [2017, 2018] summarized and developed the main works. The current development of directional statistics helps us understand ’s nature, and provides some important methods and tools. However, due to ’s high-dimensional essence, it is not easy to directly apply the existing results and methods. A natural idea is first to explore the directional statistical properties of a standardized high-dimensional normal distribution. Even in a normal distribution background, it is also a challenging problem. One of the most cutting-edge research concerned in the paper is Presnell and Rumcheva [2008], which obtained the closed-form expressions of the mean direction () and mean resultant length () of the projected normal distributed in the homoscedastic condition of .

In this paper, we set up models and develop their probabilistic properties. First, we clarify the standardized random vector and its linear combination. We define the centralizing and unitizing standardization as a mapping and generate the standardized random vector on a hypersphere from the pre-standardized on , which is different from the projected random vector . Given the standardized weight , we define the linear combination of the standardized random vector’s components , standing for in finance. Second, we develop their probabilistic properties. We propose a representation theorem to connect the standardized random vector with a projected one . In a homoscedastic condition, we express ’s / and covariance matrix explicitly. We then derive ’s expectation and variance from ’s first two moments and their closed-form expressions in the homoscedastic condition. Third, we discuss the optimization problems of ’s expectation and variance: ’s maximum is ’s , ’s minimum is ’s second smallest eigenvalue, and the two optimizations share the same solution in the homoscedastic condition.

We carry out the numerical simulation, aiming to supplement the probabilistic properties. Due to the standardized distribution’s inherent complication, we can hardly get an intuitive sense of the theory. We illustrate the impact of the parameters of and on the intuitively in -dim cases and simulate the p.d.f.’s of with real market parameters, from which we analyze the impact of the dimension and heteroscedasticity, meeting the previous conclusion in Coggin and Hunter [1983] and Grinold [1994]. We also compare the approximate in theory and its true value in simulation.

We implement empirical studies based on the Chinese stock market to explore the high-dimensional statistics in the real market. For one thing, we assume the returns to be i.i.d., and clarify their statistical properties. Specifically, we first explore the descriptive statistics of the sample of the standardized vectors in a traditional approach in directional statistics, such as the sample / and the scatter matrix. The high- and low-value components of the sample vary in different patterns, indicating the distinct behaviors between the high- and low-return stocks. The scatter matrix’s eigenvalues are uneven in the sense that the sum of the largest eigenvalues accounts for more than of the sum of the all ones, implying the standardized returns vary along with few specific directions. Then, we reduce the dimension of the sample , by taking their inner product with a vector such as the sample , and generate the -dim sample . We illustrate the descriptive statistics, histograms, and box plots of . The market’s centralization varies in different time windows, and may be multimodal distributed. The sample of and the sample standard deviation of result in opposing conclusions about the variance, which could be interpreted as their different perspectives. What’s more, we analyze the connection between pre- and post-standardized and : The sample correlation coefficient between and is significantly lower than that between and on average, which, in finance, means that the standardization eliminates the beta part of the returns. For another, we analyze their time-series properties. In detail, we illustrate the time series of the representative and , discovering similar volatility clustering phenomena. The standardized has more information than the pre-standardized . The time series of the estimate of is compared with the cross-sectional standard deviation, revealing different market information.

2 Models and Theoretical Results

Given the probability space , directional statistics concerns the random vector , where . We introduce two basic numerical characteristics: the mean direction () and the mean resultant length () of :

where the plays the role of the expectation and the the variance (see Mardia and Jupp, 2000, §9.2, p. 163-164 and Ley and Verdebout, 2017, §1.3, p. 10-12 for more details). For simplicity, we assume that, in the paper, all the ’s are strictly greater than , so the ’s are well-defined. One of the most common approaches to set up a random vector on relies on the following projection function:

| (1) | ||||

Then, for a random vector , we have , and call it has a projected distribution. Particularly, if has a multivariate normal distribution, then has a projected normal distribution (PND, see Mardia and Jupp, 2000, §1.5, p. 12 and §3.5.6, p. 46).

2.1 Model Setup and Basic Probabilistic Properties

In some studies concerning high-dimensional random vectors taking values in , people standardize the data cross-sectionally by centralization and unitization, say . The standardized random vectors are a particular kind of random vectors in directional statistics. It is fundamentally different from the function (1) because the centralization leads to the natural singularity of its covariance matrix. This subsection discusses the connection between pre-standardized high-dimensional random vectors in and the standardized direction statistics in , and explore the properties of the linear combination of the components of the directional statistics.

2.1.1 The Standardized Random Vector in Directional Statistics:

We define the standardization function, introduce the particular random vector, and then clarify its basic properties with -dim cases.

To begin with, we define the centralizing and unitizing standardization function . Define the -dim centering matrix as

| (2) |

where is an -dim identity matrix and . Given , is similar to subtracting the mean from every component of a vector, and to , where . Thus, is the result of the centralizing and unitizing standardization process of . For convenience and conciseness, we define the standardization process formally as a multivariate function:

| (3) | ||||

where is excluded in the domain for well-definition.

Then, we introduce the standardized random vector . Give a random vector , such that its expectation , and its covariance matrix ( is positive definite). We are interested in the random vector

| (4) |

which is the standardized random vector from with function (3).

Last, we clarify the basic properties of in the following five points. First, the support of the random vector is , where , which is the intersection of the unit sphere centered at the origin and the hyperplane with normal passing through the origin. Thus, is a particular random vector in directional statistics subjecting to .

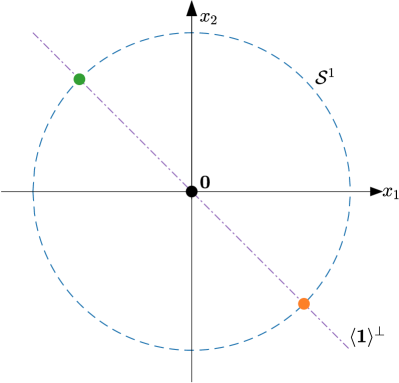

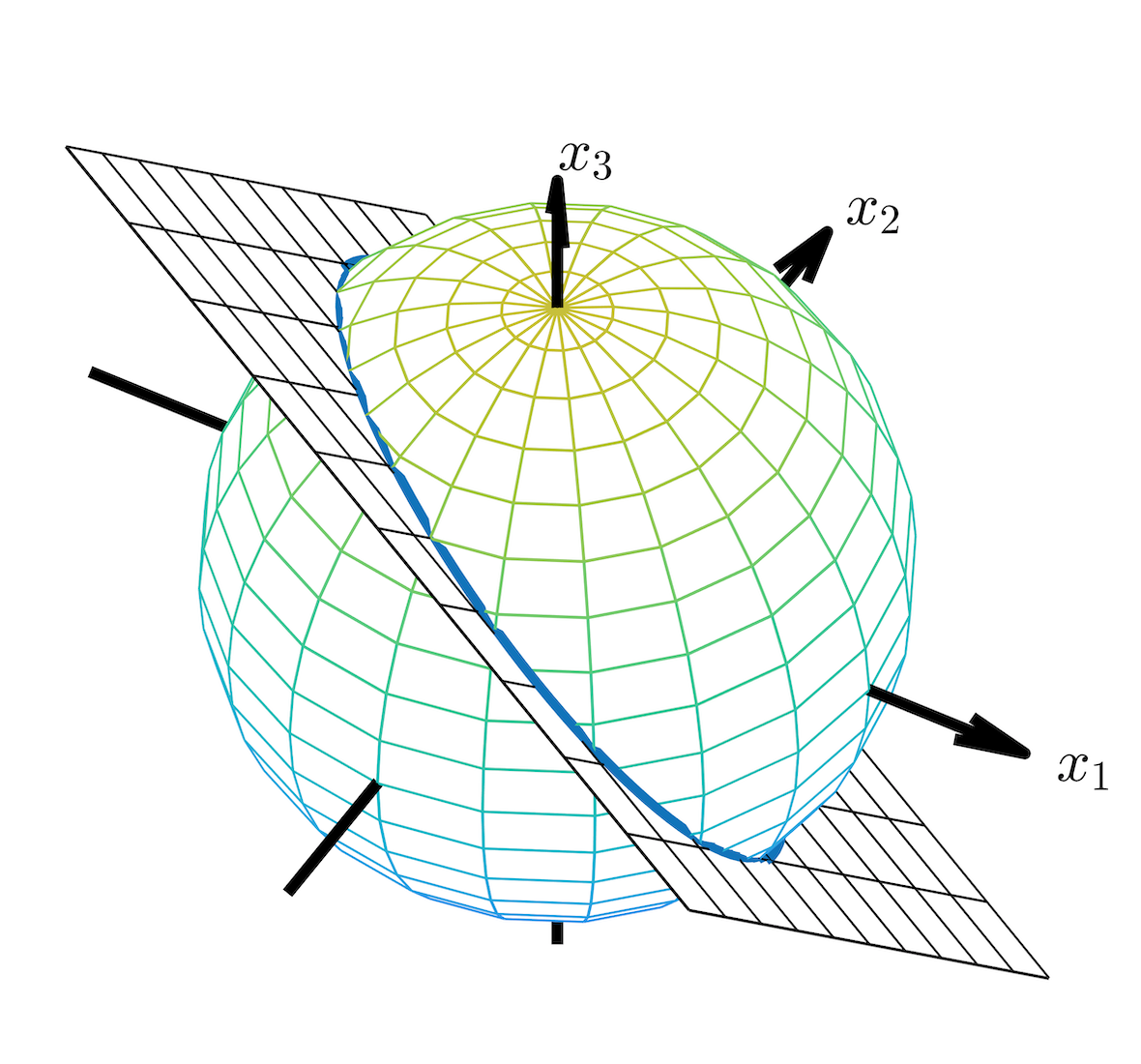

To illustrate the generality and particularity of intuitively, we show the supports of of and in Figure 1. In detail, subfigure 1(a) portrays the case: The dashed blue circle is , and the purple dotted line is the subspace . The support of is the intersection of them — a two-point set composed of the orange dot and the green dot: . Subfigure 1(b) illustrates the case: the light-colored sphere is , and the black plain is the subspace . The support of is the intersection of them — the blue circle.

Second, in high-dimensional cases, notably when , the support area diminishes dramatically. In detail, the surface area of the support is ,where . In other words, the surface area of the support decreases exponentially, as the dimension increases. In finance, the dimension of is generally higher than .

Third, the random vector is a compound operator of . In detail, there are two projections implied in . One is the linear projection , which projects from to the subspace . leads to the degeneration of the random vectors — the covariance matrix of must be singular.The other is the directional projection, which projects radically on the sphere . It is also inherently difficult because there is some “singular nature” on [Mardia and Jupp, 2000, p. 166].

Fourth, there is no ready-made result about . Although the transformation is pervasive in academia and industry, the results of the transformed variables are rare. In the existing literature, models were usually set up on the sphere directly, particularly on cases like the paleomagnetism and wildfire orientation.

Fifth, ’s basic properties in the -dim cases are given in Proposition 1, helping us have a fundamental and concrete understanding of .

Proposition 1.

Given a -dim random vector , we have

| (5) |

where . The distribution of is:

The and of are

| (6) | ||||

| (7) |

Proposition 1 is a general -dim proposition in the sense of the weak assumption of the distribution of , showing an intricate property of : is affected by only a part of the information in — In the -dim case, it is that determines and its distribution and numerical characteristics, irrelevant to the other information in . Besides, (6) shows that, when , the . In directional statistics, it corresponds to the case where is symmetric about the origin. One of the possible sufficient assumption is that is i.i.d.. In the paper, we assume that .

Furthermore, we give ’s properties of the -dim normal distributed for a deeper understanding. If has a -dim normal distribution, say then

| (8) | ||||

| (9) |

where is the cumulative distribution function of the standard normal distribution. For one thing, (8) shows that increases with the dispersion () and the correlation coefficient , but decreases with the volatility . Particularly, when there is no dispersion (i.e., ), we have , implying that ’s is not well-defined. For another, as implied in (9), determines , because, in the 2-dim case, . The choice of the two possible vectors is based on whose expectation of the component , say , , is higher.

2.1.2 The Linear Combination of the Components of :

Instead of the -dim random vector itself, some practical problems emphasize the linear combination of ’s components. This subsection first defines the linear combination, lists its properties in -dim cases, and interprets them in finance.

To begin with, given a deterministic vector representing the forecasts/weights, we have , . Thus, we restrict the domain of to , and define function

| (10) | ||||

and denote (10) by

For the random vector defined in (4), we define a random function as

Then, we list the expression, distribution, and numerical characteristics of the -dim in the following four points. First, it is symmetric with domain and function value. The domain of in is symmetric , as in Figure 1(a), so there are only two ways to combine and . The values are also symmetric: . Without essential difference, we denote and only discuss in a certain case. Second,

Thus, is a random function of , taking value in . Third, the distribution of is

which shows that the distribution of is a two-point distribution determined by the , also irrelevant to the other exact values of . Fourth, the numerical characteristics of the random variable are

For the expectation, is symmetric about : . If and , then , and vice versa. Its implication is entirely intuitive: If the “order” of is equal to the “order” of , then the expectation is positive. For the variance, is irrelevant to the choice of but only determined by .

In finance, is interpreted as the Information Coefficient (IC), a popular and useful performance measure of investment strategies. IC is

| (11) |

where is the return of stock at the next-period time , and is the forecasts of the return at the current-period time . IC is the same as , where is the standardized forecasts and is the next-period returns . The randomness in IC is similar to that in at time . From this point of view, IC is the weighted sum of rather than the correlation coefficient of two random variables.

The research on is challenging. First, ’s value is in , free from the support of the pre-standardized random vector . We have found little research on the linear combination of the components of a random vector on , let alone that of the particular random vector . Second, the probabilistic property of for given is nontrivial. As is clarified above, the research on is difficult, so investigating from is also hard. Meanwhile, there need to develop tools and techniques to investigate .

2.2 The Probabilistic Properties of and

and are the main research topics in the paper. This subsection discusses their specific probabilistic properties. We first extend the -dim case studies on in § 2.1.1 to a more general condition, exploring the distribution, , and of the random vector . Based on , we introduce the distribution and numerical characteristics of .

2.2.1 The Properties of

The properties of of a general () dimension are given below. Specifically, we transform the particular to a general one in directional statistics. Further, we give closed-form expressions of ’s numerical characteristics in a relatively general condition.

When is a general -dim random vector, we can transfer into a particular projected random vector. Thus, we give a representation theorem, which transforms into an -dim component-uncorrelated random vector (i.e., is diagonal).111 In this paper, is an -dim column vector. If exists, then is the first components of , i.e., . is an matrix. If exists, then we use to represent the -th order leading principal submatrix of , i.e., .

Theorem 2.

Given an -dim random vector , whose covariance matrix is positive definitive, then there exists an -dim orthogonal matrix such that

| (12) |

and the covariance matrix is diagonal, where

| (13) | ||||

| (14) | ||||

| (15) |

is an -dim orthogonal matrix defined as

| (16) |

and . is an -dim orthogonal matrix such that is a diagonal matrix.222 In other words, is the orthogonal matrix such that the covariance matrix of is a diagonal matrix . is the -dim orthogonal matrix such that the covariance matrix of is a diagonal matrix .

Theorem 2 transforms into a standardized multivariate distribution, say the projected distribution. One of the direct applications of Theorem 2 is the concise expression of numerical characteristics of : Corollary 3.

Corollary 3.

If has a multivariate normal distribution, then is a component-independent random vector of multivariate normal distribution. So Theorem 2 transforms into , which is a random vector of projected component-independent normal distribution. has some basic and standard distribution due to its diagonal covariance matrix. Thus, we could obtain ’s numerical characteristics from a projected component-independent normal distributed .

Unfortunately, there are very few results of the closed-form expressions of the and of a projected multivariate normal distribution, even in the independent case. The most cutting-edge research that we have known about the closed-form expressions of the and of a projected normal distribution is Presnell and Rumcheva [2008]. It gives the closed-form expressions in a particular case, where the covariance matrix of is a scalar matrix , listed as Proposition 5 in the paper.

In Theorem 4, we obtain closed-form expressions of the and with a relative general dependent case, in which the components of the pre-standardized normal-distributed random vector is homogeneous.

Theorem 4.

Given , where is a correlation coefficient matrix with off-diagonal elements equaling to , i.e.,

| (19) |

we have

| (20) | ||||

| (21) |

where is defined in (25).

We give some interpretations of Theorem 4 here. First, is a covariance matrix widely used in statistical modeling, such as responds’ covariance matrix with the single-factor model. entails the special independent conditions: If , then . Second, under this specific situation, (20) implies an exchangeability of operators and , that

| (22) |

only depends on , irrelevant to the correlation coefficient between ’s components in the case of homogeneous distribution. Third, increases with the dispersion of (i.e., ) and the correlation coefficient , while decreases with volatility . The properties are similar to that in the -dim case.

Proposition 5 (Eq(6) in Presnell and Rumcheva [2008]).

Given an -dim random vector , for the projected normal distribution , we have

| (23) | ||||

| (24) |

where

| (25) |

and is the confluent hypergeometric function of the first kind.333 is a solution of a confluent hypergeometric equation, which can be written as where . When , it can be represented as an integral: For detailed properties, one can refer to Abramowitz and Stegun [1964, p. 503, §13].

2.2.2 The Properties of

is a random function. Given , then is a random variable. The expectation and variance of are discussed.

First, the expectation is

| (26) |

spans on — If , then reaches the maximum , and if , then the minimum . Therefore, is a strict bound of , i.e.,

| (27) |

When , i.e., the particular condition in Theorem 4, we have

| (28) |

So when , reaches the maximum , and when , reaches the minimum .

Second, the variance is

| (29) |

By (12) in Theorem 2, we have , where defined in (14) is a positive definite diagonal covariance matrix . Consequently,

| (30) |

If we figure out the covariance matrix of the particular projected component-uncorrelated distribution , then ’s variance can be expressed.

However, solving the covariance matrix of the projected distribution is not an easy work. The following result (see [Mardia and Jupp, 2000, Eq(9.2.12), p. 166]) is one of the relative works for :

| (31) |

We obtain a closed-form expression of , where has a homoscedastic normal distribution.

Theorem 6.

The proof is enlightened by Presnell and Rumcheva [2008]. In the proof, the diagonal of the covariance matrix is easy to derive, but the closed-form expression of each element is a nontrivial result. In essence, we give the expression of refer to Presnell and Rumcheva [2008].

The skeleton of the proof of Theorem 6.

We first show is a diagonal matrix like (32), and then prove its closed-form expressions.

To begin with, is a diagonal matrix of the form of (32) — . The diagonal is deduced by symmetry and independence.

Furthermore, we need to prove

| (35) | ||||

| (36) |

in which .

Last, the closed-form expression of is solved in three steps. First, we give the simplified integral expression of .

Second, the integral can be simplified by modified Bessel function .

Third, it can be concisely expressed by confluent hypergeometric function.

When , we deduce a closed-form expression of .

Theorem 7 implies that, given , the extremums of are or , and they are reached when or . We discuss the details of the optimization of ’s expectation and variance in the next subsection.

2.3 The Optimization of

In some applications of , we concern about the maximum of the expectation or the minimum of the variance of subjecting to . Mathematically, it is an optimization problem of or . This subsection specifies the optimization and connects it with above .

2.3.1 The Maximization of the Expectation and the Minimization of the Variance

First, we give a general result: maximizes the expectation. Proposition 8 connects the optimization problem with the and of .

Proposition 8.

Given an -dim random vector such that , then the solution to the optimization problem

uniquely exists. The unique solution is the of , i.e., The value of the maximum is the of , i.e.,

The proposition is a direct corollary of (26). However, in finance, and are the core topics, whose properties are of paramount importance. Specifically, in active portfolio management, a strategy of a high average of IC is equivalent to maximizing . If the joint distribution of the standardized returns of assets within a given pool were known, the maximum of IC and the optimal portfolio should be equivalent to the and of the standardized returns of assets within the pool.

Second, we give the minimization of the variance of in the following proposition.

Proposition 9.

Given an -dim random vector whose covariance matrix is positive definitive, then the minimum value of the optimization problem

| (37) |

is the second smallest eigenvalue of . The solutions to the optimization problem are the corresponding unitized eigenvectors.

We interpret Proposition 9. First, the uniqueness of the solution relies on the distribution of . For instance, in the case , every minimizes the variance. Second, the eigenvectors corresponding to the smallest eigenvalue are excluded from the domain, so the minimum value to the optimization problem of (37) is the second smallest eigenvalue. To be more specific, different from (37), the minimum value of the optimization problem

| (38) |

is the smallest eigenvalue of , i.e., . The solution is the corresponding unitized eigenvectors . However, . Therefore, for (37), we can only take the second smallest eigenvalue and its corresponding unitized eigenvector.

2.3.2 In the Homoscedastic World

When is homoscedastic, i.e., , is the mean-variance solution.

Corollary 10.

It implies that in the homoscedastic world, the same solution applies to two different optimizations: the expectation’s maximization and the variance’s minimization. In detail, there are two particular instances of the corollary: and . When , it is the application of (26). The optimization problem is , and the maximum is , which is reached at . When , it is the corollary of Theorem 7. The optimization problem is equivalent to . The minimum is , which can be reached at .

3 Simulation

In this section, we aim to get a better understanding of and figure out the distribution of given or . We begin the analysis with an intuitive -dim background and then consider a realistic financial market environment with -dim and -dim.

3.1 The Numerical Analysis of -Dim

In this subsection, we examine how varies with respect to the distribution changes on , where

We simulate the samples of for changed and separately.

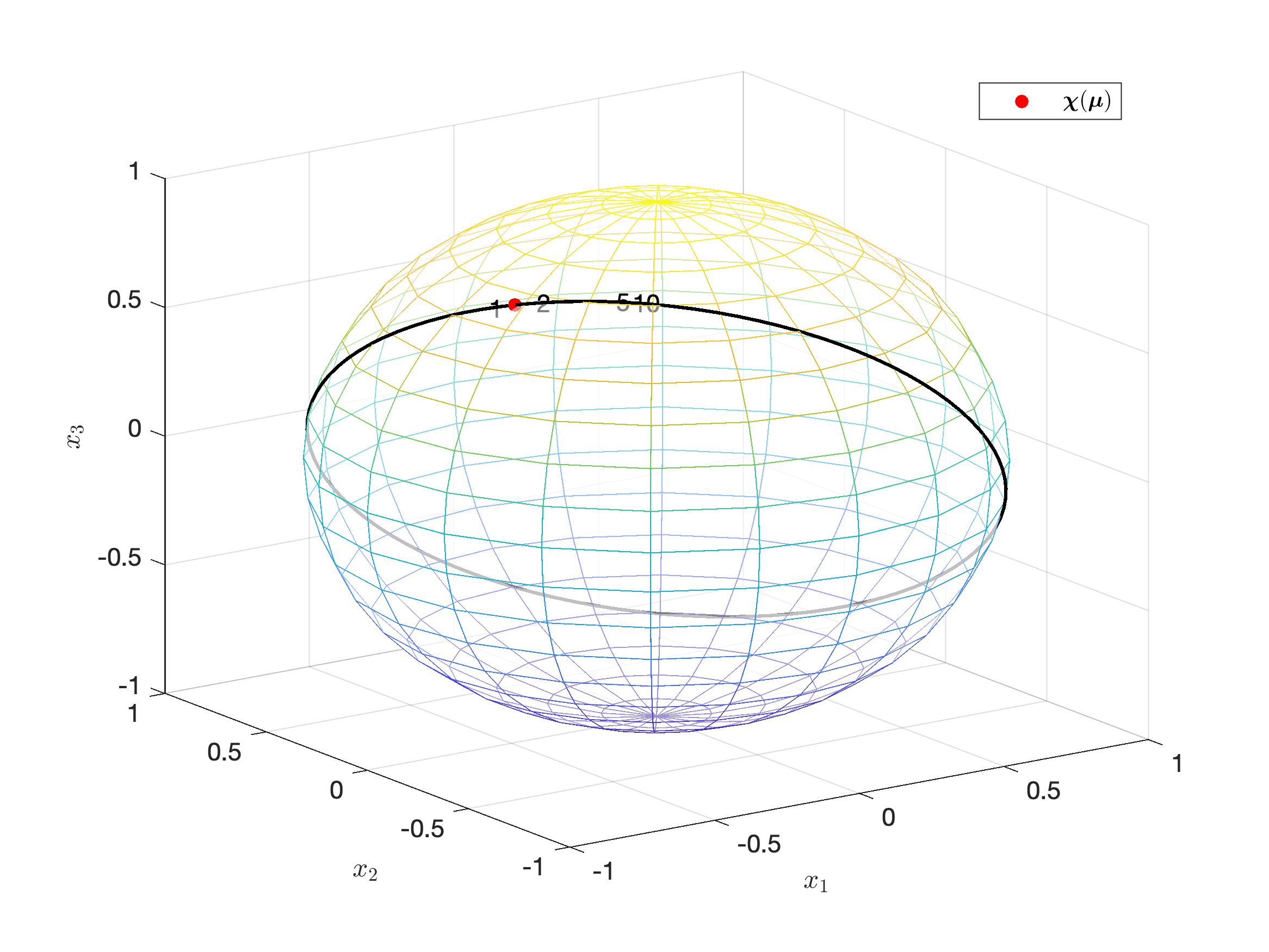

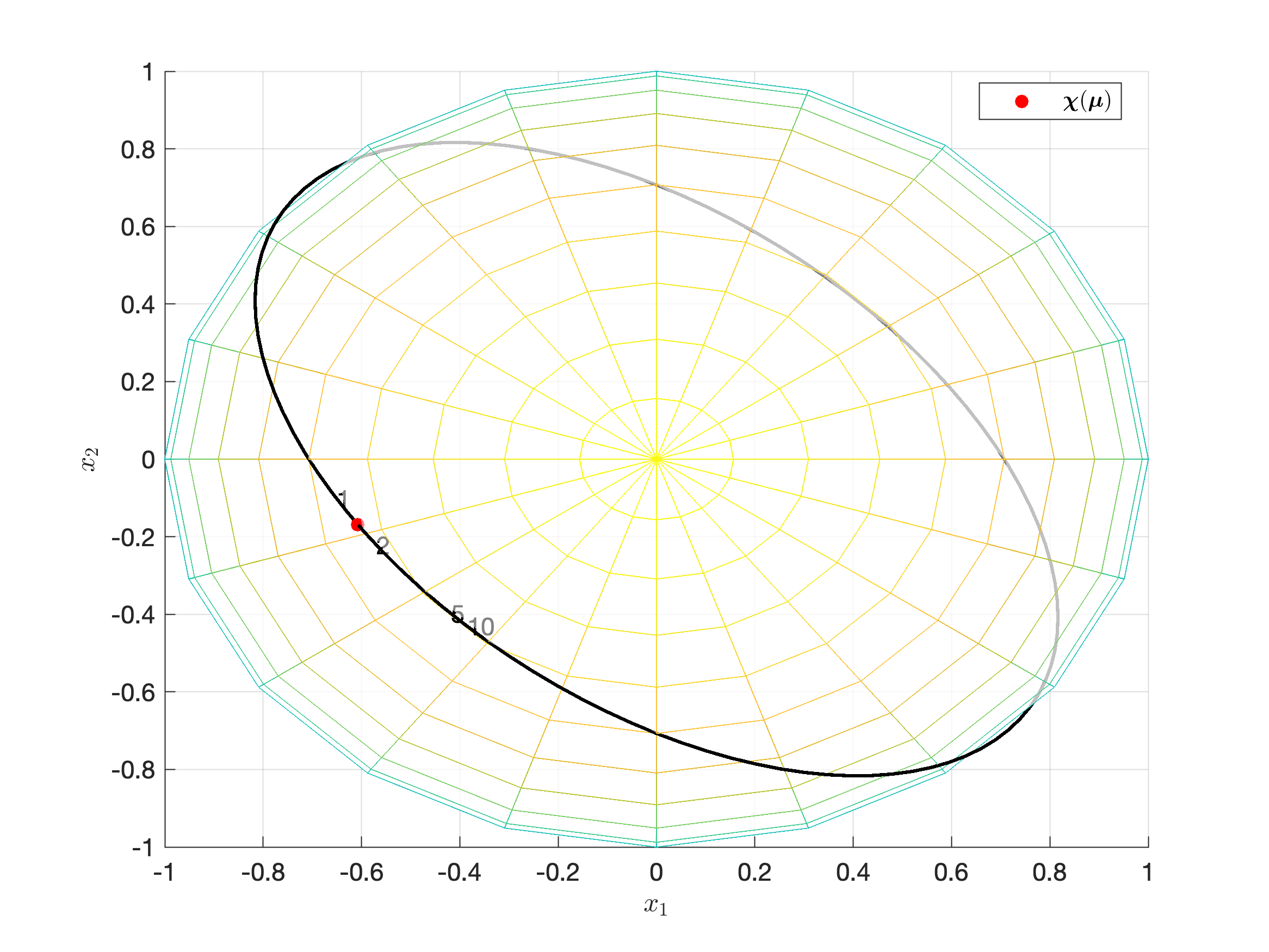

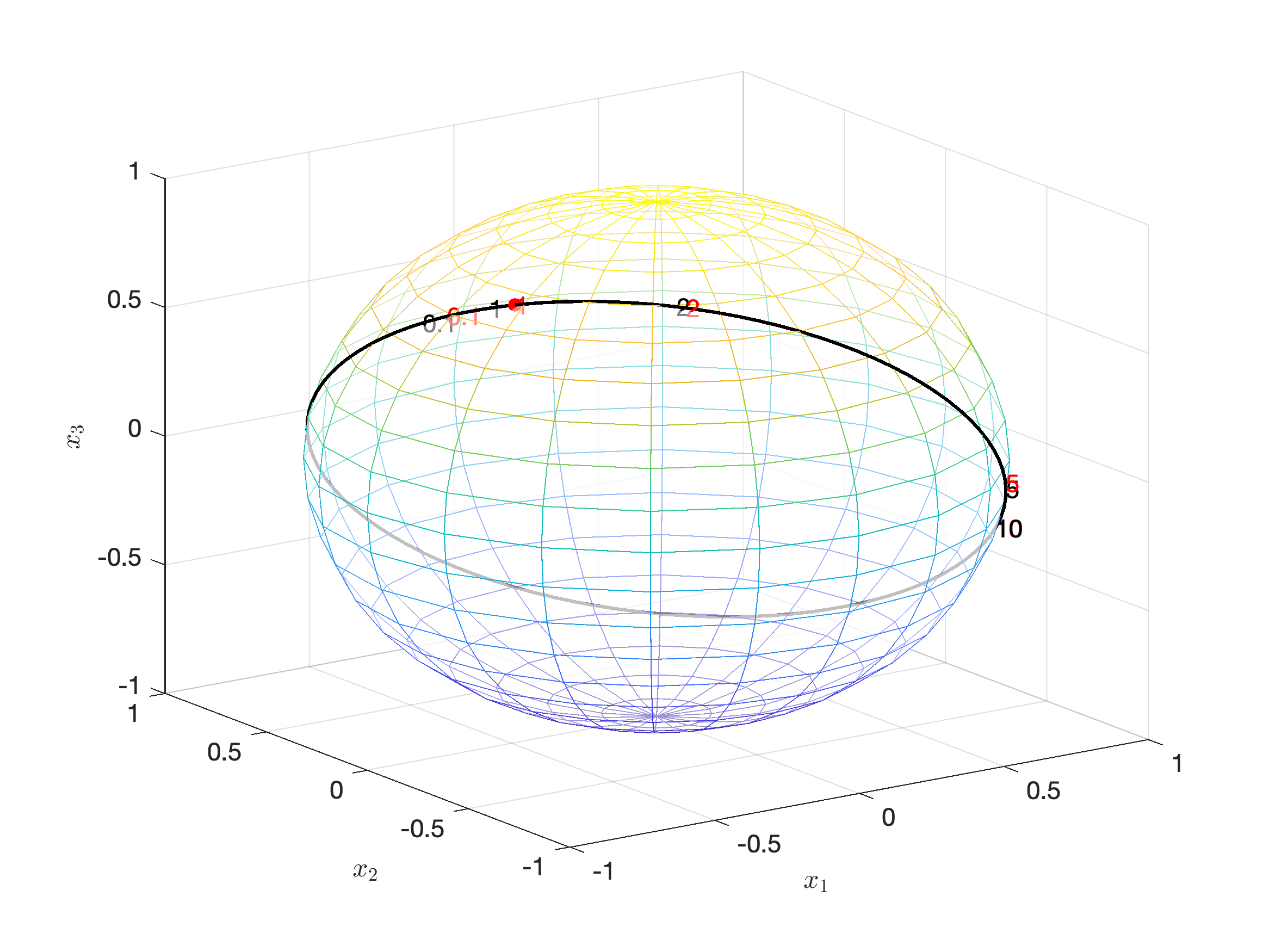

First, we focus on the impact of the heteroscedasticity of on . Figure 2 shows the simulated results, where subfigure (2(b)) is a top view of (2(a)). In detail, the red point is , which, in the above homoscedastic condition, equals to the . The numbers are all ’s of different parameters. The number is the simulated from in which , in other words, the standard deviation of the first component is amplified by .

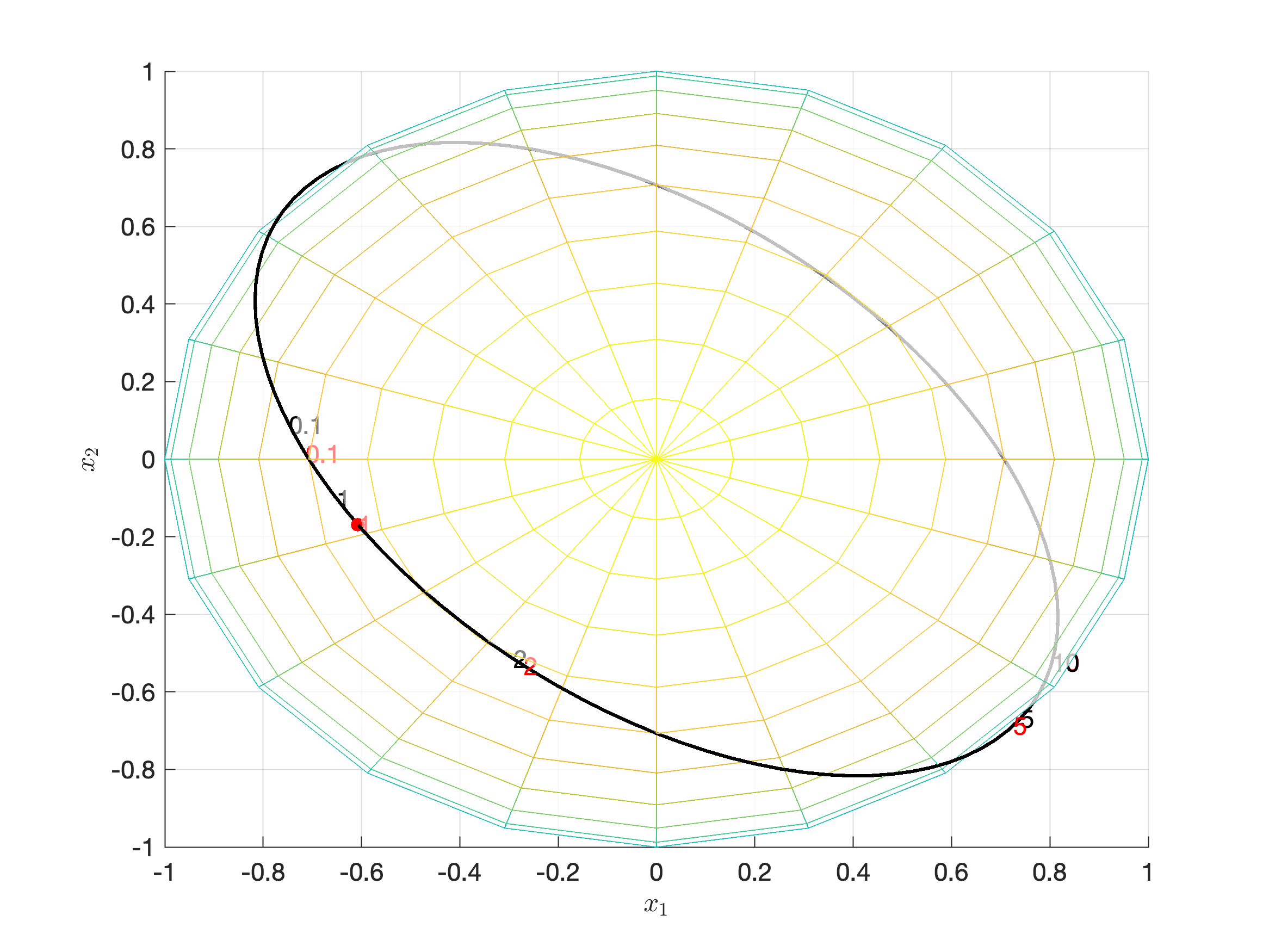

Second, we illustrate the impact of . Figure 3 shows the simulated results. In detail, the red numbers are the ’s and the black numbers are the , where number ’s are calculated and simulated from in which , . In other words, we amply the first component by .

We interpret Figure 2 and 3. First, is different from , as the red point is different from the number . It accords that the structure of in Theorem 4 is a sufficient condition that renders the equal to . Second, the more heteroscedastic the , the more the difference between and that is represented by number from , , to . Third, the distance between the red and black is broader than . Thus the higher the , the smaller the difference between the and .

3.2 The Distribution of High-Dimensional

To get more realistic results, we consider high-dimensional cases with parameters estimated from the real market — a part of the component stocks of CSI 300 Index of Chinese stock market. Specifically, we calculate the sample mean and covariance matrix of the simple daily returns from January 2017 to November 2018 as the parameters . In detail, we choose the first stocks to generate and , and the first stocks to generate and . All the simulation parameters are in A.

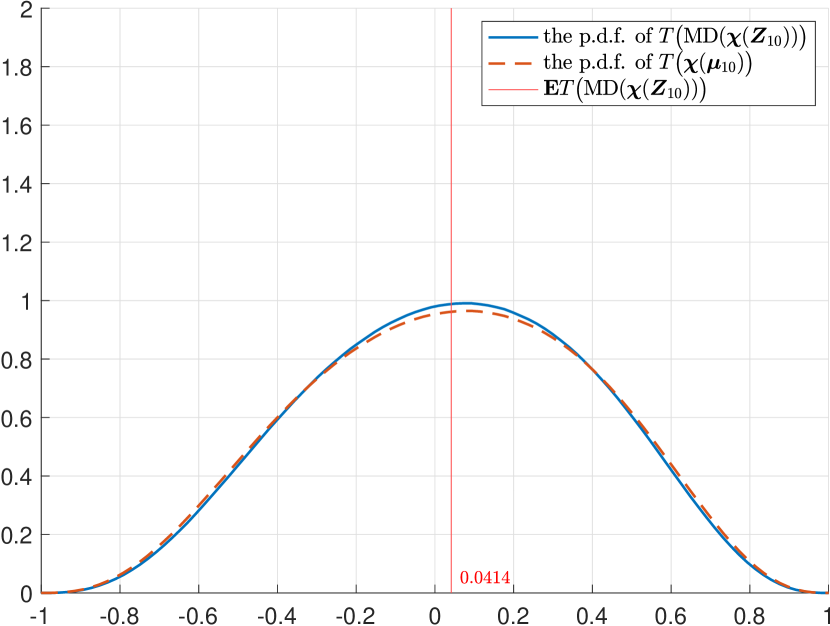

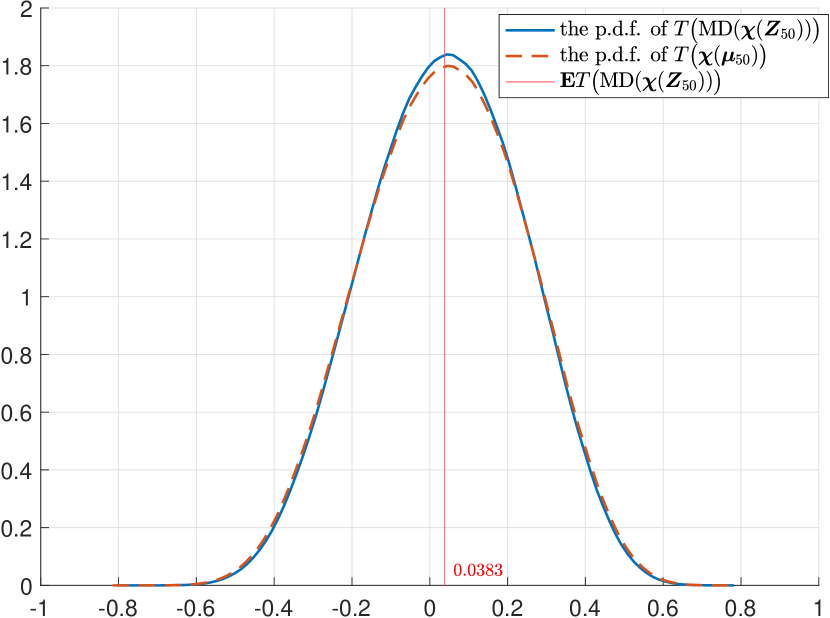

We simulate the sample distribution of , when and , on , , and . By amplifying the maximum of the standard deviance by , we derive the heteroscedastic from .

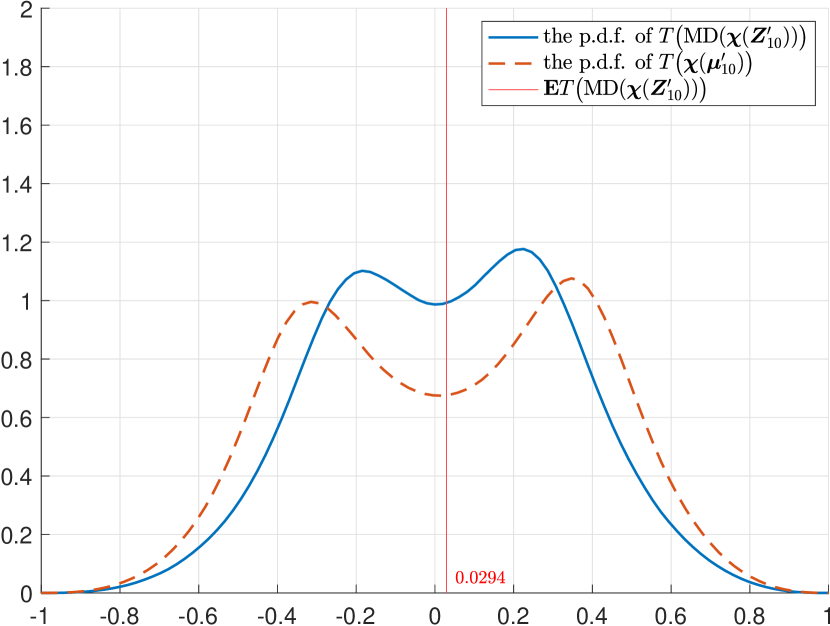

The simulated kernel smoothing empirical p.d.f.’s of are in Figure 4 where the red vertical line is , i.e., the by Proposition 8.

Some points in Figure 4 are discussed below in detail. First, there is little difference between the in subfigure (4(a)) and (4(b)). It seems that the reveals some basic facts of the financial market — the value of in expectation with a known future in the real market is usually around . It follows Grinold [1994, p. 10-11]: “A reasonable IC for an outstanding (top ) manager forecasting the returns on stocks is about . If the manager is good (top quartile), is a reasonable number.” Second, the difference of volatility of the p.d.f.’s between the two subfigures (4(a)) and (4(b)) is significant, where is more volatile than . It shows that the dimension mainly impacts the variance, rather than the expectation. In portfolio management, the increase in the number of stocks does not impact ’s mean, but significantly decreases ’s variance. Third, the difference between subfigures (4(a)) and (4(c)) is significant, suggesting that heteroscedasticity leads to the distinction of the distribution between . The heteroscedasticity renders the p.d.f. of no longer a bell-shaped unimodal one. Fourth, the difference between the p.d.f.’s of and in subfigure (4(c)) is more significant than that in other subfigures. It enlightens us that, in some cases, replacing with may lead to fallacy.

3.3 Comparing the Simulation and the Theoretical Results of High-Dimensional

In this subsection, we propose an approach to estimate using estimated parameters of and compare the approximate result with the true value by simulation.

According to Theorem 4, can be calculated approximately by regarding the as the . In the simulation, we have , , and . Therefore, , while the simulated true value is . Furthermore, by a similar approach, we can calculate the -dim cases where , while the simulated true value is .

Thus, in some stationary scenarios, we can use Theorem 4 to approximate quickly.

4 Empirical Study

In this section, we aim at exploring the empirical facts about the high-dimensional directional statistics of , analyzing the connection between and statically, and clarifying their time-series properties.

We collect the historical daily return of the component stocks of the CSI Index at the end of . In detail, the daily data ranges from to , including trading days in years. However, not all stocks were traded throughout the time interval, so we remove those stocks not traded more than of all days, leaving stocks. As a result, a matrix of representing the returns is generated, called . The -th row of is a -dim vector representing the return of stock returns at time , and we denote the vector as . With the pre-standardized at hand, we can calculate easily.

The section is composed of two parts. First, we carry out the exploratory data analysis by assuming the sample points to be i.i.d.. Second, we show the time-series properties.

4.1 Exploratory Data Analysis

In this subsection, we explore the data , to have a basic understanding of . We assume the -dim time-series sample to be i.i.d..

The analysis is composed of two parts. One of them is the high-dimensional exploration of . We calculate the and of the -dim sample and generate a -dim sample of given an estimated , discussing their characteristics and interpretations. The other one is the analysis of the connection between and . We list the descriptive statistics of the selected and . The covariance matrix of and are estimated and compared.

4.1.1 Exploration of High-Dimensional Directional Statistics of

We show the sample and of first

The sample is the norm of the mean vector . The sample is estimated as , which is the unitization of the mean vector.

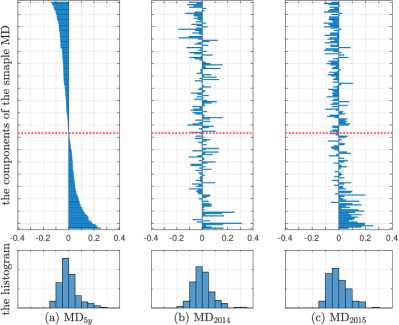

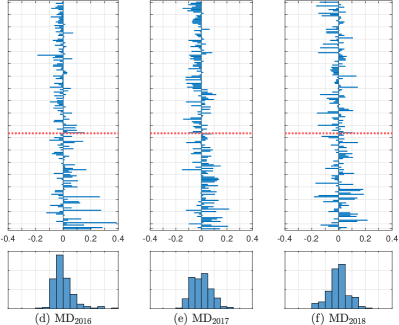

We show the -dim sample ’s as bar charts in the upper part of Figure 5, where the x-axis shows the values of every components. In detail, the upper subfigure on the left, (5) , is the sample of the whole years, and we sort its order of components by their values from smallest to biggest.444We give specific details about the meanings of the bar graph. For instance, the sorted ’s first component is , so the top bar in (5) is toward left with a length of . The second component is , so the second top bar in (5) is toward left with a length of . And forth on. The last component is , so the bottom bar in (5) is toward right with a length of . The upper subfigures on the right, (5 to 5), are the sample ’s of to , and their components are in the same order of . The red dotted line in each one lies between the th and th components of the column vector , the watershed between positive and negative components in . The downer part of Figure 5 is the histograms of the components of the sample as a sample, and they share the same x-axis with the upper part.

\phantomsubcaption\phantomsubcaption\phantomsubcaption

\phantomsubcaption\phantomsubcaption\phantomsubcaption

\phantomsubcaption\phantomsubcaption\phantomsubcaption

\phantomsubcaption\phantomsubcaption\phantomsubcaption

We draw some intuitive conclusions from Figure 5. First, the six sample ’s are different from each other. Each bar chart has different shapes from others, and we can hardly put them in categories. We calculate the angle among the vectors, where the smallest is about and the biggest is about . Second, the first components above the red dotted line are different from the last ones below, in different time window samples. It means that the behaviors of the top-ranked and the bottom-ranked stock returns are different, and we need to treat them separately. Compared with , the most matched year is — in fact, has the smallest angle with , i.e., . The components are more stable than the others every year. Third, the histograms are different. In order to clarify the difference clearly, we need to describe their characteristics.

| time window | - | |||||

|---|---|---|---|---|---|---|

| median | ||||||

| skewness | ||||||

| kurtosis | ||||||

| positive counts | ||||||

| negative counts |

Table 1 lists the descriptive statistics of the components of the sample ’s. It reveals the characteristics of the sample ’s from a different viewpoint. First, from to , the median changes from negative to positive, and the skewness varies from positive to almost . The number of positive numbers gradually increases to a half with the negative decreases. All the phenomena can be interpreted as the results of the development of the market. Second, the samples of and can be regarded as special ones. The median is more negative than others, and the skewness and kurtosis are very large. On the contrary, the samples , , and are general ones. The numbers of their positive and negative components are very close. Their median and skewness are close to .

We list the sample ’s in Table 2. The -year sample is smaller than other -year ones because of its large sample size and the bias of the statistics of small samples. For a -year time window, the sample is around and less than . Combined with the information in Table 1, is the most different year from others in terms of the cross-section.

| time window | - | |||||

|---|---|---|---|---|---|---|

| sample size | 1220 | 245 | 244 | 244 | 244 | 243 |

| 0.0331 | 0.0658 | 0.0849 | 0.0592 | 0.0804 | 0.0601 |

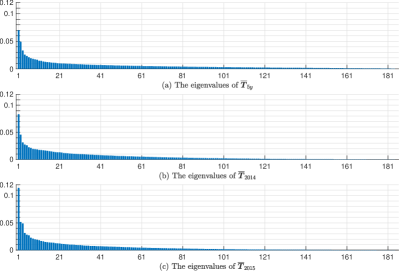

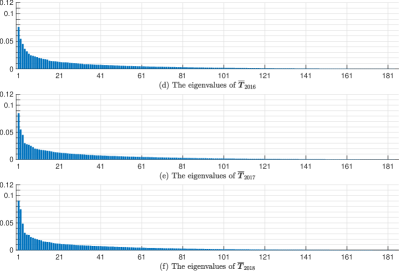

The scatter matrix about the origin measures the dispersion, where . We sort eigenvalues of of different time windows samples and show them in Figure 6. If we denote the eigenvalues of from large to small as , and mark one of their corresponding unit eigenvectors as , then the larger the , the higher the volatility along .

We interpret the figure. First, the eigenvalues in each subfigure are all not evenly distributed. It can be interpreted as that stabilizes in some direction but fluctuates in some others. Furthermore, the sum of the largest eigenvalues accounts for more than of the sum of all ones. The sum of the smallest ones in each subfigure is about . These phenomena indicate that the principal component analysis method may be applicable in the directional statistics of stock returns. Second, subfigure (c) of has the largest maximum eigenvalue, , which is the only one larger than . Thus, in , along , there is the highest volatility. Meanwhile, in , the Chinese stock market experienced tremendous ups and downs. Third, the minimum eigenvalue in each subfigure is , and the eigenvectors corresponding to are , which is implied in the definition of the standardization .

We then discuss the properties of

“Non-parametric techniques are almost non-existent on higher-dimensional spheres.” Mardia and Jupp [2000, §10.1, p. 193]. is a quite large dimension in statistics. We can hardly make any further inferences from this high-dimension sample directly. Therefore, we take the inner product between a given vector and the -dim sample to generate a new -dim sample . One of the most natural selections of is the sample of , so we denote the generated sample as , where .

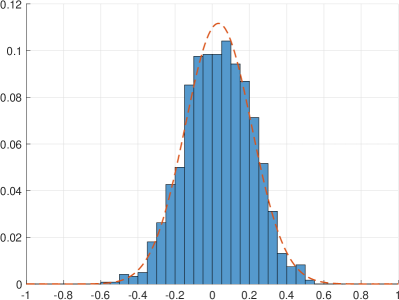

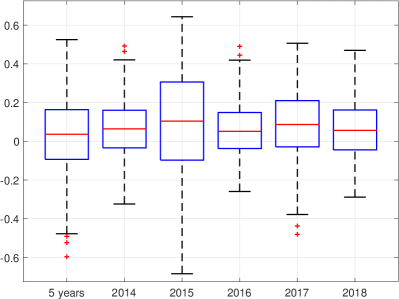

Table 3 shows ’s descriptive statistics. Figure 7 illustrates ’s empirical distribution, where (7(a)) is the histogram of the - time window, and (7(b)) is the box plots. In (7(a)), we use the orange dashed line to show the p.d.f. of the normal distribution with the same sample mean and standard deviation.

| time window | - | |||||

|---|---|---|---|---|---|---|

| mean | ||||||

| standard deviation | ||||||

| skewness | ||||||

| kurtosis |

To begin with, we interpret the sample of a -year time window -. First, the mean of the -year sample is , and its sample standard deviation is , indicating a non-concentrating distribution — there are many sample points whose angles to the sample are greater than . Its skewness is , implying that the left tail is thicker than the right. Its kurtosis is , so its distribution has slightly lighter tails than a normal distribution, consistent with the intrinsic bounded property of the inner product of two unit vectors. Second, in the central part of the subfigure (7(a)), the histogram is lower than the p.d.f. of the normal distribution. It means that the concentration around the mean of is less than that of the normal distribution. The phenomenon may mean that the samples are generated from a multimodal distribution. Third, the most left box plot in (7(b)) shows the quartiles and the extreme values of the -year sample. The median (i.e., the solid red line) is , and there are almost half of the sample points in the blue box, which is between the two quartiles . The number corresponds to IC in an active investment strategy. The extreme values all lie on the left tail, as the red +’s lie on the bottom of the box.

Furthermore, we interpret the descriptive statistics of each -year sample . First, is a particular year. has the highest sample mean and standard deviation, while the smallest sample skewness and kurtosis in Table 3. Also, the box plot of in Figure 7(b) is the widest. We suggest that one of the reasons is that in the notorious stock market crash broke out. Second, , , and are quite similar. Their sample means are all about , and their standard deviations are around . They are positively skewed: in , the skewness is about ; in , ; and in , . Their box plots also have similar shapes, no matter from the viewpoint of the quartiles, or of the range of each sample. The extreme values in and are all lies on the right tail. These similar years imply the possible stationarity of in most time. Third, we interpret the sample of year. Its sample mean is , one of the only two greater than besides . Its skewness is , which is also one of the only two that smaller than . However, its standard deviation is lower than the special and very close to that in the -year sample. The sample has the largest sample kurtosis , almost identical to that of a normal distribution. The box plot is most similar to the -year box plot — their quartiles and extreme values are almost the same.

Last but least, the sample of high-dimensional and the standard deviation of projected -dim interpret ’s concentration from different viewpoints. The sample mean in Table 3 is equal to the sample in Table 2, which is not a coincidence but a corollary of their definition. The of plays the opposing role of variance, that the higher the , the higher the concentration. So the higher the sample mean in Table 3, the more concentrated is. However, ’s sample standard deviation varies consistent with the sample mean in Table 3, so the higher the sample mean, the more volatile the .

4.1.2 The Statistics Analysis from to

First, we compare the similarity and difference between the representative components of and their corresponding with basic descriptive statistics. Table 4 is the descriptive statistics about two representative stocks: One is 000001.SZ, Ping An Bank Co., Ltd.; The other is 600018.SH, Shanghai International Port (Group) Co., Ltd. For simplicity, let an represent the returns and the standardized value of 000001.SZ, and 600018.SH.

| statistics | 000001.SZ | 600018.SH | ||

|---|---|---|---|---|

| mean | 0.0005 | -0.0022 | 0.0004 | -0.0026 |

| standard deviation | 0.0205 | 0.0508 | 0.0235 | 0.0649 |

| coefficient of variance | 41.3871 | 22.9746 | 65.0917 | 25.3970 |

| minimum | -0.1002 | -0.1810 | -0.0999 | -0.2509 |

| maximum | 0.1000 | 0.3274 | 0.1007 | 0.4661 |

-

1.

The minimum and maximum of and are resulted from the price limit system, , in Chinese stock market, leading to the inefficacy of the information expression of daily simple returns.

We discuss Table 4 in two points. First, the descriptive statistics of and are significantly different, where the standardization increases the absolute value of sample means individually. Also, the standard deviation of are larger than that of significantly. The sample coefficient of variance decreases through the standardization. Second, we interpret some facts. The range of , worth emphasizing here, is broader than that of restricted by the price limit.Thus, the standardization reveals the hidden dynamic information.

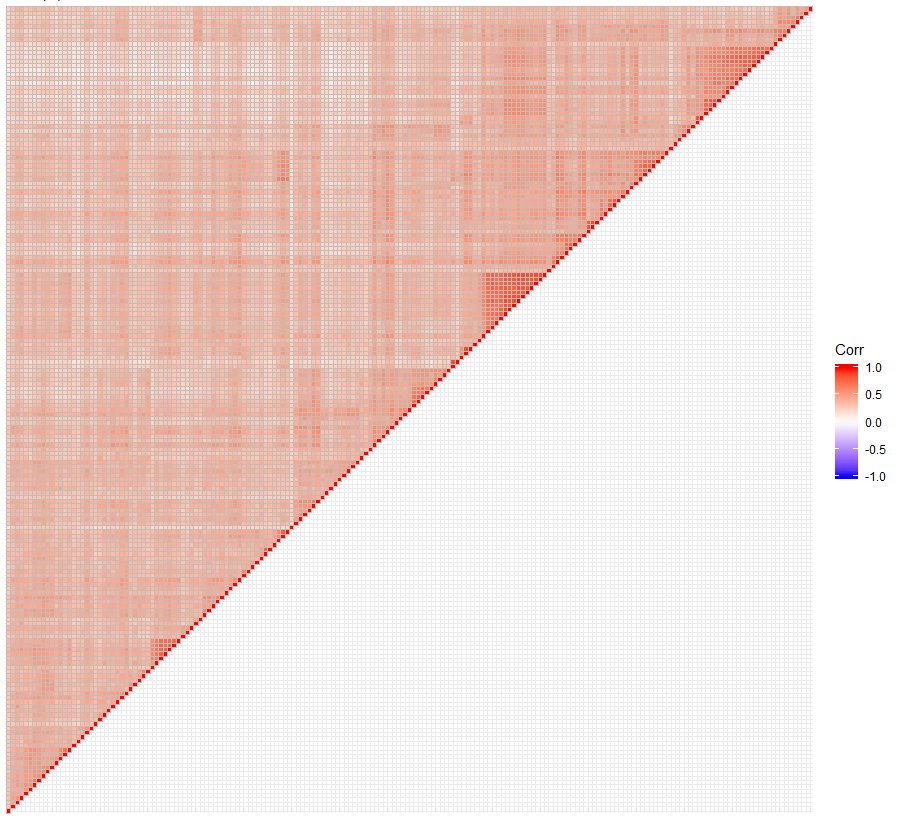

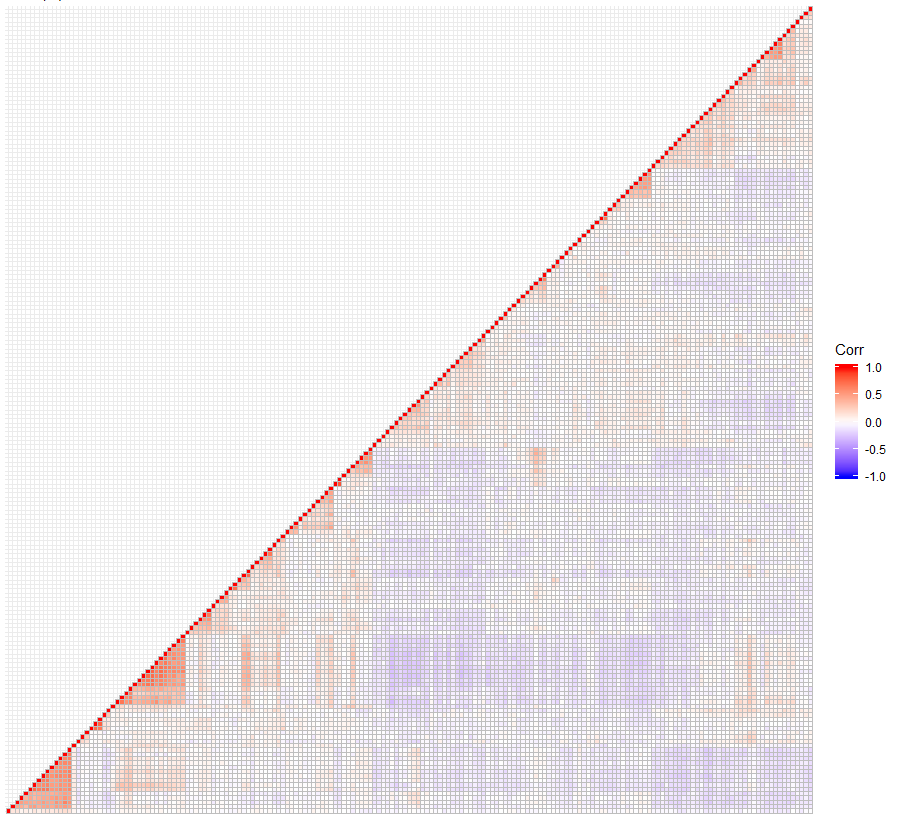

Second, the standardization almost eliminates the cross-sectional correlation between each stock. In detail, we plot two heat maps of the sample cross-sectional correlation coefficient matrix between each stock in Figure 8: The left one (8(a)) is of , and the right (8(b)) of .

We interpret Figure 8. It is difficult to ignore the difference that is greater than . In fact, by simple calculation, the mean of sample correlation coefficients of is , while that of is . In addition, the standard deviation of the sample correlation coefficients of , , is close to that of , . As a consequence, the standardization from to eliminates the cross-sectional correlation significantly.555 , and . In finance, it can be interpreted as that the standardization from to eliminates the beta part, to a certain degree.

4.2 The Time Series of , , and

In this subsection, we discuss the time-series properties. Because is a -dim vector, then its time series could not be directly shown. We first show the time series of two selected representative components and interpret their characteristics in finance. Then the time series of are given with discussion.

4.2.1 The Time Series of and

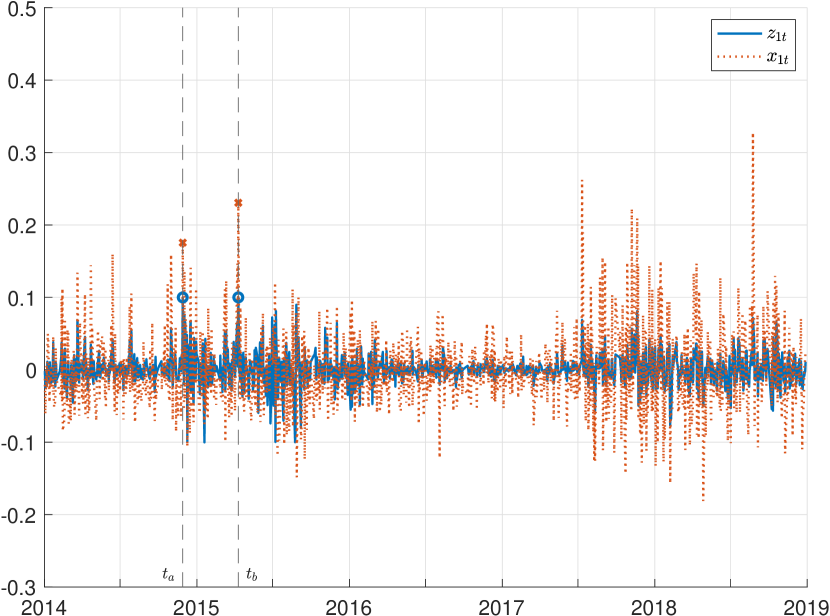

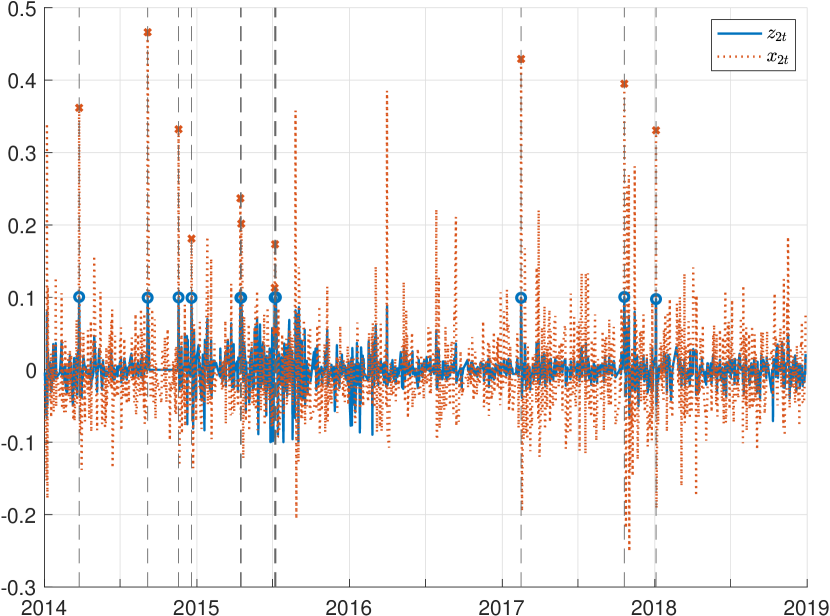

Corresponding to the above § 4.1.2, we take the time series analysis of the two representatives: and , , in Figure 9.

Three points about the properties of the time series in Figure 9 are clarified here. First, fundamental time series analysis shows that the classical hypothesis tests of autoregression and moving average are not significant, and the BIC chooses ARMA(). Second, the time series of has more information than that of . For instance, the solid blue lines of are strictly bounded in , while the dotted orange lines of are not. Third, it is easy to see similar volatility clustering. The standardization does not change the property of volatility clustering.

We interpret Figure 9 in finance. First, ’s and ’s reveal different aspects of security returns. In detail, ’s are absolute, while ’s are relative. ’s faithfully represent the returns of security, but it requires additional information (such as the market index) to attribute the returns. In contrast, one can not infer the exact returns from ’s, but she can speculate its relative rank in the whole market. Second, ’s can break through some limitation implied ’s in the financial market: such as the price limit. The price limit sometimes suppresses the market liquidity, so that ’s cannot adequately express market information. However, ’s can give different explanations for the same ’s that reach the daily limit and reveal more market information to a certain degree. For instance, in Figure 9(a), on 2014-11-28 and 2015-04-10, and reach the up limit resulting in , marked as dark circles. However, , as the orange crosses. Then one can conclude that the stock ranked higher on than on . The number of stocks that reach the up limits on is about twice that on , so on the stock is more superior.

4.2.2 The Time Series of

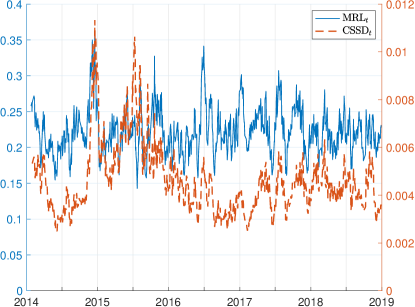

The rolling calculation estimates at , where is the length of the rolling period and is the time. According to Proposition 8, , so we can estimate the maximum of ’s expectation by the . To compare the time series properties, we also calculate the CSSD of the rolled stock returns.666, where and . Taking , the time series of and CSSD are in Figure 10.

We interpret Figure 10. First, we provide some descriptive statistics: For , the sample mean is , and the standard deviation is . For CSSD, the sample mean is , and the standard deviation is . Furthermore, it is difficult to ignore the mean-reverting property of them. Last, there is some co-movement between and CSSD. The correlation coefficient of these two time series is about . Moreover, the most correlated periods are about January 2015, when the Chinese stock market suffered the notorious meltdown crash.

5 Conclusion

The paper focuses on some probabilistic properties of high-dimensional directional statistics and their applications in financial investment.

is a linear combination of the components of . In definition, is the standardized random vector generated by linear and directional projections, which represents the standardization of next-period cross-sectional returns. Theoretically, we first give a representation theorem on and its and . Then, the covariance matrix of is expressed and simplified by a projected particular random vector. We derive the closed-form expression of the matrix by expanding the methodology in Presnell and Rumcheva [2008]. Last, we prove that the solutions to the maximization of could be expressed as the and in directional statistics. The solutions to the minimization of are the eigenvectors corresponding to the second smallest eigenvalue of . According to the theoretical results, is influenced by the dispersion and correlation of cross-sectional returns positively, while volatility negatively. These conclusions are consistent with those in the finance literature.

Our simulation analysis supplements the theoretical results. We intuitively simulate by different parameters and . We also illustrate ’s distributions, showing the impact of stock number and heteroscedasticity: The more stocks, the less dispersive the ; In some heteroscedastic condition, the distribution of may be multimodal. Then, we compare the theoretical and simulation results of the .

The empirical studies reveal that the standardization of -dim returns behaves significantly different statistical characteristics from the original data and excavates more information about the whole market. For one thing, the sample ’s of vary significantly during different time windows, whose components’ descriptive statistics could hardly be categorized, and the smallest angle between them is . Notably, the components of the top- and bottom-ranked of the sample also behave differently. The sample and scatter matrix of perform similarly during different time windows. The reveals not only the above difference but also the possible multimodality of the distribution of the sample. It provides a different view of the concentration of the sample rather than the . For another, keeps most information of : and are highly correlated, and maintains the similar volatility clustering property of . The sample covariance matrix of and is significantly different, implying that the standardization eliminates the correlation. Meanwhile, the time series of is bounded, and mean-reverting, different from that of and revealing more information. The time series about also interpret the market condition. These observations in the Chinese stock market were rarely found and revealed.

This paper is the first to apply high-dimensional directional statistics to financial investment strategy. We believe that this is a very potential research area. The cross-sectional standardization keeps the cross-rank while eliminating noise, having a higher signal-to-noise ratio for better prediction. High-dimensional directional statistics has become a significantly theoretical topic because of its complicated support set and few available tools.

Acknowledgments

The authors report no conflicts of interest. The authors alone are responsible for the content and writing of the paper.

References

- Abramowitz and Stegun [1964] Abramowitz, M., Stegun, I.A., 1964. Handbook of Mathematical Functions with Formulas, Graphs, and Mathematical Tables. National Bureau of Standards.

- Coggin and Hunter [1983] Coggin, T.D., Hunter, J.E., 1983. Problems in measuring the quality of investment information: the perils of the information coefficient. Financial Analysts Journal 39, 25–33. doi:10.2469/faj.v39.n3.25.

- Ding and Martin [2017] Ding, Z., Martin, R.D., 2017. The fundamental law of active management: redux. Journal of Empirical Finance 43, 91 – 114. doi:10.1016/j.jempfin.2017.05.005.

- Fisher [1953] Fisher, R.A., 1953. Dispersion on a sphere. Proceedings of the Royal Society of London A: Mathematical, Physical and Engineering Sciences 217, 295–305. doi:10.1098/rspa.1953.0064.

- Grinold [1994] Grinold, R.C., 1994. Alpha is volatility times ic times score. The Journal of Portfolio Management 20, 9–16. doi:10.3905/jpm.1994.409482.

- Ley and Verdebout [2017] Ley, C., Verdebout, T., 2017. Modern Directional Statistics. Chapman and Hall/CRC. doi:10.1201/9781315119472.

- Ley and Verdebout [2018] Ley, C., Verdebout, T., 2018. Applied Directional Statistics: Modern Methods and Case Studies. Chapman and Hall/CRC. doi:10.1201/9781315228570.

- Mardia [1972] Mardia, K., 1972. Statistics of Directional Data. Probability and Mathematical Statistics: A Series of Monographs and Textbooks, Academic Press. doi:10.1016/C2013-0-07425-7.

- Mardia and Jupp [2000] Mardia, K.V., Jupp, P.E., 2000. Directional Statistics. John Wiley & Sons. doi:10.1002/9780470316979.

- Presnell and Rumcheva [2008] Presnell, B., Rumcheva, P., 2008. The mean resultant length of the spherically projected normal distribution. Statistics & Probability Letters 78, 557 – 563. doi:10.1016/j.spl.2007.09.007.

- Qian and Hua [2004] Qian, E., Hua, R., 2004. Active risk and information ratio. Journal of Investment Management 2, 1–15.

- Ye [2008] Ye, J., 2008. How variation in signal quality affects performance. Financial Analysts Journal 64, 48–61. doi:10.2469/faj.v64.n4.5.

Appendix A Simulation Parameters

The parameters of the -dim and are omitted due to the length. But it is worth mentioning, that the first components of the is just . is the th order leading principal submatrix of . The parameters of the -dim and in Section 3 are as follows:

Particularly, . It is a heteroscedastic case where a stock has high volatility. The -dim is the first three components of , and are the rd order leading principal submatrix of .

Appendix B Proofs as Online Supplement

We list all necessary proofs.

B.1 The Proof of Theorem 2

The proof of Theorem 2..

We prove the theorem by three steps.

First, one can show that and are all orthogonal matrix. By the definition, we have and .

Third, we just need to show the diagonal of the covariance matrix of .

By the definition of , we prove that is diagonal. ∎

B.2 The Proof of Theorem 4

B.3 The Complete Proof of Theorem 6

The details of the proof of Theorem 6.

We first show is a diagonal matrix like (32), and then prove its closed-form expressions.

. The diagonal is deducted by the symmetry and independence. Specifically, for one thing, is a diagonal matrix. It is equivalent to . For another, the component of the diagonal components of have the form like (32). It is because , due to the i.i.d. of .

Furthermore, we show that and are all based on . By the definition of variance, we have

| (39) |

in which . Note that , so . Supplemented with , we have

| (40) |

Below, the closed-form expression of is solved in three steps.

First, we give the simplified integral expression of . Define the two independent random variables: where has the non-central chi-squared distribution of the degrees of freedom and has the central one of . Their p.d.f.’s are

By the integral transformation and , we have

| (41) |

Second, the integral can be simplified by modified Bessel function . In detail, from Abramowitz and Stegun [1964, (9.6.18)] we can derive that

| (42) |

Substituting (42) into (41), we have

| (43) |

Third, it can be concisely expressed by confluent hypergeometric function. Specifically, by the integral transformation and Abramowitz and Stegun [1964, (9.6.3) and (11.4.28)], we have

| (44) | ||||

| (45) |

Substituting (44) and (45) into (43), we have

By Abramowitz and Stegun [1964, (13.1.27)], we can eliminate :

By Abramowitz and Stegun [1964, (13.4.4)], we can combine the two confluent hypergeometric function into a single one:

B.4 The Proof of Theorem 7

Lemma 11.

The proof of Lemma 11.

By the definition of and , can be expressed as

We have the expectation in (46).

The last equation is because the construction of the first column of is the unitization of the first components of .

Furthermore, we show the expression of the covariance matrix in (46).

Therefore, the expectation and the covariance matrix of are proved. ∎

The proof of Theorem 7.

First, we show that can be expressed by , where is independent and has identical variance. In detail, by Lemma 11, there exists an orthogonal matrix such that

We denote Then the last components of and are always , so we have

where is the first components of and is the first components of . The distribution of is

Second, we give the expression of . By Theorem 6, we have

where and are in (33) and (34). So

Note that is a unit vector, so

Therefore,

Last, we convert into . To be more specific,

Note the construction of , and the first column of is the unitization of the first components of , i.e. , so

Therefore,

Consequently,

∎