A Many-Server Functional Strong Law For A Non-Stationary Loss Model

Abstract

The purpose of this note is to show that it is possible to establish a many-server functional strong law of large numbers (FSLLN) for the fraction of occupied servers (i.e., the scaled number-in-system) without explicitly tracking either the age or the residual service times of the jobs in a non-Markovian, non-stationary loss model. This considerable analytical simplification is achieved by exploiting a semimartingale representation. The fluid limit is shown to be the unique solution of a Volterra integral equation.

keywords:

Fluid limit, many-server, loss model, non-stationary.MSC:

[2010] 60K25, 60F17, 90B221 Introduction

This note establishes a functional strong law of large numbers (FSLLN) for a non-Markovian, non-stationary loss model in the many-server limit as . Stationary loss models have been studied extensively, with the Erlang-B formula being a cornerstone consequence of this literature. Non-stationary models, on the other hand, are much harder to analyze, and closed form expressions are almost impossible to derive. Stochastic process approximations are therefore crucial for performance analysis of loss models. There is a significant body of work focused on establishing fluid approximations in many-server settings, though the methods are non-trivial. In the formative paper [1], the elapsed waiting time (or ‘age’) of the jobs in the system are tracked, using which it is possible to obtain a martingale representation of the number-in-system process that yields the desired FSLLN for a queue. In contrast, [2] develops a method where the residual service times of jobs in the queue are tracked, in which case it is possible to establish the fluid limit without recourse to a martingale representation. Of course, while the latter approach in essence assumes that the service times are known at the time of arrival, as commented on in [2] the approach offers significant analytical simplification.

The purpose of this note is to show that it is possible to establish a many-server FSLLN for the fraction of occupied servers (i.e., the scaled number-in-system) in a loss model, without explicitly tracking either the age or the residual service times of the jobs. We capitalize on the fact that this process is the sum of a pure jump bounded semimartingale and a bounded finite variation process. Indeed, we show that in the many server limit the fraction of occupied servers converges to the solution of a non-linear Volterra integral equation by exploiting the fact that the semimartingale is uniformly zero and the bounded finite variation process converges to a deterministic function. This semimartingale representation is natural and allows us to avoid tracking the residual service times. Our proofs are also considerably simpler and easier to follow. Consequently, we anticipate that our analysis will be intuitive and useful for a broad range of applications. For instance, as a consequence of our main result, we present a fluid limit for the fraction of arrivals that are blocked. This result can be used as a proxy for the blocking probability in the many-server limit. A crucial motivation for this paper is the need to develop ‘transitory fluid’ traffic models; i.e., systems where a finite volume of jobs (in a continuum) enter a system over time. Queueing models fed by this type of traffic have been studied in [3, 4, 5] – however all of these consider discrete-event models of traffic. Transitory fluid traffic models have not been studied in the literature, and would be of considerable use in the modeling of capacitated energy storage systems and high-speed computer networks. As an auxiliary result, therefore, we also establish a FSLLN for the integrated fraction of occupied servers. This process is a non-decreasing stochastic fluid with a maximum rate of increase. This type of model can be used to model the energy production from a solar array, for instance.

While our proof of the main result is not complicated, some commentary is in order. We consider a sequence of models with nonstationary Poisson traffic with deterministic intensity where and stationary general service times with finite first moment. We assume that the traffic and service processes are statistically independent of each other for every . Thus, the number of servers (i.e., the system capacity) is in scale with the arrival intensity. Using the fact that the fraction of occupied servers in the th system can be represented as a stochastic integral with respect to a random counting measure, we extract the desired semimartingale representation. In Theorem 3.4 we show that the fraction of occupied servers converges to a deterministic limit. Identifying the limit function itself turns out to be a little tricky, owing to the fact that the fraction of occupied servers is the solution of a discontinuous stochastic integral equation. In order to identify the limit, we smooth the representation of the process by using a mollifier of the discontinuity. This allows us to identify the limit function as the solution of a specific non-linear Volterra integral equation. Finally, to establish uniqueness of the limit, we exploit the fact that the first time that the limit function hits the level (i.e., the system fluid level is full) is unique, from which it follows recursively that the first (and subsequent) times the limit leaves the fully occupied level and/or (re)enters state are unique.

Related Literature

There is a significant body of work establishing many-server fluid limits for stationary and non-stationary models, both with and without abandonment, starting with the seminal work in [6]; see [7] for a recent survey. Our work is related to the development of proof techniques for many-server limits, and to work on approximations to nonstationary loss models. As noted before, Kaspi and Ramanan established a fluid limit for the number-in-system process in the formative paper [1], using a martingale representation of extracted using the elapsed waiting time or age of the jobs in the system. [8] on the other hand established a fluid (and diffusion) limit for the number-in-system process of a stationary queue by using a representation of the number in system process that is similar to the system equations of a queue. By establishing a link between the equations, [8] was able to prove both a FSLLN and a functional central limit theorem (FCLT). Our approach is similar, in the sense that we exploit a random measure representation of the number-in-system process akin to system state representations in infinite server queues. Note that since we focus on nonstationary loss models, our representation is different from that of [8]. While the analysis of models without abandonment are most relevant to our setting, [2] analyzed the number in system process of a queue by tracking the residual service times. In the nonstationary setting, in a series of papers [9, 10] Lu and Whitt proved a fluid limit for a queue that experiences alternating periods of overload and underload, by tracking the age of the jobs in the system a la [1]. More broadly, there has been a growing body of work on nonstationary loss models and various approximations, particularly for computing blocking probabilities [11, 12, 7, 13, 14]. Our results complement these works by providing fluid limits that characterize the fraction of arrivals that encounter a blocked system.

2 Preliminaries

In this section we present some preliminary results that will be useful later on.

2.1 Right continuous functions.

Let denote the space of right continuous functions on that have left limits. For a function and , let

Now, for let

where runs over the set of all partitions of , in the sense that a generic looks like

and denotes the mesh or norm of the partition :

It can be shown that a function lies in if and only if

The proof of this result and related discussion can be found in [15, Ch. 14]. The Skorohod distance between two functions and in is defined by

This topology created on by the Skorohod distance is the Skorohod topology.

Theorem 2.1.

A set has compact closure in the Skorohod topology if and only if:

and

Remark 2.2.

It can be shown that is not a complete space with respect to the Skorohod distance but there exists a topologically equivalent metric with respect to which is complete.

2.2 Counting measure.

Let be a filtered probability space. Let be a point process given by a sequence of jump times, that is

Suppose in addition the jump time or arrival has a corresponding random variable taking values in some measurable space . Then is called an -marked point process. For each , let the counting process be given by

and the corresponding counting measure by

This means that for functions

| (1) |

For a point process , its intensity with respect to a given filtration is given by

If and are independent, and are independent and identically distributed (iid) from a distribution with density , then it is easy to see that the intensity of the marked point process for some is given by

| (2) |

We now say that admits the intensity kernel . Let denote the predictable -field on . Then for any mapping , measurable with respect to satisfies the following projection result (cf. [16, T3 Theorem, pp 235])

| (3) |

Thus defining the compensated measure

we have for every as in (3) that is a local martingale.

2.3 Notations

We denote convergence in probability by , convergence uniformly on compact intervals and in probability by .

3 Model and Results

3.1 Description of model.

We now introduce our model along with a useful representation of our main quantity of interest.

Assumption 3.1.

Consider a loss model; namely, a queueing model with

-

i.

a non-homogeneous Poisson arrival process with rate , where is locally integrable;

-

ii.

general service times sampled iid from a distribution with density ; and,

-

iii.

servers and zero buffer.

Let be the marked process where , are the arrival time epochs corresponding to the arrival process , and denotes the corresponding service time sampled iid from . We assume that relevant random variables for every sit in a common filtered probability space . Let denote the counting measure associated with the process . Recall from (1), is a random measure on such that for functions we have:

| (4) |

Moreover note from (2), is a random measure with intensity

| (5) |

Denote to be the compensated random measure:

| (6) |

Remark 3.2.

We explain the need for Poisson arrival processes in our considerations. In the sequel we would need finiteness of the second moment of stochastic integrals of bounded predictable processes with respect to the compensated measure, that is

| (7) |

for a bounded predictable process . This is well established when results from Poisson arrivals. However, we note that this is the only crucial requirement and all the results stated in this article hold true for any arrival process satisfying (7).

3.2 Fraction of occupied servers

Let denote the fraction of occupied servers at time . Observe that the number of busy servers at time is the cumulative sum of arrivals at times , satisfying:

-

(i)

the number of occupied servers at time is less than .

-

(ii)

the corresponding service requirement exceeds .

Consequently we have:

| (8) |

Using (4), the right hand side of (8) can be expressed as a stochastic integral with respect to the counting measure :

| (9) |

where

is a predictable process.

Remark 3.3.

Note that has paths of finite variation on compacts. Indeed, the process is piecewise constant with jumps corresponding to arrivals according to only if the current state is less than one. This means that the total variation of is bounded by that of which is a non-homogeneous Poisson process and hence is of finite variation. In addition, is adapted and càdlàg, and consequently by [17, Theorem 26] is a pure jump quadratic semimartingale.

We now state a functional fluid limit for as tends to infinity.

Theorem 3.4.

Let the conditions in Assumption 3.1 hold. Then for any we have:

| (10) |

where is the solution to a non-linear Volterra integral equation:

| (11) |

Proof.

Recall that the counting measure posseses a compensator given by (5). Now, observe that from (8) and (6) the fraction of occupied servers has the following decomposition:

where is given by (6) and is another bounded cadlag semimartingale. Indeed, is the difference of a bounded cadlag semimartingale and the bounded finite variation process . In fact, we have

where the second quantity is finite because of our assumption that is locally integrable according to Assumption 3.1. In addition we have almost surely

where . This follows from the facts that (almost surely has finitely many jumps in and is constant in between), and the fact that for all one must have . In order to obtain this last assertion observe that where is continuous on and hence also uniformly continuous.

We thus have that has compact closure in the Skorohod topology. In other words we have obtained tightness.

Next, fix and obtain (cf. [18, Theorem 2.3.7]):

Consequently for each , . Thus for any , the finite dimensional vectors as a consequence of the Cramer-Wold device [15, Theorem 7.7]. Recalling the tightness condition we have thus obtained that converges in distribution to the constant zero function and hence also in probability. Since the limiting function is non-random, the convergence is also in probability under the uniform topology. Thus we have:

Observe that we have

| (12) |

For every , by definition belongs to the Skorohod space . Furthermore there exists such that and for every the sequence has compact closure in the Skorohod topology because

-

(i)

.

-

(ii)

,

where

and is the modulus of continuity of in . Note that item (ii) is true almost surely because almost surely will have finitely many jumps in the time horizon .

Consider any . The above considerations thus show that for every subsequence of the naturals, has a convergent subsequence which converges to an element of . That is, there exists a subsequence such that

| (13) |

Henceforth, we try to identify . To that attempt, we give a slightly different representation of . Observe that the set is identical to the set . This is because only takes values in . This gives us the opportunity to replace the indicator in (12) by a smooth approximation. In particular consider a sequence of smooth functions for such that

In addition let for de defined as:

Using this notation we can replace in (12) by as both the quantities are the same. Thus our alternate representation of is given by:

Fix any arbitrary . Since is a separable Banach space with dual and is bounded in , there is a subsequence , where is as in (13) such that

| (14) |

for every . In particular, let us consider the function given by:

Observe that our assumption on ensures that this specific lies in . We thus have:

Recall that . Consequently there exists a subsequence , (which we conveniently choose to be a subset of ) such that

for every , where satisfies . For this sequence we thus obtain:

Due to (13) we must then have:

Observe that the above representation guarantees that is continuous and the convergence stated in (13) is in the uniform topology for each . Consequently fix and choose large enough such that for all we have and . Then it is readily checked that

Consider any such that . Let us multiply each side of the above equation by and integrate. We thus obtain:

Note that

Consequently taking (this is okay as we need ) and then we have by the dominated convergence theorem and (14) that:

We now take and thus we conclude that

Observe that our considerations above hold for any and hence (11) holds true for any . ∎

Remark 3.5.

Our considerations so far as stated in Assumption 3.1 are constrained on systems which start empty, that is, , for all . However this is easily relaxed as stated in the following corollary which holds under the following assumption

Assumption 3.6.

Let the conditions under Assumption 3.1 hold. In addition let the initial fraction of occupied servers satisfy the following asymptotic result:

where . Moreover, assume that the remaining service times for each of these occupied servers are iid drawn from a distribution .

Corollary 3.7.

Let the conditions in Assumption 3.6 hold. Then for any we have:

| (15) |

where is the solution to a non-linear Volterra integral equation:

| (16) |

Proof.

Let the initial number of occupied servers be , so that . Let the remaining service times for these many jobs be . Then can be represented as:

Observing that goes to infinity since , we can represent this as follows:

We have already analyzed the second quantity on the right hand side in Theorem 3.4. Now using Assumption 3.6 we have that the first quantity converges almost surely. In particular, we have:

This completes the proof. ∎

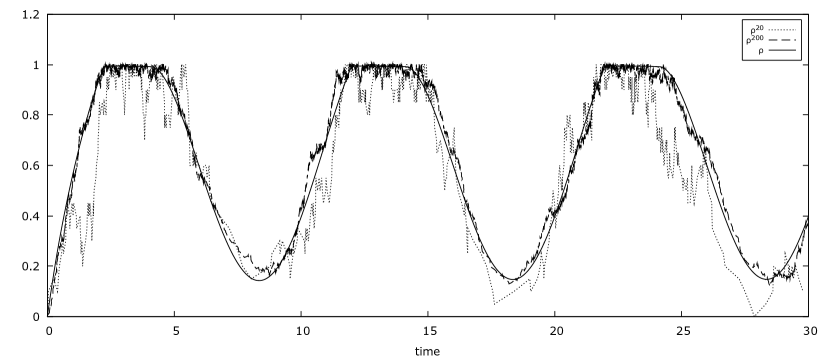

has been simulated for and with service times drawn from while the intensity of arrivals is sinusoidal with . has been approximated using a mollified version of the indicator function in relation (11) (note doesn’t reach as a consequence).

3.3 Existence and uniqueness of fluid limit.

In this subsection we prove the existence and uniqueness of the fluid limits and .

Theorem 3.8.

For all there exists a unique solution to the non-linear Volterra equation given by (16).

Proof.

Existence of a solution is well known and its proof is very similar to what we have presented in the proof to Theorem 3.4. Namely, we mollify the discontinuous coefficient by a smooth version, use existence results for smooth coefficients and then show that the limit satisfies (16). See [19] for the existence result in a more general setup, and for a more general definition of solution to nonlinear Volterra equations with discontinuous coefficient. Now we will show that for all , (16) has a unique solution for . We first show that given by:

takes values in . The fact that is positive is immediate by the positivity of , , and . Suppose there exists a such that . Since is non-increasing and

is continuous as a function of , the jumps of if any are negative. Thus there must exist an such that and for . Consequently we must have:

However, since and are non-increasing, we have:

Thus we obtain the contradiction that . Having obtained that takes values in it is easy to obtain the following hitting times to and exit times from for a solution . We denote:

Here denotes the first hitting time from below for a solution and () denotes the first exit time from when the initial condition (). The next set of hitting and exit times are defined similarly. For denote:

and

| (17) |

In addition the specific solution can now be actually represented as

| (18) |

where

Let us justify the above representation rigorously. Consider first the case when is continuous. This yields that must also be continuous. Now observe that the interval is open in and as such the pre-image of with respect to :

is an open set of . Consequently this pre-image can be represented as countable union of open intervals in :

| (19) |

where ’s are open intervals in . If however is not continuous, the fact that it is right continuous and non-decreasing guarantees, as we have already mentioned before, that has at most countably many jumps of negative size. The addition of this complexity doesn’t complicate the pre-image too much. We just have at most countably many ’s in (19) replaced by left-closed right-open intervals, that is:

where each is either an open or a left-closed right-open interval of . In our considerations above we have denoted to be:

Note that for the purposes of obtaining the solution from using equation (18) we may replace the open intervals in by left-closed right-open intervals without affecting the solution because the solution would be continuous at the left limit point of the said interval. We have thus obtained a one-one correspondence between solutions of (16) and the corresponding intervals through relation (18). Now suppose (16) admits two solutions and . By the one-one correspondence established these two solutions will differ only if they admit two different countable collection of intervals and . Let

If , deriving a contradiction is straightforward. Indeed, if , then it is immediate that the solution would be unique until the first time it hits , and consequently and are unique. Similarly, if , , which is unique and by translation one can obtain a new equation on as follows:

which also admits a unique solution until it hits . Thus in both cases, the first interval is determined by , and , and hence unique. The argument for the latter case can be modified and applied to derive a contradiction when . In this case is given by (17) with , and is hence unique. We therefore translate our equation to to obtain like before:

where . Again, this admits a unique solution until the first time it hits , and hence is also unique. This provides our required contradiction. ∎

3.4 Related processes

3.4.1 Integrated fraction of occupied servers

Let denote the integrated fraction of occupied servers, that is, for :

Observe that is the cumulative idleness (in the sense that this counts the time instants when any server is idle) since only if all the servers are occupied. Indeed, the fluid limit in (21) below provides a relation between the mean service times, arrival intensity and the integrated process.

It is readily seen that has an integral representation with respect to the counting measure :

| (20) |

where . Similar to Theorem 3.4 we now have the following fluid limit for the integrated process .

Theorem 3.9.

Remark 3.10.

Proof.

By Corollary 3.7 we have that

for all such that and . Consequently fix and to obtain large enough such that

for all . Thus we have

for all . This completes the proof.

Alternate explicit proof. From (20) we have the following decomposition

where is a semimartingale bounded above by (since is positive) and in turn by (since we are in a finite time horizon and ).

Also, notice that is a continuous function and since , its modulus of continuity satisfies:

In addition, the modulus of continuity of satisfy:

where is given by

which is uniformly continuous on . As a consequence of all this we have:

Observe that the -norm of the semimartingale satisfies:

Consequently for each , . Thus the finite dimensional vectors . Recalling the tightness condition we have thus obtained that converges in distribution to the constant zero function and hence also in probability. Since the limiting function is continuous, the convergence is also in the uniform topology. Thus we have:

By our previous considerations since we have

where is given by . We have thus obtained

A similar trick as employed in the previous section guarantees almost sure convergence. This is because for any subsequence there is a further subsequence such that the convergence of and happen almost surely. In addition, there exists an with such that for every , the sequence is tight. Similar calculations as employed in the previous section now yield:

with uniform convergence over . ∎

The following regarding the integrated process is an easy corollary of Theorem 3.8.

3.4.2 Blocked arrivals

Blocking probabilities and congestion measurement are the most important measures of performance in loss models. Computing these quantities in non-stationary models is rather hard to do requiring approximations [11, 13]. As a direct consequence of Theorem 3.4, our next result establishes a fluid limit for the fluid-scaled cumulative number of blocked arrivals,

Note that counts the number of arrivals by that encountered a fully occupied system on arrival.

Theorem 3.12.

We omit the proof as it closely follows that of Theorem 3.4. Observe that the ratio

can be used as a measure of system congestion or an approximation of the likelihood of being blocked on arrival at the queue.

4 Conclusions

The results in this note complement extant results establishing many-server fluid limits, by considering the nonstationary, non-Markovian loss model setting, and by using a bespoke semimartingale representation of the fraction of occupied servers. The primary result shows that the fraction of occupied servers converges to the unique solution of a Volterra integral equation. As a consequence of our main result, we also establish a fluid limit to the integrated number of occupied servers and the fraction of arriving jobs that are blocked on arrival. We anticipate our results, proofs of which are quite simple, should be broadly useful. In future work we anticipate extending the analysis to include functional central limit theorems. However, the analysis is much harder than the fluid limit results in this note and merit a separate paper.

5 Acknowledgements

PC gratefully acknowledges support from a Purdue Research Foundation dissertation fellowship. HH was partly supported by the National Science Foundation through grant CMMI/1636069.

6 References

References

- Kaspi et al. [2011] H. Kaspi, K. Ramanan, et al., Law of large numbers limits for many-server queues, The Annals of Applied Probability 21 (2011) 33–114.

- Zhang [2013] J. Zhang, Fluid models of many-server queues with abandonment, Queueing Systems 73 (2013) 147–193.

- Chakraborty and Honnappa [2019] P. Chakraborty, H. Honnappa, Strong embeddings for transitory queueing models, arXiv preprint arXiv:1906.06740 (2019).

- Honnappa et al. [2015] H. Honnappa, R. Jain, A. R. Ward, A queueing model with independent arrivals, and its fluid and diffusion limits, Queueing Systems 80 (2015) 71–103.

- Bet et al. [2019] G. Bet, R. van der Hofstad, J. S. van Leeuwaarden, Heavy-traffic analysis through uniform acceleration of queues with diminishing populations, Mathematics of Operations Research (2019).

- Halfin and Whitt [1981] S. Halfin, W. Whitt, Heavy-traffic limits for queues with many exponential servers, Operations research 29 (1981) 567–588.

- Whitt [2018] W. Whitt, Time-varying queues, Queueing models and service management 1 (2018).

- Reed et al. [2009] J. Reed, et al., The g/gi/n queue in the halfin–whitt regime, The Annals of Applied Probability 19 (2009) 2211–2269.

- Liu et al. [2014] Y. Liu, W. Whitt, et al., Many-server heavy-traffic limit for queues with time-varying parameters, The Annals of Applied Probability 24 (2014) 378–421.

- Liu and Whitt [2012] Y. Liu, W. Whitt, A many-server fluid limit for the gt/gi/st+ gi queueing model experiencing periods of overloading, Operations Research Letters 40 (2012) 307–312.

- Pender [2015] J. Pender, Nonstationary loss queues via cumulant moment approximations, Probability in the Engineering and Informational Sciences 29 (2015) 27–49.

- Pender and Ko [2017] J. Pender, Y. M. Ko, Approximations for the queue length distributions of time-varying many-server queues, INFORMS Journal on Computing 29 (2017) 688–704.

- Whitt and Zhao [2017] W. Whitt, J. Zhao, Many-server loss models with non-poisson time-varying arrivals, Naval Research Logistics (NRL) 64 (2017) 177–202.

- Massey and Whitt [1994] W. A. Massey, W. Whitt, An analysis of the modified offered-load approximation for the nonstationary erlang loss model, The Annals of applied probability (1994) 1145–1160.

- Billingsley [2013] P. Billingsley, Convergence of probability measures, John Wiley & Sons, 2013.

- Brémaud [1981] P. Brémaud, Point processes and queues: martingale dynamics, volume 50, Springer, 1981.

- Protter [2005] P. Protter, Stochastic Integration and Differential Equations, Springer, Berlin, Heidelberg, 2005.

- Applebaum [2009] D. Applebaum, Lévy processes and stochastic calculus, Cambridge university press, 2009.

- Kiffe [1979] T. Kiffe, A discontinuous volterra integral equation, The Journal of Integral Equations (1979) 193–200.