Exact Blind Community Detection from Signals on Multiple Graphs

Abstract

Networks and data supported on graphs have become ubiquitous in the sciences and engineering. This paper studies the ‘blind’ community detection problem, where we seek to infer the community structure of a graph model given the observation of independent graph signals on a set of nodes whose connections are unknown. We model each observation as filtered white noise, where the underlying network structure varies with every observation. These varying network structures are modeled as independent realizations of a latent planted partition model (PPM), justifying our assumption of a constant underlying community structure over all observations. Under certain conditions on the graph filter and PPM parameters, we propose algorithms for determining () the number of latent communities and () the associated partitions of the PPM. We then prove statistical guarantees in the asymptotic and non-asymptotic sampling cases. Numerical experiments on real and synthetic data demonstrate the efficacy of our algorithms.

I Introduction

The analysis of systems via graph-based representations has become a prevalent paradigm across science and engineering [2, 3, 4]. By representing a system as a graph, a plethora of system properties can be analyzed, including the importance of individual agents in the system [5], the (possible) presence of a modular organization [6], and the prevalence of other connection motifs [7].

However, while we may measure certain signals defined on the nodes or agents of the system, the edges coupling these agents are commonly unknown and need to be inferred from data. This can be done either via an ad-hoc procedure such as thresholding a statistical association measure (e.g., correlation or coherence) between the signals observed at the nodes [8], or via more sophisticated statistical methods such as graphical LASSO and others [9]. While the former kind of approach has been successful in practice, it lacks theoretical guarantees as to its validity. In contrast, a reliable exact inference of a graph requires a large number of independent samples, which are often not obtainable in practice.

Other issues faced in the inference of the exact network structure include fluctuations in the system structure itself: even though the large-scale features of the system are constant, the specific set of active edges between nodes may change with time or between realizations of the graph. As concrete examples, consider observing the expression of opinions over time in a social network [10, 11, 12, 13, 14] or fMRI signals of different healthy patients in resting state [15, 16]. For the former case, individual active links might vary in each observation even when assuming a stable social fabric. For the latter example, while individuals will have differing brain network structures at a fine scale, the large-scale network features will be similar. As an additional example, consider observing daily stock returns in a market index. There is a time-varying underlying network reflecting interactions between companies, which influences the price of individual stocks at a fine scale, even when the large-scale interactions between market sectors is stable [17]. We shall revisit this last example with numerical experiments in Section VII.E.

In the above scenarios, there is not a single correct graph to be inferred and, therefore, any network inference method trying to find the correct graph structure will fail. However, certain features of the graphs may nevertheless be stable over each instance of the system and, thus, can be inferred from signals defined on these graphs. Moreover, since features of common interest – such as modular structure, centrality measures, and clustering coefficients – are typically low-dimensional descriptions of the system (compared to the complete adjacency structure), we may recover these features directly from the observed signals with relatively few samples.

In this paper, we address the problem of inferring communities from the observation of data defined on the nodes of multiple (latent) graphs. Using the framework of graph signal processing, we model these data as graph signals induced by filters on the latent graphs [18]. In particular, we concentrate on the inference of () the number of blocks and () the associated partitions of a planted partition model.

I.A Related literature

The problem of network topology inference has been studied extensively in the literature from different perspectives including partial correlations [19], Gaussian graphical models [20, 21, 22], structural equation models [23, 24], Granger causality [25], and their nonlinear (kernelized) variants [26]. Recently, graph signal processing based methods for graph inference have emerged, which postulate that the observed data has been generated according to a network process defined on a latent graph [27, 28, 29, 30].

While this work aims to recover structural properties of graphs from signals on the nodes, we do not recover the exact structure of any graph. Rather, we use graph signals to detect communities of nodes, i.e., sets of nodes with statistically similar connection profiles. Community detection on graphs is a well-studied problem, typically seeking to partition the node set into blocks with a high density of edges within blocks and few edges between them [31, Section II-C]. Community detection methods include spectral clustering [32] that leverages approximately low-rank structures of connectivity-related matrices, statistical inference techniques that fit a generative model to the observed graph [33, 34], and optimization approaches that find communities that maximize modularity [35]. For an extensive review of community detection, we refer to [31].

Our analysis focuses on the observation of signals supported by graphs drawn from a planted partition model (PPM), a popular graph model with ground-truth communities that has been extensively studied in the literature [36, 37, 38]. In contrast to existing techniques for community detection, our problem formulation only observes signals on the nodes of a graph, rather than the set of edges. This falls along the existing line of work on ‘blind’ community detection, seeking to infer community structure in graphs with unknown edge sets. Existing work in this direction considers the observation of node signals resulting from a diffusion process on a single graph [39], a low-rank excitation signal [40], or a transformation of a low-dimensional latent time series [17]. In contrast, our work considers the observation of signals over multiple graphs, all drawn from the same latent PPM and each used to drive a network process yielding the corresponding observed signals. We also note recent work on the blind inference of the eigenvector centrality for nodes in a graph, where [41] considers the problem of ranking nodes according to their centrality in this regime, and [42] considers the estimation of eigenvector centrality with colored excitations.

I.B Contributions and outline

Our main contributions are as follows. First, we provide an algorithm to detect communities from graph signals supported on a sequence of graphs generated by a PPM. Second, we develop an algorithm to infer the number of groups in the underlying graph model from the observed signals. Lastly, we derive both asymptotic as well as non-asymptotic statistical guarantees for both algorithms whenever the partition structure is induced from a planted partition model. More specifically, we characterize the sampling requirements of both algorithms to achieve desired performance guarantees when finitely many samples are taken.

We first gather notation, background information, and preliminary results in Section II. In Section III, we formally state the considered problems (Problems III.A and III.A) as well as the proposed algorithmic solutions (Algorithms 1 and 2), together with an illustrative example to highlight their effectiveness. Our main theoretical results (Theorems 1 and 2) provide statistical guarantees for our algorithms, and are discussed in Section IV. Sections V and VI contain the associated proofs of these results. We complement our theoretical investigations with numerical experiments in Section VII, before concluding with a short discussion highlighting potential avenues for future work in Section VIII.

II Preliminaries: Graph Signal Processing and Random Graph Models

General notation. The entries of matrix and (column) vector are denoted by and , respectively. For clarity, the alternative notation and will occasionally be used for indexed matrices and vectors, respectively. The notation ⊤, and denote transpose and expected value, respectively. and refer to the all-ones vector and the identity matrix, and denotes the th standard basis vector. For a given vector , is a diagonal matrix whose th diagonal entry is . The norm indicates the when the argument is a vector, and the induced operator norm when the argument is a matrix. The notation , , , and take the established function approximation meaning [43, Chapter 3], with denoting an approximation that ignores logarithmic terms.

Graphs and graph shift operators. An undirected graph consists of a set of nodes, and a set of edges, corresponding to unordered pairs of elements in . By identifying the node set with the natural numbers , such a graph can be compactly encoded by a symmetric adjacency matrix , with entries for all , and otherwise. Given a graph with adjacency matrix , the (combinatorial) graph Laplacian is defined as , where is the diagonal matrix containing the degrees of each node.

The Laplacian and the adjacency matrix are two instances of a graph shift operator [44]. A graph shift operator is any matrix whose sparsity pattern coincides with (or is sparser than) that of the graph Laplacian [44]. More precisely, only if or , and otherwise. In this paper, we consider graph shift operators given either by the adjacency or the Laplacian matrices. We denote the spectral decomposition of the graph shift operator by . Here, collects the eigenvectors of as columns and collects the eigenvalues .

Graph signals and graph filters. We consider (filtered) signals defined on graphs as described next. A graph signal is a vector that associates a scalar-valued observable to each node in the graph. A graph filter of order is a linear map between graph signals that can be expressed as a matrix polynomial in of degree :

| (1) |

For each graph filter, we define the (scalar) generating polynomial .

In this work, we are concerned with filtered graph signals of the form

| (2) |

where is an excitation signal. By choosing appropriate filter coefficients, the above signal model can account for a range of signal transformations and dynamics. This includes consensus dynamics [45], random walks and diffusion [46], as well as more complicated dynamics mediated via interactions commensurate with the graph topology described by the Laplacian [47].

Stochastic block model. The SBM is a latent variable model that defines a probability measure over the set of unweighted networks of size . In an SBM, the network is assumed to be divided into groups of nodes. Each node in the network is endowed with one latent group label . That is, if node is a member of group , then . Conditioned on these latent group labels, each link of the adjacency matrix is an independent (up to symmetry of the matrix) Bernoulli random variable that takes value with probability and value otherwise,

| (3) |

To compactly describe the model, we collect all the link probabilities between the different groups in the symmetric affinity matrix . Furthermore, we define the partition indicator matrix with entries if node belongs to group and otherwise. Based on these definitions, we can write the expected adjacency matrix under the SBM as

| (4) |

The planted partition model (PPM) is a particular case of the SBM, governed by two parameters for the link probabilities and having equally-sized groups. In the PPM, the affinity matrix for a graph with groups and nodes can be written as

| (5) |

Thus, the probability of an edge between any nodes within the same community is governed by the parameter , whereas the probability of a link between two nodes of different communities is determined by .

III Problem Statement and Algorithms

In this section, we formally introduce the two ‘blind’ community detection problems to be studied. We then specify the proposed algorithms to solve these problems, and provide an intuitive justification and an illustrative example.

III.A System model and problem statement

As mentioned in Section I, we are concerned with the inference of a statistical network model based on the observation of a set of graph signals, i.e., a scenario where the edges of the graph are unobserved. Consider a set of graph signals obtained as the outputs of graph filters. For the th instance, we observe given by [cf. (1) and (2)]

| (6) |

For every , the graph shift operator corresponds to an independently drawn PPM network with a constant parameter matrix . The excitation signals are assumed to be independent of the graph topology as well as i.i.d. with zero mean and .

We introduce two specific ‘blind’ problems that pertain to inferring properties of the unknown PPM without observing the edges in the graphs drawn from this model. The first goal is to select the model order, specified as follows: {problem}[Model order selection] Given a set of graph signals following (6), infer the number of groups of the latent PPM generating . We estimate the number of blocks (or communities) in the graph in Section III.A. This gives an initial coarse estimate of the structure of the network model.

The estimated number of groups allows us to solve the following partition recovery problem: {problem}[Partition recovery] Given a set of graph signals following (6) and a number of groups , infer the community structure of the latent PPM generating .

There are several challenges related to solving Problems III.A and III.A. First, the graph topology is observed indirectly through the graph signals (6). Second, the graph topology is time-varying, as each is drawn independently from the PPM.

Remark 1

We make the assumption of a white noise input with in (6) for simplicity, but successful recovery is possible even when this does not hold. This is illustrated in Section VII.B, where the system is excited by colored noise that is either not identical at every node, or has a rank-deficient covariance matrix.

III.B Proposed blind identification algorithms

We summarize our proposed solutions to Problems III.A and III.A in Algorithms 1 and 2, respectively. Both algorithms build upon the intuition that the spectral properties of the covariance matrix of our observed signals will be shaped according to the block structure of the underlying PPM. Note that the expectation is computed both with respect to the stochastic inputs as well as the random graph . To gain intuition, we first sketch the overarching algorithmic ideas and provide an illustrative example. We postpone a more rigorous discussion to Sections V and VI.

From (6) it follows that for each instance , the observed graph signal can be written as

| (7) |

Observe that the expectation of will be low rank for every positive , with a block structure inherited from the underlying PPM. Since is a white noise input, it can be shown (see Section V) that the covariance matrix is given by a low-rank matrix plus a multiple of the identity matrix, thus inheriting the block structure from the PPM (see (4)). As we do not have access to the true covariance matrix, both Algorithms 1 and 2 employ a sample covariance estimator instead of as follows.

Model order selection

| (8) |

| (9) |

| (10) | ||||

Since the empirical sample covariance matrix is only a (noisy) estimator of the true covariance, it will not be exactly low-rank plus identity, but will approximate this structure. Intuitively, our aim is thus to estimate the model order such that the rank- approximation of approximates the data well, while keeping as small as possible. Algorithm 1 achieves this by employing a minimum description length criterion [cf. (10)] to select an “optimal” number of groups , see [48].

Partition recovery

Not only the eigenvalues of the sample covariance matrix, but also the eigenvectors carry valuable information to identify the underlying PPM. It can be shown that the dominant eigenvectors of the (sample) covariance matrix are correlated with the partition structure of the PPM. We can thus employ a procedure akin to classical spectral graph clustering [32, 49] to reveal the underlying partition structure via a -means clustering of the rows of the matrix of dominant eigenvectors; see Algorithm 2.

III.C Example: Inference with planted partition model

Let us illustrate the proposed algorithms with a simple example. We generate synthetic data from a PPM with nodes, communities, , and . Note that for smaller , the community structure in the randomly drawn graphs is more pronounced. The input signal is uniform i.i.d. with and the graph filter is of the form , where and is the Laplacian matrix of the th sampled graph.

Intuitively, for a large sample size, the sample covariance will be a good approximation of the true covariance matrix, thus, we should obtain a satisfactory solution to our problems. To illustrate this, in the top plots of Fig. 1 we show a snapshot of the estimated covariance matrix with sample sizes and , with fixed . It is clear that with a large sample size such as , the estimated covariance matrix admits a clear partition into two blocks, which indeed correspond to the planted partition structure. Note that the nodes are ordered in the plots for illustrative purposes, but in our observations we are not given such a convenient ordering.

The bottom plots in Fig. 1 confirm the intuition that a larger sample size improves our estimates: here we plot the error rate of model order estimation and partition recovery (with known ) against the sample size . For both problems, the error rates decay to zero as regardless of the parameter . However, the error rate varies markedly over when the number of samples is finite, highlighting the need for analysis of both asymptotic and non-asymptotic performance.

IV Main Results

In this section, we describe our main theoretical results on the consistency and convergence rates of our algorithms to solve Problems III.A and III.A.

For a generic graph filter , the second order moments can be characterized by the relative community membership of nodes . Using the expression to denote that both nodes and belong to the same group, whereas indicates the contrary, the possible values of the second order moments can be specified by nine parameters:

| (11) | |||||

which depend on the graph filter and the PPM parameters . Furthermore define the following three parameters to simplify the presentation of our results.

| (12) |

Assumption 1

It holds for the parameters in (12) that:

| (13) |

In Section IV.A we show that Assumption 1 indeed holds for some common filter types. Using the above notation, we now state the following results about the asymptotic behavior of Algorithms 1 and 2 when .

Theorem 1

Assume that there exists such that almost surely and 1 holds. As the number of samples :

-

1.

(Section III.A) Algorithm 1 yields w.h.p.

-

2.

(Section III.A) Algorithm 2 recovers the true partition of the PPM w.h.p.

The proof can be found in Sec. V. We remark that the almost surely boundedness of is guaranteed under mild conditions. For example, it holds if () the spectral norm of the graph filter is bounded, i.e., for any , and () the signal is bounded.

In the non-asymptotic case when is finite, we have:

Theorem 2

Assume that there exists such that almost surely and 1 holds.

- 1.

- 2.

The proof can be found in Sec. VI. Although the MDL criterion here is only guaranteed not to underestimate in Problem III.A when (14) holds, we empirically observe in Section VII.A that it tends to select with sufficiently many samples, selecting otherwise.

Theorems 1 and 2 rely on the convergence of the covariance estimator (8). To facilitate our discussions, let us borrow the following result from [50, Corollary 5.52]

Proposition 1

Assume that there exists such that almost surely. With probability at least :

| (16) |

where the constant satisfies .

It shows that the sample covariance converges at a rate of for any fixed . These results can be generalized to the case of sub-gaussian , see [50, Corollary 5.50].

Lastly, we remark that although we have focused on the special case of the PPM, the above results can be extended to the more general SBM model.

IV.A Examples

Verifying 1 requires evaluating the second-order moments (IV), which is generally non-trivial. In Example 1, we show that the simple graph filter given by the adjacency matrix of a PPM fulfills 1.

Example 1

Consider the simple case where , i.e., the output of the underlying process at node corresponds to the sum of the initial values in the one-hop neighborhood of . For this case, we may explicitly compute the parameters in (IV) to obtain , , , , and , where we have allowed for self-loops in to simplify the notation. From (12) it then follows that the constants are given by , , and . It follows immediately that Assumption 1 holds as long as .

For the general case where the graph filter is any polynomial of the adjacency matrix with positive coefficients, we can extend the above findings as illustrated in the next example.

Example 2

Let be a polynomial of with positive coefficients. It can be shown that for a planted partition model with , , and communities of size nodes each, the block structure of powers of is maintained, i.e., for sufficiently large , where we dropped the superscript (ℓ) for clarity. Thus, a positive coefficient polynomial maintains this block diagonally dominant structure in expectation. Consequently, the covariance is also block diagonally dominant, so we can leverage Proposition 2 (to be stated in Section V) to show that Assumption 1 holds.

V Proof of 1

In this section, we prove our asymptotic consistency results stated in 1.

We first characterize the spectral properties of the population covariance (Proposition 2 and Proposition 3), and then discuss how the correct number of groups and the group memberships can be deduced from these properties. We then use the fact that the sample covariance matrix converges to as , yielding the desired consistency guarantees.

V.A Spectral properties of population covariance

We start by characterizing the covariance of the observed graph signals.

Proposition 2

Proof:

We show (17) by explicitly computing the entries of for a generic graph filter . The block structure of the PPM implies that we only have a finite set of cases to consider.

First, we compute the diagonal entries of :

Using the fact that and , we have:

| (18) | ||||

Second, we consider an off-diagonal entry in within a block of the PPM ( but ).

where (a) follows from whenever , and (b) follows from . We thus conclude that

| (19) |

Remark 2

A similar result for the structure of the covariance matrix can be established if the underlying generating model of the graph is an SBM and not a PPM. However, the exact description of will depend, in general, on all model parameters. For simplicity, we thus concentrate on the case of the PPM in this work.

Proposition 2 reveals the specific structure of the covariance matrix , which yields the following spectral properties.

Proposition 3

Under Assumption 1, the spectrum of is characterized by:

| (20) |

where denotes the largest eigenvalue. The largest eigenvalue has multiplicity one. The eigenvalues and have multiplicity and , respectively.

Moreover, the matrix of the top- eigenvectors of can be expressed as:

| (21) |

where is the normalized partition indicator matrix such that and is a unitary matrix.

Proof:

From (17), we can see that the covariance is composed of two terms, an identity matrix multiplied by a non-negative scalar , and a rank- matrix . Under Assumption 1, is positive semidefinite and therefore the top eigenvectors of coincide with the eigenvectors of .

Let us define the diagonal matrix and the matrix , such that . Using the eigendecomposition , it can be shown by direct computation that the matrix gathers the eigenvectors of :

Finally we note that since is symmetric, the matrix is unitary. It is then easy to verify that the eigenvectors are properly normalized. ∎

From the above result, it can be seen that the top- eigenvectors of span and can therefore be used to recover the blocks of the underlying PPM.

V.B Establishing Theorem 1

Proof:

From Propositions 1 and 3, we observe that the sample covariance matrix converges to as , and thus has three unique non-zero eigenvalues given by , and (in the limit). Moreover, under Assumption 1 the top eigenvalues of are strictly larger than the lower eigenvalues.

Accordingly, minimizing the MDL criterion yields . To show that the objective function in (10) has a minimum at , we use (20) and obtain for any :

| (22) |

so .

In addition, for any , we have

| (23) |

The fraction inside the logarithm can be expressed as

| (24) |

which holds as and ; see Appendix A for a detailed derivation. This shows that the second term in (23) must be a nonnegative number independent of .

We thus conclude that the MDL criterion attains its minimum at for the true eigenvalues . Finally, by Proposition 1 and Weyl’s inequality, we have as . ∎

Proof:

Denote the th row vector of the eigenvector matrix of by . From Proposition 3, we know that the matrix has unique orthogonal row vectors (one for each group). From 1 we know that as the empirical covariance matrix will converge to . Hence, the vector corresponding to node will correspond to one of those unique rows. Clustering the vectors into groups using -means yields the desired partitioning. ∎

VI Proof of 2

The previous section shows the asymptotic behavior of the proposed algorithm, when the covariance matrix is estimated perfectly. In this section, we characterize the non-asymptotic behavior of our algorithms in terms of the number of samples required to solve the considered problems with high probability.

VI.A Proof of Theorem 2 (Section III.A)

Our proof for Section III.A rests on two lemmas. First, we bound the difference between the MDL criterion when applied to the empirical covariance and the true covariance .

Lemma 1

For any , it holds that

| (25) |

Proof:

Recall the notation and , and let be the estimation error of eigenvalue . Observe that

| (26) |

Taking absolute value on both sides of (26) leads to

where (a) is due to for any .

To simplify this expression further, we make use of the following generalization of Weyl’s inequality:

| (27) |

which holds for any and follows from [51, Corollary 6.3.8] and the equivalence of norms.

Second, we bound the difference between the MDL criterion when and , both with respect to the true covariance.

Lemma 2

Let . If , then

for some constant which depends on .

Proof:

If , we observe that the first term in the MDL criterion (10) is monotonically decreasing in , so it suffices to lower bound the difference by evaluating . This expression evaluates to

Observing that , as well as , the conclusion of the lemma follows. ∎

With these two results in place we can now conclude our proof of Theorem 2 (Section III.A).

VI.B Proof of Theorem 2 (Section III.A)

To prove the second part of Theorem 2 related to Section III.A, we need to bound the labeling error we obtain from applying -means to the rows of the eigenvectors of the sample covariance matrix. To this end, we proceed in three steps.

Let (resp. ) be the normalized indicator matrix induced by the candidate labeling (resp. the true community labeling ). Consider the -means objective function:

| (29) |

Our first step in the analysis is to lower bound when is selected as the top eigenvectors of the true covariance matrix .

Lemma 3

Assume that the true communities are of equal size with nodes. If there is no labeling error of the nodes, then . Otherwise, we have that

| (30) |

Proof:

From 3, we know that . Moreover, as for any group permutation matrix , it follows that if for some permutation map .

Next, we consider the case when mislabels at least one node. We have the following chain of equivalence for :

| (31) |

Notice that since . This gives,

| (32) |

Recalling from Proposition 3 that , this can be be further simplified to

| (33) |

Observe that

| (34) |

where and indicate the size of the th partition under and , respectively.

Consider the case when mislabels exactly one node. Without loss of generality, this scenario can be captured by mislabeling node . We have , , and

| (35) |

Using (34), it can be shown by direct calculation that

| (36) |

Under the assumption that the communities are of equal size, i.e., , this directly yields the right-hand side of (30). We remark that minimizing (36) over the possible choices of will yield a lower bound for a PPM where the communities are not equally sized.

We conclude the proof by noting that the cost function is increasing in the number of errors made by the labeling function, so (30) presents a lower bound for the cost when the candidate labeling is incorrect. ∎

Before proceeding, we first note that when the sample bound (15) is attained, the following holds as a direct result of Propositions 1 and 3:

| (37) |

We then bound the suboptimality of the communities found by Algorithm 2 as follows.

Proposition 4

Proof:

Given a candidate partition with labeling , we define the normalized indicator matrices as in the proof of Lemma 3.

Let be an error matrix. We observe the chain

| (39) |

where (a) is due to , (b) is due to yielding an optimal -means solution given , and (c) used together with the triangle inequality.

Furthermore, we observe that the error between the top- eigenvectors of and is bounded by

| (40) |

where (a) is due to [52, Lemma 7], denotes the matrix formed by the eigenvectors of orthogonal to , and (b) is due to a result noted in [53]. Define . The -largest eigenvalue of does not exceed :

| (41) |

where the last inequality is due to condition (37). We can now apply the Davis-Kahan theorem [53]:

| (42) |

Substituting the above into (40) and then into (39) yields the desired bound (38). ∎

When the sample bound (15) is attained, (37) holds. Then, combining 3 and 4 shows that if

| (43) |

then Algorithm 2 always returns a partition with zero error rate, relative to the true PPM communities. Applying 1 with the boundedness assumption on shows that the sampling condition fulfills (43), as desired.

Remark 3

Due to the non-convexity of the -means objective, the assumption made in 4 that Algorithm 2 yields an optimal solution is not practical. However, under certain conditions, there are algorithms that guarantee optimality [54], i.e., that bound the suboptimality gap with respect to the true non-convex optimum. Under these conditions, an expression analogous to (38) can be derived. More precisely, we obtain

| (44) |

Ultimately, the required sampling rate in 2 remains unchanged even if one can only guarantee a near-optimal solution of the -means problem.

VII Numerical Experiments and Applications

In this section, we demonstrate the performance of the proposed methods for model order selection and partition recovery in both synthetic and real-world data. Unless specified otherwise, experiments are run with graphs of size nodes, and PPM model parameters where . As done in Section III.C, we consider a network process represented by the graph filter , with . To benchmark the performance of community detection, we define the permutation-invariant error rate of a predicted labeling on :

| (45) |

where is the set of permutations .

VII.A Model order selection

We consider a PPM with communities and analyze the estimated order as a function of the ratio for different number of observed signals ; see Fig. 2 (left). We focus on two different methods to obtain : () the MDL method described in (10) and () a naive thresholding method that counts the number of eigenvalues greater than the mid-point between the th and the th eigenvalue of the true covariance .

We call this method naive, since it does not take into account the noise stemming from considering a finite number of observations . Note that while this method would be optimal for , it requires knowledge of , and is thus not implementable in practice.

The results in Fig. 2 (left) indicate that both estimators perform well when is small, i.e., when the parameters of the PPM yield an easily detectable model. Naturally, estimators based on larger number of observed signals are more robust to increasing values of , with both methods estimating the correct order for when . However, when grows large enough, both estimators behave in distinct ways: the MDL method tends to underestimate the model order whereas the naive threshold method overestimates it.

To see why this is the case, notice that the first term in the MDL expression (10) promotes orders for which the lower eigenvalues of are flat whereas the second term penalizes high model orders. Thus, whenever there is no clear jump between the th and the th eigenvalues because is large, the second term in (10) dominates and the model order is reduced to its minimum of . In contrast, the naive threshold method simply counts the number of eigenvalues of greater than . For small , the eigenvalues of are strongly perturbed versions of those of . Thus, some of these perturbed eigenvalues tend to exceed the threshold , increasing the estimated order . Moreover, as increases, the gap between and becomes smaller, rendering it more likely for eigenvalues to cross the threshold by chance.

VII.B Colored excitation

For a PPM of communities, our algorithm is predicated upon the system being approximately rank- (plus a multiple of the identity). If the excitation is white (, ), the eigenvectors of the system are excited uniformly. Accordingly, the covariance matrix will be () approximately described by a rank- matrix plus a multiple of the identity and () have top eigenvectors that (approximately) capture the community structure.

We relax the assumption of a white excitation by coloring the excitation signal and observing the partition recovery performance of our algorithm as a function of the number of samples .

We consider the following different scenarios for our excitation signal. The white excitation is drawn from the normal distribution . The diagonal excitation varies the diagonal entries of the covariance matrix, drawing the excitation from the distribution . The Wishart excitation is drawn from a Gaussian distribution whose covariance matrix is a Wishart matrix of samples. That is, . Clearly, as , , approaching the white excitation. So, we consider the case where , yielding a rank-deficient covariance matrix. Finally, the adversarial excitation colors the excitation covariance to be strongly biased towards the lower eigenvectors of the system. Specifically, for , where the top and lower eigenvector matrices are denoted by and , respectively, the excitation is drawn from the distribution .

The only case that preserves both the identically distributed and independence conditions at each node is the white excitation. The diagonal excitation maintains independence at each node (since the covariance matrix is diagonal), but the variances are different across nodes, breaking the identically distributed condition. The Wishart and adversarial cases break both conditions. Note that the Wishart excitation has a chance of not exciting the leading eigenvectors of the system, resulting in poor performance, but could also excite all (or some) of them, due to the rank-deficient nature of its covariance matrix. Moreover, the adversarial excitation very weakly excites the leading eigenvectors, almost guaranteeing poor performance.

The results in Fig. 2 (center-left) indicate that the diagonal input closely matches the white input’s performance, suggesting that having identically distributed input at each node is not very important, as long as independence is maintained.

When the independence condition is broken, as in the rank-deficient Wishart excitations, the performance of our algorithm degrades. However, as the rank of the excitation increases, the average performance increases as well. This is intuitive, as a higher-rank excitation is more likely to excite the top eigenvectors of the system, improving the algorithm’s performance.

Finally, the adversarial excitation does no better than a random guess (error rate ) for all . This confirms our expectation, as this input scheme does not excite the top eigenvectors that reflect the community structure of the PPM.

VII.C Graph sequence independence

In the studied setting of only observing signals on a graph (as opposed to the graph itself), our algorithm is able to successfully detect communities in a PPM even though the parameters of the PPM are below known detectability thresholds [55]. This non-intuitive result is due to the fact that each observation corresponds to an independent initial condition and an independent realization of the underlying PPM. We can leverage the information from these independent draws by averaging over many different samples, thereby sidestepping the detectability limit (which assumes that we observe a single graph).

To demonstrate how our algorithm leverages the implicit observation of many realizations of an undetectable PPM for a given number of samples , we conduct the following experiment. Instead of sampling an independent graph for each initial condition, we consider a sequence of graphs modeled by a Bernoulli (graph)-process: starting with some realization of the PPM , let the next realization be the same graph with probability , and draw randomly from the PPM with probability . So, when , this is equivalent to drawing graphs independently, and when , this is equivalent to only using a single graph. Note, however, that we still observe the system for independently drawn white excitation signals .

The results in Fig. 2 (center-right) reflect our intuition: the partition recovery performance improves with the Bernoulli parameter .

Specifically, the (constant) case fails for all , since performance is upper bounded by the case when the graph is directly observed. The considered PPM is undetectable when observing a single graph, so our algorithm fails. The case does better than the constant case, but does not achieve the required number of graphs observed to match the (independent) case. However, the case behaves quite similarly to the independent sequence, suggesting there may be some point at which it is sufficient to excite a few () graphs multiple times each, rather than excite many () graphs once each.

VII.D Signal-to-noise ratio from community structure

To understand how the community structure influences our algorithm’s performance, we measure the overlap score between the predicted labeling and the true labeling for an increasing number of communities , where all communities have a fixed size . That is, for some , the PPM will have nodes. The overlap score, defined in [39] as

| (46) |

where is the fraction of correctly labeled nodes, and is the probability of correctly guessing a node’s true group assignment. So, an overlap score of indicates that the candidate labeling is no better than a random guess, and an overlap score of indicates a perfect match. Using this metric rather than the error rate accounts for the different community structures, allowing for a fair comparison.

As increases, is kept constant, but is either () kept constant or () scaled to keep the expected number of inter-cluster edges incident to each community constant.

That is,

| (47) |

is constant for all , where it is implicit that varies with . In fact, using the signal to noise ratio (SNR) defined in [38], this scheme where is scaled with yields

| (48) |

where is the ratio when .

Fig. 2 (right) illustrates the error rate for each graph model. When is fixed, the performance degrades with , as the ratio of inter-cluster to intra-cluster edges increases linearly with . However, normalizing maintains consistent performance for all values of .

VII.E Clustering stock data

We apply our algorithm to the task of inferring community structure in the S&P 100 stock market index. The daily closing prices for 92 stocks from 4 January 2016 to 30 December 2018 were obtained from Yahoo! Finance111https://finance.yahoo.com, and the daily log-returns calculated. These daily returns are then normalized to have zero mean and unit variance.

The assumption here is that stocks have an underlying community structure dictated by a stochastic block model, and that the log-returns for each day are independent and the result of a filter on a graph drawn from an SBM. These are clearly very strong assumptions to make for real data, so we justify the application of our algorithm to this dataset by measuring its “stability” over the time-series. We split the dataset into 4 contiguous blocks of size , where is the total number of samples, and apply our algorithm to with to recover communities for different periods of time. A random labeling is also generated for reference. Then, the pairwise success rate () between each sample set is computed [cf. (45)], as shown in Fig. 4 (left). Although the detected communities do not overlap perfectly, they clearly exhibit a high degree of consistency.

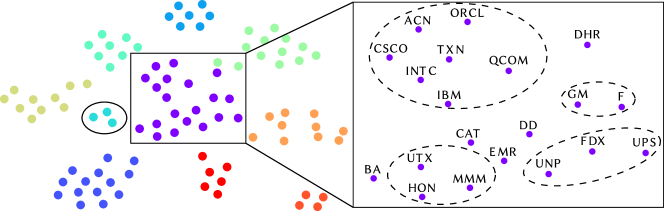

Obviously, there is no ground-truth partition of the stock data, so we apply our algorithm to the whole dataset, yielding communities as determined by the MDL (Algorithm 1). Fig. 3 shows the t-SNE embedding [56] of the dominant eigenvectors. Despite companies often not strictly belonging to one sector, the communities seem to capture obvious commonalities between companies222For a table of detected communities, as well as code for the other experiments, see https://github.com/tmrod/timevary-netfeat-supplement. Moreover, the block structure of the covariance matrix for all samples, shown in Fig. 4 (center-left), is apparent. This further justifies treating the dataset as if it is driven by an SBM. Proceeding under the assumption that this “final” result reflects the true community structure, we evaluate our algorithm with respect to order selection and community detection.

Fig. 4 (center-right) shows the order estimation with respect to the sample size. For some number of samples , a single “block” of consecutive samples is observed, from which the model order is inferred. This tends to underestimate the true model order as observed in Section VII.A.

Note that in the full processing pipeline (), an incorrect model order estimate will lead to poor classification performance. Hence, in Fig. 4 (right) we show the community detection performance for both the full pipeline (where is determined via MDL) and for fixed (both using the same consecutive sampling scheme as before). Fig. 4 (right) shows an expected drop in the classification error rate for both settings as increases, with the gap between the two curves closing as the estimate becomes more accurate.

VIII Discussion

In this work, we considered the ‘blind’ community detection problem, where we observe signals on the nodes of a family of graphs, rather than the edges of the graph itself. Stated differently, the observations correspond to the output of a (time-varying, random) graph filter applied to random initial conditions [cf. the system model (6)]. Assuming that the underlying graphs correspond to (unobserved) realizations of a PPM, we aim to infer the number of communities present as well as the corresponding partition of the nodes. We propose the use of spectral algorithms on the empirical covariance of these signals to infer the latent structure of the graph sequence. We show that our algorithms have statistical performance guarantees for both the asymptotic and finite sampling cases, as also demonstrated via extensive numerical experiments.

There are many potential avenues for future research. Our proof of the MDL criterion’s performance in the finite sample regime only provides sampling requirements to guarantee that the order is not underestimated. As shown empirically in Section VII.A, the model order is typically not overestimated. We leave further analysis of this behavior for future work. As shown in Section VII.B, the clustering algorithm does not strictly require the initial condition to be white. If the observer can manipulate the covariance matrix of the inputs, it appears possible to get better performance by adaptively coloring the inputs to the system. Furthermore, Section VII.C shows that the graph sequence does not need to be strictly independent for the algorithm to perform well. Analysing these dependencies in more detail could yield algorithms with refined performance guarantees, e.g., for more realistic sampling regimes in which there is a correlation over time in the observed graph signal — a scenario that is highly relevant for data emerging from real-world applications.

Appendix A Proof of (24)

References

- [1] M. T. Schaub, S. Segarra, and H. Wai, “Spectral partitioning of time-varying networks with unobserved edges,” in IEEE Intl. Conf. Acoust., Speech and Signal Process. (ICASSP), May 2019, pp. 4938–4942.

- [2] S. H. Strogatz, “Exploring complex networks,” Nature, vol. 410, no. 6825, pp. 268–276, Mar. 2001.

- [3] M. E. J. Newman, Networks: An Introduction. Oxford University Press, USA, Mar. 2010.

- [4] M. O. Jackson, Social and Economic Networks. Princeton university press, 2010.

- [5] L. Page, S. Brin, R. Motwani, and T. Winograd, “The PageRank citation ranking: Bringing order to the web,” Stanford InfoLab, Technical Report 1999-66, November 1999.

- [6] M. E. J. Newman, “Modularity and community structure in networks,” Proc. of the National Academy of Sciences, vol. 103, no. 23, pp. 8577–8582, Jun. 2006.

- [7] R. Milo, E. Al, and C. Biology, “Network motifs: Simple building blocks of complex networks,” Science, vol. 298, no. 5594, pp. 824–827, Oct. 2002.

- [8] P. Bickel and E. Levina, “Covariance regularization by thresholding,” Ann. of Stat., vol. 36, no. 6, pp. 2577–2604, Feb. 2009.

- [9] J. Friedman, T. Hastie, and R. Tibshirani, “Sparse inverse covariance estimation with the graphical lasso,” Biostatistics, vol. 9, no. 3, pp. 432–441, Jul. 2008.

- [10] H.-T. Wai, A. Scaglione, and A. Leshem, “Active sensing of social networks,” IEEE Trans. Signal Inf. Process. Netw., vol. 2, no. 3, pp. 406–419, Sep. 2016.

- [11] S. Segarra, M. T. Schaub, and A. Jadbabaie, “Network inference from consensus dynamics,” in IEEE Conf. Decision and Control (CDC), Dec. 2017, pp. 3212–3217.

- [12] S. Shahrampour and V. M. Preciado, “Reconstruction of directed networks from consensus dynamics,” in American Control Conf. (ACC), Jun. 2013, pp. 1685–1690.

- [13] X. Wu, H. T. Wai, and A. Scaglione, “Estimating social opinion dynamics models from voting records,” IEEE Trans. Signal Process., vol. 66, no. 16, pp. 4193–4206, Aug. 2018.

- [14] Y. Zhu, M. T. Schaub, A. Jadbabaie, and S. Segarra, “Network inference from consensus dynamics with unknown parameters,” arXiv preprint arXiv:1908.01393, 2019.

- [15] J. Damoiseaux, S. Rombouts, F. Barkhof, P. Scheltens, C. Stam, S. M. Smith, and C. Beckmann, “Consistent resting-state networks across healthy subjects,” Proc. of the National Academy of Sciences, vol. 103, no. 37, pp. 13 848–13 853, Aug. 2006.

- [16] W. Huang, T. A. W. Bolton, J. D. Medaglia, D. S. Bassett, A. Ribeiro, and D. Van De Ville, “A graph signal processing perspective on functional brain imaging,” Proc. IEEE, vol. 106, no. 5, pp. 868–885, May 2018.

- [17] T. Hoffmann, L. Peel, R. Lambiotte, and N. S. Jones, “Community detection in networks with unobserved edges,” arXiv preprint arXiv:1808.06079, 2018.

- [18] S. Segarra, G. Mateos, A. G. Marques, and A. Ribeiro, “Blind identification of graph filters,” IEEE Trans. Signal Process., vol. 65, no. 5, pp. 1146–1159, Mar. 2017.

- [19] J. Friedman, T. Hastie, and R. Tibshirani, “Sparse inverse covariance estimation with the graphical lasso,” Biostatistics, vol. 9, no. 3, pp. 432–441, 2008.

- [20] B. M. Lake and J. B. Tenenbaum, “Discovering structure by learning sparse graphs,” in Annual Cognitive Sc. Conf., Aug. 2010, pp. 778–783.

- [21] N. Meinshausen and P. Buhlmann, “High-dimensional graphs and variable selection with the lasso,” Ann. of Stat., vol. 34, no. 3, pp. 1436–1462, 2006.

- [22] H. E. Egilmez, E. Pavez, and A. Ortega, “Graph learning from data under Laplacian and structural constraints,” IEEE J. Sel. Topics Signal Process., vol. 11, no. 6, pp. 825–841, Sep. 2017.

- [23] X. Cai, J. A. Bazerque, and G. B. Giannakis, “Sparse structural equation modeling for inference of gene regulatory networks exploiting genetic perturbations,” PLOS, Computational Biology, vol. 8, no. 12, Dec. 2013.

- [24] B. Baingana, G. Mateos, and G. B. Giannakis, “Proximal-gradient algorithms for tracking cascades over social networks,” IEEE J. Sel. Topics Signal Process., vol. 8, no. 4, pp. 563–575, Aug. 2014.

- [25] O. Sporns, Discovering the Human Connectome. Boston, MA: MIT Press, 2012.

- [26] Y. Shen, B. Baingana, and G. B. Giannakis, “Kernel-based structural equation models for topology identification of directed networks,” IEEE Trans. Signal Process., vol. 65, no. 10, pp. 2503–2516, May 2017.

- [27] X. Dong, D. Thanou, P. Frossard, and P. Vandergheynst, “Learning Laplacian matrix in smooth graph signal representations,” IEEE Trans. Signal Process., vol. 64, no. 23, pp. 6160–6173, Aug. 2016.

- [28] V. Kalofolias, “How to learn a graph from smooth signals,” Jan. 2016, pp. 920–929.

- [29] S. Segarra, A. G. Marques, G. Mateos, and A. Ribeiro, “Network topology inference from spectral templates,” IEEE Trans. Signal Inf. Process. Netw., vol. 3, no. 3, pp. 467–483, Aug. 2017.

- [30] G. Mateos, S. Segarra, A. G. Marques, and A. Ribeiro, “Connecting the dots: Identifying network structure via graph signal processing,” IEEE Signal Process. Mag., vol. 36, no. 3, pp. 16–43, May 2019.

- [31] S. Fortunato and D. Hric, “Community detection in networks: A user guide,” Physics Reports, vol. 659, pp. 1–44, Jul. 2016.

- [32] U. Von Luxburg, “A tutorial on spectral clustering,” Statistics and computing, vol. 17, no. 4, pp. 395–416, Dec. 2007.

- [33] B. Ball, B. Karrer, and M. E J Newman, “Efficient and principled method for detecting communities in networks,” Physical Review. E, Statistical, nonlinear, and soft matter physics, vol. 84, p. 036103, Sep. 2011.

- [34] M. E. J. Newman and E. A. Leicht, “Mixture models and exploratory analysis in networks,” Proc. of the National Academy of Sciences, vol. 104, no. 23, pp. 9564–9569, Jul. 2007.

- [35] M. E.J. Newman and M. Girvan, “Finding and evaluating community structure in networks,” Physical Review. E, Statistical, nonlinear, and soft matter physics, vol. 69, p. 026113, Mar. 2004.

- [36] P. W. Holland, K. B. Laskey, and S. Leinhardt, “Stochastic blockmodels: First steps,” Social Networks, vol. 5, no. 2, pp. 109–137, Jun. 1983.

- [37] B. Karrer and M. Newman, “Stochastic blockmodels and community structure in networks,” Physical Review. E, Statistical, nonlinear, and soft matter physics, vol. 83, p. 016107, Jan. 2011.

- [38] E. Abbe, “Community detection and stochastic block models: Recent developments,” J. Mach. Learn. Res, vol. 18, pp. 1–86, Apr. 2017.

- [39] M. T. Schaub, S. Segarra, and J. Tsitsiklis, “Blind identification of stochastic block models from dynamical observations,” SIAM J. Math. Data Science (SIMODS) (under review), 2019.

- [40] H.-T. Wai, S. Segarra, A. E. Ozdaglar, A. Scaglione, and A. Jadbabaie, “Blind community detection from low-rank excitations of a graph filter,” IEEE Trans. Signal Process. (under review), 2019.

- [41] T. M. Roddenberry and S. Segarra, “Blind inference of centrality rankings from graph signals,” in IEEE Intl. Conf. Acoust., Speech and Signal Process. (ICASSP) (submitted), 2019.

- [42] Y. He and H. Wai, “Estimating centrality blindly from low-pass filtered graph signals,” in IEEE Intl. Conf. Acoust., Speech and Signal Process. (ICASSP) (submitted), 2019.

- [43] T. H. Cormen, C. E. Leiserson, R. L. Rivest, and C. Stein, Introduction to Algorithms, 3rd ed. The MIT Press, 2009.

- [44] D. I. Shuman, S. K. Narang, P. Frossard, A. Ortega, and P. Vandergheynst, “The emerging field of signal processing on graphs: Extending high-dimensional data analysis to networks and other irregular domains,” IEEE Signal Process. Mag., vol. 30, no. 3, pp. 83–98, Apr. 2013.

- [45] R. Olfati-Saber, J. A. Fax, and R. M. Murray, “Consensus and cooperation in networked multi-agent systems,” Proc. IEEE, vol. 95, no. 1, pp. 215–233, Mar. 2007.

- [46] N. Masuda, M. A. Porter, and R. Lambiotte, “Random walks and diffusion on networks,” Physics Reports, vol. 716, pp. 1–58, Nov. 2017.

- [47] S. Segarra, A. G. Marques, and A. Ribeiro, “Optimal graph-filter design and applications to distributed linear network operators,” IEEE Trans. Signal Process., vol. 65, no. 15, pp. 4117–4131, Aug. 2017.

- [48] M. Wax and T. Kailath, “Detection of signals by information theoretic criteria,” IEEE Trans. Acoust., Speech and Signal Process., vol. 33, no. 2, pp. 387–392, Apr. 1985.

- [49] K. Rohe, S. Chatterjee, B. Yu et al., “Spectral clustering and the high-dimensional stochastic blockmodel,” The Annals of Statistics, vol. 39, no. 4, pp. 1878–1915, 2011.

- [50] R. Vershynin, “Introduction to the non-asymptotic analysis of random matrices,” in Compressed Sensing: Theory and Applications, Y. C. Eldar and G. Kutyniok, Eds. Cambridge university press, 2012.

- [51] R. A. Horn and C. R. Johnson, Matrix analysis. Cambridge university press, 2012.

- [52] C. Boutsidis, P. Kambadur, and A. Gittens, “Spectral clustering via the power method-provably,” in International Conference on Machine Learning, 2015, pp. 40–48.

- [53] C. Davis and W. Kahan, “The rotation of eigenvectors by a perturbation. iii,” SIAM Journal on Numerical Analysis, vol. 7, no. 1, pp. 1–46, 1970.

- [54] A. Kumar, Y. Sabharwal, and S. Sen, “A simple linear time -approximation algorithm for -means clustering in any dimensions,” in IEEE Symp. on Foundations of Comp. Sci., 2004, pp. 454–462.

- [55] E. Mossel, J. Neeman, and A. Sly, “Reconstruction and estimation in the planted partition model,” Probability Theory and Related Fields, vol. 162, no. 3–4, pp. 431–461, Aug. 2015.

- [56] L. van der Maaten and G. Hinton, “Visualizing data using t-SNE,” J. Mach. Learn. Res, vol. 9, pp. 2579–2605, Nov. 2008.