Almost sure convergence of the largest and smallest eigenvalues of high-dimensional sample correlation matrices

Abstract.

In this paper, we show that the largest and smallest eigenvalues of a sample correlation matrix stemming from independent observations of a -dimensional time series with iid components converge almost surely to and , respectively, as , if and the truncated variance of the entry distribution is “almost slowly varying”, a condition we describe via moment properties of self-normalized sums. Moreover, the empirical spectral distributions of these sample correlation matrices converge weakly, with probability , to the Marčenko–Pastur law, which extends a result in [7]. We compare the behavior of the eigenvalues of the sample covariance and sample correlation matrices and argue that the latter seems more robust, in particular in the case of infinite fourth moment. We briefly address some practical issues for the estimation of extreme eigenvalues in a simulation study.

In our proofs we use the method of moments combined with a Path-Shortening Algorithm, which efficiently uses the structure of sample correlation matrices, to calculate precise bounds for matrix norms. We believe that this new approach could be of further use in random matrix theory.

Key words and phrases:

Sample correlation matrix, infinite fourth moment, largest eigenvalue, smallest eigenvalue, spectral distribution, sample covariance matrix, self-normalization, regular variation, combinatorics.1991 Mathematics Subject Classification:

Primary 60B20; Secondary 60F05 60F10 60G10 60G55 60G701. Introduction and notation

In modern statistical analyses one is often faced with large data sets where both the dimension of the observations and the sample size are large. The dramatic increase and improvement of computing power and data collection devices have triggered the necessity to study and interpret the sometimes overwhelming amounts of data in an efficient and tractable way. Huge data sets arise naturally in wireless communication, finance, natural sciences and genetic engineering. For such data one commonly studies the dependence structure via covariances and correlations which can be estimated by their sample analogs. Principal component analysis, for example, uses an orthogonal transformation of the data such that only a few of the resulting vectors explain most of the variation in the data. The empirical variances of these so-called principal component vectors are the largest eigenvalues of the sample covariance or correlation matrix.

Throughout this paper we consider the data matrix

of identically distributed entries with generic element , where we assume and if the first and second moments of are finite, respectively. A column of represents an observation of a -dimensional time series.

Random matrix theory provides a great variety of results on the ordered eigenvalues

| (1.1) |

of the (non-normalized) sample covariance matrix . Here we will only discuss the case and, unless stated otherwise, we assume the growth condition

| () |

For the finite case, we refer to [3, 32, 26]. When studying the asymptotic properties of estimators under () one often obtains results that dramatically differ from the standard fixed, case, in which the spectrum of converges to its population covariance spectrum. In 1967, Marčenko and Pastur [30] observed that even in the case of iid entries with the eigenvalues do not concentrate around . For more examples, see [6, Chapter 1] and [21]. Typical applications where () seems reasonable are discussed in [28, 19].

In comparison with , much less is known about the ordered eigenvalues

of the sample correlation matrix with entries

| (1.2) |

In this paper we will often make use of the notation and

| (1.3) |

Note that the dependence of and on is suppressed in the notation.

1.1. The case iid, and

In this case the behaviors of the eigenvalues of the sample covariance matrix and the sample correlation matrix are closely intertwined.

For any random matrix with real eigenvalues the empirical spectral distribution is defined by

Many functionals of the eigenvalues can be expressed in terms of [5], for instance

A major problem in random matrix theory is to find the weak limit of for suitable sequences ; see for example [6, 39] for more details. By weak convergence of a sequence of probability distributions to a probability distribution , we mean for all continuity points of . In this context a useful tool is the Stieltjes transform of the empirical spectral distribution :

where denotes the complex numbers with positive imaginary part. Weak convergence of to is equivalent to a.s. for all .

Under the growth condition (), the sequence of empirical spectral distributions of the normalized sample covariance matrix converges weakly to the Marčenko–Pastur law with density

| (1.6) |

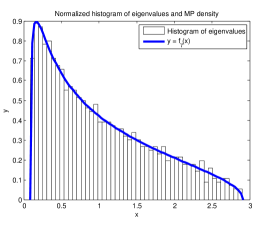

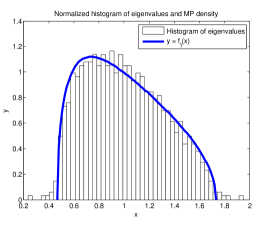

where , and . This classical result is sometimes referred to as Marčenko–Pastur theorem [30]. Informally, the histogram of is asymptotically non-random and the limiting shape depends only on the fraction . For an illustration, see Figure 1.

The Marčenko–Pastur law has -th moment

| (1.7) |

and Stieltjes transform

| (1.8) |

The a.s. behavior of the extreme eigenvalues is more involved and therefore it has received significant attention in the literature. From the Marčenko–Pastur theorem one can infer

| (1.9) |

The finiteness of the fourth moment of is necessary for the almost sure convergence of ; see [8]. If , one has (see [6])

| (1.10) |

The minimal moment requirement for the convergence of the normalized smallest eigenvalue, however, was an open question for a long time. Recently, it was proved in [36] that only requires a finite second moment. Under suitable moment assumptions and possess Tracy–Widom fluctuations around their almost sure limits. For instance, the paper [28] complemented (1.10) by the corresponding central limit theorem in the special case of iid standard normal entries:

| (1.11) |

where the limiting random variable has a Tracy–Widom distribution of order 1. Notice that the centering can in general not be replaced by . This distribution is ubiquitous in random matrix theory. Its distribution function is given by

where is the unique solution to the Painlevé II differential equation

where as and Ai is the Airy kernel; see Tracy and Widom [37] for details.

Sometimes practitioners would like to know “to which extent the random matrix results would hold if one were concerned with sample correlation matrices and not sample covariance matrices [21]”. A partial answer is that the aforementioned results also hold for the sample correlation matrix and its eigenvalues . With , we have which has the same eigenvalues as . Weyl’s inequality (see [14]) yields

| (1.12) |

where for any matrix , denotes its spectral norm, i.e., its largest singular value.

Lemma 2 in [9] implies that is equivalent to

while Hence, This approach was used in [27, 38] to derive

| (1.13) |

If the assumption is weakened to , the paper [9] proves that and . As a consequence, the limit results for and hold in probability instead of a.s.

Distributional limit results have been derived for the appropriately centered and normalized eigenvalues of sample correlation matrices. The authors of [13] assumed iid, symmetric entries and that there exist positive constants such that . They showed (1.11) with replaced by . A similar limit result holds for .

1.2. The case iid and

Asymptotic theory for the eigenvalues of in the case of an entry distribution with infinite fourth moment was studied in [33, 34, 4] in the cases when , while the authors of [15, 25] allowed nearly arbitrary growth of the dimension . In their model, the entries of are regularly varying with index , implying that

| (1.14) |

for a slowly varying function . For , which implies an infinite fourth moment, they showed that converges to a Fréchet distributed random variable with parameter while . Here the normalizing sequence is defined via , hence .

To illustrate the stark contrast between the cases and , assume () and if . Then it follows from (1.10) that

where the rate in the last line can even be increased. To the best of our knowledge, a suitable normalization such that has a nontrivial limit is not available when .

Under () the asymptotic behavior of the eigenvalues of sample correlation matrices can be very different from that of sample covariance matrices, especially for an entry distribution with infinite fourth moment. If , the Marčenko–Pastur theorem and Theorem 2.3 in [7] assert that and converge weakly to the Marčenko–Pastur law. From [8] it is known that

For , the approach to sample correlation matrices from (1.12) fails. No limit results for or seem to be available in the literature at this point, although Theorem 2.3 in [7] ensures the weak convergence of the empirical spectral distribution to the Marčenko–Pastur law if is in the domain of attraction of the normal distribution. Analogously to (1.9), the weak limit of provides a first idea what the limits of the extreme eigenvalues might be.

1.3. identically distributed, but dependent

For practical purposes it is important to work with arbitrary population covariance matrices and not just . Based on well understood results in the iid case, numerous generalizations and estimation techniques have been developed. For many models the limiting spectral distribution can only be characterized in terms of an integral equation (=Marčenko–Pastur equation) for its Stieltjes transform. Explicit solutions are more involved; see the monographs [6, 5, 39]. Over the last couple of years significant progress on limiting spectral distributions for dependent time series was achieved; see for example [12, 11, 10]. Since the sample covariance matrix is a poor estimator for the population covariance matrix in high dimension, a different approach to the fundamental problem of estimating population eigenvalues is needed. In [22] the authors find that the bootstrap works for the top eigenvalues if they are sufficiently separated from the bulk. Among others, El Karoui [20] proposed to use the Marčenko–Pastur equation, which basically requires more insight into the empirical spectral distribution and its support. This was achieved in [18], where an algorithm for calculating the spectral distribution based on certain approximate integral equations for its Stieltjes transform was presented.

In view of [17, 16, 15] the behavior of the top eigenvalues is reasonably well understood in the case of linear dependence among the and . If , similar arguments to (1.12) can be developed to show that methods for sample covariance matrices can be applied to sample correlation matrices; see for example [21]. Theorem 1 in [21] proves that if the spectral norm of the population correlation matrix is uniformly bounded and , then the spectral properties of and are asymptotically the same. In particular, if , then .

1.4. About this paper

In Section 2 we introduce the basic assumptions of this paper and discuss their meaning. The main results are given in Section 3. We show that the limiting spectral distribution of the sample correlation matrices is the Marčenko–Pastur law (Theorem 3.1) and that the extreme eigenvalues converge a.s. to the endpoints of the limiting support (Theorem 3.3) provided has iid entries such that their truncated variance is “almost slowly varying”. In this sense, the limiting spectral distribution of sample correlation matrices is universal. A similar kind of universality holds for the limiting spectral distribution of sample covariance matrices given a finite variance, while the asymptotic behavior of their extreme eigenvalues is totally different if the fourth moment is infinite. Thus the eigenvalues of sample correlation matrices exhibit a “more robust” behavior than their sample covariance analogs. This is perhaps not surprising in view of the self-normalizing property of sample correlations. Self-normalization also has the advantage that one does not have to worry about the correct normalization. This is a crucial problem in the study of sample covariance matrices in the case of an infinite fourth moment where one needs a normalization stronger than the classical one. We conclude Section 3 with a small simulation study which shows that the asymptotic results work nicely.

We continue with some technical results in Section 4. These are of independent interest because they provide a Path-Shortening Algorithm for the calculation of bounds for the very high moments of . We believe that this technique is novel and will be of further use for proving results in random matrix theory. The proofs of our main results Theorems 3.3 and 3.1 are given in Sections 5 and 6, respectively. Both proofs heavily depend on the techniques developed in Section 4. We conclude with an Appendix which contains some auxiliary analytical results.

Condition () is crucial for the proof of Theorem 3.1. In Section 2 we discuss this condition and find out that it is very close to condition (2.2) which in turn is very close (but not equivalent) to membership of the distribution of in the domain of attraction of the Gaussian law. We conjecture that the statement of Theorem 3.1 may be proved only under (2.2).

2. Assumptions

In this section we will present some distributional assumptions and discuss their meaning. We assume that is an iid field with generic element . In order to exclude the degenerate case we assume . Recall the notation

| (2.1) |

For ease of notation we will sometimes write , and .

2.1. Domain of attraction type-condition for the Gaussian law

One of the basic assumptions in this paper is

| (2.2) |

In [24] it was proved that condition (2.2) holds if the distribution of is in the domain of attraction of the normal law, which is equivalent to being slowly varying.

The converse implication is not valid. Indeed, let be a positive function such that and consider a symmetric random variable with tail for sufficiently large. Then we have

and therefore is not slowly varying, or, equivalently, the distribution of is not in the domain of attraction of the normal law, but (2.2) is valid as a domination argument shows.

Jonsson [29] proved that , with equality if and only if is symmetric. He also gave an explicit expression for the mixed moment

In view of the identity , one makes the interesting observation that is always nonnegative.

2.2. Condition ()

This condition will be crucial for the proofs in this paper:

There exists a sequence such that for some integer sequence

with we have , and the moment inequality

| () |

holds for and any positive integers satisfying , where .

Next we shed some light on this condition. It turns out to be closely related to (2.2). Indeed, assume (). Iteration of () for any fixed yields

In particular, . Thus, () provides some precise rate at which converges to zero. Condition () implies that

which is satisfied for regularly varying distributions with index .

Moreover, () does not hold if . If () were valid we would have for large ,

For example, Proposition 1 in [31] asserts that the distribution of is in the domain of attraction of an -stable distribution with if and only if

| (2.3) |

hence () does not hold if has a regularly varying tail with index .

The expectations in () can be calculated by using the following formula due to [24]:

| (2.4) |

where , and .

Example 2.1 (Standard normal distribution).

3. Main results

Our first result identifies the limit of the empirical spectral distribution of the sample correlation matrix for iid random fields with generic element .

Theorem 3.1 (Limiting spectral distribution).

Remark 3.2.

Part (1) with condition (2.2) replaced by was proved in [27]. Later, in [7] the finite variance assumption was replaced by the weaker condition that the distribution of belongs to the domain of attraction of the normal law. We discussed in the previous section that (2.2) holds under the latter condition. Part (2) shows that (2.2) is the minimal condition for part (1) if is symmetric. By Lemma B.1 in [6], implies weak convergence of to the Marčenko–Pastur distribution as the latter is uniquely determined by its moments .

If is symmetric, and , a slight modification of the proof of part (2) combined with the method of moments yields weakly. Consequently, for any the number of eigenvalues outside is a.s. In particular, if is fixed, then and converge to a.s. In view of part (2), one concludes that is a necessary and sufficient condition for the a.s. convergence of the eigenvalues if is symmetric and fixed.

When one has to deal with the potentially eigenvalues outside the support of the limiting spectral distribution. We develop a method to overcome this problem at the expense of strengthening the assumption to ().

A Borel–Cantelli argument to obtain an upper bound for requires an adequate bound on , where . To this end, we use the inequality

and determine those summands on the right-hand side which are largest when weighted by their multiplicities. Using our Path-Shortening Algorithm, which is a novel technique that efficiently uses the inherent structure of sample correlation matrices, their contribution is calculated explicitly. The other summands can –with considerable technical effort– be controlled by (). Note that because of the identity the behavior of moments of the empirical spectral distribution is closely linked to the above upper bound.

The following result provides general conditions for the a.s. convergence of the largest and smallest eigenvalues and of to the endpoints of the Marčenko–Pastur law. The proof of this result is given in Section 5.

Theorem 3.3 (Limit of extreme eigenvalues).

Remark 3.4.

Part (1) was proved in [27, 38]; see the discussion in Section 1. Theorem 3.3 indicates that the a.s. convergence of the extreme eigenvalues of does not depend on the finiteness of the fourth or even second moment; see also the discussion in section 2.2. This is in stark contrast to the a.s. behavior of , the largest eigenvalue of the sample covariance matrix . Note that there is a phase transition of the a.s. asymptotic behavior of the extreme eigenvalues at the border between finite and infinite fourth moment of , while such a transition occurs for the empirical spectral distribution at the border between finite and infinite variance.

3.1. Simulation study

In this subsection we simulate a large data matrix of iid entries. We compare the spectra of and to the limiting Marčenko–Pastur spectral density with appropriate parameter ; see Theorem 3.1. We simulate from different distributions of and choose various values for and to cover Marčenko–Pastur distributions of several shapes. In what follows, we assume , whenever the second moment is finite.

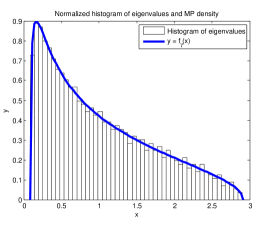

In Figure 1 we simulated a data matrix with iid entries drawn from a -distribution which we renormalized to meet the requirement . To illustrate the weak convergence of and we plot the histograms of the eigenvalues and and compare them to the Marčenko–Pastur distribution with . As expected in the case , the values and are very close to their theoretical almost sure limits and , respectively. The same is valid for and .

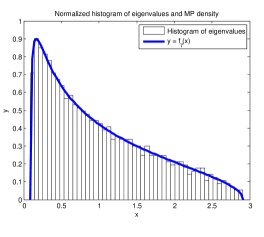

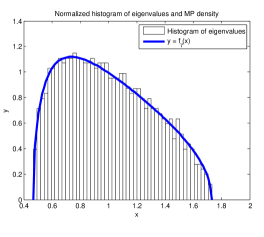

In Figure 2 we simulate from a renormalized -distribution with unit variance. The histograms of and resemble the corresponding Marčenko–Pastur density . Note that can be larger than the right endpoint since it has a different limit behavior than in the case , while and are close to the endpoints and , respectively, for which Theorem 3.3 provides a formal justification.

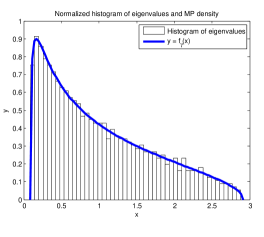

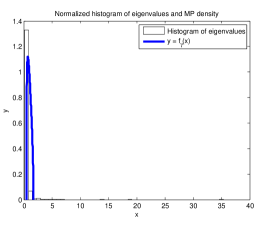

In Figures 4 and 4 we simulated from distributions with infinite fourth moment. We drew from a symmetrized Pareto distribution with parameter to create the plots in Figure 4. Note that in this case , while for any , i.e., we are at the “border” between finite and infinite fourth moment. The extreme eigenvalues in the sample correlation case are very close to their theoretical limits stated in Theorem 3.3, whereas the largest eigenvalues of the sample covariance matrix cease to lie within the support of the Marčenko–Pastur distribution. Note that the assumption is superfluous for the sample correlation plots due to self-normalization. For the histogram of the knowledge of the correct value is crucial since, for instance, In applications, needs to be estimated first and estimation errors might significantly alter the conclusion. One can easily imagine that Figure 1(b) with a misspecified variance of the data could have resembled Figure 4(b). In this respect sample correlations are more robust.

In Figure 4, we choose from the standardized -distribution, moving closer to the infinite variance case. The histogram of fits the Marčenko–Pastur density very well and the extreme eigenvalues are located in a close proximity of the endpoints of the Marčenko–Pastur support. The sample covariance case in (b) does not look particularly appealing due to the fact that there are a few relatively large eigenvalues. For example, while is only . By [4, 25, 15], the properly normalized converges to a Fréchet distributed random variable. The correct normalization is roughly and hence it is expected that is separated from the bulk, whose behavior ultimately determines the limiting spectral distribution, which is the Marčenko–Pastur law with parameter . However, due to the separation between the top eigenvalues and the bulk, it is not obvious from a histogram with only classes that the Marčenko–Pastur law provides a good fit to the spectral distribution in (b). This different behavior of sample correlations and covariances is an additional argument for the higher stability of results obtained from an analysis of the sample correlation matrix.

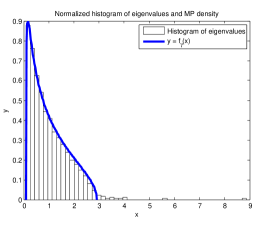

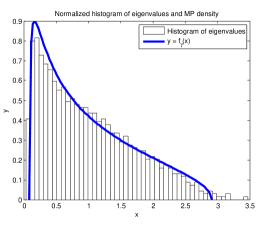

Finally, we turn to the case where the assumptions of Theorem 3.1 are violated. We present two histograms of with in Figure 5. In (a), we choose the non-symmetric for . In (b), the simulated is standardized . The plots look surprisingly stable, given that the empirical spectral distribution does not weakly converge to the Marčenko–Pastur law; see Theorem 3.1(2). The extreme eigenvalues and are much further away from and , respectively, than in all the other sample correlation histograms we have seen so far.

3.2. A version of condition () for finite fourth moment and beyond

In applications it is quite challenging to check condition () for a given distribution. In principle, () can be verified by direct calculation using (2.4). However, for some classical distributions, such as the - and symmetrized Pareto distributions, (2.4) requires the calculation of a high-dimensional integral which might not always be as easy to compute as in Examples 2.1 and 2.2. Due to the complexity of the calculations, this paper does not contain a nicely worked out example of a distribution with infinite fourth moment that satisfies ().

In the existing literature the almost sure convergence of the extreme eigenvalues was established for finite fourth moment only. Section 3.1 indicates that the result holds for infinite fourth moment too. A necessary and sufficient condition, however, is unknown. Our condition () is a step towards the optimal condition which we believe to be for symmetric distributions. From our constructive method of proof one can see how comes into play; see also Theorem 3.1 and especially the proof of part (2) for a better understanding how the behavior of influences the limiting spectral distribution of .

In this subsection we show that a version of condition () holds for essentially all distributions with finite fourth moment. We also provide an explicit example of a distribution with infinite fourth moment such that and .

For a slowly varying sequence define and set

| (3.3) |

The sample correlation matrix of the truncated data with and

| (3.4) |

has largest and smallest eigenvalues and , respectively. If , then by Lemma 2.2 in [40], , which implies

-

Condition : There exists a slowly varying sequence such that

(3.5) and there exists a sequence such that for some integer sequence with we have and the moment inequality

(3.6) holds for and any positive integers satisfying , where .

Remark 3.5.

Loosely speaking, condition () fails if the probability of one being much larger than the sum of the other is “not small enough”. In some cases it might be easier to check condition (3.6) instead of () since one is allowed to include an extra truncation step which alleviates the aforementioned issue at the cost of the additional restriction (3.5).

We have the following version of Theorem (3.3) part (2).

Proof.

Equation (3.5) in condition is designed for comparison of the eigenvalues of and . Under (3.5), one has , which implies

| (3.8) |

Next we present a rather crude way to check for distributions with finite moment.

Corollary 3.7.

Let . If , and , then condition is valid and can be chosen as any slowly varying sequence tending to .

Proof.

If , a slowly varying sequence that satisfies (3.5) does not always exist. For instance if is regularly varying with index , we have

for some slowly varying function . For a slowly varying sequence we therefore have

| (3.12) |

As a consequence we need and a particular relationship between and for both and (3.5) to hold. An example of such a distribution is presented next.

Example 3.8 (Weak limit of extreme eigenvalues under infinite fourth moment).

Let and . Consider a symmetric random variable satisfying and

Then . If , we have for the largest eigenvalue and the smallest eigenvalue of the sample correlation matrix :

| (3.13) |

Using the crude bounds in (3.9), the almost sure convergence of the extreme eigenvalues is replaced by weak convergence.

3.3. A remark on the centered sample correlation matrix

We presented results for the matrices and , assuming that when . In practice, the expectation of typically has to be estimated. We discuss what has to be changed in the aforementioned theory in this case. We consider the matrix , where

and the corresponding correlation matrix , where is the diagonal matrix with entries

In contrast to (1.12) an application of Weyl’s inequality [6] yields

| (3.14) |

where, in general, the right-hand side does not converge to zero. However, since is a rank matrix, it is known from [6] that and share the same limiting spectral distribution (if it exists) with right endpoint say. Therefore we have

Following [21], we let , where . Then one can write and since is a symmetric matrix with eigenvalues equal to and one eigenvalue equal to we see that

We conclude

whenever a.s. Therefore the a.s. behavior of the largest eigenvalues of and is closely related.

Due to the shift and scale invariance of sample correlations, the aforementioned arguments remain valid for the ordered eigenvalues

of if and (not necessarily zero), as shown in [27]. Then we have a.s. and a.s. In Theorem 2 of [27] it was proven that if and , the empirical spectral distribution of converges weakly to the Marčenko–Pastur law.

4. Technical results

In this section we provide most technical results required for the proofs of the main theorems. We develop a new approach which efficiently uses the structure of sample correlation matrices. The goal of this section is to prove Proposition 4.7.

Throughout are iid symmetric, which implies that the are symmetric as well. We will study the moments

for and various choices of paths . In this case, is the length of the path. We say that a path is an -path if it contains exactly distinct components. A path is canonical if and . A canonical -path satisfies . Two paths are isomorphic if one becomes the other by a suitable permutation on . Each isomorphism class contains exactly one canonical path. For more details and examples of these path notions consult Section 3.1.2 in [6] and the references therein. For , define

Finally, define and

Note that if lie in the same isomorphism class. Therefore, whenever we are interested in we can assume without loss of generality that is canonical.

In what follows, we will consider transformations of the path leading to a new path . For ease of notation, we will also assume canonical. If it is not canonical, we can always work with its canonical representative, the unique canonical path in its isomorphism class.

We will show that can be often expressed as times a certain power of , where is a shorter path than . We start with two examples.

Example 4.1.

Let and recall that are symmetric. We have

Since we get , where is interpreted as a path of length zero.

Example 4.2.

For we get

Therefore we have for the shorter path .

The ideas of Examples 4.1 and 4.2 will be formalized in the path-shortening algorithm and Lemma 4.4. When calculating values of , the path-shortening function will be useful. Let . is the output of the following algorithm.

Path-Shortening Algorithm .

-

Input:

Path . Set and .

-

Step 0:

Set . Go to Step 1.

-

Step 1:

Erase runs.

-

–

If for some , where we interpret as , erase element from the path. Set , and return to Step 0.

-

–

Otherwise proceed with Step 2.

-

–

-

Step 2:

Let be the number of elements of the path which appear exactly once. Set . Then define to be the resulting (possibly shorter) path which is obtained by deleting those elements from the path . Go to Step 3.

-

Step 3:

-

–

If , then return as output.

-

–

If , set and return to Step 0.

-

–

Definition 4.3.

The path-shortening function is the output of the Path-Shortening Algorithm (PSA) where is the resulting shortened path and is the total number of elements that were removed in Step 2 of the PSA. We write .

Properties of .

Clearly, . If then , which shows that can have length zero. Furthermore, all elements in appear at least twice. If is an -path then .

Lemma 4.4.

For any , we have .

Proof.

We shall look at the changes made to in Steps 1 and 2 of the PSA separately.

Assume we are in Step 1.

-

•

If for some , where we interpret as , erase element from the path. Set .

-

•

Otherwise, .

Since Step 1 does not influence the value of it suffices to show . If there is nothing to show. Therefore assume for some . In this case, we have

| (4.1) | |||||

where we used . This proves that Step 1 poses no problem.

Next we turn to Step 2. Without loss of generality we can assume that

does not contain any runs. If all elements of appear at least twice there is nothing to prove.

Therefore assume the th element appears only once and .

Let denote the path with the th element removed.

Thus we have to show . In this case, we have

| (4.2) | |||||

where first and third equality come from writing out the definition of . For the second equality we used that is necessary for to be non-zero and . If we can apply the above argument iteratively to obtain . The proof is complete. ∎

Define for , a function by and

| (4.3) |

From now on, we assume the -paths to be canonical.

Lemma 4.5.

Let be a canonical -path of length . For any such that we have .

Proof.

Without loss of generality we may assume that is canonical. We shall sometimes refer to the ’s as -indices. In the beginning one should think of the -indices as pairwise distinct whenever possible. Their actual values are not relevant for the value . In all cases, except , there are certain -indices that have to coincide such that can be positive: for some , . This is due to the symmetry of . We will see that in some cases these are not unique. More precisely, it may happen that there is a set with distinct such that is necessary for . In these cases, the cardinality of is less than provided .

We start with the two simplest cases. If , we have for any , and hence . Moreover, if , we have if and only if , and hence .

Now we assume . Our arguments will rely on the proof of Lemma 4.4. Clearly, . From the definition of in the PSA we have . From (4.1) and (4.2) one infers

| (4.4) |

First, we analyze paths with , or equivalently . This implies ; otherwise the path-shortening function stops earlier and . Therefore, we get from the identity

| (4.5) |

that , which finishes the proof in the case . Note that (4.5) holds for all . This follows from the proof of Lemma 4.4.

Next, assume . In this case, we immediately see

| (4.6) |

Since each element in has to appear at least twice and we have . Moreover, has distinct components. As a consequence, it must hold

| (4.7) |

In view of (4.5), we have to bound . Without loss of generality may be assumed canonical: there is exactly one canonical path in the isomorphism class of and every path in an isomorphism class has the same -value. If, for example, happens to be , then we will work with the canonical representative . Write . Since is canonical, we have

For define . If we now let be the set of all such that appears as an index in , then . Finally, define

For example, if , then , and we have and .

By construction, can only be positive if . More precisely every -index in the vector needs to coincide with at least other -index of this vector. Otherwise, which would imply . The quantity is the maximum number of distinct -indices such that . Hence, there can be at most distinct -indices in . Since each appears exactly twice in ,

| (4.8) |

Remark 4.6.

The above proof reveals that if and only if . For -paths of length with , the bound is sharp. Consider for instance , where

From this relation it is easily deduced that the only canonical representatives leading to are and . The first three of them have the highest number of distinct values. We conclude . In general, the canonical paths for which the maximum in (4.3) is attained are not unique, whenever . On the other hand, if there exists exactly one canonical -path of length for which the maximum is obtained. This is an immediate consequence of the above proofs. In [6], Bai and Silverstein present a way to describe this .

For a canonical -path of length let

| (4.9) |

The function satisfies and . The set of canonical -paths of length , denoted by , can be written as a disjoint union

where contains those with .

Lemma 3.4 in [6] determines the cardinality of : for and ,

| (4.10) |

Proposition 4.7.

Proof.

is equivalent to . By Lemma 4.4,

Therefore, we only have to prove (4.11) for paths with . Without loss of generality we assume is a canonical -path. We use the notation for paths with developed in the proof of Lemma 4.5. We know that

where is a permutation of the path

Clearly, . By Lemma 4.5,

and by definition of the function ,

The main idea will be to compare to . Both of them are sums of expressions of the type

| (4.12) |

where for all , , for all and . We write

| (4.13) |

Observe that in

the non-zero summands have to satisfy . Hence, the above sum is effectively a sum only over -indices. The point we want to stress is that there is never a choice, in the sense that even though there are distinct -indices, something like is never possible. The reason is that the associated canonical -path for the -indices is unique.

For , however, the associated canonical -path for the -indices is not unique, as mentioned in Remark 4.6. Depending on the sets there are several possibilities. For instance, for we have , and . To produce a positive summand one needs with every -index appearing at least twice. In this case, has to take the same value as one of the other three -indices. Then there are two -indices left which all have to appear at least twice. In this specific example, there are three canonical paths of -indices which are listed in Remark 4.6.

We are interested in the general case. How many distinct canonical -paths of length with can exist? With the reasoning which lead to (4.8) one can show that this number is at most . This bound is attained if which implies .

For our purpose we will use a much larger bound, namely

| (4.14) |

Now let us compare and , which look very similar at first sight. The main difference is the dimension of the index sets in the summation. While the sum for contains positive elements, the sum for has at most positive elements. Let denote the set of all canonical for which the maximum in (4.3) is attained. By the above considerations, . Each element in corresponds to a different configuration of -indices in , i.e., it tells us which -indices have to be equal. Therefore, we have

| (4.15) |

where is defined as follows. Write . By construction,

. Set . Then

| (4.16) |

We will show later that

| (4.17) |

Then it follows from (4.15) and (4.17) that

Finally, an application of Lemma 4.4 gives

which completes the proof.

Next, we show (4.17) by matching each of the positive summands in (4.16) with of the positive summands in , where we recall that

| (4.18) |

By matching we mean the following. Assume we want to prove

| (4.19) |

for nonnegative and . If for every there exists a such that and the ’s are distinct, then (4.19) holds. In this case, we say that each is matched by some .

We say that and are in class if they can be written in the form

| (4.20) |

By construction, takes values in the set . A summand in class is fully determined by the vector ; see (4.13) for this notation. Hence, we call this summand of type and denote it . Note that the class is comprised of all elements of type such that and satisfies the restriction stated below equation (4.12).

Let and be index sets which contain the exact type of all summands (counted with multiplicity) of class in (4.18) and (4.16), respectively. As mentioned before, we must have

With this notation we can write

| (4.21) | |||||

| (4.22) |

We show (4.17) by a matching argument. We start by matching summands in class . From (4.20) we see that elements of class are necessarily of the form

in other words they are all equal. Note that

Therefore, we have

This shows that for each summand in class on the left-hand side of (4.17) we can find at least one summand of the same type on the right-hand side of (4.17).

Since a large number of summands of the class have not been used for matching of summands from the same class, we can use () to match them with summands of classes .

Applying () to a summand of class we obtain that it is bounded by times a summand in class . Hence, we can perform the matching in (4.17) also between different classes. Clearly, for the index set is much larger than . In fact, we have for some constant . Note that is not a strictly increasing function since some can be empty.

The matching is performed as follows: first match the class summands on the left-hand side of (4.17). Then match the class summands on the left-hand side of (4.17) with the remaining class summands on the right-hand side which have not been used for the matching yet.

Let . The general strategy is to match class summands on the left-hand side with class summands on the right-hand side. During the matching one tries to use the (still available) class summands on the right-hand side first, then turns to class , and so forth. Whenever a matching between different classes is performed an application of () is necessary to ensure that the expression on the left-hand side is bounded by whatever we have matched it with on the right-hand side. This leads to powers of and since is the highest possible power we have explained the factor in (4.17).

Note that the factor in (4.17) is there to guarantee

for sufficiently large , but it is of no central importance.

The last step in the procedure is the matching of the summands with the highest possible powers on the left-hand side of (4.17), which appear when all -indices are equal. They are elements of the class . We have

which is a simple explanation why matching of (4.21) and (4.22) with summands in the same class cannot work in general. Using () times, we can bound class summands by class summands of which we originally have , which explains the factor in (4.17). The general matching strategy applies and the proof of (4.17) is complete. ∎

5. Proof of Theorem 3.3

The following proposition contains our main technical novelty. Its proof is given after the proof of Theorem 3.3.

Proposition 5.1.

Proof of Theorem 3.3.

(2) Now assume (). The convergence of to a deterministic distribution supported on a compact interval implies that the number of the eigenvalues outside this interval is . Since the right and left endpoints of the Marčenko–Pastur law are and , respectively, we conclude from Theorem 3.1(1) that

see [6] for details. Together with Proposition 5.1 this completes the proof. ∎

Proof of equation (5.1) in Proposition 5.1

We follow [23]. By Borel–Cantelli, (5.1) holds if

| (5.3) |

where and . We choose such that and , which exists by condition (). Our goal is to show (5.3). We use that and

We rewrite by sorting according to the number of distinct components in the path . Any -path of length is an element in the disjoint union , where is the set of all -paths of length with ; see (4.9) for the definition of . Hence we have

| (5.4) |

Given a path we can look at the positions where the distinct components appear for the first time. There are such positions. The first such position is always , in general can take different values. For the second such position there are possibilities; the original minus the one from the first position. In total there are ways to assign values to these positions. For this reason

| (5.5) |

where is the set of all canonical -paths of length with . The only difference between the definitions of and is that the elements of the latter are canonical. Note that for all .

Next we bound . Consider . We will see how elements of can be constructed by modifying elements of . Let be the subset of for whose elements the integer appears exactly times as a component. Here are positive integers satisfying . Obviously it is possible to obtain by permuting the components of any . Consider the following permutation of : two components of exchange places, all others remain untouched. We denote such a switching permutation by . The number of such permutations is bounded by . Indeed, the first component can switch places with the remaining components, the second with components, etc. In total there are

ways how two components can switch positions.

Let . For any there exists an and a switching permutation such that . Here and are in general not unique. This is a consequence of the proof of Lemma 4.5. This implies

Similarly, for and there exists an and switching permutations such that which shows

| (5.8) |

5.1. Proof of equation (5.2) in Proposition 5.1

We start with the following result.

Proof.

The general idea is the same as in the proof of equation (5.1) in Proposition 5.1: we will bound the spectral norm of by the trace of high powers of this matrix and then take an appropriate root. To this end we choose an integer sequence such that and , which exists by condition (). Since the matrices and commute we have

By linearity of the trace,

| (5.10) |

From (5) combined with (4.10) we know that for sufficiently large

| (5.11) |

where . Additionally, we established

| (5.12) |

Hence, by (5.10), Lemma A.2, and noting that is continuous on , and , we have for sufficiently large,

for any . The last inequality follows from

Using the same Borel-Cantelli argument as in the proof of (5.1), one obtains the desired relation

∎

6. Proof of Theorem 3.1

6.1. Proof of Theorem 3.1(1)

We appeal to the proof of Theorem 2.3 in [7]. The following lemma is a version of Corollary 1.1 in [7].

Lemma 6.1.

Let be a non-random matrix with bounded norm and

If ,

| (6.1) | |||||

| (6.2) |

then Condition 1 of Theorem 1.1 in [7] holds, i.e.,

where .

Proof.

Remark 6.2.

Now we are ready for the proof of Theorem 3.1(1). If the distribution of is in the domain of attraction of the normal law the claim follows from Theorem 2.3 in [7], using our Lemma 6.1.

Now assume the alternative condition (2.2). We will apply Theorem 2.2 in [7] and our Lemma 6.1. Our goal is to find the limiting spectral distribution of via the limit of the Stieltjes transform of , using the fact that and have the same non-zero eigenvalues. Since for any of these matrices whenever we obtain a connection between the two spectral distributions:

Hence

| (6.3) | |||||

where we used that for a constant we have .

We introduce the matrix which is a circulant matrix whose eigenvalues can be determined as and where the latter appears with multiplicity . By [24], we have for and hence is bounded. The empirical spectral distribution

converges to the degenerate distribution with all mass at .

Now we turn to in (6.2). If we distinguish between the types of indices in we find that either possible structure for the summands in is of the type or . Keeping this in mind, we conclude that for some constant ,

The right-hand side converges to zero in view of assumption (2.2) and because (see [24])

Applications of Theorem 2.2 in [7] and our Lemma 6.1 yield for ,

Thus is the solution of the quadratic equation

By convention of [6], the square root of a complex number is the one with a positive imaginary part. Hence

Writing for the limiting Stieltjes transform of , we conclude from (6.3) and since that

which we recognize as the Stieltjes transform of the Marčenko–Pastur law in (1.6); see (1.8). The proof is complete.

6.2. Proof of Theorem 3.1(2)

Appendix A

In this section we provide some auxiliary tools for the proofs of the main results.

Lemma A.1.

Let and . Then

| (A.1) |

Proof.

For and , define the function

| (A.3) |

The following is our key lemma.

Lemma A.2.

We have for and

Proof.

From [6, page 41] we know that

Changing the order of summation one obtains

where the last equality followed from Lemma A.1 and its equivalent formulation (A.2).

For define

| (A.4) |

We have and . A straightforward induction proves the recursion

| (A.5) |

From this recursive construction one deduces that is a polynomial of degree with positive coefficients.

Next we show . Clearly we have and . Therefore assume

Then for ,

In view of (A.4), this finishes the proof. ∎

Acknowledgments A large part of this paper was written during a research visit of JH at the Statistics Department of Columbia University in the City of New York. JH thanks the Department for its great hospitality. JH and TM thank Richard A. Davis, Olivier Wintenberger and Gennady Samorodnitsky for valuable discussions on the subject.

References

- [1] Adamczak, R., Litvak, A. E., Pajor, A., and Tomczak-Jaegermann, N. Quantitative estimates of the convergence of the empirical covariance matrix in log-concave ensembles. J. Amer. Math. Soc. 23, 2 (2010), 535–561.

- [2] Adamczak, R., Litvak, A. E., Pajor, A., and Tomczak-Jaegermann, N. Sharp bounds on the rate of convergence of the empirical covariance matrix. C. R. Math. Acad. Sci. Paris 349, 3-4 (2011), 195–200.

- [3] Anderson, T. W. Asymptotic theory for principal component analysis. Ann. Math. Statist. 34 (1963), 122–148.

- [4] Auffinger, A., Ben Arous, G., and Péché, S. Poisson convergence for the largest eigenvalues of heavy tailed random matrices. Ann. Inst. Henri Poincaré Probab. Stat. 45, 3 (2009), 589–610.

- [5] Bai, Z., Fang, Z., and Liang, Y.-C. Spectral theory of large dimensional random matrices and its applications to wireless communications and finance statistics. World Scientific Publishing Co. Pte. Ltd., Hackensack, NJ; University of Science and Technology of China Press, Hefei, 2014. Random matrix theory and its applications.

- [6] Bai, Z., and Silverstein, J. W. Spectral Analysis of Large Dimensional Random Matrices, second ed. Springer Series in Statistics. Springer, New York, 2010.

- [7] Bai, Z., and Zhou, W. Large sample covariance matrices without independence structures in columns. Statist. Sinica 18, 2 (2008), 425–442.

- [8] Bai, Z. D., Silverstein, J. W., and Yin, Y. Q. A note on the largest eigenvalue of a large-dimensional sample covariance matrix. J. Multivariate Anal. 26, 2 (1988), 166–168.

- [9] Bai, Z. D., and Yin, Y. Q. Limit of the smallest eigenvalue of a large-dimensional sample covariance matrix. Ann. Probab. 21, 3 (1993), 1275–1294.

- [10] Banna, M. Limiting spectral distribution of Gram matrices associated with functionals of -mixing processes. J. Math. Anal. Appl. 433, 1 (2016), 416–433.

- [11] Banna, M., and Merlevède, F. Limiting spectral distribution of large sample covariance matrices associated with a class of stationary processes. J. Theoret. Probab. 28, 2 (2015), 745–783.

- [12] Banna, M., Merlevède, F., and Peligrad, M. On the limiting spectral distribution for a large class of symmetric random matrices with correlated entries. Stochastic Process. Appl. 125, 7 (2015), 2700–2726.

- [13] Bao, Z., Pan, G., and Zhou, W. Tracy-Widom law for the extreme eigenvalues of sample correlation matrices. Electron. J. Probab. 17 (2012), no. 88, 32.

- [14] Bhatia, R. Matrix Analysis, vol. 169 of Graduate Texts in Mathematics. Springer-Verlag, New York, 1997.

- [15] Davis, R. A., Heiny, J., Mikosch, T., and Xie, X. Extreme value analysis for the sample autocovariance matrices of heavy-tailed multivariate time series. Extremes 19, 3 (2016), 517–547.

- [16] Davis, R. A., Mikosch, T., and Pfaffel, O. Asymptotic theory for the sample covariance matrix of a heavy-tailed multivariate time series. Stochastic Process. Appl. 126, 3 (2016), 767–799.

- [17] Davis, R. A., Pfaffel, O., and Stelzer, R. Limit theory for the largest eigenvalues of sample covariance matrices with heavy-tails. Stochastic Process. Appl. 124, 1 (2014), 18–50.

- [18] Dobriban, E. Efficient computation of limit spectra of sample covariance matrices. Random Matrices Theory Appl. 4, 4 (2015), 1550019, 36.

- [19] Donoho, D. High-dimensional data analysis: the curses and blessings of dimensionality. Technical Report, Stanford University (2000).

- [20] El Karoui, N. Spectrum estimation for large dimensional covariance matrices using random matrix theory. Ann. Statist. 36, 6 (2008), 2757–2790.

- [21] El Karoui, N. Concentration of measure and spectra of random matrices: applications to correlation matrices, elliptical distributions and beyond. Ann. Appl. Probab. 19, 6 (2009), 2362–2405.

- [22] El Karoui, N., and Purdom, E. The bootstrap, covariance matrices and pca in moderate and high-dimensions. Technical Report, University of California (2016).

- [23] Geman, S. A limit theorem for the norm of random matrices. Ann. Probab. 8, 2 (1980), 252–261.

- [24] Giné, E., Götze, F., and Mason, D. M. When is the Student -statistic asymptotically standard normal? Ann. Probab. 25, 3 (1997), 1514–1531.

- [25] Heiny, J., and Mikosch, T. Eigenvalues and eigenvectors of heavy-tailed sample covariance matrices with general growth rates: the iid case. Stochastic Process. Appl. (2016), 29.

- [26] Janssen, A., Mikosch, T., Mohsen, R., and Xiaolei, X. The eigenvalues of the sample covariance matrix of a multivariate heavy-tailed stochastic volatility model. Available at https://arxiv.org/abs/1605.02563 (2016).

- [27] Jiang, T. The limiting distributions of eigenvalues of sample correlation matrices. Sankhyā 66, 1 (2004), 35–48.

- [28] Johnstone, I. M. On the distribution of the largest eigenvalue in principal components analysis. Ann. Statist. 29, 2 (2001), 295–327.

- [29] Jonsson, F. On the quadratic moment of self-normalized sums. Statist. Probab. Lett. 80, 17-18 (2010), 1289–1296.

- [30] Marčenko, V. A., and Pastur, L. A. Distribution of eigenvalues in certain sets of random matrices. Mat. Sb. (N.S.) 72 (114) (1967), 507–536.

- [31] Mason, D. M., and Zinn, J. Acknowledgment of priority: “When does a randomly weighted self-normalized sum converge in distribution?” [Electron. Comm. Probab. 10 (2005), 70–81 (electronic); mr2133894]. Electron. Comm. Probab. 10 (2005), 297 (electronic).

- [32] Muirhead, R. J. Aspects of Multivariate Statistical Theory. John Wiley & Sons, Inc., New York, 1982. Wiley Series in Probability and Mathematical Statistics.

- [33] Soshnikov, A. Poisson statistics for the largest eigenvalues of Wigner random matrices with heavy tails. Electron. Comm. Probab. 9 (2004), 82–91 (electronic).

- [34] Soshnikov, A. Poisson statistics for the largest eigenvalues in random matrix ensembles. In Mathematical physics of quantum mechanics, vol. 690 of Lecture Notes in Phys. Springer, Berlin, 2006, pp. 351–364.

- [35] Srivastava, N., and Vershynin, R. Covariance estimation for distributions with moments. Ann. Probab. 41, 5 (2013), 3081–3111.

- [36] Tikhomirov, K. The limit of the smallest singular value of random matrices with i.i.d. entries. Adv. Math. 284 (2015), 1–20.

- [37] Tracy, C. A., and Widom, H. Distribution functions for largest eigenvalues and their applications. In Proceedings of the International Congress of Mathematicians, Vol. I (Beijing, 2002) (2002), Higher Ed. Press, Beijing, pp. 587–596.

- [38] Xiao, H., and Zhou, W. Almost sure limit of the smallest eigenvalue of some sample correlation matrices. J. Theoret. Probab. 23, 1 (2010), 1–20.

- [39] Yao, J., Zheng, S., and Bai, Z. Large sample covariance matrices and high-dimensional data analysis. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, New York, 2015.

- [40] Yin, Y. Q., Bai, Z. D., and Krishnaiah, P. R. On the limit of the largest eigenvalue of the large-dimensional sample covariance matrix. Probab. Theory Related Fields 78, 4 (1988), 509–521.