Risk-Averse Learning by Temporal Difference Methods

Abstract

We consider reinforcement learning with performance evaluated by a dynamic risk measure.

We construct a projected risk-averse dynamic programming equation and study its properties. Then

we propose risk-averse counterparts of the methods of temporal differences and we prove their convergence with probability one.

We also perform an empirical study on a complex transportation problem.

Keywords: Reinforcement Learning, Risk, Stochastic Approximation

AMS:

49L20, 62L20, 90C39

1 Introduction

The objective of this paper is to propose and analyze new risk-averse reinforcement learning methods for Markov Decision Processes (MDPs). Our goal is to combine the efficacy of the methods of temporal differences with the robustness of dynamic risk measures, and to provide a rigorous mathematical analysis of the methods.

MDPs are well-known models of stochastic sequential decision problems, covered in multiple monographs [5, 32, 55, 7], and having countless applications. In the classical setting, the goal of an MDP is to find a policy minimizing the expected cost over a finite or infinite horizon. Traditional MDP models, although effective for small to medium size problems, suffer from the curse of dimensionality in problems with large state space. Approximate dynamic programming approaches try to tackle the curse of dimensionality and provide an approximate solution of an MDP (see [52] for an overview). Such methods usually involve value function approximations, where the value of a state of the Markov process is approximated by a simple, usually linear, function of some selected features of the state [6].

Reinforcement learning methods [67, 52] involve simulation or observation of a Markov process to approximate the value function and learn the corresponding policies. The first studies attempted to emulate neural networks and biological learning processes, learning by trial and error [46, 27]. Some learning algorithms, such as Q-Learning [73, 74] and SARSA [59], follow this idea. One of core approaches in reinforcement learning is the method of temporal differences [66], known as TD(). It uses differences between the values of the approximate value function at successive states to improve the approximation, concurrently with the evolution of the system. TD() is a continuum of algorithms depending on a parameter which is used to exponentially weight past observations. Consequently, related methods such as Q() [73, 49, 50, 58] and SARSA() were developed [59, 58]. The methods of temporal differences have been proven to converge in the mean in [19] and almost surely by several studies, with different degrees of generality and precision [49, 20, 71, 34, 72].

We introduce risk models into temporal difference learning. In the extant literature, three basic approaches to risk aversion in MDPs have been employed: utility functions (see, e.g., [35, 36, 17, 21, 29, 4, 37]), mean–variance models (see. e.g., [76, 28, 44, 1, 13]), and entropic (exponential) models (see, e.g., [33, 45, 8, 18, 24, 41, 4]). Our research is rooted in the theory of dynamic measures of risk, which has been intensively developed in the last 15 years (see [64, 56, 57, 30, 14, 61, 3, 51, 39, 38, 15] and the references therein).

In [60], we introduced the class of Markov dynamic risk measures, specially tailored for the MDPs. It allowed for the development of dynamic programming equations and corresponding solution methods, generalizing the well-known results for the expected value problems. Our ideas were successfully extended to undiscounted problems in [11, 12], partially observable and history-dependent systems in [26, 25], and further generalized in [42, 65].

A number of works introduce models of risk into reinforcement learning: exponential utility functions [10, 9] and mean-variance models [69, 54]. Few later studies propose heuristic approaches involving coherent risk measures and their mean-risk counterparts [16, 68]; these studies employ policy gradients and use them in actor-critic type algorithms. Distributed policy gradient methods with risk measures were proposed in [43]. Model-related uncertainties are discussed in [70].

In this paper, we use Markov risk measures of [60] in conjunction with linear approximations of the value function. Our contributions can be summarized as follows:

2 The Projected Risk-Averse Dynamic Programming Equation

We consider a Markov decision process (MDP) with a finite state space , finite action sets for all , controlled transition probabilities where and , and one-step cost function , where and . For a discount factor and any non-anticipative policy for determining controls , , the expected discounted cost

is finite. For every Markovian policy , the value function associated with this policy satisfies the linear equation

Viewing as a vector, and defining the vector with elements , , and the matrix with entries , , we can compactly write the policy evaluation equation as

| (1) |

In [60], in a more general setting in a Polish space , Markov risk measures for cost evaluation in an MDP were introduced. In a finite-horizon setting, a Markov risk measure evaluates the sequence of discounted costs , , under a Markov policy , in a recursive way. Denoting by the risk of the system starting from state at time , we have

| (2) |

with , . In equation (2), the operator , where is the space of probability measures on and is the space of bounded functions on , is a transition risk mapping. It can be interpreted as risk-averse analog of the conditional expectation. Its first argument is the state (which we write as a subscript). The second argument, the vector , is the th row of the matrix : the probability distribution of the state following under the policy . The last argument, the function , is the risk of running the system from the next state in the time interval from to . The transition risk mapping is a special case of a risk form: a generalization of a risk measure introduced in [23] to accommodate the dependence of measures of risk on the underlying probability distribution. In the case of controlled Markov systems, this dependence is germane for the analysis.

As in [60], we assume that for each and each , the transition risk mapping , understood as a function its last argument, satisfies the axioms of a coherent measure of risk [2]. In the axioms below we suppress the argument , focusing on the dependence on the third argument, a function of a state:

-

Convexity:

, , ;

-

Monotonicity:

If (componentwise) then ;

-

Translation equivariance:

, for all ;

-

Positive homogeneity:

, for all .

Under these conditions, one can pass to the limit with in (2) and prove the existence of an infinite-horizon discounted risk measure [60]

We still denote its value at state by ; it will never lead to misunderstanding. The policy value satisfies the risk-averse policy evaluation equation:

We introduce the space of transition kernels on , define a vector-valued transition risk operator , with components , , and rewrite the last equation in a way similar to (1):

| (3) |

The only difference between (1) and (3) is that the matrix has been replaced by a convex operator (which still depends on ). The risk-neutral case is a special case of (3) with . References [60, 11, 12, 25] outline the theory, provide examples and applications.

Coherent risk measures admit a dual representation [62], which in our case can be stated as follows. For every a convex, closed and bounded set of probability measures on exists, such that

| (4) |

In a risk-neutral case, the set contains only one element, , but in general it is larger and has as one of its elements, provided we always have . The multifunction is called the risk multikernel. Every is absolutely continuous with respect to .

While equation (3) can be solved by a nonsmooth Newton’s method and the resulting evaluation used in a policy iteration method [60], all these techniques become impractical, when the size of the state space is very large.

An established approach to such a situation in expected value models is to assume that each state has a number of relevant features , , where , and that the value of a state can be approximated by a linear combination of its features:

| (5) |

From now on, we suppress the superscript , because most of our considerations focus on evaluating a fixed policy. We define the matrix of the features of all states, namely

Now we can write our approximation as . Similar to the expected value case, if we attempt to emulate (3) with the approximate value function, we may observe that the right hand side of the equation, , may not be represented as a linear combination of the features. Therefore, we need to project this vector on the subspace spanned by the features, . Accordingly, we define a projection operator, , and formulate the projected risk-averse approximate dynamic programming equation:

| (6) |

Still following the expected value case, we assume that the Markov system under policy is ergodic, and we denote its vector of stationary probabilities by . We define the projection operator using the following scalar product and the associated norm: , . Then

| (7) |

The fundamental question is the existence and uniqueness of a solution of equation (6). This can be answered by establishing the contraction mapping property of the right hand side of (6):

| (8) |

which would imply the existence and uniqueness of a solution of the equation

| (9) |

Crucial in this context is the distortion coefficient of the risk multikernel :

By definition, , with the value 0 corresponding to the risk-neutral model. We also recall that for we always have , for all .

Lemma 1.

The transition risk operator satisfies for all the inequalities:

| (10) | |||

| and | |||

| (11) | |||

Proof.

For brevity, we omit the argument of , because it is fixed. For every , by the mean value theorem for convex functions [75, 31], a point exists, with , and a subgradient exists, such that

Since the subdifferential , we have . Therefore, for a matrix having , , as its rows,

| (12) |

As each is a probability vector, Jensen’s inequality with , and the equation yield

| (13) |

The last two relations imply (10). In a similar way, it follows from (12) that

which is (11). ∎

We can now prove the existence and uniqueness of the solution of the risk-averse equation (9).

Theorem 2.

If then the equation (9) has a unique solution .

Proof.

We verify that the operator (8) is a contraction mapping in the norm . The orthogonal projection is nonexpansive. The operator is nonexpansive in the norm as well (this is a special case of (13) with and ). The transition risk operator multiplied by is a contraction by Lemma 1. The assertion follows now from the Banach contraction mapping theorem. ∎

If has full column rank, equation (6) has a unique fixed point as well.

3 The Risk-Averse Method of Temporal Differences

We propose to solve (6) by a risk-averse analog of the classical method of temporal differences [66]. We define to be the solution of equation (9) (which exists and is unique, if ).

Consider the evolution of the system under policy , resulting in a random trajectory of states , . At each time , we have an approximation of a solution of the equation (6). Let be the -algebra defined by all observations gathered up to time .

The difference between the left and the right hand sides of equation (6) with coefficient values and state is the risk-averse temporal difference:

| (14) |

Evidently, it cannot be easily computed or observed; this would require the evaluation of the risk and thus consideration of all possible transitions from state . Instead, we assume that we can observe a random estimate , such that

| (15) |

with some random errors . The conditions on will be specified later. This allows us to define the observed risk-averse temporal differences,

| (16) |

and to construct the risk-averse temporal difference method as follows:

| (17) |

Before proceeding to the detailed convergence proof in the stochastic case, we analyze a deterministic model of the method, in which the errors are ignored and the updates of the sequence are averaged over all states (with the distribution ). We define the operator:

| (18) |

The deterministic analog of (16)–(17) reads:

| (19) |

By the definition of the projection operator , a point is a solution of (6) if and only if

This occurs if and only if is a zero of and thus supports our idea of using the method (16)–(17).

Theorem 3.

If , then exists, such that for all the algorithm (19) generates a sequence convergent to a point such that .

Proof.

We shall show that for sufficiently small the operator is a contraction. For arbitrary and , we have

The last term (with ) can be bounded by where is some constant. Then

The scalar product can be bounded by (10), and thus

Since , then using , we have

| (20) |

with some . In particular, setting and for a solution of (6), we obtain the following relation between the successive iterates of the method (19):

| (21) |

This immediately proves that the sequence is bounded and . Every accumulation point of must be then a solution of equation (6). Substituting this accumulation point for in the last inequality, we conclude that . ∎

4 Convergence of the Risk-Averse Method of Temporal Differences

We shall use the following result on convergence of deterministic nonmonotonic algorithms [47].

Theorem 4.

Let . Suppose is a bounded sequence which satisfies the following assumptions:

-

A)

If a subsequence converges to , then , as , ;

-

B)

If a subsequence converged to , then would exist such that for all and for all , the index would be finite;

-

C)

A continuous function exists such that if converged to then would exist such that for all we would have

where is defined in B);

-

D)

The set does not contain any segment of nonzero length.

Then the sequence is convergent and all limit points of the sequence belong to .

We define the set of solutions of equation (6):

where is the unique solution of (9), provided We shall show that the method (17) converges to , under the above-mentioned condition and some additional conditions on the stepsizes and errors .

We define to be the -algebra generated by , , and make the following assumptions about the stepsize and error sequences. We allow the stepsizes to be random.

Assumption 1.

The sequence is adapted to the filtration and such that

-

(i)

, , and ;

-

(ii)

;

-

(iii)

;

-

(iv)

For any ,

Assumption 2.

The sequence of errors satisfies for the conditions

-

(i)

a.s.;

-

(ii)

a.s..

First, we establish an important implication of the ergodicity of the chain. We write for the th unit vector in .

Lemma 5.

If the chain is ergodic with stationary distribution and Assumption 1 is satisfied, then

| (22) |

and for any ,

| (23) |

Proof.

Due to the ergodicity of the chain, the vectors

are finite and satisfy the Poisson equation

| (24) |

Consider the sums . By the Poisson equation,

| (25) |

We consider the two components of the right hand side of (25), marked with brackets, separately. Due to Assumption 1, (i)—(iii), the series

is a convergent martingale. Therefore,

We now focus on the sums

Using Assumption 1(iv) and [63, Lem. A.3], we obtain (22)–(23). ∎

We can now prove the convergence of the method.

Theorem 6.

Proof.

We use the global Lyapunov function:

| (26) |

The direction used in (17) at step can be represented as

| (27) |

with the operator defined in (18), and

| (28) |

Our intention is to verify the conditions of Theorem 4 for almost all paths of the sequence . For this purpose, we estimate the decrease of the function (26) in iteration . For any we have:

The term involving was estimated in the derivation of (21). We obtain the inequality

| (29) |

Now we can verify the conditions of Theorem 4 for almost all paths of the sequence .

Condition A. Due to the boundedness of the sequence is bounded as well. In view of (27),

it is sufficient to verify that . By Assumption 2(i), the sequence

| (30) |

is a martingale.

Due to Assumption 2(ii), . In view of Assumption 1(ii), by virtue of the martingale convergence theorem, is convergent a.s.,

which yields .

Condition B.

Suppose for (on a certain path ).

If B were false, then for all we could find and such that

for all . Then for all , , we have for all . Since is not optimal,

we can choose small enough, large enough, and small enough, so that for all . Then

(29) yields

| (31) |

We fix and estimate the growth of the sums involving . We write , where, in view of (28),

Since (30) is a convergent martingale and the terms are bounded and -measurable, we have

To deal with the sum involving , observe that and thus

| (32) |

where and is a fixed vector (depending on only). It follows that

| (33) |

Dividing both sides of (33) by and using (22), we see that we can choose small enough and large enough, so that the entire expression

in parentheses in (31) is smaller than , if is large enough. But this yields , as , a contradiction.

Therefore, Condition B is satisfied.

Condition C. The inequality (31) remains valid for . By the definition

of ,

By the convergence of (30), and the boundedness of , a constant exists such that for all sufficiently large and sufficiently small , we have

Using (23), by a similar argument as in the analysis of Condition B, we can choose small enough that for all large enough so that the entire expression in parentheses in (31) is smaller than . Therefore, for all and all sufficiently large

We fix on the right hand side, and obtain

Now, the limit with respect to , , proves

Condition C.

Condition D is satisfied trivially, because for .

∎

The only question remaining is the boundedness of the sequence . It is a common issue in the analysis of stochastic approximation algorithms [40, §5.1]. In our case, no additional conditions and analysis are needed, because our Lyapunov function (26) is the squared distance to the optimal set. Therefore, a simple algorithmic modification: the projection on a bounded set intersecting with , is sufficient to guarantee boundedness. The modified method (17) reads:

| (34) |

Now, and we require that this set is nonempty. This modification does not affect our analysis in any meaningful way, because the projection is nonexpansive. In the proof of Theorem 3, we use the inequality

and proceed as before. In the proof of Theorem 6, we start from

and then continue in the same way as before. We did not include projection into the method originally, because it obscures the presentation. In practice, we have not yet encountered any need for it.

5 The Multistep Risk-Averse Method of Temporal Differences

In the method discussed so far, the residuals are corrected by moving in the direction of the last feature vector . Alternatively, we may use the weighted averages of all previous observations, where the highest weight is given to the most recent observation and the weights decrease exponentially as we look into the past observations. This idea is the core of the well-known TD() algorithm [66]. We generalize it to the risk-averse case.

For a fixed policy , we refer to as , and to as , for simplicity. The multistep risk-averse method of temporal differences carries out the following iterations:

| (35) | |||

| (36) |

where , and is given by (16). For simplicity, is assumed to be the zero vector. In the risk-neutral case, when , the method reduces to the classical TD().

Our convergence analysis will use some ideas from the analysis in the previous two sections, albeit in a form adapted to the version with exponentially averaged features. However, contrary to the expected value setting, the method (35)–(36) will converge to a solution of an equation different from (9), but still relevant for our problem.

We start from a heuristic analysis of a deterministic counterpart of the method, to extract its drift. In the next section, we make all approximations precise, but we believe that this introduction is useful to decipher our detailed approach to follow. By direct calculation,

| (37) |

and thus

Heuristically assuming that , we focus on the operator acting on the expected temporal differences. As each of the observed feature vectors affects all succeeding steps of the method, via the filter (35), we need to study the cumulative effect of many steps. We look, therefore, at the sums

Changing the order of summation and using the fact that diminishes very fast, as compared to , we get

Therefore

The last approximations are possible because and at an exponential rate. We now define the multistep transition matrix,

| (38) |

By construction, . With these approximations, we can simply write

Define the operators

| (39) |

and consider the following deterministic counterpart of (35)–(36), with :

| (40) |

Our intention is to show that for sufficiently small the method (40) converges to a point such that . Such a point is also a solution of the following projected multistep risk-averse dynamic programming equation:

| (41) |

where is the projection operator defined in (7). The solutions of (41) differ from the solutions of (6), unlike in the risk-neutral case (). If we replace with , (41) reduces to (6).

Theorem 7.

If , then exists, such that for all the algorithm (40) generates a sequence convergent to a point such that .

Proof.

For two arbitrary points and we have

| (42) |

We focus on the scalar product in the middle of the right hand side of (42):

| (43) |

Setting , we can estimate the first (quadratic) term on the right hand side of (43) by a calculation borrowed from [72, Lem. 8], with :

The last inequality is due to the fact that both and are nonexpansive in .

The second (nonsmooth) term on the right hand side of (43) can be estimated by (11), again with the use of the nonexpansiveness of :

The last term on the right hand side of (42) (with ) can be bounded by , where is some constant. Integrating all these estimates into (42), we obtain the inequality

If , then using , we obtain:

| (44) |

with some . In particular, setting and for a solution of (6), we obtain the following relation between successive iterates of the method (40):

| (45) |

This immediately proves that the sequence is bounded and . Every accumulation point of must be then a solution of equation (41). Substituting this accumulation point for in the last inequality, we conclude that the entire sequence is convergent to . ∎

6 Convergence of the Risk-Averse Multistep Method

Lemma 8.

For any array of uniformly bounded random variables

Proof.

We need another auxiliary result, extending Lemma 5 to our case.

Lemma 9.

| (46) |

and for any ,

| (47) |

Proof.

Consider the sums appearing in the numerator of (9):

In view of Lemma 8, it is sufficient to consider the sums

We transform the inner sum:

We can thus write , with

and

The second sum is a convergent martingale, because . Therefore, it satisfies (46).

Applying Lemma 5 to , we obtain both assertions. ∎

Now we can follow the arguments of §4 and establish the convergence of the multistep method.

Theorem 10.

Proof.

We represent the direction used in (36) at step as

with the operator defined in (39), and

For any solving (41), with , we have

Our intention is to verify the conditions of Theorem 4 for almost all paths of the sequence .

Condition A. The sequence is bounded by construction. Since the series (30) is a convergent martingale,

we conclude that .

Conditions B and C: We follow the proof of Theorem 6. The deterministic term involving can be estimated as in (45):

Since and are bounded, Assumptions 1 and 2 imply that is a convergent martingale.

It is worth mentioning that the convergence condition for the multistep method: , is slightly stronger that the condition for the basic method: .

Again, as in the case of the basic method, discussed in §4, the boundedness of the sequence is not an issue of concern, because it can be guaranteed by projection on a bounded set . The modified method has the following form:

| (49) |

We just need to have a nonempty intersection with the set of solutions of (41). Due to the nonexpansiveness of the projection operator, all our proofs remain unchanged with this modification, as discussed at the end of §4.

7 Empirical Study

7.1 Risk estimation

We first discuss the issue of obtaining stochastic estimates satisfying (15) and Assumption 2:

| (50) |

In the expected value case, where , we could just use the approximation value at the next state observed, , as the stochastic estimate of the expected value function. However, due to the nonlinearity of a risk measure with respect to the probability measure , such a straightforward approach is no longer possible.

Statistical estimation of measures of risk is a challenging problem, for which, so far, only solutions in special cases have been found [22]. To mitigate this problem, we propose to use a special class of transition risk mappings which are very convenient for statistical estimation. For a given transition risk mapping , we sample conditionally independent transitions from the state , resulting in states . This sample defines a random empirical distribution, , where is the th unit vector in . Since the sample is finite, we can calculate the plug-in risk measure estimate,

| (51) |

by a closed-form expression. One can verify directly from the definition that the resulting sample-based transition risk mapping

satisfies all conditions of a transition risk mapping of §2, if does. The expectation above is over all possible -samples. Therefore, if we treat as the “true” risk measure that we want to estimate, the plug-in formula (51) satisfies (15) and Assumption 2. In fact, for a broad class of measures of risk , we have a central limit result: is convergent to at the rate , and the error has an approximately normal distribution [22]. However, we do not rely on this result here, because we work with fixed . In our experiments, the sample size turned out to be sufficient, and even would work well.

7.2 Example

We apply the risk-averse methods of temporal differences to a version of a transportation problem discussed in [53]. We have vehicles at locations. At each time period , a stochastic demand for transportation from location to location occurs, , . The demand arrays in different time periods are independent. The vehicles available at location may be used to satisfy this demand. They may also be moved empty. The state of the system at time is the -dimensional integer vector containing the numbers of vehicles at each location.

For simplicity, we assume that a vehicle can carry a unit demand, and the total demand at the location at time can be satisfied only if ; otherwise, the demand may be only partially satisfied and the excess demand is lost. One can relocate the vehicles empty or loaded, and we denote the cost of moving a vehicle empty from location to location as . Since we stay in a cost minimization setting, we also denote the net negative profit of moving a vehicle loaded from location to location as . Let be the number of vehicles moved empty from location to location at time and be the number of vehicles that are moved loaded. For simplicity, let us refer to the combination of and as and denote:

In this problem, the control is decided after the state and the demand are observed. The next state is a linear function of and :

where can be written in an explicit way by counting the outgoing and incoming vehicles.

We denote by the set of decisions that can be taken at state under demand . Our approach allows us to evaluate a look-ahead policy defined by a simple linear programming problem:

| (52) |

Here, is the vector of approximate next-state values fully defining the policy. In our case, the immediate cost depends on , and thus the risk-averse policy evaluation equation (3) has the following form:

with denoting the distribution of the demand. Our objective is to evaluate the policy and to improve it. As the size of the state space is enormous, we resort to linear approximations of form , using the state as the feature vector: . The approximate risk-averse dynamic programming equation (6) takes on the form:

| (53) |

We omit the projection operator, because the feature space has full dimension. Thanks to that, the multistep approximate risk-averse dynamic programming equation (41) coincides with (53), and all risk-averse methods with solve the same equation.

In fact, we can combine the learning and policy improvement in one process, known as the optimistic approach, in which we always use the current as the vector defining the policy.

7.3 Results

We tested the risk-averse and the risk-neutral TD() methods under the same long simulated sequence of demand vectors. At every time , we sampled instances of the demand vectors, and for each instance, we computed the best decisions by (52), and the resulting states. Then we computed the empirical risk measure (51) of the approximate value of the next state, and we used it in the observed temporal difference calculation (16):

We used the mean–semideviation risk measure [48] as , which can be calculated in closed form for an empirical distribution with observed transition costs :

We used , , and . In the expected value model (), we also used observations per stage, and we averaged them, to make the comparison fair. The choice of was due to the use of a four-core computer, on which the transitions can be simulated and analyzed in parallel.

We compared the performance of the risk-averse and risk-neutral TD() algorithms for , 0.5, and 0.9, in terms of average profit per stage, on a trajectory with 20,000 decision stages. The results are depicted in Figure 1.

We observe that the risk-averse algorithms outperform their risk-neutral counterparts in terms of the average profit in the long run. We also observe that the difference in performance is more significant when is closer to zero. It would appear that with risk-averse learning no additional advantage is gained by using .

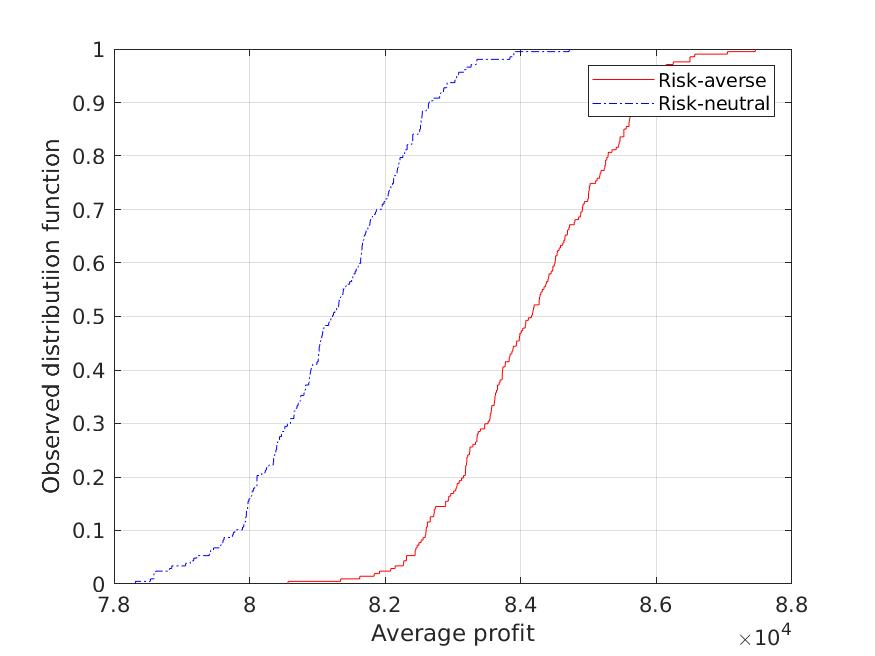

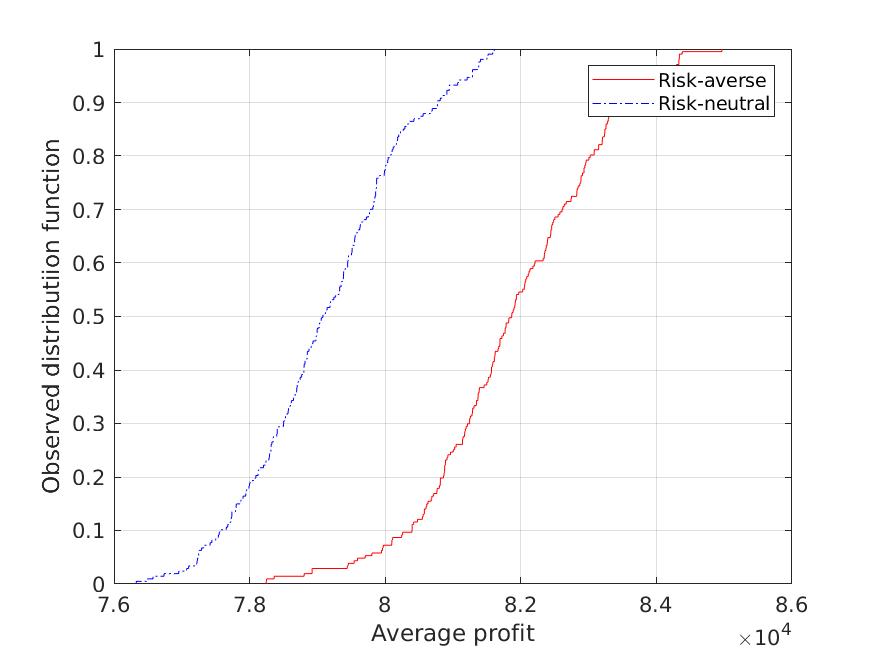

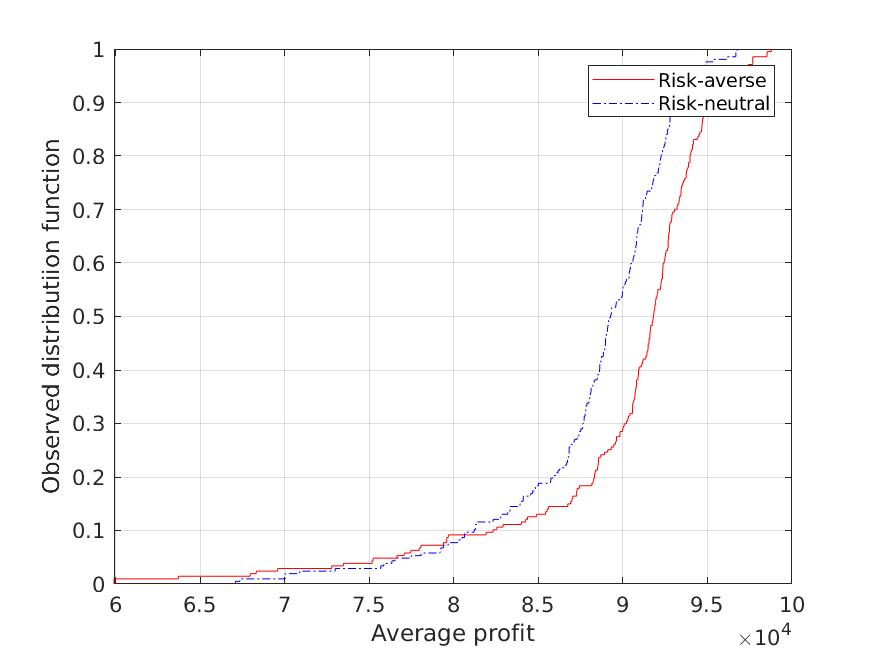

In addition to these results, we used 207 distinct trajectories, each with 200 decision stages, to compare the performance of the risk-averse and risk-neutral algorithms at the early training stages in terms of profit per stage. Figure 2 shows the empirical distribution function of the profit per stage of the risk-averse and risk-neutral algorithms at , for , 0.5, and 0.9. The results demonstrate that in the early stages of learning (), the average profit of the risk-averse algorithm is more likely to be higher than that of the risk-neutral algorithm, and the difference is very pronounced for lower values of . The first order stochastic dominance relation between empirical distributions appears to exist.

Although the risk-averse methods aim at optimizing the dynamic risk measure, rather than the expected value, they outperform the expected value model also in expectation. This may be due to the fact that the use of risk measures makes the method less sensitive to the imperfections of the value function approximation.

Acknowledgments

The authors acknowledge the Office of Advanced Research Computing (http://oarc.rutgers.edu) at Rutgers, The State University of New Jersey, for providing access to the Amarel cluster and associated research computing resources that have contributed to the results reported here.

References

- [1] A. Arlotto, N. Gans, and J. M. Steele. Markov decision problems where means bound variances. Operations Research, 62(4):864–875, 2014.

- [2] P. Artzner, F. Delbaen, J.-M. Eber, and D Heath. Coherent measures of risk. Mathematical Finance, 9(3):203–228, 1999.

- [3] P. Artzner, F. Delbaen, J.-M. Eber, D. Heath, and H. Ku. Coherent multiperiod risk adjusted values and Bellman’s principle. Annals of Operations Research, 152:5–22, 2007.

- [4] N. Bäuerle and U. Rieder. More risk-sensitive Markov decision processes. Mathematics of Operations Research, 39(1):105–120, 2013.

- [5] R. E. Bellman. A Markovian decision process. Journal of Mathematics and Mechanics, 6(5):679–684, 1957.

- [6] Richard Bellman, Robert Kalaba, and Bella Kotkin. Polynomial approximation – a new computational technique in dynamic programming. Math. Comp., 17(8):155–161, 1963.

- [7] D. P. Bersekas. Dynamic Programming and Optimal Control. Athena Scientific, 4 edition, 2017.

- [8] T. Bielecki, D. Hernández-Hernández, and S. R. Pliska. Risk sensitive control of finite state Markov chains in discrete time, with applications to portfolio management. Mathematical Methods of Operations Research, 50(2):167–188, 1999.

- [9] V. S. Borkar. Q-learning for risk-sensitive control. Mathematics of Operations Research, 27(2):294–311, 2002.

- [10] V.S. Borkar. A sensitivity formula for risk-sensitive cost and the actor–critic algorithm. Systems & Control Letters, 44(5):339 – 346, 2001.

- [11] Ö. Çavus and A. Ruszczyński. Computational methods for risk-averse undiscounted transient Markov models. Operations Research, 62(2):401–417, 2014.

- [12] Ö. Çavus and A. Ruszczyński. Risk-averse control of undiscounted transient Markov models. SIAM Journal on Control and Optimization, 52(6):3935–3966, 2014.

- [13] Z. Chen, G. Li, and Y. Zhao. Time-consistent investment policies in Markovian markets: a case of mean-variance analysis. J. Econom. Dynam. Control, 40:293–316, 2014.

- [14] P. Cheridito, F. Delbaen, and M. Kupper. Dynamic monetary risk measures for bounded discrete-time processes. Electronic Journal of Probability, 11:57–106, 2006.

- [15] P. Cheridito and M. Kupper. Composition of time-consistent dynamic monetary risk measures in discrete time. International Journal of Theoretical and Applied Finance, 14(01):137–162, 2011.

- [16] Y. Chow and M. Ghavamzadeh. Algorithms for CVaR optimization in MDPs. In Advances in neural information processing systems, pages 3509–3517, 2014.

- [17] K. J. Chung and M. J. Sobel. Discounted MDPs: distribution functions and exponential utility maximization. SIAM, 25:49–62, 1987.

- [18] S. P. Coraluppi and S. I. Marcus. Risk-sensitive and minimax control of discrete-time, finite-state Markov decision processes. Automatica, 35(2):301–309, 1999.

- [19] P. Dayan. The convergence of TD() for general . Machine Learning, 8:341–362, 1992.

- [20] P. Dayan and T. Sejnowski. TD() converges with probability 1. Machine Learning, 14:295–301, 1994.

- [21] E. V. Denardo and U. G. Rothblum. Optimal stopping, exponential utility, and linear programming. Math. Programming, 16(2):228–244, 1979.

- [22] D. Dentcheva, S. Penev, and A. Ruszczyński. Statistical estimation of composite risk functionals and risk optimization problems. Annals of the Institute of Statistical Mathematics, 69(4):737–760, 2017.

- [23] D. Dentcheva and A. Ruszczyński. Risk forms: representation, disintegration, and application to partially observable two-stage systems. Mathematical Programming, pages 1–21, 2019.

- [24] G. B. Di Masi and Ł. Stettner. Risk-sensitive control of discrete-time Markov processes with infinite horizon. SIAM J. Control Optim., 38(1):61–78, 1999.

- [25] J. Fan and A. Ruszczyński. Process-based risk measures and risk-averse control of discrete-time systems. Mathematical Programming, pages 1–28, 2018.

- [26] J. Fan and A. Ruszczyński. Risk measurement and risk-averse control of partially observable discrete-time markov systems. Mathematical Methods of Operations Research, pages 1–24, 2018.

- [27] B. G. Farley and W. A. Clark. Simulation of self-organizing systems by digital computer. IRE Transactions on Information Theory, 4:76–84, 1954.

- [28] J. A. Filar, L. C. M. Kallenberg, and H.-M. Lee. Variance-penalized Markov decision processes. Math. Oper. Res., 14(1):147–161, 1989.

- [29] W. H. Fleming and S. J. Sheu. Optimal long term growth rate of expected utility of wealth. The Annals of Applied Probability, 9:871–903, 1999.

- [30] H. Föllmer and I. Penner. Convex risk measures and the dynamics of their penalty functions. Statistics & Decisions, 24(1/2006):61–96, 2006.

- [31] JB Hiriart-Urruty. Mean value theorems in nonsmooth analysis. Numerical Functional Analysis and Optimization, 2(1):1–30, 1980.

- [32] R. A. Howard. Dynamic Programming and Markov Processes. John Wiley & Sons, 1960.

- [33] R. A. Howard and J. E. Matheson. Risk-sensitive Markov decision processes. Management Sci., 18:356–369, 1971/72.

- [34] T. Jaakkola, M. I. Jordan, and S. P. Singh. On the convergence of stochastic iterative dynamic programming algorithms. Neural Computation, 6:1185–1201, 1994.

- [35] S. C. Jaquette. Markov decision processes with a new optimality criterion: discrete time. Ann. Statist., 1:496–505, 1973.

- [36] S. C. Jaquette. A utility criterion for Markov decision processes. Management Sci., 23(1):43–49, 1975/76.

- [37] A. Jaśkiewicz, J. Matkowski, and A. S. Nowak. Persistently optimal policies in stochastic dynamic programming with generalized discounting. Mathematics of Operations Research, 38(1):108–121, 2013.

- [38] A. Jobert and L. C. G. Rogers. Valuations and dynamic convex risk measures. Mathematical Finance, 18(1):1–22, 2008.

- [39] S. Klöppel and M. Schweizer. Dynamic indifference valuation via convex risk measures. Math. Finance, 17(4):599–627, 2007.

- [40] H. Kushner and G. G. Yin. Stochastic Approximation Algorithms and Applications. Springer, New York, 2003.

- [41] S. Levitt and A. Ben-Israel. On modeling risk in Markov decision processes. In Optimization and Related Topics (Ballarat/Melbourne, 1999), volume 47 of Appl. Optim., pages 27–40. Kluwer Acad. Publ., Dordrecht, 2001.

- [42] K. Lin and S. I. Marcus. Dynamic programming with non-convex risk-sensitive measures. In American Control Conference (ACC), 2013, pages 6778–6783. IEEE, 2013.

- [43] W.-J. Ma, D. Dentcheva, and M. M. Zavlanos. Risk-averse sensor planning using distributed policy gradient. In 2017 American Control Conference (ACC), pages 4839–4844. IEEE, 2017.

- [44] S. Mannor and J. N. Tsitsiklis. Algorithmic aspects of mean-variance optimization in Markov decision processes. European J. Oper. Res., 231(3):645–653, 2013.

- [45] S. I. Marcus, E. Fernández-Gaucherand, D. Hernández-Hernández, S. Coraluppi, and P. Fard. Risk sensitive Markov decision processes. In Systems and Control in the Twenty-First Century (St. Louis, MO, 1996), volume 22 of Progr. Systems Control Theory, pages 263–279. Birkhäuser, Boston, MA, 1997.

- [46] M. L. Minsky. Theory of Neural-Analog Reinforcement Systems and Its Application to the Brain-Model Problem. PhD thesis, Princeton University, 1954.

- [47] E. A. Nurminski. Convergence conditions for nonlinear programming methods. Kibernetika (Kiev), (6):79–81, 1972.

- [48] W. Ogryczak and A. Ruszczyński. From stochastic dominance to mean–risk models: semideviations as risk measures. European Journal of Operational Research, 116:33–50, 1999.

- [49] J. Peng. Efficient Dynamic Programming-Based Learning for Control. PhD thesis, Northeastern University, 1993.

- [50] J. Peng and R. J. Williams. Incremental multi-step Q-learning. Proceedings of the Eleventh International Conference on Machine Learning, pages 226–232, 1994.

- [51] G.Ch. Pflug and W. Römisch. Modeling, Measuring and Managing Risk. World Scientific, Singapore, 2007.

- [52] W. B. Powell. Approximate Dynamic Programming - Solving the Curses of Dimensionality. Wiley, 2011.

- [53] W. B. Powell and H. Topaloglu. Approximate dynamic programming for large-scale resource allocation problems. In Models, Methods, and Applications for Innovative Decision Making, pages 123–147. INFORMS, 2006.

- [54] L. A. Prashanth and Mohammad Ghavamzadeh. Actor-critic algorithms for risk-sensitive reinforcement learning. CoRR, abs/1403.6530, 2014.

- [55] M. L. Puterman. Markov Decision Processes. Wiley, 1994.

- [56] F. Riedel. Dynamic coherent risk measures. Stochastic Processes and Their Applications, 112:185–200, 2004.

- [57] B. Roorda, J. M. Schumacher, and J. Engwerda. Coherent acceptability measures in multiperiod models. Mathematical Finance, 15(4):589–612, 2005.

- [58] G. A. Rummery. Problem Solving with Reinforcement Learning. PhD thesis, Cambridge University, 1995.

- [59] G. A. Rummery and M. Niranjan. On-line Q-learning using connectionist systems. Technical report, Engineering Department, Cambridge University, 1994.

- [60] A. Ruszczyński. Risk-averse dynamic programming for Markov decision processes. Math. Program., 125(2, Ser. B):235–261, 2010.

- [61] A. Ruszczyński and A. Shapiro. Conditional risk mappings. Mathematics of Operations Research, 31(3):544–561, 2006.

- [62] A. Ruszczyński and A. Shapiro. Optimization of convex risk functions. Mathematics of Operations Research, 31(3):433–452, 2006.

- [63] A. Ruszczyński and W. Syski. Stochastic approximation method with gradient averaging for unconstrained problems. IEEE Transactions on Automatic Control, 28(12):1097–1105, 1983.

- [64] G. Scandolo. Risk Measures in a Dynamic Setting. PhD thesis, Università degli Studi di Milano, Milan, Italy, 2003.

- [65] Y. Shen, W. Stannat, and K. Obermayer. Risk-sensitive Markov control processes. SIAM Journal on Control and Optimization, 51(5):3652–3672, 2013.

- [66] R. S. Sutton. Learning to predict by the method of temporal differences. Machine Learning, 3:9–44, 1988.

- [67] R. S. Sutton and A. G. Barto. Reinforcement Learning: An Introduction. Cambridge: MIT press, 1998.

- [68] A. Tamar, Y. Chow, M. Ghavamzadeh, and S. Mannor. Sequential decision making with coherent risk. IEEE Transactions on Automatic Control, 62(7):3323–3338, 2017.

- [69] A. Tamar, D. Di Castro, and S. Mannor. Policy gradients with variance related risk criteria. In Proceedings of the twenty-ninth international conference on machine learning, pages 387–396, 2012.

- [70] A. Tamar, S. Mannor, and H. Xu. Scaling up robust mdps using function approximation. In International Conference on Machine Learning, pages 181–189, 2014.

- [71] J. N. Tsitsiklis. Asynchronous stochastic approximation and Q-learning. Machine Learning, 16:185–202, 1994.

- [72] J. N. Tsitsiklis and B. Van Roy. An analysis of temporal-difference learning with function approximation. IEEE Fransactions on Automatic Control, 42(5):674–690, 1997.

- [73] C. J. C. H. Watkins. Learning from Delayed Rewards. PhD thesis, Cambridge University, 1989.

- [74] C. J. C. H. Watkins and P. Dayan. Q - learning. Machine Learning, 8(3-4):279–292, 1992.

- [75] L. L. Wegge. Mean value theorem for convex functions. Journal of Mathematical Economics, 1(2):207–208, 1974.

- [76] D. J. White. Mean, variance, and probabilistic criteria in finite Markov decision processes: a review. J. Optim. Theory Appl., 56(1):1–29, 1988.