Discrete-time Simulation of Stochastic Volterra Equations444We are grateful to Eduardo Abi Jaber for helpful discussions, and to two anonymous reviewers for their useful comments and suggestions.

Abstract

We study discrete-time simulation schemes for stochastic Volterra equations, namely the Euler and Milstein schemes, and the corresponding Multilevel Monte-Carlo method. By using and adapting some results from Zhang [31], together with the Garsia-Rodemich-Rumsey lemma, we obtain the convergence rates of the Euler scheme and Milstein scheme under the supremum norm. We then apply these schemes to approximate the expectation of functionals of such Volterra equations by the (Multilevel) Monte-Carlo method, and compute their complexity. We finally provide some numerical simulation results.

Key words: Stochastic Volterra equations, Euler scheme, Milstein scheme, Monte-Carlo method, MLMC.

MSC2010 subject classification: 60H20 ; 65C05 ; 65C30.

1 Introduction

We study the discrete-time approximation problem for stochastic Volterra equations of the form

| (1) |

by means of the Euler scheme, the Milstein scheme and the corresponding Multilevel Monte-Carlo method. In the above equation, is an -valued process, is a -dimensional standard Brownian motion, are (possibly singular) kernels, and are coefficient functions whose properties will be detailed below.

As natural extension of (deterministic) Volterra equations, the stochastic Volterra equation is motivated by the physics of heat transfer (see for instance the introductory example of the book of Gripenberg, Londen and Staffans [17] with a random source term), the physics of dissipative dynamics and anomalous diffusions (see for instance Jakšić and Pillet [20], resp. Lutz [25]), and has been studied since the works of Berger and Mizel [6] and Protter [27] in the non-singular kernels and Lipschitz coefficients case. Let us also mention the recent rough volatility modelling in mathematical finance, which leads to some affine Volterra equations, see e.g. El Euch and Rosenbaum [10], and Abi Jaber, Larsson, and Pulido [2].

The main objective of the paper is to study the discrete-time simulation problem for the stochastic Volterra equation (1). Observe that when , the Volterra equation degenerates into a standard SDE, and the corresponding Monte-Carlo simulation problem has been tremendously studied during the last decades. In general, the simulation of SDEs is based on discrete-time schemes, and to estimate the expectation of a functional of an SDE by Monte-Carlo method, one has two kinds of error: the discretization error and the statistical error. The statistical error is proportional to , where is the number of simulated copies of the SDE, by an application of the Central Limit Theorem. The discretization error depends essentially on the time step . For the most simple Euler scheme, a (weak) convergence rate of the discretization error has been initially obtained by Talay and Tubaro [29]. Since then, many works have been devoted to study various schemes under different conditions. For an overview on this subject, let us refer to Kloeden and Platen [22], Graham and Talay [16], and also Jourdain and Kohatsu-Higa [21] for a recent review. To reduce the discretization error, one needs to use finer discretization, which increases the computational complexity for the simulation of the process, and hence increases the statistical error given a fixed total computation effort. Then one needs to make a trade-off between the two errors to minimize the total error.

To improve the usual trade-off between the two errors, Giles [14] introduced the so-called Multilevel Monte-Carlo (MLMC) method, which has been applied and improved in various situations, and has generated a stream of literature, see e.g. Giles and Szpruch [15], Alaya and Kebaier [4], etc. The main idea of the MLMC method is to consider different levels of the time discretization, and rewrite the finest discrete scheme as a telescopic sum of differences between consecutive levels, and then to choose the number of simulations at each level in an optimal way. Let us mention that MLMC has already been studied in the setting of SDEs driven by fractional Brownian motions (denoted later by fBm): first in Kloeden, Neuenkirch and Pavani [23] with Hurst exponent and additive fractional noise, and then extensions to rough SDEs in Bayer, Friz, Riedel, and Schoenmakers [3]. This latter article corresponds to a Hurst exponent , which is still far from the observed roughness of the volatility (, see Gatheral, Jaisson and Rosenbaum [12]). The advantage of the Volterra approach compared to integration w.r.t. fBm is that one can achieve very low path regularities, while an equivalent approach through rough paths would be restricted, in practice (although not theoretically), to ([3]).

In this paper, we will study the discretization error of the Euler scheme and the Milstein scheme for the stochastic Volterra equation (1) with any Hölder regularity (Hurst exponent) between and , and then adapt the MLMC technique in our context. For the stochastic Volterra equation in a more general form, the corresponding Euler scheme has already been studied by Zhang [31], where the main results state that, for the uniform discretization scheme with time step , the discretization error is bounded by , for some constant (which is not given explicitly but might be found in the proof). In this paper, we let denote the solution of the Euler scheme with a general (not necessary uniform) discretization , and adapt the techniques in [31] to our context to obtain an explicit convergence rate of for each fixed and . Then, in place of the argument with Kolmogorov’s continuity criterium used in [31], we apply the technique based on the Garsia-Rodemich-Rumsey lemma to obtain an explicit rate for the supremum norm error . Our new technique provides a better convergence rate than the one in [31], in particular when not all moments of the initial condition are integrable, and the discretization could be arbitrary rather than the special uniform discretization of size that is required in the technical proof of [31] (see also Remark 2.3). Next, we introduce and extend our techniques and results to a higher order scheme, the Milstein scheme, in order to improve the convergence rate. We then study the MLMC method based on the Euler scheme, and compare their computational cost for a given theoretical error. These different methods are also tested with various numerical examples. We would like also to mention the recent paper [24] which appeared at the same time as ours, where the authors study both Euler and Milstein scheme of Volterra equation (1) with special kernel and . The paper establishes a convergence rate result on for every fixed , which is essentially the same as ours.

The rest of the paper is organized as follows. In Section 2, we state some conditions on and that we require for the Euler and Milstein schemes. We then present these two schemes and the corresponding convergence rate results in Theorems 2.2 and 2.4. In the third part of this section, we detail the Multilevel Monte-Carlo method to approximate quantities of the form and provide some complexity analysis for a given error. Then, in Section 3, we provide some numerical examples for these simulation methods. Finally, Section 4 gathers the proofs of Theorems 2.2 and 2.4.

2 Time discretization of the stochastic Volterra equation and the error analysis

Let us denote by the set of all -dimensional matrices, equipped with the norm defined by for all . The space is equipped with the Euclidean norm, denoted by or according to the context. Let . We consider the following stochastic Volterra equation, with the kernels , and coefficient functions , ,

| (2) |

where is a -dimensional standard Brownian motion in a filtered probability space , and the solution is an -valued continuous adapted process. Throughout the paper, we assume the conditions on and in Assumption 2.1. In particular, under Assumption 2.1, the Volterra equation (2) has a strong solution, which is unique in for some large enough (see e.g. Coutin and Decreusefond [8, Theorem 3.2] or Wang [30, Theorem 1.1]).

Let us consider, for each , a discrete grid , and denote

| (3) |

Assumption 2.1.

Let , , , , and be fixed constants,

-

whenever , and

-

for all , and , it holds that

and

-

for all , and , it holds that

and

-

for all , , it holds that

-

for all and , it holds that one has ,

Example 2.1.

2.1 The Euler scheme

As for standard SDEs, the Euler scheme can be obtained by freezing the time between two time points and in Equation (2). More precisely, for each , with defined in (3), the solution of the Euler scheme of (2) is given by

| (4) |

Remark 2.2.

In practice, we will only simulate the value of on the discrete-time grid , and this can be achieved by simulations of the increment of the Brownian motion , : let , , and then

Theorem 2.2.

Let Assumption 2.1 hold true with the constant defined therein.

Let . There exists a constant depending only on , , , and , , in Assumption 2.1 such that, for all and ,

Let, in addition, . Then for all , there exists such that

| (5) |

Remark 2.3.

When and they are equal to the identity matrix , so that the Volterra equation (2) degenerates into a standard SDE and Assumption 2.1 holds with , the convergence rate result in Theorem 2.2.(i) is consistent with results on the strong error of Euler scheme for standard SDEs.

The convergence rate result in Theorem 2.2.(ii) is less general than that of the standard SDEs. The main reason is that the solution of (2) is not a semi-martingale in general, and the Burkholder-Davis-Gundy inequality fails in this context. We instead use the Garsia-Rodemich-Rumsey lemma to obtain an estimation of the strong error on the uniform convergence norm, and need to sacrifice a small in the convergence rate.

A convergence rate result similar to (5) has also been given in Zhang [31], but without an explicit expression of the rate. Their main idea is to consider a nested sequence of uniform discretizations of the interval , and then consider as a random variable indexed by . Using the (multi-dimensional) Kolmogorov’s continuity Theorem, they obtained a strong convergence rate under the uniform convergence norm for some un undetermined . After a careful examination of their proof, their needs to be taken in instead of in our results. In this sense, our convergence rate in (5) is better than that in [31].

Nevertheless, in the case that is finite for all , one can take the constant large enough, so that can be arbitrarily small for both convergence rate results. But still, the technique of [31] requires a special nested uniform discretizations , while we can consider an arbitrary discrete time grid on .

2.2 The Milstein scheme

To obtain a higher order of convergence rate, we introduce a Milstein scheme. Let us first assume some additional conditions on the coefficient functions.

Assumption 2.3.

Let , , , be the same constants as in Assumption 2.1. Assume in addition that so that satisfies .

-

For all , it holds that

-

The coefficient functions and are in , and moreover, for all and , it holds that

and

Remark 2.4.

In the context of Example 2.1, when and , Condition still holds true. Indeed, in this example, it follows by the Cauchy-Schwarz inequality that

Recall that is defined in (3), then by freezing the time in coefficient functions (but not in ), and expanding and in the space variable , we obtain the following Milstein scheme for Equation (2):

| (6) | |||||

where

| (7) |

and

Remark 2.5.

Remark 2.6.

In the Milstein scheme (6), we do not freeze the second time variable for . In fact, in view of the last term in (6) and Condition , replacing by would induce an –error of the order

which is the same convergence as the Euler scheme (Theorem 2.2). In order to obtain an improvement of the convergence rate compared to the Euler scheme, we need to use in place of to construct the Milstein scheme. Notice that similar terms with freezing the second argument in have also appeared in the Hybrid scheme of [5], where the authors suggested

for some constants . In particular, when the Hurst constant is closed to , the singularity problem could become important. With freezing the argument in but not in when , it has a better numerical performance. See also our numerical results in Section 3.1.

Remark 2.7.

Let us consider the simulation of the Milstein scheme on the discrete-time grid , then the equation (6) and (7) can be reduced to an induction system of finite number of random variables , where is a function of , which can be written as, for some functionals ,

| (8) | |||||

The challenge would be the simulation of the (correlated) double stochastic integrals

In general, one may need to consider a finer discrete-time grid on to approximate the above integrals appearing in the induction expression of .

Nevertheless, in a first special case, where is independent of , so that , there is no double stochastic integral in the Milstein scheme (6) anymore. The problem reduces to the simulation of a fractional Brownian motion, which can be simulated exactly by computing the correlation of the increment of fractional Brownian motion. In a second special case, where , the double stochastic integral reduces to the form , which can be simulated exactly when , but is a Lévy area when as in the Milstein scheme for classical SDEs.

Theorem 2.4.

Let . There exists a constant depending only on , , and , , in Assumptions 2.1 and 2.3 such that, for all and ,

| (9) |

Let, in addition, . Then for all , there exists such that

Remark 2.8.

When , the Volterra equation (2) degenerates into the standard SDE, and Assumptions 2.1 and 2.3 hold with , so that . In this case, one has and hence the term containing in (6) disappears. Consequently, our Milstein scheme (6) turns to be exactly the same as the Milstein scheme for standard SDEs studied in the literature. Moreover, the convergence rate (9) is also the same as that of the Milstein scheme for standard SDEs (see e.g. [16, Chapter 7]).

However, for the rate under the uniform convergence norm, it is less general due to the use of Garsia-Rodemich-Rumsey lemma in our technical proof.

2.3 The (Multilevel) Monte-Carlo method and complexity analysis

Let be a functional, Lipschitz under the uniform convergence norm. We aim at estimating the expectation value:

Based on copies of simulations of on the discrete-time grid , we can use linear interpolation to obtain continuous path on , and then obtain the Monte-Carlo estimator

Given , we will compute the number of operations a computer must perform to achieve an error of order between and the corresponding Monte-Carlo estimator, such as . The number of such operations is called computational cost or complexity of the algorithm. We will first study the Euler scheme (4), and then, based on the convergence rate results for the Euler scheme, study the corresponding Multilevel Monte-Carlo (MLMC) method.

Let us assume all the conditions in Theorem 2.2.

The complexity and error analysis for the Euler scheme.

To simulate a path of solution to the Euler scheme (4) on the discrete-time grid , one needs to simulate increments of the Brownian motion and take the sum times (see Remark 2.2). The complexity to simulate copies of paths of will then be .

Now to achieve an error of order for any , we need to let both the discretization error and statistical error be of order . To control the statistical error, it is clear that one needs to set . As for the discretization error, Theorem 2.2 implies that, with satisfying

one needs to set . We summarize the previous discussion in the following proposition.

Proposition 2.9.

Denote by the complexity of the Monte-Carlo estimation of by the Euler scheme, then

| (10) |

Remark 2.10.

For Milstein scheme, if the terms in (8) can be simulated with computation effort (e.g. when , or , see Remark 2.7), the complexity to simulate copies of paths of the Milstein scheme is also of order . Then using the same argument for Euler scheme, together with the convergence rate of Milstein scheme in Theorem 2.4, one can deduce that the complexity of the Milstein scheme is bounded by with

When the terms in (8) cannot be simulated exactly, its complexity analysis would depend on how to approximate terms in practice and the corresponding approximation error.

The MLMC method.

We adapt the MLMC method of Giles [14] to our context. Although the statement of [14, Theorem 3.1] does not apply directly here, the arguments stay the same. Let be some positive integer, set so that for all . Let denote the numerical solution of the Euler scheme using the uniform discretization with step size , and

so that

| (11) |

for some constant independent of . Notice that

To estimate , we simulate i.i.d. copies of and use the estimator

To estimate for , we simulate i.i.d. copies of and use the estimator

| (12) |

Then our MLMC estimator for is given by

To meet the error level , one can set and such that

where the bound of follows from (11). By direct computations, one obtains that the complexity of the MLMC estimator is bounded, for some constant independent of , by

We summarize the previous discussion in the following proposition.

Proposition 2.11.

Denote by the complexity of the Multilevel Monte-Carlo estimation of , then

| (13) |

Remark 2.12.

The MLMC method for the Milstein scheme (6)-(7) seems also to be very interesting. Nevertheless, due to the implementation problems (see e.g. Remark 2.7), it seems less clear how to introduce an implementable algorithm. A possible approach would be extending the (antithetic) Milstein MLMC method of classical SDEs such as in [13, 15] to our context. We would like to leave this for future research.

3 Numerical examples

We will implement the simulation methods introduced above, including the Euler scheme, Milstein scheme and the MLMC method, on three Volterra equations, including two affine equations and another equation from statistical mechanics. For the two affine equations, we are able to compute explicitly the reference values for comparison in some cases.

3.1 A Volterra Ornstein-Uhlenbeck equation

We first consider a one-dimensional Volterra Ornstein-Uhlenbeck equation which is a special case of Equation (2), where for some constants and kernel , that is,

The above Volterra Ornstein-Uhlenbeck equation appears naturally in many applications, for instance in turbulence [7], or as a non-Markovian Langevin equation in statistical mechanics (see [19, 25]), and its solution can be computed explicitly (see e.g. [2]):

where

Then is a Gaussian random variable, with

We aim at estimating by the methods introduced previously, namely the Euler scheme, Milstein scheme and the MLMC method. Notice that is a constant, and hence the Milstein scheme can be easily implemented (see Remark 2.2). Let us choose parameters , , . For these parameter values, since is Gaussian, one can evaluate theoretically with arbitrary accuracy. When , one has ; when , one has ; and when , one obtains , with an error smaller than in all cases. These will serve as reference values for our numerical tests.

For both Euler scheme and Milstein scheme, we use the uniform discretisation, with time step . We will test different values on the time discretisation parameter , and for each test, we simulate copies of . The statistical error is given by , where is the empirical variance of .

For the implementation of the MLMC method (described in Section 2.3), we choose so that and . Then for each (MSE) error level , we choose the maximum level and simulation numbers for , so that the discretization error and statistical error are both bounded by . Following the arguments in [14], we choose the maximum level as follows: assume that (recall Theorem 2.2), for some constant ,

Then one has

Recall that is the estimation of , for each numerical experiment, the constant is chosen as the smallest number satisfying

| (14) |

in order to ensure (empirically) that the discretization error . To choose , we let denote the empirical variance of when (with ), the statistical error is measured by

Recall that the computation effort to estimate is proportional to , we choose which minimizes the computational effort, under the statistical error constraint, that is,

This leads to the optimal choice of :

| (15) |

Remark 3.1.

To summarize, the pseudo-code for MLMC method is given as follows:

Step 1. Initiate with .

Step 2. Set the initial value and simulate copies of , and compute its empirical variance .

Step 3. Update the values for , using (15).

Step 4. Simulate extra samples according to the updated values , and update the estimators by (12), and compute the corresponding empirical variances .

Step 5. If or (14) is not true, set and go to Step 2. Otherwise, quit the program and return the estimation .

The simulations are implemented in Python, and the simulation results, together with the reference values, are given in Tables 1, 2 and 3. We can observe the convergence of the Euler scheme and the Milstein scheme, as increases. When , the Euler scheme does not perform as well as the cases and , but the Milstein scheme performs relatively well for all the cases. This should be due to the no-time-freezing on in the Milstein scheme, which is also consistent with the results in [5] for their Hybrid scheme (see also Remark 2.6). The MLMC method converges well when decreases, and it performs better (in terms of computation time) for the regular case when than the singular case when or . We also provide the computation time for different examples, which is however only indicative. Indeed, the computation time depends not only on the complexity of the scheme, but essentially on the way the schemes are implemented in a concrete programming language. For example, for the Euler scheme, when the number of simulations are given, one can use array operations in the simulation and computation of the estimator in Python. However, for the implementation of MLMC method, one needs to use loop operations (see Remark 3.1) which may take more time for the same complexity of computation in Python.

| Mean Value | Statistical Error | Computation time(s) | |

|---|---|---|---|

| Reference value | 0.397800 | - | - |

| Euler Scheme (n=8) | 0.362125 | 0.001613 | 0.733955 |

| Euler Scheme (n=20) | 0.374513 | 0.001707 | 1.632285 |

| Euler Scheme (n=40) | 0.377491 | 0.001797 | 3.131211 |

| Euler Scheme (n=80) | 0.385454 | 0.001896 | 6.086132 |

| Milstein Scheme (n=8) | 0.399300 | 0.001690 | 5.753037 |

| Milstein Scheme (n=20) | 0.392401 | 0.001684 | 34.479045 |

| Milstein Scheme (n=40) | 0.394541 | 0.001699 | 343.109104 |

| MLMC () | 0.386223 | 0.009216 | 1.830342 |

| MLMC () | 0.406156 | 0.00738 | 9.688824 |

| MLMC () | 0.393942 | 0.005917 | 204.701933 |

| Mean Value | Statistical Error | Computation time(s) | |

|---|---|---|---|

| Reference value | 0.397202 | - | - |

| Euler Scheme (n=8) | 0.387355 | 0.001628 | 0.681871 |

| Euler Scheme (n=20) | 0.391123 | 0.001676 | 1.481485 |

| Euler Scheme (n=40) | 0.393647 | 0.001691 | 2.724405 |

| Euler Scheme (n=80) | 0.395506 | 0.001718 | 5.356922 |

| Milstein Scheme (n=8) | 0.406978 | 0.001670 | 5.532334 |

| Milstein Scheme (n=20) | 0.399021 | 0.001649 | 30.704011 |

| Milstein Scheme (n=40) | 0.398021 | 0.001642 | 339.831242 |

| MLMC () | 0.395004 | 0.003565 | 1.192638 |

| MLMC () | 0.396933 | 0.002435 | 5.099278 |

| MLMC () | 0.396543 | 0.001679 | 26.984565 |

| Mean Value | Statistical error | Computation time(s) | |

|---|---|---|---|

| Reference value | 0.373444 | - | - |

| Euler Scheme (n=8) | 0.393690 | 0.001582 | 0.677893 |

| Euler Scheme (n=20) | 0.382303 | 0.001544 | 1.453350 |

| Euler Scheme (n=40) | 0.377869 | 0.001527 | 2.673218 |

| Euler Scheme (n=80) | 0.376531 | 0.001518 | 5.246249 |

| Milstein Scheme (n=8) | 0.382396 | 0.001698 | 4.926303 |

| Milstein Scheme (n=20) | 0.378372 | 0.001693 | 17.486181 |

| Milstein Scheme (n=40) | 0.375271 | 0.001670 | 141.646946 |

| MLMC () | 0.382145 | 0.004835 | 0.389519 |

| MLMC () | 0.370043 | 0.003060 | 1.034552 |

| MLMC () | 0.374237 | 0.002400 | 1.544744 |

3.2 A Volterra equation arising in statistical mechanics

We consider next an example of stochastic Volterra equation which originates from works in statistical mechanics (see e.g. Jakšić and Pillet [20]). Namely, let denotes the couple position-speed of a particle evolving in a heat bath in a one-dimensional space. Then, adapting slightly the equations of Hamiltonian mechanics, the following equations can be derived

for some Brownian motion . Now, provided that does not vanish, rewriting the whole system in an augmented form with

yields the following stochastic Volterra equation

| (16) |

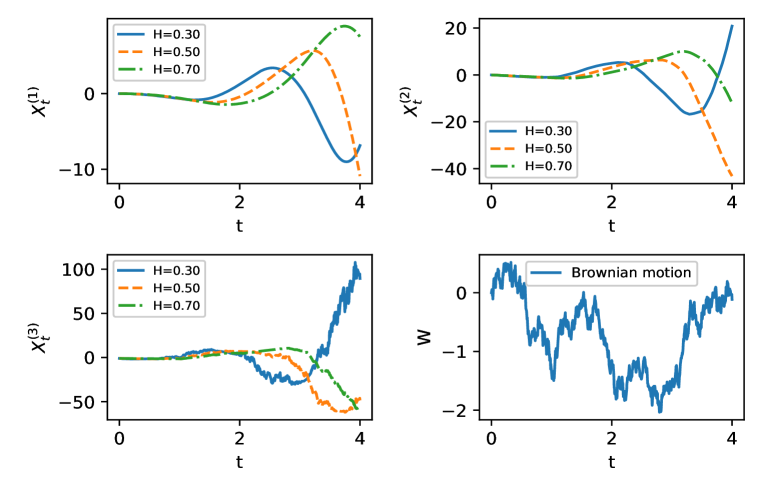

We simulate the above Volterra equation with the following parameters: , , , with or , and (which corresponds to the physical confining potential ) with . Notice that represents the position of the particle, represents the speed and the acceleration of the particle at time . In Figure 1, we provide a simulation of the paths of on time interval with different constants , by using the Euler scheme with time steps number . As expected, the roughness of increases as decreases (in fact the Hölder regularity of is almost ). As expected for Langevin-type dynamics, one can observe a mean-reversion phenomena in the simulation of in Figure 1.

We provide some estimation by Monte Carlo simulation on the 1st, 2nd and 3rd moments of the position, i.e. , and for , based on the Euler scheme and the corresponding MLMC method. For Euler scheme, each estimation is obtained with simulated copies of , and the statistical errors are given by , where is the empirical variance of for according to the case. We try different number of time steps . For the MLMC method, we use the same parameter and follow the same procedure as in Section 3.1 to compute the estimations with different MSE error .

The simulation results are provided in Tables 4 and 5. From the simulation results of the MLMC method with , for , the estimated mean value, variance and skewness of are approximately , and for , the corresponding values are approximately . It seems that the estimations from the Euler scheme simulation converge to these values as increases.

| Mean() | S. Error | Mean() | S. Error | Mean() | S. Error | |

| Euler Sch. (n=100) | 0.678132 | 0.005183 | 0.728080 | 0.007653 | 0.844422 | 0.013723 |

| Euler Sch. (n=500) | 0.783380 | 0.004610 | 0.826746 | 0.007585 | 0.948628 | 0.013016 |

| Euler Sch. (n=1000) | 0.790071 | 0.004441 | 0.825749 | 0.007319 | 0.947221 | 0.012555 |

| MLMC () | 0.775920 | 0.025893 | 0.829574 | 0.041700 | 0.969688 | 0.039718 |

| MLMC () | 0.791636 | 0.015919 | 0.807127 | 0.027351 | 0.926160 | 0.026580 |

| MLMC () | 0.810689 | 0.013005 | 0.827675 | 0.021849 | 0.934001 | 0.024089 |

| Mean() | S. Error | Mean() | S. Error | Mean() | S. Error | |

| Euler Sch. (n=100) | -1.382149 | 0.004254 | 2.085036 | 0.012392 | -3.447007 | 0.031222 |

| Euler Sch. (n=500) | -1.315642 | 0.004440 | 1.927117 | 0.012459 | -3.104342 | 0.031140 |

| Euler Sch. (n=1000) | -1.311788 | 0.004525 | 1.882418 | 0.012361 | -2.992574 | 0.029891 |

| MLMC () | -1.341978 | 0.033149 | 1.939615 | 0.055981 | -3.154188 | 0.053123 |

| MLMC () | -1.346259 | 0.029277 | 1.914329 | 0.034501 | -2.961424 | 0.040303 |

| MLMC () | -1.296778 | 0.024512 | 1.870580 | 0.027123 | -2.967358 | 0.029538 |

3.3 The Rough Heston model

We consider next the so-called rough Heston model introduced by El Euch and Rosenbaum [10] (see also [18] for a rough local volatility model). It consists of a two-dimensional equation, given by

| (17) |

where W and B are two correlated Brownian motions, with constant correlation , are positive constants, and the kernel is given by . As the square root function is defined only for , we shall replace in (17) by in the numerical implementation to avoid the technical problems when becomes negative in the simulation. Unfortunately, our main results require the Lipschitz condition on (see Assumption 2.1), and hence they do not really apply to this case. We would like to leave this question for future research. We also refer to [1] for an approximation result on this model, where one approximate the kernel by a sequence of Markovian kernels .

We choose the following parameters: , and . We will first estimate the European call option price with strike , that is, , and then consider a path-dependent Asian option with payoff

One can compute a reference value of . As described in [10], the characteristic function of the log-price is given by

where is a solution of the following fractional Ricatti equation

with and the fractional derivative and integral defined by

We use the fractional Adams method from [9] to solve the above fractional Ricatti equation, and hence obtain the function . Then can be obtained by applying the inverse Fourier transform on .

However, for the (path-dependent) Asian option pricing , it seems that there is no other method except the Monte Carlo simulation method. This is also one of our main motivations to consider the supremum norm error of the discrete time schemes.

We will implement the Euler scheme and MLMC method. For the Euler scheme, we use the uniform discretization, with time step and denote the numerical solution by . For each simulation, we simulate copies of paths of , and then estimate and by correspondingly

For the MLMC method, as the convergence rate result is not available, due to the non-Lipschitz property of the function , we will provide the simulation result of the MLMC method with different level . For a given level L, we fix the total simulation number , and then compute the optimal to minimize the statistical error under the constraint that . This leads to the optimal allocation , where is the (empirical) variance of . We choose so that .

The simulation results for European call option and the Asian option are given in Table 6. Again, one can observe the convergence of the Euler scheme as number of time steps increases, and that of MLMC method as the simulation level increases. For the estimation of the European call option price, the relative error of the Euler scheme estimation with is around 2%, and that of the MLMC estimation with is around 1%.

| Mean(Call) | Stat. Error(Call) | Mean(Asian) | Stat. Error(Asian) | |

| Reference | 0.056832 | - | - | - |

| Euler Sch. (n=4) | 0.059756 | 0.000245 | 0.040524 | 0.000169 |

| Euler Sch. (n=10) | 0.059138 | 0.000238 | 0.036344 | 0.000145 |

| Euler Sch. (n=20) | 0.058403 | 0.000234 | 0.034551 | 0.000136 |

| Euler Sch. (n=40) | 0.058494 | 0.000232 | 0.033404 | 0.000131 |

| Euler Sch. (n=80) | 0.058518 | 0.000232 | 0.033014 | 0.000128 |

| Euler Sch. (n=160) | 0.058051 | 0.000230 | 0.032626 | 0.000128 |

| MLMC () | 0.059875 | 0.000429 | 0.040321 | 0.000435 |

| MLMC () | 0.059249 | 0.000604 | 0.034407 | 0.000548 |

| MLMC () | 0.059014 | 0.000771 | 0.032762 | 0.000643 |

| MLMC () | 0.057497 | 0.000919 | 0.033050 | 0.000733 |

4 Proof of Theorems 2.2 and 2.4

Throughout this section, is a generic constant, whose value may change from line to line.

4.1 Proof of Theorem 2.2.(i)

The result and proof of Theorem 2.2.(i) are almost the same to Zhang [31, Theorem 2.3], except that we provide an explicit expression of the convergence rate. We give the proof for completeness, and more importantly, in order to provide this explicit rate. This will also allow for a better presentation of our more original contributions (i.e. Theorem 2.2.(ii) and Theorem 2.4) on the subject.

Let us first repeat and adapt [31, Lemmas 2.1 and 2.2], by adding an explicit rate estimation.

Proposition 4.1.

Let . There exists a constant depending only on , , , and , , in Assumption 2.1 such that, for all and ,

and

Proof.

Without loss of generality, let us assume that . Under more general conditions on , , and , the existence and uniqueness of in is established in the proof of Theorem 1.1 of [30], using a fixed point argument.

Let us consider first the estimation of .

Using (2), it follows by the Hölder inequality and the BDG inequality that

Further, notice that is uniformly bounded by the Hölder continuity of in (Condition ). Using again the Lipschitz condition in Condition , one has for some constant . Then by using and Hölder’s inequality (recall that , and ), one obtains a constant such that

The result then follows by Grönwall’s lemma.

We consider next the estimation of , where the proof is almost the same. Indeed, we have to consider here the integrals

| (18) |

These are Riemann sums which therefore converge, as , respectively to and , which are finite real values by . As any convergent sequence of real numbers is uniformly bounded, the two sequences in (18) are uniformly bounded in . Then one can conclude as in that, for some constant independent of and ,

Let and denote , we consider the term . Let us rewrite

and then consider , , , separately.

For , by applying Minkowski’s integral inequality (see [28, p.271]) and condition , it follows that

For , we apply BDG’s inequality, Minkowski’s integral inequality, Conditions , and on , it follows that

For , we use Minkowski’s integral inequality and Condition to obtain that

For , we apply BDG’s inequality, Minkowski’s integral inequality and use to obtain that

Then it follows that

Finally, for the estimation of , one can similarly write

Notice that the conditions in and are given also on

one can apply the same arguments to obtain the estimations for . ∎

For , we use Minkowski’s integral inequality, Proposition 4.1 and to obtain that

For , notice that by , then it follows by Minkowski’s integral inequality together with Condition and Proposition 4.1 that

For , we obtain by Hölder’s inequality and that

For , it follows by BDG’s inequality, Minkowski’s integral inequality and that

For , we use BDG’s inequality, Minkowski’s integral inequality, Proposition 4.1 and the Hölder regularity in time of (Condition ) to obtain that

For , we have by BDG’s inequality and Hölder’s inequality that, for that appears in ,

where in the last lign we used again Hölder’s inequality with .

Combining all the above estimations, it follows that

Then by Grönwall’s Lemma, we conclude that for some constant independent of and . ∎

4.2 Proof of Theorem 2.4.

We now consider the solution to the Milstein scheme (6). For ease of presentation, we consider the one-dimensional case with , and write (resp. ) in place of (resp. ). The high-dimensional case will only change the generic constant depending on . Similarly to Proposition 4.1, we first provide some related a priori estimations.

Proposition 4.2.

Proof.

Let us first consider the term . Notice that the solution is essentially defined on the discrete-time grid . When , using the induction argument and Condition , together with the boundedness of and , it is easy to deduce that for every and . Then we do not really need to localise the process to obtain the a priori estimation.

Then by the BDG inequality and Hölder’s inequality with , it follows that

| (21) |

where we applied Hölder’s inequality for the second inequality with . Next, applying again the BDG inequality and then Hölder’s inequality as before,

By the boundedness condition of and in Assumption 2.3, it follows that

Then we obtain the first estimation in (19) by Grönwall’s Lemma.

Let . By direct computation, we write

For , we deduce from the BDG inequality and Minkowski’s integral inequality that

Notice that by (4.2) and the first estimation in (19), hence it follows by Condition that

For , we use BDG’s inequality, Minkowski’s integral inequality, the first estimation in (19) and then to deduce that

Further, by similar arguments, one can also obtain the estimation on and :

and it follows that

Finally, using the first estimation in (19), one obtains from the BDG inequality and Minkowski’s integral inequality that

∎

Proof of Theorem 2.4.. Let us rewrite

For , by similar computations as in Theorem 2.2, it is easy to obtain that

For , notice that and , we have by Hölder’s inequality, Condition and Proposition 4.2 that

For , a Taylor expansion gives

where (using that the second derivative of is bounded). Then by Minkowski’s integral inequality, one has

| (22) |

Thus using the boundedness of (Assumption ) and the definitions of and in (6)-(7),

We apply Minkowski’s integral inequality for the first and third summand, and the BDG inequality for the second and the fourth, in order to obtain

Now one uses the boundedness of and , the bound from Proposition 4.2, the bound on from Proposition 4.2, and Minkowski’s integral inequality on the second and fourth summand to get

Observe that it follows from Proposition 4.2 that and that by Condition . Then the bound on from Proposition 4.2, together with conditions and , gives that

where we recall that was defined in Assumption 2.3. Plugging this bound in (22), it follows that

For , we denote by for , then by the boundedness of , , Minkowski’s integral inequality and the classical Fubini theorem, it follows that

For , we have by BDG’s inequality and Hölder’s inequality that

For , we have by BDG’s inequality, Minkowski’s integral inequality and Assumption (2.3) that

The proof to bound is the same as for : first, we have by the BDG inequality and Minkowski’s integral inequality that

where comes from the Taylor expansion of : . Similarly to the computations made for , it is clear that

Hence

In summary, one has

and one can conclude with Grönwall’s Lemma. ∎

4.3 Proof of Theorems 2.2. and 2.4.

4.3.1 Garsia-Rodemich-Rumsey’s estimates

Let us first state the following consequences of Garsia-Rodemich-Rumsey’s lemma [11].

Lemma 4.3.

Let be an -valued continuous stochastic process on , Then for all , and such that ,

Proof.

With the notations of [26, p.353-354], we apply the Garsia-Rodemich-Rumsey lemma with and to obtain the first inequality. Then the second inequality follows by the Hölder’s inequality. ∎

As a consequence of Lemma 4.3, we easily deduce the following corollary.

Corollary 4.4.

Let be a sequence of continuous processes on . Assume that there exist constants , , , , and a sequence of positive real numbers such that

Then there exists a constant , depending only on , , and , such that ,

4.3.2 Proof of Theorems 2.2. and 2.4.

Let us first consider Theorems 2.2., for which we will apply Corollary 4.4 to , with the solution to the Euler scheme (4).

Let , one has

The two first terms on the r.h.s. can be controlled using Proposition 4.1, and the two last terms would be controlled using Theorem 2.2., and it follows that, for some constant depending on but independent of and ,

| (23) |

For any and , one can set and , and let . Then the estimation in (23) satisfies the conditions in Corollary 4.4, and it follows that, for some constant ,

which proves Theorems 2.2..

The proof for Theorem 2.4. is similar. It is enough to apply Corollary 4.4 on . In place of the estimations in Proposition 4.1 and Theorem 2.2, one can use those in Proposition 4.2 and Theorem 2.4. to obtain that

for some constant independent of . The rest of the proof is then almost the same as in item . ∎

References

- Abi Jaber and El Euch [2019] E. Abi Jaber and O. El Euch. Multifactor approximation of rough volatility models. SIAM Journal on Financial Mathematics, 10(2): 309-349, 2019.

- Abi Jaber et al. [2019] E. Abi Jaber, M. Larsson, and S. Pulido. Affine Volterra processes. Ann. Appl. Probab., 29(5):3155–3200, 2019.

- Bayer et al. [2016] C. Bayer, P. K. Friz, S. Riedel, and J. Schoenmakers. From rough path estimates to multilevel Monte Carlo. SIAM J. Numer. Anal., 54(3):1449–1483, 2016.

- Alaya et al. [2015] M. Ben Alaya, A. Kebaier. Central limit theorem for the multilevel Monte Carlo Euler method. Ann. Appl. Probab., 25(1):211–234, 2015.

- [5] M. Bennedsen, A. Lunde, and M. S. Pakkanen. Hybrid scheme for Brownian semistationary processes. Finance and Stochastics 21(4): 931-965, 2017.

- Berger and Mizel [1980] M. A. Berger and V. J. Mizel. Volterra equations with Itô integrals. I. J. Integral Equations, 2(3):187–245, 1980.

- Chevillard [2017] L. Chevillard. Regularized fractional Ornstein-Uhlenbeck processes and their relevance to the modeling of fluid turbulence. Phys. Rev. E, 96(3):033111, 2017.

- Coutin and Decreusefond [2001] L. Coutin and L. Decreusefond. Stochastic Volterra equations with singular kernels. In Stochastic analysis and mathematical physics, volume 50 of Progr. Probab., pages 39–50. Birkhäuser Boston, Boston, MA, 2001.

- Diethelm et al. [2004] K. Diethelm, N. J. Ford, and A. D. Freed. Detailed error analysis for a fractional Adams method. Numer. Algorithms, 36(1):31–52, 2004.

- El Euch and Rosenbaum [2019] O. El Euch and M. Rosenbaum. The characteristic function of rough Heston models. Math. Finance, 29(1):3–38, 2019.

- Garsia et al. [1970] A. M. Garsia, E. Rodemich, and H. Rumsey. A real variable lemma and the continuity of paths of some Gaussian processes. Indiana Univ. Math. J., 20(6):565–578, 1970.

- Gatheral et al. [2018] J. Gatheral, T. Jaisson, and M. Rosenbaum. Volatility is rough. Quant. Finance, 18(6):933–949, 2018.

- Giles [2008a] M. B. Giles. Improved multilevel Monte Carlo convergence using the Milstein scheme. In Monte Carlo and quasi-Monte Carlo methods 2006, pages 343–358. Springer, Berlin, 2008a.

- Giles [2008b] M. B. Giles. Multilevel Monte Carlo path simulation. Oper. Res., 56(3):607–617, 2008b.

- Giles and Szpruch [2014] M. B. Giles and L. Szpruch. Antithetic multilevel Monte Carlo estimation for multi-dimensional SDEs without Lévy area simulation. Ann. Appl. Probab., 24(4):1585–1620, 2014.

- Graham and Talay [2013] C. Graham and D. Talay. Stochastic simulation and Monte Carlo methods: Mathematical foundations of stochastic simulation, volume 68 of Stochastic Modelling and Applied Probability. Springer, Heidelberg, 2013.

- Gripenberg et al. [1990] G. Gripenberg, S.-O. Londen, and O. Staffans. Volterra integral and functional equations, volume 34 of Encyclopedia of Mathematics and its Applications. Cambridge University Press, Cambridge, 1990.

- Jacquier and Oumgari [2019] A. J. Jacquier and M. Oumgari. Deep PPDEs for rough local stochastic volatility. ArXiv preprint, arXiv:1906.02551, 2019.

- Jakšić and Pillet [1997] V. Jakšić and C.-A. Pillet. Ergodic properties of the non-Markovian Langevin equation. Lett. Math. Phys., 41(1):49–57, 1997.

- Jakšić and Pillet [1998] V. Jakšić and C.-A. Pillet. Ergodic properties of classical dissipative systems. I. Acta Math., 181(2):245–282, 1998.

- Jourdain and Kohatsu-Higa [2011] B. Jourdain and A. Kohatsu-Higa. A review of recent results on approximation of solutions of stochastic differential equations. In Stochastic analysis with financial applications, volume 65 of Progr. Probab., pages 121–144. Birkhäuser/Springer Basel AG, Basel, 2011.

- Kloeden and Platen [1992] P. E. Kloeden and E. Platen. Numerical solution of stochastic differential equations, volume 23 of Applications of Mathematics (New York). Springer-Verlag, Berlin, 1992.

- Kloeden et al. [2011] P. E. Kloeden, A. Neuenkirch, and R. Pavani. Multilevel Monte Carlo for stochastic differential equations with additive fractional noise. Ann. Oper. Res., 189(1):255–276, 2011.

- Li [2020] M. Li, C. Huang, and Y. Hu. Numerical methods for stochastic Volterra integral equations with weakly singular kernels. ArXiv preprint arXiv:2004.04916, 2020.

- Lutz [2012] E. Lutz. Fractional Langevin equation. In Fractional dynamics, pages 285–305. World Sci. Publ., Hackensack, NJ, 2012.

- Nualart [2006] D. Nualart. The Malliavin calculus and related topics. Probability and its Applications (New York). Springer-Verlag, Berlin, second edition, 2006.

- Protter [1985] P. Protter. Volterra equations driven by semimartingales. Ann. Probab., 13(2):519–530, 1985.

- Stein [1970] E. M. Stein. Singular integrals and differentiability properties of functions. Princeton Mathematical Series, No. 30. Princeton University Press, Princeton, N.J., 1970.

- Talay and Tubaro [1990] D. Talay and L. Tubaro. Expansion of the global error for numerical schemes solving stochastic differential equations. Stoch. Anal. Appl., 8(4):483–509, 1990.

- Wang [2008] Z. Wang. Existence and uniqueness of solutions to stochastic Volterra equations with singular kernels and non-Lipschitz coefficients. Statist. Probab. Lett., 78(9):1062–1071, 2008.

- Zhang [2008] X. Zhang. Euler schemes and large deviations for stochastic Volterra equations with singular kernels. J. Differential Equations, 244(9):2226–2250, 2008.