Can Two Forecasts Have the Same Conditional Expected Accuracy?††thanks: We thank Todd Clark and Mike McCracken for comments on an early version of the paper.

Abstract

The approach for testing equal predictive accuracy for pairs of forecasting models proposed by Giacomini and White, (2006) assumes that the parameters of the underlying forecasting models are estimated using a rolling window of fixed width and incorporates the effect of parameter estimation in the null hypothesis. We show that a necessary and sufficient condition for the conditionally expected loss differential of two forecasting models to be a martingale difference sequence is that the outcome is a simple average of the two forecasts. When the forecasts contain parameter estimation errors, this means that the conditional mean of the outcome has to be a function of past estimation errors–a condition that fails in many situations. We also show that the null can fail even in the absence of parameter estimation for many types of stochastic processes in common use.

1 Introduction

In an important contribution to the literature on economic forecasting, Giacomini and White, (2006) (GW, henceforth) develop a novel approach for comparing the accuracy of alternative economic forecasts and test the null of equal expected predictive accuracy. GW incorporate the effect of parameter estimation in the null hypothesis and assume that estimation error does not vanish asymptotically by requiring that fixed-length windows are used to estimate the parameters of the underlying forecasting models. Using this approach, simple tests of equal predictive accuracy do not have a degenerate limiting distribution even in comparisons of nested forecasting models, thus addressing a key problem causing difficulties for earlier tests.111See, e.g., West, (1996), Clark and McCracken, (2001), Clark and McCracken, (2005) and McCracken, (2007).

The GW test has found widespread use in applied work in economics and has become the standard method for comparing the predictive accuracy of nested forecasting models while accounting for the effect of parameter estimation.222As of end-May, 2020, Giacomini and White, (2006) has nearly 1,400 Google Scholar citations. It is, therefore, important to establish conditions under which the null hypothesis entertained by GW is valid and so can be used to compare the predictive accuracy of alternative forecasts. The null hypothesis in GW is that the expected loss differential, i.e., the difference between the expected loss of a pair of forecasts, is a martingale difference sequence (MDS) conditional on some information set which typically includes, at a minimum, current and past observations of the outcome and data used to generate the forecasts.

We show here that the MDS property conditional on past data fails to hold in many situations when the forecasts are generated using a set of estimated model parameters as assumed in the analysis of GW. This conclusion holds regardless of whether a fixed-width rolling window or an expanding window is used to estimate the parameters of the underlying forecasting models and regardless of whether the models are nested or non-nested. Caution should therefore be exercised when applying the conditional GW test to compare the performance of forecasting models. Even in the absence of parameter estimation error, we show that the MDS property fails whenever the underlying data generating process (DGP) for the outcome does not satisfy a restrictive finite dependence condition that rules out many standard models used in applied work.

This conclusion has important practical implications. In particular, there can be substantial autocorrelation in the loss difference and we show that the GW test can result in severe size distortions for testing an unconditional null using popular schemes for estimating the long-run variance of the loss differential. We also establish a valid procedure for testing that the null of equal predictive accuracy of two rolling-window forecasts holds “on average”. This sub-sampling t-test approach uses a self-normalization structure and avoids directly constructing robust standard errors that account for serial correlation in the loss differentials.

It is worth emphasizing that our analysis pertains to tests of the null hypothesis that the expected loss differential is mean-zero conditional on the parameter estimates used by the underlying forecasting models and possibly other information. It does not apply to tests of the null that the unconditional mean of the loss differential equals zero. This unconditional null does not require that two forecasts are equally accurate at each point in time but only that they are equally accurate on average. Testing this unconditional null is more common in practice and is typically conducted using the popular Diebold-Mariano test.

The outline of our analysis is as follows. Section 2 introduces our setup and demonstrates that the GW null fails to be valid in the presence of estimated parameters and also fails in the absence of a restrictive finite dependence condition on the DGP. Second 3 pursues practical implications of our theoretical results, while Second 4 analyzes tests of the null that the forecasts have the same unconditionally expected loss, and Section 5 concludes. Proofs are contained in an appendix.

2 The null of equal conditional expected predictive accuracy

This section introduces the forecast environment and demonstrates that the GW null is not, in general, appropriate for comparing the conditionally expected loss of a pair of forecasting models.

2.1 Setup

Our forecast environment closely mirrors the setup in GW. We are interested in comparing the predictive accuracy of a pair of one-step-ahead forecasts of some variable .333For simplicity, we restrict the forecast horizon to a single period, but our results are easily generalized to arbitrary horizons of finite length. Each forecast is generated using information available at time , where , and is a set of predictor variables. Hence, contains current and past values of the outcome, forecast and predictors. GW carefully state that the forecasts are adapted to the most recent values of , i.e., .444Note that the estimation window, , can differ for the two forecasting models, i.e., we can have and define and all results continue to go through. The setup includes, but is not limited to, linear prediction models of the form estimated by least squares, i.e., .

The precision of the forecasts is evaluated using a loss function, which is a mapping from the space of outcomes and forecasts to the real line. Under the commonly used squared error loss, , where () is the forecast error. Furthermore, following Diebold and Mariano, (1995), define the loss differential as the loss of model 1 relative to that of model 2:

| (1) |

Under squared error loss,

| (2) |

The null hypothesis considered by GW is that, conditional on some information set, , the loss differential is a martingale difference sequence (MDS):

| (3) |

almost surely for . GW write that “Note that we do not require , although this is a leading case of interest…” For simplicity, in the rest of the paper, we focus on this leading case with .

Forecast comparisons are often conducted using (pseudo) out-of-sample evaluation methods which split a sample of observations into an initial sample using observations for parameter estimation and a forecast evaluation sample which consists of the remaining observations, so .555Out-of-sample forecast evaluations can have substantially weaker power than full-sample tests (see, e.g., Inoue and Kilian, (2005) and Hansen and Timmermann, 2015b ), but are less prone to data mining biases (Hansen and Timmermann, 2015a ) and can provide important information about the time-series evolution in a prediction model’s performance and its value in real time. GW assume that is bounded by a finite constant although, in general, we can regard and as functions of . For notational simplicity, we suppress the subscripts.

To test the null in (3), GW propose the test statistic666For simplicity, we choose the instrument to be a constant.

| (4) |

The simple expression in the denominator exploits the property that, under the null (3) that follows a MDS, there is no need to correct for possible serial correlation in .

To test the hypothesis that almost surely, GW point out that one can choose any random variable and test the unconditional moment condition . However, when , there exists a variable such that . Hence, results in GW hinge on the MDS condition which we examine in this paper.

2.2 Implications of the MDS null

We first establish a necessary and sufficient condition for the validity of the null hypothesis in (3):

Proposition 1.

Assume that almost surely. Then under squared error loss almost surely if and only if almost surely.

This result shows that the conditionally expected loss differential follows an MDS process if and only if the conditional expectation of the outcome is a simple average of the two forecasts. When the forecasts contain parameter estimation errors, this means that the conditional mean of has to be a function of past estimation errors. This is quite unnatural as DGPs are typically considered to be objective processes whose dynamics is not related to an estimation scheme.

Proposition 1 can be used constructively to establish cases in which the null hypothesis in (3) is valid, as we next show.

Example 1.

Suppose that with =0, so . Moreover, if and , then so that, from Proposition 1, the squared error loss differential follows an MDS process.

A popular practice is to estimate the parameters of the forecasting model using the most recent observations. In our leading case as well as in GW, is fixed or bounded, so that estimation errors do not vanish, while the asymptotic analysis lets . As we shall see, this case can never satisfy almost surely without a restrictive finite dependence condition and so the MDS condition (3) cannot hold.

Example 2.

As a simple example with estimation error, let for be -period moving averages, while

where is an MDS so . Setting and , both forecasts use misspecified (under-dimensioned) forecasting models that omit one moving average component. However, once again we have , so it follows from Proposition 1 that the squared error loss follows an MDS process. 777We thank a referee for suggestion these two examples.

Even for forecasts that do not depend on estimated parameters, we can show that the MDS property fails whenever the underlying DGP does not satisfy the restrictive finite dependence condition. In particular, let denote the -algebra generated by data from time to . All forecasts based on a rolling window of size are -measurable; this allows for any estimation methodology ranging from the basic least-squares estimators to sophisticated machine learning methods. Recall that denotes the -algebra generated by all the data up to time .

We next show that the MDS condition (3) cannot hold for if the outcome variable does not have finite dependence:

Proposition 2.

Assume that almost surely and . If and are both -measurable, then is not a martingale difference sequence, i.e., .

The finite-dependence condition in Proposition 2 requires that the conditional mean of only depends on the most recent data points. This condition is ruled out by many widely used models that are not finite-order Markov such as MA and ARMA processes as well as unobserved components (state space) models and GARCH-in-mean processes.

2.3 MDS Property and Estimation Scheme

Proposition 2 shows that unless with probability one, the loss difference cannot be an MDS, no matter how one computes the forecasts with or without estimated parameters and regardless of the estimation method. The result also does not require us to make specific assumptions on the DGP such as stationarity. Hence, in the absence of the restrictive finite dependence condition, there is an inherent contradiction between the MDS property and rolling window estimation.

In most forecasting problems, the main challenge is to model and estimate the conditional mean . However, Proposition 1 says that the MDS null is equivalent to . Since and are computed from a fixed-width rolling window, this result is saying that the true conditional mean can be learned from the data without letting the sample size increase.

This is quite a restrictive setup. Even if we have a correctly specified parametric model for the entire distribution with parameter , the optimal estimator (i.e., the maximum likelihood estimate) for in the rolling window of length would have an error of rate . Hence, having no estimation error at all for for fixed is hard to imagine.

In the following AR example, we show that the MDS null fails to hold under realistic estimation schemes with finite estimation windows.

Example 3.

, where is i.i.d with . Thus, the -algebra from the observed data is . Suppose that and , where and with are vectors with elements in . For , we assume that for some measurable function , where is finite. Notice that some components of are allowed to be zero; hence, without loss of generality, we can assume that .

Building on this example, we have the following result:

Lemma 1.

Suppose that , where is i.i.d with . Assume that almost surely and that has a density. If , then is not a martingale difference sequence.

The requirement that almost surely is very weak and only rules out cases in which is never positive, for sure. Typically, the estimation window is larger than the number of lags . Therefore, we should expect that entries for will affect . As a result, conditional on , we should expect non-zero variations in . By Lemma 1, for autoregressive DGPs with lags, we should not expect the MDS null to hold if the estimation window is larger than under commonly used estimators (OLS, MLE or GMM).

2.4 Nested models

For the nested case, consider the DGP

| (5) |

where is a vector of fixed regressors and is i.i.d from . Consider the forecasts from a big model (intercept and ) and a small model (intercept only): with and .

Proposition 3.

Let , , and . Suppose that

| (6) |

Then, under squared error loss (2),

-

1.

.

-

2.

is not a Martingale Difference Sequence, i.e., .

Proposition 3 holds for any sample size and has two implications. First, the MDS condition fails when is fixed (rolling estimation window) and the length of the out-of-sample period () tends to infinity. Second, the MDS condition also fails when both and tend to infinity, i.e., with an expanding estimation window.

2.5 Non-nested models

For the case with non-nested models consider the DGP

| (7) |

where . We use and , where for . The following result states that the MDS condition (3) fails:

Proposition 4.

Proposition 4 holds regardless of the sample size, , used to estimate the parameters , . This again means that the MDS condition fails when is fixed and tends to infinity or when both and tend to infinity.888Part 2 of Proposition 4 allows for any estimator that uses information up to time and so is not limited to the OLS estimator.

3 Practical Implications

Proposition 1 has some interesting practical implications. To see this, define the forecast error from a simple equal-weighted average of forecasts:

| (8) |

From Proposition 1, the MDS null hypothesis for the loss differential can equivalently be stated as , motivating a test that is different from the GW test that is based on the loss differential.

A priori, it may not be obvious whether it is better, in a given sample, to test or . Although such tests are equivalent, their finite sample power could well be very different and practitioners will want to maximize power in testing the MDS null. In some situations, an alternative test based on might have better power properties than one based on .

We next illustrate this point through an analytical example and an empirical application.

3.1 Power for AR(1) Process

Following McCracken, (2020), consider the following first-order autoregressive DGP:

| (9) |

where is i.i.d with and . Assume that is bounded. Let and so that when . To examine local power, let , where is a constant and is the sample sized used for the test. To simplify notations, let and consider the following test statistics:

| (10) |

and

| (11) |

Both test statistics use critical values from a standard Gaussian distribution, . For a test of nominal size , we therefore reject the null if and under the GW and tests, respectively. The following result can be used to compute the power of the tests.

Proposition 5.

Suppose is generated from a first-order autoregressive process . Then

and

where and follows the stationary distribution of .

This result implies that the local power of always exceeds that of the test for this example. To see this, notice that by Holder’s inequality,

which implies that

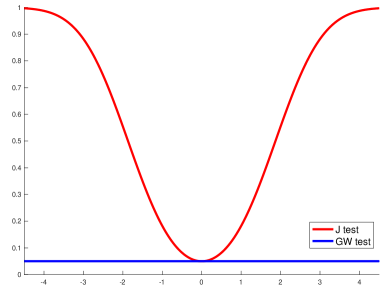

If has a symmetric distribution, i.e., and have the same distribution, then the test based on has no power at all because has a symmetric distribution and thus . For example, if , then , which implies that and for any . We illustrate this result in Figure 1.

For this example, , which means that the power of the test based on increases in ; in other words, the power of this test is higher for more persistent DGP’s.

It is worth emphasizing that the result in Proposition 5 hinges on using the equal-weighted forecast as our instrument, . The key point is that although and are testing the same MDS null for loss differences, they can have very different power properties for a given choice of instrument.

3.2 Empirical Application

We next illustrate how the insights from our analysis can be used to compare the accuracy of forecasts of two important economic variables, namely US monthly inflation and GDP growth. Specifically, we obtain data from the St. Louis Federal Reserve on the seasonally adjusted consumer price index for all urban consumers (CPIAUCSL) from 1947:01 to 2022:07. From this we compute the monthly inflation rate. Next, we consider the seasonally adjusted Gross Domestic Product (GDP), again obtained from the St. Louis Federal Reserve Fred data base. This is a quarterly series and runs from 1947Q1 through 2022Q2. Again we compute the quarter-over-quarter growth rate and use this as our dependent variable.

For both variables our benchmark models the conditional mean of the dependent variable as a constant while the alternative model uses an AR(4) process. Model parameters are estimated recursively using a 10-year rolling window that gets updated as new data arrive.

As our first instrument, we use the lagged value of the equal-weighted forecast error, i.e., . For this case, we obtain test statistics and for the inflation rate data and and for the GDP growth data. Hence, in both cases the test strongly rejects the null while the GW test fails to reject.

The empirical results will of course depend on the chosen instrument. To examine the robustness of our finding, we also consider using instead the difference between the two forecasts as our instrument, setting . Using this instrument, we obtain test statistics and for the inflation data and and for the GDP growth data. In this case, the test strongly rejects the null of equal conditional predictive accuracy for the inflation data while the test fails to reject. Neither test rejects the null for the GDP growth rate data.

4 Testing Equal Unconditional Expected Predictive Accuracy

So far we have demonstrated that the null that the loss differential follows an MDS generally, though not always, fails to hold conditional on the information set used to generate the forecasts. One might wonder what the GW test is actually testing when the MDS null fails. The obvious candidate is the corresponding unconditional null:

| (12) |

To examine whether we can use the GW approach to test the null in (12), we separately consider cases with a rolling and an expanding estimation window.

4.1 Rolling estimation window

To see what happens with a rolling estimation window, consider the following simple example:

Example 4.

Suppose that where is iid with , and . We use and . Assuming squared error loss, we can simply choose to make the unconditional null hold (i.e., ).

For the rolling window case, is fixed and tends to infinity. Because is fixed, is weakly dependent and stationary. However, the asymptotic distribution of the GW test statistic under the unconditional null hypothesis is not . To obtain higher power, GW prefer to use an estimator of the variance of the loss differences that exploits the MDS property of loss differences under the null. However, they also note in Comment 5 that one can use a HAC estimator in situations with, e.g., positive autocorrelation in loss differences. In practice, tests of the unconditional null in (12) are therefore often conducted using an approach similar to that adopted by Diebold and Mariano, (1995) which uses a consistent estimator of the long-run variance of the loss differences and so accounts for any temporal dependencies that may exist.

Using Example 4, we next show that converges in distribution to a normal distribution but with variance different from one:

Proposition 6.

In Example 4, converges in distribution to , where

From Proposition 6, the GW test introduces size distortions asymptotically if . This can easily be the case for skewed distributions. For example, let and . Then one can use simulations to see that for . Moreover, the asymptotic variance can be arbitrarily close to 1/2 as the rolling window size increases, leading to an undersized test.

Remark 1.

We can fix this issue by replacing the denominator in with the Newey and West, (1987) or another heteroskedasticity and autocorrelation consistent (HAC) estimator. This is in fact the procedure recommended for the classical test proposed by Diebold and Mariano, (1995). The drawback is that even if is i.i.d, has non-zero autocorrelation for at least lags. The performance of Newey-West or other HAC estimates might not be satisfactory when the serial dependence in the loss differentials does not decay fast enough.

Remark 2.

Another possibility is to use subsample t-tests similar to those proposed by Ibragimov and Müller, (2010, 2016). Thus, suppose we divide into blocks and let denote the sample mean of in the -th block, . Consider the test statistic

| (13) |

where . The limiting distribution of is the student -distribution with degrees of freedom.

Remark 3.

It is well known that the outcome of tests of equal unconditional predictive accuracy can be sensitive to the choice of the bandwidth used to estimate the long-run variance of the loss differential, see McCracken, (2020) and Coroneo and Iacone, (2020). Choosing the right bandwidth is often challenging, and McCracken, (2020) finds that very large bandwidths can be required for some data generating processes. An advantage of the above subsample -test is that it does not require a well-defined long-run variance. For example, the variance can change in a non-stationary manner, e.g. with structural breaks, as long as it is bounded.

Proposition 7.

Suppose that is stationary and . Assume that is bounded for some and is strong mixing of size . Then converges in distribution to the student -distribution with degrees of freedom.

The self-normalizing feature used to construct the test statistic in (13) means that we do not need to explicitly compute a HAC estimate, although we still need to choose .999HAC estimates require us to choose the number of lags to include which, in practice, can be quite complicated.

The key assumption needed for Proposition 7 is stationarity of the loss difference . Conversely, the proof does not require us to specify the functional form of the loss (MSE or other loss) and allows for nonlinear models with general estimators computed using a rolling window.

4.2 Monte Carlo simulation results

Consider the setting in Section 4.1. We set and . We report the size of three tests: the original GW test (GW), the Diebold-Mariano test using Newey-West standard errors (DM)101010The number of lags follows the “textbook NW” (Lazarus et al.,, 2018) choice and is set to . and a subsample t-test with (Sub). All Monte Carlo experiments are based on 10,000 random samples. To study the asymptotic distribution of the tests, we set the sample size to be a large number (), but we also consider finite-sample performance in samples with or 1,000 observations.

Table 1 reports the results. First, consider the performance of the tests in the very large sample (). The last three columns show that the original GW test tends to have an incorrect size. For , the original GW test is oversized for small () and undersized for large (), while both the DM and sub-sampling tests have approximately the right size. For , we observe serious size distortions for the original GW test which strongly over-rejects. Using Newey-West standard errors improves the accuracy of the GW test but clearly fails to effectively address the issue and this test remains heavily oversized. By far the most accurate test is the subsample t-test of Ibragimov and Müller, (2010, 2016) for which we only see a very small tendency to over-reject (e.g., 6% for a nominal size of 5%). Similar results are seen in the finite samples (columns 1-9) with the original GW and DM Newey-West test statistics tending to over-reject, while the sub-sampling approach is only modestly oversized.

| GW | DM | Sub | GW | DM | Sub | GW | DM | Sub | GW | DM | Sub | |

| 3 | 0.0915 | 0.0860 | 0.0465 | 0.0952 | 0.0792 | 0.0495 | 0.0895 | 0.0580 | 0.0468 | 0.0955 | 0.0530 | 0.0537 |

| 5 | 0.0742 | 0.0799 | 0.0487 | 0.0737 | 0.0723 | 0.0498 | 0.0725 | 0.0598 | 0.0483 | 0.0755 | 0.0537 | 0.0521 |

| 10 | 0.0545 | 0.0732 | 0.0524 | 0.0527 | 0.0616 | 0.0505 | 0.0543 | 0.0595 | 0.0517 | 0.0554 | 0.0541 | 0.0496 |

| 30 | 0.0430 | 0.0604 | 0.0543 | 0.0378 | 0.0500 | 0.0500 | 0.0381 | 0.0452 | 0.0502 | 0.0349 | 0.0435 | 0.0484 |

| 3 | 0.2593 | 0.2022 | 0.0585 | 0.2568 | 0.1748 | 0.0554 | 0.2489 | 0.1217 | 0.0543 | 0.2383 | 0.0725 | 0.0517 |

| 5 | 0.2282 | 0.1883 | 0.0564 | 0.2364 | 0.1772 | 0.0590 | 0.2368 | 0.1179 | 0.0461 | 0.2589 | 0.0734 | 0.0489 |

| 10 | 0.1680 | 0.1573 | 0.0510 | 0.1708 | 0.1451 | 0.0506 | 0.1928 | 0.1255 | 0.0508 | 0.2053 | 0.0762 | 0.0508 |

| 30 | 0.1029 | 0.1182 | 0.0505 | 0.1030 | 0.1059 | 0.0458 | 0.1037 | 0.0946 | 0.0482 | 0.1213 | 0.0854 | 0.0488 |

| 3 | 0.5324 | 0.4635 | 0.1246 | 0.5196 | 0.4268 | 0.1084 | 0.4942 | 0.3481 | 0.0966 | 0.4182 | 0.2293 | 0.0667 |

| 5 | 0.5028 | 0.4274 | 0.1091 | 0.5166 | 0.4118 | 0.0969 | 0.5301 | 0.3362 | 0.0896 | 0.5048 | 0.2195 | 0.0640 |

| 10 | 0.4241 | 0.3819 | 0.0875 | 0.4497 | 0.3754 | 0.0867 | 0.5052 | 0.3362 | 0.0788 | 0.5620 | 0.2218 | 0.0605 |

| 30 | 0.2698 | 0.2718 | 0.0673 | 0.2979 | 0.2828 | 0.0721 | 0.3523 | 0.2894 | 0.0656 | 0.4707 | 0.2357 | 0.0639 |

4.3 Expanding estimation window

Proposition 2 demonstrates the implausibility of the MDS condition with a rolling window estimation scheme. However, one might wonder whether testing equal predictive accuracy would be easier if one adopts an expanding estimation window. We next examine this point through a simple example:

Example 5.

Consider the following DGP:

where is i.i.d with and . Let denote the -algebra generated by .

Consider an expanding window estimation scheme under which the forecast for at time is , where with and for . We compare this forecast with the simple prediction . Clearly, both and have a vanishing bias for . Under squared error loss, one can easily verify that and . Since the bias vanishes with the sample size as the estimation window expands, this example is similar to the local-to-zero setting considered by Clark and McCracken, (2015).

| (14) |

where is a standard Brownian motion.

The second term in (14) has a distribution:

Conversely, the first term in (14) has a non-standard distribution and so the limiting distribution of is also non-standard.111111This is similar to the result for the MSE-t test in Theorem 3.2 of Clark and McCracken, (2005).

In Table 2, we simulate the limiting distribution in (14) and tabulate the 95% quantile of the absolute value limiting distribution for various values of . We also record the asymptotic null rejection probability if we simply choose 1.96 as the critical value (the standard normal limiting distribution stated in GW). We observe substantial size distortions if is small, even in the limit. Hence, in practice, if the expanding window starts early in the sample, we would falsely reject the null hypothesis too often.

| 95% quantile | Size if use 1.96 | |

|---|---|---|

| 0.05 | 3.993 | 0.247 |

| 0.10 | 3.769 | 0.226 |

| 0.15 | 3.573 | 0.215 |

| 0.20 | 3.389 | 0.203 |

| 0.25 | 3.250 | 0.196 |

| 0.30 | 3.103 | 0.188 |

| 0.35 | 2.981 | 0.181 |

| 0.40 | 2.880 | 0.175 |

| 0.45 | 2.781 | 0.166 |

| 0.50 | 2.697 | 0.158 |

| 0.55 | 2.598 | 0.147 |

| 0.60 | 2.534 | 0.135 |

| 0.65 | 2.445 | 0.122 |

| 0.70 | 2.379 | 0.111 |

| 0.75 | 2.307 | 0.099 |

| 0.80 | 2.238 | 0.089 |

| 0.85 | 2.190 | 0.081 |

| 0.90 | 2.108 | 0.070 |

| 0.95 | 2.057 | 0.062 |

| 0.99 | 1.992 | 0.054 |

5 Conclusion

Economic forecasts feature prominently in governments’ decisions on fiscal policy, central banks’ monetary policy, households’ consumption and investment decisions and companies’ hiring and capital expenditure choices, so it is important to be able to tell if one forecast can be expected to be more accurate than an alternative forecast. In an influential and innovative paper, Giacomini and White, (2006) develop methods for testing the null hypothesis that two forecasts have identical conditionally expected loss. Equivalently, their null is that the loss differential follows a martingale difference sequence. They use this null to construct a test statistic that does not require Newey-West HAC type adjustments for serial correlation in loss differentials.

The Giacomini-White approach has been used extensively in empirical work as it provides a way to formally compare the accuracy of economic forecasts in situations that are challenging for other tests such as the case with nested models. It turns out that the null that the loss differential is a martingale difference sequence is quite restrictive. We establish that a necessary and sufficient condition for the conditionally expected loss differential of two forecasts to follow an MDS process is that the conditional expectation of the outcome is a simple average of the forecasts. When the underlying forecasts contain parameter estimation errors, this means that the conditional mean of the outcome depends on past estimation errors. One can construct examples where this condition is valid but in many settings of interest to economic forecasters this condition seems hard to justify.

Appendix A Proofs

Proof of Proposition 1.

Notice that

Since and are both -measurable, it follows that

Since almost surely, if and only if , which implies . ∎

Proof of Proposition 2.

We proceed by contradiction. Suppose the MDS condition holds, i.e., with probability one. Then by Proposition 1, almost surely. By the law of iterated expectation, we have

Therefore, almost surely. This contradicts the assumption of . The desired result follows. ∎

Proof of Lemma 1.

We proceed by contradiction. Suppose that . Let and . Then by Proposition 1, we have that . On the other hand, since and is i.i.d with , we have that . Hence, we have almost surely. Therefore, almost surely.

However, note that

Let denote the event on which is positive definite. Since almost surely, it follows that on the event , . Thus, . By assumption, , which means that . However, this is impossible because by assumption has a density with respect to the Lebesgue measure on and thus . The proof is complete. ∎

Proof of Proposition 5.

We prove the two claims in two steps.

Step 1: show the result for

By , we have

By , we have that . Let . Clearly, is an MDS and . Hence,

and

Since is an MDS, we have

By Theorem 3.35 of White, (2001), is stationary and ergodic. By Theorem 3.34 therein, . By Corollary 5.26 therein, we have

In other words, we have . Again, by Theorems 3.34 and 3.35 of White, (2001), we have

Therefore,

| (15) |

On the other hand, by , we have that

Since , we have

| (16) |

Step 2: show the result for .

The result for follows by an analogous argument. We provide a brief proof and point out the difference. Again, define , where

and . Notice that besides a constant factor, the difference from Step 1 is that we now have rather than .

By essentially the same argument, we have

| (17) |

and

| (18) |

as well as

| (19) |

Then by (19), we have that

The proof is complete. ∎

Proof of Proposition 3.

To prove this result, we compute the mean squared error for the individual models. To this end, define and . For the small model, . Since and , we have

Simple computations yield

| (20) |

For the big model, . Since , we have . By simple computations, we obtain

| (21) |

The first result follows by setting and using (20) and (21).

We now show the second result. Let be the -algebra generated by and notice that

and

Therefore,

Since contains a column of , there is always a term containing that cannot be canceled in the above equation. Therefore, it is not possible that with probability one, . Hence, is not an MDS. ∎

Proof of Proposition 4.

We proceed in two steps in which we verify the result in the absence and presence of estimation errors.

Step 1: First, ignore estimation errors.

We proceed by contradiction. Suppose that almost surely. In this case, and . By Proposition 1, we have

However, from the DGP with , we have

It follows that almost surely. This contradicts the assumption, from which the result follows.

Step 2: Next, consider parameter estimation errors.

We proceed by contradiction. Suppose that almost surely. In this case, and , where and are OLS estimates using information in . By Proposition 1, we have

On the other hand, we have . This means that almost surely. This contradicts the assumption, from which the result follows. ∎

Proof of Proposition 6.

Let . Then and . Hence,

Since is fixed, is stationary and weakly dependent; in fact, and are independent for . We next compute the autocovariances, . Clearly, for , so we can focus on . Since is iid with mean zero and , we observe that

| (22) |

The rest of the proof proceeds in three steps.

Step 1: Compute for .

Define , and . These three quantities are well defined because . Notice that , and are mutually independent with mean zero and satisfy , and . Moreover, and . Therefore, we have

Notice that . Thus, we have

| (23) |

Since , we have

| (24) |

We observe that

| (25) |

Step 2: Compute for .

We notice that and are independent. This means that . Moreover, . Finally, . It follows by (22) that

| (27) |

Step 3: Compute for .

We observe that

By a similar argument as in the computation for , we can show that . It follows that

| (28) |

By the law of large numbers, converges in probability to . Therefore, since the test statistic would have an asymptotic variance equal to

The proof is complete. ∎

Proof of Proposition 7.

Let , where . For simplicity, assume that is an integer. By Theorem 5.20 of White, (2001) and the Cramer-Wold device, converges in distribution to , where . Define the function by

with . Then . The desired result follows by the continuous mapping theorem. ∎

Proof of Proposition 8.

Define . Then by the functional central limit theorem (e.g., Theorem 7.13 of White, (2001)), converges weakly to , where is a standard Brownian motion. In fact, this weak convergence can be strengthened to a strong approximation on a possible extended probability space, i.e., ; see e.g., Theorem 2.1.2 of Csörgo and Révész, (1981).

We notice that and . Hence,

| (29) |

Therefore,

| (30) |

Similarly,

Notice that

and

Finally, we observe that

The above four displays imply that

Therefore, the desired result follows by (30). ∎

References

- Clark and McCracken, (2001) Clark, T. E. and McCracken, M. W. (2001). Tests of equal forecast accuracy and encompassing for nested models. Journal of econometrics, 105(1):85–110.

- Clark and McCracken, (2005) Clark, T. E. and McCracken, M. W. (2005). Evaluating direct multistep forecasts. Econometric Reviews, 24(4):369–404.

- Clark and McCracken, (2015) Clark, T. E. and McCracken, M. W. (2015). Nested forecast model comparisons: a new approach to testing equal accuracy. Journal of Econometrics, 186(1):160–177.

- Coroneo and Iacone, (2020) Coroneo, L. and Iacone, F. (2020). Comparing predictive accuracy in small samples using fixed-smoothing asymptotics. Journal of Applied Econometrics, 35(4):391–409.

- Csörgo and Révész, (1981) Csörgo, M. and Révész, P. (1981). Strong approximations in probability and statistics. Academic Press.

- Diebold and Mariano, (1995) Diebold, F. X. and Mariano, R. S. (1995). Comparing predictive accuracy. Journal of Business & Economic Statistics, pages 253–263.

- Giacomini and White, (2006) Giacomini, R. and White, H. (2006). Tests of conditional predictive ability. Econometrica, 74(6):1545–1578.

- (8) Hansen, P. R. and Timmermann, A. (2015a). Comment on comparing predictive accuracy, twenty years later. Journal of Business and Economic Statistics, 33:17–21.

- (9) Hansen, P. R. and Timmermann, A. (2015b). Equivalence between out-of-sample forecast comparisons and wald statistics. Econometrica, 83(6):2485–2505.

- Ibragimov and Müller, (2010) Ibragimov, R. and Müller, U. K. (2010). t-statistic based correlation and heterogeneity robust inference. Journal of Business & Economic Statistics, 28(4):453–468.

- Ibragimov and Müller, (2016) Ibragimov, R. and Müller, U. K. (2016). Inference with few heterogeneous clusters. Review of Economics and Statistics, 98(1):83–96.

- Inoue and Kilian, (2005) Inoue, A. and Kilian, L. (2005). In-sample or out-of-sample tests of predictability: Which one should we use? Econometric Reviews, 23(4):371–402.

- Lazarus et al., (2018) Lazarus, E., Lewis, D. J., Stock, J. H., and Watson, M. W. (2018). Har inference: Recommendations for practice. Journal of Business & Economic Statistics, 36(4):541–559.

- McCracken, (2007) McCracken, M. W. (2007). Asymptotics for out of sample tests of granger causality. Journal of Econometrics, 140(2):719–752.

- McCracken, (2020) McCracken, M. W. (2020). Tests of conditional predictive ability: Existence, size, and power. FRB St. Louis Working Paper, (2020-050).

- Newey and West, (1987) Newey, W. K. and West, K. D. (1987). A simple, positive semi-definite, heteroskedasticity and autocorrelation-consistent covariance matrix. Econometrica, 55 (3):703–708.

- West, (1996) West, K. D. (1996). Asymptotic inference about predictive ability. Econometrica: Journal of the Econometric Society, pages 1067–1084.

- White, (2001) White, H. (2001). Asymptotic theory for econometricians. New York: Academic Press.