A cumulant approach for the first-passage-time problem of the Feller square-root process

Abstract

The paper focuses on an approximation of the first passage time probability density function of a Feller stochastic process by using cumulants and a Laguerre-Gamma polynomial approximation. The feasibility of the method relies on closed form formulae for cumulants and moments recovered from the Laplace transform of the probability density function and using the algebra of formal power series. To improve the approximation, sufficient conditions on cumulants are stated. The resulting procedure is made easier to implement by the symbolic calculus and a rational choice of the polynomial degree depending on skewness, kurtosis and hyperskewness. Some case-studies coming from neuronal and financial fields show the goodness of the approximation even for a low number of terms. Open problems are addressed at the end of the paper.

1 Introduction

One-dimensional diffusion processes play a key role in the description of fluctuating phenomena belonging to different fields of applications as physics, biology, neuroscience, finance and others (Karlin and Taylor, 1981; Øksendal, 1998). In particular, the class of stochastic processes with a linear drift and driven by a Wiener process is widely used for its mathematical tractability and flexibility. These models are described by a stochastic differential equation of the following type

| (1) |

where is a standard Wiener process, is the initial condition, and the volatility

are such that a strong solution of Eq.(1) exists (Arnold (2013) p.105).

The volatility determines the amplitude of the noise and, according to its dependence on , it characterizes families of stochastic processes which are solution of Eq. (1).

If

| (2) |

the solution of Eq. (1) is called Pearson diffusion process (Forman and Sørensen, 2008). The coefficients and are such that the square root is defined for all the values of the state space of with . A wide range of well-known processes belongs to this class ():

- Ornstein-Uhlenbeck process

-

and

- Inhomogeneous geometric Brownian motion

-

, and

- Jacobi diffusion

-

and

- Feller process (CIR model)

-

and

Throughout this paper we will focus on this last process for its variety of applications not only in a biological context (Ditlevsen and Lansky, 2006; Feller, 1951; Lansky, Sacerdote, and Tomassetti, 1995) but also in survival analysis, in the modeling of nitrous oxide emission from soil and in other applications such as physics and computer science (see Ditlevsen and Lansky (2006) and references therein). In the mathematical finance it is known under the name of Cox-Ingersoll-Ross model (CIR) (Cox, Ingersoll, and Ross, 1985).

While general properties of the Feller process are well known since long, less known are properties related to first-passage-time (FPT) events which are very significant phenomena in all of the above mentioned situations. In this paper we consider the dynamics of until it crosses a threshold for the first time, the so called (upcrossing) FPT, defined as

| (3) |

Many contributions in the literature (Giorno et al., 1986; Going-Jaeschke and Yor, 2003; Linetsky, 2004; Masoliver and Perelló, 2014) focus on computing the Laplace transform (LT) of the probability density function (PDF) of , namely

| (4) |

The reason why the literature is focused on the LT of , is that the PDF is usually not known analitically and neither can be obtained by direct inversion of Eq. (4). Nevertheless from we can compute the probability of crossing the threshold , , and the mean FPT, as follows:

| (5) |

Moments of of any orders can be computed using higher derivatives of when they exist. As it is well-known, the moments of allow nice interpretation of statistical properties of the PDF and of FPT events. A different strategy to get the moments of is using the transition PDF of the process Indeed if admits a stationary distribution independent of the Siegert formula (Siegert, 1951) allows us to compute the moments of as

| (6) |

Both the depicted strategies are impractical to compute the moments of for a Feller process. Despite the closed form formula of (see Section ), the computation of higher derivatives is awkward and some efforts have focused in evaluating just the mean and the variance of (Ditlevsen and Lansky, 2006; D’Onofrio, Lansky, and Pirozzi, 2018) or at most the third moment (Giorno et al., 1988). In terms of computational complexity, similar difficulties apply in computing moments of through Eq. (6), although the stationary distribution of is known to be a shifted gamma distribution (see Section 2). As the distribution of is often unavailable, simulations of the paths through Monte Carlo methods are still an efficient tool to get manageable estimations of useful to analyze especially asymptotic properties. One more strategy consists in writing the FPT distribution as a Sturm-Liouville eigenfunction expansion series, first given for the Feller process in Linetsky (2004), using the classical argument of Kent (1980) and Kent (1982). Although this strategy provides an expression for the FPT density, information on the moments of can be obtained only numerically and refers exclusively to diffusion processes without natural boundaries.

A discussion on FPT of the Feller process in the presence of entrance, exit and reflecting boundary at the origin is given in Martin, Behn, and Germano (2011), solving the Sturm-Liouville boundary problem in the case .

The goal of this paper is twofold: to give closed form formulae for the cumulants of of any order for the Feller process regardless of the nature of the boundaries and to give approximations of by using moments recovered from cumulants.

Recall that if has moment generating function for all in an open interval about then its cumulants are such that

| (7) |

for all in some (possibly smaller) open interval about

Cumulants have nice properties compared with moments such as the semi-invariance and the additivity (McCullagh, 1987). Further properties on cumulants are given in Section 3. Overdispersion and underdispersion as well as asymmetry and tailedness of the FPT PDF might be analized through the first four cumulants. Examples on how to employ the first four cumulants in the estimation of the parameters of a model fitted to data is given in (Antunes et al., 2020; Seneta, 2004).

The employment of cumulants in the FPT literature is not new (Ramos-Alarcón and Kontorovich, 2013). However, their application has been limited to few cases and not in the direction addressed in this paper. Here, the idea to use cumulants essentially relies on the form of for the Feller process. Indeed is the ratio of two power series whose algebra is simplified if we consider We take advantage of the formal power series algebra (Charalambides, 2002) to give first a closed form expression of and then to recover moments. In Section 4, we propose to use a Laguerre series to approximate the PDF taking into account the properties of To the best of our knowledge, this approach in evaluating the FPT PDF of the Feller process has not been investigate before in the literature. Such an approximation works if moments (or cumulants) of are known and gives better results when the series is of Laguerre-Fourier type. As the PDF is unknown, we give sufficient conditions on the cumulants of to guarantee the approximation with the Laguerre-Fourier series. We show how to take advantage of the formal power series algebra and of the symbolic calculus (Di Nardo, 2012) in implementing the proposed procedure. Some new results on the Kummer’s function are also given.

Then we apply our method to different case-studies inspired by neuronal and financial models. One of the advantages of the method is that few terms are sufficient to have a good description of and the complexity of the overall computation is strongly reduced. Statistical arguments motivate the choice of stopping the Laguerre series at the fifth term. The case-studies show that the resulting approximation is accurate also when the sufficient conditions are not completely fulfilled. A discussion section ends the paper, addressing future research and open problems.

2 The Feller process and the FPT problem

We consider model (1) such that the function depends on the process itself and on . The Feller process investigated here is given by

| (8) |

The state space of the process is the interval .

The endpoints and can or cannot be reached in a finite time depending on the underlying parameters. According to the Feller classification of boundaries (Karlin and Taylor, 1981), is an entrance boundary if it cannot be reached by in finite time, and there is no probability flow to the outside of the interval , that is, the process stays in with probability 1. In particular, set . Then is an entrance boundary if .

In the absence of a threshold, the Feller process admits a stationary distribution which is a shifted gamma distribution with the following shape, scale and location parameters

| (9) |

Let evolve in the presence of a threshold . Let be the FPT random variable of through defined in Eq. (3). Three distinct situations for the FPT can occur. Indeed, the process is said to be in the suprathreshold, subthreshold and threshold regimes if and , respectively, where the asymptotic mean of is

| (10) |

The Siegert equation (Masoliver and Perelló, 2014)

| (11) |

with initial conditions if and for any , provides the LT of the FPT PDF. Indeed the solution of Eq. (11) is

| (12) |

where is the confluent hypergeometric function of the first kind (or Kummer’s function) , and

| (13) |

is the generalized hypergeometric function, with the rising factorial and . For more details on Eqs. (9)-(12) see D’Onofrio, Lansky, and Pirozzi (2018). In particular, the mean of is (Giorno et al., 1988)

| (14) |

where is the gamma function.

3 FPT cumulants

Suppose a formal power series (Charalambides, 2002)

| (15) |

where denotes the ring of formal power series with coefficients in Then is well defined

| (16) |

and the coefficients are named formal cumulants of There are different formulae expressing formal cumulants in terms of , Di Nardo (2012). Here we use the logarithmic (partition) polynomials such that

| (17) |

where

| (18) |

and are the partial exponential Bell polynomials (Charalambides, 2002). Let us recall that, for a fixed positive integer and the -th partial exponential Bell polynomial in the variables is a homogeneous polynomial of degree given by

| (19) |

where the sum is taken over all sequences of non negative integers such that

| (20) |

The -th logarithmic polynomial (18) is a special case of the -th general partition polynomial

| (21) |

when for The first five general partition polynomials are given in Table 1.

If we set for then

| (22) |

are the inverse relations, with given in Eq. (19). The polynomial is the -th complete Bell (exponential) polynomial and is a special case of in Eq. (21) when for

The logarithmic and the complete Bell polynomials allow us to deal with moments and cumulants of . Indeed if is the Laplace transform of the PDF and the rhs of Eq. (15) is its Taylor expansion about then

| (23) |

and there exist cumulants of any order see for instance Abate and Whitt (1996). In particular, from Eq. (16) and Eq. (17), we have

| (24) |

Vice-versa, if cumulants are known, moments of might be computed by using the inverse relations (22)

| (25) |

or the well-known recursion formula (Di Nardo and Senato, 2006)

| (26) |

If is the FPT random variable of a Feller process modeled by Eq. (8), the following theorem gives the closed-form expression of the -th cumulant for any order

Theorem 1.

Remark 1.

Proof.

In Eq. (12), set and From Eq. (24) we get

| (31) |

where

| (32) |

To expand the rhs of Eq. (32) in formal power series in , observe that

| (33) |

where are the unsigned Stirling numbers of the first type. Replacing Eq. (33) in Eq. (32), after some algebra, we get

| (34) |

From Eqs. (16) and (17), we get

| (35) |

where is the -th logarithmic polynomial given in Eq. (18) and is given in Eq. (29). Moreover Eq. (27) follows taking into account Eq. (31) and by observing that

∎

Corollary 1.

The mean FPT and the variance of are respectively

| (36) |

where for

| (37) |

with the harmonic numbers.

Proof.

Remark 2.

Corollary 2.

If is the FPT cumulant sequence, then

| (39) |

where are the complete Bell polynomials given in Eq. (22) and

Proof.

3.1 Computing FPT cumulants

For the subsequent applications of Theorem 1, we add some remarks on the efficiency of the implementation of Eq. (27). The logarithmic partition polynomials with might be generated by using the recurrence relation (Charalambides, 2002)

| (43) |

About the computation of in Eq. (29), from Eq. (34), note that

| (44) |

Derivatives of the Kummer’s function with respect to the parameter have been computed in Ancarani and Gasaneo (2008). The special case is given in terms of generalized Kampé de Fériet-like hypergeometric functions. An algorithm for the computation of the -th derivative of the Kummer’s function is given in Abad and Sesma (2003). Here, we propose to use a standard implementation of the series in Eq. (29) involving the unsigned Stirling number of first type, as procedures implementing the well-known triangular recurrence relation (Charalambides, 2002)

| (45) |

are available in many classical technical computing systems as Mathematica or R.

From Eq. (44) it turns out that the usefulness of expression (29) for the functions is twofold. It also constitutes an alternative way to express the derivative in Eq. (44) and so it can simplify the form of the Kampé de Fériet function for particular values of the involved parameters. Moreover from Eq. (44) and the following expression (Abramowitz and Stegun, 1964)

| (46) |

we infer the following formula for the forward differences of order -th of the Kummer function:

| (47) |

4 The Laguerre-Gamma polynomial approximation

The Edgeworth expansion is widely used in the literature to approximate a PDF around the Gaussian PDF, using a linear combination of Hermite polynomials with coefficients depending on the cumulants of the target PDF. To approximate a non-Gaussian PDF, a different family of polynomials is necessary together with a different reference density (Asmussen, Goffard, and Laub, 2019). If the target PDF is unknown but expected to be close to some reference density then is used as a first approximation to and later the approximation is improved by using suitable correction terms depending on a set of orthonormal polynomials. The following theorems show how to approximate the FPT PDF of a Feller process by using as reference density the gamma PDF with scale parameter and shape parameter

| (48) |

Theorem 2.

Let where

| (49) |

and is the -th generalized Laguerre polynomial

| (50) |

For the series

| (51) |

converges if and

| (52) |

Proof.

Set and observe that in Eq. (51) the series might be rewritten as

| (53) |

where for

| (54) |

with the PDF of and as given in Eq. (48). A sufficient condition to have the convergence of the series (53) for at every point of continuity of is (Hille, 1926)

| (55) |

for every which is fulfilled when is the FPT random variable of a Feller process from Eq. (12). Therefore

| (56) |

and Eq. (52) follows from Eq. (56) after some algebra, replacing by and recalling that ∎

Eqs. (51) and (52) justify the approximation of with the polynomial of degree

| (57) |

for a suitable choice of that we discuss in the next section.

Remark 3.

The polynomial approximation (57) is particularly suited when the PDF of is unknown, but its moments are available, as happens for the FPT random variable of the Feller process thanks to Corollary 2. Indeed by observing that

some algebra allows us to rewrite in Eq. (57) as

| (58) |

with coefficients

| (59) |

depending on the moments of Note that might be expressed directly in terms of cumulants of by using Eq. (25).

Sufficient conditions for the convergence of the series

| (60) |

can be recovered by using the analogous on the Laguerre series (Hille, 1926). Indeed in such a case we have and

| (61) |

The next corollary gives a sufficient condition on to have the series representation (61).

Corollary 3.

The PDF has the series representation (61) if

| (62) |

Proof.

Condition (62) is equivalent to ask , equipped with the usual inner product and the measure having density As admits moment generating function and all its moments are finite, there exists a complete set of orthonormal polynomials in such that if we may expand in terms of these polynomials. Let us observe that is a family of orthonormal polynomials in since is a family of orthogonal polynomials with respect to the weight function Therefore the Laguerre series (60) with represents the Fourier-Laguerre expansion of from whose uniqueness Eq. (61) follows. ∎

As is unknown, it’s not easy to verify directly the condition (62). If

| (63) |

then expansion (61) holds, due to the Parseval identity. The accuracy of the approximation (57) depends upon the decay rate of as the -loss is for a given order of truncation A sufficient condition to have Eq. (62) is

| (64) |

So it is fundamental to have a good algorithm to evaluate the coefficients This issue will be analyzed in the next paragraph.

4.1 Computational issues

To simplify the implementation, the approximating polynomial has been computed by using Eq. (58). The first five generalized Laguerre polynomials are given in Table 2.

Many packages111See for example the package orthopolynom in R. return the first generalized Laguerre polynomials by using the following recursion formula (Charalambides, 2002)

| (65) |

with The same recursion (65) allows an efficient computation of the coefficients This result is proved in the following lemma where we use the symbolic calculus (Charalambides, 2002) formalized through the employment of a linear operator acting on a ring of polynomials, for details see Di Nardo (2012).

Proposition 1.

Let for Then

| (66) |

where is a linear operator transforming in that is and

Proof.

Note that the moments are calculated from cumulants using the recursive relation (26).

The question of how to select the parameters and in Eq. (58) results to be a crucial point. A general guideline to their selection consists in matching the first two moments of with the first two of From a statistical point of view this choice mimics the well-known method of moments. From a computational point of view, if the first two moments of and coincide, then for simplifying the computation of Eq. (58) (Asmussen, Goffard, and Laub (2019)). According to this rule, if

| (68) |

then in Eq. (58).

The choice of and in Eq. (68) deserves some deeper analysis. First note that the shape parameter is given by the mean of the scaled random variable

Instead, the rate parameter measures the inverse relative variance of The relative variance of a PDF is a normalized measure of its dispersion. Thus, the more spread out is the greater is the underdispersion of The next section gives some examples and applications of Eq. (58) stopped at The motivation of this choice stems from the statistical meaning of the coefficients As symbolic calculus shows that the coefficients are related to the -th moment without the normalizing constant which depends on the orthonormal property of Thus the third-order coefficient accounts for the skewness of while the fourth-order coefficient involves the weight of tails in causing dispersion, that is the kurtosis. The fifth-order coefficient involves the hyper-skewness of (Khademalomoom, Narayan, and Sharma, 2019). Hyper-skewness measures the asymmetric sensitivity of the kurtosis, that is the relative importance of tails versus the center in causing skewness. Note that the sixth moment in is the PDF hyper-kurtosis and measures both the peakedness and the tails compared with the normal distribution. As we are considering PDFs with support , the contribution of this coefficient is not statistically meaningful and not considered here.

Some suitable choices of the rate parameter might improve the approximation, as the following propositions show.

Proposition 2.

If then

Proof.

Thus in the following proposition we give a sufficient condition for the ratio to be in assuming

| (71) |

under the choice (68).

Proposition 3.

We have

if and with

5 Examples

As mentioned before, the Feller process plays a key role in a variety of applications. In this section we will investigate three examples coming from different areas of study.

5.1 Example 1

In the first example we consider dimensionless quantities to show the way the approximation is implemented and how it performs.

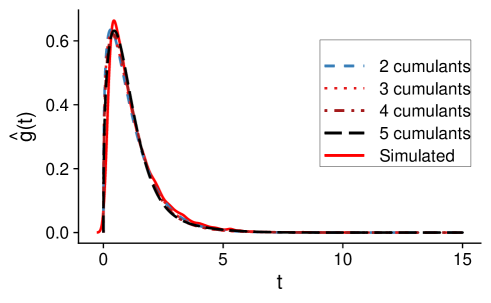

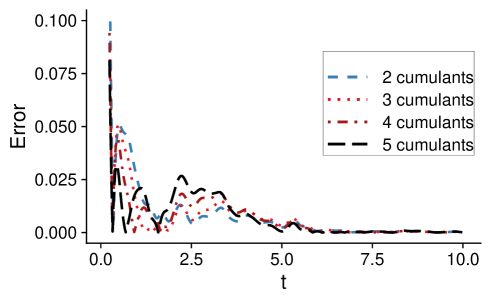

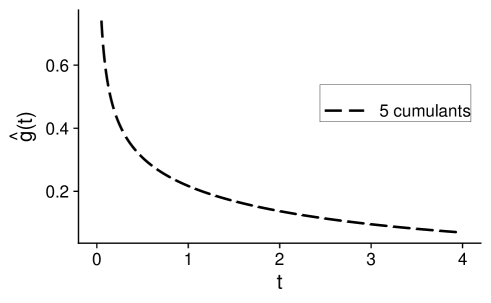

In Figure 1-top we show the PDF of the first passage time through for the Feller process solution of Eq. (8) for , , , and . The curves are obtained using just or cumulants in the approximation method, i.e. from Eq. (58) for . The approximations are compared to the FPT PDF obtained through simulation of first passage times of the process by discretization of Eq. (8) (see the Appendix). We observe that the agreement is satisfactory even for small , altough the expression of the cumulants of any order is available and in principle can be used to improve the approximation. The absolute error between the simulated PDF and the approximated one is shown in Figure 1-bottom. We observe that the error remains smaller than for . In the error is bigger, but the difference is due mainly to the error in the simulation rather than in the approximation. The reason is in the criteria for the bandwidth chosen in building the density from the histograms of the simulated first passage times.

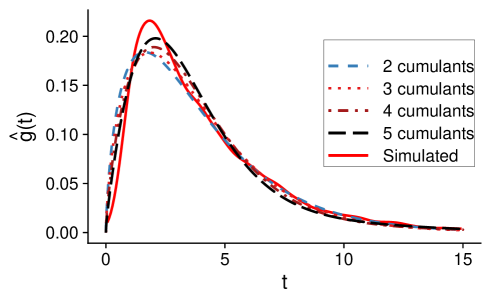

5.2 Example 2: Neuronal modeling

The Feller model was proved to fit experimental data of in vitro neurons under different conditions (Hopfner, 2007). For this reason in this subsection we focus on an application to neuronal modeling of Eq. (8). The solution process describes the evolution in time of the depolarization of the membrane potential of the neuron that is modelled as a leaky RC circuit with a drift characterizing the input stimuli. Eq. (8) describes the membrane depolarization until the occurence of a spike. In accordance with the model, the spikes are generated when the process crosses a voltage threshold for the first time, involving thus the FPT random variable. The process is reset to the starting point after the spike and the evolution starts anew. In this framework is the starting depolarization, determines the amplitude of the noise, is the inhibitory reversal potential, is the inverse of the characteristic time constant of the neuron that takes into account the spontaneous voltage decay towards the resting potential in the absence of inputs and characterizes the input the neuron under consideration receives. In the following, we consider the same parameters values used in Lansky, Sacerdote, and Tomassetti (1995), the resetting potential is equal to zero, i.e. mV, the inhibitory reversal potential is fixed to mV, the noise amplitude , mV/ms and the firing threshold to mV. The parameter of spontaneous decay is chosen ms (Figure 2).

In Ditlevsen and Lansky (2006) the noise amplitude is chosen (Figure 5.3). In this case the density is more skewed and the approximation fails to fit well the mode, altough the error remains of the order of (not shown).

The reason is in the properties of the gamma distribution that is our reference distribution: the mode is indeed not defined for , ( in the example).

Another property of the gamma distribution to take care of is the shape of the distribution for small . In fact in this case the gamma density stops to have the typical bell-shape, and might fail a good approximation of for small . This situation is presented in the following example.

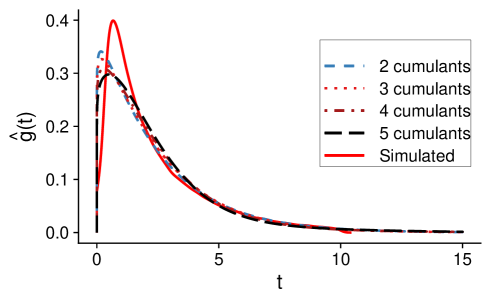

5.3 Example 3 : Financial mean-reverting models

In mathematical finance the Feller process goes under the name of CIR model and it is used to study the term structure of interest rates (Cox, Ingersoll, and Ross, 1985) or mean-reverting models for a credit spread (Linetsky, 2004). In the option pricing literature, the Feller process is used to describe the variance in models with stochastic volatility, where the most notable example is probably the Heston model (Heston, 1993; Rouah, 2013). In this example we consider a stochastic model for an instantaneous credit spread following Eq. (8) in with the long-run credit spread level of basis points , the initial spread level of bp (), the rate of mean-reversion , and the volatility parameter (parameters given in Linetsky (2004)). We are interested in the first passage time density of the long-run level , starting from . Comparing the plot in Figure 5.4 with the one given by Linetsky (2004) obtained with a different method of approximation, we observe a good asymptotic agreement. We stress that the term asymptotic can be measliding since the agreement is good already for relatively small . The PDF shape is not preserved for . The reason is that for ( in this case) the mode of the gamma distribution is not defined, and thus it cannot be matched with the one of , if it exists. However if we impose the teoretical information that , the behaviour of the PDF is reproduced. Note that using Eq. (58) we overcome the difficulties arisen from the simulation and the need to use terms in approximation expansion suggested by Linetsky.

6 Conclusions and open problems

We considered the well-known Feller stochastic process and the related FPT problem through a constant boundary. We provided a manageable closed form expression for the cumulants of of any order by which moments can be easily obtained, improving the current results available for the first three moments only. Note that the knowledge of higher moments gives qualitative information on the FPT PDF such as skewness, kurtosis, hyper-skewness and hyper-kurtosis.

We used cumulants to build a polynomial approximation of the FPT PDF whose expression in closed form is still missing in the literature. The method is carried out involving the gamma distribution as a first approximation to and then improving this approximation by adding suitable correction terms based on a set of Laguerre polynomials. The resulting Laguerre-Gamma polynomial has coefficients whose computation was lightened by using the well-known recurrence relation of the Laguerre polynomials and the symbolic calculus. This computation was further simplified choosing the parameters of the gamma distribution with the method of moments. We have shown that the proposed method allows us to obtain good approximation of even using a low degree ( in the analyzed case-studies). Moreover it overcomes the difficulties arisen from the simulation for time close to zero. Some care must be taken when the PDF is expected to have a mode differently from the gamma distribution selected from the choice of its parameters. This circumstance deserves to be further investigated either in the choice of the parameters and in the expected properties of Moreover, we give sufficient conditions to improve the approximation of the PDF with the Laguerre-Gamma polynomial; criteria that are fulfilled in most cases of application.

Future work includes the extension of this approach to other processes belonging to the class of Pearson’s diffusion, since the expression of the Laplace transform of the FPT PDF for these processes is often written as a ratio of two hypergeometric functions. More in general, when the Laplace transform of the FPT PDF is a ratio of functions admitting a power series representation, cumulants might be recovered by using the algebra of formal power series and different polynomial approximations might be tested. For example if the transition PDF of the process has a power series representation of the Laplace transform thus the proposed method might be investigated as is again a ratio of power series, that is

Appendix A The Milstein method

To estimate the FPT PDF we have implemented a classical Monte Carlo method and simulated the paths of using the stochastic differential equation (8). The algorithm we refer relies on the Milstein scheme of discretization that is often used when the term of the SDE depends on the process (see for instance Kloeden and Platen (2011)). Truncation of the Itô-Taylor expansion at the second order produces Milstein’s method:

| (72) | |||||

for for some . The Milstein scheme exhibits convergence of order in the strong sense and is a generalization of the Euler-Marayuma discretization scheme (the two methods coincide when does not depend on ). In case of Eq. (8), Eq. (72) gives

| (73) |

Acknowledgements

The second author was supported in part by Gruppo Nazionale per il Calcolo Scientifico (GNCS-INdAM).

References

- Abad and Sesma (2003) Abad, J. and Sesma, J., “Successive derivatives of Whittaker functions with respect to the first parameter,” Computer Physics Communications 156, 13 – 21 (2003).

- Abate and Whitt (1996) Abate, J. and Whitt, W., “An operational calculus for probability distributions via Laplace transforms,” Advances in Applied Probability 28, 75–113 (1996).

- Abramowitz and Stegun (1964) Abramowitz, M. and Stegun, I., Handbook of Mathematical Functions: With Formulas, Graphs, and Mathematical Tables (Dover Publications, 1964).

- Ancarani and Gasaneo (2008) Ancarani, L. U. and Gasaneo, G., “Derivatives of any order of the confluent hypergeometric function with respect to the parameter or ,” Journal of Mathematical Physics 49, 063508, 16 (2008).

- Antunes et al. (2020) Antunes, P., Ferreira, S. S., Ferreira, D., Nunes, C., and Mexia, J. T., “Estimation in additive models and ANOVA-like applications,” Journal of Applied Statistics 0, 1–10 (2020).

- Arnold (2013) Arnold, L., Stochastic Differential Equations: Theory and Applications (Dover Publications, 2013).

- Asmussen, Goffard, and Laub (2019) Asmussen, S., Goffard, P.-O., and Laub, P. J., “Orthonormal polynomial expansions and lognormal sum densities,” in Risk and Stochastics (2019) Chapter 6, pp. 127–150, https://www.worldscientific.com/doi/pdf/10.1142/9781786341952_0008 .

- Charalambides (2002) Charalambides, C. A., Enumerative Combinatorics (Chapman & Hall/CRC, Boca Raton, FL, 2002) pp. 609.

- Cox, Ingersoll, and Ross (1985) Cox, J. C., Ingersoll, J. E., and Ross, S. A., “A theory of the term structure of interest rates,” Econometrica 53, 385–407 (1985).

- Di Nardo (2012) Di Nardo, E., “Symbolic calculus in mathematical statistics: a review,” Seminaire Lotharingien de Combinatoire 67, Art. B67a, 72 (2012).

- Di Nardo and Senato (2006) Di Nardo, E. and Senato, D., “An umbral setting for cumulants and factorial moments,” European Journal of Combinatorics 27, 394 – 413 (2006).

- Ditlevsen and Lansky (2006) Ditlevsen, S. and Lansky, P., “Estimation of the input parameters in the Feller neuronal model,” Physical Review E 73, 061910 (2006).

- D’Onofrio, Lansky, and Pirozzi (2018) D’Onofrio, G., Lansky, P., and Pirozzi, E., “On two diffusion neuronal models with multiplicative noise: The mean first-passage time properties,” Chaos: An Interdisciplinary Journal of Nonlinear Science 28, 043103 (2018), https://doi.org/10.1063/1.5009574 .

- Feller (1951) Feller, W., “Two Singular Diffusion Problems,” Annals of Mathematics 54, 173–182 (1951).

- Forman and Sørensen (2008) Forman, J. and Sørensen, M., “The Pearson diffusions: A class of statistically tractable diffusion processes,” Scandinavian Journal of Statistics 35, 438–465 (2008).

- Giorno et al. (1988) Giorno, V., Lansky, P., Nobile, A., and Ricciardi, L., “Diffusion approximation and first-passage-time problem for a model neuron,” Biological Cybernetics 58, 387–404 (1988).

- Giorno et al. (1986) Giorno, V., Nobile, A. G., Ricciardi, L. M., and Sacerdote, L., “Some remarks on the Rayleigh process,” Journal of Applied Probability 23, 398–408 (1986).

- Going-Jaeschke and Yor (2003) Going-Jaeschke, A. and Yor, M., “A survey and some generalizations of Bessel processes,” Bernoulli 9, 313–349 (2003).

- Heston (1993) Heston, S.L., “A closed-form solution for options with stochastic volatility with applications to bond and currency options,” The Review of Financial Studies 6(2), 327–343 (1993) .

- Hille (1926) Hille, E., “On Laguerre’s series,” Proceedings of the National Academy of Sciences 12, 265–269 (1926), https://www.pnas.org/content/12/4/265.full.pdf .

- Hopfner (2007) Hopfner, R., “On a set of data for the membrane potential in a neuron,” Mathematical Biosciences 207, 275 – 301 (2007).

- Karlin and Taylor (1981) Karlin, S. and Taylor, H., A Second Course in Stochastic Processes, v. 2 (Academic Press, 1981).

- Kent (1980) Kent, J. T., “Eigenvalue expansions for diffusion hitting times,” Zeitschrift fur Wahrscheinlichkeitstheorie und Verwandte Gebiete 52, 309–319 (1980).

- Kent (1982) Kent, J. T., “The spectral decomposition of a diffusion hitting time,” Annals of Probability 10, 207–219 (1982).

- Khademalomoom, Narayan, and Sharma (2019) Khademalomoom, S., Narayan, P. K., and Sharma, S. S., “Higher moments and exchange rate behavior,” Financial Review 54, 201–229 (2019), https://onlinelibrary.wiley.com/doi/pdf/10.1111/fire.12171 .

- Kloeden and Platen (2011) Kloeden, P. and Platen, E., Numerical Solution of Stochastic Differential Equations, Stochastic Modelling and Applied Probability (Springer Berlin Heidelberg, 2011).

- Lansky, Sacerdote, and Tomassetti (1995) Lansky, P., Sacerdote, L., and Tomassetti, F., “On the comparison of Feller and Ornstein-Uhlenbeck models for neural activity,” Biological Cybernetics 73, 457–465 (1995).

- Linetsky (2004) Linetsky, V., “Computing hitting time densities for CIR and OU diffusions: Applications to mean-reverting models,” Journal of Computational Finance 7, 1–22 (2004).

- Martin, Behn, and Germano (2011) Martin, E., Behn, U., and Germano, G.,“First-passage and first-exit times of a Bessel-like stochastic process,” Physical Review E 83, 051115 (2011).

- Masoliver and Perelló (2014) Masoliver, J. and Perelló, J., “First-passage and escape problems in the Feller process,” Physical Review E 86(4-1), 041116 (2014).

- McCullagh (1987) McCullagh, P., Tensor Methods in Statistics, (Chapman & Hall, London, 1987) .

- Øksendal (1998) Øksendal, B., Stochastic Differential Equations: An Introduction with Applications (Springer, 1998).

- Ramos-Alarcón and Kontorovich (2013) Ramos-Alarcón, F. and Kontorovich, V., “First-passage time statistics of Markov gamma processes,” Journal of the Franklin Institute 350, 1686–1696 (2013).

- Rouah (2013) Rouah, F.D., The Heston Model and Its Extensions in Matlab and C, (John Wiley & Sons, 2013).

- Seneta (2004) Seneta, E., “Fitting the variance-gamma model to financial data,” Journal of Applied Probability 41, 177–187 (2004) .

- Siegert (1951) Siegert, A. J. F., “On the first passage time probability problem,” Physical Review 81, 617–623 (1951).