Expert-Supervised Reinforcement Learning for Offline Policy Learning and Evaluation

Abstract

Offline Reinforcement Learning (RL) is a promising approach for learning optimal policies in environments where direct exploration is expensive or unfeasible. However, the adoption of such policies in practice is often challenging, as they are hard to interpret within the application context, and lack measures of uncertainty for the learned policy value and its decisions. To overcome these issues, we propose an Expert-Supervised RL (ESRL) framework which uses uncertainty quantification for offline policy learning. In particular, we have three contributions: 1) the method can learn safe and optimal policies through hypothesis testing, 2) ESRL allows for different levels of risk averse implementations tailored to the application context, and finally, 3) we propose a way to interpret ESRL’s policy at every state through posterior distributions, and use this framework to compute off-policy value function posteriors. We provide theoretical guarantees for our estimators and regret bounds consistent with Posterior Sampling for RL (PSRL). Sample efficiency of ESRL is independent of the chosen risk aversion threshold and quality of the behavior policy.

1 Introduction

With increasing success in reinforcement learning (RL), there is broad interest in applying these methods to real-world settings. This has brought exciting progress in offline RL and off-policy policy evaluation (OPPE). These methods allow one to leverage observed data sets collected by expert exploration of environments where, due to costs or ethical reasons, direct exploration is not feasible. Sample-efficiency, reliability, and ease of interpretation are characteristics that offline RL methods must have in order to be used for real-world applications with high risks, where a tendency is exhibited towards sampling bias. In particular there is a need for policies that shed light into the decision-making at all states and actions, and account for the uncertainty inherent in the environment and in the data collection process. In healthcare data for example, there is a common bias that arises: drugs are mostly prescribed only to sick patients; and so naive methods can lead agents to consider them harmful. Actions need to be limited to policies which are similar to the expert behavior and sample size should be taken into account for decision-making [1, 2].

To address these deficits we propose an Expert-Supervised RL (ESRL) approach for offline learning based on Bayesian RL. This method yields safe and optimal policies as it learns when to adopt the expert’s behavior and when to pursue alternative actions. Risk aversion might vary across applications as errors may entail a greater cost to human life or health, leading to variation in tolerance for the target policy to deviate from expert behavior. ESRL can accommodate different risk aversion levels. We provide theoretical guarantees in the form of a regret bound for ESRL, independent of the risk aversion level. Finally, we propose a way to interpret ESRL’s policy at every state through posterior distributions, and use this framework to compute off-policy value function posteriors for any given policy.

While training a policy, ESRL considers the reliability of the observed data to assess whether there is substantial benefit and certainty in deviating from the behavior policy, an important task in a context of limited data. This is embedded in the method by learning a policy that chooses between the optimal action or the behavior policy based on statistical hypothesis testing. The posteriors are used to test the hypothesis that the seemingly optimal action is indeed better than the one from the behavior policy. Therefore, ESRL is robust to the quality of the behavior policy used to generate the data.

To understand the intuition for why hypothesis testing works for offline policy learning, we discuss an example. Consider a medical setting where we are interested in the best policy to treat a complex disease over time. We first assume there is a standardized treatment guideline that works well and that most physicians adopt it to treat their patients. The observed data will have very little exploration of the whole environment —in this case, meaning little use of alternative treatments. However, the state-action pairs observed will be near optimal. For any fixed state, those actions not recommended by the treatment guidelines will be rare in the data set and the posterior distributions will be dominated by the uninformative wide priors. The posteriors for the value associated with the optimal actions will incorporate more information from the data as they are commonly observed. Thus, testing for the null hypothesis that an alternative action is better than the treatment guideline will likely yield a failure to reject the null, and the agent will conclude the physician’s action is best. Unless the alternative is substantially better for a given state, the learned policy will not deviate from the expert’s behavior when there is a clear standard of care.

On the other hand, if there is no treatment guideline or consensus among physicians, different doctors will try different strategies and state-action pairs will be more uniformly observed in the data. At any fixed state, some relatively good actions may have narrower posterior distributions associated with their value. Testing for the null hypothesis that a fixed action is better than what the majority of physicians chose is more likely to reject the null and point towards an alternative action in this case, as variance will be smaller across the sampled actions. Deviation from the (noisy) behavior policy will occur more frequently. Therefore, whether there is a clear care guideline or not, the method will have learned a suitable policy. A central point in Bayesian RL is that the posterior provides not just the expected value for each action, but also higher moments. We leverage this to produce interpretable policies which can be understood and analyzed within the context of the application. We illustrate this with posterior distributions and credible intervals (CI). We further propose a way to produce posterior distributions for OPPE with consistent and unbiased estimates.

Handling Uncertainty.

To the best of our knowledge, there is no work that has incorporated hypothesis testing directly into the policy training process. However, accounting for the uncertainty in policy estimation is a successful idea which has been widely explored in other works. Methods range from confidence interval estimation using bootstrap, to model ensembles for guiding online exploration [3, 4, 5]. For example, a simple and effective way of incorporating uncertainty is through random ensembles (REM) [6]. These have shown promise on Atari games, significantly outperforming Deep networks (DQN) [7] and naive ensemble methods in the offline setting. We adopt the Bayesian framework, which has been proven successful in online RL [8, 9], as it provides a natural way to formalize uncertainty in finite samples. Bayesian model free methods such as temporal difference (TD) learning provide provably efficient ways to explore the dynamics of the MDP [10, 11, 12]. Gaussian Process TD can be also used to provide posterior distributions with mean value and CI for every state-action pair [13]. Although efficient for online exploration, TD methods require large data in high dimensional settings, which can be a challenge in complex offline applications such as healthcare. ESRL is model-based which makes it sample efficient [14]. Within model-based methods, the Bayesian framework allows for natural incorporation of uncertainty measures. Posterior sampling RL proposed by Strens efficiently explores the environment by using a single MDP sample per episode [15]. ESRL fits within this line of methods, which are theoretically guaranteed to be efficient in terms of finite time regret bounds [16, 17].

Hypothesis Testing for Offline RL

Naively applying model-based RL to offline, high dimensional tasks can degrade its performance, as the agent can be led to unexplored states where it fails to learn reliable policies. There are environments where simple approaches like behavior cloning (BC) on the offline data set is enough to ensure reliability. BC has actually been shown to perform quite well in offline benchmarks like RL Unplugged [18], D4RL [19] and Atari when the data is collected from a single noisy behavior policy [20]. The issue with these approaches is that there is to be gained in terms of optimality with respect to the expert, and there is no guarantee that the learned policies are safe in all states, a necessary condition when treating patients. A common strategy is to regularize the learned policy towards the behavior policy whether directly in the state space or in the action space [21, 22, 23, 18, 20]. However, there are cases where the data logging policy is a noisy representation of the expert behavior, and regularization will lead to sub-optimal actions. ESRL can detect these cases through hypothesis testing [24] to check whether improvement upon the behavior policy is feasible and, if so, incorporate new actions into the policy in accordance with the user’s risk tolerance. Additionally, as opposed to the regularization hyper-parameter that one must choose for methods like Batch Constrained deep Q-learning (BCQ) [18, 20], the risk-aversion parameter has a direct interpretation as the significance level that the user is comfortable with for the policy to deviate from the expert behavior. It allows the method to be tailored to different scientific and business applications where one might have different tolerance towards risk in search for higher rewards.

Off-Policy Policy Evaluation and Interpretation.

Many of the aforementioned methods can be easily adapted for offline learning and often importance sampling is used to address the distribution shift between the behavior and target policies [25]. However, importance sampling can yield high variance estimates in finite samples, especially in long episodes. Doubly robust estimation of the value function is proposed to address these issues. These methods will have low variance and consistent estimators if either the behavior policy or the model is correctly specified [26, 27]. Still, in finite samples or environments with high dimensional state-action spaces, these doubly robust estimators may still not be reliable, because only a few episodes end up contributing to the actual value estimate due to the product in the importance sampling weights [2]. Additionally, having point estimates without any measure of associated uncertainty can be dangerous, as it is hard to know whether the sample size is large enough for the estimate to be reliable. To this end, we use the ESRL framework to sample MDP models from the posterior and evaluate the policy value. Our estimates are unbiased and consistent, and are equipped with uncertainty measures.

2 Problem Set-up

We are interested in learning policies that can be used in real-world applications. To develop the framework we will use the clinical example discussed in Section 1. Consider a finite horizon MDP defined by the following tuple: , where is the state-space, is the action space, is the model over all rewards and state transition probabilities with prior is the reward distribution for fixed state-action pair under model , with mean . is the probability distribution function for transitioning to state from state-action pair under model , is the fixed episode length, and is the initial state distribution. The true MDP model has distribution .

The behavior policy function is a noisy version of a deterministic policy. Going back to the clinical example there is generally a consensus of what the correct treatment is for a disease, but the data will be generated by different physicians who might adhere to the consensus to varying degrees. Thus, we model the standard of care as a deterministic policy function . The behavior policy is with probability (w.p.) , and sampled uniformly at random from w.p. . For a fixed , generates the observed data which consists of episodes (i.e. patient treatment histories), where . Note that may generally yield high rewards, however it is not necessarily optimal and can be improved upon.

We’ll denote a policy function by . The associated value function for , model is and the action-value function is At any fixed , arg max, note that we allow in the function to differ from . This distinction will be useful as can be , (or the ESRL policy defined in Section 3). Finally, is the probability of given (), under the behavior policy.

3 Expert-Supervised Reinforcement Learning

We are interested in finding a policy which improves upon . Directly regularizing the target policy to the behavior might restrict the agent from finding optimal actions, especially when has a high random component , or is not close to optimal. Thus we want to know when to use versus . This motivates the use of posterior distributions to quantify how well each state has been explored in and how close is to . At every state and time in the episode we can sample MDP models from . These samples are used to compare the quality of the behavior and target policy actions. We consider both the expected values of each action versus , and their second moments for any fixed . In particular, posterior distributions of are used to test if the value for is significantly better than . This makes the learning process robust to the quality of the behavior policy. Next we formalize these arguments by a sampling scheme, define the ESRL policy, and state its theoretical properties.

Sampling functions.

The distribution over the MDP model implicitly defines a posterior distribution for any function: . As the true MDP model is stochastic, we want to approximate the conditional mean value: We do this by sampling MDP models , compute , and use .

Lemma 3.1.

is consistent and unbiased for

Lemma 3.1 establishes desirable properties for our function estimation. Choosing yields an immediate result: every from model is unbiased.

The stochasticity of and suggests the mean values for and are not enough to make a decision for whether it is beneficial to deviate from . Next we discuss how to directly incorporate this uncertainty assessment into the policy training through Bayesian hypothesis testing.

ESRL Policy Learning Through Hypothesis Testing.

For a fixed -level, denote the ESRL policy by , we next describe the steps to learn this policy. By iterating backwards as in dynamic programming, assume we know , and we have . Intuitively, at any we want to assess whether there is enough information in to support choosing the seemingly best action over . Denote arg max as the best action if we follow the ESRL policy onward, we formalize this with the following hypothesis:

| (1) |

Note that in (1), both functions assume the agent proceeds with ESRL policy onward. If we can reject , then it is safe to follow , if we fail to reject the null, it does not necessarily mean the behavior policy is better, but there is not enough information in the data to support following . To construct a safe ESRL policy we simply evaluate by computing the null probability , if this is below a pre-specified risk-aversion level then we can safely choose . In other words if the learned policy does not yield a significantly better value estimate, then we fail to reject the null and proceed to use the behavior policy’s action. The ESRL policy at is then

To compute , we start by sampling MDP models from the posterior distribution, computing and splitting the samples into two disjoint sets . We use to draw the policy based on majority voting. Then we use to assess the null hypothesis in (1), with estimator We next discuss convergence of the null probability estimator, and how to choose .

Lemma 3.2.

Let be the null probability under true MDP with policy ,

Lemma 3.2 guarantees that we can construct a consistent policy by sampling from the MDP posterior. There are two factors that come into play in (1): the difference in mean values, and the second moments. If is much higher than , but there are very few samples in for , the wide posterior will translate into a high leading ESRL to adopt . To choose there needs to be both a substantial benefit for this new action and a high certainty of such gain. How averse the user is to deviating from is controlled by parameter . A small risk averse will allow to deviate from only with high certainty. When , Algorithm 1 boils down to an offline version of PSRL after episodes, which uses majority voting for a robust policy. Algorithm 1 collects these ideas in order to learn an ESRL policy . Disjoint sets , ensure independence and keep theoretical guarantees under the Assumption 3.3.

Assumption 3.3.

Let be defined as in (1) for the true . The chosen risk-averse parameter satisfies .

As is set by the user, Assumption 3.3 is easily satisfied as long as is chosen carefully. Let be the value under the true MDP and let be an ESRL policy which uses the null hypotheses in (1) defined under . Then, for episode we can define the regret for from Algorithm 1 as , and the expected regret after episodes as .

Theorem 3.4 (Regret Bound for ESRL).

Theorem 3.4 shows ESRL is sample efficient, flexible to risk aversion level , and robust to the quality of behavior policy . As the regret bound is true for any level of risk aversion , Algorithm 1 universally converges to the oracle. This makes ESRL flexible for a wide range of applications. It also shows that ESRL is suitable to a large class of models, as the regret bound does not impose a specific form on . Regarding access to for sampling MDPs in real-world problems, as data increases, dependency of results on the prior decreases, so we can use any working model to approximate the MDP. Several models are computationally simple to sample from, and can be used for learning. For example, we use the Dirichlet/multinomial, and normal-gamma/normal conjugates for and respectively, which work well for all simulation and real data settings explored in Section 5. In fact, if a Dirichlet prior over the transitions is assumed, the regret bound in Theorem 3.4 can be improved. Chosen priors should be flexible enough to capture the dynamics and easy to sample from efficiently. Next we consider how to discern whether ESRL, or any other fixed policy, is an improvement on the behavior policy.

4 Off-Policy Policy Evaluation and Uncertainty Estimation

We now illustrate how the ESRL framework can be used to construct efficient point estimates of the value function, and their posterior distributions. Hypothesis testing can also be used to assess whether the difference in value of two policies is statistically significant (i.e. vs. ).

To compute the estimated value of a given policy , we sample models from the posterior and navigate using . This yields samples . We estimate with . Note that we average over the initial states as well, as we are interested to know the marginal value of the policy. A conditional value of the policy function can also be computed simply by starting all samples at a fixed state .

Theorem 4.1.

Let be a pre-specified policy,

Theorem 4.1 ensures that we are indeed estimating the quantity of interest. It establishes that is consistent and unbiased for . As MDP is stochastic, point estimates without measures of uncertainty are not sufficient to evaluate the quality of a policy. For example in an application such as healthcare, there might be policies for which the second best action (treatment) is not significantly different in terms of value, but has less associated secondary risks. Including a secondary risk directly into the method might force us to make strong modeling assumptions. Therefore, testing whether such policies yield a statistically significant difference in value is important. With this information, one can devise a policy that always chooses the safest action (e.g. in clinical terms) and if this yields an equivalent value to the optimal policy, then it is preferable.

Policy-level hypothesis testing.

Define the value function null hypothesis for two fixed policies as the event in which policy has a higher expected value than conditional on : . The probability of the null under the true model is

We use samples , to estimate the probability of the null with Consistency of this estimator is shown in the Appendix C.2.

5 Experiments and Application

We perform several analyses to assess ESRL policy learning, sensitivity to the risk aversion parameter , value function estimation, and finally illustrate how we can interpret the posteriors within the context of the application. The code for implementing ESRL with detailed comments is publicly available111https://github.com/asonabend/ESRL. We use the Riverswim environment [28], and a Sepsis data set built from MIMIC-III data [29]. We compare ESRL to several methods: a) a naive baseline made from an ensemble of DQN models (DQNE), where we simply use the mean for selecting actions, this benchmark is meant to shed light into the empirical benefit of the hypothesis testing in ESRL. b) We argue ESRL can deviate from the behavior policy when allowed by the hypothesis testing, for further investigating the benefit of hypothesis testing, we implement behavior cloning (BC). c) We explore Batch Constrained deep Q-learning (BCQ) which uses regularization towards the behavior policy for offline RL [18, 20, 30]. d) Finally, we also implement a strong benchmark which leverages ensembles and uncertainty estimation in the context of offline RL using random ensembles (REM) [6]. For Riverswim we use 2-128 unit layers, for Sepsis we use 128, 256 unit layers respectively [31]. For ESRL, we use conjugate Dirichlet/multinomial, and normal-gamma/normal for the prior and likelihood of the transition and reward functions respectively.

5.1 Riverswim

The Riverswim environment [28] requires deep exploration for achieving high rewards. There are 6 states and two actions: swim right or left. Only swimming left is always successful. There are only two ways to obtain rewards: swimming left while in the far left state will yield a small reward (5/1000) w.p. 1, swimming right in the far right state will yield a reward of 1 w.p. 0.6. The episode lasts 20 time points. We train policy using PSRL [16] for 10,000 episodes, we then generate data set with , varying both size and noise . The offline trained policies are then tested on the environment for 10,000 episodes. This process is repeated 50 times.

Policy Learning.

We first assess ESRL on Riverswim. The training set sample size is kept low to make it hard to completely learn the dynamics of the environment. We train an offline policy using ESRL with different risk aversion parameters . Figure 1 (a) shows mean reward for episodes while varying . ESRL proves to be robust to the behavior policy quality. This is expected as when is low the environment is not fully explored. This yields high variance in the posteriors, which leads ESRL to reject the null more often and favor the behavior policy. For low quality data generating policies there is greater exploration of the environment, which yields narrower posterior distributions for the function posteriors, leading ESRL to reject the null when it is indeed beneficial to do so. When behavior policy is almost deterministic, the smaller risk aversion parameter seems to yield good results as ESRL almost always imitates the behavior policy. BC does well as it seems to estimate the expert behavior well enough regardless of the noise level. Overall -learning methods lack enough data to learn a good policy. Figure 1 (b) compares methods on an almost constant behavior policy (), so there is little exploration in . ESRL is robust as wide posteriors keep it from deviating from . Methods other than BC generally fail likely to lack of exploration in . However note that in real world data is not necessarily optimal, in which case BC will likely not perform very well relative to ESRL or others if there is a high-noise expert policy, which yields a well explored MDP, this is the case in the Sepsis results shown in Figure 4 (c). Finally it’s worth noting that REM does better than DQNE in Riverswim but not on Sepsis, we believe this is because the DQN neural networks are smaller, REM outperforms DQNE in a more complex and higher variance setting with more training data such as the Sepsis setting in Section 5.2.

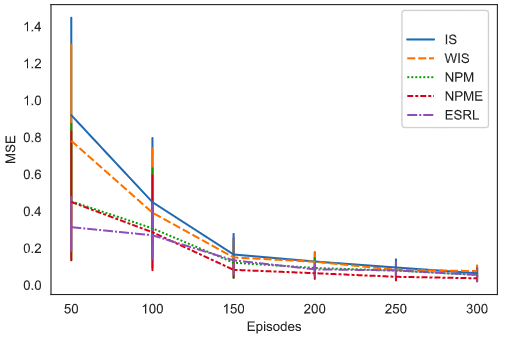

Figure 2 shows Mean Squared Error (MSE) and 95% confidence bands for value estimation of an ESRL policy using while varying . We compare it with sample-based estimates: step importance sampling (IS), and step weighted IS (WIS), and model based estimates which use a full non parametric model (NPM), and an NPM ensemble (NPME). The non parametric models compute the rewards and transition probability tables based on observed counts. The policy is evaluated by using the tables as an MDP model where states are drawn using the estimated transition probability matrix. NPM uses 1000 episodes to evaluate a policy, NPME is an average over 100 NPM estimates. In small data sets ESRL performs substantially better as it uses the model posteriors to overcome rarely visited states in . Eventually the priors (which are miss-specified for some state-action pairs) loose importance and ESRL converges to the non-parametric estimates. Sample based estimates are consistently less efficient but converge to the true policy with enough data.

Hypothesis testing and interpretability with function posterior distributions.

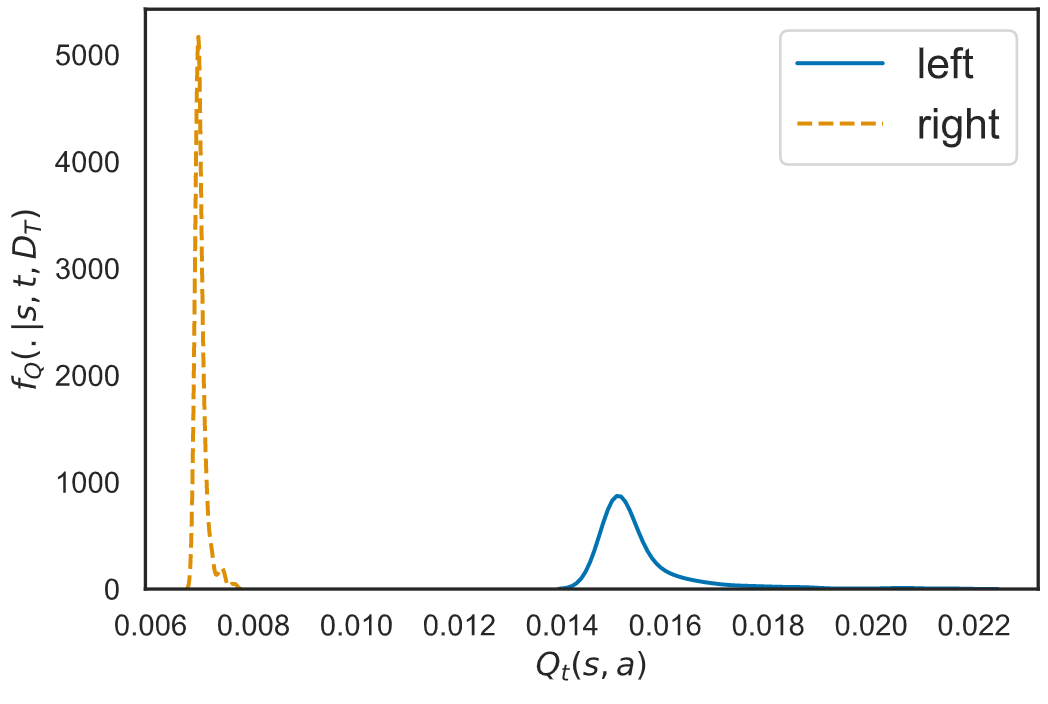

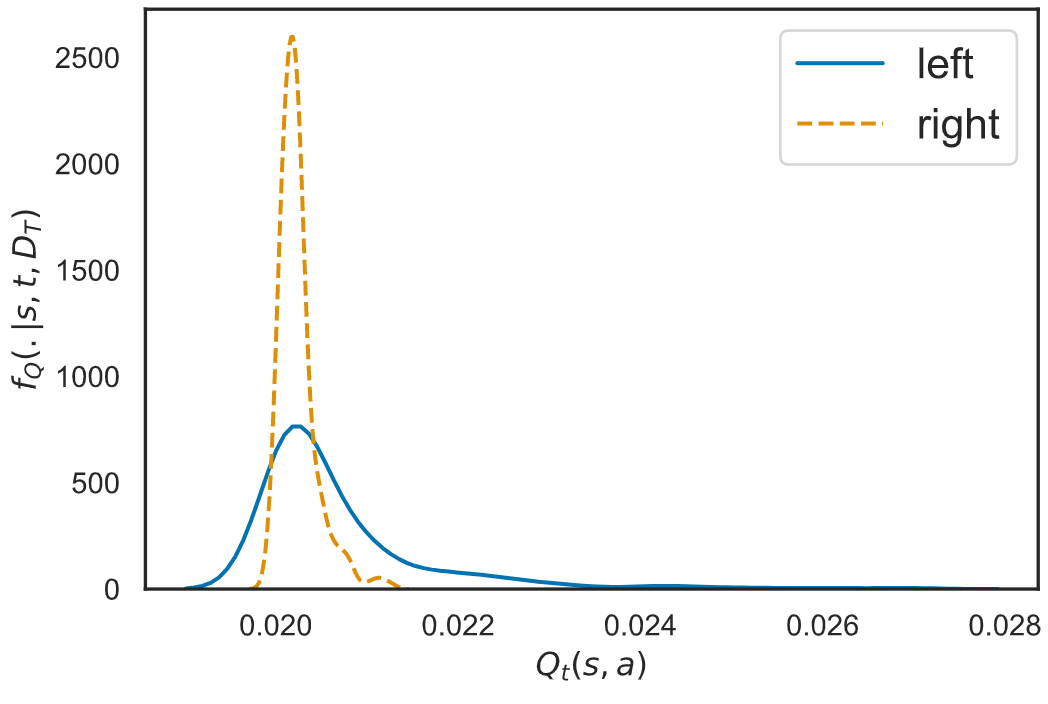

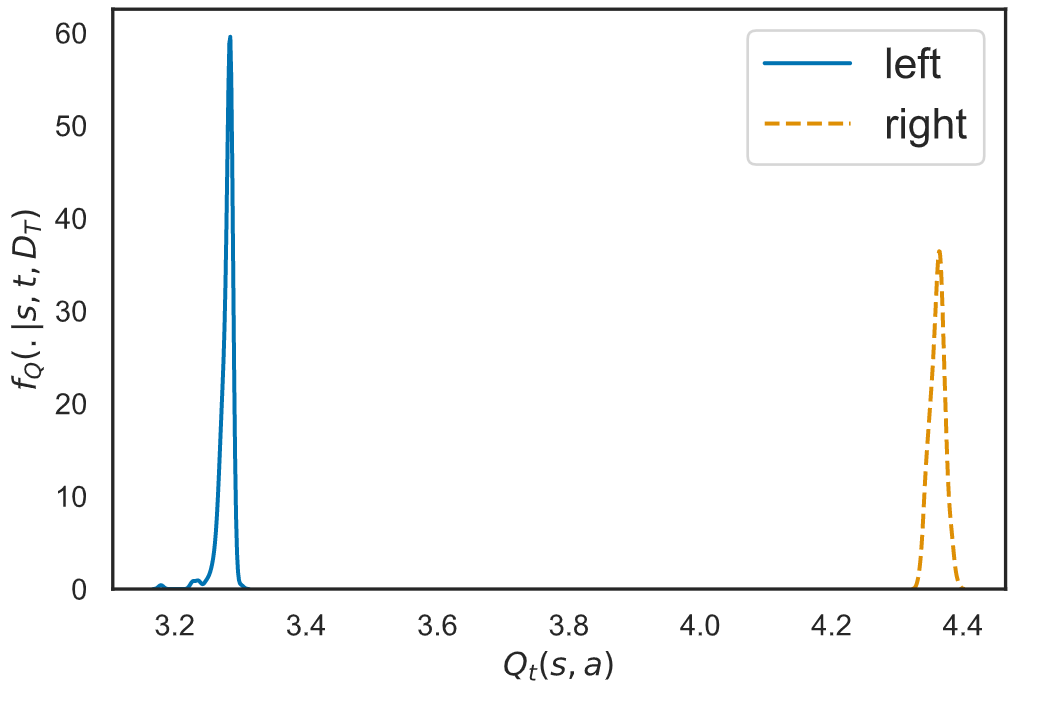

We illustrate interpretability of the ESRL method in Riverswim as it is a simple, intuitive setting. Figure 3 shows 3 function posterior distributions , each for a fixed state-time pair . Display (a) shows functions for the far left state and an advanced time point . There is high certainty (no overlap in posteriors) that swimming left will yield a higher reward, as left is successful w.p. 1. has a wider posterior as this is not common in . Display (b) is the most interesting, it sheds light into the utility of uncertainty measures. A naive RL method that only considers mean values, would choose the optimal action according to : swimming left. However, there is high uncertainty associated with such a choice. In fact, we know that the optimal strategy in Riverswim is , hypothesis testing will fail to reject the null and use the behavior action which will lead to a higher expected reward. Display (c) shows posteriors for the state furthest to the right, at . Choosing right will be successful with high certainty: narrow posterior. Swimming left will still yield a relatively high reward as in the next time point the agent will proceed with the optimal policy (choosing right). As there is no overlap in (a) and (c), the best choice is clear as would be reflected with a hypothesis test.

.

.

for , ESRL, BC, BCQ, DQN,

DQNE, REM.

5.2 Sepsis.

We further test ESRL on a Sepsis data set built from MIMIC-III [29]. Sepsis is a state of infection where the immune system gets overwhelmed and can cause tissue damage, organ failure, and death. Deciding treatments and medication dosage is a dynamic and highly challenging task for the clinicians. We consider an action space representing dosage of intravenous fluids for hypovolemia (IV fluids) and vasopressors to counteract vasodilation. The action space is size 25: a matrix over discretized dose of vasopressors and IV fluids. The state space is composed of 1,000 clusters estimated using K-means on a 46-feature space which contains measures of the patient’s physiological state. We used negative SOFA score as a reward [31], we transform it to be between 0 and 1. The data set used has 12,991 episodes of 10 time steps- measurements every 4-hour interval. We used 80% of episodes for training and 20% for testing.

Figure 4 (a) & (b) show posterior distributions for two different pairs in the Sepsis data set hand-picked to illustrate interpretability. For simplicity we restrict to show the best action: , physician’s action , and four other low dose actions . Display (a) shows posterior distributions over a state rarely observed in , hence the functions have relatively high standard errors. The expected cumulative inverse SOFA value for this state seems to be relatively stable no matter what action is taken. The posteriors for and are practically overlapping so there’s no reason to deviate from , this is encoded into through hypothesis testing. Interpertability is useful in these cases, as a physician might see there is no difference in actions: all will yield similar SOFA scores. Therefore, an action can be chosen to lower risk of side effects. Display (b) on the other hand shows a common state in : the low standard errors allow the policy to deviate from at any level. Within this state, actions and are usually selected so the posteriors for their functions are narrow, as opposed to those for . These actions are not prevalent in as they seem to be sub-optimal, so they are less often chosen by doctors and seen in .

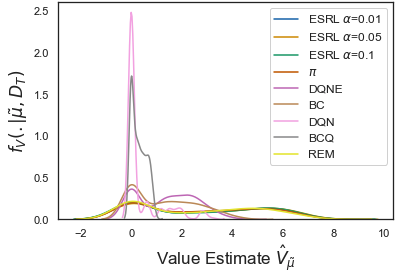

Figure 4 (c) shows the posterior distribution of the Sepsis value function for different policies. There seems to be a bi-modal distribution: it is easier to control the SOFA scores for patients in the set of states shown in the right mode of the distribution. Physicians know how to do this well as shown by the posterior value function for ; and ESRL picks up on this. The other clusters of states in the left mode seem to be harder to control. We can appreciate how deviating from the physician’s policy is strikingly damaging to the expected value on the test set. DQN and BCQ, DQNE and BC generalize better but under preform relative to ESRL and REM. The is probably not enough to generalize to the test set due to the high dimensional state and action spaces. ESRL through hypothesis testing captures this and hardly deviates from the behavior policy. Thus, it is clear that we cannot do better than given the information in the data, but the posterior suggest the need to learn safe policies as we can do substantially worse with methods that don’t account for uncertainty and safety.

6 Conclusion

We propose an Expert-Supervised RL (ESRL) approach for offline learning based on Bayesian RL. This framework can learn safe policies from observed data sets. It accounts for uncertainty in the MDP and data logging process to assess when it is safe and beneficial to deviate from the behavior policy. ESRL allows for different levels of risk aversion, which are chosen within the application context. We show a Bayesian regret bound that is independent of the risk aversion level tailored to the environment and noise level in the data set. The ESRL framework can be used to obtain interpretable posterior distributions for the functions and for OPPE. These posteriors are flexible to account for any possible policy function and are amenable to interpretation within the context of the application. An important limitation of ESRL is that it cannot readily handle continuous state spaces which are common in real world applications. Another extension we are interested in is in exploring the comparison of credible intervals as opposed to the null probability estimates. We believe ESRL is a step towards bridging the gap between RL research and real-world applications.

Broader Impact

We believe ESRL is a tool that can help bring RL closer to real-world applications. In particular this will be useful in the clinical setting to find optimal dynamic treatment regimes for complex diseases, or at least assist in treatment decision making. This is because ESRL’s framework lends itself to be questioned by users (physicians) and sheds light into potential biases introduced by the data sampling mechanism used to generate the observed data set. Additionally, using hypothesis testing and accommodating different levels of risk aversion makes the method sensible to offline settings and different real-world applications. It is important when using ESRL and any RL method, to question the validity of the policy’s decisions, the quality of the data, and the method that was used to derive these.

Acknowledgments and Disclosure of Funding

We thank Eric Dunipace for great discussions on Bayesian hypothesis testing and the reviewers for thoughtful feedback, especially regarding state-of-the-art benchmark methods. Funding in support of this work is in part provided by Boehringer Ingelheim Pharmaceuticals. Leo A. Celi is funded by the National Institute of Health through NIBIB R01 EB017205.

References

- [1] Omer Gottesman, Fredrik Johansson, Matthieu Komorowski, Aldo Faisal, David Sontag, Finale Doshi-Velez, and Leo Anthony Celi. Guidelines for reinforcement learning in healthcare. Nature medicine, 25(1):16, 2019.

- [2] Omer Gottesman, Fredrik D. Johansson, Joshua Meier, Jack Dent, Donghun Lee, Srivatsan Srinivasan, Linying Zhang, Yi Ding, David Wihl, Xuefeng Peng, Jiayu Yao, Isaac Lage, Christopher Mosch, Li-Wei H. Lehman, Matthieu Komorowski, Aldo Faisal, Leo Anthony Celi, David A. Sontag, and Finale Doshi-Velez. Evaluating reinforcement learning algorithms in observational health settings. CoRR, abs/1805.12298, 2018.

- [3] Leslie Pack Kaelbling. Learning in Embedded Systems. A Bradford Book Ser. 1993.

- [4] Martha White and Adam White. Interval estimation for reinforcement-learning algorithms in continuous-state domains. In J. D. Lafferty, C. K. I. Williams, J. Shawe-Taylor, R. S. Zemel, and A. Culotta, editors, Advances in Neural Information Processing Systems 23, pages 2433–2441. Curran Associates, Inc., 2010.

- [5] Thanard Kurutach, Ignasi Clavera, Yan Duan, Aviv Tamar, and Pieter Abbeel. Model-ensemble trust-region policy optimization. 2018.

- [6] Rishabh Agarwal, Dale Schuurmans, and Mohammad Norouzi. An optimistic perspective on offline reinforcement learning, 2019.

- [7] Volodymyr Mnih, Koray Kavukcuoglu, David Silver, Andrei A. Rusu, Joel Veness, Marc G. Bellemare, Alex Graves, Martin Riedmiller, Andreas K. Fidjeland, Georg Ostrovski, Stig Petersen, Charles Beattie, Amir Sadik, Ioannis Antonoglou, Helen King, Dharshan Kumaran, Daan Wierstra, Shane Legg, and Demis Hassabis. Human-level control through deep reinforcement learning. Nature, 518(7540):529, 2015.

- [8] Mohammad Ghavamzadeh, Shie Mannor, Joelle Pineau, and Aviv Tamar. Bayesian reinforcement learning: A survey. Foundations and Trends® in Machine Learning, 8(5-6):359–483, 2015.

- [9] Brendan O’Donoghue, Ian Osband, Rémi Munos, and Volodymyr Mnih. The uncertainty bellman equation and exploration. CoRR, abs/1709.05380, 2017.

- [10] Richard Dearden, Nir Friedman, and Stuart J. Russell. Bayesian q-learning. In AAAI/IAAI, 1998.

- [11] John Asmuth, Lihong Li, Michael L. Littman, Ali Nouri, and David Wingate. A bayesian sampling approach to exploration in reinforcement learning. 2012.

- [12] Alberto Maria Metelli, Amarildo Likmeta, and Marcello Restelli. Propagating uncertainty in reinforcement learning via wasserstein barycenters. In H. Wallach, H. Larochelle, A. Beygelzimer, Falche-Buc, E. Fox, and R. Garnett, editors, Advances in Neural Information Processing Systems 32, pages 4333–4345. Curran Associates, Inc., 2019.

- [13] Yaakov Engel, Shie Mannor, and Ron Meir. Reinforcement learning with gaussian processes. In Proceedings of the 22nd international conference on machine learning, volume 119 of ICML ’05, pages 201–208. ACM, 2005.

- [14] Marc Deisenroth and Carl Rasmussen. Pilco: A model-based and data-efficient approach to policy search. pages 465–472, 01 2011.

- [15] Malcolm Strens. A bayesian framework for reinforcement learning. In In Proceedings of the Seventeenth International Conference on Machine Learning, pages 943–950. ICML, 2000.

- [16] Ian Osband, Daniel Russo, and Benjamin Van Roy. (more) efficient reinforcement learning via posterior sampling. 2013.

- [17] Ian Osband and Benjamin Van Roy. Why is posterior sampling better than optimism for reinforcement learning? 2016.

- [18] Caglar Gulcehre, Ziyu Wang, Alexander Novikov, Tom Le Paine, Sergio Gomez Colmenarejo, Konrad Zolna, Rishabh Agarwal, Josh Merel, Daniel Mankowitz, Cosmin Paduraru, Gabriel Dulac-Arnold, Jerry Li, Mohammad Norouzi, Matt Hoffman, Ofir Nachum, George Tucker, Nicolas Heess, and Nando de Freitas. Rl unplugged: Benchmarks for offline reinforcement learning, 2020.

- [19] Justin Fu, Aviral Kumar, Ofir Nachum, George Tucker, and Sergey Levine. D4rl: Datasets for deep data-driven reinforcement learning, 2020.

- [20] Scott Fujimoto, Edoardo Conti, Mohammad Ghavamzadeh, and Joelle Pineau. Benchmarking batch deep reinforcement learning algorithms, 2019.

- [21] Aviral Kumar, Justin Fu, George Tucker, and Sergey Levine. Stabilizing off-policy q-learning via bootstrapping error reduction. CoRR, abs/1906.00949, 2019.

- [22] Rahul Kidambi, Aravind Rajeswaran, Praneeth Netrapalli, and Thorsten Joachims. Morel : Model-based offline reinforcement learning, 2020.

- [23] Yifan Wu, George Tucker, and Ofir Nachum. Behavior regularized offline reinforcement learning, 2019.

- [24] Quentin F. Gronau, Alexander Ly, and Eric-Jan Wagenmakers. Informed bayesian t-tests. The American Statistician, 74(2):137–143, 2020.

- [25] Richard S. Sutton and Andrew G. Barto. Reinforcement Learning: An Introduction. The MIT Press Cambridge, Massachusetts London, England, 2017.

- [26] Nan Jiang and Lihong Li. Doubly robust off-policy value evaluation for reinforcement learning. arXiv.org, 2016.

- [27] Philip S. Thomas and Emma Brunskill. Data-efficient off-policy policy evaluation for reinforcement learning. 2016.

- [28] Alexander L Strehl and Michael L Littman. An analysis of model-based interval estimation for markov decision processes. Journal of Computer and System Sciences, 74(8):1309–1331, 2008.

- [29] Johnson A. E. W, Pollard T. J., Shen L., Lehman L.-W. H., Feng M., Ghassemi M., Moody B., Szolovits P., Anthony Celi L., , and R. G. Mark. A freely accessible critical care database mimic-iii. Scientific Data, 4(160035), 2016.

- [30] Scott Fujimoto, David Meger, and Doina Precup. Off-policy deep reinforcement learning without exploration. In International Conference on Machine Learning, pages 2052–2062, 2019.

- [31] Aniruddh Raghu, Matthieu Komorowski, Leo Anthony Celi, Peter Szolovits, and Marzyeh Ghassemi. Continuous state-space models for optimal sepsis treatment - a deep reinforcement learning approach. 2017.

Supplementary Material for Expert-Supervised Reinforcement Learning for Offline Policy Learning and Evaluation

Appendix A Off-Policy Policy Evaluation and Uncertainty Estimation

In this Section, we follow the lines of Section 4 in the main text with more discussion. We show an Algorithm that collects the ideas presently discussed and an additional Lemma regarding the convergence of the null probability estimator.

We leverage to estimate the value function for any policy, and use hypothesis testing for whether there is a meaningful difference in two policy functions (i.e. vs. ). Recall, we compute the estimated value of a given policy , by sampling models from the posterior and navigating using to obtain . We estimate with . This process is shown in Algorithm 2.

Note that we average over the initial states as well, as we are interested to know the marginal value of the policy. A conditional value of the policy function can also be computed simply by starting all samples at a fixed state. Analogous to Section 3, we use samples to define a CI using the and quantiles. Note that for policies which are very different from the behavior policy, the posterior distribution will have wider CIs due to the wide distribution shift. This signals that there is not enough information in for the rarely visited state-action pairs . This happens with OPPE importance sampling estimators as well [2]. As opposed to only considering point estimators of the value function, these CI help to assess whether the estimated value is likely to be accurate or if the estimate is unreliable given the information in . Importance sampling based estimators reflect this large distribution shift in high variance estimators.

Policy-level hypothesis testing.

We use Algorithm 2 to assess whether there is a statistically significant difference in value from two different policies. Define the value function null hypothesis for two fixed policies as the event in which policy has a higher expected value than conditional on : . The probability of the null under the true model is

We use the following estimator from samples generated from Algorithm 2:

| (2) |

Lemma A.1.

Let , be two pre-specified policy functions, and let be defined as in (2),

Lemma A.1 ensures consistency of the probability of the null-hypothesis for the value function testing.

Appendix B Supporting Lemma

Lemma B.1.

(Lemma 1 in [16]) If is the distribution of then, for any measurable function , and model :

Appendix C Proof of results in main body

C.1 Theorem 3.4

In this Subsection we develop the necessary definitions and lemmas, and eventually go on to prove Theorem 3.4. To simplify notation let and . Given the behavior policy as defined in Algorithm 1 and the optimal policy under the true MDP , we can write the ESRL policy obtained from any sample from Algorithm 1, and it’s equivalent version under as:

we show our result is true for any and thus it’s true for the ESRL policy . Next we define the policy which uses the true null probabilities and as:

finally let

Consider function , is measurable for a fixed as , are fixed , thus, by Lemma B.1 for any

now using iterated expectations we get .

We use this to re-express the expected regret for episode under model computed with Algorithm 1 as

where the last step follows from adding and subtracting .

We first consider , we use a strategy similar to [16], but do not make an assumption for within-episode observations. Define the following Bellman operator for any MDP , policy , and value function to be

| (3) |

this lets us write .

The next Lemma will let us express term in terms of the Bellman operator.

Lemma C.1.

If is the distribution of , then

We now define a confidence set for the reward and transition estimated probabilities.

Lemma C.2.

Let denote the set of index for episodes in , that is: . Further let be the number of times was sampled in : , let and be non-parametric estimators for the distribution of transitions and rewards observed after sampling episodes:

Define the confidence set:

where then .

Proof of Theorem 3.4.

We start by summing over all episodes:

where the first step follows by conditioning on event and it’s complement, and from the fact that as all rewards . The second step follows from iterated expectations and Lemma C.2 as . Also since is a -measurable function by Lemma B.1 we have , using iterated expectations we have . The last step follows from Lemma C.1. Next using (3) the last equation can be re-written as

where the last step follows by Lemma C.2, next:

where the last step follows by Appendix B in [16] with constants .

We next analyze

We can write the second term as

we extend the null probability notation to be explicit on the time index: . By Lemma 3.2, such that with high probability, therefore

| (4) | ||||

As in Algorithm 1 are mutually exclusive, are independent to , therefore starting with we have

where the first step follows from being independent, the second step follows from (4) and last step from definition of . Iterating backards from and applying the same steps as above we get

therefore we have choosing we get which is dominated by .

Putting both terms together we have

∎

C.2 Proofs for other results in main body

Proof of Lemma 3.1.

To establish is unbiased, note that for any fixed , are , now for a given policy function

where the last step follows from Lemma B.1 with which is measurable.

To establish the rate, we have that , thus . By definition if and only if for any , such that

Note that for any ,

which follows from Hoeffding’s inequality as conditional on and , are with mean . The result follows from choosing large enough such that .

∎

Proof of Lemma 3.2.

To simplify notation, let , then by definition if and only if for any , such that

Note that for any ,

where the inequality follows from Hoeffding’s inequality as are with mean , since , in Algorithm 1 are disjoint. We can choose large enough such that . Next note that as is fixed, by Lemma B.1, with for any

which follows from using disjoint sets , in Algorithm 1. Substituting this in the probability statement gives us

which is our required result. ∎

Proof of Theorem 4.1.

We start by showing is unbiased:

where the first step follows from definition, and the being , now by Lemma B.1 with we have

To establish the rate, we have that as all rewards are between by definition if and only if for any , such that

Note that for any ,

where the inequality follows from Hoeffding’s inequality as are with mean . The result follows from choosing large enough such that . ∎

Appendix D Proofs for Supplementary results

Proof of Lemma A.1.

First note that conditional on with , by Lemma B.1

By definition if and only if for any , such that

Now, for any ,

where the inequality follows from Hoeffding’s inequality as the indicators are with mean . We can choose large enough such that . ∎

Proof of Lemma C.1.

We first write the estimated regret as a sum of difference in value functions and a Bellman error.

I) We’ll denote the sequence of states for an episode as , define

using (3) we can write

with the same steps we can generalize this to

| (5) |

Next let

using the Bellman operator we get

then we can write , with the above definitions and repeated use of (5):

II) Next we consider :

which follows by the expectation conditional on , and definition of policy .

Putting I) and II) together we get

∎

Proof of Lemma C.2.

First consider Azuma-Hoeffding’s Inequality:

Let be a martingale sequence difference with . Then and .

By definition the difference between the estimated transition and reward functions and their true respective functions are:

now let , and consider the transition probability function, for a fixed state action pair , let , we have

where the first step follows from multiplying by , and eliminating the absolute value with , we use a union bound for the second step as there are possible for a fixed pair. Next we use Azuma-Hoeffding’s inequality to bound the probability terms, note that within the probability function we are summing over terms:

next we sum over all pairs and get

which follows from using a union bound again. Analogous we can show that , thus

∎