Analysis of the Global Banking Network by Random Matrix Theory

Abstract

Since 2008, the network analysis of financial systems is one of the most important subjects in economics. In this paper, we have used the complexity approach and Random Matrix Theory (RMT) for analyzing the global banking network. By applying this method on a cross border lending network, it is shown that the network has been denser and the connectivity between peripheral nodes and the central section has risen. Also, by considering the collective behavior of the system and comparing it with the shuffled one, we can see that this network obtains a specific structure. By using the inverse participation ratio concept, we can see that after 2000, the participation of different modes to the network has increased and tends to the market mode of the system. Although no important change in the total market share of trading occurs, through the passage of time, the contribution of some countries in the network structure has increased. The technique proposed in the paper can be useful for analyzing different types of interaction networks between countries.

keywords:

Global Banking Network , Complex Systems , Random Matrix Theory , Financial Contagion1 Introduction

Since the recent global financial crisis, cross-border lending and financial contagions have gained importance. This importance stems from the propagated effects [1, 2] of financial crises on political and economic situations [3, 4]. This fact has prompted a lot of research on the systemic dependence of the international banking sector [5, 6, 7, 8, 9, 10, 11].

One of the most recent approaches for analyzing this situation comes from the notion of complexity [5, 12]. The purpose of complexity science in finance focuses on the analysis of the structure and the dynamics of entangled systems. Many scholars have applied complexity techniques for analyzing financial contagion [13, 10, 9, 6, 14]. Their findings suggested that connectivity of financial institutions is the source of potential contagions.

Random Matrix Theory is one of the useful methods for analyzing the behavior of complex systems [15, 16, 17, 18, 19, 12, 20, 21, 22, 23]. This theory was developed by researchers to describe the situation of energy levels of quantum systems [24, 25].

The universality regime of the eigenvalue statistics is the success factor of Random Matrix Theory [26, 27, 28]. Based on previous studies, it is shown that when the size of the matrix is very large, the eigenvalue distribution tends towards a specific distribution [28].

Random Matrix Theory has been applied to analyze the behavior of coupling matrices [12]. This technique divides the contents of the coupling matrix into noise and information parts. The noise part of the coupling matrix conforms to the Random Matrix Theory findings and the information part deviates from them. This concept stems from the idea of solving the problem of non-stationary cross correlation and measurement noise, as a result of market conditions and the finite length of time series [28, 26].

It is shown that the majority of their eigenvalues agree with the random matrix predictions, but the largest eigenvalue has deviations from those estimations [27, 26, 29, 22]. In essence, this eigenvalue develops an energy gap that separates it from the other eigenvalues [17]. The largest eigenvalue is related to a strongly delocalized eigenvector that presents the collective evolution of the system, and this is called the market mode. From this perspective, the largest eigenvalue’s magnitude reflects the coupling strength of the system [17].

One of the systems which can be analyzed by the complexity approach, is the global banking network [30]. In this paper, by applying Random Matrix Theory as a useful technique from complexity science, we want to analyze the global banking network.

Our paper is organized as follows. In Section 2 we present our methods and, in section 3 we apply Random Matrix Theory on the global banking network and present our findings. Then, in section 4 we conclude.

2 Methods

Primarily Random Matrix Theory has been presented by some scholars in nuclear physics such as Mehta [24, 25], for analyzing the energy levels of complex quantum systems. Subsequently, the mentioned method helped to address specific issues in other fields, such as finance [17, 28, 27, 26].

Based on the perception from random matrix theory, the eigenvalues –in the real matrix– which deviate from the range of the eigenvalues –in the random matrix– possess relatively more complete information from the system [27, 23, 28].

In Random Matrix Theory, there is a parameter named as the Inverse Participation Ratio which is based on the theory of Anderson’s localization [31], and it computes the number of components which significantly participate in each eigenvector. This notion shows the effect of components of each eigenvector, and specifically how the largest eigenvalues deviate from the bulk region which is densely occupied by eigenvalues of the random matrix. Based on the previous papers [17, 32], can be applied as an indicator for measuring the collective behavior of the networks. The formula of this concept is as follows:

| (1) |

where and is the element of eigenvector (). To further clarify the concept, one may consider examples below:

– In case all elements of a certain eigenvector are equal to , will be equal to . This implies that whole elements are significantly influential on the systems’ behavior.

– On the other hand, if just a single element is equal to and the others are equal to , would be equal to . This implies that only this component is effective in the corresponding eigenvector.

Hence, one can perceive that clarifies the number of influential elements in a certain eigenvector.

3 Analysis of Global Banking Network by Random Matrix Theory

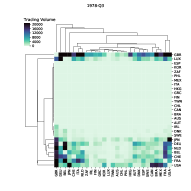

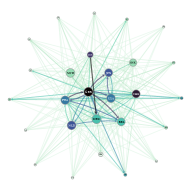

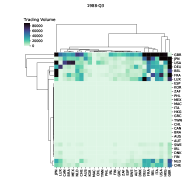

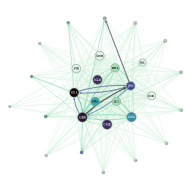

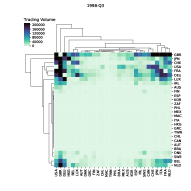

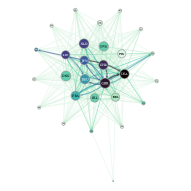

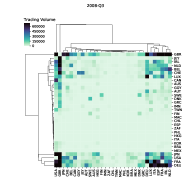

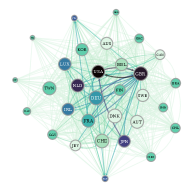

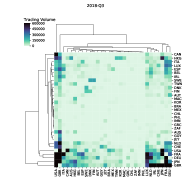

The banking industry is one of the most important sectors in finance. In this regard, one of the significant aspects of financial contagion is the emergence and transmission of crisis throughout the banking network. In Fig. 1, the evolution of the global banking network in 5 snapshots (1978-Q3, 1988-Q3, 1998-Q3, 2008-Q3 and 2018-Q3) has been depicted. The left panel in Fig. 1 shows the dendrogram structure of communities for trading weighted matrices. Also, the right column shows the evolution of the network topology. As depicted, the network has been denser over time. Not only the contributions have risen, but also the peripheral nodes are arranged closer and connected to the central section.

In this study, we apply Random Matrix Theory for the data of BIS bilateral locational statistics provided by the Bank for International Settlements (BIS) [33] from 1978 until 2019. This data includes all ‘core’ countries (the qualifier ‘core’ is used by many researchers such as [30], for 31 countries which regularly report their financial data to BIS).

We create a weighted and directed financial transaction network corresponding to each quarter from 1978 until 2019. Each link corresponds to a loan given by a certain country to another one. Previous studies specifically shed light onto countries’ dependency network and showed an increase in the dependency structure of the network of those countries during the passage of time [30]. As already discussed, Random Matrix Theory is a powerful approach for analyzing complex systems. In this paper we apply this concept for the analysis of the global banking network as a complex network. For this purpose, we choose the shuffling technique for the construction of a random matrix. The shuffling method which is applied in this research is randomization of bilateral trading volume (or links) in the network. It means that the PDF remains unchanged and the bilateral trading relations will be shuffled. The Shuffled matrix is an indication of no information in the system.

The global banking network possesses an adjacency matrix. This matrix can intrinsically be explained by the eigenvalue decomposition methods [34]. The eigenvector corresponding to the largest eigenvalue, , is the most significant and is the market mode of the network [35, 17, 27, 26].

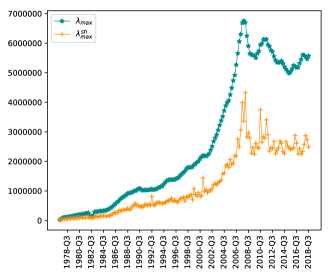

In this regard, we assess the temporal behavior of the largest eigenvalue, as shown in Fig. 2.

By evaluating the behavior of and comparing it with the of the corresponding shuffled matrix in Fig. 2, one can observe the information content of the market mode. As depicted in Fig. 2, the temporal behavior of the largest eigenvalue in the banking interaction matrix, is totally different from that of the largest eigenvalue in the shuffled matrix. This phenomenon determines the existence of information content embedded in the largest eigenvalue of the banking interaction matrix.

When it comes to Fig. 2, the behavior of the maximum eigenvalue has been ascending. This issue – as stated before— has bilateral effects.

The reasoning behind this is that on the one side, it causes more strength and stability in the network, whilst on the other side, it yields to a more agile contagion throughout the network [7]. In the post-crisis era after 2008, simultaneous to a decrease in the maximum eigenvalue, the collective behavior of the system has reduced and accordingly, local identities have been more significant.

Since the so-obtained eigenvalue does not describe all the details and properties of the collective behavior, one should investigate other quantities in the network.

It is observable that during the global financial crisis, a structural emergence with an increase in the difference between and , Fig. 2, has occurred.

However, after the crisis, a significant decrease in the behavior of the largest eigenvalue of the banking matrix relating to that of the shuffled matrix has emerged.

Based on the above concepts, one of the best approaches for analyzing the global banking network is the Random Matrix Theory technique.

As already discussed, one should keep in mind that possesses the ability of information extraction from the collective behaviors of the systems.

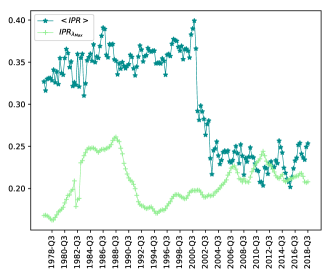

In Fig. 3, By comparing and , one is able to distinguish the temporal evolution of participation in the network.

In Fig. 3, we investigate the inverse participation ratio (IPR) in a temporal process. In this context, by focusing on the mean inverse participation ratio , , and also, the inverse participation ratio of the largest eigenvalue corresponding to the largest eigenvector , we investigate banking behaviors of the countries and their influences on the network structure and the market trend. In Fig. 3, implies the effectiveness of the banking system of most countries on the global network. However, from the temporal behavior of , we observe that over time, less participation from those countries on the largest eigenvector emerges.

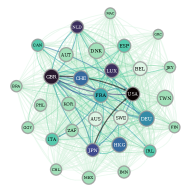

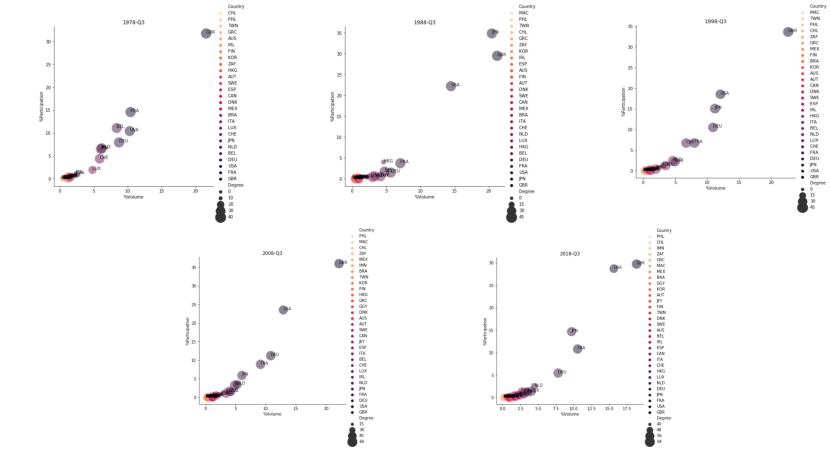

In Fig. 4, stands for the contribution percentage of each country in the eigenvector corresponding to the largest eigenvalue. is the trading volume of a country divided by the total trading volume. Hence, shows the contribution in the structure, and, shows the contribution in the total trading volume. Thereby, Fig. 4 visualizes the contributions in the structure versus the contribution in trading volume within each year. In 2018-Q3, for the US, while the percentage of contribution in the structure has been approximately constant, the percentage of contribution in trading volume decreased.

4 Conclusion

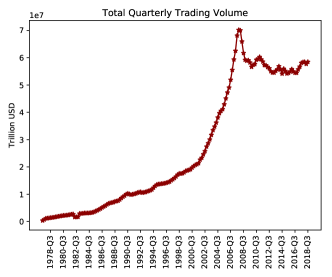

In this paper, by applying Random Matrix Theory, the global banking network is investigated. For this purpose, we compute the matrix of interaction of banking sectors of BIS countries, and then by using the Random Matrix Theory approach, the behavior of the largest eigenvalue and Inverse Participation Ratio of this eigenvalue, as the market mode of the system over time, has been analyzed. The value of the largest eigenvalue increases during the passage of time. By observing the behavior of trading volume, it is shown that these increases stem from the expansion of the network to some extent. Also, by comparing with the shuffled one, we can deduce that the system gets a specific structure. Generally speaking, the global banking network, today, is more dense and interconnected. Also, we can see that after the year 2000 the value of the mean has dropped and converged to . It means that more countries have become more influential on the global banking network. Furthermore, despite small changes in the share of total trading volume, some countries such as the UK, have become more important in the network structure.

As a concluding remark, the identities of banking systems of BIS countries stems from two parts, i.e. i) from their own identities individually and, ii) from their interactions in the global banking network. As a suggestion for further work, one can construct the interaction matrices of the countries based on other variables such as commercial interactions and so on.

References

- [1] G. Iori, R. N. Mantegna, L. Marotta, S. Miccichè, J. Porter, M. Tumminello, Networked relationships in the e-MID interbank market: A trading model with memory, Journal of Economic Dynamics and Control 50 (2015) 98–116. doi:10.1016/j.jedc.2014.08.016.

- [2] A. G. Haldane, R. M. May, Systemic risk in banking ecosystems, Nature 469 (7330) (2011) 351–355. doi:10.1038/nature09659.

- [3] K. R. Carmen M. Reinhart, This Time Is Different: Eight Centuries of Financial Folly, 1st Edition, Princeton University Press, 2009.

- [4] M. G. A. Contreras, G. Fagiolo, Propagation of economic shocks in input-output networks: A cross-country analysis, Physical Review E 90 (6). doi:10.1103/physreve.90.062812.

- [5] A. S. E. B. e. Cont, Rama; Moussa, Network structure and systemic risk in banking systems, SSRN Electronic Journaldoi:10.2139/ssrn.1733528.

-

[6]

J. Etesami, A. Habibnia, N. Kiyavash,

Econometric modeling

of systemic risk: going beyond pairwise comparison and allowing for

nonlinearity, LSE Research Online Documents on Economics 70769, London

School of Economics and Political Science, LSE Library (Mar. 2017).

URL https://ideas.repec.org/p/ehl/lserod/70769.html - [7] S. Battiston, D. D. Gatti, M. Gallegati, B. Greenwald, J. E. Stiglitz, Liaisons dangereuses: Increasing connectivity, risk sharing, and systemic risk, Journal of Economic Dynamics and Control 36 (8) (2012) 1121–1141. doi:10.1016/j.jedc.2012.04.001.

-

[8]

F. Betz, N. Hautsch, T. A. Peltonen, M. Schienle,

Systemic risk spillovers in

the european banking and sovereign network, Journal of Financial Stability

25 (2016) 206–224.

doi:10.1016/j.jfs.2015.10.006.

URL https://doi.org/10.1016/j.jfs.2015.10.006 - [9] M. D’Errico, S. Battiston, T. Peltonen, M. Scheicher, How does risk flow in the credit default swap market?, ECB Working Paper 2041 (2017). doi:10.2866/086521.

-

[10]

S. Battiston, G. Caldarelli,

Systemic risk in

financial networks, Journal of Financial Management, Markets and

Institutions, Rivista semestrale on line (2/2013) (2013) 129–154.

doi:10.12831/75568.

URL https://www.rivisteweb.it/doi/10.12831/75568 - [11] F. Atyabi, O. Buchel, L. Hedayatifar, Driver countries in global banking network.

- [12] G. Jafari, A. H. Shirazi, A. Namaki, R. Raei, Coupled time series analysis: Methods and applications, Computing in Science & Engineering 13 (6) (2011) 84–89. doi:10.1109/mcse.2011.102.

- [13] P. Glasserman, H. P. Young, Contagion in financial networks, Journal of Economic Literature 54 (3) (2016) 779–831. doi:10.1257/jel.20151228.

- [14] M. Bardoscia, S. Battiston, F. Caccioli, G. Caldarelli, Pathways towards instability in financial networks, Nature Communications 8 (1). doi:10.1038/ncomms14416.

- [15] M. POTTERS, J.-P. BOUCHAUD, Financial applications of random matrix theory: a short review, arXiv preprint arXiv:0910.1205.

- [16] X. F. Jiang, T. T. Chen, B. Zheng, Structure of local interactions in complex financial dynamics, Scientific Reports 4 (1). doi:10.1038/srep05321.

- [17] A. Namaki, A. Shirazi, R. Raei, G. Jafari, Network analysis of a financial market based on genuine correlation and threshold method, Physica A: Statistical Mechanics and its Applications 390 (21-22) (2011) 3835–3841. doi:10.1016/j.physa.2011.06.033.

- [18] M. MacMahon, D. Garlaschelli, Community detection for correlation matrices, Physical Review X 5 (2). doi:10.1103/physrevx.5.021006.

- [19] L. Sandoval, I. D. P. Franca, Correlation of financial markets in times of crisis, Physica A: Statistical Mechanics and its Applications 391 (1-2) (2012) 187–208. doi:10.1016/j.physa.2011.07.023.

- [20] A. H. Shirazi, G. R. Jafari, J. Davoudi, J. Peinke, M. R. R. Tabar, M. Sahimi, Mapping stochastic processes onto complex networks, Journal of Statistical Mechanics: Theory and Experiment 2009 (07) (2009) P07046. doi:10.1088/1742-5468/2009/07/p07046.

- [21] J. Jurczyk, T. Rehberg, A. Eckrot, I. Morgenstern, Measuring critical transitions in financial markets, Scientific Reports 7 (1). doi:10.1038/s41598-017-11854-1.

- [22] J. Kwapień, S. Drożdż, Physical approach to complex systems, Physics Reports 515 (3-4) (2012) 115–226. doi:10.1016/j.physrep.2012.01.007.

- [23] A. Namaki, G. Jafari, R. Raei, Comparing the structure of an emerging market with a mature one under global perturbation, Physica A: Statistical Mechanics and its Applications 390 (17) (2011) 3020–3025. doi:10.1016/j.physa.2011.04.004.

- [24] M. L. MEHTA, Random Matrices, Elsevier, 1991. doi:10.1016/c2009-0-22297-5.

- [25] M. L. MEHTA, Preface to the third edition, in: Random Matrices, Elsevier, 2004, pp. xiii–xiv. doi:10.1016/s0079-8169(04)80088-6.

- [26] V. Plerou, P. Gopikrishnan, B. Rosenow, L. A. N. Amaral, T. Guhr, H. E. Stanley, Random matrix approach to cross correlations in financial data, Physical Review E 65 (6). doi:10.1103/physreve.65.066126.

- [27] L. LALOUX, P. CIZEAU, M. POTTERS, J.-P. BOUCHAUD, RANDOM MATRIX THEORY AND FINANCIAL CORRELATIONS, International Journal of Theoretical and Applied Finance 03 (03) (2000) 391–397. doi:10.1142/s0219024900000255.

- [28] A. NAMAKI, R. RAEI, G. R. JAFARI, COMPARING TEHRAN STOCK EXCHANGE AS AN EMERGING MARKET WITH a MATURE MARKET BY RANDOM MATRIX APPROACH, International Journal of Modern Physics C 22 (04) (2011) 371–383. doi:10.1142/s0129183111016300.

- [29] G.-J. Wang, C. Xie, S. Chen, J.-J. Yang, M.-Y. Yang, Random matrix theory analysis of cross-correlations in the US stock market: Evidence from pearson’s correlation coefficient and detrended cross-correlation coefficient, Physica A: Statistical Mechanics and its Applications 392 (17) (2013) 3715–3730. doi:10.1016/j.physa.2013.04.027.

- [30] J. A. Reyes, C. Minoiu, and, A network analysis of global banking:1978-2009, IMF Working Papers 11 (74) (2011) 1. doi:10.5089/9781455227051.001.

- [31] G. Lim, S. Kim, J. Kim, P. Kim, Y. Kang, S. Park, I. Park, S.-B. Park, K. Kim, Structure of a financial cross-correlation matrix under attack, Physica A: Statistical Mechanics and its Applications 388 (18) (2009) 3851–3858. doi:10.1016/j.physa.2009.05.018.

- [32] M. Saeedian, T. Jamali, M. Kamali, H. Bayani, T. Yasseri, G. Jafari, Emergence of world-stock-market network, Physica A: Statistical Mechanics and its Applications 526 (2019) 120792. doi:10.1016/j.physa.2019.04.028.

-

[33]

Bank for international settlements (bis).

URL https://stats.bis.org/ - [34] P. Barucca, M. Kieburg, A. Ossipov, Eigenvalue and eigenvector statistics in time series analysis, arXiv preprint arXiv:1904.05079.

- [35] A. Utsugi, K. Ino, M. Oshikawa, Random matrix theory analysis of cross correlations in financial markets, Physical Review E 70 (2). doi:10.1103/physreve.70.026110.