Efficient Tensor Decomposition††thanks: Chapter 19 of the book Beyond the Worst-Case Analysis of Algorithms [Rou20].

Abstract

This chapter studies the problem of decomposing a tensor into a sum of constituent rank one tensors. While tensor decompositions are very useful in designing learning algorithms and data analysis, they are NP-hard in the worst-case. We will see how to design efficient algorithms with provable guarantees under mild assumptions, and using beyond worst-case frameworks like smoothed analysis.

1 Introduction To Tensors

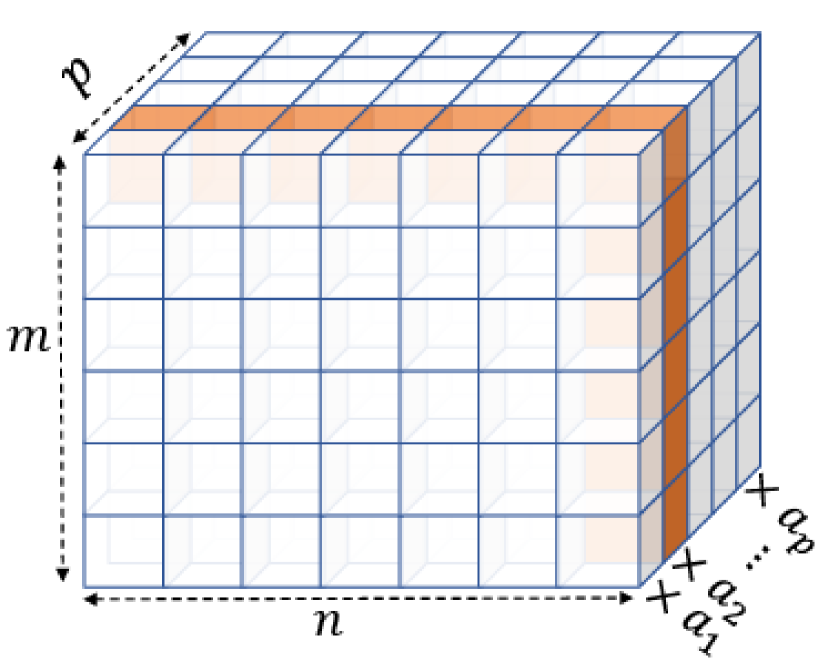

Tensors are multi-dimensional arrays, and constitute natural generalizations of matrices. Tensors are fundamental linear algebraic entities, and widely used in physics, scientific computing and signal processing to represent multi-dimensional data or capture multi-wise correlations. The different dimensions of the array are called the modes and the order of a tensor is the number of dimensions or modes of the array, as shown in Figure 1. The order of a tensor also corresponds to the number of indices needed to specify an entry of a tensor. Hence every specifies an entry of the tensor that is denoted by .

While we have a powerful toolkit of algorithms like low rank approximations and eigenvalue decompositions for matrices, our algorithmic understanding in the tensor world is limited. As we will see soon many basic algorithmic problems like low-rank decompositions are NP-hard in the worst case for tensors (of order and above). But on the other hand, many higher order tensors satisfy powerful structural properties that are simply not satisfied by matrices. This makes them particularly useful for applications in machine learning and data analysis. In this chapter, we will see how we can indeed overcome this worst-case intractability under some natural non-degeneracy assumptions or using smoothed analysis, and also exploit these powerful properties for designing efficient learning algorithms.

1.1 Low-rank decompositions and rank

We start with the definition of a rank one tensor. An order tensor is rank one if and only if it can be written as an outer product for some vectors i.e.,

Note than when , this corresponds to being expressible as .

Definition 1.1.

[Rank decomposition] A tensor is said to have a decomposition of rank iff it is expressible as the sum of rank one tensors i.e.,

Moreover has rank if and only if is the smallest natural number for which has a rank decompostion.

The vectors are called the factors of the decomposition. To keep track of how the factors across different modes are grouped, we will use for to represent the factors. These “factor matrices” all have columns, one per term of the decomposition. Finally, we will also consider symmetric tensors – a tensor of order is symmetric iff for every permutation over (see Exercise 5 for an exercise about decompositions of symmetric tensors).

Differences from matrix algebra and pitfalls.

Observe that these definition of rank, low-rank decompositions specialize to the standard notions for matrices (). However it is dangerous to use intuition we have developed from matrix algebra to reason about tensors because of several fundamental differences. Firstly, an equivalent definition for rank of a matrix is the dimension of the row space, or column space. This is not true for tensors of order and above. In fact for a tensor of order in , the rank as we defined it could be as large as , while the dimension of the span of dimensional vectors along any of the modes can be at most . The definition that we study in Definition 1.1 (as opposed to other notions like Tucker decompositions) is motivated by its applications to statistics and machine learning.

Secondly, much of the spectral theory for matrices involving eigenvectors and eigenvalues does not extend to tensors of higher order. For matrices, we know that the best rank- approximation consists of the leading terms of the SVD. However this is not the case for tensor decompositions. The best rank- approximation may not be a factor in the best rank- approximation. Finally, and most importantly, the algorithmic problem of finding the best rank- approximation of a tensor is NP-hard in the worst-case, particularly for large ;111For small , there are algorithms that find approximately optimal rank- approximations in time exponential in (see e.g., [BCV14, SWZ19]). for matrices, this is of course solved using singular value decompositions (SVD). In fact, this worst-case NP-hardness for higher order tensors is true for most tensor problems including computing the rank, computing the spectral norm etc. [Hås90, HL13].

For all of the reasons listed above, and more,222 There are other definitional issues with the rank – there are tensors of a certain rank, that can be arbitrarily well-approximated by tensors of much smaller rank i.e., the “limit rank” (or formally, the border rank) may not be equal to the rank of the tensor. See Exercise 2 for an example. it is natural to ask, why bother with tensor decompositions at all? We will now see a striking property (uniqueness) satisfied by low-rank decompositions of most higher order tensors (but not satisfied by matrices), that also motivates many interesting uses of tensor decompositions.

Uniqueness of low-rank decompositions.

A remarkable property of higher order tensors is that (under certain conditions that hold typically) their minimum rank decompositions are unique upto trivial scaling and permutation. This is in sharp contrast to matrix decompositions. For any matrix with a rank decomposition , there exists several other rank decompositions , where and for any rotation matrix i.e., ; in particular, the SVD is one of them. This rotation problem, is a common issue when using matrix decompositions in factor analysis (since we can only find the factors up to a rotation).

The first uniqueness result for tensor decompositions was due to Harshman [Har70](who in turn credits it to Jennrich), assuming what is known as the “full rank condition”. In particular, if has a decomposition

(or the factor matrix is full rank), then this is the unique decomposition of rank up to permuting the terms. (The statement is actually a little more general and also handles non-symmetric tensors; see Theorem 3.1). Note that the full rank condition requires (moreover it holds when the vectors are in general position in dimensions). What makes the above result even more surprising is that, the proof is algorithmic! We will in fact see the algorithm and proof in Section 3.1. This will serve as the workhorse for most of the algorithmic results in this chapter. Kruskal [Kru77] gave a more general condition that guarantees uniqueness up to rank , using a beautiful non-algorithmic proof. Uniqueness is also known to hold for generic tensors of rank (here “generic” means all except a measure zero set of rank tensors). We will now see how this remarkable property of uniqueness will be very useful for applications like learning latent variable models.

2 Applications to Learning Latent Variable Models

A common approach in unsupervised learning is to assume that the data (input) that is given to us is drawn from a probabilistic model with some latent variables and/or unknown parameters , that is appropriate for the task at hand i.e., the structure we want to find. This includes mixture models like mixtures of Gaussians, topic models for document classification etc. A central learning problem is the efficient estimation of such latent model parameters from observed data.

A necessary step towards efficient learning is to show that the parameters are indeed identifiable after observing polynomially many samples. The method of moments approach, pioneered by Pearson, infers model parameters from empirical moments such as means, pairwise correlations and other higher order correlations. In general, very high order moments may be needed for this approach to succeed and the unreliability of empirical estimates of these moments leads to large sample complexity (see e.g., [MV10, BS10]). In fact, for latent variable models like mixtures of Gaussians, an exponential sample complexity of is necessary, if we make no additional assumptions.

On the computational side, maximum likelihood estimation i.e., is NP-hard for many latent variable models (see e.g., [TD18]). Moreover iterative heuristics like expectation maximization (EM) tend to get stuck in local optima. Efficient tensor decompositions when possible, present an algorithmic framework that is both statistically and computationally efficient, for recovering the parameters.

2.1 Method-of-moments via tensor decompositions: a general recipe

The method-of-moments is the general approach of inferring parameters of a distribution, by computing empirical moments of the distribution and solving for the unknown parameters. The moments of a distribution over are naturally represented by tensors. The covariance or the second moment is an matrix, the third moment is represented by a tensor of order in (the entry is ), and in general the th moment is a tensor of order . More crucially for many latent variable models with parameters , the moment tensor or a suitable modification of it, has a low-rank decomposition (perhaps up to some small error) in terms of the unknown parameters of the model. Low rank decompositions of the tensor can then be used to implement the general method-of-moments approach, with both statistical and computational implications. The uniqueness of the tensor decomposition then immediately implies identifiability of the model parameters (in particular, it implies a unique solution for the parameters)! Moreover, a computationally efficient algorithm for recovering the factors of the tensor gives an efficient algorithm for recovering the parameters .

General Recipe.

This suggests the following algorithmic framework for parameter estimation. Consider a latent variable model with model parameters . These could be one parameter each for the possible values of the latent variable (for example, in a mixture of Gaussians, the could represent the mean of the th Gaussian component of unit variance).

-

1.

Define an appropriate statistic of the distribution (typically based on moments) such that the expected value of has a low-rank decomposition

-

2.

Obtain an estimate of the tensor from the data (e.g., from empirical moments) up to small error (denoted by the error tensor ).

-

3.

Use tensor decompositions to solve for the parameters in the system , to obtain estimates of the parameters.

The last step involving tensor decompositions is the technical workhorse of the above approach, both for showing identifiability, and getting efficient algorithms. Many of the existing algorithmic guarantees for tensor decompositions (that hold under certain natural conditions about the decomposition e.g., Theorems 3.1 and 4.1) provably recover the rank- decomposition, thereby giving algorithmic proofs of uniqueness as well. However, the first step of designing the right statistic with a low-rank decomposition requires a lot of ingenuity and creativity. In Section 2.2 we will see two important latent variable models that will serve as our case studies. You will see another application in the next chapter on topic modeling.

Need for robustness to errors.

So far, we have completely ignored sample complexity considerations by assuming access to the exact expectation , so the error (this requires infinite samples). In polynomial time, the algorithm can only access a polynomial number of samples. Estimating a simple 1D statistic up to accuracy typically requires samples, the th moment of a distribution requires samples to estimate up to inverse polynomial error (in Frobenius norm, say). Hence, to obtain polynomial time guarantees for parameter estimation, it is vital for the tensor decomposition guarantees to be noise tolerant i.e., robust up to inverse polynomial error (this is even assuming no model mis-specification). Fortunately, such robust guarantees do exist – in Section 3.1, we will show robust analogue of Harshman’s uniqueness theorem and related algorithms (see also [BCV14] for a robust version of Kruskal’s uniqueness theorem). Obtaining robust analogues of known uniqueness and algorithmic results is quite non-trivial and open in many cases (see Section 6).

2.2 Case studies

Case Study 1: Mixtures of Spherical Gaussians.

Our first case study is mixtures of Gaussians. They are perhaps the most widely studied latent variable model in machine learning for clustering and modeling heterogenous populations. We are given random samples, where each sample point is drawn independently from one of Gaussian components according to mixing weights , where each Gaussian component has a mean and a covariance . The goal is to estimate the parameters up to required accuracy in time and number of samples that is polynomial in . Existing algorithms based on method of moments have sample complexity and running time that is exponential in in general [MV10, BS10]. However, we will see that as long as certain non-degeneracy conditions are satisfied, tensor decompositions can be used to get tractable algorithms that only have a polynomial dependence on (in Theorem 3.3 and Corollary 4.9).

For the sake of exposition, we will restrict our attention to the uniform case when the mixing weights are all equal and variances . Most of these ideas also apply in the more general setting [HK13].

For the first step of the recipe, we will design a statistic that has a low-rank decomposition in terms of the means .

Proposition 2.1.

For any integer , one can compute efficiently a statistic from the first moments such that .

Let denote a Gaussian r.v. The expected value of the statistic

| (1) |

Now the first term in the inner expansion (where every ) is the one we are interested in, so we will try to “subtract” out the other terms using the first moments of the distribution. Let us consider the case when to gain more intuition. As odd moments of are zero, we have

Hence, we can obtain the required tensor using a combination of and ; the corresponding statistic is . We can use a similar inductive approach for obtaining (or use Iserlis identity that expresses higher moments of a Gaussian in terms of the mean and covariance)333An alternate trick to obtain a statistic that only loses constant factors in the dimension involves looking at an off-diagonal block of the tensor after partitioning the co-ordinates into equal sized blocks..

Case study 2: Learning Hidden Markov Models (HMMs).

Our next example is HMMs which are extensively used for data with a sequential structure. In an HMM, there is a hidden state sequence taking values in , that forms a stationary Markov chain with transition matrix and initial distribution (assumed to be the stationary distribution). The observation is represented by a vector in . Given the state at time , is conditionally independent of all other observations and states. The observation matrix is denoted by ; the columns of represent the means of the observation conditioned on the hidden state i.e., , where represents the th column of . We also assume that satisfies strong enough concentration bounds to use empirical estimates. The parameters are .

We now define appropriate statistics following [AMR09]. Let for some to be chosen later. The statistic is . We can also view this moment tensor as a 3-tensor of shape . The first mode corresponds to , the second mode is and the third mode is . Why does it have a low-rank decomposition? We can think of the hidden state as the latent variable which takes possible values.

Proposition 2.2.

The above statistic has a low-rank decomposition with factor matrices , , and s.t. ,

Moreover, and can be recovered from .

3 Efficient Algorithms in the Full Rank Setting

3.1 Simultaneous Diagonization (Jennrich’s algorithm)

We now study Jennrich’s algorithm (first described in [Har70]), that gives theoretical guarantees for finding decompositions of third-order tensors under a natural non-degeneracy condition called the full-rank setting. Moreover this algorithm also has reasonable robustness properties, and can be used as a building block to handle more general settings and for many machine learning applications. Consider a third-order tensor that has a decomposition of rank :

Our algorithmic goal is to recover the unknown factors . Of course, we only hope to recover the factors up to some trivial scaling of vectors (within a rank-one term) and permuting terms. Note that our algorithmic goal here is much stronger than usual. This is possible because of uniqueness of tensor decompositions – in fact, the proof of correctness of the algorithm also proves uniqueness!

The algorithm considers two matrices that are formed by taking random linear combinations of the slices of the tensor as shown in Figure 2. We will show later in (2) that both have low-rank decompositions in terms of the unknown factors . Hence, the algorithm reduces the problem of decomposing one third-order tensor into the problem of obtaining a “simultaneous” decomposition of the two matrices (this is also called simultaneous diagonalization).

In the following algorithm, refers to the pseudoinverse or the Moore-Penrose inverse of (if a rank- matrix has a singular value decomposition where is a diagonal matrix, then ).

Input: Tensor .

-

1.

Draw independently. Set .

-

2.

Set to be the eigenvectors corresponding to the largest (in magnitude) eigenvalues of . Similarly let be the eigenvectors corresponding to the largest (in magnitude) eigenvalues of .

-

3.

Pair up if their corresponding eigenvalues are reciprocals (approximately).

-

4.

Solve the linear system for the vectors .

-

5.

Return factor matrices .

In what follows, denotes the Frobenius norm of the tensor ( is the sum of the squares of all the entries), and the condition number of matrix is given by , where are the singular values. The guarantees (in terms of the error tolerance) will be inverse polynomial in the condition number , which is finite only if the matrix has rank (full rank).

Theorem 3.1.

Suppose we are given tensor , where has a decomposition satisfying the following conditions:

-

1.

Matrices have condition number at most ,

-

2.

For all , .

-

3.

Each entry of is bounded by .

Then the Algorithm 1 on input runs in polynomial time and returns a decomposition s.t. there is a permutation with

We start with a simple claim that leverages the randomness in the Gaussian linear combinations (in fact, this is the only step of the argument that uses the randomization). Let and .

Lemma 3.2.

With high probability over the randomness in , the diagonal entries of are separated from each other, and from , i.e.,

The proof just uses simple anti-concentration of Gaussians and a union bound. We now proceed to the proof of Theorem 3.1.

Proof of Theorem 3.1.

We first prove that when , the above algorithm recovers the decomposition exactly. The robust guarantees when uses perturbation bounds for eigenvalues and eigenvectors.

No noise setting (). Recall that has a rank decomposition in terms of the factors . Hence

| (2) |

Moreover are full rank by assumption, and diagonal matrices have full column rank of with high probability (Lemma 3.2). Hence

Moreover from Lemma 3.2, the entries of are distinct and non-zero with high probability. Hence the column vectors of are eigenvectors of with eigenvalues . Similarly, the columns of are eigenvectors of with eigenvalues . Hence, the eigendecompositions of and are unique (up to scaling of the eigenvectors) with the corresponding eigenvalues being reciprocals of each other.

Finally, once we know (up to scaling), step 4 solves a linear system in the unknowns . A simple claim shows that the corresponding co-efficient matrix given by has “full” rank i.e., rank of . Hence the linear system has a unique solution and algorithm recovers the decomposition.

Robust guarantees ( is non-zero). When , we will need to analyze how much the eigenvectors of can change, under the (worst-case) perturbation . The proof uses perturbation bounds for eigenvectors of matrices (which are much more brittle than eigenvalues) to carry out this analysis. We now give a a high-level description of the approach, while pointing out a couple of subtle issues and difficulties. The primary issue comes from the fact that the matrix is not a symmetric matrix (for which one can use the Davis-Kahan theorem for singular vectors). In our case, while we know that is diagonalizable, there is no such guarantee about , where is the error matrix that arises at this step due to . The key property that helps us here is Lemma 3.2, which ensures that all of the non-zero eigenvalues of are separated. In this case, we know the matrix is also diagonalizable using a standard strengthening of the Gershgorin disc theorem. One can then use the separation in the eigenvalues of to argue that the eigenvectors of are close, using ideas from the perturbation theory of invariant subspaces (see Chapter 5 of[SS90]). See also [GVX14, BCMV14] for a self-contained proof of Theorem 3.1. ∎

3.2 Implications in learning applications

These efficient algorithms that (uniquely) recover the factors of a low-rank tensor decomposition give polynomial time guarantees for learning non-degenerate instances of several latent variable models using the general recipe given in Section 2.1. This approach has been used for several problems including but not limited to, parameter estimation of hidden markov models, phylogeny models, mixtures of Gaussians, independent component analysis, topic models, mixed community membership models, ranking models, crowdsourcing models, and even certain neural networks (see [AGH+14, Moi18] for excellent expositions on this topic) .

For illustration, we give the implications for our two case studies. For Gaussian mixtures, the means are assumed to be linear independent (hence ). We apply Theorem 3.1 to the order tensor obtained from Proposition 2.1.

Theorem 3.3.

[HK13] Given samples from a mixture of spherical Gaussians, there is an algorithm that learns the parameters up to error in time (and samples), where is the matrix of means.

4 Smoothed Analysis and the Overcomplete Setting

The tensor decomposition algorithm we have seen in the previous section requires that the factor matrices have full column rank. As we have seen in Section 3.2, this gives polynomial time algorithms for learning a broad variety of latent variable models under the full-rank assumption. However, there are many applications in unsupervised learning where it is crucial that the hidden representation has much higher dimension (or number of factors ) than the dimension of the feature space . Obtaining polynomial time guarantees for these problems using tensor decompositions requires polynomial time algorithmic guarantees when the rank is much larger than the dimension (in the full-rank setting , even when the factors are random or in general position in ). Can we hope to obtain provable guarantees when the rank ?

This challenging setting when the rank is larger than the dimension is often referred to as the overcomplete setting. Tensor decompositions in the overcomplete setting is NP-hard in general. However for tensors of higher order, we will see in the rest of this section how Jennrich’s algorithm can be adapted to get polynomial time guarantees even in very overcomplete settings for non-degenerate instances – this will be formalized using smoothed analysis.

4.1 Smoothed analysis model.

The smoothed analysis model for tensor decompositions models the situation when the factors in the decomposition are not worst-case.

-

•

An adversary chooses a tensor .

-

•

Each vector is randomly “-perturbed” using an independent Gaussian with mean and variance in each direction 444Many of the results in the section also hold for other forms of random perturbations, as long as the distribution satisfies a weak anti-concentration property, similar to the setting in Chapters 13-15; see [ADM+18] for details..

-

•

Let .

-

•

The input instance is , where is some small potentially adversarial noise.

Our goal is to recover (approximately when ) the sets of factors (up to rescaling and relabeling), where . The parameter setting of interest is being at least some inverse polynomial in , and the maximum entry of being smaller than some sufficiently small inverse polynomial . We will also assume that the Euclidean lengths of the factors is polynomially upper bounded. We remark that when (as in the full-rank setting), Theorem 3.1 already gives smoothed polynomial time guarantees when , since the condition number with high probability.

Remarks. There is an alternate smoothed analysis model where the random perturbation is to each entry of the tensor itself, as opposed to randomly perturbing the factors of a decomposition. The two random perturbations are very different in flavor. When the whole tensor is randomly perturbed, we have “bits” of randomness, whereas when only the factors are perturbed we have “bits” of randomness. On the other hand, the model where the whole tensor is randomly perturbed is unlikely to be easy from a computational standpoint, since this would likely imply randomized algorithms with good worst-case approximation guarantees.

Why do we study perturbations to the factors? In most applications each factor represents a parameter e.g., a component mean in Gaussian mixture models. The intuition is that if these parameters of the model are not chosen in a worst-case configuration, we can potentially obtain vastly improved learning algorithms with such smoothed analysis guarantees.

The smoothed analysis model can also be seen as the quantitative analog of “genericity” results that are inspired by results from algebraic geometry, particularly when we need robustness to noise. Results of this generic flavor give guarantees for all except a set of instances of zero measure. However, such results are far from being quantitative; as we will see later we typically need robustness to inverse polynomial error with high probability for polynomial time guarantees.

4.2 Adapting Jennrich’s algorithm for overcomplete settings.

We will give an algorithm in the smoothed analysis setting for overcomplete tensor decompositions with polynomial time guarantees. In the following theorem, we consider the model in Section 4.1 where the low-rank tensor , and the factors are -perturbations of the vectors , which we will assume are bounded by some polynomial of . The input tensor is where represents the adversarial noise.

Theorem 4.1.

Let for some constant , and . There is an algorithm that takes as input a tensor as described above, with every entry of being at most in magnitude, and runs in time to recover all the rank one terms up to an additive error measured in Frobenius norm, with probability at least .

To describe the main algorithmic idea, let us consider an order- tensor . We can “flatten" to get an order three tensor

This gives us an order- tensor of size . The effect of the “flattening" operation on the factors can be described succinctly using the following operation.

Definition 4.2 (Khatri-Rao product).

The Khatri-Rao product of and is an matrix whose column is .

Our new order three tensor also has a rank decomposition with factor matrices and respectively. Note that the columns of and are in dimensions (in general they will be dimensional). We could now hope that the assumptions on the condition number in Theorem 3.1 are satisfied for . This is not true in the worst-case (see Exercise 3 for the counterexample). However, we will prove this is true w.h.p. in the smoothed analysis model!

As the factors in are all polynomially upper bounded, the maximum singular value is also at most a polynomial in . The following proposition shows high confidence lower bounds on the minimum singular value after taking the Khatri-Rao product of a subset of the factor matrices; this of course implies that the condition number has a polynomial upper bound with high probability.

Proposition 4.3.

Let be constants such that . Given any , then for their random -perturbations, we have

where are constants that depend only on .

The proposition implies that the conditions of Theorem 3.1 hold for the flattened order- tensor ; in particular, the condition number of the factor matrices is now polynomially upper bounded with high probability. Hence by running Jennrich’s algorithm to the order- tensor recovers the rank-one factors w.h.p. as required in Theorem 4.1. The rest of the section outlines the proof of Proposition 4.3.

Failure probability. We remark on a technical requirement about the failure probability (that is satisfied by the above proposition) for smoothed analysis guarantees. We need our bounds on the condition number or to hold with a sufficiently small failure probability, say or even exponentially small (over the randomness in the perturbations). This is important because in smoothed analysis applications, the failure probability essentially describes the fraction of points around any given point that are bad for the algorithm. In many applications, the time/sample complexity has an inverse polynomial dependence on the least singular value. For example, if we have a guarantee that with probability at least , then the probability of the running time exceeding (upon perturbation) is at most . Such a guarantee does not suffice to show that the expected running time is polynomial (also called polynomial smoothed complexity).

Note that our matrix is a random matrix with highly dependent entries e.g., there are only independent variables but matrix entries. This presents very different challenges compared to well-studied settings in random matrix theory, where every entry is independent.

While the least singular value can be hard to handle directly, it is closely related to the leave-one-out distance, which is often much easier to deal with.

Definition 4.4.

Given a matrix with columns , the leave-one-out distance of is

The leave-one-out distance is closely related to the least singular value, up to a factor polynomial in the number of columns of , by the following simple lemma.

Lemma 4.5.

For any matrix , we have

| (3) |

The following (more general) core lemma that lower bounds the projection onto any given subspace of a randomly perturbed rank-one tensor implies Proposition 4.3.

Lemma 4.6.

Let and be constants, and let be an arbitrary subspace of dimension at least . Given any , then their random -perturbations satisfy

where are constants that depend only on .

The polynomial of in the exponent of the failure probability is tight; however it is unclear what the right polynomial dependence of in the least singular value bound, and the right dependence on should be. The above lemma can be used to lower bound the least singular value of the matrix in Proposition 4.3 as follows: we can lower bound the leave-one-out distance of Lemma 4.5 by applying Lemma 4.6 for each column with being the subspace given by and being ; a union bound over the columns gives Proposition 4.3. The first version of this lemma was proven in Bhaskara et al. [BCMV14] with worse polynomial dependencies both in lower bound on the condition number, and in the exponent of the failure probability. The improved statement presented here and proof sketched in Section 4.3 are based on Anari et al. [ADM+18].

Relation to anti-concentration of polynomials.

We now briefly describe a connection to anti-concentration bounds for low-degree polynomials, and describe a proof strategy that yields a weaker version of Lemma 4.6. Anti-concentration inequalities (e.g., the Carbery-Wright inequality) for a degree- polynomial with , and are of the form

| (4) |

This can be used to derive a weaker version of Lemma 4.6 with an inverse polynomial failure probability, by considering a polynomial whose co-efficients “lie” in the subspace . As we discussed in the previous section, this failure probability does not suffice for expected polynomial running time (or polynomial smoothed complexity). On the other hand, Lemma 4.6 manages to get an inverse polynomial lower bound with exponentially small failure probability, by considering different polynomials. In fact one can flip this around and use Lemma 4.6 to show a vector-valued variant of the Carbery-Wright anti-concentration bounds, where if we have “sufficiently different” polynomials each of degree , then we can get where is a constant, for the bound in (4). The advantage is that while we lose in the “small ball” probability with the degree , we gain an factor in the exponent on account of having a vector valued function with co-ordinates. See [BCPV19] for a statement and proof.

4.3 Proof Sketch of Lemma 4.6

The proof of Lemma 4.6 is a careful inductive proof. We sketch the proof for to give a flavor of the arguments involved. See [ADM+18] for the complete proof. For convenience, let and . The high level outline is the following. We will show that there exist matrices of bounded length measured in Frobenius norm (for general these would be order tensors of length at most ) which additionally satisfy certain “orthogonality” properties; here . We will use the orthogonality properties and the random perturbations to extract enough “independence” across ; this will allow us to conclude that at least one of these inner products is at least in magnitude with probability .

What orthogonality property do we want?

Case . Let us start with . In this case we have a subspace of dimension at least . Here we could just choose the vectors to be an orthonormal basis for , to conclude the lemma, since are independent. However, let’s consider a slightly different construction where are not orthonormal which will allow us to generalize to higher .

Claim 4.7 (for ).

There exists a set of , and a set of distinct indices , for such that for all :

(a) , (b) , (c) for all .

Hence, each of the vectors has a non-negligible component orthogonal to the span of . This will give us sufficient independence across the random variables . Consider the inner products in reverse order i.e., . Let where . First , where is an independent Gaussian due to the rotational invariance of Gaussians. Hence for some absolute constant , from simple Gaussian anti-concentration with probability . Now, let us analyze the event is small, after conditioning on the values of . By construction, , whereas . Hence

Proof of Claim 4.7.

We will construct the vectors iteratively. For the first vector, pick any vector in , and rescale it so that ; let be an index where . For the second vector, consider the restricted subspace . This has dimension ; so we can again pick an arbitrary vector in it and rescale it to get the necessary . We can repeat this until we get vectors (when the restricted subspace becomes empty). ∎

Proof sketch for .

We can use a similar argument to come up with an analogous set of matrices inductively. It will be convenient to identify each of these matrices with an (row,column) index pair . We will also have a total order among all of the index pairs as follows. We first have a ordering among all the valid row indices (say ). Moreover, among all index pairs in the same row (i.e., ), we have a total ordering (note that it could be the case that and , since the orderings for and could be different).

Claim 4.8 (for ).

Given any subspace of dimension , there exists many (row,column) index pairs as outlined above, and a set of associated matrices such that for all :

(a) , (b) ,

(c) for all and for any where .

Further there are at least valid row indices, and each of these indices has index pairs associated with it.

The approach to proving the above claim is broadly similar to that of Claim 4.7. The proof repeatedly treats the vectors in as vectors in and applies Claim 4.7 to extract a valid row with valid column indices, and iterates. We leave the formal proof as Exercise 5.

Once we have Claim 4.8, the argument for Lemma 4.6 is as follows. Firstly, since . Hence, we just need to show that there exists s.t. in magnitude with probability . Consider the vectors obtained by applying just . For each valid row , consider only the corresponding vectors with row index from and set to be the vector with the largest magnitude entry in coordinate . By our argument for we can see that with probability at least , , for some constant . Now by scaling these vectors by at most each, we see that they satisfy Claim 4.7. Hence, using the argument for again, we get Lemma 4.6. Extending this argument to higher is technical, and we skip the details.

4.4 Implications for applications

The smoothed polynomial time guarantees for overcomplete tensor decompositions in turn imply polynomial time smoothed analysis guarantees for several learning problems. In the smoothed analysis model for these parameter estimation problems, the unknown parameters of the model are randomly perturbed to give , and samples are drawn from the model with parameters .

However, as we alluded to earlier, the corresponding tensor decomposition problems that arise, e.g., from Proposition 2.1 and 2.2 do not always fit squarely in the smoothed analysis model in Section 4.1. For example, the random perturbations to the factors may not all be independent. In learning mixtures of spherical Gaussians, the factors of the decomposition are for some appropriate , where is the mean of the th component. In learning hidden Markov models (HMMs), each factor is a sum of appropriate monomials of the form , where correspond to length- paths in a graph.

Fortunately the bounds in Proposition 4.3 can be used to derive similar high confidence lower bounds on the least singular value for random matrices that arise from such applications using decoupling inequalities. For example, one can prove such bounds (as in Proposition 4.3) for the matrix where the th column is (as required for mixtures of spherical Gaussians). Such bounds also hold for other broad classes of random matrices that are useful for other applications like hidden markov models; see [BCPV19] for details.

In the smoothed analysis model for mixtures of spherical Gaussians, the means are randomly perturbed. The following corollary gives polynomial time smoothed analysis guarantees for estimating the means of a mixture of spherical Gaussians. See [BCMV14, ABG+14] for details.

Corollary 4.9 (Mixture of spherical Gaussians in dimensions).

For any , there is an algorithm that in the smoothed analysis setting learns the means of a mixture of spherical Gaussians in dimensions up to accuracy with running time and sample complexity and succeeds with probability at least .

In the smoothed analysis setting for hidden markov models (HMM), the model is generated using a randomly perturbed observation matrix , obtained by adding independent Gaussian random vectors drawn from to each column of . These techniques also give similar smoothed analysis guarantees for learning HMMs in the overcomplete setting when dimensions (using consecutive observations), and under sufficient sparsity of the transition matrix. See [BCPV19] for details. Smoothed analysis results have also been obtained for other problems like overcomplete ICA [GVX14], learning mixtures of general Gaussians [GHK15], other algorithms for higher-order tensor decompositions [MSS16, BCPV19], and recovering assemblies of neurons [ADM+18].

5 Other Algorithms for Tensor Decompositions

The algorithm we have seen (based on simultaneous diagonalization) has provable guarantees in the quite general smoothed analysis setting. However, there are other considerations like running time and noise tolerance, for which the algorithm is sub-optimal – for example, iterative heuristics like alternating least-squares or alternating minimization are more popular in practice because of faster running times [KB09]. There are several other algorithmic approaches for tensor decompositions that work under different conditions on the input. The natural considerations are the generality of the assumptions, and the running time of the algorithm. The other important consideration is the robustness of the algorithm to noise or errors. I will briefly describe a selection of these algorithms, and comment along these axes. As we will discuss in the next section, the different algorithms are incomparable because of different strengths and weaknesses along these three axes.

Tensor Power Method. The tensor power method gives an alternate algorithm for symmetric tensors in the full-rank setting that is inspired by the matrix power method. The algorithm is designed for symmetric tensors with an orthogonal decomposition of rank of the form where the vectors are orthonormal. Note that not all matrices need to have such an orthogonal decomposition. However in many learning applications (where we have access to the second moment matrix), one can use a trick called whitening to reduce to the orthogonal decomposition case by a simple basis transformation.

The main component of the tensor power method is an iterative algorithm to find one term in the decomposition that repeats the following power iteration update (after initializing randomly) until convergence . Here the vector where . The algorithm then removes this component and recurses on the remaining tensor. This method is also known to be robust to inverse polynomial noise, and is known to converge quickly after the whitening. See [AGH+14] for such guarantees.

FOOBI algorithm and variants. In a series of works, Cardoso and others [Car91, DLCC07] devised an algorithm, popularly called the FOOBI algorithm for symmetric decompositions of overcomplete tensors of order and above. At a technical level, the FOOBI algorithm finds rank-one tensors in a linear subspace, by designing a “rank-1 detecting gadget”. Recently, the FOOBI algorithm and generalizations have been shown to be robust to inverse polynomial error in the smoothed analysis setting for order tensors up to rank (see [MSS16, HSS19] for order and [BCPV19] for higher even orders).

Alternating Minimization and Iterative Algorithms. Recently, Anandkumar et al. [AGJ17] analyzed popular iterative heuristics like alternating minimization for overcomplete tensors of order and gave some sufficient conditions for both local convergence and global convergence. Finally, a closely related non-convex problem is that of computing the “spectral norm” i.e., maximizing subject to ; under certain conditions one can show that the global maximizers are exactly the underlying factors. The optimization landscape of this problem for tensors has also been studied recently(see [GM17]). But these results all mainly apply to the case when the factors of the decomposition are randomly chosen, which is much less general than the smoothed analysis setting.

Sum-of-squares algorithms. The sum-of-squares hierarchy (SoS) or the Lasserre hierarchy is a powerful family of algorithms based on semidefinite-programming. Algorithms based on SoS typically consider a related polynomial optimization problem with polynomial inequalities. A key step in these arguments is to give a low-degree sum-of-squares proof of uniqueness; this is then “algorithmicized” using the SoS hierarchy. SoS-based algorithms are known to give guarantees that can go to overcomplete settings even for order tensors (when the factors are random), and are known to have higher noise tolerance. In particular, they can handle order- symmetric tensors of rank , when the factors are drawn randomly from the unit sphere [MSS16]. The SoS hierarchy also gives robust variants of the FOOBI algorithm, and get quasi-polynomial time guarantees under other incomparable conditions [MSS16]. SoS based algorithms are too slow in practice because of large polynomial running times. Some recent works explore an interesting middle-ground; they design spectral algorithms that are inspired by these SoS hierarchies, but have faster running times (see e.g., [HSSS16]).

6 Discussion and Open questions

The different algorithms for tensor decompositions are incomparable because of different strengths and weaknesses. A major advantage of SoS-based algorithms is their significantly better noise tolerance; in some settings it can go up to constant error measured in spectral norm (of an appropriate matrix flattening), while other algorithms can get inverse polynomial error tolerance at best. This is important particularly in learning applications, since there is significant modeling errors in practice. However, many of these results mainly work in restrictive settings where the factors are random (or incoherent). On the other hand, the algorithms based on simultaneous decompositions and variants of the FOOBI algorithm work in the significantly more general smoothed analysis setting, but their error tolerance is much poorer. Finally, iterative heuristics like alternating minimization are the most popular in practice because of their significantly faster running times; however known theoretical guarantees are significantly worse than the other methods.

Another direction where there is a large gap in our understanding is about conditions and limits for efficient recovery. This is particularly interesting under conditions that guarantee that the low-rank decomposition is (robustly) unique, as they imply learning guarantees. We list a few open questions in this space.

For the special case of -tensors in , recall that Jennrich’s algorithm needs the factors to be linearly independent, hence . On the other hand, Kruskal’s uniqueness theorem (and its robust analogue) guarantees uniqueness even up to rank . Kruskal in fact gave a more general sufficient condition for uniqueness in terms of what is known as the Kruskal rank of a set of vectors [Kru77]. But there is no known algorithmic proof!

Open Problem. Is there a (robust) algorithm for decomposing a -tensor under the conditions of Kruskal’s uniqueness theorem?

We also do not know if there is any smoothed polynomial time algorithm that works for rank for any constant . Moreover, we know powerful statements using ideas from algebraic geometry that generic tensors of order have unique decompositions up to rank [CO12]. However, these statements are not robust to even inverse polynomial error. Is there a robust analogue of this statement in a smoothed analysis setting? These questions are also interesting for order tensors. Most known algorithmic results for tensor decompositions also end up recovering the decomposition (thereby proving uniqueness). However, even for order- tensors with random factors, there is a large gap between conditions that guarantee uniqueness vs conditions that ensure tractability.

Open Problem. Is there a (robust) algorithm for decomposing a -tensor with random factors for rank ?

Acknowledgments

I thank Aditya Bhaskara for many discussions related to the chapter, and Tim Roughgarden, Aidao Chen, Rong Ge and Paul Valiant for their comments on a preliminary draft of this chapter.

References

- [ABG+14] Joseph Anderson, Mikhail Belkin, Navin Goyal, Luis Rademacher, and James R. Voss. The more, the merrier: the blessing of dimensionality for learning large Gaussian mixtures. Conference on Learning Theory, 2014.

- [ADM+18] Nima Anari, Constantinos Daskalakis, Wolfgang Maass, Christos Papadimitriou, Amin Saberi, and Santosh Vempala. Smoothed analysis of discrete tensor decomposition and assemblies of neurons. In Advances in Neural Information Processing Systems, 2018.

- [AGH+14] Animashree Anandkumar, Rong Ge, Daniel Hsu, Sham M. Kakade, and Matus Telgarsky. Tensor decompositions for learning latent variable models. Journal of Machine Learning Research, 15, 2014.

- [AGJ17] Animashree Anandkumar, Rong Ge, and Majid Janzamin. Analyzing tensor power method dynamics in overcomplete regime. Journal of Machine Learning Research, 18, 2017.

- [AMR09] Elizabeth S Allman, Catherine Matias, and John A Rhodes. Identifiability of parameters in latent structure models with many observed variables. The Annals of Statistics, 37, 2009.

- [BCMV14] Aditya Bhaskara, Moses Charikar, Ankur Moitra, and Aravindan Vijayaraghavan. Smoothed analysis of tensor decompositions. In Symposium on the Theory of Computing (STOC), 2014.

- [BCPV19] Aditya Bhaskara, Aidao Chen, Aidan Perreault, and Aravindan Vijayaraghavan. Smoothed analysis in unsupervised learning via decoupling. In Foundations of Computer Science (FOCS), 2019.

- [BCV14] Aditya Bhaskara, Moses Charikar, and Aravindan Vijayaraghavan. Uniqueness of tensor decompositions with applications to polynomial identifiability. Conference on Learning Theory, 2014.

- [BS10] Mikhail Belkin and Kaushik Sinha. Polynomial learning of distribution families. In Foundations of Computer Science (FOCS). IEEE, 2010.

- [Car91] J. . Cardoso. Super-symmetric decomposition of the fourth-order cumulant tensor. blind identification of more sources than sensors. In Proceedings of ICASSP’91, 1991.

- [CO12] L. Chiantini and G. Ottaviani. On generic identifiability of 3-tensors of small rank. SIAM Journal on Matrix Analysis and Applications, 33, 2012.

- [DLCC07] L. De Lathauwer, J. Castaing, and J. Cardoso. Fourth-order cumulant-based blind identification of underdetermined mixtures. IEEE Trans. on Signal Processing, 55, 2007.

- [GHK15] Rong Ge, Qingqing Huang, and Sham M. Kakade. Learning mixtures of Gaussians in high dimensions. In Symposium on Theory of Computing, 2015.

- [GM17] Rong Ge and Tengyu Ma. On the optimization landscape of tensor decompositions. In Advances in Neural Information Processing Systems 30. 2017.

- [GVX14] Navin Goyal, Santosh Vempala, and Ying Xiao. Fourier PCA and robust tensor decomposition. In Symposium on Theory of Computing, 2014.

- [Har70] Richard A Harshman. Foundations of the parafac procedure: models and conditions for an explanatory multimodal factor analysis. 1970.

- [Hås90] Johan Håstad. Tensor rank is np-complete. Journal of Algorithms, 11(4), 1990.

- [HK13] Daniel Hsu and Sham M Kakade. Learning mixtures of spherical Gaussians: moment methods and spectral decompositions. In Proceedings of the 4th conference on Innovations in Theoretical Computer Science, 2013.

- [HKZ12] Daniel Hsu, Sham M. Kakade, and Tong Zhang. A spectral algorithm for learning hidden markov models. Journal of Computer and System Sciences, 78(5), 2012.

- [HL13] Christopher J. Hillar and Lek-Heng Lim. Most tensor problems are np-hard. J. ACM, 60, 2013.

- [HSS19] Samuel B. Hopkins, Tselil Schramm, and Jonathan Shi. A robust spectral algorithm for overcomplete tensor decomposition. In Proceedings of the Thirty-Second Conference on Learning Theory, 2019.

- [HSSS16] Samuel B. Hopkins, Tselil Schramm, Jonathan Shi, and David Steurer. Fast spectral algorithms from sum-of-squares proofs: Tensor decomposition and planted sparse vectors. In STOC, 2016.

- [KB09] Tamara G Kolda and Brett W Bader. Tensor decompositions and applications. SIAM review, 51(3), 2009.

- [Kru77] Joseph B Kruskal. Three-way arrays: rank and uniqueness of trilinear decompositions, with application to arithmetic complexity and statistics. Linear algebra and its applications, 18(2), 1977.

- [Moi18] Ankur Moitra. Algorithmic Aspects of Machine Learning. Cambridge University Press, 2018.

- [MR06] Elchanan Mossel and Sébastien Roch. Learning nonsingular phylogenies and hidden markov models. The Annals of Applied Probability, 2006.

- [MSS16] Tengyu Ma, Jonathan Shi, and David Steurer. Polynomial-time tensor decompositions with sum-of-squares. In IEEE Symposium on the Foundations of Computer Science, 2016.

- [MV10] Ankur Moitra and Gregory Valiant. Settling the polynomial learnability of mixtures of Gaussians. In Foundations of Computer Science (FOCS), 2010.

- [Rou20] Tim Roughgarden. Beyond the Worst-Case Analysis of Algorithms. Cambridge University Press, 2020.

- [SS90] G. W. Stewart and Ji-guang Sun. Matrix Perturbation Theory. Academic Press, 1990.

- [SWZ19] Zhao Song, David P. Woodruff, and Peilin Zhong. Relative error tensor low rank approximation. In Symposium on Discrete Algorithms (SODA), 2019.

- [TD18] Christopher Tosh and Sanjoy Dasgupta. Maximum likelihood estimation for mixtures of spherical gaussians is np-hard. Journal of Machine Learning Research, 18, 2018.

7 Exercises

-

1.

The symmetric rank of a symmetric tensor is the smallest integer s.t., can be expressed as for some . Prove that for any symmetric tensor of order , the symmetric rank is at most times the rank of the tensor555Comon’s conjecture asks if for every symmetric tensor, the symmetric rank is equal to the rank. A counterexample was shown recently by Shitov. It is open what the best gap between these two ranks can be as a function of .. Hint: For , if was a term in the decomposition, we can express .

-

2.

Let be two orthonormal vectors, and consider the tensor . Prove that it has rank . Also prove that it can be arbitrarily well approximated by a rank tensor.

Hint: Try to express as a difference of two symmetric rank one tensors with large entries (Frobenius norm of ), so that the error term is . -

3.

Construct an example of a matrix such that the Kruskal-rank of is at most twice the Kruskal-rank of . Hint: Express the identity matrix as for two different orthonormal basis.

-

4.

Prove Proposition 2.2.

- 5.