MS-MKG-20-03054 \TITLETargeting for long-term outcomes

Jeremy Yang \AFFHarvard Business School, \EMAILjeryang@hbs.edu \AUTHORDean Eckles \AFFMassachusetts Institute of Technology, \EMAILeckles@mit.edu \AUTHORParamveer Dhillon \AFFUniversity of Michigan, \EMAILdhillonp@umich.edu \AUTHORSinan Aral \AFFMassachusetts Institute of Technology, \EMAILsinan@mit.edu

Decision makers often want to target interventions so as to maximize an outcome that is observed only in the long-term. This typically requires delaying decisions until the outcome is observed or relying on simple short-term proxies for the long-term outcome. Here we build on the statistical surrogacy and policy learning literatures to impute the missing long-term outcomes and then approximate the optimal targeting policy on the imputed outcomes via a doubly-robust approach. We first show that conditions for the validity of average treatment effect estimation with imputed outcomes are also sufficient for valid policy evaluation and optimization; furthermore, these conditions can be somewhat relaxed for policy optimization. We apply our approach in two large-scale proactive churn management experiments at The Boston Globe by targeting optimal discounts to its digital subscribers with the aim of maximizing long-term revenue. Using the first experiment, we evaluate this approach empirically by comparing the policy learned using imputed outcomes with a policy learned on the ground-truth, long-term outcomes. The performance of these two policies is statistically indistinguishable, and we rule out large losses from relying on surrogates. Our approach also outperforms a policy learned on short-term proxies for the long-term outcome. In a second field experiment, we implement the optimal targeting policy with additional randomized exploration, which allows us to update the optimal policy for future subscribers. Over three years, our approach had a net-positive revenue impact in the range of $4-5 million compared to the status quo.

long-term effect, statistical surrogate, policy learning, targeting, proactive churn management \HISTORYFirst version: October 2020. This version: February 2022.

1 Introduction

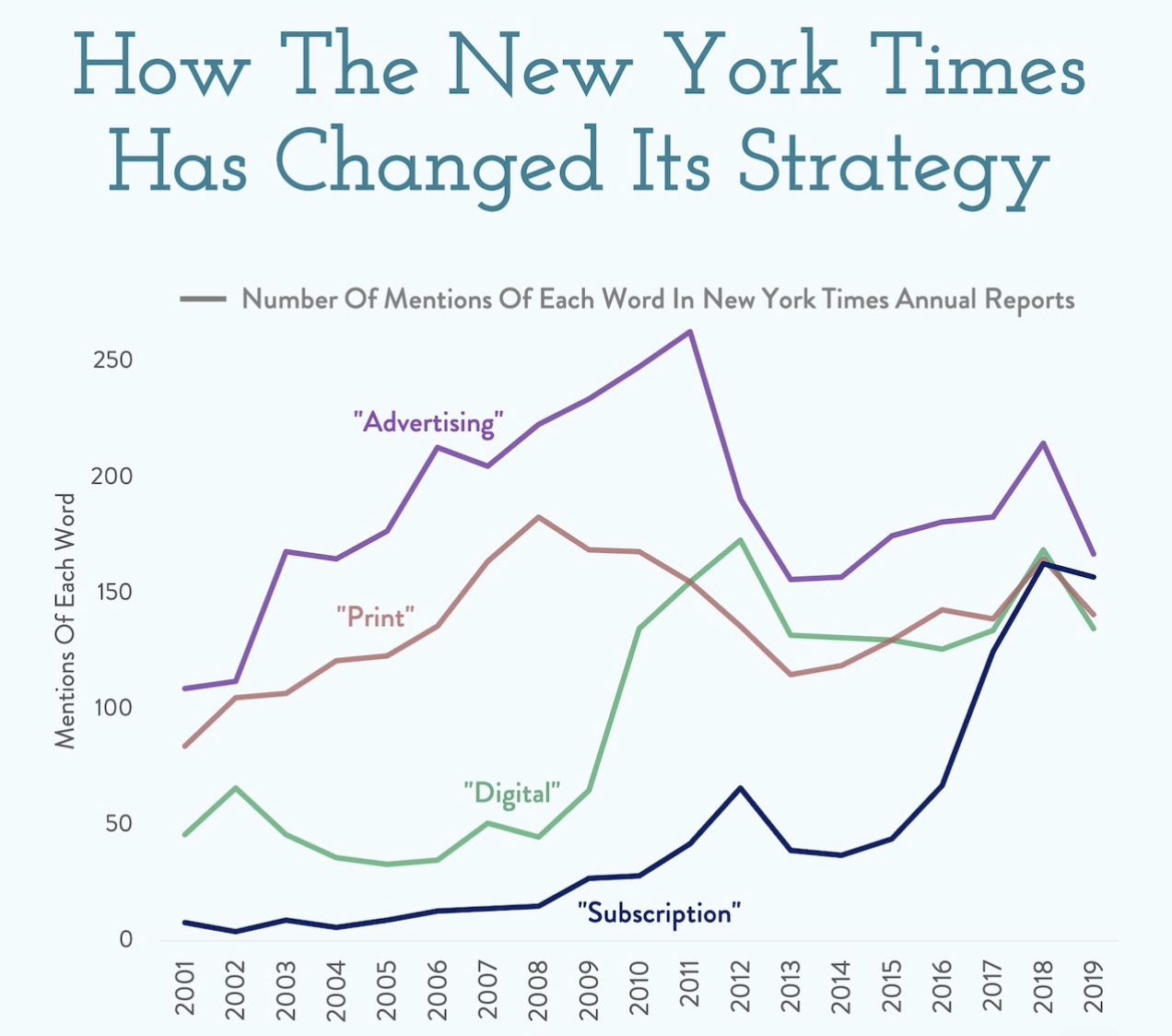

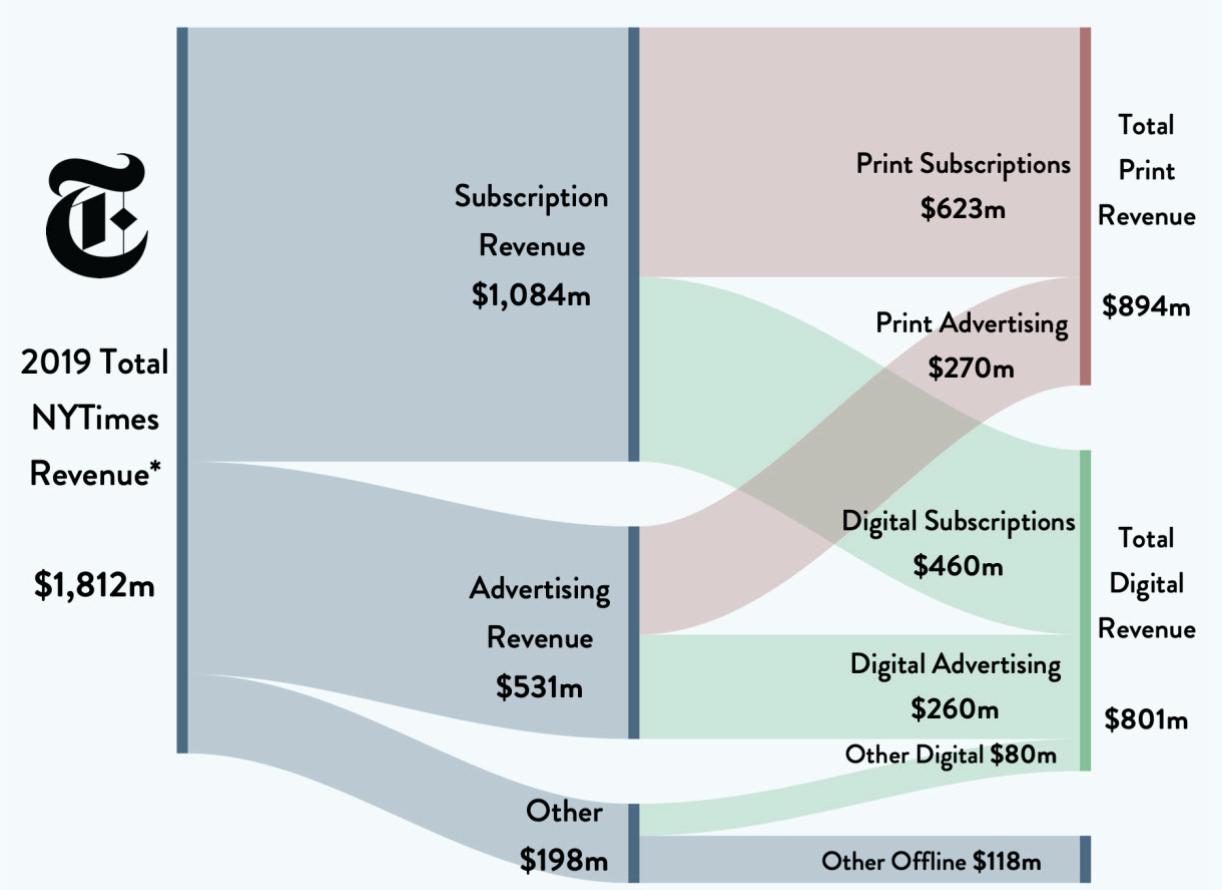

Advertising revenues have been stagnating for newspapers in recent years.111The print advertising revenue is declining with a compound annual growth rate (CAGR) of -12.6% from 2016-2021, while digital ads revenue is still growing at a CAGR of 2.2%, it’s not enough to compensate for the loss in print. Source: US Online and Traditional Media Advertising Outlook As a consequence, newspapers are looking for ways to strengthen their subscription-based business model. Take The New York Times as an example: in 2019, their total subscription revenue was twice their total advertising revenue (Figure A.1, A.2). Their CEO recently said: “ we still regard advertising as an important revenue stream, but we believe that our focus on establishing close and enduring relationships with paying, deeply engaged subscribers, and the long-range revenues which flow from those relationships, is the best way of building a successful and sustainable news business”.222Source: https://www.nytimes.com/2018/02/08/business/new-york-times-company-earnings.html Hence, to succeed in a subscription-based business model, news publishers must retain their existing subscribers and maximize their long-term values. A common approach to achieving this goal is to target existing subscribers with marketing interventions, such as price discounts or other personalized offers.

We use news publishers as a motivating example, and it matches our empirical application. But how to optimize long-term customer outcomes by targeting interventions is a problem faced by most firms. Even more generally, decision makers in education, government, and medicine typically care about intervening for long-term outcomes such as employment, income, and survival.

“Long-term” and “short-term” outcomes are fruitfully understood as defined relative to the targeting cycle. For example, if a firm runs a campaign every year, then all outcomes that are observed within a year, such as their one-year revenue, might be considered “short-term” because these outcomes are observed before the firm takes action (decides whom to target with what) in their next campaign. Hence, future policies can be optimized on these observed outcomes. In contrast, “long-term” outcomes materialize over time horizons longer than the window of opportunity for action, for example, three-year or five-year revenue, rendering the firm incapable of optimizing their next campaign based on them. So, a natural question arises: How can firms learn and implement an optimal targeting policy when the primary outcome of interest is “long-term”?

A straightforward solution to this problem is to wait until the long-term outcome materializes and choose a policy based on the realized long-term outcome. But this implies that the firm can not learn anything in the meantime, and therefore is unable to implement updated targeting policies until years later. Another solution is to find a short-term proxy (e.g., short-term revenue) for the long-term outcome and optimize for it instead. However, this could be problematic as the proxy and the long-term outcome might not be well aligned. Hence, a policy that performs well on the proxy might not perform well in the long-run.

In this paper we propose to use surrogates (Prentice 1989, VanderWeele 2013) to impute the missing long-term outcomes and use the imputed long-term outcomes to optimize a targeting policy. We estimate the missing long-term outcome as the expectation of the long-term outcome conditional on surrogates of that outcome in a historical dataset in which the long-term outcome was observed. Surrogate index estimators combine multiple surrogates by estimating the conditional expectation of the long-term outcome given the surrogates and using this to impute long-term outcomes (Xu and Zeger 2001, Athey et al. 2019). Once we have the imputed long-term outcomes, we optimize the targeting policy efficiently by using a doubly-robust approach (Dudík et al. 2014, Athey and Wager 2020, Zhou et al. 2018) on the imputed long-term outcomes. We prove this surrogate-index-based approach recovers the optimal policy learned on true long-term outcomes under certain assumptions. We implement the optimal policy via bootstrapped Thompson sampling (Eckles and Kaptein 2014, Osband et al. 2016) to maintain exploration so we can update and re-optimize the policy for future subscribers to allow for potential non-stationarity.

We evaluate the efficacy of our approach empirically by running two large-scale field experiments that target discounts to the digital subscribers of The Boston Globe, a regional leader in news media. Boston Globe Media, which operates The Boston Globe newspaper and associated websites, is facing a similar problem to many other publishers. Our goal is to learn an optimal targeting policy that treats some subscribers with certain discounts to maximize their retention and long-term revenue. Here a policy is a mapping from subscriber characteristics to offering a specific discount (or no discount, or a distribution over discounts when the policy is stochastic). In this subscriber retention context, this is also known as proactive churn management.333Here proactive simply means that the intervention (discount) happens before a churn intention is observed; by contrast, reactive churn management means that the company first waits for customers to request to cancel their subscription then offers some discount or other benefits in reaction to this in the hope of retaining them. One analogy is that the proactive approach is like diagnosing and preventing illness before a patient shows clear symptoms, and the reactive approach is like treating patients who are already ill. To construct the surrogate index, we use the observed revenue and content consumption in the 6 months after treatment as our surrogates. We compare how well the policies learned using surrogate index perform against policies optimized directly on short-term proxies (a benchmark) or realized long-term outcomes (the ground truth). We also consider alternative selections of surrogates for the construction of surrogate index — perhaps most importantly whether we can use less than 6 months of revenue and consumption data. We estimate that this approach increases the firm’s total projected digital subscription revenue by $4–5 million over a three-year period relative to the status quo in the two experiments.

The rest of the paper is organized as follows. In Section 2 we review related work. The empirical context is described in Section 3. We introduce our method in Section 4: We first explain the imputation of the long-term outcome using the surrogate index and prove sufficient conditions for it to be valid for policy evaluation and optimization, then we describe the policy learning framework and how it is implemented. Experimental results and empirical validation of our approach are reported in Section 5. We conclude in Section 6.

2 Related Work

Our paper builds on a large body of literature in biostatistics and medicine on surrogate outcomes (i.e., endpoints, biomarkers); see, e.g., Joffe and Greene (2009) and Weir and Walley (2006) for reviews. In clinical trials the goal is often to study the efficacy of an intervention on outcomes such as the long-term health or survival rate of patients. However, the primary outcome of interest might be very rare, only observed after years of delay, or have high variance compared with the treatment effects (e.g., a 5 or 10-year survival rate). It is common to use the effect of an intervention on surrogate outcomes as a proxy for its effect on long-term outcomes. In a seminal paper, Prentice (1989) argued that to be a valid surrogate, treatment and outcome have to be independent conditional on the surrogate. One intuitive way for this condition to be satisfied is if the surrogate fully mediates the treatment effect. In practice it is hard to find a single variable that plausibly satisfies the condition (Freedman et al. 1992), but Xu and Zeger (2001) showed that combining multiple surrogates to predict the outcome can be preferable to using a single surrogate because the treatment effect may operate through multiple pathways and, even when there is a single pathway, using multiple surrogates can reduce measurement error. This idea is further developed in a recent paper in econometrics (Athey et al. 2019), where the combination is referred to as a surrogate index. This literature focuses on using surrogates to identify treatment effects on long-term outcomes and, in this paper, we extend this to targeting policy optimization.

Another popular approach to modeling long-term outcomes is to posit a particular parametric generative model for the long-term outcomes. In the context of marketing, this is typically a model of customer lifetime value (CLV or LTV). CLV models are widely used in marketing for customer segmentation and targeting; see, for example, Gupta et al. (2006), Fader et al. (2014), Fader and Hardie (2015), and Ascarza et al. (2017) for surveys. CLV is defined as the sum of discounted future revenues or profits from a customer. To calculate CLV we typically need to posit a parametric, e.g., survival function and extrapolate the survival or retention probability into the future. A recent example in the context of churn management is Godinho de Matos et al. (2018), where a parametric survival function is used. One advantage of this approach is that we can apply it even when the long-term outcomes are never observed because the prediction is based on functional form assumptions, unlike the surrogate index approach which needs access to long-term outcomes in a historical dataset; on the other hand, standard parametric CLV approachs may suffer from model misspecification. Also, the primary goal of CLV models is typically to predict outcomes, whereas the surrogate index approach focuses on learning treatment effects or optimizing policies, imputing outcomes is just a means to an end; more importantly, outcomes imputed via surrogate index have provable properties regarding treatment effect estimation (Athey et al. 2019) or policy learning, as developed here. Furthermore, building a CLV model may require substantial work to formalize business logic in anything but the simplest subscription businesses. A synthesis of these approaches is also possible in that a CLV prediction, if already available, can also be used as one of the surrogates in the construction of a surrogate index.

This paper is also related to the literature on targeting policy evaluation and optimization, which has recently further developed within marketing research. Hitsch and Misra (2018) proposed an estimation method for conditional average treatment effects (CATEs) based on k-nearest neighbors (kNN) and used it for policy optimization. Simester et al. (2019a) showed that we can compare targeting policies more efficiently if we only compare the outcome of units on whom the policies prescribe different actions. Simester et al. (2019b) documented non-stationarity such as covariate and concept shifts between two experiments and evaluated how robust different machine learning models used to optimize policies are to these changes in the environment. Yoganarasimhan et al. (2020) used different machine learning models to estimate CATEs and evaluated how targeting policies constructed using these models perform against each other. In another recent work, Lemmens and Gupta (2020) examine using a CLV model combined with field experimentation to optimize targeting in the policy learning framework.

Our work complements this literature by developing an approach that is novel in a few ways. First, we focus directly on targeting for long-term outcomes; outcomes used in these other works are short-term (in the sense that they are observable when we optimize and implement the policy) or extrapolation is done using a parametric CLV model.444Yoganarasimhan et al. (2020) showed in their particular case the policy learned on short-term outcome also does well on long-term outcomes, but the policy is not directly optimized on long-term outcome. Second, we systematically add randomized exploration around the learned policy, which allows us to evaluate and update the policy for future units in case the environment changes. Hitsch and Misra (2018) and Yoganarasimhan et al. (2020) studied the problem in a static setting. Simester et al. (2019b) did look at changes in the environment but they focused on evaluating the robustness of different machine learning models. Third, we use a doubly-robust (DR) approach (Dudík et al. 2014) for both policy evaluation and learning in contrast to Hitsch and Misra (2018) and Yoganarasimhan et al. (2020) who used an inverse probability weighting (IPW) estimator for policy evaluation. Lemmens and Gupta (2020) introduce a specialized incremental profit based loss function that performs well in their empirical evaluation, but lacks the asymptotic efficiency results available for doubly-robust policy learning; it is also unclear how to combine this with known probabilities of treatment (i.e., design-based propensity scores) that arise in sophisticated experiments. In particular, even when probabilities of treatment are known exactly (as in our setting), DR estimators have advantages in statistical efficiency compared with IPW estimators (Athey and Wager 2020, Zhou et al. 2018).

Substantively, our study adds to the literature on subscriber management and proactive churn management in particular. Earlier work focused on developing better prediction algorithms to more accurately identify potential churners; Neslin et al. (2006) provides a detailed comparison of different churn prediction models. Recently, the literature has examined causal effects of targeting interventions on churn using field experiments. For example, Ascarza (2018) and Lemmens and Gupta (2020) note that firms should not target customers based on their outcome level (churn risk) but should target based on treatment effects. Ascarza et al. (2016) showed evidence from a field experiment with a telecommunication company that proactive churn interventions can backfire and increase the churn rate in practice. They argued that this is because proactive intervention lowers customers’ inertia to switch plans and increases the salience of past-usage patterns among potential churners. Our paper contributes to this literature by proposing an experimental framework that can be applied to directly optimize targeting policies for long-term customer retention and revenues.

3 Empirical Context

Founded in 1872, The Boston Globe is the oldest and largest daily newspaper in the greater Boston area. It has won a total of 26 Pulitzer Prizes and is widely regarded as one of the most prestigious papers in the US. We ran two targeting experiments on all digital only555The Globe also has a combined print and digital subscription. All subscribers are paying customers. subscribers of The Boston Globe in two experiments. While we return to the details of our experiments and analyses in Section 5, we introduce the empirical context here so as to help fix ideas as we describe the methods.

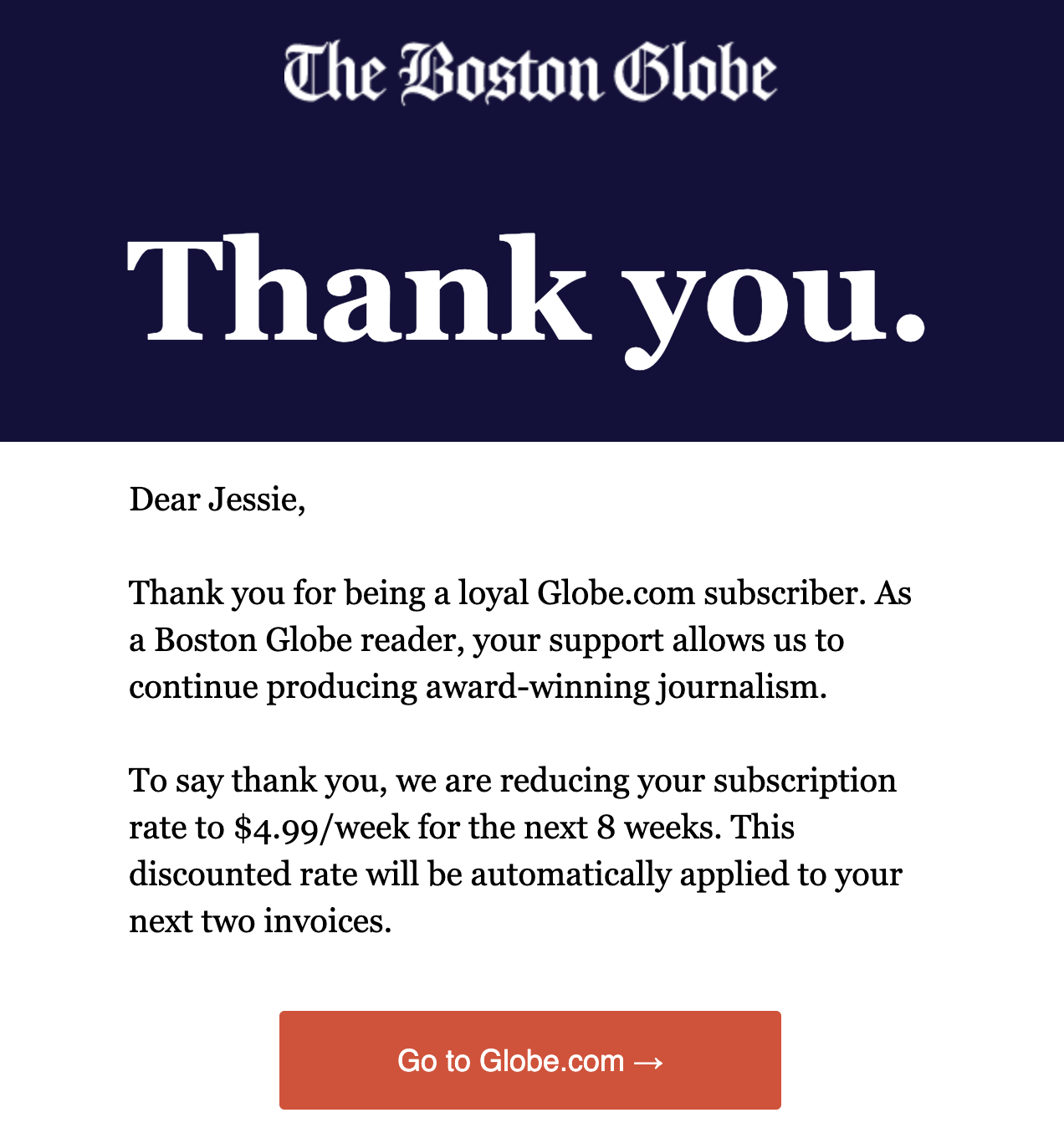

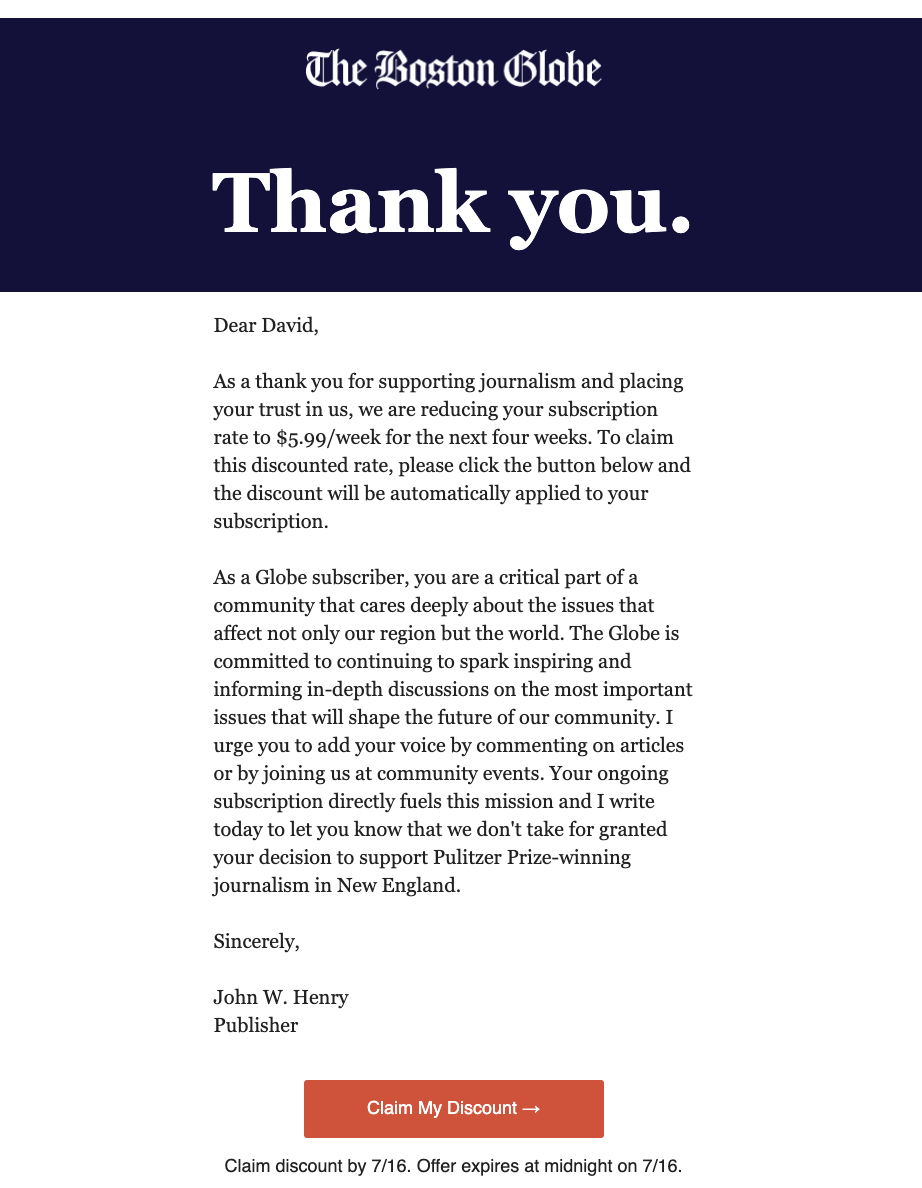

Our analysis is of a random sample of about 45,000 digital subscribers in the first experiment and 95,000 in the second. For each subscriber we observed the short-term outcome (e.g., monthly churn and revenue) and three sets of features: demographics (e.g., zip code), account activities (e.g., billing address change, credit card expiration date, complaints), and content consumption (e.g., when and what articles they read). There was only one intervention in the first experiment, which lowered the price for treated subscribers from $6.93 per week to $4.99 per week for 8 weeks. An email (Figure 1(a)) was sent to all treated subscribers in August 2018 telling them that a discount had been automatically applied to their accounts. We implemented 6 interventions in the second experiment: a thank you email, a $20 gift card, a discount to $5.99 for 8 weeks, a discount to $5.99 for 4 weeks, a discount to $4.99 for 8 weeks (the same as the intervention in the first experiment), and a discount to $3.99 for 8 weeks. A similar email (Figure 1(b)) was sent to all treated subscribers in July 2019 with the corresponding message, and a treated subscriber had to click on a button at the bottom of the email to redeem the benefit. There was no overlap of treated subscribers between the two experiments.

4 Methods

In our application, the primary outcome of interest is long-term subscriber retention or revenue666Being a digital service, marginal costs are negligible compared with subscription revenue., but we do not observe these outcomes in the short-term, i.e., after the intervention in the first experiment and before we implemented the learned policy for the second experiment of customers. Hence, we use a surrogate index to address this problem.

Our framework has two components: First, we fit a model for long-term outcomes and use the resulting surrogate index to impute long-term outcomes; second, we learn an optimal policy using the imputed long-term outcomes. In Section 4.1 we explain the imputation and prove sufficient conditions for it to be valid for policy evaluation and optimization. In Section 4.2 we describe the policy evaluation and optimization framework and how it is implemented.

We first introduce the notation that we use throughout the section: Let be a targeting policy that maps from the space of unit characteristics to a space of distributions (simplex) over a set of discrete actions ; we index actions by , where 0 is control and others are different interventions. When the policy is non-deterministic, it defines a non-degenerate probability distribution over possible actions conditional on covariates . When it is deterministic, it maps to a fixed action with probability 1. Depending on the action chosen, we observe the corresponding potential outcome, i.e., . These potential outcomes may be correlated with unit characteristics .

The goal is to learn a policy that maximizes some average outcome (if the goal is to minimize some average outcome , we can add a negative sign and turn it into a maximization problem).

Definition 1

A Policy and its Value

| (1) | |||

| (2) |

Definition 2

Optimal Policy

| (3) |

4.1 Imputing a Long-term Outcome with a Surrogate Index

We use intermediate outcomes that are observed over the short-term period following the intervention as surrogates. Intuitively, the idea is to select surrogates that capture some of the ways that the actions affect the long-term outcome; in our application, these are subscriber’s content consumption and short-term revenue. These surrogate variables are then combined with the long-term outcomes in the historical dataset to impute missing long-term outcomes for units in the experiment.

Assume we have two datasets, one from the experiment labeled and one based on historical (observational) data labeled . We observe draws of the tuple in the experiment where represents units’ baseline characteristics, is the action (i.e., treatments, interventions), and is the potentially vector valued set of intermediate outcomes or surrogates. Note that the long-term outcome is unobserved in the experiment. In the historical dataset, we observe draws of the tuple ; note that is no known, randomized intervention in this dataset (i.e., it is observational), but the long-term outcome is observed. We can define a surrogate index for the long-term outcome as the expectation of the long-term outcome conditional on unit covariates and surrogates in the historical dataset :777One advantage of this approach is that the estimation of the conditional expectation can be treated as a supervised learning problem and can be performed using flexible non-parametric machine learning methods like XGBoost (Chen et al. 2015).

Definition 3

Surrogate Index

| (4) |

Under Assumptions 1–3 stated below, a central result in Athey et al. (2019) is that the average treatment effect (ATE) on recovers the ATE on long-term outcome . That is, by constructing the surrogate index we can identify and feasibly estimate the ATE on some long-term outcomes without having to wait until they are observed.

Assumption 1

Regular treatment assignment mechanism (Ignorability and Positivity): The treatment assignment is conditionally independent of potential long-term outcomes (Ignorability) and all units have positive probability of being assigned to each action (Positivity) in the experimental dataset.

| (5) | |||

| (6) |

Assumption 1 is satisfied when we have indeed conducted a randomized experiment, even if the probability of assignment to actions is conditional on observed covariates, as in our application.

Assumption 2

Surrogacy: The treatment assignment is independent of long-term outcomes conditional on the surrogates in the experimental dataset.

| (7) |

While there can be other ways to satisfy this assumption, surrogacy is perhaps most intuitively implied by a generative model in which the set of surrogates fully mediate the causal effects from treatment to the long-term outcome (cf. Lauritzen 2004), as depicted in Figure 1(a) if the to edge is absent. In our empirical context, it means the effects of price discounts on long-term retention and revenue should occur via some intermediate outcomes we observe, e.g., content consumption and short-term revenue. While it may have some testable implications, Assumption 2 is not directly testable.888This can also be described as an exclusion restriction, as in instrumental variables. Like that case this assumption has both testable and untestable implications. It might be tempting to regress the outcome on surrogate and treatment and test if the coefficient of treatment is zero. This naive test is not valid when there are unobserved confounders for the surrogate and outcome: conditioning on the surrogate or a “collider” in such a case will generate spurious correlation between treatment and confounder, and hence between treatment and outcome. See Joffe and Greene (2009) for a more detailed discussion. Surrogacy is more plausible if we have a rich set of surrogates; perhaps this is more widely available given the increasing digitization of, e.g, commerce and media consumption (as in our application).

Assumption 3

Comparability: The distribution of the long-term outcome conditional on the covariates and surrogates is the same across the experimental and historical datasets.

| (8) |

In our case, this assumption implies that the distribution of long-term retention and revenue (conditional on content consumption and short-term retention and revenue) should be the same between the experimental and historical datasets. Note that under comparability assumption we have:

| (9) |

In other words, the conditional expectation of in the experimental dataset is equal to the conditional expectation in the historical dataset, which is a quantity we can compute because in the historical dataset is observed. This assumption would fail if the distribution of long-term outcome conditional on covariates and surrogates are changing between the experimental and historical datasets. For instance, if the intervention itself modifies the relationship between long-term outcome and surrogates, the two distributions will be different. For example, in our empirical setting, it may be that, in the absence of an intervention, only very dedicated (i.e. high retention rate) subscribers read some categories of content; however, some actions might induce other, less dedicated subscribers to read that content. For this reason, having similar (even unobserved) interventions in the historical data could strengthen our confidence in this assumption. More extreme violations of this assumption can occur when measurement of a surrogate is changing (e.g., what counts as reading an article has a different definition in historical data). Note that, while not put in potential outcomes notion here or in Athey et al. (2019), one way for comparability to be satisfied involves observational causal inference about effects of on using the historical data to succeed; thus, we expect that, as in observational causal inference, this is a very strong assumption that is often not exactly true. This motivates our consideration of weaker assumptions and the use of empirical evaluation in our application.

Given these assumptions, we prove that the surrogate index is valid for policy evaluation and optimization. Policy evaluation is the estimation of for a given policy . Policy optimization is finding a that maximizes . See Section 4.2 for more details about doing so in finite samples; here we simply consider the optimal policy defined on the population. We show that the value of a policy with respect to surrogate index is identical to its value on the long-term outcome; this in turn implies that the optimal policy with respect to the surrogate index coincides with that optimal policy with respect to long-term outcomes. We state the main results here and the proofs are in Appendix C. Let denote the value of with respect to rather than .

Proposition 1

Under Assumption 1-3, policy evaluation conducted on surrogate index identifies the true policy value defined on long-term outcomes.

| (10) |

Then, since the function being maximized is identical at all points, it is also identical at its maximum.

Proposition 2

Under Assumption 1-3, policy optimization conducted on surrogate index recovers the true optimal policy.

| (11) |

Proposition 10 and 11 are analytical results that could justify the approach developed here and employed in our empirical application. However, somewhat weaker assumptions than have been used for results for estimation of the ATE or CATEs are in fact sufficient for Proposition 11.

Define real and surrogate-index-imputed CATEs, and . When, e.g., Assumption 2 is violated (perhaps the set of surrogates does not fully mediate the treatment effect on long-term outcomes), the CATE estimated using surrogate index can be biased (even with infinite data). That is, for some . Here our aim is not estimating CATEs, but simply optimizing the policy. Bias in CATEs (i.e. non-zero ) does not result in a loss in the value of the optimized policy unless the bias changes the sign of that CATE.999Concern with getting the sign of the treatment effect correct using surrogates has featured prominently in the literature on the “surrogate paradox”, in which various surrogacy definitions are satisfied by the effect on the surrogate and outcome have opposite signs; see, e.g., Chen et al. (2007), VanderWeele (2013), Jiang et al. (2016).

Thus, we can introduce a somewhat weaker assumption, replacing Assumptions 2 and 3, that is sufficient for policy optimization. The intuition that sign preservation is sufficient is that, for policy optimization purposes, we only care about identifying which is the best action for each unit, not how much better it is (i.e., we just need to correctly order the actions with respect to treatment effects, the magnitude of differences between actions do not matter).

Assumption 4

Sign Preservation: The sign of conditional average treatment effects is the same for the surrogate index and the long-term outcome.

| (12) |

This is an assumption directly on CATEs, and so is not as readily interpretable with respect to the data-generating process. Nonetheless, we can reason about how this assumption may be more plausible in some settings than others. For example, in cases with a binary treatment, if we hypothesize that a treatment “works” (i.e., has a large positive effect) on some groups but not others, and this treatment has some small cost (which is incorporated into the definition of ), then the distribution of CATEs may be bi-modal with no density near zero. This could contrast with other cases where theory might lead us to expect highly heterogeneous benefits and costs of the treatment (both incorporated into the definition of ). For example, in our empirical application, for subscribers whose behavior is unaffected by a discount, this will reduce long-term revenue to varying degrees depending on how long they are retained; similarly, for those affected, this may affect long-run revenue in complex, heterogeneous ways. This highlights the value of empirical validation of surrogate-index-based policy optimization in our setting (Section 5.3). Even in the favorable case where the distribution of CATEs is bi-modal with no density near zero, analysis with an impoverished set of covariates may result in loss. Say these available covariates are less informative about treatment effects; then the distribution of CATEs might have substantial mass near zero, raising the concern that any bias in CATE estimation may translate to selecting a sub-optimal policy when using a surrogate index.

One can analytically characterize the loss in policy optimization, much as Athey et al. (2019) develop bounds on the bias for the ATE. Here we state this result, with details in Appendix C.

Proposition 3

There is a loss in the value of optimal policy only when the optimal action estimated on surrogate index is different than the true optimal action. The total loss, or regret, is:

| (13) |

| (14) |

| (15) |

In summary, assumptions introduced in the surrogacy literature can be used to justify policy evaluation and optimization with a surrogate index. Furthermore, it is possible to relax these assumptions for policy optimization precisely because the optimal policy is only sensitive to the sign of treatment effects.

4.2 Evaluating, Learning, and Implementing Targeting Policies

We describe the off-policy evaluation and learning framework using the imputed long-term outcome obtained via the procedure in Section 4.1.101010In an abuse of notation, we now use (rather than, e.g., ) to denote the actually imputed long-term outcome, which is estimated, while in Definition 3 it denoted the true conditional expectation, as otherwise this makes some further expressions cumbersome. Under assumptions articulated in the previous section, this can identify the same optimal policy as using the true long-term outcome . We use on variables or functions with parameters constructed with . We will describe each term generically but also make some connections to the quantities in our experiments. Readers familiar with counterfactual policy evaluation and learning may choose to skip to Section 5 where we discuss the experiments and results.

4.2.1 Off-policy Evaluation

In off-policy evaluation we use data collected under the design (or behavior) policy111111In the reinforcement learning literature (e.g., Sutton and Barto 2018), the policy used to collect training data is called a behavior policy. We call it a design policy in our experimental setting. to estimate the value of a counterfactual policy . One popular choice of estimator is based on inverse probability weighting (IPW). The Hájek estimator, a normalized version of the Horvitz–Thompson estimator (Horvitz and Thompson 1952), is typically used to implement IPW (Särndal et al. 1992). The Hájek estimate of the average outcome under an arbitrary targeting policy using data collected under a design or behavior policy is:

| (16) |

where is the imputed outcome (e.g., predicted 3-year revenue), is the action (e.g., discount) received by unit assigned by the design policy , and is the probability of assigning unit to a given condition under the counterfactual policy that we want to evaluate.121212The corresponding unnormalized Horvitz–Thompson estimator is: We will use to denote the control and to denote the treatment when actions are binary.131313For example, when it means unit was in treatment and she was assigned to treatment with probability , and is the probability that receives treatment under counterfactual policy . Similarly, when it means unit was in the control and she was assigned to control with probability , and is the probability that will be in control (or not be treated) under counterfactual policy . The first term in Equation 16 is simply a normalization term; the ratio between and is also known as the importance weight. As specified by Assumption 18, we need to be strictly positive for all unit–action pairs. Note that we do not require the policy being evaluated to have this property; it can be a deterministic policy. The Horvitz–Thompson estimator is unbiased but typically has higher variance. The Hájek estimator is biased in finite samples but consistent, and it typically has lower variance; it is therefore more widely used in practice.141414For more discussion about of normalization in IPW estimation, see Owen (2019, ch. 9) and Khan and Ugander (2021). The main advantage of IPW is that it is fully non-parametric when the propensity scores are known and it does not require us to specify a model for the outcome process.

However, the IPW estimator has two main limitations: First, the Hájek estimator can still suffer from high variance. Second, when evaluating a deterministic policy , it only uses observations for which the actions prescribed by the target policy and design policy agree (when they don’t agree is always zero). This reduces the effective sample size, especially when and are very different.151515Two policies are similar if they tend to prescribe the same action for a given unit profile, the more often they prescribe different actions for a given unit, the more different they are. Following Robins et al. (1994), one way to improve upon IPW is by augmenting it with an outcome model to use all observations and further stabilize the estimator. This is known as the augmented inverse probability weighted (AIPW) or doubly-robust (DR) estimator (Dudík et al. 2014). Under the DR approach, the value of a policy can be estimated as:

| (17) |

where

| (18) |

The first term in Equation 17, , is an outcome model that estimates the expectation of the imputed outcome for a random covariates profile and distribution of actions given by a policy using data from the experiment. (In the most common case of evaluating a deterministic policy, is just for the action to which assigns units with covariate profile .) For example, in our empirical application, it corresponds to the estimated 3-year revenue for a subscriber profile under a particular discount . Note that this outcome model is different from the one for in Equation 9; there the outcome is estimated as a function of surrogates and covariates using historical data, whereas estimates outcome as a function of actions and covariates using the experimental data. The second term is the importance weight multiplied by the prediction error; it corrects the first term towards the direction of the long-term outcome by an amount that is proportional to the prediction error. For a deterministic target policy it does so whenever the actions prescribed by and agree. Note that the high variance of IPW estimators is from the importance weights (dividing by a small probability when is very unbalanced), this term vanishes if the prediction error is small. Both IPW and DR estimators are consistent, but DR estimation can achieve semiparametric efficiency (see, e.g., Robins et al. 1994, Hahn 1998, Farrell 2015), and typically has lower variance. We use the DR estimator for policy evaluation.

4.2.2 Off-policy Optimization

As shown in the previous section, policy optimization builds on CATE estimation. We focus on using doubly-robust estimation.161616Estimation of CATE can also be implemented in different ways. Hitsch and Misra (2018) distinguish between what they label “indirect” approaches (which first estimate the outcome model as a function of covariates and actions and then take the difference between actions as treatment effects) and “direct” methods estimate the CATE directly without first estimating an outcome function (e.g., causal trees (Athey and Imbens 2016)), causal forest (Wager and Athey 2018) and causal kNN (Hitsch and Misra 2018)). This typology may be confusing to readers familiar with contextual bandit and policy learning literatures where, at least since Dudík et al. (2014), “direct methods” are those using outcome regressions without IPW (i.e. what Hitsch and Misra (2018) label “indirect”). We can first construct a doubly-robust score for each unit–action pair (which also has the interpretation of an estimate of an individual potential outcome) (Robins et al. 1994, Chernozhukov et al. 2016, Dudík et al. 2014, Athey and Wager 2020, Zhou et al. 2018):

| (19) |

These doubly-robust scores are equal to the prediction of an outcome model plus a correction term based on IPW; the correction is applied if and only if the action being evaluated is the same as the action taken. This is intuitive because the correction term depends on , which is the outcome under a realized action ; it is informative only when the action being evaluated is the same as , otherwise the term drops out and the doubly-robust scores reduce to the outcome model. The CATE, relative to the control, given a covariate profile can then be estimated as:

| (20) |

We can use these doubly-robust scores for policy optimization (Murphy et al. 2001, Dudík et al. 2014) by solving a cost-sensitive classification problem.171717When must be estimated, this approach comes with guarantees on asymptotic regret compared with the true optimal policy (Athey and Wager 2020, Zhou et al. 2018). That is, the estimated optimal policy is:

| (21) |

or, in multi-action case:

| (22) |

where is a vector of doubly-robust scores based on Equation 19 and is a vector of probabilities with which the policy assigns a unit to each action. is the dot product between vector valued and .

In the cost-sensitive classification problem, for each unit, the correct label is the action that corresponds to the highest doubly-robust score, and the loss for classifying a unit to action a, when the correct label is , is , which is the loss the imputed outcome (e.g., predicted 3-year revenue) when a unit is assigned to a suboptimal action. In multi-action cases, a cost-sensitive binary classification is done on every pair of actions, and the final action is chosen by a majority vote. In practice, the policy class is often restricted by the choice of a specific type of classifier (e.g., logistic regression or decision trees for interpretation or transparency reasons), or by using only a subset of covariates in the classifier (while still using all information to construct the doubly-robust scores). A practical advantage of this approach is that once the doubly-robust scores or labels are constructed, we can plug them into off the shelf classifiers to optimize the policy.

4.2.3 Policy Implementation and Exploration

While we have estimated the optimal policy, it is typically desirable to account for remaining statistical uncertainty and continue randomized exploration, which can be particularly important if there is non-stationarity, i.e., changes in the environment that make a policy that is optimal today no longer optimal in the future. While other approaches can be suitable, we find particularly suitable a variant of Thompson sampling, bootstrap Thompson sampling (BTS) (Eckles and Kaptein 2014, Lu and Van Roy 2017, Osband et al. 2016), that is readily implemented with models for which Thompson sampling might be cumbersome to implement; see Eckles and Kaptein (2019) and Osband et al. (2017) for reviews. We use BTS as a heuristic approach to adding randomized uncertainty-based exploration to the estimated optimal targeting policy where a unit is assigned to action with probability proportional to the fraction of times an action is estimated to be optimal across all bootstrap replicates of the data. That is,

| (23) |

where is the policy estimated according to Equation 21 or 22 on the th bootstrap replicate.181818In cases where a unit is always or never assigned to some conditions, we may want to impose a probability floor and ceiling to ensure that all units have positive probability being assigned to all conditions, thereby satisfying Assumption .

4.3 Summary of the Methods

We summarize the key steps in combining these methods as follows:

0) Identify the long-term outcome of interest (), intervention (), covariates (), and surrogates ().

1) Run a randomized experiment through a design policy to generate experimental data . Gather historical data .

2) Impute the missing long-term outcomes in the experiment using the surrogate index through Equation 9.

3) Do policy optimization using imputed long-term outcomes to get an estimated optimal policy through Equation 19 and 21 or 22.

4) Implement the estimated optimal policy , potentially with added randomization as in through Equation 23.

5) Consider Step 4 as running a new randomized experiment with being the new , and repeat Step 1 – 4 as desired.

5 Experiments and Results

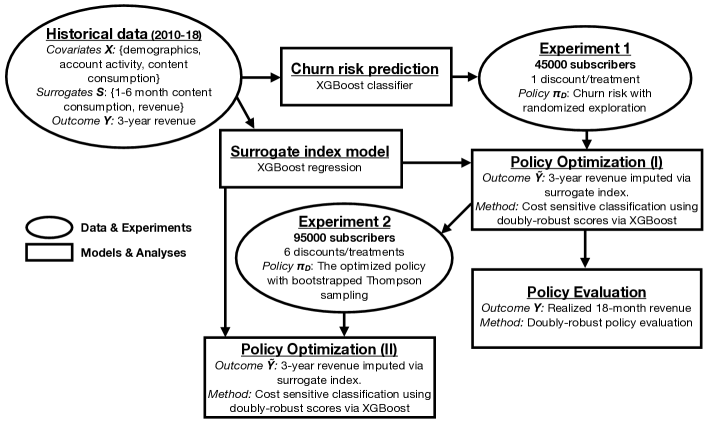

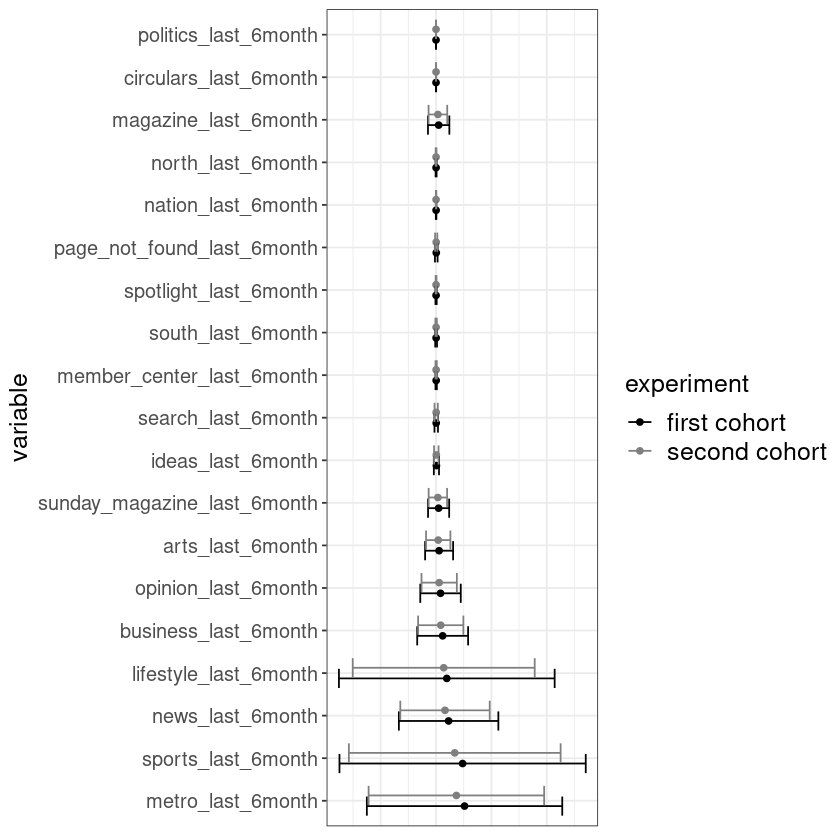

We now turn to applying and evaluating this approach in the context of reducing churn at The Boston Globe, where we offer discounts to existing subscribers. Figure 2(a) gives an overview of how the historical observational data and two field experiments relate to each other and the main analyses. Experiment 1 randomized subscribers to receive a discount or not. We then optimized the targeting policy using results from Experiment 1 and a surrogate index constructed from historical data, the surrogates we use are: content consumption (number of articles read in each of the 20 most visited sections191919The sections are: metro, sports, news, lifestyle, business, opinion, arts, Sunday magazine, ideas, search, member center, south, spotlight, page not found, nation, north, magazine, circulars, politics. on The Boston Globe’s website) and revenue over the first 6 months. We selected these surrogates based on the following reasoning. First, revenue captures whether a subscriber has already churned, as well as whether they have perhaps received other discounts (e.g., via reactive churn management). Second, subscribers get value from their subscription primarily by consuming articles and other content on The Boston Globe’s website. We expected that some of this content is more differentiated from that otherwise available (e.g., local sports coverage). These surrogates could be measured over shorter or longer periods. Intuitively, the longer we wait, the better we can estimate the long-term revenue, but firms also want to learn the optimal policy quickly so we can implement it. In particular, we should expect that it will be important to observe revenue and consumption for some time after the discounts expire. Given these considerations, we used surrogates computed over 6 months of data.

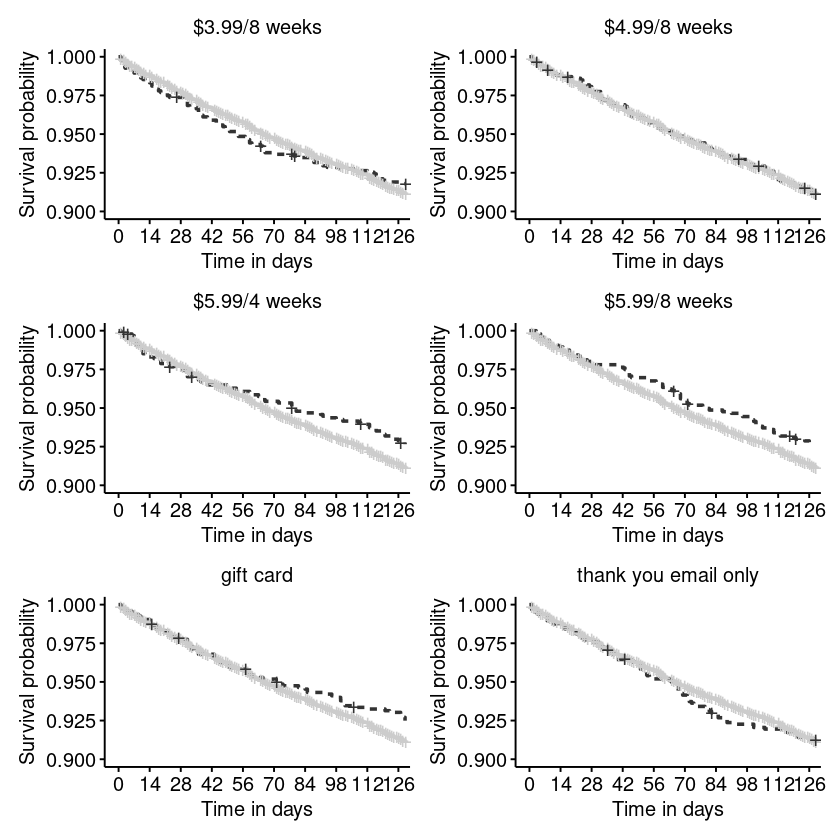

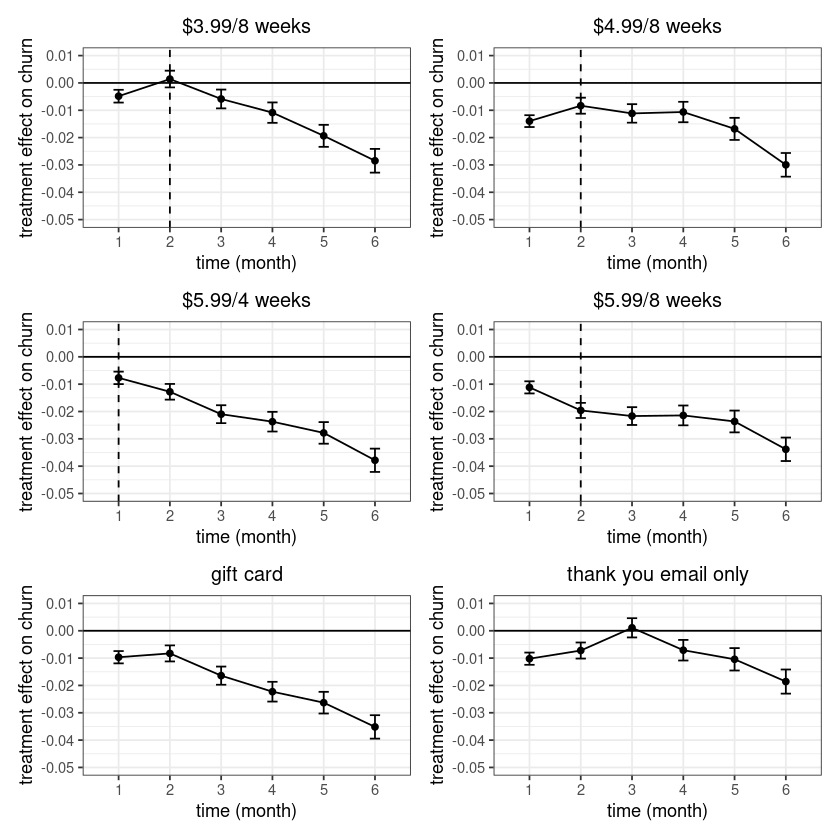

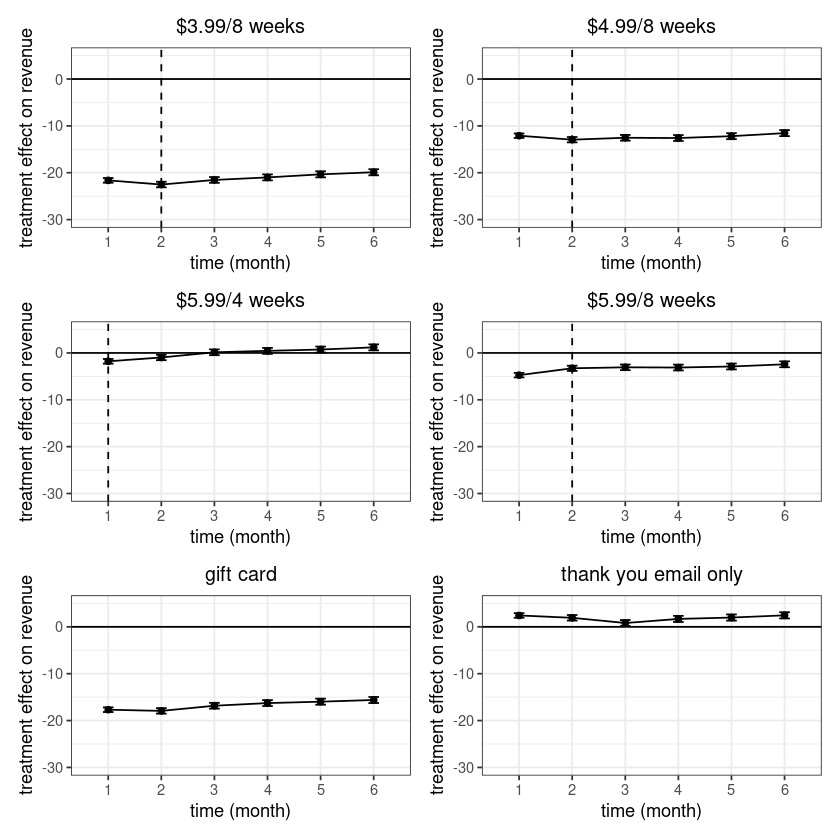

We implemented the policy, with additional randomized exploration, in Experiment 2. Once 18 months had passed since the start of Experiment 1, we were able to compare the performance of the policy we learned using the surrogate index to that we would have learned using the longer-term, 18-month outcomes.202020We use the most recent historical data to do the imputation; that is, for Experiment 1, run in 2018, we used the observed revenue data from 2015–2018 to estimate the 3-year revenue for subscribers in the experiment. All treatment effects are from intent-to-treat (ITT) analyses that do not condition on potentially endogenous post-treatment behaviors, such as opening the email or redeeming the benefit. We report the survival curves and treatment effects estimated from the resulting data in both experiments in Appendix D.3. In this section, we focus on the experiment design, policy learning, and surrogate index validation results.

5.1 Experiment 1

As is typical of a new effort in proactive churn management, we lacked prior experimental data in which subscribers were assigned to discounts. However, we anticipated that the discount treatment would not have substantial beneficial effects on subscribers with a low probability of churning. Thus, we assigned subscribers to treatment using a design policy in the first experiment that balances exploration and exploitation; we do so by assigning subscribers with higher predicted churn probability into treatment with higher probability, while ensuring that all subscribers , thus satisfying Assumption 18; see Appendix D.1 and D.2 for a more detailed discussion. This assigned 806 subscribers to receive a discounted subscription rate ($4.99 per week) for 8 weeks.

We estimate the optimal policy via the binary cost-sensitive classification (Equation 21) on imputed long-term revenue, defined as either 18-month or 3-year revenue. In this section, we focus on the policy using imputed 3-year revenue; we return to the policy using imputed 18-month revenue in our validation in Section 5.3. We first construct doubly-robust scores for each subscriber using Equation 19 where is estimated using XGBoost via cross-fitting.212121Cross-fitting means that for individual is estimated without using ’s own data in the training process. We can split data randomly into folds, then for individuals in a given fold is trained only using data from the other folds, it reduces over-fitting and improves efficiency (Athey and Wager 2020, Zhou et al. 2018). We use in our estimation. We then split the data into training (80%) and test sets (20%) and use XGBoost as the classifier with hyper-parameters tuned via cross-validation. The policy learned using the surrogate index, , would treat 21% of subscribers in the experimental data. We evaluate policy performance on the test data using the doubly-robust estimator as in Equation 17. According to the surrogate index, it would generate a $40 revenue increase per subscriber (95% confidence interval [$10, $75]) over 3 years compared to the current policy that treats no one, which is $1.7 million dollars in total for subscribers in the first experiment.

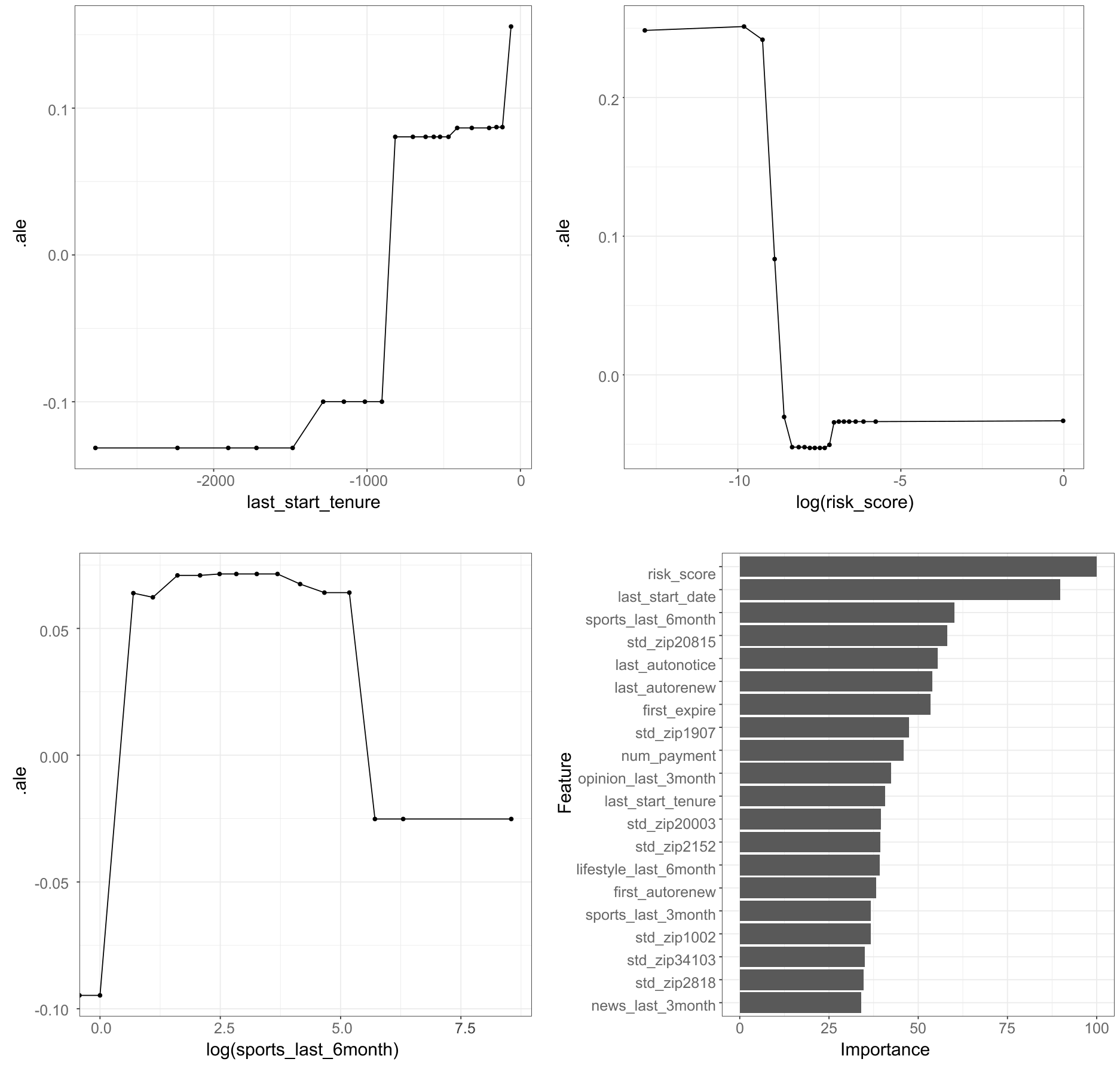

We use tools in interpretable machine learning to look at what variables are most important in determining the optimal policy, and how the optimal policy depends on these variables (see Appendix D.4). The top three variables are risk score (predicted risk of churn), tenure, and number of sports articles read in the last 6 months. The optimized policy treats subscribers with shorter tenure (more recently registered subscribers) at a higher rate. The relationship between number of sports articles read and treatment is not monotone: The fraction treated is low for very inactive and very active subscribers, but higher for subscribers in between. The relationship with risk score is interestingly also not monotone, for subscribers with the highest risk scores the treatment fractions are higher, this is consistent with our prior. But for some subscribers with very low risk scores, the treatment probabilities are even higher. This also highlights potential blind spots of targeting solely based on risk scores.

5.2 Experiment 2

Having learned a policy using the first experiment, we turned to exploiting this knowledge and further learning through experimentation in a second experiment. Furthermore, the success of the first experiment prompted creating and trying a larger set of 6 treatments: a thank you email, a $20 gift card, a discount to $5.99 for 8 weeks, a discount to $5.99 for 4 weeks, a discount to $4.99 for 8 weeks (the same as the intervention in the first experiment), and a discount to $3.99 for 8 weeks.

We use the learned policy based on imputed 3-year revenue — with two modifications — to allocate subscribers to treatments. First, as discussed in Section 4.2.3, adding randomization to an estimated optimal policy is a desirable practice especially in a potentially non-stationary environment. We added randomization to the optimized policy through bootstrap Thompson sampling as in Equation 23. This assigned 5,688 subscribers to treatments. Second, since all but one of the treatments were new, the learned policy was not directly informative about which non-control actions to take; therefore, conditional on a subscriber being assigned to treatment, we assigned them to the 6 non-control conditions uniformly at random. For future subscribers, we can learn and implement an optimal policy over all interventions based on the results from Experiment 2.

We optimize the policy via multi-class cost-sensitive classification (Equation 22) using data from Experiment 2 following a similar procedure as in Experiment 1. The optimized policy using the surrogate index, , allocates around a quarter of subscribers each to control, the thank you email, and the two smallest discounts; a few subscribers are allocated to other actions (Table 1(a)). This optimized policy improves 3-year revenue by $30 per subscriber (95% confidence interval [$12, $50]) relative to the status quo that treats no one, such that it would have generated $2.8 million for subscribers in Experiment 2.

| Action | Percentage |

|---|---|

| control | 23% |

| thank you email only | 25% |

| gift card | <1% |

| $5.99/8 weeks | 25% |

| $5.99/4 weeks | 27% |

| $4.99/8 weeks | <1% |

| $3.99/8 weeks | <1% |

We further compare the two experiments to see whether there are significant changes in the environment in terms of covariate and concept shift (Appendix D.5). When the environment is stationary, it is more efficient to pool data from the two experiments together to estimate the optimal policy for future subscribers, and when the environment is substantially changing, it is better to down-weight observations from the first experiment using a time-decaying case weight (e.g., Russac et al. 2019). We only use data from the second experiment to estimate the optimal policy because there is some evidence for concept shift and there is only one common treatment condition between the two experiments.

5.3 Surrogate Index Validation and Comparison

The assumptions underlying surrogate-index-based policy learning are strong, and it is often implausible that they are strictly true; this is similar to, e.g., doubts about conditional ignorability in observational causal inference or the exclusion restriction in instrumental variables analyses. Thus, like in those settings (e.g., Dehejia and Wahba 2002, Gordon et al. 2019, Eckles and Bakshy 2021), it is often valuable to empirically evaluate the results of our approach when that is possible (i.e., when we do observe long-term outcomes). Researchers can wait until the true long-term outcomes are observed, and then compare the effect estimates and policies based on the surrogate index with those based on the true long-term outcomes. Here it takes 3 years to observe the long-term outcome The Boston Globe is targeting for; instead, we use 18-month revenue (from August 2018 to February 2020), which is already realized at the time this is written, as the long-term outcome and repeat the analysis. Policy values are estimated using the doubly-robust approach as in Equation 17, except that the outcomes we use are observed , not imputed .

We first look at how well the surrogate index recovers the treatment effect estimated on the true long-term outcome. We then evaluate it by looking at how it performs against a benchmark policy that is learned on some short-term proxies of the long-term outcomes (e.g., 1–6 month revenue) and a policy learned on the true long-term outcome (e.g., realized 18-month revenue). We also look at how the performance changes if we chose a different subset of surrogates. All policy values here are defined relative to the status quo of treating no one. We report confidence intervals from 1,000 bootstrap draws on the test data.

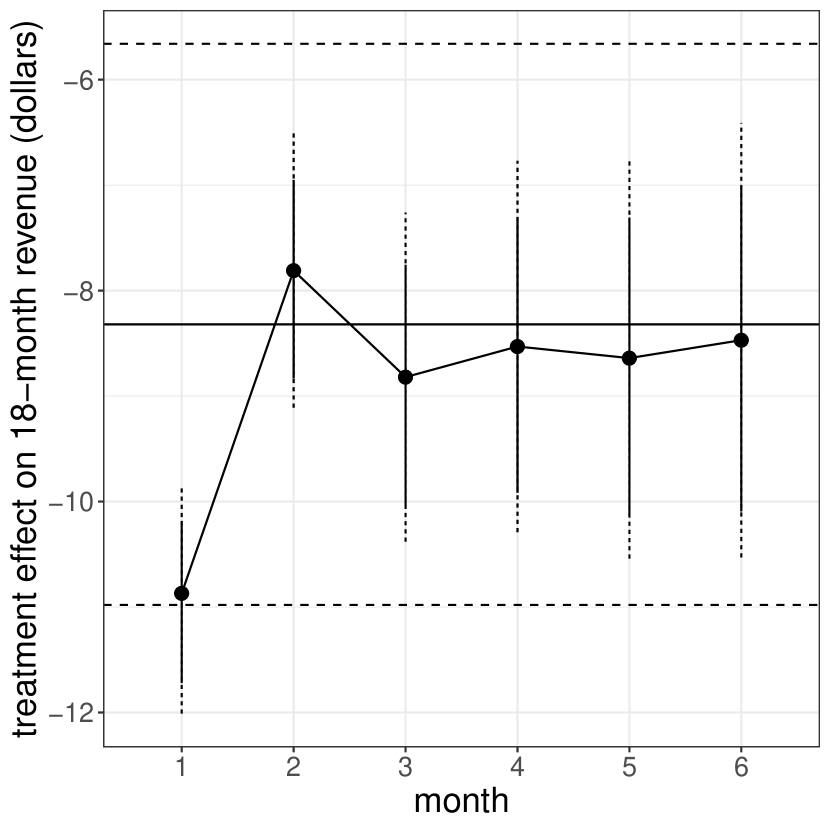

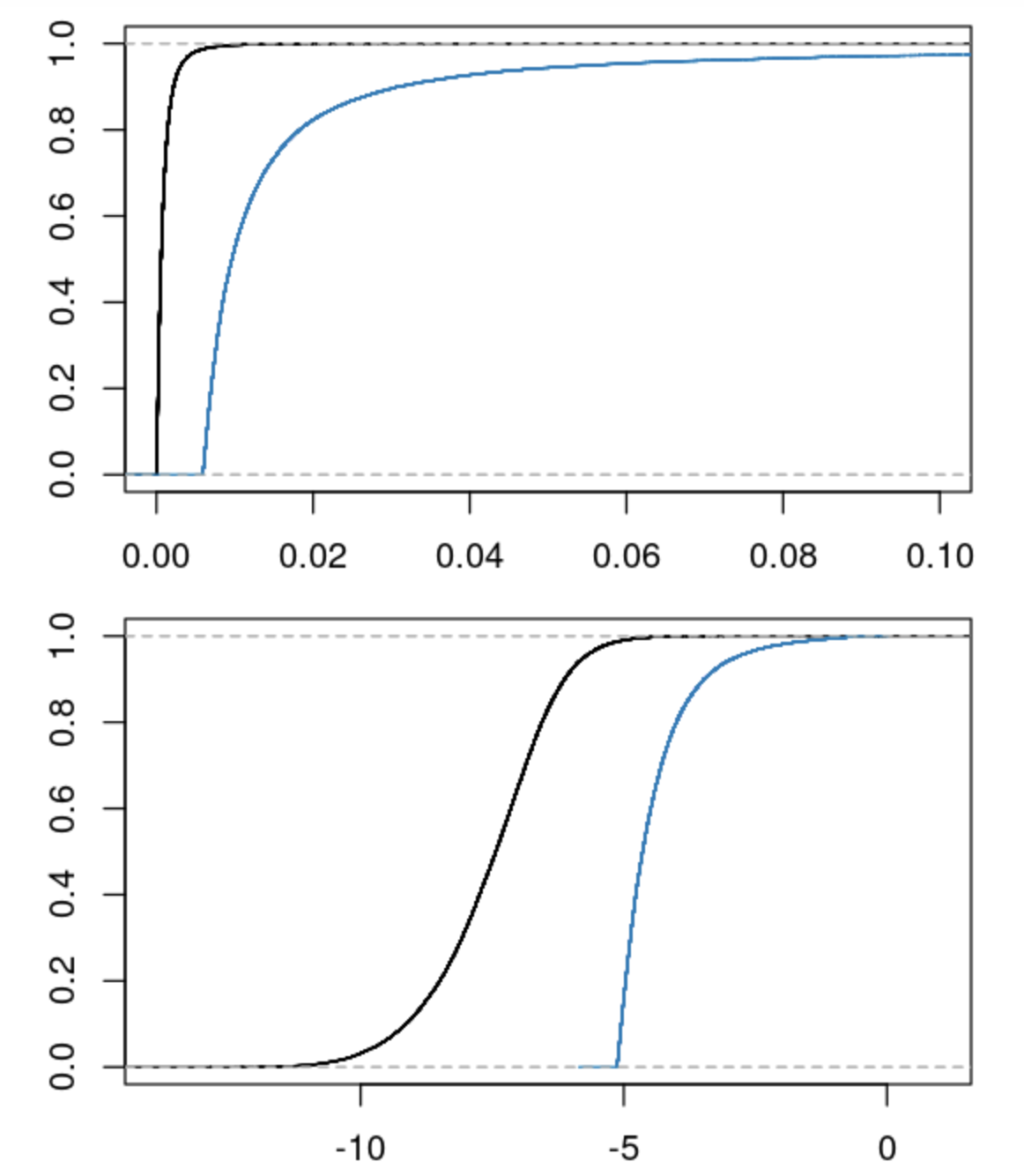

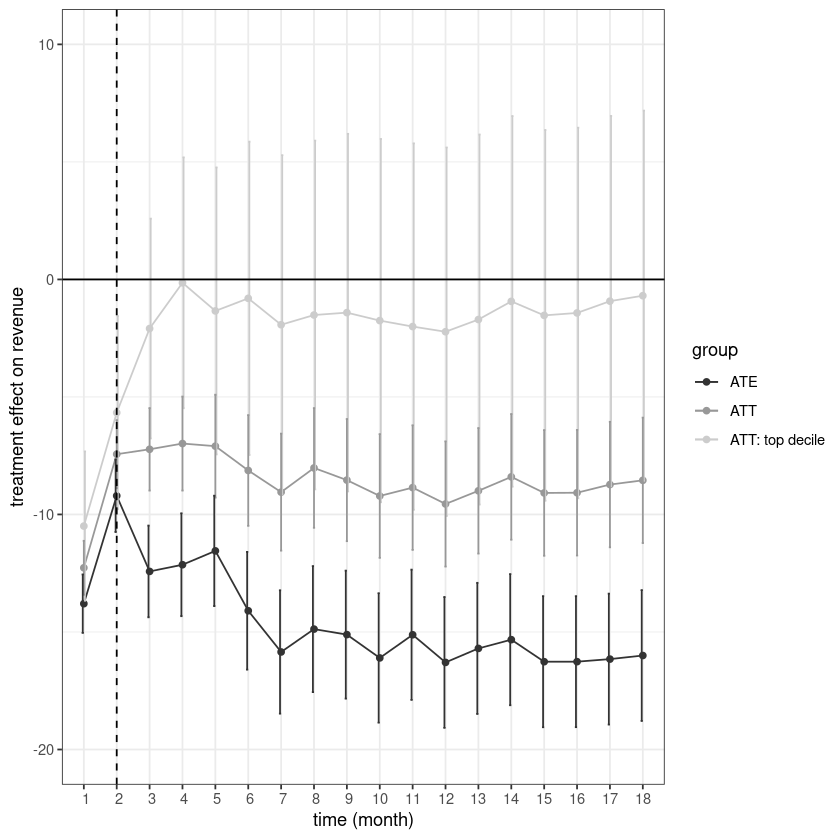

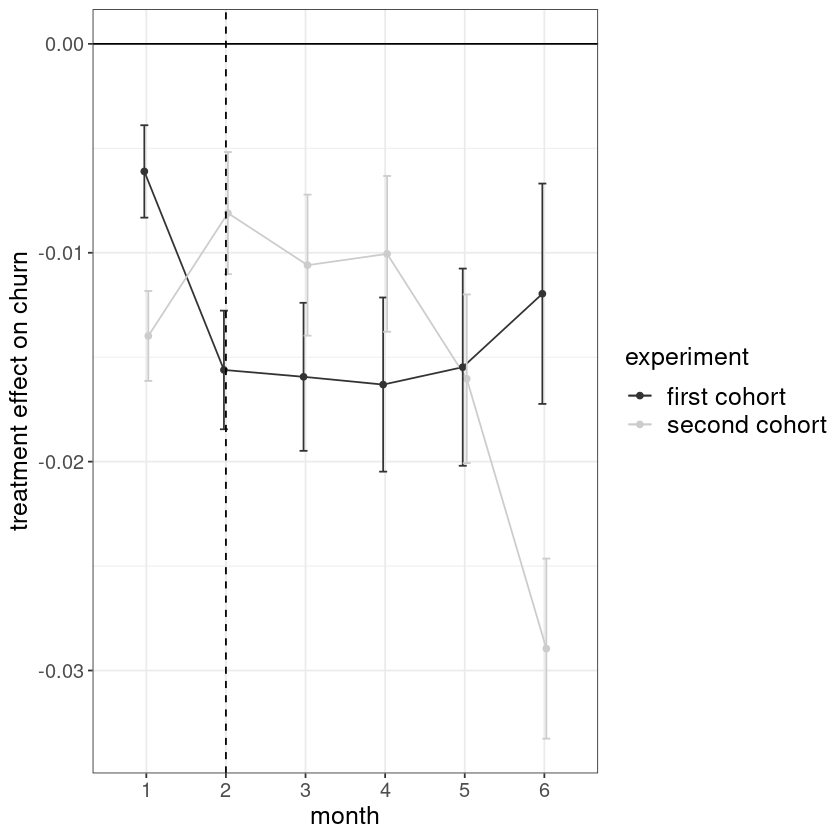

First, we look at how the average treatment effect on the treated (ATT) calculated using the surrogate index compares with ATT calculated using the true outcome (Figure 3(a)). After the first month, the surrogate-index-based ATT estimates are indistinguishable from the estimates using realized 18-month revenue. That the 1-month surrogate-index-based ATT is distinguishable from those using surrogates computed on longer periods may indicate that one month is too short a period; this is intuitively consistent as the treatment is a 8-week discount, so no reaction to the subsequent price increase is yet observed. Note that the confidence intervals of ATT estimated on true outcomes are wider than the ones estimated on surrogate index. When the surrogacy assumption holds, it is more efficient to estimate the treatment effect on surrogate index because it discards irrelevant variation in the long-term outcome.

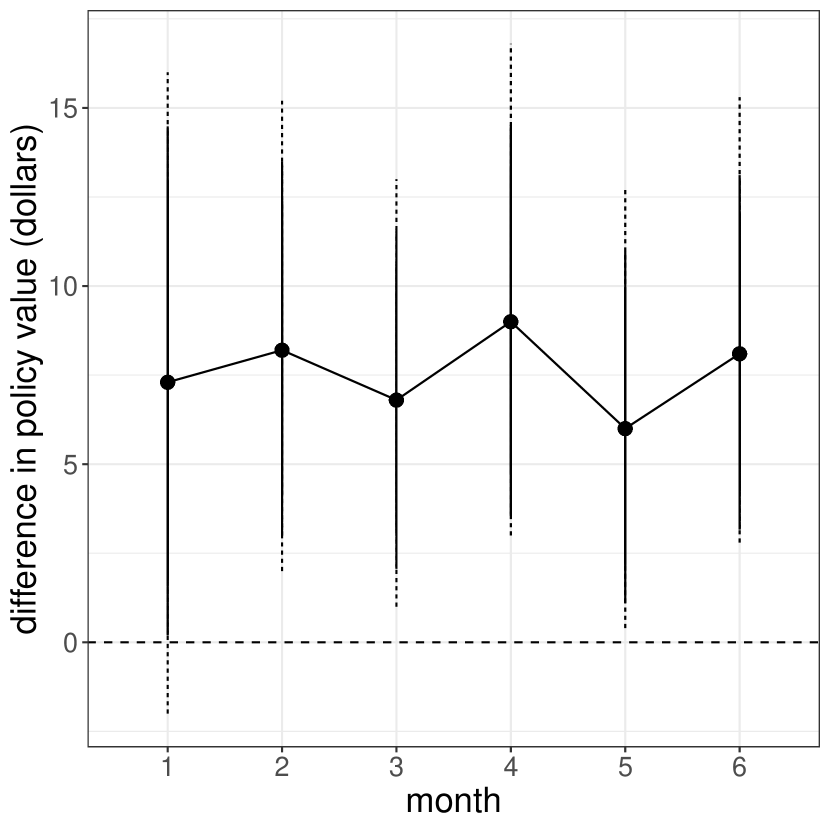

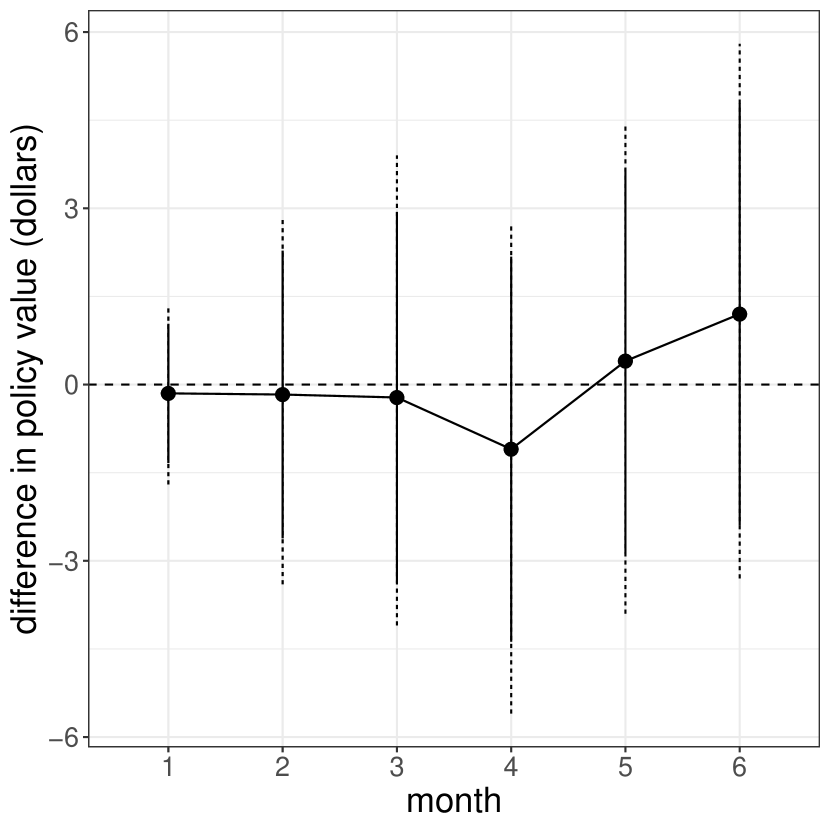

Next, we look at the value of surrogate-index-based policy (Figure 3(b)). All results are significantly better than the status quo except when we only use information from the first month; recall that the discount ends after 8 weeks. By contrast, optimizing the policy directly on short-term proxies (1–6 month revenue) does not detectably outperform the status quo (Figure 3(c)). We also compare the surrogate-index-based policy with a policy learned on the true long-term outcome (Figure 3(d)). Although all the point estimates of the value difference are negative, none of them is distinguishable from zero; the difference between the value of policy learned on surrogate indices using the first 6 month and true outcomes is -$8 per subscriber (95% confidence interval [-$24, $5]). This comparison does not take into account the gain in time and opportunity cost by implementing an optimized policy at 6 vs. 18 months. These two policies also agree on 72% of subscribers, i.e., they assign them to the same treatment condition. This is encouraging, but it is also contributes to imprecision in estimating differences between them, as they estimates are determined by the long-term revenue of a smaller number of subscribers.

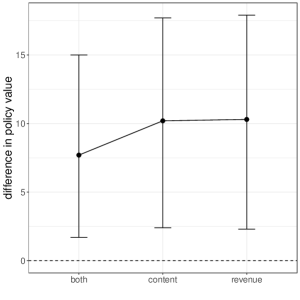

Lastly, we compare the performance of policies learned on surrogate indices constructed using only content consumption information, only short-term revenue, and both; the three approaches are not detectably different, though there is substantial uncertainty, so this does not rule out relevant differences (Appendix D.6).222222Athey et al. (2019) suggests that when the surrogacy condition holds, the smallest set of surrogates has the highest precision in estimating the treatment effect.

6 Conclusion

Many applied problems, from the subscriber management problem studied here to others in business, medicine, public policy, and social sciences, where there is a need to personalize interventions to optimize some long-term outcomes, can be fruitfully characterized as learning a targeting policy for some long-term outcomes. Here we advance the practice of policy learning by incorporating the use of a learned surrogate index to impute the long-term outcomes. We first show analytically when a surrogate index is valid for policy evaluation and optimization in place of true unobserved long-term outcomes. Then to validate our approach empirically, we run two large-scale experiments that prescribe who should be targeted with what incentives in order to maximize long-term subscription revenue for The Boston Globe. Combining data from the first experiment and the passage of time, we show that the policy optimized on long-term outcomes imputed by a surrogate index outperforms a policy optimized on a short-term proxy of the long-term outcomes and that it performs similarly to the policy optimized on true long-term outcomes. We then implement the optimized policy with additional randomized exploration so that we can respond to potential non-stationarity and update the optimized policy after each experiment. The total 3-year revenue impact of implementing policies optimized using the surrogate index, relative to the status quo, in the two experiments sums to $4–5 million. Our paper adds to and complements a recent and growing literature in marketing on policy evaluation and learning (e.g., Hitsch and Misra 2018, Simester et al. 2019a, b, Yoganarasimhan et al. 2020) and empirical work in proactive churn management (e.g., Ascarza 2018) by focusing on optimizing targeting policies for long-term retention and revenue.

A natural question is how to choose surrogates when imputing long-term outcomes. If we have the generative model in Figure 1(a) in mind, we want to choose variables that lie on the causal path from treatment to long-term outcomes, as suggested by domain knowledge or theory. We also want to choose surrogates that are observable shortly after the intervention so that the policy can be learned quickly. These two considerations may be in tension. If relevant experiments have been conducted in the past then the quality of surrogates can be evaluated on the realized long-term outcomes, as we have done here. Surrogates that are highly predictive of the outcome are potential candidates but there is no guarantee that they will produce high policy values, as predicting the outcome level is a different task than predicting the treatment effect or learning the policy. Future research may further examine selection of potential surrogates. In practice, we may only have noisy measurements of such surrogates; thus, a fruitful direction for future work may be incorporating recent developments from mediation analysis with multiple noisy measurements (Ghassami et al. 2021). Finally, since surrogacy is fundamentally a question about the underlying causal mechanism, once some surrogates have been shown to be valid for a given problem, they may be likely to remain valid for similar problems in the future. For example, we showed short-term revenues and content consumption are suitable surrogates for the effect of price discounts on long-term retention and subscription revenues, so the firm can tentatively rely on this assumption as they continue to iterate on targeting policies. We can imagine building such a knowledge base for different sets of problems and long-term outcomes as more empirical researchers work in this general framework.

The present work is not without important limitations. Some of these are limitations of the approach as developed here. For example, it is directly applicable when there is essentially no constraint on how many units can be treated, as in our case. When there is a budget constraint and heterogeneous treatment costs, a policy can be optimized based on the ratio between individual-level treatment effect and the cost of treatment as in Sun et al. (2021). There are also important limitations to the strength of the conclusions from our empirical application. For example, while we were not able to detect differences in performance between the surrogate-index-based policy and one based on true long-term outcomes, this may reflect remaining statistical uncertainty in estimating this contrast; similar considerations apply to other comparisons, such as between the value of policies using different sets of surrogates. More generally, the quite promising results observed here may not be indicative of what practitioners can expect in other, even somewhat similar subscriber management settings, perhaps especially if a very different variety of actions are used. Thus, we hope that subsequent work offers both further methodological development and empirical validation.

Acknowledgements

Correspondence should be addressed to J.Y. (jeryang@hbs.edu) and D.E. (eckles@mit.edu). This research was supported in part by a grant from Boston Globe Media. We thank Boston Globe Media and particularly Jessica Bielkiewicz, Thomas Brown, Ryan McVeigh, and Shannon Rose for their partnership in conducting the field experiments. This work benefited from comments by Susan Athey, John Hauser, Günter Hitsch, Duncan Simester, participants in seminars at MIT, the Harvard Business School Digital Doctoral Workshop, the NeurIPS CausalML Workshop and the Quantitative Marketing and Economics (QME) Conference.

References

- Apley and Zhu (2016) Daniel W Apley and Jingyu Zhu. Visualizing the effects of predictor variables in black box supervised learning models. arXiv preprint arXiv:1612.08468, 2016.

- Ascarza (2018) Eva Ascarza. Retention futility: Targeting high-risk customers might be ineffective. Journal of Marketing Research, 55(1):80–98, 2018.

- Ascarza et al. (2016) Eva Ascarza, Raghuram Iyengar, and Martin Schleicher. The perils of proactive churn prevention using plan recommendations: Evidence from a field experiment. Journal of Marketing Research, 53(1):46–60, 2016.

- Ascarza et al. (2017) Eva Ascarza, Peter S Fader, and Bruce GS Hardie. Marketing models for the customer-centric firm. In Handbook of Marketing Decision Models, pages 297–329. Springer, 2017.

- Athey and Imbens (2016) Susan Athey and Guido Imbens. Recursive partitioning for heterogeneous causal effects. Proceedings of the National Academy of Sciences, 113(27):7353–7360, 2016.

- Athey and Wager (2020) Susan Athey and Stefan Wager. Policy learning with observational data. arXiv preprint arXiv:1702.02896, 2020.

- Athey et al. (2019) Susan Athey, Raj Chetty, Guido W Imbens, and Hyunseung Kang. The surrogate index: Combining short-term proxies to estimate long-term treatment effects more rapidly and precisely. Technical report, National Bureau of Economic Research, 2019.

- Blattberg et al. (2008) Robert C Blattberg, Byung-Do Kim, and Scott A Neslin. Why database marketing? In Database Marketing, pages 13–46. Springer, 2008.

- Chen et al. (2007) Hua Chen, Zhi Geng, and Jinzhu Jia. Criteria for surrogate end points. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 69(5):919–932, 2007.

- Chen and Guestrin (2016) Tianqi Chen and Carlos Guestrin. XGBoost: A scalable tree boosting system. In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 785–794. ACM, 2016.

- Chen et al. (2015) Tianqi Chen, Tong He, Michael Benesty, et al. xgboost: Extreme gradient boosting. R package version 0.4-2, pages 1–4, 2015.

- Chernozhukov et al. (2016) Victor Chernozhukov, Juan Carlos Escanciano, Hidehiko Ichimura, Whitney K Newey, and James M Robins. Locally robust semiparametric estimation. arXiv preprint arXiv:1608.00033, 2016.

- Dehejia and Wahba (2002) Rajeev H Dehejia and Sadek Wahba. Propensity score-matching methods for nonexperimental causal studies. Review of Economics and Statistics, 84(1):151–161, 2002.

- Dudík et al. (2014) Miroslav Dudík, Dumitru Erhan, John Langford, and Lihong Li. Doubly robust policy evaluation and optimization. Statistical Science, 29(4):485–511, 2014.

- Eckles and Bakshy (2021) Dean Eckles and Eytan Bakshy. Bias and high-dimensional adjustment in observational studies of peer effects. Journal of the American Statistical Association, 116(534):507–517, 2021.

- Eckles and Kaptein (2014) Dean Eckles and Maurits Kaptein. Thompson sampling with the online bootstrap. arXiv preprint arXiv:1410.4009, 2014.

- Eckles and Kaptein (2019) Dean Eckles and Maurits Kaptein. Bootstrap Thompson sampling and sequential decision problems in the behavioral sciences. SAGE Open, 9(2):2158244019851675, 2019.

- Fader and Hardie (2015) Peter S Fader and Bruce GS Hardie. Simple probability models for computing clv and ce. In Handbook of Research on Customer Equity in Marketing. Edward Elgar Publishing, 2015.

- Fader et al. (2014) Peter S Fader, Bruce GS Hardie, and Subrata Sen. Stochastic models of buyer behavior. In The History of Marketing Science, pages 165–205. 2014.

- Farrell (2015) Max H Farrell. Robust inference on average treatment effects with possibly more covariates than observations. Journal of Econometrics, 189(1):1–23, 2015.

- Freedman et al. (1992) Laurence S Freedman, Barry I Graubard, and Arthur Schatzkin. Statistical validation of intermediate endpoints for chronic diseases. Statistics in Medicine, 11(2):167–178, 1992.

- Ghassami et al. (2021) AmirEmad Ghassami, Ilya Shpitser, and Eric Tchetgen Tchetgen. Proximal causal inference with hidden mediators: Front-door and related mediation problems. arXiv preprint arXiv:2111.02927, 2021.

- Godinho de Matos et al. (2018) Miguel Godinho de Matos, Ferreira Pedro, and Belo Rodrigo. Target the ego or target the group: Evidence from a randomized experiment in proactive churn management. Marketing Science, 2018.

- Gordon et al. (2019) Brett R Gordon, Florian Zettelmeyer, Neha Bhargava, and Dan Chapsky. A comparison of approaches to advertising measurement: Evidence from big field experiments at Facebook. Marketing Science, 38(2):193–225, 2019.

- Gupta et al. (2006) Sunil Gupta, Dominique Hanssens, Bruce Hardie, Wiliam Kahn, V Kumar, Nathaniel Lin, Nalini Ravishanker, and S Sriram. Modeling customer lifetime value. Journal of Service Research, 9(2):139–155, 2006.

- Hahn (1998) Jinyong Hahn. On the role of the propensity score in efficient semiparametric estimation of average treatment effects. Econometrica, pages 315–331, 1998.

- Hitsch and Misra (2018) Günter J Hitsch and Sanjog Misra. Heterogeneous treatment effects and optimal targeting policy evaluation. Working paper, 2018.

- Horvitz and Thompson (1952) Daniel G Horvitz and Donovan J Thompson. A generalization of sampling without replacement from a finite universe. Journal of the American Statistical Association, 47(260):663–685, 1952.

- Jiang et al. (2016) Zhichao Jiang, Peng Ding, and Zhi Geng. Principal causal effect identification and surrogate end point evaluation by multiple trials. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 78(4):829–848, 2016.

- Joffe and Greene (2009) Marshall M Joffe and Tom Greene. Related causal frameworks for surrogate outcomes. Biometrics, 65(2):530–538, 2009.

- Khan and Ugander (2021) Samir Khan and Johan Ugander. Adaptive normalization for IPW estimation. arXiv preprint arXiv:2106.07695, 2021.

- Lauritzen (2004) Steffen L Lauritzen. Discussion on causality. Scandinavian Journal of Statistics, 31(2):189–201, 2004.

- Lemmens and Croux (2006) Aurélie Lemmens and Christophe Croux. Bagging and boosting classification trees to predict churn. Journal of Marketing Research, 43(2):276–286, 2006.

- Lemmens and Gupta (2020) Aurélie Lemmens and Sunil Gupta. Managing churn to maximize profits. Marketing Science, 2020. forthcoming.

- Lu and Van Roy (2017) Xiuyuan Lu and Benjamin Van Roy. Ensemble sampling. In Advances in Neural Information Processing Systems, pages 3258–3266, 2017.

- Misra et al. (2019) Kanishka Misra, Eric M Schwartz, and Jacob Abernethy. Dynamic online pricing with incomplete information using multiarmed bandit experiments. Marketing Science, 38(2):226–252, 2019.

- Murphy et al. (2001) Susan A Murphy, Mark J van der Laan, James M Robins, and Conduct Problems Prevention Research Group. Marginal mean models for dynamic regimes. Journal of the American Statistical Association, 96(456):1410–1423, 2001.

- Neslin et al. (2006) Scott A Neslin, Sunil Gupta, Wagner Kamakura, Junxiang Lu, and Charlotte H Mason. Defection detection: Measuring and understanding the predictive accuracy of customer churn models. Journal of Marketing Tesearch, 43(2):204–211, 2006.

- Osband et al. (2016) Ian Osband, Charles Blundell, Alexander Pritzel, and Benjamin Van Roy. Deep exploration via bootstrapped DQN. In Advances in Neural Information Processing Systems, pages 4026–4034, 2016.

- Osband et al. (2017) Ian Osband, Daniel Russo, Zheng Wen, and Benjamin Van Roy. Deep exploration via randomized value functions. Journal of Machine Learning Research, 2017.

- Owen (2019) Art B Owen. Monte Carlo Theory, Methods and Examples. 2019. Book manuscript. Available at https://statweb.stanford.edu/~owen/mc/.

- Prentice (1989) Ross L Prentice. Surrogate endpoints in clinical trials: definition and operational criteria. Statistics in medicine, 8(4):431–440, 1989.

- Robins et al. (1994) James M Robins, Andrea Rotnitzky, and Lue Ping Zhao. Estimation of regression coefficients when some regressors are not always observed. Journal of the American Statistical Association, 89(427):846–866, 1994.

- Russac et al. (2019) Yoan Russac, Claire Vernade, and Olivier Cappé. Weighted linear bandits for non-stationary environments. In Advances in Neural Information Processing Systems, pages 12017–12026, 2019.

- Särndal et al. (1992) CE Särndal, B Swensson, and JH Wretman. Model Assisted Survey Sampling. Springer-Verlag, 1992.

- Simester et al. (2019a) Duncan Simester, Artem Timoshenko, and Spyros Zoumpoulis. Efficiently evaluating targeting policies: Improving upon champion vs. challenger experiments. 2019a.

- Simester et al. (2019b) Duncan Simester, Artem Timoshenko, and Spyros I Zoumpoulis. Targeting prospective customers: Robustness of machine learning methods to typical data challenges. Management Science, 2019b.

- Sun et al. (2021) Hao Sun, Shuyang Du, and Stefan Wager. Treatment allocation under uncertain costs. arXiv preprint arXiv:2103.11066, 2021.

- Sutton and Barto (2018) Richard S Sutton and Andrew G Barto. Reinforcement learning: An introduction. MIT press, 2018.

- VanderWeele (2013) Tyler J VanderWeele. Surrogate measures and consistent surrogates. Biometrics, 69(3):561–565, 2013.

- Wager and Athey (2018) Stefan Wager and Susan Athey. Estimation and inference of heterogeneous treatment effects using random forests. Journal of the American Statistical Association, 113(523):1228–1242, 2018.

- Weir and Walley (2006) Christopher J Weir and Rosalind J Walley. Statistical evaluation of biomarkers as surrogate endpoints: a literature review. Statistics in Medicine, 25(2):183–203, 2006.

- Xu and Zeger (2001) Jane Xu and Scott L Zeger. The evaluation of multiple surrogate endpoints. Biometrics, 57(1):81–87, 2001.

- Yoganarasimhan et al. (2020) Hema Yoganarasimhan, Ebrahim Barzegary, and Abhishek Pani. Design and evaluation of personalized free trials. arXiv preprint arXiv:2006.13420, 2020.

- Zhou et al. (2018) Zhengyuan Zhou, Susan Athey, and Stefan Wager. Offline multi-action policy learning: Generalization and optimization. arXiv preprint arXiv:1810.04778, 2018.

Online appendix for:

“Targeting for long-term outcomes”

Appendix A New York Times Example

Appendix B Targeting Emails

Appendix C Proof of Propositions

Proof.

Proposition 1: Consider a case with binary actions. Let . We show that the value of a policy as defined on true long-term outcomes is identified using the surrogate index .

| (24) |

is the propensity score. The first line is from the definition of the value of a policy. The second line is because under Assumption 18 (ignorability and positivity) we have

| (25) |

The third line is because is a constant. The fourth line is from the law of iterated expectation: We first condition on surrogates and covariates and . The fifth line is based on Assumption 2 (surrogacy) so the expectation of product can be factorized into the product of expectations. The last line is based on undoing the law of iterated expectations, the definition of surrogate index and Assumption 3 (comparability) as in Equation 9. The same argument also goes through for multi-action cases. ∎

Proof.

Proposition 2: For policy optimization, consider the case of binary actions, we can see that an optimal policy maximizes the average outcome by assigning a subscriber to treatment if and only if the conditional average treatment effect (CATE) for that subscriber is positive (net of the cost of treatment if any):

| (26) |

| (27) |

| (28) |

Because the optimal policy depends only on the sign of CATE on the long-term outcome, the policy optimized on surrogate index is valid as long as CATE estimated on the surrogate index is of the same sign as the true CATE.

Following a similar derivation as in the proof of Proposition 1:

| (29) |

The surrogate index can be used to construct an unbiased estimator of CATE, therefore, it can be used for policy learning. ∎

Proof.

Proposition 3: There is no loss in policy value if surrogate-index-based policy identifies the true optimal action, i.e., . Note that this can be true even when the CATE is biased. When the surrogate-index-based policy doesn’t identify the true optimal actions, the loss in policy value is the difference in outcome under the true optimal action and the one identified by the policy, i.e., . Therefore, the total loss in policy value when integrating over the distribution of is:

| (30) |

When Assumption 2 (surrogacy) is violated, the CATE estimated using surrogate index is biased. In binary cases, Athey et al. [2019] showed that the bias on ATE is bounded by :

| (31) |

where and is the of the regression of long-term outcome on surrogates (in the historical dataset), and the regression of actions on surrogates (in the experimental dataset), respectively. Similarly, the bias on CATE is bounded by :

| (32) |

because an optimal policy assigns actions based on the sign of true CATE, as long as the CATE estimated on surrogate index has the same sign as the true CATE, there’s no loss on the value of policy. When the signs are different, the loss is the true CATE, it follows that the total loss in policy value is bounded above by:

| (33) |

where is the CATE estimated with the surrogate index. ∎

Appendix D Supplementary Analyses

D.1 Churn Prediction

The dataset we have includes demographic, transaction history and browsing history for all digital only subscribers from 2010/12/16 to now. We first pick a date and use all the information before that date to predict outcomes (whether a given subscriber churned or not) that happened within six months after that date. We picked 2018/01/30 because it gives us the most recent information before targeting subscribers in the first experiment, although model performance is robust to other dates that we picked.

We select active subscribers defined by the company, it includes all subscribers who are currently active, in grace period, or in temporary stop.232323Most common reason for this is traveling. Then we construct features from transaction history using frequency and recency by each transaction type, which are standard features in the churn prediction literature [Lemmens and Croux, 2006]. Frequency is the number of times a certain transaction type occurred, and recency is the first and last time a certain transaction type occurred compared with the date we picked (in days). Then we count the number of articles read in the last week, month, 3 months and 6 month to measure the level of engagement. We also extracted how many articles a subscriber read in each section on the newspaper’s website over time, although this content consumption information is not used for churn prediction, we use it for policy learning. We look at churn that happened between 2018/01/30 and 2018/07/18 to get the outcome labels, if a churn happened it’s coded as 1, and 0 otherwise. We handle missing data in the following way: if a feature is a measure of recency, then missing means that a certain type of event has not happened yet, so we impute a large positive number 1000 (a positive number means it is in the future) and create a separate column indicating if that value is missing (1 or missing, 0 for not missing). If a feature is categorical, we create “missing” as a new category. Altogether we have 183 features. We also removed recent subscribers whose tenure is less than 60 days and who hasn’t opened any emails sent by the company in the last 6 months. The reason is that recent subscribers are likely to be on an introductory rate which is already discounted, we don’t want to give them more discounts.