myequation

| (1) |

A Game-Theoretic Analysis of

Cross-Chain Atomic Swaps with HTLCs

Abstract

To achieve interoperability between unconnected ledgers, hash time lock contracts (HTLCs) are commonly used for cross-chain asset exchange. The solution tolerates transaction failure, and can “make the best out of worst” by allowing transacting agents to at least keep their original assets in case of an abort. Nonetheless, as an undesired outcome, reoccurring transaction failures prompt a critical and analytical examination of the protocol. In this study, we propose a game-theoretic framework to study the strategic behaviors of agents taking part in cross-chain atomic swaps implemented with HTLCs. We study the success rate of the transaction as a function of the exchange rate of the swap, the token price and its volatility, among other variables. We demonstrate that in an attempt to maximize one’s own utility as asset price changes, either agent might withdraw from the swap. An extension of our model confirms that collateral deposits can improve the transaction success rate, motivating further research towards collateralization without a trusted third party. A second model variation suggests that a swap is more likely to succeed when agents dynamically adjust the exchange rate in response to price fluctuations.

Index Terms:

atomic swap, blockchain, game theory, stochastic priceI Introduction

I-A Background

An atomic swap is a coordination task where two parties are willing to exchange assets such that either both parties receive each other’s original assets upon successful execution, or nothing in the event of failure [1]. Atomic swaps are easily achievable on a single ledger by implementing smart contracts such as automated market-making protocols [2].

For cross-chain asset swaps, the conventional approach is to use a centralized exchange, characterized by high efficiency and transaction speed. However, this requires intermediary fees and trust in the exchange (in terms of privacy and transparency of its matching mechanisms). In addition, centralized exchanges are vulnerable to different kinds of attacks [3], from wallet hacking [4], to DDoS attacks [5]. Over-the-counter (OTC) operations [6, 7] remain frequent for financial transactions. In the financial industry, it is common to use trusted third parties for OTC settlements, such as central clearing counterparties or broker-dealers, that have similar disadvantages as centralized exchanges.

To address some of the issues with centralized exchanges, and transactions with an intermediary in general, distributed exchanges (DEXs) have recently become a popular tool for cross-chain asset exchange [8, 9, 10, 11]. In such a peer-to-peer (P2P) environment, the transacting agents typically do not know each other and are thus exposed to malicious behaviors from their counterparty in DEXs that only provide match-making services. Therefore, the major challenge in such settings is to achieve atomicity of the cross-ledger transaction; that is, either the entirety of the transaction is executed, or, in case of failure, nothing occurs [1].

HTLCs,111The full name may be found with the suffix “ed” after hash or lock in research papers. There is no official convention as far as we know. first proposed on a Bitcoin forum by TierNolan [12], have been adopted by some DEXs[9, 10] to achieve atomicity of cross-chain transactions without direct communications between the ledgers. Studying and improving HTLCs has since been of high interest [13, 14, 15].

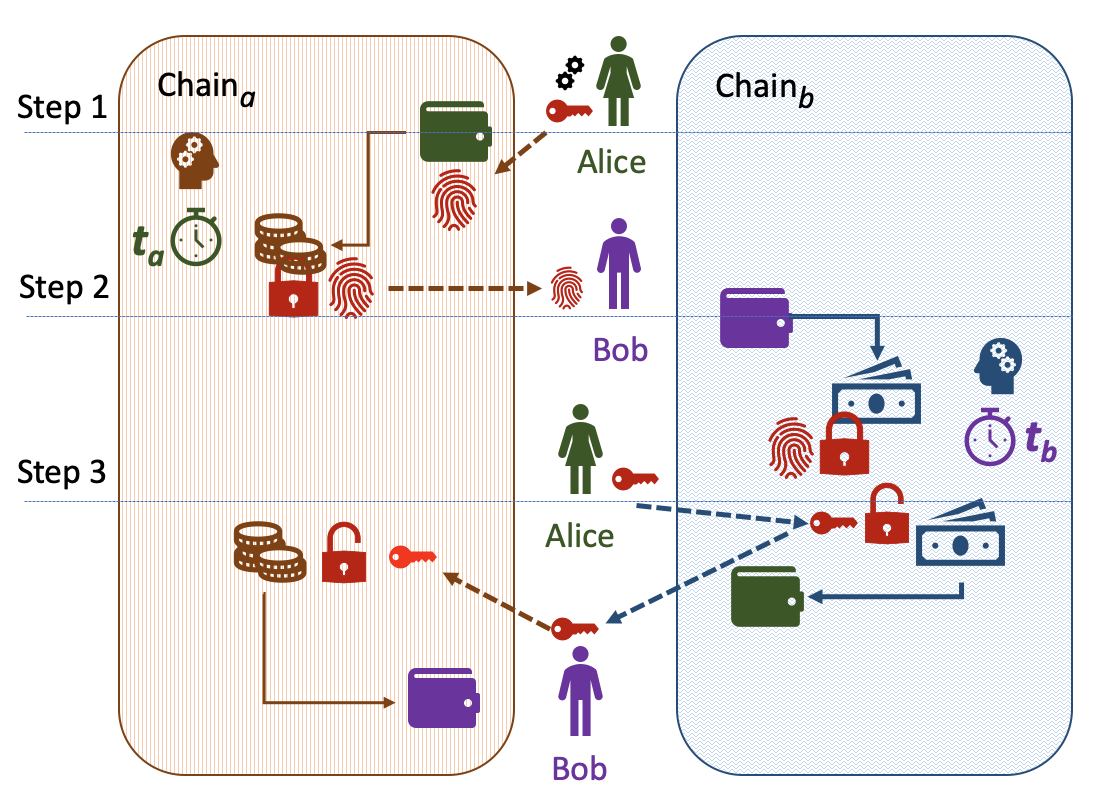

A hash time lock contract (HTLC) requires the two agents separately locking their assets on the respective blockchains, using the hash of a secret, generated by one of the users. The assets can then be unlocked upon revealing the preimage of a hash.

The users have accounts (wallets) on two disconnected ledgers (Chaina and Chainb) executing smart contracts. Consider that Alice wants to send assets on Chaina to Bob, in exchange for assets on Chainb from Bob. At Step 1, Alice initiates the transaction by generating a secret (a key) that will be used to unlock the asset transfers later on. She then deploys a smart contract on Chaina, that will lock her assets until time . This contract will transfer to Bob the assets only if the secret generated by Alice is revealed and entered into the smart contract. To verify the secret, Alice reveals its hash as part of the smart contract (cf. Figure 1 Step 1). One important feature of this contract is that after time , should the secret have not been revealed, the smart contract expires and Alice’s assets will be unlocked and returned to her wallet.

Next, Bob can verify the contract deployed by Alice on Chaina (assets, delivery address, etc.) and use the hash submitted by Alice in order to deploy a similar contract on Chainb (cf. Figure 1 Step 2), specifying the amount he is willing to transfer to Alice and expiry time . Until then Bob’s assets are locked on Chainb.

At Step 3, Alice can verify the contract deployed on Chainb, unlock the assets, and initiate their transfer to her wallet by revealing the secret on Chainb. As early as when the secret is revealed in the mempool of Chainb (even before Alice’s transfer is confirmed), Bob can use the secret to unlock the assets on Chaina and complete the cross-ledger transaction. In the best-case scenario, this mechanism enables atomic cross-ledger exchange of the assets without relying on a trusted party and without connection between ledgers. If Alice does not unlock the assets on Chainb before , then the assets are transferred back to Bob, thus, she has no incentive to reveal the secret as that would allow Bob to execute the smart contract on Chaina and transfer the assets to his wallet while keeping his assets on Chainb. In turn, once the secret is revealed, Bob’s assets are transferred to Alice and he should execute the smart contract on Chaina immediately in order to complete the transaction, otherwise he transferred his assets without receiving Alice’s assets.

I-B Contributions

In this paper, we focus on the standard implementation of a cross-ledger atomic swap with hash time lock contracts, HTLCs between two agents who wish to exchange tokens. In our framework, we assume a stochastic token price and that the counterparties can choose to either continue or stop at any stage of the transaction.

We define a game-theoretic framework to study the agents’ behaviors and the transaction outcome in atomic swaps. We focus on the standard protocol with HTLCs, yet the approach can be applied to different setups. The agents’ utility functions depend on

-

1.

the transaction outcome (success or failure),

-

2.

the asset price variation (trading profits),

-

3.

the duration of the transaction (locked in the game).

The agents’ utility functions are symmetric, but the agents may have a different idiosyncratic willingness to complete the transaction, the so-called success premium. By backward induction, we derive the agents’ optimal decisions, as well as the transaction success rate as a function of the agreed swap rate, actual token price and its volatility, among other variables. The standard setup has complete information symmetry, and we study the game with uncertainty in counterparties’ success premium.

In an extension, we show that if agents would be required to post collateral, everything else being equal, the transaction success rate would be higher. In another extension, we show that if agents can adjust the amount of tokens that they lock in the HTLCs, everything else being equal, the transaction success rate would be higher.

To the best of our knowledge, our work is the first to perform a thorough step-by-step examination of HTLC agents’ behavior through a game-theoretic model with numerical simulations.

II Related work

Recent years have witnessed a plethora of cross-ledger transaction solutions besides HTLC. Wanchain [16] enables interfacing and asset conversion to the native Wanchain token (Wancoins) in order to perform a cross-ledger asset exchange subsequently. Wanchain implements a privacy protection mechanism through a ring signature scheme [17] and a one-time account mechanism via one-time use wallets created for each transaction. Interledger [18] uses Byzantine notaries to construct a payment chain from sender to recipient over multiple ledgers, and the STREAM Interledger Transport protocol [19] apply packetized payments [20]. Relays [21], sidechains [22, 23], off-chain payment channels [24, 25, 26], and solutions based on chain relays [27] require building interfaces to such systems, similar to the case of a blockchain-based medium like Wanchain.

Cross-ledger transaction protocols are actively studied by the distributed ledger community: Borkowski et al. [28] surveyed atomic swaps for distributed ledgers, Herlihy provided a first extensive analysis of the scheme and demonstrated that HTLCs are still vulnerable to attacks, such as DDoS or secret hack [29]. Moreover, asset price volatility and malicious behaviour from agents driven by an attempt to maximize financial profits could negatively affect the transaction counterpart. For instance, if Alice becomes inactive before completion of the transaction, then the assets will be blocked on both ledgers [30, 27]. While it can be tolerated by an agent, this can incur significant losses to a counterparty.

To reduce the risk of agents being exposed to adverse behaviour, collateral deposits or transaction fees can be used. In a recent work, Han et al. [30] view atomic swaps as American options (without premium), and discuss “optionality” as a risk imposed by the swap initiator. The initiator can choose at any moment before revealing the secret whether to proceed with the swap or to abort it. To reduce the risk of malicious behaviour by the swap initiator, the authors propose to implement a premium mechanism. In our work, we do not define honest or malicious actors explicitly. Instead, we assume that both actors act rationally in their attempts to maximize their utility, and may appear as either “honest” or “malicious” depending on the movement of the token price. One of the trading protocols that support atomic swaps between parties and exchanges is Arwen. Arwen leverages off-chain RFQ trades and uses an escrow-fee mechanism based on blockchain to incentivize a swap initiator to unlock the coins in a timely manner and address lockup griefing in HTLC [31].

Zamyatin et al. [27] suggested posting collateral at least equal to the assets locked on the blockchain for a trade. The authors also proposed overcollateralization and a liquidation mechanism to mitigate extreme price fluctuations for both short and long term cross-ledger transactions. While such approach reduces economically rational agents’ incentive to misbehave, it is disadvantageous in that if an agent would like to transfer all his assets of one kind, he will be obliged to execute multiple transactions, each with an amount (approximately) equal to half the amount of the assets he currently possesses. In the extension of our model (Section IV), we also propose that both agents place collateral on one of the chains. We then study the impact of the collateralization on the transaction success rate. This analysis allows us to determine the optimal level of collateral for both agents.

Zakhary et al. [32] highlight that even if both participants are honest, the atomicity of HTLC can be violated due to crash failures, preventing smart contract execution before the expiry time of the contract. To address this problem, the authors present all-or-nothing atomic cross-chain commitment protocols and discuss their implementations: the -atomic cross-chain commitment protocol with centralized trusted witness and the -atomic cross-chain commitment protocol that uses another blockchain as a witness network. This approach shares some similarities with the recently proposed notion of a so-called cross-chain deal [33], which, as a generalization of the atomic swap, aims to enhance its expressive power to support various types of commercial practices. Both cross-chain deals and the protocols proposed in [32] are based on exchange of “proofs” or “votes” instead of relying on hashed time locks.

Belotti et al. [34] are among the first to conduct a game-theoretical analysis of cross-chain swaps (including HTLC as presented in [35, 29] and commitment-based protocols and from [32]) and characterise their equilibria. In our work, we focus on the intuition behind the strategic behavior of the participants of HTLC and show that it heavily depends on parameters such as the token price trend and volatility, as well as transaction confirmation time on the employed blockchains.

III A game-theoretic analysis

We seek to establish a model with a good balance of simplicity and fidelity. To this end, we apply reasonable and justifiable assumptions, and set realistic parameter values for numeric demonstration.

III-A Basic setup

Alice, denoted by , wishes to trade some amount of Tokena for 1 unit of Tokenb, while Bob, denoted by , is willing to do the opposite. Tokena and Tokenb are assets from two different blockchains, namely Chaina and Chainb. and intend to swap assets with each other and agree on the exchange rate: . Table I summarizes the expected balance change of ’s and ’s assets on the two chains through the swap.

| Expected balance change by swap | ||

|---|---|---|

| Agent | on Chaina | on Chainb |

| Alice () | Tokena | Tokenb |

| Bob () | Tokena | Tokenb |

For simplification, we make the following assumptions:

-

1.

The time it takes for a transaction to be confirmed on Chaina or Chainb is constant, equal to and respectively.

-

2.

Transaction fees are negligible relative to transaction volume.

-

3.

Tokena is the numéraire, in which Tokenb is priced and in which both transacting agents’ utilities are measured.

-

4.

Tokenb’s price (denominated in Tokena), , follows a geometric Brownian motion:

((2)) where follows a Wiener process with drift and infinitesimal variance .

-

5.

and are fully rational, which means they always choose the option that maximizes their utility.

-

6.

and have the same parametric utility function:

((3)) where

: agent indicator,

: time when the utility is assessed

: asset value denominated in Tokena

: time until end of game, when no further events directly connected to swap will occur

: discount rate,

: success indicator, 1 if the swap succeeds (i.e. agents balance change follows Table I), 0 if fails

: success premium

-

7.

and are aware of the value of each other’s parameter set, i.e. knows , and knows .

According to Equation (2), given Tokenb’s price at time , , the expectation (denoted by ), probability density function (PDF, denoted by ), and cumulative density function (CDF, denoted by ) of its price at can be expressed as:

where is the complementary error function, and .

All actors act rationally to maximize their utility as defined in Equation (3). Intuitively, actors with a higher success premium will act more “honestly”, i.e. ceteris paribus, they are more likely to continue the game; on the other hand, actors with a lower success premium may appear “malicious”, since ceteris paribus, they are more likely to withdraw from the game.

| Notation | Description |

|---|---|

| , | Alice, Bob |

| , | Transaction confirmation time on Chaina, Chainb |

| Time for an initiated transaction to become discoverable | |

| in the mempool of Chainb | |

| Point in time | |

| , | Points in time when the HTLCs on Chaina, Chainb expire |

| Price of Tokenb denominated in Tokena | |

| Agreed price of Tokenb denominated in Tokena | |

| Agent’s utility denominated in Tokena | |

| Asset value denominated in Tokena | |

| Discount rate representing time preference | |

| Indicator of whether the swap succeeds () or not () | |

| Success premium | |

| Time until end of game | |

| Wiener Process drift, see Equation (2) | |

| Wiener Process variance, see Equation (2) | |

| Expectation of Tokenb price at given its time- price | |

| PDF of Tokenb price at given its time- price | |

| CDF of Tokenb price at given its time- price |

III-B Decision timeline

Let denote the time needed to look up a transaction in the mempool of Chainb after it has been initiated. This time is smaller than the transaction confirmation time on Chainb, i.e.

| ((4)) |

Let denote the points in time when agents have to make a decision, and () denote the point in time when the HTLC on Chaina (Chainb) expires. See Table II for a comprehensive list of notations used in this paper.

According the HTLC protocol described in Section I-A, an atomic swap should work as follows:

III-B1 Agreement and preparation

and agree on the swap conditions, including exchange rate , contract lock expiration time and etc. generates a secret and its hash.

III-B2 Action

uses the hash generated at to lock Tokena on Chaina through an HTLC that expires at ; thus,

| ((5)) |

uses the same hash to lock 1 Tokenb on Chainb through another HTLC that expires at .

does so only after verifying that ’s contract is in order and that its deployment has been confirmed on Chaina; thus,

| ((6)) |

uses the secret to unlock the 1 Tokenb on Chainb. does so only after verifying that ’s contract is in order and that its deployment has been confirmed on Chainb; thus,

| ((7)) |

At

uses the same secret to unlock the Tokena on Chaina. does so only after seeing the secret been revealed by in the mempool of Chainb; thus

| ((8)) |

III-B3 Receipt

Which token an agent receives, and when, depends on the outcome of the swap. If both and hold on to their agreement by following the steps during the action phase as described in Section III-B2, then the swap succeeds and and receive tokens at the following two points in time respectively:

receives the 1 Tokenb after her transaction is confirmed on Chainb, and this must take place before the lock contract expires at ; thus

| ((9)) |

receives the Tokena after his transaction is confirmed on Chaina, and this must take place before the lock contract expires at ; thus

| ((10)) |

If, however, or withdraws at any point during the action phase as described in III-B2, then the swap fails and and have their original tokens returned to them at the following two points in time respectively:

the HTLC on Chainb returns ’s original 1 Tokenb to him when the time lock expires at , and receives the 1 Tokenb at ; thus

| ((11)) |

the HTLC on Chaina returns ’s original 1 Tokena to her when the time lock expires at , and receives the Tokena at ; thus

| ((12)) |

The relationship between different points in time can thus be illustrated as 2(a).

III-C Zero waiting time

An idealized decision-making time of 0 allows the game to be characterized as a discrete one, where actions can only be taken at a specified, finite set of points in time. In this way, we can express the relationships between the critical points in time as (2(b)):

| ((14)) |

This model simplification can be justified for multiple reasons. Firstly, at the outset of the swap, it should be of both agents’ interest to agree on the terms such that the swap can be carried out in a swift manner. From a game-theoretical perspective, lengthening the decision-making time increases optionality for at , thus reducing the expected utility for . in turn would postpone his decision at until as late as possible, to maximize his own optionality and minimize ’s future optionality. in turn would wait as long as possible at to kick off the swap in order to minimize ’s future optionality and maximize her own. In turn at , is incentivised to only agree to the shortest time possible to reduce ’s optionality at .

In addition, a long lock time can reduce liquidity for and collectively. Formally, the negative impact of lock time on agents’ utility is captured by their positive discount rate , as shown in (3). Therefore, the agents would set the contract expiration time as early as possible, to reduce the time of assets being locked, in two ways:

-

1.

An agent can receive his/her counterparty’s original asset earlier rather than later in case the swap eventually succeeds. This is because an agent is forced to choose whether to continue or to withdraw immediately each time it is his/her turn to take an action; no immediate action (i.e. waiting) is equivalent to withdrawal since it precludes timely completion of necessary transactions before the contract expiration time, and thus lead to failure of the swap.

-

2.

An agent can get back his/her original asset as soon as the counterparty withdraws from the swap, i.e. when the swap eventually fails.

III-D Default parameters

We use backward induction to derive the optimal strategy for each agent. We solve for agents’ best strategy numerically and graphically, as we show later in Section III-E that it quickly becomes non-trivial to analytically derive a closed-form expression. To this end, we set the default value of certain parameters as in Table III. We additionally specify the unit of parameters to put the model into perspective. In the following, we discuss the plausibility of selected values for blockchain-specific parameters.

Transaction confirmation time

We set the confirmation time on both chains to be in the order of hours. Confirmation time in this paper refers to the time needed to reach transaction finality with a high probability, which typically equals a multiple of the block time. Given the wide adoption of the computationally heavy consensus mechanism—Proof of Work [36], it is to date still common for a blockchain to have an hour-long confirmation time.222See e.g. https://support.kraken.com/hc/en-us/articles/203325283-Cryptocurrency-deposit-processing-times

Price trend

The default value of a positive price trend suggests the deflationary nature of Tokenb, for example caused by higher levels of token buyback and burn compared to Tokena [37]. In Section III-F, we explore the possibility when Tokenb is inflationary, i.e. , and when .

Volatility

The default hourly volatility value of 10% aligns with empirical evidence [38].

In Section III-F, we inspect modelling results with an array of different values for each parameter.

As per assumption, the values of all the parameters displayed in Table III are common knowledge (i.e. knows, knows, and knows that knows etc).

III-E Backward induction

With backward induction, we start from , the last possible action point. We then move backward to an earlier action point each time, assuming the swap is still ongoing (i.e. nobody has withdrawn up until that point). Recall that we use the idealized framework where decision-making time is reduced to a point in time. That is, at each decision-making point in time, agents choose an action from the two-element action set .

III-E1

decides whether to unlock Tokena () or not (). Once has unlocked Tokenb with her pre-generated secret, it does not make sense for to withdraw and forgo the locked Tokena (which yields to zero utility). Therefore, as soon as sees the secret revealed through ’s transaction from Chainb’s mempool, uses the secret to unlock Tokena. Thus, chooses to continue with certainty.

III-E2

decides whether to unlock Tokenb () or not ().

unlocks the 1 Tokenb, and receives it at , in which case gets Tokena at .

| ((15)) | ||||

| ((16)) |

waives the contract and has the Tokena returned to her at , in which case gets 1 Tokenb at .

| ((17)) | ||||

| ((18)) |

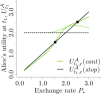

By assumption, chooses the option that maximizes her utility. Intuitively, when current Tokenb price is sufficiently large, chooses to stop so that she receives Tokenb in the end; when is sufficiently small, chooses to continue so that she receives Tokena in the end.

Let denote the cut-off price that equates and , i.e.

| ((19)) |

Clearly, increases with (see also Figure 3). This is because higher makes the option stop more attractive for , driving the threshold price higher.

’s strategy at can be summarized as:

| ((20)) |

III-E3

decides whether to write an HTLC on Chainb () or not ().

Even when chooses to continue, whether the swap eventually succeeds depends on how Tokenb price evolves until . Therefore, the utility of and at can be expressed with their time-discounted, expected utility at :

| ((21)) | ||||

| ((22)) |

withdraws from the deal and keeps 1 Tokenb at . Since already locked Tokena, she will receive her original Tokena back at .

| ((23)) | ||||

| ((24)) |

By assumption, also chooses the option that maximizes his utility. In Figure 3, and are plotted as a function of . Intuitively, if current Tokenb price is very low, then although would want to swap to receive Tokena, he can safely assume that Alice would not honor the agreement at anyway, so will not bother to continue; if is very high, then would like to keep Tokenb and won’t swap at all.

Therefore, Bob chooses when falls in a feasible range, denoted by . Figure 4 shows that this range expands and shifts to the higher end with larger .

’s strategy at can be summarized as:

| ((25)) |

Note that depending on the value of parameters, the two utility curves might not always have two intersections (disregarding the origin). For example, the lower is, the narrower the feasible range of is, because is less desperate to swap. When is sufficiently small, , and the swap always fails. This will be further discussed in Section III-F.

III-E4

decides whether to initiate the swap by writing an HTLC on Chaina () or not ().

The utility of and at can be expressed by time-discounting their expected utility at :

| ((26)) | ||||

| ((27)) |

does not initiate the swap and keeps Tokena at . also keeps his 1 Tokenb.

| ((28)) | ||||

| ((29)) |

Recall that in our idealized swap game, must initiate the swap immediately after the terms of swap are agreed upon, as allowing for waiting time only reduces agents’ utility. Therefore, and must agree on a rate that makes willing to take the first step. Intuitively, if is too high, then would not want to swap; if is too low, then understands the high likelihood of fail because would not want to continue at , so would not start the swap either.

Thus, the exchange rate must lie within a range to ensure the start of the swap (see Figure 5). Using the values from Table III we numerically solve the feasible range as:333Note that since is assumed in (14).

| ((30)) |

’s strategy at can be summarized as:

| ((31)) |

III-F Success rate

We define the success rate () of a swap to be the likelihood of completion of the swap after it has been initiated, i.e. after has made the first move at . With the values of all other parameters being fixed (Table III), is a function of , and can be expressed as:

| ((32)) |

In Figure 6, we show how success rate changes with the exchange rate . curves with the default parameter setting (Table III) are plotted in blue line ( ), which are compared with curves with different parameter values. Irrespective of the parameter values, the curve is always concave, with the -maximizing point residing between and . As suggested in Section III-E, this is because overly low reduces the likelihood of continuation at and , while overly high reduces the likelihood of continuation at .

Next, we discuss how the value setting of other parameters affects the success rate.

III-F1 Success premium

The parameter success premium describes the excess utility that an agent receives when the swap succeeds. The parameter captures not only the excess utility an agent gains from possessing the counterparty’s token over his/her own token, but also the utility of guarding his/her reputation. That is to say, the more an agent cares about honoring an agreement, the higher will be. As shown in Figure 6, ceteris paribus, higher leads to higher . This is true for both and . In addition, higher renders a bigger feasible range of . Note that when is too small (either with or ), the swap would never be initiated.

III-F2 Time preference

The parameter time preference describes an agent’s impatience level. Larger suggests a higher degree of impatience, i.e. possessing an asset right now is more valuable for the agent than obtaining it later. As an HTLC swap requires an asset-locking period, a certain degree of patience is needed for both and to enter the agreement. Thus, as shown in Figure 6, larger results in a narrower viable range of values for ; exceedingly high renders any value infeasible, i.e. the swap would never be initiated.

III-F3 Transaction confirmation time

With the presence of time preference (), longer transaction confirmation time, either on Chaina or Chainb, reduces agents’ utility in engaging in a swap. Therefore, higher or shrinks the viable range of . When is always chosen optimally (as to maximize ), lower or increases .

III-F4 Price trend and volatility

Figure 6 shows that, ceteris paribus, higher degree of upward price trend of Tokenb increases . In contrast, higher volatility reduces max .

IV Model extension

In this section, we expand on our basic model described in Section III and discuss two derivations.

IV-A HTLC with collateral

In this section, we discuss an HTLC game where both agents place collateral into a smart contract before the actual swap. All assumptions from Section III-A with the exception of Assumption 6 remain unchanged. We assume additionally:

-

1.

and move an allowance to a trusted smart contract on Chaina in order to charge each of them simultaneously the same amount of collateral, Tokena, before the swap;

-

2.

the smart contract is connected to an Oracle which observes the transaction outcomes on Chaina and Chainb;

-

3.

if the swap succeeds, the Oracle transfers to each agent their original collateral; if an agent chooses at any point during the swap, the other agent receives both agents’ collateral from the Oracle;

-

4.

agent’s utility function is as follows:

((33)) where

: value of collateral to be received back,

: time until receiving the collateral.

We use subscript “” only when an expression differs from the one in the basic setup (Section III-E).

This setup is theoretical as there is presently no Oracle service that would be able to monitor the actions as described, to the best of our knowledge. Yet, the Bisq framework is similar in spirit with the key difference that a human arbitrator replaces the Oracle. The goal of this section is to study the impact of collateralization on the agents’ behaviors and thus on the transaction outcome. A new atomic swap protocol with collateral will be discussed in a follow-up work.

We again employ backward induction to derive agents’ utility-maximizing strategy.

IV-A1

At this point, if has released the secret, the Oracle will determine that has fulfilled all her obligations and releases her collateral Tokena at . Thus, will receive Tokena at . Same as in the basic scenario described in Section III-E1, chooses to unlock Tokena () with certainty. If has not released the secret, the Oracle will transfer ’s collateral to .

IV-A2

At this point, has written an HTLC on Chainb as agreed, and hence has no further chance for foul play. The Oracle thus return’s ’s collateral, and receives Tokena at . If now waives the contract, then her utility equals as described in Equation (17) and her collateral will be transferred to be in the next step. If chooses to unlocks the 1 Tokenb, the swap succeeds and she receives Tokenb at plus her collateral Tokena at .

Therefore, chooses over if:

| ((34)) |

Since , we express ’s lower bound as:

IV-A3

decides whether to write an HTLC on Chainb () or not ().

As discussed in Section IV-A2, if chooses at this point, the Oracle will determine at that has fulfilled his obligations, and will return his collateral at that time.

In addition, expects that at , will honour the deal when in which case gets Tokena at , and waive the deal otherwise in which case Bob gets 1 Tokenb at plus ’s collateral at .

Therefore, the utility of and utility at is:

| ((35)) | ||||

| ((36)) |

withdraws from the deal and keep 1 Tokenb. ’s utility is the same as Equation (24). The swap stops due to ’s foul play. The Oracle thus releases both agents collateral, in total, to at , who will receive the fund at .

Intuitively, if is too high, then would like to keep the valuable Tokenb and wouldn’t want to swap, and would therefore choose ; if is too low (say, close to zero), forfeiting the valuable collateral to keep the worthless TokenB would not be sensible—even if chooses not to reveal secret in the next step, would at least be able to receive the collateral; therefore, would choose .

Thus, Equation has an odd number of roots. Figure 7 shows that there can be 1 or 3 intercepts between curve and , depending on the value of and . Define set such that:

Hence, would choose if and only if falls in .

IV-A4

and simultaneously make the decision on whether to engage in the swap () or not ().

The utility of and at can be expressed with their time-discounted, expected utility at :

| ((37)) | ||||

| ((38)) |

and decide not to engage in the swap so that they can keep their original token and the collateral. Thus:

| ((39)) | ||||

| ((40)) |

Define set and such that:

Hence, the exchange rate must be in , since otherwise agents’ external utility () exceeds the expected utility from the swap () and the swap would not be initiated (see Figure 8).

The swap’s success rate can thus be expressed as:

| ((41)) |

Figure 9 shows increases with collateral amount . This is because higher allows for larger price movement, by expanding the feasible Tokenb price range at both (see Figure 7) and (see Equation (34)).

IV-B Uncertain exchange rate

In this model variation, we discuss an HTLC game in which agents not only choose between and , but also the exact amount of funds to lock in: Tokena at and Tokenb , respectively. This renders the actual exchange rate uncertain at the outset of the game. We apply subscript “” for expressions different from their counterpart in the baseline model.

IV-B1

Same as Section III-E1

IV-B2

IV-B3

determines the value of that maximizes his excess utility, namely the utility he obtains by proceeding with locking less the utility he keeps by retaining Tokenb.

| ((43)) | ||||

| ((44)) |

Denote the optimal as , a function of . Thus,

| ((45)) |

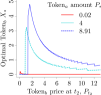

10(a) shows at any given amount of Tokena that has locked at , , the optimal amount of Tokenb that should lock first increases and then decreases with .

This aligns with the intuition that when is too low, i.e. Tokenb is valueless, then the likelihood of ’s withdrawal at is high, making unwilling to lock in big funds at ; when is too high, i.e. Tokenb is very valuable, then the amount of Tokenb that needs to commit also becomes low to make the deal worthwhile for himself. Generally at a given , increases with , reflecting a degree of fairness of the game.

IV-B4

takes into account the fact that will choose an amount of Tokenb to lock in at that maximizes his own utility, based on Tokenb price at and the amount of Tokena that she commits, .

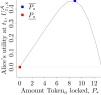

thus chooses the value of that maximizes her excess utility, namely the utility she obtains by entering the swap with Tokena in excess of the utility she keeps by retaining Tokena. Therefore,

Similar to Figure 5, 10(b) shows that the excess utility first increases and then decreases with . represents the amount that maximizes . Nevertheless, might only be able to afford a lesser amount due to a possible budget constraint on her side. represents the lowest possible amount that needs to enter for a non-negative excess utility.

We can express the swap’s success rate under uncertain exchange rate as:

| ((47)) |

Figure 11 compares the success rate between the basic setup and the scenario with uncertain exchange rate. Interestingly, absence of pre-determined interest rate boosts the success rate.

V Discussion

V-A Interpretation of findings

Multiple findings can be drawn from our analysis that are relevant for real-world applications. It has previously been mentioned that the agent completing the transaction receives a free American option, meaning that she has the choice to complete the transaction, or not, based on whether the asset price changes at her advantage. However, in this work, we show that the other agent (not only the swap initiator) may also leave the game midway, incentivized by a potentially higher financial gain. This scenario has thus far been neglected in the literature.

Our analysis also suggests that the collateral deposits can be dynamically adjusted depending on the terms of the swap (e.g. exchange rate) and optimization goal (e.g. maximizing utility, or maximizing success rate).

In the last model extension we show that the likelihood of completing the transaction is higher when the agents dynamically adjust the exchange rate to account for token price fluctuations. This is because an arbitrarily fixed exchange rate takes away the flexibility for agents to adjust their commitment based on the latest market condition (price change in our case).

V-B Limitations and future work

Our work motivates multiple future research directions.

Firstly, simulation studies can be performed based on our model framework and its derivation using real market data.

Secondly, trustless protocols supporting collateral deposit without a third party can be designed. To date, collaterals are typically deposited at a trusted third party in practice which is then responsible for resolving payment disputes. For instance, Bisq [8], an information platform for quotes and P2P transactions with arbitrators, uses a postage of collateral with possible intervention of an arbitrator, thus providing only a limited level of “distributiveness” and still requiring some trust in the arbitration system. Note that transactions executed via Bisq require a collateral deposit and an arbitrator fee. Discussion with community members revealed that 3-5% of transactions fail and go to arbitration, and that this percentage increases during periods of higher market volatility.

Thirdly, HTCL protocols can be further improved. HTLCs have known limitations [27, 39], including strong assumptions required to maintain security, interactiveness, exclusiveness to public blockchains (for public mempools), and the need for synchronizing clocks between blockchains and temporal locking of assets.

Lastly, a more realistic and sophisticated setup can be brought into our framework. For example, future models may incorporate different risk-free rates for the two exchanged tokens, which resembles the settings of the Garman Kohlhagen model. In addition, blockchain transaction fees or coin stacking (similar to earning dividends or interest on a locked-in asset) may have an impact on agents’ actions. Our model can also be extended to consider repeated games, stochastic individual utility, success premium as a random variable, etc.

VI Conclusion

We introduce a game-theoretic approach to model agent behaviors in cross-ledger transactions. This allows us to study the viability and sensitivity of different protocols with respect to environment variables: agents’ knowledge and utility functions, and the price dynamics. We study in-depth the atomic swap as implemented with hash time lock contracts, for which we derived the success rate of a transaction. In particular, we showed that both transacting counterparties can rationally decide to walk away from the transaction, and at different times. This is a more realistic setup that relaxes the assumptions from previous works [30, 40] that only the swap initiator can benefit from price variation and act upon it. A sensitivity analysis reveals that price volatility significantly affects the success rate of the transaction.

We extend our basic setup along two directions. First, we show that introducing collateral deposit, in a purely theoretical way, increases the success rate of the transaction. Second, we sketch out the scenario where agents are uncertain about the amount of funds their counterparty intends to commit.

Two important conclusions are therefore that cross-ledger atomic swap trustless protocols could benefit from the use of disciplinary mechanisms, such as collateral deposit, and that allowing agents to dynamically adjust the swap amount can increase the success rate.

References

- [1] H. Garcia-Molina, “Using semantic knowledge for transaction processing in a distributed database,” ACM Transactions on Database Systems (TODS), vol. 8, no. 2, pp. 186–213, 1983.

- [2] J. Xu, K. Paruch, S. Cousaert, and Y. Feng, “SoK: Decentralized Exchanges (DEX) with Automated Market Maker (AMM) protocols,” 2022. [Online]. Available: http://arxiv.org/abs/2103.12732

- [3] T. Moore and N. Christin, “Beware the middleman: Empirical analysis of Bitcoin-exchange risk,” in International Conference on Financial Cryptography and Data Security. Springer, 2013, pp. 25–33.

- [4] “Details of $5 Million Bitstamp Hack Revealed.” [Online]. Available: https://www.coindesk.com/unconfirmed-report-5-million-bitstamp-bitcoin-exchange

- [5] “Crypto Exchange Bitfinex Bounces Back after a DDoS Attack.” [Online]. Available: https://www.ccn.com/crypto-exchange-bitfinex-bounces-back-after-a-ddos-attack

- [6] “itBit.” [Online]. Available: https://www.itbit.com/otc

- [7] “HiveEx-Large Volume Cryptocurrency OTC Brokerage.” [Online]. Available: https://www.hiveex.com

- [8] “Bisq White Paper.” [Online]. Available: https://docs.bisq.network/exchange/whitepaper.html

- [9] “Decred-compatible cross-chain atomic swapping,” 2018. [Online]. Available: https://github.com/decred/atomicswap/

- [10] Komodo, “Komodo’s Atomic-Swap Powered, Decentralized Exchange: Barterdex,” 2021. [Online]. Available: https://docs.komodoplatform.com/whitepaper/chapter6.html

- [11] “0x White paper.” [Online]. Available: https://0x.org/pdfs/0x_white_paper.pdf

- [12] “Bitcoin Wiki: Atomic cross-chain trading.” [Online]. Available: https://en.bitcoin.it/wiki/

- [13] J. Kirsten and H. Davarpanah, “Anonymous Atomic Swaps Using Homomorphic Hashing,” Available at SSRN 3235955, 2018.

- [14] G. Zyskind, C. Kisagun, and C. Fromknecht, “Enigma Catalyst: A machine-based investing platform and infrastructure for crypto-assets,” 2018.

- [15] J. A. Liu, “Atomic Swaptions: Cryptocurrency Derivatives,” arXiv preprint arXiv:1807.08644, 2018.

- [16] “Building Super Financial Markets for the New Economy.” [Online]. Available: https://wanchain.org/files/Wanchain-Whitepaper-EN-version.pdf

- [17] R. L. Rivest, A. Shamir, and Y. Tauman, “How to leak a secret: Theory and applications of ring signatures,” in Theoretical Computer Science. Springer, 2006, pp. 164–186.

- [18] S. Thomas and E. Schwartz, “A protocol for interledger payments,” 2015. [Online]. Available: https://interledger.org/interledger.pdf

- [19] Interledger, “STREAM: A Multiplexed Money and Data Transport for ILP,” 2020. [Online]. Available: https://github.com/interledger/rfcs/blob/master/0029-stream/0029-stream.md

- [20] A. Dubovitskaya, D. Ackerer, and J. Xu, “A Game-Theoretic Analysis of Cross-ledger Swaps with Packetized Payments,” in Workshop Proceedings of Financial Cryptography and Data Security, 2021, pp. 177–187. [Online]. Available: https://link.springer.com/10.1007/978-3-662-63958-0_16

- [21] “Btc relay.” [Online]. Available: https://github.com/ethereum/btcrelay

- [22] A. Back, M. Corallo, L. Dashjr, M. Friedenbach, G. Maxwell, A. Miller, A. Poelstra, J. Timón, and P. Wuille, “Enabling blockchain innovations with pegged sidechains,” URL: http://www. opensciencereview. com/papers/123/enablingblockchain-innovations-with-pegged-sidechains, 2014.

- [23] S. Johnson, P. Robinson, and J. Brainard, “Sidechains and interoperability,” arXiv preprint arXiv:1903.04077, 2019.

- [24] J. Poon and T. Dryja, “The bitcoin lightning network: Scalable off-chain instant payments,” 2016.

- [25] L. Luu, V. Narayanan, C. Zheng, K. Baweja, S. Gilbert, and P. Saxena, “A secure sharding protocol for open blockchains,” in Proceedings of the 2016 ACM SIGSAC Conference on Computer and Communications Security. ACM, 2016, pp. 17–30.

- [26] A. Miller, I. Bentov, R. Kumaresan, and P. McCorry, “Sprites: Payment channels that go faster than lightning,” arXiv preprint arXiv:1702.05812, 2017.

- [27] A. Zamyatin, D. Harz, J. Lind, P. Panayiotou, A. Gervais, and W. Knottenbelt, “XCLAIM: Trustless, interoperable, cryptocurrency-backed assets,” in IEEE Symposium on Security and Privacy. IEEE, 5 2019, pp. 193–210. [Online]. Available: https://ieeexplore.ieee.org/document/8835387/

- [28] M. Borkowski, D. McDonald, C. Ritzer, and S. Schulte, “Towards Atomic Cross-Chain Token Transfers: State of the Art and Open Questions within TAST,” Distributed Syste ms Group, TU Wien (Technische Universität Wien), Vienna, Austria, Tech. Rep, 2018.

- [29] M. Herlihy, “Atomic cross-chain swaps,” in Proceedings of the 2018 ACM Symposium on Principles of Distributed Computing, ACM. Association for Computing Machinery, 7 2018, pp. 245–254.

- [30] R. Han, H. Lin, and J. Yu, “On the optionality and fairness of Atomic Swaps,” in AFT 2019 - Proceedings of the 1st ACM Conference on Advances in Financial Technologies. New York, New York, USA: ACM Press, 2019, pp. 62–75. [Online]. Available: http://dl.acm.org/citation.cfm?doid=3318041.3355460

- [31] E. Heilman, S. Lipmann, and S. Goldberg, “The Arwen Trading Protocols (Full Version).” [Online]. Available: https://eprint.iacr.org/2020/024.pdf

- [32] V. Zakhary, D. Agrawal, and A. E. Abbadi, “Atomic commitment across blockchains,” arXiv preprint arXiv:1905.02847, 2019.

- [33] M. Herlihy, B. Liskov, and L. Shrira, “Cross-chain Deals and Adversarial Commerce,” Proceedings of the VLDB Endowment, vol. 13, no. 2, pp. 100–113, 2019. [Online]. Available: http://www.vldb.org/pvldb/vol13/p100-herlihy.pdf

- [34] M. Belotti, S. Moretti, M. Potop-Butucaru, and S. Secci, “Game theoretical analysis of Atomic Cross-Chain Swaps,” 2020. [Online]. Available: https://hal.archives-ouvertes.fr/hal-02414356

- [35] TierNolan, “Atomic swaps using cut and choose,” 2016. [Online]. Available: https://bitcointalk.org/index.php?topic=1364951

- [36] M. S. Ferdous, M. J. M. Chowdhury, M. A. Hoque, and A. Colman, “Blockchain Consensus Algorithms: A Survey,” 1 2020. [Online]. Available: http://arxiv.org/abs/2001.07091

- [37] S. Tang and S. S. Chow, “Systematic market control of cryptocurrency inflations: Work-in-progress,” in 2nd ACM Workshop on Blockchains, Cryptocurrencies, and Contracts. New York, New York, USA: ACM Press, 2018, pp. 61–63. [Online]. Available: http://dl.acm.org/citation.cfm?doid=3205230.3205240

- [38] Digiconomist, “Guide to Cryptocurrency Volatility,” 2014. [Online]. Available: https://digiconomist.net/guide_to_cryptocurrency_volatility/

- [39] T. Koensa and E. Polla, “Assessing Interoperability Solutions for Distributed Ledgers.” [Online]. Available: https://www.ingwb.com/media/2667864/assessing-interoperability-solutions-for-distributed-ledgers.pdf

- [40] T. Eizinger, L. Fournier, and P. Hoenisch, “The state of atomic swaps,” 2018. [Online]. Available: http://diyhpl.us/wiki/transcripts/scalingbitcoin/tokyo-2018/atomic-swaps/