Functional Linear Regression with Mixed Predictors

Abstract

We study a functional linear regression model that deals with functional responses and allows for both functional covariates and high-dimensional vector covariates. The proposed model is flexible and nests several functional regression models in the literature as special cases. Based on the theory of reproducing kernel Hilbert spaces (RKHS), we propose a penalized least squares estimator that can accommodate functional variables observed on discrete sample points. Besides a conventional smoothness penalty, a group Lasso-type penalty is further imposed to induce sparsity in the high-dimensional vector predictors. We derive finite sample theoretical guarantees and show that the excess prediction risk of our estimator is minimax optimal. Furthermore, our analysis reveals an interesting phase transition phenomenon that the optimal excess risk is determined jointly by the smoothness and the sparsity of the functional regression coefficients. A novel efficient optimization algorithm based on iterative coordinate descent is devised to handle the smoothness and group penalties simultaneously. Simulation studies and real data applications illustrate the promising performance of the proposed approach compared to the state-of-the-art methods in the literature.

Keywords: Reproducing kernel Hilbert space, functional data analysis, high-dimensional regression, minimax optimality.

1 Introduction

Functional data analysis is the collection of statistical tools and results revolving around the analysis of data in the form of (possibly discrete samples of) functions, images and more general objects. Recent technological advancement in various application areas, including neuroscience (e.g. Petersen et al., 2019; Dai et al., 2019), medicine (e.g. Chen et al., 2017; Ratcliffe et al., 2002), linguistic (e.g. Hadjipantelis et al., 2015; Tavakoli et al., 2019), finance (e.g. Fan et al., 2014; Benko, 2007), economics (e.g. Yan, 2007; Ramsay and Ramsey, 2002), transportation (e.g. Chiou et al., 2014; Wagner-Muns et al., 2017), climatology (e.g. Fraiman et al., 2014; Bonner et al., 2014), and others, has spurred an increase in the popularity of functional data analysis.

The statistical research in functional data analysis has covered a wide range of topics and areas. We refer the readers to a recent comprehensive review (Wang et al., 2016). In this paper, we are concerned with a general functional linear regression model that deals with functional responses and accommodates both functional and vector covariates.

By rescaling if necessary, without loss of generality, we assume the domain of the functional variables is . Let be a bivariate coefficient function and be a collection of univariate coefficient functions. The functional linear regression model concerned in this paper is as follows:

| (1) |

where is the functional response, is the functional covariate, is the vector covariate and is the functional noise such that and for all . The index denotes independent and identically distributed samples. The vector dimension is allowed to diverge as the sample size grows unbounded. Furthermore, instead of assuming the functional variables are fully observed, we consider a more realistic setting where the functional covariates and responses are only observed on discrete sample points and , respectively. The two collections of sample points do not need to coincide.

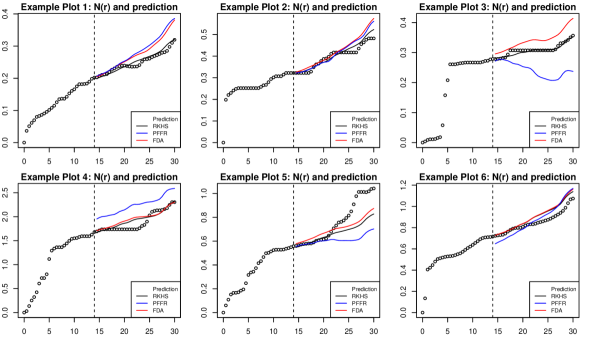

As an important real-world example, consider a dataset collected from the popular crowdfunding platform kickstarter.com (see more details in Section 5.4). The website provides a platform for start-ups to create fundraising campaigns and charges a 5% service fee from the final fund raised by each campaign over its 30-day campaign duration. Denote as the pledged fund for the campaign indexed by at time . Note that forms a fundraising curve. For both the platform and the campaign creators, it is of vital interest to generate an accurate prediction of the future fundraising path at an early time , as the knowledge of helps the platform better assess its future revenue and further suggests timing along for potential intervention by the creators and the platform to boost the fundraising campaign and achieve better outcome.

At time , to predict the functional response , i.e. , a functional regression as proposed in model (1) can be built based on the functional covariate , i.e. , and vector covariates such as the number of creators and product updates of campaign . Figure 1 plots the normalized fundraising curves of six representative campaigns and the functional predictions given by our proposed method (RKHS) and two competitors, FDA in Ramsay and Silverman (2005) and PFFR in Ivanescu et al. (2015). In general, the proposed method achieves more favorable performance. More detailed real data analysis is presented in Section 5.4.

1.1 Literature review

As mentioned in recent reviews, e.g. Wang et al. (2016) and Morris (2015), there are in general three types of functional linear regression models: 1) functional covariates and scalar or vector responses (e.g. Cardot et al., 2003; Cai and Hall, 2006; Hall and Horowitz, 2007; Yuan and Cai, 2010; Raskutti et al., 2012; Cai and Yuan, 2012; Jiang et al., 2014; Fan et al., 2015); 2) functional covariates and functional responses (e.g. Wu et al., 1998; Liang et al., 2003; Yao et al., 2005; Fan et al., 2014; Ivanescu et al., 2015; Sun et al., 2018) and 3) vector covariates and functional responses (e.g. Laird and Ware, 1982; Li and Hsing, 2010; Faraway, 1997; Wu and Chiang, 2000). Another closely related area is functional time series. For instance, functional autoregressive models also preserve the regression format. The literature on functional time series is also abundant, including van Delft et al. (2017), Aue et al. (2015), Bathia et al. (2010), Wang et al. (2020a) and many others.

Regarding the sampling scheme, to establish theoretical guarantees, it is often assumed in the literature that functions are fully observed, which is generally untrue in practice. To study the properties of functional regression under the more realistic scenario where functions are observed only on discrete sample points, one usually imposes certain smoothness conditions on the underlying functions. The errors introduced by the discretization of functions can therefore be controlled as a function of the smoothness level and , the number of discretized observations available for each function. Some fundamental tools regarding this aspect were established in Mendelson (2002) and Bartlett et al. (2005), and were further applied to various regression analysis problems (e.g. Raskutti et al., 2012; Koltchinskii and Yuan, 2010; Cai and Yuan, 2012).

Regarding the statistical inference task, in the regression context, estimation and prediction are two indispensable pillars. In the functional regression literature, Valencia and Yuan (2013), Cai and Yuan (2011), Yuan and Cai (2010), Lin and Yuan (2006), Park et al. (2018), Fan et al. (2014), Fan et al. (2015), and Reimherr et al. (2019), among many others, have studied different aspects of the estimation problem. As for prediction, the existing literature includes Cai and Yuan (2012), Cai and Hall (2006), Ferraty and Vieu (2009), Sun et al. (2018), Reimherr et al. (2018) to name but a few.

In contrast to the aforementioned three paradigms of functional regression, in this paper, we study the functional linear regression problem in model (1) with functional responses and mixed predictors that consist of both functional and vector covariates. We assume the functions are only observed on discrete sample points and aim to derive optimal upper bounds on the excess prediction risk (see Definition 1). More detailed comparisons with existing literature are deferred till we present the main results in Section 3.

1.2 Main contributions

The main contributions of this paper are summarized as follows.

Firstly, to the best of our knowledge, the model we study in this paper, as defined in (1), is among the most flexible ones in the literature of functional linear regression. In terms of predictors, we allow for both functional and vector covariates. In terms of model dimensionality, we allow for the dimension of vector covariates to grow exponentially as the sample size diverges. In terms of function spaces, which will be elaborated later, we allow for the coefficients of the functional and vector covariates to be from different reproducing kernel Hilbert spaces (RKHS). In terms of dependence between the functional and vector covariates, we allow the correlation to be of order up to , which is a rather weak condition, especially considering that the vector covariates are of high dimensions. In terms of the sampling scheme, we allow for the functional covariate and response to be observed on (possibly different) discretized sample points. This general and unified framework imposes new challenges on both theory and optimization, as we elaborate in detail later.

Secondly, we develop new peeling techniques in our theoretical analysis, which is crucial and fundamental in dealing with the potentially exponentially growing vector covariate dimension. Existing asymptotic analysis techniques and results in the functional regression literature are insufficient to provide Lasso-type guarantees with the presence of high-dimensional covariates. See Remark 2 for more details.

Thirdly, we demonstrate an interesting phase transition phenomenon in terms of the smoothness of the functional covariate and the dimensionality of the vector covariate. To be specific, let be the sparsity of , i.e. the number of non-zero univariate coefficient functions. Let be a quantity jointly determined by the complexities and the alignment of the two RKHS’s where the functional covariates and the bivariate coefficient function reside; see Theorem 2 for the detailed definition of . We show that the excess prediction risk of our proposed estimator is upper bounded by

-

•

When , the excess risk is dominated by , which is the standard excess risk rate in the high-dimensional parametric statistics literature (e.g. Bühlmann and van de Geer, 2011). Therefore, the difficulty is dominated by estimating , the univariate coefficient functions.

-

•

When , the excess risk is dominated by , which suggests that the difficulty is dominated by estimating the bivariate coefficient function . We show that in this regime, the optimal excess risk of model (1) is of order . As a result, in this regime the difficulty is dominated by estimating the bivariate coefficient function .

-

•

We further develop matching lower bounds to justify that this phase transition between high-dimensional parametric rate and the non-parametric rate is indeed minimax optimal; see Section 3.3. To the best of our knowledge, this is the first time such phenomenon is observed in the functional regression literature.

Note that, this phase transition and its associated optimality are not with respect to the discretization error, i.e. - the minimum number of observations obtained for each function.

Lastly, we derive a representer theorem and further propose a novel optimization algorithm via iterative coordinate descent, which efficiently solves a sophisticated penalized least squares problem with the presence of both a ridge-type smoothing penalty and a group Lasso-type sparsity penalty.

The rest of the paper is organized as follows. In Section 2, we introduce relevant definitions and quantities. The main theoretical results are presented in Section 3. The optimization procedure is discussed in Section 4. Numerical experiments and real data applications are conducted in Section 5 to illustrate the favorable performance of the proposed estimator over existing approaches in the literature. Section 6 concludes with a discussion.

Notation

Let denote the collection of positive integers. Let and be two quantities depending on . We say that if there exists and an absolute constant such that for any , . We denote , if and . For any function , denote

For any and , let .

Let be the space of all square integrable functions with respect to the uniform distribution on , i.e. . For any , let be the Sobolev space of order . For a positive integer , we have

where is the -th weak derivative of , . In this case the Sobolev norm of is defined as

For non-integer valued , the Sobolev space and the norm are also well-defined (e.g. see Brezis, 2010). Note that if , then .

2 Background

In this section, we provide some background on the fundamental tools used in this paper, with RKHS and compact linear operators studied in Section 2.1 and Section A.1, respectively.

2.1 Reproducing kernel Hilbert spaces (RKHS)

Consider a Hilbert space and its associated inner product , under which is complete. We assume that there exists a continuous symmetric nonnegative-definite kernel function such that the space is an RKHS, in the sense that for each , the function and , for all . To emphasize this relationship, we write as an RKHS with as the associated kernel. For any , we say it is a bounded kernel if .

It follows from Mercer’s theorem (Mercer, 1909) that there exists an orthonormal basis of , , such that a non-negative definite kernel function has the representation where are the eigenvalues of and are the corresponding eigenfunctions. In the rest of this paper, when there is no ambiguity, we drop the dependence of ’s and ’s on their associated kernel function for ease of notation.

Note that any function can be written as

and its RKHS norm is defined as Thus, for the eigenfunctions, we have . Throughout this section, we further denote and note that for .

Define the linear map , associated with , as . It holds that , for . Furthermore, define such that , and define such that , for . For any two bivariate functions , define , . It holds that , where represents the composition of and , which is a linear map from to given that both and are linear maps from to .

2.2 Bivariate functions and compact linear operators

To regulate the bivariate coefficient function in model (1), we consider a class of compact linear operators in . Specifically, for any compact linear operator , denote

Note that is well defined for any due to the compactness of . Let be the eigenbasis of and , . We thus have for any , it follows from Remark 4 in the appendix that

| (2) |

Note that via (2), we can define a bivariate function , affiliated with the compact operator . Specifically, plugging and into (2), we have that

From the above set up, it holds that for all , we have

We have established an equivalence between a compact linear operator and its corresponding bivariate function , therefore any compact linear operator can be viewed as a bivariate function .

To facilitate the later formulation of penalized convex optimization and the derivation of the representer theorem, we further focus on the Hilbert–Schmidt operator, which is an important subclass of compact operators. A compact operator is Hilbert–Schmidt if

| (3) |

In the rest of this paper, for ease of presentation, we adopt some abuse of notation and refer to compact linear operators and the corresponding bivariate functions by the same notation .

3 Main results

3.1 The constrained/penalized estimator and the representer theorem

Recall that in model (1), the response is the function , the covariates include the function and vector , and the unknown parameters are the bivariate coefficient function and univariate coefficient functions . Given the observations , our main task is to estimate and .

Define the weight functions for and for , where by convention we set . In addition, for any , define

We propose the following constrained/penalized least squares estimator

| (4) |

where is a tuning parameter that controls the group Lasso penalty, and characterize the spaces of coefficient functions and respectively such that

| (5) |

Here are two absolute constants and is defined in (3). Note that we allow the RKHS’s and to be generated by two different kernels and . The detailed optimization scheme is deferred to Section 4.

The above optimization problem essentially constrains three tuning parameters. The tuning parameters and control the smoothness of the regression coefficient functions. These constrains are standard and ubiquitous in the functional data analysis and non-parametric statistical literature. The tuning parameter controls the group Lasso penalty, which is used to encourage sparsity when the dimensionality diverges faster than the sample size .

The optimization problem in (3.1) makes use of the weight functions and , which are determined by the discrete sample points and respectively. This is designed to handle the scenario where the functional variables are observed on unevenly spaced sample points. Indeed, for evenly spaced sample points and , we have that for all . We remark that it is well known that the integral of a regular function can be well approximated by its weighted sum evaluated at discrete sample points.

Note that (3.1) is an infinite dimensional optimization problem. Fortunately, Proposition 1 states that the estimator can in fact be written as linear combinations of their corresponding kernel functions evaluated at the discrete sample points and .

Proposition 1

Denote and as the RKHS kernels of and respectively. There always exists a minimizer of (3.1) such that,

and

Proposition 1 is a generalization of the well-known representer theorem for RKHS (Wahba, 1990). Various versions of representer theorems are derived and used in the functional data analysis literature (e.g. Yuan and Cai, 2010).

3.2 Model assumptions

To establish the optimal theoretical guarantees for the estimator , we impose some mild model assumptions, on the coefficient functions (1), functional and vector covariates (2) and sampling scheme (3).

Assumption 1 (Coefficient functions)

-

(a)

The bivariate coefficient function belongs to defined in (5), where is the RKHS associated with a bounded kernel and is an absolute constant.

-

(b)

The univariate coefficient functions belong to defined in (5), where is the RKHS associated with a bounded kernel and is an absolute constant.

In addition, there exists a set such that for all and there exists a sufficiently large absolute constant such that

(6) where denotes the cardinality of the set .

1(a) requires the bivariate coefficient function to be a Hilbert–Schmidt operator mapping from to . 1(b) imposes smoothness and sparsity conditions on the univariate coefficient functions to handle the potential high-dimensionality of the vector covariate. Note that we allow to be from a possibly different RKHS than and thus would allow users to choose kernels based on their practical needs.

Assumption 2 (Covariates)

-

(a)

The functional noise is a collection of independent and identically distributed Gaussian processes such that and for all . In addition, are independent of .

-

(b)

The functional covariate is a collection of independent and identically distributed centered Gaussian processes with covariance operator and

-

(c)

The vector covariate is a collection of independent and identically distributed Gaussian random vectors from , where is a positive definite matrix such that

and are absolute constants.

-

(d)

For any deterministic and deterministic , it holds that

2(a) and (b) state that both the functional noise and functional covariates are Gaussian processes. In fact, one could further relax them to be sub-Gaussian processes. Such assumptions are frequently used in high-dimensional functional literature such as Kneip et al. (2016) and Wang et al. (2020b). 2(d) allows that the functional and vector covariates to be correlated up to , which means that the correlation, despite the functional and high-dimensional nature of the problem, can be of order . We do not claim the optimality of the constant but emphasize that this correlation cannot be equal to one, as detailed in Section A.2.

Assumptions 1 and 2 are sufficient for establishing theoretical guarantees if we require all functions (i.e. the functional responses and functional covariates) to be fully observed, which is typically not realistic in practice. To allow for discretized observations, we further introduce assumptions on the sampling scheme and on the smoothness of the functional covariates.

Assumption 3 (Sampling scheme)

-

(a)

The discrete sample points and are collections of points with and , and there exists an absolute constant such that

where by convention we set .

-

(b)

Suppose that for some . In addition, suppose that

(7)

3(a) allows the functional variables to be partially observed on discrete sample points. Importantly, 3(a) can accommodate both fixed and random sampling schemes. In particular, suppose the sample points are randomly generated from an unknown distribution on with a density function such that , we have 3(a) holds with high probability. We refer to Theorem 1 of Wang et al. (2014) for more details.

To handle the partially observed functional variables, 3(b) imposes the smoothness assumption that , and can be enclosed by a common superset, the Sobolev space . In particular, (7) is a commonly used assumption for bivariate function estimation in the functional data analysis literature. See for example, Cai and Yuan (2010) and Wang et al. (2020b) and references therein. We emphasize that 3(b) indeed allows different smoothness levels for , and , and only requires that the least smooth space among , and is covered by .

The condition (7) requires that the second moment of is finite, which implies almost surely. Due to the fact that the functional covariates are partially observed, to derive finite-sample guarantees, we need to establish uniform control over the approximation error

This requires the realized sample paths to be regular. In particular, the second moment condition in (7) can be used to show that are bounded with high probability, which implies are Hölder smooth with Hölder parameter by the Morrey inequality (see Theorem 32 in Appendix E.1 for more details). In Example 1 in Section A, we further provide a concrete example to illustrate a sufficient condition for (7).

3.3 Theoretical guarantees

With the assumptions in hand, we establish theoretical guarantees and investigate the minimax optimality of the proposed estimator (3.1), via the lens of excess risk defined in Definition 1. The derivation of (8) is collected in Lemma 31.

Definition 1 (Excess prediction risk)

Remark 1

Definition 1 is ubiquitously used to measure prediction accuracy in regression settings. Excess risks are usually considered to provide better quantification of prediction accuracy for the estimators of interest than the error bounds. Consequently, throughout our paper, we evaluate our proposed estimators using excess risks. We remark that as pointed out by Cai and Hall (2006) and Cai and Yuan (2012), much of the practical interest in the functional regression parameters is centered around applications for the purpose of prediction.

We are now ready to present our main results, which provide upper and lower bounds on the excess risk of the proposed estimator defined in (3.1). For notational simplicity, in the following, we assume without loss of generality that . For , all the statistical guarantees continue to hold by setting .

Upper bounds

Theorem 2

Under Assumptions 1, 2 and 3, suppose that the eigenvalues of the linear operator satisfy

| (9) |

for some . Let be any solution to (3.1) with the tuning parameter for some sufficiently large constant . For any , there exists an absolute constant such that with probability at least , it holds that

| (10) |

where , is the sparsity parameter defined in 1(b) and .

Theorem 2 provides a high-probability upper bound on the excess risk . The result is stated in a general way for any RKHS’s and , provided that the spectrum of satisfies the polynomial decay rate in (9). There are three components in the upper bound in (10).

-

•

The term is an upper bound on the error associated with the estimation of the bivariate coefficient function in the presence of functional noise. As formally stated in (9), is determined by the alignment between the kernel of the RKHS that resides in and the covariance operator of . This is the well-known nonparametric rate frequently seen in the functional regression literature, see e.g. Cai and Yuan (2012).

-

•

The term is an upper bound on the error associated with the estimation of the high-dimensional sparse univariate coefficient functions and is a parametric rate frequently seen in the high-dimensional linear regression settings (e.g. Bühlmann and van de Geer, 2011).

-

•

The term is an upper bound on the error due to the fact that the functional variables are only observed on discrete sample points. Recall model (1) consists of two components and . The discretization errors are captured through , which only depends on the smoothness of with .

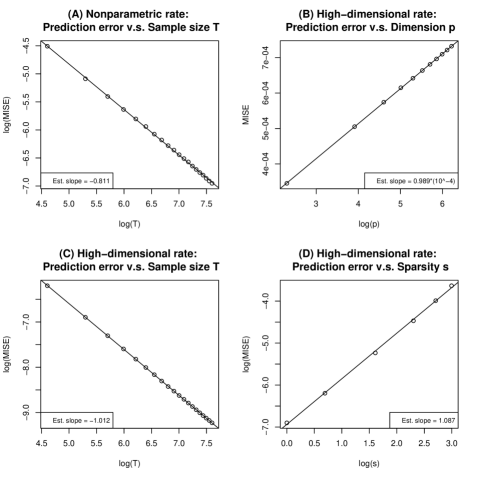

We show later in Proposition 3 that, provided the sample points are dense enough, e.g. , up to a logarithmic factor of , this upper bound achieves minimax optimality. In Section L, we further provide numerical illustration for the nonparametric rate and the high-dimensional parametric rate in Theorem 2.

Remark 2 (New peeling techniques)

To prove Theorem 2, we develop new peeling techniques to obtain new exponential tail bounds, which are crucial in dealing with the potentially exponentially growing dimension .

Remark 3 (Phase transition)

For sufficiently many samples, i.e. large , the upper bound in (10) implies that, there exists an absolute constant such that with large probability

This unveils a phase transition between the nonparametric regime and the high-dimensional parametric regime, governed by the eigen-decay of the linear operator and the sparsity of the univariate coefficient functions . To be specific, if , the high-probability upper bound on the excess risk is determined by the nonparametric rate ; otherwise, the high-dimensional parametric rate dominates.

Corollary 11 in Section B.2 further presents a formal theoretical guarantee which quantifies a discretized version of the excess risk defined in Definition 1 for the proposed estimators . Due to the fact that the functional variables are only partially observed on discrete sample points, the discretized version of the excess risk can be more relevant in certain practical applications.

Lower bounds

In this section, we derive a matching lower bound on the excess risk and thus show that the upper bound provided in Theorem 2 is nearly minimax optimal in terms of the sample size , the dimension and the sparsity parameter , saving for a logarithmic factor. We establish the lower bound under the assumption that the functional variables are fully observed, which is equivalent to setting . Thus, we do not claim optimality in terms of the number of sample points for the result in Theorem 2.

Proposition 3

3.4 Extension to functional responses with measurement errors

In this subsection, we consider the setting where the functional responses are corrupted with measurement errors. More precisely, let the functional response be generated as in (1). Assume we observe

where is a collection of independent and identically distributed sub-Gaussian measurement errors with mean zero and .

Given the observations ,

consider

| (11) |

where and are defined in (5). Note that without the presence of measurement errors, i.e. for all and , the estimator (3.4) is identical to (3.1) proposed for the setting with only functional noise. In what follows, we show that the excess risk of the estimator (3.4) also achieves the same convergence rate as that in Theorem 2.

Theorem 4

4 Optimization

In this section, we propose an efficient convex optimization algorithm for solving (3.1) given the observations . We remark that identical optimization can be applied to (3.4). To ease presentation, in the following we assume without loss of generality that , and thus . The general case where can be handled in exactly the same way with more tedious notation. Section 4.1 formulates (3.1) as a convex optimization problem and Section 4.2 further proposes a novel iterative coordinate descent algorithm to efficiently solve the formulated convex optimization.

4.1 Formulation of the convex optimization

By the equivalence between constrained and penalized optimization (see e.g. Hastie et al., 2009), we can reformulate (3.1) into a penalized optimization such that

| (13) |

where denote tuning parameters. Note that for notational simplicity, we drop the factor of the squared loss. In the following, we show that (4.1) can be solved via convex optimization.

We first define some necessary notation. For , denote the functional curves observed on discrete grids as

Define and

For any , denote the RKHS kernels as

Denote and . Note that and , thus both are symmetric and positive definite matrices. Furthermore, denote and as the diagonal weight matrices. Define , and .

By the representer theorem (Proposition 1), we have the minimizer of (4.1) taking the form

where is an matrix and is an -dimensional vector for . Denote , where .

By straightforward algebra, we can rewrite the optimization problem in (4.1) as

| (14) |

where and are the Frobenius norm and trace of a matrix. We refer to Section F.1 for the detailed derivation.

4.2 Iterative coordinate descent

In this section, we propose an efficient iterative coordinate descent algorithm which solves (14) by iterating between the optimization of and .

Optimization of (i.e. the bivariate coefficient function ): Given a fixed , denote . We have that (14) reduces to a function of that

| (15) |

Define and Denote and denote . We can rewrite (15) as

| (16) |

which can be seen as a classical ridge regression with a structured design matrix . This ridge regression has a closed-form solution and can be solved efficiently by exploiting the Kronecker structure of , see Section F.2 for more details. Thus, given , can be updated efficiently.

Optimization of (i.e. the univariate coefficient functions ): Given a fixed , with some abuse of notation, denote . For , define and . Further define . We have that (14) reduces to a function of (and thus ), i.e.

| (17) |

which can be seen as a linear regression with two group penalties: a weighted group Lasso penalty and a standard group Lasso penalty. We solve the optimization of (4.2) by performing coordinate descent on . See Friedman et al. (2010) for a similar strategy used to solve the sparse group Lasso problem for a linear regression with both a Lasso and a group Lasso penalty.

Specifically, for each , the Karush–Kuhn–Tucker condition for is

Define as the root of i.e. We have that and are the subgradients of and respectively, such that

Define . Thus, given , we have that is the optimal solution if there exist two vectors and with and , and

This is equivalent to checking

which is a standard constrained optimization problem and can be solved efficiently.

Otherwise, and to update , we need to optimize

| (18) |

We again solve this optimization by performing coordinate descent on , where for each , given , we can update by solving a simple one-dimensional optimization

| (19) |

Thus, given , can also be updated efficiently.

The iterative coordinate descent algorithm: Algorithm 1 formalizes the above discussion and outlines the proposed iterative coordinate descent algorithm. The convergence of coordinate descent for convex optimization is guaranteed under mild conditions, see e.g. Wright (2015). Empirically, the proposed algorithm is found to be efficient and stable, and typically reaches a reasonable convergence tolerance within a few iterations.

5 Numerical results

In this section, we conduct extensive numerical experiments to investigate the performance of the proposed RKHS-based penalized estimator (hereafter RKHS) for the functional linear regression with mixed predictors. Sections 5.1-5.3 compare RKHS with popular methods in the literature via simulation studies. Section 5.4 presents a real data application on crowdfunding prediction to further illustrate the potential utility of the proposed method. The implementations of our numerical experiments can be found at https://github.com/darenwang/functional_regression.

5.1 Simulation settings

Data generating process: We simulate data from the functional linear regression model

| (20) |

for Note that for , (20) reduces to the classical function-on-function regression.

We generate the functional covariate and the functional noise from a -dimensional subspace spanned by basis functions , where consists of orthonormal basis of . Following Yuan and Cai (2010), we set if and for . Thus, we have and . For , we simulate , . For , we simulate , . For the vector covariate , we simulate , .

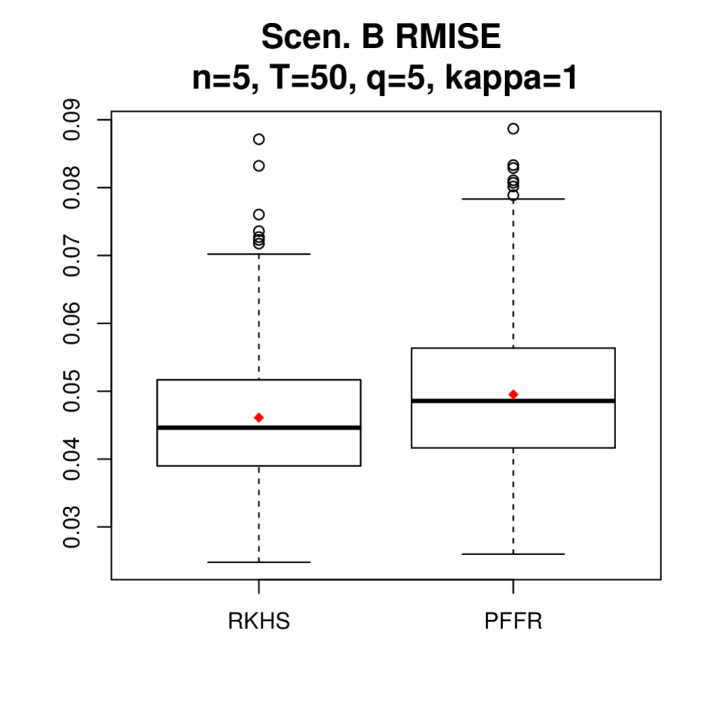

For the coefficient functions and , we consider Scenarios A and B.

-

•

Scenario A (Exponential): We set , and , .

-

•

Scenario B (Random): We set , and , . Define matrix and We simulate and rescale such that its spectral norm For , we simulate and rescale such that

Note that in Scenario B is more complex than that in Scenario A, especially when is large, while for Scenario A, its complexity is insensitive to . The parameter is later used to control the signal-to-noise ratio (SNR). Here, we define the SNR for as

which roughly equals to 1, 2 and 4 as we vary Similarly, we define SNR for (note that only is a non-zero function) as

which also roughly equals to 1, 2 and 4 as we vary

For simplicity, we set the discrete sample points for and for to be evenly spaced grids on with the same number of grids . The simulation result for random sample points where and are generated independently via the uniform distribution on [0,1] is similar and thus omitted.

Evaluation criteria: We evaluate the performance of the estimator by its excess risk. Specifically, given the sample size , we simulate observations , which are then split into the training data for constructing the estimator and the test data for the evaluation of the excess risk. Based on and the predictors , we generate the prediction and define

| (21) | |||

| (22) |

where is the oracle prediction of . Note that nRMISE is a normalized RMISE, which can be viewed as a percentage error and thus is easy to assess and interpret. Smaller RMISE and nRMISE indicate a better recovery of the signal.

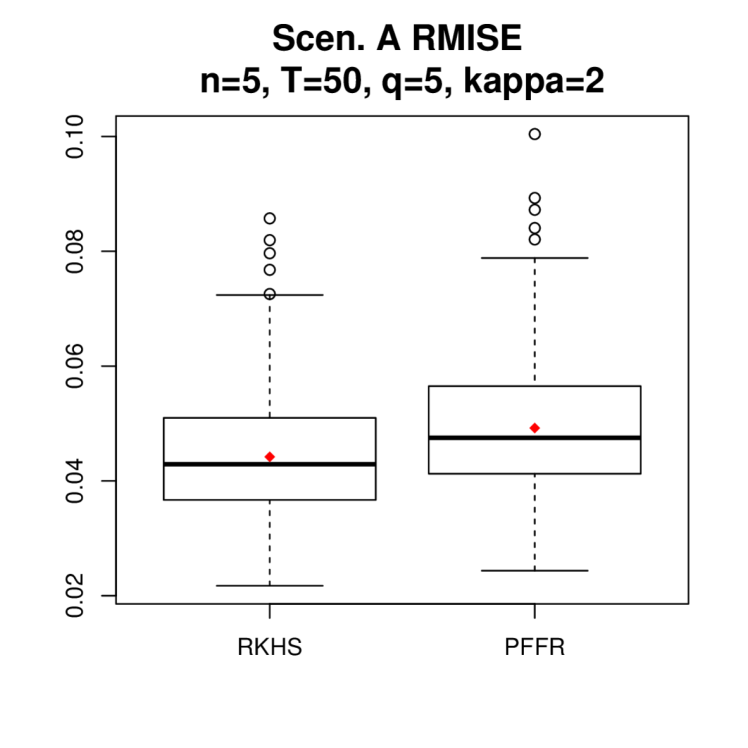

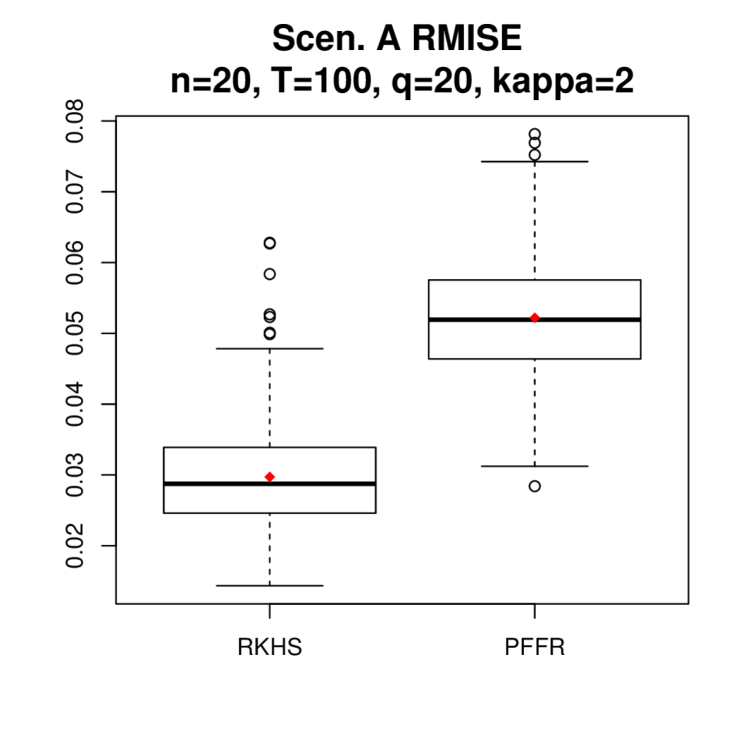

Simulation settings: We consider three simulation settings for where For each setting, we vary , which roughly corresponds to As for the number of scalar predictors , Section 5.2 considers the classical function-on-function regression, which is a special case of (20) with and Section 5.3 considers functional regression with mixed predictors and sets . For each setting, we conduct 500 experiments.

Implementation details of the RKHS estimator: We set and use the rescaled Bernoulli polynomial as the reproducing kernel such that

where , , , , and , . Such is the reproducing kernel for . See Chapter 2.3.3 of Gu (2013) for more details. In Algorithm 1, we set the tolerance parameter and the maximum iterations A standard 5-fold cross-validation (CV) on the training data is used to select the tuning parameters . Note that for , we explicitly set in the penalized optimization , which reduces to the structured ridge regression in (16) and can be solved efficiently with a closed-form solution as detailed in Section 4.2.

5.2 Function-on-function regression

In this subsection, we set and compare the proposed RKHS estimator with two popular methods in the literature for function-on-function regression.

The first competitor (Ramsay and Silverman, 2005) estimates the coefficient function based on a penalized B-spline basis function expansion. We denote this approach as FDA and it is implemented via the R package fda.usc (fregre.basis.fr function). The second competitor (Ivanescu et al., 2015) is the penalized flexible functional regression (PFFR) in and is implemented via the R package refund (pffr function). Unlike our proposed RKHS method, neither FDA or PFFR has optimal theoretical guarantees.

Both FDA and PFFR are based on penalized basis function expansions and require a hyper-parameter , which is the number of basis. Intuitively, the choice of is related to the complexity of , which is unknown in practice. In the literature, it is recommended to set at a large number to guard against the underfitting of . On the other hand, a larger can potentially incur higher estimation variance and will also increase the computational cost. For a fair comparison, for both FDA and PFFR we set , which is sufficient to accommodate the model complexity across all simulation settings except for Scenario B with . See more discussions later. We use a standard 5-fold CV to select the tuning parameter of RKHS and the roughness penalty of FDA from the range . PFFR uses a restricted maximum likelihood (REML) approach to automatically select the roughness penalty.

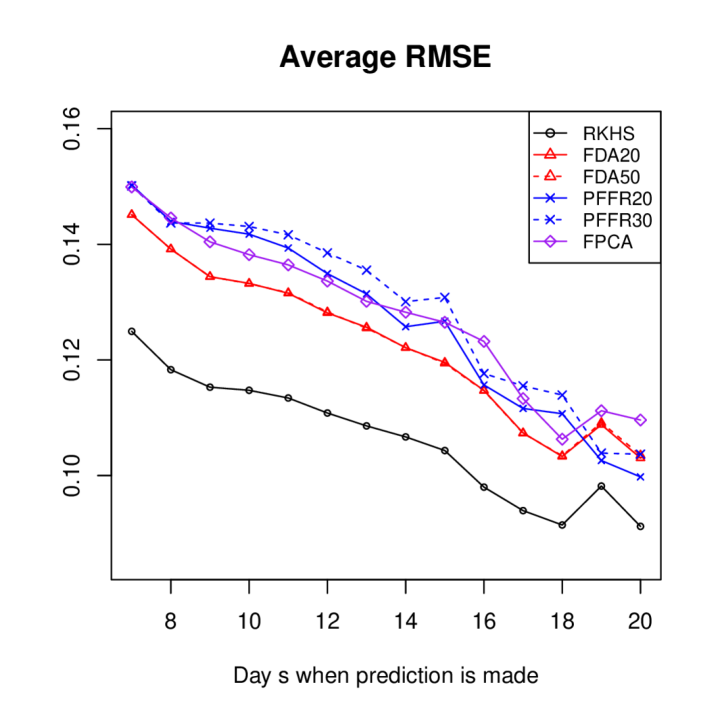

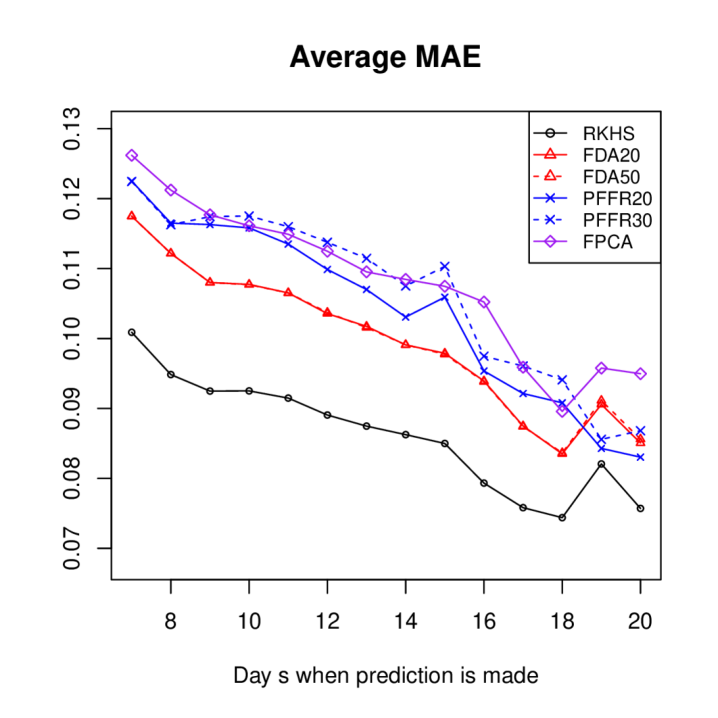

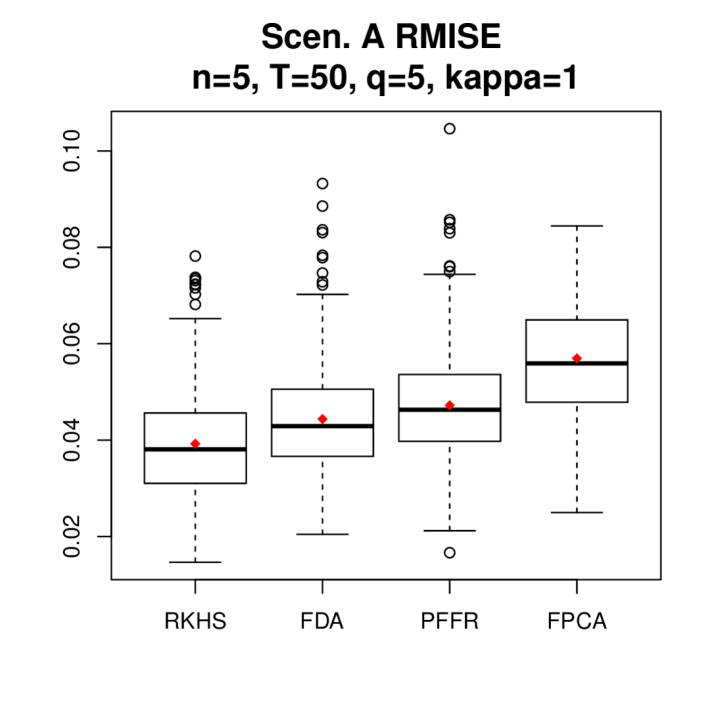

Besides the penalized method based on basis function expansions (i.e. FDA and PFFR), another popular method for function-on-function regression in the literature is based on functional PCA (i.e. the Karhunen–Loéve expansion, FPCA), see for example Yao et al. (2005). However, FPCA does not seem to perform competitively in our simulation and real data analysis, see similar observations in Cai and Yuan (2012) and Sun et al. (2018). For completeness, we report the performance of FPCA in Section H and Section K.

Numerical results: For each method, Table 1 reports its average nRMISE (nRMISEavg) across 500 experiments under all simulation settings. For each simulation setting, we further report Ravg, which is the percentage improvement of excess risk given by RKHS defined as

Ravg=[nRMISEavg(FDA), nRMISEavg(PFFR) / nRMISEavg(RKHS.

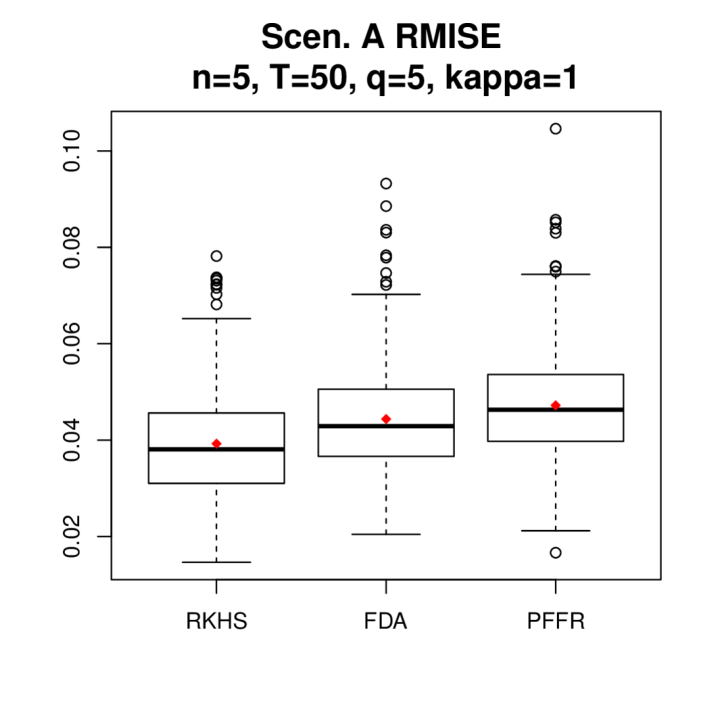

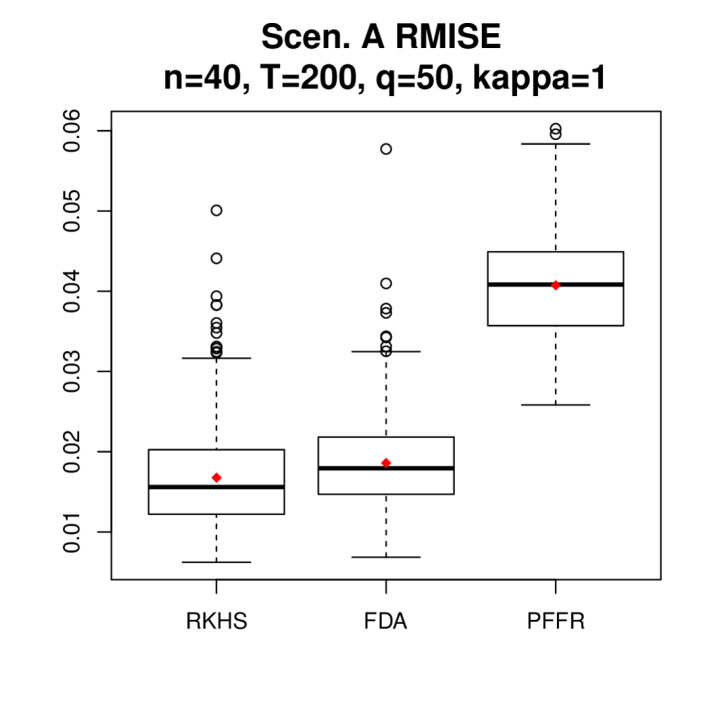

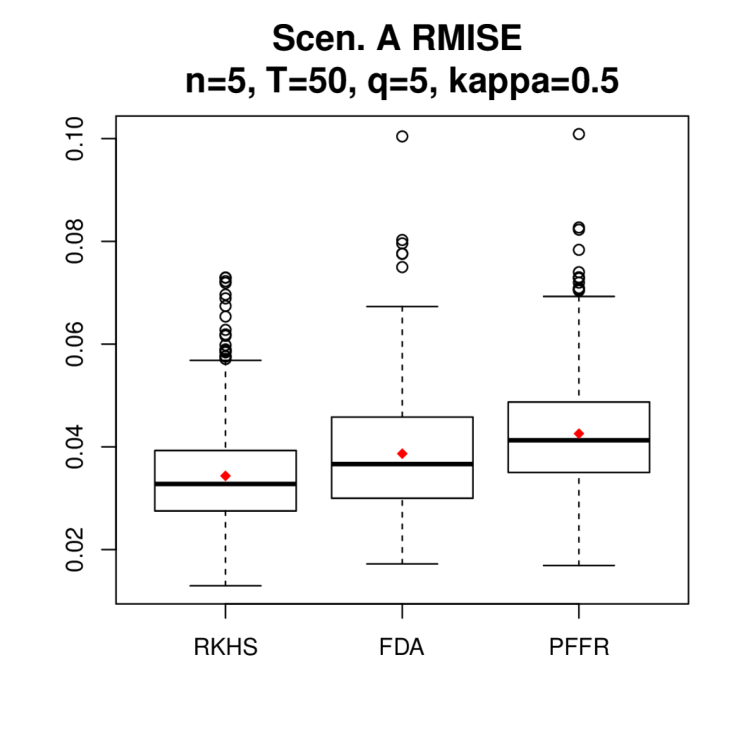

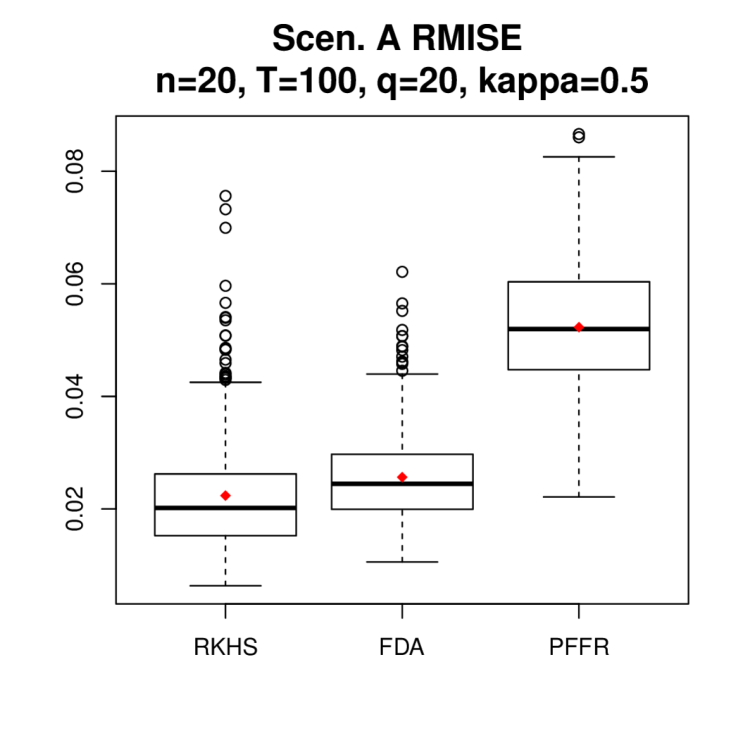

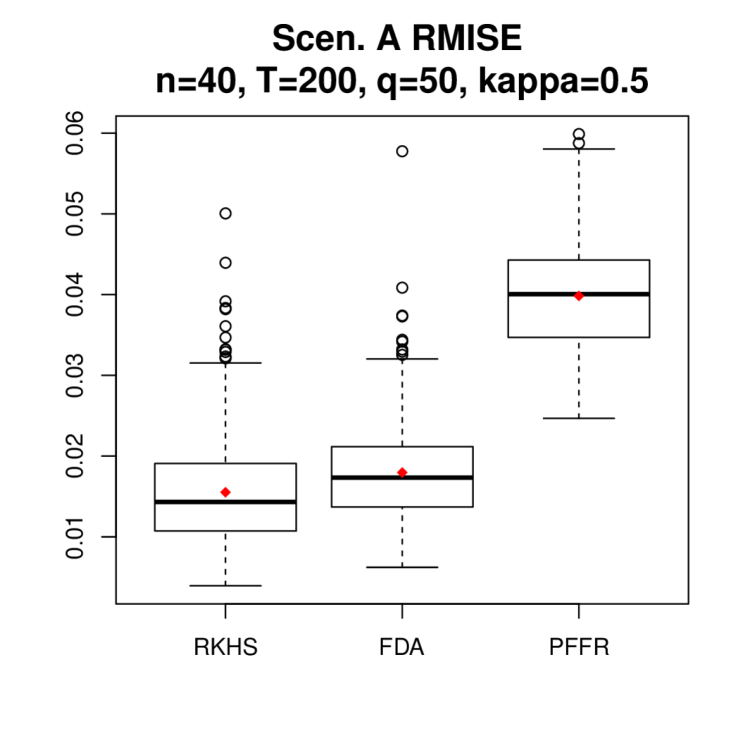

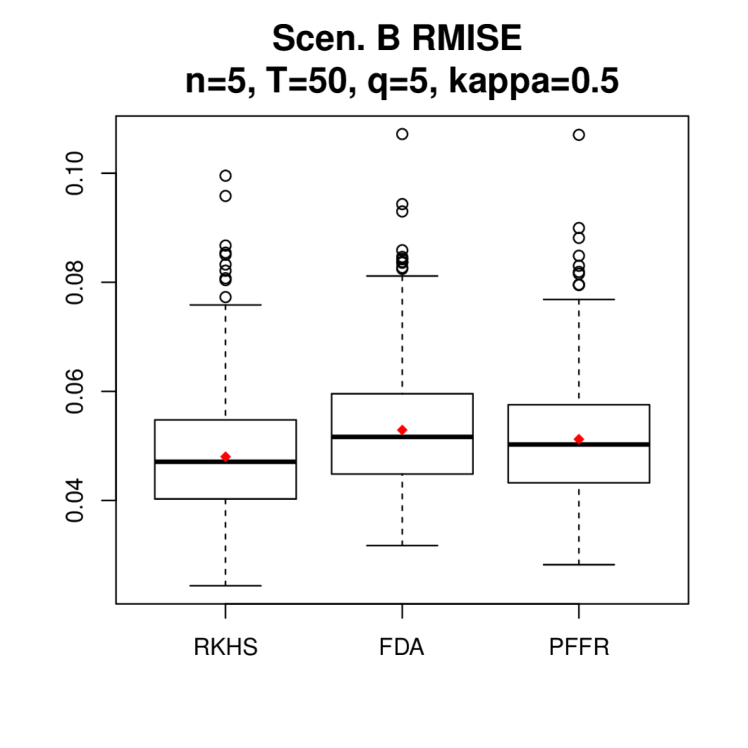

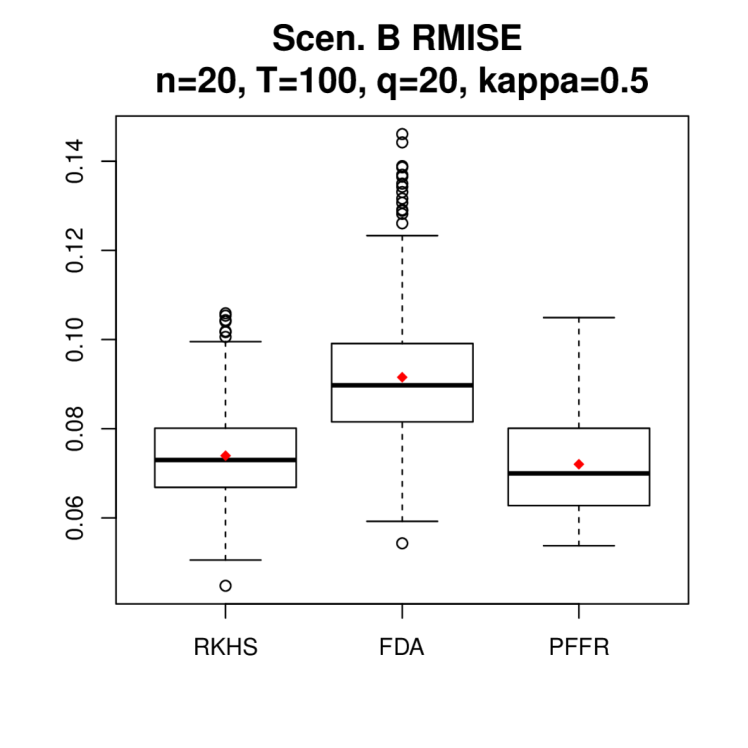

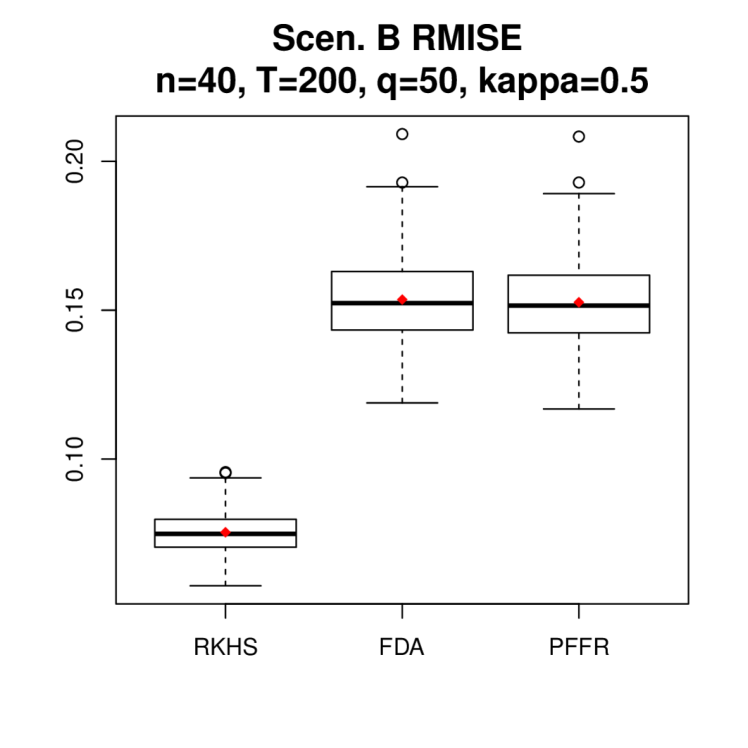

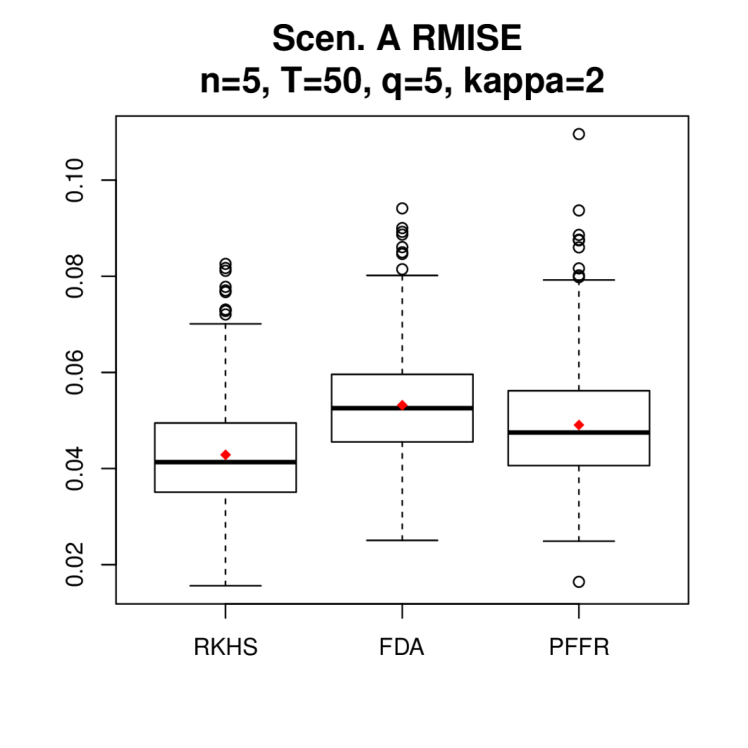

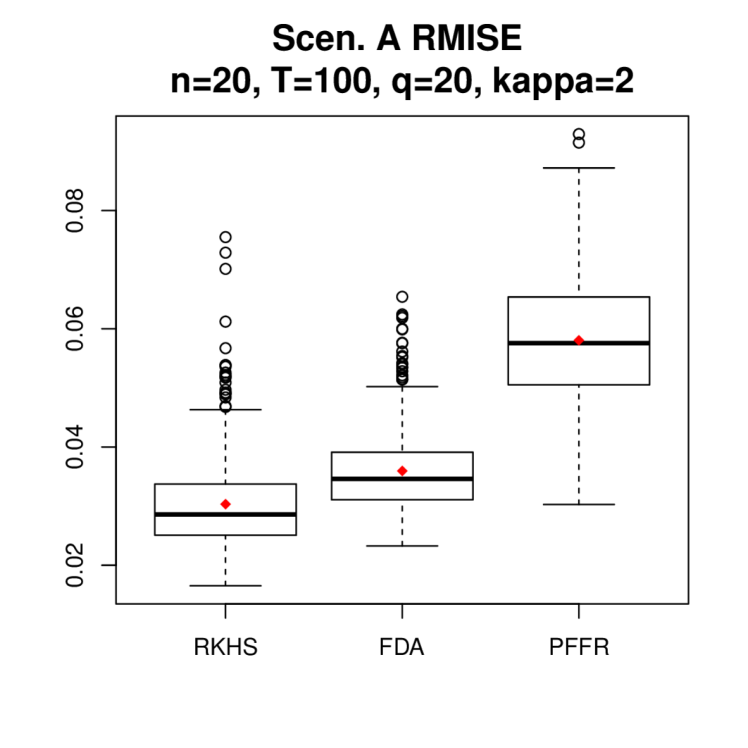

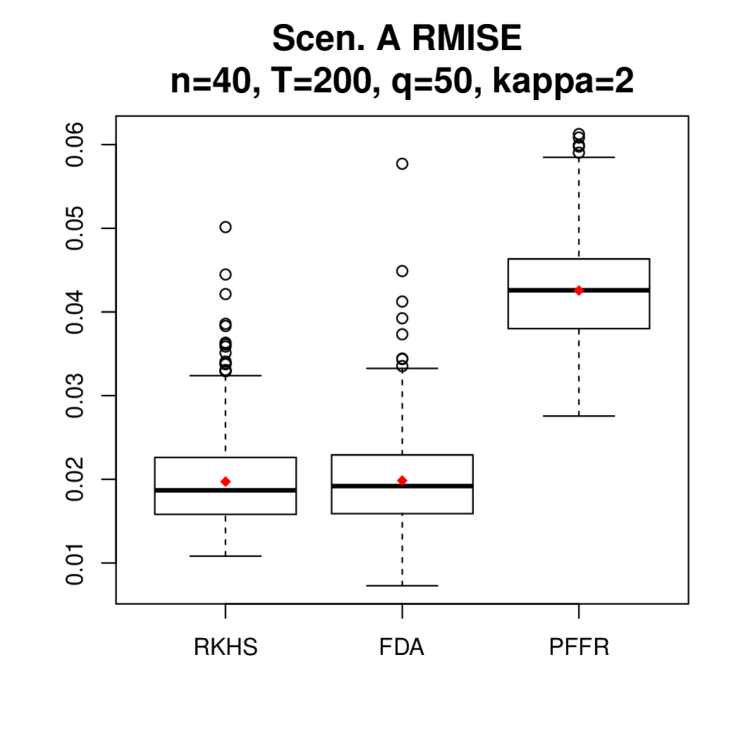

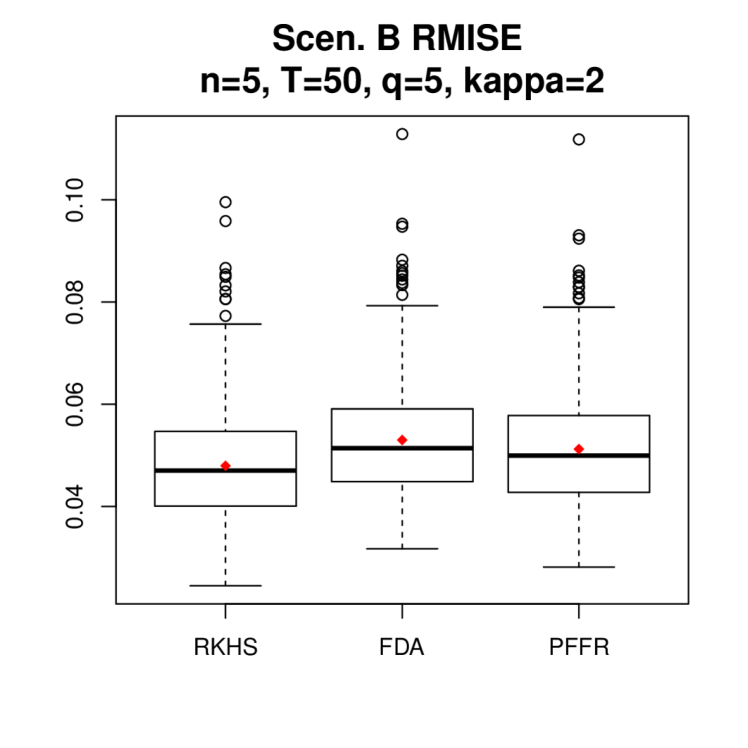

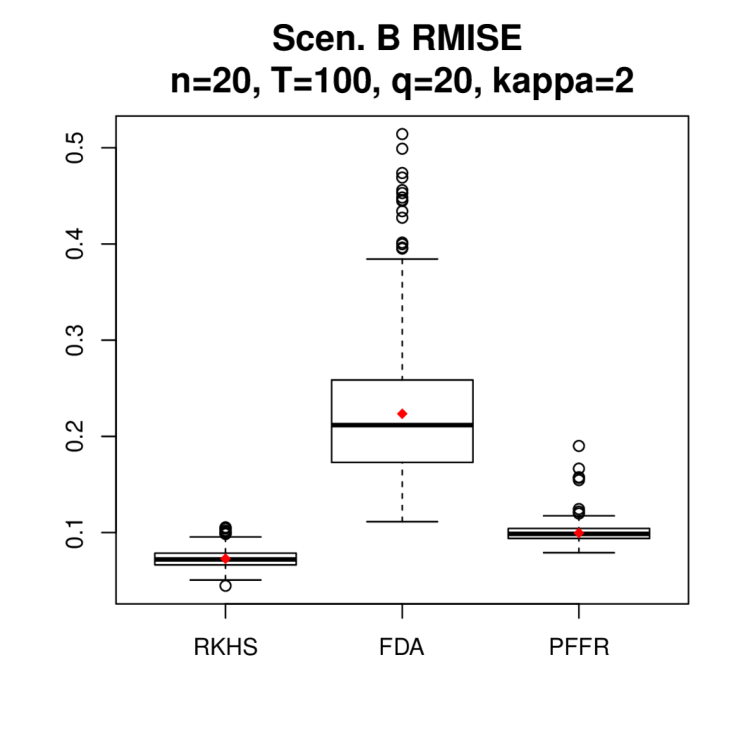

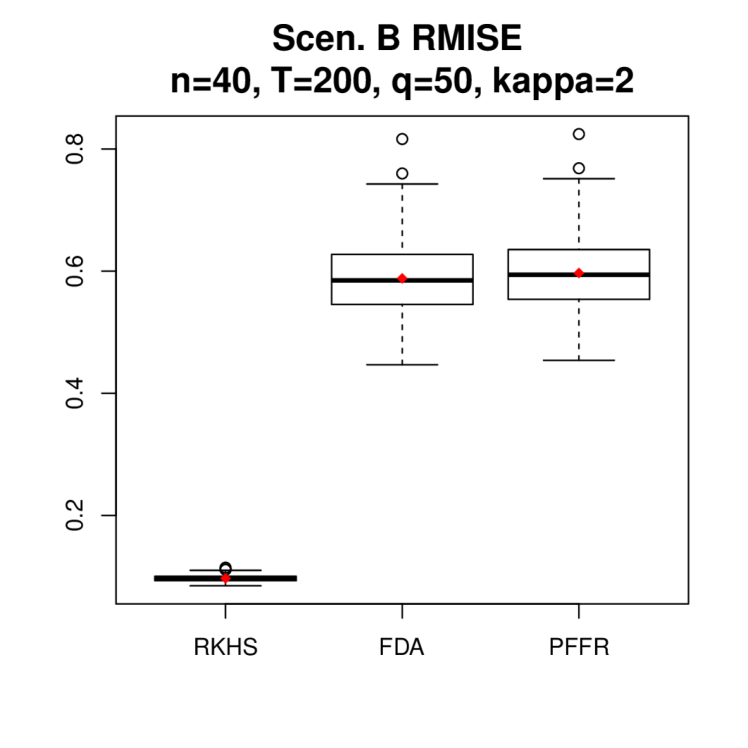

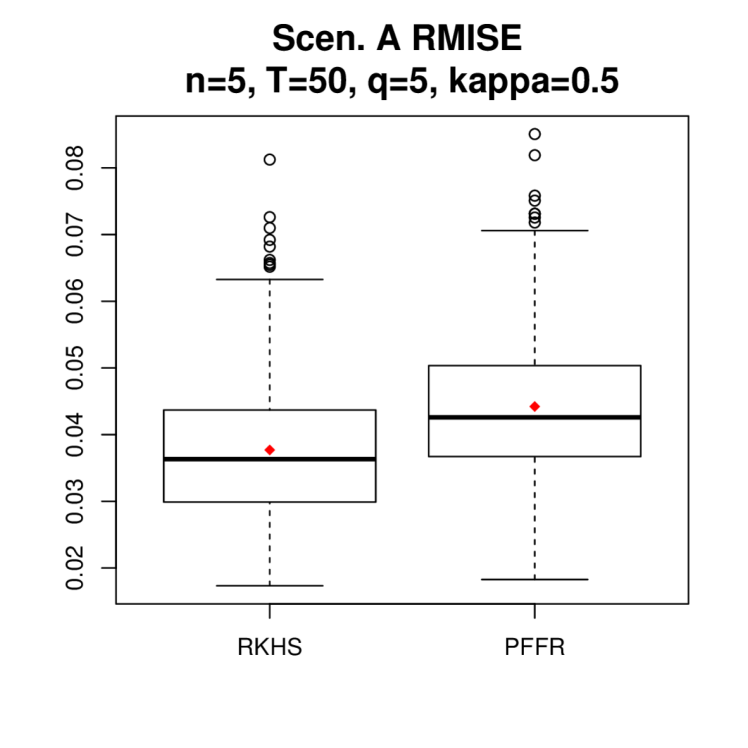

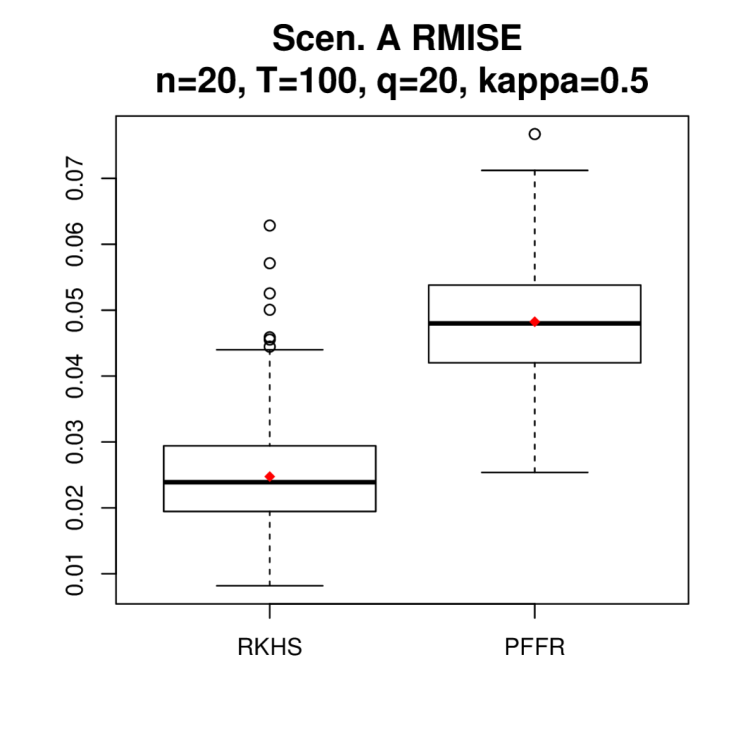

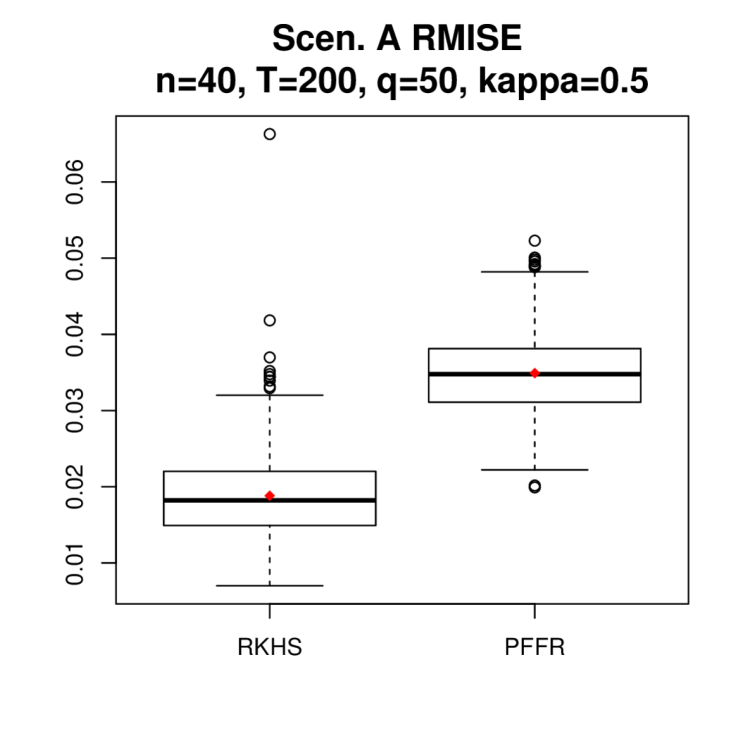

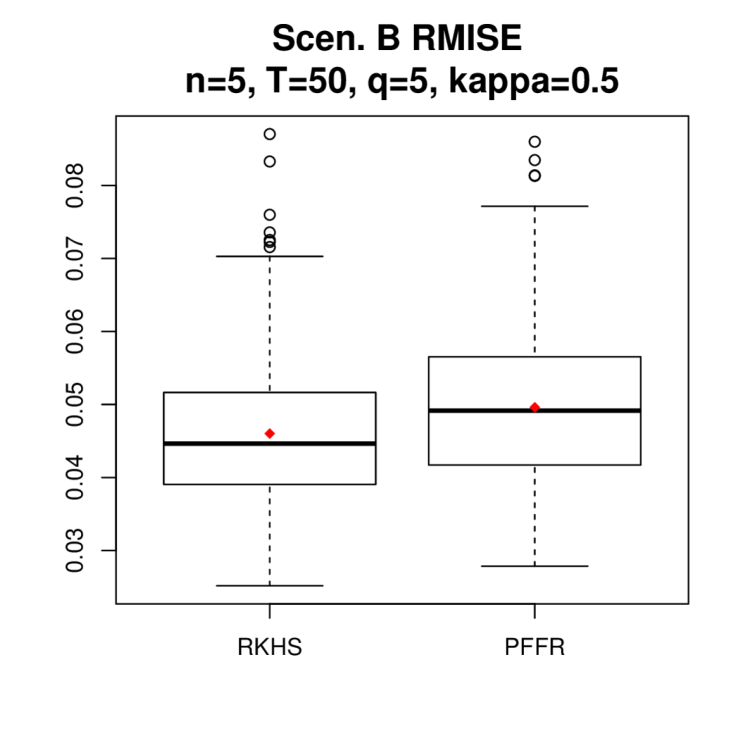

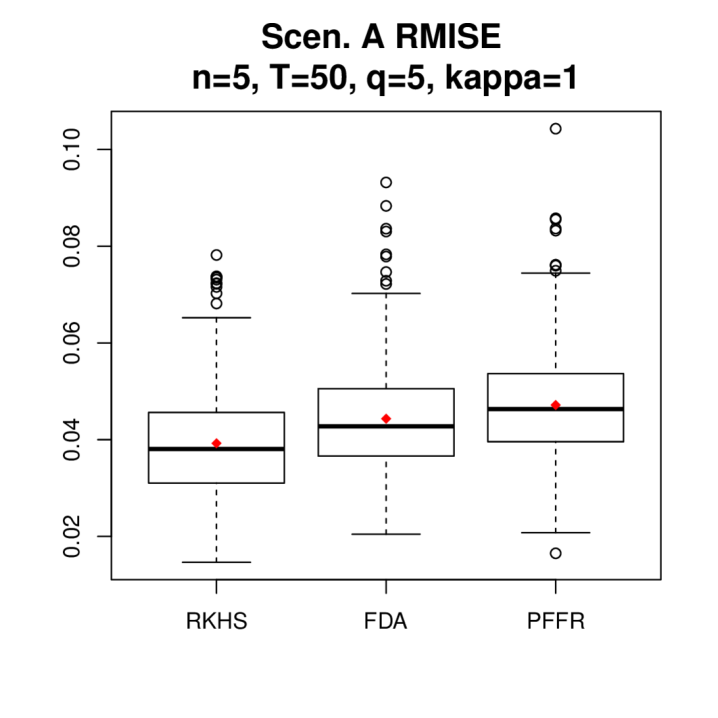

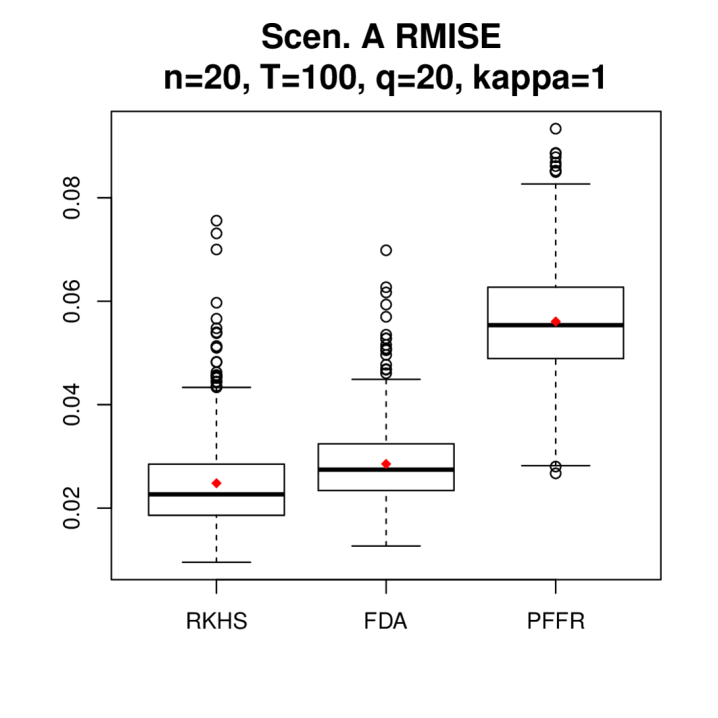

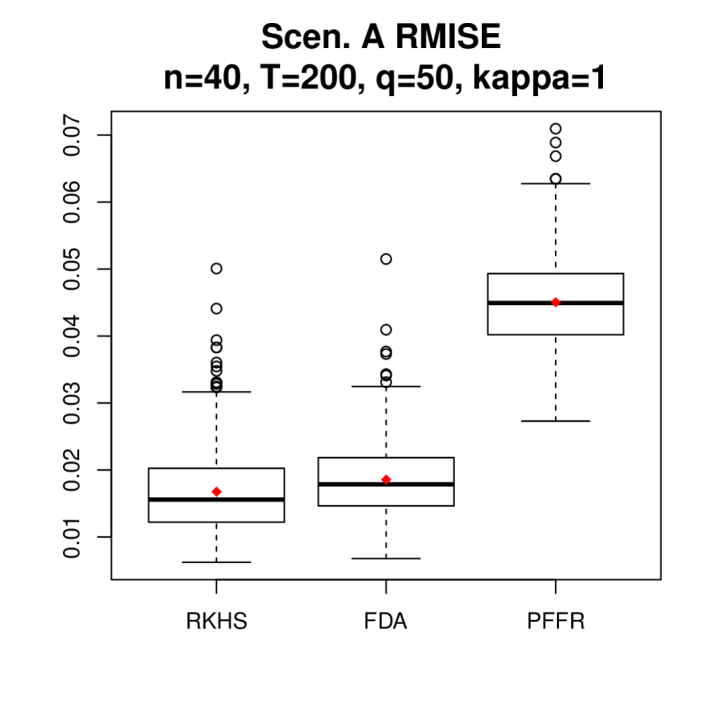

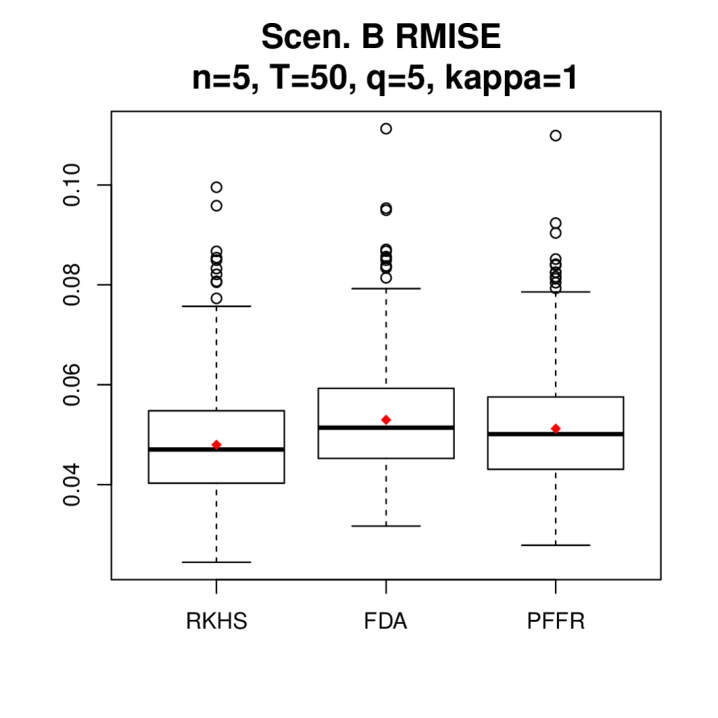

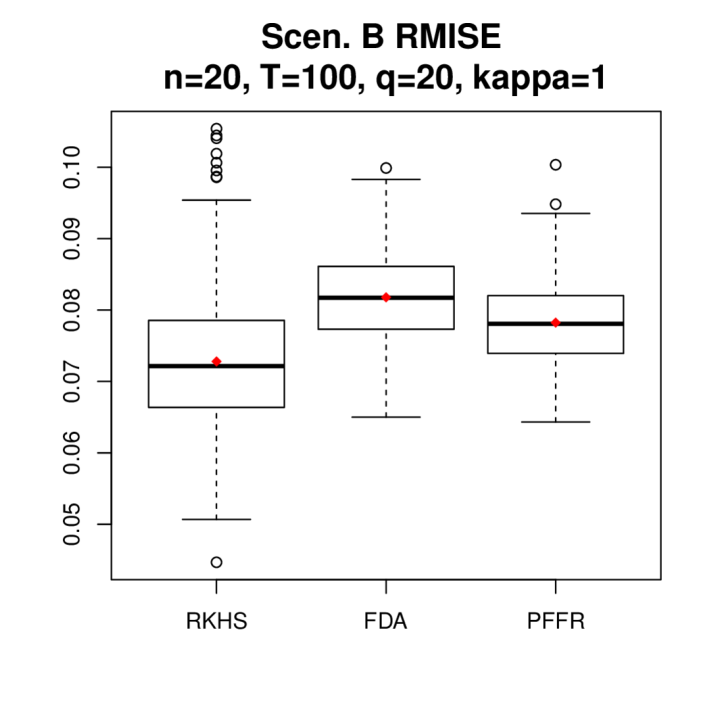

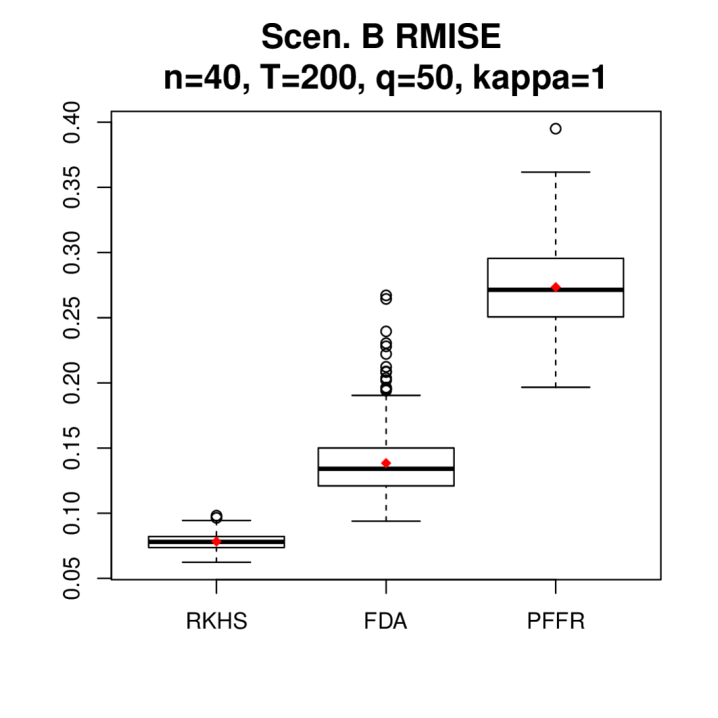

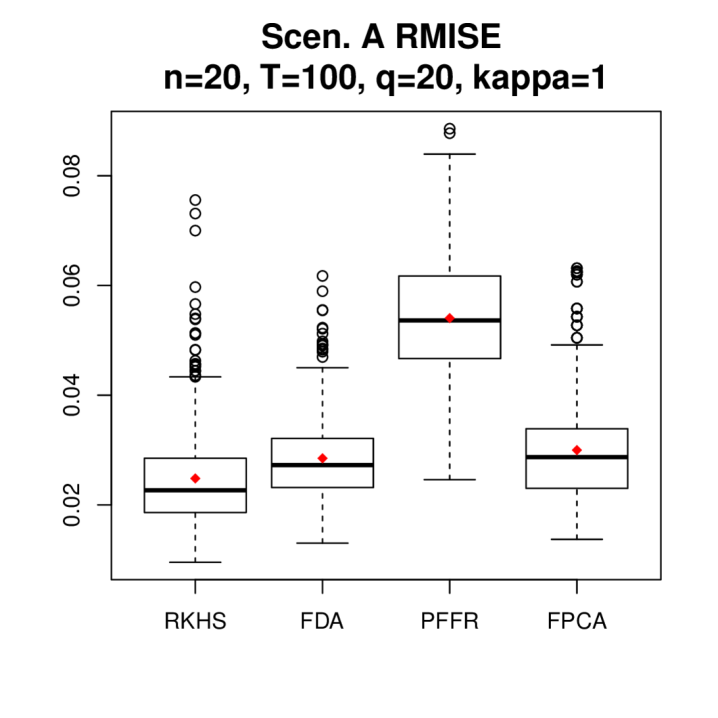

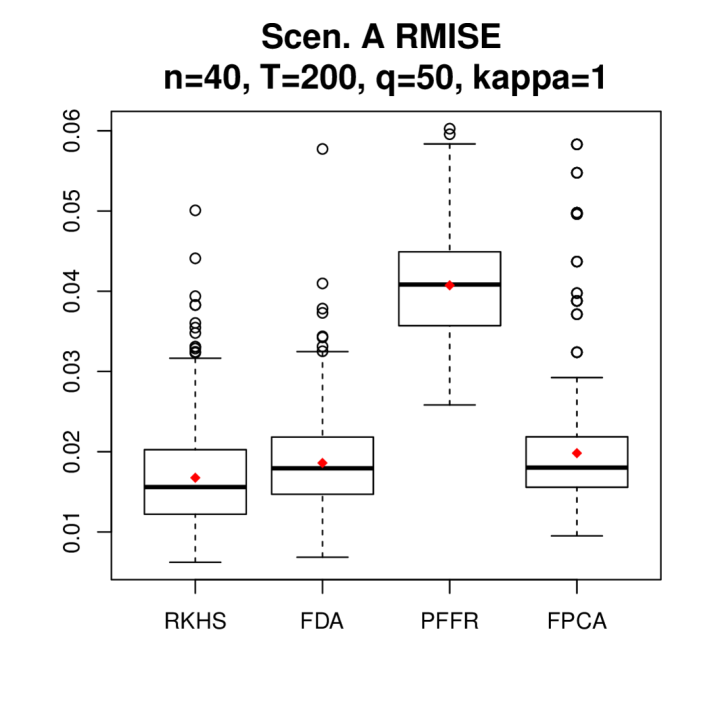

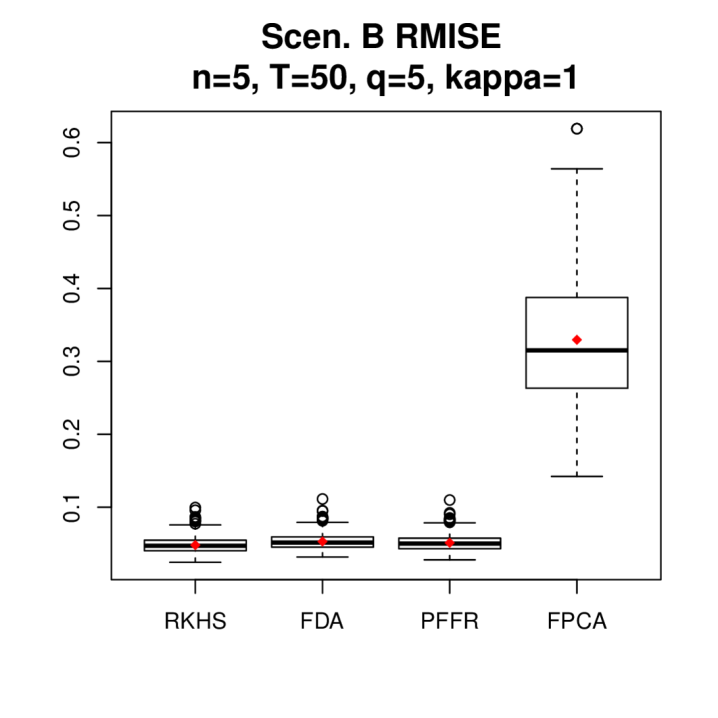

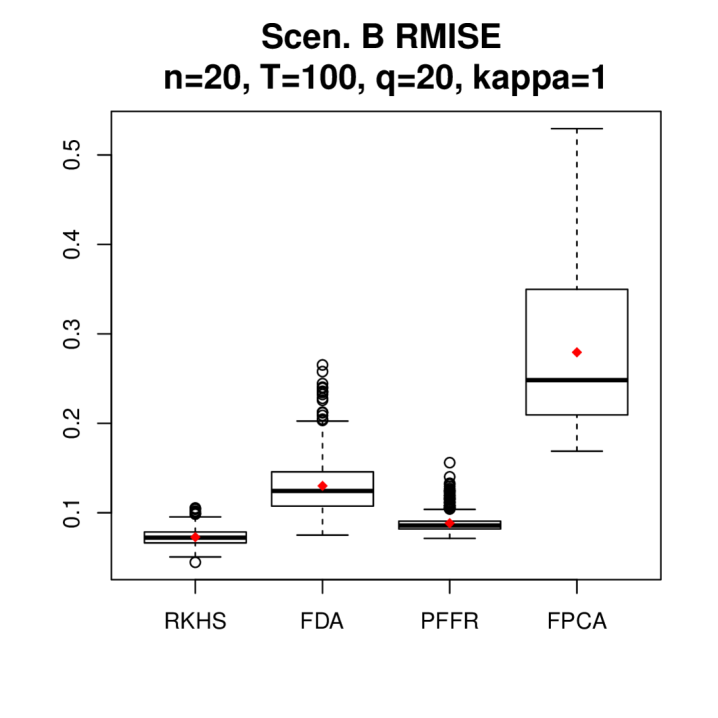

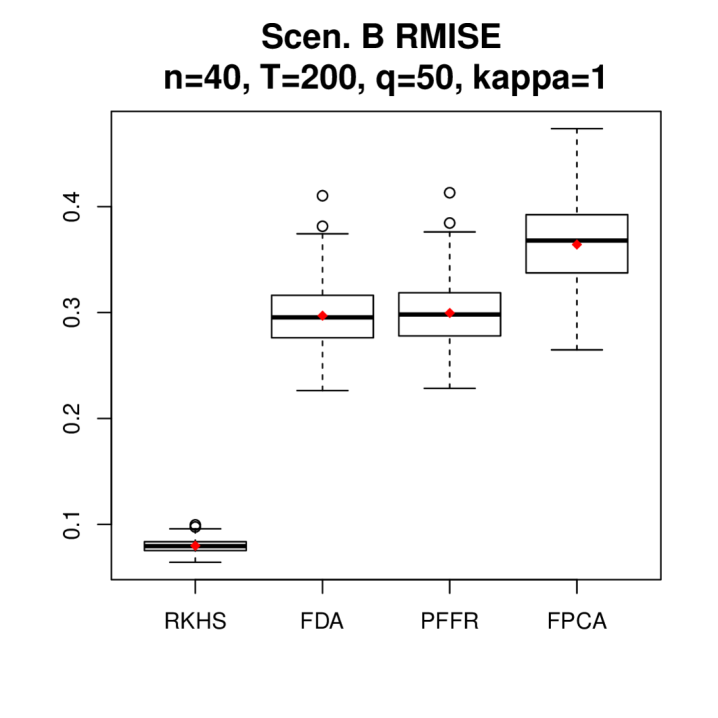

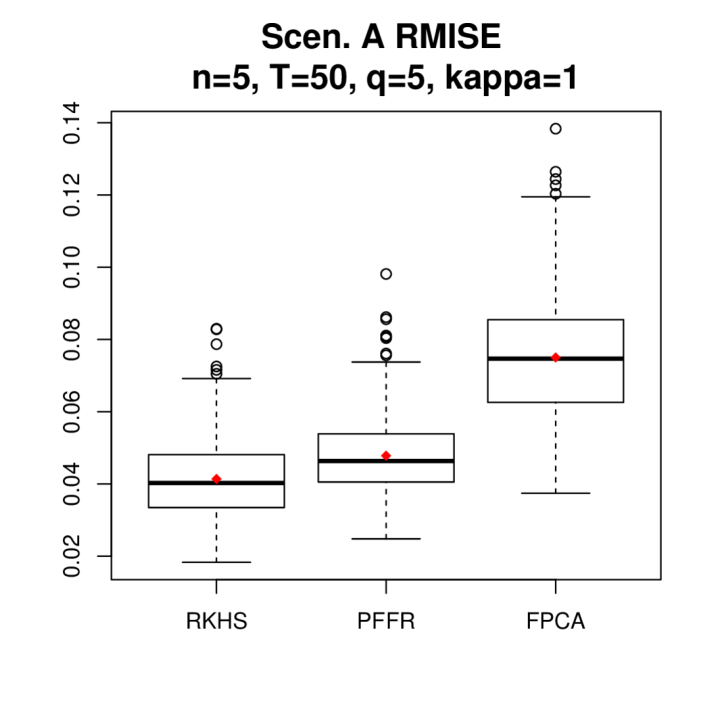

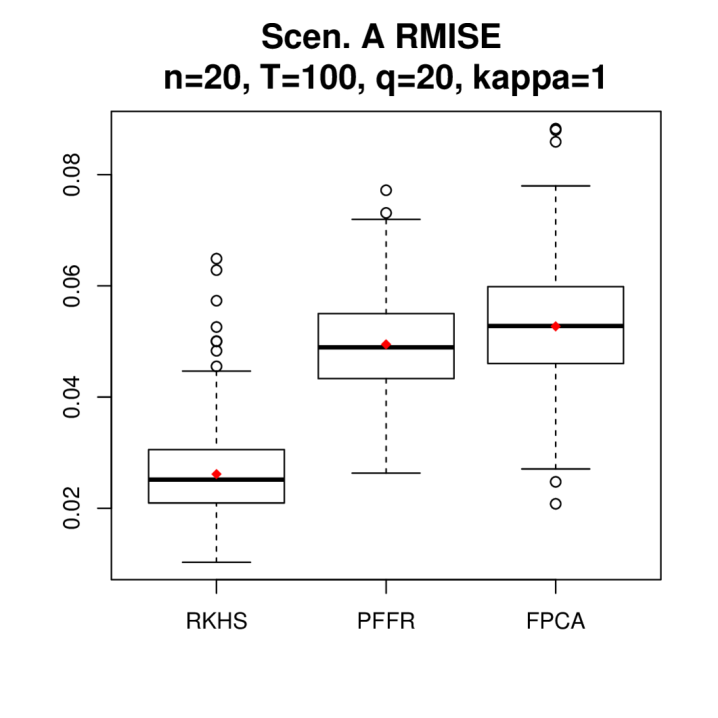

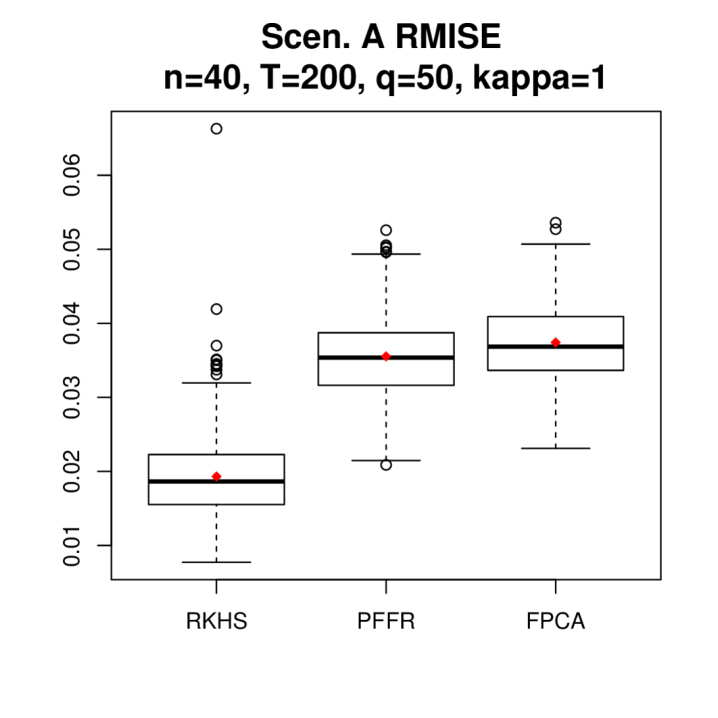

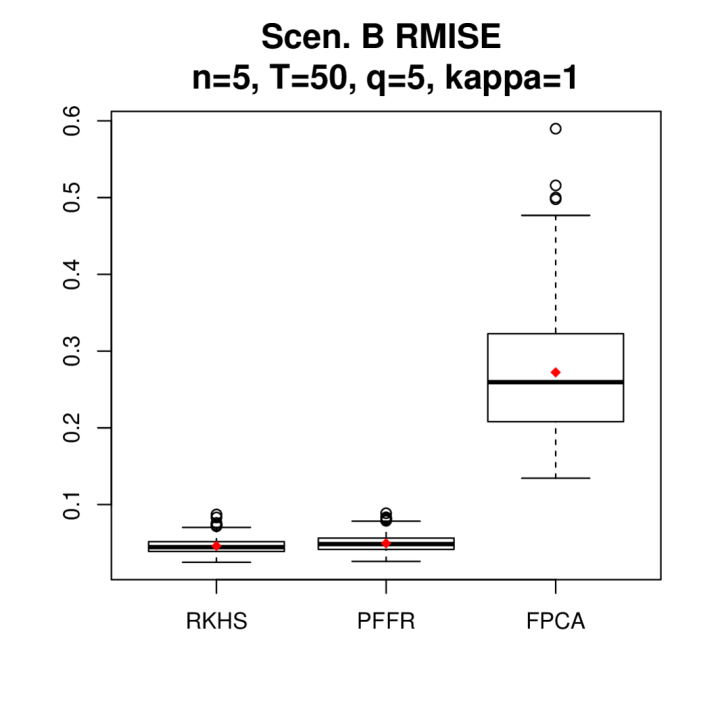

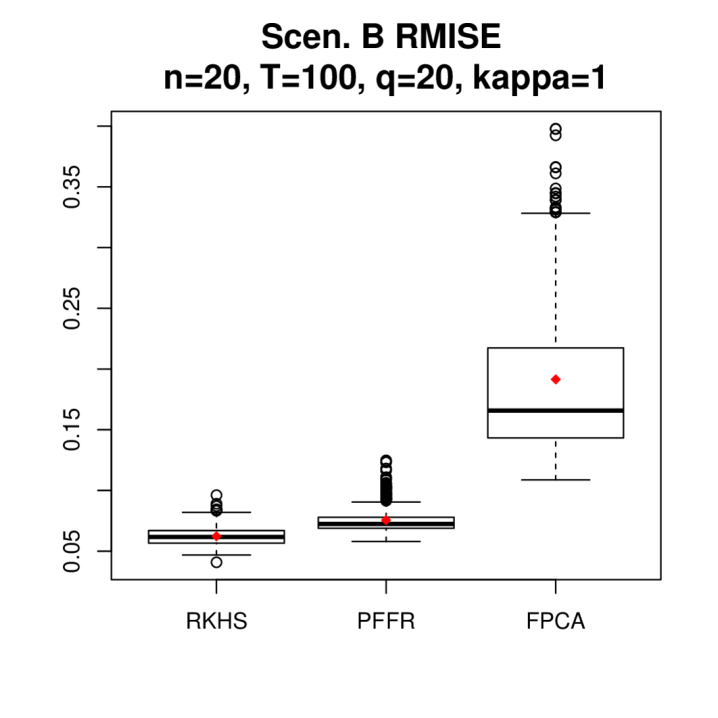

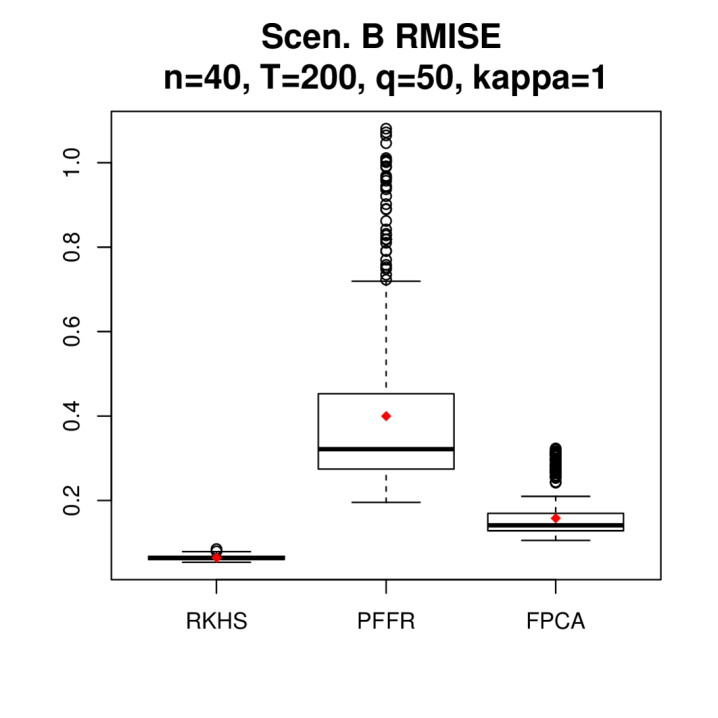

In addition, we report Rw, which is the percentage of experiments (among 500 experiments) where RKHS gives the lowest RMISE. We further give the boxplot of RMISE in Figure 2 under . The boxplots of RMISE under can be found in Section G.

As can be seen, RKHS in general delivers the best performance across almost all simulation settings. For all methods, the estimation performance improves with a larger SNR (reflected in ). Since the complexity of Scenario A is insensitive to , the performance of all methods improve as increases under Scenario A. However, this is not the case for Scenario B, as a larger increases the estimation difficulty. Compared to Scenario A, the excess risk RMISE of Scenario B is larger, especially for , due to the more complex nature of the operator In general, the improvement of RKHS is more notable under high model complexity and SNR.

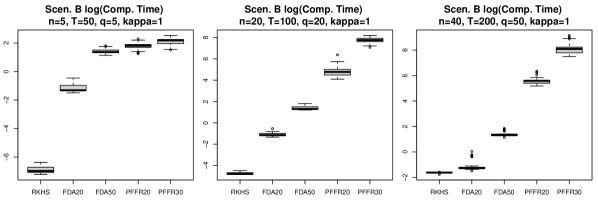

Note that for Scenario B with , both FDA and PFFR incur significantly higher excess risks due to the underfitting bias caused by the insufficient basis dimension , indicating the potential sensitivity of the penalized basis function approaches to the hyper-parameter. In comparison, RKHS automatically adapts to different levels of model complexity. In Section J, we further conduct the same simulation but with a larger number of basis dimension for FDA and for PFFR. For Scenario A, where the bivariate function is a simple exponential function, FDA and PFFR give essentially the same performance, while for Scenario B with , FDA and PFFR give much improved performance due to lower underfitting bias, though still having a notable performance gap compared to RKHS. In addition, note that a larger can significantly increase the computational cost of the penalized basis function approaches. We refer to Section J for more details.

In addition, Section I collects the results of the same simulation but with the observed functional responses being additionally corrupted with measurement errors, i.e. the scenario discussed in Section 3.4 (see Theorem 4). It is seen that the performance of RKHS only worsens slightly with the additional measurement errors, providing numerical support for Theorem 4 that measurement errors do not affect the convergence rate of RKHS.

| Scenario A: | Scenario B: | |||||||||

| RKHS | FDA | PFFR | Ravg(%) | Rw (%) | RKHS | FDA | PFFR | Ravg(%) | Rw (%) | |

| 15.98 | 17.97 | 19.80 | 12.46 | 64 | 20.86 | 22.98 | 22.28 | 6.79 | 63 | |

| 9.14 | 10.31 | 10.98 | 12.81 | 68 | 10.42 | 11.50 | 11.12 | 6.63 | 71 | |

| 4.99 | 6.18 | 5.70 | 14.37 | 72 | 5.21 | 5.75 | 5.56 | 6.68 | 74 | |

| Scenario A: | Scenario B: | |||||||||

| RKHS | FDA | PFFR | Ravg(%) | Rw (%) | RKHS | FDA | PFFR | Ravg(%) | Rw (%) | |

| 10.61 | 12.15 | 24.84 | 14.57 | 80 | 37.41 | 45.91 | 36.51 | 2.41 | 47 | |

| 5.89 | 6.75 | 12.84 | 14.66 | 81 | 18.39 | 32.41 | 22.32 | 21.37 | 92 | |

| 3.60 | 4.26 | 6.89 | 18.45 | 84 | 9.19 | 27.71 | 12.56 | 36.58 | 100 | |

| Scenario A: | Scenario B: | |||||||||

| RKHS | FDA | PFFR | Ravg(%) | Rw (%) | RKHS | FDA | PFFR | Ravg(%) | Rw (%) | |

| 7.37 | 8.53 | 18.93 | 15.72 | 81 | 39.22 | 79.37 | 78.92 | 101.21 | 100 | |

| 3.98 | 4.41 | 9.68 | 10.96 | 75 | 20.75 | 76.74 | 77.40 | 269.73 | 100 | |

| 2.34 | 2.36 | 5.05 | 0.71 | 49 | 12.59 | 75.95 | 77.09 | 503.19 | 100 | |

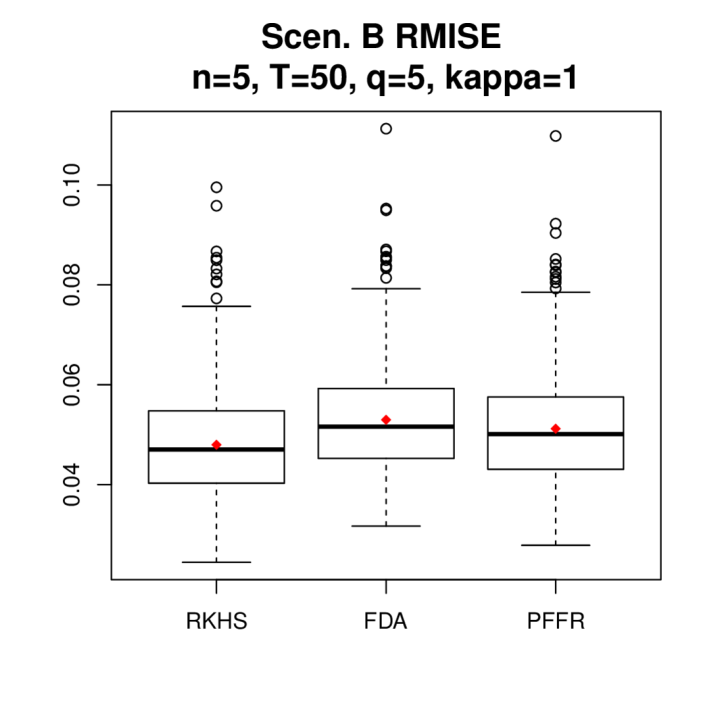

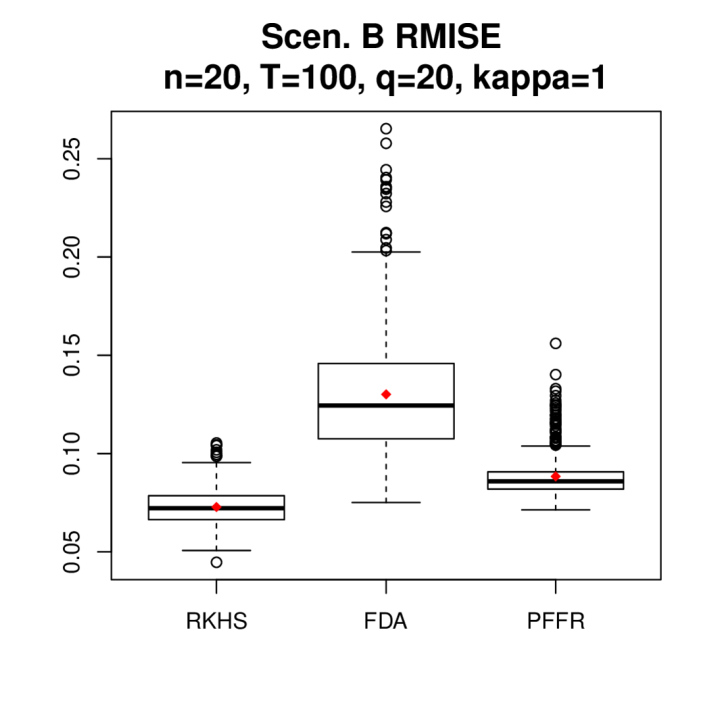

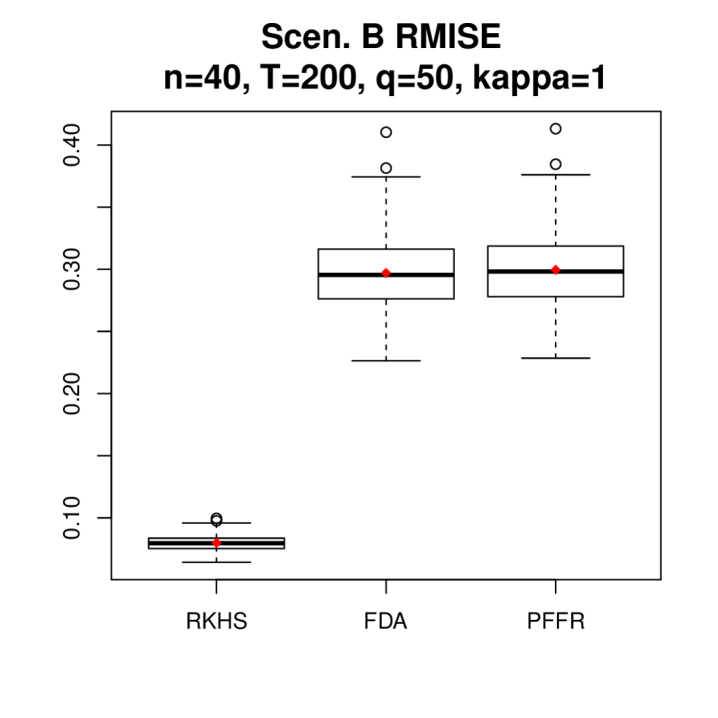

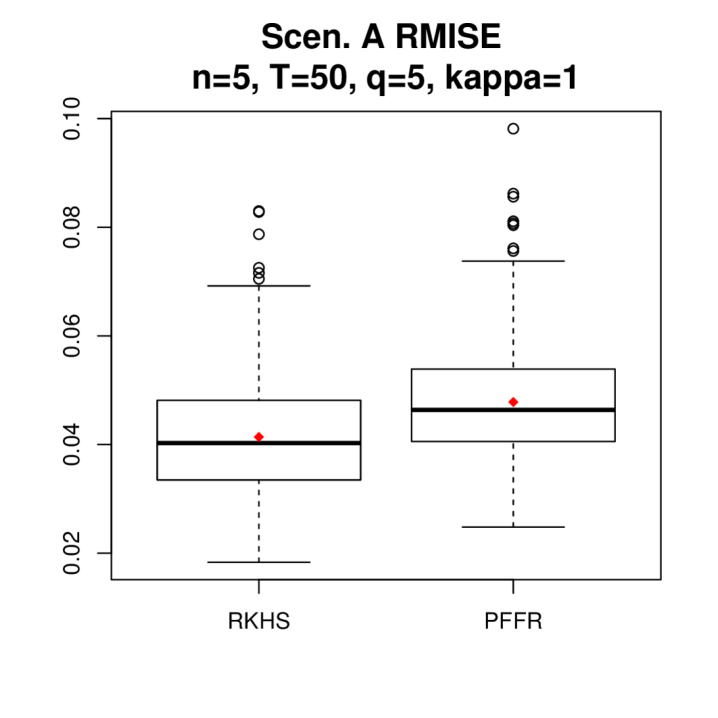

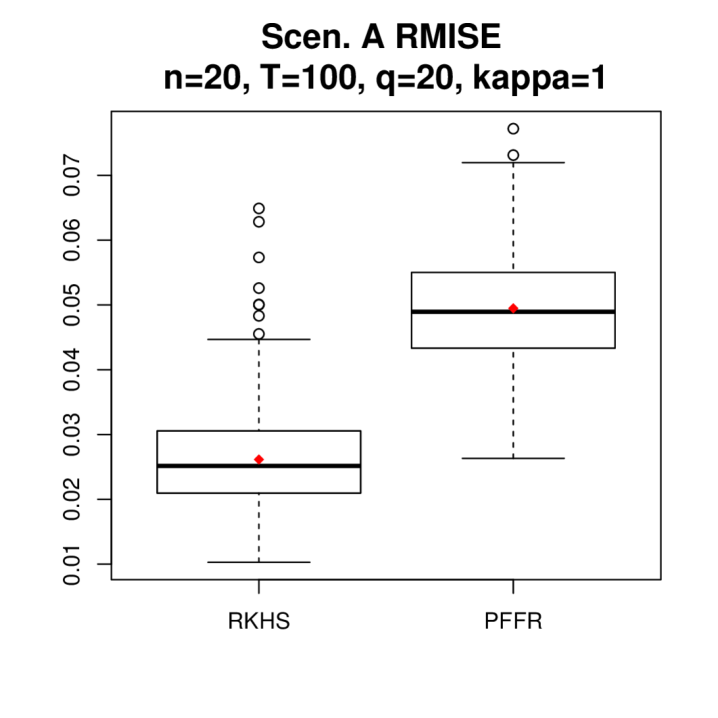

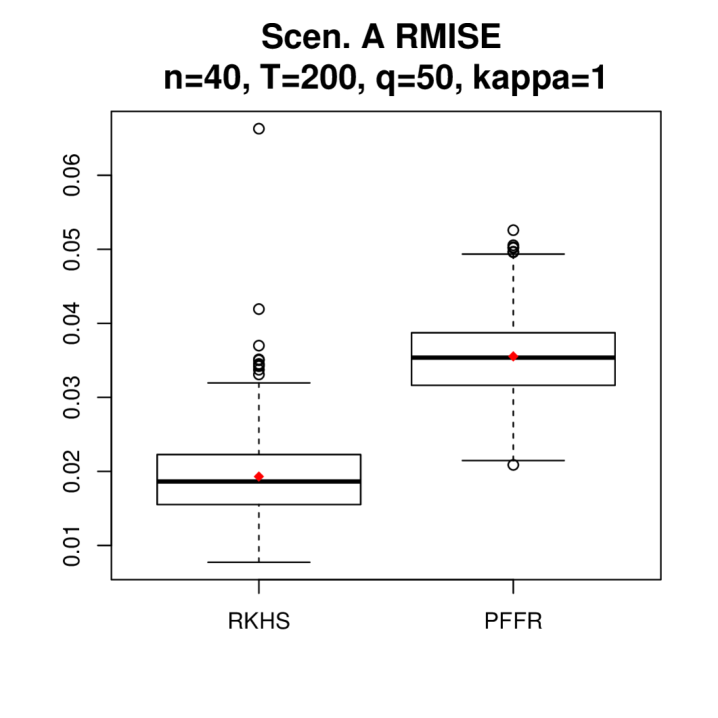

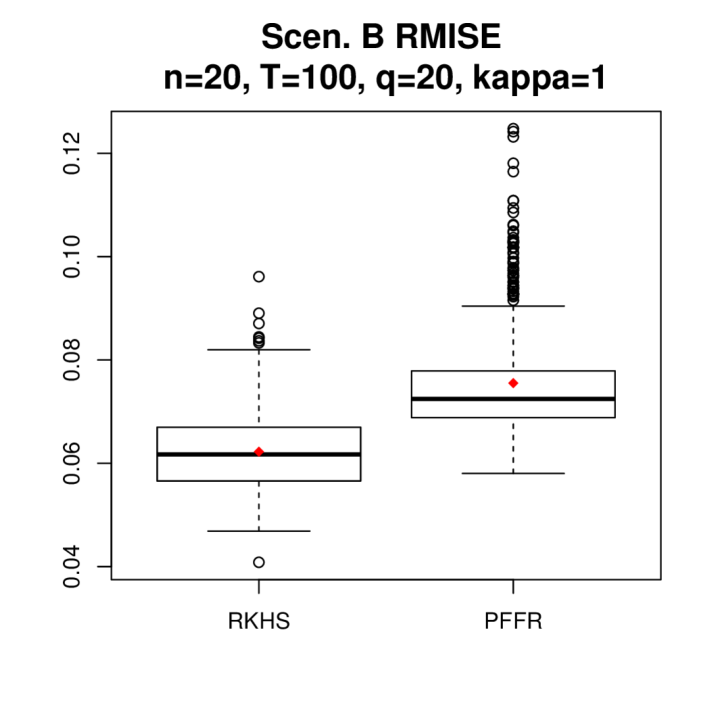

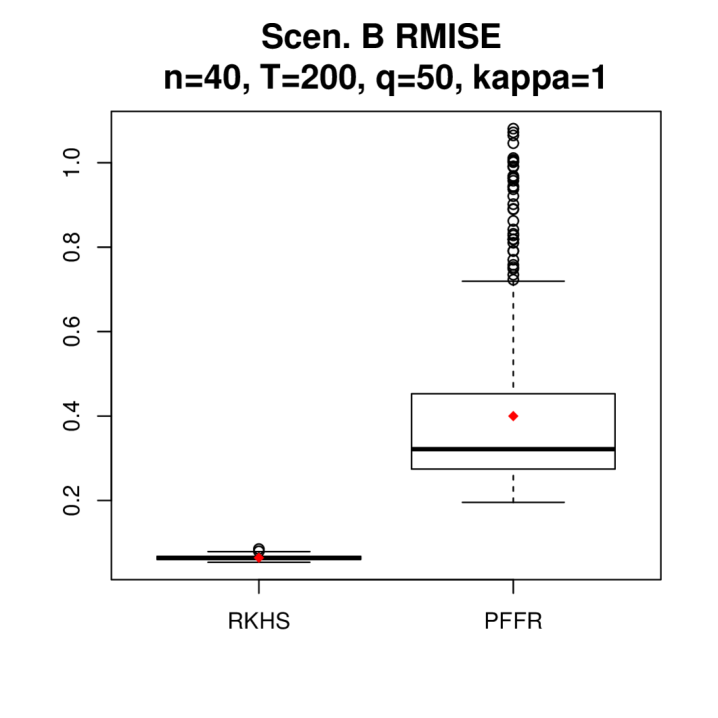

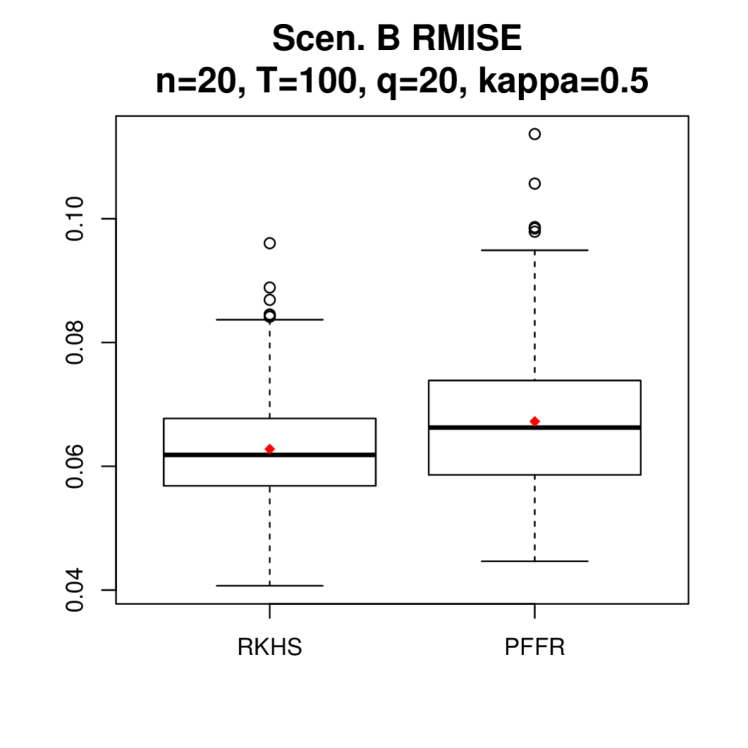

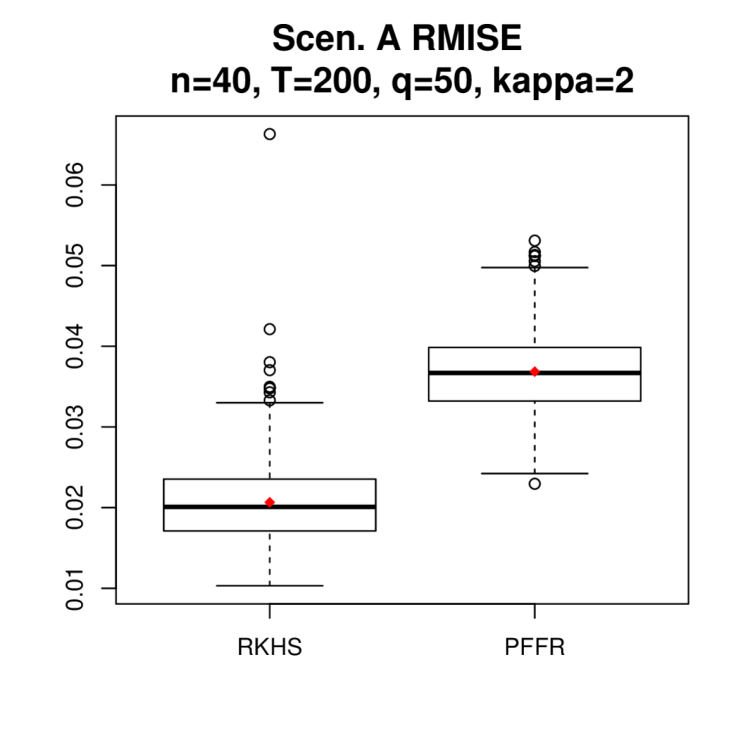

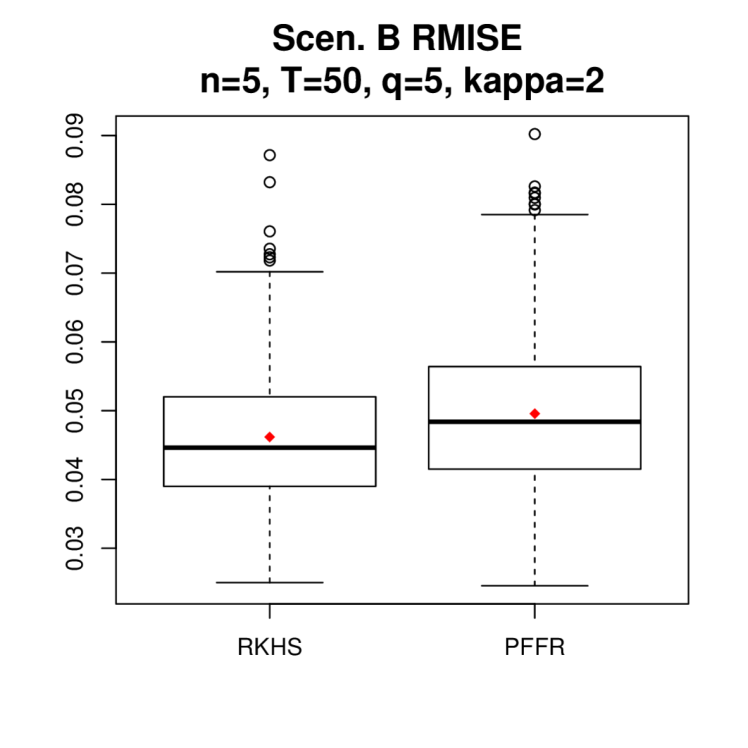

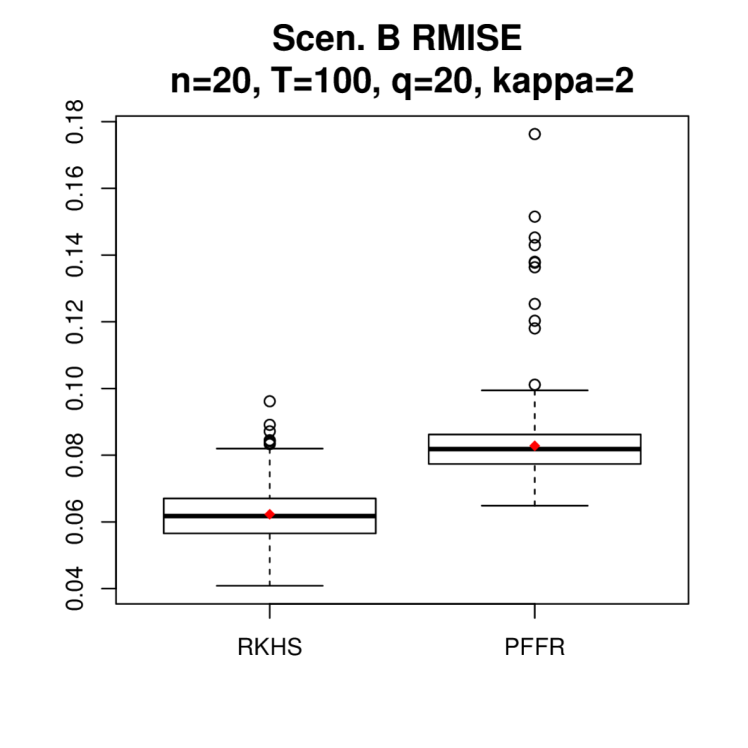

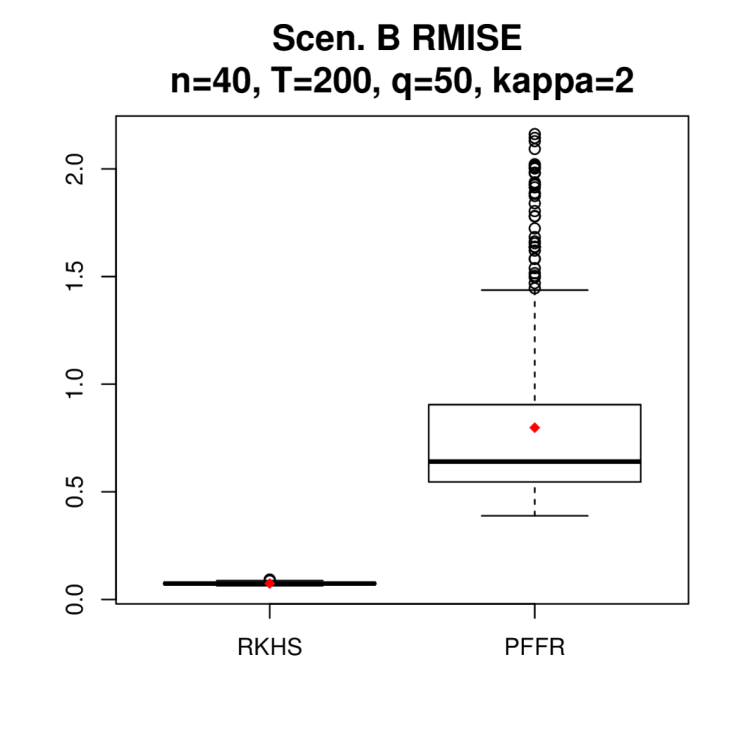

5.3 Functional regression with mixed predictors

In this subsection, we set and compare the performance of RKHS with PFFR, as FDA cannot handle mixed predictors. For RKHS, we use the standard 5-fold CV to select the tuning parameter from the range for Scenario A and from the range for Scenario B. PFFR uses REML to automatically select the roughness penalty and we set for PFFR as before.

Numerical results: Table 2 reports the average nRMISE (nRMISEavg) across 500 experiments for RKHS and PFFR under all simulation settings. Table 2 further reports Ravg, the percentage improvement of RKHS over PFFR, and Rw, the percentage of experiments (among 500 experiments) where RKHS returns lower RMISE. We further give the boxplot of RMISE in Figure 3 under . The boxplots of RMISE under can be found in Section G. The result is consistent with the one for function-on-function regression, where RKHS delivers the best performance across almost all simulation settings with notable improvement.

| Scenario A: | Scenario B: | |||||||

| RKHS | PFFR | Ravg(%) | Rw (%) | RKHS | PFFR | Ravg(%) | Rw (%) | |

| 17.16 | 20.14 | 17.35 | 77 | 14.81 | 15.99 | 8.02 | 70 | |

| 9.43 | 10.89 | 15.53 | 76 | 7.42 | 7.97 | 7.46 | 75 | |

| 5.03 | 5.60 | 11.35 | 74 | 3.72 | 3.99 | 7.29 | 75 | |

| Scenario A: | Scenario B: | |||||||

| RKHS | PFFR | Ravg(%) | Rw (%) | RKHS | PFFR | Ravg(%) | Rw (%) | |

| 11.25 | 21.95 | 95.11 | 100 | 23.95 | 25.74 | 7.48 | 63 | |

| 5.95 | 11.25 | 89.31 | 100 | 11.83 | 14.44 | 22.03 | 90 | |

| 3.38 | 5.94 | 75.77 | 100 | 5.92 | 7.85 | 32.47 | 99 | |

| Scenario A: | Scenario B: | |||||||

| RKHS | PFFR | Ravg(%) | Rw (%) | RKHS | PFFR | Ravg(%) | Rw (%) | |

| 8.50 | 15.76 | 85.46 | 99 | 27.52 | 77.13 | 180.22 | 100 | |

| 4.36 | 8.02 | 84.03 | 100 | 14.23 | 76.19 | 435.38 | 100 | |

| 2.33 | 4.16 | 78.36 | 100 | 8.20 | 75.99 | 827.09 | 100 | |

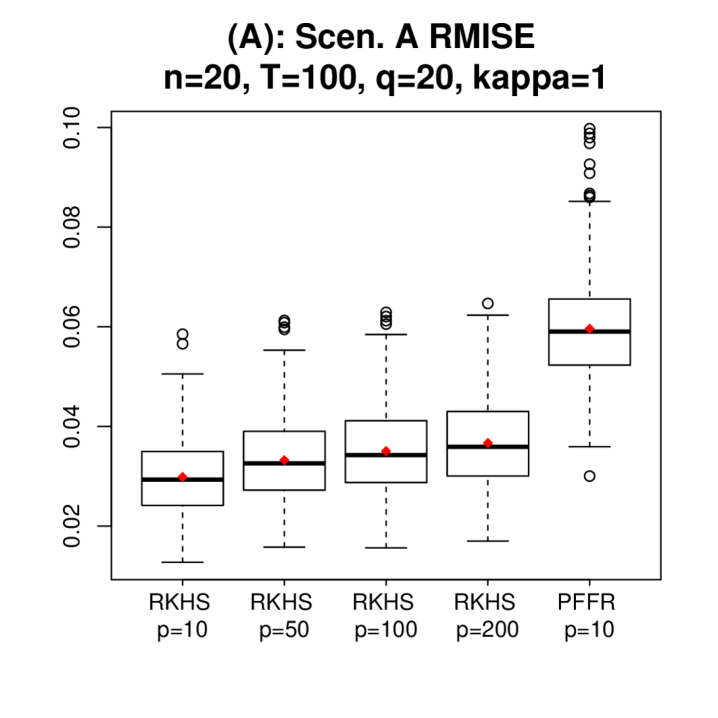

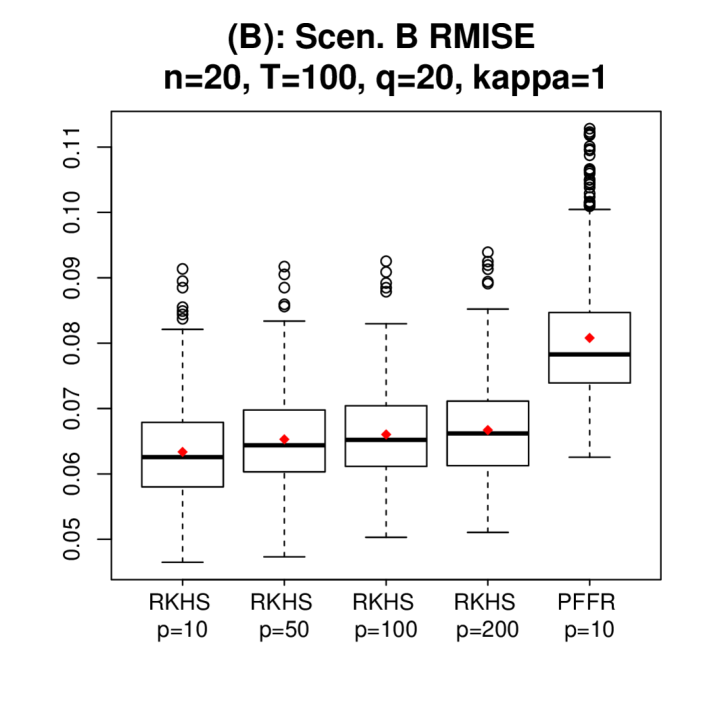

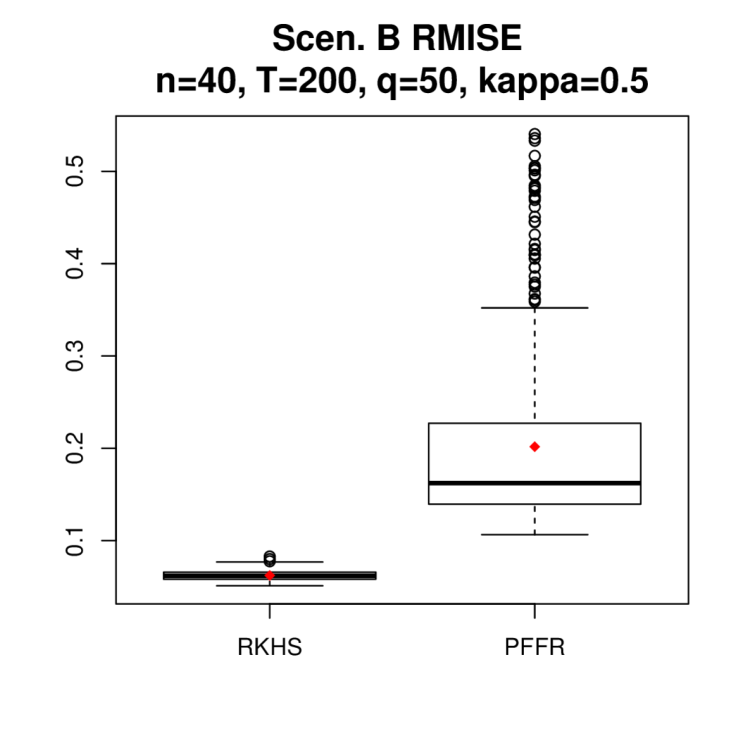

In the following, we further examine the performance of RKHS for high-dimensional scalar predictors. Specifically, keep the simulation setting identical as above, we increase the number of scalar predictors to . As a reminder, the sparsity of is 1 as only is a non-zero function. In other words, the additionally introduced scalar predictors are purely noise. Thus, compared to the case of , the performance of RKHS and PFFR are expected to worsen with an increasing dimension However, thanks to the group Lasso-type penalty, which induces sparsity of the estimated coefficient functions , we expect the excess risk of RKHS to grow at the rate of , as suggested in Theorem 2.

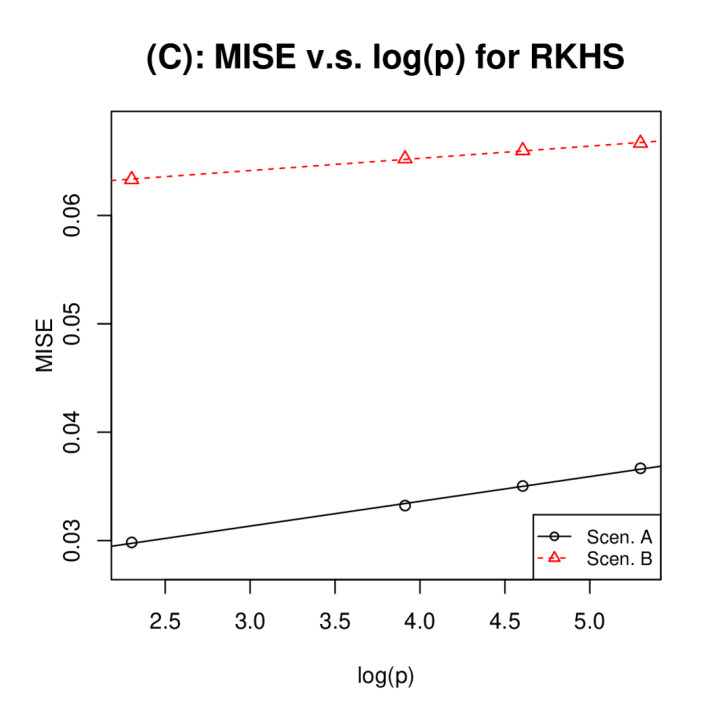

To conserve space, we present the result under the simulation setting with and Results under other settings are similar and thus omitted. Due to the lack of sparsity penalty, PFFR may not be suitable for the setting of high-dimensional predictors. For comparison, we only implement PFFR for . Figure 4 (A) and (B) give the boxplot of RMISE for RKHS and PFFR across 500 experiments. As expected, the RMISE of RKHS increases as the dimension increases though at a rate slower than . Indeed, RKHS at still gives better performance than PFFR at . Figure 4 (C) gives the plot between average MISE111To match the result in Theorem 2, we compute MISE, which is the squared RMISE with MISE = RMISE2. across 500 experiments and , where the relationship is seen to be roughly linear. This confirms that the excess risk of RKHS increases in the order of as suggested in Theorem 2.

5.4 Real data applications

In this section, we conduct real data analysis to further demonstrate the promising utility of the proposed RKHS-based functional regression in the context of crowdfunding. In recent years, crowdfunding has become a flexible and cost-effective financing channel for start-ups and entrepreneurs, which helps expedite product development and diffusion of innovations.

We consider a novel dataset collected from one of the largest crowdfunding websites, kickstarter.com, which provides an online platform for creators, e.g. start-ups, to launch fundraising campaigns for developing a new product such as electronic devices and card games. The fundraising campaign takes place on a webpage set up by the creators, where information of the new product is provided, and typically has a 30-day duration with a goal amount preset by the creators. Over the course of the 30 days, backers can pledge funds to the campaign, resulting in a functional curve of pledged funds . At time , the webpage displays real-time along with other information of the campaign, such as its number of creators , number of product updates and number of product FAQs .

A fundraising campaign succeeds if . Importantly, only creators of successful campaigns can be awarded the final raised funds and the platform kickstarter.com charges a service fee () of successful campaigns. Thus, for both the platform and the creators, an accurate prediction of the future curve at an early time is valuable, as it not only reveals whether the campaign will succeed but more importantly suggests timing along for potential intervention by the creators and the platform to boost the fundraising campaign and achieve greater revenue.

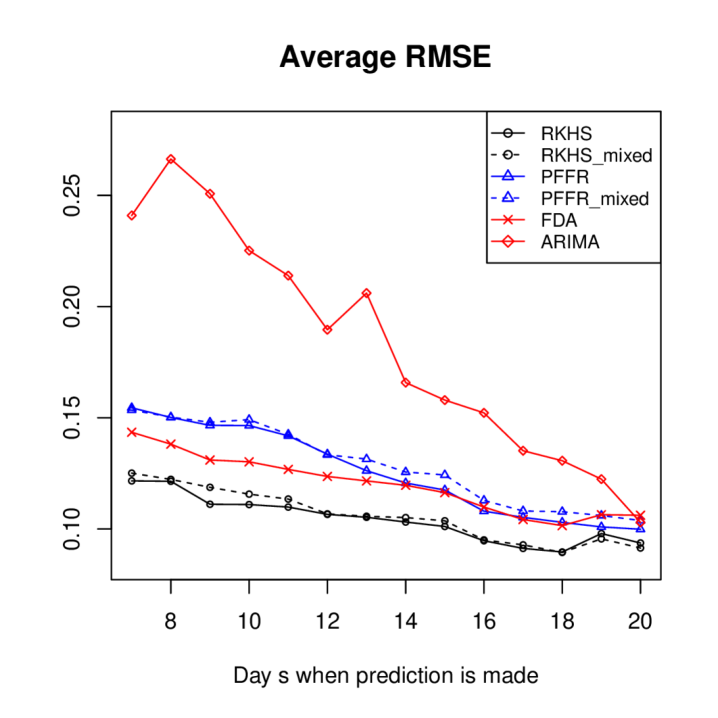

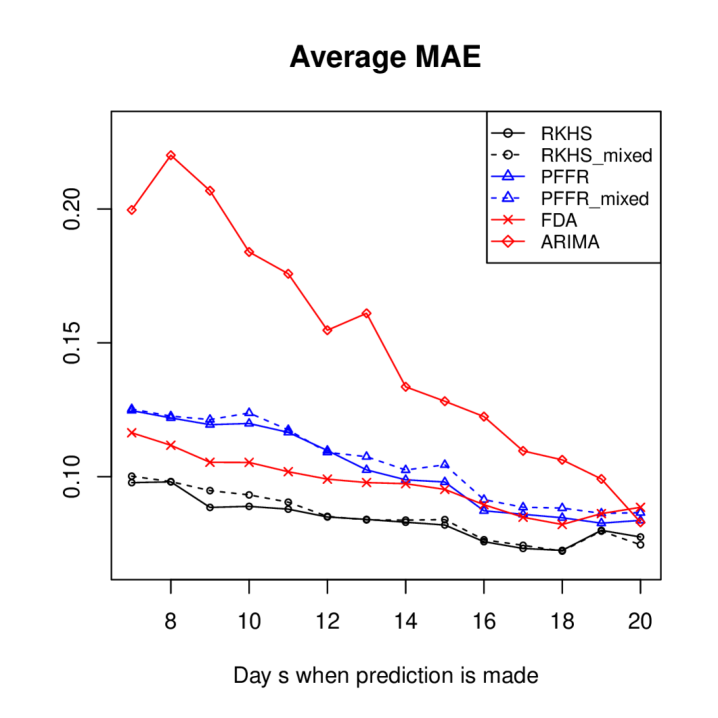

The dataset consists of campaigns launched between Dec-01-2019 and Dec-31-2019. For each campaign , we observe its normalized curve 222Note that the normalized curve is as sufficient as the original curve for monitoring the fundraising process of each campaign. at 60 evenly spaced time points over its 30-day duration and denote it as . See Figure 1 for normalized curves of six representative campaigns. At a time , to predict for campaign , we employ functional regression, where we treat as the functional response , use as the functional covariate and as the vector covariate. We compare the performances of RKHS, FDA and PFFR. Note that FDA only allows for one functional covariate, thus for RKHS and PFFR, we implement both the function-on-function regression and the functional regression with mixed predictors (denoted by RKHS and PFFR). The implementation of each method is the same as that in Sections 5.2 and 5.3.

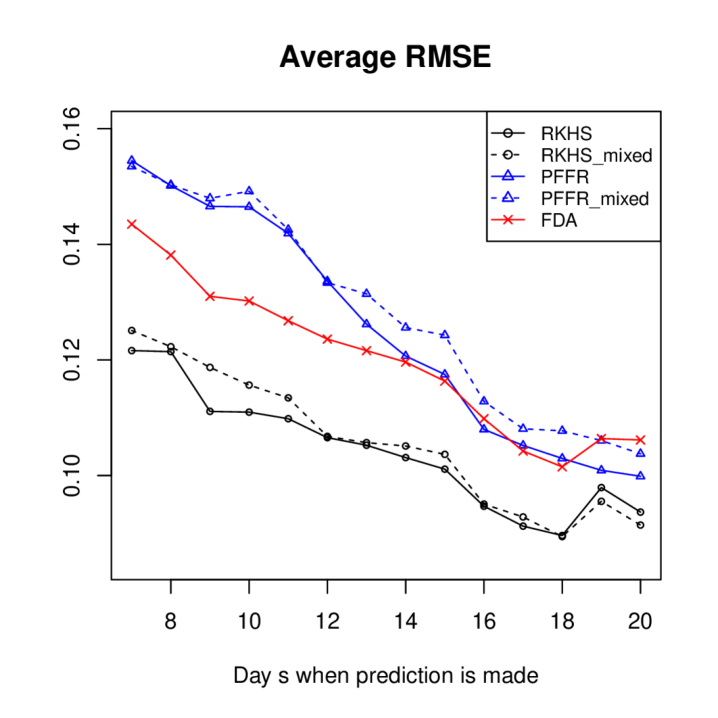

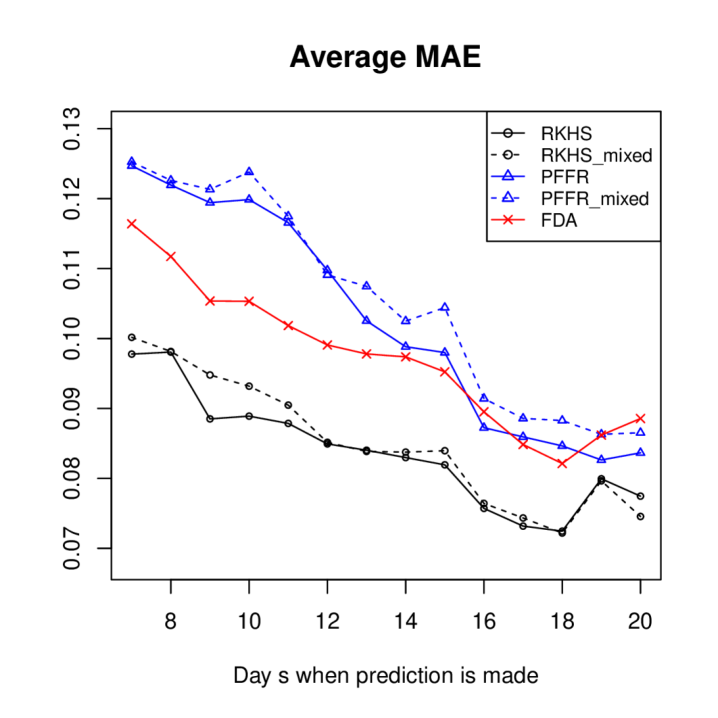

We vary the prediction time such that day of a campaign. Note that we stop at as prediction made in the late stage of a campaign is not as useful as early forecasts. To assess the out-of-sample performance of each method, we use a 2-fold CV, where we partition the 454 campaigns into two equal-sized sets and use one set to train the functional regression and the other to test the prediction performance, and then switch the role of the two sets. For each campaign in the test set, given its prediction generated at time , we calculate its RMSE and MAE with respect to the true value , where

and

Figure 5 visualizes RMSE and MAE achieved by different functional regression methods across In general, the two RKHS-based estimators consistently achieve the best prediction accuracy. As expected, the performance of all methods improve with approaching 20. Interestingly, the functional regression with mixed predictors does not seem to improve the prediction performance, which is especially evident for PFFR. Thanks to the group Lasso-type penalty, RKHS can perform variable selection on the vector covariate. Indeed, among the 28 (2 folds 14 days) estimated functional regression models based on RKHS, 19 models select no vector covariate and thus reduce to the function-on-function regression, suggesting the potential irrelevance of the vector covariate. We further provide a robustness check of the above analysis in Section H, where we repeat the 2-fold CV procedure 100 times for RKHS, FDA and PFFR. It is seen that RKHS consistently provides the best performance, confirming the robustness of our findings. We refer to Section H for more details.

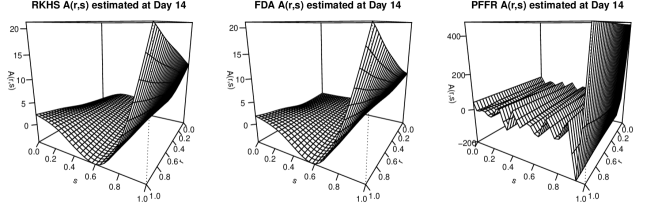

For more intuition, Figure 1 plots the normalized fundraising curves of six representative campaigns and further visualizes the functional predictions given by RKHS, FDA and PFFR at th day. Note that FDA and RKHS provide more similar prediction while the prediction of PFFR seems to be more volatile. This is indeed consistent with the estimated bivariate coefficient functions visualized in Figure 6, where of RKHS and FDA resembles each other while PFFR seems to suffer from under-smoothing.

6 Conclusion

In this paper, we study a functional linear regression model with functional responses and accommodating both functional and high-dimensional vector covariates. We provide a minimax lower bound on its excess risk. To match the lower bound, we propose an RKHS-based penalized least squares estimator, which is based on a generalization of the representer lemma and achieves the optimal upper bound on the excess risk. Our framework allows for partially observed functional variables and provides finite sample probability bounds. Furthermore, the result unveils an interesting phase transition between a high-dimensional parametric rate and a nonparametric rate in terms of the excess risk. A novel iterative coordinate descent based algorithm is proposed to efficiently solve the penalized least squares problem. Simulation studies and real data applications are further conducted, where the proposed estimator is seen to provide favorable performance compared to existing methods in the literature.

Throughout the paper, we assume knowledge of the kernel functions and . In practice, it would be ideal if one would be able to learn the kernel functions from data. However, to our best knowledge, assuming knowing the true kernel functions is adopted in all RKHS-based functional data analysis literature. Learning kernels is beyond the scope of our paper and we would like to pursue this direction in the future research. We would also like to point out that our estimator is a constrained estimator, with the constraints related with the true kernels. A mis-specification might lead to an over/under penalization, which will affect the final prediction error rate.

Finally, we briefly discuss important distinctions between non-parametric regression and functional regression for interested readers. To make the comparison easier, we consider a simpler setting: the scalar response functional linear regression and the classical non-parametric regression.

In non-parametric regression, we have

where are assumed to be random or fixed grid points in . In scalar response functional linear regression with fully observed functional data, we have

| (23) |

where are assumed to be i.i.d. stochastic processes in . Note that we can treat and as infinite-dimensional vectors w.r.t. some basis system, thus model (23) can be rewritten as

where . Under the standard assumption that , the eigenvalue sequence of the covariance matrix converges to . As such, model (23) was described as a high-dimensional or infinitely-dimensional “ill-posed” linear regression model in Hall and Horowitz (2007), which is fundamentally different from the standard non-parametric regression.

Acknowledgments

We would like to thank the action editor, Dr. Pradeep Ravikumar, as well as the four anonymous reviewers for their thoughtful assessment and constructive comments which helped us to improve the quality and the presentation of our paper. Z.Z. would like to acknowledge support from NSF DMS-2014053. Y.Y. would like to acknowledge support from DMS-EPSRC EP/V013432/1 and EPSRC EP/W003716/1. R.W. would like to acknowledge support from AFOSR FA9550‐18‐1‐0166, DOE DE‐AC02‐06CH113575, NSF DMS‐1925101, ARO W911NF-17-1-0357, and NGA HM0476-17-1-2003.

References

- Aue et al. (2015) Alexander Aue, Diogo Dubart Norinho, and Siegfried Hörmann. On the prediction of stationary functional time series. Journal of the American Statistical Association, 110(509):378–392, 2015.

- Bartlett et al. (2005) Peter L Bartlett, Olivier Bousquet, and Shahar Mendelson. Local rademacher complexities. The Annals of Statistics, 33(4):1497–1537, 2005.

- Bathia et al. (2010) Neil Bathia, Qiwei Yao, and Flavio Ziegelmann. Identifying the finite dimensionality of curve time series. The Annals of Statistics, 38(6):3352–3386, 2010.

- Benko (2007) Michal Benko. Functional data analysis with applications in finance. Humboldt-Universität zu Berlin, Wirtschaftswissenschaftliche Fakultät, 2007.

- Bonner et al. (2014) Simon J Bonner, Nathaniel K Newlands, and Nancy E Heckman. Modeling regional impacts of climate teleconnections using functional data analysis. Environmental and ecological statistics, 21(1):1–26, 2014.

- Brezis (2010) Haim Brezis. Functional analysis, Sobolev spaces and partial differential equations. Springer Science & Business Media, 2010.

- Bühlmann and van de Geer (2011) Peter Bühlmann and Sara van de Geer. Statistics for high-dimensional data: methods, theory and applications. Springer Science & Business Media, 2011.

- Cai and Hall (2006) T Tony Cai and Peter Hall. Prediction in functional linear regression. The Annals of Statistics, 34(5):2159–2179, 2006.

- Cai and Yuan (2011) T Tony Cai and Ming Yuan. Optimal estimation of the mean function based on discretely sampled functional data: Phase transition. The annals of statistics, 39(5):2330–2355, 2011.

- Cai and Yuan (2012) T Tony Cai and Ming Yuan. Minimax and adaptive prediction for functional linear regression. Journal of the American Statistical Association, 107(499):1201–1216, 2012.

- Cai and Yuan (2010) Tony Cai and Ming Yuan. Nonparametric covariance function estimation for functional and longitudinal data. University of Pennsylvania and Georgia inistitute of technology, 2010.

- Cardot et al. (2003) Hervé Cardot, Frédéric Ferraty, and Pascal Sarda. Spline estimators for the functional linear model. Statistica Sinica, pages 571–591, 2003.

- Chen et al. (2017) Kehui Chen, Pedro Francisco Delicado Useros, and Hans-Georg Müller. Modelling function-valued stochastic processes, with applications to fertility dynamics. Journal of the Royal Statistical Society. Series B, Statistical Methodology, 79(1):177–196, 2017.

- Chiou et al. (2014) Jeng-Min Chiou, Yi-Chen Zhang, Wan-Hui Chen, and Chiung-Wen Chang. A functional data approach to missing value imputation and outlier detection for traffic flow data. Transportmetrica B: Transport Dynamics, 2(2):106–129, 2014.

- Dai et al. (2019) Xiongtao Dai, Hans-Georg Müller, Jane-Ling Wang, and Sean CL Deoni. Age-dynamic networks and functional correlation for early white matter myelination. Brain Structure and Function, 224(2):535–551, 2019.

- Evans (2010) Lawrence C Evans. Partial differential equations. second. vol. 19. Graduate Studies in Mathematics. American Mathematical Society, 2010.

- Fan et al. (2014) Yingying Fan, Natasha Foutz, Gareth M James, and Wolfgang Jank. Functional response additive model estimation with online virtual stock markets. The Annals of Applied Statistics, 8(4):2435–2460, 2014.

- Fan et al. (2015) Yingying Fan, Gareth M James, and Peter Radchenko. Functional additive regression. The Annals of Statistics, 43(5):2296–2325, 2015.

- Faraway (1997) Julian J Faraway. Regression analysis for a functional response. Technometrics, 39(3):254–261, 1997.

- Ferraty and Vieu (2009) Frédéric Ferraty and Philippe Vieu. Additive prediction and boosting for functional data. Computational Statistics & Data Analysis, 53(4):1400–1413, 2009.

- Fraiman et al. (2014) Ricardo Fraiman, Ana Justel, Regina Liu, and Pamela Llop. Detecting trends in time series of functional data: A study of antarctic climate change. Canadian Journal of Statistics, 42(4):597–609, 2014.

- Friedman et al. (2010) Jerome H. Friedman, Trevor Hastie, and Robert Tibshirani. A note on the group lasso and a sparse group lasso. arXiv:1001.0736, 2010.

- Gu (2013) Chong Gu. Smoothing Spline ANOVA Models. Springer-Verlag, New York, 2 edition, 2013.

- Hadjipantelis et al. (2015) Pantelis Z Hadjipantelis, John AD Aston, Hans-Georg Müller, and Jonathan P Evans. Unifying amplitude and phase analysis: A compositional data approach to functional multivariate mixed-effects modeling of mandarin chinese. Journal of the American Statistical Association, 110(510):545–559, 2015.

- Hall and Horowitz (2007) Peter Hall and Joel L Horowitz. Methodology and convergence rates for functional linear regression. The Annals of Statistics, 35(1):70–91, 2007.

- Hastie et al. (2009) Trevor Hastie, Robert Tibshirani, and Jerome H. Friedman. The Elements of Statistical Learning. Springer-Verlag New York, 2 edition, 2009.

- Ivanescu et al. (2015) Andrada E Ivanescu, Ana-Maria Staicu, Fabian Scheipl, and Sonja Greven. Penalized function-on-function regression. Computational Statistics, 30(2):539–568, 2015.

- Jiang et al. (2014) Ci-Ren Jiang, Wei Yu, Jane-Ling Wang, et al. Inverse regression for longitudinal data. The Annals of Statistics, 42(2):563–591, 2014.

- Kneip et al. (2016) Alois Kneip, Dominik Poß, and Pascal Sarda. Functional linear regression with points of impact. The Annals of Statistics, 44(1):1–30, 2016.

- Koltchinskii and Yuan (2010) Vladimir Koltchinskii and Ming Yuan. Sparsity in multiple kernel learning. The Annals of Statistics, 38(6):3660–3695, 2010.

- Laird and Ware (1982) Nan M Laird and James H Ware. Random-effects models for longitudinal data. Biometrics, pages 963–974, 1982.

- Li and Hsing (2010) Yehua Li and Tailen Hsing. Uniform convergence rates for nonparametric regression and principal component analysis in functional/longitudinal data. The Annals of Statistics, 38(6):3321–3351, 2010.

- Liang et al. (2003) Hua Liang, Hulin Wu, and Raymond J Carroll. The relationship between virologic and immunologic responses in aids clinical research using mixed-effects varying-coefficient models with measurement error. Biostatistics, 4(2):297–312, 2003.

- Lin and Yuan (2006) Yi Lin and Ming Yuan. Convergence rates of compactly supported radial basis function regularization. Statistica Sinica, pages 425–439, 2006.

- Loh and Wainwright (2012) Po-Ling Loh and Martin J Wainwright. High-dimensional regression with noisy and missing data: Provable guarantees with nonconvexity. The Annals of Statistics, 40(3):1637–1664, 2012.

- Mendelson (2002) Shahar Mendelson. Geometric parameters of kernel machines. In International Conference on Computational Learning Theory, pages 29–43. Springer, 2002.

- Mercer (1909) James Mercer. Xvi. functions of positive and negative type, and their connection the theory of integral equations. Philosophical transactions of the royal society of London. Series A, containing papers of a mathematical or physical character, 209(441-458):415–446, 1909.

- Morris (2015) Jeffrey S Morris. Functional regression. Annual Review of Statistics and Its Application, 2:321–359, 2015.

- Park et al. (2018) Byeong U Park, Chun-Jui Chen, Wenwen Tao, and Hans-Georg Müller. Singular additive models for function to function regression. Statistica Sinica, 28(4):2497–2520, 2018.

- Petersen et al. (2019) Alexander Petersen, Sean Deoni, and Hans-Georg Müller. Fréchet estimation of time-varying covariance matrices from sparse data, with application to the regional co-evolution of myelination in the developing brain. The Annals of Applied Statistics, 13(1):393–419, 2019.

- Ramsay and Ramsey (2002) James O Ramsay and James B Ramsey. Functional data analysis of the dynamics of the monthly index of nondurable goods production. Journal of Econometrics, 107(1-2):327–344, 2002.

- Ramsay and Silverman (2005) J.O. Ramsay and B.W. Silverman. Functional Data Analysis. Springer-Verlag, New York, 2005.

- Raskutti et al. (2010) Garvesh Raskutti, Martin J Wainwright, and Bin Yu. Restricted eigenvalue properties for correlated gaussian designs. The Journal of Machine Learning Research, 11:2241–2259, 2010.

- Raskutti et al. (2011) Garvesh Raskutti, Martin J Wainwright, and Bin Yu. Minimax rates of estimation for high-dimensional linear regression over lq -balls. IEEE transactions on information theory, 57(10):6976–6994, 2011.

- Raskutti et al. (2012) Garvesh Raskutti, Martin J Wainwright, and Bin Yu. Minimax-optimal rates for sparse additive models over kernel classes via convex programming. Journal of machine learning research, 13(2), 2012.

- Ratcliffe et al. (2002) Sarah J Ratcliffe, Gillian Z Heller, and Leo R Leader. Functional data analysis with application to periodically stimulated foetal heart rate data. ii: Functional logistic regression. Statistics in medicine, 21(8):1115–1127, 2002.

- Reimherr et al. (2018) Matthew Reimherr, Bharath Sriperumbudur, Bahaeddine Taoufik, et al. Optimal prediction for additive function-on-function regression. Electronic Journal of Statistics, 12(2):4571–4601, 2018.

- Reimherr et al. (2019) Matthew Reimherr, Bharath Sriperumbudur, and Hyun Bin Kang. Optimal function-on-scalar regression over complex domains. arXiv preprint arXiv:1902.07284, 2019.

- Sun et al. (2018) Xiaoxiao Sun, Pang Du, Xiao Wang, and Ping Ma. Optimal penalized function-on-function regression under a reproducing kernel hilbert space framework. Journal of the American Statistical Association, 113(524):1601–1611, 2018.

- Tavakoli et al. (2019) Shahin Tavakoli, Davide Pigoli, John AD Aston, and John S Coleman. A spatial modeling approach for linguistic object data: Analyzing dialect sound variations across great britain. Journal of the American Statistical Association, 114(527):1081–1096, 2019.

- Valencia and Yuan (2013) Carlos Valencia and Ming Yuan. Radial basis function regularization for linear inverse problems with random noise. Journal of Multivariate Analysis, 116:92–108, 2013.

- van Delft et al. (2017) Anne van Delft, Vaidotas Characiejus, and Holger Dette. A nonparametric test for stationarity in functional time series. arXiv preprint arXiv:1708.05248, 2017.

- Vershynin (2018) Roman Vershynin. High-dimensional probability: An introduction with applications in data science, volume 47. Cambridge university press, 2018.

- Wagner-Muns et al. (2017) Isaac Michael Wagner-Muns, Ivan G Guardiola, VA Samaranayke, and Wasim Irshad Kayani. A functional data analysis approach to traffic volume forecasting. IEEE Transactions on Intelligent Transportation Systems, 19(3):878–888, 2017.

- Wahba (1990) Grace Wahba. Spline models for observational data. SIAM, 1990.

- Wang et al. (2020a) Daren Wang, Zifeng Zhao, Rebecca Willett, and Chun Yip Yau. Functional autoregressive processes in reproducing kernel hilbert spaces. arXiv preprint arXiv:2011.13993, 2020a.

- Wang et al. (2016) Jane-Ling Wang, Jeng-Min Chiou, and Hans-Georg Müller. Functional data analysis. Annual Review of Statistics and Its Application, 3:257–295, 2016.

- Wang et al. (2020b) Jiayi Wang, Raymond KW Wong, and Xiaoke Zhang. Low-rank covariance function estimation for multidimensional functional data. Journal of the American Statistical Association, pages 1–14, 2020b.

- Wang et al. (2014) Yu-Xiang Wang, Alex Smola, and Ryan Tibshirani. The falling factorial basis and its statistical applications. In International Conference on Machine Learning, pages 730–738. PMLR, 2014.

- Wright (2015) Stephen J. Wright. Coordinate descent algorithms. Mathematical Programming, 151:3–34, 2015.

- Wu and Chiang (2000) Colin O Wu and Chin-Tsang Chiang. Kernel smoothing on varying coefficient models with longitudinal dependent variable. Statistica Sinica, pages 433–456, 2000.

- Wu et al. (1998) Colin O Wu, Chin-Tsang Chiang, and Donald R Hoover. Asymptotic confidence regions for kernel smoothing of a varying-coefficient model with longitudinal data. Journal of the American statistical Association, 93(444):1388–1402, 1998.

- Yan (2007) Ming-Yi Yan. Economic data analysis: an approach based on functional viewpoint of data [j]. Modern Economic Science, 1, 2007.

- Yao et al. (2005) Fang Yao, Hans-Georg Müller, and Jane-Ling Wang. Functional linear regression analysis for longitudinal data. The Annals of Statistics, pages 2873–2903, 2005.

- Yu (1997) Bin Yu. Assouad, fano, and le cam. In Yang G.L. Pollard D., Torgersen E., editor, Festschrift for Lucien Le Cam, pages 423–435. Springer, New York, NY, 1997.

- Yuan and Cai (2010) Ming Yuan and T Tony Cai. A reproducing kernel hilbert space approach to functional linear regression. The Annals of Statistics, 38(6):3412–3444, 2010.

Appendices

Section A provides more discussions on the connection between bivariate functions and compact linear operators, Assumptions 2 and 3. Section B collects proofs of results in Section 3. Section C contains a series of deviation bounds, which are interesting per se. Section D contains the proof of Proposition 3. Section E includes additional details on technical proofs. Section F collects additional details on optimization. Additional numerical details are exhibited in Appendices G, H, I, J, K and L.

A More discussions on bivariate functions, Assumptions 2 and 3

A.1 Bivariate functions and compact linear operators

Remark 4

Fro any compact linear operator denote

Note that is well defined for any due to the compactness of . Define , . We thus have for any , it holds that

where the fourth identity follows from the compactness of This justifies Equation 2.

A.2 2(d)

In 2(d), we assume that

i.e. the functional and vector covariates are allowed to be correlated up to . In this subsection, we emphasize that the correlation cannot be equal to one. We first note that

| (24) |

For model identification, we require the inequality in (24) to be strict. To see this, we suppose that there exist and such that

Since and are both normal random variables, the above equality implies that the correlation between and is 1 and thus for some constant . This means that the model defined in (1) is no longer identifiable, because the covariates are perfectly correlated. Even in finite-dimensional regression problems, if the covariates are perfectly correlated, the solution to the linear system is ill-defined.

A.3 3(b)

Recall that 3 is required for handling the case where the functional observations are on discrete sample points. 3(a) formalizes the sampling scheme and 3(b) requires that the second moment of the random variable is finite.

In the following, via a concrete example, we show that the second moment assumption in (7) holds under mild conditions. Specifically in Example 1, we provide a simple sufficient condition on the eigen-decay of the covariance operator , under which (7) holds for with .

Example 1

Let and suppose the Sobolev space is generated by the kernel

where due to the property of the Sobolev space, we have and can be taken as the Fourier basis such that . To better understand the second moment condition

we proceed by following the same strategy as in Cai and Hall (2006) and Yuan and Cai (2010) and assume that and are perfectly aligned, i.e., they share the same set of eigen-functions.

Let . We have that is a collection of independent Gaussian random variables such that , where are the eigenvalues of . Thus we have

and

To assure that , it suffices to have that

for any constant . Note that when is close to , this means that the eigenvalues of decay at a polynomial rate slightly faster than 2.

B Proofs of the results in Section 3

B.1 Proof of Proposition 1

Proof [Proof of Proposition 1]

For any linear subspaces , let and be the projection mappings of the spaces and , respectively with respect to . For any and any compact linear operator , denote

Let be any solution to (3.1). Let , and . Denote , , and .

Let and be the orthogonal complements of and in , respectively. Then for any compact linear operator , we have the decomposition

Due to Lemma 5, there exist such that

Step 1. In this step, it is shown that for any compact linear operator , its associated bivariate function satisfies that only depend on . The details of the bivariate function is explained in Section A.1.

Observe that

Similar arguments also lead to that and , .

Step 2. By Step 1, it holds that , . By Lemma 5, we have that there exist such that for any ,

Therefore the associated bivariate function satisfies that, for all ,

where is used in the last inequality.

Step 3. For any and , by the definition of , we have that

Therefore

In addition, by Lemma 5 we have that

which completes the proof.

Lemma 5

Let be any Hilbert–Schmidt operator. Let be a collection of functions in . Let and be the subspaces of spanned by and , respectively. Let and be the projection mappings of the spaces and , respectively. Then there exist , which are not necessarily unique, such that for any ,

and that .

Proof Let and be orthogonal basis of subspaces and of , respectively, with . Since each () can be written as a linear combination of (), it suffices to show that there exist , such that for any ,

Since and are linear subspaces of , there exist , such that and are two orthogonal basis of , and that

where . Therefore

Moreover, we have that

which concludes the proof.

B.2 Proof of Theorem 2

Proof [Proof of Theorem 2]

First note that , then and . These inequalities will be used repeatedly in the rest of this proof. Recall the notation that and , . Note that for any , it holds that

The above expression will also be used repeatedly in the rest of the proof. Observe that for any , it holds that

where the first inequality follows from 3 b, which assumes that , the second inequality follows from Lemma 30 and the last inequality follows from the assumption that . Throughout the proof, we assume without loss of generality that In addition, observe that by Lemma 27, it holds that

By a union bound argument,

The rest of the proof is shown in the event of .

Let for sufficiently large constant . From the minimizer property, we have that

which implies that

| (25) | ||||

| (26) | ||||

| (27) | ||||

| (28) | ||||

| (29) |

In the rest of the proof, for readability, we will assume that

This assumption is equivalent to the case that and are equally spaced grid.

We note that in view of Lemma 33, the general case follows straightforwardly from the same argument and thus will be omitted for readability.

Step 1.

Observe that

| (30) | ||||

| (31) |

As for the term (30), we have that for any and ,

where the first inequality follows from Lemma 34 and event . By Lemma 33, it holds that for all ,

where and depends on and only. So,

for some absolute constant .

In addition, for Equation 31, note that with probability at least ,

| (32) |

where the second inequality holds because , the fourth inequality follows from Lemma 28, and the last inequality follows from the assumption that with sufficiently large . In addition, by 2(c),

So

Putting calculations for Equation 30 and Equation 31 together, we have that

| (33) |

Step 2. It follows from (43) that with probability at least , it holds that

| (34) |

where is an absolute constant.

It follows from (47) and (51), we have that with probability at least , it holds that

where is an absolute constant.

Step 3. Note that for Equation 29,

Step 4. Putting all previous calculations together leads to that

| (35) | ||||

| (36) |

where is some absolute constant.

For Equation 35, note that by constrain set , we have that

Therefore

From Theorem 21, it holds that with probability at least ,

Substitute the above inequality into Equation 35 gives

| (37) | ||||

Step 5. Note that by 2c,

where , the cardinality of the support set . This gives

| (38) |

which implies that

Substituting the above inequality into (37) gives

| (39) |

Step 6. Note that by definition, for any estimators and , and that

| (40) |

where and are the covariance of and , as defined in 2.

It follows from (54) that with probability at least ,

| (41) |

with being absolute constants. In addition, with absolute constants , due to (55), we have that

| (42) |

Finally, (39), (40), (41) and (42) together imply that with probability at least it holds that

where is some absolute constant. This directly leads to the desired result.

B.3 Additional proofs related to Theorem 2

In this section, we present the technical results related to Theorem 2. Recall in the proof of Theorem 2, we set that and , . Note that for any , it holds that

We also assume that the following good event holds:

It was justified in the proof of Theorem 2 that

Lemma 6

Let . Under the same conditions as in Theorem 2, with probability at least , it holds that

| (43) |

Proof Let and . Observe that for any and , we have

where the first inequality follows Lemma 34. By Lemma 33, we have that

where is an absolute constant. Therefore, we have that

| (44) |

By Lemma 14 and the fact that

we have that with probability at least , it holds that uniformly for all ,

where is an absolute constant. Thus the above display implies that

| (45) |

Therefore,

| (46) |

where the first inequality follows from (44) and the second inequality follows from (45).

Lemma 7

Let and . Under the same conditions as in Theorem 2, if in addition, , then with probability at least , it holds that

| (47) |

In addition, let be a collection of standard normal random variables independent of , and . Then with probability at least , it holds that

| (48) |

Proof Let . For Equation 47, note that

| (49) | ||||

| (50) |

Since for all

Lemma 12 implies that with probability , it holds that uniformly for all ,

where is an absolute constant. Therefore

To control the term (50), we deploy Lemma 13. Since

then with probability at least , it holds that that

where is an absolute constant.

Therefore, we have that with probability at least

that

where is an absolute constant. Equation 47 follows from the assumption that

The argument of Equation 48 is the same as that of Equation 47 and will be omitted for brevity.

Lemma 8

Let and . Under the same conditions as in Theorem 2, with probability at least , it holds that

| (51) |

In addition, let be a collection of standard normal random variables independent of , and . Then with probability at least , it holds that

| (52) |

Proof Let . For Equation 51, note that since is centered Gaussian with variance bounded by and is Gaussian with variance bounded by , is sub-exponential with parameter . Therefore by a union bound argument, there exists an absolute constant such that, for any ,

| (53) |

Therefore, with probability at least , it holds that

where the second inequality follows from (53), the third inequality follows from Hölder’s inequality, and the last inequality follows from the assumption that

for sufficiently large constant .

The argument of Equation 52 is the same as that of Equation 51 and will be omitted for brevity.

Lemma 9

Let . Under the same conditions as in Theorem 2, with probability at least , it holds that

| (54) |

Proof We have

where is the predictor in the test set. By Lemma 27, we have with probability at least that So it holds that

Let . Then

Applying Lemma 33 to , we have that

and this implies that

Lemma 10

Let . Under the same conditions as in Theorem 2, it holds that

| (55) |

Proof Note that since the minimal eigenvalue of is lower bounded by ,

By Lemma 33, there exists an absolute constant such that

| (56) |

As a result,

where the second inequality follows from (56), and the third inequality follows from

Therefore

| (57) |

where the last inequality follows from the fact that for all .

B.4 Extensions

Corollary 11

Corollary 11 is a direct consequence of Theorem 2 and provides a formal theoretical guarantee for using to evaluate the proposed estimators in practice.

B.5 Proof of Theorem 4

Proof [Proof of Theorem 4] The proof is almost identical to the proof of Theorem 2. As a result, we only point out the difference.

From the minimizer property, we have that

which implies that

| (60) | ||||

| (61) | ||||

| (62) | ||||

| (63) | ||||

| (64) | ||||

| (65) |

Note that Equation 60 - (64) are identical to Equation 25 - (29). So it suffices to analyzed Equation 65. Without loss of generality, we will assume that

It follows from (48) and (52), we have that with probability at least , it holds that

where is an absolute constant. The rest of the argument is identical to Theorem 2 and therefore is omitted.