Design-Robust Two-Way-Fixed-Effects Regression For Panel Data 00footnotetext: Generous support from the Office of Naval Research through ONR grants N00014-17-1-2131 and N00014-19-1-2468 is gratefully acknowledged.

Abstract

We propose a new estimator for average causal effects of a binary treatment with panel data in settings with general treatment patterns. Our approach augments the popular two-way-fixed-effects specification with unit-specific weights that arise from a model for the assignment mechanism. We show how to construct these weights in various settings, including the staggered adoption setting where units opt into the treatment sequentially but permanently. The resulting estimator converges to an average (over units and time) treatment effect under the correct specification of the assignment model even if the fixed effect model is misspecified. We show that our estimator is more robust than the conventional two-way estimator: it remains consistent if either the assignment mechanism or the two-way regression model is correctly specified. In addition the proposed estimator performs better than the two-way-fixed-effect estimator if both outcome model and assignment mechanism are locally misspecified. This strong double robustness property underlines and quantifies the benefits from modeling the assignment process and motivates using our estimator in practice. We also discuss an extension of our estimator to handle dynamic treatment effects.

Keywords: fixed effects, panel data, causal effects, treatment effects, double robustness, staggered adoption.

1 Introduction

Difference-in-difference (DiD) methods (e.g., Ashenfelter and Card (1985); Angrist and Krueger (1999)) are commonly used in empirical economics to establish causal relationships (see (Currie et al., 2020) for some evidence regarding the usage in the empirical literature). In particular, researchers estimate regression functions of the form

| (1.1) |

using ordinary least squares (OLS), treating and as fixed parameters – the fixed effects, leading to the two-way fixed effect (TWFE) estimator. Here is the outcome variable of interest, is a binary treatment, are observed exogenous characteristics, and is the main object of interest. Practitioners routinely justify regression (1.1) by appealing to “quasi-experimental” variation in treatment paths . Formal and informal arguments are invoked to make a case that this variation is not associated with unobserved unit and time-specific components . In other words, to motivate (1.1), researchers reason about the underlying model for . This model, however, does not explicitly enter the estimation process. Moreover, econometric assumptions that justify the OLS estimation apply conditionally on and do not appeal to randomness in the treatment paths (e.g., Arellano (2003)).

In this paper, we develop new methods for estimating causal effects that explicitly incorporates design assumptions on the assignment process without abandoning the transparency and simplicity of the two-way model. We incorporate assumptions about the assignment mechanism by augmenting the specification (1.1) with unit-specific weights , leading to

| (1.2) |

We compute the weights using the assignment model for .

We start our analysis by assuming that the assignment process for is known. In Section 2, we show how to use this knowledge to construct oracle weights and conduct design-based inference. Under the correct specification of the assignment model, our inference procedure is valid regardless of the underlying model for potential outcomes, and in particular, we do not rely on the validity of the equation (1.1). Our results substantially generalize the properties established in Athey and Imbens (2018), allowing for an arbitrary assignment process (subject to overlap restrictions).

To construct , we need to solve a nonlinear equation that depends on the support of . Practically, this means that the construction and the values of the weights vary across different types of designs. In Appendix C we provide solutions for several prominent examples, including staggered adoption, i.e., a situation where units opt into treatment sequentially. Another input we need for is the probability distribution of (generalized propensity score, Imbens (2000))).

After establishing design-based properties of the oracle estimator based on knowledge of the assignment process, we turn to the robustness – the behavior of the estimator in settings where the postulated assignment model is incorrect. At this point, we use the structure of the regression problem (1.2) to demonstrate that has a strong double-robustness property (Robins et al. (1994); Kang and Schafer (2007); Bang and Robins (2005); Chernozhukov et al. (2018)): it has a small bias whenever either the assignment or the regression model is approximately correct. We view these results as the primary motivation for using our estimator in practice, where we cannot expect either the TWFE model or the assignment model to be fully correct.

In practice, the assignment model is rarely completely known – unless -s are assigned in the controlled experiment – and has to be estimated. We use the insights from the known assignment setting as a building block in Section 3, where the assignment process is unknown but can be estimated consistently from the data. In Section 5 we use two empirical examples to show how to estimate this distribution for the staggered adoption design using duration models. This approach is connected to Shaikh and Toulis (2019) that uses a duration model to test a sharp null hypothesis that specifies no treatment effects.

Our focus on TWFE regression (1.2) is motivated by its increased popularity in economics (see Currie, Kleven, and Zwiers (2020) for documentation on this). In applications, this model provides an effective and parsimonious approximation for the baseline outcomes, allowing researchers to capture unobserved confounders and to improve the efficiency of the resulting estimator by reducing noise. At the same time, recent research shows that regression estimators for average treatment effects based on TWFE models might have undesirable properties, particularly negative weights for unit-time specific treatment effects. These concerns are particularly salient in settings with heterogeneity in treatment effects and general assignment patterns (e.g., De Chaisemartin and d’Haultfoeuille (2020); Goodman-Bacon (2018); Abraham and Sun (2018); Callaway and Sant’Anna (2018); Borusyak and Jaravel (2017)). Our results show that some of the concerns raised in this literature regarding negative weights lose some of their force under random assignment, or more generally once we properly reweight the observations. The insights from the current analysis, however, are not limited to the TWFE setting.

Our main analysis assumes that the treatment affects only contemporaneous outcomes, ruling out dynamic effects. We make this choice to crystallize the connection between the TWFE regression model (1.2) and the assignment process. We do not restrict heterogeneity in contemporaneous treatment effects that can vary over units and periods. To test for, or estimate, dynamic treatment effects, one has to compare units that receive treatment at different times. Such comparisons are justified only if we restrict individual heterogeneity in treatment effects or treat the assignment as random. Consequently, and this is of course a key insight from the causal inference literature in cross-section settings since Rosenbaum and Rubin (1983), it is imperative to model both the assignment mechanism and the outcome model. In Bojinov et al. (2020a) the authors show how to use the assignment process to estimate dynamic treatment effects (see also Blackwell and Yamauchi (2021) for the related analysis in large- setup). Our results suggest that a fruitful approach may be to construct robust estimators by combining Bojinov et al. (2020a) approach to estimation with conventional dynamic panel regression models using the weighting methods derived in the current paper for the static case. We discuss a particular realization of this in Section 4.

Our results are related to recent literature on doubly robust estimators with panel data. Conceptually the closest paper to us is Arkhangelsky and Imbens (2019) that also emphasizes the role of the assignment process in the same setting and shows double robustness. In Arkhangelsky and Imbens (2019) the focus is on a class of estimators defined as a linear function of realized outcomes, with the coefficients in that linear representation chosen to lead to consistent estimators for average treatment effects under either assumptions on the outcome model or on the assignment mechanism. Here we start with a different class of estimators, restricted to weighted versions of the TWFE estimator in (1.2). We also show how to estimate a flexible class of average treatment effects with user-specified weights over units and time. The double robustness property in our paper is distinct from the one analyzed recently in the difference-in-difference setting (e.g., Sant’Anna and Zhao (2020)): our estimator is robust to arbitrary violations of parallel trends assumptions, as long as the assignment model is correctly specified.

We also connect to recent work on causal panel model with experimental data (e.g., Athey and Imbens (2018); Bojinov et al. (2020a); Roth and Sant’Anna (2021)). Similar to these papers, we establish properties of regression estimators under design assumptions. Importantly, we consider a general setting without restricting our attention to staggered adoption design. Our contribution to this literature is the characterization of the behavior of for a large class of weighting functions and general designs. By establishing a connection between weighting functions and limiting estimands, we allow users to construct consistent estimators for a pre-specified weighted average treatment effect of interest.

Finally, the form of our estimator (1.2) connects it to the Synthetic Difference in Differences (SDID) estimator introduced in Arkhangelsky et al. (2019). The difference between these two procedures is in the way they construct the weights . The SDID estimator uses pretreatment outcomes to build a synthetic control unit that follows the path of the average treated unit as closely as possible (up to an additive shift). This strategy is infeasible if varies over time. However, precisely in situations with enough variation in , we can estimate the assignment process and use it to construct the weights . As a result, the two estimators are complementary and can be used in applications with different assignment patterns.

Throughout the paper, we adopt the standard probability notation . For any vector , denote by the transpose of , the norm of , and by the diagonal matrix with the coordinates of being the diagonal elements. For a pair of vectors , we write for their inner product . Furthermore, let denote the set , the identity matrix, and the -dimensional vector with all entries . Finally, the support of a discrete distribution is the set of elements with positive probabilities under .

2 Reshaped IPW Estimator With Known Assignment Mechanisms

We consider a setting with units and each unit is characterized by potential outcomes and a set of covariates .111Time-invariant covariates can be handled by letting . By writing the potential outcomes in this form, we assume away any dynamic effects of past treatments on current outcomes, thus focusing on static models. Analysis of such models is useful both theoretically and practically. First, they constitute a building block for more general environments. Second, when the treatment is irreversible, as in staggered adoption designs, we are likely interested in its average (over time) effect on the outcome rather than the transitory dynamics. This makes the static model a reasonable approximation for a more complicated dynamic model. Finally, if we observe the data at a lower frequency than the one that is relevant for dynamics (e.g., days vs. months), then the static model is the only available option.

Given the realized treatment assignment , the observed outcomes are defined in the usual way:

| (2.1) |

Throughout the paper, we treat covariates as fixed and consider as a random vector (jointly) drawn from a distribution (conditional on ). We let denote the joint distribution of the entire random vector (conditional on ) and denote the expectation over this distribution. We consider the asymptotic regime with going to infinity and fixed .

This structure nests the conventional sampling-based framework, which is common in panel data analysis, going back to (Chamberlain, 1984), and which was used to establish statistical results in the recent DiD literature (e.g. Abadie, 2005; Callaway and Sant’Anna, 2018). It also extends the standard fixed effects framework, where the distribution for each unit is characterized by unit-specific parameters, but units themselves are usually assumed independent (e.g. Neyman and Scott, 1948; Lancaster, 2000). Even in the absence of any covariates we do not assume that unit-level observations are independent or exchangeable, which brings two practical advantages. First, it allows us to accommodate correlated potential outcomes among units, which is natural in applications involving networks or multilevel structures. Second, it allows the assignments to be correlated across units, which is natural for many commonly used experimental designs. We elaborate on this point in the next section.

In this section we study a special case where the assignment mechanism is known. This assumption is natural for experimental settings, but in economics it has also been used to analyze the quasi-experimental settings as well (e.g. Borusyak and Hull, 2022). It allows us to derive inferential results under mild assumptions. We will consider the case of unknown designs in Section 3 at the cost of stronger (yet, standard) assumptions.

2.1 A design-based causal framework

We assume that, for any and ,

| (2.2) |

where is a distribution known to the analyst. We call it the generalized propensity score (Imbens (2000); Athey and Imbens (2018); Bojinov et al. (2020a, b)) – the marginal probability of the treatment path.

This structure allows for covariate-adaptive designs, where the probability of depends on past covariates. However, we rule out sequentially-adaptive designs where the assignment can depend on past outcomes, even if the randomization protocol is known.222Even if units are i.i.d. and is known, would depend on the unknown conditional distribution of given Furthermore, our framework places no restriction on the support of and substantially generalizes the previous works that focus on simple random sampling for non-staggered difference-in-differences (Rambachan and Roth, 2020) and staggered adoption (Athey and Imbens, 2018; Roth and Sant’Anna, 2021).

If the treatment paths are independent across units, then the marginal distributions characterize the joint distribution of . However, as discussed above, we allow the assignments to be correlated across units. In practice, this correlation can range from being very mild, as in the case of completely randomized experiments with a fixed share of treated units (Neyman, 1923/1990), to being sizable, as in cases of cluster-level randomization such as cluster randomized design (Abadie et al., 2023) and two-stage randomization. We impose technical restrictions on the dependence across units in Section 2.3.

2.2 Causal estimands

We define the unit and time-specific treatment effect as:

| (2.3) |

Note that can vary with both and since we assume neither identically distributed units nor time-homogeneous treatment effects. For time period , we define the time-specific ATE as:

| (2.4) |

and consider a broad class of weighted average of time-specific ATE:

| (2.5) |

for some user-specified deterministic weights such that

| (2.6) |

We refer to (2.5) as a doubly average treatment effect (DATE). For example, the weights yield the usual ATE over units and time periods. In the difference-in-differences setting with two time periods, . In a particular application, one might also be interested in an effect with time discounting factor that puts more weight on initial periods, i.e. for some .

Remark 2.1.

We can further generalize DATE by allowing for unequal unit weights:

| (2.7) |

where , and . Using appropriate propensity-based weights one can build estimands that target a given subpopulation.

2.3 Technical assumptions

We allow to be dependent across units to capture different assignment processes. Such dependence arises in applications, sometimes for technical reasons (e.g., in case of sampling without replacement as in Athey and Imbens (2018)), and sometimes by the nature of the assignment process (spatial experiments). To quantify this dependence as well as the dependence among the potential outcomes, we follow Rényi (1959) and define the maximal correlation:

| (2.8) |

In the standard design-based framework where potential outcomes are assumed fixed, it reduces to the -mixing coefficient between and . In the main text, we maintain a simplified restriction on leaving a more general one to Appendix A. The assumption is stated as follows:

Assumption 2.1.

There exists such that as approaches infinity the following holds:

| (2.9) |

Since by construction , measures the strength of correlation. When are independent across units, (2.9) holds with . More generally, when have a network dependency with if there is no edge between and , (2.9) is satisfied if the number of edges is . Note that it imposes no constraint on the maximum degree of the dependency graph. Even if the network is fully connected, it can still hold if the pairwise dependence is weak, e.g., sampling without replacement; see Appendix A.4. On the other hand, (2.9) excludes the case where all units are perfectly correlated or equicorrelated with a positive maximal correlation that is bounded away from .

We also impose minimal overlap restrictions on each :

Assumption 2.2.

There exists a universal constant and a non-stochastic subset with at least two elements and at least one element not in , such that

| (2.10) |

Our final assumption restricts the second moment of outcomes:

Assumption 2.3.

There exists such that .

It is presented here only for simplicity. We relax it substantially in Appendix A.

2.4 Reshaped IPW estimator

We consider a class of weighted TWFE regression estimators without covariates. We refer to them as reshaped inverse propensity weighted (RIPW) estimators, and formally define them as follows:

| (2.11) |

where is a density function on , i.e.,

| (2.12) |

We refer to the distribution as a reshaped distribution, and the weight as a RIP weight. To ensure that the RIPW estimator is well-defined, we require to be absolutely continuous with respect to each , i.e.

| (2.13) |

The estimator (2.11) is feasible for any such because is assumed to be known.

Adding covariates to the objective function (2.11) is relatively straightforward, however it considerably complicates the notation without contributing substantially to the primary narrative. We will explicitly incorporate covariates in the objective function in Section 3. Note that the covariates still play a role in the RIPW estimator through for covariate-adaptive designs.

The reshaped distribution can be interpreted as an experimental design. If , then and (2.11) reduces to the standard unweighted TWFE regression. If this is not the case, then acts like a likelihood ratio that changes the original design to one provided by . For cross-sectional data, we would like to shift the distribution to uniform , making the weights equal to if the fixed effects are not included. This would yield the standard IPW estimator. However, as we alluded to in the introduction, the situation is more complicated with the panel data, and shifting towards the uniform design might not deliver consistent estimators for the DATE of interest. We explore this formally in the next section where we characterize the set of that one can use. This interpretation of has one caveat: RIP weights only shift the marginal distribution of to , but they do not say anything about the joint distribution of which can remain complicated.

2.5 DATE equation and consistency of RIPW estimators

We now derive sufficient conditions under which the RIPW estimator is a consistent estimator for a given DATE of interest. The following theorem presents a precise condition for consistency of for :

Theorem 2.1.

This result has two user-specified parameters: time weights , and the reshaped distribution . They are naturally connected: to guarantee consistency for we can select such that the following holds:

| (2.14) |

Alternatively, for a given we can look for such that (2.14) is satisfied. We call (2.14) the DATE equation hereafter. For a fixed , it is a quadratic system with being the variables. Together with the density constraint (2.12) and the support constraint in Theorem 2.1 that for , there are equality constraints and inequality constraints that impose the positivity of for each . We will show in Appendix C that the DATE equation have closed-form solutions in various examples and provide a generic solver based on nonlinear programming in Appendix C.5.

Without further restrictions on , we can show that the DATE equation is also a necessary condition for consistency of for . To see this assume that

| (2.15) |

for some vector that is not proportional to . Because we can vary individual treatment effects without changing the average one, we can find a set that yields the same DATE but , leading to inconsistency. For we get that the inner product of the LHS of (2.15) and is because , while that of the right-hand side and is equal to . This entails that , and thus the DATE equation.

Notably, when the DATE equation has a solution, our estimator is consistent without any restrictions on the potential outcomes, except Assumption 2.3. This is in sharp contrast to usual results about TWFE estimators, which typically require the trends to be parallel among units, at least conditionally on observed covariates (e.g. Callaway and Sant’Anna, 2018; Sant’Anna and Zhao, 2020). Theorem 2.1 shows that if the assignment process is known and the DATE equation has a solution, we can correct the potentially misspecified TWFE regression model by simply reweighting the objective function.

To further parse the DATE equation, we discuss two alternative interpretations. First, fix and let be the solution of the DATE equation. Then consider a class of complete randomized experiments where all propensity scores are identical and are equal to . Then, by definition, the RIPW estimator with reshaped distribution reduces to the standard (unweighted) TWFE estimator. Theorem 2.1 guarantees that this estimator converges to , and by the above necessity argument, the DATE equation characterizes all complete randomized experiments under which this holds.

As an alternative interpretation, consider a fixed instead. For any such the (2.14) can be rewritten as

| (2.16) |

It is easy to see that

where . It is strictly positive since the support of involves a point , for which . Therefore, (2.16) implies that

| (2.17) |

By Theorem 2.1, in a randomized experiment with , the effective estimand of the unweighted TWFE regression is the DATE with weight vector . In particular, if corresponds to a uniformly distributed adoption date, then is equal to weights derived in (Athey and Imbens, 2018). The following result shows that the induced weights are guaranteed to be non-negative for arbitrary design.

Proposition 2.1.

Let be defined in (2.17). Then for any on , for all .

This result generalizes the conventional cross-sectional logic that says that in randomized experiments, regression estimators are consistent for average effects (e.g. Lin, 2013). However, in the case of the TWFE regression, the situation is more nuanced. While the resulting estimand always corresponds to a weighted average effect with non-negative weights, it still depends on the experimental design. As a result, if two analysts were to split a given population into two random subpopulations and conduct two distinct experiments on each part, the resulting estimands would have been different.

There are two reasons for this unusual behavior. First, in the cross-sectional case, has two points of support, while in the panel case the support of ranges from to points (as long as Assumption 2.2 is satisfied). For example, if none of the units is treated in the first period, it is impossible to identify any DATE that puts positive weight on the first period. Second, fixed effects lead to a familiar incidental parameter problem (Neyman and Scott, 1948), albeit in a mild form. To see this, consider , in which case the RIPW estimator corresponds to the conventional TWFE regression. The effective estimand for this regression is equal to the solution of (2.17) and is different from the effective estimand for the regression without the unit fixed effects. In other words, the presence of the unit fixed effects changes the estimator of the main parameter, which now has a different probability limit. This result demonstrates that the conventional wisdom that there is no incidental parameter bias in linear models is not valid for misspecified models.

Remark 2.2.

To estimate the generalized DATE defined in (2.7), we only need to mildly adjust the RIPW estimator:

| (2.18) |

In Appendix A.6 we prove that the adjusted RIPW estimator consistently estimates under the same set of assumptions as in Theorem 2.1, provided that , namely that all entries of are on the same scale.

2.6 Inference on RIPW estimators

To enable statistical inference of DATE, we first present an asymptotic expansion showing the asymptotic linearity of RIPW estimators.

Theorem 2.2.

Note that the asymptotic linear expansion holds under fairly general dependency structure in the treatment assignments. Below, we derive a valid confidence intervals for when are independent. The general case is discussed in Appendix A.4. If are well-behaved, Theorem 2.2 implies that

where is known by design. If were known, a natural estimator for would be the empirical variance:

We should not expect to converge to since in general varies over . Nonetheless, is an asymptotically conservative estimate of since

| (2.19) |

where the second term measures the heterogeneity of and is always non-negative, implying that is a conservative estimator for . This is unsurprising because even in the cross-section case, the asymptotic design-based variance is only partially identifiable due to the unknown correlation structure between two potential outcomes; see e.g. Neyman’s variance formula (Neyman, 1923/1990; Rubin, 1974).

In general, is unknown due to and the expectation terms. Nonetheless, we can estimate by replacing each expectation with the corresponding plug-in estimate, i.e.

| (2.20) |

and use them to compute the variance:

| (2.21) |

This yields a Wald-type confidence interval for as

| (2.22) |

where is the -th quantile of the standard normal distribution. Properties of this confidence interval are established in the next theorem.

In Appendix A.4, we discuss a generic result for general dependent assignments (Theorem A.6), which covers completely randomized experiments, blocked and matched pair experiments, two-stage randomized experiments, and so on. We present a detailed result (Theorem A.7) for completely randomized experiments where potential outcomes are fixed and ’s are sampled without replacement from a user-specified subset of . This substantially generalizes the setting of Athey and Imbens (2018) and Roth and Sant’Anna (2021) where the assignments are sampled without replacement from the set of staggered assignments.

2.7 Discussion

Theorem 2.1 and Proposition 2.1 might appear counter-intuitive given well-understood problems of TWFE estimators (e.g., de Chaisemartin and d’Haultfoeuille (2019); Goodman-Bacon (2018); Abraham and Sun (2018)). To put our result in context we emphasize two important features of the setup. First, we restrict attention to static models, and second, we use the randomness that is coming from . Both of these restrictions play a key role in Theorem 2.1. Absence of dynamic effects implies that we can meaningfully average units with different histories of past treatments. A version of this assumption is inescapable if we want the method to work for general designs where controlling for past history is practically infeasible. As we explain below, randomness of assignments helps to resolve the issue that TWFE estimators put negative weights on some individual treatment effects.

In de Chaisemartin and d’Haultfoeuille (2019); Goodman-Bacon (2018); Abraham and Sun (2018) the authors show that treated units are averaged with potentially negative weights, but these results are conditional on the assignments being fixed. Let be these weights for the general weighted least squares estimator defined in (1.2) such that

where we now explicitly allow them to depend on . When the assignments are treated as random, the large sample limit of is

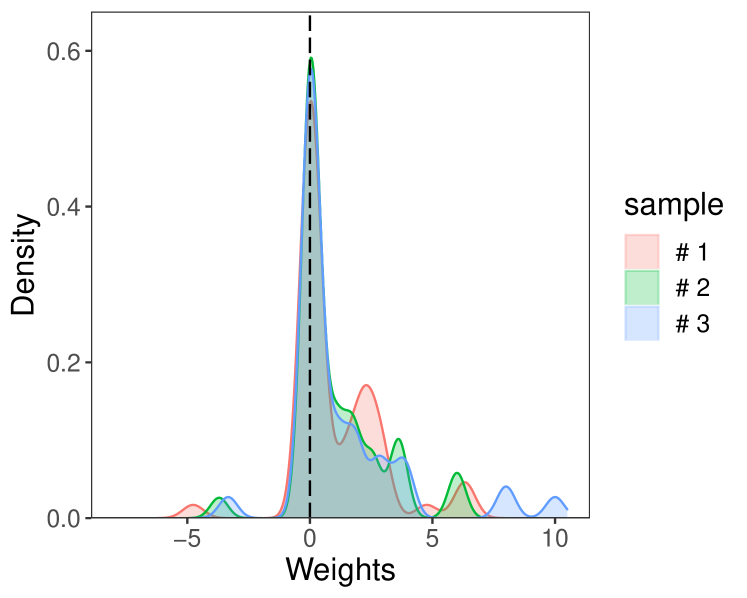

where . While is non-empty almost surely for every realization of , it is still possible that all are positive due to the averaging over . For illustration, we consider a simulation study with and other details specified in Section 5.1. We consider the conditional and unconditional weights induced by the unweighted and RIP weighted TWFE estimator in Figure 1 and Figure 2 respectively. We plot the histograms of for three realizations of and the histogram of , approximately by averaging over a million realizations of , where the multiplicative factor is chosen to normalize the weights into a more interpretable scale. Clearly, despite the large fraction of negative weights in each realization, their averages do not have any negatives. Therefore, the criticism on TWFE estimators does not apply in this case. Indeed, it never applies to the RIPW estimator by Proposition 2.1. In this study, all weights are designed to be when is a solution of the DATE equation with , as shown in Figure 2(b), regardless of the data generating process.

The discussion above demonstrates that while for each cell , a particular realization of weights can be negative, this fact is not systematic, i.e., on average. If we use the RIPW estimator designed for the equally-weighted DATE, then all cells will receive the same weight. An alternative description of the same phenomenon is that once correctly weighted, the realized treatment paths are uncorrelated with potential outcomes. This independence implies that there cannot be systematic differences in treatment effects among units with distinct assignment paths. The presence of such heterogeneity (together with dynamic treatment effects) is the main reason why negative weights create complications for the interpretation of the estimates.

Remark 2.3.

One might ask if Figure 1 (b) presents a general feature of unweighted TWFE estimators with random assignments. For completely randomized experiments where , the standard TWFE estimator is equivalent to the RIPW estimator with reshaped distribution . By Proposition 2.1, all weights are guaranteed to be non-negative.

When varies across units, the weights are not guaranteed to be non-negative. Consider the extreme case where assigns mass on one assignment pass and mass on all others. As , this approaches the case of fixed treatment assignments, for which the unconditional weights are almost the same as the conditional weights, which always include negative ones.

3 Reshaped IPW Estimator With Unknown Assignment Mechanisms

In this section, we move to non-experimental settings where the assignment mechanism is not controlled by the researcher and is unknown. We assume that researchers constructed unit-level estimates . In addition, we assume that the researchers have access to a set of estimates of . Further, let be the double-centered version of and be a shifted version of :

| (3.1) | |||

| (3.2) |

For notational convenience, we write for the vector and for the vector . Given a set of estimates , we define the RIPW estimator as

| (3.3) |

The above estimator generalizes (2.11) by allowing for regression adjustment. Throughout the rest of the paper, we will abuse the notation by denoting it as . This two-stage formulation replaces the regression with covariates by regression on the modified outcome without covariates, yielding a simplified structure which allows us to use previously established results. In the rest of this section, we discuss several strategies for constructing and formal properties they need to satisfy to guarantee consistency and asymptotic normality of .

In the previous section, we assumed that the researcher controlled the assignment process, which led to the restriction (2.2). In observational studies, the assignment process is unknown,, and we must substitute this restriction with a different assumption. Throughout this section, we impose a high-level restriction on the relationship between unit-specific potential outcomes and assignment paths.

Assumption 3.1.

(unit-specific mean ignorability)

| (3.4) |

Recall that we do not assume that are identically distributed across units. As a result, Assumption 3.1 imposes separate restrictions, one for each unit. It follows the tradition of the part of the panel data literature that treats unit-specific unobservables as fixed parameters (e.g. Lancaster, 2000; Hahn and Newey, 2004), rather than random variables as in (Chamberlain, 1984). It is trivially satisfied in an extreme case where has a degenerate distribution for each , which corresponds to the finite population analysis (e.g. Abadie et al., 2020). In applications where is random, this assumption imposes a strict exogeneity restriction. It describes the average behavior of the outcomes conditional on the whole treatment path and does not allow the current treatment to depend on past outcomes. To illustrate this connection, consider the classical linear TWFE model where

| (3.5) |

Assumption 3.1 is equivalent to for , which is a strict exogeneity restriction. In contrast, if only satisfies contemporenous restrictions , Assumption 3.1 does not necessarily hold.

Assumption (3.1) is also related to the recent cross-sectional literature on quasi-experimental designs (e.g. Borusyak and Hull, 2022). A typical restriction in that literature is that while the distribution of the treatment of interest varies over units in a complicated way it still can be estimated and then used to construct counterfactuals. For this approach to be valid, one needs to impose a version of Assumption 3.1.

To construct estimators we use the observed covariates . For the most par of the paper we do not explicitly specify these objects. However, our assumptions implicitly restrict the set of feasible covariates. In particular to respect Assumption 3.1, we do not allow any parts of the observed outcomes to be used as covariates. Situation is more delicate for and we allow fixed functions of to be part of as long as Assumption 2.2 holds. We elaborate on this in the next two sections.

3.1 Assignment model estimation

In strictly exogenous panel models, the distribution of is commonly left unspecified and the analysis is based on the outcome model alone. In particular, the distribution of can be degenerate for each , which is another extreme case where Assumption 3.1 trivially holds. However, researchers often informally appeal to random or quasi-random variation in as a source of identification, even though they continue using outcome-based methods, such as the TWFE regression. We interpret these informal statements as statistical restrictions on that go beyond Assumption 3.1.

Precisely because the arguments used in the applied work are often informal, we cannot offer and analyze a general methodology of how to use them to construct . Instead, we discuss several strategies that are potentially relevant for a large class of applications. Our goal is to demonstrate how to utilize the information used to construct the outcome-based estimators and thus is readily available. In practice, researchers can have other sources of information that we do not incorporate in our analysis. After this discussion, we continue our formal analysis under high-level assumptions on .

We use to estimate . At first glance, it might appear to be challenging to estimate the distribution of the whole vector. Nevertheless, treatment paths often have restricted support with a size much smaller than , such as staggered adoption and/or special structures that reduce the complexity of the distribution, such as the Markov structure. We present a few examples below for illustration.

In the staggered adoption designs is equivalent to an adoption time , where for never-treated units and for units initially treated at time . Then can be viewed as an event or during outcome, and one can apply any survival or duration model, such as the Cox proportional hazard model and accelerated failure time model, to estimate its distribution which yields by taking the difference between the consecutive points; see Section 5.2 for an empirical illustration that uses this strategy and additional discussion.

For transient treatments that occur at most once during the study period, can be expressed by the adoption time as above. The propensity score can then be estimated via a discrete choice model. Alternatively, one can use the strategy from Carneiro et al. (2003) though it would require the availability of additional information.

For general designs where the treatment can be alternated on and off, can be reparametrized as a sequence of conditional distributions and estimated by a Markov model. In particular, Arkhangelsky and Imbens (2019) show that if incorporates appropriate sufficient statistics, then conditioning on eliminates the ex-ante present unobserved heterogeneity from the distribution of .

Given an estimate , we say that it estimates the assignment model well if is close to in distance. Specifically, for each unit we define the accuracy of as

| (3.6) |

Here, the expectation is taken over both and (conditional on ). In the setting of Section 2, because .

3.2 Outcome model estimation

In this section, we discuss the construction of the terms which we use to build the estimator (3.3). We start with unit specific quantities , which we view as estimators for . There are many ways of constructing such estimators, and our results require only high-level restrictions on these objects. For example, one can consider a generalization of the linear TWFE model (3.5):

| (3.7) |

Then can be chosen as

| (3.8) |

where the parameters are estimated by regressing on , the covariate-treatment interaction , and a set of fixed effects. When we estimate for a new unit whose unit fixed effect is not estimated, we can simply set .

In the cross-sectional case, an estimate is considered an accurate estimate of if is small on average (e.g. Robins et al., 1994; Kang and Schafer, 2007). Constructing such estimators for panel models with fixed effects and a finite number of periods is impossible. Thus, the standard approach of measuring accuracy does not apply in our setting, and we need to consider alternative measures.

We start by defining the estimands that attempt to estimate:

| (3.9) | |||

| (3.10) |

We say that the outcome model is correctly specified if , where

| (3.11) |

The first term captures the estimation accuracy of , and the second term captures the estimation accuracy of . By definition, is invariant if we replace by and by for any , and . Thus, requiring to be small is strictly less stringent than requiring the standard measure of outcome model accuracy for cross-sectional data to be small.

In the simplest TWFE model (3.5) without covariates, if we choose . For the more general TWFE model (3.7), regardless whether unit is used for fitting the TWFE regression,

Standard assumptions (e.g. Arellano, 2003; Wooldridge, 2010) guarantee that are consistent for even with a finite number of periods. We can further generalize the model by replacing and with nonlinear functions and and estimate them by nonparametric TWFE regressions (Boneva et al., 2015).

The requirement that , at least on average, puts restrictions on the treatment effects. These requirements, however, can be redundant, depending on the structure of . For example, Wooldridge (2021) shows that the problems with heterogeneous treatment effects can be solved, under conditional parallel trends and linearity, by including a sufficiently rich set of controls, which includes functions of . In the staggered adoption case, one needs to include interactions with all the adoption dates. Unfortunately, including such interactions into violates the overlap assumption 2.2.

3.3 Consistency of RIPW estimators

We need extra assumptions to investigate the consistency of the estimator (3.3). We start with the simplified case where are independent of the data and thus can be treated as fixed. In addition to Assumptions 2.1 - 2.3, we need extra assumptions on these estimates. Similar to Section 2, these assumptions are stated for ease of interpretation and further relaxed in Appendix A.

Assumption 3.2.

There exists such that, for the same defined in Assumption 2.2,

Assumption 3.3.

There exists such that .

Theorem 2.1 implies that the RIPW estimator with being a solution of the DATE equation, if any, is a consistent estimator of DATE without any outcome model when is known. On the other hand, when the outcome model is correctly specified, is a linear model with two-way fixed effects and a single predictor and is approximately a weighted least squares estimator which is consistent under mild conditions on the weights (e.g., Wooldridge, 2010). This shows a weak double robustness property that is consistent if either the outcome model or the assignment model is exactly correct.

For cross-sectional data, the augmented IPW estimator enjoys a strong double robustness property, which states that the asymptotic bias is the product of estimation errors of the outcome and assignment models (e.g., Robins et al., 1994; Kang and Schafer, 2007; Chernozhukov et al., 2017, 2018). Clearly, this implies the weak double robustness. It further implies the estimator has higher asymptotic precision than estimators based on merely the outcome or assignment modeling when both models are estimated well. The next result provides a sufficient condition for strong double robustness of when the estimated treatment and outcome models are independent of the data.

Theorem 3.1.

Assume that are independent of the data. Under Assumptions 2.1-2.3 and 3.1 - 3.3, conditional on the estimates,

In particular, is a consistent estimator of if .

Assumptions 2.3 and 3.3 guarantee that is bounded. Thus, the RIPW estimator is consistent whenever is consistently estimated without any requirement on the rate of convergence. On the other hand, under the TWFE model (3.7) or nonparametric TWFE models discussed in the last subsection, and the estimator is consistent even if the assignment model is globally misspecified.

3.4 Inference with independent model estimates

Similar to Theorem 2.2, we can derive an asymptotic linear expansion for .

Theorem 3.2.

Similar to Section 2, we can estimate the asymptotic variance via (2.21) and construct the Wald-type confidence interval as (2.22) when units are independent. This is a special case of Theorem A.6 in Appendix A.4 for general dependent designs.

Theorem 3.3.

Under Assumption 3.1, Theorem 3.2 and Theorem 3.3 strictly generalize Theorem 2.2 and Theorem 2.3 – when is known, and hence regardless of the accuracy of the outcome model estimates. When is unknown, and are typically no less than without external data. As a result, both models should be consistently estimated to achieve though the estimates can have a slower convergence rate than . For example, it would be satisfied if . We emphasize that this rate requirement is standard for inference with cross-sectional data (Chernozhukov et al., 2017, 2018). Under this rate condition, by virtue of the asymptotic linear expansion in Theorem 3.2, the researcher can safely ignore the variability of the model estimates and use them in the variance calculation as if they are the truth.

Even when condition is violated, the asymptotically valid inference may still be possible at the cost of more involved variance estimation. We do not develop formal results for these cases because they rely on particular implementations of the underlying estimators but otherwise follow standard practice. In particular, if the estimators come from a smooth parametric model, then one can use their asymptotic expansion (around their limits, which do not necessarily correspond to the true parameters) to compute the asymptotic variance. In particular, if are estimated by the standard TWFE regressions and are well-behaved, then one can use standard inference results for correctly specified weighted OLS regressions.

In practice, it is uncommon to obtain estimates of that are independent of the data, except in the design-based inference where and , or when external data is available. Usually, these parameters need to be estimated from the data. The resulting dependence invalidates the assumptions of Theorem 3.2 and 3.3. However, as we show in Appendix B similar results hold if we use a particular version of cross-fitting. Note that this implies that cannot contain unit-specific fixed effects.

4 Design-robust event study specifications

A key limitation of our analysis in previous sections is the focus on static models. This is important both theoretically and practically. Theoretically, some policies of interest are transient in nature, e.g., a large infrastructure investment, but policymakers expect them to have a lasting impact, which requires a dynamic model. Practically, a large part of applied work in economics uses regression models that explicitly incorporate lags of treatment variables.

We consider a relatively simple class of linear potential outcome modes to address these concerns. For every and , we specify the potential outcomes as a function of the current treatment and its lags:

| (4.1) |

As in Section 3, the expectation is conditional on covariates, and we do not require the units to be independent or identically distributed. This model does not restrict the baseline outcomes but puts structure on the dynamic effects of the treatment. First, the effect of the treatment is present only for periods after it is implemented. Second, the effect is linear, i.e., the causal effect of being treated one period ago, , does not depend on whether the unit was treated two periods ago . Finally, the effects are homogenous over time, meaning that do not depend on calendar time . These restrictions are important: the first eliminates the possibility of long-term effects, while the other two eliminate state dependence. Still, we think this model is flexible enough to be useful for a large class of empirical applications.

Interestingly, if the treatment timing is fixed and common across units, and is large enough, then (4.1) is a parametrization of all realizable potential outcomes and thus does not impose any testable restrictions. To see this, let denote the adoption time and set . Then each unit has potential outcomes and . It is easy to see that (4.1) holds with , , and

Similar logic extends to staggered adoption designs as long as we treat the assignment as fixed. However, it breaks if we assume that the adoption time is randomly assigned. In this case, we can test the static model from Section 2 and the dynamic model (4.1) by comparing outcomes across units that were previously treated at different periods. This emphasizes the importance of the assignment model for the analysis of dynamic effects.

In this case, it is natural to consider the RIPW estimator coupled with an event-study regression model, i.e.,

| (4.2) |

where is defined as whenever . Our next result describes the probability limit of . The proof is presented in Appendix A.7.

Theorem 4.1.

This result justifies using the RIPW estimator in a large class of applications. If -s are unknown, then one can estimate them using one of the strategies discussed in the previous section. Similarly, one can introduce covariates in this model in the same way as before. Also, applied researchers often consider leads in addition to lags in their regressions, especially in the context of staggered adoption designs. To incorporate this practice into our framework, one simply needs to shift the treatment path appropriately. The resulting estimators for the leads can then be used to test for the validity of the underlying model.

We do not establish analogs of Theorems 3.1 - 3.3 for this estimator, but we expect them to hold under appropriate technical conditions. In particular, under (4.1), if the TWFE model holds for the baseline potential outcomes such that and , then (4.2) is consistent for since it is a weighted least squares estimator for a correctly specified linear model. Compared to our analysis in previous sections, the reshaping distribution does not play a major role in these results. The reason for this behavior is that the model for treatment effects is time-homogeneous. If we relax this assumption and allow for time-varying dynamic effects , then the distribution becomes important again. The corresponding DATE equation for this problem is more complicated than the one presented in Section 2, and its analysis is beyond the scope of this paper.

5 Numerical Studies

In this section, we investigate the properties of our estimator in simulations and show how to apply it to real datasets. The R programs to replicate all results in this section is available at https://github.com/xiaomanluo/ripwPaper.

5.1 Synthetic data

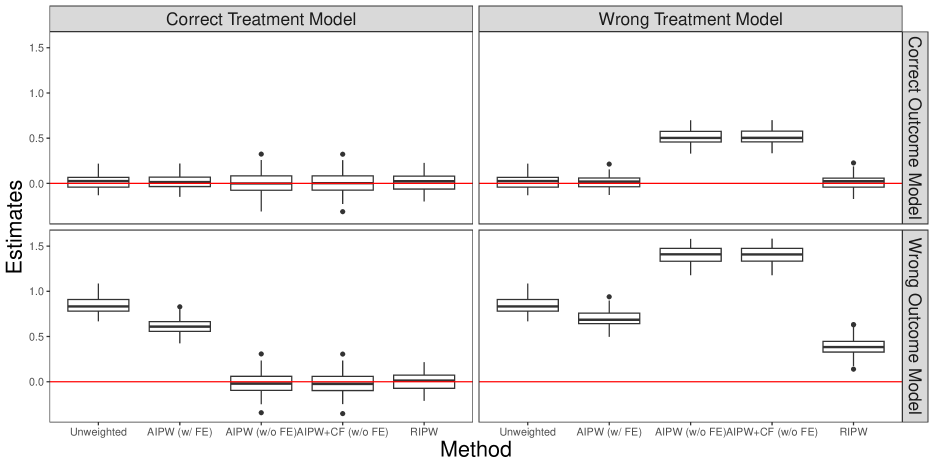

To highlight the central role of the reshaping function in eliminating the bias, we focus on inference with known assignment mechanisms. Put another way, in such settings, the bias of the unweighted or IPW estimators is purely driven by the wrong reshaping function rather than other sources of variability. We consider the DATE with for simplicity. We also design a simulation study with unknown assignment mechanisms and present the results in Appendix D, which involves all -by- settings with correct/incorrect assignment/outcome model and a detailed comparison between the RIPW estimator and several other competing estimators.

We consider a short panel with and sample size . We generate a single time-invariant covariate with and and a single time-invariant unobserved confounder with . Within each experiment, the covariates and unobserved confounders are only generated once and then fixed to ensure a fixed design. For treatment assignments, we consider a staggered adoption design, i.e., . We assume that is less likely to be treated when . In particular,

The potential outcome and the treatment effect are generated as follows:

where , , , , , and . For , we consider two settings: we either set thus making unit-invariant; or , in which case varies over units and periods. As with the covariates , the time fixed effects and factors are generated once for each setting and then fixed over runs. In contrast, will be resampled in every run as the stochastic errors. Note that both and are generated from rank-one factor models.

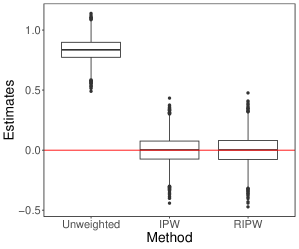

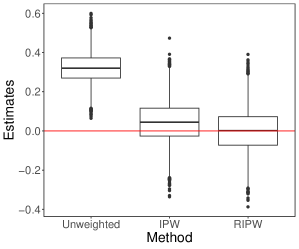

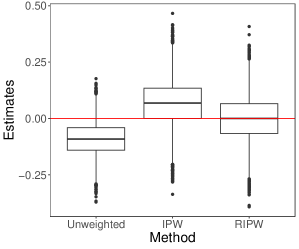

The parameters and measures two types of deviations from the TWFE model: measures the violation of parallel trend because we will not adjust for in the design-based inference, and measures the violation of constant treatment effects. We consider two settings: we either set — a model without parallel trends, but constant treatment effects; alternatively, we set — a TWFE model with heterogeneous effects, but parallel trends. In the first setting regardless of the model for , thus, we have different scenarios in total.

We consider three estimators: the unweighted TWFE estimator, the IPW estimator, and the RIPW estimator with given by (C.9). For each of the three experiments, we resample ’s and ’s, while keeping other quantities fixed, for times and collect the estimates and the confidence intervals. Figure 3 presents the boxplots of the bias . In all settings, the unweighted estimator is clearly biased, demonstrating that both the parallel trend and treatment effect homogeneity are indispensible for classical TWFE regression. In contrast, the IPW estimator is biased when the treatment effects are heterogeneous, but unbiased otherwise even if the parallel trend assumption is violated. This is by no means a coincidence; in this case, for all and, by Theorem 2.1, the asymptotic bias for RIPW estimators with any reshaped function including the IPW estimator. Finally, as implied by our theory, the RIPW estimator is unbiased in all settings. Moreover, the coverage of confidence intervals for the RIPW estimator is , and in these three settings, respectively, confirming the inferential validity stated in Theorem 2.3.

5.2 Analysis of OpenTable data in the early COVID-19 pandemic

On February 29th, 2020, Washington declared a state of emergency in response to the COVID-19 pandemic. A state of emergency is a situation in which a government is empowered to perform actions or impose policies that it would normally not be permitted to undertake.333Definition from Wikipedia: https://en.wikipedia.org/wiki/State_of_emergency. It alerts citizens to change their behaviors and urges government agencies to implement emergency plans. As the pandemic has swept across the country, more states declared the state of emergency in response to the COVID-19 outbreak.

The state of emergency restricts various human activities. It would be valuable for governments and policymakers to get a sense of the short-term effect of this urgent action. Since mid-February of 2020, OpenTable has been releasing daily data of year-over-year seated diners for a sample of restaurants on the OpenTable network through online reservations, phone reservations, and walk-ins.444Source: https://www.opentable.com/state-of-industry. This provides an opportunity to study how the state of emergency affects the restaurant industry in short-time. The data covers 36 states in the United States, which we will focus our analysis on.

Policy evaluation in the pandemic is extremely challenging due to the complex confounding and endogeneity issues (e.g., Chetty et al., 2020; Chinazzi et al., 2020; Goodman-Bacon and Marcus, 2020; Holtz et al., 2020; Kraemer et al., 2020; Abouk and Heydari, 2021). Fortunately, compared to the policies later in the pandemic, the state of emergency was less confounded since it was basically the first policy that affected the vast majority of the public. On the other hand, the restaurant industry is responding to the policy swiftly because the restaurants are forced to limit and change operations, thereby eliminating some confounders that cannot take effect in a few days.

Despite being more approachable, the problem remains challenging due to the effect heterogeneity and the difficulty of building a reliable model for the dine-in rates in a short time window. In contrast, the declaration time of the state of emergency is arguably less complex to model because it is mainly driven by the progress of the pandemic and the authority’s attitude towards the pandemic.

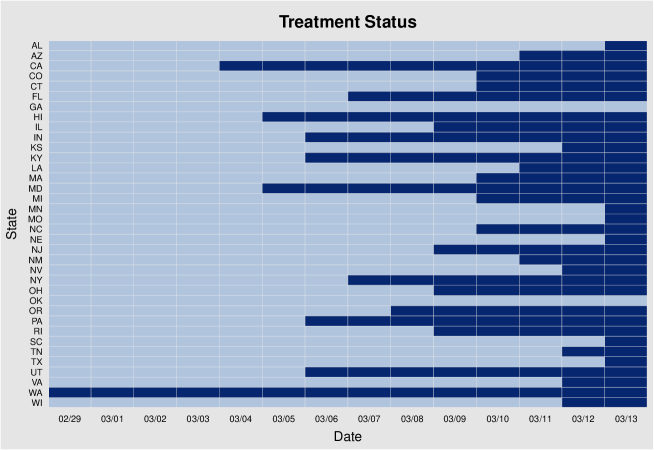

We demonstrate our RIPW estimator on this data. The outcome variable is the daily state-level year-over-year percentage change in seated diners provided by OpenTable.555Source: https://www.opentable.com/state-of-industry. The treatment variable is the indicator of whether the state of emergency has been declared.666Source: https://www.businessinsider.com/ california-washington-state-of-emergency-coronavirus-what-it-means-2020-3. We also include the state-level accumulated confirmed cases to measure the progress of the pandemic,777Source: https://coronavirus.jhu.edu/. the vote share of Democrats based on the 2016 presidential election data to measure the political attitude towards COVID-19,888Source: https://dataverse.harvard.edu/dataset.xhtml?persistentId=doi:10.7910/DVN/VOQCHQ. and the number of hospital beds per capita as a proxy for the amount of regular medical resources.999Source: https://github.com/rbracco/covidcompare. For demonstration purposes, we restrict the analysis to February 29th – March 13th, the first 14 days since the first declaration by Washington. As of March 13th, 34 out of 36 states have declared a state of emergency; thus, the declaration times are right-censored. The treatment paths are plotted in Figure 4.

For the treatment model, we fit a Cox proportional hazard model on the declaration date to derive an estimate of the generalized propensity scores. Specifically, letting be declaration time of state , a Cox proportional hazard model with time-varying covariates assumes that

where denotes the hazard function for state , and denotes a nonparametric baseline hazard function. The estimates and yield an estimate of the survival function for state , differencing which yields an estimate of the generalized propensity score

Here, we include as the time-varying covariates the logarithms of the accumulated confirmed cases and as the time-invariant covariates the logarithms of the number of hospital beds per-capita and the vote share. Note that fixed effects cannot be added into the Cox model because each state has only one outcome. To address unobserved heterogeneity, we include region fixed effects (Northeast, North Central, South, and West). While we will cross-fit the Cox model for the RIPW estimator, we fit the model on the entire data to illustrate the effect of covariates on the adoption time. Table 1 summarizes the exponentiated parameter estimates along with their standard errors with and without region fixed effects. It also reports the p-value of the joint significance test for the null hypothesis that all coefficients are zero. While most of the coefficients are not significant individually, they are jointly significant, suggesting that the generalized propensity score is non-constant.

| w/o Region FE | w/ Region FE | |

| 1.252 | 1.181 | |

| (0.257) | (0.245) | |

| vote share | 1.073∗∗ | 1.051 |

| (0.029) | (0.036) | |

| 0.850 | 1.213 | |

| (0.282) | (0.342) | |

| Logrank test p-value | 0.002∗∗∗ | 0.006∗∗∗ |

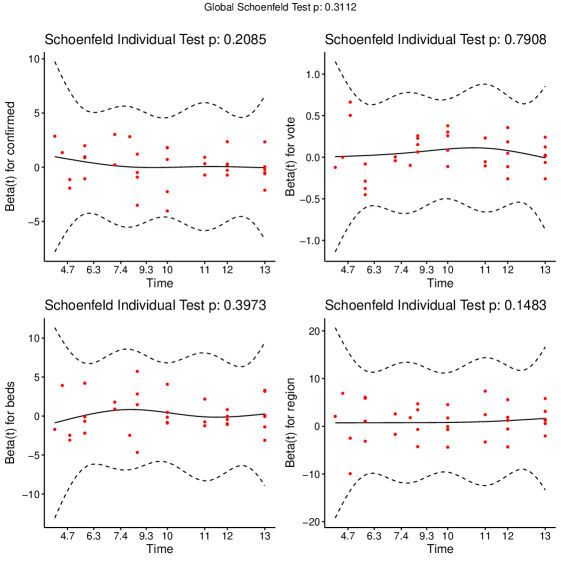

The proportional hazard assumption imposed by the Cox model is often controversial. Here, we apply the standard statistical tests based on Schoenfeld residuals (Schoenfeld, 1980) as a specification test for the Cox model. Figure 5 presents the p-values yielded by the Schoenfeld’s test. Clearly, none of them show evidence against the proportional hazard assumption. The p-value of the Schoenfeld’s test is , suggesting no evidence against the specification.

For the outcome model, we fit an interacted TWFE regression in the form of (3.7) with the same set of covariates. Since unit fixed effects are included, no time-invariant covariate can be added into the main effects due to perfect collinearity. Thus, we add log confirmed cases, treatment, and the interactions between treatment and all variables, including region fixed effects, into the TWFE regression. Table 2 summarizes the results. As with Table 1, it reports the p-value of the joint significance test for the null hypothesis that all coefficients other than the two-way fixed effects are zero. Again, the null hypothesis that for all is rejected in both settings.

| w/o Region FE treat | w/ Region FE treat | |

| treat | -0.641 | -0.619 |

| (1.640) | (1.640) | |

| -3.022∗∗ | -2.896∗∗ | |

| (1.230) | (1.232) | |

| 0.580 | 0.662 | |

| (2.466) | (2.491) | |

| -0.251∗∗ | -0.217 | |

| (0.115) | (0.134) | |

| -0.925 | -0.125 | |

| (1.288) | (1.440) | |

| F-test p-value | 0.002∗∗∗ | 0.001∗∗∗ |

Finally, we compute the RIPW estimator for equally-weighted DATE with the reshaped distribution (C.9) in Appendix C for staggered adoption and -fold cross-fitting that is discussed at length in Appendix B. Since this problem has a small sample size, the estimate exhibits large variation across different data splits. We thus apply the de-randomization procedure discussed in Appendix B.2 with splits. Our de-randomized cross-fitted RIPW estimate is (percentage points) with standard error (percentage points). It is significant at the level and the magnitude is larger than that given by the unweighted TWFE regressions shown in Table 2.

6 Conclusion

We demonstrate both theoretically and empirically that the unit-specific reweighting of the OLS objective function improves the robustness of the resulting treatment effects estimator in applications with panel data. The proposed weights are constructed using the assignment process (either known or estimated) and thus appropriate in situations with substantial cross-sectional variation in the treatment paths. Practically, our results allow applied researchers to exploit domain knowledge about outcomes and assignments, thus resulting in a more balanced approach to identification and estimation.

References

- Abadie [2005] Alberto Abadie. Semiparametric difference-in-differences estimators. The Review of Economic Studies, 72(1):1–19, 2005.

- Abadie et al. [2020] Alberto Abadie, Susan Athey, Guido W Imbens, and Jeffrey M Wooldridge. Sampling-based versus design-based uncertainty in regression analysis. Econometrica, 88(1):265–296, 2020.

- Abadie et al. [2023] Alberto Abadie, Susan Athey, Guido W Imbens, and Jeffrey M Wooldridge. When should you adjust standard errors for clustering? The Quarterly Journal of Economics, 138(1):1–35, 2023.

- Abouk and Heydari [2021] Rahi Abouk and Babak Heydari. The immediate effect of covid-19 policies on social-distancing behavior in the united states. Public health reports, 136(2):245–252, 2021.

- Abraham and Sun [2018] Sarah Abraham and Liyang Sun. Estimating dynamic treatment effects in event studies with heterogeneous treatment effects. arXiv preprint arXiv:1804.05785, 2018.

- Angrist and Krueger [1999] Joshua D Angrist and Alan B Krueger. Empirical strategies in labor economics. In Handbook of labor economics, volume 3, pages 1277–1366. Elsevier, 1999.

- Arellano [2003] Manuel Arellano. Panel data econometrics. Oxford university press, 2003.

- Arkhangelsky and Imbens [2019] Dmitry Arkhangelsky and Guido W Imbens. Double-robust identification for causal panel data models. arXiv preprint arXiv:1909.09412, 2019.

- Arkhangelsky et al. [2019] Dmitry Arkhangelsky, Susan Athey, David A Hirshberg, Guido W Imbens, and Stefan Wager. Synthetic difference in differences. Technical report, National Bureau of Economic Research, 2019.

- Ashenfelter and Card [1985] Orley Ashenfelter and David Card. Using the longitudinal structure of earnings to estimate the effect of training programs. The Review of Economics and Statistics, pages 648–660, 1985.

- Athey and Imbens [2018] Susan Athey and Guido W Imbens. Design-based analysis in difference-in-differences settings with staggered adoption. Technical report, National Bureau of Economic Research, 2018.

- Bang and Robins [2005] Heejung Bang and James M Robins. Doubly robust estimation in missing data and causal inference models. Biometrics, 61(4):962–973, 2005.

- Blackwell and Yamauchi [2021] Matthew Blackwell and Soichiro Yamauchi. Adjusting for unmeasured confounding in marginal structural models with propensity-score fixed effects. arXiv preprint arXiv:2105.03478, 2021.

- Bojinov et al. [2020a] Iavor Bojinov, Ashesh Rambachan, and Neil Shephard. Panel experiments and dynamic causal effects: A finite population perspective. arXiv preprint arXiv:2003.09915, 2020a.

- Bojinov et al. [2020b] Iavor Bojinov, David Simchi-Levi, and Jinglong Zhao. Design and analysis of switchback experiments. Available at SSRN 3684168, 2020b.

- Boneva et al. [2015] Lena Boneva, Oliver Linton, and Michael Vogt. A semiparametric model for heterogeneous panel data with fixed effects. Journal of Econometrics, 188(2):327–345, 2015.

- Borusyak and Hull [2022] Kirill Borusyak and Peter Hull. Non-random exposure to exogenous shocks. NBER Working Paper, (27845), 2022.

- Borusyak and Jaravel [2017] Kirill Borusyak and Xavier Jaravel. Revisiting event study designs. Available at SSRN 2826228, 2017.

- Callaway and Sant’Anna [2018] Brantly Callaway and Pedro HC Sant’Anna. Difference-in-differences with multiple time periods and an application on the minimum wage and employment. arXiv preprint arXiv:1803.09015, 2018.

- Carneiro et al. [2003] Pedro Carneiro, Karsten T Hansen, and James J Heckman. Estimating distributions of treatment effects with an application to the returns to schooling and measurement of the effects of uncertainty on college, 2003.

- Chamberlain [1984] Gary Chamberlain. Panel data. Handbook of econometrics, 2:1247–1318, 1984.

- Chernozhukov et al. [2017] Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, and Whitney Newey. Double/debiased/neyman machine learning of treatment effects. American Economic Review, 107(5):261–65, 2017.

- Chernozhukov et al. [2018] Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 21(1):C1–C68, 2018.

- Chernozhukov et al. [2020] Victor Chernozhukov, Whitney Newey, Rahul Singh, and Vasilis Syrgkanis. Adversarial estimation of riesz representers. arXiv preprint arXiv:2101.00009, 2020.

- Chetty et al. [2020] Raj Chetty, John N Friedman, Nathaniel Hendren, Michael Stepner, and The Opportunity Insights Team. How did COVID-19 and stabilization policies affect spending and employment? A new real-time economic tracker based on private sector data. National Bureau of Economic Research Cambridge, MA, 2020.

- Chinazzi et al. [2020] Matteo Chinazzi, Jessica T Davis, Marco Ajelli, Corrado Gioannini, Maria Litvinova, Stefano Merler, Ana Pastore y Piontti, Kunpeng Mu, Luca Rossi, Kaiyuan Sun, et al. The effect of travel restrictions on the spread of the 2019 novel coronavirus (covid-19) outbreak. Science, 368(6489):395–400, 2020.

- Currie et al. [2020] Janet Currie, Henrik Kleven, and Esmée Zwiers. Technology and big data are changing economics: Mining text to track methods. In AEA Papers and Proceedings, volume 110, pages 42–48, 2020.

- de Chaisemartin and d’Haultfoeuille [2019] Clément de Chaisemartin and Xavier d’Haultfoeuille. Two-way fixed effects estimators with heterogeneous treatment effects. Technical report, National Bureau of Economic Research, 2019.

- De Chaisemartin and d’Haultfoeuille [2020] Clement De Chaisemartin and Xavier d’Haultfoeuille. Two-way fixed effects estimators with heterogeneous treatment effects. American Economic Review, 110(9):2964–96, 2020.

- Goodman-Bacon [2018] Andrew Goodman-Bacon. Difference-in-differences with variation in treatment timing. Technical report, National Bureau of Economic Research, 2018.

- Goodman-Bacon and Marcus [2020] Andrew Goodman-Bacon and Jan Marcus. Using difference-in-differences to identify causal effects of covid-19 policies. 2020.

- Hahn and Newey [2004] Jinyong Hahn and Whitney Newey. Jackknife and analytical bias reduction for nonlinear panel models. Econometrica, 72(4):1295–1319, 2004.

- Hoeffding [1951] Wassily Hoeffding. A combinatorial central limit theorem. The Annals of Mathematical Statistics, pages 558–566, 1951.

- Holtz et al. [2020] David Holtz, Michael Zhao, Seth G Benzell, Cathy Y Cao, Mohammad Amin Rahimian, Jeremy Yang, Jennifer Allen, Avinash Collis, Alex Moehring, and Tara Sowrirajan. Interdependence and the cost of uncoordinated responses to covid-19. Proceedings of the National Academy of Sciences, 117(33):19837–19843, 2020.

- Imbens [2000] Guido Imbens. The role of the propensity score in estimating dose–response functions. Biometrika, 87(0):706–710, 2000.

- Kang and Schafer [2007] Joseph Kang and Joseph Schafer. Demystifying double robustness: A comparison of alternative strategies for estimating a population mean from incomplete data. Statistical science, 22(4):523–539, 2007.

- Kraemer et al. [2020] Moritz UG Kraemer, Chia-Hung Yang, Bernardo Gutierrez, Chieh-Hsi Wu, Brennan Klein, David M Pigott, Louis Du Plessis, Nuno R Faria, Ruoran Li, and William P Hanage. The effect of human mobility and control measures on the covid-19 epidemic in china. Science, 368(6490):493–497, 2020.

- Lancaster [2000] Tony Lancaster. The incidental parameter problem since 1948. Journal of econometrics, 95(2):391–413, 2000.

- Li and Ding [2017] Xinran Li and Peng Ding. General forms of finite population central limit theorems with applications to causal inference. Journal of the American Statistical Association, 112(520):1759–1769, 2017.

- Lin [2013] Winston Lin. Agnostic notes on regression adjustments to experimental data: Reexamining freedman’s critique. 2013.

- Neyman [1923/1990] J. Neyman. On the application of probability theory to agricultural experiments. Essay on principles. Section 9. Translated by Dabrowska, D. M. and Speed, T. P. Statistical Science, 5:465–472, 1923/1990.

- Neyman and Scott [1948] Jerzy Neyman and Elizabeth L Scott. Consistent estimates based on partially consistent observations. Econometrica: Journal of the Econometric Society, pages 1–32, 1948.

- Ohlsson [1989] Esbjörn Ohlsson. Asymptotic normality for two-stage sampling from a finite population. Probability theory and related fields, 81(3):341–352, 1989.

- Pashley and Miratrix [2021] Nicole E Pashley and Luke W Miratrix. Insights on variance estimation for blocked and matched pairs designs. Journal of Educational and Behavioral Statistics, 46(3):271–296, 2021.

- Petrov [1975] VV Petrov. Sums of independent random variables. Yu. V. Prokhorov. V. StatuleviCius (Eds.), 1975.

- Rambachan and Roth [2020] Ashesh Rambachan and Jonathan Roth. Design-based uncertainty for quasi-experiments. arXiv preprint arXiv:2008.00602, 2020.

- Rényi [1959] Alfréd Rényi. On measures of dependence. Acta Mathematica Academiae Scientiarum Hungarica, 10(3-4):441–451, 1959.

- Robins et al. [1994] James M Robins, Andrea Rotnitzky, and Lue Ping Zhao. Estimation of regression coefficients when some regressors are not always observed. Journal of the American statistical Association, 89(427):846–866, 1994.

- Rosenbaum and Rubin [1983] Paul R Rosenbaum and Donald B Rubin. The central role of the propensity score in observational studies for causal effects. Biometrika, 70(1):41–55, 1983.

- Roth and Sant’Anna [2021] Jonathan Roth and Pedro HC Sant’Anna. Efficient estimation for staggered rollout designs. arXiv preprint arXiv:2102.01291, 2021.

- Rubin [1974] Donald B Rubin. Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of educational Psychology, 66(5):688, 1974.

- Sant’Anna and Zhao [2020] Pedro HC Sant’Anna and Jun Zhao. Doubly robust difference-in-differences estimators. Journal of Econometrics, 2020.

- Schoenfeld [1980] David Schoenfeld. Chi-squared goodness-of-fit tests for the proportional hazards regression model. Biometrika, 67(1):145–153, 1980.

- Shaikh and Toulis [2019] Azeem Shaikh and Panagiotis Toulis. Randomization tests in observational studies with staggered adoption of treatment. University of Chicago, Becker Friedman Institute for Economics Working Paper, (2019-144), 2019.

- von Bahr and Esseen [1965] Bengt von Bahr and Carl-Gustav Esseen. Inequalities for the -th absolute moment of a sum of random variables, . The Annals of Mathematical Statistics, 36:299–303, 1965.

- Wooldridge [2010] Jeffrey M Wooldridge. Econometric analysis of cross section and panel data. MIT press, 2010.

- Wooldridge [2021] Jeffrey M Wooldridge. Two-way fixed effects, the two-way mundlak regression, and difference-in-differences estimators. Available at SSRN 3906345, 2021.

Appendix A Statistical Properties of RIPW Estimators

A.1 Setup and preliminaries

We will consider the more general setting in Section 3 since it nests the setting in Section 2. For ease of reference, we state the framework here, along with the list of assumptions some of which are weaker than those stated in the main text.

Suppose the -th unit is characterized by potential outcomes , the treatment path , and a set of covariates . The vector of time-varying treatment effects for unit is denoted by . We treat covariates as fixed and consider as a random vector (jointly) drawn from a distribution (conditional on ). We let denote the joint distribution of the entire random vector (conditional on ) and denote the expectation over this distribution.

The assignment model is characterized by the generalized propensity score defined as

The outcome model is characterized by where ,

Let be an estimate of . Further let and , where

The results in Section 2 are given by the special case where .

Define the modified potential outcomes as

and the modified treatment effects as

| (A.1) |

By definition,

| (A.2) |

Then the modified observed outcome is where

With a reshaped distribution on , the RIPW estimator is defined as

We will suppress from and from throughout the section.

Since remains invariant if we replace by , we assume that

| (A.3) |

by setting , and

.

The accuracy of the assignment model and the outcome model for unit are defined as

In the proofs, we need the conditional version of these measures

We then define the unconditional and conditional average accuracy measures

and

By law of iterated expectations,

By Markov inequality,

| (A.4) |

Therefore, if we can prove the result only assuming conditional on , we can prove it assuming that as in Section 3.

To be self-contained, we list all quantities involved in the DATE equationand the asymptotically linear expansion of the RIPW estimator. Let ,

and

This coincides with the definition in Theorem 2.2 when and .

Finally, we state the core assumptions, some of which are repeated and combined for ease of reference and the rest of which are weakened. We start by restating the unit-specific mean ignorability assumption.

Assumption A.1.

For each ,

| (A.5) |

Next, we combine the overlap condition for the true propensity scores (Assumption 2.2) and that for the estimated propensity scores (Assumption 3.2) with the constant replaced by to be more informative in the proofs.

Assumption A.2.

There exists a universal constant and a non-stochastic subset with at least two elements and at least one element not in , such that

| (A.6) |

Assumption A.3.

There exists ,

and

We close this section by a basic property of the maximal correlation.

Lemma A.1.

Let and be any deterministic function on the domain of . Then

Proof.

By definition of ,

Thus,

∎

A.2 A non-stochastic formula of RIPW estimators

Theorem A.1.

With the same notation as Theorem 2.2, , where

| (A.7) |

Proof.

Let be any vector with . First we derive the optimum given any values of and . Recall that

Since the weight only depends on , it is easy to see that

As a result,

This yields a profile loss function for and :

where the last equality uses the fact that . Given , the optimizer is simply the weighted average of in absence of the constraint , i.e.

Noting that since , is also the minimizer of the constrained problem, i.e.

Plugging in yields a profile loss function for

A direct calculation shows that

Since is a convex quadratic function of , the first-order condition is sufficient and necessary to determine the optimality. The proof is then completed by solving . ∎

A.3 Statistical properties of RIPW estimators with deterministic

A.3.1 Asymptotic linear expansion of RIPW estimators

As a warm-up, we assume that are deterministic. This, for example, includes the pure design-based inference where and . In this case, the measures of accuracy can be simplified as

| (A.8) |

As a result, are deterministic.

We start by a lemma showing that concentrate around their means. For notational convenience, we let denote for a random vector .

Proof.

By Assumption A.2, almost surely. Moreover, since . Thus,

Next, we derive bounds for and separately. For ,

where the last step follows from the Assumption A.3. For ,

where the last step follows from the Assumption A.3. Putting the pieces together, the bound on the sum of expectations is proved.

Next, we turn to the bound on the variances. By Lemma A.1,

The Assumption A.2 implies that

Therefore, . For ,

where the last equality uses the fact that . For ,

where (i) follows from the Cauchy-Schwarz inequality and that , (ii) is obtained from the fact that and , and (iii) follows from the Assumption A.3.

For , recall that is the sum of the variance of each coordinate of . By Lemma A.1,

For , analogues to inequalities (i) - (iii) for , we obtain that

where the last step follows from the Assumption A.3.

Finally, by Markov’s inequality,

∎

The following lemma shows that the denominator of is bounded away from .

Lemma A.3.

Proof.

By definition,

Let be two distinct elements from with and

| (A.9) |

This is enabled by Assumption A.2. Note that iff for some , which is impossible since and all entries of and are binary. In addition, since has support , . Let

Then

where the second inequality follows from the fact that . By (A.9),

Furthermore, by Lemma A.1,

Putting pieces together, we obtain that

On the other hand, by Lemma A.1, for ,

By Markov’s inequality, for ,

Therefore,

∎

Proof.

Next, we prove the second statement on . By Lemma A.3, . It is left to show that