Performance of a Markovian neural network versus dynamic programming on a fishing control problem

Abstract

Fishing quotas are unpleasant but efficient to control the productivity of a fishing site. A popular model has a stochastic differential equation for the biomass on which a stochastic dynamic programming or a Hamilton-Jacobi-Bellman algorithm can be used to find the stochastic control – the fishing quota. We compare the solutions obtained by dynamic programming against those obtained with a neural network which preserves the Markov property of the solution. The method is extended to a similar multi species model to check its robustness in high dimension.

keywords:

Stochastic optimal control, partial differential equations, neural networks.1 Introduction

Too much fishing can deplete the biomass to a disastrous level and leave fishermen out of work, or even, in some part of the world, starving. There are several ways to control fishing. One is to forbid fishing in regions and to alternate fishing and non-fishing zones moussaoui . Another is by imposing quotas. In augerOP statistical learning was shown to be very efficient to calibrate the parameters of the fishing model of MP18 . In pagespironneau a stochastic control problem was derived from the model used in MP18 and to speed up the computation of optimal quotas, a solution by statistical learning was proposed and compared to standard stochastic control solutions like the Hamilton-Jacobi-Bellman equations (HJB). However the solution provided by the neural network was not Markovian as it used the future states, given by the stochastic model, to optimise the present. In this article we propose to study the performance of a Markovian neural network, in the spirit of GobetMunos05 ; HanE16 ; CarmonaLauriere19b .

The unpopularity of severe quotas is modeled by a penalty in the cost of an optimisation problem to compute the best fishing strategy which preserves the fish biomass, i.e., keeps it close to an ideal state . Quotas on fishing should also be as stable in time as possible because fishermen need to know that the quota will not move too much from one day to the next. This is modeled by another penalty on the time variations of the quota.

Let be the fish biomass at time , the fishing effort, interpreted as the number of boats at sea. In MP18 , , with the catchability constant , is the maximum weight of fish that a boat can mechanically catch, meaning that the more fish there is the more fishermen will catch them, but proportionally to the capacity of his equipment.

Ideally a fisherman may want to catch a quantity on day . Imposing a quota means .

2 The fishing site model

Consider a fishing site with types of fish in interaction, in the sense that some depend on others for food. Let be the fish biomasses at time , the fishing effort – interpreted as the number of boats at sea – and the capacity to catch type is , with the catchability constant over types for simplicity.

An optimal strategy with quotas for each species is given to each fisherman, to impose the maximum weight of fish, , of that species caught on a day . Hence the total amount of fish of type caught on a day is .

The logistic equation for says that the biomasses is a consequence of the natural growth or decay rate , the long time limit of , where is the species interaction matrix, and the depletion due to fishing:

| (1) |

The operator transforms a vector into a diagonal matrix. For example, with and , then, in (1),

which means that the first species lives on its own but profit from the second species because it eats it as shown by the equation for the second species which has a death rate augmented by .

Let . The fishing effort is driven by the profit minus the operating cost of a boat , where is the price of fish of species :

| (2) |

The price is driven by the difference between the demand and the resource :

| (3) |

where is the inverse time scale at which the fish market price adjusts. When , (3) may be approximated by:

where the trace operator is defined by . Let us denote , , , and . Then the whole system (1)–(2) rewrites:

| (4) |

where is matrix-vector product . Since we are not going to use the original variables in the sequel, we drop the tildas and write and instead of and .

Finally we use another change of variables to get rid of the variable: we replace by , by and by . Then the above system (4) is identical but now with . In the end, with , the whole system for the evolution of the fish biomass and the fishing effort is:

| (5) |

2.1 The Stochastic vector control problem

To prevent fish extinction, a constraint is set on the total catch per species. The value of is found by solving an optimisation problem described below. It is expected that otherwise the policy of quota is irrelevant in the sense that the fisherman is given a maximum allowed catch which is greater than what he could mechanically catch.

Let us add a constraint so that . Denote the optimal fishing policy for species per unit mass. We formulate the optimal control problem in terms of rather than . Then no longer appears and the problem becomes:

| (6) |

where the control is in the constraint space

which reflects a desire to ensure a minimal fishing and a maximum one so as to guarantee that at all time.

2.2 More constraints on quotas

To avoid small fishing quotas we use penalty and add to the criteria . Moreover, to avoid too many daily changes we penalise the quadratic variation of over the time period , i.e., to we add , where the quadratic variation is defined as:

where ranges over partitions of the interval and the limit is in probability when . Here Itô calculus BIC tells us that:

Hence, an optimal policy in the presence of noise is a solution of

| (8) | |||||

For the sake of clarity we assume for all .

Remark 1

Let . A multiplication of the SDE (8) by leads to

Thus, if all the terms on the diagonal of are equal and if the initials conditions are equal, then the components of are independent and equal because and commute. It happens only if .

2.3 Existence of solution

First, the solution of the SDE exists and is positive. For clarity the proof is done for :

Note that is locally Lipschitz, uniformly in since . Hence for every realization there is a unique strong solution until a blow-up time which is a stopping time for the filtration .

On by Itô calculus,

so:

Hence is impossible unless , a.s. Therefore

Let and . From lebris , if , then has a PDF and the following equivalent control problem has a solution:

where .

Remark 2

This result also gives a computational method, by discretizing the above and solving it as an optimisation problem. Of the four methods discussed in this article, this is the most expensive. It was tested in MLOP and shown not to be superior in precision to other methods.

3 Time discretization

We consider a uniform grid with points in time. Let , and, for any defined on , an approximation of . Define the Euler scheme:

| (9) |

where , . Note that positivity may not be preserved by this scheme, but in practice negative values do not seem to appear.

A Monte-Carlo method is used with sample solutions of (9) to compute the cost:

with the convention that .

Remark 3

Let and be two given differentiable functions. Let . The following holds (reading hint: is at , not times ):

where the derivative is evaluated at or at . Hence:

so:

| (10) |

Even though the first term in (10) is dominated by the second term, we may keep it for numerical convenience.

4 Stochastic Dynamic Programming (SDP)

Consider the value function

| (12) | |||||

Let be the next iterate of a numerical scheme for the SDE starting at . For instance:

Bellman’s dynamic programming principle tells us that the optimal control of the problem is the minimiser, , in:

| (13) | |||

| (14) | |||

| (15) | |||

| (16) |

Evidently,

For every component, to compute , we use a quadrature formula with points and weights based on optimal quantization of the normal distribution (see PaPr2003 or (Pagesbook2018, , Chapter 5) and the website www.quantize.maths-fi.com for download of grids) so that

| (17) |

Finally at every time step and every (with ), the result is minimised with respect to by a dichotomic search. In this fashion is obtained on a grid and a piecewise linear interpolation is constructed to prepare for the next time step .

4.1 Numerical results for a single species

For the numerical tests we have chosen: ,

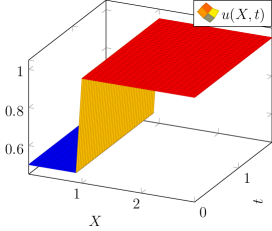

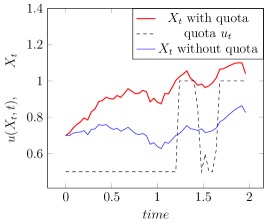

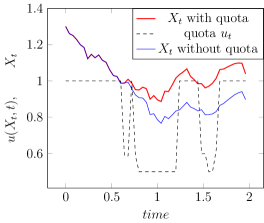

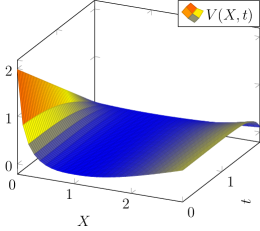

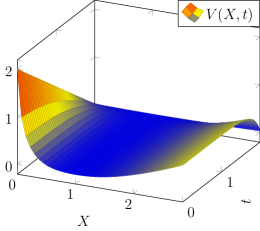

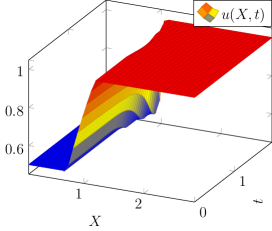

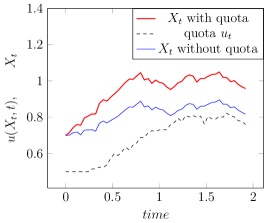

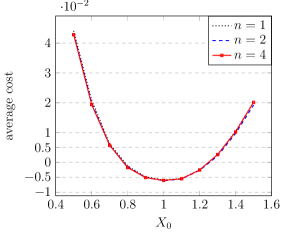

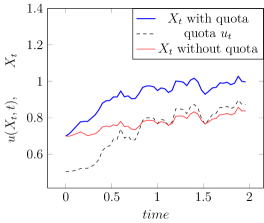

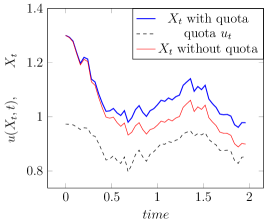

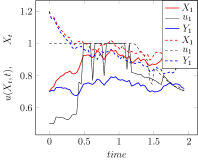

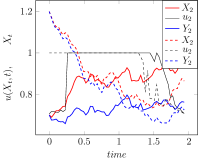

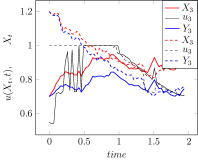

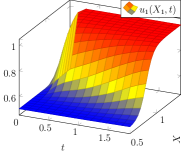

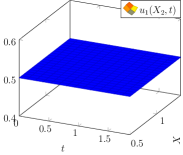

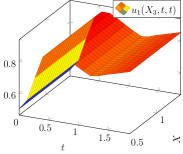

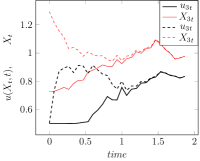

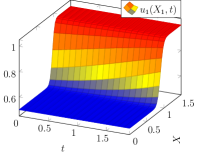

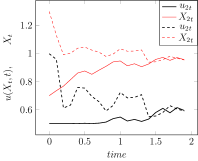

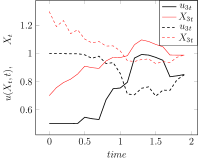

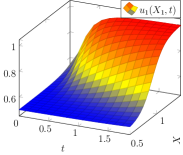

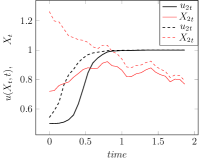

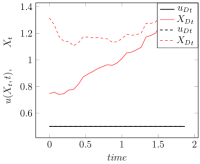

and . Figures 2 and 6 show the control surface and the value function . Although the control seems to be either 0.5 or 1 everywhere, there is a small interval near in which it is not bang-bang. It is an important region, as seen on the sample solutions which are shown on Figure 4 and 4 where it is clear that the control is not always 0.5 or 1. For these an initial condition is chosen, a noise is generated and the SDE are integrated by the Euler scheme with the approximately optimal control obtained by the SDP method described above. Then, by definition of the cost function, should tend to be equal to as much as possible without too many jumps for . The trajectory is compared with one on which , i.e., no quota.

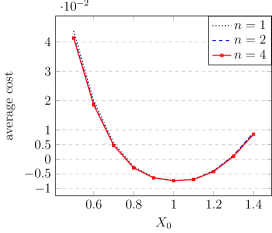

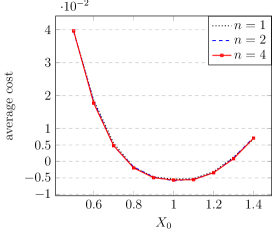

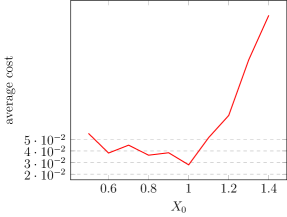

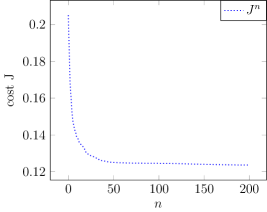

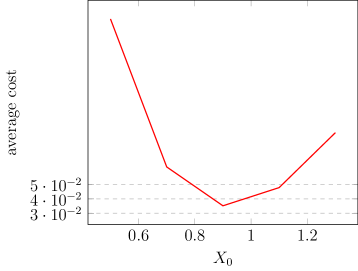

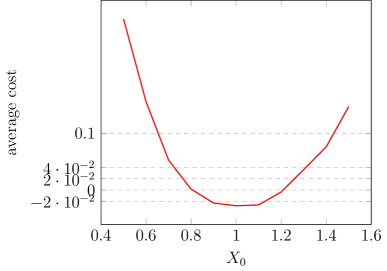

Finally on Figure 2 the cost function of the control problem is plotted for 100 samples and various values of . Away from , it increases, which makes sense because means that we start with the optimal value in terms of fish biomass.

5 Hamilton-Jacobi-Bellman solutions (HJB)

Let us return to (13) and note that:

| (19) | |||||

with . According to Remark 3

| (20) | |||

| (21) |

Also, by Itô formula,

| (22) | |||

| (23) |

Consequently, with replaced by for numerical convenience, (13) becomes

| (24) | |||

| (25) |

The last line is an approximation motivated by the search for a stable implicit numerical scheme for :

| (26) | |||

| (27) |

Furthermore, is given by minimising the right hand side of (26):

| (28) |

capped by the bounds and . Boundary conditions are not needed at because the PDE is self starting but for large , cancelation of the quadratic terms requires .

5.1 Numerical results for a single species by HJB

The finite element method of degree 1 on intervals was used to approximate spatially (26). The linear systems were solved using the FreeFem++ software freefem . The range of was approximated by the segment discretized into intervals; time steps were used.

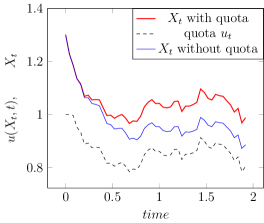

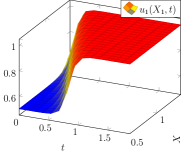

With the same parameters as in Section 4.1 the results are shown on Figures 8, 6, 10, 10 and 8. These should be compared, respectively, with Figures 2, 6, 4, 4 and 2.

Except for the singularity at final time, which is not handled in the same way, the results are similar. HJB seems to handle better the penalty term with as is not bang-bang.

6 Optimisation with Markovian feedback neural network controls

In this section, we look for Markovian feedback controls, i.e., functions , adapted to , satisfying for every . We restrict our attention to such functions which are encoded by neural networks. This strategy has been used previously in the optimal control literature, see e.g. GobetMunos05 ,HanE16 ,CarmonaLauriere19b ,PHA .

Given an activation function (e.g. a sigmoid or ReLU), let us introduce some helpful notation:

| (29) |

is the set of layer functions with input dimension and output dimension .

Let ; define the set of feedforward fully connected neural networks with hidden layers and one output layer,

| (30) |

where denotes the composition of functions. Denote by the set of parameters:

For each , the corresponding network function will be denoted by . Hence (30) may be rewritten as:

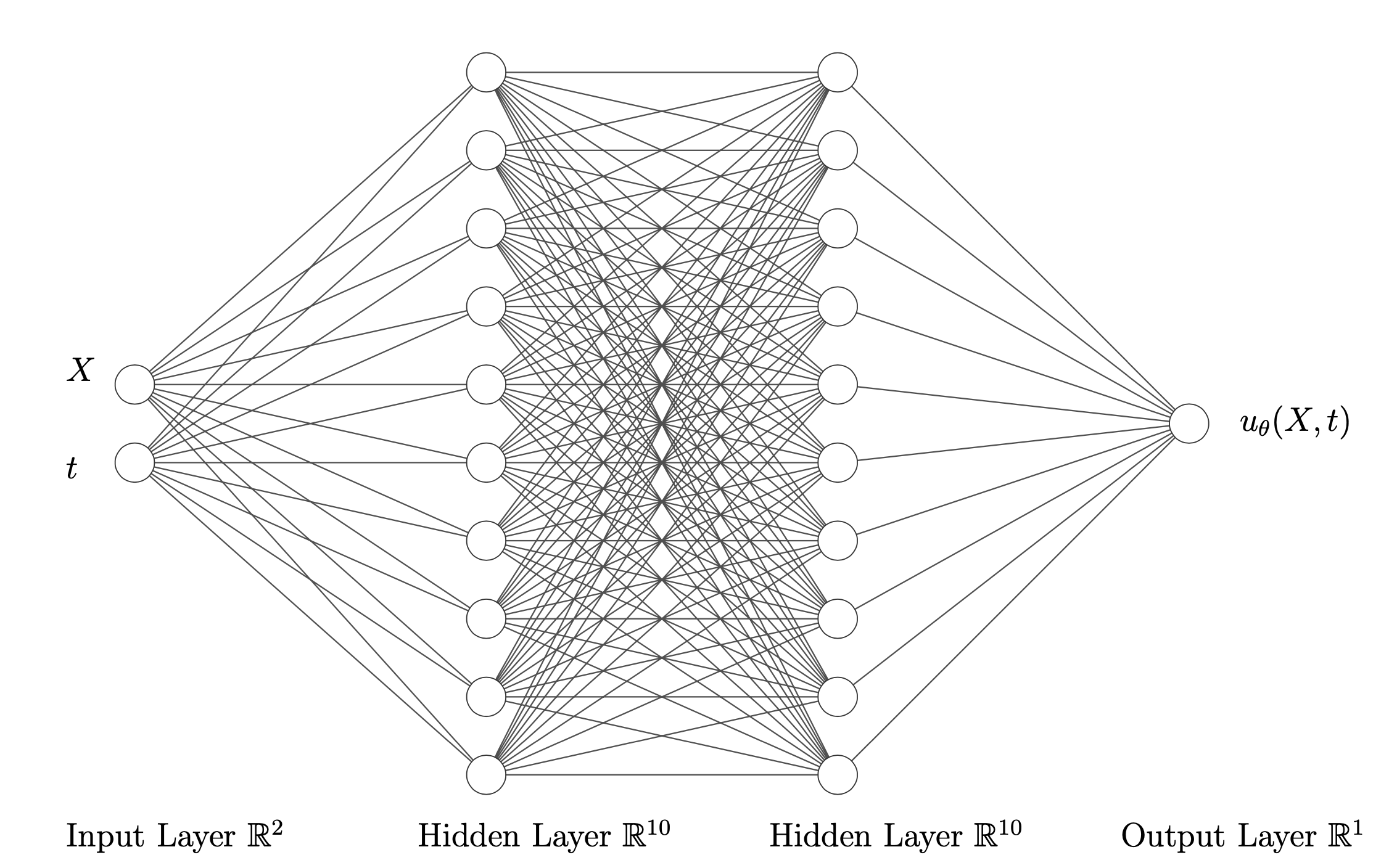

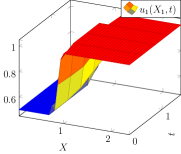

For the fishing control problem ( species for the space variable, plus the time variable) and (the dimension of the control variable ). Furthermore, to ensure the constraint , it is sufficient to take the last activation function which satisfies this constraint. In the present implementation we have used where is the sigmoid function. Figure 11 shows a fully connected 2 layers neural network with 2 inputs, one output and 10 neurons in each layer.

The control problem is approximated by the minimisation over of:

| (31) |

where is the result of one step of the Euler scheme (9) with and a realization of the noise.

Noting that (31) is a sum of terms, we can run a Stochastic Gradient Descent or one of its variants like ADAM. At each iteration, we sample a mini-batch of initial positions and realizations of the noise which allow us to compute random realizations of trajectories and compute a partial sum of (31). It is then used to compute a gradient and back-propagate it to adjust .

The stochastic gradient algorithm ADAM is used to update towards a local minimum of needs the gradient of . A mini-batch is a random subset ; the gradients with respect to are computed as follows. Let where

The gradient of with respect to is made of:

| (32) |

where is defined by and

| (33) |

Softwares for neural networks such as tensorflow provide automatic differentiation tools (back propagation) to compute .

Recall that ADAM algorithm consists in choosing randomly and then

-

1.

Let , , , .

Loop on i:

-

2.

Set

-

3.

Set

-

4.

Set

-

5.

Set , ,

-

6.

Update , , the number of parameters.

6.1 Numerical results using a neural network for a single species

Notice that we use the tools of AI but there is no learning phase from known solutions, rather the learning phase is simply to find the best parameters to achieve the minimum of a given cost function.

To check the results we implemented also a single layer neural network with 15000 neurons directly in C++ using the automatic differentiation in reverse mode of the library adept adept and a conjugate gradient algorithm instead of ADAM. Convergence is fast (20 to 40 iterations) but this simple method does not work for multiple layered neural network because of memory limitation.

For the single species numerical test, the results are the same whether obtained by the one layer or the two layers networks.

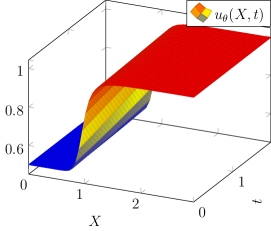

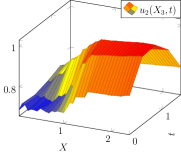

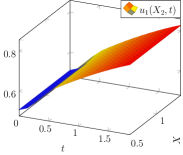

Results are shown on Figures 13, 15, 15 and 13 and should be compared, respectively, with Figures 8, 10, 10 and 8 and/or, respectively, with Figures 2, 4, 4 and 2.

Note that the results are closer to those obtained with HJB than those obtained with SDP.

Our general impression is that all 3 methods are equal, with a slight reserve for SDP for which the control oscillates much more than with the other two methods, implying that it does not handle as well the -penalisation term.

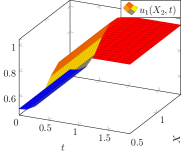

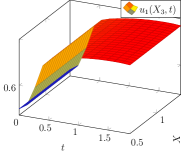

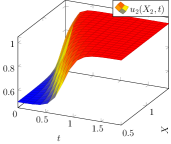

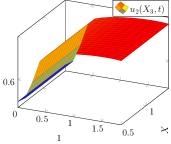

7 Numerical results: 3 species

We now turn our attention to an example with 3 species. Consider the following interaction matrix between species:

All other parameters are as in Section 4.1 and .

With SDP (Stochastic Dynamic Programming) there is a difficulty: the minimisation in (17) is now 3 dimensional and cannot be obtained by dichotomy. So the method was not tested. We have compared HJB and Neural Network optimisation with 1 and then with 2 layers. The results differ; according to the last subsection none of the methods found the true solution.

7.1 Numerical results for 3 species with HJB

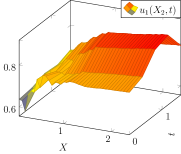

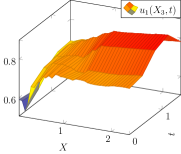

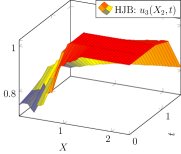

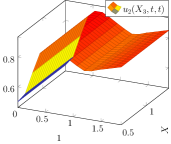

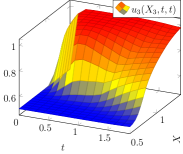

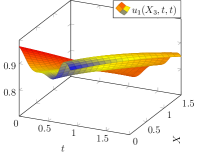

The computation is done with time steps. Here too a finite element discretisation was used with elements on tetraedra. The mesh for the cube is obtained from an automatic mesh generator from a surface mesh resulting into 29791 vertices and 16200 tetraedra. It took 7 min on an M1 Apple laptop. The vector valued optimal control computed with HJB is shown on Figures 18 to 24. In these, two of the 3 coordinates of , are fixed at their values.

Then the fishing model is integrated with the optimal and a random realization of for 2 values of : or . The results are compared with a similar simulation without quota, i.e., . See Figures 27, 27, 27. The quality of the optimisation is seen visually when is closest to and numerically from the lowest value of the cost function, plotted versus on Figure 29.

7.2 Optimisation with a Neural Network with one layer of 15000 Neurons

The parameters are the same. The neural network has one layer with 15000 neurons. Conjugate gradient with optimal step size is used and the derivatives are computed with automatic differentiation in reverse mode.

Convergence of the conjugate gradient algorithm is seen on Figure 29. The norm of the gradient is reduced from 0.1 to 0.00017.

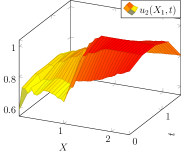

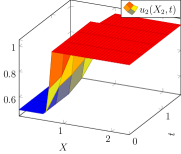

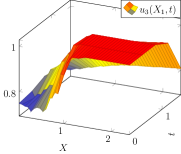

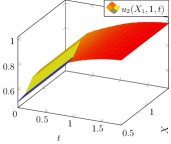

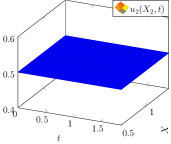

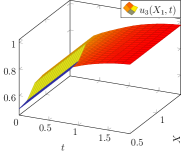

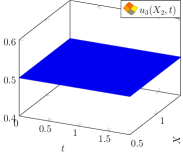

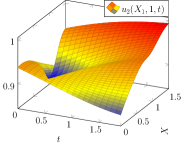

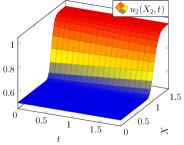

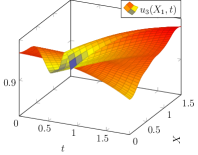

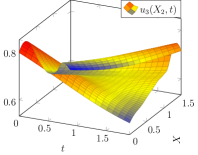

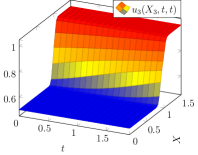

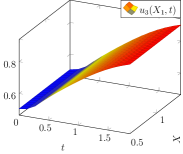

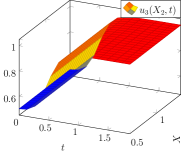

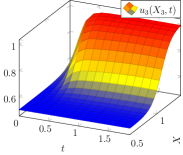

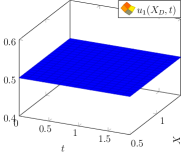

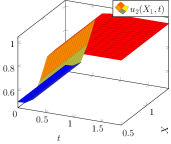

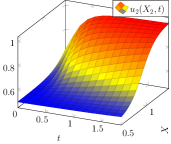

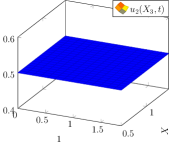

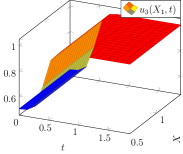

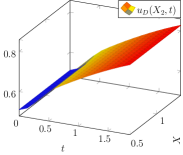

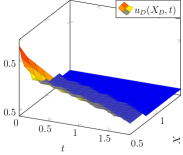

Then the results are displayed as above: first the optimal quota vector function, with 9 surfaces on Figures 32 to 38. The fact that the surface is flat is an obvious indication that the solution found by the NN with one layer is only suboptimal.

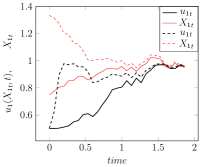

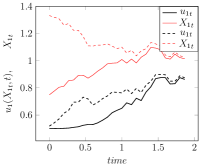

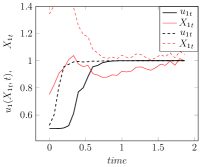

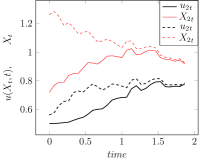

Then two types of random trajectories, one starting at , the other at . Results are shown on Figures 41, 41 and 41. The section ends with a display of the cost function versus on Figure 42. The results seem less accurate than with HJB. Figure 35 is surprising! It shows also on Figure 41 where the optimal quota does not steer anywhere near .

7.3 With two layers

The same problem is solved with a two layers neural network with 100 neurons on each layer.

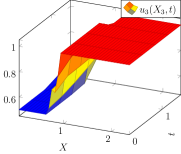

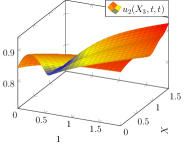

The results are displayed as above: first the optimal quota vector function, with 9 surfaces on Figures 45 to 51.

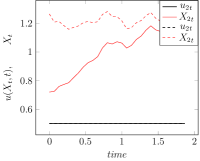

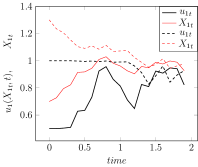

Then two types of random trajectories, one starting at , the other at . Results are shown on Figures 54, 54 and 54. The section ends with a display of the cost function versus on Figure 55.

Consequently, the neural network with 2 layers give decent results, better than HJB. The neural network with one layer only gives poor results.

7.4 Assessment of the results

Remark 1 allows the construction of a simple 3D solution from a 1D solution.

Let be solution of

Let , , , , , and . Then

Let . It implies

The matrix is diagonal and all terms are equal, so it commutes with . Therefore

and is solution of

because this is 3 times the cost function of the problem in .

Let be the solution of this problem, then by construction and

For instance, .

Now we build on the fact that is approximatively bang-bang and equal to 0.5 when and 1 otherwise.

Example

The scaling plays no role.

Hence is expected to be bang-bang at , is expected to be bang bang at , and is expected to be bang bang at .

Hence is expected to be bang bang at , and is expected to be bang-bang at and is expected equal to be bang bang at .

Hence and , are expected equal to everywhere and is expected to be bang-bang at .

7.5 Optimisation with HJB when

The same numerical test was done with HJB but with . The results are shown on Figures 58 to 67. The lowest cost is , for .

The solution is nearer to the one constructed above but still fairly different. The Neural Networks performances are poor on this test. It is likely that they produced a local minimum.

8 Numerical results: 5 species

The great advantage of Neural Network optimisation is that it scales well with dimensions. So to show that it is possible, with the same computer code with very few modifications we computed with the one-layer NN with 150000 neurons a case with 5 species. 20 iterations of conjugate gradients were done.

All parameters are as above except the species correlation matrix:

Only components 1,2,5 are shown see Figures 70 to 76. On Figures 79, 79 and 79 trajectories with optimal quotas show that the NN solution is in general driving towards .

The minimum of the cost function is 0.038 for .

9 Conclusion

Control of the biomass of a fishing site has been here a mathematical opportunity to test the numerical methods at hand. One of the advantage of the model is that it is meaningful in any dimension, the number of species. Thus it is a testbed for stochastic control numerical methods.

We have compared Hamilton-Jacobi-Bellman solutions and stochastic dynamic programming with two implementation of a neural network based optimisation.

The later is conceptually very simple and the computer libraries of AI and Automatic Differentiation can be used. But they need to be validated and it is the object of this article.

Stochastic dynamic programming is difficult to use numerically beyond dimension 2 and HJB solutions do not scale beyond dimension 4, unless sophisticated discretisation tools are used like sparse grids.

Neural network based optimisation can be used for large dimension problems but assessing the precision of the answer seems difficult. Here in dimension 3 the one layer network did not work well and with the two layers network we could observe discrepancies with HJB solutions. In dimension 5, the numerical solution seems reasonable but it is probably suboptimal.

References

- (1) P.M. Allen and J.M. McGlade: Modelling complex human systems: A fisheries example. European Journal of Operational Research 30 (1987) 147-167.

- (2) P. Auger and O. Pironneau, Parameter Identification by Statistical Learning of a Stochastic Dynamical System Modelling a Fishery with Price Variation. Comptes-Rendus de l’Académie des Sciences. May 2020.

- (3) A. Bachouch, C.Huré, N. Langrené and Huyên Pham; Deep neural networks algorithms for stochastic control problems on finite horizon: numerical applications; arXiv:1812.05916v3 [math.OC] 27 Jan 2020.

- (4) S. Balakrishnan and V. Biega. Adaptive-critic-based neural networks for aircraft optimal control. Journal of Guidance, Control and Dynamics, 19(4), 893–898. 1996.

- (5) R. Bellman, Dynamic Programming, Princeton, NJ: Princeton University Press, 1957.

- (6) D. Bertsekas, Reinforced Learning and Optimal Control. Athena Scientific, Belmont Mass. 2019.

- (7) A. Bick. Quadratic-Variation-Based dynamic strategies. Management Sciences, vol 41, No 4, p722-732 (1995).

- (8) S. Boyd and C. Barratt: Linear Controller Design – Limits of Performance. Prentice-Hall, 1991.

- (9) T. Brochier, P. Auger, D. Thiao, A. Bah, S. Ly, T. Nguyen Huu, P. Brehmer. Can overexploited fisheries recover by self-organization? Reallocation of the fishing effort as an emergent form of governance. Marine Policy, 95 (2018) 46-56.

- (10) R. Carmona and M. Laurière: Convergence Analysis of Machine Learning Algorithms for the Numerical Solution of Mean Field Control and Games: II–The Finite Horizon Case. arXiv preprint arXiv:1908.01613, 2019. To Appear in Annals of Applied Probability.

- (11) F. Chollet : Deep learning with Python. Manning publications (2017).

- (12) E Gobet and R Munos. Sensitivity Analysis Using Itô–Malliavin Calculus and Martingales, and Application to Stochastic Optimal Control. SIAM Journal on control and optimisation, 2005

- (13) I. Goodfellow, Y. Bengio and A. Courville (2016): Deep Learning, MIT-Bradford.

- (14) J. Han and W. E. Deep learning approximation for stochastic control problems. Deep Reinforcement Learning Workshop, NIPS (2016)

- (15) F. Hecht (2012): New development in FreeFem++, J. Numer. Math., 20, pp. 251-265. (see also www.freefem.org.)

- (16) R. G. Hogan : Fast reverse-mode automatic differentiation using expression templates in C++. ACM Trans. Math. Softw., 40, 26:1-26:16 (2014) : www.met.reading.ac.uk/clouds/adept/

- (17) R. Kamalapurkar and P. Walters and J. Rosenfeld and W. Dixon, Reinforcement Learning for Optimal Feedback Control. Springer 2018.

- (18) M. Laurière and O. Pironneau : Dynamic Programming for mean-field type control J. Optim. Theory Appl. 169 (2016), no. 3, 902–924.

- (19) C. Le Bris and P.L. Lions, Existence and uniqueness of solutions to Fokker-Planck type equations with irregular coefficients. Comm. Partial Differential Equations, 33, 1272-1317 , 2008.

- (20) A. Moussaoui and P. Auger: A bioeconomic model of a fishery with saturated catch and variable price: Stabilizing effect of marine reserves on fishery dynamics. Ecological Complexity 45 (2021) 100906.

- (21) A. Moussaoui, M. Bensenane, P. Auger, A. Bah, On the optimal size and number of reserves in a multi-site fishery model, Journal of Biological Systems. Vol. 23, No. 01, pp. 31-47 (2015)

- (22) G. Pagès. Numerical Probability: An Introduction with Applications to Finance. Springer, Berlin, 2018, 574p.

- (23) G. Pagès, H. Pham and J. Printems: An Optimal Markovian Quantization Algorithm For Multi-Dimensional Stochastic Control Problems, Stochastics and Dynamics , 4(4):501–545, 2004.

-

(24)

G. Pagès and O. Pironneau, Protection of a fishing Site with Optimal Quotas:

Dynamic Programming versus Supervised Learning. Encyclopedia, E. Trélat ed. (to appear) - (25) G. Pagès, J. Printems. Optimal quadratic quantization for numerics: the Gaussian case, Monte Carlo Methods and Appl., 9(2):135–165, 2003.

- (26) J. Yong and X. Y. Zhou: Stochastic Controls Hamiltonian Systems and HJB Equations Application of Mathematics series vol 43. Springer 1991.