Computer Science Department, Brown University, Providence, RI USA daniel_engel1@brown.edu This research was supported by NSF grant 1917990 Computer Science Department, Brown University, Providence, RI USA maurice.herlihy@gmail.com https://orcid.org/0000-0002-3059-8926 This research was supported by NSF grant 1917990

Presentation and Publication: Loss and Slippage in Networks of Automated Market Makers

Abstract

Automated market makers (AMMs) are smart contracts that automatically trade electronic assets according to a mathematical formula. This paper investigates how an AMM’s formula affects the interests of liquidity providers, who endow the AMM with assets, and traders, who exchange one asset for another at the AMM’s rates. Linear slippage measures how a trade’s size affects the trader’s return, angular slippage measures how a trade’s size affects the subsequent market price, divergence loss measures the opportunity cost of providers’ investments, and load balances the costs to traders and providers. We give formal definitions for these costs, show that they obey certain conservation laws: these costs can be shifted around but never fully eliminated. We analyze how these costs behave under composition, when simple individual AMMs are linked to form more complex networks of AMMs.

1 Introduction

An automated market maker (AMM) is an automaton that trades electronic assets according to a fixed formula. Unlike traditional “order book” traders, AMMs have custody of their own asset pools, so they can trade directly with clients, and do not need to match up (and wait for) compatible buyers and sellers. Today, AMMs such as Uniswap [5], Bancor [17], and others have become one of the most popular ways to trade electronic assets such as cryptocurrencies, electronic securities, or tokens. An AMM is typically implemented as a smart contract on a blockchain such as Ethereum [13]. Like circuit elements, AMMs can be composed into networks. They can be composed sequentially, where the output of one AMM’s trade is fed to another, and they can be composed in parallel, where a trade is split between two AMMs with different formulas. Compositions of AMMs can themselves be treated as AMMs [12]. This paper makes the following contributions. AMMs have well-known inherent costs. One such cost is slippage, where a large trade increases the price of the asset being purchased, both for the trader making the trade, and for later traders. We give two alternative mathematical definitions of slippage expressed directly in terms of the AMM’s formula: linear slippage focuses on the buyer’s price difference, and angular slippage characterizes how that buyer affects prices for later buyers.

Another cost is divergence loss (sometimes called impermanent loss), where the value of the liquidity providers’ investments end up worth less than if the invested assets had been left untouched. We give a precise mathematical definition of divergence loss, expressed in directly terms of the AMM’s formula,

We introduce a new figure of merit, called load, that measures how costs are balanced among parties on different sides of a trade.

We show how these costs can be analyzed in either worst-case or in expectation. We identify various conservation laws that govern these costs: they can be shifted, but never fully eliminated. We characterize how these costs behave under sequential and parallel composition, showing how to compute these costs for networks of AMMs, not just individual AMMs. Finally, we propose novel AMM designs capable of adapting to changes in these costs.

The paper is organized as follows. Section 2 describes our model and terminology. Section 3 introduces our cost measures and their conservation laws. Section 4 shows how these measure are affected by sequential composition, where the output of one AMM becomes the input of another AMM. Section 4 shows how these measure are affected by parallel composition, where traders split their trade between two AMMs that trade the same assets but according to different formulas. Section 6 surveys some simple adaptive strategies that can mitigate the costs’ conservation laws. Section 7 surveys related work.

Some of our numbered equations require long, mostly routine derivations which have been moved to the appendix to save space. A few of the longer proofs have also been moved to the appendix.

2 Definitions

We use bold face for vectors and italics for scalars (). Variables, scalar or vector, are usually taken from the end of the alphabet (), and constants from the beginning (). We use “:=” for definitions and “=” for equality. A function is strictly convex if for all and distinct , . Any tangent line for a strictly convex function lies below its curve.

Here is an informal example of a constant-product AMM [20]. An AMM in state has custody units of asset , and units of asset , subject to the invariant that the product , for and some constant . The AMM’s states thus lie on the hyperbolic curve . If a trader transfers units of to the AMM, the AMM will return units of to the trader, where is chosen to preserve the invariant .

Formally, the state of an AMM that trades assets and is given by a pair , where is the number of units in the AMM’s pool, and the number of units. The state space is given by a curve , where . Except when noted, the AMMs considered here satisfy the boundary conditions and , meaning that traders cannot exhaust either pool of assets. The function is subject to further restrictions discussed later.

There are two kinds of participants in decentralized finance. (1) Traders transfer assets to AMMs, and receive assets back. Traders can compose AMMs into networks to conduct more complicated trades involving multiple kinds of assets. (2) Liquidity providers (or “providers”) fund the AMMs by lending assets, and receiving shares, fees, or other profits. Traders and providers play a kind of alternating game: traders modify AMM states by trading one asset for another, and providers can respond by adding or removing assets, reinvesting fees, or adjusting other AMM properties.

AMM typically charge fees for trades. For example, Uniswap v1 diverts 0.3% of the assets returned by each trade back into that asset’s pool. Although there is no formal difficulty including fees in our analysis, we neglect them here because they have little impact on costs: fees slightly reduce both slippage costs for traders and divergence loss for providers.

A valuation assigns relative values to an AMM’s assets: units of are deemed worth units of . At valuation , a trader who moves an AMM from state to makes a profit if is positive, and otherwise incurs a loss. The trader’s profit is maximal precisely when is minimal. We assume that at any time, there is a single market valuation accepted by most traders. An arbitrage trade is one in which a trader makes a profit by moving an AMM from a state reflecting a prior market valuation to a distinct state reflecting the current market valuation.

A stable point for an AMM and valuation is a point that minimizes . If is the market valuation, then any trader can make an arbitrage profit by moving the AMM from any state to a stable state, and no trader can make a profit by moving the AMM out of a stable state. Valuations, stable points, and exchange rates are related. If is the stable point for valuation , then

| (1) |

Following Engel and Herlihy [12], we require the AMM function to satisfy certain reasonable properties, expressed here as axioms. A detailed discussion and justification for each axiom appears elsewhere [12].

Every AMM state should define a unique rate of exchange between its assets, and trades should change that rate gradually rather than abruptly.

Axiom 1 (Continuity).

The function is strictly decreasing and (at least) twice-differentiable.

An AMM must be able to adapt to any market conditions. The exchange rate of asset in units of at state is , the negative of the curve’s slope at that point.

Axiom 2 (Expressivity).

The exchange rate can assume every value in the open interval .

Slippage should work to the disadvantage of the trader. To prevent runaway trading, buying more of asset should make more expensive, not less.

Axiom 3 (Convexity).

For every AMM , is strictly convex.

It can be shown [12] that for any AMM satisfying these axioms, every valuation has a unique stable state.

Theorem 2.1 (Stability).

The function

| (2) |

is a homeomorphism that carries each valuation to the unique stable state that minimizes .

For example, the stable state map for the constant-product AMM is . Sometimes it is convenient to express in vector form as , where . We will sometimes use , the inverse function of :

| (3) |

The vector form is .

Most of the properties of interest in this paper can be expressed either in the asset domain, as functions of and , or in the valuation domain, as functions of and .

These definitions extend naturally to AMMs that trade more than two assets. Many (but not all) if the results presented below also generalize, but for brevity we focus on AMMs that trade between two assets.

3 Properties of Interest

3.1 AMM Capitalization

Let be a valuation with stable point . What is a useful way to define the capitalization (total value) of an AMM’s holdings? It may be appealing to pick one asset to act as numéraire, computing the AMM’s capitalization at point in terms of that asset alone:

For example, the numéraire capitalization of the constant-product AMM at the stable point for valuaton is .

Unfortunately, this notion of capitalization can lead to counter-intuitive results if the numéraire asset becomes volatile. As the value of the numéraire tends toward zero, “bad money drives out good”, and arbitrage traders will replace more valuable with less valuable . As the AMM fills up with increasingly worthless units of , its numéraire capitalization grows without bound, so an AMM whose holdings have become worthless has infinite numéraire capitalization.

A more robust approach is to choose a formula that balances the asset classes in proportion to their relative valuations. Define the (balanced) capitalization at to be the sum of the two asset pools weighted by their relative values. Let and .

| (4) |

If is the current market valuation, then will usually be in the corresponding stable state , yielding

| (5) |

For example, AMMs and have capitalization at their stable points:

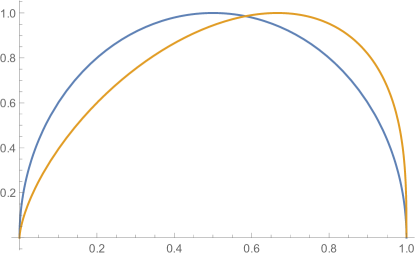

See Figure 1. Both have minimum capitalization 0 at and , where one asset is worthless, and maximal capitalizations at respective valuations and .

Theorem 3.1.

An AMM’s capitalization is maximal at the fixed-point , where the amounts of and are equal.

However, Figure 1 shows that the valuation that maximizes an AMM’s capitalization is not necessarily . An AMM is symmetric if . (Both Uniswap and Curve use symmetric curves.)

Lemma 3.2.

The stable state map for any symmetric AMM satisfies

Theorem 3.3.

Any symmetric AMM has maximum capitalization at .

3.2 Divergence Loss

Consider the following simple game. A liquidity provider funds an AMM , leaving it in the stable state for the current market valuation . Suppose the market valuation changes from to , and a trader submits an arbitrage trade that would take to the stable state for the new valuation. The provider has a choice: (1) immediately withdraw its liquidity from instead of accepting the trade, or (2) accept the trade. It is not hard to see that the provider should always choose to withdraw. The shift to the new valuation changes the AMM’s capitalization. If is the stable state for , then it cannot be stable for , so the difference between the capitalizations must be positive, so the arbitrage trader would profit at the provider’s expense. (In practice, a provider would take into account the value of current and future fees in making this decision.)

Define the divergence loss for an AMM to be

where . Sometimes it is useful to express divergence loss in the trade domain, as a function of liquidity pool size instead of valuation:

Informally, divergence loss measures the difference in value between funds invested in an AMM and funds left in a wallet. Recall that by definition minimizes , so divergence loss is always positive when .

Is it possible to bound divergence loss by bounding trade size? More precisely, can an AMM guarantee that any trade that adds or fewer units of incurs a divergence loss less than some , for positive constants ?

Unfortunately, no. There is a strong sense in which divergence loss can be shifted, but never eliminated. For example, for the constant-product AMM , the divergence loss for a trade of size is

| (6) |

Holding constant and letting approach 0, the divergence loss for even constant-sized trades grows without bound. This property holds for all AMMs.

Theorem 3.4.

No AMM can bound divergence loss even for bounded-size trades.

Proof 3.5.

For AMM ,

Note that , and . All other terms have finite limits, so

What is a provider’s worst-case exposure to divergence loss? Consider an AMM in state . As the asset becomes increasingly worthless, the valuation approaches as its stable state approaches .

Symmetrically, if the asset becomes worthless,

The provider’s worst-case exposure to divergence loss in state is thus . The minimum worst-case exposure occurs when . Recall from Section 3.1 that this fixed-point is exactly the state that maximizes the AMM’s capitalization. (See Appendix Section 10 for a more formal treatment of this claim.)

Divergence loss is sometimes called impermanent loss, because the loss vanishes if the assets return to their original valuation. The inevitability of impermanent loss does not mean that an AMM’s capitalization cannot increase, only that there is always an opportunity cost to the provider for not cashing in earlier.

3.3 Linear Slippage

Linear slippage measures how increasing the size of a trade diminishes that trader’s rate of return. Let be an AMM in stable state for valuation . Suppose a trader sends units of to , taking from to , the stable state for valuation . If the rate of exchange were linear, the trader would receive units of in return for units of . In fact, the trader receives only units, for a difference of .

The linear slippage(with respect to ) is the value of this difference:

| (7) |

In the trade domain, . Linear slippage with respect to is defined symmetrically.

For example, the linear slippage for the constant-product AMM for a trade of size is

| (8) |

Just as for divergence loss, holding constant and letting approach 0, the linear slippage across constant-sized trades grows without bound.

Theorem 3.6.

No AMM can bound linear slippage for bounded-size trades.

Proof 3.7.

As in the proof of Theorem 3.4, the claim follows because .

3.4 Angular Slippage

Angular slippage measures how the size of a trade affects the exchange rate between the two assets. This measure focuses on how a trade affects the traders who come after. Recall that the (instantaneous) exchange rate in state is the slope of the tangent . Let denote the angle of that tangent with the -axis. (We could equally well use the tangent’s angle with the -axis.) A convenient way to measure the change in price is to measure the change in angle. Consider a trade that carries from valuation with stable point , to valuation with stable point . Define the angular slippage of that trade to be the difference in tangent angles at and (expressed in the valuation domain):

In the trade domain, . Angular slippage is additive: for distinct valuations , Note that linear slippage is not additive.

Angular slippage and linear slippage are different ways of measuring the same underlying phenomenon: their relation is illustrated in Figure 2.

Here is how to compute angular slippage. By definition,. Let , , and .

| (9) |

The next lemma says says that the overall angular slippage, , is a constant independent of the AMM.

Theorem 3.8.

For every AMM , .

Proof 3.9.

Consider an AMM . As , implying . As implying . Because , .

The additive property means that no AMM can eliminate angular slippage over every finite interval. Lowering angular slippage in one interval requires increasing it elsewhere.

Corollary 3.10.

For any AMM , and any level of slippage , , there is an interval such that .

For example, the Curve [11] AMM advertises itself as having lower slippage than its competitors. Theorem 3.8 helps us understand this claim: compared to a constant-product AMM, Curve does have lower slippage than a constant-product AMM for stable coins when they trade at near-parity, but it must have higher slippage when the exchange rate wanders out of that interval.

3.5 Load

Divergence loss is a cost to providers, and linear slippage is a cost to traders. Controlling one without controlling the other is pointless because AMMs function only if both providers and traders consider their costs acceptable. We propose the following measure to balance provider-facing and trader-facing costs. The load (with respect to ) across an interval is the product of that interval’s divergence loss and linear slippage:

| (10) |

Load can also be expressed in the trade domain: .

3.6 Expected Load

We have seen that cost measures such as divergence loss, linear slippage, angular slippage, and load cannot be bounded in the worst case. Nevertheless, these costs can be shifted. Not all AMM states are equally likely. For example, one would expect stablecoins to trade at near parity [11].

Suppose we are given a probability density for future valuations. This distribution might be given a priori, or it may be learned from historical data. Can we compare the behavior of alternative AMMs given such a distribution?

Let be the distribution over possible future valuations. The expected load when trading for starting in the stable state for valuation is

Weighting this expectation with the probability that the trade will go in that direction yields

Define the expected load of AMM at valuation to be:

Of course, one can compute the expected value of any the measures proposed here, not just load.

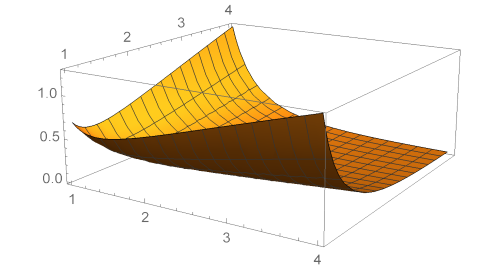

Figure 3 shows the expected load for , starting at valuation , where the expectation is taken over the distributions [22], where parameters range independently from 1 to 4. Inspecting the figure shows that symmetric distributions , which are increasingly concentrated around as grows, yield decreasing loads as the next valuation becomes increasingly likely to be close to the current one. By contrast, asymmetric distributions, which favor unbalanced valuations, yield higher loads because the next valuation is likely to be farther from the current one.

4 Sequential Composition

The sequential composition of two AMMs is constructed by using the output of one AMM as the input to the other. (See Engel and Herlihy [12] for a proof that the sequential composition of two AMMs is an AMM.) For example, if trades between florins and guilders, and trades between guilders and francs, then their sequential composition trades between florins and francs. A trader might deposit florins in , receiving guilders, then deposit those guilders in , receiving francs. In this section, we investigate how linear slippage and divergence loss interact with sequential composition.

Consider two AMMs , where trades between and , and between and . If is in state and in state then their sequential composition is , where [12]. (The sequential composition of more than two AMMs can be constructed by repeated two-way compositions.)

Let be the market valuation linking , inducing pairwise valuations

along with their vector forms . Let be a three-way valuation inducing analogous pair-wise valuations. Let be the stable point maps for respectively, and their vector forms.

Our composition rules apply when and start in their respective stable states111 If and do not start in stable states for the current market valuation, then an arbitrage trader will eventually put them there. for a market valuation : is the stable state for , for . for , and for . We analyze the changes in divergence loss and linear slippage when the market valuation changes from to .

4.1 Divergence Loss

Initially, the combined capitalization of and is . A trader sends units to , reducing the combined capitalization by

| (11) |

Next the trader sends the assets returned from the first trade to , reducing the combined capitalization by:

| (12) |

Finally, treating both trades as a single transaction reduces the combined capitalization by:

| (13) |

Combining Equations 11-13 yields

| (14) |

The effect of sequential composition on divergence loss is linear but not additive: the divergence loss of the composition is a weighted sum of the divergence losses of the components.

4.2 Linear Slippage

With respect to , a trader who sends units of to incurs the following slippage

| (15) |

Next the trader sends the assets returned from the first trade to , incurring the following slippage:

| (16) |

Finally, treating both trades as a single transaction yields slippage:

| (17) |

4.3 Angular Slippage

A trader sends to , where is the stable point for , the stable point for . By construction,

Define to be the respective angles of , , and with their -axes. We can express the tangents of the composite AMM’s angles in terms of the tangents of the component AMMs’ angles.

The component AMMs and determine the valuations , which induce the remaining valuations .

| (19) |

It follows that the angular slippage of the sequential composition of two AMMs can be computed from the component AMMs’ valuations.

4.4 Load

5 Parallel Composition

Parallel composition [12] arises when a trader is presented with two AMMs and , both trading assets and , and seeks to treat them as a single combined AMM . Let be the stable point maps for respectively, with their vector forms, and their inverses. (The parallel composition of more than two AMMs can be constructed by repeated two-way compositions.)

As shown elsewhere [12], a trader who sends units of to the combined AMM maximizes return by splitting those units between and , sending to and to , for , where .

We assume traders are rational, and always split trades in this way. Because the derivatives are equal, and are stable points of and respectively for the same valuation , so , and . If is in state and in , then , where . Our composition rules apply when both are in their stable states for valuation . We analyze the change in divergence loss and linear slippage when the common valuation changes from to . The new valuation may be the new market valuation, or it may be the best the trader can reach with a fixed budget of .

5.1 Divergence Loss

If a trader sends units of to , the combined capitalization suffers a loss of

| (21) |

It follows that divergence loss under parallel composition is additive.

5.2 Linear Slippage

A straightforward calculation shows:

| (22) |

Linear slippage is thus additive under parallel composition.

Linear slippage is also linear under scalar multiplication. Any AMM can be scaled by a constant yielding a distinct AMM . Let be the stable point for valuation , and the stable point for .

| (23) |

5.3 Angular Slippage

Because both and go from stable states for to stable states for ,

It follows that

| (24) |

5.4 Load

6 Adaptive Strategies

So far we have proposed several ways to quantify the costs associated with AMMs. Now we turn our attention to strategies for adapting to cost changes. A complete analysis of adaptive AMM strategies is material for another paper, so here we summarize two broad strategies motivated by our proposed cost measures. We focus on adjustments that might be executed automatically, without demanding additional liquidity from providers.

6.1 Change of Valuation

Suppose an AMM learns, perhaps from a trusted Oracle service, that its assets’ market valuation has moved away from the AMM’s current stable state, leaving the providers exposed to substantial divergence loss. Specifically, suppose has valuation with stable state , when it learns that the market valuation has changed to with stable point .

An arbitrage trader would move from to , pocketing a profit. Informally, can eliminate that divergence loss by “pretending” to conduct that arbitrage trade itself, leaving the state the same, but moving the curve. We call this strategy pseudo-arbitrage.

changes its function using linear changes of variable in and . Suppose and . First, replace with , shifting the curve along the -axis. Next, replace with , shifting the curve along the -axis. The transformed AMM is now . The current state still lies on the shifted curve, but now with slope , matching the new valuation. The advantage of this change is that ’s providers are no longer exposed to divergence loss from the new market valuation.

The disadvantage is that pseudo-arbitrage produces AMMs that do not satisfy the usual boundary conditions and , although they continue to satisfy the AMM axioms. In practical terms, now has more units of than it needs, but not enough units of to cover all possible trades. The AMM must refuse trades that would lower its holdings below zero, and there are units of inaccessible to the AMM. The liquidity providers might withdraw this excess, they might “top up” with more units of to rebalance the pools, or they might leave the extra balance to cover future pseudo-arbitrage changes. (Note that ’s ability to conduct trades only while the valuation stays within a certain range is similar to Uniswap v3’s “concentrated liquidity” option.)

6.2 Change of Distribution

Suppose an AMM’s formula was initially chosen to match a predicted distribution on future valuations. If that prediction changes, then it may be possible to adjust the AMM’s formula to match the new prediction. Such an adjustment might be built into the AMM’s smart contract, or it could be imposed from outside by the liquidity providers. The AMM’s current function could be replaced with an alternative that improves some expected cost measure, say, reducing expected load or increasing expected capitalization. But replacing AMM , in the stable state for the market valuation, with another , must follow certain common-sense rules.

First, any such replacement should not change the AMM’s reserves: if the AMM is in state , then the updated AMM is in state where . Adding or removing liquidity requires the active participation of the AMM’s providers, which can certainly happen, but not as part of the kind of automatic strategy considered here.

Second, any such replacement should not change the AMM’s current exchange rate: if the AMM is in state , then the updated AMM is in state where . To do otherwise invites further divergence loss. If is the stable state for the current valuation, and , then is not stable, and a trader can make an arbitrage profit (and divergence loss) by moving the AMM’s state back to the stable state.

For example, an AMM’s expected capitalization under distribution is

where . If the distribution changes to , then an adaptive strategy is to find a function with associated stable-point function that optimizes (or at least improves) the difference

subject to boundary conditions and , where . Developing practical ways to find such functions is the subject of future work.

7 Related Work

Today, the most popular automated market maker is Uniswap [2, 5, 16, 23], a family of constant-product AMMs. Originally trading between ERC-20 tokens and ether cryptocurrency, later versions added direct trading between pairs of ERC-20 tokens, and allowed liquidity providers to restrict the range of prices in which their asset participate. Bancor [17] AMMs permit more flexible pricing schemes, and later versions [7] include integration with external “price oracles” to keep prices in line with market conditions. Balancer [18] AMMs trade across more than two assets, based on a constant mean formula that generalizes constant product. Curve [11] uses a custom curve specialized for trading stablecoins , maintaining low slippage and divergence loss as long as the stablecoins trade at near-parity. Pourpouneh et al. [21] provide a survey of current AMMs.

The formal model for AMMs used here, including the axioms constraining AMM functions, and notions of composition, are taken from Engel and Herlihy [12].

Angeris and Chitra [3] introduce a constant function market maker model and focus on conditions that ensure that agents who interact with AMMs correctly report asset prices.

In event prediction markets [1, 9, 10, 14, 15], parties effective place bets on the outcomes of certain events, such as elections. Event prediction AMMs differ from DeFi AMMs in important ways: pricing models are different because prediction outcome spaces are discrete rather than continuous, prediction securities have finite lifetimes, and composing AMMs is not a concern.

AMM curves resemble consumer utility curves from classical economics [19], and trader arbitrage resembles expenditure minimization. Despite some mathematical similarities, there are fundamentally differences in application. In particular, traders interact with AMMs via composition, an issue that does not arise in the consumer model.

Aoyagi [6] analyzes strategies for constant-product AMM liquidity providers in the presence of “noise” trading, which is not intended to move prices, and “informed” trading, intended to move the AMM to the stable point for a new and more accurate valuation.

Angeris et al. [4] propose an economic model relating how the curvature of the AMM’s function affects LP profitability in the presence of informed and uninformed traders.

Bartoletti et al. [8] give a formal semantics for a constant-product AMM expressed as a labeled transition system, and formally verify a number of basic properties.

References

- [1] Jacob Abernethy, Yiling Chen, and Jennifer Wortman Vaughan. An optimization-based framework for automated market-making. In Proceedings of the 12th ACM conference on Electronic commerce - EC ’11, page 297, San Jose, California, USA, 2011. ACM Press. URL: http://portal.acm.org/citation.cfm?doid=1993574.1993621, doi:10.1145/1993574.1993621.

- [2] Hayden Adams, Noah Zinsmeister, and Dan Robinson. Uniswap v2 core. https://uniswap.org/whitepaper.pdf, March 2020. As of 8 February 2021.

- [3] Guillermo Angeris and Tarun Chitra. Improved Price Oracles: Constant Function Market Makers. SSRN Electronic Journal, 2020. URL: https://www.ssrn.com/abstract=3636514, doi:10.2139/ssrn.3636514.

- [4] Guillermo Angeris, Alex Evans, and Tarun Chitra. When does the tail wag the dog? Curvature and market making. arXiv:2012.08040 [q-fin], December 2020. arXiv: 2012.08040. URL: http://arxiv.org/abs/2012.08040.

- [5] Guillermo Angeris, Hsien-Tang Kao, Rei Chiang, Charlie Noyes, and Tarun Chitra. An analysis of Uniswap markets. arXiv:1911.03380 [cs, math, q-fin], February 2021. arXiv: 1911.03380. URL: http://arxiv.org/abs/1911.03380.

- [6] Jun Aoyagi. Lazy Liquidity in Automated Market Making. SSRN Electronic Journal, 2020. URL: https://www.ssrn.com/abstract=3674178, doi:10.2139/ssrn.3674178.

- [7] Bancor. Proposing bancor v2.1: Single-sided amm with elastic bnt supply. https://blog.bancor.network/proposing-bancor-v2-1-single-sided-amm-with-elastic-bnt-supply-bcac9fe655b, October 2020. As of 8 February 2021.

- [8] Massimo Bartoletti, James Hsin-yu Chiang, and Alberto Lluch-Lafuente. A theory of Automated Market Makers in DeFi. arXiv:2102.11350 [cs], April 2021. arXiv: 2102.11350. URL: http://arxiv.org/abs/2102.11350.

- [9] Yiling Chen and David M. Pennock. A utility framework for bounded-loss market makers. In Proceedings of the Twenty-Third Conference on Uncertainty in Artificial Intelligence, UAI’07, page 49–56, Arlington, Virginia, USA, 2007. AUAI Press.

- [10] Yiling Chen and Jennifer Wortman Vaughan. A new understanding of prediction markets via no-regret learning. In Proceedings of the 11th ACM Conference on Electronic Commerce, EC ’10, page 189–198, New York, NY, USA, 2010. Association for Computing Machinery. doi:10.1145/1807342.1807372.

- [11] Michael Egorov. Stableswap - efficient mechanism for stablecoin liquidity. https://www.curve.fi/stableswap-paper.pdf, November 2019. As of 8 February 2021.

- [12] Daniel Engel and Maurice Herlihy. Composing Networks of Automated Market Makers. arXiv:2106.00083 [cs], June 2021. arXiv: 2106.00083. URL: http://arxiv.org/abs/2106.00083.

- [13] Gavin Wood. Ethereum: A secure decentralised generalised transaction ledger, July 2021. URL: https://ethereum.github.io/yellowpaper/paper.pdf.

- [14] Robin Hanson. Combinatorial Information Market Design. Information Systems Frontiers, 5(1):107–119, January 2003. URL: https://ideas.repec.org/a/spr/infosf/v5y2003i1d10.1023_a1022058209073.html, doi:10.1023/A:1022058209073.

- [15] Robin Hanson. Logarithmic market scoring rules for modular combinatorial information aggregation. Journal of Prediction Markets, 1(1):3–15, 2007. URL: https://EconPapers.repec.org/RePEc:buc:jpredm:v:1:y:2007:i:1:p:3-15.

- [16] Hayden Adams, Noah Zinsmeister, Moody Salem, River Keefer, and Dan Robinson. Uniswap v3 Core, March 2021. URL: https://uniswap.org/whitepaper-v3.pdf.

- [17] Eyal Hertzog, Guy Benartzi, and Galia Benartzi. Bancor protocol. https://whitepaper.io/document/52/bancor-whitepaper, 2017.

- [18] Fernando Martinelli and Nikolai Mushegian. Balancer: A non-custodial portfolio man- ager, liquidity provider, and price sensor. https://balancer.finance/whitepaper/, 2109. As of 2 February 2021.

- [19] Andreu Mas-Collell, Michael Whinston, and Jerry R. Green. Microeconomic Theory. Oxford University Press, 1995.

- [20] Pintail. Uniswap: A good deal for liquidity providers? https://medium.com/@pintail/uniswap-a-good-deal-for-liquidity-providers-104c0b6816f2.

- [21] Mohsen Pourpouneh, Kurt Nielsen, and Omri Ross. Automated Market Makers. IFRO Working Paper 2020/08, University of Copenhagen, Department of Food and Resource Economics, July 2020. URL: https://ideas.repec.org/p/foi/wpaper/2020_08.html.

- [22] wikipedia. Beta distribution. https://en.wikipedia.org/wiki/Beta_distribution. As of 11 August 2021.

- [23] Yi Zhang, Xiaohong Chen, and Daejun Park. Formal specification of constant product (x . y = k) market maker model and implementation. https://github.com/runtimeverification/verified-smart-contracts/blob/uniswap/uniswap/x-y-k.pdf, 2018.

8 Appendix: Derivations of Equations

Equation 7

Equation 9

Equation 11

Equation 12

Equation 13

Equation 14

Equation 15

Equation 16

Equation 17

Equation 18

Equation 18

Equation 20

Equation 21

Equation 22

Equation 23

9 Appendix: Proofs

Theorem 3.1

Proof 9.1.

Let be the capitilization at . Note that is a continuous function on the compact set which guarantees the existence of the maximum. Let be the point where the maximum occurs. The first derivative is

The second derivative is

Now take a derivative with respect to of

Recall that is strictly convex, so for all .

We can then write the second derivative of the capitalization as

Thus is strictly concave so the maximum is unique. Finally, the first-order conditions tell us that or .

Lemma 3.2

Proof 9.2.

Let .

Thus .

Theorem 3.3

10 Appendix: Minimizing Divergence Loss Exposure

Let be an AMM currently in state , the stable state for . Define an -partition to be a sequence of values in such that , , and .

Given a partition , define the total divergence loss with respect to that partition as

Writing this out explicitly gives

Note that each term . We also know that for each . This gives us the upper bound

and the lower bound

Simply put

How tight can this lower bound get? Well, let be the point where is maximized. If we let , then we know that . We know that . But if then this means

which is entirely independent of the chosen partition , so

or . Additionally, total loss is conserved even if we modify the AMM for . No matter how you choose to drain asset type by depositing asset type , in the end you will drain all of if you deposit an infinite amount of .

We get a similar result when trading along the -axis. Define a -partition to be a sequence of elements in such that , , and .

Let be a Y-partition, . and so . Thus where . That is, . The total cost with respect to this partition is

For symmetry, define .

Note that and for each . We now get the upper bound

and the lower bound

So again we get the bounds

Similar to the -axis case this inequality is tight if and . Thus we do get a loss conservation result if we start at . Namely

The valuation thus corresponds to the AMM state where half of the wealth may be lost to trades and half can be lost to trades.

11 Mathematica Code

This section shows the Mathematica scripts used to generate Figure 3.