Ying Yang and Fang Yao

Department of Probability and Statistics, School of Mathematical Sciences,

Center for Statistical Science, Peking University, Beijing, China

Fang Yao is the corresponding author, fyao@math.pku.edu.cn. This research is supported by National Natural Science Foundation of China Grants No.11931001 and 11871080, the LMAM, and the Key Laboratory of Mathematical Economics and Quantitative Finance (Peking University), Ministry of Education.

Abstract

Functional data analysis has attracted considerable interest and is facing new challenges, one of which is the increasingly available data in a streaming manner. In this article we develop an online nonparametric method to dynamically update the estimates of mean and covariance functions for functional data. The kernel-type estimates can be decomposed into two sufficient statistics depending on the data-driven bandwidths. We propose to approximate the future optimal bandwidths by a sequence of dynamically changing candidates and combine the corresponding statistics across blocks to form the updated estimation. The proposed online method is easy to compute based on the stored sufficient statistics and the current data block. We derive the asymptotic normality and, more importantly, the relative efficiency lower bounds of the online estimates of mean and covariance functions. This provides insight into the relationship between estimation accuracy and computational cost driven by the length of candidate bandwidth sequence. Simulations and real data examples are provided to support such findings.

Modern technology has promoted the prevalence of functional data in many fields, such as biomedical studies, engineering, social sciences and so on. A fundamental problem in functional data analysis is the estimation of mean and covariance functions, which sets stage for subsequent analyses such as functional principal component analysis and functional regression.

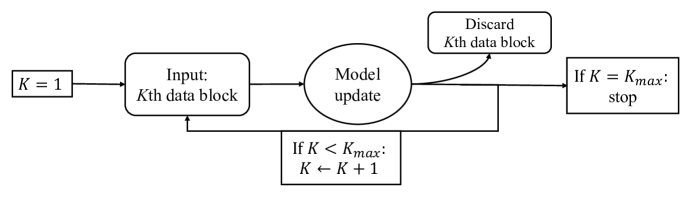

Technological advancements have improved the speed and volume of data acquisition and brought new challenges to model such data in a streaming manner using online approaches, which updates the model estimation with only the current available data and avoid storing the previous data, as illustrated in Figure 1. Such online methods not only provide a way to analyze the out-of-memory data but also allow real-time output of results, and hence are practically useful.

It has been studied extensively in machine learning and statistics. Langford et al. (2009), Duchi and Singer (2009), Xiao (2010) and Dekel et al. (2012) discussed stochastic gradient descent problems with explicit regularizations. Schifano et al. (2016) proposed an online version of predictive residual test for linear model and improved the aggregated estimating equation of Lin and Xi (2011) for generalized linear model. Extensions of linear and quadratic discriminant analyses have also been studied, see Hiraoka et al. (2000), Kim et al. (2007) and Pang et al. (2005). Following the custom of these papers, we refer to the classical approaches using the full data as batch methods.

Figure 1: Online estimation scheme.

To extend functional data analysis to the online context, the primary interest is to effectively and efficiently estimate the mean and covariance functions under various sampling schemes. Suppose that we have subjects which are observed at time points within the domain for the th individual, denoted by . In this work, we focus on the case that each subject is observed at possibly different times, i.e., are randomly distributed, referred to as independent design. This is distinguished from the common design where all subjects are observed on a common set of times, as discussed in Cai and Yuan (2011). From the online perspective, the latter is easier for it may take sample mean and sample covariance as sufficient statistics and store historical data in a linear fashion. For independent design, there are typically two types of estimation methods: pre-smoothing and pooling methods. The former is to smooth each individual curve and take the cross-sectional average to form the estimates, which is additive over subjects and can be extended to online settings straightforwardly. However, pre-smoothing technique is only applicable to sufficiently dense data and requires , i.e., ,

to attain the root- convergence rate for the mean and covariance estimation when tuning parameter (e.g., bandwidth) is chosen optimally for each subject, see Zhang and Chen (2007) and Kong et al. (2016). By contrast, pooling method can be adopted to both sparse and dense data. It borrows information from neighboring data and pools all subjects to estimate the mean and covariance functions, which is typically achieved by nonparametric methods including splines (Rice and Silverman, 1991; James et al., 2000; Paul and Peng, 2009) and local polynomials (Yao et al., 2005a, b; Li and Hsing, 2010), the later only requires to attain the root- convergence rate (Zhang and Wang, 2016).

In this work, we focus on the pooling method using local polynomial smoothing which is still challenging to extend to online estimation with theoretical guarantees. Here we take advantage of the extensive theory of local polynomial regression. Specifically, such kernel-based estimators have the form of locally weighted least squares and can be decomposed into two sufficient statistics that are additive on data depending on the bandwidth. The major difficulty is that the optimal bandwidth changes over data collection and the sufficient statistics vary accordingly. For instance, Zhou et al. (2003), Kristan et al. (2010) and Kong and Xia (2019) studied online local polynomial estimation, but did not update the bandwidths when accessing the stored statistics from previous data, thus lost the optimality to some extent. To overcome this, our key proposal is to generate a dynamic sequence of candidate bandwidths that contain the current optimal bandwidth as well as smaller values to approximate the future optimal bandwidths. The corresponding statistics based on the current data block with these dynamically updated candidate bandwidths are computed, which contain information only from one data block and are referred to as “sub-statistics”. The stored sufficient statistics are then updated by aggregating with the current sub-statistics. Consequently, we are able to update the estimate based on not only the current data block but also historical data, while only storing one set of dynamically updated sufficient statistics.

We employ the proposed online mean and covariance estimation to both dense and sparse functional data, which are also accessible for theoretical analysis. We derive the asymptotic normality of the online mean and covariance estimates from sparse to dense designs that is shown to coincide with the phase transition regime in Zhang and Wang (2016), even when the estimated mean is used in the covariance estimation. More importantly, when compared to the classical results based on full data, our online estimates have explicit lower bounds of the relative efficiency attained by the dynamically updated bandwidth sequences. These lower bounds indicate that the efficiency is proportional to the length of candidate bandwidth sequence, which suggests computing time and memory needed in a linear manner, especially for similar block sizes. Therefore we can make an informed choice on the trade-off between estimation accuracy and computational cost according to the real problems at hand.

The rest of the paper is organized as follows. In Section 2, we briefly describe the classical estimation of the mean and covariance functions for functional data analysis. In Section 3, we elucidate the proposed online method for the mean and covariance estimation using dynamic candidate bandwidths. In Section 4, we investigate theoretical properties of the proposed method and establish the lower bounds of the relative efficiency for the online estimators. Simulations and real data applications are presented in Section 5 and 6 to validate our theoretical findings. Technical assumptions and bandwidth selection are delineated in the Appendix, and proofs of theoretical results are collected in an online Supplementary Material for space economy.

2 Mean and Covariance Estimation

We first review the classical estimation of the mean and covariance functions for functional data analysis. Let be an stochastic process on an interval that can be expressed as

where is the mean function, is the stochastic part of with and for all , which implies that .

In the sequel, is assumed to be for simplicity.

Denote the current block as which increases to that tends to as data accumulate. Suppose that we have observed subjects in the th data block for , among which the th subject has measurements at possibly irregular time points, , , . In this work, we focus on the setting where only the number of subjects are increasing as data accumulate. This setting is different from the online time series analysis, where the measurements of one or a few sequences are increasing, as discussed in Bacher et al. (2009), Anava et al. (2013), Yang et al. (2019) and Richard et al. (2009). They usually considered, e.g., autoregressive models with time-invariant parameters, hence the accumulation of measurements can improve the estimation. By contrast, in functional data analysis, the trajectory of each subject is viewed as a random function, while the mean/covariance functions are modeled nonparametrically with information accumulated across subjects to improve estimation. We further remark that, if measurements for each subject are also collected in a streaming fashion, it raises the challenge due to dependence between newly arriving measurements and the previously discarded ones from the same subjects when considering nonparametric modeling of the mean/covariance function. One possibility is to incorporate some parametric structures such as those in time series models, coupled with functional data methods. This leads to a different line of research that can be a topic of future investigation.

Suppose that observations are contaminated with noises following

(1)

where are independently and identically distributed (i.i.d) with and . For notations, the subscript “” or “” denotes statistics based on only the th or th data block. The superscript “” or “” denotes statistics calculated either using the full data up to or by classical batch method (denoted by “ ”), or using only the - or -th data block and stored statistics by online method (denoted by “ ”), both of which contain information of data blocks up to or . Recall that Zhang and Wang (2016) discussed two weighting schemes, equal weight per observation/subject, which has no material difference when coupled with online estimation except for their expressions. Thus we focus on the case of equal weight per observation for conciseness in the sequel.

Denote , where is the kernel function and is the bandwidth. Classical mean estimate based on local linear smoother at block is , where

and is the bandwidth selected by the batch method using the full data up to block . Let and , and the solution can be explicitly written as

(2)

where only depends on the th block given by

To estimate , let for no contribution to covariance estimation otherwise. Let be the raw covariance based on in (2), i.e.

(3)

where . Let be the batch bandwidth up to block for covariance estimation, and the estimate of is give by , where

Let and , and the explicit solution is

(4)

where

3 Proposed Online Method

In this section, we give a detailed description of the online estimation for mean function , and the covariance estimation can be derived similarly. It can be seen from (2) that and are a pair of precise sufficient statistics. Given , we only need to store and in computer memory instead of the entire data blocks. However, it is noteworthy that takes different values as block varies, e.g., in streaming problems. This data-driven feature makes the online local polynomial estimation rather difficult, as storing all violates the virtue of online method. For example, Kong and Xia (2019) did not re-calculate the stored statistics with the updated bandwidth. This is a general issue for online statistical estimation involving data-driven parameters or structures and partially explains lack of proper online algorithms for local polynomial estimation that is arguably one of the most popular nonparametric regression methods.

To overcome this obstacle, we propose to generate a dynamic sequence at block () consisting of candidate bandwidths, denoted by . The key idea is to use appropriately selected as a surrogate of future optimal bandwidths for .

For the flow of presentation, the expressions of and the corresponding online estimator as well as the optimal form for are deferred to (17), (18) and (19) of Section 4.

We prove in Theorem 3 that converges to when , and propose to select from to approximate empirically.

Note that decreases with respect to , i.e., for , we set .

At every block , we compute pairs of statistics with candidate bandwidths based on the th data block. This gives a sequence of statistics referred to as “sub-statistics” as they contain only information of the th block (the definition of is given in (2)). To combine information across blocks, we introduce the so-called “pseudo-sufficient statistics” , whose update depends on only the sub-statistics of the current data block and the stored pseudo-sufficient statistics of previous blocks. Specifically,

(5)

with initialization , where the definition of would be presented later.

The formula (5) indicates that are of form which are calculated at different candidates across blocks, and hence the motivation is to select appropriately to make these candidates close to .

Recall that there are subjects in the th block and the th one has measurements. Define

(6)

i.e., are the sub-total numbers of observations of the th block for estimating and , and are the total numbers of observations up to block , respectively.

Let be the weight with respect to numbers of observations.

To update in an online fashion, we define the centroids as the weighted average of all previous candidate bandwidths whose sub-statistics are aggregated, i.e.,

(7)

We now give the definition of .

For and , we propose to select to be the index of the closest one of (available at block ) to , i.e.,

(8)

The selection of in (8) guarantees that is close to , which makes in (7) close to as well. Combined with the definition of , we conclude that the combined candidate bandwidths to produce are close to on average. Note that , the regression estimate at block is given by

(9)

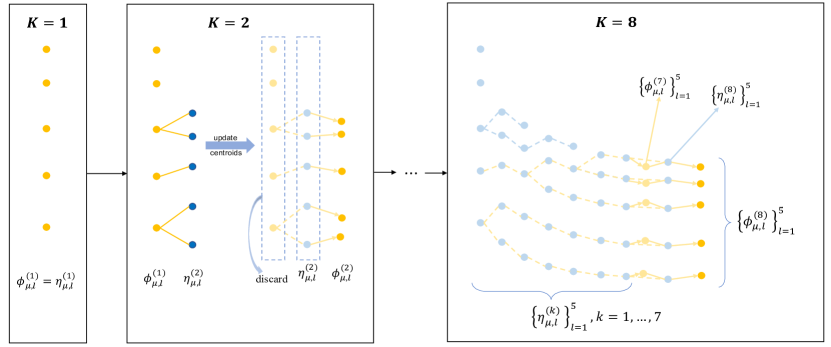

Since the definitions of and are entangled with each other, we take and for example in Figure 2 to illustrate the update procedure. We also display the candidates that produce for with and in Figure 3. Note that one does not need to store the previous candidates or the pseudo-bandwidths in practice.

Figure 2:

A sketch for the update procedure with and .

When (the left panel), and it can be obtained from (7) and (5) that and for .

When , are generated, and for each , selects the one closest to from , then the corresponding statistics are aggregated as illustrated by the solid lines in the middle panel. Once are determined, we update and according to (7) and (5), and can be discarded.

For , we select an update accordingly, and the procedure continues. By (5), are comprised of the sub-statistics of blockwise candidates connected by the dashed lines for the first 8 blocks in the right panel.

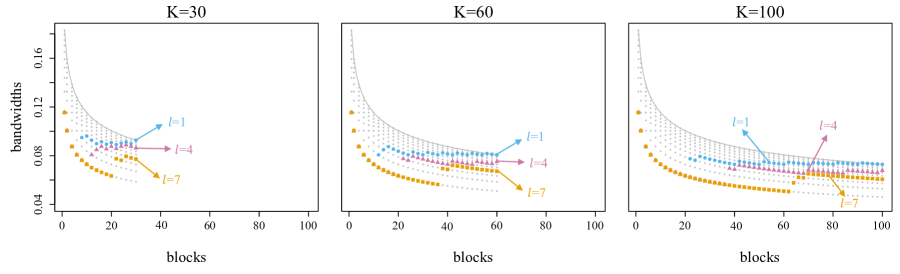

Figure 3: The solid line by connecting the largest values at each block corresponds to the online bandwidths . For illustration, we set with for . The vertical dot series represent the dynamic candidate sequences , , which are calculated by (19) given . The bold points are the bandwidths used in whose weighted averages are the centroids with , respectively.

To better appreciate (9), let denote the candidate bandwidth of the th block used in and , which correspond to the bold dots of in Figure 3 (). We refer to the dynamic sequence as the “pseudo-bandwidth” chain at block and formulate an equivalent expression of in (9):

(10)

where are defined as in (2). Compared (10) to the batch estimate (2), we are using to approximate which converges to the optimal bandwidth . As mentioned, the definition of centroids and the combination rule for statistics guarantee that pseudo-bandwidth chain is close to on average, as shown in Figure 3. Hence the online estimation using the pseudo-bandwidths shall perform well as long as converges to .

An implementation algorithm is given at the end of this section. We mention that and are recalculated at each , and only the newest and are stored in memory during the procedure. Hence the algorithm is computational efficient.

For estimating the covariance function , similar to (3), define the “raw” covariance observations for each block based on the online mean estimate as

(11)

where .

Let be the online bandwidth given explicitly in (18) of Section 4 and be the dynamic candidate bandwidths at block satisfying .

Then by setting and substituting with in (5), (8) and (7), we obtain the dynamic centroids and pseudo-sufficient statistics which are of form , where are defined as in (4). Let , and the online covariance estimate is given by

(12)

To conclude, we state the following algorithm for the mean estimation.

We mention that the proposed method can be applied to the general -dimensional local linear regression as well as higher-order local polynomials. Please see S.3 of Supplementary Material for more detail.

Algorithm 1 Online Estimation for Mean Function

1:Initialize:, , , , , for .

2:While:

3:input:

4:, , ;

5: compute as in (18) based on pilot estimates as introduced in Appendix B;

In this section, we illustrate the asymptotic normality of the online mean and covariance estimates of different sampling schemes. Then we study the convergence of online bandwidth selection and derive the optimal dynamic candidate bandwidth sequence, which gives a lower bound for the relative efficiency versus the batch estimates.

Recall that there are subjects in the th block and the th subject is measured at times for , and are defined in (6). To describe the phase transition phenomenon of the mean and covariance estimators, we denote the total number of subjects up to block and the individual averages of observations for and by,

(13)

Write if as . Recall that is the total number of blocks, and is the number of subjects. We stress that the asymptotic results in this section are for in spirit of streaming data accumulation.

Recalling that and , we further define

(14)

Theorem 1.

Under (A.1)–(A.4), (A.6) and (A.8)–(A.9) in Appendix A, let be the density of and be defined as in (14). Suppose that , , and , where are defined as in (13). Denote , and recall that is the noise variance. For a fixed interior point , as , the estimate as in (9) satisfies

where

which gives the following phase transition,

(1)

when ,

(2)

when , the variance becomes

where , and ;

(3)

when , the bias vanishes and the distribution is simplified to

Theorem 1 gives a systematic partition of functional data into three categories according to the numbers of repeated measurements on experimental subjects, yielding different convergence properties, which shall be discussed more after representing the asymptotic behaviors of covariance estimate. Note that in case (2) we have and , then holds when . Though we assume that are i.i.d. across and within subjects, it is noted that when may be dependent within subjects, such as scheduled visit times with random missing and/or fluctuation, the proposed online estimator also attains the same convergence result as the batch estimator by slightly modifying the proofs.

Recall that Zhang and Wang (2016) has taken the mean function as known in the covariance estimation, so is not entangled in the asymptotic distribution of . In the batch setting, we use the batch estimator instead and establish the asymptotic normality of the covariance estimation which is proved to be the same as using . To see this, denote and , then

On one hand, and are of the same order, both dominated by . On the other, note that is the weighted average of , and is weakly correlated to , which makes the bias induced by negligible. The bias of is also negligible compared to .

This argument also applies to the online estimation, and indicates that the bandwidth selection for mean and covariance estimators can be decoupled, which greatly facilitates the derivation. For space economy, we present the result for the online covariance estimation (using ), and defer the batch version (using ) to Lemma 1 in Appendix A, while the detailed proofs are offered in the Supplementary Material. Denote

(15)

Theorem 2.

Under (A.1)–(A.4) and (A.7)–(A.9) in Appendix A, let be defined as in (14). Suppose that , , and are the same as in Theorem 1.

For a fixed interior point , as , the covariance estimator in (12) satisfies

where

and the following statements hold,

(1)

when ,

(2)

when ,

where , , and ;

(3)

when , the bias vanishes and the distribution is simplified to

Similar to case (2) of Theorem 1, holds as long as . Note that the partition in Theorem 2 is identical to that in Theorem 1. Case (1) in these two theorems is the so-called sparse design, where mean and covariance estimates attain nonparametric convergence rate that is slower than root-. Case (2) and (3) are dense data such that the parametric convergence rate can be achieved. We refer to case (2) as moderately dense and case (3) ultra dense for that, under the latter scheme, both the bias term and the variance discontinuity vanish. Such phase transition phenomenon for online estimation is accordant with the classical batch result in Zhang and Wang (2016). Using the same techniques, one can further prove that, in terms of and uniform convergences, the online estimates can also attain the rates as the batch results in Zhang and Wang (2016).

To derive the optimal bandwidths, we introduce the integrated mean squared error. For a function and its estimate , let be the density function of supported on , then is a global loss criterion defined as

Note that , we have the following results for the batch and online estimates.

Corollary 1.

Under (A.1)–(A.4) and (A.6)–(A.9) in Appendix A, as ,

where

(16)

Corollary 2.

Suppose that the conditions in Theorem 1–2 hold, then as ,

From Corollary 1, the optimal bandwidths to minimize and are, respectively,

(17)

We suggest to use pilot estimates adopting the online method to approximate the unknown integrals and the variance terms , see details in Appendix B. The online estimates of optimal bandwidths are

(18)

where and are given explicitly in Appendix B.

Let be the bandwidth selected by replacing the online pilot estimates in (18) with the batch ones. When the bandwidths for pilot estimates are of appropriate orders, the online bandwidths (18) can attain the same convergence rates as the batch competitors, as stated in the following theorem.

Theorem 3.

Suppose that the conditions in Theorem 1–2 hold.

Let and be the proposed online bandwidth estimates (18) where and are based on online local polynomials with bandwidths and candidates given explicitly in (B.1) of Appendix B.

Then the online bandwidth selection satisfies that as ,

Define the relative efficiency in terms of integrated mean squared errors by

which measures the performance of the proposed online method compared to the classical estimate using full data. We now present our key result, the choice of candidate bandwidth sequence which makes (or ) as close to (or ) as possible for all and maximizes the relative efficiency with a lower bound.

Theorem 4.

Under (A.1)–(A.9) in Appendix A, when the candidate bandwidths are

(19)

then as , the corresponding online estimates and attain the optimal relative efficiency with the following lower bound,

where for and for . Specifically,

(20)

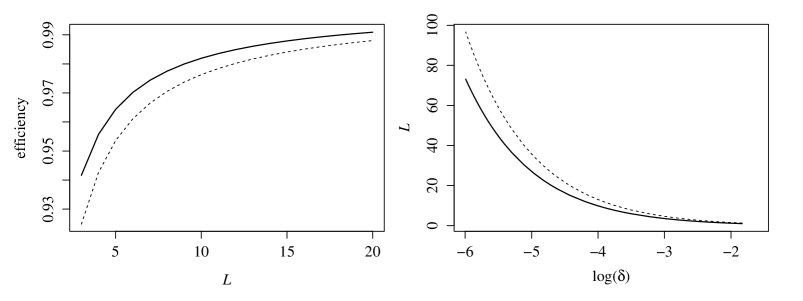

From the illustration in the left panel of Figure 4, the relative efficiencies of the proposed online mean and covariance estimates increase rapidly to exceed 95% when . This is desirable to attain high efficiency with a small/moderate . Note that the computational cost in terms of time and memory is proportional to , this lower bound helps make an informed trade-off between statistical and computational efficiency, which makes the proposed method practically useful. We also define the relative error,

whose upper bound can be derived from (4). We plot versus the upper bound of in the right panel of Figure 4 as a suggestion for the selection of in practice.

Figure 4: The left panel shows lower bounds for the relative efficiencies of the proposed online mean (solid lines) and covariance (dashed lines) estimates versus different lengths of candidate bandwidth sequences. The right panel plots the selection of under different upper bounds of for the proposed online mean (solid lines) and covariance (dashed lines) estimates.

We conclude this section by mentioning that the asymptotic distributions of and have the consistent form with the general -dimensional local linear regression. Hence Theorem 3 and 4 hold for general local linear regression with -dimensional covariates. See details in S.4 of Supplementary Material.

5 Simulation

We conduct simulation to illustrate the performance of the proposed online method and verify the theoretical findings in Section 4. Let noises be i.i.d. from and follow a uniform distribution on . Data are generated by , where with the mean function and the stochastic part , where , , are independently sampled from with . Recall that there are subjects in the th block, among which the th one has observations. For sparse data, we let follow the normal distribution and follow ; for dense data, we let and follow ; which are all rounded off to the nearest integers. The experiment is repeated 100 times, each with blocks.

We derive in (B.1) of Appendix B that bandwidths for pilot estimates of and in (1) shall be

After experimenting an extensive range of and , we find that the convergence rate of the online bandwidth is not sensitive to the values of these two quantities. Values in are in general adequate, thus we set in the sequel, where for estimating and for estimating . Let be the length of candidate bandwidth sequences for the pilot estimates of and , and recall that is the length of candidate bandwidth sequences for estimating and , we set when estimating and when estimating to ease computation. We also stop updating and after to further reduce computation without influencing the convergence rate as . Note that the classical batch method is computational expensive when sample size tends large, we implement it at every 40 blocks, i.e. . For mean and covariance estimation of sparse and dense data, we examine the following measures.

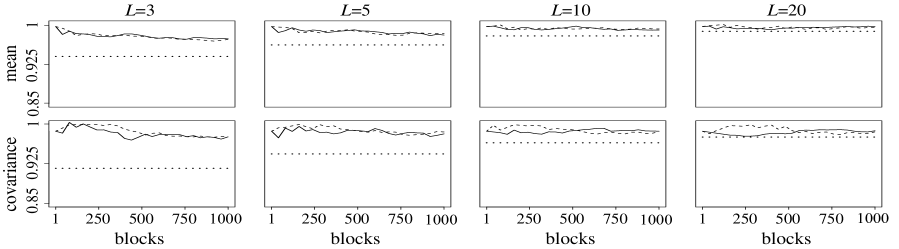

1. Relative efficiency. Figure 5 shows the empirical relative efficiencies of the mean and covariance estimates that increase with and are stably higher than the theoretical lower bounds in Theorem 4 when tends large. Recall that Kong and Xia (2019) studied the -dimensional online local linear regression of independent noises, which is not applicable to functional data. Even under the assumption of independent errors, their theoretical lower bounds of relative efficiency, which are 0.943 when and 0.924 when , are still smaller than ours. An explanation is that their stored statistics are fixed, and if the bandwidths of previous blocks deviate from the optimal values, there is no data-driven adjustment in the sequential estimates. By contrast, our stored statistics are updated dynamically by selecting different bandwidths from the candidate sequences and hence produce more efficient estimates.

Figure 5: The empirical relative efficiencies of the proposed online mean and covariance estimates for functional data based on sparse design (solid) and dense design (dashed) versus the theoretical lower bound (dotted) with candidate bandwidth sequence length and .

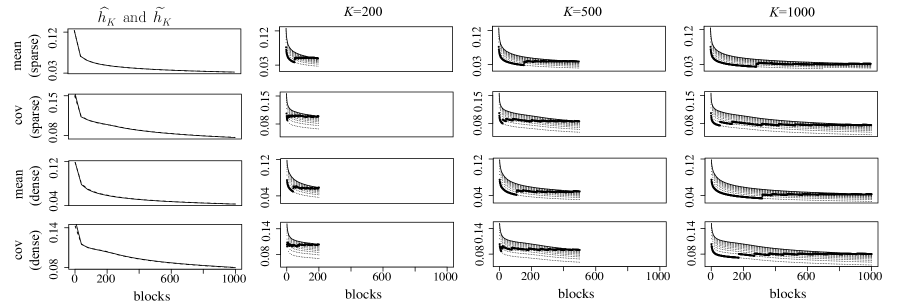

2. Bandwidth selection. The convergence of bandwidths in Theorem 3 is also examined in Figure 6, where both batch and online selections converge to the theoretical optimal bandwidth along with data collection.

Moreover, we depict the dynamically updated pseudo-bandwidth sequences and that are used to produce the estimates at time , similar to that shown in Figure 3. This provides empirical support for the fact that the our method is indeed able to adjust the sub-statistics in previous blocks in spite of no access to those data.

Figure 6: The four rows show, respectively, the bandwidth selection for mean and covariance estimation of sparse and dense data. The first column shows the Monto Carlo averages of the bandwidths selected by the online method (solid) and the batch method (dashed) based on 100 runs for , and the other three columns depict the dynamically updated bandwidths (thick dots) at time , respectively, along with the dynamic candidate sequences (light dots) and optimal bandwidth estimates (connected by solid line) at each .

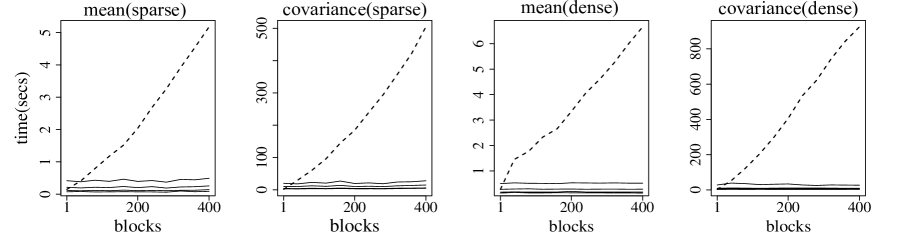

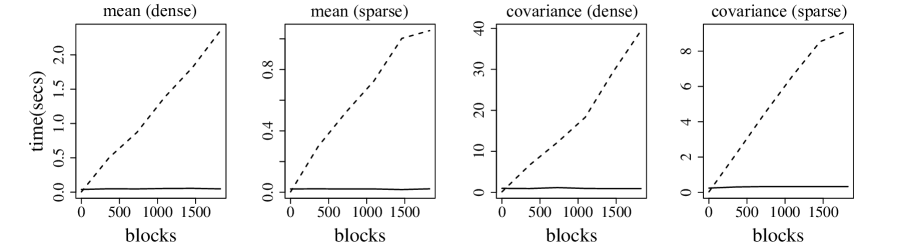

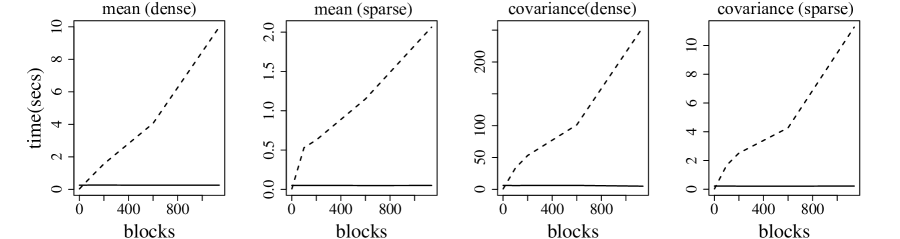

3. Computational time. We compare the computing times of the classical batch and the proposed online methods using the Unix server of 2.10GHz CPU and 188G memory with 176 logic cores. It is noted from Figure 7 that the computing time of the classical batch method grows approximately linearly with data blocks, while the online method spends nearly constant time given similar block sizes. Thus we graphed only the first 400 blocks for visualization when compared with the online method using that achieves substantial computational saving proportional to .

Figure 7: The comparison of computing times between the proposed online method and the batch method when estimating mean and covariance functions based on sparse and dense functional data. The dashed lines correspond to the computing times of the batch method and the solid lines to the online method, from the lowest to the highest in each panel representing , respectively.

We close this section by suggesting a reasonable range of based on our empirical and theoretical findings. The choice shall be made depending on whether accuracy or computation is of main concern.

6 Real Data Examples

In this section, we present two real data examples to illustrate the usefulness of the proposed online method.

6.1 Airline delay example

The airline dataset consists of flight arrival and departure details for all commercial airports in the USA, from January 1989 to December 2000 (https://community.amstat.org/jointscsg-section/dataexpo/dataexpo2009). This involves 304 airports whose daily numbers of flights range from 1 to 1269. We are interested in the pattern of delay time (unit: minute) during peak hours, i.e., from 6:00 to 23:00. Airports with flights less than 50 per day are removed. For each airport, flights departed during off-peak hours are also removed. Suppose that the departure delay time is independent across days and we treat the daily airport as a subject with flight departure delay times as measurements. Let one block represent a day and there are 4383 blocks in total.

We randomly select airports from the th day to form the th data block, where are discretely distributed with equal probability among . To obtain comparable results, the dense and sparse designs use the same airports for each block, and the dense measurements contain the sparse ones for each subject. Recall the number of measurements of the th subject in the th block is denoted by . For dense scheme, we let follow the discrete uniform distribution on and randomly pick flights with equal probability as measurements; for sparse case, choose equal-likely from 8 to 10 to form the measurements, where , . We also plot the results obtained from all airports and all flights as baseline for comparison.

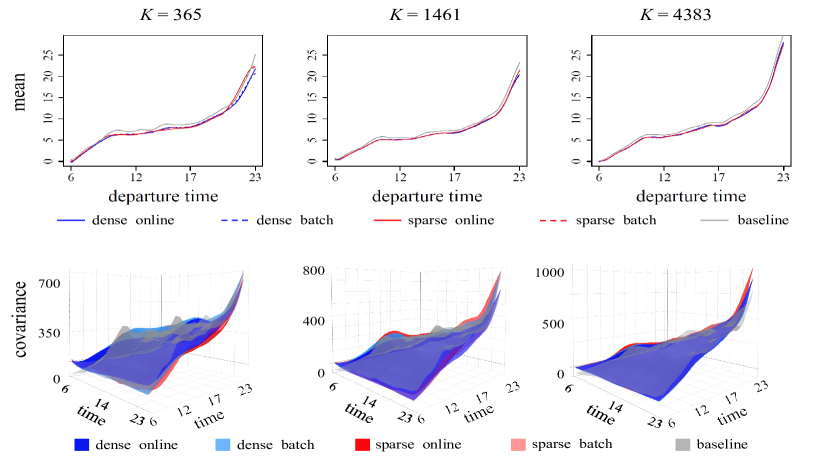

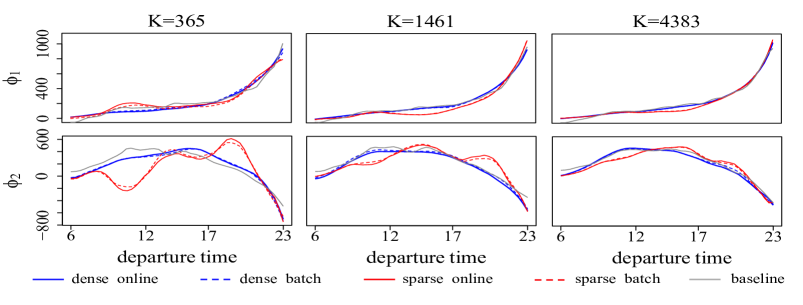

We set for the estimation of mean function, and and for covariance estimation, where is the length of candidate bandwidth sequence for main estimation, and is for the pilot bandwidths. As in simulation, we update the pilot estimates in bandwidth selection for covariance estimation till . Delay aggravates along time, which is probably due to the cumulative effect of congestion for flight runways. For both designs, the online and the batch estimates agree well when more data enter the model. We also conduct functional principal component analysis based on the covariance estimates. We show the first two eigenfunctions in Figure 9 at time (the end of year 1989, 1992, 2000), whose aggregated fractions of variation explained (FVE) exceeds 95%.

In both dense and sparse designs, as data accumulate, the online estimates become closer to the batch ones as well as the baseline results using all airports and flights. The first component has similar pattern to the mean function showing more variation in later hours, while the second represents the influence of different handling strategies of airports. An explanation may be that those airports with sound management system and adequate resource matching can alleviate the aggravating effect of delay to a certain extent, and vice versa. Comparison of computation times is given in Figure 10, where the online method shows substantial gains over the batch method.

Figure 8: Mean and covariance estimates for the airline delay dataset at (the end of year 1989,1992,2000), where the dashed lines and light-colored surfaces represent the batch results, and the solid lines and dark-colored surfaces represent the proposed online estimates, with color blue representing the dense case and red representing the sparse case. The estimates based on all airports and flights are also plotted in gray as the baseline. Figure 9: Estimates of the first two eigenfunctions for the airline delay dataset at (the end of year 1989, 1992, 2000), where the dashed lines correspond to the batch results and the solid to the proposed online method with dense design plotted in blue and sparse in red. The first eigenfunction has similar pattern to the mean function, and occupies 88% FVE. The estimates based on all airports and flights are also plotted in gray as the baseline.Figure 10: The comparison of computing times for the airline delay dataset between our method and the batch method of the first 1821 blocks/five years for mean and covariance estimation. The dashed lines correspond to the time complexity of the batch method and the solid lines to our method.

6.2 Online news example

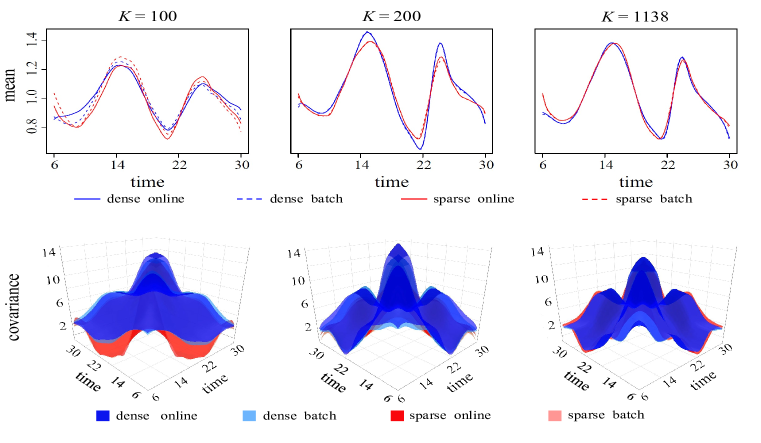

The second example is the online news data, which contains 93239 news items published during 2015/11/08 to 2016/07/07 and their hourly social feedback (number of clicks) of 48 hours after publishing on LinkedIn, Facebook and Google, which can be downloaded from http://archive.ics.uci.edu/ml/datasets/News+Popularity+in+Multiple+Social+Media+Platforms?tdsourcetag=s_pctim_aiomsg. Denote the publish time for the th news as and measurement time as , where , and (unit: hour). The release time can be viewed as random, and hence the observations are irregular by space. We refer to the news published during 0:00 to 6:00 as morning news and aim to study their number of clicks per hour over the domain . i.e., 24 hours after 6:00. We add up the number of clicks from the four platforms for the morning news and further remove the inactive news whose total number of clicks is less than 6. The remaining 5689 news are divided into 1138 blocks. We set the blockwise number of subjects as for and for . For each subject, let the dense measurements contain the sparse ones. For dense scheme, we set and for sparse scheme with measurements randomly chosen from the dense set with equal probability, , . Let denote the original hourly click number, and we make the following transformation: .

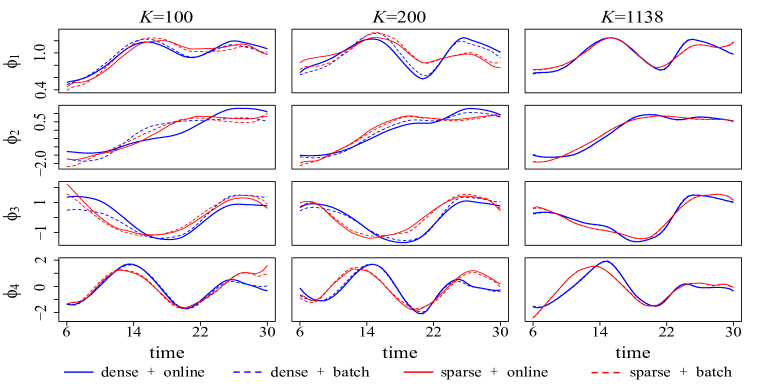

Parameter and are set the same as in the airline delay data and the pilot estimates in bandwidth for covariance estimation update till . Estimates for the mean and covariance function, and eigenfunctions are shown in Figure 11-12, where difference between online estimates and batch ones narrows down when data accumulate. Mean function estimates in Figure 11 reveals that the hourly clicks attain peaks at 14:00 and 00:00, i.e., after the lunch break and before night sleeping. Here we plot the first four eigenfunction estimates whose aggregated FVE is about 95%. The first eigenfunction indicates again that the attention a news received is influenced by people’s daily activity pattern. The second represents sustained growth or decrease of the news consumption, which is determined by the news quality, as people like to share valuable news, while articles that attract hits by headlines are gradually ignored. Finally, one can conclude from Figure 13 that our online method saves substantial computational time compared to the batch method.

Figure 11: Mean and covariance estimates for the online news dataset when , where the dashed lines and light-colored surfaces correspond to the batch results, and the solid lines and light-colored surfaces to the online estimates, with color blue representing the dense case and red representing the sparse case. The first eigenfunction has similar pattern to the mean function, and occupies nearly 66% FVE.Figure 12: Estimates of the first four eigenfunctions for the online news dataset using the online (solid) and batch (dashed) methods at time with dense design plotted in blue and sparse in red.Figure 13: The comparison of computing times for the online news dataset between our method and the batch method from to for mean and covariance estimation. The dashed lines correspond to the time complexity of the batch method and the solid lines to our method.

7 Concluding Remarks

In this work, we propose a dynamic candidate bandwidth method and apply it to functional data analysis for the mean and covariance estimation in the online context. By pre-storing a sequence of statistics and selecting appropriate candidates, our method dynamically updates statistics for all blocks. To the best of our knowledge, we are the first to implement dynamic update of previous statistics with changing bandwidths for streaming data. The proposed method is both computational and statistical efficient. It requires nearly constant memory and computing time and has a lower bound for the relative efficiency in terms of integrated mean squared errors. The computation and estimation trade-off is achieved by the parameter that provides useful guidance in practice.

The proposed method can be adopted to the higher-order local polynomials as well as other kernel-type estimates. For instance, one can combine the dynamic candidate bandwidths with profiling algorithm to fit semiparametric partially linear models, or with backfitting algorithm for additive models. Due to the interaction between component estimates in the iterative algorithm, the pseudo-sufficient statistics for each component function would depend on the estimates of other components and the relative efficiency needs to be further investigated.

Supplementary Material

The supplementary material contains the proofs for Theorem 1-4 and Lemma 1.

Appendix

A Assumptions and Auxiliary results

Recall that we observe , where , , with . Denote . The following assumptions are imposed for theoretical analysis in Section 4.

(A.1)

The observed time points are i.i.d. copies of a random variable defined on [0,1]. The density of is bounded away from 0 and its second derivative is bounded.

(A.2)

is independent of , and is independent of and .

(A.3)

The second and fourth derivatives of and are bounded and continuous.

(A.4)

The sample size satisfies , , , , where are defined in (13).

(A.5)

as for .

(A.6)

and .

Assumption (A.1)–(A.4) are general for functional mean and covariance estimation, see Zhang and Wang (2016). Assumption (A.5) is reasonable to require the number of measurements in each block is relatively small compared to the total number of measurements in all blocks. Assumption (A.6) is a standard requirement for mean estimation. For covariance estimation, further assumption on the moments of the random part is needed.

(A.7)

and .

We also impose the following assumptions on the kernel function.

(A.8)

is a symmetric probability density function on and .

(A.9)

is Lipschitz continuous: There exists such that

The lemma below states the asymptotic normality of the batch covariance estimate based on the batch estimator , corresponding to Theorem 2, which also improves the result of Zhang and Wang (2016) that used the underlying mean function .

Lemma 1.

Under (A.1)–(A.4) and (A.7)–(A.9) in Appendix A, suppose that , and let be the density of .

Denote , and recall that is the noise variance.

For a fixed interior point , as , the covariance estimator in (4) satisfies

where

The proof for the above lemma is similar to the online case which can be found in S.2 of the Supplementary Material.

B Bandwidth Selection

Recall that the optimal bandwidths for estimating and are, respectively,

where , , and , where are delineated below.

We suggest to use pilot estimates adopting online approach to approximate these quantities.

Take as an example. We first estimate by an online local cubic smoother with candidate bandwidth sequence , , and use to estimate , then integrate to obtain . And can be estimated by the same method, with candidate sequence denoted by .

When estimating and , the density function can be estimated by and , and we need only estimate and , which have distinguished expressions in the cases listed below and require different estimation procedures. These estimates are based on other local polynomials whose bandwidth selection is specified after presenting the methodology.

(a)

Mean function estimation for sparse data. Recall the definitions of and in the underlying models are (1), and

We need only estimate .

We follow the method of Fan and Yao (1998) to estimate :

1.

Estimate by an online local linear smoother denoted by with bandwidth and the corresponding candidate bandwidth sequence , ;

2.

Compute , and smooth by an online local linear smoother with the above and to obtain .

(b)

Covariance function estimation for sparse data. Recall the definition of in (4) and

We only need estimate that equals

,

where is the noise variance and is the stochastic part of . Estimating consists of three parts:

1.

Estimate by an online local linear smoother with bandwidth and the corresponding candidate bandwidth sequence , . Denote the estimate by ;

2.

Estimate by , where is obtained when estimating in step 2 of (a), and note that it is assumed that the noise variance is a constant, we estimate by ;

3.

Smooth by an online local linear smoother with the above and to obtain the estimate .

Based on these,

.

(c)

Mean function estimation for dense data. Recall that for dense data,

Estimating based on the raw covariance is infeasible as is not available.

As in (a), is estimated by , we can make use of the dense measurements for each subject , pre-smooth to obtain an estimate of which gives the estimate of noise variance (Zhang and Chen, 2007) and estimate by :

1.

Adopt the same method of (a) to compute ;

2.

Pre-smooth to estimate . Specifically, for each at block , apply local linear smooth to with bandwidth to obtain smoothed ,

then . To de-bias, let

and estimate by

then estimate by .

(d)

Covariance function estimation for dense data. Recall that

where are defined as in (4) of Section 4 and can be written as , , .

One can solve by based on approximations of and .

The estimation of and consists of the three parts below:

1.

Adopt the same method as in step 1 of (b) to compute ;

2.

Estimate by in step 2 of (c);

3.

Adopt the method in step 3 of (b) to compute .

The above processes to estimate and involve further bandwidth selection. Take the standard local linear regression as an instance.

According to Wand and Jones (1994) and Fan and Yao (1998), the optimal bandwidths for estimating and are

where involve unknown quantities depending on an . As literature on classical bandwidth selection has demonstrated, the convergences of in (18) hold as long as the bandwidths for estimating and satisfy, for ,

(B.1)

Hence it is usually adequate to select appropriate constants to compute . Based on extensive numerical experiments, we recommend to set and .

Using the same argument of deriving (19), we use the following candidate bandwidths for and , for ,

(B.2)

So far we have delineated the whole process of online estimation for mean and covariance functions in functional data.

REFERENCES

(1)

Anava et al. (2013)

Anava, O., Hazan, E., Mannor, S. and Shamir, O. (2013), ‘Online learning for time series prediction’, Journal of Machine Learning Research30, 172–184.

Bacher et al. (2009)

Bacher, P., Madsen, H. and Nielsen, H. A. (2009), ‘Online short-term solar power forecasting’, Solar Energy83(10), 1772–1783.

Cai and Yuan (2011)

Cai, T. T. and Yuan, M. (2011),

‘Optimal estimation of the mean function based on discretely sampled

functional data: Phase transition’, The Annals of Statistics39(5), 2330–2355.

Dekel et al. (2012)

Dekel, O., Ran, G. B., Shamir, O. and Xiao, L. (2012), ‘Optimal distributed online prediction using

mini-batches’, Journal of Machine Learning Research13(1), 165–202.

Duchi and Singer (2009)

Duchi, J. C. and Singer, Y. (2009),

‘Efficient online and batch learning using forward backward splitting’, Journal of Machine Learning Research10(18), 2899–2934.

Fan and Yao (1998)

Fan, J. and Yao, Q. (1998),

‘Efficient estimation of conditional variance functions in stochastic

regression’, Biometrika85(3), 645–660.

Hiraoka et al. (2000)

Hiraoka, K., Yoshizawa, S., Hidai, K.-i., Hamahira, M., Mizoguchi, H.

and Mishima, T. (2000),

Convergence analysis of online linear discriminant analysis, in

‘International Joint Conference on Neural Networks’, Vol. 3, pp. 387–391.

James et al. (2000)

James, G., Hastie, T. and Sugar, C. (2000), ‘Principal component models for sparse functional

data’, Biomatrika87(3), 587–602.

Kim et al. (2007)

Kim, T.-K., Wong, S.-F., Stenger, B., Kittler, J. and Cipolla, R.

(2007), Incremental linear discriminant

analysis using sufficient spanning set approximations, in ‘2007 IEEE

Conference on Computer Vision and Pattern Recognition’, pp. 1–8.

Kong et al. (2016)

Kong, D., Xue, K., Yao, F. and Zhang, H. H. (2016), ‘Partially functional linear regression in high

dimensions’, Biometrika103(1), 147–159.

Kong and Xia (2019)

Kong, E. and Xia, Y. (2019), ‘On the

efficiency of online approach to nonparametric smoothing of big data’, Statistica Sinica29(1), 185–201.

Kristan et al. (2010)

Kristan, M., Skocaj, D. and Leonardis, A. (2010), ‘Online kernel density estimation for interactive

learning’, Image and Vision Computing28(7), 1106–1116.

Langford et al. (2009)

Langford, J., Li, L. and Zhang, T. (2009), ‘Sparse online learning via truncated gradient’, Journal of Machine Learning Research10(2), 777–801.

Li and Hsing (2010)

Li, Y. and Hsing, T. (2010),

‘Uniform convergence rates for nonparametric regression and principal

component analysis in functional/longitudinal data’, The Annals of

Statistics38(6), 3321–3351.

Lin and Xi (2011)

Lin, N. and Xi, R. (2011),

‘Aggregated estimating equation estimation’, Statistics and Its

Interface4(1), 73–83.

Pang et al. (2005)

Pang, S., Ozawa, S. and Kasabov, N. (2005), Incremental linear discriminant analysis for

classification of data streams, in ‘IEEE transactions on Systems, Man

and Cybernetics, part B (Cybernetics)’, Vol. 35, pp. 905–914.

Paul and Peng (2009)

Paul, D. and Peng, J. (2009),

‘Consistency of restricted maximum likelihood estimators of principal

components’, The Annals of Statistics37(5), 1229–1271.

Rice and Silverman (1991)

Rice, J. A. and Silverman, B. W. (1991), ‘Estimating the mean and covariance structure

nonparametrically when the data are curves’, Journal of the royal

statistical society series b-methodological53(1), 233–243.

Richard et al. (2009)

Richard, C., Bermudez, J. C. M. and Honeine, P. (2009), Online Prediction of Time Series Data With

Kernels, Vol. 57, pp. 1058–1067.

Schifano et al. (2016)

Schifano, E. D., Wu, J., Wang, C., Yan, J. and Chen, M. H.

(2016), ‘Online updating of statistical

inference in the big data setting’, Technometrics58(3), 393–403.

Wand and Jones (1994)

Wand, M. P. and Jones, M. C. (1994),

Kernel Smoothing, Chapman and Hall.

Xiao (2010)

Xiao, L. (2010), ‘Dual averaging method for

regularized stochastic learning and online optimization’, Journal of

Machine Learning Research11(1), 2543–2596.

Yang et al. (2019)

Yang, H., Pan, Z. and Tao, Q. (2019), ‘Online Learning for Time Series Prediction of AR Model with

Missing Data’, Neural Processing Letters50(3), 2247–2263.

Yao et al. (2005a)

Yao, F., Muller, H. G. and Wang, J. L. (2005a), ‘Functional data analysis for sparse longitudinal

data’, Journal of the American Statistical Association100(June), 577–590.

Yao et al. (2005b)

Yao, F., Muller, H. and Wang, J. (2005b), ‘Functional linear regression analysis for longitudinal

data’, The Annals of Statistics33(6), 2873–2903.

Zhang and Chen (2007)

Zhang, J. and Chen, J. (2007),

‘Statistical inferences for functional data’, The Annals of Statistics35(3), 1052–1079.

Zhang and Wang (2016)

Zhang, X. and Wang, J.-L. (2016),

‘From sparse to dense functional data and beyond’, The Annals of

Statistics44(5), 2281–2321.

Zhou et al. (2003)

Zhou, A., Cai, Z., Wei, L. and Qian, W. (2003), M-kernel merging: Towards density estimation over

data streams, in ‘Eighth International Conference on Database Systems

for Advanced Applications’, pp. 285–292.