Auto-Regressive Approximations to Non-stationary Time Series, with Inference and Applications

Abstract

Understanding the time-varying structure of complex temporal systems is one of the main challenges of modern time series analysis. In this paper, we show that every uniformly-positive-definite-in-covariance and sufficiently short-range dependent non-stationary and nonlinear time series can be well approximated globally by a white-noise-driven auto-regressive (AR) process of slowly diverging order. To our best knowledge, it is the first time such a structural approximation result is established for general classes of non-stationary time series. A high dimensional test and an associated multiplier bootstrap procedure are proposed for the inference of the AR approximation coefficients. In particular, an adaptive stability test is proposed to check whether the AR approximation coefficients are time-varying, a frequently-encountered question for practitioners and researchers of time series. As an application, globally optimal short-term forecasting theory and methodology for a wide class of locally stationary time series are established via the method of sieves.

keywords:

[class=MSC2020]keywords:

and

1 Introduction

The Wiener-Kolmogorov prediction theory [37, 38, 63] is a fundamental result in time series analysis which, among other findings, guarantees that a weakly stationary time series can be represented as a white-noise-driven auto-regressive (AR) process of infinite order under some mild conditions. The latter structural representation result has had profound influence in the development of the classic linear time series theory. Later, [1, 2] studied the truncation error of AR prediction of stationary processes when finite many past values, instead of the infinite history, were used in the prediction. Nowadays, as increasingly longer time series are being collected in the modern information age, it has become more appropriate to model many of those series as non-stationary processes whose data generating mechanisms evolve over time. Consequently, there has been an increasing demand for a systematic structural representation theory for such processes. Nevertheless, it has been a difficult and open problem to establish linear structural representations for general classes of non-stationary time series. The main difficulty lies in the fact that the profound spectral domain techniques which were essential in the investigation of the AR() representation for stationary sequences are difficult to apply to non-stationary processes where the spectral density function is either difficult to define or only defined locally in time.

The first main purpose of the paper is to establish a unified AR approximation theory for a wide class of non-stationary time series. Specifically, we shall establish that every short memory and uniformly-positive-definite-in-covariance (UPDC) non-stationary time series can be well approximated globally by a non-stationary white-noise-driven AR process of slowly diverging order; see Theorem 2.5 for a more precise statement. Similar to the spirit of the Wiener-Kolmogorov prediction theory, the latter structural approximation result connects a wide range of fundamental problems in non-stationary time series analysis such as optimal forecasting, dependence quantification, efficient estimation and adaptive bootstrap inference to those of AR processes and ordinary least squares (OLS) regression with diverging number of dependent predictors. In fact, the very reason for us to consider the AR approximation instead of a moving average approximation or representation (c.f. Wold decomposition [64]) to non-stationary time series is due to its close ties with the OLS regression and hence the ease of practical implementation. Our proof of the structural approximation result resorts to modern operator spectral theory and classical approximation theory [22] which control the decay rates of inverse of banded matrices. Consequently the decay speed of the best linear projection coefficients of the time series can be controlled via the Yule-Walker equations; see Theorem 2.4 for more details.

The last two decades have witnessed the rapid development of locally stationary time series analysis in statistics. Locally stationary time series refers to the subclass of non-stationary time series whose data generating mechanisms evolve smoothly or slowly over time. See [15] for a comprehensive review. For locally stationary processes, we will show that the UPDC condition is equivalent to the uniform time-frequency positiveness of the local spectral density of (c.f. Proposition 2.9) and the approximating AR process has smoothly time-varying coefficients (c.f. Theorem 2.11).

In practice, one may be interested in testing various hypotheses on the AR approximation such as whether some approximation coefficients are zero or whether the approximation coefficients are invariant with respect to time. The second main purpose of the paper is to propose a high-dimensional test and an associated multiplier bootstrap procedure for the inference of the AR approximation coefficients of locally stationary time series. For the sake of brevity we concentrate on the test of stability of the approximation coefficients with respect to time for locally stationary time series (c.f. (3.2)). It is easy to see that similar methodologies can be developed for other problems of statistical inference such as tests for parametric assumptions on the approximation coefficients. Our test is shown to be adaptive to the strength of the time series dependence as well as the smoothness of the underlying data generating mechanism; see Propositions 3.7 and 3.8 and Algorithm 1 for more details. The theoretical investigation of the test critically depends on a result on Gaussian approximations to quadratic forms of high-dimensional locally stationary time series developed in the current paper (c.f. Theorem 3.5). In particular, uniform Gaussian approximations over high-dimensional convex sets [9, 31] as well as -dependent approximations to quadratic forms of non-stationary time series are important techniques used in the proofs.

Interestingly, the test of stability for the AR approximation coefficients is asymptotically equivalent to testing correlation stationarity in the case of locally stationary time series; see Theorem 3.1 for more details. Here correlation stationarity means that the correlation structure of the time series does not change over time. As a result, our stability test can also be viewed as an adaptive test for correlation stationarity. In the statistics literature, there is a recent surge of interest in testing covariance stationarity of a time series using techniques from the spectral domain. See, for instance, [23, 29, 45, 47]. But it seems that the tests for correlation stationarity have not been carefully discussed in the literature. Observe that the time-varying marginal variance has to be estimated and removed from the time series in order to apply the aforementioned tests to checking correlation stationarity [25, 72]. However, it is unknown whether the errors introduced in such estimation would influence the finite sample and asymptotic behaviour of the tests. Furthermore, estimating the marginal variance usually involves the difficult choice of a smoothing parameter. One major advantage of our test when used as a test of correlation stationarity is that it is totally free from the marginal variance as the latter quantity is absorbed into the errors of the AR approximation and hence is independent of the AR approximation coefficients.

Historically, the Wiener-Kolmogorov prediction theory was motivated by the optimal forecasting problem of stationary processes. Analogously, the AR approximation theory established in this paper is directly applicable to the problem of optimal short-term linear forecasting of non-stationary time series. For locally stationary time series, thanks to the AR approximation theory, the optimal short-term forecasting problem boils down to that of efficiently estimating the smoothly-varying AR approximation coefficient functions at the right boundary. We propose a nonparametric sieve regression method to estimate the latter coefficient functions and the associated MSE of forecast. Contrary to most non-stationary time series forecasting methods in the literature where only data near the end of the sequence are used to estimate the parameters of the forecast, the nonparametric sieve regression is global in the sense that it utilizes all available time series observations to determine the optimal forecast coefficients and hence is expected to be more efficient. Furthermore, by controlling the number of basis functions used in the regression, we demonstrate that the sieve method is adaptive in the sense that the estimation accuracy achieves global minimax rate for nonparametric function estimation in the sense of [58] under some mild conditions; see Theorem 4.3 for more details. In the statistics literature, there have been some scattered works discussing non-stationary time series prediction from some different angles. See for instance [19, 24, 32, 36, 55], among others. With the aid of the AR approximation, we are able to establish a unified globally-optimal short-term forecasting theory for a wide class of locally stationary time series asymptotically.

The rest of the paper is organized as follows. In Section 2, we introduce the AR approximation results for both general non-stationary time series and locally stationary time series. In Section 3, we test the stability of the AR approximation using statistics of the estimated AR coefficient functions for locally stationary time series. A multiplier bootstrap procedure is proposed and theoretically verified for practical implementation. In Section 4, we provide one important application of our AR approximation theory in optimal forecasting of locally stationary time series. In Section 5, we use extensive Monte Carlo simulations to verify the accuracy and power of our proposed methodologies. In Section 6, we conduct analysis on a financial real data set using our proposed methods. Technical proofs are deferred to the supplementary material [27].

Convention. Throughout the paper, we will consistently use the following notations. For a matrix or vector we use and to stand for their transposes. For a scalar or vector we use to denote its (Euclidean) norm. For a random variable or vector and some constant denote by its norm. For two sequences of real numbers and means that for some finite constant and means that for some positive sequence as For a sequence of random variables and positive real values we use the notation to state that is stochastically bounded. Similarly, we use the notation to say that converges to 0 in probability. Moreover, we use the notation to state that is bounded in norm; that is, for some finite constant . Similarly, we can define . We will always use as a genetic positive and finite constant independent of whose value may change from line to line.

2 Auto-Regressive Approximations to Non-stationary Time Series

In this section, we establish a general AR approximation theory for a non-stationary time series under mild assumptions related to its covariance structure. Specifically, in Section 2.1, we study general non-stationary time series. In Section 2.2, we investigate the special case of locally stationary time series where the covariance structure is assumed to be smoothly time-varying. Before proceeding to our main results, we pause to introduce two mild assumptions.

First, in order to avoid erratic behavior of the AR approximation, the smallest eigenvalue of the time series covariance matrix should be bounded away from zero. For stationary time series, this is equivalent to the uniform positiveness of the spectral density function which is widely used in the literature. Further note that the latter assumption is mild and frequently used in the statistics literature of covariance and precision matrix estimation; see, for instance, [7, 12, 71] and the references therein. In this paper we shall call this uniformly-positive-definite-in-covariance (UPDC) condition and formally summarize it as follows.

Assumption 2.1 (UPDC).

For all sufficiently large we assume that there exists a universal constant such that

| (2.1) |

where is the smallest eigenvalue of the given matrix and is the covariance matrix of the given vector.

As discussed earlier, the UPDC is a mild assumption and is widely used in the literature. Moreover, for locally stationary time series, we will provide a necessary and sufficient condition from spectral domain (c.f. Proposition 2.9) for practical checking. Second, we impose the following assumption to control the covariance decay speed of .

Assumption 2.2.

For all and we assume that there exists some constant such that

| (2.2) |

where is some universal constant independent of In addition, we assume that

Assumption 2.2 states that the covariance structure of decays polynomially fast and it can be easily satisfied for many non-stationary time series; see Example 2.7 for a demonstration. Note that amounts to a short range dependent requirement for in the sense that is bounded above by a fixed finite constant for all and while the latter sum may diverge if .

Remark 2.3.

In (2.2), we assume a polynomial decay rate. We can easily obtain analogous results to those established in this paper when the covariance decays exponentially fast,

| (2.3) |

For the sake of brevity, we focus on reporting our main results under the polynomial decay Assumption 2.2. From time to time, we will briefly mention the results under the exponential decay assumption (2.3) without providing extra details.

2.1 AR approximation for general non-stationary time series

In this subsection, we establish an AR approximation theory for general non-stationary time series satisfying Assumptions 2.1 and 2.2. Denote by a generic value which specifies the order of the AR approximation. In what follows, we investigate the accuracy of an AR() approximation to and provide the error rates using such an approximation. Observe that for theoretical and practical purposes is typically required to be much smaller than in order to achieve a parsimonious approximating model. For the best linear prediction (in terms of the mean squared prediction error) of is denoted as

| (2.4) |

where are the prediction coefficients. Denote It is well-known that is a time-varying white noise process, i.e.,

Armed with the above notation, we write

| (2.5) |

We point out that the coefficients {} are closely related to the Cholesky decomposition of the covariance and precision matrices of [26, 34, 50]. For more details, we refer the readers to Section C.2.1 of our supplement [27]. To provide an AR approximation of order where may be much smaller than we need to examine the theoretical properties of the coefficients . We summarize the results in Theorem 2.4.

Theorem 2.4.

On the one hand, Theorem 2.4 is general and only needs mild assumptions on the covariance structure of On the other hand, all error bounds in Theorem 2.4 are adaptive to the decay rate of the temporal dependence and the order of the AR approximation. Particularly, by (2.6), we only need to ensure a polynomial decay of the coefficients as a function of . Meanwhile, (2.9) establishes that the best linear forecast coefficients of based on and are close provided that and are sufficiently large. We point out that unlike the results in [1], our result (2.9) are stated in norm.

Based on Theorem 2.4, we establish an AR approximation theory for the time series in Theorem 2.5. Denote the process by

| (2.10) |

Since is a time-varying white noise process, by construction, we have that is a time-varying AR() process.

Theorem 2.5.

Suppose the assumptions of Theorem 2.4 hold. Then we have that for all

| (2.11) |

Furthermore, we have

| (2.12) |

Recall from convention in the end of Section 1 that the notation means bounded in the norm. Note that the AR approximation error diminishes as if Theorem 2.5 demonstrates that every sufficiently short-range dependent and UPDC non-stationary time series can be efficiently approximated by an AR process of slowly diverging order (c.f. (2.12)). Furthermore, the approximation error is adaptive to the decay rate of the time series covariance as well as the approximation order .

Remark 2.6.

Before concluding this subsection, we provide an example of a general class of non-stationary time series using their physical representations [65, 75] and illustrate how to check the short range dependence assumption 2.2 for this class of non-stationary processes.

Example 2.7.

For a non-stationary time series , we assume that it has the following form

| (2.13) |

where and are i.i.d. random variables and the sequence of functions are measurable such that for all is a properly defined random variable. The above representation is very general since under some mild regularity conditions, any non-stationary time series can be represented in the form of (2.13) via the Rosenblatt transform [54]; see [67, Section 4] and Section F of our revised supplement [27] for more detailed discussion.

Under the representation (2.13), temporal dependence can be quantified using physical dependence measures [65, 73, 76]. Let be an i.i.d. copy of For we define the physical dependence measure of by

| (2.14) |

where

Hence (2.2) can be directly checked by the physical dependence measures of a non-stationary time series. For a more specific example, consider the following non-stationary linear processes where are i.i.d. random variables with finite variance and are some constants. In this case, it is easy to see that (2.15) is satisfied if For more examples in the form of (2.13), we refer the readers to [65] and [26, Section 2.1].

2.2 AR approximation for locally stationary time series

From the discussion of Section 2.1, we have seen that every UPDC and sufficiently short-range dependent non-stationary time series can be well approximated by an AR process with diverging order (c.f. (2.10) and Theorem 2.5). However, from an estimation viewpoint, since we assume that only one realization of the time series is observed, the Yule-Walker equations by which the AR coefficients (c.f. (2.5) or (2.7)) are governed are clearly underdetermined linear systems (i.e. there are more unknown parameters than the number of equations). Therefore, additional constraints/assumptions on the non-stationary temporal dynamics have to be imposed in order to estimate the AR approximation coefficients consistently. In this section, we shall consider an important subclass of non-stationary time series, the locally stationary time series [15, 23, 24, 61, 75]. This class of non-stationary time series is characterized by assuming that the underlying data generating mechanism evolves smoothly over time.

In this subsection, we will establish an AR approximation theory for locally stationary time series under certain smoothness assumptions of their covariance structure. We start with the following definition. Analogous definitions have been used in [36, 55].

Definition 2.8 (Locally stationary time series).

A non-stationary time series is a locally stationary time series (in covariance) if there exists a function such that

| (2.16) |

Moreover, we assume that is Lipschitz continuous in and for any fixed is the autocovariance function of a stationary process.

Our Definition 2.8 only imposes a smoothness assumption on the covariance structure of . In particular, (2.16) means that the covariance structure of in any small time segment can be well approximated by that of a stationary process. Definition 2.8 covers many locally stationary time series models used in the literature [15, 23, 24, 61, 75]. For more discussions, we refer the readers to Example 2.13 below. Finally, we point out that for locally stationary time series with short-range dependence satisfying Assumption 2.2, we can update (2.16) to

| (2.17) |

Equipped with Definition 2.8, we first provide a necessary and sufficient condition for the UPDC assumption in the case of locally stationary time series. For stationary time series, Herglotz’s theorem asserts that UPDC holds if the spectral density function is bounded from below by a constant; see [5, Section 4.3] for more details. Our next proposition extends such results to locally stationary time series with short-range dependence.

Proposition 2.9.

If is locally stationary time series satisfying Assumption 2.2 and Definition 2.8, and there exists some constant such that for all and where

| (2.18) |

then satisfies Assumption 2.1. Conversely, if satisfies Assumptions 2.1 and 2.2 and Definition 2.8, then there exists some constant such that for all and

Note that is the local spectral density function. Proposition 2.9 implies that the verification of UPDC reduces to showing that the local spectral density function is uniformly bounded from below by a constant, which can be easily checked for many non-stationary processes. We refer the readers to Example 2.13 below for a demonstration.

Next, we establish an AR approximation theory for locally stationary time series. As mentioned earlier, we need some smoothness assumptions such that the AR approximation coefficients in (2.7) can be estimated consistently. Till the end, unless otherwise specified, we shall use the following Assumption 2.10, which states that the mean and covariance functions of are -times continuously differentiable, for some positive integer .

Assumption 2.10.

For some given integer , we assume that there exists a smooth function where is the function space on of continuous functions that have continuous first derivatives, such that Moreover, we assume that for any .

We now proceed to state the AR approximation theory for locally stationary time series (c.f. Theorem 2.11). We first prepare some notation. Denote such that

| (2.19) |

where and are defined as Here for any matrix , denotes its entry at the th row and th column. For a vector , denotes its th entry. As we will see in the proof of Theorem 2.11, is always invertible under the UPDC assumption. With the above notation, we further define as

| (2.20) |

Analogous to (2.10), denote

| (2.21) |

Theorem 2.11.

Theorem 2.11 establishes that a locally stationary time series can be well approximated by an AR process of smoothly time-varying coefficients and a slowly diverging order under mild conditions. In particular, the AR coefficient functions has the same degree of smoothness as the time-varying covariance functions . Observe that the smooth functions can be well approximated by models of small number of parameters using, for example, the theory of basis function expansion or local Taylor expansion. Therefore Theorem 2.11 implies that the approximating AR model can be consistently estimated using various popular nonparametric methods such as the local polynomial regression or the method of sieves provided that the underlying data generating mechanism is sufficiently smooth and the temporal dependence is sufficiently weak. We point out some special form of (2.22) has been established in Lemma 2.8 of [26] assuming mean zero time series, a physical representation form (2.27) and a specific satisfying In this regard, our result is a generalization of the existing result.

Remark 2.12.

As we can see from Theorem 2.11, the approximation error for the locally stationary AR approximation comprises of two parts. The first part is the truncation error, i.e., using an AR() approximation instead of an AR() approximation to . This part of the error is represented by the first term on the right hand side of equations (2.22) to (2.25). The second part is the error caused by using the smooth AR coefficients to approximate . This part of the error is represented by the second term on the right hand side of equations (2.22) to (2.25). In order to balance the aforementioned two types of errors, an elementary calculation shows that the choice of should satisfy that

| (2.26) |

We want to point out that [26] uses another special choice of in the setting of precision matrix estimation. Finally, we point out that in practice, can be chosen using a data-driven cross-validation procedure. The arguments and details can be found in Section E of our supplement [27].

Before concluding this subsection, we provide an example to illustrate two frequently-used models of locally stationary time series in the literature and how the assumptions in this subsection can be verified for those models.

Example 2.13.

We shall first consider the locally stationary time series model in [75, 76] using a physical representation. Specifically, the authors define locally stationary time series as follows

| (2.27) |

where is a measurable function such that is a properly defined random variable for all In (2.27), by allowing the data generating mechanism depending on the time index in such a way that changes smoothly with respect to , one has local stationarity in the sense that the subsequence is approximately stationary if its length is sufficiently small compared to . Analogous to (2.14), one can define the physical dependence measure for (2.27) as follows

| (2.28) |

Moreover, the following assumptions are needed to ensure local stationarity.

Assumption 2.14.

defined in (2.27) satisfies the property of stochastic Lipschitz continuity, i.e., for some and

| (2.29) |

where Furthermore,

| (2.30) |

It can be shown that time series with physical representation (2.27) and Assumption 2.14 satisfies Definition 2.8. In particular, for each fixed in Definition 2.8 can be found easily using the following

| (2.31) |

Note that the assumptions (2.29) and (2.30) ensure that is Lipschiz continuous in . Moreover, for each fixed is the autocovariance function of which is a stationary process.

The physical representation form (2.27) includes many commonly used locally stationary time series models. For example, let be zero-mean i.i.d. random variables (or a white noise) with variance . We also assume be functions such that

| (2.32) |

(2.32) is a locally stationary linear process. It is easy to see that Assumptions 2.2, 2.10 and 2.14 will be satisfied if and

| (2.33) |

Furthermore, we note that the local spectral density function of (2.32) can be written as where is defined such that with being the backshift operator. By Proposition 2.9, the UPDC is satisfied if for all and where is some universal constant. For more examples of locally stationary time series in the form of (2.27) especially nonlinear time series, we refer the readers to [65], [26, Section 2.1] , [18, Example 2.2 and Proposition 4.4], [35, Proposition E.6] and [28, 35, 43]. Especially, the time-varying AR and ARCH models can be written into (2.32) asymptotically (see Section C.2.5 of our supplement [27] for more detail), and Assumptions 2.2, 2.10 and 2.14 can be easily satisfied under mild assumptions. We refer the readers to the aforementioned references for more details.

For a second example, note that in [17, 23, 61], the locally stationary time series is defined as follows (see Definition 2.1 of [61]). is locally stationary time series if for each scaled time point there exists a strictly stationary process such that

| (2.34) |

where for some By similar arguments as those of model (2.27), Definition 2.8 as well as assumptions of this subsection can be verified for (2.34), especially (2.34) implies (2.16). We refer the readers to Section C.2.3 of our supplement [27].

3 A Test of Stability for AR Approximations

In this section, we study a class of statistical inference problems for the AR approximation of locally stationary time series using a high dimensional test. We point out here that, thanks to the AR approximation (2.24), a wide class of hypotheses on the structure of can be performed using the aforementioned testing procedure. Moreover, for the sake of brevity, in this paper we concentrate on the test of stability of the AR approximating coefficients with respect to time for locally stationary time series (c.f. (3.2)). The latter is an important problem as in practice one is usually interested in checking whether the time series can be well approximated by an AR process with time-invariant coefficients. For notational convenience, till the end of the paper, unless otherwise specified, we omit the subscript and simply write and . From line to line, we will emphasize this dependence if some confusions can be caused.

In order to theoretically investigate the test, time series dependence measures should be defined and controlled for the locally stationary time series . Throughout this section, we assume that the locally stationary time series admits the representation as in (2.27) equipped with physical dependence measures (2.28). In addition, note that in Section 2.2, all our AR approximation results are established under smoothness and fast decay assumptions of the covariance structure of without the need of any specific time series dependence measures. Therefore, we believe that the theoretical results of this section can be easily established using other measures of time series dependence such as the strong mixing conditions. For the sake of brevity, we shall concentrate on establishing results using the physical dependence measures in this paper. Finally, in the current paper we focus on locally stationary time series with smoothly time-varying dynamics. Our results can be generalized to piecewise locally stationary time series by allowing for some abrupt changes in the underlying data generating mechanism as introduced in [25, 66, 73]. For more discussions, we refer the readers to Section C.3.2 of our supplement [27].

3.1 Problem setup and test statistics

In this subsection, we formally state the testing problems and propose our statistics based on nonparametric sieve estimators of .

Since is related to the trend of the time series and in many real applications the trend is removed via differencing or subtraction, we focus our discussion on the test the stability of For the test of stability including the trend, we refer the readers to Remark 3.2. Formally, the null hypothesis we would like to test is

Let diverges to infinity at the rate such that

| (3.1) |

By Remark 2.12, the AR approximation for locally stationary time series at order achieves the smallest error. According to (2.6) and (2.22), when is sufficiently large, we have that for . Therefore, from an inferential viewpoint, for can be effectively treated as zero. Together with the approximation (2.24), it suffices for us to test

| (3.2) |

Before providing the test statistic for , we shall first investigate the interesting insight that is asymptotically equivalent to testing whether is correlation stationary, i.e., there exists some function such that

| (3.3) |

where stands for the correlation between and We formalize the above statements in Theorem 3.1 below.

Theorem 3.1.

Note that the right hand sides of (3.4) and (3.5) are of the order if is sufficiently large. Hence Theorem 3.1 establishes the asymptotic equivalence between and for short range dependent locally stationary time series. We point out that when the variance of the time series is constant, the error term will disappear from the right-hand side of (3.4). We mention that there exist important time series models which are non-stationary in covariance but stationary in correlation. For instance, the following model has been widely used in the literature [14, 19, 53, 68], where is a stationary time series. In fact, if a time series is correlation stationary with smooth mean and marginal variance, can always be approximated by the above form. In this sense, testing (3.3) is actually a test for against a more general non-stationary structure in terms of

Finally, we point out that even though the primary goal of our test is to investigate the stability of the AR coefficients, it provides an efficient and easier way to study correlation stationarity. For more details, we refer the readers to Section C.2.2 of our supplement [27].

For the rest of this subsection, we shall propose a test statistic for in (3.2). We start with the estimation of the coefficient functions for a generic order . Since it is natural for us to approximate it via a finite and diverging term basis expansion (method of sieves [10]). Specifically, by [10, Section 2.3], we have that

| (3.6) |

where are some pre-chosen basis functions on and is the number of basis functions. For the ease of discussion, throughout this section, we assume that is of the following form

| (3.7) |

Moreover, for the reader’s convenience, in Section I of [27], we collect the commonly used basis functions.

In view of (3.6), we need to estimate the ’s in order to get an estimation for as in [26]. For by (2.24), write

| (3.8) |

where for and By (3.8), we can estimate all the using only one ordinary least squares (OLS) regression with a diverging number of predictors. In particular, we write all as a vector then the OLS estimator for can be written as , where and is the design matrix. After estimating is estimated using (3.6) as

| (3.9) |

where has blocks and the -th block is and zeros otherwise.

With the estimation (3.9), we proceed to provide the test statistic. To test we use the following statistic in terms of (3.9)

| (3.10) |

The heuristic behind is that is equivalent to for , where . Hence the test statistic should be small under the null.

Remark 3.2.

We remark that in some cases practitioners and researchers may be interested in testing whether all optimal forecast coefficient functions including the trend do not change over time. That is equivalent to testing whether both the trend and the correlation structure of the time series stay constant over time. In this case, one will test

| (3.11) |

Similar to (3.10), for the test of , we shall use

| (3.12) |

Remark 3.3.

In this remark, we discuss how the statistics in (3.10) and in (3.12) can be simplified under some specific basis functions as considered in [33]. We focus our discussion on For some specific bases, for example, the Walsh transform [33], the Fourier basis, the Legendre polynomial and the Haar wavelet basis as summarized in Section I of our supplement [27], the first basis function is always one. That is to say

| (3.13) |

Due to the orthonormality, this leads to Consequently, using the definition in (3.9), i.e., we have that Consequently, we have

which does not include the global average anymore. Moreover, using the orthonormality of the basis functions, can be further simplified as

| (3.14) |

which is defined only in terms of the OLS estimators. We point out that using the simplified the version (3.14) has slightly better finite sample performance in terms of both accuracy and power, especially when the sample size is smaller. For more details on numerical performance, we refer the readers to Section G.1 of our supplement [27].

3.2 High dimensional Gaussian approximation and asymptotic normality

In this subsection, we prove the asymptotic normality of The key ingredient is to establish Gaussian approximation results for quadratic forms of high dimensional locally stationary time series.

We first show that the study of the statistic reduces to the investigation of a weighted quadratic form of high dimensional locally stationary time series. We prepare some notation. Denote and where we recall that Let be a dimensional diagonal block matrix with diagonal block and be a dimensional diagonal matrix whose non-zero entries are ones and in the lower major part. Recall and set

| (3.15) |

Recall in (2.5). We denote the sequence of -dimensional vectors by

| (3.16) |

where is the Kronecker product. We point out that when from Lemma C.3 of our supplement [27] we see that is a locally stationary time series and can be expressed using a physical representation. For notational convenience, we write

| (3.17) |

Recall (2.31). We also denote the matrix such that

Lemma 3.4.

Denote and the matrix by where

| (3.18) |

Suppose Assumptions 2.1, 2.10, 2.14 and C.1 of [27] hold true. Moreover, we assume that the physical dependence measure in (2.28) satisfies

| (3.19) |

for some constant and , where is some fixed small constant. Then for in the form of (3.7) and satisfying (3.1), when is sufficiently large, we have that

| (3.20) |

Based on Lemma 3.4, for the purpose of statistical inference, it suffices to establish the distribution of , which is a high dimensional quadratic form of since is divergent as . To this end, we shall establish a Gaussian approximation result for the latter quadratic form. Specifically, choose a sequence of centered Gaussian random vectors which preserves the covariance structure of and define Denote We shall establish a Gaussian approximation result by controlling the Kolmogorov distance

| (3.21) |

Theorem 3.5.

Remark 3.6.

Several remarks are in order. First, is the number of predictors in our least squares regression. is a tuning parameter which needs to be selected by the user; see Section E of [27]. Second, the parameters and are parameters needed in the M-dependence approximation and the Stein’s method implementation of our theoretical investigations. Those parameters are only needed in the theoretical investigations and are not needed in practical implementation of our methodology. In particular, is the truncation level for the locally stationary time series in (3.16), is the level of the M-dependence approximation, and is defined in such a way that is the probability that the truncated time series approximates the original time series sufficiently well. Third, we remark that in (3.23) can be well controlled for many commonly used basis functions. For instance, for the Fourier basis and the normalized orthogonal polynomials and for orthogonal wavelet; see Section I of [27] for more details. Fourth, it is easy to see that the approximation rate in Theorem 3.5 converges to 0 under mild conditions. For example, when is sufficiently large, i.e., the temporal relation decays fast polynomially, is sufficiently large, i.e., the time series have sufficiently large fiinte moments and we only need for some fixed sufficiently small constant and can be any fixed constant.

By Theorem 3.5, the asymptotic normality of can be readily obtained as in Proposition 3.7 below. Denote the long-run covariance matrix for at time as

| (3.24) |

and the aggregated covariance matrix as can be regarded as the integrated long-run covariance matrix of For and in (3.20), we define

| (3.25) |

where is the trace of the given matrix.

Proposition 3.7.

Next, we discuss the power of the test under a class of local alternatives. For a given set

where and as

Proposition 3.8.

Proposition 3.8 implies that our test can detect local alternatives when the distance between and dominates . Observe that Proposition 3.7 requires that . Therefore converges to 0 faster than . We mention that in the literature, for example [48], the authors studied the local power properties of frequency domain based covariance stationarity tests. For some discussions and connections with our current time domain test of correlation stationarity, we refer the readers to Section C.2.4 of our supplement [27].

Remark 3.9.

In this remark, we discuss how to deal with in (3.12). By a discussion similar to Lemma 3.4, can also be expressed as a quadratic form where we recall (3.18). Consequently, the only difference lies in the deterministic weight matrix of the quadratic form. By Theorem 3.5, we can prove similar results to as in Propositions 3.7 and 3.8. We omit further details.

3.3 Multiplier bootstrap procedure

In this subsection, we propose a practical procedure to implement the stability test based on a multiplier bootstrap procedure.

On the one hand, it is difficult to directly use Proposition 3.7 to carry out the stability test since the quantities and rely on which is hard to estimate in general. On the other hand, the high-dimensional Gaussian quadratic form converges at a slow rate. To overcome these difficulties, we extend the strategy of [73] and use a high-dimensional mulitplier bootstrap statistic to mimic the distributions of Note that (3.20) can be explicitly written as

| (3.26) |

Recall (3.16). For some positive integer denote

| (3.27) |

where are i.i.d. standard Gaussian random variables. is an important statistic since the covariance of is close to conditional on the data; see (D.62) of [27] for a more precise statement.

Since is based on which cannot be observed, we shall instead use the residuals

| (3.28) |

Denote similarly as in (3.16) by replacing with Accordingly, we denote as in (3.27) using With the above notations, we denote the bootstrap quadratic form as

| (3.29) |

where with Note that is a consistent estimator of

In Theorem 3.10 below, we prove that the conditional distribution of can mimic that of asymptotically. Denote

| (3.30) |

Theorem 3.10.

Remark 3.11.

First, can be well controlled by the commonly used sieve basis functions. For example, we have for the Fourier basis and orthogonal wavelets, and for the Legendre polynomials; see Section I of [27] for more details. Second, in the scenario where (3.31) is equivalent to Hence, in the optimal case when we are allowed to choose if . In this regime, Theorem 3.5 still holds true. Third, for the detailed construction of we refer the reader to (D.63) of [27]. Finally, a theoretical discussion of the accuracy of the bootstrap can be found in Section C of [27] and the choices of the hyperparameters are discussed in Section E of [27]. We point out that the performance of our proposed statistic and the multiplier bootstrap procedure are robust against these hyperparameters, especially and . For more detailed discussion on this aspect, we refer the readers to Section B.3 of our supplement [27] for more details.

Based on Theorem 3.10, we can use Algorithm 1 for practical implementation to calculate the -value of the stability test.

Inputs: tuning parameters , and chosen by the data-drive procedure demonstrated in Section E of [27], time series and sieve basis functions.

Step one: Compute using and the residuals according to (3.28).

Step two: Generate B (say 1000) i.i.d. copies of Compute correspondingly as in (3.29).

Step three: Let be the order statistics of Reject at the level if where denotes the largest integer smaller or equal to Let

Output: -value of the test can be computed as

4 Applications to globally optimal forecasting

In this section, independent of Section 3, we discuss an application of our AR approximation theory in optimal global forecasting for locally stationary time series. We first introduce the notion of asymptotically optimal predictor.

Definition 4.1.

A linear predictor of a random variable based on is called asymptotically optimal if

| (4.1) |

and the predictor is called strongly asymptotically optimal if

| (4.2) |

where is the mean squared error (MSE) of the best linear predictor of based on .

The rationale for the definition of strong asymptotic optimality is that, in practice, the MSE of forecast can only be estimated with a smallest possible error of when the time series length is . Specifically, it is well-known that the parametric rate for estimating the coefficients of a time series model is . When one uses the estimated coefficients to forecast the future, the corresponding influence on the MSE of forecast is (at best). Therefore, if a linear predictor achieves an MSE of forecast within range of the optimal one, it is practically indistinguishable from the optimal predictor asymptotically.

In what follows, we shall focus on the discussion of one-step ahead prediction. The general -step ahead prediction for where is some fixed constant, can be handled similarly with some necessary modification; we refer the readers to Section C.3.1 of our supplement [27] for more details. In order to make the forecasting feasible, we assume that the smooth data generating mechanism extends to time . That is, we assume that the time series satisfies the locally stationary assumptions imposed in the paper. Naturally, we propose the following estimate for , the best linear predictor of based on its predecessors ,

| (4.3) |

Observe that (4.3) is a truncated linear predictor where (instead of ) is used to forecast . Note that here is a generic order which may be different from the order used in the test of stability. The next theorem shows that is an asymptotic optimal predictor satisfying (4.1) or (4.2) in Definition 4.1 under mild conditions.

Theorem 4.2.

It is easy to see that the order which minimizes the right hand side of (4.4) is of the same order as that in (2.26). When is sufficiently large, the corresponding error on the right-hand side of (4.4) equals Hence Theorem 4.2 states that the estimator (4.3) is an asymptotic optimal one-step ahead forecast if and it is asymptotically strongly optimal if

Theorem 4.2 verifies the asymptotic global optimality of truncated linear predictors for locally stationary time series under mild conditions. For general stationary processes, [1] and [2], among others, established profound theory on the decay rate of the AR approximation coefficients as well as the magnitude of the truncation error. As we mentioned in the Introduction, those results are derived using sophisticated spectral domain techniques which are difficult to extend to non-stationary processes. In this section, using the AR approximation theory established in this paper, we are able to establish a global optimal forecasting theory for the truncated linear predictors for a general class of locally stationary processes.

In practice, one needs to estimate the optimal forecast coefficients , as well as the MSE of the forecast . To investigate the estimation accuracy of those parameters, we need to impose certain dependence measures for the series. Therefore, for the rest of this subsection, we shall focus on the physical representation as well as dependence measures as in (2.27) and (2.28). To obtain an estimation for the predictor, in light of (3.9), based on (4.3), we shall estimate or equivalently, forecast using

| (4.5) |

Next, we discuss the estimation of the MSE of the forecast. Denote the series of estimated forecast error by and the variance of by Recall the definition of in (3.8). According to [26, Lemma 3.11], we find that there exists a smooth function such that for some constant

| (4.6) |

Therefore the estimation of reduces to the estimation of the smooth function as the estimation error of (4.6) is sufficiently small for appropriately chosen . Similar to the estimation of the smooth AR approximation coefficients, one can again use the method of sieves to estimate the smooth function . Specifically, similar to (3.6), write Furthermore, by equation (3.14) of [26], we write

where is a centered sequence of locally stationary time series satisfying Assumptions 2.1, 2.2, 2.10 and 2.14. Consequently, we can use an OLS with being the response and , being the explanatory variables to estimate ’s, which are denoted as Finally, we estimate

| (4.7) |

and use to estimate the MSE of the forecast. We now state the asymptotic behaviour of the MSE of (4.5) in Theorem 4.3 below. Recall (3.30).

Theorem 4.3.

We point out that the error term on the right-hand side of the above equation vanishes asymptotically under mild conditions. For instance, assuming that is sufficiently large, slowly diverges as (for example, as in (2.26)) and the temporal dependence decays fast enough (i.e. is some large constant), the leading error term in Theorem 4.3 is Moreover, if we assume exponential decay of temporal dependence as in Remark 2.6 and is infinitely differentiable, then the error almost achieves the parametric rate except a factor of logarithm.

5 Simulation studies

In this section, we perform Monte Carlo simulations to study the finite-sample accuracy and power of the multiplier bootstrap Algorithm 1 for the test of stability of AR approximation coefficients and compare it with some existing methods on testing covariance stationarity in the literature. We point out that in Section B.2 of our supplement [27], we also conduct some simulations to examine the numerical performance of our proposed forecast (4.5). Due to space constraint, the simulation setups and results will be mainly reported in Section B.1 of our supplement [27].

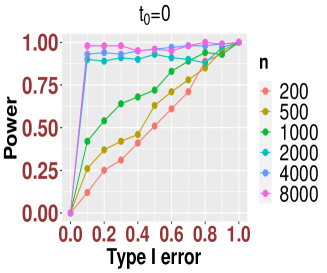

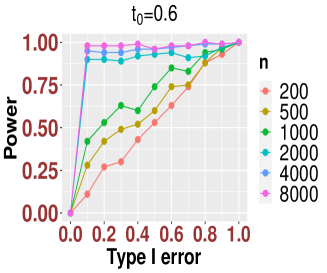

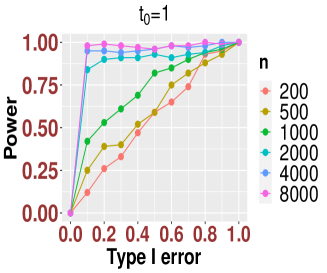

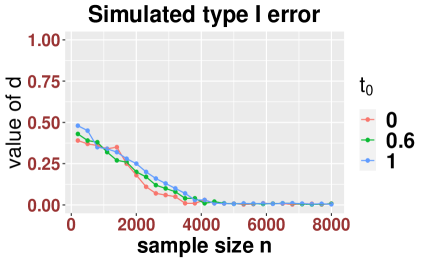

5.1 Accuracy and power of the stability test

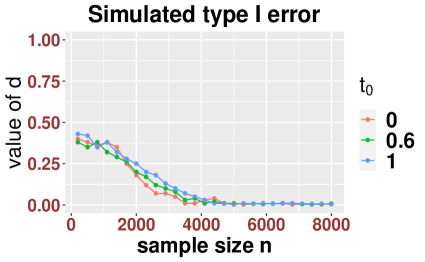

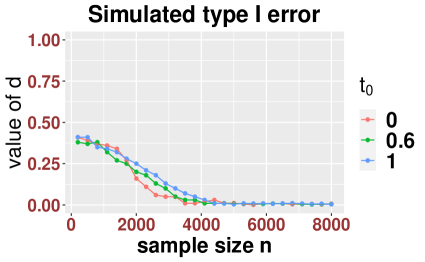

In this subsection, we study the performance of the proposed test (3.2). The simulation setups can be found in Section B.1 of our supplement [27]. First, we study the finite sample accuracy of our test under the null hypothesis that

| (5.1) |

Observe that the simulated time series are not covariance stationary as the marginal variances change smoothly over time. We choose the values of and according to the methods described in Section E of [27]. The simulation results can be found in Section B.1 of our supplement [27]. It can be seen from Table B.1 of [27] that our bootstrap testing procedure is reasonably accurate for all three types of sieve basis functions even for a smaller sample size

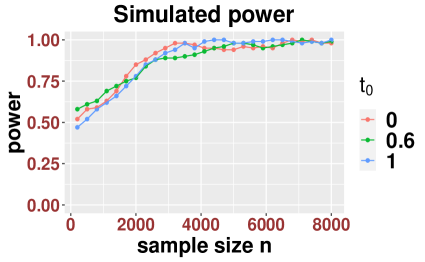

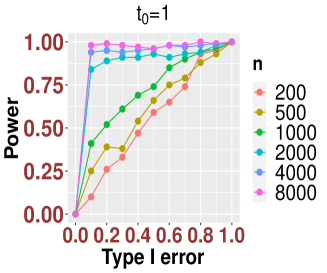

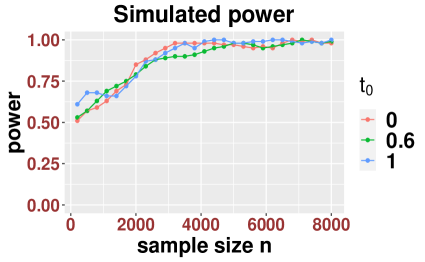

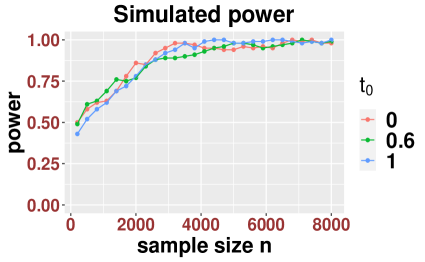

Second, we study the power of the tests and report the results in Table B.2 of [27] when the underlying time series is not correlation stationary, i.e., the AR approximation coefficients are time-varying. Specifically, we use

| (5.2) |

for the model setups in Section B.1 of [27]. It can be seen that the simulated powers are reasonably good even for smaller values of and sample sized, and the results will be improved when and the sample size increase. Additionally, the power performances of the three types of sieve basis functions are similar in general.

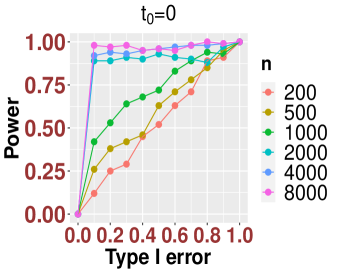

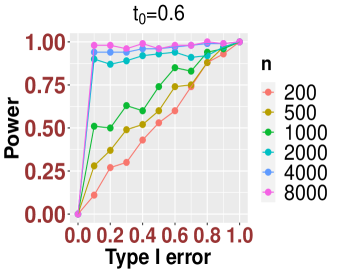

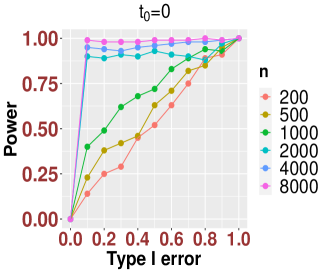

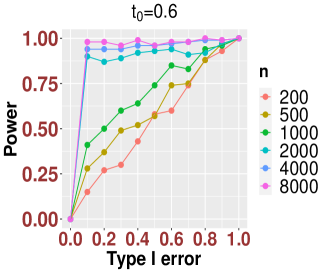

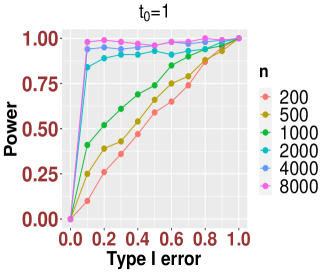

5.2 Comparison with tests for covariance stationarity

In this subsection, we compare our method with some existing works on the tests of covariance stationarity: the non-smoothed distance method in [23], the smoothed distance method in [46], the Kolmogorov-Smirnov(KS) type test in [51], the discrete Fourier transform method in [29] and the Haar wavelet periodogram method in [45]. The first three methods are easy to implement; for the fourth method, we use the codes from the author’s website (see https://www.stat.tamu.edu/~suhasini/test_papers/DFT_covariance_lagl.R); and for the last method, we employ the R package locits, which is contributed by the author. The detailed setups of those models can be found in Section B.1 of our supplement [27].

For all the simulations, we report the type I error rates under the nominal levels and for all the seven models in Table B.3 of [27], where for models 1-5 we use the setup (5.1). Our simulation results are based on 1,000 repetitions, where NS- refers to the non-smoothed distance method, S- refers to the smoothed method, KS refers to the Kolmogorov-Smirnov type method, DFT 1-3 refer to the approaches using the imagery part, real part, both imagery and real parts of the discrete Fourier transform method, respectively, HWT is the Haar wavelet periodogram method and MB is our multiplier bootstrap method Algorithm 1 using orthogonal wavelets constructed by (I.2) of [27] with Daubechies-9 wavelet.

Since HWT needs the length to be a power of two, we set the length of time series to be 256 and 512. For the parameters of the first three tests, we use for and for For the DFT, we choose the lag to be as suggested by the authors in [29]. Since the mean of model 5 is non-zero, we test its first order difference for the methods mentioned above. Moreover, we report the power of the above tests under certain alternatives in Table B.4 of [27] for models and models 1-5 under the setup (5.2).

We first discuss the results for models 6-7 since they are not only correlation stationary but also covariance stationary. It can be seen from Table B.3 of [27] that all the methods including our MB achieve a reasonable level of accuracy for the linear model 6. However, for the nonlinear model 7, we conclude from Table B.3 of [27] that the non-smoothed method tends to be over-conservative due to the fact that the latter test is designed only for linear models driven by independent errors. Moreover, the performance of the smoothed method is better. Regarding the power in Table B.4 of [27], we shall first discuss the results for models and where the errors of the models are i.i.d. For model , when the sample size and are smaller (, or ), our MB method is significantly more powerful than the other methods. When and increases, the first three tests starts to become similarly powerful. But when is smaller (i.e., the alternative is weaker), we find that the smoothed test outperforms the non-smoothed . This is consistent with the observations as in Sections 4.2 and 5 of [48] and can be understood using the results of Section 3.2 therein. Further, when both the sample size and increase, the HWT method becomes similarly powerful. Similar discussion holds for model Therefore, we conclude that, when the variances of the AR approximation errors stay constant, other methods in the literature are accurate for the purpose of testing for correlation stationarity (which is equivalent to covariance stationarity in this case). Furthermore, in this case the MB method is more powerful when the sample size is moderate and/or the departure from covariance stationarity is small for the alternative models experimented in our simulations.

Next, we study models 1-5. None of these models is covariance stationary. For the type I error rates, we use the setting (5.1) where all the models are correlation stationary. For the power, we use the setup (5.2). We find that DFT-3 is accurate for models 1-4 but with low power across all the models. Moreover, both smoothed and non-smoothed tests seem to have a high power for models 3-5. But this is at the cost of blown-up type I error rates. Similar conclusions can be made for the KS type test. This inaccuracy in Type-I error increases when the sample size becomes larger. In addition, for models 1-2, the first three methods seem to be accurate. The KS and smoothed methods have reasonably higher power, especially the KS method has a high power even is relatively small. In this regard, it seems that the conclusions of [48] still hold true beyond the time-varying linear Gaussian process. For the HWT method, even though its power becomes larger when the sample size and increase, it also loses its accuracy. Finally, for all the models 1-5, our MB method obtains both reasonably high accuracy and power. In summary, most of the existing tests for covariance stationarity are not suitable for the purpose of testing for correlation stationarity. Of course, the latter is expected as those tests are designed for testing covariance stationarity which is surely a different problem from correlation stationarity or stability of AR approximation. From our simulation studies, our multiplier bootstrap method Algorithm 1 performs well for the latter purpose.

6 An empirical illustration

In this section, we illustrate the usefulness of our results by analyzing a financial data set. In Section B.5 of our supplement [27], we also apply our method to study a global temperature data set.

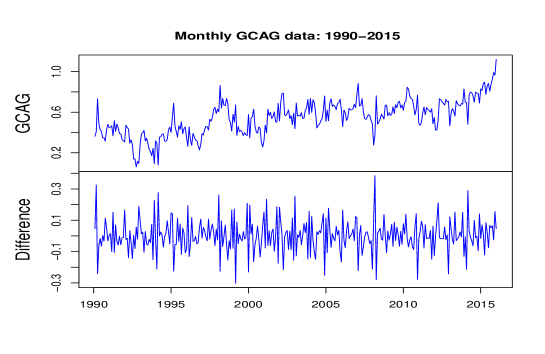

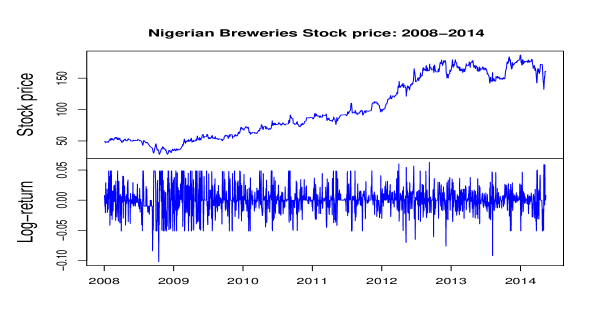

We study the stock return data of the Nigerian Breweries (NB) Plc. This stock is traded in Nigerian Stock Exchange (NSE). Regarding on market returns, the brewery industry in Nigerian has done pretty well in outperforming Brazil, Russia, India, and China (BRIC) and emerging markets by a wide margin over the past ten years. Nigerian Breweries Plc is the largest brewing company in Nigeria, which mainly serves the Nigerian market and also exports to other parts of West Africa. The data can be found on the website of morningstar (see http://performance.morningstar.com/stock/performance-return.action?p=price_history_page&t=NIBR®ion=nga&culture=en-US). We are interested in understanding the volatility of the NB stock. We shall study the absolute value of the daily log-return of the stock for the latter purpose.

We perform our analysis on the time period 2008-2014 (Figure G.5 of our supplement [27]). This time series contains the data of the 2008 global financial crisis and its post period. As said in the report from the Heritage Foundation [56], ”the economy is experiencing the slowest recovery in 70 years” and even till 2014, the economy does not fully recover.

Then we apply the methodologies described in Sections 3 for the absolute values of log-return time series. We point out that we focus on the log-return in our study without imposing any specific model assumption. We refer the readers to [35] for a nonparametric model-based approach to volatility inference where a locally stationary GARCH model is imposed. It is clear that we need to fit a mean curve for this model. Then we test the stability of the AR approximation as described in Section 3 using Algorithm 1. For the sieve basis functions, we use the orthogonal wavelets constructed by (I.2) of [27] with Daubechies-9 wavelet. We choose the parameters and based on the discussion of Section E of [27] which yields (i.e., ) and . We apply the bootstrap procedure described in Algorithm 1 and find that the -value is . We hence conclude that the prediction is likely to be unstable during this time period.

Next, we use the time series 2008-2014 as a training dataset to study the (rolling) forecast performance over the first month of 2015 using (4.5). We employ the data-driven approach from Section E of [27] to choose and The averaged MSE is . We point out that this leads to a improvement compared to simply fitting a stationary ARMA model using all the data from 2008 to 2014 where the MSE is 0.239, and leads to a improvement compared to the benchmark of simply using where the MSE is 0.251. In Table B.6 of our supplement [27], we also compare our proposed forecasting (4.5) with other methods in the literature.

Finally, we study the absolute value of the stock return from 2012 to 2014. We apply our bootstrap procedure Algorithm 1 to test correlation stationarity of the sub-series. We select (i.e., ) and for this sub-series and find that the -value is . We hence conclude that the prediction is stable during this time period. Therefore, we fit a stationary ARMA model to this sub-series and do the prediction. This yields an MSE of 0.192 which is close to 0.189, the MSE when we use the whole non-stationary time series and the methodology proposed in Section 4. The result from this sub-series shows an interesting trade-off between forecasting using a shorter and correlation-stationary time series and a longer but non-stationary series as described by the Rules of Thumb in [36]. The forecast model of the shorter stationary period via segment can be estimated at a faster rate but at the expense of a smaller sample size. The opposite happens to the longer non-stationary period. Note that 2012-2014 is nearly half as long as 2008-2014 and hence the length of the shorter stationary period is substantial compared to that of the long period. In this case we see that the forecasting accuracy using the shorter period is comparable to that of the longer period. In many applications where the data generating mechanism is constantly changing, the stable period is typically very short and in this case the methodology proposed in Section 4 is expected to give better forecasting results under the assumption that the time series is locally stationary. Finally, we emphasize that the correlation stationarity test proposed in this paper is an important tool to determine a period of prediction stability.

Acknowledgments

The authors would like to thank the editor, associated editor and three anonymous reviewers for their valuable and insightful comments which have improved the paper significantly.

SUPPLEMENT TO ”AUTO-REGRESSIVE APPROXIMATIONS TO NON-STATIONARY TIME SERIES, WITH INFERENCE AND APPLICATIONS

Appendix A Some conventions

Throughout the supplement, we consistently use the conventions listed in the end of Section 1 of the main manuscript. Moreover, for notational convenience and simplicity, till the end of the supplement, unless otherwise specified, we omit the subscript and simply write and . From line to line, we will emphasize this dependence if some confusions can be caused. We also recall that for any random variable we simply write to denote the norm of . For any deterministic vector we use to denote its Euclidean norm. For two sequences of positive real values and we write if and

Moreover, we use to denote the operator norm if is a matrix. Consequently, if is a sequence of deterministic matrices and is a sequence of positive real values, the notation means that there exists some constant so that Moreover, if is a sequence of random matrices, the notation means that the operator norm of is stochastically bounded by Finally, for two integers we define .

Appendix B Results on simulations and real data analysis

B.1 Simulation setup and results

In this subsection, we introduce our simulation setups and summarize the main simulation results.

We first consider four different types of non-stationary time series models: two linear time series models, a two-regime model, a Markov switching model and a bilinear model.

-

1.

Linear AR model: Consider the following time-varying AR(2) model

where are i.i.d. random variables whose distributions will be specified when we finish introducing the models. It is elementary to see that when are constants, the prediction is stable.

-

2.

Linear MA model: Consider the following time-varying MA(2) model

- 3.

-

4.

Markov two-regime switching model: Consider the following Markov switching AR(1) model

where the unobserved state variable is a discrete Markov chain taking values and with transition probabilities It is easy to check that the above model is stable if the functions are constants and bounded by one [52]. In the simulations, the initial state is chosen to be 1.

-

5.

Simple bilinear model: Consider the first order bilinear model

It is known from [30] that when the functions are constants and bounded by one, has an ARMA representation and hence stable.

In the simulations below, we record our results based on 1,000 repetitions and for Algorithm 1, we choose For the choices of random variables we set to be student- distribution with degree of , i.e., (5), for models 1-2 and standard normal random variables for models 3-5. For the purpose of comparison of accuracy, besides the above five models, we also consider two strictly stationary time series models, model 6 for a stationary ARMA(1,1) and model 7 for a stationary SETAR. Furthermore, for the comparison of power, we consider two non-stationary time series models whose errors have constant variances, denoted as models and

-

6.

Linear time series: stationary ARMA(1,1) process. We consider the following process

where are i.i.d. random variables.

-

7.

Nonlinear time series: stationary SETAR. We consider the following model

where are i.i.d. random variables.

-

.

Non-stationary linear time series. We consider the following process

where are i.i.d. standard normal random variables.

-

.

Piece-wise locally stationary linear time series. We consider the following process

where are i.i.d. standard normal random variables.

| Basis/Model | 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|---|---|---|---|---|

| =256 | ||||||||||

| Fourier | 0.132 | 0.11 | 0.12 | 0.13 | 0.11 | 0.067 | 0.07 | 0.06 | 0.04 | 0.06 |

| Legendre | 0.091 | 0.136 | 0.13 | 0.12 | 0.13 | 0.06 | 0.059 | 0.041 | 0.07 | 0.07 |

| Daubechies-9 | 0.132 | 0.12 | 0.11 | 0.133 | 0.132 | 0.063 | 0.067 | 0.059 | 0.068 | 0.065 |

| =512 | ||||||||||

| Fourier | 0.09 | 0.13 | 0.11 | 0.13 | 0.127 | 0.05 | 0.06 | 0.067 | 0.068 | 0.069 |

| Legendre | 0.09 | 0.094 | 0.092 | 0.12 | 0.118 | 0.04 | 0.058 | 0.07 | 0.043 | 0.057 |

| Daubechies-9 | 0.091 | 0.11 | 0.098 | 0.11 | 0.118 | 0.048 | 0.052 | 0.054 | 0.053 | 0.054 |

| Basis/Model | 1 | 2 | 3 | 4 | 5 | 1 | 2 | 3 | 4 | 5 |

|---|---|---|---|---|---|---|---|---|---|---|

| =256 | ||||||||||

| Fourier | 0.84 | 0.86 | 0.84 | 0.837 | 0.94 | 0.97 | 0.97 | 0.96 | 0.99 | 0.98 |

| Legendre | 0.8 | 0.806 | 0.81 | 0.84 | 0.83 | 0.97 | 0.968 | 0.95 | 0.97 | 0.91 |

| Daubechies-9 | 0.81 | 0.81 | 0.86 | 0.81 | 0.81 | 0.97 | 0.96 | 0.983 | 0.98 | 0.98 |

| =512 | ||||||||||

| Fourier | 0.91 | 0.9 | 0.96 | 0.9 | 0.93 | 0.96 | 0.97 | 0.973 | 0.98 | 0.97 |

| Legendre | 0.9 | 0.91 | 0.92 | 0.893 | 0.91 | 0.94 | 0.95 | 0.98 | 0.97 | 0.96 |

| Daubechies-9 | 0.87 | 0.88 | 0.93 | 0.91 | 0.91 | 0.96 | 0.99 | 0.97 | 0.97 | 0.96 |

| Model | NS- | S- | KS | DFT1 | DFT2 | DFT3 | HWT | MB | NS- | S- | KS | DFT1 | DFT2 | DFT3 | HWT | MB |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| =256 | ||||||||||||||||

| 1 | 0.08 | 0.084 | 0.078 | 0.148 | 0.057 | 0.13 | 0.18 | 0.132 | 0.024 | 0.032 | 0.029 | 0.067 | 0.017 | 0.063 | 0.083 | 0.063 |

| 2 | 0.081 | 0.088 | 0.082 | 0.097 | 0.068 | 0.12 | 0.085 | 0.12 | 0.038 | 0.042 | 0.039 | 0.04 | 0.07 | 0.057 | 0.028 | 0.067 |

| 3 | 0.171 | 0.19 | 0.134 | 0.183 | 0.04 | 0.137 | 0.227 | 0.11 | 0.087 | 0.087 | 0.092 | 0.103 | 0.011 | 0.033 | 0.093 | 0.059 |

| 4 | 0.2 | 0.24 | 0.19 | 0.163 | 0.05 | 0.12 | 0.176 | 0.133 | 0.077 | 0.086 | 0.082 | 0.087 | 0.013 | 0.034 | 0.113 | 0.068 |

| 5 | 0.46 | 0.39 | 0.23 | 0.293 | 0.077 | 0.19 | 0.153 | 0.132 | 0.29 | 0.19 | 0.15 | 0.21 | 0.03 | 0.14 | 0.12 | 0.065 |

| 6 | 0.11 | 0.103 | 0.089 | 0.105 | 0.096 | 0.09 | 0.087 | 0.088 | 0.047 | 0.053 | 0.059 | 0.053 | 0.053 | 0.039 | 0.052 | 0.057 |

| 7 | 0.051 | 0.088 | 0.13 | 0.097 | 0.08 | 0.092 | 0.085 | 0.127 | 0.018 | 0.039 | 0.036 | 0.04 | 0.06 | 0.047 | 0.038 | 0.061 |

| =512 | ||||||||||||||||

| 1 | 0.087 | 0.089 | 0.083 | 0.127 | 0.03 | 0.13 | 0.237 | 0.091 | 0.023 | 0.035 | 0.03 | 0.1 | 0.02 | 0.043 | 0.137 | 0.048 |

| 2 | 0.051 | 0.087 | 0.079 | 0.096 | 0.085 | 0.093 | 0.075 | 0.11 | 0.026 | 0.035 | 0.033 | 0.036 | 0.067 | 0.044 | 0.033 | 0.052 |

| 3 | 0.26 | 0.17 | 0.22 | 0.16 | 0.04 | 0.117 | 0.243 | 0.098 | 0.127 | 0.18 | 0.233 | 0.1 | 0.007 | 0.037 | 0.14 | 0.054 |

| 4 | 0.287 | 0.22 | 0.197 | 0.167 | 0.027 | 0.09 | 0.247 | 0.11 | 0.177 | 0.16 | 0.11 | 0.103 | 0.013 | 0.073 | 0.163 | 0.053 |

| 5 | 0.64 | 0.26 | 0.22 | 0.303 | 0.087 | 0.283 | 0.35 | 0.118 | 0.413 | 0.15 | 0.17 | 0.26 | 0.063 | 0.167 | 0.23 | 0.054 |

| 6 | 0.11 | 0.1 | 0.104 | 0.093 | 0.084 | 0.088 | 0.088 | 0.092 | 0.035 | 0.043 | 0.048 | 0.046 | 0.047 | 0.048 | 0.053 | 0.048 |

| 7 | 0.051 | 0.078 | 0.077 | 0.087 | 0.113 | 0.083 | 0.093 | 0.092 | 0.013 | 0.037 | 0.039 | 0.037 | 0.047 | 0.043 | 0.04 | 0.051 |

| Model | NS- | S- | KS | DFT1 | DFT2 | DFT3 | HWT | MB | NS- | S- | KS | DFT1 | DFT2 | DFT3 | HWT | MB |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 0.263 | 0.29 | 0.33 | 0.14 | 0.03 | 0.07 | 0.3 | 0.81 | 0.503 | 0.49 | 0.43 | 0.113 | 0.053 | 0.089 | 0.4 | 0.97 |

| 2 | 0.183 | 0.28 | 0.3 | 0.497 | 0.08 | 0.092 | 0.585 | 0.81 | 0.68 | 0.69 | 0.85 | 0.14 | 0.06 | 0.047 | 0.38 | 0.96 |

| 3 | 0.44 | 0.53 | 0.62 | 0.153 | 0.04 | 0.16 | 0.393 | 0.86 | 0.7 | 0.84 | 0.79 | 0.14 | 0.05 | 0.09 | 0.64 | 0.983 |

| 4 | 0.603 | 0.598 | 0.71 | 0.16 | 0.04 | 0.203 | 0.44 | 0.81 | 0.86 | 0.83 | 0.79 | 0.2 | 0.07 | 0.12 | 0.647 | 0.98 |

| 5 | 0.92 | 0.83 | 0.88 | 0.243 | 0.143 | 0.24 | 0.57 | 0.81 | 0.997 | 0.9 | 0.85 | 0.347 | 0.193 | 0.397 | 0.797 | 0.98 |

| 0.697 | 0.88 | 0.9 | 0.12 | 0.093 | 0.11 | 0.327 | 0.86 | 0.923 | 0.93 | 0.98 | 0.16 | 0.15 | 0.15 | 0.563 | 0.94 | |

| 0.463 | 0.54 | 0.69 | 0.137 | 0.107 | 0.133 | 0.273 | 0.85 | 0.81 | 0.79 | 0.87 | 0.193 | 0.203 | 0.223 | 0.483 | 0.96 | |

| 1 | 0.477 | 0.532 | 0.48 | 0.173 | 0.04 | 0.08 | 0.52 | 0.87 | 0.857 | 0.86 | 0.86 | 0.137 | 0.03 | 0.1 | 0.75 | 0.96 |

| 2 | 0.51 | 0.58 | 0.49 | 0.297 | 0.082 | 0.092 | 0.385 | 0.88 | 0.918 | 0.9 | 0.94 | 0.24 | 0.06 | 0.047 | 0.838 | 0.99 |

| 3 | 0.657 | 0.66 | 0.65 | 0.24 | 0.05 | 0.083 | 0.61 | 0.93 | 0.96 | 0.98 | 0.93 | 0.17 | 0.24 | 0.113 | 0.95 | 0.97 |

| 4 | 0.84 | 0.8 | 0.798 | 0.23 | 0.043 | 0.143 | 0.773 | 0.91 | 0.987 | 0.97 | 0.976 | 0.293 | 0.053 | 0.19 | 0.97 | 0.97 |

| 5 | 0.963 | 0.93 | 0.95 | 0.297 | 0.127 | 0.263 | 0.87 | 0.91 | 0.983 | 0.97 | 0.964 | 0.523 | 0.24 | 0.478 | 0.994 | 0.96 |

| 0.847 | 0.89 | 0.94 | 0.147 | 0.087 | 0.103 | 0.67 | 0.88 | 0.95 | 0.96 | 0.98 | 0.13 | 0.09 | 0.133 | 0.963 | 0.95 | |

| 0.69 | 0.79 | 0.88 | 0.14 | 0.13 | 0.217 | 0.383 | 0.91 | 0.953 | 0.99 | 0.978 | 0.3 | 0.313 | 0.383 | 0.823 | 0.943 | |

B.2 Performance of forecasting for locally stationary time series

In this subsection, we study the prediction accuracy of our proposed adaptive sieve forecast (4.5) by comparing it with some state-of-the-art methods. Specifically, we compare with the Tapered Yule-Walker estimate (TTVAR) in [55], the non-decimated wavelet estimate (LSW) in [32], the model switching method (SNSTS) in [36], the best linear prediction using all the previous samples (SBLP) 111The prediction is based on the stationary assumption and an ARMA model., the best linear prediction using recent samples (PBLP) and our adaptive sieve forecast (4.5) (Sieve). We implement TTVAR with constant taper function and the bandwidth is selected according to [55, Corollary 4.2]. For the wavelet method, we use the matlab codes from the first author’s website (see http://stats.lse.ac.uk/fryzlewicz/flsw/flsw.html) and for the model switching method, we use the R package forecastSNSTS. For our sieve method, we use the orthogonal wavelets (I.2) with Daubechies-9 wavelet and the data-driven approach described in Section E to choose and

In Table B.5, we record the mean square error over 1,000 simulations for one-step ahead prediction of the models 1-5 in Section B.1 with the coefficients chosen according to (5.2). Here we choose for models 1-2 and for models 3-5. It can be seen that our proposed method outperforms the other methods in literature for five models in both sample sizes and . The forecasting accuracy improvement is more significant for non-AR type models such as the MA and bilinear models.

| Model | TTVAR | LSW | SNSTS | SBLP | PBLP | Sieve | Improvement |

|---|---|---|---|---|---|---|---|

| =256 | |||||||

| 1 | 0.24 | 0.21 | 0.45 | 0.284 | 0.24 | 0.189 | 10 |

| 2 | 0.28 | 0.27 | 0.28 | 0.273 | 0.283 | 0.22 | 18.5 |

| 3 | 0.21 | 0.185 | 0.198 | 0.241 | 0.194 | 0.178 | 3.8 |

| 4 | 0.207 | 0.195 | 0.2 | 0.247 | 0.199 | 0.187 | 4.1 |

| 5 | 0.22 | 0.22 | 0.24 | 0.246 | 0.273 | 0.176 | 20 |

| =512 | |||||||

| 1 | 0.21 | 0.2 | 0.2 | 0.233 | 0.209 | 0.181 | 9.5 |

| 2 | 0.26 | 0.26 | 0.264 | 0.276 | 0.283 | 0.196 | 24.62 |

| 3 | 0.207 | 0.183 | 0.192 | 0.213 | 0.194 | 0.18 | 1.7 |

| 4 | 0.205 | 0.175 | 0.188 | 0.211 | 0.181 | 0.17 | 2.86 |

| 5 | 0.23 | 0.21 | 0.24 | 0.23 | 0.22 | 0.183 | 12.86 |

Before concluding this subsection, we compare the (rolling) forecasting performance of the aforementioned different methods for the real application (i.e., the stock return data of the Nigerian Breweries Plc.) in Section 6. Especially, we use the time series 2008-2014 as the training dataset to study the prediction performance over the first month of 2015. We employ the data-driven approach from Section E to choose the parameters and we obtain that and The MSE is for our proposed Sieve prediction (4.5). We compare this result with the other methods and record the results in Table B.6. We find that our prediction performs better than the other methods. Especially, we get a improvement compared to simply fitting a stationary model using all the time series from 2008 to 2014.

| Method | Sieve | TTVAR | LSW | SNSTS | SBLP | PBLP |

| MSE | 0.189 | 0.198 | 0.198 | 0.202 | 0.239 | 0.249 |

Finally, we make a comment on our proposed method with the model choice methodology proposed by [36], where one of two competing approaches was chosen based on its empirical, finite-sample performance with respect to forecasting in terms of the empirical mean squared prediction error (MSPE). The two competing approaches are: a stationary AR() prediction model and a time-varying AR() model. For the stationary AR() model, the paper estimated the coefficients using the standard Yule-Walker equation, and for the time-varying AR() model, the paper used the stationary method on short overlapping segments of the time series as in [16]. Our method utilizes all the data points and [36] only uses the most recent data points via segmentation. In practice, the data generating mechanism can be complicated so that the stationary period can be very short. Therefore, the segmentation approach could be misleading. In fact, based on our simulations and data analysis, we see improvements in all the simulations and real data analysis. In this regard, for the estimation of the time-varying AR model of [36], we suggest using our proposed optimal sieve prediction instead of the segment based estimator.

B.3 Discussion on the robustness of the choices of parameters

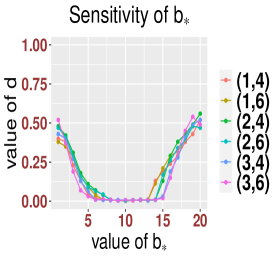

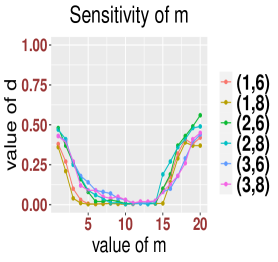

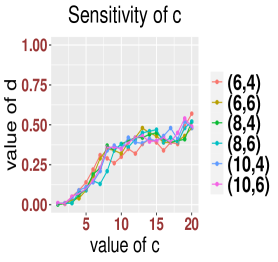

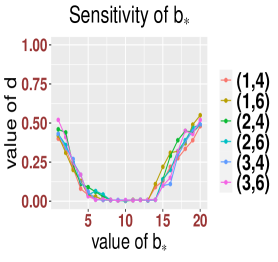

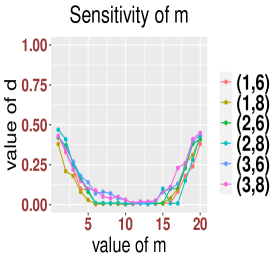

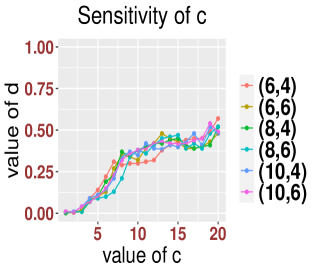

In this subsection, we use Monte-Carlo simulations to conduct sensitivity analysis to our proposed statistics and the multiplier bootstrap procedure. Especially, we will examine the robustness of the key hyperparameters and In what follows, we focus on reporting the results of Models 2 and 5 as in Section B.1. In fact, we also conducted simulations for the AR type Models 1,3 and 4, the results and discussions are similar. Due to space constraint, we will not report these results here.

First, we examine the sensitivity of the hyperparameters to the simulated type I error under the null hypothesis (5.1). As concluded in Section 5.1, the performance of different basis functions are similar in general. Hence, for ease of discussion, we use the Fourier basis functions in the following simulations. Moreover, we use the sample size and focus on the type I error For other simulation settings (e.g., or ), the results are similar and we will not present the detail to avoid distraction.

In order to have a through understanding of the impact of all three parameters, we discuss a wide range of all three parameters so that

Then for each chosen triplet we apply our proposed multiplier bootstrap procedure Algorithm 1 to obtain the simulated type I error For comparison, for each triplet, we consider the discrepancy between the true type error and the simulated type I error

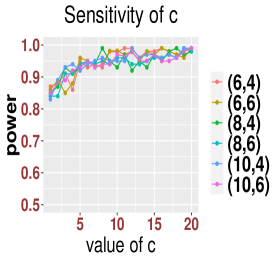

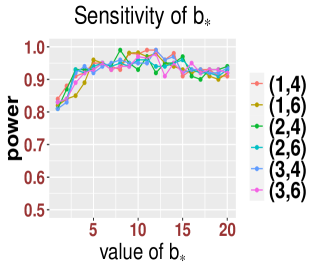

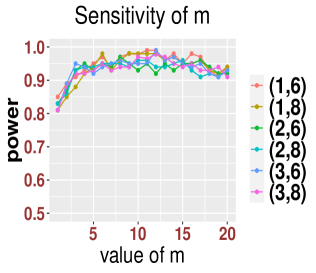

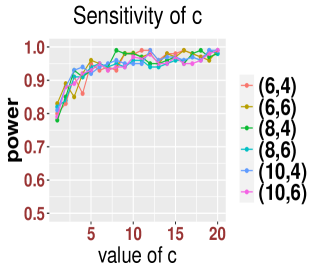

In order to visualize how the values of change with each of the parameters, we discuss them one by one by fixing the rest two of the parameters. The results are recorded in Figure B.1 for Model 2 and in Figure B.2 for Model 5. Based on the simulations, we see that the performance is overall robust against the choices of the parameters. Especially, we observe a U curve for and , and the choices of these two parameters are quite flexible. For example, and can result in accurate testings. Moreover, we also observe that our results are more sensitive to the value of . Under the null hypothesis (5.1) (i.e., ), we should choose a smaller value of like This range is much narrower than those of and We emphasize that our proposed data-driven procedure in Section E can successfully provide a triplet lying in the range of these hyperparameters which can result in accurate testings. For example, our data-driven procedure will select for Model 2 and for Model 5 which match our sensitivity analysis.

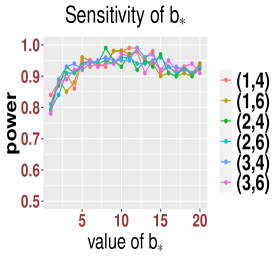

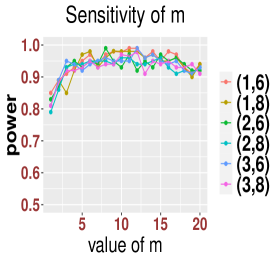

Second, we examine the sensitivity of the hyperparameters to the simulated power under the alternative hypothesis (5.2) with for Model 2 and for Model 5. We mention that other values of have similar performance and we will not report such results. Analogous to the findings for type I error, we see that the performance is overall robust against the choices of the parameters in terms of power. Especially, we observe an upside down U curve for and , and the choices of these two parameters are quite flexible. For example, and can result in accurate testings. We mention that the U shape is not as clear as that in the type I error analysis. The main reason is because it is very likely that larger values of and will result in larger errors so that the testing statistic will be in favor of rejecting. Moreover, we also observe that our results are more sensitive to the value of . Under the alternative (5.2) (i.e., ), we should choose that We also observe that no U curve exists for . The main reason is that a larger value of will increase the estimation error significantly. Therefore, the value of the test statistics will be much larger so that it will reject the null hypothesis. We emphasize that our proposed data-driven procedure in Section E can successfully provide a triplet lying in the range of these hyperparameters which can result in accurate and powerful testings. For example, our data-driven procedure will select for Model 2 and for Model 5 which match our sensitivity analysis.

B.4 Examination for roots of AR polynomials: additional simulation setting

In this section, we consider some additional simulations using the locally stationary AR(2) considered by Dahlhaus in [13]. Especially, Dahlhaus considered the model that

| (B.1) |

where are i.i.d. Gaussian random variables with variance and

| (B.2) |

It was shown in Section 6 of [13] that for the above AR(2) model, when is fixed, the roots of the AR(2) characteristics polynomials are complex number so that

Note that the AR polynomial of the above model has complex roots and these roots are rather close to the unit circle.