Pricing European Options under Stochastic Volatility Models:

Case of five-Parameter Variance-Gamma Process

Abstract.

The paper builds a Variance-Gamma (VG) model with five parameters: location (), symmetry (), volatility (), shape (), and scale (); and studies its application to the pricing of European options. The results of our analysis show that the five-parameter VG model is a stochastic volatility model with a Ornstein–Uhlenbeck type process; the associated Lévy density of the VG model is a KoBoL family of order , intensity , and steepness parameters and ; and the VG process converges asymptotically in distribution to a Lévy process driven by a normal distribution with mean and variance . The data used for empirical analysis were obtained by fitting the five-parameter Variance-Gamma (VG) model to the underlying distribution of the daily SPY ETF data. Regarding the application of the five-parameter VG model, the twelve-point rule Composite Newton–Cotes Quadrature and Fractional Fast Fourier (FRFT) algorithms were implemented to compute the European option price. Compared to the Black–Scholes (BS) model, empirical evidence shows that the VG option price is underpriced for out-of-the-money (OTM) options and overpriced for in-the-money (ITM) options. Both models produce almost the same option pricing results for deep out-of-the-money (OTM) and deep-in-the-money (ITM) options..

Key words and phrases:

stochastic volatility, Lévy process, Ornstein-Uhlenbeck process, infinitely divisible distributions, Variance-Gamma (VG) model, function characteristic, Esscher transform1. Introduction

Black-Scholes (BS) model [12] is considered the cornerstone of option pricing theory. The model relies on the fundamental assumption that the asset returns have a normal distribution with a known mean and variance. However, based on empirical studies, the Black-Scholes (BS) model is inconsistent with a set of well-established stylized features [15]. Due to the subsequent development of the option pricing theory, a new class of models has emerged in the literature to address the stylized characteristics of the markets. The probabilistic property of infinity divisibility is the main characteristic of these new models, and they belong to the family of Levy processes [23].

The new class of models can be divided into two subclasses of Jump-Diffusion models and Stochastic Volatility models. The Jump-Diffusion process is modeled as an independent Brownian motion plus a Compound Poisson Process. The popular models in the literature are Merton’s jump-diffusion model [27] and Kou’s jump-diffusion model [22], where logarithmic jump size follows a normal distribution and an asymmetric double exponential distribution respectively. The stochastic volatility (SV) model is another extension of the standard geometric Brownian motion (GBM) model, where the observed volatility is modeled as a stochastic process. In a stochastic volatility framework [2], the constant volatility () in a standard geometric Brownian motion (GBM) model is replaced by a deterministic function of a stochastic process () where represents the solution of the stochastic differential equation (SDE). We have two main types of SV models in the literature: Diffusion based SV models and non-Gaussian Ornstein-Uhlenbeck-based SV models. In the popular diffusion-based SV models, follows a Cox-Ingersoll-Ross(CIR) process [17] or a Log-normal process [18] and the deterministic function is a squared root of the stochastic process (). The non-Gaussian Ornstein-Uhlenbeck-based SV models have been introduced and thoroughly studied in [10, 11, 6, 7]. The SV model with the Ornstein-Uhlenbeck type process is mathematically tractable and has many appealing features.

From the perspective of derivative asset analysis, we will build a five-parameter VG model as a Stochastic volatility model with Ornstein-Uhlenbeck type process. While there is a great number of studies on option pricing under the VG Model, most of the VG Model in the literature has three parameters [24, 28, 25, 1], certainly due to technical issues of fitting a high parametric model to the marginal distribution of asset returns. The amount of literature considering the VG Model with five parameters is rather limited. Using the five-parameter Variance-Gamma model as an underlying distribution of the European option will allow controlling both the excess kurtosis and the skewness of the underlying data. In the option pricing theory, the challenge is often the existence of the Equivalent Martingale Measure (EMM) and whether it preserves the structure of the Variance-Gamma measure. The Variance-Gamma (VG) process is not a Gaussian process, and the market is incomplete; therefore, the Equivalent Martingale Measure is not unique. The Esscher transform of the historical measure is considered optimal with respect to some optimization criterion [13]. The Esscher martingale measure was shown [3] to coincide with the minimal entropy martingale measure for Lévy processes.

The remainder of this paper is organized as follows. Section 2 is devoted to building a five-parameter VG process and presenting parameter estimations and simulations of the VG process. Section 3 investigates the Lévy density and the asymptotic distribution of the VG process. And section 4 extends the Black-Scholes framework, provides the integral representation for the option price, and computes the VG option price numerically.

2. Variance - Gamma Process: Stochastic Volatility Model

2.1. Lévy Framework and Asset Pricing

Let be a filtered probability space, with and is a filtration. is a -algebra included in and for , .

A stochastic process is a Lévy process, if it has the following properties

(L1): a.s;

(L2): has independent increments, that is, for , the random variables , , …, are independent;

(L3): has stationary increments, that is,

for any , the probability distribution of depends only on ;

(L4): is stochastically continuous: for any and , ;

(L5): paths, that is, is a.s right continuous with left limits

Given a Lévy process on the filtered probability space , we define the asset value process such as .

Theorem 2.1

(Lévy-Khintchine representation)

Let be a Lévy process on . Then the characteristic exponent admits the following representation.

| (2.1) |

where , and is a -finite measure called the Lévy measure of Y, satisfying the property

For the Theorem-proof, see [4, 20, 36]

Each Lévy process is uniquely determined by the Lévy–Khintchine triplet . The terms of this triplet suggest that a Lévy process can be seen as having three independent components: a linear drift, a Brownian motion, and a Lévy jump process. When the diffusion term , we have a Lévy jump process; in addition, if , we have a pure jump process.

2.2. Ornstein-Uhlenbeck proces

The Ornstein-Uhlenbeck process is a diffusion process introduced by Ornstein and Uhlenbeck [37] to model the stochastic behavior of the velocity of a particle undergoing Brownian motion. The Ornstein-Uhlenbeck diffusion is the solution of the Langevin Stochastic Differential Equation (SDE) (2.2)

| (2.2) |

where and is a Brownian motion. In recent years, the Ornstein-Uhlenbeck process has been used in finance to capture important distributional deviations from Gaussianity and to model dependence structures. The extension of the Ornstein-Uhlenbeck processes was obtained by replacing the Brownian motion in (2.2) by z(t), a background driving Lévy process (BDLP) [11, 8, 10]. The SDE (2.2) becomes

| (2.3) |

where the process is subordinator; a process with non-negative, independent and stationary increments, which implies . Correspondingly z(t) moves up entirely by jumps and then tails off exponentially [7].

Lemma 2.2

The general form of the stationary process , solution of (2.3) is given by :

| (2.4) |

Proof.

Expression (2.5) can be written as follows:

| (2.7) |

Theorem 2.3

Assume is a compound poison process, that is, N(t) is Poisson process with the instantaneous rate , and follows an exponential distribution with the rate .

The stationary marginal distribution of is Gamma distribution

Proof.

| (2.8) |

The stationary solution of (2.3) can be written as in (2.8). Because of the stationarity, we have

| (2.9) |

is the characteristic function of the stationary distribution of and is the characteristic function of . We have for , and the relation (2.8) shows that is self-decomposable.

is a compound poison process with the function characteristic.

| (2.10) |

It was shown in [6] that can be expressed as follows

| (2.11) |

By replacing, , we have

| (2.12) |

is continuous at zero, and we have:

| (2.13) |

From (2.13), is the function characteristics of the gamma distribution; and the stationary marginal distribution of is the Gamma distribution.

Another method developed in [7, 9, 11, 8, 10] uses the relationship between the Lévy density and the Lévy density of .

| (2.14) |

From (2.10), we have the Lévy density and the Lévy density of can be deduced as follows.

| (2.15) |

u(x) is the Lévy density of Gamma distribution . ∎

We can integrate the stationary non-negative process .

| (2.16) |

By integration by part method, (2.16) becomes

| (2.17) | ||||

| (2.18) |

It results from (2.18) that the process is continuous as and co-break [10, 9]. In addition, the shape of is determined by . In fact, and co-integrate. The co-integration can be shown by transforming the equation (2.18) into (2.19). is a stationary process such that.

| (2.19) |

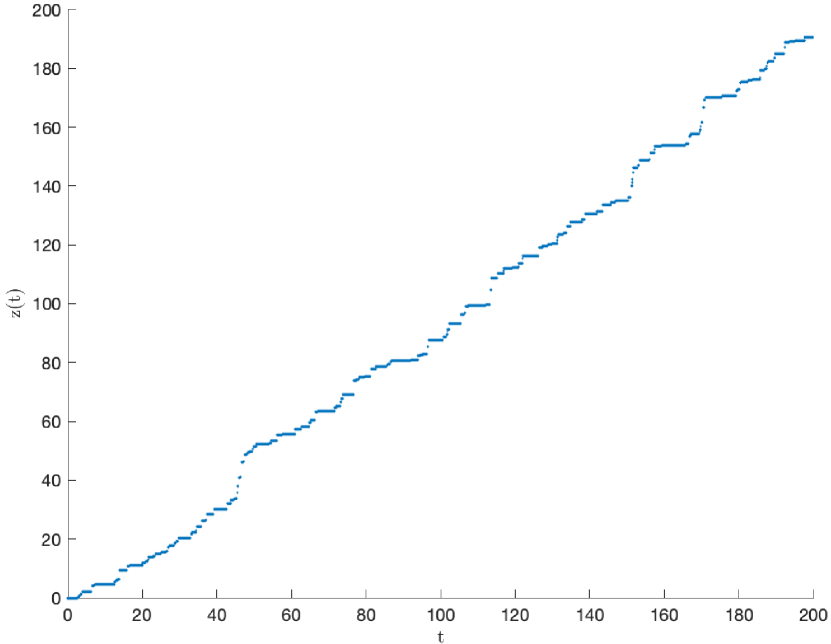

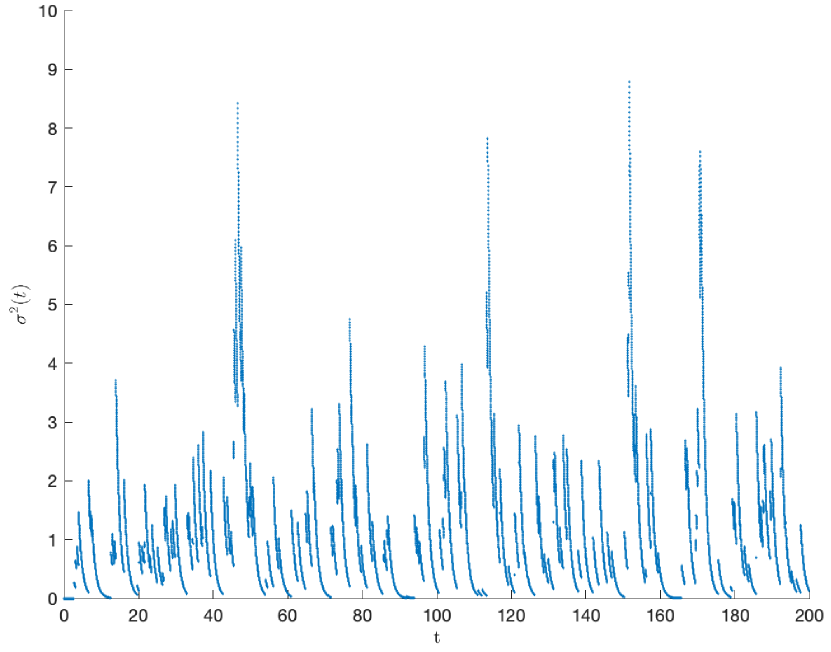

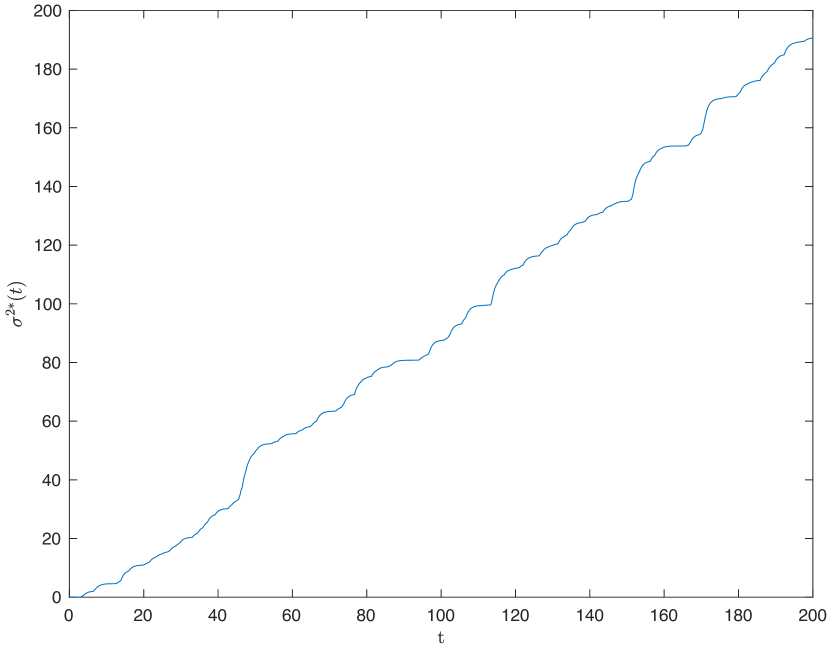

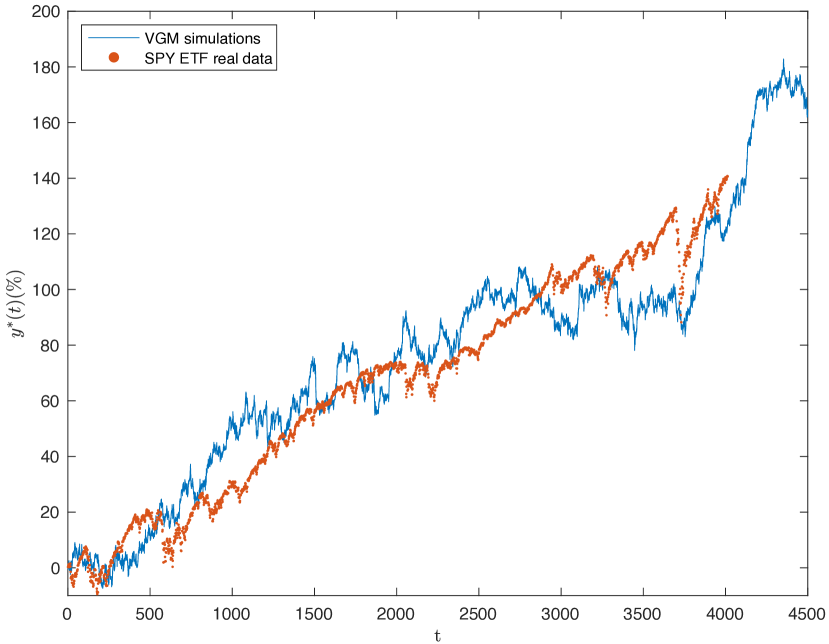

For and , the compound poison process (), the Ornstein-Uhlenbeck process in (), and in (2.20) were simulated and the results are in Fig 1(a), Fig 1(b), and Fig 1(c) respectively.

| (2.20) |

The estimations of the gamma distribution parameter were performed by the FRFT Maximum likelihood on the daily SPY prices [31].

2.3. Variance - Gamma Process: Semi-Martingale

Let , a stochastic process used to model the log of an asset price.

| (2.21) | ||||

| (2.22) |

where and are the drift parameters, represents the continuous time clock, and is the standard Brownian motion and independent of .

| (2.23) |

is the spot or instantaneous volatility, and is the chronometer or the integrated variance of the process. As shown in Fig 1(c), the Gamma process () is a strictly increasing process of the stationary process ().

The mean process is a predictable process with locally bounded variation. In fact, is continuous and differentiable because of .

is a local martingale. The derivative of in (2.22) can be written as a Stochastic Differential Equation (SDE) (2.24)

| (2.24) |

is a special semi-martingale [35, 10] and the decomposition is unique.

2.4. Variance - Gamma Process: Parameter Estimations

The stochastic process in (2.21) is the solution of the following Stochastic Differential Equation (SDE):

| (2.25) |

Given an interval of length , we define and over the interval [; ].

| (2.26) |

The volatility component can be transformed into a normally distributed variable as follows:

| (2.27) | ||||

where and denotes a standard normal distribution.

By integrating the instantaneous return rate (2.25) per component, we have:

Based on (2.26) and (2.27), we have the following equation over the interval [; ]

| (2.28) |

In case is a daily length, becomes the daily return rate. The equation (2.28) was analyzed in [31, 32] as a daily return rate, and the parameters were estimated. The data came from the daily SPY ETF historical data and the period spans from January 4, 2010, to December 30, 2020. See [31, 32, 34] for more details on the methodology and the results.

Table 1 presents the estimation results of the five parameters of in (2.28) along with some statistical indicators.

| Model | Parameters | Statistics |

|---|---|---|

| VG | ||

| Source: Nzokem(2021) [31, 32] |

As shown in Table 2, with initial parameter values (, ), the maximization procedure convergences after 21 iterations. is the function to maximize and is the norm of the partial derivative function (). During the maximization process, both quantities converge respectively to and ; where the parameter vector is stable. The location parameter is positive, the symmetric parameter is negative, and other parameters have the expected sign.

| Iterations | |||||||

|---|---|---|---|---|---|---|---|

| 1 | 0 | 0 | 1 | 1 | 1 | -3582.8388 | 598.743231 |

| 2 | 0.05905599 | -0.0009445 | 1.03195903 | 0.9130208 | 1.03208412 | -3561.5099 | 833.530396 |

| 3 | 0.06949925 | 0.00400035 | 1.04101444 | 0.88478895 | 1.05131996 | -3559.5656 | 447.807305 |

| 4 | 0.07514039 | 0.00055771 | 1.17577397 | 0.67326429 | 1.17778666 | -3569.6221 | 211.365781 |

| 5 | 0.08928373 | -0.0263716 | 1.03756321 | 0.83842661 | 0.94304967 | -3554.4434 | 498.289445 |

| 6 | 0.08676498 | -0.0521887 | 1.03337015 | 0.85591875 | 0.95066351 | -3550.6419 | 204.467192 |

| 7 | 0.086995 | -0.0608517 | 1.02788937 | 0.87382621 | 0.95054954 | -3549.8465 | 66.8039738 |

| 8 | 0.08542912 | -0.058547 | 1.02705241 | 0.88258411 | 0.94321299 | -3549.7023 | 15.3209117 |

| 9 | 0.08478622 | -0.0576654 | 1.02995166 | 0.88447791 | 0.93670036 | -3549.6921 | 1.14764198 |

| 10 | 0.08477798 | -0.0577736 | 1.02922308 | 0.88449072 | 0.93831041 | -3549.692 | 0.17287708 |

| 11 | 0.08476475 | -0.0577271 | 1.02960343 | 0.88450434 | 0.93755549 | -3549.692 | 0.07850459 |

| 12 | 0.08477094 | -0.0577488 | 1.02942608 | 0.8844984 | 0.93790784 | -3549.692 | 0.03723941 |

| 13 | 0.08476804 | -0.0577386 | 1.02950937 | 0.88450117 | 0.93774266 | -3549.692 | 0.01732146 |

| 14 | 0.0847694 | -0.0577434 | 1.02947043 | 0.88449987 | 0.93781995 | -3549.692 | 0.00813465 |

| 15 | 0.08476876 | -0.0577411 | 1.02948868 | 0.88450048 | 0.93778375 | -3549.692 | 0.00380345 |

| 16 | 0.08476906 | -0.0577422 | 1.02948014 | 0.88450019 | 0.9378007 | -3549.692 | 0.00178206 |

| 17 | 0.08476892 | -0.0577417 | 1.02948414 | 0.88450033 | 0.93779276 | -3549.692 | 0.00083415 |

| 18 | 0.08476898 | -0.0577419 | 1.02948226 | 0.88450026 | 0.93779648 | -3549.692 | 0.00039063 |

| 19 | 0.08476895 | -0.0577418 | 1.02948314 | 0.88450029 | 0.93779474 | -3549.692 | 0.00018289 |

| 20 | 0.08476897 | -0.0577419 | 1.02948273 | 0.88450028 | 0.93779555 | -3549.692 | 8.56E-05 |

| 21 | 0.08476896 | -0.0577418 | 1.02948292 | 0.88450029 | 0.93779517 | -3549.692 | 4.01E-05 |

3. Variance - Gamma Process: Probability versus Lévy Density

Based on (2.21) and (2.22), the VG Process with five parameters can be written as follows:

| (3.1) |

where , , , , represents the continuous time clock, and is the standard Brownian motion and independent of .

| (3.2) |

where is the spot or instantaneous volatility, is the spot or instantaneous variance, and is the chronometer or the integrated variance of the process.

We consider the characteristic function of the VG process

| (3.3) |

is the It integral with respect to the Brownian motion, and we have :

| (3.4) |

where is a standard normal distribution.

From expressions (3.3) and (3.4), we have

| (3.5) | ||||

is a Lévy process generated by the Gamma distribution and we have

| (3.6) | ||||

From expressions (3.3), (3.5) and (3.6), we have

| (3.7) |

We define two related functions and such that

| (3.8) |

The characteristic function can be written as follows.

| (3.9) |

3.0.1. Lévy measure and the structure of the jumps

Lemma 3.1

(Frullani integral) and with .

we have

For lemma proof, see [5]

Theorem 3.2

(Variance-Gamma Model representation)

Let be a Lévy process on generated by the VG model with parameter . The characteristic exponent of the Lévy process has the following representation.

| (3.10) |

is the Lévy density of :

| (3.11) |

with

| (3.12) |

and satisfies the properties

| (3.13) |

Proof.

We consider the characteristic function in (3.8) of the VG model with parameter developed previously

We factor the quadratic function in the denominator of .

| (3.14) |

with

We apply the lemma 3.1 on each factor of the quadratic function (3.14).

we take into account the expression (3.14) and have

| (3.15) |

where

From expression (3.8), we have:

We have

| (3.16) |

For , we have the expression (3.10)

We can check some properties of

| (3.17) |

with

And we have:

| (3.18) |

∎

The results in (3.17) show that the VG process is not a finite activities process and can not be written as a Compound Poisson process [10]. The VG process is an infinite activity process with an infinite number of jumps in any given time interval. The arrival rate of jumps of all sizes in the VG process is defined by the Lévy density (3.19)

| (3.19) |

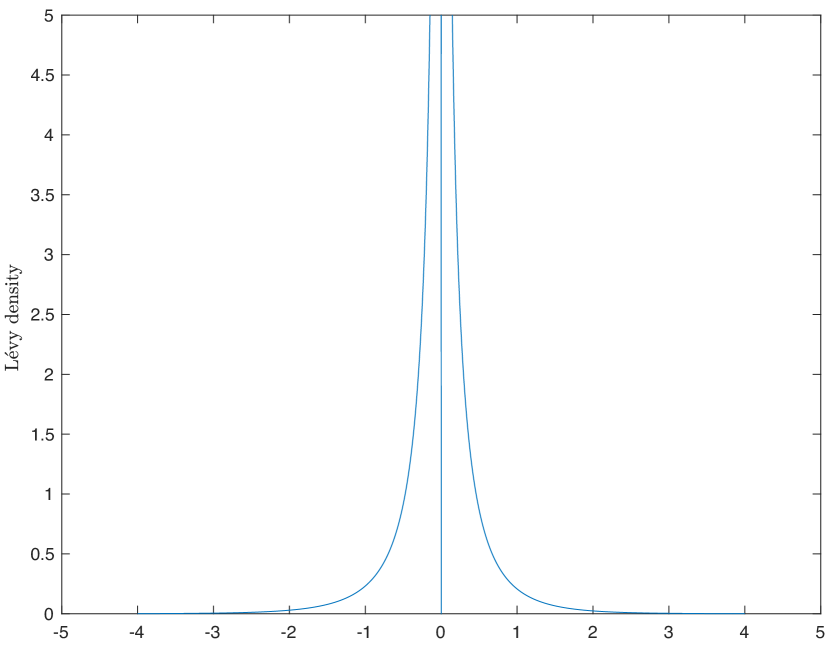

As shown in Fig 3(a), the high arrival rates of jumps are concentrated around the origin . The smaller the jump size, the higher the arrival rate for the VG model. The steepness parameters [13], and , defined the rate of exponential decay of the tails on each side. As shown in Fig 3(a) and (3.19), the Lévy density is asymmetric, and the left tail is heavier as . On the other hand, the result in (3.18) proves that the VG process is a finite variation process, which is contrary to the Brownian motion process. The Gamma distribution Parameter (), called the process intensity [13], plays an important role in the Lévy density. The intensity of the process has a similar role as the variance parameter in the Brownian motion process. The Lévy density function (3.19) is different for negative and positive jump size. The difference has led [25] to see the VG process as the difference between two increasing processes, with one process providing the upward movement and another the downward movement in the market.

Using the VG parameter estimations in table 1, we have and . Fig 3(a) and Fig 3(b) display the Lévy and the probability densities. As shown in Fig 3, the shape of the density functions are different; even-though, both densities are linked by the same characteristic function.

Variance-Gamma (VG) Process can be described as a subfamily of the KoBoL family, which is the extension of Koponen’s family by Boyarchenko and Levendorskii [13]. The KoBoL family is also called CGMY- model (named after Carr, German, Madan, and Yor) [14]. Under the KoBoL family, the Lévy density has the following general form. See [13] for more details

| (3.20) |

where , , and

As a subfamily of the KoBoL family, the VG process belongs to the process class of order , intensity and steepness parameters and . For , see [30] for a general case of tempered stable distribution.

3.1. Variance - Gamma Process: Asymptotic distribution

Theorem 3.3

(Variance-Gamma process probability density)

Let be a Lévy process on generated by the VG model with parameter . The probability density function can be written as follows

| (3.21) |

Proof:.

in (3.16) provides the relation between the characteristic exponent and the Lévy density. the expression is used as follows:

| (3.22) |

Theorem 3.4

(Asymptotic distribution of Variance-Gamma process)

Let be a Lévy process on generated by the VG model with parameter .

Then converges in distribution to a Lévy process driving by a Normal distribution with mean and variance .

| (3.23) |

Proof:.

Let us have

is the characteristic function of the process , we use the expression (3.7).

is the characteristic function of the stochastic process and we have

Let us have

We can use the Taylor expansions of

The characteristic function, , developed previously becomes:

We have

| (3.24) |

By applying the limit in (3.24), we produce the cumulant-generating function [21] of the Normal distribution. We have the following convergence in distribution

∎

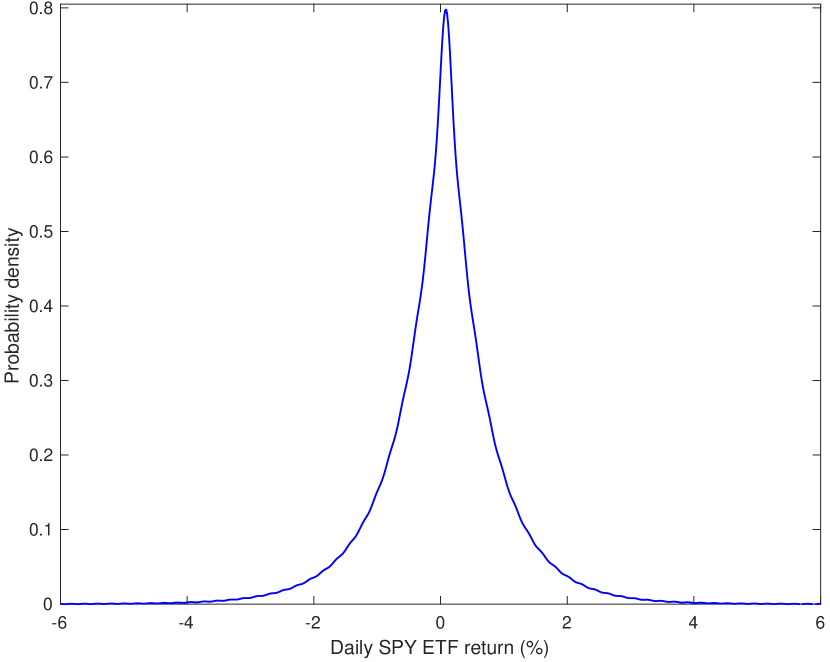

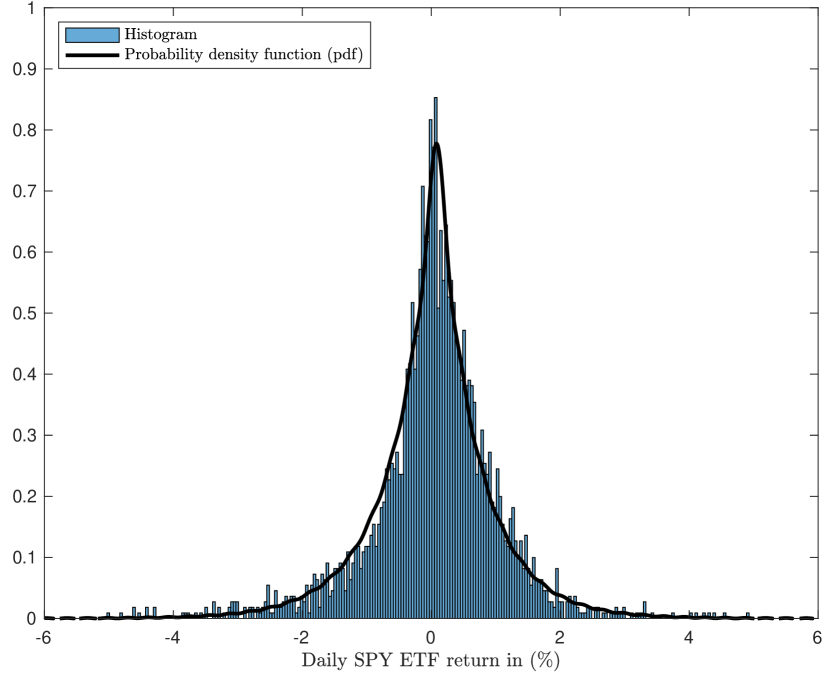

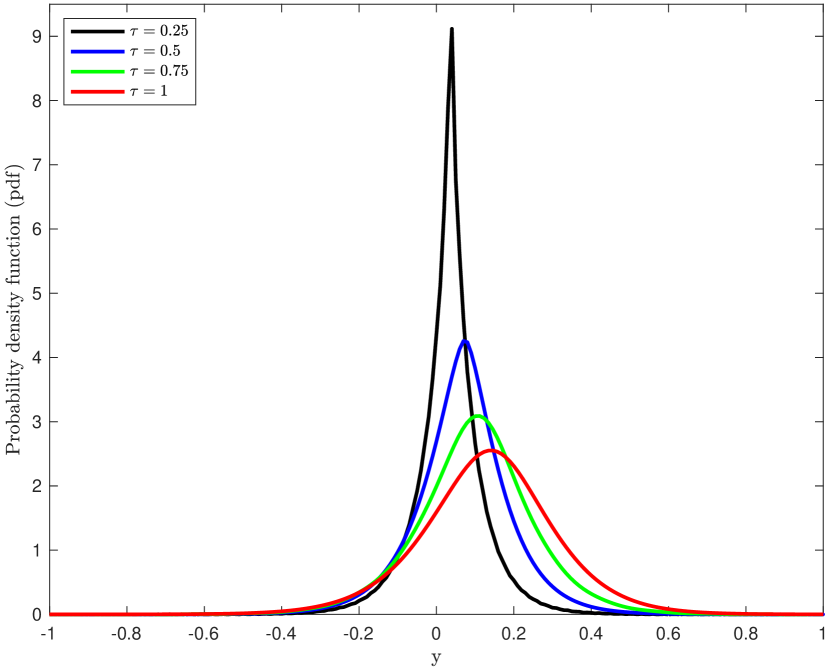

As shown in (3.22), the dynamic of the probability density is carried by two parameters: and . can be compared to the histogram of the daily SPY ETF return data, as shown in Fig 4(a). Fig 4(b) shows the shape of the probability densities (3.21) adjusted at different timeframes: Quarterly (), Semi-Annual (), Third-Quarterly (), and Annual ().

The discrepancy between the shape of the probability densities (3.21) can be explained by the Asymptotic distribution in Theorem 3.4. When the time frame becomes large, The VG probability density generated by the Lévy Process changes its nature and becomes a Normal distribution Process. Empirically, the convergence is illustrated in Fig 4(b).

4. Variance - Gamma Process: Pricing European Options

4.1. Variance - Gamma Process: Risk Neutral Esscher Measure

The method of Esscher transforms introduced by [16] as an efficient technique for pricing derivative securities if a Lévy process models the logarithms of the underlying asset prices. An Esscher transform of a stock-price process provides an equivalent martingale measure; under such measure, the price of any derivative security is calculated as the expectation of the discounted payoffs. In some cases, the Esscher transform of a distribution [16] remains in the family of the original distributions. In particular, Gamma, Exponential, Normal, Inverse Gaussian, Negative Binomial, Geometric, Poisson, and Compound Poisson distributions are examples of such conservative distributions. The existence of the equivalent Esscher transform measure is not always guaranteed, and the issue of the unicity of the equivalent martingale measure remains recurrent when pricing an option with a Lévy process.

From the characteristic function in (3.8), We have the Moment generating function of the VG model.

| (4.1) | ||||

Under the Esscher transform with parameter h, the probability density of becomes:

| (4.2) |

The Moment generating function of the Esscher transform VG model with

| (4.3) | ||||

with

| (4.4) | |||

is the modified probability density of defined in (3.21). The function is a strictly increasing function, and the probability measure generated by is equivalent to the original probability measure generated by . Both probability measures have the same null sets [16](sets of probability measure zero).

Given the process with the constant risk-free rate of interest. We look into the conditions to have such that

| (4.5) |

We have , with is the Variance - Gamma process. The equation (4.5) becomes

| (4.6) |

The first condition is that

The equation (4.6) is equivalent to (4.7).

| (4.7) |

We consider the function defined as follows

we have

| (4.8) |

(4.8) shows the existence and the unicity of in such that

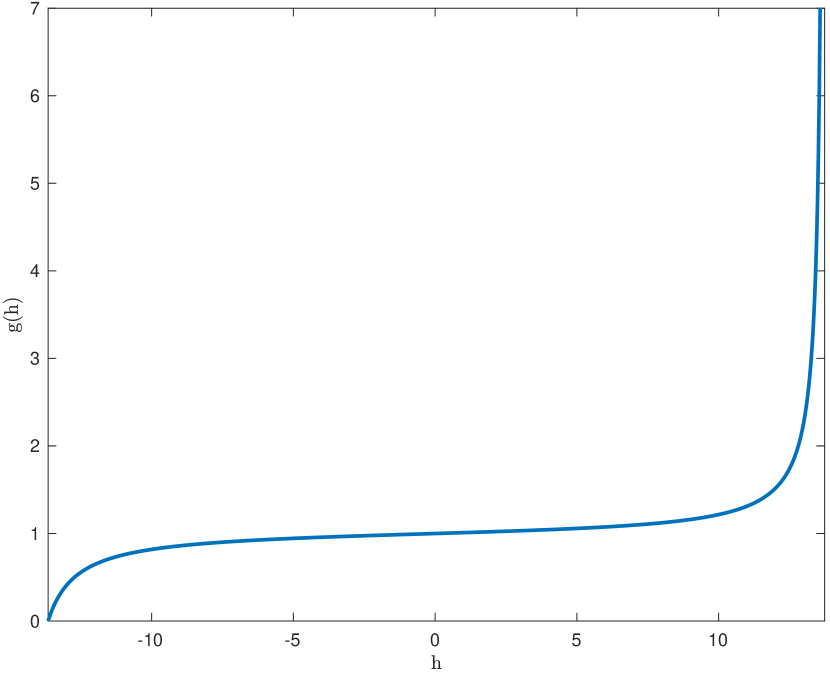

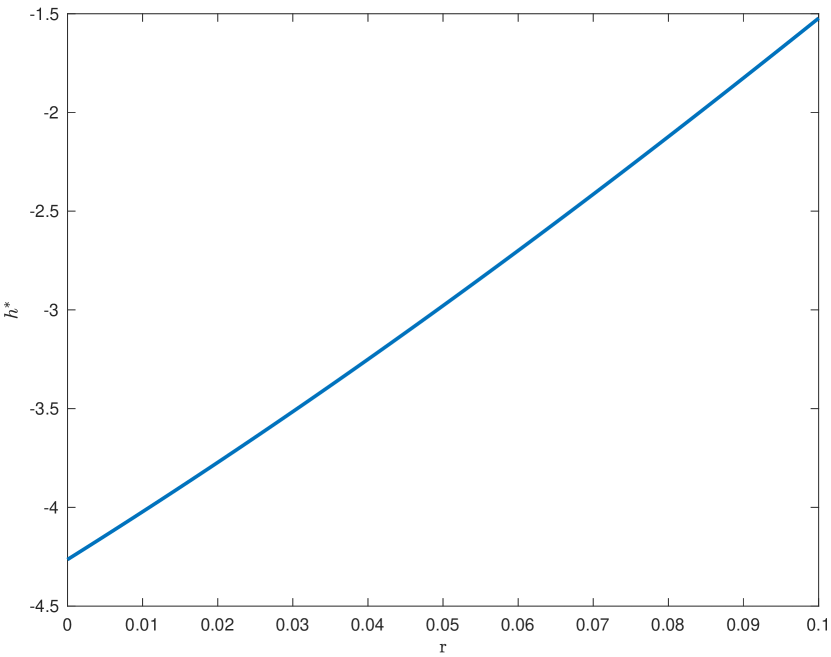

For VG Model in Table 1 [31, 32], the existence and unicity of can be studied empirically as shown in Fig 5. Over the interval , g(h) is an increasing function, as shown in Fig 5(a). Fig 5(b) provides the solution of equation (4.7) for free interest rate less than 10%. The solution increases with the free interest rate .

From the Esscher transform, we have the Equivalent Martingale Measure (EMM) , which can be written as the Radon-Nikodym derivative:

| (4.9) |

and for expectation with respect to

we have

| (4.10) |

Theorem 4.1

(Variance - Gamma Esscher transform distribution)

Esscher transform of Variance - Gamma process with parameter is also a Variance - Gamma process with parameter

| (4.11) |

Proof:.

From (4.4), we have

| (4.12) |

We can divide the denominator by the numerator of the function in (4.12) and rearrange the resulting expression.

| (4.13) |

in (4.4) becomes

| (4.14) |

Using the Esscher transform method, the moment generating function for Variance - Gamma process becomes:

| (4.15) |

We have a new Variance - Gamma process with parameter ∎

The Esscher transform method preserves the structure of the five-parameter VG process; it introduces an addition symmetric parameter () and inflates the Gamma scale parameter by factor.

4.2. Variance - Gamma Model: Extended Black-Scholes Formula

Corollary 4.2

(Extended Black-Scholes)

Let a continuously compounded risk-free rate of interest; , a VG Process with parameter ; and the terminal payoff for a contingent claim with the expiry date .

Then at time , the arbitrage price of the European call option with the strike price can be written as follows.

| (4.16) | ||||

| (4.17) |

where , and and are the cumulative distribution of VG Model with parameter and parameter respectively

Proof:.

Under the Equivalent Martingale Measure (EMM), is the probability density of VG model with parameter . We note

We can now show the relation in (4.16)

with

∎

From Theorem 3.3 and Theorem 4.1, is the probability density of the VG model with parameter .

| (4.18) |

Following the same methodology, is the probability density of the VG model with parameter . we have

| (4.19) |

In fact, as in (4.18), we have :

And

We have the expression of the probability density,

| (4.20) |

4.2.1. Equivalent Martingale Measure (EMM) Computation

Under the Equivalent Martingale Measure (EMM), is the probability density of VG model with parameter . The Fourier transform is:

| (4.21) |

and are, respectively, the Fourier Transform of the probability density and the characteristic exponent of the VG model with parameter

can be written as the inverse Fourier Transform from (4.21)

It was shown in [31] that we can have

| (4.22) |

Based on (4.22), we deduce

We have the probability density and cumulative functions

| (4.23) |

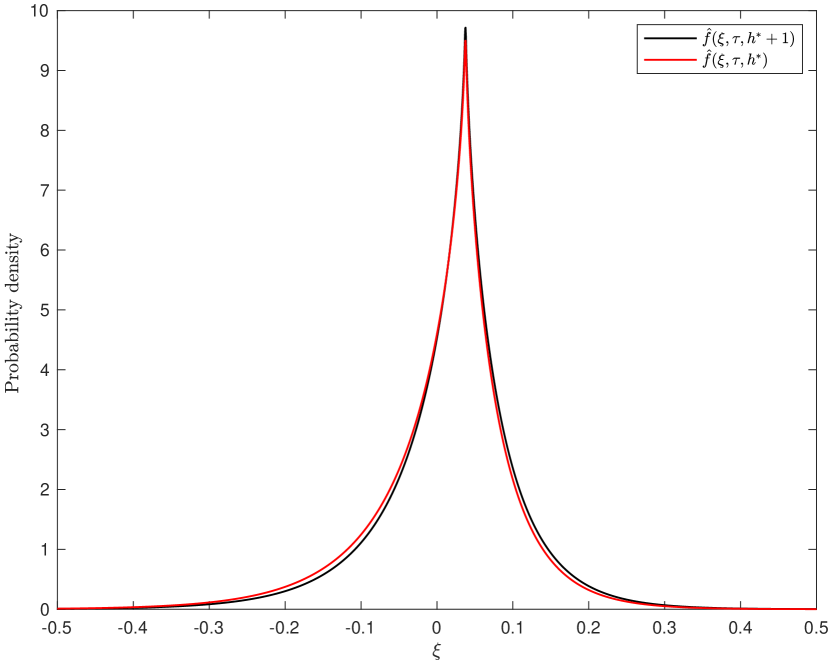

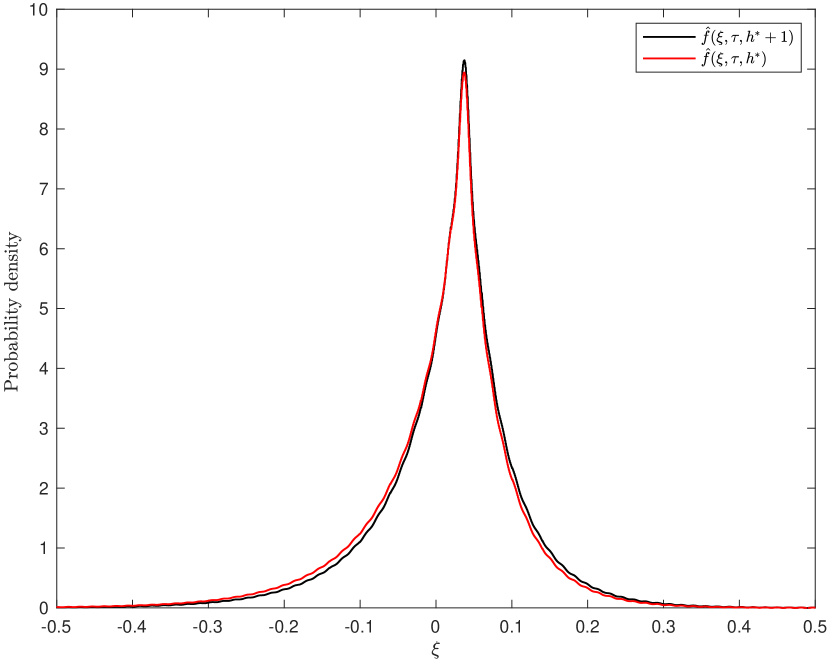

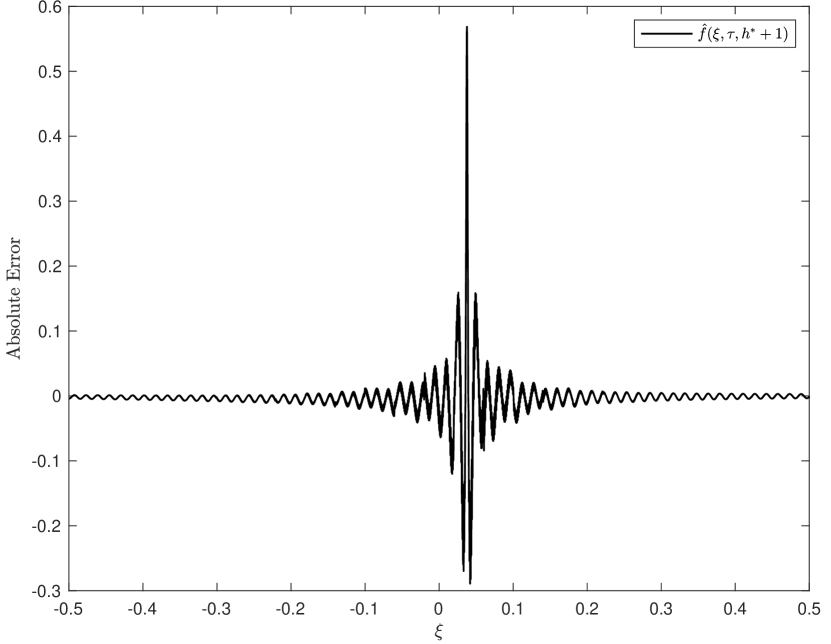

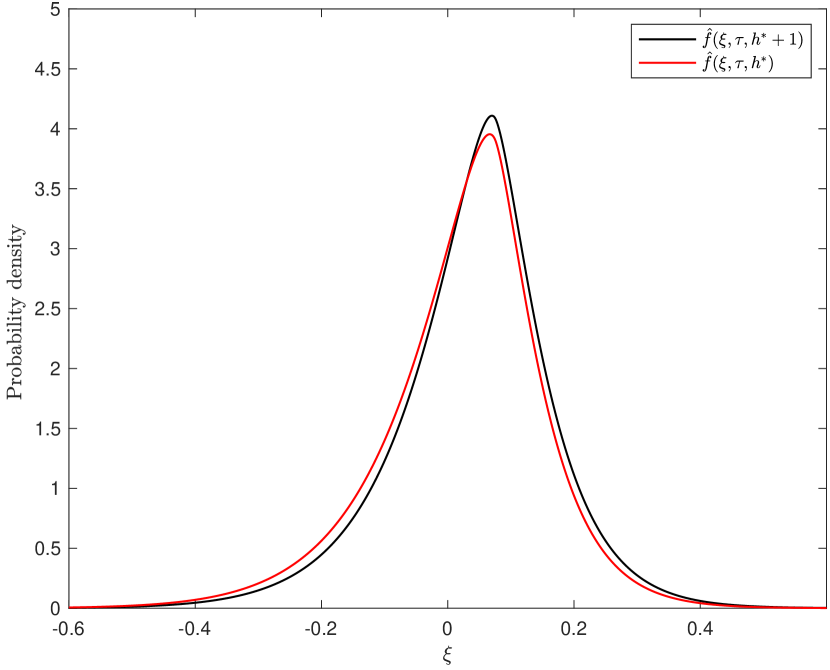

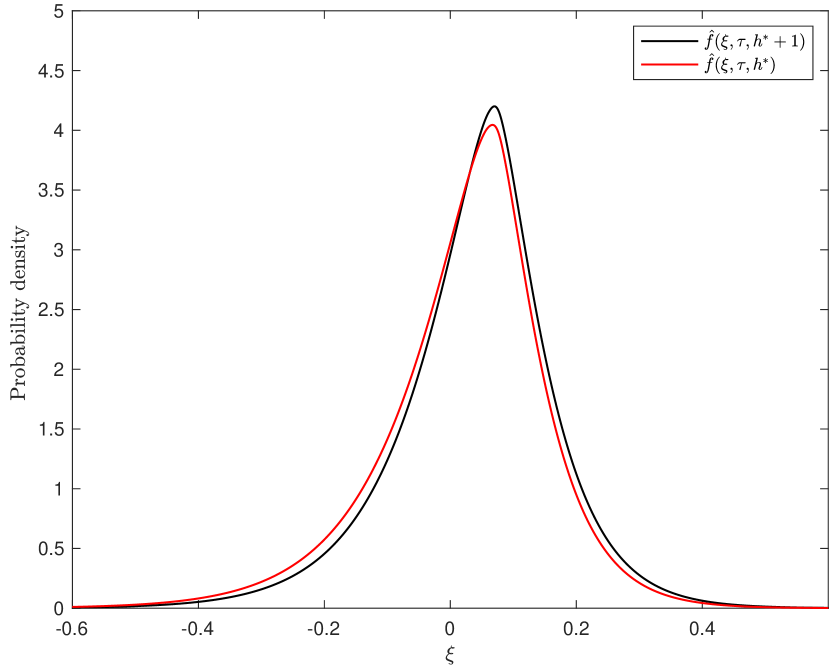

For VG Model in Table 1 [31, 32]: : , , , , ; and a risk-free rate of interest , we have a Esscher transform parameter in (4.6). and were computed by the Fractional Fast Fourier (FRFT) [31] as shown in Fig 6(b) and Fig 7(b).

Using the numerical integration technique, and were computed by implementing the following 12-point rule Composite Newton-Cotes Quadrature Formulas [33, 29].

| (4.24) | ||||

In order to compute (4.24) for and , the following parameter values are used: , , , , and the weights values come from Table 1 [33] and table 4.1 [29]. The results are shown in Fig 6(a) and Fig 7(a).

Both methods produce smooth density functions as shown in Fig 6 and Fig 7. Fig 6(c) and Fig 7(c) provide the estimation error of . The Fractional Fast Fourier (FRFT) underestimates the peakedness of the density function when the timeframe is small () in Fig 6(c). The estimation error decreases significantly when the timeframe increases. see Fig 7(c) when .

Both methods will be used to compute the arbitrage price of the European call option.

4.3. Variance - Gamma Model: Generalized Black-Scholes Formula

Theorem 4.3

Let a continuously compounded risk-free rate of interest, , a VG Process with parameter , and , the terminal payoff for a contingent claim with the expiry date . Then at time , the arbitrage price of the European call option with the strike price can be written as follows.

| (4.25) |

where is the characteristic exponent of VG model with parameter in (4.11), and .

Proof:.

| (4.26) | ||||

| (4.27) |

is the payoff of the call option. The Fourier transform can be written

We have the Fourier transform of call payoff

| (4.28) |

It is shown in (4.23) and in (4.21) that and can be written as follows

| (4.29) |

with (, ) defines in (4.11)

is the call function under the Equivalent Martingale Measure(EMM), and we can now find a good expression of the function

We have the formula (4.25)

| (4.30) |

∎

4.4. European Option Pricing by Fractional Fast Fourier (FRFT)

4.4.1. Parameter Evaluation

Let us considerate the stock or index price and the strike price ; it was shown in (4.28) that the Fourier transform of the call payoff can be written as follows.

We can recover the call payoff from the inverse of Fourier in (4.28)

| (4.31) |

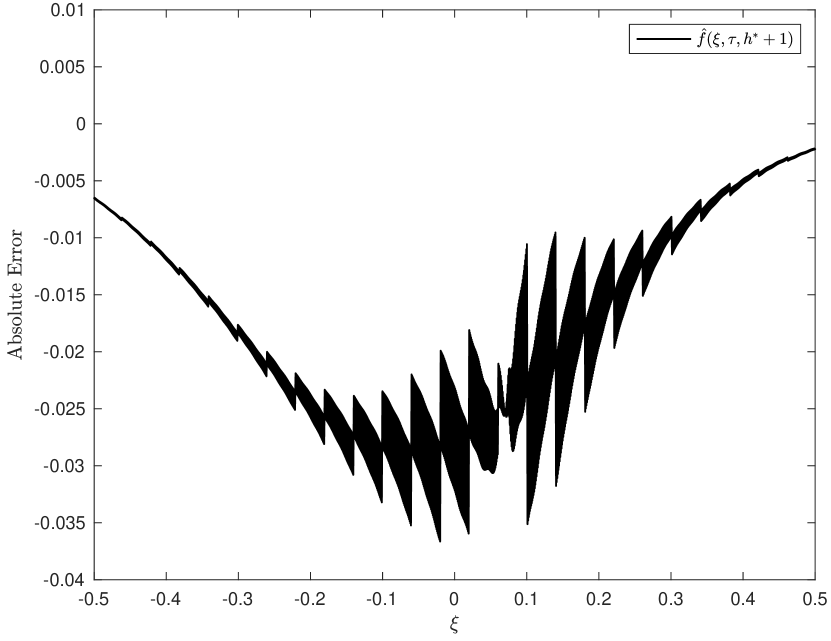

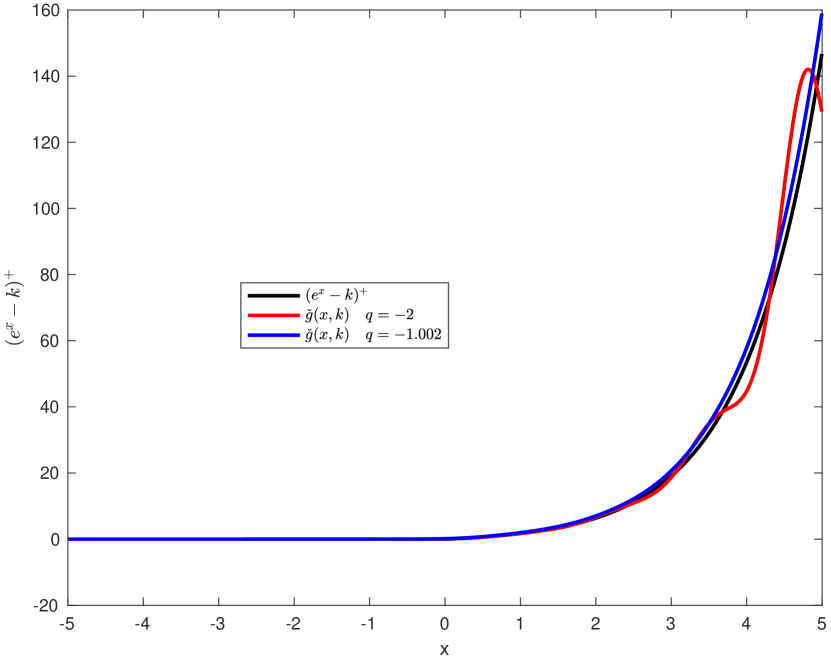

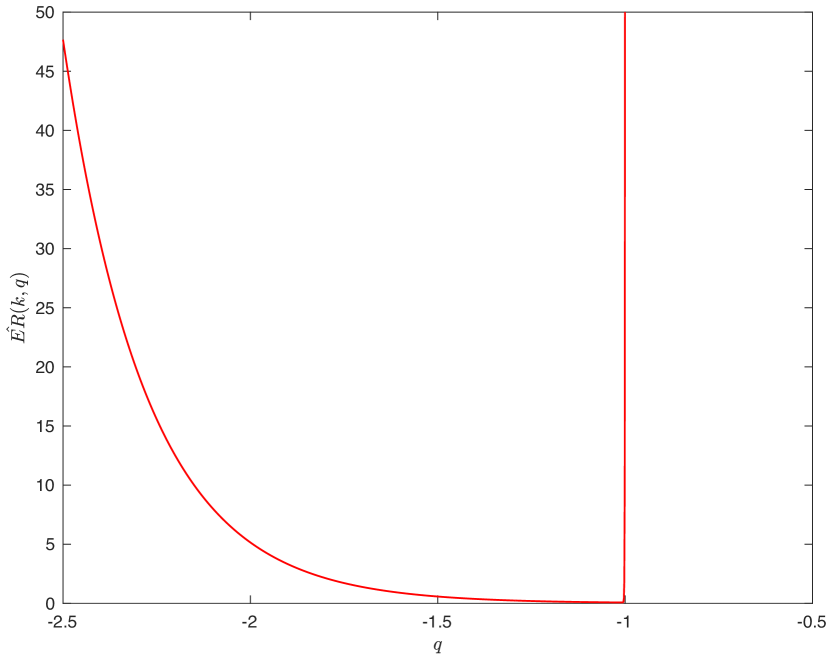

The payoff in (4.31) depends on the parameter . As shown in Fig 8(a), for , the inverse of Fourier in (4.31) produces poor results; in fact, the curve in red fluctuates around real call payoff . For , the inverse of Fourier over-estimates the call payoff.

To find value with a high level of accuracy, we define the error function () between the real call payoff and the inverse Fourier payoff, with (strike price) and the parameter as inputs.

| (4.32) |

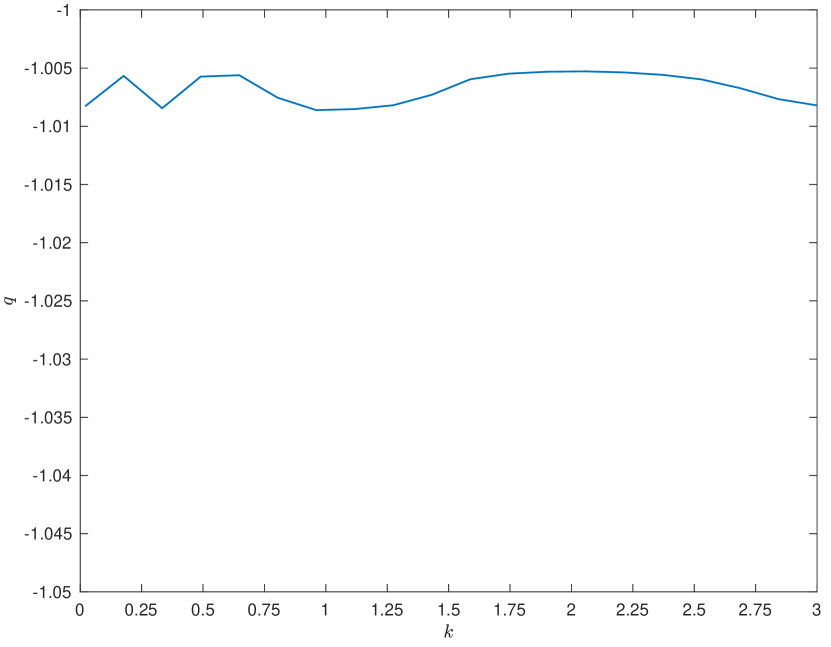

At the money (ATM) option, the strike price and the can be analyzed as a function of one variable . Fig 8(b) displays the error function () graph as a function of . is a convex function, which decreases and increases over the interval . The section method was applied to determine , which minimizes .

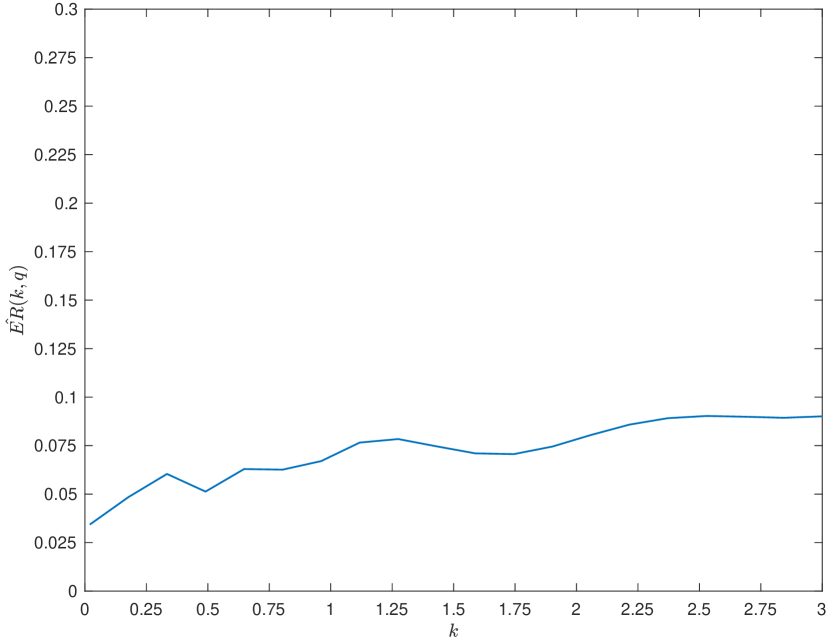

Fig 9(a) displays the minimum value as a function of the strike price ; and the correspondent optimal parameter as a function of the strike price (Fig 9(b)). Both graphs display almost a constant function with respect to the strike price.

4.4.2. Calculating the Fourier Integral by FRFT

The method of Fourier transform [24] provides valuable and powerful tools for option pricing under a class of Lévy processes when the characteristic function is much simpler than their density function. We compute the call option’s value on the SPY ETF with the Fractional Fast Fourier (FRFT).

For , is the price per one dollar of the strike price. We have

we assume

| (4.33) |

Following the notation of the Fractional Fast Fourier (FRFT) developed in [31] (Section 2 and Appendix A.1.)

| (4.34) |

4.5. Empirical Analysis

Based on parameter data from VG Model [31, 32]: , , , , ; risk-free interest rate is added and the Esscher transform parameter () was computed. The VG option pricing will be calculated across maturity and option moneyness using Extended and Generalized Black-Scholes formulas. The closed-form Black-Scholes model [19] was added to the analysis as a benchmark.

| (4.35) | ||||

The variance is the annualized variance computed from the daily SPY ETF return variance in [31].

Option Moneyness describes the intrinsic value of an option in its current state. It indicates whether the option would make money if exercised immediately. Option moneyness can be classified into three categories: At-The-Money (ATM) option (), Out-of-The Money (OTM) option (), and In-The-Money (ITM) option (). On August 04, 2021, the SPY ETF market price closed at . We compute the VG call option price on SPY ETF with the spot price () . The results are summarised in Table 3.

| Strike Price | Moneyness | BSM | VGM(4.16) | VGM(4.25) | BSM | VGM(4.16) | VGM(4.25) | BSM | VGM(4.16) | VGM(4.25) | BSM | VGM(4.16) | VGM(4.25) | BSM | VGM(4.16) | VGM(4.25) | BSM | VGM(4.16) | VGM(4.25) |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Period ( in year) | 0.0625 | 0.125 | 0.25 | 0.5 | 0.75 | 1 | |||||||||||||

| 219.49 | 2.00 | 220.31 | 220.28 | 219.86 | 221.13 | 221.10 | 220.48 | 222.76 | 222.72 | 221.71 | 225.98 | 225.93 | 224.14 | 229.15 | 229.13 | 226.53 | 232.27 | 232.26 | 228.88 |

| 225.12 | 1.95 | 214.70 | 214.74 | 214.10 | 215.54 | 215.58 | 214.74 | 217.21 | 217.25 | 216.01 | 220.52 | 220.54 | 218.53 | 223.77 | 223.82 | 221.01 | 226.97 | 227.04 | 223.45 |

| 231.04 | 1.90 | 208.80 | 208.83 | 208.18 | 209.66 | 209.69 | 208.84 | 211.38 | 211.41 | 210.16 | 214.77 | 214.80 | 212.77 | 218.10 | 218.16 | 215.34 | 221.39 | 221.47 | 217.88 |

| 237.29 | 1.85 | 202.58 | 202.53 | 202.10 | 203.47 | 203.42 | 202.79 | 205.23 | 205.18 | 204.16 | 208.71 | 208.67 | 206.86 | 212.13 | 212.13 | 209.53 | 215.51 | 215.53 | 212.16 |

| 243.88 | 1.80 | 196.02 | 196.06 | 195.38 | 196.92 | 196.97 | 196.10 | 198.73 | 198.78 | 197.51 | 202.31 | 202.37 | 200.32 | 205.83 | 205.93 | 203.10 | 209.31 | 209.43 | 205.84 |

| 250.85 | 1.75 | 189.07 | 189.16 | 188.47 | 190.01 | 190.10 | 189.21 | 191.87 | 191.96 | 190.68 | 195.55 | 195.66 | 193.61 | 199.17 | 199.33 | 196.50 | 202.75 | 202.94 | 199.36 |

| 258.22 | 1.70 | 181.72 | 181.81 | 181.36 | 182.69 | 182.78 | 182.13 | 184.60 | 184.69 | 183.66 | 188.39 | 188.52 | 186.70 | 192.12 | 192.30 | 189.71 | 195.81 | 196.03 | 192.70 |

| 266.05 | 1.65 | 173.93 | 173.98 | 173.53 | 174.92 | 174.97 | 174.33 | 176.89 | 176.95 | 175.92 | 180.79 | 180.91 | 179.09 | 184.64 | 184.83 | 182.24 | 188.45 | 188.69 | 185.37 |

| 274.36 | 1.60 | 165.64 | 165.64 | 165.45 | 166.67 | 166.66 | 166.28 | 168.70 | 168.70 | 167.94 | 172.73 | 172.82 | 171.26 | 176.70 | 176.87 | 174.56 | 180.63 | 180.88 | 177.84 |

| 283.21 | 1.55 | 156.83 | 156.75 | 156.56 | 157.88 | 157.81 | 157.43 | 159.98 | 159.91 | 159.18 | 164.14 | 164.21 | 162.66 | 168.25 | 168.42 | 166.14 | 172.33 | 172.59 | 169.60 |

| 292.65 | 1.50 | 147.42 | 147.28 | 146.81 | 148.51 | 148.38 | 147.73 | 150.68 | 150.56 | 149.56 | 154.98 | 155.05 | 153.24 | 159.24 | 159.45 | 156.93 | 163.49 | 163.79 | 160.59 |

| 302.75 | 1.45 | 137.37 | 137.50 | 136.72 | 138.50 | 138.63 | 137.69 | 140.74 | 140.89 | 139.62 | 145.20 | 145.61 | 143.53 | 149.64 | 150.21 | 147.45 | 154.08 | 154.76 | 151.34 |

| 313.56 | 1.40 | 126.60 | 126.45 | 126.29 | 127.77 | 127.64 | 127.31 | 130.09 | 129.99 | 129.36 | 134.73 | 135.00 | 133.53 | 139.39 | 139.85 | 137.71 | 144.06 | 144.63 | 141.86 |

| 325.17 | 1.35 | 115.03 | 115.01 | 114.85 | 116.24 | 116.25 | 115.94 | 118.65 | 118.71 | 118.15 | 123.51 | 124.07 | 122.64 | 128.44 | 129.20 | 127.14 | 133.40 | 134.25 | 131.59 |

| 337.68 | 1.30 | 102.57 | 102.48 | 102.35 | 103.83 | 103.80 | 103.53 | 106.34 | 106.39 | 105.94 | 111.50 | 112.20 | 110.84 | 116.79 | 117.68 | 115.72 | 122.10 | 123.05 | 120.53 |

| 351.18 | 1.25 | 89.11 | 89.15 | 88.69 | 90.42 | 90.55 | 90.00 | 93.08 | 93.33 | 92.69 | 98.68 | 99.71 | 98.12 | 104.44 | 105.61 | 103.48 | 110.16 | 111.34 | 108.71 |

| 365.82 | 1.20 | 74.53 | 74.60 | 74.52 | 75.91 | 76.15 | 76.02 | 78.82 | 79.18 | 79.08 | 85.10 | 86.32 | 85.17 | 91.45 | 92.73 | 91.09 | 97.65 | 98.88 | 96.78 |

| 381.72 | 1.15 | 58.69 | 59.15 | 58.38 | 60.22 | 60.94 | 60.20 | 63.67 | 64.34 | 63.82 | 70.94 | 72.47 | 70.85 | 77.99 | 79.48 | 77.46 | 84.70 | 86.09 | 83.68 |

| 399.07 | 1.10 | 41.51 | 42.09 | 41.76 | 43.56 | 44.29 | 44.08 | 48.03 | 48.30 | 48.53 | 56.55 | 57.74 | 56.68 | 64.32 | 65.45 | 64.03 | 71.52 | 72.55 | 70.80 |

| 418.08 | 1.05 | 23.73 | 24.37 | 24.15 | 27.03 | 27.33 | 27.36 | 32.83 | 32.25 | 33.00 | 42.51 | 43.25 | 42.47 | 50.85 | 51.63 | 50.57 | 58.42 | 59.16 | 57.83 |

| 438.98 | 1.00 | 8.92 | 6.45 | 6.76 | 13.11 | 11.13 | 11.40 | 19.53 | 18.35 | 18.43 | 29.61 | 29.17 | 29.01 | 38.11 | 38.01 | 37.61 | 45.79 | 45.79 | 45.20 |

| 462.08 | 0.95 | 1.64 | 1.19 | 1.27 | 4.40 | 2.94 | 3.02 | 9.62 | 7.41 | 7.50 | 18.70 | 17.17 | 17.09 | 26.72 | 25.85 | 25.50 | 34.12 | 33.67 | 33.01 |

| 487.76 | 0.90 | 0.10 | 0.35 | 0.40 | 0.89 | 0.96 | 1.02 | 3.68 | 2.82 | 2.94 | 10.42 | 8.69 | 8.83 | 17.24 | 15.73 | 15.71 | 23.87 | 22.75 | 22.48 |

| 516.45 | 0.85 | 0.00 | 0.10 | 0.13 | 0.09 | 0.31 | 0.34 | 1.02 | 1.03 | 1.11 | 4.96 | 3.92 | 4.09 | 10.02 | 8.48 | 8.63 | 15.46 | 13.90 | 13.93 |

| 548.73 | 0.80 | 0.00 | 0.03 | 0.04 | 0.00 | 0.10 | 0.12 | 0.19 | 0.37 | 0.41 | 1.94 | 1.66 | 1.78 | 5.12 | 4.19 | 4.37 | 9.10 | 7.80 | 7.96 |

| 585.31 | 0.75 | 0.00 | 0.01 | 0.01 | 0.00 | 0.03 | 0.04 | 0.02 | 0.12 | 0.14 | 0.60 | 0.64 | 0.72 | 2.23 | 1.85 | 2.02 | 4.76 | 3.91 | 4.14 |

| 627.11 | 0.70 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | 0.01 | 0.00 | 0.04 | 0.04 | 0.14 | 0.23 | 0.26 | 0.80 | 0.75 | 0.83 | 2.15 | 1.77 | 1.91 |

| 675.35 | 0.65 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | 0.01 | 0.02 | 0.07 | 0.09 | 0.22 | 0.27 | 0.31 | 0.81 | 0.72 | 0.81 |

| 731.63 | 0.60 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.02 | 0.03 | 0.05 | 0.09 | 0.11 | 0.24 | 0.26 | 0.31 |

| 798.15 | 0.55 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | 0.01 | 0.01 | 0.02 | 0.03 | 0.06 | 0.08 | 0.10 |

| 877.96 | 0.50 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 | 0.01 | 0.01 | 0.01 | 0.02 | 0.03 |

The Fractional Fourier Transform (FRFT) algorithm performs poorly for the in-the-money (ITM) option. The FRFT underprices the VG option for in-the-money (ITM), whereas the 12-point rule Composite Newton-Cotes Quadrature produces consistent option pricing results with the Black-Scholes model. Both algorithms yield consistent results for at-the-money and out-of-the-money options.

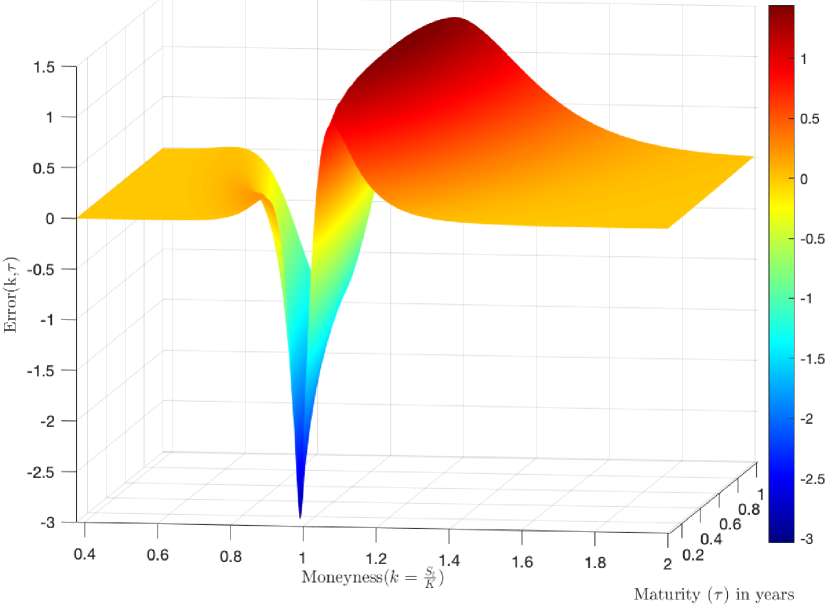

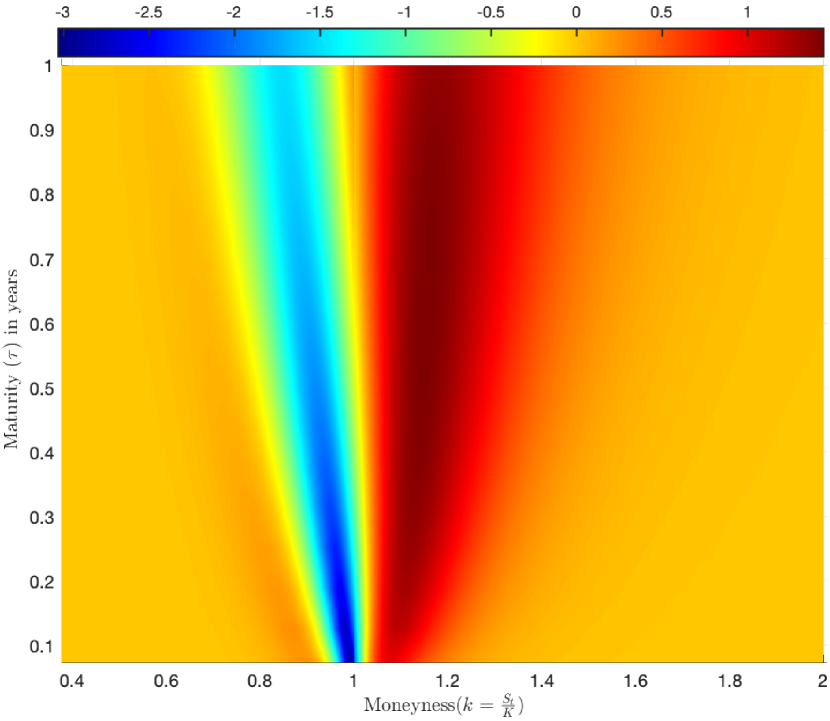

To generalize the analysis and account for a large range of option moneyness and maturity, The error (4.36) was computed as the difference between VG option and BS option prices.

| (4.36) |

Fig 10 graphs the error as a function of the time to maturity () and the option moneyness (). The spot price () is a constant, and the option moneyness depends on the strike price.

The Black-Scholes (BS) and VG models produce different option pricing results. The Black-Scholes model is overpriced for the out-of-the-money (OTM) option (blue color in Fig 10) and underpriced for the in-the-money (ITM) option (red color).

The results in Fig 10 are consistent with [28], where the VG pricing was performed on S&P500 index data. The shape in Fig 10(a) looks similar to Fig 6 in [28] when the Option moneyness variable replaces the strike price. However, the overpriced Black-Scholes model in bleu color (Fig 10) does not support the findings [26] that the VG option prices are typically higher than the Black-Scholes model prices, with the percentage bias rising when the stock gets out-of-the-money (OTM). One of the limitations of these studies is that the VG model is symmetric and uses three parameters. The five-parameter VG model controls the excess kurtosis and the skewness of the daily SPY ETF return data.

5. Conclusion

In the paper, a Ornstein-Uhlenbeck type process was used to build a continuous sample path of a five-parameter Variance-Gamma (VG) process (): location (), symmetric (), volatility (), and shape () and scale (). The data parameters [31, 32] were used to simulate the gamma process () and the continuous sample path of the subordinator process (). Both simulations were used as inputs to simulate the VG process’s continuous sample path. The Lévy density of the VG process was derived and shown to belong to a KoPoL family of order , intensity and steepness parameters and . It was shown that the VG process converges asymptotically in distribution to a Lévy process driven by a Normal distribution with mean and variance . The existence of the Equivalent Martingale Measure (EMM) of the five-parameter VG process was shown. The EMM preserves the structure of the five-parameter VG process with an inflated Gamma scale parameter and a constant term adjustment symmetric parameter. The extended Black-Scholes formula provides the closed form of the VG option price. The Lévy process generated by the VG model provides the Generalized Black-Scholes Formula. The daily SPY ETF return data illustrates the computation of the European option price under the five-parameter VG process. The 12-point rule Composite Newton-Cotes Quadrature and the Fractional Fast Fourier (FRFT) algorithms were implemented to compute the European option price. It results that the FRFT yields inconsistent European option prices for in-the-money options. The Black-Scholes (BS) and VG models produce different option pricing results. The Black-Scholes model is overpriced for out-of-the-money (OTM) options and underpriced for in-the-money (ITM) options. However, for deep out-of-the-money (OTM) and deep-in-the-money (ITM) options, Black-Scholes (BS) and VG models yield almost the same option price.

References

- [1] ME Adeosun, SO Edeki, and OO Ugbebor. On a variance gamma model (vgm) in option pricing: A difference of two gamma processes. Journal of Informatics and Mathematical Sciences, 8(1):1–16, 2016.

- [2] Mohammed Alhagyan, Masnita Misiran, and Zurni Omar. Discussions on continuous stochastic volatility models. Global and Stochastic Analysis, 7(1):55–64, 2020.

- [3] Andrii Andrusiv and Hans-Jürgen Engelbert. On the minimal entropy martingale measure for lévy processes. Stochastics, 92(8):1223–1243, 2020.

- [4] David Applebaum. Lévy processes and stochastic calculus. Cambridge university press, 2009.

- [5] Juan Arias-de Reyna. On the theorem of frullani. Proceedings of the American Mathematical Society, 109(1):165–175, 1990.

- [6] Ole E Barndorff-Nielsen, Jens Ledet Jensen, and Michael Sørensen. Some stationary processes in discrete and continuous time. Advances in Applied Probability, 30(4):989–1007, 1998.

- [7] Ole E Barndorff-Nielsen and Neil Shephard. Non-Gaussian OU based models and some of their uses in financial economics. Nuffield College Oxford, 1999.

- [8] Ole E Barndorff-Nielsen and Neil Shephard. Modelling by lévy processess for financial econometrics. Lévy processes, pages 283–318, 2001.

- [9] Ole E Barndorff-Nielsen and Neil Shephard. Non-gaussian ornstein–uhlenbeck-based models and some of their uses in financial economics. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 63(2):167–241, 2001.

- [10] Ole E Barndorff-Nielsen and Neil Shephard. Financial volatility, lévy processes and power variation. Unpublished book, Nuffield College, 2002.

- [11] Ole E Barndorff-Nielsen and Neil Shephard. Integrated ou processes and non-gaussian ou-based stochastic volatility models. Scandinavian Journal of statistics, 30(2):277–295, 2003.

- [12] Fischer Black and Myron Scholes. The pricing of options and corporate liabilities. Journal of Political Economy, 81(3):637–654, 1973.

- [13] Svetlana Boyarchenko and Sergei Z Levendorskii. Non-Gaussian Merton-Black-Scholes Theory, volume 9. World Scientific, 2002.

- [14] Peter Carr, Hélyette Geman, Dilip B Madan, and Marc Yor. Stochastic volatility for lévy processes. Mathematical finance, 13(3):345–382, 2003.

- [15] R. Cont. Empirical properties of asset returns: stylized facts and statistical issues. Quantitative Finance, 1(2):223–236, feb 2001.

- [16] Hans U Gerber, Elias SW Shiu, et al. Option pricing by Esscher transforms. HEC Ecole des hautes études commerciales, 1993.

- [17] Steven L Heston. A closed-form solution for options with stochastic volatility with applications to bond and currency options. The review of financial studies, 6(2):327–343, 1993.

- [18] John Hull and Alan White. The pricing of options on assets with stochastic volatilities. The journal of finance, 42(2):281–300, 1987.

- [19] John C Hull. Options futures and other derivatives. Pearson Education India, 2003.

- [20] Sato Ken-Iti. Lévy processes and infinitely divisible distributions. Cambridge university press, 1999.

- [21] Maurice George Kendall et al. The advanced theory of statistics. The advanced theory of statistics., (2nd Ed), 1946.

- [22] Steven G Kou. A jump-diffusion model for option pricing. Management science, 48(8):1086–1101, 2002.

- [23] Andreas E Kyprianou. Fluctuations of Lévy processes with applications: Introductory Lectures. Springer Science & Business Media, 2014.

- [24] Cuixiang Li, Huili Liu, Mengna Wang, and Wenhan Li. The pricing of compound option under variance gamma process by fft. Communications in Statistics-Theory and Methods, pages 1–15, 2020.

- [25] Dilip B Madan, Peter P Carr, and Eric C Chang. The variance gamma process and option pricing. Review of Finance, 2(1):79–105, 1998.

- [26] Dilip B Madan and Frank Milne. Option pricing with vg martingale components 1. Mathematical finance, 1(4):39–55, 1991.

- [27] Kazuhisa Matsuda. Introduction to merton jump diffusion model. Department of Economics. The Graduate Center, The City University of New York, 2004.

- [28] Sharif Mozumder, Ghulam Sorwar, and Kevin Dowd. Revisiting variance gamma pricing: An application to s&p500 index options. International Journal of Financial Engineering, 2(02):1550022, 2015.

- [29] A. H. Nzokem. Stochastic and Renewal Methods Applied to Epidemic Models. PhD thesis, York University , YorkSpace institutional repository, 2020.

- [30] A. H. Nzokem and V. T. Montshiwa. Fitting generalized tempered stable distribution: Fractional fourier transform (frft) approach. ARXIV.2205.00586[q-fin.ST], 2022.

- [31] A.H. Nzokem. Fitting infinitely divisible distribution: Case of gamma-variance model, 2021.

- [32] A.H. Nzokem. Gamma variance model: Fractional fourier transform (FRFT). Journal of Physics: Conference Series, 2090(1):012094, nov 2021.

- [33] A.H. Nzokem. Numerical solution of a gamma - integral equation using a higher order composite newton-cotes formulas. Journal of Physics: Conference Series, 2084(1):012019, nov 2021.

- [34] A.H. Nzokem. Sis epidemic model: Birth-and-death markov chain approach. International Journal of Statistics and Probability, 10(4):10–20, July 2021.

- [35] Philip Protter. Stochastic integration and differential equations. A new approach, volume 21. 01 2005.

- [36] Peter Tankov. Financial modelling with jump processes. Chapman and Hall/CRC, 2003.

- [37] GE Uhlenback and LS Ornstein. On the theory of the brownian motion. Phys. Rev, 36:823–841, 1930.