First-Order Context-Specific Likelihood Weighting in Hybrid Probabilistic Logic Programs

Abstract

Statistical relational AI and probabilistic logic programming have so far mostly focused on discrete probabilistic models. The reasons for this is that one needs to provide constructs to succinctly model the independencies in such models, and also provide efficient inference.

Three types of independencies are important to represent and exploit for scalable inference in hybrid models: conditional independencies elegantly modeled in Bayesian networks, context-specific independencies naturally represented by logical rules, and independencies amongst attributes of related objects in relational models succinctly expressed by combining rules.

This paper introduces a hybrid probabilistic logic programming language, DC#, which integrates distributional clauses’ syntax and semantics principles of Bayesian logic programs. It represents the three types of independencies qualitatively. More importantly, we also introduce the scalable inference algorithm FO-CS-LW for DC#. FO-CS-LW is a first-order extension of the context-specific likelihood weighting algorithm (CS-LW), a novel sampling method that exploits conditional independencies and context-specific independencies in ground models. The FO-CS-LW algorithm upgrades CS-LW with unification and combining rules to the first-order case.

Under consideration for publication in the journal of artificial intelligence research.

1 Introduction

Statistical relational AI (StarAI) and probabilistic logic programming (PLP) (?, ?) have contributed many languages for declaratively modeling expressive probabilistic models and have devised numerous inference techniques. They have been applied to many applications in databases, knowledge graphs, social networks, robotics, chemical compounds, genomics, etc.

To enable scalable probabilistic inference, it is essential to represent three different types of independencies in the modeling language. Firstly, the traditional classical conditional independencies (CIs) represented by Bayesian networks (BNs). Secondly, the context-specific independencies (CSIs): independencies that hold only in certain contexts (?). These independencies arise due to structures present in conditional probability distributions (CPDs) of BNs, which BNs do not qualitatively represent, but rule-based representations do by making structures explicit in the clauses (?). Thirdly, the combining rules such as NoisyOR to express probabilistic influences among attributes of related objects (?, ?). Combining rules are particularly interesting since they allow one to qualitatively represent independence of causal influences (?, ICIs), where each influence is considered independent of others. This independence is natural and commonly assumed to keep relational models succinct (?). In probabilistic logic programs that deal with only discrete random variables, combining rules are the core component (?, ?).

Over the past few decades, many PLP languages have been proposed; however, only a few of them are hybrid, i.e., support both discrete and continuous random variables. Nevertheless, such hybrid PLP are needed to cope with applications in areas such as activity recognition, robotics, sensing, perception, etc. Current hybrid PLP languages suffer from two problems. Firstly, they generally do not support combining rules (?, ?, ?, ?, ?). Secondly, and more importantly, there exist, to the best of our knowledge, no inference techniques that exploit all three types of independencies for hybrid PLPs.

To remedy this, we first introduce DC# (pronounced “DC sharp”), a hybrid PLP language that supports combining rules. DC# uses a special form of clauses called distributional clauses (DCs) to express probabilistic knowledge. We borrow the syntax of DCs from (?) but introduce an extended new semantics based on Bayesian Logic Programs (?, BLPs). Thus, in terms of representation, DC#, a rule-based representation, differs from graphical model-based relational representations, such as BLPs, which are associated with CPDs. However, the semantics of DC# are based on BLPs, so DC# programs can be seen as BLPs qualitatively representing CSIs.

Our second contribution is the first-order context-specific likelihood weighting (FO-CS-LW) algorithm that exploits these three types of independencies for scalable inference in DC# programs. Before going to the first-order case, we introduce the CS-LW algorithm for ground programs. CS-LW exploits both CIs and CSIs, which is an approximate inference algorithm that, until our earlier work, has not been well-studied yet (?).

There exist state-of-the-art inference algorithms for exact inference (?) in discrete models. These algorithms are based on the knowledge compilation technique (?) that uses logical reasoning to exploit CSIs. However, for many models, exact inference quickly becomes infeasible. Stochastic sampling for approximate inference is a standard solution. Sampling algorithms are simple yet powerful tools, and they can be applied to arbitrary complex hybrid models, unlike exact inference. It is widely believed that CSI properties in distributions are difficult to exploit for approximate inference (?). To solve this difficult problem, we introduce the context-specific likelihood weighting (CS-LW), a sampling algorithm that exploits both CI and CSI properties, leading to faster convergence and faster sampling speed than standard likelihood weighting (LW).

Next, we extend CS-LW to first-order DC# programs specifying relational probabilistic models. Due to the use of combining rules, such models, when grounded, have many symmetrically repeated parameters. Inference algorithms designed for grounded models can not exploit these symmetries, rendering inference infeasible even for very simple relational models. It is widely believed that the inference can be feasible if one does not ground out these models, but reason at the first-order level with unification (?). There have been several attempts at doing this for various simple languages (?, ?, ?, ?), but not for hybrid and expressive languages like DC#. For example, well-known graphical model-based relational representation languages that do not qualitatively represent CSIs, construct ground BNs for inference (?, ?). Similarly, well-known PLP systems, which do represent CSIs qualitatively, first ground the first-order programs and then perform inference at the ground level (?). In contrast, FO-CS-LW reasons at the first-order level. Using the tools of logic, i.e., unification, substitution, and resolution, FO-CS-LW samples only relevant variables from first-order DC# programs determined by various forms of independencies present in the programs. We empirically demonstrate that FO-CS-LW scales with domain size and provide an open-source implementation of our framework111The code is publicly available: https://github.com/niteshroyal/DC-Sharp.

This paper is a significantly extended and completed version of our previous paper (?), where we introduced CS-LW to exploit the structures present in CPDs of BNs. The present paper first introduces a language to describe first-order probabilistic models and then extends CS-LW to the first-order case.

Contribution

We summarise our contributions in this paper as follows:

-

•

We introduce a new PLP language DC# that supports combining rules to describe hybrid relational probabilistic models succinctly.

-

•

We present a novel sampling methodology, CS-LW, that exploits both CIs and CSIs for probabilistic inference in BNs and ground probabilistic logic programs.

-

•

We present a first-order extension of CS-LW that applies directly to first-order DC# programs and in additional exploits the symmetries present through combining rules.

-

•

We empirically show that our inference algorithm scales with the domain size when applied to hybrid relational probabilistic models described as DC# programs.

Organization

The paper is organized as follows. We start by motivating our discussion with some examples in Section 2. In Section 3, we review the standard likelihood weighting and basic concepts of logic programming. Section 4 presents the DC# language. Section 5 presents the CS-LW algorithm for ground DC# programs describing BNs, which is then extended to first-order DC# programs in Section 6. We then evaluate our algorithms in Section 7. Before concluding, we finally touch upon related work and directions for future work.

2 Motivating Examples

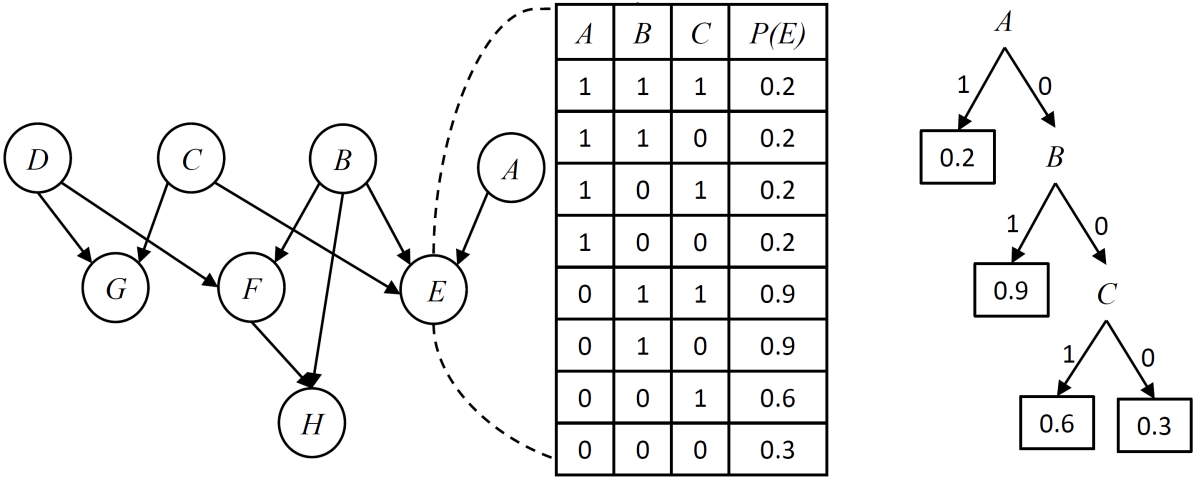

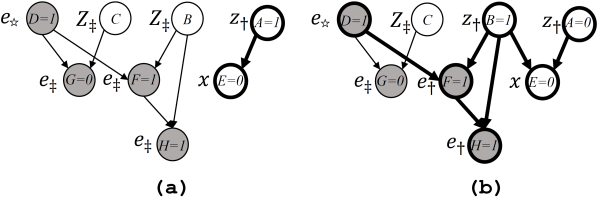

Let us illustrate, with examples, the independencies that DC# programs will qualitatively represent and that our algorithm will exploit. Consider a BN in Figure 1(a), where a tree-structure is present in the CPD of variable . If one observes the CPD carefully, one can conclude that , that is, is the same for all values of and . The variable is said to be independent of variables in the context . This local independence statement corresponds to the influence of edges vanishing in this context; consequently, it may have global implications. For example, implies . These independencies are called CSIs. They arise naturally in various real-world situations (?), including when one writes if-then conditions in probabilistic programs (?). Our CS-LW algorithm aims to exploit CSIs arising due to the structures present within CPDs of BNs when ground DC# programs describe such BNs.

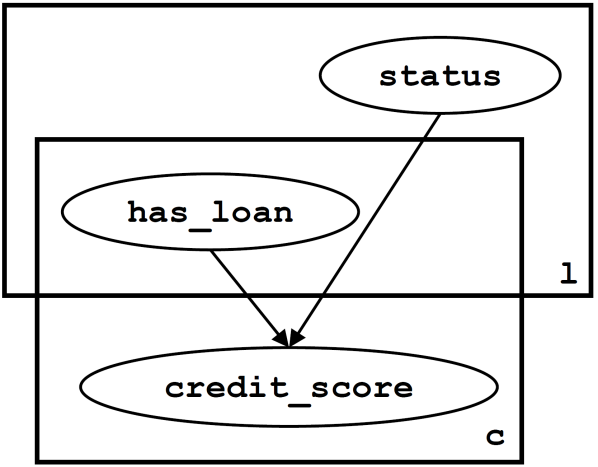

The exploitation of CSIs in relational probabilistic models is even more crucial since a huge amount of CSIs is present in these models. As a simple example, consider the model in Figure 1(b), where the plate notation is used to represent direct influence relationships among credit scores of clients, statuses of loans, and number of type random variables for each client-loan pair, which can be either true or false. Given that a client has a loan, it is easy to imagine that the status of the loan may affect the client’s credit score. On the other hand, if a client has only a few loans, then it is just as easy to imagine that the status of the loans that the client does not have will not affect the client’s credit score. That is, the client’s credit is independent of the status of all those loans that the client does not have. This is a first-order level CSI, which BNs with plates do not qualitatively represent. We will introduce a PLP language to represent it.

Furthermore, it is natural to imagine that the client’s credit score depends on the number of loans that the client has with approved and rejected statuses but not on the identity of those approved and rejected loans. That is, loans are exchangeable objects. In such a case, it is common to consider that each loan’s status independently has its own probabilistic influence on the client’s credit score, and the final probabilistic influence is a combination of all these influences (?, ?). This independence assumption implies exchangeability. Relational models written as DC# programs qualitatively represent these independencies and the first-order level CSIs that our FO-CS-LW algorithm aims to exploit for scalability.

3 Background

A Bayesian network is a pair , where is a directed acyclic graph structure specifying direct influence relationships among random variables (nodes), and is a set of CPDs associated with each node. The CPD specifies the conditional probability of the variable given its parents. The graph structure represents local CI statements, which states that each variable is conditionally independent of its non-descendants given its parents. The local CIs and the set of CPDs together induce a joint probability distribution over all the variables.

We denote random variables (RVs) with uppercase letters () and their assignments with lowercase letters (). Bold letters denote sets of RVs () and their assignments (). Parents of the variable are denoted with and their assignments with . Suppose is a probability distribution over disjoint sets of variables , then denotes a set of observed variables, a set of unobserved query variables and a set of unobserved variable other than query variables. The expected value of relative to a distribution is denoted by .

3.1 Likelihood Weighting

Next, we briefly review likelihood weighting (LW), one of the most popular sampling algorithms for BNs.

A typical query to the distribution is to compute , that is, the probability of being assigned given that is assigned . Following Bayes’s rule, we have:

where is an indicator function , which takes value when , and otherwise. We can estimate using LW if we specify using a Bayesian network. LW belongs to a family of importance sampling schemes that are based on the observation,

| (1) |

where is a proposal distribution such that whenever . The distribution is different from and is used to draw independent samples. Generally, is selected such that the samples can be drawn easily. In the case of LW, to draw a sample, variables are assigned values drawn from and variables in are assigned their observed values. These variables are assigned in a topological ordering relative to the graph structure of . Thus, the proposal distribution in the case of LW can be described as follows:

Consequently, it is easy to compute the likelihood ratio in Equation 1. All factors in the numerator and denominator of the fraction cancel out except for where . Thus,

where , which is also a RV, is the weight of evidence . The likelihood ratio is the product of all of these weights, and thus, it is also a RV. Given independent weighted samples from , we can estimate the query:

| (2) |

3.2 Likelihood Weighting + Bayes-Ball

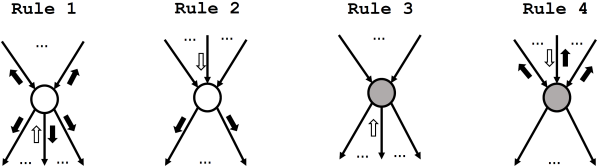

In the previous section, we used all random variables to estimate . However, due to CIs encoded by the graph structure in a Bayesian network , observed states and CPDs of only some variables “might” be required for computing . These variables are called requisite variables. To get a better estimate of , it is recommended to use only these variables. The standard approach is to first apply the Bayes-ball algorithm (?) over the graph to obtain a sub-network of requisite variables, then simulate the sub-network to obtain the weighted samples. An alternative approach is to use Bayes-ball to simulate the original network and focus on only requisite variables to obtain the weighted samples. This approach is trivial and might already be used by many BN inference tools. However, it is not described in the literature clearly, so we will describe it next. It will form the basis of our discussion on CS-LW, where we will also exploit structures within CPDs of BNs.

) based on the direction of the current visit (indicated using

) based on the direction of the current visit (indicated using  ) and the type of variable. To distinguish observed variables from unobserved variables, the former type of variables are shaded.

) and the type of variable. To distinguish observed variables from unobserved variables, the former type of variables are shaded.To obtain the samples, we need to traverse the graph in a topological ordering. The Bayes-ball algorithm, which is linear in the graph’s size, can be used for it. The advantage of using Bayes-ball is that it also detects CIs; thus, it traverses only a sub-graph that depends on the query and evidence. We can also keep assigning unobserved variables, and weighting observed variables along with traversing the graph. In this way, we assign/weigh only requisite variables. The Bayes-ball algorithm uses four rules to traverse the graph (when deterministic variables are absent in ), and marks variables to avoid repeating the same action. These rules are illustrated in Figure 2. Next, we discuss these rules and also indicate how to assign/weigh variables, resulting in a new algorithm that we call Bayes-ball simulation of BNs. Starting with all query variables scheduled to be visited as if from one of their children, we apply the following rules until no more variables can be visited:

-

1.

When the visit of an unobserved variable is from a child, and is not marked on top, then do these in the order: i) Mark on top; ii) Visit all its parents; iii) Sample a value from and assign to ; iv) If is not marked on bottom, then mark on bottom and visit all its children.

-

2.

When the visit of an unobserved variable is from a parent, and the variable is not marked on bottom, then mark the variable on bottom and visit all its children.

-

3.

When the visit of an observed variable is from a child, then do nothing.

-

4.

When the visit of an observed variable is from a parent, and is not marked on top, then do these in the order: i) Mark on top; ii) Visit all its parents; iii) Let be an observed value of and let be the probability at according to , then the weight of is .

The above rules define an order for visiting parents and children so that variables are assigned/weighted in a topological ordering. Indeed we can define the order since the original rules for Bayes-ball do not prescribe any order. The marks record important information, and the following result holds.

Lemma 1.

Let be marked on top, be visited but not marked on top, and be marked on top. Then the query can be computed as follows,

| (3) |

The proof is straightforward and is present in Appendix A. Now, since are variables of and they form a sub-network such that variables in do not have any parent, we can write,

such that . This means the CPDs of some observed variables are not required for computing . Now we define these variables.

Definition 1.

The observed variables whose observed states and CPDs might be required to compute will be called diagnostic evidence.

Definition 2.

The observed variables whose observed states, but not their CPDs, might be required to compute will be called predictive evidence.

Diagnostic evidence (denoted by ) is marked on top, while predictive evidence (denoted by ) is visited but not marked on top. The variables , , , will be called requisite variables.

Example 1.

Consider the network of Figure 1(a), and assume that our evidence is , and our query is . Suppose we start by visiting the query variable from its child and apply the four rules of Bayes-ball. One can easily verify that observed variables will be marked on top; hence is diagnostic evidence (). The observed variable will only be visited; hence is predictive evidence (). Variables will be marked on top and are requisite unobserved variables ().

Now, we can sample from a factor of such that,

| (4) |

When we use Bayes-ball, precisely this factor is considered for sampling. Starting by first setting to their observed values, is assigned and is weighted in the topological ordering. Given weighted samples from , we can estimate:

| (5) |

In this way, we sample from a lower-dimensional space; thus, the new estimator has a lower variance compared to due to the Rao-Blackwell theorem. Consequently, fewer samples are needed to achieve the same accuracy. Hence, for improved inference, we exploit CIs encoded by the graph structure in .

3.3 Context-Specific Independence

Next, we formally define the independencies that arise due to the structures present within CPDs, which were informally discussed in Section 2.

Definition 3.

Let be a probability distribution over variables , and let be disjoint subsets of . The variables and are independent given and context if whenever . This is denoted by . If is empty then and are independent given context , denoted by .

Independence statements of the above form are called context-specific independencies (CSIs). When is independent of given all possible assignments to then we have: . The independence statements of this form are generally referred to as conditional independencies (CIs). Thus, CSI is a more fine-grained notion than CI. The graphical structure in can only represent CIs. Any CI can be verified in linear time in the size of the graph. However, verifying any arbitrary CSI has been recently shown to be coNP-hard (?).

3.4 A Bit of Logic Programming

Probabilistic logic programming is a probabilistic characterization of logic programming. So, before describing our system, in this section, we review relevant syntactic and semantic notions related to logic programming. More details can be found in (?).

An atom consists of a predicate of arity and terms . A term is either a constant (written in lowercase), a variable (in uppercase), or a structured term of the form where is a functor and the are terms. For example, , and are atoms and , , and are terms. A literal is an atom or the negation of an atom. A positive literal is an atom. A negative literal is the negation of an atom. A clause is a universally quantified disjunction of literals. A definite clause is a clause which contains exactly one positive literal and zero or more negative literals. For example, is a definite clause, where are atoms. In logic programming, one usually writes definite clauses in the implication form (where we omit the universal quantifiers for ease of writing). Here, the atom is called head of the clause; and the set of atoms is called body of the clause. A clause with an empty body is called a fact. A definite program consists of a finite set of definite clauses.

Example 2.

A clause is a definite clause. Intuitively, it states that a client has a loan if has an account and is associated to the loan .

An expression, which can be either a term, an atom or a clause, is ground if it does not contain any variable. A substitution assigns terms to variables . The element is a binding for variable . Applying to an expression yields , the instance of , where all occurrences of in are replaced by the corresponding terms . A substitution is a grounding for if is ground, i.e., contains no variables (when there is no risk of confusion we drop “for ”).

Example 3.

Applying a substitution to the clause from Example 2 yields which is .

A substitution unifies two expressions and if and are identical (denoted ). Such a substitution is called a unifier. Unifiers may not always exist. If there exists a unifier for two expressions and , we call such atoms unifiable and we say that and unify.

Example 4.

A substitution unify and .

A substitution is said to be more general than a substitution iff there exists a substitution such that . A unifier is said to be a most general unifier (mgu) of two expressions iff is more general than any other unifier of the expressions. Expression is a renaming of if they differ only in the names of variables.

Example 5.

Unifiers and are both most general unifiers of and . The resulting applications,

are renamings of each other.

The Herbrand universe of a definite program , denoted , is the set of all ground terms constructed from functors and constants appearing in . The Herbrand base is the set of all ground atoms that can be constructed by using predicates from with ground terms from as arguments. Subsets of the Herbrand base are called Herbrand interpretations. A Herbrand interpretation is a model of a clause iff for all grounding substitutions , such that , it also holds that . A Herbrand model of a set of clauses is a Herbrand interpretation which is a model of every clause in the set.

The least Herbrand model of a definite program , denoted , is the intersection of all Herbrand models of , i.e., is the set of all ground atoms that are logical consequences of the program. is unique for definite programs and can be constructed by repeatedly applying the so-called operator, which is defined as a function on Herbrand interpretations of as follows:

where, are grounding substitutions. Let be the set of all ground facts in the program. Now, applying the operator on , it is possible to use every ground instance of each clause to construct new ground atoms from . In this way, a new set is obtained, which can be used again to construct more ground atoms. The new atoms added to are those which must follow immediately from . It is possible to construct by recursively applying the operator until a fixpoint is reached (), i.e., until no more ground atoms can be constructed.

A query is of the form where the are atoms and all variables are understood to be existentially quantified. Given a definite program , a correct answer to the query is a substitution such that is entailed by , denoted by . That is, belongs to . The answer substitution is often computed using SLD-resolution. Finally, the answer set of is the set of all correct answer substitutions to .

4 DC#: A Representation Language for Hybrid Relational Models

This section presents a PLP language DC# for describing hybrid relational probabilistic models. The syntax of our language is based on the elegant syntax of distributional clauses (DCs) used by (?). However, we extend its semantics to support combining rules. The new semantics, however, do not allow for describing open-universe probabilistic models (OUPMs) (?), which was possible in the previous system. The semantics supporting both OUPMs and combining rules is another topic of research. We do not study it in this paper. The new semantics have been developed along the lines of Bayesian Logic Programs (BLPs) (?).

4.1 Syntax

DC is a natural extension of definite clauses for representing conditional probability distributions.

Definition 4.

A DC is a formula of the form , where is a special binary predicate used in infix notation, and are atoms. Term is called a random variable term and is called a distributional term.

Intuitively, the clause states that RV is distributed as whenever all are true for a grounding substitution . The ground terms and belong to the Herbrand universe.

Ground RV terms are interpreted as RVs. To refer to the values of RV terms, we use a binary predicate , which is used in infix notation for convenience. A ground atom is defined to be true if is the value of RV (or ground RV term) .

Example 6.

Consider the following clause,

Applying a grounding substitution to the clause results in defining a RV distributed as when RVs and take values and (“approved”) respectively; that is, when atoms and are true.

A DC without body is called a probabilistic fact, for example:

This clause states that the age of is normally distributed with mean and variance . It is also possible to define deterministic variables that take only one value with probability 1, e.g., to express our absolute certainty that the age of takes value , we can write,

Hence, it is also possible to write the definite clause of Example 2 as a DC like this:

DC also supports comparing the values of RVs with constants or with values of other RVs in the ground instance of clauses. This can be done using the binary infix predicates , which are especially useful while conditioning continuous RVs as illustrated by the following clause:

This clause specifies the distribution of a client’s credit score when the client’s age is less than .

A distributional program consists of a set of distributional clauses.

Example 7.

The following program describes probabilistic influences among attributes of clients and related loans. Here, we have used as a shorthand for , for , for approved, and for declined.

Now, we provide the semantics of such a program.

4.2 Semantics

First, we specify the form of DCs allowed in our programs.

Definition 5.

A DC# program is a finite set of DCs whose atoms are either of the following form222Even though only two forms of atoms are allowed, one can still write a deterministic atom as in definite clauses like this: . So, by restricting the form of allowed atoms, we are not losing expressivity. Recall that a definite clause can be expressed as a DC.:

-

1.

, where is a RV term and can either be a variable or a constant belonging to the domain of the RV. If is a variable then it must not appear in RV terms of the DC.

-

2.

, where can be logical variables or constants belonging to the corresponding domains of RVs, and is a comparison infix predicate that can be either of these: . The predicates have the same meaning as they have in Prolog.

For example, all clauses shown in Section 4.1 are already of this form, and the program in Example 7 is a DC# program. The reason why logical variables , in the above-stated form (Condition 1), are not allowed to appear in RV terms is that the existence of RVs is not uncertain in DC# programs. This is not the case in the following program:

Here, the first clause models the identity of loans as a Poisson distribution with a mean of . Thus, can be any natural number starting with , and the existence of the statuses of loans, say , is uncertain. We disallow writing such open-universe models in the DC# framework because identifying RVs in such models may require analyzing the programs dynamically. It is not clear how to exploit CSIs in such a case. For closed-universes, they can be identified using simple static analysis, which we describe next.

Definition 6.

Let be a DC# program. An RV set of the program, denoted , is the set of definite clauses obtained by transforming each clause as follows:

-

1.

Let be the empty set.

-

2.

For each atom of the form , an atom is added to .

-

3.

A clause is added to .

Notice that we ignore comparison atoms while constructing the RV set since they do not contain RV terms. They only deal with the values of RVs.

Example 8.

The RV set for the program in Example 7 is:

Atom is in the least Herbrand model of the above RV set but is not. So, term is identified as a RV but the meaningless term is not, even though it belongs to the Herbrand universe. Recall that a ground instance of a DC defines a RV only when its body is true. No ground DC defines as a RV since term is a loan and not a client. We will show that the RV set of a program identifies all RVs defined by the program. This is similar to Bayesian clauses in Bayesian logic programs, where atoms in the least Herbrand model of Bayesian clauses are RVs over which a probability distribution is defined (?).

Now, it is possible to ground a DC# program given an assignment of RVs. We denote such ground programs by .

Example 9.

One might wonder why we require RVs and their assignment to be given before grounding DC# programs. There are two main reasons. First, the programs may define continuous RVs that can take infinitely many values, so we would be constructing infinitely large ground programs without knowing the values of RVs. Second, we do not want meaningless terms like to appear in the head of clauses in the ground programs. These clauses define RVs, and it does not make sense to treat these meaningless terms as RVs. So, we should know RVs before grounding the programs.

Furthermore, the assignment can be thought of as asserted facts in the ground programs, which decide the truth values of atoms of the form in the body of clauses. Since the truth values of bodies of clauses depend on the assignment of RV terms, when the body of a clause is true, we say that the body is true with respect to .

Clearly, the next step is to identify direct influence relationships among RVs defined by programs.

Definition 7.

Let be a DC# program, be an assignment of RVs, and be a ground program constructed given . A ground RV term directly influences if there is clause for some such that , is in the body of the clause, and the body is true with respect to .

For example, we observe from the ground program of Example 9 that ground RV terms , , , and directly influence . However, these relationships are defined with respect to assignments , and it is hard to construct ground programs with respect to all for identifying these relationships. For this purpose, we need a simple approach that can be implemented and executed efficiently. Next, we present such an approach. It performs a simple transformation of the RV sets of DC# programs.

Definition 8.

Let be the RV set of a DC# program . The dependency set is the union of and the set of definite clauses obtained by transforming each clause with non empty body as follows:

-

•

For each , such that , a clause is added to .

Example 10.

One can easily infer from the above definite program that directly influences since is entailed by the above program. Basically, states that the parent of is . Note that Definition 7 defines the direct influences and Definition 8 presents an approach to identify them efficiently. The dependency set is similar to the dependency graph in BLPs (?). The only difference is that we use definite clauses instead of graphs to represent direct influences. These clauses can be automatically constructed from DC# programs using the transformations.

However, it is still unclear how to interpret the clauses, in the ground programs, which may specify multiple distributions for RVs.

Definition 9.

Let be a ground DC# program constructed given an assignment , and let

be clauses for in , whose bodies are true with respect to . Then, there is a multiset of distributions specified for in . If for some then we say the clauses in are mutually inclusive; otherwise, they are mutually exclusive.

For example, there are two distributions specified for in the above example since client has two loans and these loans make the bodies of two clauses for true according to the used assignment of RVs. This, however, raises several questions: According to which distribution is the RV distributed? How to describe that multiple loans probabilistically influence the credit score using DCs?

The standard answer to these questions is to combine multiple distributions into a single distribution using so-called combining rules (?, ?, ?, ?). Combining rules are based on the assumption of independence of causal influence (ICI), where it is assumed that multiple causes on a target variable can be decomposed into several independent causes whose effects are combined to yield a final value (?). In terms of the above example, this means that we can let each loan independently define a distribution for the credit score and then somehow combine all the defined distributions into a single distribution using a combining rule . The most commonly used combining rules in relational systems are Mean, and NoisyOR (?, ?, ?).

Let be a non-empty multiset of probability distributions. Then, the mean combining rule is defined as follows:

where the right-hand side of the equation is a mixture of distributions. When all distributions in the multiset are Bernoulli distributions, denoted , with parameters , then generally noisy OR combining rule is used, which is defined as follows:

To specify a proper probability distribution, a DC# program has to be well-defined.

Definition 10.

Let be a DC# program, be the set of all RVs identified from , be an assignment of , and be the set of all such . The program is well-defined if it satisfies the following conditions:

-

1.

Exhaustiveness: For all and for all , there is at least one clause of the form in such that the clause’s body is true with respect to .

-

2.

Acyclicity: There exists a function that maps to natural numbers . Let be a clause in , and let be the set of RV terms in . For all , for all clauses in , and for all , .

-

3.

Finite Support: The set is non-empty and each is directly influenced by a finite set of RVs.

These conditions are similar to the conditions imposed on BLPs for them to be well-defined (?). Since BLPs consist of Bayesian clauses along with CPDs, the exhaustiveness condition is implicitly imposed. Recall that CPDs define a conditional probability distribution for an RV given any possible assignment of the RV’s parents, which means CPDs are exhaustive.

Let us investigate some ill-defined programs.

Example 11.

The program

is not well-defined since the least Herbrand model of the RV set of the program is empty. The program

is ill-defined because is influenced by infinite number of RVs: , , , and so on. However, the following program

is well-defined since each RV is influenced by a finite number of RVs. Such programs allow for writing models that can have infinite RVs such as hidden Markov models. The following program violates the exhaustiveness condition.

This is because the distribution of when is (“false”) is undefined. The program

is ill-defined as well since it has a cyclic dependency.

We can show that the RV set of a well-defined DC# program identifies all RVs defined by the program, and the dependency set all direct influences among RVs.

Proposition 2.

Let be a RV set of a well-defined DC# program . Then, defines as a RV iff is in the least Herbrand model of .

The proofs of all results presented in this paper are in Appendix A.

Proposition 3.

Let be a dependency set of a well-defined DC# program . Then, directly influences iff is in the least Herbrand model of .

A possible world is an assignment of all RVs defined by a program. Since can be an infinite set, as discussed in Example 11, defining how probabilities are assigned to possible worlds is non-trivial 333To define a probability distribution over infinite RVs, one uses the Kolmogorov extension theorem.. However, we can still define how probabilities are assigned to assignments of a certain subset of RVs.

Definition 11.

Let be the set of all RVs defined by a well-defined DC# program , be an assignment of a finite subset . Denote the set of RVs that directly influence by . The assignment is said to be closed under direct influence relationships if implies .

Example 12.

Reconsider the DC# program of Example 7. Partial assignment is closed under direct influence relationships, but partial assignment is not closed under such relationships. This is because random variable term directly influences , but is not assigned in .

Definition 12.

Let be a well-defined DC# program, be an assignment that is closed under direct influence relationships, and be the ground program constructed given . Then the probability (or density) that assigns to is given by

where is a multiset of distributions specified for RV term in and is the conditional probability density/mass of at according to the combined distribution obtained after applying on the multiset.

Example 13.

Suppose we use Mean as a combining rule for the program of Example 9. Then, to compute the probability density given to the assignment in the example, we will use the following conditional probability densities/masses:

where, the last entry is the probability density at according to the mixture of Gaussians . Thus, the density assigned to the assignment is .

We can show that these probability (or density) assignments define a unique probability distribution.

Proposition 4.

Let be a well-defined DC# program, and be a set of all RVs defined by it. Then specifies a unique probability distribution over .

Since well-defined DC# programs satisfy all conditions of well-defined BLPs, this proposition follows from Proposition 1 of (?)

5 Inference in Ground DC# Programs

Before presenting the sampling algorithm for first-order DC# programs, we will first design an efficient sampling algorithm for ground DC# programs describing BNs with structured CPDs. Thus, this section will focus only on programs having mutually exclusive clauses, which are sufficient to describe such BNs. The algorithm presented in this section aims to exploit structures within CPDs or the structure of clauses in ground programs. However, in this section, we will assume that continuous RVs are absent for simplicity. Once this algorithm is clear, the extended algorithm for first-order DC# programs presented in the next section will be easy to comprehend.

A natural representation of the structures in CPDs is via tree-CPDs (?), as illustrated in Figure 1(a). For all assignments to the parents of a variable , a unique leaf in the tree specifies a (conditional) distribution over . The path to each leaf dictates the contexts, i.e., partially assigned parents, given which this distribution is used. We can easily represent tree-CPDs using DCs, where each path from the root to a leaf in each tree-CPD maps to a rule.

Conversely, we can view a ground program with mutually exclusive clauses as a representation of tree-CPDs of all variables of a BN. Thus, we can alternatively define the probability distribution specified by such ground programs as follows,

Definition 13.

Let be a Bayesian network with tree-CPDs specifying a distribution . Let be a set of distributional clauses such that each path from the root to a leaf of each tree-CPD corresponds to a clause in . Then specifies the same distribution .

To avoid confusion, such ground programs will be called DC() programs.

While an efficient sampling algorithm for only exploits the graph structure (CIs properties) in , the key to designing an efficient sampling algorithm for DC() programs is to exploit both the underlying graph and the clause structure (CSIs properties). To this end, we start with our discussion on the estimation of unconditional probability queries, which is necessary to support our further discussion on conditional probability queries, where we present the full algorithm for DC() programs.

5.1 Top-Down Proof Procedure for DC() programs

Estimating unconditional probability queries in BNs is easy. We just need to generate some random samples of query variables and to find the fraction of times the query is true, which is the estimated probability of the query. In this sampling process, all ancestors of query variables are also sampled. However, due to the clause structure in DC() programs, it is possible to generate random samples of query variables by sampling only some (not all) ancestors, which makes the sampling process more efficient. A simplified version of an approach due to (?) is discussed in Algorithm 1. This approach resembles SLD resolution (?) for definite programs. However, there are some differences due to the stochastic nature of sampling. Unlike SLD resolution, this approach maintains global variable to record sampled values of RVs.

-

•

Proves a conjunction of ground atoms .

-

•

Returns if there is a choice that makes empty; otherwise the procedure fails.

-

1.

While is not empty:

-

(a)

Select the first atom from .

-

(b)

If is of the form :

-

i.

If a value of is recorded in :

-

A.

If : remove from .

-

A.

-

ii.

Else:

-

A.

Choose with in the head.

-

B.

Set .

-

A.

-

i.

-

(c)

Else If is of the form :

-

i.

Sample a value from , record , and remove from .

-

i.

-

(a)

-

2.

Return .

Given an initial goal and global variable , the algorithm recursively produces new goals ,, etc., and updates . There are two cases when it is not possible to obtain from :

-

•

the first is when the selected subgoal of the form cannot be resolved because the sampled value of the RV term already recorded in is different from .

-

•

the other case appears when (i.e. the empty goal).

The procedure444Since cyclic dependency among RVs is not allowed in well-defined programs, and the number of clauses in the program is finite, the procedure is guaranteed to terminate. results in a derivation of , a finite sequence of goals starting with the initial goal

Example 15.

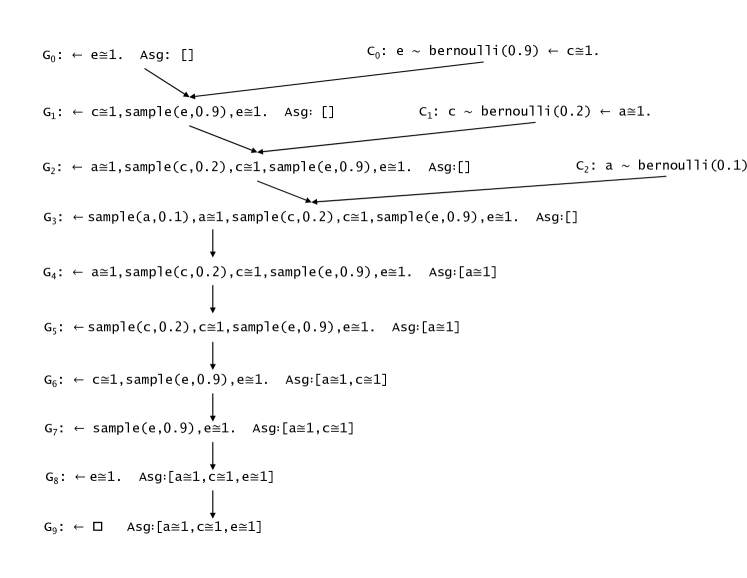

Consider the initial goal () and the following DC() program:

Use as a shorthand notation for . A derivation of , the state of and the program clause used in each step is shown in Figure 3.

As usual, the derivation of goal that ends in the empty goal corresponds to a refutation of the goal. Not all derivations lead to refutations. As already pointed out, if the selected subgoal cannot be resolved, the derivation fails. A refutation or a failed derivation is a complete derivation. If the selected subgoal of some goal can be resolved with more than one program clause, there can be many complete derivations. The procedure searches a refutation by generating multiple complete derivations in a depth-first search fashion. Notice that, unlike SLD-resolution, here derivations might depend on previous complete derivations. This is because the previous derivations might have updated the table, which in turn might influence the current derivation. Additionally, it should be clear that no or only one derivation can be the refutation when clauses in a program are mutually exclusive. So, for efficiency, one should stop generating more derivations in such programs once a refutation is obtained.

To estimate the probability of , we call PROVE-GROUND() repeatedly. The fraction of times we get refutation (i.e., the algorithm returns ) is the estimated probability. Notice that some ancestors of the query variables may not be sampled on some occasions, e.g., in Example 15, variables and were not sampled. Thus, we speed up the sampling process and, in this way, exploit the structure of clauses while estimating marginal probabilities.

5.2 Exploiting Context-Specific Independencies

We now turn our attention to the problem of estimating conditional probabilities, which is more interesting but is significantly more complicated. Exploiting CSIs in this problem is unexplored in in (?). Here we introduce a sampling algorithm that combines the proof procedure, discussed in the previous section, with the Bayes-ball simulation, discussed in Section 3.2. The combined algorithm then exploits both the clause structures and the underlying graph structure of DC() programs. As we will see, it samples variables given the states of only some of their requisite ancestors. This contrasts with the Bayes-ball simulation of BNs, where knowledge of all such ancestors’ states is required. This section is divided into two parts. The first part presents a novel notion of contextual assignment that allows for exploiting CSIs. It provides insight into the computation of using partial assignments of requisite variables. We will show that CSIs allow for breaking the main problem of computing into several sub-problems that can be solved independently. The second part presents the sampling algorithm and justifies it using the notion introduced in the first part.

5.2.1 Notion of Contextual Assignments

Recall from Section 3.2 that variables , , , are requisite for computing the query and the requisite network is formed by these variables. We will consider partial assignments of these variables, which will be used to compute . Let us start by defining these assignments.

Definition 14.

Let and . Denote by , and by . A partial assignment , , , , will be called contextual assignment if due to CSIs in ,

where is a set of partially assigned parents of , that is, .

Here, we summarise some important RVs or their assignments:

| Query variables | |

|---|---|

| Unobserved requisite variables apart from query variables | |

| Diagnostic evidence | |

| Predictive evidence | |

| Assigned subset of in a contextual assignment | |

| Subset of not assigned in a contextual assignment | |

| Subset of in a contextual assignment | |

| Subset of not in a contextual assignment |

Example 16.

Consider the network of Figure 1(a), and assume that our diagnostic evidence is , predictive evidence is , and query is . From the CPD’s structure, we have: ; consequently, a contextual assignment is . We also have: ; consequently, another such assignment is .

We aim to treat the evidence independently, thus, we define it first.

Definition 15.

The diagnostic evidence in a contextual assignment , , , , will be called residual evidence.

However, contextual assignments do not immediately allow us to treat the residual evidence independently. We need the assignments to be safe.

Definition 16.

Let be a diagnostic evidence, and let be an unobserved ancestor of in the graph structure in , where is the sub-network formed by the requisite variables. Let be a causal trail such that either no is observed or there is no . Let be the set of all such . Then the variables will be called basis of . Let , and let be the set of all such for all . Then will be called basis of .

Reconsider Example 16; the basis of is .

Definition 17.

Let , , , , be a contextual assignment, and let be the basis of the residual evidence . If then the contextual assignment will be called safe.

Example 17.

Before showing that the residual evidence can now be treated independently, we first define a random variable called weight.

Definition 18.

Let be a diagnostic evidence, and let be a random variable defined as follows:

The variable will be called weight of . The weight of a subset is defined as follows:

Now we can show the following result:

Theorem 5.

Let , and let be the basis of . Then the expectation of weight relative to the distribution as defined in Equation 4 can be written as:

Hence, apart from unobserved variables , the computation of does not depend on other unobserved variables.

Let denotes a contextual assignment , , , , . The range of , denoted , is the set of all full assignments constructed by assigning the unobserved variables in . Reconsider the contextual assignment of Example 17. Since is a Boolean random variable, the range of the contextual assignment is .

It is worth noting that a full assignment is a safe contextual assignment, where the set of unobserved variables and the residual evidence set are empty. In such a case, .

The next theorem requires contextual assignments to be mutually exclusive. Two contextual assignments and are mutually exclusive if .

Theorem 6.

Let be a set of mutually exclusive contextual assignments such that each full assignment , , , of the requisite network is under the range of a safe contextual assignment . Let , , , , denote assigned variables, unobserved variables and evidence in . Then the query to can be computed as follows:

| (6) |

where denotes .

We draw some important conclusions: i) can be exactly computed by performing the summation over safe contextual assignments; notably, variables in vary, and so do variables in ; ii) For all , the computation of does not depend on the context since no basis of is assigned in the context (by Theorem 5). Hence, can be computed independently. However, the context decides which evidence should be in the subset . That is why we can not cancel from the numerator and denominator.

5.2.2 Context-Specific Likelihood Weighting

First, we present an algorithm that simulates a DC() program and generates safe contextual assignments. Then we discuss how to estimate the expectations independently before estimating .

Simulation of DC() Programs

We start by asking a question. Suppose we modify the first and the fourth rule of Bayes-ball simulation, discussed in Section 3.2, as follows:

-

•

In the first rule, when the visit of an unobserved variable is from its child, everything remains the same except that only some parents are visited, not all.

-

•

Similarly, in the fourth rule, when the visit of an observed variable is from its parent, everything remains the same except that only some parents are visited.

Which variables will be assigned, and which will be weighted using the modified simulation rules? Intuitively, only a subset of variables in should be assigned, and only a subset of variables in should be weighted. But then how to assign/weigh a variable knowing the state of only some of its parent. We can do that when structures are present within CPDs of , and these structures are explicitly represented using clauses in a DC() program . Recall that the proof procedure, discussed in Section 5.1, can sample random variables without sampling some of their ancestors. Hence, the key idea is to visit only some parents (if possible due to structures); consequently, those unobserved parents that are not visited might not be needed to be sampled.

To realize that, we need to adapt the Bayes-ball simulation such that it works on DC() programs. However, there is a problem: is a set of clauses, and no explicit graph is associated with it on which the Bayes-ball can be applied. Fortunately, we can infer direct influence relationships using the dependency set of , which is automatically constructed, as discussed in Section 4.2. The adapted simulation for DC() programs is defined procedurally in Algorithm 2. The algorithm visits variables from their parents and calls the top-down proof procedure (Algorithm 3) to visit variables from their children. Like Bayes-ball, these algorithms also mark variables on top and bottom to avoid repeating the same action.

-

•

Simulates a DC() program based on inputs: i) : a query; ii) : evidence.

-

•

Let be the dependency set of .

-

•

The procedure maintains global data structures: i) , a table that records assignments of variables (); ii) , a set of variables whose children to be visited from parent; iii) , a set of variables marked on top; iv) , a set of variables marked on bottom.

-

•

Output: i) that can be either or ; ii) : a table of weights of diagnostic evidence ().

-

1.

Empty .

-

2.

If prove-marked-ground() is then else .

-

3.

While is not empty:

-

(a)

Remove from and add to .

-

(b)

For all such that :

-

i.

If is observed with value in and :

-

A.

Choose such that prove-marked-ground() is . Add to .

-

B.

Let be the likelihood at according to distribution . Record .

-

A.

-

ii.

If is not observed in and : add to .

-

i.

-

(a)

-

4.

Return .

-

•

Proves a conjunction of ground atoms , consequently, visits variables from child.

-

•

Accesses , , and as defined in Algorithm 2.

-

•

Returns if there is a choice that makes empty; otherwise the procedure fails.

-

1.

While is not empty:

-

(a)

Select the first atom from .

-

(b)

If is of the form :

-

i.

If is observed in and its observed value is : remove from .

-

ii.

Else if :

-

A.

If : remove from .

-

A.

-

iii.

Else:

-

A.

Add to .

-

B.

Choose with in the head.

-

C.

Set .

-

A.

-

i.

-

(c)

Else If is of the form :

-

i.

Sample a value from , record , and remove from .

-

ii.

If : add to

-

i.

-

(a)

-

2.

Return .

-

•

Generates residual evidence’s weights based on input: i) , a list of residual evidence. This procedure accesses of Algorithm 2.

-

•

Output: i) , a table of residual evidence’s weights.

-

1.

For all random variables in .

-

(a)

Let be the value observed for in .

-

i.

Choose such that prove-marked-ground() is .

-

ii.

Let be the likelihood of according to distribution . Record .

-

i.

-

(a)

-

2.

Return .

Since the simulation of follows the same four rules of Bayes-ball simulation except that only some parents are visited in the first and fourth rule, we show that

Lemma 7.

Let be a set of observed variables weighed and let be a set of unobserved variables, apart from query variables, assigned in a simulation of , then,

The query variables are always assigned since the simulation starts with visiting these variables as if visits are from one of their children. To simplify notation, from now on we use to denote the subset of variables in that are assigned, to denote the subset of variables in that are weighted in the simulation of . to denote , and to denote We show that the simulation performs safe contextual assignments to requisite variables.

Theorem 8.

Partial assignments , , , , generated in simulations of DC() programs are safe contextual assignments.

The proof of Theorem 8 relies on the following Lemma.

Lemma 9.

Let be a DC() program specifying a distribution . Let be disjoint sets of parents of a variable . In a simulation of , if is sampled/weighted, given an assignment , and without assigning , then,

Furthermore, two contextual assignments generated in two simulations of a DC() program are either identical or mutually exclusive. This is because the algorithm behind the two simulations is the same, so both will generate identical contextual assignments unless a different value is sampled for at least one unobserved variable. However, the two contextual assignments will clearly become mutually exclusive when a different value is sampled for an unobserved variable.

Hence, just like the standard LW, we sample from a factor of the proposal distribution , which is given by,

where if . It is precisely this factor that Algorithm 2 considers for the simulation of . Starting by first setting , their observed values, it assigns and weighs in the topological ordering. In this process, it records partial weights , such that: and . Given partially weighted samples from , we could estimate using Theorem 6 as follows:

| (7) |

However, we still can not estimate it since we still do not have expectations . Fortunately, there are ways to estimate them from partial weights in . We discuss one such way next.

Estimating the Expected Weight of Residuals

We start with the notion of sample mean. Let be a data set of observations of weights of diagnostic evidence drawn using the standard LW. How can we estimate the expectation from ? The standard approach is to use the sample mean: . In general, can be estimated using the estimator: . Since LW draws are independent and identical distributed (i.i.d.), it is easy to show that the estimator is unbiased.

However, some entries, i.e., weights of residual evidence, are missing in the data set obtained using CS-LW. The trick is to fill the missing entries by drawing samples of the missing weights once we obtain . More precisely, missing weights in row of are filled in with a joint state of the weights. To draw the joint state, we use Algorithm 4 and call weight-res-ground() to visit observed variables from parent. Once all missing entries are filled in, we can estimate using the estimator as just discussed. Once we estimate all required expectations, it is straightforward to estimate using Equation 7.

Interpretation

At this point, we can gain some insight into the role of CSIs in sampling. They allow us to estimate the expectation separately. We estimate it from all samples obtained at the end of the sampling process, thereby reducing the contribution makes to the variance of our main estimator . The residual evidence would be large if much CSIs are present in the distribution; consequently, we would obtain a much better estimate of using significantly fewer samples. Moreover, drawing a single sample would be faster since only a subset of requisite variables is visited. Hence, in addition to CIs, we exploit CSIs and improve LW further. We observe all these speculated improvements in our experiments.

6 Inference in First-Order DC# Programs

-

•

Simulates a DC program based on inputs: i) , a ground query; ii) : evidence.

-

•

Let be the dependency set of .

-

•

The procedure maintains global data structures: i) , a table that records partial assignments of unobserved variables; ii) , a set of variables whose children to be visited from parent; iii) , a set of variables marked on top; iv) , a set of variables marked on bottom; v) , a table that records variables’ distributions.

-

•

Output: i) that can be either or ; ii) : a table of weights of diagnostic evidence ().

-

1.

Empty . Let be combining rules used for .

-

2.

If prove-marked() fails then else

-

3.

While is not empty:

-

(a)

Remove from and add to

-

(b)

For all such that :

-

i.

If is observed to be in and :

-

A.

Add to .

-

B.

For all (renamed) clause such that mgu unifies and : call prove-marked()

-

C.

Let be distributions for recorded in table , and let be the likelihood at according to . Record .

-

A.

-

ii.

If is not observed in and : add to

-

i.

-

(a)

-

4.

Return

This section extends CS-LW to first-order DC# programs where clauses need not be mutually exclusive. The extended algorithm is called first-order context-specific likelihood weighting (FO-CS-LW).

Using tools of logic such as unification and substitution, it is easy to simulate first-order programs without completely grounding them first. The simulation process defined in Algorithm 5 does that. It uses dependency sets of programs to visit RVs from parents and calls Algorithm 7 to visit RVs from children. The RV sets of programs are used to identify RVs defined by programs. There are two important features of the top-down proof procedure with logical variables defined in Algorithm 7, which are worth highlighting.

Firstly, it computes answer substitutions of a query , that is, the substitutions of the refutations of the query restricted to the variables in the query. To realize that, instead of the query, the initial goal is of the form:

where are the logical variables that appear in the query. This allows the procedure to return the answer when the body of goal is empty after applying the resolution rules. This is just like the proof procedure for definite programs with logical variables (?).

Secondly and more importantly, the procedure searches and collects all distributions defined for an RV in a global variable before sampling values of the RV from the combined distribution obtained using the combining rules. This is as per the semantics of DC# programs, and in this way, the algorithm also exploits ICIs.

The generation of residual evidence’s weights is defined in Algorithm 7.

-

•

Proves a conjunction of atoms with variables .

-

•

Accesses , , , and as defined in Algorithm 5.

-

•

Returns substitutions of variables if refutation exists; otherwise fails.

-

•

Let be an RV set of .

-

1.

Set to a clause

-

2.

While the body of is not empty:

-

(a)

Suppose is . Select

-

(b)

If is an atom of the form :

-

i.

Choose a grounding substitution such that

-

ii.

If is observed in : let be the observed value.

-

iii.

Else if : let be .

-

iv.

Else:

-

A.

For all (renamed) clause such that mgu unifies and : call prove-marked()

-

B.

Let be distributions for recorded in table . Let be value sampled from . Record .

-

C.

Add to . If then add to

-

A.

-

v.

If mgu unify and : set

-

i.

-

(c)

Else if is of the form : // will always be ground here

-

i.

Record and set

-

i.

-

(d)

Else if is of the form and evaluates to true:

-

(a)

-

3.

Return when is

-

•

Generates residual evidence’s weights based on input: i) , a list of residual evidence. This procedure accesses and of Algorithm 5.

-

•

Output: i) , a table of residual evidence’s weights.

-

1.

For all random variable in .

-

(a)

Let be the value observed for in .

-

i.

For all (renamed) clause such that mgu unifies and : call prove-marked()

-

ii.

Let be distributions for recorded in table , and let be the likelihood at according to . Record .

-

i.

-

(a)

-

2.

Return .

Dealing with Continuous RVs

Till now, we have not talked about inference in programs with continuous RVs. Nevertheless, the notions discussed so far are sufficient to explain inference in such programs. Likelihood weighting naturally extends to continuous domains (?). We just need rules to resolve comparison atoms of the form that appear in the body of clauses. These rules are already present in the proof procedure.

To ensure that FO-CS-LW correctly estimates the probabilities, we need to ensure that the simulation of DC# programs also generates safe contextual assignments that are identical or mutually exclusive. For this, we just need to ensure that Lemma 9 also holds for the DC# programs’ simulation.

Theorem 10.

Lemma 9 is also true for simulation of DC# programs.

7 Empirical Evaluation

In this section, we empirically evaluate our inference algorithms and answer several research questions.

7.1 How do the sampling speed and the accuracy of estimates obtained using CS-LW compare with the standard LW in the presence of CSIs?

To answer it, we need BNs with structures present within CPDs. Such BNs, however, are not readily available since the structure while designing inference algorithms is generally overlooked. We identified two BNs from the Bayesian network repository (?), which have many structures within CPDs: i) Alarm, a monitoring system for patients with 37 variables; ii) Andes, an intelligent tutoring system with 223 variables.

LW CS-LW BN N MAE Std. Time MAE Std. Time Alarm 100 0.2105 0.1372 0.09 0.0721 0.0983 0.06 1000 0.0766 0.0608 0.86 0.0240 0.0182 0.53 10000 0.0282 0.0181 8.64 0.0091 0.0069 5.53 100000 0.0086 0.0067 89.93 0.0034 0.0027 57.64 Andes 100 0.0821 0.0477 1.07 0.0619 0.0453 0.22 1000 0.0257 0.0184 10.62 0.0163 0.0139 2.20 10000 0.0087 0.0069 106.55 0.0058 0.0042 22.62 100000 0.0025 0.0015 1074.93 0.0020 0.0016 233.72

We used the standard decision tree learning algorithm to detect structures and overfitted it on tabular-CPDs to get tree-CPDs, which was then converted into clauses. Let us denote the program with these clauses by . CS-LW is implemented in the Prolog programming language, thus to compare the sampling speed of LW with CS-LW, we need a similar implementation of LW. Fortunately, we can use the same implementation of CS-LW for obtaining LW estimates. Recall that if we do not make structures explicit in clauses and represent each entry in tabular-CPDs with clauses, then CS-LW boils down to LW. Let denotes the program where each rule in it corresponds to an entry in tabular-CPDs. Table 1 shows the comparison of estimates obtained using (CS-LW) and (LW). Note that CS-LW automatically discards non-requisite variables for sampling. So, we chose the query and evidence such that almost all variables in BNs were requisite for the conditional query.

As expected, we observe that less time is required by CS-LW to generate the same number of samples. This is because it visits only the subset of requisite variables in each simulation. Andes has more structures compared to Alarm. Thus, the sampling speed of CS-LW is much faster compared to LW in Andes. Additionally, we observe that the estimate, with the same number of samples, obtained by CS-LW is much better than LW. This is significant. It is worth mentioning that approaches based on collapsed sampling obtain better estimates than LW with the same number of samples, but then the speed of drawing samples significantly decreases (?). In CS-LW, the speed increases when structures are present. This is possible because CS-LW exploits CSIs.

Hence, we get the answer to our first question: When many structures are present, and when they are made explicit in clauses, then CS-LW will draw samples faster compared to LW. Additionally, estimates will be better with the same number of samples.

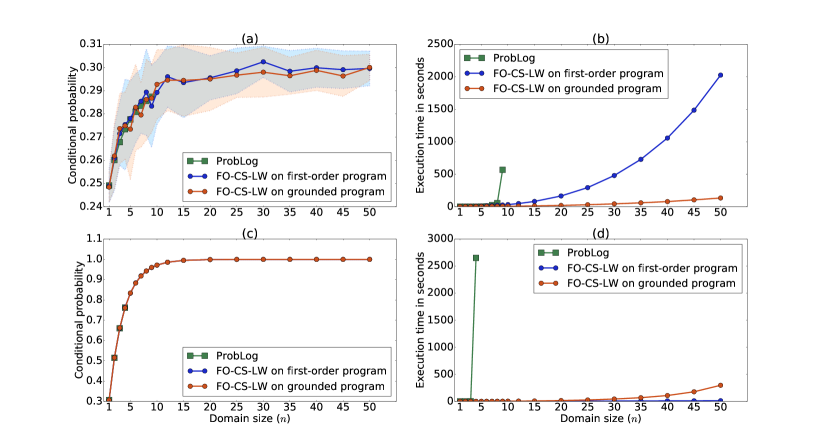

7.2 How does FO-CS-LW perform as the domain size increases?

The exact inference algorithms that PLP systems generally use for inference do not scale with domain sizes of logical variables in the program. Large domain sizes result in a huge ground program on which exact inference becomes intractable even for PLPs supporting only Boolean RVs. Thus, it is interesting to investigate how FO-CS-LW, an approximate inference algorithm, performs on such PLPs.

For this purpose, we compared FO-CS-LW with the inference algorithm used in ProbLog, one of the most popular PLP systems. This algorithm first grounds first-order programs and then performs exact inference to exploit structures of clauses in the programs. We used a ProbLog program shown in Figure 5 for this experiment. Note that in ProbLog, when multiple distributions are specified for an RV, they are combined using NoisyOR, and when no distribution is specified, the RV is set to false. So, using this combining rule, the ProbLog program of Figure 5 can be expressed as a DC# program. The domain size of each logical variable in the program is two since there are two clients, two accounts, and two loans. In such cases, instead of specifying the domain size of each logical variable separately, we will simply say that the domain size is two. Notice that relationships among clients, accounts, and loans are also probabilistic, so the number of RVs explicated by the program becomes huge as the domain size increases. More precisely, there are RVs when domain size is .

We also compared the performance of FO-CS-LW when applied directly to equivalent first-order programs versus when applied to the grounded programs. Indeed, when the full ground network is huge, and the requisite network is also huge, it is better first to ground the programs and then apply FO-CS-LW. This is because unifications used to reason in first-order programs are somewhat costly operations, which are performed once if programs are grounded first. This case is illustrated in Figure 6, where the probability of query ( , , ) is estimated and FO-CS-LW performs well if programs are grounded first. However, if the full ground network is huge, but the requisite network is very small, it is better to reason on the first-order level. This is because the cost of searching a few relevant clauses in a huge set of ground clauses exceeds the unification cost. This is the case when the query () is to compute given all other RVs (all RVs of type were set to (“false”), all RVs of type were set to , and rest RVs were set to (“true”). Furthermore, ProbLog could not compute probabilities beyond the domain size of on a machine with GB main memory, whereas FO-CS-LW quickly scaled to a domain size of 50.

One might expect that FO-CS-LW would perform poorly as domain size increases, and more samples would be required to get a reasonable estimate of probabilities. Figure 6 suggests the opposite. Using the same number of samples, the standard deviation from the mean does not increase as domain size increases. This is because FO-CS-LW exploits symmetries that arise due to noisy OR. Notice that exact probabilities do not change much as domain size increases because unique parameters do not increase even though the domain size increases and the number of parameters increases.

We conclude that FO-CS-LW scales with the domain size and can be useful on problems where the ProbLog inference algorithm fails.

7.3 How does FO-CS-LW compare to the state-of-the-art inference algorithms for hybrid relational probabilistic models?

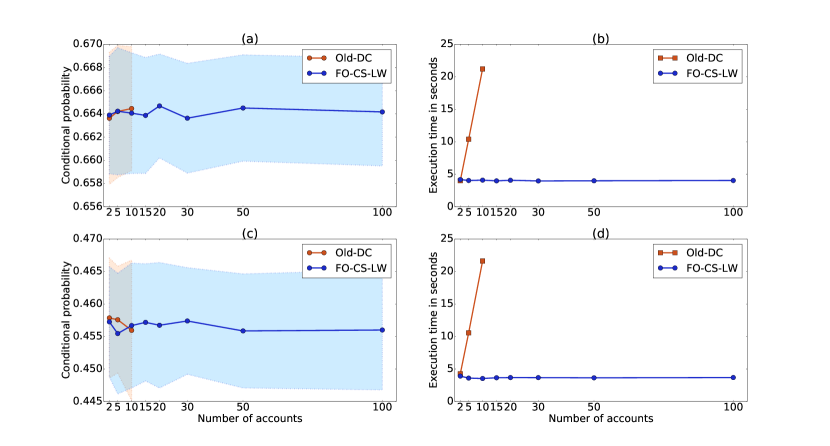

Those exact inference algorithms that exploit CSIs are not readily applicable to hybrid relational probabilistic models. There are not many open-source implementations of inference algorithms for such models555The publicly available code for BLPs is based on SICStus Prolog 3, the version that SICStus no longer supports. So, it is difficult to run the code.. The exploitation of first-order CSIs and symmetries arising due to aggregations in such models is challenging, and to the best of our knowledge, no algorithm can exploit them in such models. To some extent, the likelihood weighting-based inference algorithm developed for the old version of DC can exploit them (?). However, it does not filter out irrelevant evidence before inference, which is crucial in the case of relational databases. So, in this experiment, we aim to investigate how much FO-CS-LW improves upon old-DC’s inference algorithm.

For this purpose, we used a real-world relational data generated by processing the financial database from the PKDD’99 Discovery Challenge. This data set is about services that a bank offers to its clients, such as loans, accounts, and credit cards. It contains information of four types of entities: clients, accounts, loans and districts. Ten attributes are of the continuous type, and three are of the discrete type. The data set contains four relations: that links clients to accounts; that links accounts to loans; that links clients to districts; and finally that links clients to loans.

We learned a model in the form of distributional clauses as described in (?) from the financial data set. The learned model, which was a program, specified a probability distribution over all attributes of all instances of the entities in the data set. Since the program was learned just as described in (?), relationships among entities could not be probabilistic. Furthermore, clauses in the program were mutually exclusive, and aggregation atoms and statistical model atoms were used in the bodies of the clauses. Negations were allowed in the bodies to deal with missing values or missing relationships. Details about these advanced constructs are present in Appendix B. A snippet of the learned program is shown in Figure 9.

Next, we created multiple subsets of the financial data set with varying numbers of accounts. These subsets were created by considering to be the central entity. All information about clients, loans, and districts related to an account appeared in the same subset. All subsets had an account that was linked with a loan . Two queries to the learned program were considered: i) () given the rest subsets of data, ii) () given the rest subsets of data. Figure 7 shows the comparison of estimates obtained for queries and . The old-DC suffered arithmetic underflow as observed data increased, whereas FO-CS-LW scaled quite well. An important observation, in this case, is that the execution time of FO-CS-LW does not increase by adding more data. This is because real-world data is often not highly relational, e.g., clients generally have one or two accounts, not ten accounts. This is the case here. By adding more data, we are just adding data irrelevant to account . FO-CS-LW that exploits CIs can detect that, but the old-DC inference engine can not.

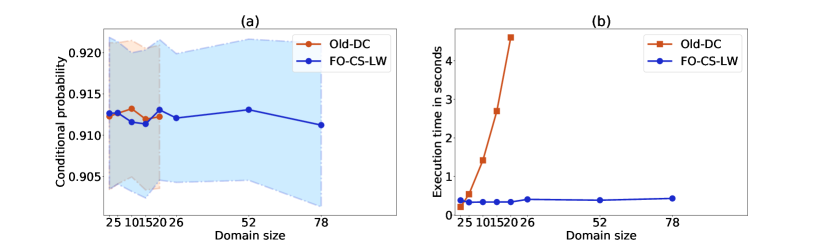

Similar observations were made when we used the program learned from the real-world NBA data set as described in (?). This data set is about basketball matches from the National Basketball Association (?). It records information about matches played between two teams and actions performed by each player of those two teams in the matches. This data set also contains relations and discrete-continuous attributes. We created multiple subsets of the data set with varying numbers of actions (the domain size). These subsets were created by considering actions to be the central entity. All subsets had actions of a player with id in game . The query that we considered was: () given the rest subsets of data. As shown in Figure 8, the observations are similar to those made for the financial dataset.

Thus, we conclude that when a significant amount of independencies are present in hybrid relational probabilistic models, FO-CS-LW outperforms the state-of-the-art inference algorithm of Old-DC.

8 Related Work

We describe relationships of the DC# framework introduced here with previous works in terms of representation and inference.

8.1 Relation to Representation Languages

Several relational representation languages based on aggregation functions and combining rules have been introduced in the past. Examples include probabilistic relational models (?, PRMs), directed acyclic probabilistic entity-relationship models (?, DAPER), probabilistic relational language (?, PRL), Bayesian logic programs (?, BLPs), and first-order conditional influence language (?, FOCIL). These languages consist of two components: a qualitative component representing the relational structure of the domain (either using graphs or definite clauses) and a quantitative component specifying conditional probability distributions (CPDs) in the tabular form. So, they do not qualitatively represent the structures present within the CPDs.

A tree or a rule-based representation lets us represent the structures qualitatively (?, ?, ?). That is why, probabilistic logic programming (PLP) has received much attention. Over the past three decades, many PLP languages have been proposed: PHA (?), Prism (?), LPADs (?), ProbLog (?), ICL (?), CP-Logic (?). However, only a few of them support both discrete and continuous RVs: HProbLog (?), DC (?, ?), Extended-Prism (?), Hybrid-cplint (?), (?). Nonetheless, the hybrid PLPs that have been studied in the past do not support combining rules, which is a core component of PLPs. BLPs do support combining rules, but then they do not qualitatively represent the structures. The syntax of DC# is the same as the syntax of DC introduced by (?), but the semantics is different as DC# supports combining rules. The semantics of DC# is based on BLPs, so one can view DC# programs as BLPs qualitatively representing structures. Furthermore, a huge fragment of Problog programs, one of the most popular PLPs, is expressible as DC# programs. Annotated disjunctions and directed cycles are not supported in DC# currently.