Parameters identification for an inverse problem arising from a binary option using a Bayesian inference approach

Abstract

No–arbitrage property provides a simple method for pricing financial derivatives. However, arbitrage opportunities exist among different markets in various fields, even for a very short time. By knowing that an arbitrage property exists, we can adopt a financial trading strategy. This paper investigates the inverse option problems (IOP) in the extended Black–Scholes model. We identify the model coefficients from the measured data and attempt to find arbitrage opportunities in different financial markets using a Bayesian inference approach, which is presented as an IOP solution. The posterior probability density function of the parameters is computed from the measured data. The statistics of the unknown parameters are estimated by a Markov Chain Monte Carlo (MCMC) algorithm, which exploits the posterior state space. The efficient sampling strategy of the MCMC algorithm enables us to solve inverse problems by the Bayesian inference technique. Our numerical results indicate that the Bayesian inference approach can simultaneously estimate the unknown trend and volatility coefficients from the measured data.

Keywords Option pricing Inverse Problem Bayesian Inference Approach

1 Introduction

he technique of inverse problems for a partial differential equation of a parabolic type is developed and used in various fields, such as Inverse heat transfer problems(IHTP), Inverse heat conduction problems(IHCP), Inverse option problems(IOP), etc[1, 2, 4, 8].

In this paper we consider the backward parabolic equation:

| (1) |

where is the price for a derivative, such as an option, bond, interest rate, futures, foreign exchange, etc. Moreover, in the underlying asset price, is the time, and are the drift and volatility coefficient of the process , the interest rate is a nonnegative constant, and is the strike price and is the maturity of the underlying asset, and is a suitable initial condition.

Now, we are interested in the following inverse option problem(IOP): Let the current time be given , and determine simultaneously and from the observation of data where is the interval.

IOP in mathematical finance were started by Dupire [8]. He derived the option premium as a solution to the dual equation of Black-Schoels equation, which is in (1), with respect to the strike price and maturity T as follows:

| (2) |

If the option price and its derivative can be determined for all possible and , then the local volatility function can be directly derived from Eq.(2) as

| (3) |

Using this approach, we can deduce the local volatility function from the quoted option prices in the financial market. Bouchouev and Isakov [4], Bouchouev et al. [5], and Ota and Kaji [24], by using a linearization method, considered the following form of the time–independent local volatility function :

| (4) |

where is a small perturbation of the constant volatility . Moreover, Mitsuhiro and Ota [23], Korolev et al. [17] and Doi and Ota [9] used the extended Black–Scholes equation (1) and then reconstructed the drift function by linearization method. The above studies provided point estimates of unknown parameters by exact determination or least squares optimization, without rigorously examining and considering the measurement errors in the inverse solutions. In [25], we considered the Option Problem, which has an initial condition in (1) such as

| (5) |

and simultaneously estimated the unknown drift and volatility coefficients from the measured data by applying Bayesian inference approach.

In this paper, we investigate the Binary Option Problem, which has an initial condition in (1), where is the Heviside function, that is,

| (6) |

And we attempt to derive the option pricing equation of so-called Dupire type which we were unable to derive in [25], and to simultaneously estimate the drift and volatility coefficients from the measured data. We can apply results of this study to the problem that we estimate the market risk from the pricing of derivatives such as interest rate.

Bayesian inference approach solves an inverse problem by formulating a complete probabilistic description of the unknowns and uncertainties from the given measured data (see [16]). Incorporating the likelihood function with a prior distribution, the Bayesian inference method provides the posterior probability density function (PPDF). Owing to the recent developments in Bayesian inference work, including Bayesian inference approach by efficient sampling methods such as Markov Chain Monte Carlo (MCMC), we can apply the Bayesian inference technique to inverse problems in remote sensing [11], seismic inversion [21], heat conduction problems [29], [30] and various other real–world problems. Moreover, several prior publications such as [6, 14, 15, 28, 27] are related to option pricing based on Bayesian inference. In those publications, the option prices are usually computed by using the analytical solution (or so-called Black-Scholes formula) or applying of Monte Carlo simulation of original stochastic differential equation under an assumption which the volatility is constant.

This paper is divided into five parts. Our inverse problem is mathematically formulated in Section 2. Section 3 outlines the general Bayesian framework for solving inverse problems and discusses the numerical exploration of the posterior state space by the MCMC method. In Section 4, we discretize our inverse problem and reconstruct the parameters by a numerical algorithm. We then discuss various aspects of our results through numerical examples. Concluding remarks are given in Section 5.

2 Mathematical formulation of IOP

In this paper, we consider that the volatility is a constant ( and the initial condition is a step function in (1):

| (7) |

We set

| (8) |

and then satisfies the differential equation (7), and

| (9) |

According to Friedman[10], satisfies for fixed as a function of the following differential equation and initial condition:

| (10) |

Then, we use the definition of , and integrate the equation (10) from to . The third term in the left-hand side can be integrated by parts as follows

where we have used the following behaviour at infinity

| (11) |

Consequently, we can obtain the following dual equation for

| (12) |

Now, the substitution

Then, we consider the following problem IOP:

Problem

If we give the data on at then identify and satisfying (13)

However, due to the nonlinearity of this inverse problem, the uniqueness and existence of its solution are hard to prove. In this paper we attempts to reconstruct the parameters by a statistical method simultaneously estimates and from the measured data .

Let us define dimensional vectors , and as follows:

where are the measurement points at , solves the Cauchy problem (13) for the unknown parameters and is the uncertainty (noise) in the market, assumed as white Gaussian noise with a known standard deviation . We then seek the parameters , which assumedly represent the true value of , such that

| (14) |

3 Bayesian inference approach to IOP

The Bayesian inference approach is now widely used with great successes for solving a variety of inverse problem (see for example [16]). The solution of the Bayesian inference approach is estimated not as single-valued, but as the posterior conditional mean (CM)

| (15) |

of the unknown parameters given the measured data , where is the conditional density function, which is called the posterior probability density function (PPDF) in this study. Now, according to the Bayes’ theorem, PPDF is defined as follows:

| (16) |

i.e. the posterior probability of a hypothesis is proportional to the product of its likelihood and its prior probability. The likelihood function is then given as

| (17) |

In some case, since we don’t know much about a prior density function , it is simply assumed as , where is a sufficiently large positive constant. Thus, the PPDF of the parameters is the same as the likelihood function as follows (cf. [16]):

| (18) |

3.1 MCMC methods

It is hard to know the explicit form of , Markov chain Monte Carlo (MCMC) algorithm given in Robert and Casella [26] can be applied to obtain a set of samples () and these independent samples can approach the distribution . Also the posterior conditional mean comes to

This is the solution of our IOP under the meaning of statistics.

In this paper, we employs a typical MCMC algorithm called the Metropolis–Hastings (M–H) algorithm (see Metropolis et al. [22]; Hastings [12]). M–H Algorithm given below builds its Markov chain by accepting or rejecting samples extracted from a proposed distribution. M–H Algorithm is generally used in Bayesian inference approach (cf. [16]).

M–H Algorithm

-

•

Step1: Generate (the normal distribution) with a given stander derivation for given .

-

•

Step2: Calculate the acceptance rate .

-

•

Step3: Update as with probability but otherwise set and re-sample from 1.

While running this M–H algorithm, we can find, by given any initial guess , the samples will come to a stable Markov chain after a burn-in time . In other word, unlike common Newton–type iterative regularization methods (for example, the Levenberg–Marquardt (LM) algorithm), the MCMC algorithm does not highly depend on the initial guess and the mean value

always reaches the global minimum after a sufficiently long sampling time (cf. [16]).

4 Numerical examples

In this section, we simultaneously estimate the unknown drift and volatility coefficients from the measured artificial data in (14), by using a Bayesian inference approach. Here, in order to investigate a small perturbation of the drift around the interest , we assume that the drift has the following type:

| (19) |

where is a small perturbation and .

4.1 Direct problems

In this section, we solve the direct problem for (13) by the numerical Crank–Nicholson scheme:

| (20) | |||

where and

| (21) |

| (22) |

| (23) |

Here, we took a uniform grid

with artificial Dirichlet boundary conditions at and , such as and , and .

| (26) |

4.2 Inverse problem solution by MCMC

In the following examples, we set

| (27) |

where are unknown constant parameters. Moreover the relative noise in all the measured artificial data is assumed as and , and the prior distribution of unknowns is

and the intervals and are large enough. General uniform distributions can be used for if we use the prior-reversible proposal that satisfies (see for example [13]). On the other hand, if we choose as a Gaussian distribution, this will turn out to be the Tikhonov regularization term in the cost function (see also for example [16]).

Then we simultaneously identify the parameters and from the measured artificial data .

For comparison, we particularly consider LM algorithm [18, 20]. That is, the recovery of is computed by the iteration given by

| (28) |

where is the Jacobian matrix and the parameter is nonnegative. This algorithm can be implemented for example by an inner embedded program lsqcurvefit in MATLAB .

Example 1:

In this example, we set

in the measured artificial data . We seek parameters in this case.

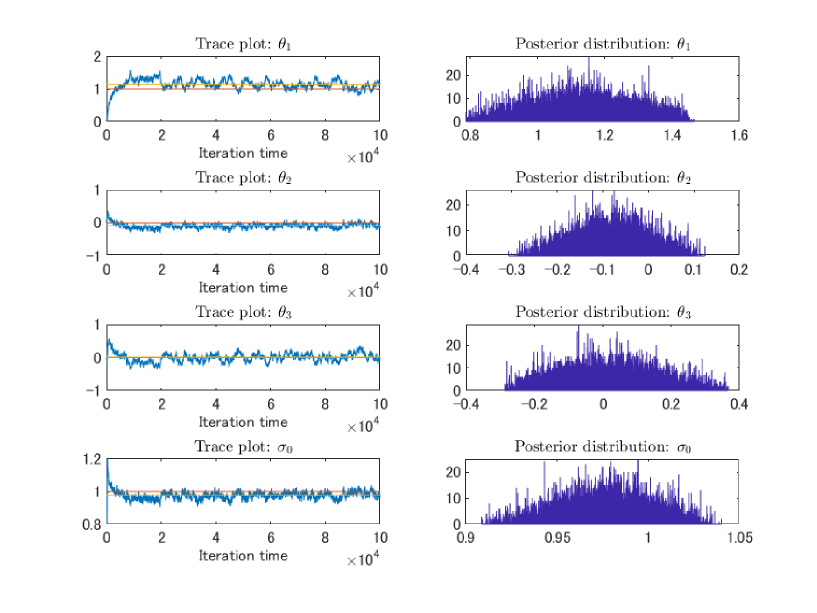

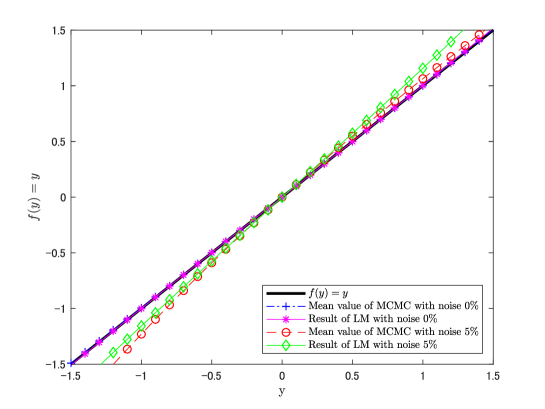

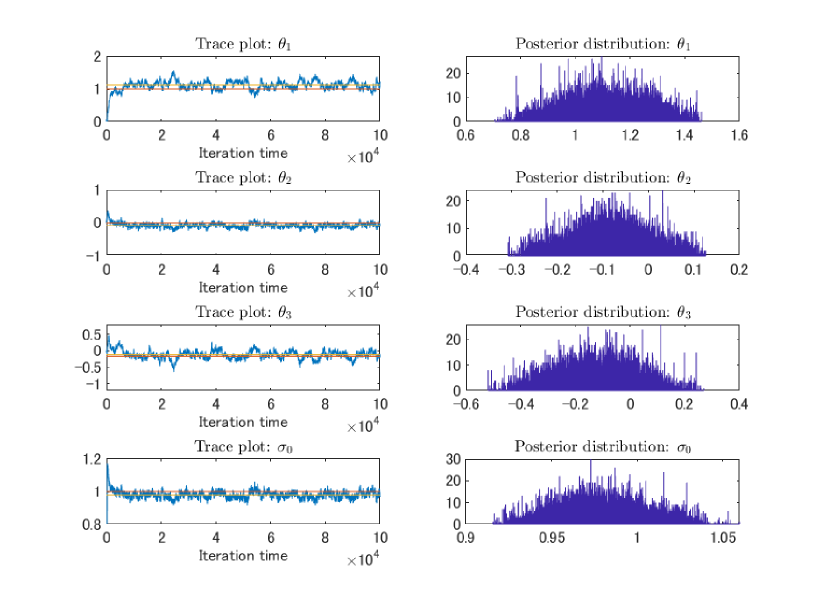

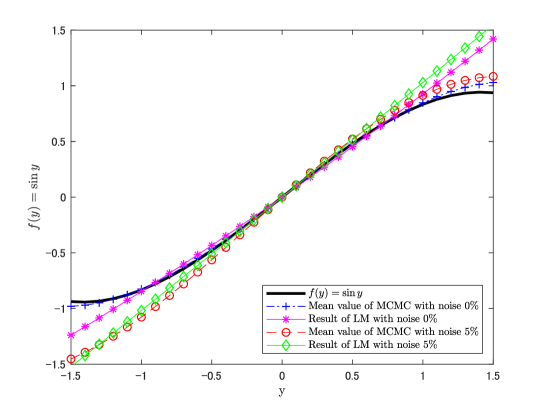

First, we set the initial guess of as to the value far from the expected value . Figure 1 are the trace plots of the chain for and PPDF. From results of trace plots, We can see that the chain mixes well. Moreover, from these results and Table 1, the recovery of represents an excellent approximation of the expected value , even if the measured data is contaminated with noise. Here, “Mean value(with or noise)” in Table 1 are the average of the value of the iteration time after burn-in time . For comparison, the converged recovery of obtained by LM algorithm with and noise are also provided in Table 1. Moreover, from Figure 2, we can see that the reconstruction of the drift is almost perfect near the center(i.e., at-the-money) in all cases. In particular, the solution obtained by MCMC is well reconstructed in the case of noise 0%.

| Parameters | ||||

| Initial guess | 0 | 0 | 0 | 0 |

| Mean value(with noise) | 0.9966 | 0.0029 | 0.0005 | 1.0008 |

| Result of LM with noise | 0.9968 | 0.0020 | 0.0052 | 1.0003 |

| Mean value(with noise) | 1.1346 | -0.0832 | 0.0121 | 0.9773 |

| Result of LM noise | 1.1434 | 0.0000 | 0.01357 | 0.9836 |

| The expected value | 1 | 0 | 0 | 1 |

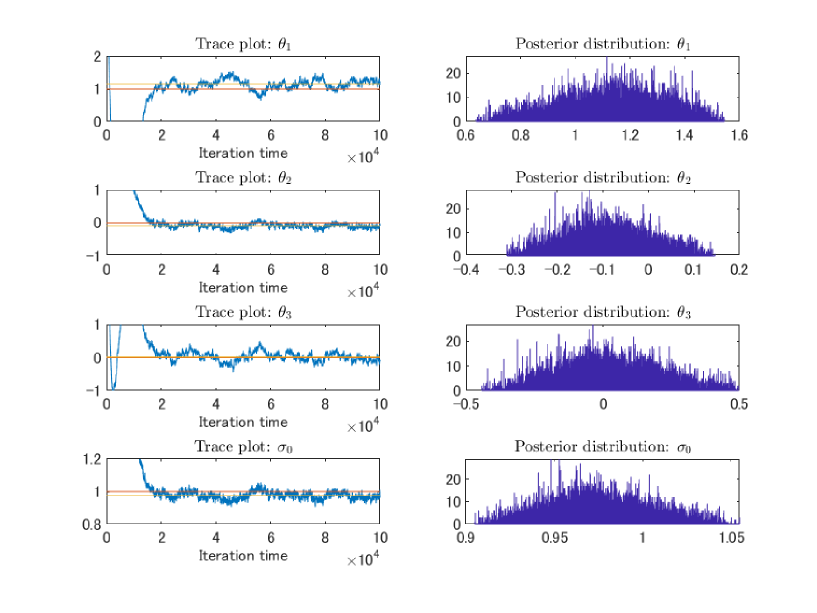

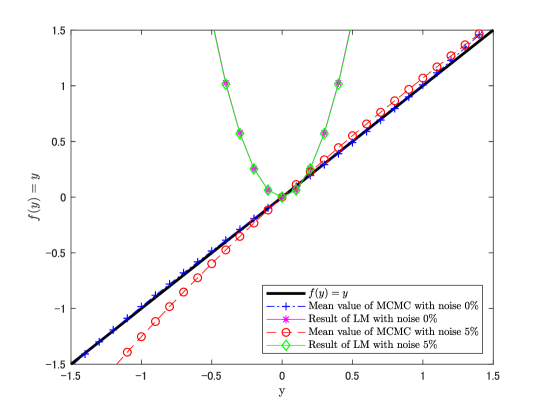

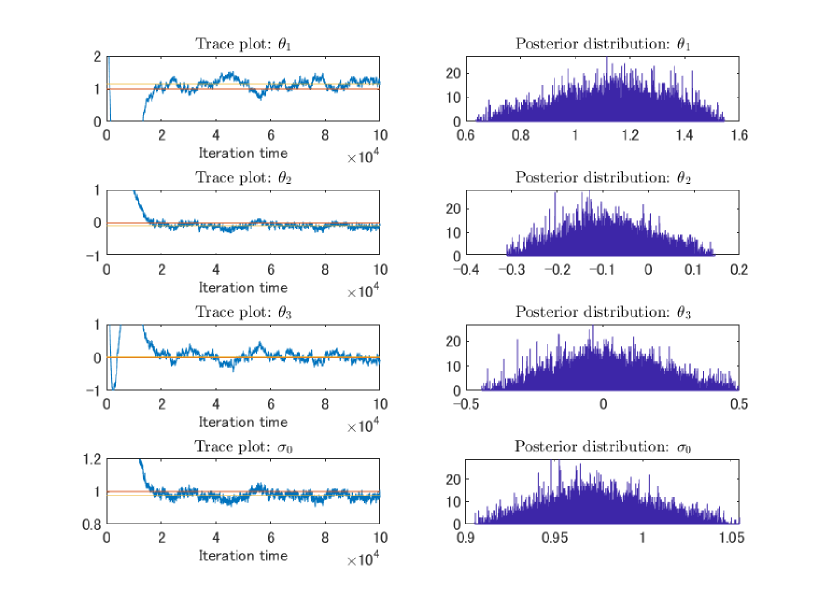

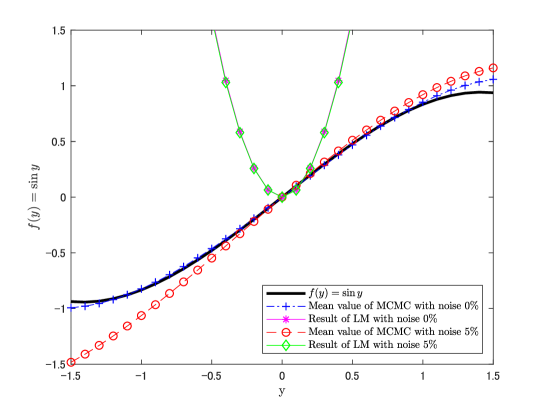

Next, the initial guess of was set to the value far from the expected value . The evolutions of the MCMC sampled and are shown in Figure 3, and we can see that the chain mixes well. Moreover recovered results for PPDF are presented in Figure 3, and Table 2. From these results the recovery of represents an excellent approximation of the expected value The recovery of obtained by the LM with and noise are also shown in Table 2. Moreover from Figure 4, we can see that the reconstruction is almost perfect near the center except for the case of LM.

| Parameters | ||||

| Initial guess | 3.5 | 3.5 | 3.5 | 3.5 |

| Mean value(with noise) | 0.9657 | 0.0124 | 0.0295 | 1.0045 |

| Result of LM with noise | 0.0000 | 6.4108 | 0.0000 | 2.8517 |

| Mean value(with noise) | 1.1451 | -0.0919 | 0.0159 | 0.9742 |

| Result of LM with noise | 0.0000 | 6.3361 | 0.0000 | 2.8430 |

| The expected value | 1 | 0 | 0 | 1 |

In both the initial guess and , from the results of the MCMC samples in Figure 1, Figure 3 and the posterior condition mean values in Table 1, 2 and Figure 2, 4, we can see that we succeeded in recovering parameters.

On the other hand, in the initial guess , the recoveries obtained by LM algorithm in Table 1 and Figure 2 succeeded as the case of MCMC algorithm. However, in the initial guess , we could not obtain the results of the recovering parameters by LM algorithm in Table 2, Figure 4. From these results, we observe that parameters are more sensitive to initial guess than MCMC algorithm and hence it is less easily recovered.

Example 2:

In this Example, we set

in the measured artificial data . In this case, we seek parameters . Here the expected values of are coefficients up to the third term of a Taylor series of the function around .

First, we set the initial guess of as to the value far from the expected value . Figure 5 are the trace plots of the chain for and the posterior probability density function. From results of trace plots, we can see that the chain mixes well. Moreover, from these results and Table 3, the recovery of represents an excellent approximation of the expected value , even if the measured artificial data is contaminated with noise. For comparison, the converged recovery of obtained by LM algorithm is also provided in Table 3. Further, from Figure 6, we can see that results of all cases are almost perfect near the center. Especially, parameters obtained by MCMC with 0% noise are recovered perfectly.

| Parameters | ||||

| Initial guess | 0 | 0 | 0 | 0 |

| Mean value(with noise) | 0.9694 | 0.0108 | -0.1331 | 1.0040 |

| Result of LM with noise | 0.8863 | 0.0404 | 0.0000 | 1.0148 |

| Mean value(with noise) | 1.1151 | -0.0818 | -0.1197 | 0.9782 |

| Result of LM with noise | 1.0234 | 0.0054 | 0.0000 | 0.9946 |

| The expected value | 1 | 0 | -1/6 | 1 |

Next, the initial guess of was set to the value far from the expected value . The evaluations of the MCMC sampled and are shown in Figure 7, and we can see that the chain mixes well. Moreover recovered results for PPDF are presented in Figure 7, and Table 4. From these results the recovery of represents an excellent approximation of the expected value The divergent recovery of obtained by LM algorithm in Table 4. Moreover, from Figure 8, we can see that the reconstruction is almost perfect near the center except for results of LM algorithm. In particular, results of MCMC with 0% noise are recovered perfectly.

| Parameters | ||||

| Initial guess | 3.5 | 3.5 | 3.5 | 3.5 |

| Mean value(with noise) | 0.9617 | 0.0143 | -0.1235 | 1.0048 |

| Result of LM with noise | 0.0000 | 6.5424 | 0.0000 | 2.8646 |

| Mean value(with noise) | 1.0804 | -0.07152 | -0.0885 | 0.9824 |

| Result of LM with noise | 0.0001 | 6.4377 | 0.0000 | 2.8553 |

| The expected value | 1 | 0 | -1/6 | 1 |

As in Example 1, in both the initial guess and from results of MCMC samples in Figure 5, 7 and the posterior condition mean values in Table 1, 3 and Figure 2, 4, we can see that we succeeded in recovering parameters.

On the other hand, in the initial guess , the recoveries obtained by LM algorithm in Table 3 and 6 almost succeeded as the case of MCMC algorithm as in Example 1. However, in the initial guess , we could not obtain the results of the recovering parameters by LM algorithm in Table 4 and 8. From this result, we observe that parameters are more sensitive to initial values than MCMC algorithm and hence it is less easily recovered as in Example 1.

5 Conclusion

In this study, we have established the method of simultaneous estimation of the unknown drift and volatility coefficients from the measured data, by using a Bayesian inference approach(MCMC-MH) based on a partial differential equation of parabolic type. In particular, we took into account an application to real financial markets and dealt with the case with Heaviside function as the initial condition, so-called binary option. In the instantaneous estimation of drift and volatility coefficients, we assumed that the volatility coefficient is a constant and the drift coefficient is a cubic function with three unknown parameters.

The posterior distributions of the unknown drift and volatility coefficients were recovered from the measured data by modeling the measurement errors as Gaussian random variables.

The posterior state space was explored by the MCMC–M–H method. As confirmed in the numerical results, the Bayesian inference approach(the MCMC algorithm) simultaneously estimated the unknown drift and volatility coefficients from the measured data than the Levenberg–Marquardt algorithm.

There are still several problems we have to settle. First, from the form of our model it is expected that we will be able to apply the results of this study to problems of term structure models for an interest rate. Moreover we will try to identify parameters of another financial model, for instance, such as the model including the dividend yield. Next, we will develop mathematical results (for instance, the uniqueness, stability, and existence) of IOP and extend our approach to two–dimensional Black–Scholes Equation such as "Spread Option". Finally, we have to study how to apply our results to the real financial market, and repeat tests.

The first author would like to acknowledge the supports from JSPS Grant-in-Aid for Scientific Research (C) 18K03439.

Declarations

-

•

Funding

The first author would like to acknowledge the supports from JSPS Grant-in-Aid for Scientific Research (C) 18K03439.

-

•

Conflict of interest/Competing interests

All authors declare that: (i) no support, financial or otherwise, has been received from any organization that may have an interest in the submitted work; and (ii) there are no other relationships or activities that could appear to have influenced the submitted work.

-

•

Availability of data and materials

The data that support the findings of this study are available from the corresponding author, [Yasushi Ota yasushio@andrew.ac.jp], upon reasonable request.

References

- [1] Alifanov M. O. 1997 Inverse Heat Transfer Problems, International Series in Heat and Mass Transfer, Springer Verlag.

- [2] Beck V. J., Blackwell B. and Clair Jr. C. R. 1985 Inverse Heat Conduction: Ill-Posed Problems, Wiley-Interscience.

- [3] Black F. and Scholes M. 1973 The pricing of options and corporate liabilities, Journal of Political Economy, 81, 637-659.

- [4] Bouchouev I. and Isakov V. 1999 Uniqueness, stability and numerical methods for the inverse problem that arises in financial markets, Inverse Problems, 15, R95-R116.

- [5] Bouchouev I., Isakov V. and Valdivia N. 2002 Recovery of volatility coefficient by linearization, Quantitative Finance, Vol2, 257-263.

- [6] Bunnin F. O., Guo Y. and Ren Y. 2002 Option pricing under model and parameter uncertainty using predictive densities Statistics and Computing, 12(1), 37–44.

- [7] Cui T., Fox C., and O’fSullivan M.J. 2011 Bayesian calibration of a large-scale geothermal reservoir model by a new adaptive delayed acceptance Metropolis Hastings algorithm, Water Resource Research, 47, W10521.

- [8] Dupire B. 1994 Pricing with a smil, Risk, 7 18-20.

- [9] Doi S. and Ota Y. 2018 Application of microlocal analysis to an inverse problem arising from financial markets Inverse Problems. 34, N11.

- [10] Friedman A. 1983 Partial Differential Equations of Parabolic Type, (Englewood Cliffs, N.J: Prentice-Hall).

- [11] Haario H., Laine M., Lehtinen M., Saksman E. and Tamminen J. 2004 Markov chain Monte Carlo methods for high dimensional inversion in remote sensing, Journal of the Royal Statistical Society: Series B (Statistical Methodology), 66, 591-608.

- [12] Hastings, W. 1970 Monte Carlo sampling methods using Markov chains and their application, Biometrika, 57, 97-109.

- [13] Iglesias M. A., Lin K and Stuart A. M. 2014 Well-posed Bayesian geometric inverse problems arising in subsurface flow, Inverse Problems, 30, 114001.

- [14] Jacquier E. and Jarrow R. 2000 Bayesian analysis of contingent claim model error, Journal of Econometrics, 94(1-2), 145–180.

- [15] Jacquier E. and Polson N. 2010 Bayesian methods in finance, Oxford handbook of Bayesian econometrics, 439–512 (Oxford University Press).

- [16] Kaipio J. and Somersalo E. 2005 Statistical and Computational Inverse Problems. (New York: Springer)

- [17] Korolev M., Kubo H. and Yagola G. 2012 Parameter identification problem for a parabolic equation-application to the Black-Scholes option pricing model, J. Inverse Ill-posed probl, 20 No.3, 327-337.

- [18] Levenberg, K. 1944 A method for the solution of certain non-linear problems in least squares, Quarterly Appl. Math., 2, 164–168.

- [19] Lishang J. and Youshan T. 2001 Identifying the volatility of underlying assets from option prices, Inverse Problems, 17, 137-155.

- [20] Marquardt D. 1963 An algorithm for least-squares estimation of nonlinear parameters, SIAM J. Appl. Math., 11, 431–441.

- [21] Martin J., Wilcox L.C., Burstedde C. and Ghattas O. 2012 A stochastic Newton MCMC method for large-scale statistical inverse problems with application to seismic inversion, SIAM Journal on Scientific Computing, 34(3), A1460-A1487.

- [22] Metropolis N., Rosenbluth A., Rosenbluth M., Teller A. and Teller E. 1953 Equations of state calculations by fast computing machines, J. Chem. Phys., 21(6), 1087-1092.

- [23] Mitsuhiro M. and Ota Y. 2015 Recovery of Foreign Interest Rates from Exchange Binary Options, Computer Technology and Application, 6, 76-88.

- [24] Ota Y. and Kaji S. 2016 Reconstruction of local volatility for the binary option model, J. Inverse Ill-posed probl., 24, No.6 727-742.

- [25] Ota Y., Jiang Y., Nakamura G. and Uesaka M. 2019 Bayesian inference approach to inverse problems in a financial mathematical model, International Journal of Computer Mathematics, submitted.

- [26] Robert, C. and Casella, G. 2004 Monte Carlo Statistical Methods. (Springer Texts in Statistics)

- [27] Tunaru R. 2015 Model risk in financial markets: From financial engineering to risk management, World Scientific Pub Co Inc.

- [28] Tunaru R. and Zheng T. 2017 Parameter estimation risk in asset pricing and risk management: A Bayesian approach, International Review of Financial Analysis, 53, 80–93.

- [29] Wang J. and Zabaras N. 2004 A Bayesian inference approach to the inverse heat conduction problem, International Journal of Heat and Mass Transfer, 47, Issues 17-18, 3927-3941.

- [30] Wang J and Zabaras N. 2005 Hierarchical Bayesian models for inverse problems in heat conduction, Inverse Problems, 21 183-206.