Approximating the first passage time density from data using generalized Laguerre polynomials

Abstract.

This paper analyzes a method to approximate the first passage time probability density function which turns to be particularly useful if only sample data are available. The method relies on a Laguerre-Gamma polynomial approximation and iteratively looks for the best degree of the polynomial such that the fitting function is a probability density function. The proposed iterative algorithm relies on simple and new recursion formulae involving first passage time moments. These moments can be computed recursively from cumulants, if they are known. In such a case, the approximated density can be used also for the maximum likelihood estimates of the parameters of the underlying stochastic process. If cumulants are not known, suitable unbiased estimators relying on -statistics are employed. To check the feasibility of the method both in fitting the density and in estimating the parameters, the first passage time problem of a geometric Brownian motion is considered.

keywords: stochastic process, cumulant, geometric Brownian motion, -statistic, recursive algorithm

2020 MSC: 65C20, 60G07, 62E17, 62M05

1. Introduction

The first-passage-time (FPT) problem arises in many applications in which a stochastic process starting in at time evolves in the presence of a threshold They range from finance to engineering including, among others, computational neuroscience, mathematical biology and reliability theory, see [41] for a comprehensive collection of results. The mathematical study of the FPT problem consists in finding the probability density function (pdf) of the random variable , defined by

| (1.1) |

There are several strategies to approach this problem, whose effectiveness depends on the properties of the stochastic process involved (see [42] for an extensive review). They range from the Doob’s representation formula [17] to the Siegert’s equation [46] that consists in a partial differential equation involving either the moments of or its Laplace transform. Closed-form expressions emerge only in a few cases [6] but numerical evaluation of can be provided as solution of non-singular second kind Volterra integral equation [7, 43, 21, 29, 14] or using Sturm-Liouville eigenfunction expansion series [33, 1, 32]. Due to the difficulty of the problem, asymptotic expressions of are studied using the Volterra integral equation [20, 38], Laplace transform techniques [34] or Large Deviation estimates [3, 16].

All these techniques rely on the knowledge of the nature of the stochastic process But if a random sample of FPTs is analyzed without any prior information on the stochastic dynamics generating the data, the identification of a model could be difficult to implement. In general classical tools as histograms or kernel density estimators are the first choices to make a guess on the shape of the FPT pdf and then postulate a model.

Following the latter approach, the aim of this paper is to propose a Laguerre-Gamma polynomial approximation to fit a suitable pdf on a random sample of FPTs. This proposal moves from some recent approaches [40, 12, 13] that use cumulants to obtain FPT pdf and related statistics.

Recall that if has moment generating function for all in an open interval about then its cumulants are such that

for all in some (possibly smaller) open interval about It is possible to recover cumulants up to order from moments up to the same order (and viceversa), using the general partition polynomials [9]. Therefore, from a theoretical point of view, there is a duality between these two numerical sequences, even if the expressions of cumulants are most of the time simpler than those of moments. Moreover, cumulants have nice properties compared with moments such as the semi-invariance and the additivity. Overdispersion and underdispersion as well as asymmetry and tailedness of the FPT pdf might be analized through the first few cumulants [35].

The approximation proposed in this paper has a twofold advantage. If the FPT moments/cumulants are not known, the special feature of this approach is the chance to recover an approximation of the FPT pdf starting from a sample of FPT data like the classical density estimators. Indeed estimates carried out from -statistics can replace the occurrences of cumulants in the polynomial approximation. Let us recall that the -th -statistic is a symmetric function of the random sample whose expectation gives the -th cumulant These estimators have minimum variance when compared to all other unbiased estimators and are built by free-distribution methods without using sample moments [31]. The method turns to be useful also if the model is known but the knowledge of the FPT moments is limited, as usually happens. In such a case, the approximation might be carried out by simulating the trajectories of the process through a suitable Monte Carlo method and using -statistics in place of cumulants. If the FPT moments/ cumulants are known or can be recovered from the Laplace transform of the FPT random variable , the method is essentially a way to find an approximated analytical expression of The approach works for a wide class of one dimensional stochastic processes and, of course, is intended for the cases in which the closed form expression of is not available. Differently from other methods, the approximating function results to be a pdf whatever order of approximation is reached. Therefore it is possible to implement a maximum likelihood procedure to carry out estimates of the parameters involved in the model.

To check the feasibility of our proposal we compare the approximated expressions (obtained analytically or estimated through -statistics) with a case in which the FPT pdf is known. In particular we use the closed analytical expression of the pdf of a Geometric Brownian motion (GBM) FPT through a constant boundary .

The GBM is a special case from the point of view of the FPT problem. In this case the Laplace transform of is known and can be inverted, obtaining a closed form expression for the FPT density. Moreover one can use the Doob’s transform since the GBM can be generated from a Brownian motion with drift (case for which the pdf of is known), it has stationary distribution and its parameters solve the Siegert’s equations. Moreover a Sturm-Liouville eigenvalue expansion for its infinitesimal generator exists [8], its can be found directly from the Volterra integral equation [24]. To test the performance of the approximated analytical expression here proposed, the choice of the GBM allows us to overcome the numerical difficulties that can arise performing simulations of the FPT, when exact method are not implemented [26]. In fact, in this case, the proposed polynomial approximation can be compared directly with a closed-form expression.

The paper is organized as follows. In Section 2 we resume the FPT problem for the GBM recalling the known results useful for carrying out the approximation including some new expressions for moments and cumulants relied on exponential Bell polynomial. In Section 3 we discuss sufficient and necessary conditions to recover the infinite series expansion of the GBM FPT pdf in terms of the generalized Laguerre polynomials and study the convergence of the method when this series is truncated at the order . In particular we investigate the chance to consider reference pdfs different from the usual Gamma density. Section 4 collects results and tools for an efficient iterative search of the best degree of approximation . Numerical results on Laguerre-Gamma approximation are given in Section 5. In particular we estimate simultaneously two parameters of the GBM using the maximum likelihood estimation starting from first passage time data. The method relies on the Laguerre-Gamma approximated FPT pdf and can be used even if is unknown. In this case it relies on -statistics.

2. The FPT problem for the Geometric Brownian Motion

The GBM is a regular diffusion process on . It can be obtained as a transformation of a Brownian motion and for this reason it is also called exponential Brownian motion [50]. In fact, if is a drifted Brownian motion, then the stochastic process

| (2.1) |

is said GBM with starting point and with infinitesimal mean and variance and , respectively [30].

The transition pdf is known to be a lognormal pdf with parameters and , obtained by solving the Fokker-Planck equation, which in the case of the GBM reduces to the canonical form of the heat equation. The transition pdf presents exponential decay in the variable so the Laplace transform exists for every .

Let us assume that the threshold is constant and In this case the Laplace transform of is given by [5]

which can be rewritten as

| (2.2) |

with

| (2.3) |

Since the moment generating function is such that from (2.2) has inverse gaussian distribution of parameters (the shape) and (the mean), that is

| (2.4) |

where denotes the FPT pdf from now on. Statistical properties of have been investigated in [48]. Thus moments of result to be

| (2.5) |

where is the modified Bessel function of second type [23]

| (2.6) |

under the conditions and Since [23], the following recursion formula holds for the FPT moments:

| (2.7) |

with and

A new and alternative expression of the FPT moments can be given using the partition polynomial [9]

| (2.8) |

where are the partial exponential Bell polynomials

| (2.9) |

with the sum taken over all sequences of non negative integers such that and

We are now ready to give the new (polynomial) closed-form expression of the moments of that relies on the simple expression of the cumulants, overcoming the evaluation of the in Eq.(2.5).

Proposition 2.1.

| (2.10) |

Proof.

From the power series expansion of with the moment generating function of , cumulants of result to be [48]

| (2.11) |

with Since with the lowering factorial, from (2.11) we also have

| (2.12) |

Moments are related to cumulants through the partial exponential Bell polynomials [11]

| (2.13) |

with given in (2.9). The result follows replacing (2.12) in (2.13) and using the well known property [10]. ∎

3. Series expansion

To approximate a pdf over using moments, a classical method [49] consists in expanding this function as an infinite series involving the generalized Laguerre polynomials defined for by

No sufficient conditions are discussed in [49] to ensure that the pdf can be expanded formally as an infinite series of generalized Laguerre polynomials, because the pdf is not known in general. This method has been applied to approximate the FPT pdf of a square-root process in [12] giving also some sufficient conditions to justify the approximation.

Here we take advantage of the knowdlege of the FPT pdf of a GBM (2.4) to discuss some conditions in order to use this method. A first step in this direction is to recall the classical results on the completeness and orthogonality of in the weighted Hilbert space equipped with the inner product see for example [44]. Using these properties, the following proposition provides the infinite series expansion of in terms of generalized Laguerre polynomials.

Proposition 3.1.

If

| (3.1) |

with then for

| (3.2) |

where is the gamma pdf with scale parameter and shape parameter

Proof.

Consider the weighted Hilbert space equipped with the inner product and set

By recalling that with the Kronecker delta function, the sequence turns to be complete and orthonormal in Condition (3.1) is equivalent to require since

| (3.3) |

Due to the completeness of the sequence, the pdf can be expanded in terms of that is

| (3.4) |

Expansion (3.2) follows after some algebraic manipulations of the rhs of (3.4). ∎

Corollary 3.2.

Proof.

Propositions 3.1 justifies the approximation of the FPT pdf with

| (3.6) |

a polynomial of degree for a suitable choice of Due to the orthogonality property of generalized Laguerre polynomials, we observe that for all and the first moments of are the same of

The main issue in the approximation (3.6) is the choice of the degree of the polynomial that we discuss numerically in the next sections. The higher is the order the better should be the approximation. Indeed using the Parseval’s formula [45] the error in replacing with for is such that

| (3.7) |

where denotes the norm in The following theorem improves (3.7) for suitable choice of

Theorem 3.3.

If and then there exists a constant such that

| (3.8) |

with

Proof.

Set and in order to write

According to Theorem 6.2.5 in [19], if for a fixed

| (3.9) |

then there exists a constant such that

| (3.10) |

By recursion, we have

| (3.11) |

where is a polynomial of degree such that

| (3.12) |

with and

Now set

Fix an integer Since we have for all and in particular condition (3.9) holds for Indeed using the modified Bessel function of second type (2.6) and the integral no. in [23], we have

| (3.13) | |||

Eq. (3.8) follows from (3.10) setting and

| (3.14) |

In (3.14), note that for as For the order of the modified Bessel function involved in might be positive, depending on the magnitude of Let us first suppose such that for all As for one has [15]

| (3.15) |

then

| (3.16) |

When grows, the dominant term in (3.16) is for and the result follows. If then might be splitted in with

where is such that and For we have for and includes the maximum number of terms, that is

| (3.17) | |||||

The dominant term in (3.17) is for and the asymptotic behaviour of is still of order . ∎

Remark 3.4.

Note that if the integral in (3.13) converges if and only if Indeed in such a case and in (3.13) reduces to

| (3.18) |

The integral on the rhs of (3.18) is convergent if and only if for all that is if and only if Therefore (3.8) still holds with In such a case we have

| (3.19) | |||||

as As the leading term in (3.19) is for we still have

Even if it is still possible to use the rhs of (3.2) due to the following proposition. Since the result is a reformulation of Theorem 2 in [12], the proof is omitted.

Proposition 3.5.

For and we have

3.1. Choosing a different reference pdf: the log-normal density

Since the gamma pdf is such that for differently from the FPT pdf for which we might test a different reference pdf to recover the polynomial approximation of A density with support and behaving as the FPT pdf of a GBM is the log-normal one with parameters and

| (3.20) |

To recover a polynomial approximation, we need to characterize the family of orthogonal polynomials with respect to the measure Unlike the generalized Laguerre ones, these polynomials are not classically known and have been computed for and in [18] and for arbitrary and in [2, 51] using a classic procedure (see for example [47, Th. 2.1.1], [39, Section 4]). Using the monic polynomials given in [51], the polynomial approximation results to be

| (3.21) |

where is a suitable normalization constant and

| (3.22) |

with the -Binomial coefficient

| (3.23) |

The main drawback of (3.21) is that the system is not complete in [2, Proposition 1.1]. Indeed the log-normal distribution is not fully characterized by its moments [27] and might converge to a density different from , but sharing the same moments as (see [18, Proposition 4.1] for a non trivial example of a family of densities for which the convergence fails). Note that (3.21) fails to approximate even a log-normal pdf [2, Fig 1.2].

3.2. Choosing a different reference pdf: the Inverse Gaussian density

Another possible choice for the reference density could be the Inverse Gaussian. In the special cases of the GBM this choice would be clearly extremely convenient since we actually know that the FPT has Inverse Gaussian distribution. In this case the choice may seem nearly cheating, but it is also the FPT density of the Brownian motion and it would make sense to use it as reference density. Unfortunately in [37] it is shown that the usual method of differentiating the density does not lead to an orthogonal polynomial system, and starting from the Laguerre polynomials leads to a system of orthogonal functions which is not complete. The only way to get a complete system of polynomials is by using the Gram–Schmidt orthogonalisation procedure, but the resulting polynomials are not easy to use (see also [22]). In [25] the authors propose a method to derive the polynomials that involves the so-called bi-orthogonality property but they do not discuss whether this construction leads to a basis.

Therefore, in the following we have considered only the gamma pdf as reference density.

4. Computational issues

In the software environment R, the package PDQutils contains a collection of tools for approximating pdf’s via classical expansions involving moments and cumulants. For the Laguerre polynomials, the PDQutils routine implements the following choice of and

| (4.1) |

In such a case, expansion (3.6) simplifies as a straightforward computation shows that and the first two moments of are equal to the first two moments of that is

| (4.2) |

If the PDQutils routine is used within an iterative procedure aiming to return the integer that allows a good approximation, such a procedure results computationally inefficient since the -th approximation cannot be obtained by updating the -th one .

Here, we propose a different approach that relies on nested products taking advantage of a different representation of the polynomial in (3.6). Indeed, combining the coefficients of with the same power of the terms of the polynomial in (3.6) can be rearranged as follows

| (4.3) |

and

| (4.4) |

Therefore is better evaluated using the recurrence relation

| (4.5) |

with the initial condition since the last value gives Also the coefficients can be computed using a recursion formula, as the following proposition shows.

Proposition 4.1.

For all we have

| (4.6) |

Proof.

For the GBM FPT random variable also the moments of the FPT random variable can be computed through recursion using (2.7). For different stochastic processes, if cumulants are known [12, 13], the following recursion might be implemented [11]:

| (4.10) |

Therefore, the updating of to might be performed by using the recursion (4.5), setting and updating the coefficients to

It must be noted that we cannot in practice take arbitrarily large, due to numerical errors incurred in calculating the coefficients . Obviously, this can be overcome by using infinite precision operations. Software tools like Mathematica allow for arbitrarily large but finite precision. However this swiftly becomes prohibitively slow. A way to push the iteration procedure up to the best order of numerical approximation relies on the subsequent normalization condition satisfied by the sequence

Proposition 4.2.

For all we have

| (4.11) |

Proof.

From the normalization condition of we have

The result follows by observing that the integrals in the lhs of (4.11) are the moments of the gamma pdf that is

∎

Condition (4.11) has been used to test the numerical stability of the computations, that is the iteration is ended as soon as this condition is no longer verified.

5. Numerical results

In this section the Laguerre-Gamma polynomial approximation (3.6) discussed previously is applied to the FPT pdf of the GBM. Since we have the closed form (2.4), we will be able to compare directly the approximation with the true density. We choose to employ in (3.6) in the form (4.3), that gives the advantage of a more efficient implementation. Moments are calculated using recursion (2.7).

As previously stated, the main issue in the approximation is the choice of the best degree of the polynomial approximation. Different possibilities arise. For example, we have considered using a convergence-based stopping criterion. It consists in choosing the smallest such that, for a fixed tolerance , we have

| (5.1) |

However, this criterion is affected by numerical instability, because the condition (5.1) is satisfied for large values of but the corresponding numerical amount of errors has already compromised the approximation. Consequently, we choose to employ the stopping criterion (4.11) as follows. Set

| (5.2) |

Since from Proposition 4.2, as stopping criterion we choose the smallest such that

| (5.3) |

For the parameters and according to (4.1) we have

| (5.4) |

Note that with these choices, we are in the limit case discussed in Remark 3.4 for what concerns the error.

To analyse the efficiency and the usefulness of the proposed method, in the following we consider two instances:

-

(1)

the FPT pdf has moments or cumulants known in a closed form;

-

(2)

the knowledge of the FPT moments or cumulants is limited to first few orders.

Indeed, for most of the stochastic processes the knowledge of the moments is limited to the mean and the variance or the expression of higher moments is cumbersome and not computationally convenient to be employed in recovering see for example [13]. In such cases the approximation might be carried out by simulating the trajectories of the process through a suitable Monte Carlo method and estimating the moments/cumulants of . In the last paragraph we suppose not known and use the approximation to perform parameter estimations using the maximum likelihood method.

5.1. Laguerre-Gamma polynomial approximation: known moments

In the following we will test the accuracy and efficiency of the approximation by comparing in (3.6) with the true FPT pdf in (2.4) through the following two approaches:

-

(a)

a graphical approach by comparing their plots,

-

(b)

a quantitative approach by computing .

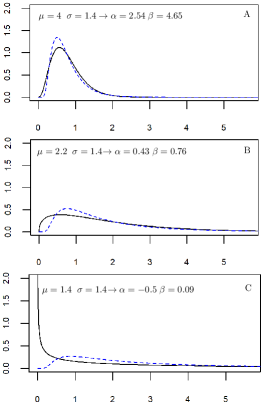

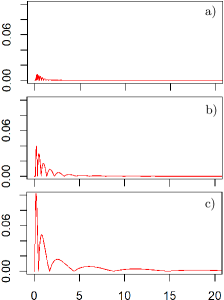

We show and study three different cases (A,B and C in Fig. 1), where we have fixed and .

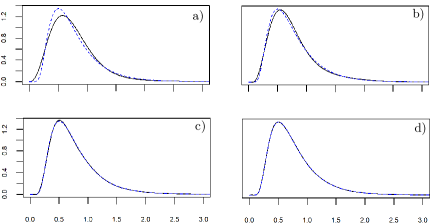

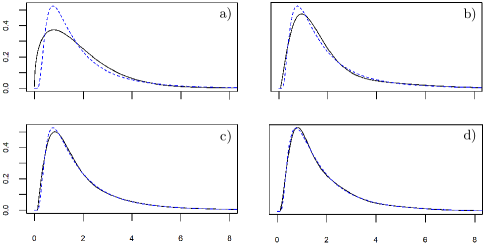

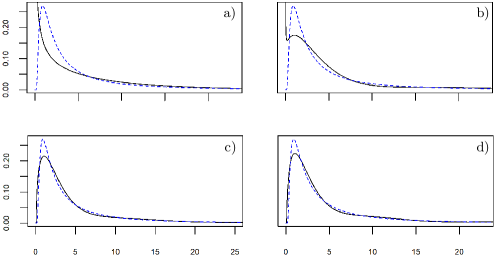

These examples show that, as the parameters change, the FPT pdf and the reference pdf can be significantly different. In Figs. 2, 3 and 4 we have plotted the polynomial approximation (black solid line) and the true density (blue dashed line) for the three mentioned cases using four different orders of approximation each time.

By comparing the three figures we observe that:

-

(a)

in case A, where the reference pdf and the FPT pdf have a similar behavior, a low degree guarantees a good approximation,

-

(b)

as decreases, the reference pdf loses its typical bell shape and deviates further away from the FPT pdf,

-

(c)

in all the considered cases the goodness of the approximation increases with as long as (4.11) is satisfied,

-

(d)

compared with the cases A and B, the case C proves to be the most difficult; in fact even for we do not match the peak of the FPT pdf . Indeed, according to Remark 3.4, in this case the order of convergence is as Theorem 3.3 does not hold. So to get a good approximation we should consider high values of but this is prevented by the increasing numerical errors, namely condition (5.3) is reached quickly. Moreover for , the mode of the reference pdf is not defined and thus the initial approximation is very far from . In addition for the choice of parameters and the stochastic component of the dynamics of the process is more dominant than the deterministic one, resulting in a flatter FPT pdf.

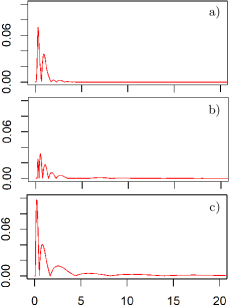

In Fig. 5 we have plotted the absolute error between the true FPT pdf and the approximated for the three cases and for the smallest such that condition (5.3) is satisfied.

5.2. Laguerre-Gamma polynomial approximation: unknown moments

In the previous paragraph, the approximation relies on the knowledge of the moments of the underlying process, which were used in the coefficients defined in (3.2) and in the approximation (3.6). In the following we will consider a different setup.

We sample FPTs of the GBM using the Milstein Method [28] to simulate the trajectories of the process, thus obtaining a random i.i.d. sample of FPTs of size . Then the approximation (3.6) is carried out using the recursion (4.10) and -statistics in place of cumulants The -th -statistic is a symmetric function of the random sample whose expectation gives the -th cumulant We have used the R-package kStatistics [36] to recover -statistics for the simulated sample of FPTs. The numerical results show that the approximations behave in essentially the same way as in the case of known moments and so we do not find useful to show the respective plots.

Instead, in Fig. 6 we have plotted the absolute error between the true FPT pdf and the approximated for the three cases of Fig.1 and for the smallest such that condition (5.3) is satisfied. We note that the absolute errors are larger (in particular case A) but this strategy is much more general and can be applied to any process whose trajectories can be simulated or to FPT data with unknown underlying process.

5.3. Parameters estimation

If the true pdf were known, the well known method of maximum likelihood estimation could have been applied to carry out parameter estimations of the process. In this paragraph we analyze the possibility to use the approximated density with known moments, instead of the true density in the likelihood function. This approach would be particularly useful if the true density is not known, as usual happens, and can be applied since is a pdf. Suppose to have a sample of FPTs The maximum likelihood estimate of is

| (5.5) |

with the log-likelihood function and

.

The maximization problem (5.5) has been numerically solved using the function Optim in the base R-package Stats. More specifically the maximum likelihood estimates of the parameters have been obtained through a global optimization algorithm known as Simulated Annealing [4]. Simulated annealing is a stochastic global optimisation technique applicable to a wide range of discrete and continuous variable problems. It makes use of Markov Chain Monte Carlo samplers, to provide a means to escape local optima by allowing moves which worsen the objective function, with the aim of finding a global optimum. Technical details can be found in [4], a variant of which is the algorithm implemented in Optim. For the same sample used in the previous subsection with , Table 1 shows the maximum likelihood estimates of and in(5.5) for and for the cases considered in Fig.1.

| A | 4 | 3.893 | ||

| B | 2.2 | 2.152 | ||

| C | 1.4 | 1.18 |

Remark 5.1.

In the case of GBM process, a simpler way to estimate the parameters is using the method of moments, since the cumulants of the pdf have the simple expression (2.11). To estimate the cumulants we employ the -statistics Starting from the sample with used in the previous subsection, we compute the -statistics and using the R-package kStatistics [36]. By simple computations, we set and and we obtain the following closed-form expressions for the estimations of and

| (5.6) |

where . Table 2 shows the numerical estimations of and for the cases considered in Fig.1.

References

- [1] L. Alili, P. Patie, and J. L. Pedersen. Representations of the first hitting time density of an Ornstein-Uhlenbeck process. Stochastic Models, 21(4):967–980, 2005.

- [2] S. Asmussen, P.-O. Goffard, and P. J. Laub. Orthonormal Polynomial Expansions and Lognormal Sum Densities, pages 127–150. World Scientific, 2019.

- [3] P. Baldi, L. Caramellino, and M. Rossi. Large deviations of conditioned diffusions and applications. Stochastic Processes and their Applications, 130(3):1289–1308, 2020.

- [4] C. J. P. Bélisle. Convergence theorems for a class of simulated annealing algorithms on . J. Appl. Probab., 29(4):885–895, 1992.

- [5] A. N. Borodin and P. Salminen. Handbook of Brownian motion—facts and formulae. Probability and its Applications. Birkhäuser Verlag, Basel, second edition, 2002.

- [6] A. Buonocore, L. Caputo, G. D’Onofrio, and E. Pirozzi. Closed-form solutions for the first-passage-time problem and neuronal modeling. Ricerche di Matematica, 64(2):421–439, 2015.

- [7] A. Buonocore, A. G. Nobile, and L. M. Ricciardi. A new integral equation for the evaluation of first-passage-time probability densities. Advances in Applied Probability, 19(4):784–800, 1987.

- [8] T. Byczkowski and M. Ryznar. Hitting distributions of geometric Brownian motion. Studia Mathematica, 173:19–38, 2006.

- [9] C. A. Charalambides. Enumerative combinatorics. CRC Press Series on Discrete Mathematics and its Applications. Chapman & Hall/CRC, Boca Raton, FL, 2002.

- [10] L. Comtet. Analyse combinatoire. Tomes I, II, volume 5. Presses Universitaires de France, Paris, 1970.

- [11] E. Di Nardo. Symbolic calculus in mathematical statistics: a review. Sém. Lothar. Combin., 67:Art. B67a, 72, 2012.

- [12] E. Di Nardo and G. D’Onofrio. A cumulant approach for the first-passage-time problem of the Feller square-root process. Appl. Math. Comput., 391:125707, 13, 2021.

- [13] E. Di Nardo and G. D’Onofrio. On the cumulants of the first passage time of the Inhomogeneous Geometric Brownian motion. Mathematics, 9(9), 2021.

- [14] E. Di Nardo, A. G. Nobile, E. Pirozzi, and L. M. Ricciardi. A computational approach to first-passage-time problems for Gauss–Markov processes. Advances in Applied Probability, 33(2):453–482, 2001.

- [15] NIST Digital Library of Mathematical Functions. http://dlmf.nist.gov/, Release 1.1.5 of 2022-03-15. F. W. J. Olver, A. B. Olde Daalhuis, D. W. Lozier, B. I. Schneider, R. F. Boisvert, C. W. Clark, B. R. Miller, B. V. Saunders, H. S. Cohl, and M. A. McClain, eds.

- [16] G. D’Onofrio, C. Macci, and E. Pirozzi. Asymptotic results for first-passage times of some exponential processes. Methodology and Computing in Applied Probability, 20(4):1453–1476, 2018.

- [17] J. L. Doob. Heuristic approach to the Kolmogorov-Smirnov theorems. The Annals of Mathematical Statistics, pages 393–403, 1949.

- [18] O. G. Ernst, A. Mugler, H.-J. Starkloff, and E. Ullmann. On the convergence of generalized polynomial chaos expansions. ESAIM Math. Model. Numer. Anal., 46(2):317–339, 2012.

- [19] D. Funaro. Polynomial approximation of differential equations, volume 8 of Lecture Notes in Physics. Springer-Verlag, Berlin, 1992.

- [20] V. Giorno, A. G. Nobile, and L. M. Ricciardi. On the asymptotic behaviour of first-passage-time densities for one-dimensional diffusion processes and varying boundaries. Advances in Applied Probability, 22(4):883–914, 1990.

- [21] V. Giorno, A. G. Nobile, L. M. Ricciardi, and S. Sato. On the evaluation of first-passage-time probability densities via non-singular integral equations. Advances in Applied Probability, 21(1):20–36, 1989.

- [22] P.-O. Goffard and P. J. Laub. Orthogonal polynomial expansions to evaluate stop-loss premiums. Journal of Computational and Applied Mathematics, 370:112648, 2020.

- [23] I. S. Gradshteyn and I. M. Ryzhik. Table of integrals, series, and products. Academic Press, Inc., Boston, MA, fifth edition, 1994.

- [24] R. Gutiérrez, L. M. Ricciardi, P. Román, and F. Torres. First-passage-time densities for time-non-homogeneous diffusion processes. J. Appl. Probab., 34(3):623–631, 1997.

- [25] A. Hassairi and M. Zarai. Characterization of the cubic exponential families by orthogonality of polynomials. The Annals of Probability, 32(3B):2463–2476, 2004.

- [26] S. Herrmann and C. Zucca. Exact simulation of first exit times for one-dimensional diffusion processes. ESAIM: Mathematical Modelling and Numerical Analysis, 54(3):811–844, 2020.

- [27] C. C. Heyde. On a property of the lognormal distribution. J. Roy. Statist. Soc. Ser. B, 25:392–393, 1963.

- [28] D. J. Higham. An algorithmic introduction to numerical simulation of stochastic differential equations. SIAM Rev., 43(3):525–546, 2001.

- [29] R. G. Jaimez, P. R. Roman, and F. T. Ruiz. A note on the Volterra integral equation for the first-passage-time probability density. Journal of Applied Probability, 32(3):635–648, 1995.

- [30] S. Karlin and H. M. Taylor. A second course in stochastic processes. Academic Press, Inc., New York-London, 1981.

- [31] M. Kendall and A. Stuart. The advanced theory of statistics. Vol. 1. Macmillan Publishing Co., Inc., New York, fourth edition, 1977.

- [32] J. T. Kent. Eigenvalue expansions for diffusion hitting times. Zeitschrift fur Wahrscheinlichkeitstheorie und Verwandte Gebiete, 52(3):309–319, 1980.

- [33] V. Linetsky. Computing hitting time densities for CIR and OU diffusions: Applications to mean-reverting models. Journal of Computational Finance, 7:1–22, 2004.

- [34] R. J. Martin, M. J. Kearney, and R. V. Craster. Long- and short-time asymptotics of the first-passage time of the Ornstein–Uhlenbeck and other mean-reverting processes. Journal of Physics A: Mathematical and Theoretical, 52(13):134001, mar 2019.

- [35] P. McCullagh. Tensor methods in statistics. Monographs on Statistics and Applied Probability. Chapman & Hall, London, 1987.

- [36] E. D. Nardo and G. Guarino. kStatistics: Unbiased Estimators for Cumulant Products and Faa Di Bruno’s Formula, 2021. R package version 2.1.

- [37] R. Nishii. Orthogonal functions of inverse gaussian distributions. In Lifetime Data: Models in Reliability and Survival Analysis, pages 243–250. Springer, 1996.

- [38] A. G. Nobile, L. M. Ricciardi, and L. Sacerdote. Exponential trends of first-passage-time densities for a class of diffusion processes with steady-state distribution. Journal of Applied Probability, 22(3):611–618, 1985.

- [39] S. B. Provost and H.-T. Ha. On the inversion of certain moment matrices. Linear Algebra Appl., 430(10):2650–2658, 2009.

- [40] F. Ramos-Alarcón and V. Kontorovich. First-passage time statistics of Markov gamma processes. J. Franklin Inst., 350(7):1686–1696, 2013.

- [41] S. Redner. A Guide to First-Passage Processes. A Guide to First-passage Processes. Cambridge University Press, 2001.

- [42] L. M. Ricciardi, A. Di Crescenzo, V. Giorno, and A. G. Nobile. An outline of theoretical and algorithmic approaches to first passage time problems with applications to biological modeling. Math. Japon., 50(2):247–322, 1999.

- [43] L. M. Ricciardi, L. Sacerdote, and S. Sato. On an integral equation for first-passage-time probability densities. Journal of Applied Probability, 21(2):302–314, 1984.

- [44] G. Sansone. Orthogonal functions. Dover Publications, Inc., New York, 1991.

- [45] J. A. Shohat. On the development of functions in series of orthogonal polynomials. Bull. Amer. Math. Soc., 41(2):49–82, 1935.

- [46] A. J. F. Siegert. On the first passage time probability problem. Phys. Rev., 81:617–623, Feb 1951.

- [47] G. Szegő. Orthogonal polynomials. American Mathematical Society, Providence, R.I., fourth edition, 1975.

- [48] M. C. K. Tweedie. Statistical properties of inverse Gaussian distributions. I, II. Ann. Math. Statist., 28:362–377, 696–705, 1957.

- [49] G. A. Wilson and A. Wragg. Numerical methods for approximating continuous probability density functions, over , using moments. J. Inst. Math. Appl., 12:165–173, 1973.

- [50] M. Yor. On some exponential functionals of Brownian motion. Advances in Applied Probability, 24(3):509–531, 1992.

- [51] Z. Zheng, L. Wei, J. Hämäläinen, and O. Tirkkonen. Approximation to distribution of product of random variables using orthogonal polynomials for lognormal density. CoRR, abs/1203.3288, 2012.