Some Optimisation Problems in Insurance with a Terminal Distribution Constraint

Abstract

In this paper, we study two optimisation settings for an insurance company, under the constraint that the terminal surplus at a deterministic and finite time follows a normal distribution with a given mean and a given variance. In both cases, the surplus of the insurance company is assumed to follow a Brownian motion with drift.

First, we allow the insurance company to pay dividends and seek to maximise the expected discounted dividend payments or to minimise the ruin probability under the terminal distribution constraint. Here, we find explicit expressions for the optimal strategies in both cases: in discrete and continuous time settings.

Second, we let the insurance company buy a reinsurance

contract for a pool of insured or a branch of business. To achieve a certain level of sustainability (i.e. the collected premia

should be sufficient to buy reinsurance and to pay the occurring

claims) the initial capital is set to be zero. We only allow for

piecewise constant reinsurance strategies producing a normally

distributed terminal surplus, whose mean and variance lead to a given

Value at Risk or Expected Shortfall at some confidence level .

We investigate the question which admissible reinsurance strategy

produces a smaller ruin probability, if the ruin-checks are due at

discrete deterministic points in time.

Keywords: insurance, reinsurance, dividends, optimal control, distributional constraints, value at risk, expected shortfall.

2020 MSC: 91G05, 91B05, 93B03

1 Introduction

This paper investigates the problem of dividend maximisation and the problem of ruin minimisation for an insurance company who aims to achieve a certain surplus distribution at a particualr future date. Knowing the surplus distribution, for instance, at regulatory check-times can be important for the calculation of the necessary capital reserves. Measuring the solvency of a collective of risks remains one of the important tasks in insurance mathematics. Over the years, several risk measures have been proposed and investigated concerning their properties, by adding risk constraints like, for example, value at risk.

One of the most popular risk measures is the value of expected discounted dividends. Here, one searches for the “optimal” dividend strategy, i.e. a strategy maximising the value of expected discounted dividends up to the time when the surplus becomes negative. By considering the optimal strategy, the focus is deliberately placed on the surplus’ evolution characteristics rather than on the company’s managerial skills. Some results on dividend maximisation problems can be found, for instance, in Asmussen and Taksar [2], Shreve et al. [18]. We further refer to Albrecher and Thonhauser [1], Avanzi [3], Hipp [11] and references therein for an overview of the existing results.

The optimal dividend payout strategy in the most “unconstrained” settings turns out to be of a barrier or of a band type, meaning that the strategy can change from “paying the maximal possible amount” to “paying nothing” in dependence on the current surplus value. This setup cannot be considered realistic or doable for an insurance company. Moreover, solvency requirements imposed by regulators may not allow to pay dividends according to the optimal, possibly bang-bang, strategy. To make the models more realistic, one needs to impose restrictions. Paulsen [16] studies the optimal dividend problem with a no-bankruptcy constraint – dividends will not be paid if the surplus is below a certain barrier. An extended setting with transaction costs is analysed in Bai et al. [4]. Hipp [10], considers optimal dividend payment strategies under the constraint that the ruin probability stays under a given boundary. Thonhauser and Albrecher [19] maximise the total discounted utility of dividend payments under strictly positive transaction costs.

The setting considered in the first part of this paper is novel in the following way. The surplus of an insurance company in a finite time interval is modelled by a diffusion process.

We concentrate on the dividend payments – described by dividend rates – with two different objective functions: expected discounted dividend payments and ruin probability. In the first case, one faces a maximisation problem, whereas in the second case the ruin probability should be minimised. The surplus can only be controlled at discrete equidistant time points. We introduce a constraint on the set of admissible strategies by requiring that the ex-dividend terminal wealth should be normally distributed with fixed exogenously given mean and variance. To the best of our knowledge, such a constraint has not been considered in an insurance optimisation problems before.

We prove that the optimal strategy in both cases should be deterministic, i.e. is decided at time zero. As it is intuitively clear, the strategy leading to the maximal discounted dividend value starts with high payments in the very beginning and decreases approaching the time horizon; the strategy minimising the ruin probability behaves in an opposite way.

The results obtained in this first part of the paper heavily rely on the very nature of dividend payments. The control is acting solely on the drift, letting the volatility unchanged. This allows to compare different strategies by comparing their paths. However, choosing a control problem with an impact on the volatility of the surplus process will not allow to use the path-comparison method and will require different, more complex techniques.

A well-established, well-investigated and still quite popular risk measure is the ruin probability – the probability that a company, a strain of business or a pool of insured risks goes bankrupt in finite time, i.e. writes red numbers – the aggregate claims exceed the collected premia. The surplus, with continuous paths or having jumps, can be controlled, for instance, by a reinsurance, dividend payments, possible surplus investments into a dependent or independent markets.

A technical ruin, when the surplus becomes negative or touches zero, does not compulsory mean that the company has to entirely stop operating.

The time and the severity of ruin are completely neglected by looking solely at the ruin probability. Also, due to Solvency II requirements companies have enough reserves to bridge a certain period of unfavorable business development. For these reasons, the ruin probability might not be a desired risk measure to assess a company’s performance. However, paired with some additional constraints it can help choosing a strategy which is, for instance, more risk averse in the eyes of the insurance company.

In the second part of this manuscript, we are looking at the surplus of an insurance company who buys proportional reinsurance contracts of a specific type.

To control the risk exposure and to be able to meet regulatory requirements, insurance companies need to pay attention to various constraints.

For instance, Bernard and Tian [5], Lo [13, 14], Huang and Yin [12] search for the optimal reinsurance strategy under a constraint (strictly positive surplus or a fixed risk measure under some prespecified boundary) on the loss at the terminal time. Optimal investment and reinsurance have been considered with constraints on the budget, see Bi et al. [7], or on Value at Risk, see, e.g. Choulli et al. [9], Bi and Cai [6], Wang and Siu [20]. The problem of choosing a reinsurance strategy to minimise the ruin probability

with a Value at Risk (or a Conditional Value at Risk) constraint is considered for instance in Zhang et al. [21], Chen et al. [8] with a finite and infinite time horizon.

In this paper, we seek to find a proportional reinsurance strategy that minimises the ruin probability under a constraint imposed on the distribution of the terminal wealth. Adding a constraint on the terminal surplus has several advantages. For instance, one will be able to calculate any risk measure acting on the terminal wealth: the Value at Risk, the Expected Shortfall or the expected terminal utility, and hence address many regulatory requirements all at once.

We consider a finite time interval , and the direct insurer can change the deductible only twice – in the beginning and in the middle of the interval. The target is twofold: the terminal post-reinsurance surplus at should be normally distributed with given mean and variance, and the chosen admissible strategy should lead to the smallest possible ruin probability. We show that the optimal strategy is deterministic, i.e. is chosen at time 0, and one is always acting in a risk averse way. That is, the insurer buys less reinsurance in the beginning, in order to let the drift push the surplus upwards, and buys more reinsurance in the second half, reducing the risk of ruin shortly before the regulator’s check. We briefly discuss the case where the insurer can update the reinsurance strategy three times, which provides some intuition on how to deal with more than two updates.

To the best of our knowledge, the presented approach is new in many aspects. The discrete nature of the problem and the structure of the optimal strategies, makes this setting easily applicable from a practical point of view.

2 Maximising Dividends Under a Terminal Distribution Constraint

In this section, we consider an insurance company who is allowed to pay dividends. The dividend rate has to be chosen in such a way that the surplus at some future deterministic time achieves a given distribution. At the same time, the value of expected discounted dividends should be maximised.

We consider a probability space , a finite time horizon and a Brownian motion . We denoted by the natural complete and right continuous filtration of , and set . The surplus of the insurance company in the interval is modelled by a Brownian motion with drift as

where represents the initial capital and .

The company is allowed to pay dividends in form of dividend rates for some given . It means that the post-dividend process under a dividend strategy is given by

| (1) |

Our objective is to determine the strategies that maximise the expected discounted dividends and simultaneously lead to a normally distributed post-dividend terminal surplus . We assume that the target distribution is Gaussian with the mean , and the variance , for some and .

At first, the company is only allowed to update a dividend strategy at equidistant time points , in the period . An admissible strategy is a sequence of dividend rates such that for all , is an -measurable random variable and the total surplus at time satisfies . We denote the set of admissible strategies by , where the subscript indicates the number of the allowed change points. The accumulated dividends up to time are then given by

It is worth mentioning that differently than in the classical dividend problems, see for instance [2], dividends can be paid (up to time ) even if the surplus is negative. This feature of our model alleviates, to some extent, the drawback of models stopping at the ruin time. A technical ruin does not mean that the company stops operating. In reality, some insurance companies proceed with dividend payments even during protracted crisis times. A famous example provides Munich Re, known for not reducing its dividends since at least 2006, see [15].

The following lemma indicates the range of achievable target expectations by a post-dividend Brownian surplus see equation (1), at time .

Lemma 2.1

The parameter in the target distribution of the surplus at time has to fulfil .

Proof.

For any admissible dividend strategy , the distribution of the surplus in equation (1) at time is Gaussian with mean

Using the fact that , for every we get that

which proves the statement. ∎

Note that, for large values of , the range of achievable means may include negative values. Although this is mathematically feasible, an insurance company would not pursue a strategy to achieve a negative expected surplus, but it would rather choose , so to obtain a expected net profit at time , even if small. Next we better identify the characteristics of admissible strategies.

Proposition 2.2

The set of admissible strategies consists of such that is -measurable, i.e. deterministic.

Proof.

Let be an arbitrary admissible dividend strategy. The corresponding surplus at time is then given by

| (2) |

We now identify the set of dividend strategies that allow to achieve a normal distribution with mean and variance . Let be a generic random variable with . Then, for it holds that . Now we consider the surplus at time , . From (2) and the fact that is an admissible strategy we get that and it holds that

| (3) |

Let be a probability measure on equivalent to , with the Radon-Nikodym derivative . Then, applying change of measure techniques in (3) we obtain

Together with (3), one gets for all

leading to

If , then by uniqueness of the moment generating functions the variable is normally distributed with mean and variance . Hence it has positive -probability to attain negative values, which contradicts the equivalence of and , since -a.s.

If, instead, , there is no random variable with such a moment generating function.

Finally, if , the variable must be a constant, i.e. deterministic.

∎

For the special case we obtain the following corollary.

Corollary 2.3

The set of admissible strategies only consists of deterministic pairs , i.e. is -measurable.

Note that the dividend strategies act solely on the drift and do not affect the volatility. This fact allows to compare different strategies by looking at the surplus “path by path”. Another implication is that, in case , the optimal dividend strategy is completely decided at time ; meaning that once the dividend rate , to be valid in , is decided, then is also uniquely determined at time so that the final distribution can be achieved. We will see in the reminder of the section that the optimal strategy is deterministic also for .

Let now be the preference rate of the insurer. The return function corresponding to a strategy is

Note, that the dependence on the initial capital is in this setting purely nominal. As stressed before, we do not stop our considerations at the time of ruin. The strategy will depend solely on the parameters of the surplus process and the target distribution.

The target of the insurance company is to find a strategy leading to

| (4) |

To analyse Problem (4), we start with the case of two periods, i.e. .

2.1 A 2-period model

Suppose that the insurance company is allowed to update its dividend strategy only once, at time . Due to Corollary 2.3, we get that the set of admissible dividend strategies consists of all deterministic pairs with , and such that

As a direct consequence of the fact that , it must also hold that , otherwise the target distribution would not be reachable. In the next step, we investigate how to determine the optimal strategy.

Proposition 2.4

The optimal strategy is given by

Proof.

We consider the problem

| (5) |

It is easy to see that, for , the discounting coefficient in the first period, , is larger than in the second period, . Therefore, to maximise the discounted dividends, must be chosen as big as possible. Taking into account that and that , we get that , and consequently, if and if . ∎

To summarise the result, in a two-period setting, the optimal dividend strategy pays dividends at the maximum rate in the first period, and then adjusts the strategy to achieve the target distribution in the second period. Such behaviour is justified by the effect of discounting which has a larger impact in the time interval .

2.2 An -period model

We now extend our analysis to an -period framework. That is, the dividend strategy can be adjusted times in the interval . Recall that, according to Proposition 2.2, strategies are not necessarily deterministic, but the sum of dividend rates is.

To better explain the mechanism for the computation of the optimal dividend strategy, we consider an example with .

Example 2.5

Let and let be an admissible strategy. The expected discounted total dividends are given by

We easily see that, that due to discounting (), the strategy to be applied in the first period has a larger weight than the others, hence, as in the two period model, it would be optimal to choose it the largest possible. Taking into account that , and that for , we have that

equivalently, . Now we move to the choice of . After choosing we get that , according to Proposition 2.2. If , since and are nonnegative, it holds that . If instead, , using the same argument like for , we choose and so that is the largest possible value according to the constraints, i.e. , and . Put in other words, if , then and . If , at time we determine both and , depending on the current surplus so that

We stress that because must be deterministic, we immediately get that is measurable. That means, once is found, then is also determined, so that the constraint on the distribution is satisfied. Moreover, the value is the biggest possible choice for .

The deterministic strategy where

| (6) |

fulfils all necessary conditions.

Next, we show that we cannot find a different, possibly stochastic, strategy with a higher expected discounted dividends value, meaning that the optimal strategy is indeed deterministic.

Let be the strategy in (6) and let be an arbitrary admissible strategy, i.e. such that for , and .

Then, there exist two random variables such that , because is the largest possible dividend rate, and , . It holds that

where in the last equality we have used the fact that .

If , then, ; hence, necessarily and . Since we get that leading to a contradiction.

Then, it must hold that . Now we have two cases:

-

i.

if , then it is immediate that and then ;

-

ii.

if , we get that

which implies that .

To conclude we observe that if then the inequality is strict and the strategy , is optimal. If we get that either in which case the inequality is strict again, or which corresponds to the case where .

The above example provides the argument for computing the optimal dividend strategy in an -period framework.

Proposition 2.6

Let be the number of sub-periods in the interval and let

| (7) |

Then, an optimal strategy is given by

| (8) |

Proof.

Assume first , then obviously the optimal strategy is .

Let now and let be an admissible strategy.

Like in Example 2.5, there exist such that for and . Then we have that

Note that since for all , and for all , it must hold for and for .

Now we observe that, the function is decreasing, and hence it attains its maximum at , i.e. . Therefore, we conclude that

The strict inequality holds true if there is at least one with . If instead for all , then strategies and coincide, i.e. in particular almost surely for all . This leads to if . ∎

Remark 2.7 (Continuous time)

This procedure allows to extend the setting to continuous time.

We denote by the set of admissible strategies, consisting of the -adapted processes with and from (1) normally distributed with mean and variance . Letting in the -period models, the optimal strategies as given in (8) converge to a deterministic strategy in continuous time:

where . We assume .

Let be an admissible strategy and define . Since we would like to achieve the same final distribution with strategies and , it must hold that . Moreover, it is clear that for , for . As for the -period models we get

A strict inequality holds true if for all where is a Lebesgue measurable non-zero set.

Therefore, in continuous time it is optimal to pay on the maximal rate as long as possible, and to pay nothing afterwards.

Note, that we have only considered the case of dividend rates. However, it is also possible to allow for lump sum payments. Then, because it is clear that one should pay the amount directly at time zero in both discrete and continuous time settings.

Considering the setting with dividend rates may be more preferable for reputational reasons. Indeed, distributing the dividends over the whole period rather than paying a lump sum at the beginning of the period, may give a better impression to shareholders. This is guaranteed in our model by the upper bound on the admissible dividend rates. The value of is a management decision: in our setting it has to be small enough to distribute dividends over the whole period, and large enough to achieve the target distribution.

3 Dividends Minimising the Ruin Probability

At first glance, the title of this sections sounds controversial. Indeed, paying dividends increases the probability of ruin, and in many settings the optimal dividend strategy even leads to a certain ruin. However, the constraint put on the terminal distribution allows to find a non-zero dividend strategy that minimises the ruin probability over the set of admissible strategies.

We consider again an insurance company who pays dividends and aims to achieve a target distribution of the terminal surplus at time . However, we now assume that the objective of the insurer is to minimise the ruin probability.

We consider the same setting like in Section 2 with a surplus, after dividends, described by equation (1). We recall that the set of achievable target means is given by (see Lemma 2.1) and that the set of admissible strategies is the set of all strategies , where is -measurable (see Proposition 2.2), and .

The goal of the insurance company is to minimise the ruin probability, which is given by

| (9) |

over all admissible dividend strategies .

3.1 A 2-period model

The set of admissible strategies is denoted by , given in Section 2.1. That is all admissible strategies are of the form with deterministic (see Corollary 2.3) and . We target to minimise the ruin probability in the time interval , i.e.

over all . Note that differently than in Section 2 the dependence on the initial capital is crucial in this setting.

Proposition 3.1

Let and be two admissible strategies, i.e. . We assume that . Then, is better than , in the sense that

Proof.

We first observe that at time , both strategies and lead to the same distribution of the final surplus, i.e. . Then, we have

Therefore, for all we get that . ∎

As a consequence of Proposition 3.1, we get that should be chosen as the smallest possible value. This leads to the following result.

Corollary 3.2

In a two-period framework, the ruin minimising dividend strategy is where

3.2 An n-period model

The extension to -periods is obtained by replicating the reasoning of Proposition 3.1 and Corollary 3.2.

Proposition 3.3

Let . Then, the ruin minimising dividend strategy fulfils

Remark 3.4 (Continuous time)

Letting will produce the following optimal strategy: we define as the time that realises . Then, the optimal dividend rate is for all and for .

Like in the dividend maximisation problem in Section 2, the ruin minimising strategy is deterministic. An intuitive consequence of the result above (Proposition 3.3) is that the optimal strategy that minimises ruin probability is also the strategy that minimises the value of expected discounted dividends.

4 Reinsurance With a Target Terminal Distribution

In this section, we change the setting considered in Sections 2 and 3. We consider an insurance company who buys reinsurance for a certain branch of their business or a pool of insured claims.

We consider a probability space , and a fixed time horizon . Let be a random variable representing a claim size having positive finite first and second moments denoted by and , respectively. We assume that the surplus of the insurance company is described by a Brownian motion with drift, approximating a Cramer-Lundberg model like, e.g., in Schmidli [17, p. 226],

where and is a Brownian motion. We also define by natural filtration of the Brownian motion, under the usual hypotheses. The insurance company is allowed to buy proportional reinsurance with retention to mitigate the losses. We assume that the reinsurance premium is calculated via the expected value principle, that is where . Then, the premium rate that remains to the insurer is

with , see, e.g. [17, Ch. 2.2] for more details.

Under a reinsurance strategy , the surplus is given by

We denote by

the net value of collective, i.e. the part of the surplus that only accounts for insurance/reinsurance premia and claims.

The insurance company wants to make sure that the collected premia are sufficient (in a certain sense) to buy reinsurance, if necessary, and to pay the occurring claims. To achieve such level of sustainability the target of the insurance is to choose a reinsurance strategy such that at time the distribution of the net collective is normal with mean , for some small and variance . To gain some intuition on the choice of and , we may interpret as a (small) positive target gain, and is fixed to fulfil for some given and . The latter is a condition on the Value at Risk (VaR) at the confidence level (for instance ). In particular, represents the loss that the insurer can bear with at most probability . This can be interpreted as the required capital ensuring the system’s solvency. Aiming at as a target distribution is justified, for instance, by the existence of the closed form formulas for the VaR or Expected Shortfall (ES) for Gaussian random variables, which can be easily calculated111Denoting by the terminal loss at time , we immediately get that and for , where and denote the density and the cumulative distribution function of the standard normal, respectively..

To reach the target distribution, the insurance company follows a sustainable strategy, that is reinsurance is only financed through premia, and we additionally require that reinsurance strategies do not produce a negative premium rate for the insurer. This condition is, in spirit, similar to the self-financing condition which is often assumed in finance. Indeed, a branch of business or a pool of insured is considered a closed system, where the insurance company does not intervene by injecting or withdrawing additional capital.

Our next step is to define the set of possible controls leading to the desired distribution. We let denote the set of strategies with for all , that are adapted to and such that .

Note that, in particular, deterministic controls make the terminal distribution of the net collective surplus Gaussian, see Example 4.1.

Example 4.1 (Deterministic controls)

Let be a continuous deterministic reinsurance strategy, with for all 222In this example we use the notation in place of to emphasise the deterministic nature of the strategy.. Then is an admissible control if the following two conditions hold:

| (10) |

To make an example, is an admissible control for constants which satisfy

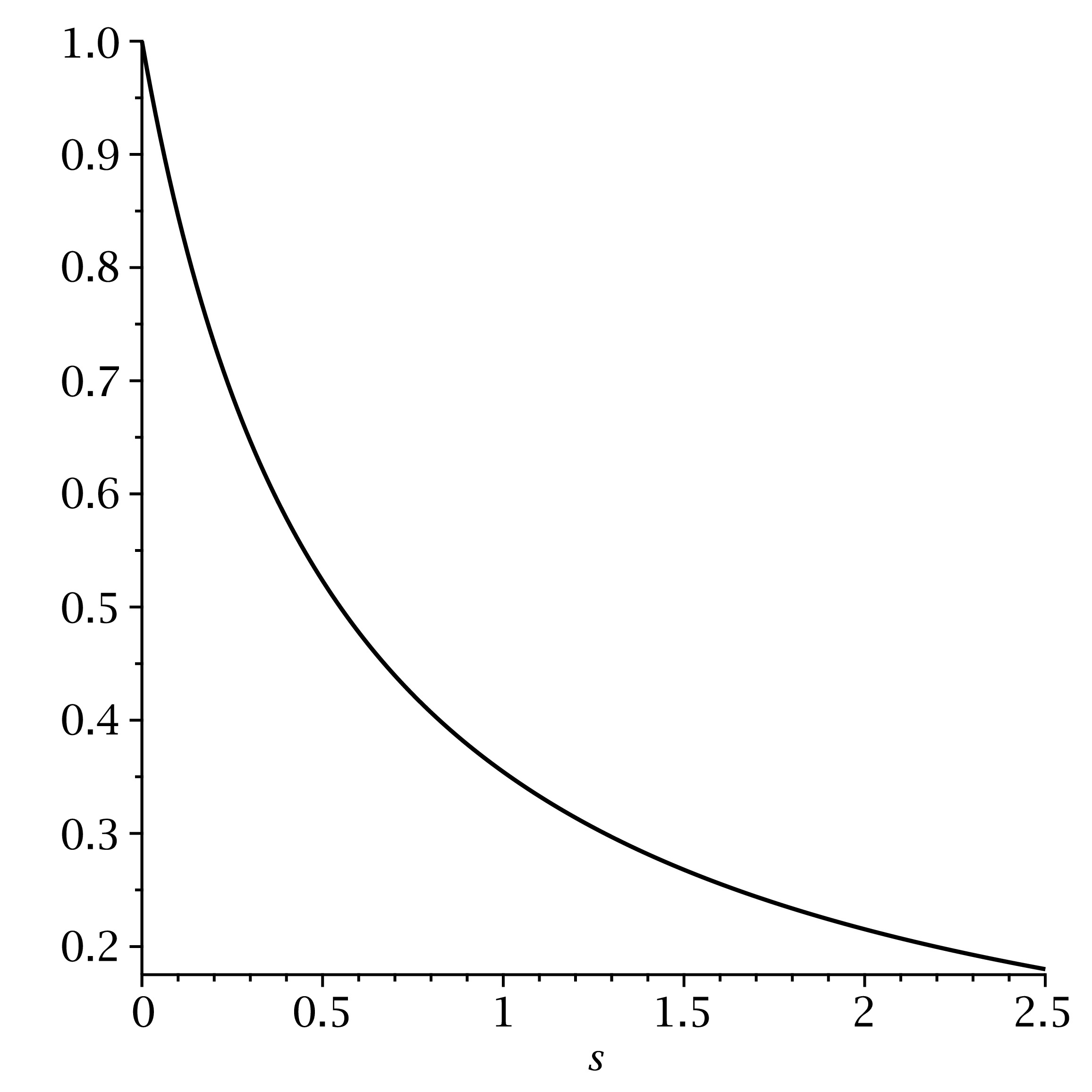

For the parameter set given by , , , , , , , , we get that , . The strategy is illustrated in Figure 1.

In the sequel, we restrict to the case where reinsurance strategies can be updated only at deterministic time points. In fact, we concentrate on the case and we refer to this case as the two period model. The reason is that differently than in the dividend case, reinsurance controls affect both the drift and the volatility. Therefore, in this case, pathwise comparison is not possible anymore, and the problem requires different techniques. In the case , we are still able to obtain an explicit solution with probabilistic methods. However, the problem becomes immediately more complicated when we increase the number of periods (see Section 4.4), even in case we restrict to deterministic strategies.

4.1 Admissible strategies in a 2-period model

We denote the set of admissible strategies by , where, like before, the subscript indicates the number of strategy updates up to time . An admissible strategy is a pair , where is -measurable and is measurable; In this setting the retention level is updated only once, at time . Hence, at time the net surplus satisfies

where .

The set of admissible strategies is characterised in the lemma below. In particular, we show that admissible strategies are deterministic.

Lemma 4.2

The set consists of all strategies where are both -measurable, taking values in , and satisfying the following two conditions:

| (11) | ||||

Proof.

Recall that for any normally distributed random variable with mean and variance , the moment generating function is given by for all . Let ; then and are independent. Since is chosen so that , it holds that

for all . Now, we let be a probability measure equivalent to , with the Radon-Nikodym derivative

Using the independence of and and the change of measure we get that

for all . This can be simplified to

Deriving the above expression with respect to and letting we see that all moments of correspond to the moments of a normal distribution, meaning that the moment generating function of (written as a power series with the moments as coefficients) corresponds to that of a normal distribution. Therefore, we conclude

However, this is impossible because can attain values only in -a.s. (hence also -a.s.), which means that must be constant. ∎

Because can take values only in , it is clear that not all arbitrary values of and are reachable. In the next lemma we specify the ranges of and .

Lemma 4.3

If there exist such that Condition (LABEL:conditions1) holds, then the target mean and the variance satisfy:m

| (12) |

Proof.

From Conditions (LABEL:conditions1), and the fact that take values in , we get that and that . Using again the conditions (LABEL:conditions1) and substituting the value of into the second equation we get that must solve

Imposing the existence of a real solution leads to

Then, using the fact that must take non-negative values leads to the bound:

∎

Notice that because we do not allow for arbitrage and require , to ensure the existence of a solution at least for the case , we must have that , which is guaranteed by (12).

There is a clear trade-off between increasing the profits and reducing the risk. This is due to the fact that a reinsurance strategy controls both the mean and the volatility. Under a reinsurance strategy the mean and the volatility move into the same direction: increasing the retention level makes the mean larger, but also the volatility. This observation has important consequences for the ruin probability. Indeed, a bigger retention level would make the drift of the net collective larger, meaning that it potentially can push the surplus away from zero; however, at the same time, it increases the riskiness by making the volatility larger. For instance, considering the parameters , , we get that the admissible values of vary in the range . If an insurance company aims at getting an expected gain of at the end of the observation period, it has to account for a relatively large risk of at least .

We can write the range for as

From this expression it is clear that if the target return is close to , the variance is approximately , which corresponds to the case where no reinsurance is bought.

4.2 Ruin probabilities in a 2-period model

For the case , the pairs of strategies that satisfy Conditions (LABEL:conditions1) are of the type and .

We assume that and are the regulatory authorities’ inspection dates. A reinsurance strategy is chosen so that the probability of having a positive surplus at both dates is maximised.

We now give a definition of ruin within this setting. We say that the ruin occurs if the insurance company showcases a negative surplus at any of the time points or .

Then, an equivalent formulation of the problem is:

Find a reinsurance strategy that minimises the ruin probability.

In mathematical terms, the problem is formulated as follows. Let and be the two admissible strategies. Without loss of generality, we assume that . For each strategy we define the corresponding survival probabilities:

Our objective is to decide which of these two probabilities, or , is the largest.

The table below illustrates survival probability for different values of so that and are achievable for . The last two columns suggest that . This result is proved in Proposition 4.4 below.

| 0.4448 | 0.7760 | 0.4088 | 0.5117 | |

| 0.3339 | 0.8298 | 0.3772 | 0.5372 | |

| 0.2468 | 0.8597 | 0.3485 | 0.5561 | |

| 0.1715 | 0.8778 | 0.3154 | 0.5720 | |

| 0.1038 | 0.8884 | 0.2637 | 0.5857 | |

| 0.0416 | 0.8935 | 0.1254 | 0.5967 |

Proposition 4.4

Let . Then the strategy is better than the strategy , i.e. .

Proof.

Let and be two independent Brownian motions and denote

Then, the survival probabilities can be rewritten as

| (13) | ||||

having set . The advantage of this representation stands in the fact that for every , and are independent. We observe that there exist standard Brownian motions and such that

| (14) | ||||

for all . We now let

for all . Due to Equations (LABEL:eq:W0) we get that for all , , hence they are identically distributed.

Next, we write and in terms of and . Since and are normally distributed, we have that

where and , and are independent, since they are all normally distributed and .

Expectations and variances of and are given by

| (15) |

Using Fubini’s theorem, we get

where is the standard normal distribution, are the densities of the random variables and , respectively, and we have used that . Since is increasing, we consider the crucial quantities

| (16) |

We have the following two cases:

Assume first that , with from (15).

Since , it holds that for all . Then, we can immediately conclude, that , and hence the strategy is better than the strategy .

Assume next that , with from (15).

Note that since and , then either , in which case there is nothing to prove since and are equal, or it cannot hold that . The latter implies that

there always exists an such that for , it holds that , and the opposite holds true for , see, e.g. the right panel in Figure 2.

Now, we consider the functions and for . We know that

meaning that and . Consequently, since we get that and , that is to say, is decreasing with respect to and is increasing.

We let and note that, in this case for any it holds that

Using this fact, equations (13) and , we get

which proves the statement in case .

Now, we let and be, respectively, the strategies and corresponding to . Assume there is an such that . Then, by the intermediate value theorem there exists an such that .

Assume that . Let be a random variable, independent of and with .

The last inequality follows from the fact that , and are normally distributed. Hence, this contradiction yields that . However, since it holds that and for , that means and , contradicting .

That concludes the fact that is always better than .

∎

In the following, we discuss the situations where and derive sufficient conditions for this to hold.

Lemma 4.5

Proof.

We observe that is equivalent to

| (18) |

for all , where we have substituted . To show that (18) holds for all , we consider the function

This function is concave and has a maximum at . We observe that and that which is negative if the first of condition (17) holds true. Moreover, under the second condition in (17) we also get that , which guarantees that . ∎

Condition (17) is meaningful in terms of insurance and reinsurance premia. Indeed, it tells us that the reinsurance is cheap and the income from the direct insurance premia is high. In this case the result of Proposition 4.4 is intuitively clear: choosing a bigger retention level (less reinsurance) in the first period is better in terms of survival probability (i.e. minimises the ruin at times and ).

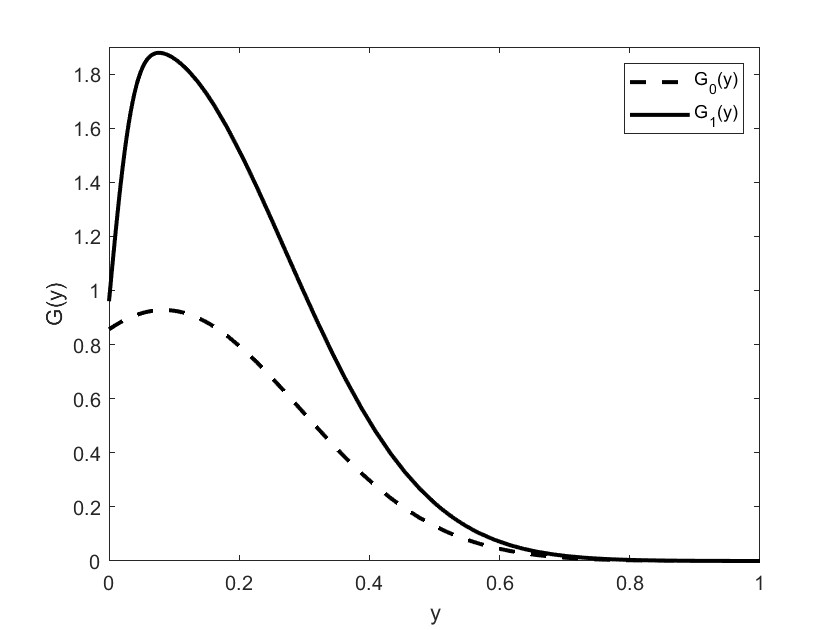

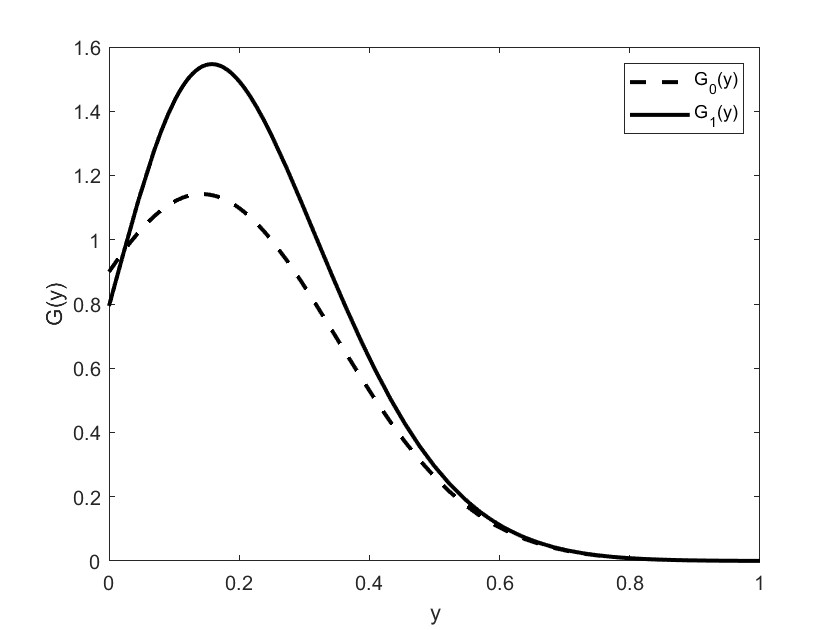

To better understand the different cases (i.e. and ) we let

for all , so that

Figure 2 represents the densities of the survival probability (i.e. and ) relative to the strategy (dashed line) and the strategy (solid line), under given parameters.

The left panel corresponds to the case where condition (17) holds, i.e., insurance is cheap and reinsurance is expensive. Here the survival probability of the strategy dominates that of the strategy for all values of . In the right panel there exist a level (small) at which these two curves switch. However the area under the curve in the set largely compensates that in the set . Such point corresponds to (and it only exists in case ). Note that, natural bounds on the value of , i.e. , guarantee that such compensation of areas always applies and hence , (see Proposition 4.4).

4.3 The penalisation problem

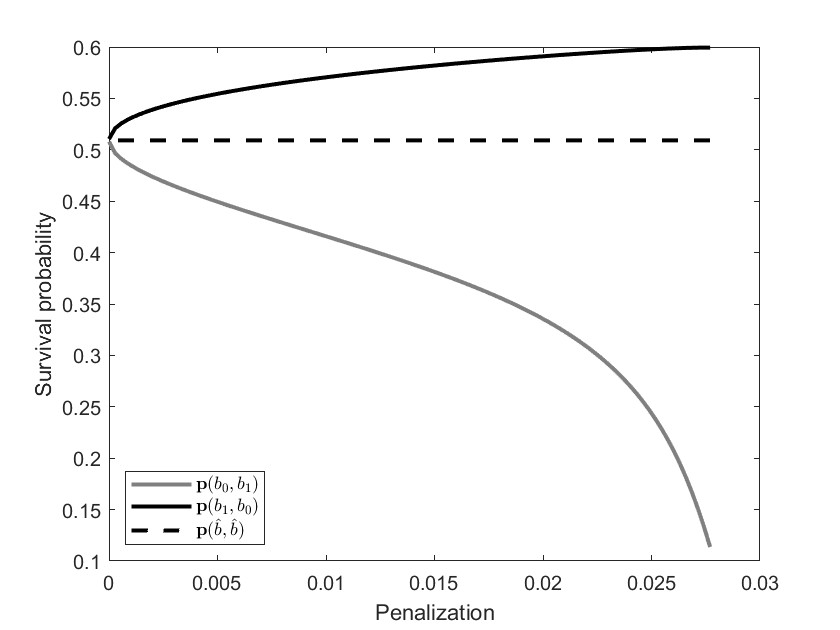

Suppose now, we have the following situation: the insurer may decide (at time zero) to have or to have not an update in the reinsurance contract at time . It she updates the contract, she will pay a penalty amounting to at time . In case of no changes, no penalty will be applied. The strategies corresponding to these two different scenarios are chosen to achieve a Gaussian distribution at time with the same target variance . If the insurer does not change the strategy at time then the mean of the net collective is , uniquely determined by the condition on the target variance. In case the strategy is changed at time , the final expected wealth will be . Next, we show that, due to the insurer’s objective to minimise the ruin probability, changing the strategy at time is more preferable, even with a smaller expected mean.

We assume that . Let be the strategy where the insurer decides to make no changes at time and let and be the admissible strategy where the insurer switches, with . We know, by Proposition 4.4, that strategy is better than . The survival probability of strategy is given by

We let . Then we get that , and we observe that

where

Random variables and are independent. This implies that

Next, for the strategy the survival probability is given by:

where , like in the proof of Proposition 4.4.

It is clear that for , there is a unique strategy, , that allows to achieve the desired distribution for the net collective. For , however the strategy has a survival probability that is always smaller than the survival probability of the optimal strategy and larger than that of . This difference is illustrated in Figure 3.

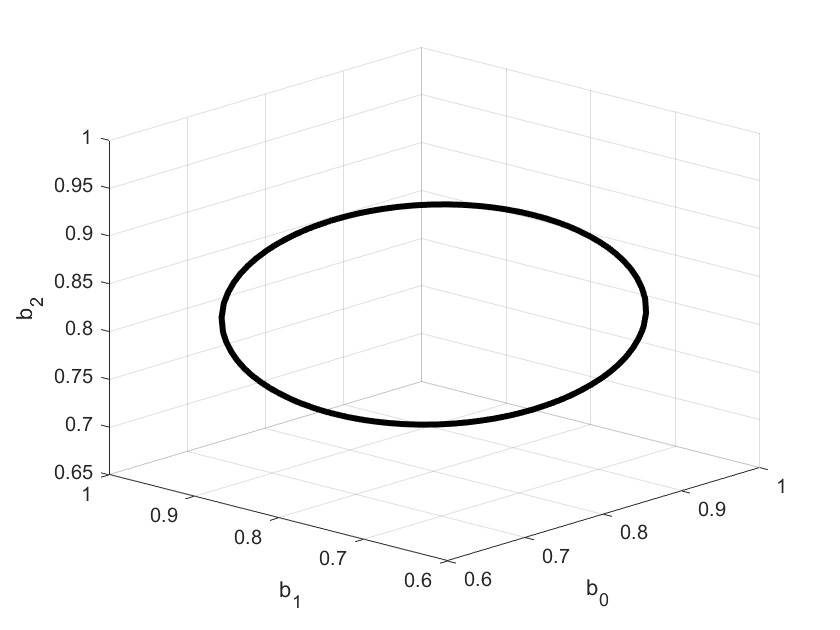

4.4 A 3 period model

To explain the complexity of the problem for , we consider the case . Here, the form of the survival probability does not allow to derive conditions that ensure a clear dominance of one strategy. In addition, the computational time increases with the number of periods.

To give some intuition on how to deal with this case, we restrict to deterministic strategies . Then, it holds that

which means that there are infinitely many combinations of that lead to the target distribution.

In particular, admissible triplets build (a part of) a circle as shown in Figure 4.

To choose the ruin-minimising strategy we look at survival probability

We define auxiliary random variables such that

which are correlated. Then, we have that

where , and is the corresponding density.

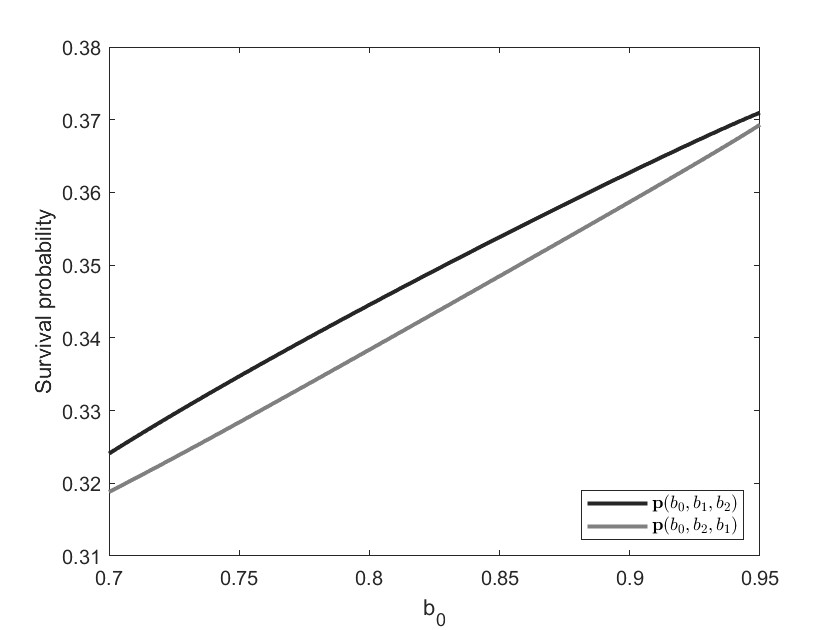

Figure 5 shows the survival probability with respect to the first component . It is clear that, once is chosen, there are only two possible choices for and . Suppose that, for instance , then for a fixed , the possible strategies are and . We see that the survival probability is maximised by the largest and the combination that leads to the higher survival probability is the sorted one, i.e. with .

We conclude the section by showing that the sorted sequence leads to a bigger survival probability than the “unsorted” sequence . This means, in particular, that like shown in Figure 5 any unsorted sequence will be overperformed by a sorted one.

To prove this, we denote by the survival probability of a strategy where the initial capital is .

Then,

where the inequality follows from the case .

5 Conclusions

In this paper, we consider an insurance company whose objective is to choose a dividend payment or a reinsurance strategy leading to a certain surplus distribution. The question which strategy to prefer depends on the underlying target functional – the value of expected discounted dividends (to be maximised) or the ruin probability (to be minimised).

Such a problem is motivated by the necessity of being able to compute risk measures, typically based on the distribution of a future loss at some fixed date. Fixing a terminal wealth distribution would allow to compute several risk measures at once, instead of choosing a specific constraint in the beginning of an optimisation task. In this line, the present paper represents the first step towards a more detailed and more realistic analysis of the problems faced by practitioners on the almost daily basis.

In addition, we would like to stress that the dividend related problems can be easily generalised to a continuous time framework. In the reinsurance setting we are able to fully analyse the 2-period problem. Since, reinsurance contracts are usually difficult or even impossible to update before the maturity date, this setting seems to be the most realistic one from a practical point of view.

Using a pool of possible distributions and mean/variance combinations instead of only one specific distribution is a possible extension direction. However, in this paper our main target is to introduce an idea and to illustrate with 2 clear settings how this idea can be implemented. For instance, in the reinsurance setting, the discrete nature of the problem does not allow to use the differential equation approach. Any return function would depend on the initial surplus and on the time. Changing the length of one interval would completely change the optimal strategy, as more weight will be put on the remaining intervals. Therefore, we are using purely probabilistic methods to prove our claims for the 2-period case. In the general n-period setting, the admissible strategies are not necessarily deterministic, and the optimal strategy may even not exist.

Our future research will concentrate on the extensions of the presented models. We plan to work on the n-period model for the reinsurance setting. We will also consider problems with non-normal target distributions and allow continuous time ruin-checks.

Acknowledgements

The work of K. Colaneri and B. Salterini has been partially supported by Indam-Gnampa though the project U-UFMBAZ-2020-000791. Part of this work has been done while K. Colaneri and B. Salterini were visiting TU Vienna.

The research of Julia Eisenberg was funded by the Austrian Science Fund (FWF), Project number V 603-N35.

References

- Albrecher and Thonhauser [2009] H. Albrecher and S. Thonhauser. Optimality results for dividend problems in insurance. Revista de la Real Academia de Ciencias Exactas, Físicas y Naturales. Serie A. Matemáticas. RACSAM, 103(2):295–320, 2009.

- Asmussen and Taksar [1997] S. Asmussen and M. Taksar. Controlled diffusion models for optimal dividend pay-out. Insurance Math. Econ, 20:1–15, 1997.

- Avanzi [2009] B. Avanzi. Strategies for dividend distribution: A review. North American Actuarial Journal, 13:217–251, 2009.

- Bai et al. [2012] L. Bai, M. Hunting, and J. Paulsen. Optimal dividend policies for a class of growth-restricted diffusion processes under transaction costs and solvency constraints. Finance and Stochastics, 16(3):477–511, 2012.

- Bernard and Tian [2009] C. Bernard and W. Tian. Optimal reinsurance arrangements under tail risk measures. Journal of risk and insurance, 76(3):709–725, 2009.

- Bi and Cai [2019] J. Bi and J. Cai. Optimal investment–reinsurance strategies with state dependent risk aversion and VaR constraints in correlated markets. Insurance: Mathematics and Economics, 85:1–14, 2019.

- Bi et al. [2014] J. Bi, Q. Meng, and Y. Zhang. Dynamic mean-variance and optimal reinsurance problems under the no-bankruptcy constraint for an insurer. Annals of Operations Research, 212(1):43–59, 2014.

- Chen et al. [2010] S. Chen, Z. Li, and K. Li. Optimal investment–reinsurance policy for an insurance company with var constraint. Insurance: Mathematics and Economics, 47(2):144–153, 2010.

- Choulli et al. [2001] T. Choulli, M. Taksar, and X. Y. Zhou. Excess-of-loss reinsurance for a company with debt liability and constraints on risk reduction. Quantitative Finance, 1(6):573, 2001.

- Hipp [2003] C. Hipp. Optimal dividend payment under a ruin constraint: Discrete time and state space. Blätter der DGVFM, 26:255–264, 2003.

- Hipp [2020] C. Hipp. Optimal dividend payment in De Finetti models: Survey and new results and strategies. Risks, 8(3):96, 2020.

- Huang and Yin [2019] Y. Huang and C. Yin. A unifying approach to constrained and unconstrained optimal reinsurance. Journal of Computational and Applied Mathematics, 360:1–17, 2019.

- Lo [2017a] A. Lo. A Neyman-Pearson perspective on optimal reinsurance with constraints. ASTIN Bulletin: The Journal of the IAA, 47(2):467–499, 2017a.

- Lo [2017b] A. Lo. A unifying approach to risk-measure-based optimal reinsurance problems with practical constraints. Scandinavian Actuarial Journal, 2017(7):584–605, 2017b.

- [15] Munich Re. The dividend at a glance. https://www.munichre.com/en/company/investors/shares/dividend.html.

- Paulsen [2003] J. Paulsen. Optimal dividend payouts for diffusions with solvency constraints. Finance and Stochastics, 7(4):457–473, 2003.

- Schmidli [2008] H. Schmidli. Stochastic Control in Insurance. Springer, London, 2008.

- Shreve et al. [1984] S.E. Shreve, J.P. Lehoczky, and D.P. Gaver. Optimal consumption for general diffusions with absorbing and reflecting barriers. SIAM J. Control and Optimization, 22:55–75, 1984.

- Thonhauser and Albrecher [2011] S. Thonhauser and H. Albrecher. Optimal dividend strategies for a compound Poisson process under transaction costs and power utility. Stochastic Models, 27(1):120–140, 2011.

- Wang and Siu [2020] N. Wang and T. K. Siu. Robust reinsurance contracts with risk constraint. Scandinavian Actuarial Journal, 2020(5):419–453, 2020.

- Zhang et al. [2016] N. Zhang, Z. Jin, S. Li, and P. Chen. Optimal reinsurance under dynamic VaR constraint. Insurance: Mathematics and Economics, 71:232–243, 2016.