Deep Partial Least Squares for Empirical Asset Pricing111This paper was presented as a keynote talk at the R in Finance Conference, Chicago, 2022. The authors would like to thank Peter Carl (Balyasny Asset Management), Francois Cocquemas (Florida State University), and Kris Boudt (KU Leuven), for useful discussions and input on this paper. 222The source code and data for this paper is available at https://github.com/Kem975/Deep_Partial_Least_Squares.

Abstract

We use deep partial least squares (DPLS) to estimate an asset pricing model for individual stock returns that exploits conditioning information in a flexible and dynamic way while attributing excess returns to a small set of statistical risk factors. The novel contribution is to resolve the non-linear factor structure, thus advancing the current paradigm of deep learning in empirical asset pricing which uses linear stochastic discount factors under an assumption of Gaussian asset returns and factors. This non-linear factor structure is extracted by using projected least squares to jointly project firm characteristics and asset returns on to a subspace of latent factors and using deep learning to learn the non-linear map from the factor loadings to the asset returns. The result of capturing this non-linear risk factor structure is to characterize anomalies in asset returns by both linear risk factor exposure and interaction effects. Thus the well known ability of deep learning to capture outliers, shed lights on the role of convexity and higher order terms in the latent factor structure on the factor risk premia. On the empirical side, we implement our DPLS factor models and exhibit superior performance to LASSO and plain vanilla deep learning models. Furthermore, our network training times are significantly reduced due to the more parsimonious architecture of DPLS. Specifically, using 3290 assets in the Russell 1000 index over a period of December 1989 to January 2018, we assess our DPLS factor model and generate information ratios that are approximately 1.2x greater than deep learning. DPLS explains variation and pricing errors and identifies the most prominent latent factors and firm characteristics.

Key Words: Deep Learning, Partial Least Squares, Shrinkage, Empirical Asset Pricing, Conditional Latent Factor Models, Non-Linear Risk.

1 Introduction

In this paper, we develop a deep factor methodology known as deep partial least squares (DPLS) as a projection based dimensionality reduction technique for empirical asset pricing regressions which, combined with deep learning, provides improved predictive performance on financial panel data while also providing information on the risk factor premia. Our DPLS approach is shown to be a natural, composable, and powerful approach to projecting both the predictors and the responses onto a relatively small set of orthonormal latent variables so as to maximize the covariance between the projected predictors and the projected responses. In contrast to principal component dimension reduction, PLS & DPLS projections are dependent on the response and thus leverage a wider dataset of firm charactersistcs for predicting returns. Polson et al. (2021) find evidence that DPLS shows superior predictive performance on non-financial cross-sectional data. Dixon and Polson (2020) show that deep learning identifies the most important interaction effects and factors. DPLS builds on this by boosting the covariance between the response and predictor, while simultaneously using the same statistical loadings generated by PLS. Furthermore, because DPLS is based on deep learning, it is able to automatically capture interaction effects.

Partial Least Squares (PLS) is a wide class of methods for modeling relations between sets of observed variables by means of latent variables. It is comprised of regression and classification tasks as well as dimension reduction techniques and modeling tools. The underlying assumption of all PLS methods is that the observed data is generated by a system or process which is driven by a smaller number of statistical latent variables.

Across hedge funds, asset management, and proprietary trading firms, it is commonplace to use supervised learning for macroeconomic and financial forecasting by performing ”feature engineering” — expanding the original set of covariates to include terms such as interactions, dummy variables or nonlinear functionals of the original predictors (Hoadley, 2001; Dobrev and Schaumburg, 2013; Dixon et al., 2017). It’s also increasingly common to aggregate multiple data sources for financial forecasting, combining traditional financial data such as stock prices with novel signals such as news sentiment (Dierckx et al., 2020; Algaba et al., 2021). Our goal is to employ supervised dimension reduction techniques which, when combined with deep learning, not only leads to a more parsimonious architecture with improved out-of-sample performance, but enable factor models to be properly seated in an equilibrium asset pricing framework in which the statistical factors serve as latent risk factors and a non-linear risk factor structure is represented by the network architecture. Our approach corresponds to the use of a non-linear stochastic discount factor (see Cochrane (2011)).

The rest of the paper is outlined as follows. Section 1.1 outlines the general connections with previous work and highlights the contribution of this paper. Section 2 surveys the related works on factor modeling works in more detail culminating in the introduction of our non-linear factor model, best viewed as a non-linear generalization of the BARRA factor model. Section 3 describes our general modeling methodology using deep learning within partial least squares for multi-index regression. Following Polson et al. (2021), we provide a nonlinear extension of partial least squares by using deep layers to model the relationship between the scores generated in PLS. Then in Section 3.4, we present the DPLS factor model and some of its variants. Section 4 demonstrates the application of our DPLS factor model to equity data consisting of monthly returns and firm characteristics. Finally, Section 5 concludes with directions for future research.

1.1 General Connection to Previous Work

Within the investment management industry, asset managers seek novel predictive firm characteristics to explain anomalies which are not captured by classical capital asset pricing and factor models. Recently a number of independent empirical studies, have shown the importance of using a higher number of, often highly correlated, predictors related to firm characteristics and other common factors (Moritz and Zimmermann, 2016; Harvey et al., 2015; Gu et al., 2018; Feng et al., 2018). In particular, Gu et al. (2018) analyze a dataset of more than 30,000 individual stocks over a 60 year period from 1957 to 2016, and determine over 900 correlated baseline signals.

Despite being widely used in the asset management industry, it is becoming increasingly well documented that ordinary linear regression is inadequate for high dimensional factor models. The frequently encountered problem of nearly collinear regressors can be addressed using regularization to provide shrinkage estimation (Hahn et al., 2013; Dobrev and Schaumburg, 2013; Cheng et al., 2016). Dobrev and Schaumburg (2013) develops a Regularized Reduced Rank Regression model, a special case of which generalizes principal component regression by applying reduced rank rather than linear regression to the principal components of the regressors, thereby disentangling the forecasting factors driving the outcomes from the factor structure in the predictors.

Moritz and Zimmermann (2016); Gu et al. (2018); Chen et al. (2019) highlight the inadequacies of OLS regression in variable selection over high dimensional datasets — in particular the inability to capture outliers. In contrast, deep neural network can explain more structure in stock returns because of their ability to fit flexible functional forms with many covariates, without apriori knowledge of the interaction effects. Feng et al. (2018) demonstrates the ability of a three-layer deep neural network to effectively predict asset returns from fundamental factors. Gu et al. (2021) apply auto-encoders to fit a latent factor conditional asset pricing model and demonstrate that the approach not only out-performs other factor models but is suitable for no-arbitrage pricing. However, techniques which project on statistical factors are difficult to economically interpret and have limited hedging utility.

Dixon and Polson (2020) demonstrate a three-layer deep neural network approach for fundamental factor modeling which not only outperforms OLS regression and LASSO but also provides interpretability –specifically, the importance of the predictors and interactions can be ranked and the uncertainty in predictor sensitivities can be estimated with bootstrap sampling techniques. Dixon and Polson (2022) extend their methodology to a Bayesian estimation framework to provide uncertainty quantification and a predictive distribution of excess returns.

There are a number of advantages of DPLS methodology over traditional deep learning. First, PLS uses linear methods to extract predictors and weight matrices. Due to a fundamental estimation result of Brillinger (2012) we show that these estimates can provide a stacking block for our DPLS model. Moreover, traditional diagnostics (bi-plots, scree-plots) to diagnose the depth and nature of the activation functions allow us to find a parsimonious model architecture. Frank and Friedman (1993) provides a Bayesian shrinkage interpretation of PLS. This permits the discrimination between unsupervised and supervised learning method. In other words, based on the value of shrinkage factors, one can deduce whether a supervised learning method such as DPLS is necessary or whether an unsupervised dimension reduction method such as PCA is adequate.

One of the remarkable discoveries by Polson et al. (2021) in fitting DPLS regression models is that the PLS projection can be entirely separated from the training of the deep network, thus enabling standard deep neural networks algorithms, such as stochastic gradient descent, to be used without modification. Drawing on a seminal result by Brillinger (1977) which paved the way for the landmark paper by Brillinger (2012) and later Naik and Tsai (2000), we formalize the critical observation that under some limiting assumptions, the projection directions in PLS are invariant to the functional form of the regression between score matrices, up to a constant of proportionality.

Our theoretical development parallels Brillinger (2012), namely that PLS regression is a strongly consistent estimator to the regression coefficient even when there exists a unknown non-linear relationship between the predictors and the responses. We invert this line of reasoning and instead show that the linear PLS estimate is strongly consistent with the score regression coefficients when the regression on scores is a (known) non-linear function. This unlocks PLS regression as a composable method – non-linear functional approximations can be composed with the PLS projection matrices without violating the consistency result. More precisely, one can use still use the same projections and x-loadings estimated by PLS, under a linear relationship between the input and output scores, while subsequently using deep learning to improve the predictive performance of the y-scores.

In the context of empirical asset pricing, the DPLS method is shown to deliver a key point of departure from Gu et al. (2018); Chen et al. (2019); Kelly et al. (2019) in enabling the modeling of a non-linear factor structure which corresponds to an assumed non-linear stochastic discount factor. Furthermore, we develop interpretative techniques for DPLS which show both firm characteristic and latent factor sensitivities and interaction effects are provided by the DPLS factor model.

As a further contribution, we show how our DPLS factor models not only provide a non-linear generalization of BARRA fundamental factor models but also briefly discuss how they provide a non-linear, non-stationary extension of dynamic factor models (Stock and Watson, 2010).

On the empirical side, we develop a no-arbitrage DPLS factor model with 50 factors for 3290 Russell 1000 indexed stocks over an approximate 30 year period and compare performance with LASSO and pure deep learning based fundamental factor models. Furthermore, we assess the risk-reward trade-off of our factor model and identify the implications of including a non-linear factor structure.

2 Factor Modeling

Our goal is to explain the differences in the cross-section of returns for individual stocks using a latent factor no-arbitrage asset pricing model, whereby any expected gain in asset returns over the risk-free rate is solely attributed to factor risk exposure. But rather than this returns model being linear in factors, or equivalently, assuming linear dependence of a stochastic discount factor on the factors, we seek to introduce non-linearity. The rationale for non-linearity in factor modeling is well motivated in the literature and can be reasoned from Stein’s lemma, that the non-linearity in the dependency of the returns on the factors arises precisely when the asset returns and factors are non-Gaussian.

While the practice of applying non-linear parametric functions, such as deep learning, to factor models is conceptually straightforward, the challenge becomes in how to go beyond a mere mechanical exercise in learning a non-linear function of predictor variables that maximizes the out- of-sample explanatory power for realized excess returns of stocks, to characterizing the risk-return tradeoff of assets built from our factor model, under the equilibrium asset pricing principle that characteristic-based predictability are determined through risk exposures to factors alone (Kelly et al., 2019). Thus, in informal terms, in order for factor models to be correctly seated in the framework of equilibrium asset pricing, it must resolve the predictability attributed to the factor exposures and not conflate this with mis-pricing. Furthermore, they must be no-arbitrage factor models and hence provide no intercept when regressed against excess returns.

The need for both explanatory power from a set of predictor variables, taken to be lagged firm characteristics, and risk-return properties inevitably leads to model design trade-offs. For example some machine learning approaches to factor modeling yield strong predictive power but yield no insight into risk factor attribution and therefore have questionable economic interpretability and practical utility. On the other hand, other approaches deploy machine learning in such a way as to guarantee that the characteristic-based predictability is attained solely through factor risk exposures while accounting for non-linearity between the factor loadings and the firm characteristics. However, those approaches that do resolve the risk factors, still rely on a linear relationship between the returns and factor loadings, or equivalently the stochastic discount factor remains linear in the factors (Chen et al., 2019).

Then there are questions of how best to reduce the set of predictor variables to a smaller number of latent factors to manage the risk-reward tradeoff. Such factors should ideally carry economic interpretability and be representable by factor mimicking portfolios. We can broadly separate the main approaches to non-linear factor models into the following three categories:

-

1.

Forecasting models which predict the excess returns directly as a non-linear function of the lagged firm characteristics. This essentially amounts to a pure exercise in prediction of excess returns given the lagged firm characteristics, without assessing the risk/return tradeoff in terms of the latent factors (see Gu et al. (2018); Dixon and Polson (2020)).

-

2.

Linear Conditional Latent Factors preserve a linear relationship between the excess returns and the factors – amounting to the use of a linear stochastic discount factor in the factors – but introducing the non-linearity between the conditional factor loadings and the lagged firm characteristics (see, for example, Kelly et al. (2019); Chen et al. (2019); Gu et al. (2021)). These approaches allow for latent factors and time-varying loadings which “can explain individual stock returns and estimate the best performing factors without taking an a prior stand on what the factors are” Kelly et al. (2019). This category of approaches is thus suitable for asset pricing as it provides insight into the factor risk premia by conditioning on firm characteristics.

-

3.

Non-linear Conditional Latent Factors model the excess returns directly as a non-linear function of the lagged firm characteristics, but allow for the estimation of the conditional factor loadings and the latent factors under a non-linear stochastic discount factor in the factors. Hence, the approach is suitable for asset pricing and it operates under the less restrictive assumption that the stochastic discount factor is linear in the factors. Equivalently, as per Stein’s lemma, such an approach does not assume that the asset returns and factors are Gaussian.

Our DPLS factor model bridges these first two categories to arrive at a model in the final category in its most general form. We stop short of claiming that the modeling approach recovers the second category of approaches, as there are nuanced issues in how the non-linearity is represented, the estimation of the latent factors, and the handling of the intercepts. Specifically, our approach is to use deep projected least squares regression to identify non-linear factor structure, that is the asset returns are attributed to non-linear risk factors, with non-linear conditional factor loadings in the lagged firm characteristics, rather than linear risk factors under non-linear conditional factor loadings. Moreover, the approach is suitable for no-arbitrage pricing as the intercept captures the portion of the model returns not attributed to the risk factors. We thus build on several ideas which culminate from the extensive factor model literature, some of the most closely related works we now detail here.

Gu et al. (2018) present a static predictive model for the excess returns at time , , which learns a flexible parameterized function, of a set of predictors – lagged firm characteristics, , observed at time :

where are the idiosyncratic zero-mean Gaussian errors. Dixon and Polson (2020) present a time dependent parameterization of this model which is trained period-by-period. The advantage of the time dependent model is that it needn’t assume stationarity in the returns and firm characteristics. Rather, at each period, a new model is fitted, which only relies on data from the current period and not over a questionably relevant history. It does however result in fewer training observations to fit the model and hence shrinkage, or other forms of model reduction, are needed to prevent over-fitting of highly parameterized models such as deep neural networks. Equivalently, Bayesian inference under a choice of prior on the parameters can reduce the number of training samples needed (see Dixon and Polson (2022) for further details of a Bayesian deep fundamental factor model).

These predictive models, however, offer no insight into the latent factor structure and therefore offer no insight into whether the characteristics/expected return relationship is driven by compensation for exposure to latent risk factors (Kelly et al., 2019). Specifically, there appears to be mechanism for identifying how the characteristics proxy for loadings on common risk factors.

Gu et al. (2021) present a conditional latent factor model for excess asset returns, in which the conditional and dynamic factor loadings are a non-linear parametric function of lagged firm characteristics, . Additionally the excess asset returns are linear in the -latent factors, , which are in turn a linear combination of all excess returns in the universe. The model is fitted period-by-period, i.e. as follows:

| (1) | |||||

| (2) | |||||

| (3) |

The advantage of their approach is three-fold: (i) asset return predictability derives entirely from the lagged firm characteristics via the exposures to the risk factors; (ii) the factors aren’t pre-determined heuristically by a two-step procedure, as in the Fama-French model, but rather the factor structure is determined statistically in a single-step, taking a data driven approach to factor structure derivation and not relying on heuristics for characterizing the factor-structure; and (iii) the factors can be interpreted from how the dynamical loadings map to firm characteristics. For example, in any given period, their model can characterise which firm characteristics are the most prominent across all assets in any factor loading.

A technical development in Gu et al. (2021) is the presentation of an auto-encoder like neural network architecture which is customized to represent the structure of the model. Specifically a feed-forward architecture for the firm characteristics yields a hidden layer output representing the factor loadings and this is subsequently multiplied by latent factors which are given by a linear feedforward layer, with excess asset returns as inputs. While this network exhibits the signature bottleneck of an autoencoder, it is technically not an auto-encoder. This is because, like PCA, autoencoders are unsupervised learning methods which rely solely on returns to identify the latent factor structure. They do not leverage conditioning variables to identify this factor structure.

However, in seeking to modify this architecture to include firm characteristic data, they have essentially arrived at what partial least squares regression was exactly designed for, namely supervised dimension reduction by accounting for the returns and leveraging the lagged firm characteristics to identify the latent factor structure. Hence, although Gu et al. (2021) serve as the inspiration for our work, we argue that the deep partial least squares regression architecture is the natural choice for non-linear conditional latent factor models.

Another important distinguishing aspect of factor models is their approach to variable selection and regularization. The literature seems to be divided in statistical variable selection and regularization approaches versus the use of financial theory or “model based” variable selection and regularization. A prime example of statistical approaches would be LASSO penalized linear models which use shrinkage and variable selection to manage high dimensionality by forcing the coefficients on most regressors near or exactly to zero. This can, however, produce sub-optimal forecasts when predictors are highly correlated. A simple example of this problem is a case in which all of the predictors are equal to the forecast target plus an iid noise term. In this situation, choosing a subset of predictors via LASSO penalty is inferior to taking a simple average of the predictors and using this as the sole predictor in a univariate regression. However, other approaches to variable selection are commonly used in factor modeling. PCA, PCR, and PLS are all examples of projection methods which rely on a shrinkage mechanism which shrinks away from the origin for certain eigen-directions. The resulting shrinkage factors along each of the eigen-directions, referred to as principle components in PCA and PCR, or scale factors in PLS, are chosen to maximize the explained covariance either in the predictors or between the predictors and the responses respectively. These static approaches appear widely in the literature, most notably the asymptotic PCA (APCA) method (Connor and Korajczyk, 1988) which is suitable when , and the use of PCA (Swanson, 2014) when . As a panel regression, , Stock and Watson (2010) and Bai and Ng (2002) apply PCA to the covariance of asset returns:

where and are the left and right singular vectors of the covariance matrix, representing the factor loadings, and is a diagonal matrix with eigenvalues, sorted in descending order, representing the factors (i.e. principle components). The first latent factor corresponds to the direction that captures the maximum variance in the asset returns, the second factor corresponds to the direction of maximum variance under a complementary projection in the remaining orthogonal subspace, and so forth. This parsimony of factors is appealing as it can explain asset return covariance by a small number of systematic factors across the market.

These approaches suffer from many shortcomings – aside from violating the no-arbitrage principle unless the PCA methodology is modified to use uncentered second moments of excess returns– the main shortfalls being that the latent factors poorly explain the outliers in asset returns. As put succinctly by Kozak et al. (2018), “It is perfectly possible for a [principle component] factor to be important in explaining return variance but to play no role in pricing”. Another point of distinction is that the factors are purely statistical and not macro-financial, hence such risks are difficult to interpret in a macro-financial model.

A key development relevant to this paper is Kelly and Pruitt (2015) , who apply PLS as a three-pass regression filter to successfully filter out the impact of irrelevant risk factors, a problem that the method of principal components alone cannot be guaranteed to do. However, unlike their three-step regression, our approach is a period-by-period single step model and, like Gu et al. (2021), our betas are dynamic. So while our latent risk factors may vary period-to-period, we avoid data stationarity assumptions which are needed by Kelly and Pruitt (2015).

Another line of reasoning is pursued by Lettau and Pelger (2020), who propose a new method for estimating latent asset pricing factors that fit the time-series and cross-section of expected returns. Their estimator generalizes PCA by including a penalty on the pricing error in expected return leading to statistical risk factors which depend only on small set of firm characteristics. Their work sheds light on the “factor zoo” problem, namely which risk factors are really important and which factors are subsumed by others (Cochrane, 2011). While our model is period-by-period cross-sectional and does not mirror the experimental design of Lettau and Pelger (2020), we do seek to identify how, in any period, out-of-sample predictions of asset returns are attributed to the statistical risk factors and which firm characteristics, combined with their interaction effects, are most prominent.

Another modernized approach, which generalizes PCA to allow both dynamic loading and factor structure derived from firm characteristics, is the instrumented PCA (IPCA) factor model Kelly et al. (2019), which for ease of exposition, we show in its restricted form:

| (4) |

where projects the lagged firm characteristics on to the latent factors and is static. Note that the loadings are now dynamic due to the reliance on the lagged firm characteristics. This model allows for a potentially large number of characteristics to be mapped on to a smaller set of common latent risk factors that explain anomalies in asset returns. The projected characteristics, or more precisely, a linear combination of characteristics, thus proxy for loadings on each of the common risk factors and admit the intuitive interpretation that higher loadings result in higher expected returns to compensate for higher exposures, i.e. increased factor risk premia. More importantly, the most important characteristics associated with each risk factor can be estimated from observed excess returns and firm characteristics without, apriori, the use of heuristic mappings between them.

Our experimental design broadly follows the cross-sectional modeling approach used by (Fama and MacBeth, 1973) and BARRA factor models (see Rosenberg and Marathe (1976); Carvalho et al. (2012)) are appealing because of their simplicity and their economic interpretability, generating tradable portfolios. The BARRA model is able to capture linear effects of macroeconomic events on individual securities. The choice of factors are microeconomic characteristics - essentially common factors, such as industry membership, financial structure, or growth orientation (Nielsen and Bender, 2010).

Under the assumption of homoscedasticity, factor realizations can be estimated in the BARRA model by ordinary least squares regression444The BARRA factor model is often presented in the more general form with heteroscedastic error but we do not consider the non-linear extension here.. OLS regression exhibits poor expressability and relies on the Gaussian errors being independent of the regressors. Generalizing to non-linearities and incorporating interaction effects is a harder task.

The BARRA fundamental factor model555Specifically, the predictive form of the BARRA model is conventionally used for risk modeling, however, we shall use adopt a non-linear version of this model for a stock selection strategy based on predicted returns. is a single-index cross-sectional model which assumes that the factor loadings are proxied by the firm characteristics. The model expresses the linear relationship between fundamental factors and the asset’s returns:

| (5) |

where is the matrix of known factor loadings (betas): is the exposure of asset to factor at time and assumed to proxy the firm characteristic. The loadings therefore correspond to asset specific attributes such as market capitalization, industry classification, style classification. is the vector of unobserved factor realizations at time , including . is the vector of single-period asset returns observed at time . The errors are assumed independent of the factor realizations with heteroschedastic Gaussian error, . Then, in principle, factor realizations can be estimated with OLS regression. Note that there are more general estimation frameworks for estimating factors under heteroschedastic error (see e.g. Korteweg and Polson (2009); Tsay (2010)). The BARRA model can be viewed as a special case of IPCA when the projection is the identity matrix (Kelly et al., 2019).

Following Dixon and Polson (2020), we can generalize the BARRA model by considering a period-by-period non-linear cross-sectional fundamental factor model of the form

| (6) |

where are single-period asset returns, is a differentiable non-linear function that maps the row of to the asset return at time . The map is assumed to incorporate a bias term so that . In the special case when is linear, the map is . are zero mean i.i.d. error variates.

The forecasted returns, are given by the conditional expectation, . Hence, we seek to predict returns over the horizon from the lagged firm charactertistcs , which are by construction measurable at time . This model can hence be mapped on to a growing body of research on returns prediction using neural networks. One appealing aspect of this approach is that stationarity of the factor realizations is not required since we only predict one period ahead and, in contrast to time series models, then retrain in each subsequent period using the latest observations only.

In Section 3.4, we show how DPLS is applied to this model to project the firm characteristics onto a smaller set of latent risk factors with resulting non-linear factor structure in the learned model and characterization of the risk factor premia.

2.1 Stochastic discount factors

For completeness, we comment on our modeling approach from an entirely different line of reasoning rooted in arbitrage pricing theory. Cochrane (2011) shows how the one-factor CAPM model of Sharpe can be obtained as a result of consumption utility maximization with the Markowitz quadratic utility function, and under the assumption that the market is at equilibrium and all investors are identical (and the same as the representative investor) and hold the market portfolio. Furthermore, Cochrane (2011) also shows how different asset pricing models can be equivalently interpreted as particular models for the stochastic discount factor (SDF) (an ‘index of bad times’) where is a set of observed or inferred dynamic variables such as market and sector returns, macroeconomic variables etc. The SDF does not depend on characteristics of individual assets such as stocks, because with this theory the SDF is universal for all assets including stocks, bonds, derivatives etc.

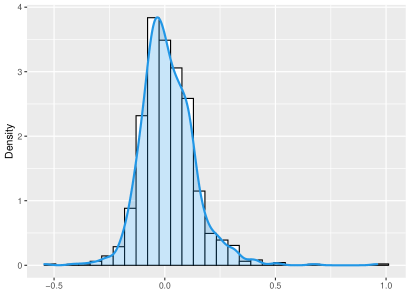

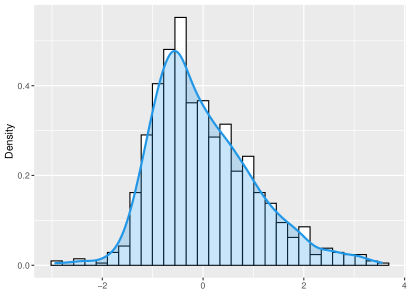

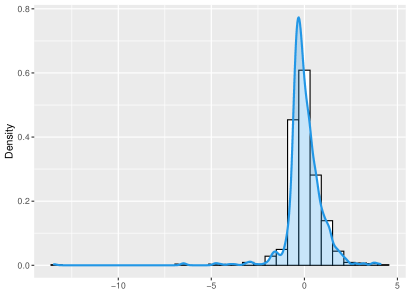

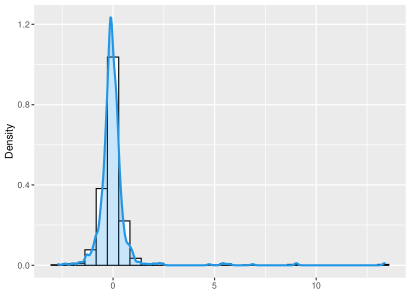

|

|

| (a) Excess returns | (b) Book-to-Price |

|

|

| (c) Total asset growth | (d) Cash flow volatility |

While less visited than the above literature on estimating risk premia, there is yet another line of reasoning that focuses on estimation of risk prices, i.e., the extent to which the factor associated with a characteristic helps price assets by contributing to variation (Kozak et al., 2018; Chen et al., 2019). The former authors arrive at a characteristics-sparse stochastic discount factor (SDF) representation that is linear in only a few such factors and conclude that there simply isn’t enough redundancy across the factors to justify only a handful of factors, e.g. FF3, FF4, FF5 etc. (Chen et al., 2019)’s approach to enforcing no-arbitrage factor modeling is predicated on the notion that the mere existence of a SDF itself is critically dependent on the absence of arbitrage, once this assumption is accepted, any model building amounts to designing a parameterized model where is a set of trainable parameters, and training the model on available data. Chen et al. (2019) introduced Generative Adversarial Networks (GANs) to incorporate the no-arbitrage condition as part of the neural network algorithm and estimate a linear stochastic discount factor that explains all stock returns from the conditional moment constraints implied by no-arbitrage. For ease of exposition, here we drop the subscript on the SDF, returns, and factors.

It is well known, as a consequence of Stein’s lemma, that any nonlinear model of the stochastic discount factor, , with a Lipschitz continuous , can be turned into a linear model by assuming normal returns, , and normal factors, (see pg. 154 of Cochrane (2011)). Such a linear stochastic discount factor corresponds to a linear factor beta pricing model , where .

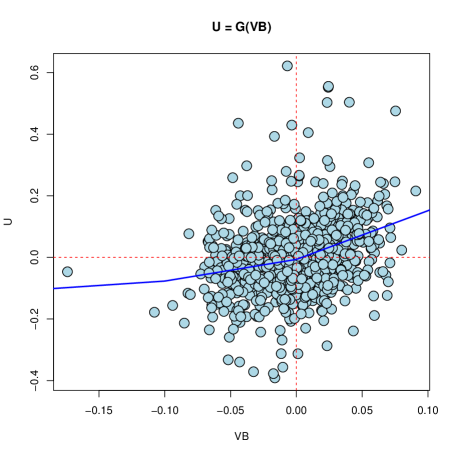

However, as demonstrated by the cross-sections of all Russell index assets on February 2013 in Figure 1, the assumption of normality on monthly excess returns and factors is too strong and we therefore seek a non-linear stochastic discount factor corresponding to a non-linear factor beta pricing model, . We show that expressing the stochastic discount factor in terms of a non-linear function, , in the factors is equivalent to the non-linear factor beta pricing model.

Theorem 1 (Non-linear discount factors).

Given the non-linear stochastic discount factor

a function s.t.

See Appendix C for the proof.

Remark 1.

Conversely, given a , a .

Remark 2.

Note for, avoidance of doubt, that we do not estimate the SDF in this paper as in Kozak et al. (2018); Chen et al. (2019). Rather we reason, on the basis of this theorem, that if we estimate risk premia via a non-linear function, , then there is a corresponding non-linear SDF. The economic implications of a corresponding utility function being non-Markowitz quadratic are beyond the scope of this paper. However, we comment in passing that many constrained utility functions used by practitioners to incorporate exposure limits, maximum drawdown limits, shorting selling limits, CVaR penalized expected returns etc, depart from the mean-variance utility function and motivate a more flexible form of the SDF than linear in the discount factors.

3 DPLS Regression

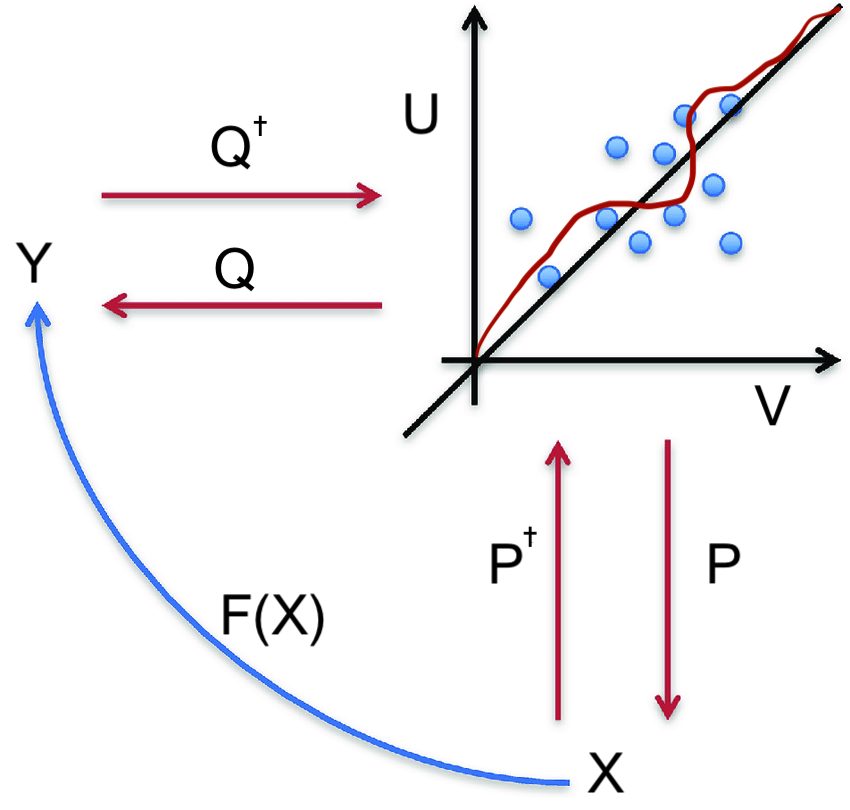

Informally, our goal is to jointly project the excess asset returns and firm characteristics with projection matrices and on to a pair of components respectively such that:

in a such a way that the prediction of excess asset returns

is based on using the learned map in the projected space. The approach is thus using conditioning information from the lagged firm characteristics and the excess asset returns to arrive at a non-linear representation of the latent risk factors.

To formalize this method, we begin by reviewing linear PLS regression in the more general setup before introducing the DPLS method of Polson et al. (2021). Then in Section 3.4 we introduce a deep PLS factor model, where the factor loadings, , are interpreted as risk premia and the latent risk factors are given by the gradient of the fitted function, , in the projected space.

In general, PLS regression uses both and to calculate the projection, further it simultaneously finds projections for both input and output , making it applicable to more general problems with multi-index output vectors as well as high dimensional input vectors. PLS searches for a set of latent vectors (i.e. components) that perform a simultaneous decomposition of and with the constraint that these components explain as much as possible of the sampled covariance between and .

PLS hence finds projection directions which maximize the sample covariance between and — the resulting projections and for and , respectively are called score matrices, and the projection matrices and are called loadings.

The input-score , has columns, one for each “feature” and is chosen via cross-validation. The key principle is that is a good predictor of , the output-scores. These relations are illustrated in Figure 2 and summarized by the equations below for the general multivariate PLS model:

Here and are low-rank projection (loading) matrices and are projections of and respectively. The columns of are orthonormal and referred to as the “latent vectors”.

DPLS uses a feedforward neural network to regress the output-score on the input-scores:

where is a deep neural network with layers, that is, a super-position of univariate semi-affine functions, , to give

and the unknown parameters are a set of weight matrices and a set of bias vectors . Any weight matrix , can be expressed as column m-vectors . We denote each weight as .

The semi-affine function is itself defined as the composition of the activation function, , and an affine map:

| (7) |

where is the output from the previous layer, . The activation functions, , e.g. , are critical to non-linear behavior of the model. Without them, would be a linear map and, as such, would be incapable of capturing interaction effects between the inputs. This is true even if the network has many layers.

Deep learning theory

The choice of feed-forward architecture is motivated on theoretical and empirical grounds. First, feed-forward networks are furnished with a universal approximation theorem (Hornik et al., 1989). It has further been shown that deep networks can achieve superior performance versus linear additive models, such as linear regression, while avoiding the curse of dimensionality (Poggio, 2016).

Martin and Mahoney (2018) show that deep networks are implicitly self-regularizing and Tishby and Zaslavsky (2015) characterizes the layers as ’statistically decoupling’ the input variables.

There are additionally many recent theoretical developments which characterize the approximation behavior as a function of network depth, width and sparsity level (Polson and Rockova, 2018). Recently Bartlett et al. (2017) prove upper and lower bounds on the expressability of deep feedforward neural network classifiers with the piecewise linear activation function, such as ReLU activation functions. They show that the relationship between expressability and depth is determined by the degree of the activation function.

These bounds are tight for almost the entire range of parameters. Letting denote the total number of weights, they prove that the VC-dimension is .

They further showed the effect of network depth on VC-dimension with different non-linearities: there is no dependence for piecewise-constant, linear dependence for piecewise-linear, and no more than quadratic dependence for general piecewise-polynomial. Thus the relationship between expressability and depth is determined by the degree of the activation function.

There is further ample theoretical evidence to suggest that shallow networks can’t approximate the class of non-linear functions represented by deep ReLU networks without blow-up. Telgarsky (2016) shows that there is a ReLU network with layers and units such that any network approximating it with only layers must have units. Mhaskar et al. (2016) discuss the differences between composition versus additive models and show that it is possible to approximate higher polynomials much more efficiently with several hidden layers than a single hidden layer.

3.1 PLS Estimation

In the literature, there are multiple types of algorithms for finding the projections (Manne, 1987). Algorithms differ on whether they estimate the score matrix as orthonormal columns or not. The original one proposed by Wold et al. (1984) uses the conjugate-gradient method (Golub and Van Loan, 2013) to invert matrices. The first PLS projection and is found by maximizing the sample covariance between the and scores

| subject to |

Then the corresponding scores are

We can see from the definition that the directions (loadings) for are the right singular vectors of and loadings for are the left singular vectors. The next step is to perform regression of on , namely . The next column of the projection matrix is found by calculating the singular vectors of the residual matrices .

The final regression problem is solved . Thus the PLS estimate is

Helland (1990) showed that PLS estimator can be calculated as

where ,

where the average is taken over training data, that is . Once the loadings and scores have been estimated, we can then train a deep learner on and then use to predict and hence obtain an estimate of .

To understand why the deep-learner can be decoupled from the estimation of the projection matrices, we need to establish that the projection directions in PLS are invariant to the functional form of the regression between score matrices, up to a constant of proportionality.

We first recall a key asymptotic result from Naik and Tsai (2000) which builds on an earlier result on OLS regression by Brillinger (2012), namely that PLS regression is a consistent estimator of the regression coefficient even when there exists an unknown non-linear relationship between the and .

Assumption 1.

Assume , where , are independent normals with mean and non-singular covariance matrix , and that the xs are independent of , where each has finite variance .

Assumption 2.

Let , where , is a scalar and . Assume that is a measurable function of with and for .

Theorem 2 (Naik and Tsai (2000)).

Assume the above two assumptions hold. Then the PLS estimator is a strongly consistent estimator of up to constants of proportionality.

The theorem is closely related to Stein’s Lemma Stein (2012), which states that the covariance between the Gaussian regressand and a non-linear Lipschitz function of the regressors can be written as the covariance between the regressand and the regressors themselves up to a multiplicative term in the expectation of the derivative of the non-linear function.

The practical implication of Brillinger’s theorem Brillinger (2012) or Naik & Tsai theorem is that OLS or PLS respectively generalize to the case is not linear when is jointly Gaussian.

For the purpose of modifying the PLS algorithm to use a deep-learner rather than the linear PLS estimator, we would like to know that the strong consistency result still holds if we introduce a non-linear regression to estimate the relation between the scores. Of course, the mere exercise of reintroducing non-linear regression when Naik & Tsai’s theorem shows that a linear PLS algorithm will generalize to a non-linear function seems like a tautology.

However, our immediate motivation, before building a regression model for non-Gaussian data, is to first show that we needn’t restrict the PLS algorithm to a linear estimator for the result of Naik & Tsai to hold. Rather, the power of PLS is in its composability — we can use the x-scores and y-scores estimated by the PLS algorithm composed with a deep learning estimate of the map between the scores, rather than needing to substantially overhaul the PLS method to embed machine learning methods. More precisely, we first seek to generalize Naik & Tsai theorem by showing that PLS can be composable with another machine learning method while preserving its consistency property.

In more detail, we show that the strongly consistent estimator, , is invariant under a parameterized non-linear function in the projected space, , s.t. , up to a constant of proportionality. The x-scores, , are jointly Gaussian if the predictors, , are jointly Gaussian, since the projection, , is a linear transformation.

Definition 3.1.

Given the system of equations:

where and are projection matrices referred to as loadings. are the y-scores and orthonormal x-scores respectively. and are independent and have finite variance and respectively. Let .

Assumption 3.

Assume that is Gaussian and is a “good” predictor of through some non-linear transformation , where is a measurable function with and for .

Theorem 3 (Composability of PLS).

Under this assumption on , embedded in the PLS method, the PLS estimator, , is a consistent estimator of .

Proof.

where .

and the PLS estimator is a consistent estimator of . ∎

We discuss and speculate on this result.

Remark 3.

Since the PLS estimator is invariant under the choice of non-linearity in functional approximation between the x-scores and y-scores, we can use the x-scores and projection matrices estimated by the PLS method without needing to modify them. This provides the justification for composability of PLS with the deep leaner.

Remark 4.

While DPLS is intended to be a general methodology and not limited to Gaussian predictors, we make no such estimator consistency claim when is not Gaussian. Rather, the stated goal of composability is simply to provide a better predictor of the Y-scores under the assumption that is non-linear as the linear estimator is no longer “valid” due to the non-Gaussian predictors.

Remark 5.

Under an idealized data generation process, we may use PLS as a baseline for measuring the performance of DPLS and thus if is Gaussian, then we might expect to characterize any relative gain in performance when using DPLS in place of PLS under infinite sample sizes. After all, in such a case, a linear approximation should suffice up to a constant of proportionality. However, we exercise some caution in over-interpreting the theorem – the Brillinger and Naik & Tsai result is simply an asymptotic consistency result and says nothing about whether linear regression is “optimal” when there is a non-linear relationship between the response and the Gaussian predictors. In fact the asymptotic covariance matrix used for the least squares estimate of the regression coefficients depends on the unknown form of the non-linearity between and . Needless to say, the limitations of an asymptotic result to sampling error from use of a finite sample size are part and parcel of any frequentist approach.

Remark 6.

One can estimate the weights in the first layer of the network using the PLS estimator. Put differently, we would expect the regression coefficients in the PLS method to match the weights in the first layer of the network when is Gaussian, irrespective of the value of the weights and choice of architecture of the remaining network layers. In practice, the comparison will not be exact due to sampling noise, but also because of the constant of proportionality. However, the functional form of is known and the constant of proportionality can be estimated. When the data is non-Gaussian, we speculate that the weights in the first can be initialized more effectively than a random initialization under the assumption that they would be similar under mild departure from Gaussian assumptions.

Our consistency result permits us to compose the loadings estimated by PLS, under the original assumption of a linear relationship between the input and output scores, with a non-linear function to improve the predictive performance of the output scores (See Figure 3 for an illustration). The theorem shows that the composition of a deep-learner with the projection matrices estimated separately by the PLS algorithm does not “break” PLS – the asymptotic consistent estimate result of Naik & Tsai still holds. With this in mind, we propose the following two-step DPLS algorithm here:

-

1.

Assume that the predictors, , are Gaussian and hence by the Naik & Tsai Theorum, the PLS estimator is a consistent estimator of the coefficients in .

-

2.

Relax the assumption of Gaussian predictors: apply a deep-learner to the non-Gaussian x-scores and y-scores estimated by PLS, estimate a non-linear map to improve the prediction of the y-scores. Optionally use the PLS coefficients as initial guesses of the weights in the first layer of .

In this respect, DPLS could be viewed, as an end-to-end deep learning architecture between and :

where in given by the PLS algorithm and is projection of on to the first layer, the next layer is non-linear in the scores (with the weights possibly even estimated by PLS), the penultimate layer is a linear projection on to space of y-scores (i.e. the activation function is linear and the final layer is the linear projection , estimated by PLS, from the -vector space to the vector space of .

More generally, PLS can be used as a layer at any stage of deep learning, not just the first. For example, in a convolutional neural network,

where denotes the convolution over the region , with input , weights and bias . Then we can add a PLS layer by regressing the output on and perform feature reduction, which results in a CNN-PLS model.

Our theorem and algorithm is not limited to use with deep learning either. PLS can be combined with many well-known machine learning models, such as kernel regression (Rosipal and Trejo (2001), Rosipal et al. (2001)), Gaussian processes (Gramacy and Lian (2012)), tree models. For example, Higdon et al. (2008) uses a PCA decomposition of the -variable before applying a nonlinear regression method. Of course deep learning is attractive because of its universal representation theorem and composability with other algebraic transformations.

3.2 PLS Algorithm

One common problem with estimation of linear prediction rules, , on high dimensional datasets is the high variance due to the typically ill-conditioned nature of the design matrix, . Shrinkage methods are used to address this issues and work by biasing coefficient vector away from directions in which the predictors have low sampling variability— or equivalently, sway from the ”least important” principal components of .

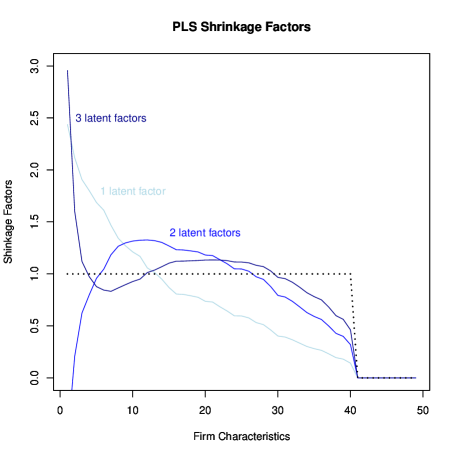

The Bayesian shrinkage interpretation of Frank and Friedman (1993) provides a useful perspective for explaining the PLS algorithm. PLS, in fact, relies on a non-standard shrinkage mechanism which shrinks away from the origin for certain eigen-directions. The shrinkage factors (a.k.a. scale factors) along each of the eigen-directions are nonlinear in the response values. They also depend on the OLS solution.

Polson and Scott Polson and Scott (2010, 2012) provide a general theory of global-local shrinkage and, in particular, analyze g-prior and horseshoe shrinkage. Bhadra et al. (2020) build on this work by demonstrating that horseshoe regularisation is useful for a wide class of machine learning methods.

We first center and standardise . Then, we provide an SVD decomposition of the sample covariance matrix:

This finds the eigenvalues and corresponding eigenvectors arranged in descending order, so we can write the eigenvector decomposition

This leads to a sequence of regression models with being the response mean and

where is the rank of (number of nonzero ). Therefore, PLS finds ”features” = .

The PLS estimator is of the form

where are PLS scale factors for the top eigenvectors (Frank and Friedman, 1993) of the form

As shown in Figure 4, the scale factors provide a diagnostic plot: . If any then one can expect supervised learning (a.k.a. PLS with ’s influencing the scaling factors) will lead to different predictions than unsupervised learning. In this sense, PLS is an optimistic procedure in that the goal is to maximise the explained variability of the output in sample with the hope of generalising well out-of-sample. For linear estimators, means that both the bias and the variance are increased. Once the projection matrices are estimated, a standard stochastic gradient descent algorithm, such as Adam (Kingma and Ba, 2014), can be used to fit the deep learning model to predict the y-scores.

3.3 Covariate sensitivities

We use a gradient-based technique for ranking the importance of the covariates in the fitted DPLS model. Note, for avoidance of doubt, that in contrast to PCA and autoencoders, the DPLS model sensitivities are given in terms of the observed covariates and not just the latent statistical factors. Our proposed method is consistent with how coefficients are interpreted in linear regression, i.e. as model sensitivities and is thus appealing to practitioners accustomed to use OLS regression. In our approach, the model sensitivities are the partial derivatives of the fitted model output w.r.t. each input. This method is consistent with Horel and Giesecke (2019) who develop statistical tests for the significance of the input variables in a neural network, using their partial derivatives. The test statistic is based on a weighted distribution of the square of the neural network partial derivative, w.r.t. each input. However, the scope of their study is limited to a single-hidden layer network and treats the asymptotic distribution of the network as a Gaussian process.

Here we shall consider deep networks with an arbitrary number of layers and do not rely on asymptotic approximations, which may be limited when the network has a small number of neurons. Indeed we derive closed form expressions for the Jacobian and Hessian - the off-diagonals provide sensitivities to interaction terms. In contrast to Horel and Giesecke (2019), our goal is to characterize the dispersion of the empirical sensitivity distribution - confidence intervals of the distributions can be found by Bootstrap sampling (see, for example, Wood (2005)). Such an approach is only useful in practice if the variance of these distributions are bounded. Our primary theoretical result then is to characterize the upper bound on the variance of the partial derivatives and show that it is bounded for finite weights.

To evaluate fitted model sensitivities analytically in the DPLS method, we require that the function is continuous and differentiable everywhere. Furthermore, for stability of the interpretation, we shall require that is a Lipschitz continuous666If Lipschitz continuity is not imposed, then a small change in one of the input values could result in an undesirable large variation in the derivative. That is, there is a positive real constant s.t. , . Such a constraint is necessary for the first derivative to be bounded and hence amenable to the derivatives, w.r.t. to the inputs, providing interpretability.

Fortunately, provided that the weights and biases are finite, each semi-affine function is Lipschitz continuous everywhere. For example, the function is continuously differentiable with derivative, , is globally bounded. With finite weights, the composition of with an affine function is also Lipschitz. Clearly ReLU is not continuously differentiable and one must instead use a softplus function, a smooth approximation to ReLU.

From the definition of the DPLS model, we can write the fitted model in the compact form

Taking first and second derivatives of the response w.r.t. the input variables gives

| (8) | |||||

| (9) |

where and are the Jacobian and Hessian matrices of the fitted deep learner w.r.t. to the X-scores, . Thus, the covariate sensitivities in the DPLS model are linear transformations of the sensitivities of the fitted deep learner w.r.t. to the latent X-scores. See Section B, for further details of the functional form of the Jacobian and Hessian matrix.

3.4 DPLS Factor Models

To fix ideas, we begin by presenting a linear PLS factor model and then show this generalizes to our deep PLS factor model. A PLS factor model is of the form

| (10) |

is the Moore-Penrose Inverse of , is a diagonal matrix with the regression coefficients on the diagonal estimated by the PLS algorithm.

The latent risk factors, , are given by the projection of the regression coefficients and the factor loadings (the X-scores), , are projections of the firm characteristics, onto the K-factors.

In any time period, , we can therefore attribute the expected excess returns of stock to the latent factors:

| (11) |

Similarly, in any period, , we can attribute the conditional variance of the excess asset returns to the latent factors

| (12) |

where is the covariance matrix of the latent factors at time and is the variance of the error.

Note that PLS does not explicitly find the explained variance of the returns. Rather for a target explained covariance between the excess returns and the characteristics, PLS determines the number of factors .

We now turn to a specific subset of deep fundamental factor models — DPLS models. DPLS projects the response and predictors below as

and a feedforward neural network is used to predict the output scores from the input-scores:

| (13) |

The primary benefit of using deep learning, is that it is able to automatically capture non-linear effects and, in particular, is robust to outliers.

The DPLS model gives the risk premia on the latent risk factors by a Taylor expansion of the deep learner, , about the origin :

| (14) | |||||

| (15) | |||||

| (16) |

where the latent risk factors are given by and the quadratic term, defining the non-linear factor structure, requires the Hessian, , evaluated at the origin. This Hessian contains the interaction effects w.r.t. to the risk premia (x-scores).

3.4.1 State-space DPLS fundamental Factor Models

For completeness, we can explore other variants of the DPLS fundamental factor model above – specifically it can be written in a more general form which includes higher order lag terms up to maximum lag . Specifically we posit the non-linear state-space model:

with the score state-vectors defined as

where and . Note, as a special case, that the vector autoregressive form (a.k.a. semi-supervised learning) of the DPLS model (i.e. ) is the system of equations

where .

If the projection matrix and parameters, are further fixed in time then we see that the DPLS factor model is in fact a non-linear Dynamic Factor Model (DFM) (Stock and Watson, 2010) with projections on to scores:

where is the latent state variable of factors (a.k.a. score state vector). In the Stock and Watson (2010) model, is a linear projection onto lagged latent factors and is replaced with a static state-space update matrix. Their model requires stationarity. One important advantage of our DPLS model, aside from the ability to capture non-linearity in the latent state update, is that can be an advanced recurrent neural network architecture such as LSTMs or GRUs, thus relaxing the requirement for stationarity (Dixon, 2022).

4 Experiments

This section presents the application of our DPLS factor model to all stocks in the Russell 1000 index, which represents the top 1000 companies by market capitalization in the United States. The historical data covers an approximately 30 year period of monthly updates between January 1989 to November 2018, with a coverage universe of 3290 stocks. In every month, each stock includes 49 BARRA model factors — 19 of which are fundamental factors and the remainder are GICS sector dummy variables (see Section A for a description of the factors).

Note that the BARRA factor model includes many more explanatory variables than used in our experiments below, but the purpose, here, is to illustrate the application of our framework to a larger set of factors. Equally, the BARRA factors are designed to explain variance in asset returns rather than capture alpha, however, our results focus both on expected asset returns and explained variance of asset returns based on conditional exposures to latent risk factors. Note, for avoidance of doubt, that our goal in this section is not to shed further light on the “factor zoo problem”, but simply to advocate for the use of DPLS as a methodology for factor modeling based on its ability to capture outliers and attribute prediction error to conditional exposures to latent risk factors.

Our experiments broadly focus on three aspects of the DPLS factor model:

-

1.

Ability to capture outliers in monthly excess returns;

-

2.

Ability to generate higher performing managed portfolios under a risk adjusted return metric; and

-

3.

Ability to explain asset returns and risk via risk premia.

Data cleaning:

All stocks with missing factor exposures are removed from the estimation universe for the date of the missing factors only. To avoid excessive turn-over in the estimation universe over each consecutive period, we include all dropped symbols in the index over the 12 consecutive monthly periods. Further details of the data preparation, including sanitization to avoid violating licensing agreements, are provided in the documentation for the source code repository referenced on the first page.

Rescaling:

Training and testing is alternated in each period. For example, in the first historical month of the data, the model is fitted to the factor exposures and monthly excess monthly returns over the next period. To avoid look-ahead bias, all factors in each training period are normalized using only the training data, i.e. the resulting mean and standard deviation of each factor across all stocks is 0 and 1 respectively. The same normalization parameters are then used to rescale the test set. This avoids introducing a bias into the test set while also avoiding incorporating knowledge of the test data when rescaling the training data. Of course, the test set is not perfectly normalized.

Hyper-parameter tuning:

Cross-validation is performed using this cross-sectional training data, with approximately 1000 symbols. Once the model is fitted and tuned, we then apply the model to the factor exposures in the next period, t+1, to predict the excess monthly returns over [t+1, t+2]. The process is repeated over all periods. Note, for computational reasons, we can avoid cross-validation over every period and instead stride the cross-validation, every other say 10 periods, relying on the optimal hyper-parameters from the last cross-validation periods for all subsequent intermediate periods. In practice we find that performing cross-validation in the first period only is adequate with the exception of the number of latent risk factors, .

Three fold cross-validation over hidden units per layer, and hidden layers is performed in the same time period. We find that the optimal architecture has two hidden layers, 100 units per layer, no regularization, and softplus (i.e. smooth ReLU) activation. For an interpretable model, continuous activation functions are required to provide sufficient smoothness (with 50 hidden units per layer being optimal).

All experiments are performed using Tensorflow (Abadi et al., 2016) to implement the deep feed-forward network and the pls R package (Liland

et al., 2021) for PLS. The LASSO model is implemented using the glmnet R package (Simon

et al., 2011). The amount of regularization in the LASSO model is tuned every period777The LASSO model uses cross-validation to optimize the regularization parameter and iterative fitting, with 50 alphas, along the regularization path.. The PCA results are generated using the asymptotic PCA method implemented in the covFactorModel R package888https://rdrr.io/github/dppalomar/covFactorModel.

4.1 Russell 1000 stocks

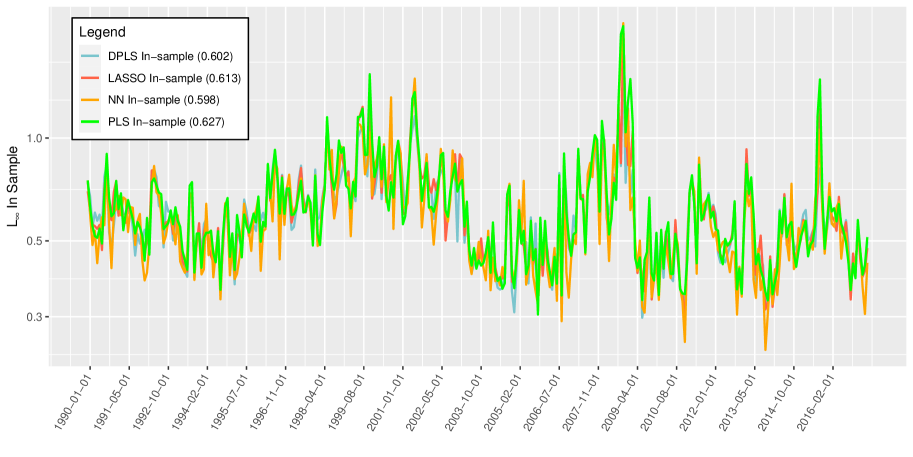

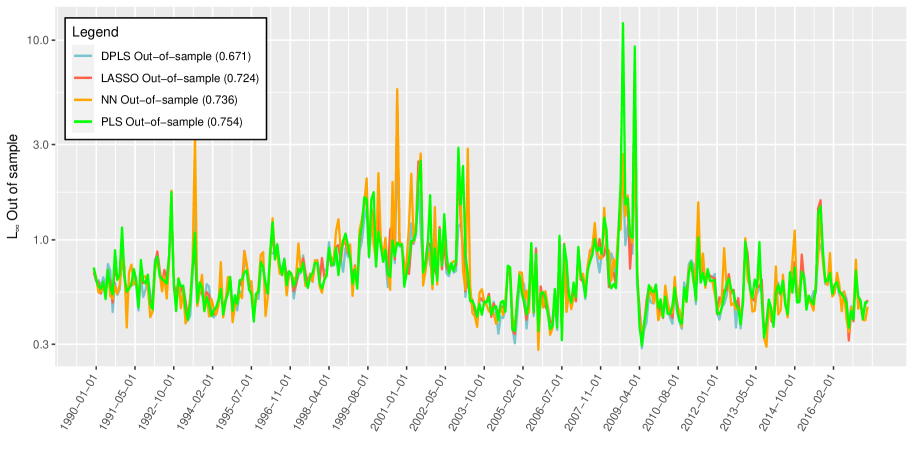

We begin by analyzing the predicted excess assets returns of the models over all constituents of the Russell 1000 index in each period999Note, for avoidance of doubt, that we do not construct index tracking portfolios – all stocks in the index are equally weighted in our analysis., with the goal of identifying the ability of DPLS to capture outliers in the excess stock returns. Figure 5 compares the in-sample and out-of-sample performance of DPLS, PLS, deep feedforward network (NN), and LASSO regression using the norm of stock return errors over the coverage universe of stocks listed in the Russell 1000 index at each monthly period. This norm measures the largest absolute error across all assets, i.e. the error associated with the most mis-predicted excess asset return in each period. The time averaged norms, over all periods, is shown in parentheses.

We observe the ability of DPLS to best capture outliers, with the norm of the error in the NN and DPLS regression respectively being on average between 8% and 12% smaller than the other methods out-of-sample. We also observe that the amount of variance between the in-sample and out-of-sample performance is most notable using NN regression. This is consistency with the high degree of parameters exhibited by the full neural network architecture relative to the training data size. This, in fact, highlights a substantial defect of using deep learning for period-by-period cross-sectional regression — the amount of training data required for deep learning required isn’t compatible with factor modeling cross-sectional datasets. On the other hand, if one simply trains across all stocks and all periods, then the model loses its dynamic nature.

We also observe periods in the out-of-sample test set where PLS exhibits the largest errors and DPLS appears to capture these. The combination of a lower time averaged error and fewer apparent outliers not captured by the PLS, provides evidence of the superiority of DPLS over PLS in capturing outliers.

(a) in-sample error

(b) out-of-sample error

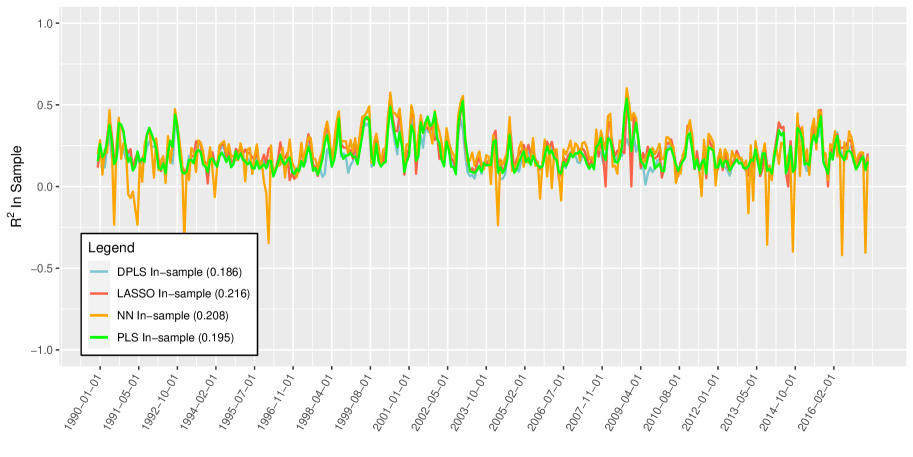

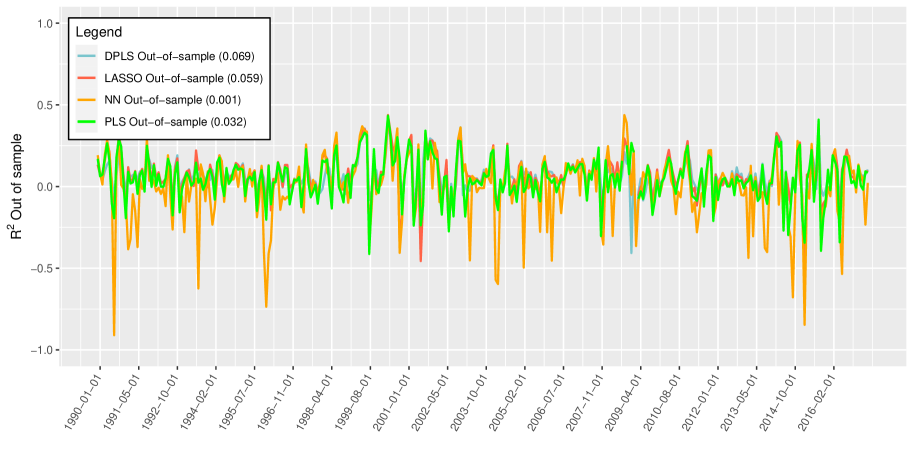

Figure 6 compares the in-sample and out-of-sample performance of DPLS, NN, and LASSO regression using the of monthly asset returns. The time averaged over all periods is shown in parentheses. Overall, we observe that DPLS regression exhibits the best out-of-sample performance. We also find further evidence that the NN is over-fitting, on account of the low out-of-sample .

(a) In sample

(b) Out-of-sample

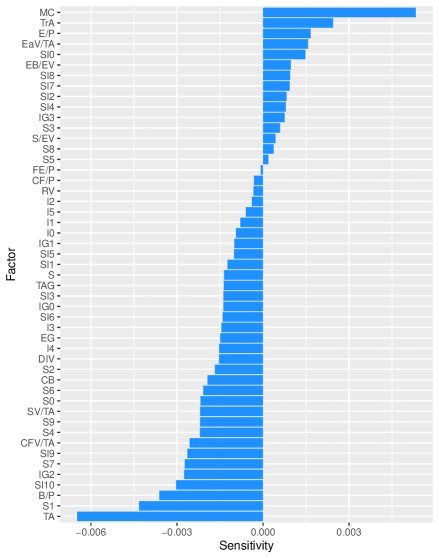

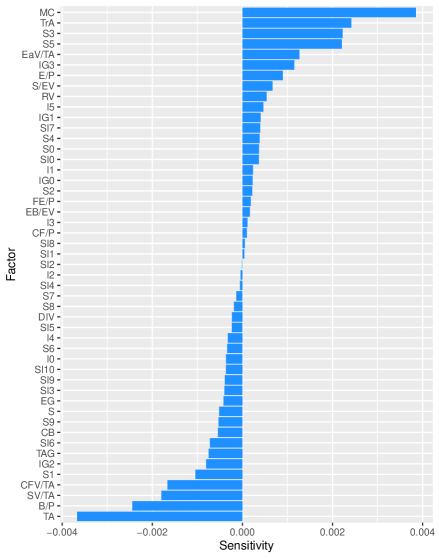

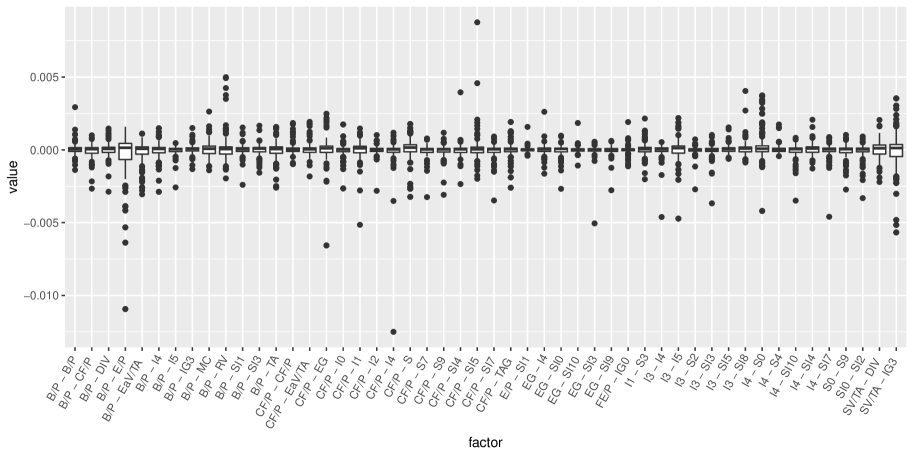

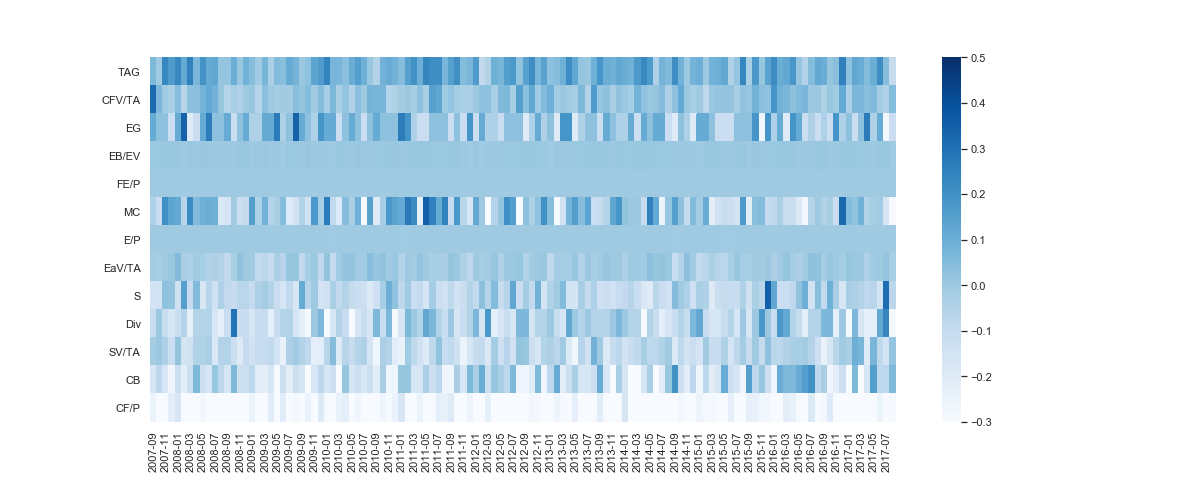

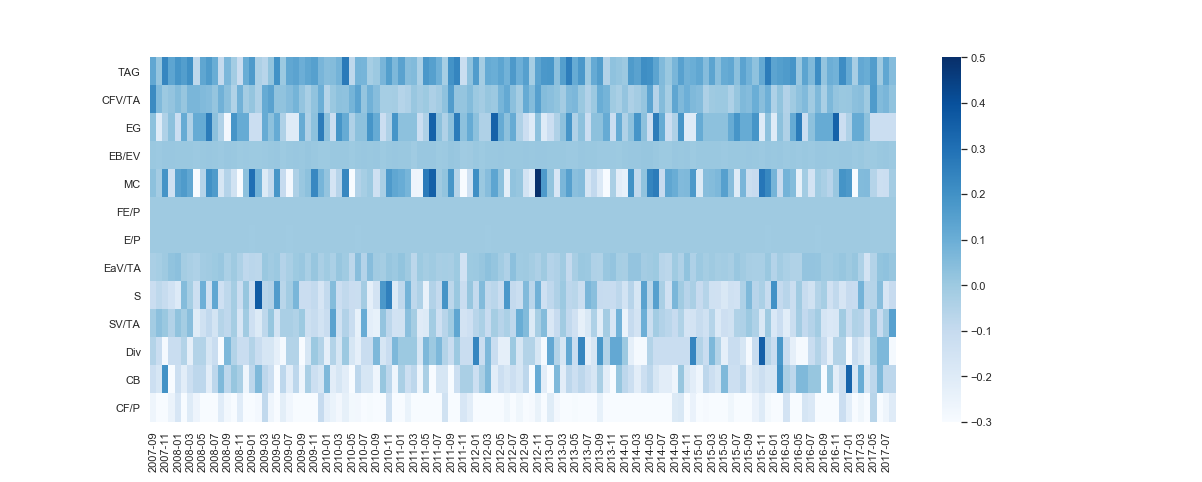

Figure 7 compares the time averaged factor model sensitivities, evaluated at , over the thirty year period using (a) full NN and (b) DPLS regression. For each method, the sensitivities are each sorted in descending order from top to bottom by their mean value over all periods. See Table 3 in Appendix A for a description of the factors.

|

|

| (a) NN | (b) DPLS |

All three methods share important consistencies. For example, Market Cap (MC), Trading Activity (TrA), and Earnings Volatility to Total Assets (EaV/TA) rank highly as positive factors. Conversely, Total Assets (TA), Book-to-Price (B/P), and Cash flow Volatility to Total Assets (CFV/TA) rank highly as negative factors. Both models also agree that expected returns are, on average, largely independent of Cash Flow to Price (CF/P).

However, there are also significant discrepancies between the methods. For example EBIDTA to Earnings Volatility (EB/EV) ranks highly as a positive factor in the NN model model, yet is weakly positive in the DPLS model. As another example, Total Assets Growth (TAG) is ranked as one of the most negative factors in the DPLS model, yet the NN model places it as weakly negative. The NN model is observed to exhibit sensitivities which are up to approximately 50% larger than in the DPLS model, suggesting that the higher degree of parameterization leads to factor over-sensitivity. The NN sensitivities are also, on average, skewed negative. Another apparent difference is the effect of dimension reduction in the DPLS model – there are many more non-zero fundamental factors in the NN model, whereas the mid-section of the DPLS plot is comparatively thin, indicating fewer material factors on average.

(a) Temporal distribution of NN factor sensitivities

(a) Temporal distribution of DPLS factor sensitivities

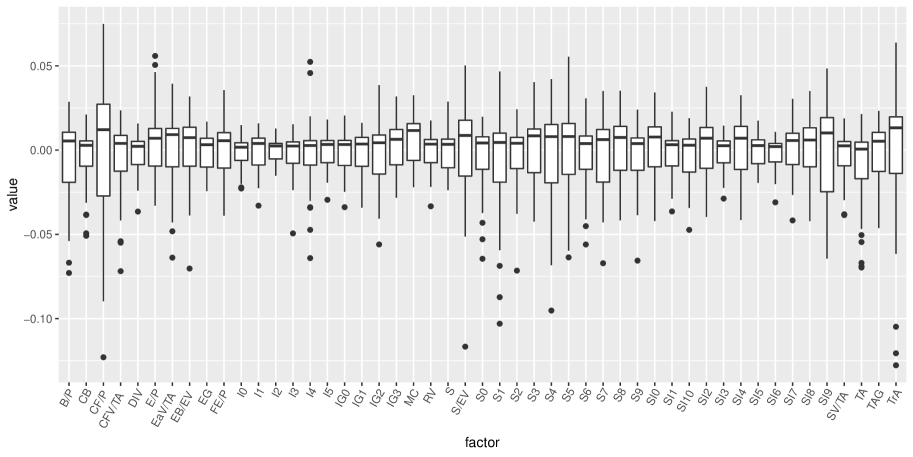

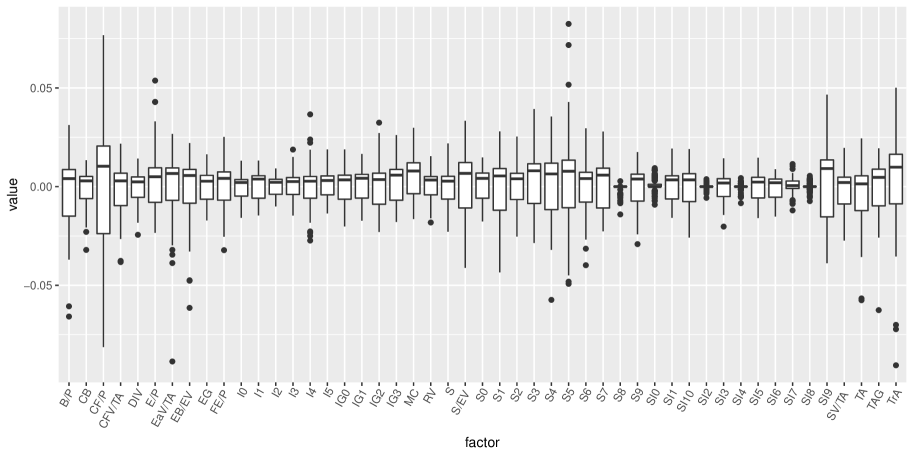

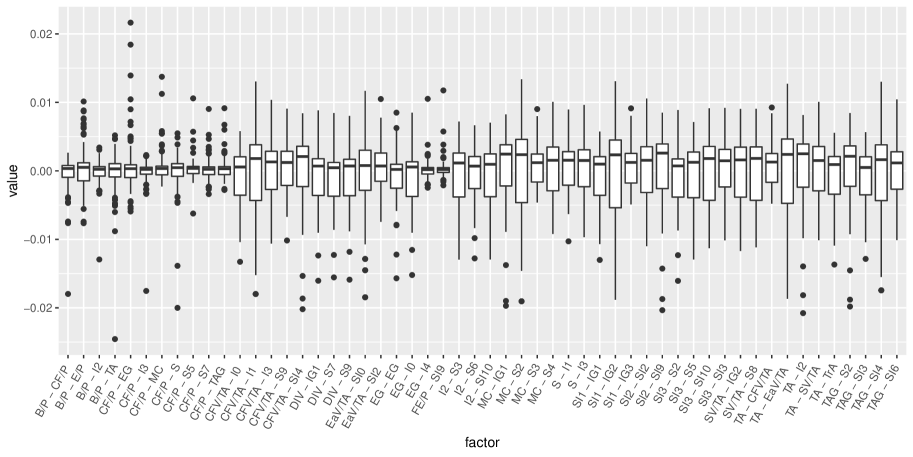

The time averages provide a limited view on the model sensitivities. We additionally plot the temporal distribution of the factor sensitivites. We observe that Cash flow to Price and sub-industry group 9 carry the most uncertainty - the inter-quartile range is the largest in both models. DPLS also collapses a number of the sector and sub-industry group variables closely around zero.

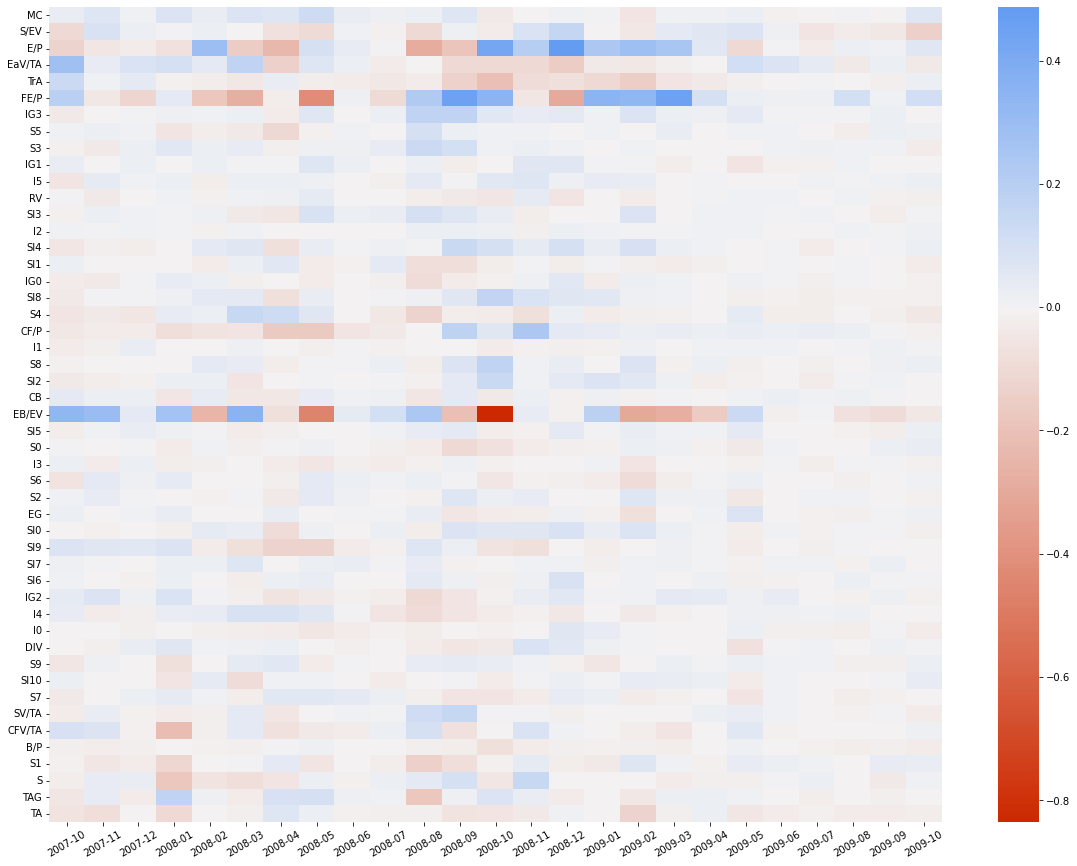

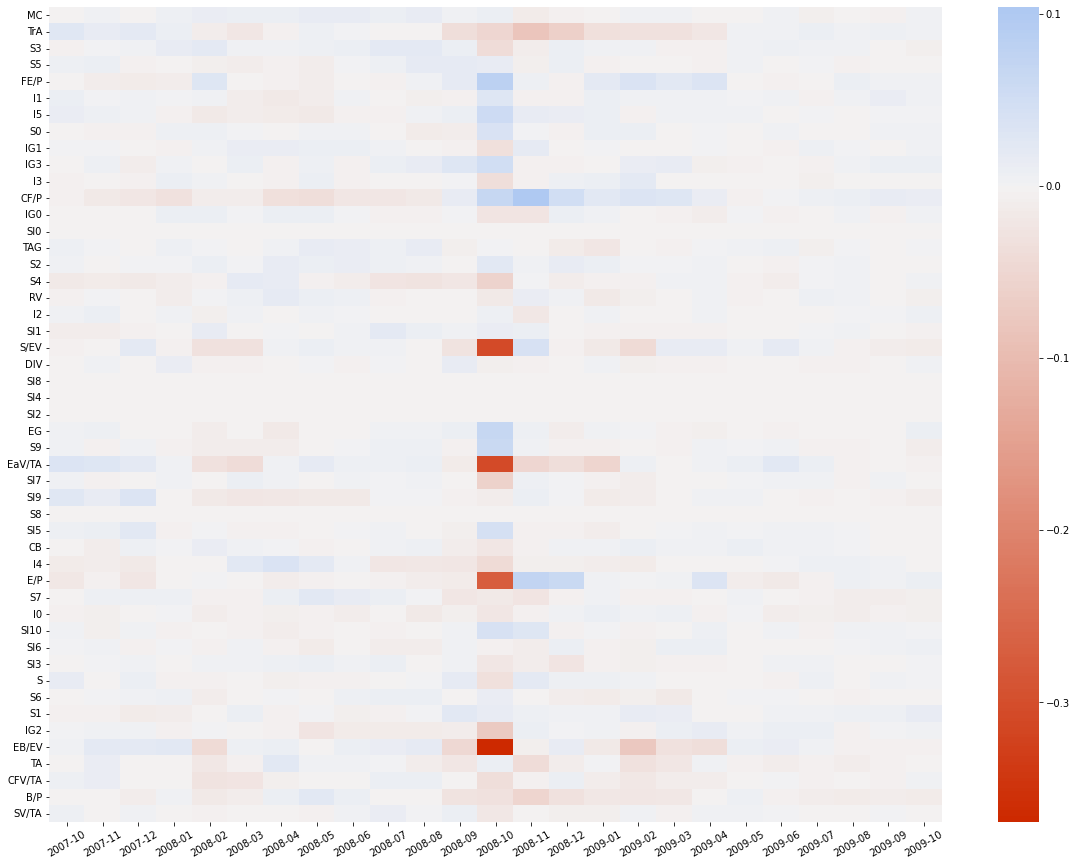

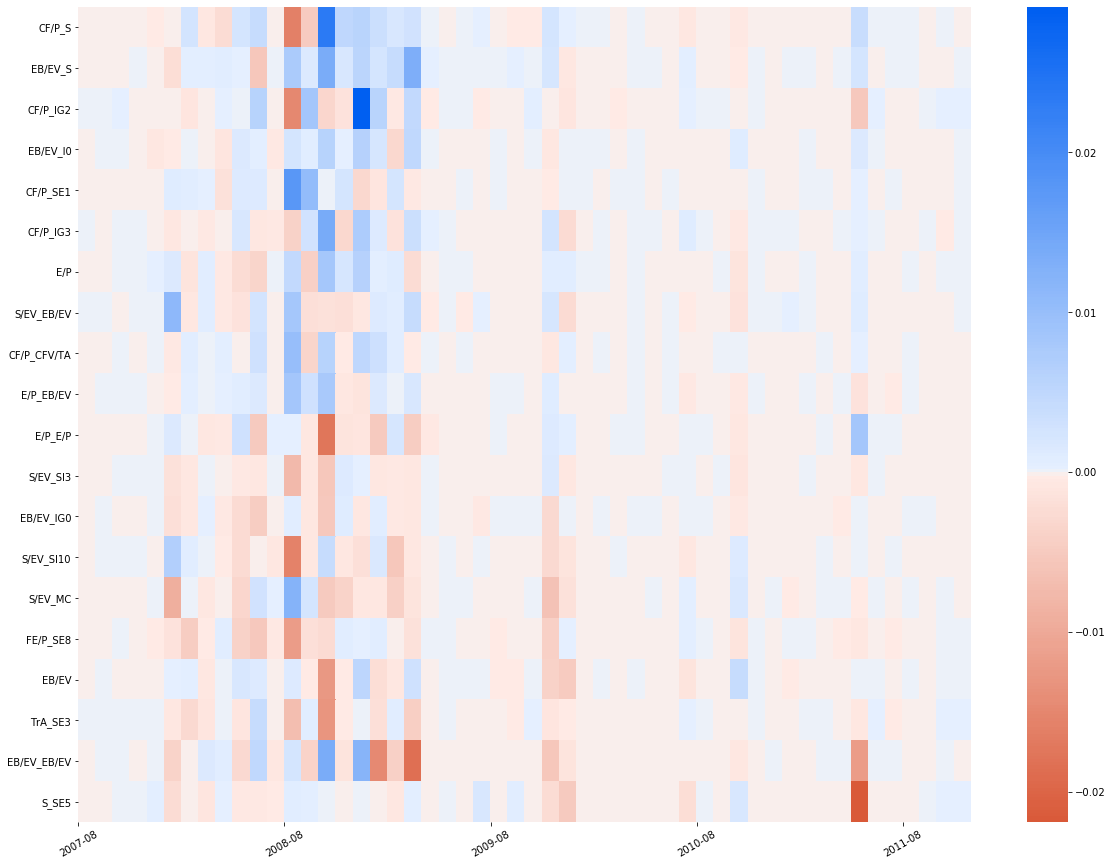

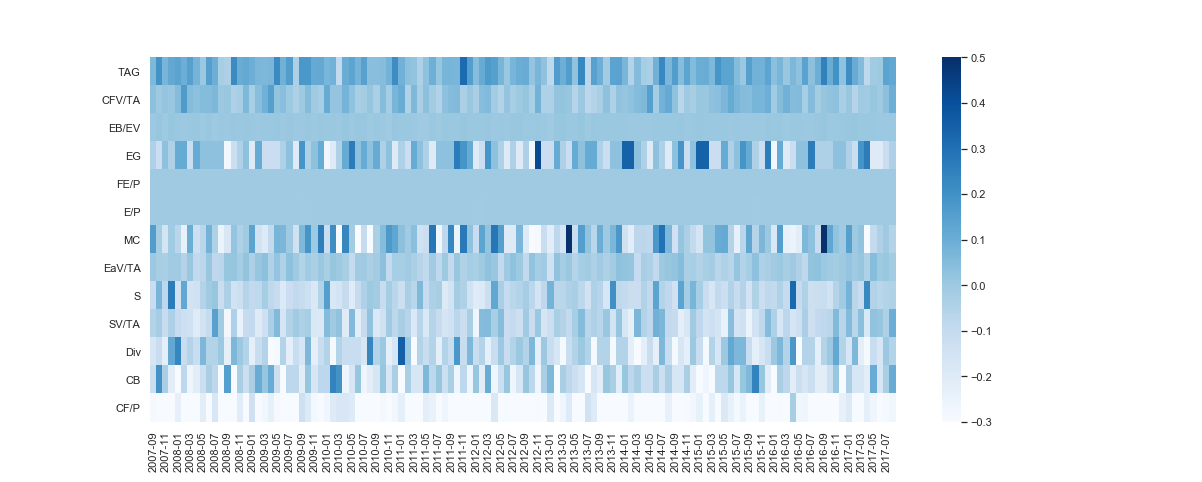

We can also study the extent to which the most dominant factors persist over multiple periods. Figure 9 compares the sensitivity of the predicted excess asset returns to the fundamental factors over the two year period between October 2007 and October 2009, covering the Lehman Brothers financial crash. We find consistency between the factor sensitivities and the September/October 2008 Lehman collapse period. In particular, DPLS is able to identify a number of prominent factors with large positive sensitivities in this period. In contrast, the NN model only identify one strongly positive sensitivity. We also see more variability from period to period in the NN model, whereas the DPLS exhibits more observations where the factor dominance persists over multiple periods.

|

|

| (a) NN | (b) DPLS |

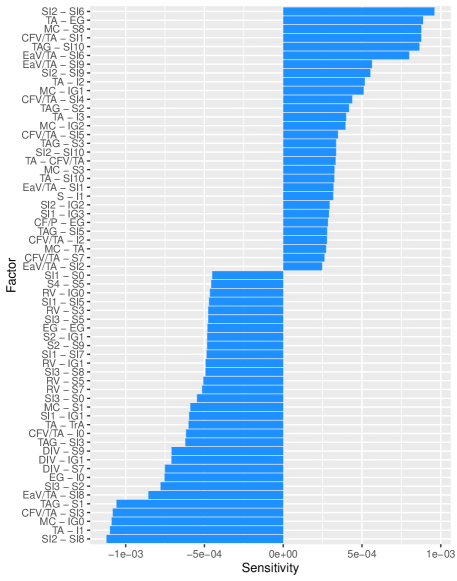

Further insight can be gained by analyzing the interaction effects and quadratic terms in the NN and DPLS models, as shown in Figure 10. These interaction terms are time averaged over the thirty year period using (a) NN and (b) DPLS regression applied to all stocks in the Russell 1000 index. denote pairwise interaction effects between factors XX and factors YY.

In contrast to the sensitivities, the most important interaction terms are different across each model. A common pattern is for a model to find a fundamental ratio across multiple sectors and industry groups. For example, the DPLS model finds the quadratic Book-to-Price ratio positively dominant, but also finds Book-to-Price across SubIndustry 5 in addition to Industry Groups 0 and 3. The DPLS model also finds Cashflow/Price strongly negatively dominant across Industry 4, SubIndustry 7, and Sectors 7 and 9. The NN model finds Earnings Volatility/Total Assets (EaV/TA), Cash Flow Volatility/Total Assets (CFV/TA), Total Asset Growth (TAG), Total assets (TA), and Market Cap (MC) positively dominant in specific SubIndustries, Sectors, and Industry Groups. Whereas Dividends (DIV) are exclusively associated with negative effects in specific SubIndustries, Sectors, and Industry Groups. We also note that DPLS isolates a few particularly dominant interaction pairs - the interaction of Book-to-Price and Earnings-to-Price is a strong negative effect and the Industry 4-Sector 0 pair is strongly positive.

The top interaction effects in the NN model are also an order of magnitude larger than in the DPLS model, suggesting that the higher degree of parameterization renders the NN interaction effects as over-sensitive.

|

|

| (a) NN | (b) DPLS |

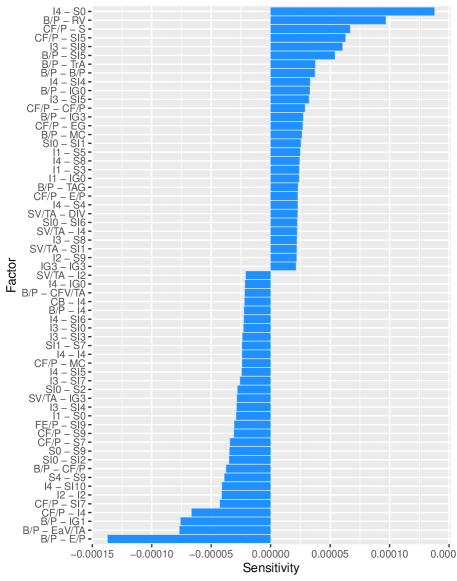

The temporal distribution of interaction effects can shed light on the degree of variability in interaction effects over time. Figure 11 compares the NN and DPLS interaction terms, listed in alphabetic order from left to right. In contrast to the NN model, most of the DPLS interaction effects are tightly distributed with a few notable exceptions - Book-to-PriceEarnings/Price (B/P-E/V), Cash flow to priceIndustry 4 (CF/P-I4) and cash flow to priceSubIndustry 5 (CF/P-SI5).

The NN interaction effects, on the other hand, are much more widely distributed and it more difficult, if not impossible, to draw meaningful conclusions from the time averaged ranking of the interaction effects, given there is so much variability.

(a) Temporal distribution of NN factor interactions

(a) Temporal distribution of DPLS factor interactions

Here we observe much less consistency between the NN and the DPLS model. The top interaction effects in the NN model are also an order of magnitude larger than in the DPLS model, suggesting that the higher degree of parameterization renders the NN interaction effects as over-sensitive.

|

|

| (a) NN | (b) DPLS |

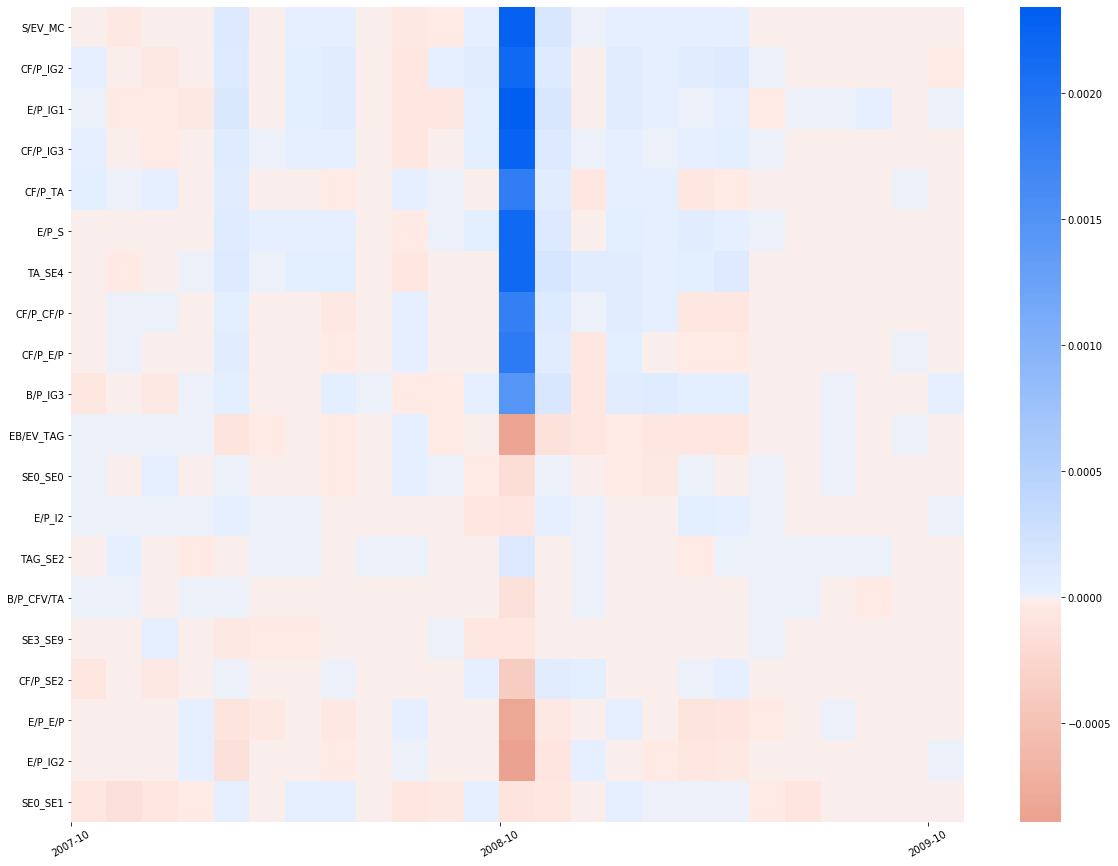

Figure 12 compares the most important interaction and quadratic effects over a multi-year period covering the Lehman Brothers financial crash. The DPLS interaction terms in October of 2008 dominant the other dates and largely govern the overall time averaged ranking. In contrast, the NN exhibits multiple outlier dates and more severe swings between an interaction effect being positive dominant and negative dominant from month to month. For example, in Figure 12(a), the interaction effects in the first and third row swing between dark red and dark blue in a relatively short period of time.

4.2 Portfolio analysis

We now evaluate the utility of the DPLS factor model as a predictive signal for constructing portfolios.

To evaluate the relative portfolio performance under a DPLS factor model versus a PLS, LASSO or NN factor model, we construct an equally weighted, long-only, portfolio of stocks with the highest predicted monthly returns in each period. The portfolio is reconstructed each period, always remaining equal but varying in composition. This is repeated over the 30 year period in the data. We then estimate the information ratios from the mean and volatility of the excess monthly portfolio returns, using the Russell 1000 index as the benchmark.

This exercise is merely to assess the relative merits of DPLS factor models versus other methods as is not intended as an exhaustive study of the implications of using DPLS factor models fro portfolio construction. One important caveat is that the information ratio does not account for trading costs, which could erode performance due to high turnover. Additionally we do not consider more complex constraints such as sector balancing of the managed portfolios.

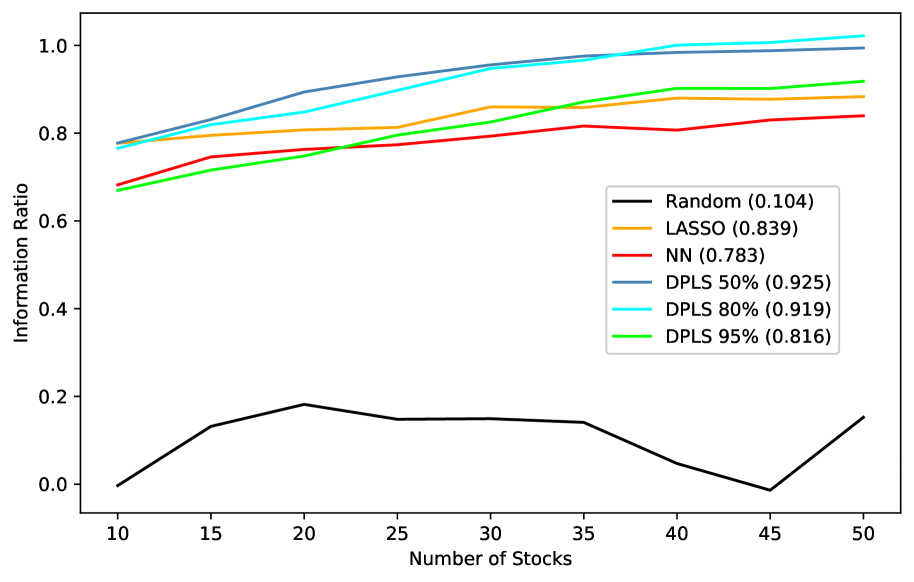

Figure 13 compares the information ratios using DPLS, NN, and LASSO regression to identify the stocks with the highest predicted returns. The information ratios are evaluated for equally weighted portfolios of various sizes. Also shown, for control, are randomly selected portfolios, without the use of a predictive signal. The mean information ratio for each model, across all portfolios, is shown in parentheses. We observe that the information ratio of the portfolio returns, using DPLS regression, is approximately 1.2x greater than NN regression. NN regression, despite exhibiting substantially lower out-of-sample error than LASSO regression results in an inferior information ratio than LASSO, suggesting that stock selection based on more accurate predicted returns does not directly translate to higher information ratios on account of the stock return covariance.

We also observe that the information ratio of the baseline random portfolio is small, but not negligible, suggesting sampling bias and estimation universe modification have a small effect.

Figure 14 shows the time averaged factor tilts of equally weighted portfolios constructed from the predicted top performing 50 stocks, in each monthly period, over all time periods.

Most of the factor tilts are consistent across the models, however, some are not. For example, Market Cap (MC), Total Asset Growth (TAG), and Dividends (Div). LASSO and NN regression overweight the TAG. LASSO also overweights Market Cap. DPLS (95%) and NN regression overweight Dividends. For completeness, the changes in factor tilts over each period are provided in Section D.1.

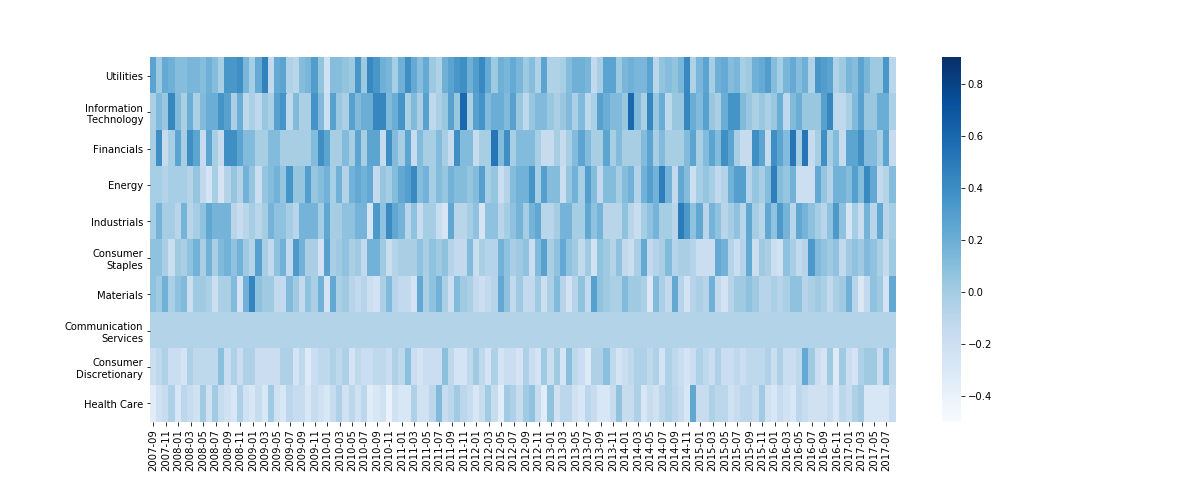

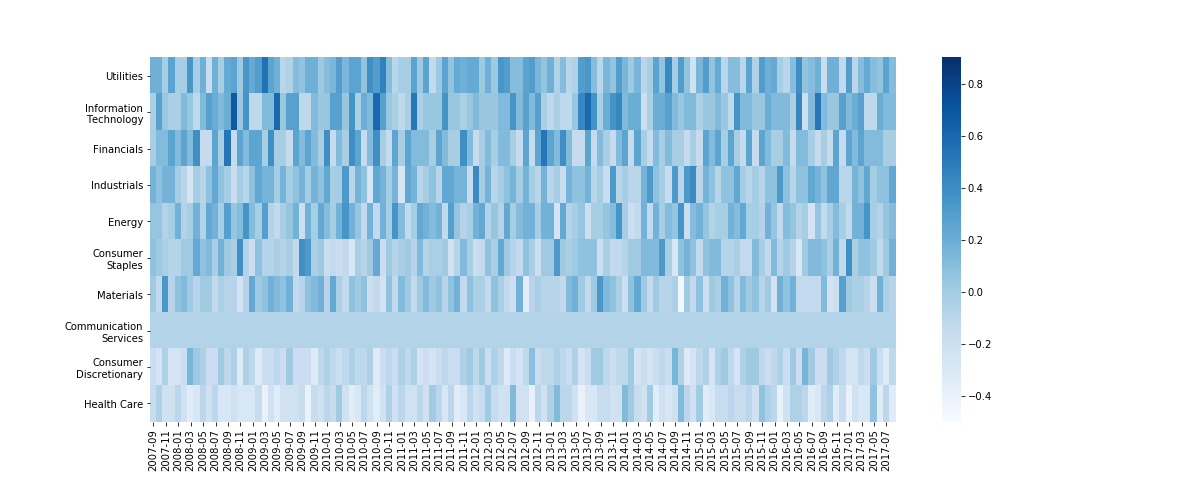

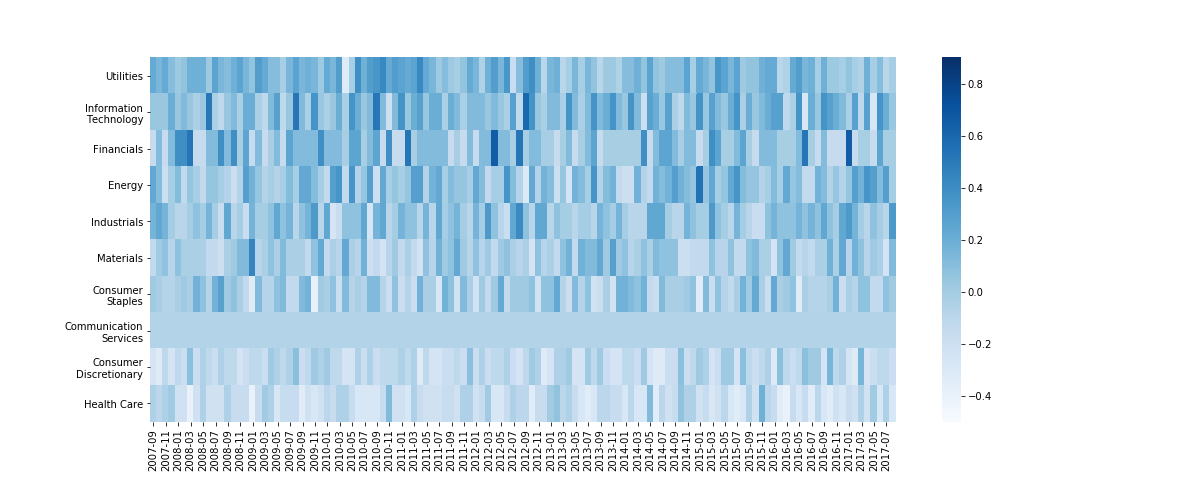

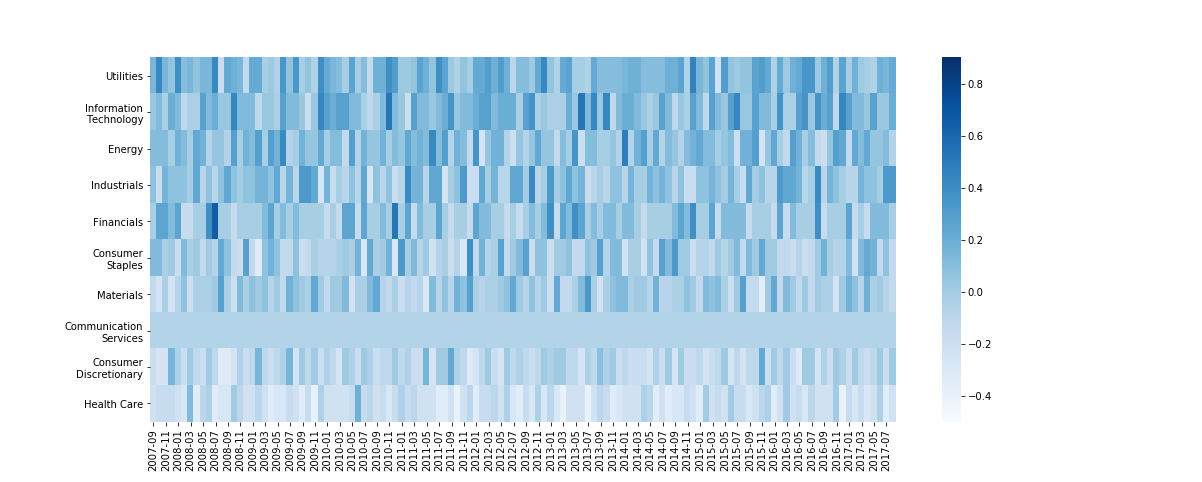

Figure 18 shows the rescaled sector tilts of equally weighted portfolios constructed from the predicted top performing 50 stocks, and then averaged over all periods. The sectors are ranked by their time averaged ratios, but their tilts vary each month due to portfolios turn-over. WN denotes a random equally weighted portfolio.

Utilities and Information Technology are the most dominant sectors, i.e. with the highest time averaged representation. In contrast, Consumer Discretionary and Health Care are the least representative sectors shown. Note that the least representative sector, Real Estate, has been excluded. The sector tilts across DPLS, NN, and LASSO regression are found to generally concur. Notable differences include DPLS (95%) favoring portfolios with a higher Information Technology and Consumer Staples tilt and lower Industrial tilt. For completeness, the changes in sector tilts over each period are provided in Section D.2.

4.3 Risk factor exposures

We estimate the K-factor DPLS model for various using the in-sample total :

and the out-of-sample total :

over all periods. These total measure the extent to which the latent risk factors capture the realized riskiness in the panel of individual stocks either in-sample or out-of-sample respectively. It can be interpreted as the amount of explained variance of the asset returns. If the intercept is set to zero in the DPLS model, each of these represent the model’s ability to describe risk compensation solely through exposure to the latent risk factors. Otherwise, they represent a risk-free compensation and, for each , incremental risk compensation adjustments.

Table 1 compares the performance of three different statistical factor models, both in-sample and out-of-sample, across all stocks in every period . The motivation for showing the in-sample and out-of-sample performance is to assess the bias-variance trade-off. In particular, a drop in performance from in-sample to out-of-sample is indicative of over-fitting whereas poor performance in-sample suggests under fitting. The table also compares the performance of an equally weighted portfolio which is long the top ten performing stocks, as predicted by each model. In that case the sum of collapses as there is just one sum of for the portfolio returns.