Differentially Private Estimation via Statistical Depth

Abstract.

Constructing a differentially private (DP) estimator requires deriving the maximum influence of an observation, which can be difficult in the absence of exogenous bounds on the input data or the estimator, especially in high dimensional settings. This paper shows that standard notions of statistical depth, i.e., halfspace depth and regression depth, are particularly advantageous in this regard, both in the sense that the maximum influence of a single observation is easy to analyze and that this value is typically low. This is used to motivate new approximate DP location and regression estimators using the maximizers of these two notions of statistical depth. A more computationally efficient variant of the approximate DP regression estimator is also provided. Also, to avoid requiring that users specify a priori bounds on the estimates and/or the observations, variants of these DP mechanisms are described that satisfy random differential privacy (RDP), which is a relaxation of differential privacy provided by Hall, Wasserman, and Rinaldo (2013). We also provide simulations of the two DP regression methods proposed here. The proposed estimators appear to perform favorably relative to the existing DP regression methods we consider in these simulations when either the sample size is at least 100-200 or the privacy-loss budget is sufficiently high.

| Ryan Cumings-Menon |

| U.S. Census Bureau |

1. Introduction

Since Dwork et al., 2006b first introduced the concept of differential privacy (DP), it has become the gold standard notion of privacy in the statistical disclosure limitation literature, both because of the strong privacy guarantees that DP mechanisms provide and the theoretical properties that make the formulation of many DP mechanisms straightforward, which are described in more detail in the next section. However, DP linear regression methods provide a few interesting theoretical issues related to the lack of exogenous bounds on the regression estimates and/or observations in typical use cases. At the same time, since linear regressions are a ubiquitous tool in applied statistics, there are compelling use cases for linear regressions using sensitive data on respondents in small samples. For example, Chetty et al., (2018) use data from the US Census Bureau and the Internal Revenue Service to estimate socioeconomic mobility of populations within each Census tract based on ordinary least squares regression (OLS) estimates.

This paper explores the use of two notions of statistical depth to formulate approximate DP mechanisms for estimators of location and linear regression coefficients. Specifically, we formulate approximate DP estimators for the Tukey median, which is a multivariate generalization of the median and is defined as the maximizer of halfspace depth, and for the deepest regression, which is defined as the maximizer of regression depth and is an estimator of the median of the dependent variable conditional on the covariates (Tukey,, 1975; Rousseeuw and Hubert,, 1999). One break we make from the norm in the DP literature is that the mechanisms proposed here do not require bounds on the observations in the dataset, but instead require bounds on the space of feasible estimates. In the case of measures of central tendency like the Tukey median, this alternative is a strict relaxation of the requirement of specifying a bounded set containing the observations, since a bounded set containing the observations also contains all reasonable estimators of central tendency, but the converse is not true in the generic case.

We also provide variants of these methods that satisfy random differential privacy (RDP), which is a relaxation of differential privacy provided by Hall et al., (2013). This definition of privacy protects against accurate inferences on individual observations of samples that are sufficiently likely to be drawn from the same population distribution, without attempting to limit inferences on the population distribution itself. The RDP variants of these estimators have the advantage of not requiring bounds on the estimates or the observations. Using bounds on the estimates themselves in our proposed DP mechanisms is also required for our derivations of the proposed RDP mechanisms, since the RDP mechanisms simply call our proposed approximate DP methods after using the dataset itself to define the feasible sets by nonparametric confidence regions for the estimators. Also, unlike the motivating example provided by Hall et al., (2013), for many input datasets, all of the proposed RDP mechanisms provided in this paper are invariant to a privacy attacker’s prior information set, in the sense that, for any such information set, these mechanisms do not reveal any respondent’s data with certainty for a wide class of input datasets. The final mechanism we introduce is an approximate DP Medsweep mechanism, which is an approximation of the deepest regression provided by Rousseeuw and Struyf, (1998) that is more computational efficient, particularly in the multivariate setting.

After introducing these estimators, we provide simulations to compare these methods to existing DP regression techniques. One advantageous feature of the DP estimators proposed here is that their statistical performance is typically less dependent on the input bounds for larger sample sizes than existing approaches, which we explore further in these simulations. Specifically, our implementation choices related to bounds on observations and the estimator are intended to err on the side of understating the relative accuracy of the proposed DP regression estimators. The estimators proposed here appear to perform favorably relative to the other DP regression methods considered when either the sample size is larger than approximately 100 and/or is sufficiently high. We also use these simulations to estimate the maximum possible rate at which the diameter of the feasible set of estimates can be increased without having any impact on the distribution of the DP estimators. In these simulations, it appears possible to define this feasible set so that its diameter increases at an exponential rate in the sample size. In contrast, the accuracy of many classical DP location and regression estimators depends strongly on the tightness of bounds on the observations. When these bounds are not provided by the use case at hand, one can estimate them using a preliminary DP mechanism; however, one motivation for the RDP estimators proposed here is that this is not always straightforward. For example, Chen et al., (2016) propose using a preliminary DP mechanism that outputs a bounding box of the form such that the proportion of datapoints in is approximately equal to the user choice parameter but this approach is not ideal when the observations are centered around a point that is far from the origin and/or each dimension of the observations have dissimilar dispersion.111One method to at least partly ameliorate this issue would be to perform multiple iterations of the approach described by Chen et al., (2016). For example, preliminary bounds could be used within a DP mechanism that outputs the approximate the center of the distribution, and new DP bounds could be computed after using this first estimate to recentering the data. This process could be repeated multiple times, at the cost of requiring additional privacy-loss budget in each iteration. Note that this variant suffers from the same issue as the more basic approach; the accuracy of the final DP estimator becomes worse as the population distribution is shifted away from the origin. Also, since the datapoints outside of are removed from the dataset prior to estimation, setting typically requires balancing a tradeoff between bias and dispersion of the final DP estimator.

In part to bound the scope of the paper, all of the estimators proposed below use perturbation methods that result in DP estimators with log-concave distributions conditional on the data. Many alternatives that do not satisfy this property can be formulated with only minor changes to the proposed approaches, so we will point out some of these possibilities throughout the paper. However, this is also an advantageous property for a DP estimator to satisfy for two reasons. First, this condition ensures the likelihood ratio test for the population mean is monotonic, which we expect will make future work on DP inference of the proposed estimators more straightforward. Second, this condition also ensures the moments of the DP estimators exist conditional on the data. This allows for the DP estimators described here to be used with data from respondents in fairly granular geographic regions and then for summary statistics of these estimates, such as the mean or variance of these estimators across the geographic regions, to have a meaningful interpretation as unbiased estimates of their finite population counterparts. For example, in the use case described by Chetty et al., (2018) and using the proposed estimators, one could estimate a measure of the socioeconomic mobility in the US using a weighted mean of the estimates in each Census tract.

After outlining notation in the next subsection, the remainder of the paper is organized as follows. Section 2 outlines the required definitions in the DP and statistical depth literature that we will use throughout the paper, and related work on DP linear regressions. Section 3 provides tighter bounds on a parameter that is used in DP mechanisms that are based on smooth sensitivity (Nissim et al.,, 2007) and that use a Laplace noise distribution, which may be of independent interest to the DP community. Afterward, the proposed DP and RDP Tukey median estimators are described in Section 4.1, and the proposed DP and RDP deepest regression estimators are described in Section 4.2. Simulations are provided in Section 5, and 6 concludes.

1.1. Notation

The mechanisms described here take datasets of observations as input; we will denote the set of all such datasets as For each dataset we will assume throughout that each respondent contributes to at most one observation in which is assumed to be an element of 222We also assume that it makes sense to talk about the data of one respondent in isolation, which, for example, fails to hold for data on the adjacency relationships in social networks. Kifer and Machanavajjhala, (2014) provides more information on how interrelated observations impacts formal privacy guarantees. Unless noted otherwise, we will not assume the observations in the input dataset are drawn from a population distribution. When introducing each of the formally private estimators proposed below, we will denote a candidate set, or feasible set, of estimators as and the non-private estimate as

We will use bold symbols to denote vectors, and also use where to denote the natural logarithm of In addition, let denote the indicator function of the set denote the largest integer less than or equal to denote the smallest integer greater than or equal to denote the order statistic of denote the probability with respect to the random variable denote the convex hull of the set and let denote the sign function. Also, let be defined so that is equal to the number of records that must be added and/or removed from to derive Note that, since substituting one record for another using only these two operations requires adding one record and then removing one record, for any that differ in records, we have We will also use to denote the norm of and to denote the Euclidean norm.

2. Preliminaries

2.1. Differential Privacy

The definition of an DP mechanism was first provided by Dwork et al., 2006b ; Dwork et al., 2006a , as described below. where all randomness is due to the mechanism

Definition 1.

(Dwork et al., 2006b, ; Dwork et al., 2006a, ) Let the neighbors of the dataset be defined as A randomized algorithm satisfies -differential privacy (DP) if and only if, for all neighboring datasets and any measurable set we have

We also follow the norm in the literature and refer to DP mechanisms as pure DP mechanisms, and we say that a given DP mechanism is an approximate DP mechanism when We will also occasionally refer to as the privacy-loss budget. Note that, since we define neighboring databases as the definition above corresponds to bounded DP because the sample size of all neighbors of is fixed at and thus is bounded. The definition of unbounded DP follows from instead defining the neighboring datasets of as We use the bounded DP definition here because some of the mechanisms proposed below do not attempt to protect inferences on the sample size of the input dataset, and the norm in the DP literature is to use the bounded DP definition in these cases.

Wasserman and Zhou, (2010) provide an intuitive interpretation of a DP guarantee; the Neyman-Pearson lemma implies that the requirement of DP is equivalent to bounding the power of any possible hypothesis test for the null hypothesis that a given respondent’s attributes are equal to a given value. Some of the many advantages of this privacy definition include invariance to post-processing, i.e., if satisfies DP then so does for any and sequential composition, i.e., if and both satisfy DP then satisfies DP. For other properties, including other forms of composition, see (Dwork et al., 2006b, ; Dwork and Roth,, 2014).

Designing an DP mechanism for a given function often requires a bound on its global sensitivity, which is described in the following definition, along with a related definition, which will also be used in the next subsection.

Definition 2.

(Dwork et al., 2006b, ; Nissim et al.,, 2007) The local sensitivity of the function is

The global sensitivity of the function is

The following lemma provides a particularly simple DP mechanism known as the Laplace mechanism. Like all methods defined using global sensitivity, this mechanism requires that the global sensitivity of the function is bounded. For example, this is the case for counting queries (e.g.: a function that releases the total population within a given geographic region). However, this is not typically the case for functions that have an unbounded domain; for example, without a priori bounds on possible incomes, the following mechanism could not be used to release the average income of the residents in a geographic region. One possible way around this issue is to use a DP mechanism to approximate bounds on the observations in the sample, and then use a Laplace mechanism to release the average income of respondents with incomes that are within these bounds (Chen et al.,, 2016). This approach is discussed in more detail in Section 5.

Lemma 1.

(Dwork et al., 2006b, ) Given the function the Laplace mechanism, where for each is DP.

One relaxation of DP is random differential privacy, which is defined below. This privacy definition limits inferences between neighboring datasets that are sufficiently likely to consist of draws from the same population distribution, rather than attempting to limit inferences between all pairs of neighboring datasets. Note that this definition does not assume that the data curator knows the population distribution is in a particular class of distributions.

Definition 3.

(Hall et al.,, 2013) A randomized algorithm satisfies -random differential privacy (RDP) if, for all neighboring datasets composed of observations drawn from the same population distribution and any measurable set we have

2.2. Smooth Sensitivity

Nissim et al., (2007) provide a method to decrease the sensitivity value used within a DP mechanism such as the Laplace mechanism for functions that have high global sensitivity but most often have low local sensitivity. A common example of one such function is the univariate median of values in a sample within a bounded interval, i.e., while it is possible to have a local sensitivity equal to the length of this interval, which is thus also equal to the global sensitivity, changing one record typically changes the median by a much smaller amount.

Definition 4.

(Nissim et al.,, 2007) Let the local sensitivity at distance of be defined as the max local sensitivity of over all datasets in in other words, the local sensitivity at distance is defined as

The smooth sensitivity of is defined as

| (1) |

and we will refer to where is an upper bound on as a smooth upper bound on the local sensitivity.

The following Lemma provides one way of deriving a smooth upper bound on the local sensitivity of a function, which we make use of below.

Lemma 2.

(Nissim et al.,, 2007) Let be defined so that (1) for all and (2) for all neighbors and all Then is a smooth upper bound on the local sensitivity.

As an example, the lemma above implies that one smooth upper bound on the local sensitivity of the function can be derived by first defining the upper bound on the local sensitivity at distance as

where and then defining the final smooth upper bound as

The following lemma provides an example of a mechanism that uses a smooth upper bound on local sensitivity.

Lemma 3.

(Nissim et al.,, 2007) Suppose and Also, if let and, if let

Then, for the mechanism that outputs where for each and is the smooth sensitivity of at satisfies DP.

2.3. Halfspace Depth

Tukey, (1975) introduced the concept of halfspace depth, which can be viewed as a multivariate generalization of rank. The halfspace depth of is the minimum number of datapoints in a halfspace with a boundary passing through which is also defined below.

Definition 5.

(Tukey,, 1975; Small,, 1990) Given a dataset consisting of observations the halfspace depth of is defined as

This measure of depth has many advantageous properties, including that it is affine equivariant, which means that, for any with full rank and we have (Donoho and Gasko,, 1992). Also, we will make use of the following property on each halfspace-depth contour of or the subset of with half-space depth at least a given value.

Proof.

This follows from the fact that see for example, (Donoho and Gasko,, 1992). ∎

Maximizing provides a measure of central tendency of a dataset that is known as the Tukey median, which is a multivariate generalization of the median. As described in the definition below, the maximizer of the halfspace depth is not generally unique, so, in cases in which this maximizer is not uniquely defined, we will define the Tukey median using a choice rule that outputs a unique element of The results in this paper only require that this choice rule outputs a point in the convex hull of data points with maximum halfspace depth, which is satisfied by any reasonable rule; one common approach in practice is to simply define the Tukey median as the arithmetic mean of the data points with maximum halfspace depth.

Definition 6.

(Tukey,, 1975) The Tukey median is defined by

where is any choice rule that selects a point from the convex hull of its input points.

To describe a few advantageous properties of the Tukey median, some additional notation will be helpful. First, we will say that a dataset consists of observations in general position if there does not exist a dimensional hyperplane that contains more than observations. Note that, when this condition does not hold, it can be ensured with probability one by dithering the dataset, i.e., adding continuously distributed mean zero noise with a low scale to each observation; this will be discussed in more detail in Section 4.1. Second, the breakdown value of an estimator is defined as the smallest possible proportion of points that must be contaminated in order to make the estimator equal to an arbitrary value, as defined below more formally.

Definition 7.

(Donoho and Gasko,, 1992) The breakdown value of the estimator is defined as

One advantageous property of the Tukey median is that it is a robust estimator. For example, for datasets with observations in general position, its breakdown value is at least and one related property that we will use below is that, for any such dataset, the maximum halfspace depth is at least (Masse,, 2002; Donoho and Gasko,, 1992). The Tukey median is also consistent at the usual parametric rate of when is composed of independent observations from a population distribution. Detail on computational considerations will also be provided in the Section 2.5, after outlining regression depth in the next section.

2.4. Regression Depth

Some notation will be helpful before describing regression depth and its maximizer, the deepest regression hyperplane, which were both first proposed by Rousseeuw and Hubert, (1999). In this section, and all sections related to the DP deepest regression estimator below, we will suppose the dataset is composed of observations We also only consider regressions with an intercept throughout the paper; in other words, we suppose that each vector corresponds to the candidate fit

Before providing the general definition of regression depth, we will start by considering the case of a simple linear regression, i.e., In this case, for any fixed value the regression depth can be defined using the integers

which correspond to the number of data points either above or below the graph of the fit and either to the left or the right of Note that rotating the graph of the fit clockwise around the point to a vertical line would intersect observations, whereas rotating this graph counterclockwise intersects observations. Thus, the regression depth in this two dimensional case is given by

Regression depth can be defined in an analogous way in higher dimensional cases by replacing with a hyperplane in space (Rousseeuw and Hubert,, 1999). We will use the definition below in this paper instead, which appears to have been first described by (Mizera,, 2002).

Definition 8.

(Rousseeuw and Hubert,, 1999; Mizera,, 2002) Given a dataset consisting of observations with the regression depth of is defined as

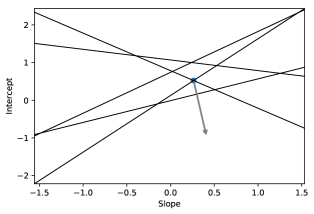

This definition can be derived by considering the regression depth in the dual space. We will briefly outline this and a few related concepts, in part because the local sensitivity of the deepest regression has a straightforward geometric interpretation in the dual space. More detail on the dual space in the context of regression depth can be found in (van Kreveld et al.,, 2008; Rousseeuw and Hubert,, 1999); for interesting historical connections to related regressions, see (Koenker,, 2000). We will use the example in Figure 1 to introduce these concepts. The left plot in Figure 1 depicts a set of five data points in space, or the primal space. Each of these primal points can alternatively be encoded as lines in dual space using the mapping or the set of all fits that pass through the data point in the primal space. The right plot in Figure 1 provides the dual lines corresponding to each of the primal points. Likewise, each point in the dual space corresponds to a single regression line in primal space using the mapping

The act of rotating the graph of a fit to a vertical hyperplane in primal space corresponds to simply moving the point in dual space corresponding to this fit along a ray. For example, in Figure 1, we can see that the regression line on the left plot has a regression depth of three in two ways. First, we can count the minimum number of data points this line must intersect when rotated to a vertical line. In this case rotating this regression line counterclockwise to a vertical line around the intersection point of this line with the right hand side of the plot results in the line crossing three points in total. Second, we can alternatively count the minimum number of observation lines that a ray in dual space, originating from this regression coefficient’s location, i.e., the blue point in the plot on the right side Figure 1, must cross. The gray ray in Figure 1 is one such example; since this ray crosses three observation lines, including the two lines at the origin of the ray, the regression depth of this fit is three.

To derive definition 8, note that the observation line intersects the ray that originates from and points in the direction if and only if there exists such that

After taking the limit as we have

which implies Definition 8.

Like halfspace depth, one advantageous property of regression depth is that it is affine equivariant. Also, below we will make use of the following property of regression depth contours, which are sets in dual space given by

Proof.

This follows from the fact that (Rousseeuw and Hubert,, 1999). ∎

One can also consider all other candidate fits to see that the fit in Figure 1 is the fit with the highest regression depth, or the deepest regression, which is defined below. Like the Tukey median, the maximizer of regression depth need not be unique, so the definition below also uses a choice rule to ensure the deepest regression estimator is defined uniquely. Also like the Tukey median, our results only require that this choice rule outputs a final estimate in the convex hull of with maximum regression depth. One common approach, and the approach we use in the simulations below, is to define this choice function so that it outputs the arithmetic mean of observation line intersections in dual space that have maximum regression depth.

Definition 9.

(Rousseeuw and Hubert,, 1999) The deepest regression is defined as

where is any choice rule that outputs a point in the convex hull of its input.

One advantageous property of this estimator is that it is robust, with a breakdown value of at least (Mizera,, 2002). In addition, the deepest regression obtains this high breakdown value without sacrificing the usual parametric rate of consistency of to the conditional median of given for more detail, see (Bai and He,, 2008; He and Portnoy,, 1998). Note that a similar consistency result also holds for the least absolute deviation (LAD) regression (Koenker and Bassett Jr,, 1978), but the deepest regression has the advantage over the LAD regression of being robust to outliers in the independent variables, Also, one property that we will use below is that the regression depth of the deepest regression is at least which, unlike the similar result described above for the halfspace depth of the Tukey median, has been shown to hold for datasets that are not in general position (Mizera,, 2002; Amenta et al.,, 2000).

2.5. Statistical Depth: Computational Considerations

In this subsection we will describe algorithms for computing halfspace and regression depth and their maximizers when where Both of the notions of statistical depth can be computed at a candidate estimate in time, and faster approximations for these methods are also available (Langerman and Steiger,, 2000; Rousseeuw and Struyf,, 1998).

In the case of the Tukey median, simply computing the halfspace depth at each datapoint provides an algorithm for computing the Tukey median in time. Faster approaches are also available when (Miller et al.,, 2001; Langerman and Steiger, 2003b, ). Struyf and Rousseeuw, (2000) also provide an approximation method for the Tukey median when the sample size and/or the dimension is prohibitively large.

In the case of regression depth, there are candidate fits that pass through data points to consider, so the naïve approach of computing the regression depth for each of these fits has a time complexity of and is most often prohibitively computationally expensive when Langerman and Steiger, 2003a provide a method for approximating the deepest regression that runs in time when Van Aelst et al., (2002) provide a method for approximating to the deepest regression in use cases in which the sample size and/or the dimension is higher.

We emphasize that the first four differentially private mechanisms provided below actually require more than the maximizer of a notion of statistical depth; in order to also compute a smooth upper bound on the local sensitivity of the estimator, these mechanisms also require upper bounds on diameters of the depth contours defined in Lemma 4 and Lemma 5.

Computationally efficient methods to compute upper bounds on these values are left as a topic for future research. For the purposes of these first four differentially private methods in this paper we simply use the two naïve approaches in order to explicitly find these diameters. Since this implies that the deepest regression mechanisms provided below are primarily applicable when Section 4.2.1 provides a mechanism for the more computationally efficient approximation of the deepest regression provided by Van Aelst et al., (2002).

2.6. Related Literature

This section mainly focuses on providing some pointers into the DP literature for linear regression and Tukey median estimators. The only paper that we are of that provides a DP Tukey median estimator is Ramsay and Chenouri, (2021), which uses a formulation based on an exponential mechanism rather than on the smooth sensitivity of the Tukey median, as is done below. One such class of DP estimators are those that pass sufficient statistics of a linear regression through a DP primitive mechanism; see for example, (Foulds et al.,, 2016; McSherry and Mironov,, 2009; Vu and Slavkovic,, 2009; Wang,, 2018; Dwork et al.,, 2014). A related class of DP estimators include the methods proposed by Dwork and Lei, (2009); Alabi et al., (2020), which are based on the Theil-Sen simple linear regression estimator (Theil,, 1950; Sen,, 1968). Bassily et al., (2014) also propose a DP OLS method that estimates the regression parameters using a DP gradient descent method. One line of work that can be used to formulate a particularly broad class of DP estimators is based on perturbing the objective function of a convex optimization problem (Kifer et al.,, 2012; Awan and Slavković,, 2021). There has also been work on DP inference; see for example, (Barrientos et al.,, 2019; Sheffet,, 2017; Awan and Slavković,, 2021; Karwa and Vadhan,, 2018).

Since some of our results are related to the input requirement for most DP estimators of a priori bounds on the observations, it is worth highlighting a few papers related to this issue. First, as described above, Chen et al., (2016) describe a DP mechanism that can be used to estimate a bounding box of the form that contains a fixed proportion of the datapoints. These bounds can be used as input to subsequent DP mechanisms after removing all observations that are outside of this bounding box from the dataset. More detail on this approach is also given in the next subsection and Section 5. Second, Karwa and Vadhan, (2018) provide DP estimators for the univariate mean of the data without the requirement of input bounds on the observations. While the RDP estimators proposed below also do not require input bounds on the data or the estimator, the RDP estimators proposed below are different from the (pure and approximate) DP estimators proposed by Karwa and Vadhan, (2018) for a few reasons. First, the accuracy of the approach described by Karwa and Vadhan, (2018) is dependent on whether or not the input dataset satisfies their assumption that it is composed of independent draws from a Gaussian distribution; in contrast, the RDP estimators proposed below do not require distributional assumptions on the population distribution. Second, since RDP is a relaxation of the privacy guarantee provided by DP, the privacy guarantee provided by the mechanisms proposed by Karwa and Vadhan, (2018) is stronger than the corresponding guarantee provided by the estimators proposed below. Third, in the case of the RDP estimators proposed below, our avoidance of distributional assumptions requires an assumption on the sample size being above a given threshold, which is not required by the approach described by Karwa and Vadhan, (2018). Later work also generalized this approach to the multidimensional case, while maintaining the normality assumption on the population distribution; see for example, Kamath et al., (2022).

3. Improved Bounds for Smooth Sensitivity

This section provides improved bounds on the maximum value of that can be used in a smooth-sensitivity-based mechanism with noise drawn from a Laplace distribution while still satisfying DP. The corresponding bounds on that are provided by Nissim et al., (2007) in this case, which are also provided in Lemma 3, prioritize tractability over tightness. For example, when and the bound proposed by Nissim et al., (2007) for this case is slightly less than half of the value provided here. The result that provides the improved lower bound on i.e., Theorem 2, follows from the next theorem, which provides three upper bounds on a certain quantile of the sum of exponential random variables, given in (2)-(4). In the simulations provided in Section 5, bound (2) is used to set to the tightest bound we derive here, as described in Theorem 2.

Theorem 1.

Suppose where for each and let be defined as the quantile of If

| (2) | ||||

| (3) | ||||

| (4) |

where is the quantile function of the gamma distribution with shape and rate parameters given by and respectively, and is the secondary branch of the Lambert W function.

Proof.

The equality given in (2) simply follows from the fact that The starting point for both of the two remaining bounds is the following Chernoff bound for which is

After plugging in into the equation above, which is the minimizer of the right hand side over and simplifying, we have

This theorem results from various definitions of that satisfy and thus imply for each such value of

Note that

| (5) |

so we will focus on bounds for this latter inequality. Topsøe, (2004) provides the bound which implies

and thus this implies the second inequality bound in the statement of the theorem. The bound given in (3) is simply the closed form solution of (5) when this inequality holds with equality;

Note that using the secondary branch of the Lambert W function ensures that for all and ∎

The next result describes how Theorem 1 can be used to derive possible values for

Theorem 2.

(Nissim et al.,, 2007) For and the mechanism with output given by where for each satisfies differential privacy if and where is defined so that and is defined as in Theorem 1.

Also, if can alternatively be defined as,

| (6) |

Proof.

In this proof, for any set and let and We will also use two results from the DP literature. First, Nissim et al., (2007) show that for any measurable set and such that we have

| (7) |

Second, Dwork et al., 2006b show that for any measurable set and such that

| (8) |

Suppose are neighbors. The result requires that Starting from the left hand side of this inequality, we have,

where the first inequality follows from (7) because the definition of ensures and the second inequality follows from (8) because and is an upper bound on

The final possible definition for in the case in which requires showing (7) holds for all such that is at most equal to this value of We will also only consider the nontrivial case in which to see that (7) is satisfied when for the value of we derive here, see Nissim et al., (2007).

First, note that is the quantile of the standard Laplace distribution. Let and let denote the event, Since this density is symmetric, so it is sufficient to show for all such that Since this function is maximized over in this range at we will define using

∎

As described previously, in the simulations presented below, we use the tightest bound implied by this result, which is The next two sections will provide the DP mechanisms that make use of the smooth upper bounds on local sensitivity.

4. DP Location and Regression Estimators

The next two subsections will introduce the proposed formally private location and regression estimators, respectively. Specifically, both sections will start by introducing an DP estimator that, as described above, requires the user to input an a priori feasible set for the estimator, and the proposed RDP mechanisms are based on estimating a suitable feasible set.

Our results on the RDP estimators will also provide sufficient conditions for these mechanisms to satisfy information-set-invariant nonrevealing (ISIN). This property ensures that, even for cases in which a privacy attacker knows all but one observation, the mechanism does not reveal any unknown observations with certainty, as defined in more detail below.

Definition 10.

The mechanism is said to satisfy information-set-invariant nonrevealing (ISIN) if for all datasets sets such that privacy attacker information sets unknown records and for all we have

Note that all pure DP mechanisms satisfy this property. In practice, most commonly used approximate DP mechanisms satisfy this property as well, but it is also possible to construct counterexamples that do not. For example, consider the DP mechanism that outputs approximate total populations of each Census block. Suppose the true counts are given by Note that the global sensitivity of this query is so one DP mechanism could be defined using where and defined so that The output of the mechanism can be defined as when and directly otherwise. Since the Laplace distribution is absolutely continuous, whenever this mechanism’s output is a vector of integers, a privacy attacker would know that this output is the vector of true counts with probability one.

Despite the fact that there exists examples of DP mechanisms that do not satisfy ISIN, these mechanisms are often avoided in practice. However, as described above, the original example of an RDP estimator provided by Hall et al., (2013), which was a sparse histogram estimator, did not satisfy ISIN. This is because the input dataset itself was used to estimate the sparsity pattern of the population distribution, and no noise was added to histogram counts that were very likely to be zero. In cases in which a privacy attacker knows the data of all but one respondent and the unknown respondent changes the sparsity pattern of the true histogram, the data of the unknown respondent is revealed with certainty. In contrast, ensuring the RDP estimators proposed here satisfy this property is straightforward because we use the input dataset for a more limited purpose.

4.1. DP Tukey Median Estimators

In this section, we describe both an DP and an RDP Tukey median estimators. Afterward, to take advantage of tighter probability bounds in the univariate case, we also provide a separate RDP median estimator. Note that we provide more detail in the proofs in this section than the next section, which provides the corresponding results for the DP and RDP deepest regression estimators, since the results for both of these estimators follow from identical arguments.

Even though the results on the deepest regression mechanisms follow from the same arguments as the corresponding results for the Tukey median mechanisms, the assumptions are not identical. Specifically, in the case of our proposed DP and RDP Tukey median estimators when we will require the additional assumption that the dataset consists of datapoints in general position. This can be ensured without assuming the input dataset consists of draws from an absolutely continuous population distribution using dithering, as is also described in Section 2.3. Specifically, each can be redefined as where is a mean zero random variable with a distribution that has a low dispersion and is absolutely continuous. Note that the result of using this technique is that we are providing privacy guarantees to the records given by for a given set of realizations of the noise random variable rather than directly to The benefit of this approach is that it allows us to constrain our view of the universe of input datasets to those that are in general position; however, in use cases that require using sequential composition to release the output of several formally private mechanisms, including a formally private Tukey median estimate, ensuring the privacy guarantee provided by each mechanism holds on the same input dataset would require using as the input dataset in all of these mechanisms. For this reason, after the next Lemma we describe how this assumption can be removed entirely using an alternative approach. In some cases, particularly when the a priori bounds on are relatively tight and/or the sample size is sufficiently large, the negative impact of using this alternative on the accuracy of the final DP estimator is likely small or even entirely nonexistant.

Both of the mechanisms provided in this section will use the following smooth upper bound on the local sensitivity of the Tukey median estimator.

Lemma 6.

If is closed and bounded and either or consists of datapoints in general position, then

| (9) |

where

| (12) |

and is a smooth upper bound on the local sensitivity of the Tukey median.

Also, can be found by only considering datapoints in the supremum in the definition of in the sense that

| (13) |

where

| (17) |

and consists of datapoints in and all points at which a depth contour intersect the boundary of

Proof.

First we will consider the impact on the halfspace depth of of removing the observation from There are two possibilities that we will consider, which both follow directly from the definition of halfspace depth, i.e., Definition 5. First, we may have which occurs if and only if there is at least one halfspace in that has on its boundary, contains datapoints, and that does not contain the datapoint Second, in all other cases, removing this observation results in halfspace depth decreasing by one, so we have, in this case. Note that removing a record cannot increase the halfspace depth, since this operation either does not change or decreases the number of datapoints in each halfspace with a boundary that contains Similar logic can be used to show that adding the observation to will either leave the halfspace depth of unchanged or will increase the halfspace depth by one.

Taking the two observations in the preceding paragraph together implies that the operation defined by substituting for results in This same logic can be applied times to show that, for any such that we have Let be a neighbor of be defined as any element of and be defined as any element of Since any neighbor of satisfies we have This implies that one upper bound on the local sensitivity at distance is given by which is the bound defining for cases in which

Next we will derive a tighter upper bound on the local sensitivity at distance for any dataset that satisfies by again considering the operation defined by substituting for in this case. Suppose there exists such that Since, for any removing an observation cannot increase the halfspace depth of and adding an observation cannot decrease the halfspace depth of the event that is only possible if both and However, since and is in general position, we have so the first of these two conditions is not possible (Donoho and Gasko,, 1992). This implies that, for any such that we have must be a subset of Thus, in the context of arbitrary not necessarily satisfying we only need to use the less tight bound on the local sensitivity at distance described in the preceding paragraph when and for any we instead use the tighter bound on the local sensitivity at distance given by as described in the definition of above.

Remark 1.

As described above, the assumption that the input dataset is in general position can also be removed entirely. This can be done by noting that the first bound in the proof did not use the fact that the input dataset was in general position. Thus, we can instead define and as

which are less tight bounds, to avoid this assumption entirely. Note that this definition will not alter the resulting smooth upper bound on the local sensitivity in some cases, particularly for input datasets with maximum halfspace depth that is sufficiently higher than For many data generating processes, this condition occurs as the sample size diverges. Donoho and Gasko, (1992) provide sufficient conditions for the maximum halfspace depth to converge to a higher value than this lower bound. We are not aware of a case in which the lower bound on the maximum halfspace depth of fails to hold for a dataset that is not in general position, but we are also not aware of a similar result that avoids this assumption.

Remark 2.

Note that the formula for given in Lemma 6 is not generally the lowest possible upper bound. For example, in the case in which Nissim et al., (2007) provide a tight bound. In our notation, and with bounds specified on the feasible set of candidates rather than the observations, this bound is given by

| (18) |

where the median is defined so that it has order statistic and, for notational convenience, for any we let and, for any we let (Nissim et al.,, 2007). In contrast, in this case our bound can also be written as

| (19) |

Note that below we also provide an example that makes the equivalence of (19) and (9) more clear. Setting aside the difference that here we specify bounds on the estimator rather than on the observations themselves, Nissim et al., (2007) describe an equivalent upper bound in their Claim 3.4, and also show this relaxation inflates the resulting smooth sensitivity bound by at most a multiplicative factor of two. Note that Nissim et al., (2007) provide an algorithm that can be used to evaluate equation (18) in time.

Example 1.

In this example we will consider the input dataset and and show that the smooth upper bound on the local sensitivity provided in Lemma 6 can be found using (19) in this case. We will use notation from Remark 2 and Lemma 6 in this example.

First, note that the depth of is because the interval contains four observations, and the interval contains five observations. This logic can be repeated at each to show that is the unique maximizer of the halfspace depth in so we have Also, for any we have and for any we have Thus, for each we have and we also have Also, note that After substituting these terms into the definition of we have,

where, in the final line, we used the substitution and

Algorithm 1 provides a mechanism to approximate the Tukey median that satisfies DP, which is an immediate consequence of the previous lemma and the main result of Nissim et al., (2007), as stated in the following corollary. Note that it is also possible to use the smooth upper bound on the local sensitivity of the Tukey median provided in Lemma 6 to formulate pure DP mechanisms, at the cost of the distribution of the resulting estimator not having exponential tails, as is described by Nissim et al., (2007) in more detail.

Corollary 1.

If is closed and bounded and consists of datapoints in general position then Algorithm 1 satisfies DP.

The next theorem also provides a method to define the set that is the input into DPTukeyMedian in a data dependent manner while satisfying RDP when Note that we treat the case in which separately in Theorem 4.

Theorem 3.

Suppose the dataset consists of independent observations from the population distribution and consists of datapoints in general position. Let

If then DPTukeyMedian where satisfies RDP.

In addition, this mechanism satisfies ISIN.

Proof.

Since this proof considers the deepest regression for different datasets, we will denote the deepest regression for by We will also define the halfspace depth of for the population distribution as where Lemma 12 in Appendix A and the definition of imply

Since a similar bound can be constructed for any alternative dataset also defined by independent observations from we have

Thus, for defined using and any such dataset we have Since the mechanism DPTukeyMedian is DP when is deterministic, this implies DPTukeyMedian is RDP.

Note that is a sufficient condition to ensure is bounded with probability one because, for any sample of observations in general position, we have (Donoho and Gasko,, 1992).

Note that the additional use of the data in this mechanism, i.e., defining only impacts the output distribution through the scale of the Laplace noise, and the mechanism satisfies ISINwhenever is not equal to a singleton set. Thus, our assumption that the data are in general position is sufficient to ensure the mechanism satisfies ISIN. ∎

Remark 3.

Recall that Remark 1 described how the assumption that the datapoints are in general position can be removed. This assumption is used in the result above in two places. First, this assumption was used to derive the sample size bound that is required for the mechanism. In the absence of a generalization of the lower bound provided by Donoho and Gasko, (1992) that avoids the assumption that the datapoints are in general position, one could resort to stating the privacy guarantee as being conditional on the assumption that holds for datasets that are not in general position. Second, we also use this assumption to show the mechanism satisfies ISIN. This use of the assumption can be avoided more easily than the first; for example, this can be done by simply redefining as an enlargement, as described in more detail in Theorem 5.

The final result of this section improves on Theorem 3 for the case in which Note that the assumption that the datapoints are in general position is not required for this Theorem.

Theorem 4.

Suppose the dataset consists of independent observations from the population distribution and

Also, let and

Then, the mechanism defined as DPTukeyMedian where satisfies RDP for any

Also, the mechanism satisfies ISINfor any

Proof.

Let the empirical distribution function for the dataset be denoted by and the median of the dataset by This result follows from inverting the two sample Kolmogorov–Smirnov test. Specifically, for composed of independent draws from the same population distribution, the two sample Kolmogorov–Smirnov test implies the two sample Dvoretzky-Kiefer-Wolfowitz type inequality (Dvoretzky et al.,, 1956)

where is a constant. Wei and Dudley, (2012) show that using i.e., setting to Euler’s number, is sufficient for all sample sizes.

The definition of implies

This implies,

Note that the lower bound on the sample size holds if and only if so this condition ensures that is bounded.

The final result follows from the same logic that was used in Theorem 3, as is a sufficient condition to ensure is not a singleton set. ∎

4.2. DP Regression Estimators

In this section, we will provide deepest regression mechanisms that satisfy formal privacy guarantees. We will start by providing the regression depth counterpart to Lemma 6.

Lemma 7.

If is closed and bounded, then

| (20) |

where

| (23) |

and is a smooth upper bound on the local sensitivity of the deepest regression.

Also, can be found by only considering fits that pass through each combination of datapoints in the maximum in the definition of in the sense that

| (24) |

where

| (28) |

and is the set of such that either or is in an intersection of the boundary of and a boundary of a depth contour.

Proof.

Algorithm 2 provides an DP mechanism for approximating the deepest regression, which is an immediate consequence of the Lemma 7 and the main result of Nissim et al., (2007), as stated in the following corollary. Note that the same comment preceding Corollary 1 also holds in this case; it is also straightforward to use Lemma 7 to formulate pure DP deepest regression estimators (Nissim et al.,, 2007).

Corollary 2.

If is closed and bounded, DPDeepestReg as described in Algorithm 2, satisfies DP.

The next theorem also provides a method to set the input of DPDeepestReg using the data directly while satisfying RDP. This mechanism can be made to satisfy ISINby simply expanding this feasible set input, as described in more detail in the theorem. The simulations in Section 5 provide evidence that even a large expansion of this feasible set input may not have any impact on the distribution of the resulting estimator when the sample size is sufficiently large.

Theorem 5.

Suppose the dataset consists of independent observations from the population distribution Let

If then DPDeepestReg where

| (29) |

and satisfies RDP.

Also, if the mechanism satisfies ISIN.

Proof.

This can be proved in a similar manner as Theorem 3. In this case Lemma 14 in Appendix B provides the required uniform error bound. Also, as in Theorem 3, the bound on i.e., ensures is bounded because (Mizera,, 2002; Amenta et al.,, 2000).

The final part of the result follows from being sufficient to ensure is not a singleton set. ∎

4.2.1. Approximate Deepest Regression

As described previously, the deepest regression methods described in the previous section are most often limited to the case in which so this section provides a computationally efficient method for computing an DP approximate deepest regression estimate called Medsweep that was proposed by Van Aelst et al., (2002). In this section it will be helpful to define so that and so that

Informally, the method can be viewed as similar to applying the Frish-Waugh-Lovell theorem when finding an ordinary least squares estimator, in the sense that the method proceeds by parsing (or “sweeping”) out of by approximating the univariate regression of on and then redefining as the residual of this regression. Afterward, a similar approach is used to iteratively parse each column out of

There are a few possible ways to formulate DP Medsweep mechanisms. The simplest approach is to replace each median evaluation within Medsweep with a DP median mechanism. Here we will describe a slightly more involved formulation that has the advantage of providing a DP estimate with exponential tails conditional on the data. Specifically, this requires formulating DP variants of two methods that are used within Medsweep. The first is simply the median; below we use the smooth sensitivity of the median provided by Nissim et al., (2007) to define the scale of a Laplace mechanism, as described in equation (18).

The second method is and is defined as

The following lemma provides the smooth upper bound on the local sensitivity of when its output is truncated to the range This method is used in two places in Medsweep algorithm, with inputs are given by either columns of or one column of and the vector Note that the final DP mechanism actually imposes bounds on the output of these intermediate mechanisms, rather than the final estimator.

Lemma 8.

Suppose and satisfy Let and

Given a smooth upper bound on the local sensitivity of is given by

| (30) |

where

| (33) |

and

Proof.

We will show that is an upper bound on the local sensitivity of at distance i.e., Let and By the definition of

where the inequality above follows from the fact that is defined by a relaxation of the optimization problem that defines Specifically, the optimization problem defining can be derived by starting from and adding the constraints and

Recall the closed form smooth sensitivity of the median is given in (18). This definition, and the fact that, for any we have implies ∎

The function can alternatively be defined using a concept from computational geometry literature; some additional notation will be helpful to describe this connection. We will let denote a set of curves in with curve defined as Let denote the arrangement of which is defined as the collection of graphs of functions in More detail on arrangements and the other concepts from the computational geometry that we briefly describe here can be found in Edelsbrunner, (1987). We will define the level of a point as the number of curves in that either pass below or through and define the level of or as the points on one or more curves in with level Also, a approximate level of an arrangement of curves is defined as a curve that is within the and levels of an arrangement, which we will denote by Using this notation, we have,

| (34) | ||||

Unfortunately, we are not aware of a computationally efficient method of computing approximations of all levels of for this use case, in which the curves in are nonlinear and defined in 333Agarwal, (1990) provides a related method, which provides approximations to all levels when is a collection of lines in This can used within a method to compute a smooth upper bound on the local sensitivity using some of the same techniques in the approach described below. For example, upper bounds on the order statistics of can be computed for in each partition element where by constructing lines that are upper bounds of over all However, there are some issues with using this approach in practice, such as the large constants in the asymptotic time complexity of the approach described by Agarwal, (1990). Algorithm 3 provides an alternative approach, which is also used in the simulations provided in the next section. This approach uses the choice parameters to define the partitions of given by and After defining a partition of as

| (35) |

we bound each of the order statistics of for each in the partition element between the corresponding order statistic of and However, if are defined to be for a choice parameter and consists of independent and identically distributed observations, this algorithm’s output still converges to zero and has a time complexity of as described in the next Lemma. In the simulations in the next section we defined and as which results in a time complexity of

Lemma 9.

The output of Algorithm 3 is a smooth upper bound on the local sensitivity of When consists of independent and identically distributed observations, the algorithm has a time complexity of

Also, if is composed of independent observations from an absolutely continuous distribution with a convex support, then the output of Algorithm 3 converges in probability to zero.

Proof.

The only difference between the bound provided by the output of Algorithm 3 and the one described in Lemma 8 is that the former does not use the exact values for the order statistics of as described in the paragraph preceding this Lemma. Since using inexact bounds on these order statistics can only increase the upper bound on the local sensitivity at distance relative to that of (33), Algorithm 3 provides a smooth upper bound on the local sensitivity.

Since the area of each cell converges to zero, the upper and lower bounds on the order statistics of converge to the corresponding true order statistic of The conditions of the lemma imply, for any fixed and where are each so the output of Algorithm 3 is also

The time complexity follows from the algorithm evaluating sort operations on vectors of length ∎

Algorithm 4 provides pseudocode for the approximate DP variant of Medsweep; the following theorem provides the privacy guarantee of this mechanism.

Lemma 10.

The mechanism DPMedsweep, as described in Algorithm 4, satisfies DP.

Proof.

This follows from the fact that the primitive mechanisms used within DPMedsweep are DP and that the primitive mechanisms are called n_mechs times. ∎

The primary advantage of the approach used in Algorithm 4 is that the noise added to the output has exponential tails. However, there are several alternatives to this approach that are worth mentioning as well, particularly in cases in which noise with exponential tails is not required. First, as described above, one can alternatively formulate a DP variant of Medsweep by replacing each median evaluation with a DP median mechanism. This can be done using a variety of DP median mechanisms, including those that use smooth sensitivity, as described by Nissim et al., (2007), or an approach based on the exponential mechanism provided by McSherry and Talwar, (2007). Second, since the mechanism below uses several calls to primitive mechanisms, especially in the case of multivariate regressions, concentrated differential privacy (CDP) variants are also worth mentioning because this privacy guarantee provides tight sequential composition. This privacy guarantee was first described by Bun and Steinke, (2016); also, Bun and Steinke, (2019) describe how CDP mechanisms can be formulated using smooth upper bounds on local sensitivity.

5. Simulations

This section provides simulations to compare the accuracy of DPDeepestReg and DPMedsweep with three other DP regression methods for three different data generating processes (DGPs). Specifically, for each each and each we define the dataset as where

| (36) |

Note that, since each is symmetric, the mean of conditional on is equal to the median of conditional on so the DP conditional mean and median estimators described in the next subsection estimate the same population value. These simulations were performed for each and, for each DP mechanism, we set to

For each simulation iteration, we estimate using DPDeepestReg DPMedsweep and the three classic DP estimators described in the next subsection. As described previously, our aim with the implementation choices described in the next section was to err on the side of understating the relative accuracy of the two proposed estimators, particularly for choices related to both datapoint bounds (in the case of two of the three classic DP methods) and estimator bounds (in the case of the proposed approaches), which are described in more detail in the final paragraph of the next subsection.

5.1. Tested DP Estimators

The implementation for DPMedsweep used the pseudocode given in Algorithm 4. The implementation of DPDeepestReg used the pseudocode given in Algorithm 2; to compute the deepest regression estimator, we simply computed the depth of all candidate regressions that pass through each pair of data points, using the function rdepth2 from Segaert et al., (2017) that was rewritten in python.

All three of the existing DP regression estimators are based on python code from Alabi et al., (2020), which is available at https://github.com/anonymous-conf/dplr. The first method is DPMedTS_exp which is a differentially private Theil-Sen estimator (Theil,, 1950; Sen,, 1968). This DP mechanism is based on the mechanism provided by Dwork and Lei, (2009), but also incorporates subsequent results in the DP literature that improve accuracy of DP median mechanisms.

Second, NoisyStats is an DP OLS estimator. This mechanism works by passing sufficient statistics for the OLS estimator through a Laplace mechanism. One disadvantage of this approach is that, whenever the DP approximation of var is negative, this mechanism uses of the total privacy-loss budget without actually providing an estimate. For the purposes of calculating the error metrics that are reported below, these simulation iterations were simply removed before computing these error metrics; the count of the simulation iterations for which no output was returned from this mechanism is provided in Table 1. Note that this occurred most often for smaller sample sizes, the simulations, and the DGPs with thicker tails that we consider.

| DGP | 50 | 100 | 200 | 300 | 400 | 500 | |

|---|---|---|---|---|---|---|---|

| 4 | 41 | 36 | 19 | 14 | 6 | 3 | |

| 4 | 39 | 31 | 21 | 17 | 11 | 9 | |

| 4 | 47 | 30 | 29 | 25 | 18 | 12 | |

| 12 | 27 | 6 | 2 | 1 | 0 | 0 | |

| 12 | 30 | 11 | 4 | 0 | 1 | 0 | |

| 12 | 30 | 21 | 13 | 2 | 1 | 1 |

Third, DPGradDesc is an DP mechanism that provides a DP OLS estimate using a DP gradient descent method. Like the methods proposed here, we used for this mechanism. We initialized these gradient descent steps at the origin and chose an iteration limit of 30. and we also set the iteration limit to 30. Another choice parameter was set so that the gradient was clipped to the unit cube These choices appeared to increase accuracy in our simulations relative to their default values, but it is possible that other choices would provide a further improvement.

These three existing mechanisms were designed to return estimates of the dependent variable at two values of the independent variable, so we also modified DPDeepestReg and DPMedsweep to output estimates of the dependent variable at two values of the independent variable. Specifically, in each simulation iteration, we saved the errors of the dependent variable estimate at the 0.25 and 0.75 quantiles of the random variable for each of the five DP estimators considered, and, after 100 simulation iterations, we computed the mean squared error and median absolute error for each of these estimators, which are provided in Figures 2 and 3 respectively. These results are also discussed in more detail in the next subsection.

The first two existing DP mechanisms described above require bounds on To define these bounds, we use an approach that was inspired by the DP mechanism provided by Chen et al., (2016), which, as described above, outputs an approximation of the bounding box given by where is as small as possible such that at least a proportion of the data points are in Setting this choice parameter in practice requires balancing two tradeoffs. First, higher values typically result in larger datapoint bounds, which leads to a higher global sensitivity and thus a higher variance of the noise in these mechanisms. Second, since all datapoints outside of these bounds are ignored in these mechanisms, lower values tend to decrease the statistical efficiency and increase the bias of the DP estimator. Rather than use this DP mechanism, we simply set the bounds on using this definition of directly, with in the simulation results presented in this section. Since this choice parameter did have a significant impact on the performance of both of these classical DP estimators, Appendix C provides the simulation results for both and The approach taken here is intended to simulate an ideal realization of the output of the preliminary DP mechanism provided by Chen et al., (2016). Note that we do not account for the privacy-loss budget that would be required to compute these data-dependent bounds in an actual use case in order to err on the side of overstating the accuracy of these existing methods for a given total privacy-loss budget. In contrast, for the two proposed DP estimators, we use the non-data-dependent bounds on of The impact of this choice is described in the final paragraph of the next subsection. As described in the paragraph preceding Lemma 9 in more detail, we defined as which results in DPMedsweep having a time complexity of

5.2. Simulation Results

Before discussing the simulation results in detail, it may be worth pointing out our reasons for including both the mean squared error and the median absolute error of these methods. Both of these error metrics are examples of loss functions that one may seek to minimize with the choice of an estimation strategies. If this is done, the mean squared error may be regarded as the more prudent choice, in the sense that the upper tail of the absolute errors are given more weight. However, since NoisyStats has an infinite expected absolute error, the mean squared error estimates for this mechanism do not converge in the number of simulation iterations. Thus, we choose to include median absolute error metrics solely because the population counterparts of these metrics exist for each mechanism, rather than because the invariance of median absolute error on the magnitude of the largest errors is an advantage in the context of selecting an estimator.

In the case of both mean squared error and median absolute error, one interesting feature of the simulation results is the consistency of DPGradDescent across DGPs, values of and sample sizes. This mechanism does not appear to exhibit a gain in accuracy as the sample sized increases; although, as described previously, this may be due to the fact that we only performed limited tuning of the choice parameters of this method. This mechanism also appears to outperform other estimators in terms of median absolute error and mean squared error in all DGPs when and In contrast, in the case of DPMedTS_exp both the error metrics we consider are more obviously decreasing in the sample sizes for most of the DGPs and combinations we consider. It is interesting to note that even the exponential tails of the Laplace distribution appear to be sufficiently thick to make the impact of sample size less apparent than for the normal distribution for DPMedTS_exp Since the NoisyStats estimator does not have finite expected squared error, we will instead focus on the median absolute errors for this estimator. The impact of the tail behavior of the DGP on the statistical efficiency, i.e., the rate at which errors decrease as the sample size increases, appears to be less obvious in this case. For both DPMedTS_exp and NoisyStats higher values of also appear to increase the statistical efficiency.

The two estimators proposed in this paper appear to provide similar performance to one another, but DPDeepestReg appears to provide a slight gain in accuracy over DPMedsweep These two estimators also appear to compare favorably to the classic DP regression estimators in these simulations when either the sample size or epsilon is sufficiently large. Also, note that this accuracy improvement is most notable in cases in which the tails of the DGP are thicker.

To assess computational costs of the proposed approaches we also measured the median runtime for each sample size. On an ordinary laptop, in each simulation iteration with a sample size of 500, the median runtime was 5.8 seconds for DPDeepestReg and 1.9 seconds for DPMedsweep Since the vast majority of the runtime of DPMedsweep was spent computing the smooth sensitivity, the runtime of this mechanism can be improved by reducing as defined in in Lemma 9, below at the cost of increasing the noise scale used within this mechanism.

One advantageous feature of the proposed approaches in these simulations is that can be defined as progressively larger sets as the sample size diverges without changing the distribution of the DP estimators. In other words, when the sample size is sufficiently large, the bound on the local sensitivity at distance multiplied by i.e., typically obtains its maximum value at a relatively low value of while the choice of only impacts the value of when is large. In contrast, for the three classical approaches, the choice of bounds has a significant impact on the distribution of the output in all sample sizes. To explore this feature in the context of these simulations, we computed the minimum required diameter of defined as that would be required to change the scale of the Laplace noise used within DPDeepestReg for at least one of the simulation iterations of any of the three DGPs we consider in these simulations, for each sample size and each As shown in Table 2, the resulting minimum diameter values appear to be increasing at an exponential rate in in these simulations, with a higher rate when

| 4 | ||||||

|---|---|---|---|---|---|---|

| 12 |

6. Discussion

This paper proposes several approximate DP and RDP estimators based on maximizing notions of statistical depth, including the Tukey median and the deepest regression estimator. An approximate DP mechanism for the Medsweep regression estimator is also proposed. Afterward, simulations are provided for both of the proposed approximate DP regression estimators, and these estimators appear to compare favorably to classic DP regression estimators when either the sample size or epsilon is large.

One reason the input requirement of bounds on the data or the estimator itself is an area of emphasis in this paper is that we are not aware of approximate DP location or regression estimators that provide a reasonable balance between accuracy and privacy in the absence of strong assumptions on the population distribution, as described in Sections 1 and 2.6. These assumptions are unlikely to hold in practice for many use cases of interest, especially for use cases in which one or more variables exhibit thick tail behavior, and we are also not aware of a way to check these assumptions using a DP mechanism without making other strong distributional assumptions.

There are also a number of areas for further research in the intersection of DP estimators and statistical depth. First, Rousseeuw and Hubert, (1999) provide a quantile regression estimator based on regression depth, along the lines of Koenker and Bassett Jr, (1978), and it appears that similar techniques to the ones used here can be used to formulate smooth upper bounds on the local sensitivity of these estimators. Second, improving the bound described in Theorem 9 would also be advantageous for multivariate regression estimation. Third, since inference is often one of the main goals when using regressions, one important area for further work is the development of methods related to DP inference on the estimators described here.

Acknowledgements

The author thanks John M. Abowd, Brian Finley, Daniel Kifer, Roger Koenker, and Tucker McElroy for their insightful comments.

Appendix A Probability Bounds on Halfspace Depth

In this section we will provide results on convergence of the function

to its population counterpart,

Let denote the class with elements given by To find uniform error bounds for we will start by bounding the shatter coefficient of the class which is the maximum number of nonempty intersections of with elements of the class (Vapnik and Chervonenkis,, 2015). More formally, the shatter coefficient is defined as

| (37) |

Lemma 11.

The shatter coefficient of the class of sets with elements given by where and satisfies

Proof.

See for example, Corollary 13.1 of (Devroye et al.,, 2013). ∎

Lemma 11 implies that converges almost surely to zero at a rate of This is also already a well known result in the literature, since deriving the limiting value of the objective function is typically a first step for showing consistency of an estimate (i.e.: in this case); see for example, (Masse,, 2002; Bai and He,, 2008). Next we will use this result to derive an explicit finite sample probability bound on

Lemma 12.

Suppose is composed of observations that were sampled independently from the population distribution Then, for the following bound holds

Proof.

This a direct consequence of Lemma 11 and the main result of (Devroye,, 1982), which states that there exists a constant such that for all

and ∎

Remark 4.

This result prioritizes the probability bounds being explicitly computable in practice and being as tight as possible for typical sample sizes. It is worth pointing out that this is not the best theoretical rate. For example, both of the main results of Talagrand, (1994) provide uniform error bounds with a better rate of convergence, but we are not aware of explicit numerical bounds on the constants in these results for them to be used in practice.

Appendix B Probability Bounds on Regression Depth

In this section we will provide results on convergence of the function

to its population counterpart,

Let denote the class with elements given by To find uniform error bounds for we will start by bounding the shatter coefficient of the class which is the maximum number of nonempty intersections of with elements of the class (Vapnik and Chervonenkis,, 2015). More formally, the shatter coefficient is defined as

| (38) |

Lemma 13.

The shatter coefficient of the class of sets with elements given by where and satisfies

Proof.

We will start by finding the shatter coefficients of several intermediate classes. Specifically, let and be defined as

Since both classes are defined by linear functions of dimension for each we have see for example, Theorem 13.9 of (Devroye et al.,, 2013) and the subsequent remark. Thus, after considering the case in which both classes pick out the most possible subsets of simultaneously, we have

This same argument can be repeated to show where

Since each element of is given by where and a similar argument that was made when defining classes using intersections results in the bound, ∎

Note that this bound on the shattering coefficient also implies converges almost surely to zero at a rate of which is already a known result in the literature; see for example, Gao, (2020). Lemma 13 also implies our required probability bound, which is provided below.

Lemma 14.

Suppose is composed of observations that were sampled independently from the population distribution Then, for the following bound holds

| (39) |

Proof.

Remark 5.

The remark following Theorem 12, regarding the rate of convergence of the probability bounds provided above being suboptimal, are also applicable in this case.

Appendix C Simulation Results For Different Choices of

As described previously, we set the bounds on each and in our simulations for both the NoisyStats and the DPMedTS_exp mechanisms by finding the smallest bounding box of the form such that a proportion of the data points are in The simulations provided above used and, since this choice did have a significant impact on the simulation results, this Appendix C provides the simulation results for the alternative choices of and Specifically, Figures 4 and 5 provide the mean squared error and median absolute error when and Figures 6 and 7 provide these error metrics for the case in which

For the case in which all of the comments regarding the relative performance of the DP estimators from Section 5 appear to still be the case; however, in almost all cases the performance appears to improve when relative to when by between 50 and 200%, with the largest improvements for cases in which and for the DGPs with thicker tails. In contrast, for the cases in which the statistical efficiency appears to change more noticeably; unsurprisingly, this is most apparent when is small and for both of the DGPs with thicker tails.

References

- Agarwal, (1990) Agarwal, P. K. (1990). Partitioning arrangements of lines I: An efficient deterministic algorithm. Discrete & Computational Geometry, 5(5):449–483.

- Alabi et al., (2020) Alabi, D., McMillan, A., Sarathy, J., Smith, A., and Vadhan, S. (2020). Differentially private simple linear regression. arXiv preprint arXiv:2007.05157.

- Amenta et al., (2000) Amenta, N., Bern, M., Eppstein, D., and H Teng, S. (2000). Regression depth and center points. Discrete & Computational Geometry, 23(3):305–323.