Wealth Dynamics Over Generations:

Analysis and Interventions

Abstract

We present a stylized model with feedback loops for the evolution of a population’s wealth over generations. Individuals have both talent and wealth: talent is a random variable distributed identically for everyone, but wealth is a random variable that is dependent on the population one is born into. Individuals then apply to a downstream agent, which we treat as a university throughout the paper (but could also represent an employer) who makes a decision about whether to admit them or not. The university does not directly observe talent or wealth, but rather a signal (representing e.g. a standardized test) that is a convex combination of both. The university knows the distributions from which an individual’s type and wealth are drawn, and makes its decisions based on the posterior distribution of the applicant’s characteristics conditional on their population and signal. Each population’s wealth distribution at the next round then depends on the fraction of that population that was admitted by the university at the previous round.

We study wealth dynamics in this model, and give conditions under which the dynamics have a single attracting fixed point (which implies population wealth inequality is transitory), and conditions under which it can have multiple attracting fixed points (which implies that population wealth inequality can be persistent). In the case in which there are multiple attracting fixed points, we study interventions aimed at eliminating or mitigating inequality, including increasing the capacity of the university to admit more people, aligning the signal generated by individuals with the preferences of the university, and making direct monetary transfers to the less wealthy population.

1 Introduction

The wealth of a population evolves over generations as a function of the opportunities available to it. Opportunities available to a generation depend not only on their talent, but also on the wealth of the previous generation. In such a dynamical system, the initial wealth of a population determines how wealth evolves and what it will be in the limit. Understanding this system can help illuminate when and why inequalities can arise and persist.

In this paper we define and analyze a simple, mathematically-tractable model for this feedback system, before considering possible interventions to make its behavior more equitable. To discuss the main conclusions of our paper, we first need to provide a sketch of our model. Individuals are divided across multiple populations, and have both a type (an abstraction of talent) and a wealth. Within a single population, the distribution of wealth and types are given by Gaussians with known means and variances. Types are distributed identically across populations, but each population has its own distribution of wealth. An individual from a particular population is sampled by sampling their type from the (universal) type distribution, and their wealth from the wealth distribution particular to their population. An individual then generates a signal , i.e., some convex combination of their wealth and type. This signal could represent e.g. an individual’s score on a standardized test, or the rating that results from an interview. Here we allow that the signal might have a dependence on wealth rather than just type because of the indirect effects it can have on evaluations: for example, the ability to engage in additional test preparation. Downstream, a university111Throughout this paper we describe the downstream agent as a university admitting students. However we could also view the downstream agent as an employer hiring employees, or any other agent allocating opportunities based on evidence that conflates talent and wealth that have effects on the long-term wealth of the selected individuals. who has no direct knowledge of applicant’s types or wealth (but with knowledge of the distributions from which they were drawn) observes the signal, and forms a posterior belief about the applicant’s type and wealth. The university seeks to select individuals for whom another convex combination exceeds some threshold , and so selects exactly those applicants for whom . Here again we allow that the university might have an explicit preference for wealth (and not purely for type). This might represent e.g. a desire for full tuition payments or future alumni donations, or a more nebulous desire for “culture fit” or for skills associated with wealth (e.g. students who can walk on to the sailing or squash team). For each population we then let the mean wealth of the next generation be a non-decreasing function of the fraction of people admitted to the university at the previous round. We also assume that the distribution of types (or talent) remains unchanged over generations and is identical for all individuals, independent of their population.

First, we consider the fixed points of these wealth dynamics. If there is only a single fixed point (and the dynamics converge to it), this implies that wealth inequality across population groups is transitory, and that over time it will equalize (as the mean wealth of all populations moves to the single attracting fixed point). On the other hand, if there are multiple fixed points of the wealth dynamics, then wealth inequality can persist, with different populations “stuck” at different fixed points.

We give conditions under which the dynamics correspond to a contraction map and have a single fixed point (implying that wealth inequality is transitory). These conditions in particular include the case when — i.e. when the university is selecting entirely based on inferred type. On the other hand, there are other situations (in which, necessarily the university places some weight on wealth) in which case there can be two attracting fixed points (and a third unstable fixed point), which can result in persistent inequality absent intervention: one population can be “trapped” in the less wealthy fixed point, while the other one is in the more wealthy fixed point.

We then turn our attention to interventions. We focus our study of interventions on ways to move a population’s wealth from the lower fixed point to the higher fixed point, or to modify the dynamics so that there is a single attracting fixed point (which leads to wealth equality). We consider three types of interventions:

-

1.

Increasing The Capacity of the University: We consider what happens when the university is able to admit more applicants (by lowering its threshold ). We show that doing this has positive effects: either it shifts the dynamics from the regime in which there are multiple fixed points to the regime in which there is a single fixed point (thus leading to long-term wealth equality), or it raises the wealth of both attracting fixed points.

-

2.

Changing the Design of the Signal : We consider what happens if we are able to better align the signal the university receives with the university’s objective function (by shifting closer to — i.e. by having the signal weight type and wealth more similarly to how they are weighted in the university’s objective function). We show that as is moved closer to the disparity between the two fixed points is reduced. Notably, and perhaps counter-intuitively, making the signal depend more on type (by increasing ) is not always the way to reduce disparities (despite the fact that type is distributed identically across populations).

-

3.

Direct Subsidies to the Disadvantaged Population: Finally we consider making direct financial subsidies to the disadvantaged population, to shift them from the lower wealth attracting fixed point to the basin of attraction of the higher wealth fixed point (from which they will naturally proceed to the higher wealth fixed point without further intervention). We consider a parameterized family of objective functions that the designer might have, that differ in how they relatively weight the cost of the subsidy with the wealth of the disadvantaged population, and in how they discount time. Within this class of interventions, we focus on two options: the most aggressive “1-shot” option makes a large 1-shot payment to directly increase the wealth of the disadvantaged population to move them to the basin of attraction of the wealthier fixed point. The least aggressive “limiting” option makes the minimal payment per round that is guaranteed to cause eventual convergence to the wealthier fixed point. We derive conditions under which the “1-shot” option is preferred by the designer over the “limiting” option and vice versa.

1.1 Discussion and Limitations

For mathematical tractability, we study a simple stylized model, which should be viewed as a first cut at attempting to model wealth inequality rather than a faithful description of the full problem. For example, we have assumed that the university has access to an applicant’s wealth only indirectly via inferences that can be drawn from their test score and population. In practice, a university has a number of other signals at their disposal. One should interpret the wealth populations in our model as equivalence classes induced by the information available to them at admissions time. Similarly, we have modeled individual talent via a static “type” distribution, when in fact talent is multi-dimensional and not static (and might depend on opportunities that different populations might have different access to prior to university admissions). We have not modelled university capacity constraints, and this allows us to treat each population independently of the others.

Nevertheless, several qualitative takeaways emerge from our modelling that we think are interesting: for example, in our model, the persistence of inequality (multiple attracting fixed points) depends on the university using a selection rule that intentionally takes into account wealth, rather than just talent. We show that if the university puts weight on type in our model, there is only a single fixed point. This suggests that changes in admission policies that reduce the focus on wealth (for example, switching to need-blind admissions and reducing or eliminating legacy admissions) might have beneficial long-term effects. As another takeaway, we find that aggressive interventions (in our model, that aim to lift the lower-wealth population in one shot to the basin of attraction of the higher-wealth fixed point) are often the most cost effective in the long run, compared to more modest interventions that would accomplish the same goal after rounds. On the other hand, incremental interventions become optimal when society heavily discounts the future. This suggests that institutions that are able to formulate longer-term goals, but have the resources to act on them immediately (for example, non-profit universities with large endowments) may be able to combat wealth inequality more effectively.

1.2 Related Work

Our paper is related to economic models of inequality, which date back to Arrow (1973) and Phelps (1972). For example, Coate and Loury (1993) and Foster and Vohra (1992) study two stage models in which the existence of self-confirming equilibria can cause inequality to be persistent even when populations are ex-ante identical.

More recently, the computer science community has begun studying dynamic models of fairness. Jabbari et al. (2017) study the costs of imposing fairness constraints on learners in general Markov decision processes. Hu and Chen (2018) study a dynamic model of the labor market similar to that of Coate and Loury (1993); Foster and Vohra (1992) in which two populations are symmetric, but can choose to exert costly effort in order to improve their value to an employer. They study a two-stage model of a labor market in which interventions in a “temporary” labor market can lead to high-welfare symmetric equilibrium in the long run. Liu et al. (2018) study a two-round model of lending in which lending decisions in the first round can change the type distribution of applicants in the 2nd round, according to a known, exogenously specified function. Liu et al. (2020) study a dynamic model where in each round, strategic individuals decide whether to invest in qualifications and the decision-maker updates his classifier that decides which individuals are qualified; they characterize the equilibria of such dynamics and develop interventions that lead to better long-term outcomes. Arunachaleswaran et al. (2020) study a model in which decisions over individuals and populations are made along a multi-layered pipeline, where each layer corresponds to a different stage of life. They consider the algorithmic problem faced by a budgeted centralized designer who aims to intervene on the transitions between layers to obtain optimally fair outcomes, when such modifications are costly. Kannan et al. (2019) study a two stage model of affirmative action in which a college may set different admissions policies for an advantaged and disadvantaged group, but a downstream employer makes hiring decisions that maximize their expected objective given their posterior belief on student qualifications (that depend on the college’s policies). Jung et al. (2020) study an equilibrium model of criminal justice in which two populations with different outside option distributions make rational decisions as a function of criminal justice policy; they show that policies that have been proposed with equity considerations in mind (equalizing false positive and negative rates) actually emerge as optimal solutions to a social planner’s optimization problem even without an explicit equity goal.

We highlight two closely related papers. Heidari and Kleinberg (2021) also study a model of inter-generational wealth dynamics across many rounds, in which both wealth (which they model as a binary) and talent play a role in success, as a function of opportunities that can be allocated to a limited portion of the population. Like us, Heidari and Kleinberg (2021) use college admissions as a running example of an institution allocating the opportunities, and like us, study a model in which admissions to college plays the role of determining wealth increase or decrease from one generation to the next. Our models differ in a number of specifics, but the primary difference between these two works is that Heidari and Kleinberg (2021) study the optimal policy for a very patient institution interested in maximizing its long-run payoff, and show that it recovers a form of affirmative action, preferentially offering opportunities to the less wealthy population so that it can reap the benefits of their resulting increased wealth in future generations. In contrast, we study institutions that are myopic, and optimize only for their short-term reward. In this setting, we study conditions under which such institutions do or do not perpetuate inequality, and study interventions in the settings in which they do. Mouzannar et al. (2019) study a continuous time dynamic in which two populations with binary, fully observable type are selected by a college with a myopic objective, whose selection rate within each population changes their type distribution at the next round. They study conditions under which imposing an “affirmative action” constraint (having the same selection rate within each population) can lead to equal or improved outcomes in the long run. In addition to various differences in the models (they study a setting with fully observed, binary types) and the class of interventions considered (we study changing what is observable to the university and offering direct subsidies), the most salient difference is that our model seeks to understand how wealth evolves over the long run, and has the crucial feature that wealth can be partially conflated with type in the signal observed by the university. We also focus on intervening directly on wealth via monetary subsidies. In contrast, Mouzannar et al. (2019) do not model wealth, and in their dynamic, the type distribution directly evolves and is fully observable. Hence their myopic college does not need to do any inference as in our model.

2 Preliminaries

Definition 1 (Attracting fixed points).

Let be a real-valued function and let be such that . We call a fixed point of . Further, let be the sequence defined by and ; we say that is attracting for if and only if converges to .

Claim 1 (Attracting fixed points).

Let be a real-valued, continuous, non-decreasing function such that is a fixed point of . If for all , is attracting on . Similarly, if for all , is attracting on .

Proof.

Let . Let be the sequence defined by and . , Since is non-decreasing , but , so this inequality is in fact strict, i.e . Note that by induction, we have for all that ; hence is increasing and for all . In particular, is a convergent sequence with a finite limit in . Now, since for all , is ’s unique fixed point on . Because is continuous, we must have , i.e. the limit must satisfy . The only point on that satisfies this condition is , yielding the first part of the result. A similar argument holds for the second part of the proof. ∎

3 Model

We consider a university that has a non-atomic set of applicants from two different sub-populations (or groups), denoted and , and must decide which applicants to admit. Each applicant has a type , where the types are random variables drawn i.i.d. from a known distribution ; we assume that the distribution of types is the same for both groups. Further, each applicant also has a wealth ; wealth is drawn i.i.d. from a known distribution which may depend on the applicant’s group . We assume that wealth and types are drawn independently of each other.

The university aims to make decisions based on each applicant’s type and wealth, and would like to admit individuals for whom

for some parameter and some threshold . Here, represents how much the university values type versus wealth. However, the university cannot directly observe this quantity. Instead, we assume that it can only see a score for each applicant (for example in the form of a standardized test result), where the score is a convex combination of both an applicant’s type and wealth . We write

for some known . The university then performs a Bayesian update and admits individuals that satisfy

We are interested in understanding the long-term dynamics of a process where the university’s decisions (made as described above) affect the individuals’ future attributes. We consider a discrete time horizon, in which at each time step , the university’s decisions shapes the distribution of wealth in each group in time step . In particular, we assume that the expected wealth of group in step is the fraction of group that is admitted by the university at time step . I.e., we write

| (1) |

This is motivated by the fact that students that are admitted to competitive universities are expected to reach better life outcomes and accumulate more wealth.

In the rest of the paper, we make the following assumptions on the functional form of the type and wealth distributions:

Assumption 1.

The type at any time instant is drawn from the distribution . The initial wealth at time for population satisfies , and at time step for a fixed constant .

Note that the type can be centered around without loss of generality, by changing the value of used by the employer by the corresponding amount. The assumption is also without loss of generality, and simply renormalizes the average wealth of a group to be between , so long as we consider populations with bounded wealth. Note that with our assumptions the mean wealth of each group always stays in the range although the sampled wealth of individuals can fall outside this interval.

4 Wealth Dynamics and Properties

We note that the dynamics of each group only depend on the decisions made by the university within that group. Therefore, we can treat groups independently. In this section, we focus on a single group at a time, and drop the dependencies on in our notations for simplicity. We show that several attracting fixed points can arise from our dynamics; in particular, there are regimes of parameters under which there is a low wealth fixed point that groups with initially low wealth converge to, and a high wealth fixed point that groups with initially high wealth converge to. In Section 5.3, we consider interventions that apply to more general update functions that the ones described in this Section, so long as they have similar fixed point properties.

4.1 Computing the Wealth Update Rule

We start by characterizing the joint distributions of the type , the wealth , and the score .

Claim 2.

Let . We have that forms a bivariate Gaussian distribution with mean and covariance matrix

Similarly, forms a bivariate Gaussian distribution with mean and covariance matrix

The proof is provided in Appendix A.1. This allows us to compute the update function that maps the wealth of a group in the current round, , to the wealth of that same group in the next round, :

Lemma 1.

Recall that is the threshold used by the university to decide admission. At every time step , we have

where and is the cumulative density function of a standard Gaussian. We denote the update rule function

| (2) |

4.2 Fixed Points and Convergence of the Dynamics

We can now use the closed-form expression for the update rule to study the properties of the wealth dynamics. In this section, we bound the number of fixed points of our dynamics, provide properties of these fixed points, and characterize which fixed point each initial wealth converges to. We start by noting that the update rule has a simple shape. Indeed:

Claim 3.

is continuous and increasing in . Further, is convex on and concave on where

The proof of the above claim is given in Appendix A.3. We now use the above properties on the shape of to derive properties of its fixed point. First we remark that has at least one fixed point, since and , and is continuous. Now, note that the number of fixed points of is also upper-bounded:

Lemma 2.

Suppose , then has at most solutions for . If has fixed points , it must be that . If or , only has a single solution for .

The proof is provided in Appendix A.4. Lemma 2 has direct implications for disparities across groups with different starting expected wealth. In particular, the number of fixed points of determines whether different groups must converge to equal wealth (the case in which there is only a single fixed point) in the long-run or whether there are cases in which wealth inequality is persistent (the case in which there are multiple fixed points). We discuss these implications in more details in the rest of this section.

The Case of a Single Fixed Point

We now study conditions under which has single vs. multiple fixed points. We first consider the case of a single fixed point. In this case, we remark that the single fixed point has the following property:

Claim 4.

If is the single fixed point of , then is attracting on .

Proof.

Since , , and is continuous and has a single fixed point , it must be that for and for . Applying Claim 1 concludes the proof. ∎

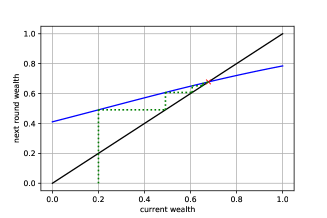

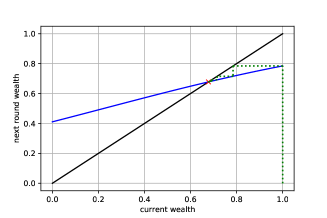

This implies in particular that when has a single fixed point , wealth dynamics converge to this fixed point no matter what the starting wealth was. This means in particular that there are no long-term disparities between populations of different initial socio-economic statuses (though they may take different amounts of time to reach the same wealth), i.e. the dynamics self correct for initial wealth disparities. Figure 1 shows an instantiation of a wealth update functions with a single fixed point and the corresponding wealth dynamics (in green); the plots illustrate convergence of the dynamics to the single fixed point starting both from an initially low wealth (Figure 1 (a)) and from an initially high wealth (Figure 1 (b)).

We note that Lemma 2 already implies that there exist interesting situations in which the dynamics have a single attracting fixed point and wealth dynamics are self-correcting. The first one is when is small (); i.e., the university is not very selective in its admissions. Intuitively, this leads to most individuals from any group being admitted (almost) independently of their starting wealth, which allows even economically disadvantaged groups to build wealth over time. The other situation deriving from Lemma 2 arises when . This can arise for two reasons: first, is the university is very selective and sets high values of , wealth becomes insufficient to qualify an individual for admission (as then ); an agent must have sufficiently high (inferred) type to be admitted, which helps reduce disparities due to wealth. This can also arise when is large and the university is mostly interested in type over wealth. Intuitively, in this case, the university pays significant attention to their posterior belief on the type of an individual, which facilitates equalizing the treatment of groups of different wealth since they have the same type distributions; while the university cannot observe type directly, they discount for average wealth more (by a factor of ) hence correct for wealth disparities more as is smaller.

Below, we provide an additional condition under which has a single fixed point:

Claim 5.

If , is a contraction mapping and has a unique attracting fixed point.

Proof.

This immediately follows from and from

(with equality at ). Note that and so the fixed point must satisfy if and only if and must be attracting.

∎

We note that where . This implies that, holding the college’s objective function (i.e., ) constant, the better the scoring rule aligns with the university’s admissions criteria (i.e. as the covariance between and increases), the smaller becomes. This makes the condition that is a contraction mapping with a single fixed point easier to satisfy, which in turn causes wealth dynamics to self-correct for initial inequality. When , the condition is always satisfied, and has a single fixed point. This may not be surprising in that in this case the university only cares about type in admissions, and the university requires a higher threshold on scores for wealthier populations; this helps reduce disparities across populations with disparate wealth.

The Case of Multiple Fixed Points

We first characterize which fixed points are attracting when multiple points arise, and which regime of initial wealth lead to which fixed points. We focus on the case of three fixed points, as the case of two fixed points is a corner case than can only arise if is tangent to at one of the fixed points.222Suppose this is not the case. hence before the first fixed point. Because it is not tangent to the identity line, it must then be that between the first and the second fixed point. Similarly, it must then be that after the second, last fixed point. This contradicts .

Claim 6.

Suppose has fixed points, denoted . Then is attracting for and is attracting for .

Proof.

This follows from the proof of lemma 2. Indeed, let , we have that , then must decrease below , increase above , and decreases below again as . This implies that for and , while for and . ∎

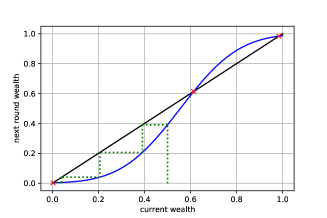

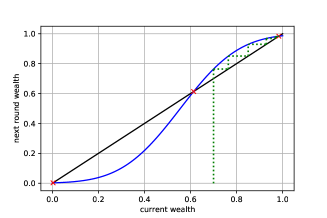

In particular, when there are three fixed points, a population that starts with low wealth will converge to the first fixed point, while a group with large initial wealth will converge to the third fixed point. In this case, initial disparities in wealth persist in the long term, and interventions are needed for different populations to obtain equitable long-term wealth outcomes. Figure 2 shows a wealth update function with three fixed points and the corresponding dynamics for two different starting points. We note that starting at low wealth leads to convergence to the first and lowest fixed point, while starting at relatively high health leads to convergence to the highest fixed point. The figure illustrates how wealth disparities can propagate and amplify over time.

We note that such situations can only arise in the regime in which . In particular:

Claim 7.

Suppose and . Then has fixed points.

Proof.

In this case, note that . Further, we know that

implying that is a fixed point of . Further,

hence in a small neighborhood and in a small neighborhood . By continuity of and the fact that , must have a solution on . Similarly, since , must have a solution on . ∎

Note that because is continuous in , must have three fixed points for any in a neighborhood of . I.e., there exists a continuous range of values of for which has three fixed points, showing that such situations are not a corner case of our framework, unlike when has two fixed points.

Remark 1.

There is a gap between the conditions given in Claim 5 and Lemma 2 under which a single fixed point arises, and the condition given in Claim 7. In particular, we remark that even if is not a contraction mapping and , or when , it may still have only a single fixed point. To investigate how often fixed points can arise, we picked a uniform grid of parameter values and investigated what fraction of the parameters that satisfy either or actually lead to an update rule with three fixed points. We found that this was the case for roughly percent of the values we explored, implying the existence of a significant range of parameters for which there are disparities in the long term wealth of different populations.

5 Interventions To Improve Long Term Population Wealth

In this section, we consider different types of intervention aiming at improving and equalizing population wealth, when the wealth dynamics have multiple fixed points (and so are not necessarily self correcting). We consider three types of interventions: i) changing the design of the admission rule used by the university, ii) changing the design of the standardized test or scoring rule that the university relies on, and iii) providing subsidies to disadvantaged groups.

5.1 Changing the Admission Rule

Since in our model, it is admission to university that confers a wealth advantage to the next generation, a natural intervention is to increase the capacity of the university, thereby admitting more people. Rather than changing the objective function of the university , we model this kind of intervention by decreasing the university’s admissions threshold . We note that although we do not explicitly quantify it, increasing the capacity of a university will come at some financial cost, and so this kind of intervention is not necessarily incomparable to the direct subsidies we consider later.

The claim below characterizes how the fixed points of change when we change the value of . For the sake of notation, we let be the update rule when the chosen threshold is , and omit the dependencies of in the other parameters of the problem.

Theorem 1.

Fix . For a given admission threshold , let be the fixed points of when all exist. Let be such that has fixed points, we have

but

Proof Sketch.

The proof follows simply by showing that the update function is decreasing in . In turn, decreasing moves the update rule “up”, which increases attracting fixed points and decreases unstable ones. The full proof is given in Appendix B.1. ∎

In interpreting Theorem 1, we recall that only the first and third fixed points and are attracting, and that is unstable (has no points for which it is attracting for ). Hence, if we are in a situation in which there is persistent wealth inequality (multiple fixed points), we find that if we can decrease the admissions threshold of the university, then either:

-

1.

We increase the wealth of both of the attracting fixed points (and hence the wealth of both populations, irrespective of which attractive fixed point they are at). By decreasing we also reduce the size of the attracting region of the lower wealth fixed point, thus enabling poorer populations to converge to the most desirable fixed point. Or

-

2.

We move the dynamics to one in which there is only a single fixed point, and hence eliminate wealth inequality.

5.2 Changing the design of the scoring rule

The college has to engage in inference about an applicant’s type and wealth when , because the signal it receives does not align with its objective function. What if we can modify the signal (by e.g. changing the design of a standardized test) to more closely align the signal with the college’s objective?

In this section we characterize how the fixed points of change when we change the value of . We denote the update rule when the scoring rule uses parameter , while the other parameters of the problem remain fixed.

Theorem 2.

Fix . For a given , let be the fixed points of when all exist. Suppose and let be such that has fixed points, then

Similarly, if and , we have

Proof Sketch.

The first part of the proof follows simply by showing that the update function is increasing in for (where the first fixed point lies) and decreasing in as for (where the third fixed point lies). In turn, increasing towards move the update rule “up” around the first fixed point and “down” around the third fixed point, which increases and decreases . A similar argument holds for . The full proof is given in Appendix B.2. ∎

Intuitively, one might suppose that to reduce wealth disparities, we should redesign tests so as to make them reflect type more strongly and wealth less strongly (since types are distributed identically across groups). But Theorem 2 shows that counter-intuitively, this need not be the case333Even when , may have three fixed points: by Claim 7, this arises for example when and . In this case, setting surprisingly leads to better outcomes than .. Instead, what Theorem 2 shows is that in order to reduce inequality, we want to move towards , causing the signal to better reflect the objective function of the college —- even when this results in reducing the extent to which the signal reflects type444Of course, if we can, we would prefer to increase the extent to which the college values type rather than wealth, but to the extent that we cannot do this, then we want to align the test with the college’s objective.. Theorem 2 shows that moving towards always has the effect of reducing wealth disparities. It either:

-

1.

Increases the wealth of the less wealthy attracting fixed point, and decreases the wealth of the more wealthy attracting fixed point, thereby decreasing the long term wealth disparity, or it

-

2.

Shifts the dynamic to one that has only a single fixed point, thereby eliminating long term wealth disparities.

5.3 Direct Subsidies

We have thus far considered interventions that can be applied by the college (admitting more students) or a testing body (changing the design of the signal). In this section, we take the point of view of a funding body or governmental agency that can provide direct monetary subsidies to populations. We generalize the class of functions we study to include any function satisfying the following properties:

Assumption 2.

is continuous and increasing. Further, has three fixed points with on and and on and .

The above assumption captures the main properties of our function when it has three fixed points and implies the same attracting properties we established for , , and , but also encompasses more general update rules that need not result from the Gaussian inference process we have studied thus far. We note that this allows us to study general S-shaped function with diminishing returns at both ends of the socio-economic spectrum. Such functions model situation in which people of very low income or very high income see little upward mobility (in the first case because of a lack of access to opportunities, and in the second case due to the fact that individuals of higher income are rare), whereas middle income individuals have significant opportunities to improve their wealth.

We denote by the subsidy given to a population with wealth at time step . The wealth of a population then depends of the wealth in time as

In this setting, we consider interventions that allow a population to reach beyond the second fixed point . Once a population reaches wealth (even slightly) over , their wealth naturally evolves to the highest attracting fixed point over time; i.e., wealth dynamics self-correct for disparities with no intervention needed. For the same reason, we only consider ; this is because populations with will converge to without intervention, and we can start intervening once reaches , while a population with will reach the best long-term outcome (the highest fixed point, ) on its own. Therefore, from now on, we assume for all . We can now formulate our centralized designer’s objective, which is to minimize the following loss function:

where , and is the first time step such that . Here is a discounting factor; the lower is, the less the designer cares about future as opposed to immediate outcomes. The objective is a convex combination of two terms, with weights controlled by . The first term consists of the discounted monetary cost of the subsidies (the sum goes up to time , since after the wealth of the population crosses , the subsidies cease. This term represents a preference to spend less money on direct subsidies. The second term consists of the sum discounted difference between the target wealth that the intervention is aiming at, and the wealth of the population at the current round. This term represents a preference to quickly increase the wealth of the lower wealth population. represents the relative strength of these two preferences.

Note that is a constant term that does not depend on the designer’s interventions, hence we will equivalently aim to minimize

where we drop the discounted difference between and the initial wealth at .

Algorithmically finding a near-optimal subsidy function

We note that in our setting, one may discretize the space of possible costs and use dynamic programming to find optimal interventions from each possible starting point. However, doing so requires carefully understanding the wealth update function . In practice, detailed knowledge of will be hard to come by. For this reason, in the rest of this section, we will aim for a “detail free” solution and consider a simple class of constant subsidies and study how they can be applied with minimal information about the wealth update .

Constant Subsidies

In the rest of this section, we consider the case in which is constant in for . I.e. there exists such that for all and otherwise. We call these -subsidy interventions. We qualify a -subsidy intervention as a -shot intervention if it takes time steps under the subsidy to reach wealth (at least) when starting at wealth , i.e. if . Note that different values of may lead to the same number of steps such that , i.e. there may be several values of that qualify as a -shot intervention for a given value of .

Our aim is to give guidelines on how to choose while using minimal information about the function . Here, we will encode this minimal information as a single, real parameter , defined as

| (3) |

Intuitively, measures how difficult it is for a subsidy to have an effect on wealth that propogates in the next round. When , we have that on , and investing a subsidy of increases the population wealth by , since . However, we have that for at least one value of , , implying that when is large, a large amount of the subsidy is lost in the next round, and so its overall effect is small. If we want to guarantee that our subsidies will eventually lift the lower wealth population to the higher wealth fixed point independently of its starting point, we need to consider subsidies in which .

Claim 8.

Suppose . Then there exists a starting wealth such that for all ; i.e., never reaches . On the other hand, if , there exists such that .

Proof.

Let be any value of such that (note that where , since on if has three fixed points). Suppose and , then . I.e., for all so long as ; note that the interval is not empty as . For the second part of the proof, note that by definition of , for all , , hence the group wealth increases by at least a constant amount at each time step. ∎

Intuitively, this holds because if is smaller than , it becomes insufficient to compensate the fact that the wealth of a group can decrease by an amount up to at each round. In the rest of this section, we aim to understand how different interventions for different values of compare to each other, and when to choose low-cost versus high-cost interventions. Before doing so, we note that there is always a single, optimal -shot intervention among all such -shot interventions:

Fact 1.

The -shot intervention with cost has smaller cost than any other -shot intervention. This immediately follows from the fact that any -shot intervention with cost has loss , and that no intervention with can reach in one shot, as .

We now provide a sufficient condition under which the -shot intervention is guaranteed to be optimal.

Theorem 3.

Suppose . Then, any -shot intervention has higher loss than the -shot, -subsidy intervention. I.e. the -subsidy intervention is optimal.

Proof.

The proof follows by induction on . First, let us consider the base case when , and let be any cost that leads to convergence in two shots. Consider any starting point . Note that the sequence of wealth must satisfy and . Further, note that because we must have . We then have that the loss satisfies

This concludes the case of .

For , note that we have and . Letting be any cost that leads to reaching in shots, we have that the loss function is given by

The second term in the last line of the inequality is the loss function when starting at instead of . Indeed, write the sequence that starts at and satisfies but (hence this new sequence converges in rather than steps); the loss of this sequence is given by:

By the induction hypothesis, since the cost of a one-shot intervention is lower than that of any -shot intervention, we have that

Therefore, is lower bounded by

∎

In particular, -shot interventions become optimal when the discounting factor is relatively large, or when is relatively small. The first result intuitively arises because when becomes large, the centralized designer cares about cost and wealth of the group at each time step; a -shot intervention allows the designer to incur a single up-front cost for intervening (instead of inefficiently investing a smaller cost per round over more rounds, and losing some of this invested cost, up to , at each time step) while immediately reaching high wealth outcomes. On the other hand, no matter what is, when becomes small, the designer only cares about reaching high wealth as soon as possible, hence prefers faster interventions. We now provide sufficient conditions under which -shot is not optimal:

Theorem 4.

If , the -subsidy intervention has lower loss than the -shot, -subsidy intervention.

Proof.

Consider any intervention with cost such that , i.e. we reach after at most time steps. First, remember that the loss for this intervention is given by

Noting that for all , hence , we can upper bound the loss by

In turn, we have that a sufficient condition for -subsidy to have a lower loss than one-shot is given by

This can be rewritten as

i.e.

which immediately leads to the theorem statement. ∎

Theorem 4 gives conditions under which the minimal 1-shot intervention has higher cost than the -subsidy intervention. But recall that we can take as small as (for arbitrarily small ) and still get an intervention that reaches the region of attraction for the highest wealth fixed point. Thus we have the following corollary, which gives a necessary condition for the 1-shot intervention to be optimal:

Corollary 1.

If , then the -subsidy intervention has lower loss than the -shot, -subsidy intervention as .

The above corollary provides the most stringent condition that we can derive from Theorem 4 for -shot not to be optimal. In particular, we note that the cheapest intervention we can use, the -subsidy one, is better than the -shot intervention so long as . We note that the combination of Theorem 3 and Corollary 1 show that when becomes small and subsidy interventions are efficient, the condition that becomes nearly tight for optimality of the -shot, -subsidy intervention. When is large, there are still situations in which the condition of Corollary 1 is essentially necessary and sufficient for the -subsidy to be better than the 1-shot intervention, as evidenced by the example below:.

Example 1.

Suppose is continuous, but such that it is linear on interval with within said interval. We have immediately that hence so long as is such that . Here, the one-shot intervention still has loss . However, the -subsidy intervention reaches , hence , after no less than time steps. In turn, it has loss at least

The proof of Theorem 4 shows that the loss is also upper-bounded by

Hence, it must be that this bound is essentially tight, i.e. that

In particular, in this case, the condition of Theorem 4 and Corollary 1 is not only sufficient but also necessary for the -subsidy intervention to have better loss than the one-shot intervention.

Acknowledgements

This work was supported in part by NSF grants AF-1763307 and FAI-2147212 and a grant from the Simons Foundation.

References

- Arrow [1973] Kenneth Arrow. The theory of discrimination. Discrimination in labor markets, 3(10):3–33, 1973.

- Arunachaleswaran et al. [2020] Eshwar Ram Arunachaleswaran, Sampath Kannan, Aaron Roth, and Juba Ziani. Pipeline interventions. arXiv preprint arXiv:2002.06592, 2020.

- Coate and Loury [1993] Stephen Coate and Glenn C Loury. Will affirmative-action policies eliminate negative stereotypes? The American Economic Review, pages 1220–1240, 1993.

- Foster and Vohra [1992] Dean P Foster and Rakesh V Vohra. An economic argument for affirmative action. Rationality and Society, 4(2):176–188, 1992.

- Heidari and Kleinberg [2021] Hoda Heidari and Jon Kleinberg. Allocating opportunities in a dynamic model of intergenerational mobility. In Proceedings of the 2021 ACM Conference on Fairness, Accountability, and Transparency, pages 15–25, 2021.

- Hu and Chen [2018] Lily Hu and Yiling Chen. A short-term intervention for long-term fairness in the labor market. In Pierre-Antoine Champin, Fabien L. Gandon, Mounia Lalmas, and Panagiotis G. Ipeirotis, editors, Proceedings of the 2018 World Wide Web Conference on World Wide Web, WWW, pages 1389–1398. ACM, 2018.

- Jabbari et al. [2017] Shahin Jabbari, Matthew Joseph, Michael Kearns, Jamie Morgenstern, and Aaron Roth. Fairness in reinforcement learning. In International Conference on Machine Learning, pages 1617–1626, 2017.

- Jung et al. [2020] Christopher Jung, Sampath Kannan, Changhwa Lee, Mallesh Pai, Aaron Roth, and Rakesh Vohra. Fair prediction with endogenous behavior. In Proceedings of the 21st ACM Conference on Economics and Computation, pages 677–678, 2020.

- Kannan et al. [2019] Sampath Kannan, Aaron Roth, and Juba Ziani. Downstream effects of affirmative action. In Proceedings of the Conference on Fairness, Accountability, and Transparency, pages 240–248, 2019.

- Liu et al. [2018] Lydia T Liu, Sarah Dean, Esther Rolf, Max Simchowitz, and Moritz Hardt. Delayed impact of fair machine learning. In International Conference on Machine Learning, 2018.

- Liu et al. [2020] Lydia T Liu, Ashia Wilson, Nika Haghtalab, Adam Tauman Kalai, Christian Borgs, and Jennifer Chayes. The disparate equilibria of algorithmic decision making when individuals invest rationally. In Proceedings of the 2020 Conference on Fairness, Accountability, and Transparency, pages 381–391, 2020.

- Mouzannar et al. [2019] Hussein Mouzannar, Mesrob I Ohannessian, and Nathan Srebro. From fair decision making to social equality. In Proceedings of the Conference on Fairness, Accountability, and Transparency, pages 359–368, 2019.

- Phelps [1972] Edmund S Phelps. The statistical theory of racism and sexism. The american economic review, pages 659–661, 1972.

Appendix A Omitted Proofs for Section 1: Wealth Dynamics

A.1 Proof of Claim 2

Because is a convex combination of and , both and are multivariate Gaussians. The covariances are given by

and

A.2 Proof of Lemma 1

A.3 Proof of Claim 3

For simplicity of notations, let us write instead of . Continuity is immediate from being the composition of a linear (hence continuous) function and the continuous function . Now, we have

showing is increasing. Finally, the second order derivative of the update rule is given by

The result immediately follows, as if and only if .

A.4 Proof of Lemma 2

Let us write . Note that has a fixed point if and only if .

-

1.

and is convex on . Then , , and is also convex. Further, note that and . Therefore, can only have one solution at most. Indeed, let be the smallest value in for which ; we have that for all , we can write for some , Then, we have by convexity.

-

2.

and is concave on . Then can have at most fixed point by the same argument as above.

-

3.

Otherwise, note that is first increasing up until then decreasing in . Therefore, has at most two zeros and . If has two zeros, they must satisfy and , and that for , for , and for . then has at most three intersection with , with the first intersection on , the second on , and the third on . When has at most one zero, can only have at most zeros

This concludes the proof.

Appendix B Omitted Proofs for Section 5: Interventions for Long-term Fairness

B.1 Proof of Theorem 1

This follows from the fact that is decreasing in for all . First, this implies that for all . Hence . For the third fixed point, note that ; because is continuous and , this immediately implies that has a fixed point on , hence .

Finally, let us consider the case of the second fixed point. First, we note that it must be that . Suppose this is not the case, it must be that for all . Further, for all , we must have , hence for all . This implies . However, we must have while , which is a contradiction.

Now that we have , note that it must be that on a small neighborhood by our characterization of the fixed points of . Since is continuous and , there exists a fixed point on . Since , this must be the second fixed point .

B.2 Proof of Theorem 2

The partial derivative of with respect to is given by

where is the probability density function of a standard Gaussian. Note that for , when and when . In particular, for all , hence has no fixed point on . This means that . Similarly, for all , hence has no fixed point on and . A similar proof follows for .