Robust distortion risk measures with linear penalty

under distribution uncertainty

Abstract

The paper investigates the robust distortion risk measure with linear penalty function under distribution uncertainty. The distribution uncertainties are characterized by predetermined moment conditions or constraints on the Wasserstein distance. The optimal quantile distribution and the optimal value function are explicitly characterized. Our results partially extend the results of Bernard, Pesenti and Vanduffel (2024) and Li (2018) to robust distortion risk measures with linear penalty. In addition, we also discuss the influence of the penalty parameter on the optimal solution.

keywords:

Distortion risk measure; Distribution uncertainty; Wasserstein distance; Penalty function.1 Introduction

Traditional risk measures, such as variance, are insufficient to address extreme risks. To tackle this, distortion risk measures have been developed. By “distorting” the risk distribution and emphasizing tail risks, this approach enables more accurate assessments of potential extreme losses, especially in volatile markets. Distortion risk measures, particularly Value-at-Risk (VaR) and Conditional VaR (CVaR), are widely used in portfolio optimization and risk management. The reader can refer to seminal documents such as Yaari (1987), Wang, Young and Panjer (1997), Wang (1996) and Artzner et al. (1999), and academic textbooks Föllmer and Schied (2016).

Meanwhile, in the financial domain, investment decisions and risk management face significant distribution uncertainty due to market fluctuations, economic changes, and external shocks, particularly in parameters such as asset returns, interest rates, and exchange rates. The theory of risk measures offers a comprehensive framework for managing uncertainties and extreme risks in financial markets when integrated with robust optimization problems for portfolio optimization, risk management, and asset pricing. The relevant literature includes Esfahani and Kuhn (2018), Gao and Kleywegt (2023), Glasserman and Xu (2014), and Bartl, Drapeau and Tangpi (2020).

Owing to their distinctive mathematical properties, distortion risk measures have also been increasingly utilized in the study of distributionally robust optimization frameworks, particularly when addressing uncertainties in probability distributions. Li (2018) investigates law invariant risk measures that evaluate maximum risk is based on limited information about the underlying distribution, and provides closed-form solutions for worst-case law invariant risk measures. Furthermore, Cai, Li and Mao (2023) and Pesenti, Wang and Wang (2024) explore worst-case scenarios under distortion risk measures, where the closedness under concentration or convex hull techniques is used for the non-convex problems.

Bernard, Pesenti and Vanduffel (2024) focus on optimization problems for robust distortion risk measures under distribution uncertainty by analyzing their robustness amid parameter uncertainty and volatility. They quantify the robustness of distortion risk measures with absolutely continuous distortion functions under distributional uncertainty by evaluating the maximum (or minimum) value of the loss distribution, characterized by its mean and variance, within a domain defined around the reference distribution using the Wasserstein distance. In addition, Hu, Chen and Mao (2024) consider the robust optimization problem for the expectile risk measures, while Pesenti and Jaimungal (2023) and Blanchet, Chen and Zhou (2022) investigate robust optimization problems for the mean-variance model and active portfolio management using the Wasserstein distance.

This study introduces a penalty term for the distance between the target and reference distributions within the framework of distortion risk measures. Another motivation is from the comonotonic convex risk measures proposed by Song and Yan (2009), the present study primarily investigates the following optimization problem:

| (1.1) |

where is a distortion function, is a predetermined linear penalty function and can be chosen as distribution uncertainty sets with given moment conditions or with constraints on Wasserstein distance (see more details in section 2). By incorporating a distance-based penalty, this approach increases the emphasis on extreme losses, encouraging decision-makers to prioritize severe risks over average or likely losses.

The paper contributes to the literature in the following four aspects. First, the optimal quantile distribution and its corresponding optimal value are explicitly obtained for with concave distortion functions. Theorem 3.1 extends the results of Li (2018) by admitting the linear penalty function. In particular, when the penalty coefficient is zero, our result aligns with the findings in Li (2018). In addition, Proposition 3.1 provides a sharper estimate between the optimal quantile distribution and the reference distribution, which is very helpful to consider the optimization problem with .

Second, we completely solve the optimal quantile function and its corresponding optimal value under for different combinations of penalty coefficient and distance parameter with concave distortion functions. Given that distance and penalty coefficients are interrelated parameters, we investigate their functional relationship, discovering a one-to-one correspondence between them, which enables us to establish different boundaries for determining the optimal quantile and its optimal value in various cases.

Theorem 3.3 indicates that the agent makes a trade-off between the distortion risk measure and the penalty term, depending on the Wasserstein distance and the penalty parameter. Especially, when the penalty parameter is less than the critical value, the optimal quantile distribution is chosen on the boundary of the Wasserstein ball, not in the interior any more. This characteristic is the key ingredient between our model and the model of Bernard, Pesenti and Vanduffel (2024). When the penalty coefficient is zero, the results are consistent with the conclusions in Bernard, Pesenti and Vanduffel (2024). Some graphic analysis is also carried out for discussion about the penalty parameter and comparison with the results of Bernard, Pesenti and Vanduffel (2024) and Li (2018).

Third, we extend our analysis to the general distortion function cases. Motivated by the isotonic projection technique employed by Bernard, Pesenti and Vanduffel (2024), under some milder conditions, Theorem 4.1 and Theorem 4.2 successfully obtain the optimal quantile distributions in distribution uncertainty sets and for the general distortion function, respectively.

Finally, we apply our theoretical findings to the practical context of CVaR. We derive explicit solutions and visualize the results, illustrating the impacts of varying distances and penalty coefficients on risk measures. These visualizations provide a more precise and intuitive understanding, facilitating a better grasp of how distance and penalty coefficients influence the outcomes of risk measures.

The structure of this paper is as follows. Section 2 introduces distortion risk measures and the formulation of optimization problem. Section 3 solves the optimization problem for the distortion risk measure with penalty under distribution uncertainty in the situation of concave distortion functions. The non-concave case is discussed in Section 4. Section 5 applies the results to the model of CVaR, and Section 6 concludes the paper.

2 Model setup and problem formulation

Let be an atomless probability space. Let be the set of all square-integrable random variables. Denote for the distribution functions with finite second moment. In particular, we write for a standard uniform random variable on . For any , define its left-continuous inverse (or quantile function) as follows:

By convention, .

2.1 Distribution uncertainty

For any , recall the second order Wasserstein distance (see Villani (2009)):

We use to characterize the distance or discrepancy of two distributions, and it is determined by their corresponding quantile functions.

For any , , , we consider the following distribution uncertainty sets:

The set contains all distribution functions whose first two moments are and respectively. The set contains all distribution functions whose first two moments are and , and the distribution function is located in a Wasserstein sphere less than from the reference distribution .

For the given as a reference distribution, suppose that we know its first two moments as follows:

We can get a more explicitly expression for the Wasserstein distance, for any ,

| (2.1) |

Noting that the distance between the reference distribution function and the desired distribution function is bounded, to be specifically,

| (2.2) |

where . Therefore, if .

2.2 Problem formulation

The function is called a distortion function if it is non-decreasing and satisfies and . For some given distortion function , define a distortion risk measure by the following Choquet integral:

whenever at least one of the two integrals is finite. When is absolutely continuous, then can also be written as a spectral risk measure (Dhaene et al. (2012), Theorem 6):

| (2.3) |

where , which satisfying .

To guarantee the finiteness or non-trivial of (2.3), we impose the following assumption on the distortion function .

Assumption A1

Based on the distortion risk measure, we also require that the distance between the desired distribution and the reference distribution cannot be too far. In order to control and emphasize the distance between the desired distribution and the reference distribution, we impose a penalty on their distance based on the distortion risk measure. Our problem is to find the optimal distribution for the distortion risk measure with some penalty function under the uncertainty sets of the distribution.

More precisely, for some given and distortion function , our problems are as follows:

| (2.4) |

where is a predetermined penalty function and can be chosen as and respectively. In addition, we want to find the distribution function that achieves the best case.

In order to make our problem more solvable, this paper focuses on the linear penalty function. The other types of penalty functions are left for future study.

Assumption A2

The penalty function , , where penalty parameter .

Remark 2.1

Remark 2.2

From the point of view of the risk measure, another motivation for the study of the distortion risk measure with penalty function is the comonotonic convex risk measures proposed by Song and Yan (2009). This kind of risk measures are also studied by Xia (2013), Tian and Jiang (2015) and Han et al. (2025).

We end this section with some notations, which are used later.

| (2.5) |

3 Main results

This section solves the optimization problem (2.4) with the concave distortion function. The situation of non-concave distortion function will be discussed in Section 4. Subsection 3.1 gives the solution for , and subsection 3.2 presents the solution for and depicts some figures for discussions.

3.1

The following theorem provides the optimal distribution result of problem (2.4) for . The result extends Theorem 2 in Li (2018) to admit the linear penalty function.

Theorem 3.1

Proof. For any , recalling , one can obtain that

| (3.2) |

where the third equality is derived from the facts that , and , respectively.

Using equations (2.1), (2.3) and (3.1), by directly calculations, then the objective function of problem (2.4) can be reduced to

From the above, one recognizes that if , then the objective function can obtain the maximum value. In other words, when is completely positive correlated with , taking account of the first two moment constraints, then the optimal value can be obtained by choosing the distribution with quantile function

where , .

Therefore, with the expression above for , the corresponding optimal value is

The proof is complete.

Remark 3.1

Theorem 3.1 indicates that the penalty parameter significantly affects the value function, while structure of the optimal solution does not change much. In particular, when there is no penalty function (), the result of Theorem 3.1 reduces to the Theorem 2 in Li (2018).

Corollary 3.1

Theorem 3.1 gives the quantile formulation of the optimal distribution among in . The next proposition investigates the boundedness of the distance between this optimal distribution and the reference distribution, which is more sharper than (2.2) under the situation of concave distortion function. Besides, this distance is very useful when we consider the problem (2.4) with .

Proposition 3.1

Proof. For any , from the definition of quantile function for distribution , obviously, . Next, we show that is uniformly bounded with respect to .

Indeed, for any given ,

For the term of correlation function, for all , define

| (3.5) |

One can verify that is (strictly, when ) increasing with respect to on . Then, we can find that

Therefore, we get the upper bound and lower bound, respectively.

3.2

The distance between the required distribution and the known reference distribution should not be too large. Therefore, this subsection will consider with a given penalty function.

Firstly, applying the results of Proposition 3.1 and Theorem 3.1, we can easily get the following theorem.

Theorem 3.2

Let be a concave distortion function and . Suppose A1 and A2 hold. For the problem (2.4), then we have the following situations.

-

(i)

Case of . In this case, and the problem is meaningless.

-

(ii)

Case of . Then contains only one element, and the optimal quantile expression of is

The corresponding optimal value function is

-

(iii)

Case of . The problem reduces to Theorem 3.1.

Proof. By (2.2), we know that the results of case (i) is obvious.

For the case (ii), when , then contains only one element with . Taking account of the moment constraints, should have the quantile expression as follows:

The optimal value is

For the case (iii), by Proposition 3.1, we find that the optimal solution , defined by (3.1) in Theorem 3.1, lies in since . Hence, when , the following two problems are equivalent:

Therefore, the problem reduces to Theorem 3.1. The proof is complete.

The following technical lemma provides the existence of a distribution with a specific structure in for the given Wasserstein distance. It is derived from the further discussion and analysis of Proposition 3.1, which will play a key role for Theorem 3.3.

Lemma 3.1

Proof. For any , for and defined by (3.3), we will choose by setting

By virtue of the definition of function by (3.5) in Proposition 3.1 and the fact that is strictly increasing with respect to on . Therefore, there exists a unique such that

| (3.7) |

By direct calculations, one can solve and get

It completes the proof.

Remark 3.2

Now we will give the main theorem of this subsection.

Theorem 3.3

Proof. For each , by Lemma 3.1, we can find determined by (3.6) with . Moreover, one can derive that

| (3.10) |

on . It implies that is strictly decreasing, then when the penalty function coefficient is fixed, there exists a similarly optimal distance .

Case (i): For any , choosing by (3.8), it implies that

| (3.11) |

From Theorem 3.1, we know that

By virtue of the fact that , then we have that

Therefore, this case is exactly the same as Theorem 3.1.

Case (ii): When , from the proof procedure and analysis in case (i), we know that in this case the optimal distribution can not be in (3.8) any more, since

resulting in .

When , we claim that

| (3.12) |

Step 1: We will show that for any given distance less than , the form of (3.8) is optimal.

Indeed, for any given and , then by Lemma 3.1, there exists a unique and . On the other hand, for any such that , we obviously have that

From the Cauchy-Schwarz inequality, it implies that

Therefore, makes the objective function greater than for the same distance, that is, for any with , then one has

In other words, for any and , we have that

Step 2: We show that for any and , is more optimized than , i.e., (3.12) holds. Here, and are determined by (3.6), respectively.

By the one-to-one corresponding relationship between and , then showing (3.12) is equivalent to verify the following fact

| (3.13) |

Specifically, for any , we can transform the form of the objective function

| (3.14) |

where

| (3.15) |

Here . The last equality is from the fact that and the formulation of .

By directly calculations, one can derive that

It implies that the objective function is monotonically decreasing with respect to .

Furthermore, we can obtain the optimal value of the objective function at .

By carefully verifications, we can also get

The proof is complete.

The results of Theorem 3.3 are attractive and fascinating. It indicates that the agent makes a trade-off between the distortion risk measure and the penalty term, depending on the Wasserstein distance and the penalty parameter . This feature is the key ingredient between our model and the model of Bernard, Pesenti and Vanduffel (2024).

More precisely, when the penalty parameter is large enough with or the penalty term is dominant, then the agent chooses the optimal distribution such that

In contrast, when the penalty parameter is strictly less than , then the agent selects the optimal distribution such that

Remark 3.3

When , then the result of Theorem 3.3 reduces to Theorem 3.1 in Bernard, Pesenti and Vanduffel (2024). Theorem 3.3 shows that the relationship between the penalty parameter and the Wasserstein distance plays a key role in determining the optimal (quantile) distribution.

Our analysis reveals that the optimal control strategy proposed in Bernard, Pesenti and Vanduffel (2024) ceases to be admissible when the penalty parameter falls below a critical threshold , particularly when the penalty term is incorporated into the objective functional. This result is exciting, and it also illustrates the non-trivial nature of the study of results with penalty term.

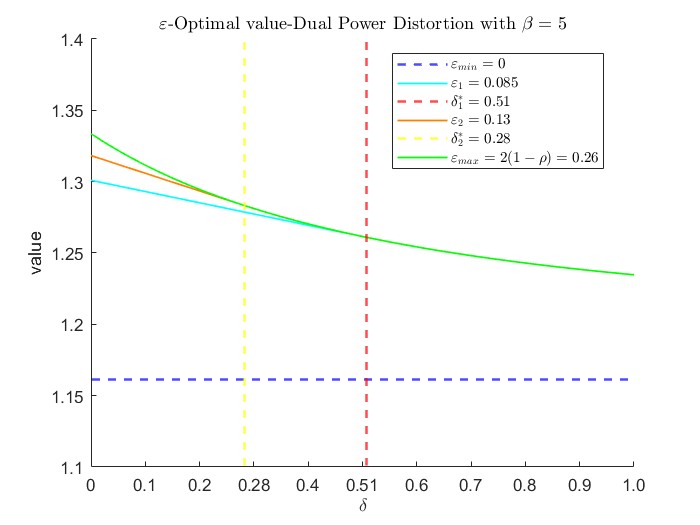

We end this subsection with some graphic discussion. In order to compare with the results of Bernard, Pesenti and Vanduffel (2024), we choose the reference distribution as the standard normal distribution with and , and the dual power distortion function with parameter .

In Figure 1(a), we examine how the optimal value changes with respect to the penalty parameter for different values of . The light blue () and orange curves () correspond to two different distances, with the corresponding critical threshold parameters (red dashed line) and (yellow dashed line), respectively. The green curve represents the case when the distance reaches the maximum value , which reflects the result of Theorem 3.2 (iii). It is clear that as the penalty coefficient increases, the resulting optimal value gradually decreases. This indicates that as the decision-maker’s risk aversion (i.e., the penalty coefficient) increases, they select a higher optimal penalty coefficient, leading to a more conservative result. However, when the penalty coefficient becomes too large, the optimal distance gradually converges to the lower bound, consistent with the result of Theorem 3.2 (ii). Thus, as the penalty coefficient continues to increase, the optimal value stabilizes and eventually approaches (blue dashed line), which represents the minimum tolerable distance.

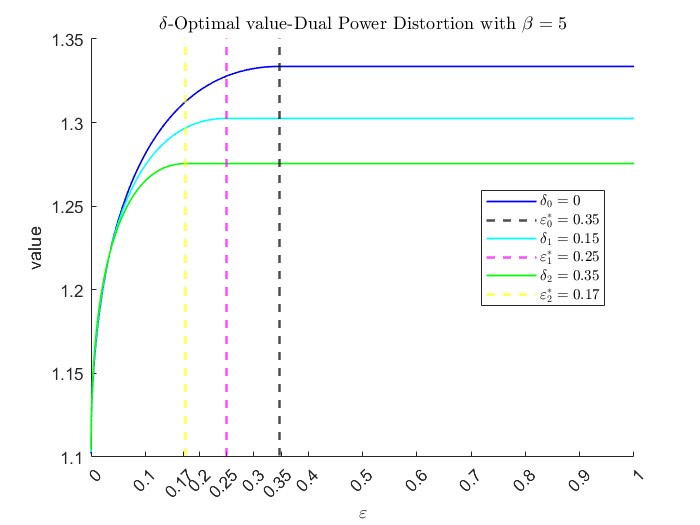

In Figure 1(b), we examine how the optimal value changes with respect to for different values of . The blue curve represents the case when , where the corresponding optimal distance is (black dashed line), which is consistent with the results from Li (2018). The light blue and green curves correspond to two different values of , (light blue) and (green), with corresponding optimal distances of (pink dashed line) and (yellow dashed line), respectively. From the figure, it can be observed that as the value of the penalty function increases, the optimal distance decreases. This phenomenon suggests that as the decision-maker’s risk aversion (i.e., the penalty function) becomes stronger, their tolerance for deviations in the distribution decreases, meaning they become more sensitive to deviations in risk.

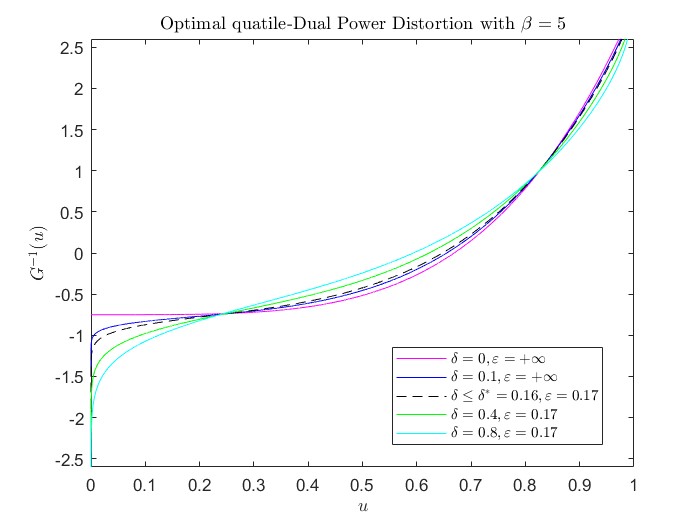

In Figure 2, we examine the impact of the presence or absence of a penalty term on the optimal quantile when there are no restrictions on the distance. The pink curve represents the results from Li (2018), and the blue curve represents the results from Theorem 3.1. Further, we investigate the effect of different penalty coefficients on the optimal quantile when there are distance restrictions. The black dashed line corresponds to Theorem 3.3 (ii), and encompasses the first case of Theorem 3.1 of Bernard, Pesenti and Vanduffel (2024), while the light blue and green curves correspond to Theorem 3.3 (i). In this figure, we analyze how the penalty term affects the selection of the optimal quantile. Specifically, when there are no distance restrictions, the optimal quantile is minimally influenced by the penalty term. However, when distance restrictions are introduced, the size of the penalty coefficient directly impacts the optimal quantile. Through the application of different theorems, we can observe how the optimal quantile changes under varying penalty coefficient conditions.

4 The general case

In the previous section, we only consider the cases where the distortion function is concave. Motivated by Bernard, Pesenti and Vanduffel (2024), this section will consider the general distortion function , which is no longer a concave function. The isotonic projection technique also works well when the penalty function appears in the objective function. The readers can also refer to Pesenti, Wang and Wang (2024), where an envelope method is used to solve the non-concave case.

4.1 General distortion function case:

Define the space of square-integrable, non-decreasing, and left-continuous functions on as follows:

When is not concave, then the term is not necessarily increasing, and thereby defined in (3.1) maybe not a quantile function any more. The following definition of isotonic projection can solve this problem. The readers can refer to Appendix A in Bernard, Pesenti and Vanduffel (2024) for more details and properties of isotonic projections.

Definition 4.1

(Isotonic projection) For , define as to an isotonic projection on a square-integrable, non-increasing, left-continuous function space on , i.e

where denotes the norm on the space.

Theorem 4.1

Proof. For any , by directly calculations, then the objective function of problem (2.4) can be reduced to

| (4.2) |

Firstly, it is obvious that , where is defined by (4.1). Then by Lemma B.4 of Bernard, Pesenti and Vanduffel (2024), we know that

| (4.3) |

Coming back to (4.2), one recognizes that is the optimal quantile function.

Noting that , we can easily get for all . Furthermore, the corresponding optimal value is

By the basic properties of the isotonic projection (see Proposition A.3, Bernard, Pesenti and Vanduffel (2024)), we have and . Hence, it implies that

Therefore, the optimal value for is

The proof is complete.

Theorem 4.1 is a general characterization of the optimal quantile under the penalty term situation. It is a natural generalization of Theorem 2 in Li (2018) and our Theorem 3.1.

Similarly, we introduce the following notations:

| (4.4) |

In the sequel, we investigate the distance between and . We add a technical condition for this purpose.

Assumption A3

Given the reference distribution and a distortion function , and suppose and the following two conditions hold:

-

(a)

For any , is strictly increasing with on , and

-

(b)

For any , is decreasing with respect to on .

4.2 General distortion function case:

Applying the estimation (4.5), for the general distortion function and , under Assumptions A1-A3, then the results of Theorem 3.2 also hold similarly. Specifically, when , then the problem (2.4) has no solution; when , then the optimal quantile for problem (2.4) is still

when , then the solution to problem (2.4) is the same as in Theorem 4.1.

The following Theorem 4.2 extends the results of Theorem 3.3 to the general distortion function and also includes the results of Theorem 3.7 in Bernard, Pesenti and Vanduffel (2024) by incorporating the penalty function.

Theorem 4.2

Proof. Similar to Lemma 3.1, for each , we can find by setting . From the directly calculation, then we have

| (4.7) |

By the continuity of the isotonic projection and and Assumption A3(a), then there exists a unique such that equation (4.7) holds. From equation (4.7) we can see that there is a one-to-one corresponding between and , and is inversely proportional to .

Conversely, for any , then there exists a unique such that

Case (i): for any , choosing by (4.1), it implies that

| (4.8) |

According to Theorem 3.1, the objective function can also be written as

and (by Lemma B.4 of Bernard, Pesenti and Vanduffel (2024)) we also have

Therefore, we know that

By virtue of the fact that , then we have that

Moreover, the optimal value of is .

Case (ii): this proof procedure is similar to Theorem 3.3. When , from the proof procedure and analysis of case (i), we know that in this case the optimal distribution can not be in (3.8) any more, since , which means .

Firstly, we claim that for any and , we have that

| (4.9) |

where since .

In fact, for any given and , since , and the fact that for any with , we have that

Therefore, makes the objective function greater than for the same distance, that is, for any with , then one has

which is exactly (4.9).

Secondly, for any and , we show that

| (4.10) |

where since .

Specifically, for any , we can transform the form of the objective function as

where . Moreover, one has

then by the Assumption A3(b), it implies that is decreasing in .

Furthermore, we can obtain the optimal value of the objective function at .

where is the projection of , and .

Theorem 4.2 shows that when the penalty term is involved, there exist similar characterizations of Theorem 3.3 under the general distortion function.

The following corollary is almost obvious. The proof is omitted.

5 An illustrate example of CVaR

In this section, we apply our results to one widely used risk measure, called Conditional Value at Risk (CVaR). We briefly introduce these as follows. The readers can refer to Acerbi (2002) and Föllmer and Schied (2016) for more details.

For any given , Value at Risk (VaR) is defined as

and its corresponding distortion function is Conditional Value at Risk (CVaR) (also called Expected Shortfall (ES)) is denoted by

where the corresponding distortion function is and the derivative of the distortion function is .

The following proposition establishes the optimal quantiles and optimal values for CVaR.

Proposition 5.1

For , and , we have the optimal penalty coefficient as , where satisfies

-

(i)

When , the value of CVaR with penalty under distribution uncertainty is

and the optimal quantile function is

where

-

(ii)

When , the value of CVaR with penalty under distribution uncertainty is

and the optimal quantile function is

where

Proof. When , since the derivative function of distortion function for CVaR is , , which is non-decreasing, applying Theorem 3.1, then we have

where

Then the optimal quantile of CVaR is

When , we apply Lemma 3.1, and we obtain

then we have the optimal penalty coefficient as , where satisfies

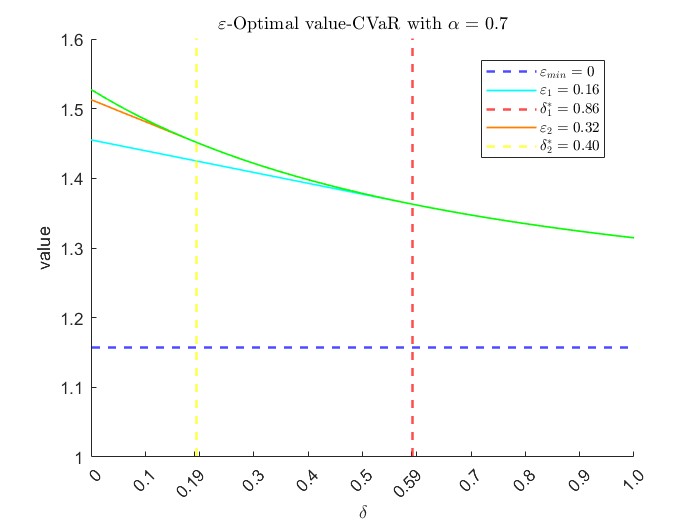

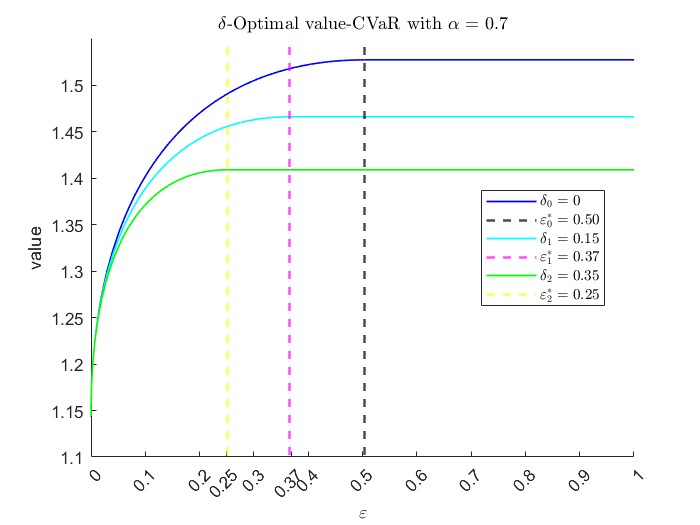

Finally, we do some numerical analysis for the situation of CVaR. We choose the reference distribution as the standard normal distribution and let , and . Figure 3 (a) reflects how the optimal value changes with respect to for different values of . The light blue and orange curves correspond to two different values of , (light blue) and (orange), with (red dashed line) and (yellow dashed line), respectively. The green curve represents the case when the distance reaches the maximum value .

Figure 3 (b) displays how the optimal value changes with respect to for different values of . The blue curve represents the case when , where the corresponding optimal distance is (black dashed line). The light blue and green curves correspond to two different values of , (light blue) and (green), with corresponding optimal distances of (pink dashed line) and (yellow dashed line), respectively.

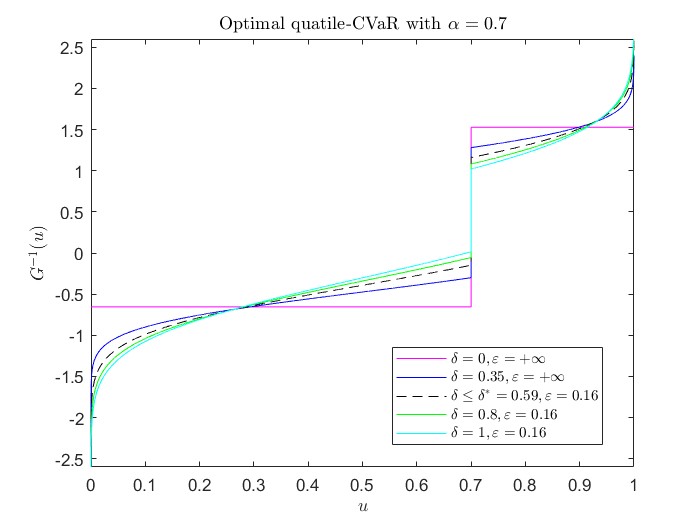

Figure 4 shows the impact of the presence or absence of a penalty term on the optimal quantile when there are no restrictions on distance. The pink curve shows the result of Li (2018), and the blue curve represents the results from Theorem 3.1. Further, we study the effect of different penalty coefficients on the optimal quantile. The black dashed line corresponds to Theorem 3.3 (ii), and includes the first case of Theorem 3.1 in Bernard, Pesenti and Vanduffel (2024), while the light blue and green curves correspond to Theorem 3.3 (i).

6 Conclusions

In this paper, we focus on studying the distortion risk measure with a linear penalty function under distributional uncertainty. This modification allows us to deeply explore the impact of the Wasserstein distance and the penalty parameter together, which reveals that the agent makes a trade-off between the distortion risk measure and the penalty term. This characteristic is the key ingredient between our model and the models of Bernard, Pesenti and Vanduffel (2024) and Li (2018). Our findings extend the corresponding results presented in Bernard, Pesenti and Vanduffel (2024) and Li (2018), notably adding the need for penalty terms in the framework of robust distortion risk measures.

Acknowledgments

The authors thank the grant supported by the Fundamental Research Funds for the Central Universities (No. 2024KYJD2008).

References

- Acerbi (2002) Acerbi, C. (2002). Spectral measures of risk: A coherent representation of subjective risk aversion. Journal of Banking and Finance, 26(7), 1505-1518.

- Artzner et al. (1999) Artzner, P., Delbaen, F., Eber, J. M., & Heath, D. (1999). Coherent measures of risk. Mathematical finance, 9(3), 203-228.

- Bartl, Drapeau and Tangpi (2020) Bartl, D., Drapeau, S., & Tangpi, L. (2020). Computational aspects of robust optimized certainty equivalents and option pricing. Mathematical Finance, 30(1), 287–309.

- Bernard, Pesenti and Vanduffel (2024) Bernard, C., Pesenti, S. M., & Vanduffel, S. (2024). Robust distortion risk measures. Mathematical Finance, 34(3), 774-818.

- Blanchet, Chen and Zhou (2022) Blanchet, J., Chen, L., & Zhou, X. Y. (2022). Distributionally robust mean-variance portfolio selection with Wasserstein distances. Management Science, 68(9), 6382-6410.

- Cai, Li and Mao (2023) Cai, J., Li, J.M., & Mao, T. (2023). Distributionally robust optimization under distorted expectations. Operations Research, online, https://doi.org/10.1287/opre.2020.0685.

- Dhaene et al. (2012) Dhaene, J., Kukush, A., Linders, D., & Tang, Q. (2012). Remarks on quantiles and distortion risk measures. European Actuarial Journal, 2, 319-328.

- Esfahani and Kuhn (2018) Esfahani, P. M., & Kuhn, D. (2018). Data-driven distributionally robust optimization using the Wasserstein metric: Performance guarantees and tractable reformulations. Mathematical Programming, 171(1-2), 115–166.

- Föllmer and Schied (2002) Föllmer, H., & Schied, A. (2002). Convex measures of risk and trading constraints. Finance and stochastics, 6, 429-447.

- Föllmer and Schied (2016) Föllmer, H., & Schied, A. (2016). Stochastic Finance: an Introduction in Discrete Time. 4th. Walter de Gruyter.

- Gao and Kleywegt (2023) Gao, R., & Kleywegt, A. (2023). Distributionally robust stochastic optimization with Wasserstein distance. Mathematics of Operations Research, 48(2), 603-655.

- Glasserman and Xu (2014) Glasserman, P., & Xu, X. (2014). Robust risk measurement and model risk. Quantitative Finance, 14(1), 29-58.

- Han et al. (2025) Han, X., Wang, Q., Wang, R., & Xia, J. (2025). Cash-subadditive risk measures without quasi-convexity. To appear at Mathematics of Operations Research. arXiv:2110.12198v6,

- Hu, Chen and Mao (2024) Hu, Y., Chen, Y., & Mao, T. (2024). An extreme worst-case risk measure by expectile. Advances in Applied Probability, 56(4), 1195-1214.

- Li (2018) Li, J.M. (2018). Closed-form solutions for worst-case law invariant risk measures with application to robust portfolio optimization. Operations Research, 66(6), 1533-1541.

- Pesenti and Jaimungal (2023) Pesenti, S.M., & Jaimungal, S. (2023). Portfolio optimization within a Wasserstein ball. SIAM Journal on Financial Mathematics, 14(4), 1175-1214.

- Pesenti, Wang and Wang (2024) Pesenti, S. M., Wang, Q., & Wang, R. (2024). Optimizing distortion riskmetrics with distributional uncertainty. Mathematical Programming, online, https://doi.org/10.1007/s10107-024-02128-6.

- Song and Yan (2009) Song, Y., & Yan, J. A. (2009). Risk measures with comonotonic subadditivity or convexity and respecting stochastic orders. Insurance: Mathematics and Economics, 45(3), 459-465.

- Tian and Jiang (2015) Tian, D., & Jiang, L. (2015). Quasiconvex risk statistics with scenario analysis. Mathematics and Financial Economics, 9, 111-121.

- Villani (2009) Villani, C. (2009). Optimal transport: old and new (Vol. 338, p. 23). Berlin: Springer.

- Wang (1996) Wang, S. (1996). Premium calculation by transforming the layer premium density. ASTIN Bulletin, 26(1), 71–92.

- Wang, Young and Panjer (1997) Wang, S., Young, V.R., & Panjer, H.H. (1997). Axiomatic characterization of insurance prices. Insurance: Mathematics and Economics, 21(2), 173-183.

- Yaari (1987) Yaari, M.E. (1987). The dual theory of choice under risk. Econometrica, 55, 95-115.

- Xia (2013) Xia, J. (2013). Comonotonic convex preferences. Available at SSRN 2298884.