Randomized Quasi-Monte Carlo with Importance Sampling for Functions under Generalized Growth Conditions and Its Applications in Finance

Abstract

Many problems can be formulated as high-dimensional integrals of discontinuous functions that often exhibit significant growth, challenging the error analysis of randomized quasi-Monte Carlo (RQMC) methods. This paper studies RQMC methods for functions with generalized exponential growth conditions, with a special focus on financial derivative pricing. The main contribution of this work is threefold. First, by combining RQMC and importance sampling (IS) techniques, we derive a new error bound for a class of integrands with the critical growth condition where . This theory extends existing results in the literature, which are limited to the case , and we demonstrate that by imposing a light-tail condition on the proposal distribution in the IS, the RQMC method can maintain its high-efficiency convergence rate even in this critical growth scenario. Second, we verify that the Gaussian proposals used in Optimal Drift Importance Sampling (ODIS) satisfy the required light-tail condition, providing rigorous theoretical guarantees for RQMC-ODIS in critical growth scenarios. Third, for discontinuous integrands from finance, we combine the preintegration technique with RQMC-IS. We prove that this integrand after preintegration preserves the exponential growth condition. This ensures that the preintegrated discontinuous functions can be seamlessly incorporated into our RQMC-IS convergence framework. Finally, numerical results validate our theory, showing that the proposed method is effective in handling these problems with discontinuous payoffs, successfully achieving the expected convergence rates.

Key words. Importance sampling, Quasi-Monte Carlo, Growth condition, Preintegration

1 Introduction

Computational finance often faces the challenge of high-dimensional numerical integration, especially in areas such as option pricing, risk measurement, and derivative valuation. A common problem involves estimating expectations of the form , where is a -dimensional standard normal random vector, and represents a payoff [9]. In many practical scenarios, may exhibit discontinuities or require evaluation over unbounded domains. The Monte Carlo (MC) method offers a flexible and widely used approach for such high-dimensional problems, but it suffers from a relatively slow theoretical convergence rate of , which can limit its efficiency when high precision is required.

Quasi-Monte Carlo (QMC) [3, 4, 5, 6, 19, 24], utilizing low-discrepancy point sets in , provide a promising alternative. These sequences are designed to fill the unit cube more uniformly than random points, leading to superior empirical performance and a theoretically faster convergence rate, potentially approaching for sufficiently smooth integrands [23]. Randomized Quasi-Monte Carlo (RQMC) methods combine the deterministic sampling of QMC with randomization. RQMC methods combine the accuracy of QMC with the error estimation advantages of MC. Common randomization methods include random shift and scramble [22]. The standard approach transforms the problem into the unit cube

| (1) |

and QMC(RQMC) estimator is

However, the effectiveness of QMC(RQMC) depends on the smoothness and boundedness of the integrand . Two major challenges arise: (1) the function arising in finance often contains discontinuities, which violate the smoothness conditions needed for QMC(RQMC); (2) even when is smooth, the integrand in 1 is actually , where denotes the cumulative distribution function of standard normal distribution . The transformation can introduce singularities or rapid growth near the boundary of the unit cube, while functions like become unbounded in Euclidean space, complicating theoretical analysis.

To overcome these significant hurdles, researchers have developed sophisticated techniques such as preintegration for smoothing discontinuous functions. For discontinuous integrands, preprocessing techniques like the preintegration [11, 12, 13, 14], which is also called conditional Monte Carlo method[8], offer a path to smoothness. This method involves integrating out one variable (say ) conditioned on the others (), defining a smoothed conditional expectation . For , under suitable monotonicity and smoothness assumptions on the discontinuity boundary and the continuous part , He [15] demonstrated that can inherit significant smoothness from and .

Importance Sampling (IS) [7, 10, 16, 21, 27] is a variance reduction method in MC. IS introduces a proposal density to rewrite the expectation:

where , and QMC(RQMC)-IS estimator is Here is the standard normal density, and maps uniform points to follow . A popular choice for proposal in finance, is Optimal Drift Importance Sampling (ODIS), which selects a proposal from the family of shifted normal densities by optimizing with . While effective in practice for variance reduction, the theoretical application of Randomized QMC (RQMC) with IS has faced limitations. Recent work by Ouyang et al. [20] established convergence rates for RQMC-IS under the condition that belongs to a function class satisfying a growth condition with and .

Critically, as highlighted in section 2 of this paper, an example arising in ODIS for constant violates this key condition, since its derivatives grow too rapidly to be bounded by (cannot even bounded by ).

This paper bridges this theoretical gap. We first extend the convergence theory for RQMC-IS to a more generalized growth condition of the form , accommodating the critical case. Specifically, we show that ODIS satisfies the conditions of our theorem. Building on this, we present and prove a theorem demonstrating that functions after preintegration also satisfy our growth condition. We thus establish that our results are applicable to problems in finance.

More specifically, our first key contribution is a generalized convergence theory for RQMC-IS. We define a broader growth condition of the form for , which enables us to prove convergence rates for the RQMC-IS estimator . For , we recover the near rate under a mild condition (i) on the proposal . Crucially, for the critical case , we prove a convergence rate under a light-tail condition (ii) on , circumventing the barrier of previous work and enabling theoretical analysis of ODIS. Second, we demonstrate the applicability of our theory to ODIS. We formally show that the Gaussian proposals used in ODIS satisfy the required light-tail condition (see proposition 7). Finally, we prove that functions after preintegration satisfy our growth condition. We analyze the preintegration operator applied to discontinuous functions of the form . Building on He’s results [15], we show that if the original components and satisfy exponential growth conditions, the smoothed function also satisfies our generalized exponential growth condition (theorem 11). This enables the application of our RQMC-IS convergence theory to preintegrated functions, providing a complete theoretical framework for handling discontinuous payoffs using a combination of preintegration, IS (like ODIS), and RQMC.

The remainder of this paper is organized as follows. section 2 reviews importance sampling and the limitations of the existing RQMC convergence theory, particularly with regard to ODIS. section 3 presents our main convergence results for RQMC-IS under generalized growth conditions and demonstrates the applicability of these results to ODIS. section 4 details the preintegration technique and proves that it preserves exponential growth rates under suitable assumptions. section 5 applies our theory to option pricing problems and presents our numerical results. section 6 concludes and discusses future research directions and proofs of supporting lemmas are provided in appendix A.

2 Preliminary and Previous Work

2.1 Importance Sampling

Many problems in financial engineering can be reduced to calculating an integral of the form , where is a standard normal random vector. The problems can be transformed into an integral over the unit cube, i.e.,

| (2) |

where is the cumulative distribution function (CDF) of , is the inverse of acting on component-wise. To estimate it, RQMC quadrature rule of the following form can be used

| (3) |

where is a randomized low discrepancy point set in .

Importance sampling methods reduce variance in MC methods by choosing a suitable importance density. Formally, let be the density of the standard normal distribution and be another density. Then we can rewrite as

| (4) |

where and follows the distribution corresponding to density . Let be the generator corresponding to , that is, follows the distribution corresponding to density when follows the uniform distribution on . Then the importance sampling estimator is

| (5) |

How to choose the proposal? Note that the original density is the standard normal distribution . Therefore, a method called Optimal Drift Importance Sampling (ODIS) considers choosing the proposal from the normal distribution family . Formally, denote the support set of as , then the density of the proposal is given by

| (6) |

where

2.2 Convergence rate of importance sampling for RQMC methods

For convenience, we specify some derivative notations. Denote and . For , denotes the derivative taken with respect to each once for all . For any multi-index whose components are nonnegative integers,

where . If for all and otherwise, then .

Definition 1.

A function defined over is called a smooth function if for any , is continuous. Let be the class of such smooth functions.

Recently, Ouyang et al. [20] defined the growth condition for the function in and demonstrated the following theorem by a projection method for this function class.

Proposition 2.

Let be a RQMC point set used in the estimator given by 3 such that each and

where is a constant independent of . For any function , if satisfies that

| (7) |

with , then we have

where the constant in depends on and .

Proof.

See the proof of Corollary 4.8 in [20]. ∎

Moreover, this projection method can be applied to IS. Suppose that in 4 has the form

| (8) |

and let be the cumulative distribution function (CDF) of . Denote . In [20], Ouyang et al. proved following theorem for IS based RQMC method.

Proposition 3.

Assume . If satisfies the conditions in proposition 2. For any function in , if the proposal satisfies that and

| (9) |

then we have

| (10) |

where the constant in depends on and .

Proof.

See the proof of Corollary 5.6 in [20]. ∎

However, this proposition is not applicable to the ODIS. For instance, when applying ODIS with the constant function , the optimal proposal distribution reduces to the original standard normal distribution . In this case, the function subject to the growth condition becomes

| (11) |

which exhibits an exponential growth rate with and . This violates the condition required by proposition 3.

Furthermore, even a theorem that accommodates the case would be insufficient if it relies on the same form of growth condition. The condition in 9 must hold for the function and its derivatives. The derivative of contains a term , which grows faster than and cannot be bounded by it. This highlights a fundamental limitation of the existing theoretical framework in handling ODIS.

This limitation persists even when optimizing , since the fundamental growth rate remains unchanged. Consequently, the RQMC-IS convergence rate cannot be guaranteed under ODIS for this scenario, revealing the method’s inherent sensitivity to the growth parameter in its theoretical framework.

3 RQMC-IS Convergence under a Generalized Growth Condition

To address the theoretical limitations discussed in the previous section, we now develop a new convergence theory for RQMC-IS. Our framework is built upon a more general growth condition that accommodates the critical case where the integrand exhibits growth proportional to .

We consider the case where and define a growth condition on the function . We assume there exist constants such that for all ,

| (12) |

To present our results, we introduce two possible conditions on the proposal density as follows.

-

(i)

The proposal has a finite second moment, i.e., .

-

(ii)

Light-Tail Condition: The proposal has tails that decay sufficiently fast. Specifically, for the case , there exist constants and such that for any ,

Now we present our main convergence results for the RQMC based IS estimator.

Theorem 4.

Before we present the formal proof of theorem 4, we introduce two key lemmas. The proofs of these lemmas are deferred to the Appendix to maintain the flow of the main argument.

Lemma 5.

Lemma 6.

If satisfies there exists such that

and satisfies the condition (ii), then for any , we have

where constant is independent of .

Proof of Theorem 4.

(a) For the case , We just need to note that we can choose an small enough such that and . Then there exists a constant for which This satisfies the condition of proposition 3 with . Given that condition (i) () holds, the claimed error rate of follows directly by proposition 3.

(b) For the case , we use the projection operator in [20]. First, we have,

By the Cauchy inequality,

And we have

By the Koksma-Hlawka inequality,

Thus we conclude that

Using lemma 5 and lemma 6, we can bound these two terms. For the first term, we have by lemma 6. For the second term, we obtain that for some constant by lemma 5. Thus we have

For different , we set

With this choice of , the first term becomes

The second term becomes

Since , the exponential factor grows slower than any polynomial in , but faster than any polylogarithmic term. Therefore, the second term dominates the error. The overall error is determined by the asymptotic behavior of , which gives the rate as stated in the theorem. ∎

Having established our main convergence results, we now demonstrate their applicability to the ODIS method introduced in the previous section.

Proposition 7.

Proof.

See the proof of Appendix A.3. ∎

4 The Applications in Finance Via Preintegration

In this section, we focus on discontinuous integrands of the following form

| (15) |

where , are smooth functions of all variables.In option pricing, the payoff funtions can usually be written in this form. It is now clear that is not a smooth function. To apply the results from the previous sections on RQMC and IS, we need to smooth integrand . To achieve this, we introduce the preintegration approach.

Denote as the components of apart from . Integrating (15) with respect to (i.e., taking as the conditioning variables) gives

where denotes the function obtained by taking the preintegration of , and is a p.d.f..

Next, we study the smoothness and growth rates of . To derive the desired results, we rely on the assumptions and conclusions established in [14, 15]. Firstly,we need is strictly monotonous with respect to .

Assumption 8.

Let be fixed. Assume that

Under the assumptions above, we can establish the following theorem, which provides conclusions about both the smoothness of and its growth rate near the boundary.

Theorem 9.

Let be a positive integer. Suppose that is given by (15) with and , , and Assumption 8 is satisfied. Denote . Let

Then is open, and there exists a unique function such that for all . Assume that the following two condition is satisfied.

-

(A)

For any , there exists a ball with such that converges uniformly on for any multi-index satisfying and (see Definition3.3 in [15] ).

-

(B)

Every function over of the form

(16) where is a constant, are integers, and are multi-indices with the constraints , , , , satisfies

(17)

Then , and for every multi-index with and ,

| (18) |

where is a nonnegative integer depending only on , and for and , has the form (16) with parameters satisfying , , , , otherwise .

Proof.

See the proof of Theorem 3.2 and 3.4 in [15]. ∎

Assumption 10.

Suppose that the integers and are fixed. There exist constants such that

| (19) |

hold for and any multi-index satisfying .

Remark 1.

This assumption is quite natural in financial engineering. Under the Black–Scholes model, option payoff functions can typically be written in the form given in equation (15), where terms and can be written as a function of , where . As a result, this condition is usually easy to satisfy. Furthermore, the growth condition is relatively simple to verify, especially when compared to Assumption 4.5 in [15], which is often difficult to check in practice.

In this paper, we consider the case where the density function is standard normal, i.e., . Based on the growth condition assumed above, we can then establish the following theorem, which provides an upper bound on the growth of the function after preintegration with respect to the th component.

Theorem 11.

Proof.

Firstly, the assumption 10 ensures that . In what follows, we just need to prove that conditions (A) and (B) in Theorem 9 are satisfied, then we can get the existence and growth condition of.

Now we verify condition (A). Let be an arbitrary point in . For any , from (19), we have

where is a constant depending on . Together with

Weierstrass test (see Theorem 3.5 in [15]) admits that converges uniformly on . So condition (A) in Theorem 9 is satisfied.

We next verify condition (B). For the function given by (16), by Assumption 10, we find that

| (21) |

where

Then as . To verify condition (B), it suffices to show that goes to infinity as approaches a boundary point of lying in and . Without loss of generality, we suppose that in Assumption 8. This implies that is an increasing function with respect to for given . We then have

As a result, as approaches a boundary point of lying in . Also,

Similarly, as approaches a boundary point of lying in . Applying Theorem 9 gives .

After imposing Assumption 8 and Assumption 10 on the discontinuous functions in finance of the form given in 15, we derive an upper bound for the growth of the preintegrated function. Consequently, we can apply the RQMC-ODIS convergence order obtained in the previous section to arrive at the following Theorem.

Corollary 12.

5 Numerical Experiments

In this section, we perform some numerical examples on pricing financial options whose payoff function has the form (15) under either the Black-Scholes model or the Heston model. In ou rexperiments, the RQMC we use is a linear-scrambled version of Sobol’points proposed by [18]. We use the ODIS proposal in all the following numerical experiments.

5.1 Black-Sholes Model

Let denote the underlying price dynamics at time under the risk-neutral measure. Denote . Under the Black-Sholes model, assume that an underlying asset price follows a geometric Brownian motion satisfying the stochastic differential equation

| (24) |

where is the risk free interest rate, is the volatility and is the standard Brownian motion. Under this framework, the solution of (24) is analytically available

| (25) |

where is the initial price of the asset. Suppose that the maturity time of the option is T. In practice, we simulate a discrete Brownian motion. Without loss of generality, we assume that the discrete time satisfies , where . And then denote . Let . We have , where is a positive definite matrix with entries .

Let be a matrix satisfying . Using the transformation , where , it follows from (25) that

| (26) |

5.1.1 Single Asset

In the single-asset case, the first step is to choose a generating matrix . There are several methods for selecting , with Cholesky decomposition being the most commonly used. Two alternative approaches principal component analysis (PCA) [2] and gradient PCA (CPCA) [25] are often used in combination with QMC methods to reduce the effective dimension.

We consider the arithmetic Asian option, whose payoff function is given by

| (27) |

where is the strike price, and . Regardless of the generation method chosen, it can be verified that Assumption 8 is satisfied [15], and obviously, (27) satisfies Assumption 10. Next, we provide the analytically expression for the preintegration of the payoff function with respect to . The derivation is presented in [26].

Denote , and is a matrix satisfying with

Then we have

| (28) |

where

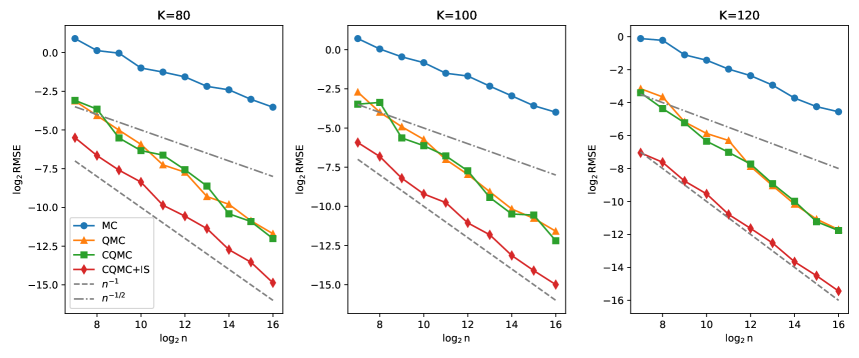

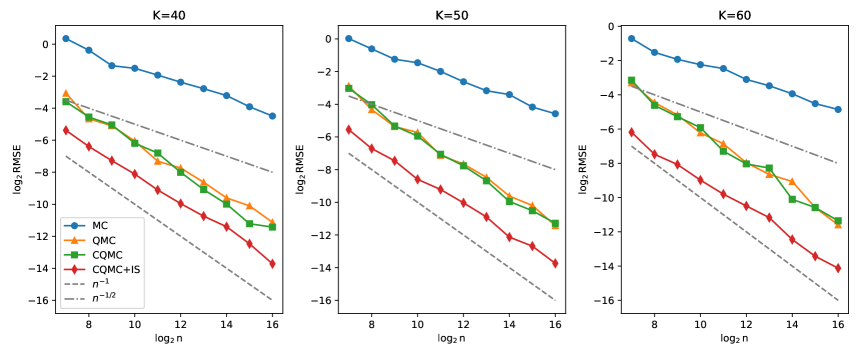

In the numerical experiments for the single-asset arithmetic Asian option, we set the parameters as follows: initial asset price , volatility , maturity , dimension , risk-free rate , and strike prices . Root mean square errors (RMSE) are estimated based on 100 repetitions. We use the CQMC+IS method with a very large sample size to obtain a high-precision estimate, which is treated as the true value. GPCA is used as the path generation method throughout all the situations. We choose the sample sizes . Figures 1 show the RMSE of plain MC, plain QMC, CQMC, and CQMC+IS methods under different strike prices for , respectively. It can be observed that the convergence rate of the CQMC+IS method closely matches the theoretical rate of . CQMC+IS achieves the lowest RMSE across all dimensions, leveraging preintegration and importance sampling to reduce variance. For , QMC and CQMC perform better than MC but are outperformed by CQMC+IS, which effectively improves efficiency through conditional smoothing and dimension reduction.

5.1.2 Multi-assets

In this section, we study a multi-assets option, which is called the basket option. A basket option depends on a weighted average of several assets [17]. Suppose that under the risk-neutral measure the assets follow the SDE

where are standard Brownian motions with correlation for all and . For some nonnegative weights , the payoff function of the Asian basket call option is given by

where is the arithmetic average of in the time interval . Here, we only consider assets. To generate with correlation , we can generate two independent standard Brownian motions and let , . Following the same discretization as before, we can generate . Then for time steps , let

| (29) |

and

| (30) |

Then the payoff function becomes

| (31) |

where

Obviously, the payoff funtion of the option satisfies the assumption 10. We choose the cholesky decomposition to generate the matrix . Thus, all coefficients preceding are positive, and Assumption 8 is thereby naturally satisfied. Next, we derive the preintegration expression of equation (31) with respect to ,

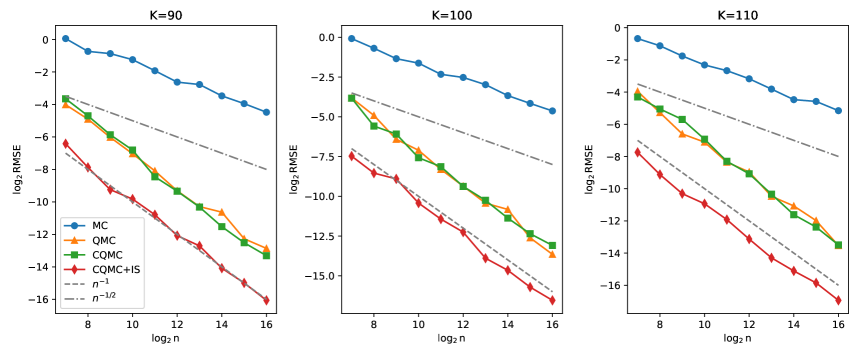

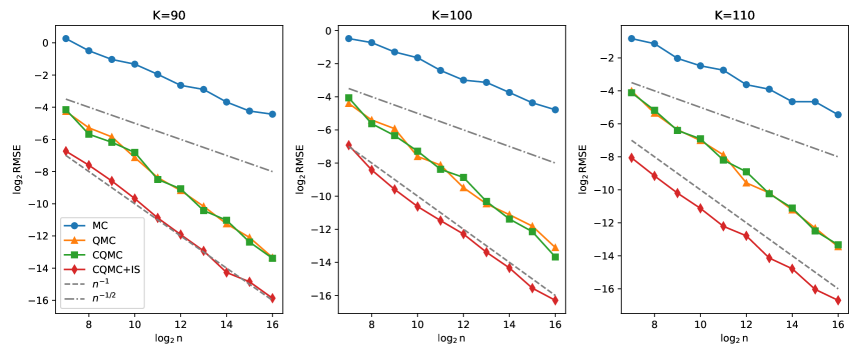

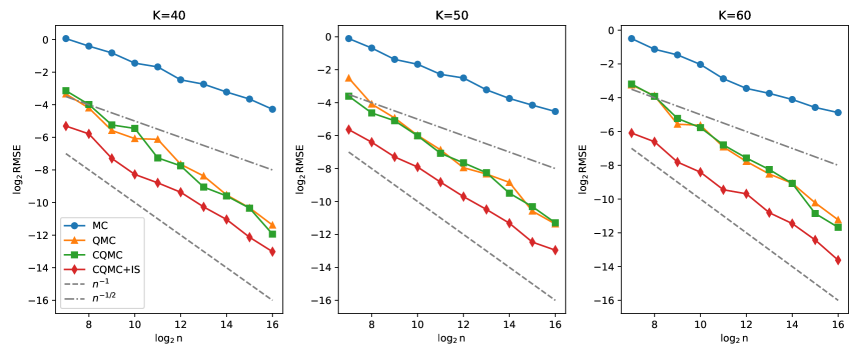

For the multi-asset basket option experiments, parameters are set as follows: initial prices of the two assets , volatilities , , maturity , weights , , dimensions , risk-free rate , strike prices , and correlation coefficient . The nominal dimensions are . The root mean square errors are estimated based on 100 repetitions. We use the CQMC+IS method with a very large sample size to obtain an accurate estimation and treat it as the true value. GPCA is used as the path generation method throughout all the situations. We choose the sample sizes . Figures 2, 3 show the RMSE of plain MC, plain QMC, CQMC, and CQMC+IS methods under different strike prices for and , respectively. It can be observed that the convergence rate of the CQMC+IS method closely matches the theoretical rate of . Notably, for out-of-the-money options (e.g., ), the variance reduction effect of IS is more pronounced: CQMC+IS achieves a significantly lower RMSE compared to other methods. This is because out-of-the-money scenarios involve rarer payoff events, and IS effectively targets these events, enhancing the efficiency of variance reduction. The weighted average structure of the basket option introduces additional complexity, but CQMC+IS still maintains the lowest RMSE. As the dimension increases (from to ), the performance gap between CQMC+IS and other methods widens: QMC and CQMC outperform MC but are surpassed by CQMC+IS, which handles multi-asset correlation and high-dimensionality through importance sampling and conditional smoothing.

5.2 Heston Model

Under the Heston framework, the risk-neutral dynamics of the asset can be expressed as

| (32) |

| (33) |

where is the mean-reversion parameter of the volatility process , is the long run average price variance, is the volatility of the volatility, and are two standard Brownian motions with an instantaneous correlation , i.e., for any . One may write that and , where and and are two independent standard Brownian motions. Let . We use the Euler-Maruyama scheme to discretize the asset paths [1], resulting in

| (34) |

| (35) |

where is the initial value of the volatility process, and represent the approximations of and for , respectively. Here we still consider estimating the price of an arithmetic average Asian call option

| (36) |

where .

Next, we provide the analytically expression for the preintegration of the payoff function with respect to . Assumption 8 is satisfied, because all coefficients preceding are positive. The derivation is presented in [27].

| (37) |

where

| (38) |

| (39) |

Remark 2.

If the growth condition in Assumption 10 is modified to be controlled by , where , then following the proof framework of Theorem 11 , it can be deduced that the preintegrated function is bounded by such an exponential function. In this case, the convergence order specified in Corollary 12 remains valid. Within the Heston model, the payoff function satisfies the aforementioned modified Assumption 10. Consequently, the convergence order can still be attained.

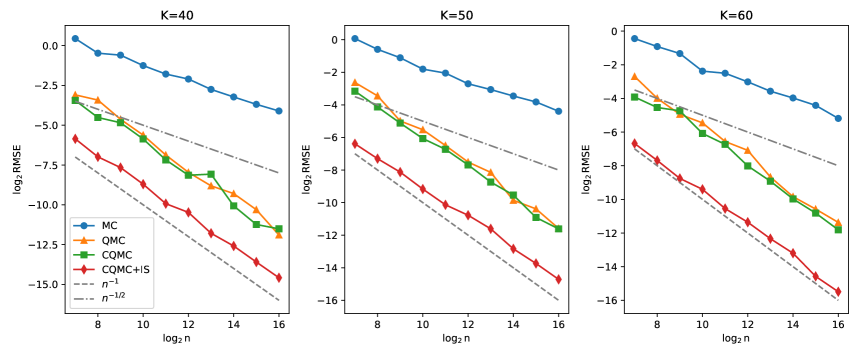

In the numerical experiments, we choose , , , , , , , and . The nominal dimension is . The root mean square errors are estimated based on 100 repetitions. We use the CQMC+IS method with a very large sample size to obtain an accurate estimation and treat it as the true value. GPCA is used as the path generation method throughout all the situations. We choose the sample sizes . Figures 4, 5, 6 show the RMSE of plain MC, plain QMC, CQMC, and CQMC+IS methods under different strike prices for and , respectively. It can be observed that the convergence rate of the CQMC+IS method closely matches the theoretical rate of . Stochastic volatility in the Heston model increases path complexity, but CQMC+IS still achieves the lowest RMSE across all dimensions, leveraging preintegration and importance sampling to handle volatility randomness. For (nominal dimension ), QMC and CQMC perform better than MC but are outperformed by CQMC+IS, which effectively reduces variance through conditional smoothing and importance sampling.

6 Conclusion

In this paper, we addressed a significant gap in the convergence theory of Randomized Quasi-Monte Carlo with Importance Sampling (RQMC-IS), particularly for problems involving integrands with critical exponential growth. Standard theories require the growth rate exponent in to be strictly less than , a condition that is often violated by practical and effective variance reduction techniques like Optimal Drift Importance Sampling (ODIS).

Our primary contribution is the development of a new, more general convergence theorem for RQMC-IS. This theorem extends the analysis to the critical case where , establishing a near- convergence rate under a verifiable light-tail condition on the proposal distribution. We then formally proved that the Gaussian proposals used in ODIS satisfy this condition, thus providing the first rigorous convergence guarantees for the widely used RQMC-ODIS method in these challenging scenarios.

Furthermore, we created a complete end-to-end framework for pricing complex financial derivatives. By integrating our new convergence theory with the preintegration technique, we demonstrated that even discontinuous payoff functions, once smoothed, can be efficiently estimated within our framework. We showed that if the components of the original payoff function have linear exponential growth, the smoothed function preserves this property, allowing it to be seamlessly combined with an IS proposal that introduces the critical quadratic exponential growth.

Numerical experiments on a variety of option pricing problems, including single-asset Asian, multi-asset basket, and stochastic volatility (Heston) models, empirically validated our theoretical findings. The results consistently demonstrated that our combined CQMC+IS method not only achieves the predicted convergence rate but also significantly outperforms standard MC, QMC, and CQMC methods in terms of accuracy and efficiency.

Future work could extend this work in several directions. One promising avenue is to investigate other families of proposal distributions beyond the Gaussian one, such as those with heavier tails, and analyze their compatibility with our theoretical framework. Another direction is to explore more practical applications of this methodology to other high-dimensional integration problems outside of finance, for example, in Bayesian statistics or computational physics.

Appendix A Appendix

This appendix provides detailed proofs for the key technical lemmas presented in the main text. We will prove lemma 6 by the mean value theorem, and calculate the as in [20] to prove the lemma 5. They both need the following lemma about . Thus, we begin by establishing a bound on the derivatives of the importance sampling integrand .

Lemma 13.

If as a function in satisfies the growth condition 12 and , then

Proof.

By Leibniz rule, we have

∎

A.1 Proof of lemma 5

Proof.

By definition,

By lemma 13, we have

where . Integrating both side and summing over all , we obtain that for ,

| (40) |

∎

A.2 Proof of lemma 6

Proof.

Let denote the hypercube in with side length centered at the origin. Then

Using the mean value theorem, we have

where lies between and . By lemma 13, we have

Combing , we have

Integrating over , we obtain

for , under the condition, we obtain the desired bound. For , we note that as a function of is continuous on , thus we can find a constant such that

implying that

Therefore, for any , we can find a constant such that

where is a constant depending on , , and . This completes the proof. ∎

A.3 Proof of proposition 7

Proof.

Consider the integral

For , we have

Thus,

Therefore,

Evaluating the integral in spherical coordinates, we obtain

Thus,

which satisfies the condition for sufficiently large . ∎

References

- [1] Nico Achtsis, Ronald Cools, and Dirk Nuyens. Conditional sampling for barrier option pricing under the Heston model. In Monte Carlo and Quasi-Monte Carlo Methods 2012, pages 253–269. Springer, 2013.

- [2] Peter A Acworth, Mark Broadie, and Paul Glasserman. A comparison of some Monte Carlo and quasi Monte Carlo techniques for option pricing. In Monte Carlo and Quasi-Monte Carlo Methods 1996: Proceedings of a conference at the University of Salzburg, Austria, July 9–12, 1996, pages 1–18. Springer, 2011.

- [3] B Owen Art. Monte Carlo theory, methods and examples, 2013.

- [4] Russel E. Caflisch. Monte carlo and quasi-Monte Carlo methods. Acta Numerica, 7:1–49, 1998.

- [5] Russel E Caflisch, William Morokoff, and Art Owen. Valuation of mortgage-backed securities using brownian bridges to reduce effective dimension. Journal of Computational Finance, 1997.

- [6] Josef Dick and Friedrich Pillichshammer. Digital nets and sequences: discrepancy theory and quasi-Monte Carlo integration. Cambridge University Press, 2010.

- [7] Josef Dick, Daniel Rudolf, and Houying Zhu. A weighted discrepancy bound of quasi-Monte Carlo importance sampling. Statistics & Probability Letters, 149:100–106, 2019.

- [8] Michael Fu and Jian-Qiang Hu. Conditional Monte Carlo gradient estimation, pages 73–131. Springer US, 1997.

- [9] Paul Glasserman. Monte Carlo Methods in Financial Engineering, volume 53. Springer, 2004.

- [10] Paul Glasserman, Philip Heidelberger, and Perwez Shahabuddin. Asymptotically optimal importance sampling and stratification for pricing path-dependent options. Mathematical finance, 9(2):117–152, 1999.

- [11] Michael Griebel, Frances Kuo, and Ian Sloan. The smoothing effect of integration in temp and the ANOVA decomposition. Mathematics of Computation, 82(281):383–400, 2013.

- [12] Michael Griebel, Frances Kuo, and Ian Sloan. Note on “the smoothing effect of integration in temp and the ANOVA decomposition”. Mathematics of Computation, 86(306):1847–1854, 2017.

- [13] Michael Griebel, Frances Y. Kuo, and Ian H. Sloan. The smoothing effect of the ANOVA decomposition. Journal of Complexity, 26(5):523–551, 2010.

- [14] Andreas Griewank, Frances Y. Kuo, Hernan Leövey, and Ian H. Sloan. High dimensional integration of kinks and jumps—smoothing by preintegration. Journal of Computational and Applied Mathematics, 344:259–274, 2018.

- [15] Zhijian He. On the error rate of conditional quasi-Monte Carlo for discontinuous functions. SIAM Journal on Numerical Analysis, 57(2):854–874, 2019.

- [16] Anthony YC Kuk. Laplace importance sampling for generalized linear mixed models. 1999.

- [17] Sifan Liu and Art B. Owen. Preintegration via active subspace. SIAM Journal on Numerical Analysis, 61(2):495–514, 2023.

- [18] Jiří Matoušek. On the -discrepancy for anchored boxes. Journal of Complexity, 14(4):527–556, 1998.

- [19] Harald Niederreiter. Random number generation and quasi-Monte Carlo methods. SIAM, 1992.

- [20] Du Ouyang, Xiaoqun Wang, and Zhijian He. Achieving high convergence rates by quasi-Monte Carlo and importance sampling for unbounded integrands. SIAM Journal on Numerical Analysis, 62(5):2393–2414, 2024.

- [21] Art Owen and Yi Zhou. Safe and effective importance sampling. Journal of the American Statistical Association, 95(449):135–143, 2000.

- [22] Art B Owen. Randomly permuted (t, m, s)-nets and (t, s)-sequences. In Monte Carlo and Quasi-Monte Carlo Methods in Scientific Computing: Proceedings of a conference at the University of Nevada, Las Vegas, Nevada, USA, June 23–25, 1994, pages 299–317. Springer, 1995.

- [23] Art B. Owen. Halton sequences avoid the origin. SIAM Review, 48(3):487–503, 2006.

- [24] Art B. Owen. Practical Quasi-Monte Carlo Integration. https://artowen.su.domains/mc/practicalqmc.pdf, 2023.

- [25] Ye Xiao and Xiaoqun Wang. Enhancing quasi-Monte Carlo simulation by minimizing effective dimension for derivative pricing. Computational Economics, 54(1, SI):343–366, 2019.

- [26] Chaojun Zhang and Xiaoqun Wang. Quasi-Monte Carlo-based conditional pathwise method for option greeks. Quantitative Finance, 20(1):49–67, 2020.

- [27] Chaojun Zhang, Xiaoqun Wang, and Zhijian He. Efficient importance sampling in quasi-Monte Carlo methods for computational finance. SIAM Journal on Scientific Computing, 43(1):B1–B29, 2021.