[

Patterns of consumption in a discrete choice model with asymmetric interactions

Abstract

We study the consumption behaviour of an asymmetric network of heterogeneous agents in the framework of discrete choice models with stochastic decision rules. We assume that the interactions among agents are uniquely specified by their “social distance” and consumption is driven by peering, distinction and aspiration effects. The utility of each agent is positively or negatively affected by the choices of other agents and consumption is driven by peering, imitation and distinction effects. The dynamical properties of the model are explored, by numerical simulations, using three different evolution algorithms with: parallel, sequential and random-sequential updating rules. We analyze the long-time behaviour of the system which, given the asymmetric nature of the interactions, can either converge into a fixed point or a periodic attractor. We discuss the role of symmetric versus asymmetric contributions to the utility function and also that of idiosyncratic preferences, costs and memory in the consumption decision of the agents.

]

I Introduction

A great body of research has been devoted to the effects that direct interactions among consumers or firms have on macroeconomics variables (Brock 1995, Brock and Durlauf 1995, Aoki 1996, Axelrod 1997, Albin 1998, Chwe 2000). Direct interactions among economic agents, usually referred to as social interactions (as opposed to market mediated interactions) are meant to capture how the decision of each individual is influenced by the choice of others in his reference group. Direct interaction models can apply to coordination problems in general, ranging from the emergence of collective political actions and the development of fads and conventions to the explanation of speculative bubbles in financial markets and the dynamics of market penetration and diffusion of technological innovations.

Different alternatives have been considered in the literature: global interactions (Brock and Durlauf 1995), where each individual tends to conform to the average behaviour of the entire population, as well as local interactions, where each individual has an incentive to conform to a specified group of neighbours (Föllmer 1974, Durlauf 1993, Blume 1993, Corneo 1994, Morris 2000). This last case has recently gained interest in economics, following the observation that network externalities are often localized. A stochastic interaction picture has also been considered. This can be implemented by considering either fixed, exogenously determined, random communication links between any pair of agents or, by taking time-dependent links and letting the neighbouring composition evolve in a self-organized way (Benabou 1996, Durlauf 1996). In this case, agents would be able to form new alliances according to some fitness maximization scheme. Moreover, links among agents can be of varying strength, often positive and negative (Axelrod 1997, Galam 2000), to account for the different externalities an agent receives from the behaviour of the other agents, depending not only on where they are but also on who they are.

Nonetheless, in the literature the attention has been mainly focused on the case of positive, pairwise symmetric, spillover, i.e. the case where the payoff of a particular action increases when others behave similarly. In this context, it has been shown that the evolution is diffusive: even in the case of heterogenous agents, social interactions create conformity in behaviour or polarized group behaviour without relying on the presence of correlated characteristics among members of the same group. While models with symmetric interactions have given numerous insights in a variety of contexts, from a sociological point of view the constraint of symmetric interactions is unsatisfactory. Two agents do not need to influence one another in the same manner. Therefore it is natural to investigate models with asymmetric couplings between agents.

Non-symmetric pairwise interactions, although common in the study of neural networks and other biological systems (Kauffman 1969, see also Müller et al. 1995 for a review), have only recently been introduced in economics (Akerlof 1997, Kirman 1997, Samuelson 1997). In a recent work, Cowan, et al. (1998), introduced a model of consumption behaviour, herefrom called the CCS model, where the utility of an individual agent is positively or negatively affected by the choices of other agents and consumption is driven by peering, imitation and distinction effects. In the CCS model, the microeconomic agents have pairwise interactions which are specified by a function of a single parameter, their “social distance” such as, for example, differences is wealth (where the wealth can be a random variable). Consumers are ordered according to their social status and are affected by the behaviour of other agents depending on their relative location on the spectrum. Agents wish to distinguish themselves from those who are below and emulate their peers and those who are above in the social spectrum. The interplay between aspiration and distinction effects can generate consumption waves, which propagate through the system.

The CCS model has been analyzed in the framework of random utility discrete choice models, extending the literature there by combining both local and global externality effects. Discrete choice models start from the assumption that each agent faces a set of mutually exclusive alternatives, and chooses the one that yields greatest utility (see Anderson et al. (1992) for a review). Two families of models have been introduced to analyze the choice process in a probabilistic setting. The first family of models assumes that the decision rule is deterministic but the utility is stochastic. The idea behind this assumption is that even though individual behaviour might be deterministic, the modeler can only imperfectly observe the factors that influence individual choice and only has an imperfect knowledge of the utility function of each agent. Models in the second family assume that the utility is deterministic but the choice process is stochastic. These models capture the idea of bounded rationality of economic agents (Sargent 1995). Even if utility is deterministic, individuals might make an error in evaluating the importance of one or another characteristic associated with a certain alternative and do not necessarily select what is best for them. The CCS model lies in the first category, namely that of random utility models with interacting agents. In this paper we reformulate the CCS model and adopt the alternative description, that of the choice as a stochastic process with the utility being deterministic.

Discrete choice models have been analyzed using the techniques of statistical mechanics. In the case of symmetric interactions, the equilibrium condition can be expressed in terms of the Boltzman distribution. This is no more the case in models with asymmetric interactions. As a consequence, the long time behaviour of the system has to be calculated by solving the dynamical problem (which in most cases is not possible analytically) and cannot be evaluated by equilibrium ensemble averages. We use numerical simulations with Glauber dynamics (Glauber 1963) to explore, the dynamical properties of the model. We implement three different evolution algorithms with: parallel, sequential and random-sequential updating rules, depending on the order on which individual agents update their decision. We first focus on the deterministic limit and study the attractors of the model, which determine the steady state, long-time behaviour of the consumption behaviour. Depending on the evolution algorithm as well as the degree of the asymmetry the attractors can be either fixed points or limit cycles. We then introduce noise in the system and study how this affects the dynamics of consumption. Eventually, extending the analysis of CCS we discuss the role of costs and memory in the consumption decision of the agents and consider different scenarios for the connectivity among the economic agents.

In section II we set the general framework by reviewing briefly the theory of discrete choice models in a stochastic environment. In section III we present our model in terms of the interactions and the possible evolution mechanisms. Section IV contains results from our simulations while section V conclude.

II Discrete Choice Models

Discrete choice models can be formalized (Brock and Durlauf 1995, Durlauf 1997) by considering a population of individuals, where each individual chooses with support . The set of all possible sets of actions by the population, denoted by , consists of all N-tuples .

In the following we briefly review the basic ideas of both stochastic utility and stochastic decision rule approaches.

A Stochastic utility models

This problem has been formulated initially in the case of non interacting agents (Anderson et al. 1992) and has been subsequently generalized by Brock and Durlauf (1995) to the case with social interactions.

Individual utility consists of two components, a deterministic term plus a random component:

| (1) |

The probability that an individual chooses is given by

| (2) |

or

| (3) |

To solve the problem one needs to make some assumption about the distribution of the random terms. The random disturbances are assumed independent and identically distributed across agents, and are known at the time agents take their decision. Let be the distribution of . Then

| (4) |

If is logistically distributed with zero mean and variance

| (5) |

then

| (6) |

The generalization to multiple choices is possible if the double exponential distribution is assumed for the noise

| (7) |

where is the Euler’s constant (). In this case

| (8) |

This problem has been generalized by Brock and Durlauf, when social externalities affect agents’ decisions, by taking into account an extra term in the utility function:

| (9) |

where represent agent’s deterministic private utility, represent his/her deterministic social utility, and represents a random private utility.

The term denotes the conditional probability measure agent places on the choices of others at the time of making his own decision. Brock and Durlauf write the social utility as

| (10) |

where is the reference group of agent and represent the conditional expectation operator associated with agent ’s beliefs. represent the interaction weight which relates ’s choice to ’s choice. The are chosen equal to 1 if a link between a pair exist and zero eitherways. Within this framework, choosing a particular realization of , the interactions among agents are completely specified.

The private utility is assumed to depend linearly on :

| (11) |

where the can be chosen the same for all agents or can have different values for different if we assume heterogeneous agents. Note that plays the role of an external field, affecting the decision of agent . Analogously, the social utility term can be interpreted as an internal field generated by the agents themselves. Defining

| (12) |

the deterministic component of the utility becomes

| (13) |

Note we have rescaled the interactions , dividing by , in order to keep finite as .

If the are independent across agents, the joint probability measure over all agents choices equals:

| (14) |

and we can rewrite eq.(9) as

| (15) |

B Stochastic decision rules models

Following the observation that adjustments to the behaviour of economic agents are often made at discrete points in time and are of finite magnitude, one can use jump Markov processes to model the evolutionary dynamics of a large collection of interacting microeconomic agents (Aoki 1996). Interactions of microeconomic units can then be specified in terms of transition probabilities of Markov chains (discrete Markov process with finite state-space). The initial condition and the state transition probability completely characterize the time evolution of a discrete-time Markov chain. The time evolution of the probabilities of states in terms of transition rates and the state’s occupancy probability is given by the master equation:

| (16) |

where denote state space variables. From this equation one sees that for the stationary or equilibrium probability to exist the (full) balance condition should be satisfied:

| (17) |

If moreover the probability flow balances for every pair of states , i.e. the detailed balance condition holds

| (18) |

it can be shown that the equilibrium distribution is path independent. More precisely, denoting by the space state of a Markov chain, if we assume that the Markov chain is ergodic***More precisely, the chain should be irreducible, aperiodic and positive (see, for example, Hammersley and Handscomb 1975), any state can be reached from an initial state through a sequence of intermediate states so that

| (19) |

If the detailed balance condition holds it can be shown that

| (20) |

In other words is a Gibbs distribution

| (21) |

where

| (22) |

, depending only on the state is a potential. It follows that any dynamical process, as long as it satisfies the detailed balance condition with the same function , will reach the same asymptotic equilibrium distribution of states and, from eq.(20), that the equilibrium probability distribution is independent of the dynamical trajectory in the configuration space.

Given a potential which we want to maximize the problem eventually becomes to find the appropriate transition probabilities which satisfy the detailed balance condition with specified by eq.(21). The Glauber dynamics, or heat-bath algorithm (Glauber 1963), serves this purpose. In our formulation we want the potential to be the total utility of the system. We assume here that the utility is the same as the one given in the previous section except for the random component which is now missing:

| (23) |

The total utility of the system in the configuration is then

| (24) |

Accordingly, to the heat-bath algorithm the probability of a agent to take a value , where can only be +1 or -1, is

| (25) |

This can be interpreted as the choice process of our agents not being entirely deterministic. Indeed, we are assuming that there is a “noise” element in the agents’ decision represented by a Glauber dynamics with a thermal agitation characterized by a temperature which is held fixed.

It is easy to show that the updating process described by eq. (25) obeys the detailed balance condition with if the are symmetric, i.e. . Following Amit (1989), we note first that the probability for a agent to go to a state only depends on the final state of that agent and the states of all other agent, who create the local field. Therefore the probability for the system to go from a configuration , in which the agent is in state to a configuration , in which that agent is in state , is and the probability to go from to is (the denominator expresses the probability to pick up that specific agent). Hence

| (26) | |||||

| (27) |

from where the detailed balance condition holds and hence

| (28) |

Nonetheless if there are asymmetric interactions, i.e. the detailed balance condition, eq. (18) is no longer valid, and the long time evolution of the system does not necessarily converge to the Gibbs equilibrium distribution defined in eq. (28). Even though nothing can be said, a priori, in this case about the equilibrium distribution, the heat-bath algorithm still gives a prescription on how to introduce a dynamics which, by maximizing , leads to an equilibrium state. Moreover, given that the contribution of any asymmetric component of the interactions to the total utility is zero when calculating the double sum, would not be a Lyapunov function in this case. We remind that in the absence of a Lyapunov function the system is not forced to approached a stable attractor state and limit cycles can occur as well as fixed points.

Note that in eq. (25) we have not specified the order of updating. Two versions of the dynamics have become popular: the first assumes that all agents update their state simultaneously at every discrete time step . The state of the other agents is in this case considered to be the one in the time interval . This type of dynamics is called synchronous or parallel. The second kind of dynamics is the asynchronous or sequential in which the state of each agent is updated one by one. In this case every agent coming up for a decision has full information about the state of the other agents that have been updated before him.

In the following sub-section we focus on the dynamics at (the deterministic limit) and review the main results concerning the nature of the attractors when using different updating rules.

C Dynamics

(a) Parallel (or synchronous) dynamics: At each time step , all agents re-evaluate simultaneously their consumption decision, relative to that taken one step before, on the basis of the utility they receive, according to:

| (29) |

where we have implicitly absorbed the factor in the definition of and introduced for later convenience the notation:

| (30) |

(b) Sequential dynamics: This is the case of asynchronous updating in which the state of each agent is updated one by one in a serial manner, according to:

| (31) |

(c) Random sequential (Glauber) dynamics: This is another case of asynchronous updating scheme, similar to the previous case, with the difference though that the order of updating is chosen randomly.

For both synchronous and asynchronous dynamics, symmetric couplings is a sufficient condition for the existence of detailed balance. Nonetheless the form of the asymptotic distribution differs in the two dynamics. In the following, we briefly review the properties of the three dynamical rules. One can draw a number of general statements about the nature of fixed points, without relying on the detailed form of .

For asynchronous dynamics (sequential or random sequential) and symmetric the distribution of configurations relaxes eventually to the Boltzmann distribution eq.(28).

In the noiseless () case, each contribution to the utility is increased (or remains constant) after each agent updates her decision, as can be seen from

| (32) | |||||

| (33) | |||||

| (34) |

Since the total utility is bounded from above, in absence of asymmetry the system will asymptotically be driven to a fixed point attractor which is either a local or a global maximum of the utility functional.

While in the case of symmetric interactions there exist only fixed points, with asymmetric cycles of longer length appear. Eventually in the limit case of anti-symmetric interactions () Gutfreund, Reger and Young (1987), have proved that there exist only 2-cycles.

In the case of synchronous dynamics and symmetric interactions the asymptotic distribution depends on (and consequently is non Gibbsian) and can only formally be written in the Boltzmann form (Amit 1989):

| (35) |

with

| (36) |

In the (i.e. ) limit reduces to

| (37) |

The dynamical process now maximizes (often called the stability function), since

| (38) | |||||

| (39) | |||||

| (40) |

If is symmetric one sees that

| (41) | |||||

| (42) |

implying that . The remains unchanged either when the consecutive states are identical, i.e. the system has reached a fixed point, or when the two states alternate , i.e. the system has reached a 2-cycle. The existence of 2-cycles with symmetric interactions is a unique feature of synchronous dynamics.

If, on the other hand is antisymmetric, then changes by

| (43) | |||||

| (44) |

and thus, again , where the equality holds when . Therefore, for antisymmetric interactions the only attractors are 4-cycles, since the first and the third states are inverses of each other, as are the second and fourth state.

Eventually we remind that the number of fixed points is the same for sequential, parallel and for random sequential dynamics.

III Model

We consider a population of agents, ordered on a one-dimensional space and labeled by a variable which represents their position in the social spectrum and in a broad sense their wealth. Agents’ wealth is chosen randomly, from the uniform distribution in the interval , and does not change with time. In this paper, wealth serves as an index of social status rather than the source of a budget constraint, as discussed below. A more realistic situation with consumers arranged over a multidimensional space (accounting, for example, for differences in age, education, etc.) should be considered, but for simplicity we only use one parameter to characterize the agents, namely their wealth.

According to our previous description, the state of our population , evolves according to a jump Markov process. Time evolves discretely and at each step an agent has a binary choice either to consume one indivisible unit of a good in which case , or not to consume, in which case . For some product that exists, or appears for the first time in the market, and given an initial state at time , each agent decides whether to consume or not at every subsequent time step, doing so if this action provides positive utility.

For example, a new restaurant opens at time zero and in each subsequent time period agents decide whether to visit it or not.

The utility function is specified in eq. (23). The local field characterizes the intrinsic value of the good to agent . This term contains all private factors that affect his consumption decision. A product with for all agents is called a “fashion” good, while a “status” good has a positive intrinsic value that might be well-suited to the characteristics or tastes of a particular class of consumers.

Each agent interacts with all the others, and the coupling constants are functions of the agents’ status according to:

| (45) |

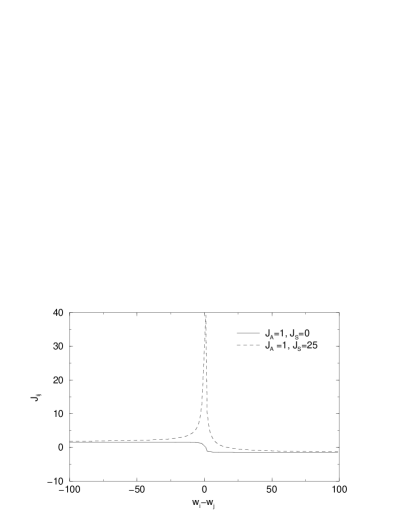

The coefficients are taken positive. The asymmetric term, proportional to , gives a negative contribution to the utility function if and a positive contribution if . This means that agent wishes to distinguish herself from the poorer while imitating the richer. The second contribution, proportional to , always generates positive utility and expresses peering effects among consumers of similar status. The level of asymmetry is defined by the ratio . Both of these contributions saturate with distance to a constant value. In Fig. (1) is plotted as a function of .

We shall further assume that agents make expectations about the choice of others according to

| (46) |

Various scenarios could be considered by changing the length of the memory of each agent and the weights, , that agents put on past realizations in the expectation formation process. We have focused on the case

| (47) |

with simulating in this way a fading memory.

Eventually we introduce a set of parameters which account both for the price of the good and for the idiosyncratic costs that each agent individually may face. In our previous example of the restaurant, the cost for a consumer may be larger (lower) if (s)he lives farther (closer) to it. We assume that costs act merely as thresholds and the decision of agent on whether to buy the good or not depends only on whether his utility of buying one unit is positive and larger than . This means that in eq.(25, 29, 31)

| (48) |

Nonetheless all agents are assumed to possess sufficient liquidity at all points in time and wealth constraints are never binding.

IV Simulations and Results

We have performed computer simulations to study the model in eq. (23, 45, 39) for each of the evolution algorithms of section II C. We studied both the time evolution of total consumption as well as the spatial distribution of consumption across the social spectrum. We explored the various patterns generated with different choices of the parameters. Our plots refer to lattice size . We have taken the agents’ wealth to be uniformly distributed in the interval with .

(a)

Initially we study the case of a fashion good which has no intrinsic value for the consumers, i.e. .

In analogy with Spin Glass models (Mezard et al. 1987) with asymmetric interaction†††Our model could be considered as a particular case of the asymmetric SK model (Iori and Marinari 1997) with the couplings taken according to eq. (45) instead of being chosen randomly. the nature of the attractors depends in a complex manner on the level of asymmetry . Given the analogy between the two systems we briefly resume in the following some of the features of the SK model. Nützel and Krey (1993) found that only fixed points or periodic attractors with period two are present in the nearly symmetric SK model while longer attractors appear in the case of highly asymmetric couplings (they locate the transition at ). While in the nearly symmetric case the average length of the attractor (measured by the number of different configurations the system goes through before repeating an identical sequence) is independent of the system size, , the dependence of is exponential in for highly asymmetric couplings. Moreover, very long transients are present and the typical number of updates before the system relaxes to the attractor grows as a power of at low asymmetry and is exponential in for high asymmetry. Furthermore the transient exhibits chaotic behaviour, i.e. sensitive dependence on the initial conditions (Crisanti et al. 1993).

In our model we do not observe the long transients before the system reaches the attractor, neither at high or low asymmetry. Nonetheless we found an interesting dependence of on which we report in the following.

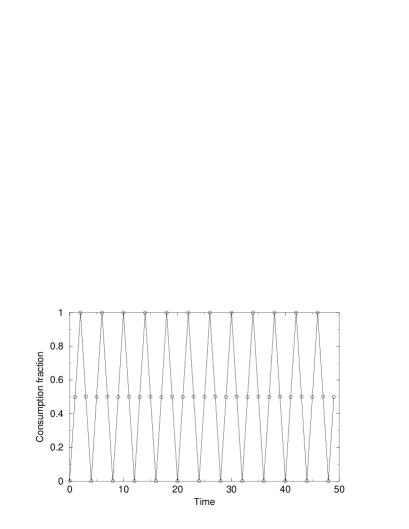

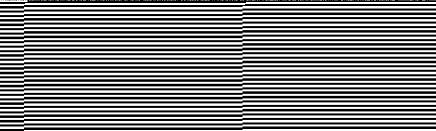

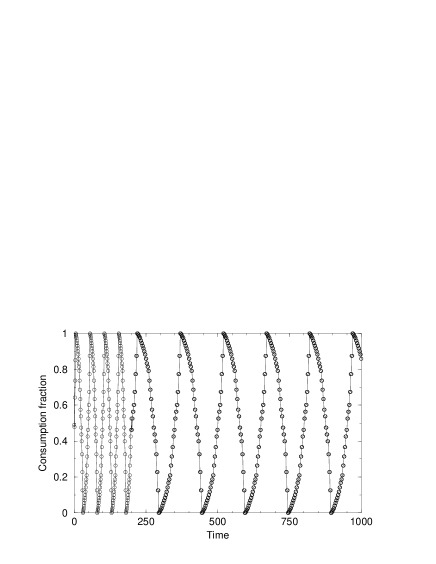

For parallel dynamics and , as we anticipated in the previous section, the system only exhibits 4-cycles (fig. (2a)) and consumption propagates very fast through the social spectrum (fig. (3a)). Note that in fig. (3) time increases from top to bottom and it is the rich who start consuming first in order to distinguish themselves from the poor.

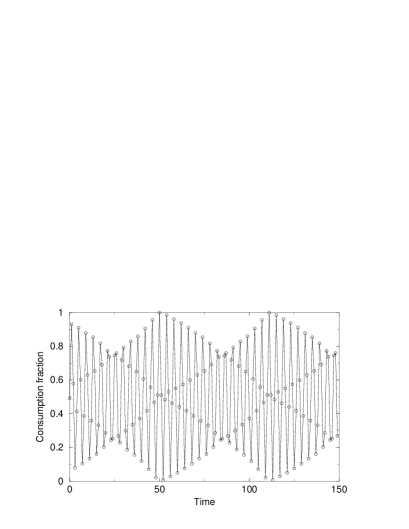

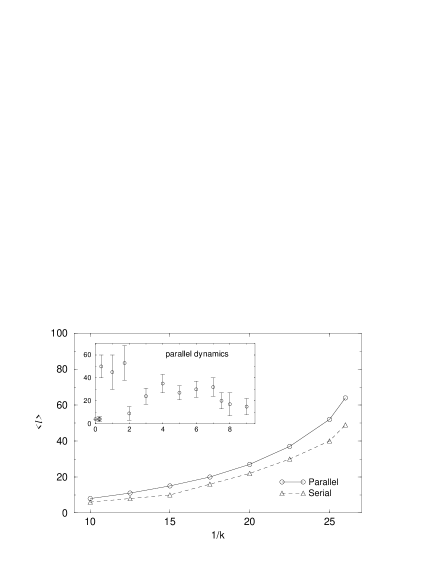

The average length of the attractors as a function of is plotted in fig.(4). The behaviour of the system is very different in the two regions of high and low asymmetry. First of all we notice that in the large limit the length of the attractor varies a lot from configuration to configuration (which explains the large error bars in the inset of fig. (4)) while at low asymmetry the length is practically independent from the realization of the (we also checked that in this regime the length of the attractor is almost independent from the system size).

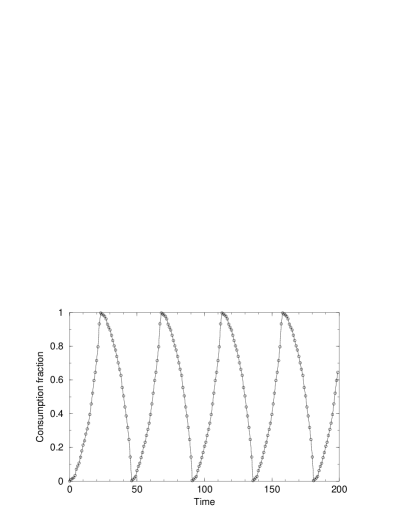

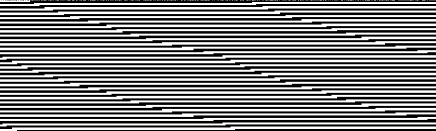

The spatial distribution of consumption also differs in the two regions. At high asymmetry, as shown in fig. (3b), consumption propagates across the social spectrum very fast. The difference with respect to the previous case is that now the location (in ) where agents stop/start consuming is different at different times and this generates a modulating effect on the total consumption (fig. (2b)). On the other hand, at low asymmetry, consumption propagatess slowly and waves of longer period appear as shown in fig. (3c). We locate the transition at . As is decreased further, the period of the waves (i.e. the length of the attractor) increases, as can be observed from the right end side of fig.(4). As decreases below a certain value (), waves disappear and the system is attracted towards a fixed point. The fixed point is characterized by either all agents consuming or nobody consuming.‡‡‡These two configurations have the same utility as the transformation is a symmetry of the system. The initial condition determines towards which of the two states the system relax.

Note that in fig. (3c) at the beginning of each cycle consumption propagates rather slowly but it spreads faster as it moves down to the poorer. -shaped curves, similar to those in fig.(2) have been observed in the case of diffusion of innovation (Rogers 1995).

For sequential dynamics and , as anticipated, in the previous section, the system only exhibits 2-cycles as depicted in fig. (5). Notice that after a short transient period during which consumption is irregular, the system ends into a periodic attractor characterized by agents clustering into groups that synchronously alternate their consumption behaviour. Starting with different initial conditions affects the position and the number of clusters which form. As we reduce towards the low asymmetru region the dynamics of sequential updating looks similar to that of parallel dynamics although the length of the attractors is shorter as can be seen from fig.(4).

For random sequential dynamics periodic attractors do not exist. Nonetheless in the low asymmetry region waves propagate through the system in a fashion similar to parallel and sequential dynamics. At very low again the dynamics converges to a fixed point where either all or nobody is consuming.

(b)

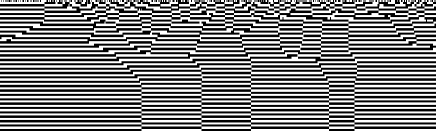

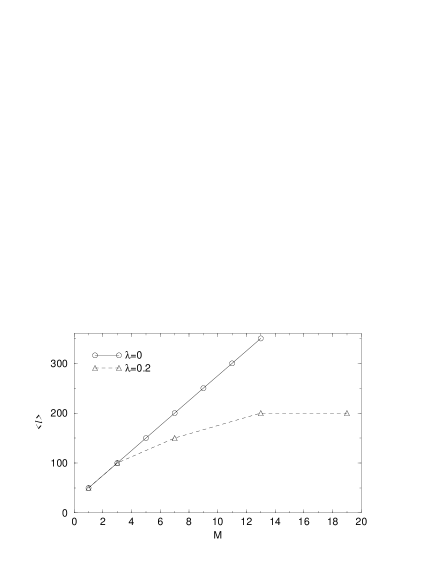

Adding finite memory to the system does not destroy the waves but it changes their frequency and the corresponding length of the attractor. This can be inspected from fig.(6) where we have run the simulation with memory for the initial 200 steps and then continued from there on with . Fig.(7) shows how the length of the attractor increases with , with all other parameters fixed. In fig. (7) we compare two cases, one with which corresponds to a non-fading memory, and another with , which corresponds to a slowly fading one. While at the dependence of on is linear, for we observe that the length of the attractor increases at a slower rate and eventually saturates (when is sufficietly large and ).

(c)

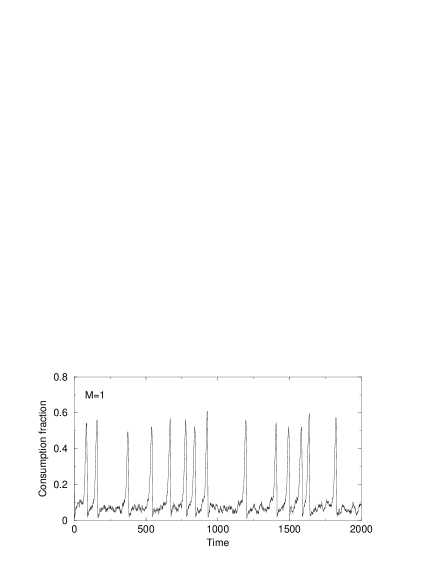

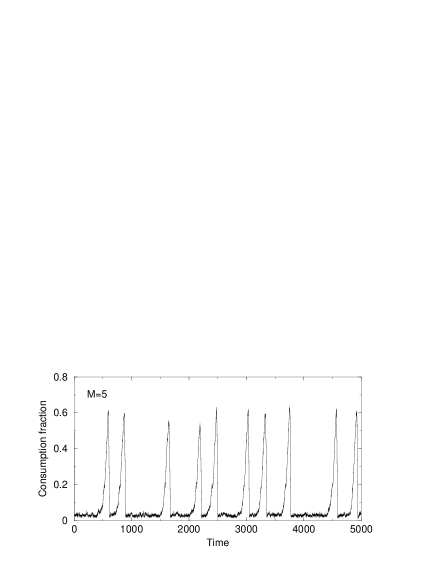

We now examne the case of and non-zero costs. Costs are chosen randomly for each agent from the uniform distribution in the interval and are fixed in time.

Averaging over many realizations of agent’s wealth we find the average critical value above which, at , nobody consumes. Keeping the same values for all the other parameters as before but taking (which is well above ) we added noise. The effect of noise is that it induces a certain number of agents to consume despite the high costs. If the number of agents who consume exceeds a critical mass then consumption waves, of varying amplitude, emerge spontaneously, even though at irregular time intervals (see Fig. (8)). Adding memory has the effect to make this occasional consumption waves more sparse. If becomes much larger, waves disappear and agents consume randomly.

(d)

We now consider the case of a “good” for which agents manifest opposite preferences independently of their social status, i.e. the intrinsic value of the good is a random number, constant in time, chosen for each agent independently from the interval .

For smaller that a certain value we still found periodic attractors with the length of the attractors decreasing with increasing. Nonetheless we do not observe consumption waves propagating along the social spectrum unless is very small. On the other hand if agents have strong preferences, the contribution of their private utility dominates in eq.(23), and only a fraction of agents update their decision under the influence of the others. Eventually, when increasing above the dynamics converges to a fixed point. Nonetheless the fixed point is not only dictated by the private utility; the social component modifies the natural distribution, i.e. the one where has the same sign of .

Another interesting case is to consider a “status” good which is designed to meet the needs of a specific group of consumers. In this case we assume the good mainly provides individual utility to consumers whose wealth is distributed around a given value choosing:

| (49) |

To analyze the interplay between the intrinsic value of the good (here ) and the costs, we fix to be larger than so that waves do not emerge in the case of a fashion good (). Therefore it is only the intrinsic value of the good which can trigger consumption.

The results which follow refer to the case and . Different behaviours are found, depending on the position of the maximum () of . For , (we remind that the agents’ wealth is distributed between zero and ), the good enters the social spectrum around , possibly migrates through the closest social classes and then finds a stable niche (see top three cases in Fig. (9)). Only when waves emerge and spread throughout the whole social spectrum (bottom case in Fig. (9)).

V Conclusions

In this paper we have focused on a potentially important mechanism that drives consumption decision: the interaction among heterogeneous consumers. Particular attention has been paid to the role of the asymmetry of interactions and the dynamical updating rules. In the sociology literature, interactions among individuals, belonging to similar or different social circles, are often seen as a major mechanism that determines new styles of behaviour. We studied how peering, distinction and aspiration effects, in addition to the intrinsic values of a good, generate different consumption patterns, under the assumption that information about the consumption behaviour of agents is public (we imagined that each agent knows the past behaviour of all other agents). Nonetheless collective behaviour may be affected by the structure of the communication channels. To check the sensitivity of our results with respect to the size of the reference group of each agent we have examined the case where individuals only communicate with a subset, chosen at random, of the entire population. If the size of the subsets is as small as of the total population we still observe (in the low asymmetry limit) waves propagating through the system whose frequencies increase when decreases.

Acknowledgments

We are grateful to C. Hiemstra and S. Jafarey for helpful comments. V.K. also wishes to thank the University of Essex for the kind hospitality provided during the initial stages of this work.

References

Akerlof G. A., Social Distance and Social decision, Econometrica,

Vol. 65, No. 5 (1997), 1005-1027.

Albin P.S., Barriers and bound to rationality,

Princeton University Press (1998)

Amit D., “Modelling Brain Functions”, Cambridge University Press (1989).

Anderson S., A. de Palma, and Thisse J.-F., “Discrete Choice Theory

of Product Differentiation”, MIT press, (1992).

Aoki M., “New approaches to macroeconomic modeling”,

Cambridge University Press (1996).

Axelrod R., The complexity of cooperation, Princeton University Press (1997)

Blume L., “The Statistical Mechanics of Strategic Interaction”,

Games and Economic Behaviour, 5, (1993), 387-423.

Benabou R., “Equity and Efficiency in Human Capital Investment: The

Local Connection”, Review of Economic Studies, 62 (1996) 237-264.

Brock W., “Asset Price Behaviour in Complex Environments”, Mimeo,

Dept. of Economics, University of Wisconsin, Madison (1995).

Brock W. and Durlauf S., “Discrete choice with social interactions”,

Mimeo, Dept. of Economics, University of Wisconsin, Madison (1995).

Chwe M. S.-Y., “Communication and Coordination in Social Networks”,

Review of Economic Studies, 67, (2000), 1-16.

Corneo G. and Jeanne O.,

“A Theory of Fashion Based on Segmented Communication”, Mimeo, Dept.

of Economics, University of Bonn (1994).

Cowan R., Cowan W. and Swan P.,

“Waves in Consumption with Interdependence among Consumers”,

MERIT preprint, Research Memoranda series, N. 011.

A. Crisanti, M. Falcioni and A. Vulpiani,

Transition from regular to complex behaviour in a discrete

deterministic asymmetric neural network model, J.Phys. A26 (1993) 3441-3454.

Durlauf S., “Statistical mechanics approaches to socioeconomic behavior”,

in The economy as an evolving complex system II, W.B. Arthur,

S.N. Durlauf and D. Lane, eds., Redwood City: Addison-Wesley (1997).

Durlauf, S., “A Theory of Persistent Income Inequality”, Journal of

Economic Growth, 1, (1996), 75-93.

Föllmer, H., “Random Economies with Many Interacting Agents”,

J. of Mathematical Economics, 1, (1974) 51-62.

S. Galam, “Spontaneous coalition forming: a model from spin glass”,

preprint, http://xxx.lanl.gov/abs/cond-mat/9901022.

R.J. Glauber, “Time-dependent statistics of the Ising model”,

J. Math Phys. 4, 294 (1963).

Hammersley J. M. and Handscomb D.C., “Monte Carlo Methods”, Methuen’s

Monographs, London (1975).

G. Iori and E. Marinari, On the Stability of the Mean-Field

Spin Glass Broken Phase under Non-Hamiltonian Perturbations,

J. Phys. A: Math. Gen. 30 (1997) 4489-4511.

Kauffman S. A., Journal of Theoretical Biology, 22 (1969) 437.

Kirman A., “Economies with interacting agents”,

in The economy as an evolving complex system II, W.B. Arthur,

S.N. Durlauf and D. Lane, eds., Redwood City: Addison-Wesley (1997).

Mezard M., Parisi G. and Virasoro M.A., “Spin glass theory and

beyond”, (World Scientific, Singapore 1987).

Morris S., “Contagion”, Review of Economic Studies, 67, (2000), 57-78.

Müller B., Reinhardt J., Strickland M.T.,

“Neural Networks : An Introduction”, Springer-Verlag, 1995.

Nützel K. and Krey U.,

“Subtle dynamic behaviour of finite-size Sherrington-Kirkpatrick

spin glasses with non-symmetric couplings”, J. Phys. A: Math. Gen. 26

(1993) 591-597.

Rogers E.M., “Diffusion of Innovations”, The Free Press, New York, 1995.

Samuelson L., “Evolutionary Games and Equilibrium Selection”, MIT

Press, 1997.

Sargent T. J., “Bounded Rationality in Macroeconomics”, Clarendon

Press, 1994.