Scale invariant distribution and multifractality of volatility multipliers in stock markets

Abstract

The statistical properties of the multipliers of the absolute returns are investigated using one-minute high-frequency data of financial time series. The multiplier distribution is found to be independent of the box size when is larger than some crossover scale, providing direct evidence of the existence of scale invariance in financial data. The multipliers with base are well approximated by a normal distribution and the most probable multiplier scales as a power law with respect to the base . We unravel that the volatility multipliers possess multifractal nature which is independent of construction of the multipliers, that is, the values of and .

keywords:

Econophysics; Stock markets; Multiplier; Volatility; Scale invariance; Multifractal analysis,

1 Introduction

It has been a long history that physicists show interests on financial markets, which can be at least traced back to 1900 when Bachelier modeled stock prices with Brownian motions [1]. In the middle of last century, Mandelbrot proposed to characterize the tail distributions of income and cotton price fluctuations with the Pareto-Lévy law and applied R/S analysis to investigate the temporal correlations in the evolution of stock prices [2]. In recent years since the seminal work of Mantegna and Stanley [3], Econophysics has attracted extensive interest in the physics community.

As an analogue to turbulence, many time series observed in the financial markets are reported to possess multifractal properties [4, 5], such as the foreign exchange rate [4, 5, 6, 7, 8, 9, 10, 11], gold price [8], commodity price [12], stock price [12, 13, 14, 15, 16, 17], stock market index [18, 19, 20, 21, 22, 23, 24, 25, 26, 27, 28], to list a few. Extensive methods have been adopted to extract the empirical multifractal properties in financial data sets, for instance, the wavelet transform module maxima (WTMM) [29, 30, 31] and the multifractal detrended fluctuation analysis (MF-DFA) [32]. A time series of the price fluctuations possessing multifractal nature usually has either fat tails in the distribution or long-range temporal correlation or both [32]. However, possessing long memory is not sufficient for the precence of multifractality and one has to have a nonlinear process with long-memory in order to have multifractality [33]. In many cases, the null hypothesis that the reported multifractal nature is stemmed from the large fluctuations of prices can not be rejected [34].

Here, we propose to investigate the multifractal nature of absolute returns of stocks based on the multiplier method, again, borrowed from turbulence [35, 36, 37, 38]. Our goal is to provide direct evidence of scale invariance in the distribution of the multipliers. The concept of multiplier was originally introduced by Novikov to describe the intermittency and scale self-similarity in turbulent flows [39]. The scale-invariant multiplier distribution is argued to be more basic than the standard curve [35, 36]. In addition, it allows us to extract both positive and negative parts of the function with exponentially less computational time and is more accurate than conventional box-counting methods [35, 36].

2 Description of the data set

We adopt a nice high-frequency data set recording the S&P 500 index to ensure better statistics in our analysis. The record contains quoted prices of the index, covering eighteen years from Jan. 1, 1982 to Dec. 31, 1999. The sampling interval is one minute. As usual, the nontrading time periods are treated as frozen such that we count merely the time during trading hours and remove closing hours, weekends, and holidays from the data. The size of the data set is about 1.7 million.

The return over a time scale is defined as follows

| (1) |

whose absolute is a measure of the volatility. In this letter, the time scale is min. We can construct an additive measure in the time interval , which is the sum of absolute returns:

| (2) |

The quantity is actually a measure of the volatility on the time interval [40]. The time series is partitioned into boxes of identical size . Each of these mother boxes is further divided into daughter boxes. The multiplier is determined by the ratio of the measure on a daughter box to that on her mother box [36]. Therefore, the multiplier is dependent of and and can be denoted as when necessary.

3 Scale invariant distribution

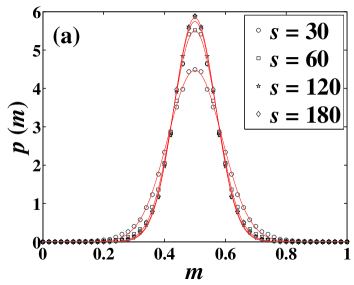

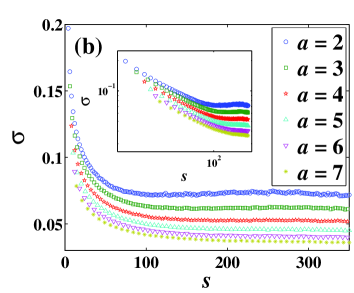

Figure 1(a) presents the probability densities of the multiplier for four different box sizes , , , and with the same base . All curves are symmetric with respect to such that by definition and close to Gaussian. The solid lines are the best fits to normal distributions, whose fitted standard deviations are for , for , for , and for , respectively. The corresponding r.m.s. of the fit residuals are , , , and . Note that the mean is fixed in the fitting procedure. It is evident that decreases in regard to and tends to a constant for large . This phenomenon is further manifested by Fig. 1(b), which plots the sample standard deviation of the multipliers as a function of the box size for different base . The inset shows the loglog plots of against .

One can see that there are two regimes in the versus relation: decays as a power law for small and saturates to a constant for large . Roughly speaking, the crossover values of are the following: for , for , for , for , for , and for , respectively. In other words, the sample variance in the case of has the fastest convergence rate to a constant.

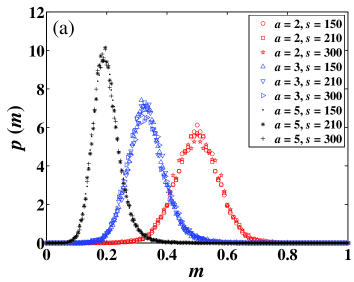

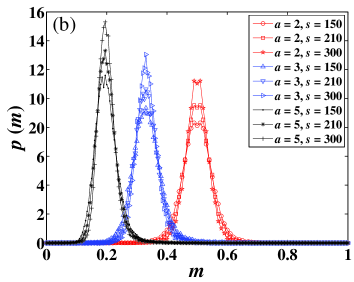

Figure 2(a) shows the empirical probability density functions of the multipliers for different bases , , and and different box sizes , , and . For each , remains invariant in respect to when . In other words, there is a scaling range in which the volatility multiplier is scale invariant, whose distribution is independent of . We shuffled the return series and found that the multiplier distributions are not scale invariant and the scaling range of disappears, as illustrated in Fig. 2(b). Therefore, can be reduced to in the scaling range. The shuffling test shows that long memory in the volatility plays an essential role in the appearance of scale invariance.

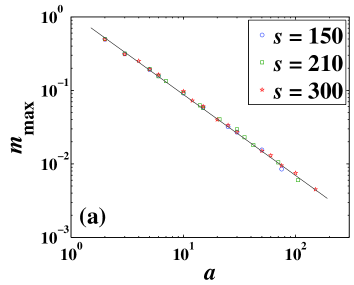

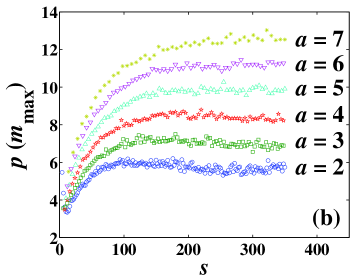

The most probable multipliers are also investigated in this work. For a given , the most probable multiplier with base is estimated such that . Figure 3(a) presents the loglog plots of versus for different values of . One can observe that the data points for different collapse on a single line, showing a power-law dependence

| (3) |

where for , for , and for , respectively. Intuitively, since a mother box is divided into daughter boxes, the sum of the multipliers is one and the multipliers is expected to aggregate around . However, it is noteworthy that this power-law dependence is nontrivial, which does not hold in turbulence [36, 41, 42]. In Fig. 3(b) is shown as a function of for different . It is evident that increases with and then approaches a plateau when . Figure 3 further verifies the scale-invariant nature of the volatility multiplier.

4 Multifractal analysis

It is shown that, for any two bases and , the density functions are related through Mellin transform in the following form [36]

| (4) |

where stands for Mellin transform. Equivalently, we have

| (5) |

The scaling exponent of the moment of can be obtained as follows [35, 36]

| (6) |

where is the fractal dimension of the support of the measure. In the current case, we have . Note that the use of the Mellin transform may indeed appear natural in the framework of scaling and power-like functions, for instance, in the analysis of Weierstrass-type functions [43].

The local singularity exponent and its spectrum are related to through Legendre transforms: and . It follows that [35, 36, 44, 45, 46]

| (7) |

and

| (8) |

Equations (5-8) predict that each of these characteristic multifractal arguments for fixed converges to constant in the scaling range and are independent of the base as well.

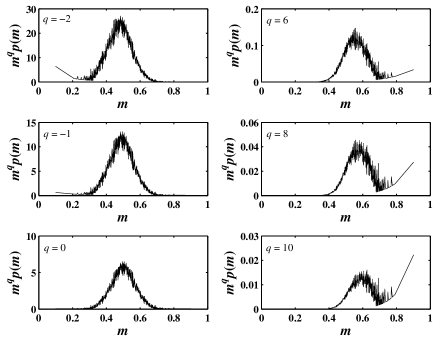

In order to test this prediction, we have to calculate first the scaling function which requires that the integrand converges for a given [47, 48]. We have investigated for different values of , , and . A typical dependence of as a function of is shown in Fig. 4 for different values of with fixed box size and base . The integrand diverges for large when is larger than 6. We shall nevertheless investigate scaling functions for for comparison. Moreover, Fig. 4 indicates that the integrand diverges when and the associated negative moments do not exist. This is a direct consequence of the fact that . Indeed, there are time moments when the local returns are zero so that the probability density at is apart from zero, i.e., . Approximately, for a small number , is a constant for . Posing , we have . Therefore, we have , which is quite analogous to the situation in turbulence [49].

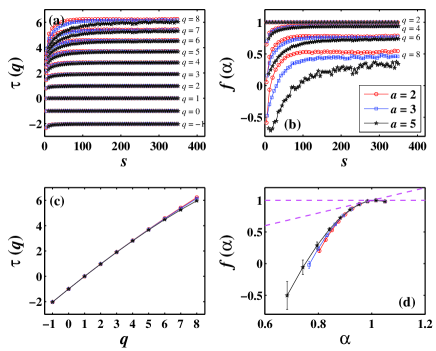

We now present in Fig. 5 the results of the multifractal analysis for varying from to . In Fig. 5(a) is shown the dependence of the scaling function upon the box size for different values of and . It is evident that, for large , is independent of for every under investigation. The function reaches constant faster for small . These results are in excellent agreement with the theoretical predictions. Figure 5(b) shows the dependence of the singularity spectrum on the box size for different values of and . Again, we witness a range of scale invariance in which is independent of . What needs to be emphasized is that, for , the three curves with different do not converge due to bad statistics as shown by the left-middle panel of Fig. 4. We plot the three scaling functions for , , and with respect to in Fig. 5(c). The error bars are estimated as the standard deviation over different . Except for large , the three curves collapse on a single nonlinear curve. In addition, Fig. 5(d) shows the three singularity spectra in respect to the local singularity exponent for the three bases. Again, the three curves collapse remarkably on a single curve when is not too large. Both Fig. 5(c) and Fig. 5(d) strongly indicate that the volatility multiplier possesses multifractal nature.

An important feature of multifractals is the possible existence of negative dimensions in the multifractal spectrum, that is, for large or small [50]. Negative dimensions are more common if the multiplier distribution is continuous [36, 44, 45, 46]. Figure 5(d) also shows that there are negative dimensions for large especially when is large. However, we should be cautious that the part of might be an artifact of bad statistics for large and , as shown by the right panel of Fig. 4 and Fig. 5(b) as well. Since the multifractal functions are more reliable statistically for , we argue that there is no negative dimension for . More data are required to investigate higher order moments and the issue of the existence of negative dimensions is still open.

In the development of Econophysics, the literature has witnessed increasing analogues between turbulence and finance. Multiplier analysis is a well-established method in the description of conservative quantities in turbulence [39, 35, 36, 37, 38]. Novikov predicted that the multiplier distribution is independent of the scale as long as is well inside the inertial subrange [39]. Our finding provides further evidence of the analogue between turbulence and finance, except that the existence of negative dimensions that was reported in turbulence is not confirmed in our financial data. Moreover, the energy dissipation multiplier with follows approximately a triangular distribution, which is much flatter than the normal distribution of volatility multiplier in this work.

5 Conclusion

In summary, we have employed the multiplier method to investigate the volatility of high-frequency data of the S&P 500 index. The distribution of volatility multiplier is found to be independent of the time scale for different when is larger than some crossover scale . We unraveled that the volatility multipliers are scale invariant and have multifractal nature, which is independent of the construction of the multipliers (characterized by and ) in the scaling range.

Acknowledgments:

This work was partially supported by the National Natural Science Foundation of China (Grant No. 70501011) and the Fok Ying Tong Education Foundation (Grant No. 101086).

References

- [1] L. Bachelier, Théorie de la Spéculation, Ph.D. thesis, University of Paris, Paris (March 29 1900).

- [2] B. B. Mandelbrot, Fractals and Scaling in Finance, Springer, New York, 1997.

- [3] R. N. Mantegna, H. E. Stanley, Scaling behaviour in the dynamics of an economic index, Nature 376 (1995) 46–49.

- [4] S. Ghashghaie, W. Breymann, J. Peinke, P. Talkner, Y. Dodge, Turbulent cascades in foreign exchange markets, Nature 381 (1996) 767–770.

- [5] R. N. Mantegna, H. E. Stanley, Turbulence and financial markets, Nature 383 (1996) 587–588.

- [6] N. Vandewalle, M. Ausloos, Sparseness and roughness of foreign exchange rates, Int. J. Mod. Phys. C 9 (1998) 711–719.

- [7] F. Schmitt, D. Schertzer, S. Lovejoy, Multifractal analysis of foreign exchange data, Appl. Stoch. Models Data Analysis 15 (1999) 29–53.

- [8] K. Ivanova, M. Ausloos, Low -moment multifractal analysis of Gold price, Dow Jones Industrial Average and BGL-USD exchange rate, Eur. Phys. J. B 8 (1999) 665–669.

- [9] R. Baviera, M. Pasquini, M. Serva, D. Vergni, A. Vulpiani, Correlations and multi-affinity in high frequency financial datasets, Physica A 300 (2001) 551–557.

- [10] S. V. Muniandy, S. C. Lim, R. Murugan, Inhomogeneous scaling behaviors in Malaysian foreign currency exchange rates, Physica A 301 (2001) 407–428.

- [11] R. Xu, Z.-X. Gençay, Scaling, self-similarity and multifractality in FX markets, Physica A 323 (2003) 578–590.

- [12] K. Matia, Y. Ashkenazy, H. E. Stanley, Multifractal properties of price fluctuations of stock and commodities, Europhys. Lett. 61 (2003) 422–428.

- [13] A. Turiel, C. J. Pérez-Vicente, Multifractal geometry in stock market time series, Physica A 322 (2003) 629–649.

- [14] P. Oświȩcimka, J. Kwapień, S. Drożdż, R. Rak, Investigating multifractality of stock market fluctuations using wavelet and detrending fluctuation methods, Acta Physica Polonica B 36 (2005) 2447–2457.

- [15] L. Olsen, Multifractal geometry, Progress in Probability 46 (2000) 3–37.

- [16] A. Turiel, C. J. Pérez-Vicente, Role of multifractal sources in the analysis of stock market time series, Physica A 355 (2005) 475–496.

- [17] P. Norouzzadeh, G. R. Jafari, Application of multifractal measures to Tehran price index, Physica A 356 (2005) 609–627.

- [18] A. Bershadskii, Multifractal diffusion in NASDAQ, J. Phys. A 34 (2001) L127–130.

- [19] X. Sun, H.-P. Chen, Z.-Q. Wu, Y.-Z. Yuan, Multifractal analysis of Hang Seng index in Hong Kong stock market, Physica A 291 (2001) 553–562.

- [20] X. Sun, H.-P. Chen, Y.-Z. Yuan, Z.-Q. Wu, Predictability of multifractal analysis of Hang Seng stock index in Hong Kong, Physica A 301 (2001) 473–482.

- [21] I. Andreadis, A. Serletis, Evidence of a random multifractal turbulent structure in the Dow Jones Industrial Average, Chaos Solitons & Fractals 13 (2002) 1309–1315.

- [22] A. Z. Górski, S. Drożdż, J. Speth, Financial multifractality and its subtleties: An example of DAX, Physica A 316 (2002) 496–510.

- [23] M. Ausloos, K. Ivanova, Multifractal nature of stock exchange prices, Computer Physics Communications 147 (2002) 582–585.

- [24] M. Balcilar, Multifractality of the Istanbul and Moscow stock market returns, Emerging Markets Finance and Trade 39 (2) (2003) 5–46.

- [25] K. E. Lee, J. W. Lee, Multifractality of the KOSPI in Korean stock market, J. Korean Phys. Soc. 46 (2005) 726–729.

- [26] K. E. Lee, J. W. Lee, Origin of the multifractality of the Korean stock-market index, J. Korean Phys. Soc. 47 (2005) 185–188.

- [27] J. W. Lee, K. E. Lee, P. A. Pikvold, Multifractal behavior of the Korean stock-market index KOSPI, Physica A 364 (2006) 355–361.

- [28] Y. Wei, D.-S. Huang, Multifractal analysis of SSEC in Chinese stock market: A different empirical result from Heng Seng, Physica A 355 (2005) 497–508.

- [29] M. Holschneider, On the wavelet transformation of fractal objects, J. Stat. Phys. 50 (1988) 953–993.

- [30] J.-F. Muzy, E. Bacry, A. Arnéodo, Wavelets and multifractal formalism for singular signals: Application to turbulence data, Phys. Rev. Lett. 67 (1991) 3515–3518.

- [31] J.-F. Muzy, E. Bacry, A. Arnéodo, Multifractal formalism for fractal signals: The structure-function approach versus the wavelet-transform modulus-maxima method, Phys. Rev. E 47 (1993) 875–884.

- [32] J. W. Kantelhardt, S. A. Zschiegner, E. Koscielny-Bunde, S. Havlin, A. Bunde, H. E. Stanley, Multifractal detrended fluctuation analysis of nonstationary time series, Physica A 316 (2002) 87–114.

- [33] A. Saichev, D. Sornette, Generic multifractality in exponentials of long memory processes, Phys. Rev. E 74 (2006) 011111.

- [34] T. Lux, Detecting multifractal properties in asset returns: The failure of the “scaling estimator”, Int. J. Mod. Phys. C 15 (2004) 481–491.

- [35] A. B. Chhabra, K. R. Sreenivasan, Negative dimensions: Theory, computation and experiment, Phys. Rev. A 43 (1991) 1114–1117.

- [36] A. B. Chhabra, K. R. Sreenivasan, Scale-invariant multiplier distribution in turbulence, Phys. Rev. Lett. 68 (1992) 2762–2765.

- [37] B. Jouault, P. Lipa, M. Greiner, Multiplier phenomenology in random multiplicative cascade processses, Phys. Rev. E 59 (1999) 2451–2454.

- [38] B. Jouault, M. Greiner, P. Lipa, Fix-point multiplier distributions in discrete turbulent cascade models, Physica D 136 (2000) 125–144.

- [39] E. A. Novikov, Intermittency and scale similarity in the structure of a turbulent flow, J. Appl. Math. Mech. 35 (1971) 231–241.

- [40] B. Bollen, B. Inder, Estimating daily volatility in financial markets utilizing intraday data, J. Emp. Fin. 9 (2002) 551–562.

- [41] J. Molenaar, J. Herweijer, W. van de Water, Negative dimensions of the turbulent dissipation field, Phys. Rev. E 52 (1995) 496–509.

- [42] R. Kluiving, R. A. Pasmanter, Stochastic selfsimilar branching and turbulence, Physica A 228 (1996) 273–294.

- [43] S. Gluzman, D. Sornette, Log-periodic route to fractal functions, Phys. Rev. E 65 (2002) 036142.

- [44] W.-X. Zhou, Z.-H. Yu, On the properties of random multiplicative measures with the multipliers exponentially distributed, Physica A 294 (2001) 273–282.

- [45] W.-X. Zhou, H.-F. Liu, Z.-H. Yu, Anormalous features arising from random multifractals, Fractals 9 (2001) 317–328.

- [46] W.-X. Zhou, Z.-H. Yu, Multifractality of drop breakup in the air-blast nozzle atomization process, Phys. Rev. E 63 (2001) 016302.

- [47] V. S. L’vov, E. Podivilov, A. Pomyalov, I. Procaccia, D. Vandembroucq, Improved shell model of turbulence, Phys. Rev. E 58 (1998) 1811–1822.

- [48] W.-X. Zhou, D. Sornette, W.-K. Yuan, Inverse statistics and multifractality of exit distances in 3D fully developed turbulence, Physica D 214 (2006) 55–62.

- [49] B. R. Pearson, W. van de Water, Inverse structure functions, Phys. Rev. E 71 (2005) 036303.

- [50] B. B. Mandelbrot, Negative fractal dimensions and multifractals, Physica A 163 (1990) 306–315.