Modeling long-range cross-correlations in two-component

ARFIMA and FIARCH processes

Boris Podobnik

Davor Horvatic

Alfonso Lam Ng

H. Eugene Stanley

Plamen Ch. Ivanov

Department of Physics, Faculty of Civil Engineering, University of Rijeka,

Rijeka, Croatia

Zagreb School of Economics and Management,

Zagreb, Croatia

Department of Physics, Faculty of Science, University of Zagreb,

Zagreb, Croatia

Center for Polymer Studies and Department of

Physics, Boston University, Boston, MA 02215

Division of Sleep Medicine, Brigham and Woman’s Hospital, Harvard

Medical School, Boston, MA 02115

Institute of Solid State Physics, Bulgarian Academy of Sciences,

Sofia, Bulgaria

Abstract

We investigate how simultaneously recorded

long-range power-law correlated

multivariate signals cross-correlate. To this end we introduce a

two-component ARFIMA stochastic process and a two-component

FIARCH process to generate coupled fractal

signals with long-range power-law correlations which are at the same time

long-range cross-correlated. We study how the degree of cross-correlations

between these signals depends on the scaling exponents characterizing the

fractal correlations in each signal and on the coupling between the signals.

Our findings have relevance when studying parallel outputs of

multiple-component

of physical, physiological and social systems.

Many empirical data are characterized by

long-range power-law auto-correlations as well as by

long-range cross-correlations.

Such scale-invariant organization in both auto-correlations and

cross-correlations can be observed either for the data variables or their

absolute values

[1, 2, 3, 4, 5, 6, 7, 8, 9].

Scale-invariant power-law auto-correlations in stochastic variables

can be

modeled by the fractionally autoregressive

integrated moving-average process (ARFIMA)

[10, 11]:

(1)

where is a scaling parameter,

denotes independent and identically

distributed (i.i.d.) Gaussian variables with and ,

are the weights defined by , where

denotes the

Gamma function and is the time scale.

We denote the auto-correlation function

for as . For

the generated variable becomes random.

To account for power-law cross-correlations

between two variables and

,

where each variable is itself power-law auto-correlated,

we propose a two-component ARFIMA stochastic process defined by two

stochastic variables and .

Each of these variables at any time depends not

only on its own past values but also on past values of the

other variable:

(2a)

(2b)

(2c)

(2d)

where and

denote i.i.d. Gaussian variables with and ,

and are the

weights defined in Eq. (1) through the scaling parameters

and (),

and is a free parameter controlling the coupling strength

between and ().

We denote the cross-correlation function between

and as .

For different values of a different degree of cross-correlation

between the variables and is observed. For example,

for the case when , the process defined in

Eqs. (2a)-(2d)

reduces to two decoupled ARFIMA processes defined in

Eq. (1). Thus, when the long-range cross-correlations

between and vanish, while both and remain

long-range power-law auto-correlated.

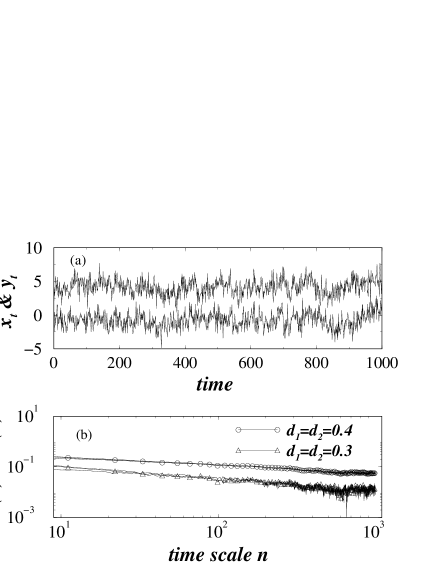

Figure 1: (a) Time series and for the process defined in

Eqs.(2a)-(WSigy)

where and . The time series

is vertically shifted for clarity. Both and exhibit

apparent comovement, indicating a high degree of cross-correlation.

(b) Log-log plots of the

auto-correlation functions for and ,

and their cross-correlation function for the

two-component ARFIMA process

with and (top three curves), and with

and (bottom three curves).

For decreasing values of the scaling parameters and

both the auto-correlations and

cross-correlations decrease, leading to smaller values of and .

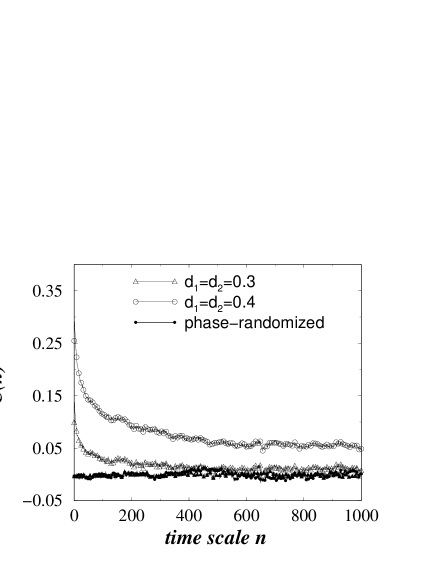

Figure 2: Cross-correlation function before

Fourier phase-randomization procedure for

the time series and shown in Fig. 1 (open symbols).

After Fourier phase randomization

of and the cross-correlation

function virtually disappears (filled symbols) for any

value of and .

In Fig. 1(a) we show segments of the time series and

generated by the process defined in Eq. (2a)-(2d)

with parameters and .

Both variables exhibit a very similar comovement.

In Fig. 1(b) we show the auto-correlation functions

for and ,

as well as the cross-correlation function .

These three curves practically overlap [Fig. 1(b), three top curves].

We also show the same

correlation functions for and [Fig. 1(b),

three bottom

curves]. Generally,

when the coupling parameter is kept fixed,

the stochastic process we introduce

in Eq. (2) generates stronger cross-correlations

for larger values of the scaling parameters and .

Motivated by the fact that for linear processes the auto-correlation

function

does not change under randomization of the Fourier phase

[13, 14], we next

test how this phase-randomization procedure

affects the degree of cross-correlation between and .

First, we perform a Fourier transform of

the original time series, e.g. ,

preserving the Fourier amplitudes

but randomizing the Fourier phases. Then, we perform

an inverse Fourier transform

and obtain a surrogate (linearized) time series .

Applying this phase-randomization procedure to

both time series and generated by the

two-component ARFIMA process

in Eq. (2), we calculate

the two auto-correlation functions for

and , as well as their

cross-correlation function

.

As expected, the

auto-correlation functions remain unchanged after Fourier

phase randomization,

but the

cross-correlation function

completely vanishes [Fig. 2].

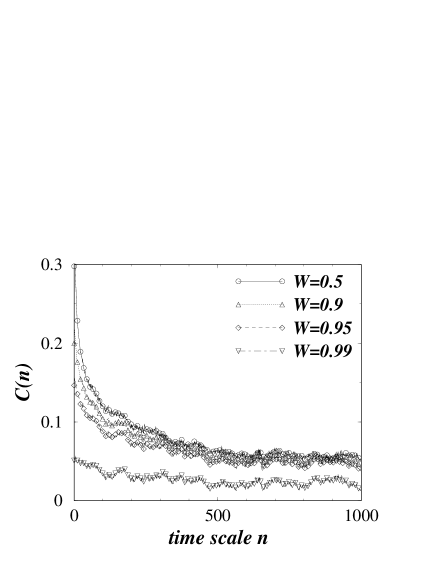

Next, we investigate the case when the scaling parameters

and are fixed,

while the coupling parameter varies.

In Fig. 3, we show how the cross-correlation function changes

for different values of

and for fixed . The closer the value of the

parameter to 1, the weaker the cross-correlations

( corresponds to the case of two

decoupled ARFIMA processes).

Figure 3: Cross-correlation function between time series and

generated by the process in Eqs.(2) for varying values of and

.

The cross-correlation function has highest values for , and

tends to zero for approaching 1. When ,

and become two decoupled ARFIMA processes.

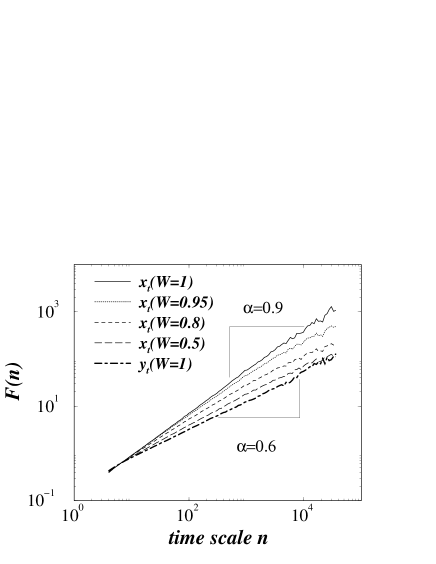

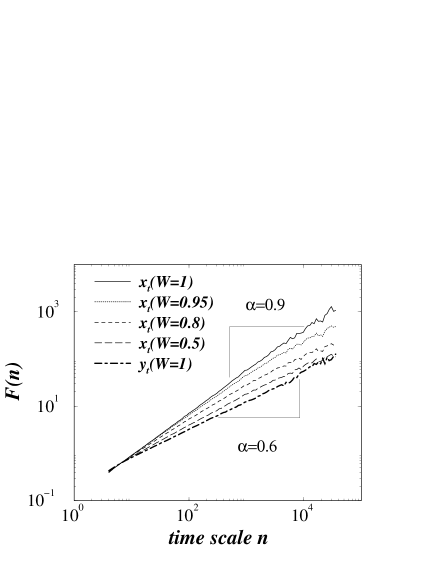

Figure 4: DFA scaling

curves for the time series

and generated by the two-component ARFIMA

process in Eqs. (2a)-(2d),

where and . For , and

are decoupled and thus not cross-correlated, and behaves as

the ARFIMA process in Eq. (1)

defined only by the scaling parameter

, while

becomes a separate ARFIMA process defined only by the

scaling parameter .

For , the scaling properties of

depend on both parameters and .

When , the

DFA correlation exponent

for becomes equal to the DFA correlation exponent for

. The DFA exponent for does not depend on .

Next we analyze how the degree of power-law

auto-correlations changes

when varying the parameters , , and in

Eqs. (2a)-(2d).

To quantify the auto-correlations

we employ the detrended fluctuations analysis

(DFA) method. We estimate the rms fluctuation

function for different time scales [15, 16, 17, 18, 19].

A power-law dependence of on the time scale —

,

where is the correlation exponent — indicates presence

of power law auto-correlations.

In Fig. 4, we show the DFA scaling curves obtained for

and generated by the two-component ARFIMA process

in Eqs. (2a)-(2d), where and , and the coupling parameter

varies.

For the processes and are decoupled and thus

not cross-correlated. In this case,

behaves as a power-law auto-correlated

ARFIMA process controlled by only the scaling parameter

, with the DFA correlation exponent equals

. Similarly,

becomes a separate ARFIMA process (decoupled from )

which is controlled only by the scaling parameter ,

where . We find that

with decreasing value of (from 1 to 0.5), becomes a mixture of

two ARFIMA processes and the DFA correlation exponent

gradually decreases towards

corresponding to the process, controlled

by parameter . In contrast to , for the process

the DFA correlation exponent

virtually does not change with varying the coupling parameter .

We next consider a separate stochastic process which generates

simultaneously two time series with

power-law auto-correlated absolute

values of their variables and long-range cross-correlations

between these absolute values.

Power-law auto-correlations in the absolute values of the stochastic variables

can be modeled by

the Fractionally Integrated ARCH (FIARCH) process

[20, 12]:

(3a)

(3b)

where denotes an i.i.d. Gaussian variable

with and , and

and .

The sum of the weights satisfies

,

yielding .

While for the time series generated by Eq. (1)

the autocorrelation function

is zero for all time scales ,

for the absolute values the auto-correlation function is

, which for

converges to the power law

.

To account for power-law cross-correlations between

the absolute values of two variables,

where the absolute values of each variable

are simultaneously power-law auto-correlated,

we have previously introduced [21]

a two-component FIARCH process

with scaling parameters

and :

(4a)

(4b)

(4c)

(4d)

where and are

i.i.d. variables

with and ,

is the coupling parameter controlling

the degree of cross-correlations,

and and .

Note, that each of the variables is controlled by a

composite volatility — e.g. for the composite volatility

is [Eq. (4a)] —

that is a combination of two FIARCH volatilities

and [Eq. (3b)].

Stability of the FIARCH process is achieved through the condition

. To retain stability for the

two-component FIARCH process in Eq. (4), the average values of the composite

volatilities

and

in Eqs. (4a)-(4b) should be 1.

For the process in

Eqs. (4a)-(4d) reduces to two decoupled

FIARCH process as defined in

Eqs. (3b)-(3b), and thus

and are not cross-correlated.

In Ref. [21] we have analyzed the

cross-correlation functions between and

for the process defined in Eqs. (4a)-(4d)

for varying values of the

parameters , , and .

Figure 5: DFA scaling curves

of the time series and generated by the

two-component FIARCH

process in Eqs. (4a)-(4d),

where and . For , and

are decoupled and thus are not cross-correlated. In this case,

becomes a separate FIARCH process as defined in

Eqs. (3), and the auto-correlation

properties of depend only on the scaling parameter , while

is another FIARCH process with auto-correlation

properties depending only on the parameter

.

For , the scaling properties of

depend on both parameters and .

When , the

DFA correlation exponent

for becomes equal to the DFA correlation exponent for

. Note that the

DFA exponent for does not depend on .

Finally, we analyze how the auto-correlations in the absolute values

change

when varying the parameters , , and .

In Fig. 5, we show the DFA scaling curves

for and , and for varying

. For , the time series

and are decoupled and so not cross-correlated.

In this case, is a FIARCH process

controlled only by the scaling parameter

, and exhibits long-range power-law auto-correlations

characterized by a

DFA correlation exponent .

Similarly,

is another FIARCH process controlled only by , and

characterized by

. We find that

with decreasing value of (from 1 to 0), is controlled

by both parameters and ,

and the DFA exponent gradually decreases towards

the value .

At the same time, the process which is controlled

only by the parameter is also characterized

by , regardless of the values of .

The presented modeling approach and findings may have relevance

when quantifying cross-correlations in simultaneously recorded multivariate

time series of fractal nature. This problem is pertinent

to multiple component physical [22, 23, 24], physiological, social

and financial

systems.

We thank the Ministry of Science of Croatia,

NIH (Grant HL071972) and NSF for

financial support.

References

[1] C. C. Ying, Econometrica 34, (1966) 676.

[2] R. L. Crouch, Financial Analystss Journal 26

(1970) 104.

[3] G. Tauchen and M. Pitts,

Econometrica 51, (1983) 485.

[4] J. Karpoff,

Journal of Financial and Quantitative Analysis 22 (1987) 109.

[5] R. Gallant, P. Rossi, and G. Tauchen,

Review of Financial Studies 5 (1992) 199.

[6] J. Campbell, A. W. Lo and A. MacKinlay,

The Econometrics of Financial Markets

Princeton NJ: Princeton University Press (1997).

[7] V. Plerou et al.,

Quantitative Finance 1 (2001) 262.

[8] P. Gopikrishnan et al.,

Physical Review E 62 (2000) 4493.

[9] B. LeBaron, W. B. Arthur, and R. Palmer,

Journal of Economic Dynamic & Control 23, (1999) 1487.

[10] C. W. J. Granger and R. Joyeux,

J. Time Series Analysis 1, (1980) 15.

[11] J. Hosking, Biometrika 68, (1981) 165.

[12] B. Podobnik et al.,

Phys. Rev. E 72, (2005) 026121.

[13] J. Theiler et al., Physica D 58, (1992)

77.

[14]

Y. Ashkenazy et al.,

Physica A 323, (2003) 19.

[15]

C.-K. Peng et al., Phys. Rev. E 49, (1994) 1685.

[16]

K. Hu et al.,

Phys. Rev. E 64(1) (2001) 011114(19).

[17] Z. Chen et al.,

Phys. Rev. E 65(4) (2002) 041107(15).

[18] Z. Chen et al.,

Phys. Rev. E 71(1) (2005) 011104(11).

[19]

L. Xu et al.,

Phys. Rev. E 71(5) (2005) 051101(14).

[20] C. W. J. Granger and Z. Ding

Annales d’Economie et de Statistique 40 (1995) 67.

[21] B. Podobnik et al.,

Eur. Phys. J. B 56, (2007) 47.

[22] G. Nugent-Glandorf et al.,

Phys. Rev. Lett. 87(19) (2001) 193002.

[23] O. A. Godin,

Phys. Rev. Lett. 97 (2006) 054301.

[24] M. Campilo and A. Paul, Science 299 (2003) 547.