Gibbs Sampling for a Bayesian Hierarchical General Linear Model

Abstract

We consider a Bayesian hierarchical version of the normal theory general linear model which is practically relevant in the sense that it is general enough to have many applications and it is not straightforward to sample directly from the corresponding posterior distribution. Thus we study a block Gibbs sampler that has the posterior as its invariant distribution. In particular, we establish that the Gibbs sampler converges at a geometric rate. This allows us to establish conditions for a central limit theorem for the ergodic averages used to estimate features of the posterior. Geometric ergodicity is also a key component for using batch means methods to consistently estimate the variance of the asymptotic normal distribution. Together, our results give practitioners the tools to be as confident in inferences based on the observations from the Gibbs sampler as they would be with inferences based on random samples from the posterior. Our theoretical results are illustrated with an application to data on the cost of health plans issued by health maintenance organizations.

1 Introduction

The flexibility of Bayesian hierarchical models makes them widely applicable. One of the most popular (see, e.g., Gelman et al., 2004; Spiegelhalter et al., 2005) is a version of the usual normal theory general linear model. Let denote an response vector and suppose is a vector of regression coefficients, is a vector, is a known design matrix having full column rank, and is a known matrix. Then for , the hierarchy is

| (1) |

where the mixture parameters , , and are known nonnegative constants which satisfy

and we say if it has density proportional to for . Further, we require and to be a posteriori conditionally independent given , , and which holds if and only if . Finally, and positive definite matrix are known and the hyperparameters , , , and are all assumed to be positive.

Let and . Then the posterior has support and a density characterized by

where is the observed data and denotes a generic density. Posterior inference is often based on the expectation of a function with respect to the posterior. For the model (1) we can only rarely calculate the expectation

since it is a ratio of two potentially high-dimensional intractable integrals. Hence inference regarding the posterior may require Markov chain Monte Carlo (MCMC) methods. We consider two-component Gibbs sampling which produces a Harris ergodic Markov chain with invariant density .

Suppose and we obtain observations from the Gibbs sampler. Then a natural estimate of is since with probability 1 as . In other words, the longer we run the Gibbs sampler, the better our estimate is likely to be. However, this gives no indication of how large must be to ensure the Monte Carlo error is sufficiently small. The size of this error is usually judged by appealing to its approximate sampling distribution via a Markov chain central limit theorem (CLT), which in the cases of current interest takes the form

| (2) |

where . Due to the serial correlation in , the variance will be complicated and require specialized techniques (such as batch means or spectral methods) to estimate consistently with , say. Suppose with probability 1 as . In this case, an asymptotically valid Monte Carlo standard error (MCSE) is given by . In turn, this can be used to perform statistical analysis of the Monte Carlo error and to implement rigorous sequential stopping rules for determining the length of simulation required (see Flegal et al., 2008; Jones and Hobert, 2001) so that the user will have as much confidence in the simulation results as if the observations were a random sample from the posterior; this is described in more detail in Section 4.

Unfortunately, for Harris ergodic Markov chains simple moment conditions are not sufficient to ensure an asymptotic distribution for the Monte Carlo error or that we can consistently estimate . In addition, we need to know that the convergence of occurs rapidly. Thus, one of our goals is to establish verifiable conditions under which the Gibbs sampler is geometrically ergodic, that is, it converges to the posterior in total variation norm at a geometric rate.

We know of three papers that address geometric ergodicity of Gibbs samplers in the context of the normal theory linear model with proper priors. These are Hobert and Geyer (1998), Jones and Hobert (2004), and Papaspiliopoulos and Roberts (2008). The linear model we consider substantively differs from those in Papaspiliopoulos and Roberts (2008) in that we do not assume the variance components are known. Our model is also much more general than the one-way random effects model in Hobert and Geyer (1998) and Jones and Hobert (2004). Gibbs sampling for the balanced one-way random effects model is also considered in Rosenthal (1995) where coupling techniques were used to establish upper bounds on the total variation distance to stationarity. However, these results fall short of establishing geometric ergodicity of the associated Markov chain.

The rest of this paper is organized as follows. Gibbs sampling for the Bayesian hierarchical general linear model is discussed in Section 2 and geometric ergodicity for these Gibbs samplers is established in Section 3. Conditions for the CLT (2) are given in Section 4 along with a description of the method of batch means for estimating the variance of the asymptotic normal distribution. Finally, our results are illustrated with a numerical example in Section 5. Many technical details are deferred to the appendix.

2 The Gibbs Samplers

The full conditional densities required for implementation of the two-component block Gibbs sampler are as follows: Conditional on and , follows the distribution corresponding to density

| (3) |

where denotes a Gamma() density and denotes a Gamma() density with

| (4) |

Also,

where

| (5) |

These follow from our assumption that .

There are two possible update orders for our 2-component Gibbs sampler. First, let denote the Markov chain produced by the Gibbs sampler which updates followed by in each iteration so that a one-step transition looks like . Then the one-step Markov transition density (Mtd) for is

Similarly, let denote the Markov chain produced by the Gibbs sampler which updates followed by in each iteration so that the one-step transition is . Then the corresponding Mtd is

Also, let and denote the associated marginal chains with Mtds

and

respectively.

Because the Mtd’s are strictly positive on the state space it is straightforward to show that and are Harris ergodic. The posterior density is invariant for and by construction. Moreover, it is easy to see that both chains are Feller. Similarly, and are Harris ergodic and Feller with invariant densities the marginal posteriors and , respectively. Hence all four Markov chains converge in total variation norm to their respective invariant distributions. In the next section we establish conditions under which this convergence occurs at a geometric rate.

3 Geometric Ergodicity

3.1 Establishing Geometric Ergodicity

Our main goal in this section is to establish conditions for the geometric ergodicity of and . Before doing so it is useful to acquaint ourselves a concept introduced by Roberts and Rosenthal (2001). Let be a Markov chain on a space and a stochastic process on a possibly different space . Then is de-initializing for if, for each , conditionally on it follows that is independent of . Roughly speaking, Roberts and Rosenthal (2001) use this concept to show that controls the convergence properties of the Markov chain .

To establish the geometric ergodicity of and it suffices to work with the marginal chains and . First, is de-initializing for and is de-initializing for . Results in Roberts and Rosenthal (2001) imply that if () is geometrically ergodic, so is (). Further, and are co-de-initializing. Hence if one is geometrically ergodic, then they both are and Lemma 3.1 follows directly.

Lemma 3.1.

If or is geometrically ergodic, then so are and .

Accordingly, we can proceed by studying the convergence behavior of the marginal chains. We establish geometric ergodicity for by establishing a drift condition. That is we need to specify a function and constants and such that

| (6) |

where the expectation is taken with respect to the Mtd . Let , and . Jones and Hobert (2004, Lemma 3.1) show that equation (6) implies

Here is the drift, (or ) is a drift function and a drift rate. If the expected change in is negative so will tend to “drift” to , that is, where the value of is small. Moreover, it also does it in such a way that the drift towards is faster when is small. On the other hand, if the drift will be slow. Thus the value of is intimately connected to the convergence rate of ; for a thorough accessible discussion of the connection see Jones and Hobert (2001, Section 3.3). Hence examination of can give us some intuition for the convergence behavior of . However, drift functions are not unique so this examination generally will not lead to definitive conclusions.

A function is unbounded off compact sets if the set is compact for any . Note that the maximal irreducibility measure for is equivalent to Lebesgue on so that its support certainly has a non-empty interior. The sufficiency of drift for geometric ergodicity now follows easily from Lemma 15.2.8 and Theorems 6.0.1 and 15.0.1 of Meyn and Tweedie (1993) and Lemma 3.1.

Proposition 3.1.

Suppose (6) holds for a drift function that is unbounded off compact sets. Then is geometrically ergodic and so are and .

3.2 Drift for

For all and , define constants

| (7) |

Also, let and denote the th rows of matrices and , respectively, and let and denote the th elements of vectors and , respectively. Next, for define

where denotes expectation with respect to the distribution.

Proposition 3.2.

Proof.

See Appendix A.2.∎

Notice that the formulations of given by Proposition 3.2 depend on the Bayesian model setting through , , , and . Therefore, the drift and convergence rates of the marginal chain (hence the Gibbs samplers) may be sensitive to changes in the dimension of , the total number of observations , or the hyperparameter setting. However, it is interesting that the dimension of , which is , has only an indirect impact on this result. Specifically, when is nonsingular the value of has no impact, that is, the drift rate is unaffected by changes in . Of course, changing does mean that changes which may impact which in turn can change the permissible hyperparameters and the drift rate when is singular.

Example 3.1.

Consider the balanced random intercept model derived from (1) for subjects with observations each. In this case, where denotes the Kronecker product and represents a vector of ones of length . Hence is nonsingular. Define

If for all , Condition 1 of Proposition 3.2 establishes drift rate . Notice that as and hence as well. This supports our intuition that the Gibbs sampler should converge more slowly as its dimension increases. On the other hand, if is held constant but increases so that , then

Thus increasing the number of observations per subject does not have the same negative, qualitative impact as increasing the number of subjects. Finally, (hence ) when is held constant and for any .

Consider the condition that for all and . The following result establishes this condition for an important special case of (1). In our experience it is often straightforward to show that is bounded and, if desired, numerical optimization methods yields appropriate .

Proposition 3.3.

Assume for all .

-

1.

If , then

for all and .

-

2.

If is nonsingular, then

for all and .

Proof.

See Appendix A.2. ∎

We are now in position to state conditions on (1) guaranteeing geometric ergodicity of the Gibbs samplers and . This follows easily from Propositions 3.1 and 3.2 if the drift function is unbounded off compact sets on . Define where . Notice that is continuous so it is sufficient to show that, on , is bounded for and is bounded for . Clearly, and it is obvious that each is bounded on hence also on . Moreover, note as . Given that the are bounded it is easy to see that as . Putting this together we see that is unbounded off compact sets. The main result of this section follows.

Theorem 3.1.

Assume the conditions of Proposition 3.1. Then the Markov chain and the Gibbs samplers and are geometrically ergodic.

4 Interval Estimation

Suppose we want to estimate an expectation where is real-valued and -integrable. It is straightforward to estimate with . A key step in the statistical analysis of is the assessment of the Monte Carlo error through its approximate sampling distribution.

Theorem 4.1.

Assume the conditions of Theorem 3.1. If for some , then there is a constant such that for any initial distribution

The proof of this theorem follows easily from Theorem 3.1, Theorem 2 of Chan and Geyer (1994) and Section 1 of Flegal and Jones (2009). Roughly speaking, results in Hobert et al. (2002), Jones et al. (2006) and Bednorz and Latuszynski (2007) show that, under conditions comparable to those required for Theorem 4.1, techniques such as regenerative simulation and batch means can be used to construct an estimator of , say , such that as almost surely. See Flegal and Jones (2009) for the conditions required to ensure consistency of overlapping batch means and spectral estimators of .

Before giving a precise discussion of the conditions for consistency we need a preliminary definition and result. Let for and be an Mtd with respect to Lebesgue measure. Suppose there exists a function and a density such that for all

Then we say there is a minorization condition for .

Lemma 4.1.

Let be compact and assume where

and some . If for each , is positive and continuous on , then there exists a minorization condition for .

Proof.

The proof follows a technique first introduced by Mykland et al. (1995). Fix . Then for all

Let be the point where the infimum is achieved. Then the minorization follows by setting and

∎

The conditions of Lemma 4.1 are not the weakest that ensure the existence of a minorization condition but they will suffice for our purposes. In particular, it is straightforward to use Lemma 4.1 to see that there exists a minorization condition for both and the Mtd’s for and , respectively. Also, Hobert et al. (2006) derived an explicit closed form expression for a minorization for a Markov chain for which is a special case.

The consistency results for in Flegal and Jones (2009), Hobert et al. (2002), Jones et al. (2006) and Bednorz and Latuszynski (2007) all require that a minorization condition hold. The efficacy of regenerative simulation is utterly dependent upon the minorization while minorization is irrelevant to the implementation of batch means and spectral methods. That is, the minorization is purely a technical device used in the proofs of consistency for batch means and spectral estimators.

We use the method of batch means in Section 5 to estimate . Let be the simulation length, and . Now define

The batch means estimate of is

| (8) |

Putting together our Theorem 3.1 and Lemma 4.1 with results in Jones et al. (2006) and Bednorz and Latuszynski (2007) we have the following consistency result.

Theorem 4.2.

Assume the conditions of Theorem 3.1. If for some set and let , then for any initial distribution for either or we have that with probability 1 as .

Using Theorems 4.1 and 4.2 we can use (8) to form an asymptotically valid confidence interval for in the usual way

| (9) |

where is a quantile from a Student’s distribution with degrees of freedom. Moreover, we can use batch means to implement the fixed-width methods of Jones et al. (2006) to determine how long to run the simulation. Following Flegal et al. (2008) let be the desired half-width of the interval in (9) and be a minimum simulation size specified by the user. Then we can terminate the simulation the first time

The final interval estimate will be asymptotically valid in the sense that the interval will have the desired coverage probability for sufficiently small ; see also Flegal et al. (2008), Flegal and Jones (2009), Glynn and Whitt (1992) and Jones et al. (2006).

5 A Numerical Example

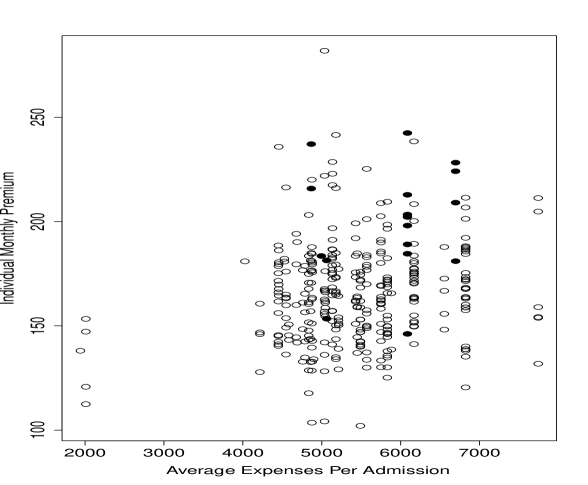

In this section we illustrate our theoretical results in the analysis of US government health maintenance organization (HMO) data. To study the cost-effectiveness of transferring military retirees from a Defense Department health plan to health plans for government employees, information was gathered from 341 state-based health maintenance organizations (HMOs). These plans represent 42 states, the District of Columbia, Puerto Rico, and Guam. An HMO plan’s cost is measured by its monthly premium for individual subscribers. Two possible factors in this cost are (1) the typical hospital expenses in the state in which the HMO operates; and (2) the region in which the HMO operates. In Figure 1, the individual monthly premiums for the 341 HMOs are plotted against the average expenses per admission in the state of operation (both in US dollars).

Let denote the individual monthly premium of the th HMO plan. To analyze these data, Hodges (1998) considered a Bayesian version of the following frequentist model:

| (10) |

where the are iid , denotes the centered and scaled average expenses per admission in the state in which the th HMO operates, and is an indicator for New England. The values were centered and scaled to avoid collinearity. Specifically, if is the raw average expense per admission and is the overall average expense per admission, .

We perform a Bayesian regression analysis based on the following hierarchical version of (10):

| (11) |

where , is the vector of individual premiums, is the vector of regression parameters, and is the data matrix.

Complete specification of the model requires values for hyperparameters . We use an approach which is empirical Bayesian in spirit. To this end, we fit (10) using least squares regression. The results are summarized in Table 1.

| Parameter | Estimate | Standard Error |

| 164.989 | 1.322 | |

| 3.910 | 1.508 | |

| 32.799 | 5.961 | |

| degrees of freedom = 338 | ||

Accordingly, we chose the following prior mean and covariance matrix for :

where is the vector of least squares estimates and the diagonal elements of are reflective of the corresponding squared standard errors in Table 1. Next, we set the prior mean and variance for to

where MSE is the least squares estimate of given in Table 1. Solving for and gives and .

Since (11) does not contain any random effects, it follows from Theorem 3.1 that the Gibbs sampler for is geometrically ergodic since

and for any the function is bounded (recall Proposition 3.3) where

and .

Consider estimating the posterior means of , , and . By Lemma A.6, the fourth posterior moments of these parameters are finite. Thus Theorems 4.1 and 4.2 in conjunction with geometric ergodicity guarantee the existence of CLTs and consistent estimators of the asymptotic variance via batch means with which was chosen based on recommendations in Jones et al. (2006).

To begin our analysis of the posterior means, we ran independent Gibbs samplers from a variety of starting values and updated followed by in each iteration. For each chain, we required a minimum simulation length of 1000. At each successive iteration, we calculated the approximate half-widths of the Bonferroni-corrected 95% intervals for the posterior means of , , and ,

Simulation continued until the half-widths for , , and , were below 0.10, 0.02, and 0.10, respectively. The results were consistent across starting values. That is, Gibbs samplers with different starting values produced similar estimates and required similar simulation effort to meet the above specifications. Here, we present the results for the chain started from the prior means of and , . Under this setting, the interval half-width thresholds were met after 16831 iterations. The corresponding estimates of the posterior means are reported in Table 2 with standard errors.

| Parameter | Estimate | Standard Error | |

|---|---|---|---|

| 165 | .0 | 0.007 | |

| 3 | .9 | 0.008 | |

| 32 | .8 | 0.032 | |

Appendix A Appendix

A.1 Proof of Proposition 3.2

We will require the following general results in our proof. A proof of Lemma A.1 is given in Henderson and Searle (1981) and Lemma A.2 follows from the convexity of the inverse function.

Lemma A.1.

Let be a nonsingular matrix, be a nonsingular matrix, be an matrix, and be an matrix. Then

When this implies

for any vector .

Lemma A.2.

Let be an vector. Also, let and be nonsingular, matrices. Then

We begin the proof of Proposition 3.2. Recall that

We must show that for all

where the constants and are given in the statement of Proposition 3.2. Let and denote expectation and variance with respect to the distribution. Similarly, let and denote expectation and variance with respect to density

defined by (3). Notice that

| (12) |

where the first equality holds by the construction of . Thus we focus on the in the next 3 lemmas.

Lemma A.3.

Suppose is nonsingular. Then for all

where

| (13) |

Proof.

Consider the inner expectation . For any we have

and

by Lemma A.1. It follows that for any we have

Combining this with the fact that

gives

∎

Lemma A.4.

For any

where

| (14) |

Proof.

Lemma A.5.

For any

where

| (17) |

Proof.

We are now ready to finish the proof of Proposition 3.2. We consider the case with nonsingular and the case in which no restrictions are placed on separately.

-

1.

Case 1: nonsingular

-

2.

Case 2: is possibly singular

A.2 Proof of Proposition 3.3

By the assumption that for all , where

Define and . Then and .

We must establish that there exists for which

Let

and note that the claim will be proven if we can show that for all . To this end, define functions , and as

Since the conditional independence of and given implies , a little algebra shows that . Thus, it suffices to find and such that for all , and .

First,

by the positive definiteness of and Notice that this also proves part 1 of the claim. Next, we have

Since and are positive semidefinite we have

where the last inequality holds by Lemma A.1. The result now follows by setting .

A.3 Lemma A.6

Lemma A.6.

The fourth posterior moments of , , and are each finite.

Proof.

We present the proof for . The proofs for and are similar. The finiteness of will follow from establishing that is finite since

To this end, recall that

Also, let and denote a vector of zeroes with a one in the third position. Then

where the inequality follows from Lemma A.1. It follows that the fourth (non-central) moment is finite. ∎

References

- Bednorz and Latuszynski (2007) Bednorz, W. and Latuszynski, K. (2007). A few remarks on “fixed-width output analysis for Markov chain Monte Carlo” by jones et al. Journal of the American Statatistical Association, 102 1485–1486.

- Chan and Geyer (1994) Chan, K. S. and Geyer, C. J. (1994). Comment on “Markov chains for exploring posterior distributions”. The Annals of Statistics, 22 1747–1758.

- Flegal et al. (2008) Flegal, J. M., Haran, M. and Jones, G. L. (2008). Markov chain Monte Carlo: Can we trust the third significant figure? Statistical Science, 23 250–260.

- Flegal and Jones (2009) Flegal, J. M. and Jones, G. L. (2009). Batch means and spectral variance estimators in Markov chain Monte Carlo. The Annals of Statistics (to appear).

- Gelman et al. (2004) Gelman, A., Carlin, J. B., Stern, H. S. and Rubin, D. B. (2004). Bayesian Data Analysis, Second edition. Chapman & Hall/CRC.

- Glynn and Whitt (1992) Glynn, P. W. and Whitt, W. (1992). The asymptotic validity of sequential stopping rules for stochastic simulations. The Annals of Applied Probability, 2 180–198.

- Henderson and Searle (1981) Henderson, H. V. and Searle, S. R. (1981). On deriving the inverse of a sum of matrices. SIAM Review, 23 53–60.

- Hobert and Geyer (1998) Hobert, J. P. and Geyer, C. J. (1998). Geometric ergodicity of Gibbs and block Gibbs samplers for a hierarchical random effects model. Journal of Multivariate Analysis, 67 414–430.

- Hobert et al. (2002) Hobert, J. P., Jones, G. L., Presnell, B. and Rosenthal, J. S. (2002). On the applicability of regenerative simulation in Markov chain Monte Carlo. Biometrika, 89 731–743.

- Hobert et al. (2006) Hobert, J. P., Jones, G. L. and Robert, C. P. (2006). Using a Markov chain to construct a tractable approximation of an intractable probability distribution. Scandinavian Journal of Statistics, 33 37–51.

- Hodges (1998) Hodges, J. S. (1998). Some algebra and geometry for hierarchical models, applied to diagnostics. Journal of the Royal Statistical Society, Series B, 60 497–536.

- Jones et al. (2006) Jones, G. L., Haran, M., Caffo, B. S. and Neath, R. (2006). Fixed-width output analysis for Markov chain Monte Carlo. Journal of the American Statistical Association, 101 1537–1547.

- Jones and Hobert (2001) Jones, G. L. and Hobert, J. P. (2001). Honest exploration of intractable probability distributions via Markov chain Monte Carlo. Statistical Science, 16 312–334.

- Jones and Hobert (2004) Jones, G. L. and Hobert, J. P. (2004). Sufficient burn-in for Gibbs samplers for a hierarchical random effects model. The Annals of Statistics, 32 784–817.

- Meyn and Tweedie (1993) Meyn, S. P. and Tweedie, R. L. (1993). Markov chains and Stochastic Stability. Springer, London.

- Mykland et al. (1995) Mykland, P., Tierney, L. and Yu, B. (1995). Regeneration in Markov chain samplers. Journal of the American Statistical Association, 90 233–241.

- Papaspiliopoulos and Roberts (2008) Papaspiliopoulos, O. and Roberts, G. (2008). Stability of the Gibbs sampler for Bayesian hierarchical models. The Annals of Statistics, 36 95–117.

- Roberts and Rosenthal (2001) Roberts, G. O. and Rosenthal, J. S. (2001). Markov chains and de-initializing processes. Scandinavian Journal of Statistics, 28 489–504.

- Rosenthal (1995) Rosenthal, J. S. (1995). Rates of convergence for Gibbs sampling for variance component models. The Annals of Statistics, 23 740–761.

- Spiegelhalter et al. (2005) Spiegelhalter, D., Thomas, A., Best, N. and Lunn, D. (2005). Winbugs version 2.10. Tech. rep., MRC Biostatistics Unit, Cambridge: UK.