Model selection by resampling penalization

Abstract

In this paper, a new family of resampling-based penalization procedures for model selection is defined in a general framework. It generalizes several methods, including Efron’s bootstrap penalization and the leave-one-out penalization recently proposed by Arlot (2008), to any exchangeable weighted bootstrap resampling scheme. In the heteroscedastic regression framework, assuming the models to have a particular structure, these resampling penalties are proved to satisfy a non-asymptotic oracle inequality with leading constant close to 1. In particular, they are asympotically optimal. Resampling penalties are used for defining an estimator adapting simultaneously to the smoothness of the regression function and to the heteroscedasticity of the noise. This is remarkable because resampling penalties are general-purpose devices, which have not been built specifically to handle heteroscedastic data. Hence, resampling penalties naturally adapt to heteroscedasticity. A simulation study shows that resampling penalties improve on -fold cross-validation in terms of final prediction error, in particular when the signal-to-noise ratio is not large.

doi:

10.1214/154957804100000000keywords:

[class=AMS]keywords:

t1The author was financed in part by Univ Paris-Sud (Laboratoire de Mathematiques, CNRS-UMR 8628).

1 Introduction

In the last decades, model selection has received much interest. When the final goal is prediction, model selection can be seen more generally as the question of choosing between the outcomes of several prediction algorithms. With such a general formulation, a natural and classical answer is the following. First, estimate the prediction error for each model or algorithm; second, select the model minimizing this criterion. Model selection procedures mainly differ on the way of estimating the prediction error.

The empirical risk, also known as the apparent error or the resubstitution error, is a natural estimator of the prediction error. Nevertheless, minimizing the empirical risk can fail dramatically: the empirical risk is strongly biased for models involving a number of parameters growing with the sample size because the same data are used for building predictors and for comparing them.

In order to correct this drawback, cross-validation methods have been introduced All:1974 ; Sto:1974 , relying on a data-splitting idea for estimating the prediction error with much less bias. In particular, -fold cross-validation (VFCV, Gei:1975 ) is a popular procedure in practice because it is both general and computationally tractable. A large number of papers exist about the properties of cross-validation methods, showing that they are efficient for a suitable choice of the way data are split (or for VFCV). Asymptotic optimality results for leave-one-out cross-validation (that is the case) in regression have been proved for instance by Li KCLi:1987 and by Shao Sha:1997 . However, when is fixed, VFCV can be asymptotically suboptimal, as showed by Arlot Arl:2008a . We refer to the latter paper for more references on cross-validation methods, including the small amount of available non-asymptotic results.

Another way to correct the empirical risk for its bias is penalization. In short, penalization selects the model minimizing the sum of the empirical risk and of some measure of complexity111Note that “complexity” here and in the following refers to the implicit modelization of a model or an algorithm, such as the number of estimated parameters. “Complexity” does not refer at all to the computational complexity of algorithms, which will always be called “computational complexity” in the following. of the model (called penalty); see FPE Aka:1969 , AIC Aka:1973 , Mallows’ or Mal:1973 . Model selection can target two different goals. On the one hand, a procedure is efficient (or asymptotically optimal) when its quadratic risk is asymptotically equivalent to the risk of the oracle. On the other hand, a procedure is model consistent when it selects the smallest true model asymptotically with probability one. This paper deals with efficient procedures, without assuming the existence of a true model. Therefore, the ideal penalty for prediction is the difference between the prediction error (the “true risk”) and the empirical risk; penalties should be data-dependent estimates of the ideal penalty.

Many penalties or complexity measures have been proposed. Consider for instance regression and least-squares estimators on finite-dimensional vector spaces (the models). When the design is fixed and the noise-level constant equal to , Mallows’ penalty Mal:1973 is equal to for a model of dimension and it can be modified according to the number of models Bir_Mas:2002 ; Sau:2006 . Mallows’ -like penalties satisfy some optimality properties Shi:1981 ; KCLi:1987 ; Bar:2002 ; Bir_Mas:2006 but they can fail when the data are heteroscedastic Arl:2008:shape because these penalties are linear functions of the dimension of the models.

In the binary supervised classification framework, several penalties have been proposed. First, VC-dimension-based penalties have the drawback of being independent of the underlying measure, so that they are adapted to the worst case. Second, global Rademacher complexities Kol:2001 ; Bar_Bou_Lug:2002 (generalized by Fromont with resampling ideas Fro:2004 ) take into account the distribution of the data, but they are still too large to achieve fast rates of estimation when the margin condition Mam_Tsy:1999 holds. Third, local Rademacher complexities Bar_Bou_Men:2005 ; Kol:2006 are tighter estimates of the ideal penalty, but their computational cost is heavy and they involve huge (and sometimes unknown) constants. Therefore, easy-to-compute penalties that can achieve fast rates are still needed.

All the above penalties have serious drawbacks making them less often used in practice than cross-validation methods: AIC and Mallows’ rely on strong assumptions (such as homoscedasticity of the data and linearity of the models) and some mainly asymptotic arguments; VC-dimension-based penalties and global Rademacher complexities are far too pessimistic; local Rademacher complexities are computationally intractable, and their calibration is a serious issue. Another approach for designing penalties in the general framework may not suffer from these drawbacks: the resampling idea.

Efron’s resampling heuristics Efr:1979 was first stated for the bootstrap, then generalized to the exchangeable weighted bootstrap by Mason and Newton Mas_New:1992 and by Præstgaard and Wellner Pra_Wel:1993 . In short, according to the resampling heuristics, the distribution of any function of the (unknown) distribution of the data and the sample can be estimated by drawing “resamples” from the initial sample. In particular, the resampling heuristics can be used to estimate the variance of an estimator Efr:1979 , a prediction error Wu:1986 ; Efr_Tib:1997 or the ideal penalty (using the bootstrap Efr:1983 ; Efr:1986 ; Ish_Sak_Kit:1997 , the out of bootstrap222Shao’s goal in Sha:1996 was not efficiency but model consistency. Sha:1996 or a -fold subsampling scheme Arl:2008a ). The asymptotic optimality of Efron’s bootstrap penalty for selecting among maximum likelihood estimators has been proved by Shibata Shi:1997 . Note also that global and local Rademacher complexities are using an i.i.d. Rademacher resampling scheme for estimating different upper bounds on the ideal penalty and Fromont’s penalties Fro:2007 generalize the global Rademacher complexities to the exchangeable weighted bootstrap.

The first goal of this paper is to define and study general-purpose penalties, that is penalties well-defined in almost every framework and performing reasonably well in most of them, including regression and classification. The main interest of such penalties would be the ability to solve difficult problems (for instance heteroscedastic data, a non-smooth regression function or the fact that the oracle model achieves fast rates of estimation) without knowing them in advance. From the practical point of view, such a property is crucial.

To this aim, the resampling heuristics with the general exchangeable weighted bootstrap is used for estimating the ideal penalty (Section 2). This defines a wide family of model selection procedures, called “Resampling Penalization” (RP), which includes Efron’s and Shao’s penalization methods Efr:1983 ; Sha:1996 as well as the leave-one-out penalization defined in Arl:2008a . To our knowledge, it has never been proposed with such general resampling schemes, so that the RP family contains a wide range of new procedures. Note that RP is well-defined in a general framework, including regression and classification, but also many other application fields (Section 7.2). Even if the main results are proved in the least-squares regression framework only, we obviously do not mean that RP should be restricted to this framework.

In this paper, the model selection efficiency of RP is studied with a unified approach for all the exchangeable resampling schemes. Therefore, comparing bootstrap with subsampling is quite straightforward (Section 5) which is not common in the resampling literature (except a few asymptotic results, see Barbe and Bertail Bar_Ber:1995 ).

The point of view used in the paper is non-asymptotic, which has two major implications. First, non-asymptotic results allow to consider collections of models depending on the sample size : in practice, it is usual to increase the number of explanatory variables with the number of observations. Considering models with a large number of parameters (for instance of order for some ) is also particularly useful for designing adaptive estimators of a function which is only assumed to belong to some Hölderian ball (see Section 3.2). Thus, the non-asymptotic point of view allows not to assume that the regression function is described with a small number of parameters.

Second, several practical problems are “non-asymptotic” in the sense that the signal-to-noise ratio is low. As noticed in Arl:2008a , with such data, VFCV can have serious drawbacks which can be naturally fixed by using the flexibility of penalization procedures. It is worth noting that such a non-asymptotic approach is not common in the model selection literature and few non-asymptotic results exist on general resampling methods.

Another important point is that the framework of the paper includes several kinds of heteroscedastic data. The observations are only assumed to be i.i.d. with

where is the (unknown) regression function, is the (unknown) noise-level and has zero mean and unit variance conditionally on . In particular, the noise-level can strongly depend on and the distribution of can depend on . Such data are generally considered as difficult to handle because no information on is known, making irregularities of the signal difficult to distinguish from noise. As already mentioned, simple model selection procedures such as Mallows’ can fail in this framework Arl:2008:shape whereas it is natural to expect that resampling methods are robust to heteroscedasticity. In this article, both theoretical and simulation results confirm this fact (Sections 3 and 5).

The two main results of the paper are stated in Section 3. First, making mild assumptions on the distribution of the data, a non-asymptotic oracle inequality for RP is proved with leading constant close to 1 (Theorem 1). It holds for several kinds of resampling schemes (including bootstrap, leave-one-out, half-subsampling and i.i.d. Rademacher weighted bootstrap) and implies the asymptotic optimality of RP, even when the data are highly heteroscedastic. For proving such a result, each model is assumed to be the vector space of piecewise constant functions (histograms) on some partition of the feature space. This is indeed a restriction, but we conjecture that it is mainly technical and that RP remains efficient in a much more general framework (see Section 7.2). Moreover, studying extensively the toy model of histograms allows to derive precise heuristics for the general framework. A major goal of the paper is to help practicioners who would like to know how to use resampling for performing model selection (see in particular Sections 6 and 7.3).

Second, RP is used to build an estimator simultaneously adaptive to the smoothness of the regression function (assuming that is -Hölderian for some unknown ) and to the unknown noise-level (Theorem 2). This result may seem surprising since RP has never been designed specifically for such a purpose. We interpretate Theorem 2 as a confirmation that RP is naturally adaptive and should work well in several other difficult frameworks.

Several results similar to Theorem 1 exist in the literature for other procedures such as Mallows’ (with homoscedastic data only), VFCV and leave-one-out cross-validation. Moreover, there exist several minimax adaptive estimators for heteroscedastic data with a smooth noise-level, for instance Efr_Pin:1996 ; Gal_Per:2008 , and the regression function and the noise level can be estimated simultaneously Gen:2008 . In comparison, the interest of RP is both its generality (contrary to Mallows’ and specific adaptive estimators) and its flexibility (contrary to VFCV, see Arl:2008a ), as detailed in Section 7.1.

A simulation study is conducted in Section 5 with small sample sizes. RP is showed to be competitive with Mallows’ for “easy” problems, and much better for some harder ones (for instance with a variable noise-level). Moreover, a well-calibrated RP yields almost always better model selection performance than VFCV. Therefore, RP can be of great interest in situations where no a priori information is known about the data. RP can deal with difficult problems, and compete with procedures that are fitted for easier problems. In short, RP is an efficient alternative to VFCV.

This article is organized as follows. The framework and the Resampling Penalization (RP) family of procedures are defined in Section 2. The main results are stated in Section 3. The differences between the resampling weights are investigated in Section 4. Then, a simulation study is presented in Section 5. Practical issues concerning the implementation of RP are considered in Section 6. RP is compared to other penalization methods in Section 7.1 and the extension of RP to the general framework is discussed in Section 7.2. Finally, Section 8 is devoted to the proofs. Some additional material (other simulation experiments and proofs) is available in a technical Appendix Arl:2008b:app .

2 The Resampling Penalization procedure

In order to simplify the presentation, we choose to focus on the particular framework of least-squares regression on models of piecewise constant functions (histograms), which is the framework of the main results of Section 3 and the simulation study of Section 5.

Nevertheless, the RP family is a general-purpose method which can easily be defined in the general prediction framework. The main interest of the histogram framework is to provide general heuristics about RP, so that the practicioner can make the best possible use of RP in the general framework. A discussion on RP in the general prediction framework is provided in Section 7.2, including a general definition of RP.

2.1 Framework

Suppose we observe some data , independent with common distribution , where the feature space is typically a compact set of . Let denote the regression function, that is . Then,

| (1) |

where is the heteroscedastic noise-level and are i.i.d. centered noise terms; the possibly depend on , but they are have zero mean and unit variance conditionally on .

The goal is to predict given where is independent of the data. The quality of a predictor is measured by the quadratic prediction loss , where and is the least-squares contrast. Since is minimal when , the excess loss is defined as

Given a particular set of predictors (called a model), the best predictor over is defined as

with its empirical counterpart

(when it exists and is unique) where is the empirical distribution. The estimator is the well-known empirical risk minimizer, also called least-squares estimator since is the least-squares contrast.

In this article, we mainly consider histogram models , that is of the following form. Let be some fixed partition of . Then, denotes the set of functions which are constant over for every ; is a vector space of dimension , spanned by the family . The empirical risk minimizer over an histogram model is often called a regressogram.

Explicit computations are easier with regressograms because is an orthogonal basis of for any probability measure on . In particular,

Note that is uniquely defined if and only if each contains at least one of the , that is .

Let us assume that a collection of models is given. Model selection consists in selecting some data-dependent such that is as small as possible. General penalization procedures can be described as follows. Let be some penalty function, possibly data-dependent, and define

| (2) |

Since the goal is to minimize the loss , the ideal penalty is

| (3) |

and we would like to be as close to as possible for every . In the histogram framework, note that is not uniquely defined when ; then, we consider that the model cannot be chosen, which is formally equivalent to add to the penalty .

When is the histogram model associated with some partition of , the ideal penalty (3) can be computed explicitly:

| (4) |

where . The ideal penalty is unknown because it depends on the true distribution ; therefore, resampling is a natural method for estimating .

2.2 The resampling heuristics

Let us recall briefly the resampling heuristics, which has been introduced by Efron Efr:1979 in the context of variance estimation. Basically, it says that one can mimic the relationship between and by drawing a -sample with common distribution , called the “resample”; let denote the empirical distribution of the resample. Then, the conditional distribution of the pair given should be close to the distribution of the pair . Hence, the expectation of any quantity of the form can be estimated by . The expectation means that we integrate with respect to the resampling randomness only. Let us emphasize that has the form .

Later on, this heuristics has been generalized to other resampling schemes, with the exchangeable weighted bootstrap Mas_New:1992 ; Pra_Wel:1993 . The empirical distribution of the resample then has the general form

where is an exchangeable333 is said to be exchangeable when its distribution is invariant by any permutation of its coordinates. weight vector independent of the data and such that . In this article, is also assumed to satisfy , a.s. and .

We mainly consider the following weights, which include the more classical resampling schemes:

-

1.

Efron (), (Efr): is a multinomial vector with parameters . A classical choice is .

-

2.

Rademacher (), (Rad): are independent, with a Bernoulli () distribution. A classical choice is .

-

3.

Poisson (), (Poi): are independent, with a Poisson () distribution. A classical choice is .

-

4.

Random hold-out (), (Rho): where is a uniform random subset of cardinality of . A classical choice is .

-

5.

Leave-one-out (Loo) = Rho ().

In the following, Efr, Rad, Poi, Rho and Loo respectively denote the above resampling weight vector distributions with the “classical” value of the parameter.

Remark 1.

The above terminology explicitly links the weight vector distributions with some classical resampling schemes. See Mas_New:1992 ; Hal_Mam:1994 ; vdV_Wel:1996 for more details about classical resampling weight names, as well as other classical examples.

-

•

The name “Efron” comes from the classical choice for which Efron weights actually are the bootstrap weights. When , Efron() is the out of bootstrap, used for instance by Shao Sha:1996 .

-

•

The name “Rademacher” for the i.i.d. Bernoulli weights comes from the classical choice for which are i.i.d. Rademacher random variables. For instance, global and local Rademacher complexities use this resampling scheme to estimate different upper bounds on (see Section 7.2.4).

-

•

Poisson weights are often used as approximations to Efron weights, via the so-called “Poissonization” technique (see (vdV_Wel:1996, , Chapter 3.5) and Fro:2004 ). They are known to be efficient for estimating several non-smooth functionals (see (Bar_Ber:1995, , Chapter 3) and (Mam:1992, , Section 1.4)).

-

•

The Random hold-out () weights can also be called “delete- jackknife”, as well as the Leave-one-out weights also refer to the jackknife (sometimes called cross-validation). They are both resampling schemes without replacement (vdV_Wel:1996, , Example 3.6.14), more often called subsampling weights (see for instance the book by Politis, Romano and Wolf Pol_Rom_Wol:1999 on subsampling). They are close to the idea of splitting the data into a training set and a validation set (for instance, leave-one-out, hold-out and cross-validation). Indeed, if one defines the training set as

and the validation set as its complement, there is a one-to-one correspondence between subsampling weights and data splitting.

2.3 Resampling Penalization

Applying directly the resampling heuristics of Section 2.2 for estimating the ideal penalty (3), we would get the penalty

| (5) | |||

Two problems have to be solved before defining properly the Resampling Penalization procedure. Here, we focus on the histogram framework; the general framework will be considered in Section 7.2.

First, (5) is not well-defined because is not unique if . Hence, even when , the problem occurs as soon as for some , which has a positive probability (except when ) for most of the resampling schemes since . In order to make (5) well-defined, let us rewrite the resampling penalty as the resampling estimate of (4), that is

where

because for every ,

With the convention when , is well-defined since is well-defined when . It remains to define properly . We suggest to replace the expectation over all the resampling weights by an expectation conditional on , separately for each and , which ensures that we only remove a small proportion of the possible resampling weights. To summarize, (5) is replaced by

| (6) |

Second, (6) is strongly biased as an estimate of when is small, because is then much closer to than is close to . Assuming the to be histogram models, we will prove in Section 3.4.1 (see Propositions 1 and 2) that the bias can be corrected by multiplying (6) by a constant which only depends on the distribution of . The values of for the classical weights are reported in Table 1. Remark that in the bootstrap case (Efr), as well as for Rad, Poi and Rho.

| Efr() | Rad() | Poi() | Rho() | Loo | |

|---|---|---|---|---|---|

We are now in position to define properly the Resampling Penalization (RP) procedure for selecting among histogram models. See Section 7.2 for the definition of RP in the general framework (Procedure 3).

Procedure 1 (Resampling Penalization for histograms).

-

1.

Replace by

-

2.

Choose a resampling scheme .

-

3.

Choose a constant where is defined in Table 1.

-

4.

Define, for each , the resampling penalty as

(7) -

5.

Select .

Remark 2.

-

1.

At step 1, we remove more models than those for which is not uniquely defined. When for some , estimating the quality of estimation of with only one data-point is hopeless with no assumption on the noise-level . The reason why we remove also models for which is that the oracle inequalities of Section 3 require it for some of the weights; nevertheless, such models generally have a poor prediction performance, so that step 1 is reasonable.

- 2.

-

3.

RP (Procedure 1) generalizes several model selection procedures. With a bootstrap resampling scheme (Efr) and , RP is Efron’s bootstrap penalization Efr:1983 , which has also been called EIC in the log-likelihood framework Ish_Sak_Kit:1997 . With an out of bootstrap resampling scheme (Efr()) and , RP has been proposed and studied by Shao Sha:1996 in the context of model identification. Note that for Efr() weights if ; this crucial point will be discussed in Section 3.4.1. RP with a (non-exchangeable) -fold subsampling scheme has also been proposed recently in Arl:2008a .

- 4.

3 Main results

In this section, we state some non-asymptotic properties of Resampling Penalization (Procedure 1) for model selection. First, Theorem 1 is an oracle inequality with leading constant close to 1. In particular, Theorem 1 implies the asymptotic optimality of RP. Second, Theorem 2 is an adaptivity result for an estimator built upon RP, when the regression function belongs to some Hölderian ball. A remarkable point is that both results remain valid under mild assumptions on the distribution of the noise, which can be non-Gaussian and highly heteroscedastic.

Throughout this section, we assume the existence of non-negative constants , , such that:

-

Polynomial size of : .

-

Richness of : s.t. .

-

The weight vector is chosen among Efr, Rad, Poi, Rho and Loo (defined in Section 2.2, with the classical value of their parameter).

is a natural restriction since RP plugs an estimator of the ideal penalty into (2). When is larger, say proportional to for some , Birgé and Massart Bir_Mas:2006 proved that penalties estimating the ideal penalty cannot be asymptotically optimal. is merely technical. can be relaxed, as explained in Section 4.2.

3.1 Oracle inequality

Theorem 1.

Assume that the data satisfy the following:

-

Bounded data: .

-

Noise-level bounded from below: a.s.

-

Polynomially decreasing bias: there exist and such that

-

Lower regularity of the partitions for : there exists such that

Let be defined by Procedure 1 (under restrictions , with ). Then, there exist a constant and an absolute sequence converging to zero at infinity such that, with probability at least ,

| (8) |

Moreover,

| (9) |

The constant may depend on constants in , , , and but not on . The term is smaller than ; can also be made smaller than for any at the price of enlarging .

Theorem 1 is proved in Section 8.3. The non-asymptotic oracle inequality (8) implies that Procedure 1 is a.s. asymptotically optimal in this framework if . When are Efr weights, the asymptotic optimality of RP was proved by Shibata Shi:1997 for selecting among maximum likelihood estimators, assuming that the distribution belongs to some parametric family of densities (see also Remark 6 in Section 3.4.1).

Resampling Penalization yields an estimator with an excess loss as small as the one of the oracle without requiring any knowledge about such as the smoothness of or the variations of the noise-level . Therefore, RP is a naturally adaptive procedure. Note that (8) is even stronger than an adaptivity result because of the leading constant close to one, whereas adaptive estimators only achieve the correct estimation rate up to a possibly large absolute constant. Hence, one can expect that an estimator obtained with RP and a well chosen collection of models is almost optimal.

We now comment on the assumptions of Theorem 1:

- 1.

-

2.

and are rather mild and neither nor need to be known by the statistician. In particular, quite general heteroscedastic noises are allowed; and can even be relaxed as explained in Section 3.3.2.

-

3.

When has a lower bounded density with respect to , is satisfied for “almost piecewise regular” histograms, including all those considered in the simulation study of Section 5.

-

4.

The upper bound in holds with when is regular on and is -Hölderian with . The lower bound in is discussed extensively in Section 3.3.1.

3.2 An adaptive estimator

A natural framework in which Theorem 1 can be applied is when is a compact subset of , has a lower bounded density with respect to the Lebesgue measure and is -Hölderian with . Indeed, the latter condition ensures that regular histograms can approximate well. In this subsection, we show that Resampling Penalization can be used to build an estimator adaptive to the smoothness of in this framework.

We first define the estimator. For the sake of simplicity444If has a smooth boundary, Procedure 2 can be modified so that the proof of Theorem 2 remains valid., is assumed to be a closed ball of , say .

Procedure 2 (Resampling Penalization with regular histograms).

For every , let be the model of regular555When has a general shape, assume that both and for are finite. Then, a partition of is regular with bins when and there exist positive constants , , , such that for every , and . histograms with bins, that is the histogram model associated with the partition

Then, define .

Theorem 2.

Let . Assume that the data satisfy the following:

-

Bounded data: .

-

Noise-level bounded from below: a.s.

-

Density bounded from below:

-

Hölderian regression function: there exist and such that

Let be the estimator defined by Procedure 2 and . Then, there exist positive constants and such that,

| (10) |

If moreover the noise-level is smooth, that is

-

is piecewise -Lipschitz with at most jumps,

then, assumption can be removed and (10) holds with replaced by .

For both results, may only depend on and . The constant may only depend on , , , , (and for (10); and for the latter result).

Theorem 2 is proved in Section 8.5. The upper bounds given by Theorem 2 coincide with several classical minimax lower bounds on the estimation of functions in with , up to an absolute constant. In the homoscedastic case, lower bounds have been proved by Stone Sto:1980 and generalized by several authors among which Korostelev and Tsybakov Kor_Tsy:1993 and Yang and Barron Yan_Bar:1999 . Up to a multiplicative factor independent of , and the best achievable rate is

Hence, (10) shows that Procedure 2 achieves the right estimation rate in terms of , and , without using the knowledge of , or .

Moreover, (10) still holds in a wide heteroscedastic framework, without using any information on the noise-level . Then, up to a multiplicative constant independent of and (but possibly of the order of some power of ), the upper bound (10) is the best possible estimation rate.

Minimax lower bounds proved in the heteroscedastic case (see for instance Efr_Pin:1996 ; Gal_Per:2008 and references therein) show that when and the noise-level is smooth enough, the best achievable estimation rate depends on through the multiplicative factor . Therefore, the upper bound given by Theorem 2 under assumption is tight, even through its dependence on the noise-level. Up to our best knowledge, such an upper bound had never been obtained when and , even with estimators using the knowledge of , and .

Theorem 2 shows that Procedure 2 defines an adaptive estimator, uniformly over distributions such that belongs to some Hölderian ball with and the noise-level is not too pathological. This result is quite strong. Although similar properties have already been proved for “ad hoc” estimators (see Efr_Pin:1996 ; Gal_Per:2008 and Section 7.1.3), Resampling Penalization has not been designed specifically to have such a property. Therefore, exchangeable resampling penalties are naturally adaptive to the smoothness of and to the heteroscedasticity of the data.

Remark 3.

3.3 Discussion on some assumptions

The aim of this subsection is to discuss some of the main assumptions made in Theorems 1 and 2. We first tackle the lower bound in which is required in Theorem 1. Then, two alternative assumption sets to Theorems 1 and 2 are provided, allowing the noise level to vanish or the data to be unbounded.

3.3.1 Lower bound in

The lower bound in may seem unintuitive because it means that is not too well approximated by the models . Assuming that is classical for proving the asymptotic optimality of Mallows’ Shi:1981 ; KCLi:1987 ; Bir_Mas:2006 .

Let us explain why is used for proving Theorem 1. According to Remark 8 in Section 8.2, when the lower bound in is no longer assumed, (8) holds with two modifications on its right-hand side: the infimum is restricted to models of dimension larger than and a remainder term is added (where and are absolute constants). This is essentially the same as (8) unless there exists a model of small dimension with a small bias; the lower bound in is sufficient to ensure this does not happen. Note that assumption was made in the density estimation framework Sto:1985 ; Bur:2002 for the same technical reasons.

As showed in Arl:2008b:app , is at least satisfied with

in the following case: is “regular” (as defined in Procedure 2 below), has a lower-bounded density with respect to the Lebesgue measure on and is non-constant and -Hölderian (with respect to ).

The general formulation of is crucial to make Theorem 1 valid whatever the distribution of which can be useful in some practical problems. Indeed, when has a general distribution, a collection satisfying , , and can always be chosen either thanks to prior knowledge on or to unlabeled data. In the latter case, classical density estimation procedures can be applied for estimating from unlabeled data (see for instance Dev_Lug:2001 on density estimation). Assumption then means that the collection of models has good approximation properties, uniformly over some appropriate function space (depending on ) to which belongs.

3.3.2 Two alternative assumption sets

Theorems 1 and 2 are corollaries of a more general result, called Lemma 7 in Section 8.2. The assumptions of Theorems 1 and 2, in particular and on the distribution of the noise , are only sufficient conditions for the assumptions of Lemma 7 to hold. The following two alternative sufficient conditions are proved to be valid in Section 8.4.

First, one can have in if moreover , is bounded and

-

Upper regularity of the partitions for : such that

-

Upper regularity of the partitions for : such that

-

is piecewise -Lipschitz with at most jumps.

Second, the can be unbounded (assuming now that in ) if moreover is bounded measurable and

-

The noise is sub-Gaussian: such that

-

Noise-level bounded from above: a.s.

-

Bound on the regression function: .

-

is -Lipschitz, piecewise and non-constant: on some interval with .

-

Regularity of the partitions for : such that

-

Density bounded from below: , , .

Third, it is possible to have simultaneously in and unbounded data, see Arl:2008b:app for details.

The above results mean that Theorem 1 holds for most “reasonably” difficult problems. Actually, Proposition 3 and Remark 7 show that the resampling penalties are much closer to than itself, provided that the concentration inequalities for are tight (Proposition 10). Therefore, up to differences within , RP with and the “ideal” deterministic penalization procedure perform equally well on a set of probability . For every assumption set such that the proof of Theorem 1 gives an oracle inequality for the penalty , the same proof gives a similar oracle inequality for RP.

3.4 Probabilistic tools

Theorems 1 and 2 rely on several probabilistic tools of independent interest: precise computation of the expectations of resampling penalties (Propositions 1 and 2), concentration inequalities for resampling penalties (Proposition 3) and bounds on expectations of the inverses of several classical random variables (Lemma 4–6). Their originality comes from their non-asymptotic nature: explicit bounds on the deviations or the remainder terms are provided for finite sample sizes.

3.4.1 Expectations of resampling penalties

Using only the exchangeability of the weights, the resampling penalty can be computed explicitly (Lemma 16 in Section 8.8). This can be used to compare the expectations of the resampling penalties and the ideal penalty. First, Proposition 1 is valid for general exchangeable weights.

Proposition 1.

Let be the model of histograms associated with some partition of and be an exchangeable random vector independent of the data. Define by (3) and by (7). Let denote expectations conditionally on . Then, if ,

| (11) | ||||

| (12) | ||||

| (13) | ||||

| (14) |

In particular,

| (15) |

where only depends on and satisfies for some absolute constant .

Remark 4.

- •

-

•

Combining Proposition 1 with (Arl:2007:phd, , Lemma 8.4), a similar result holds for non-exchangeable weights (with only a modification of the definitions of and ).

In the general heteroscedastic framework (1), Proposition 1 shows that resampling penalties take into account the fact that actually depends on . This is a major difference with the classical Mallows’ penalty

which does not take into account the variability of the noise level over . A more detailed comparison with Mallows’ is made in Section 7.1.1.

If does not depend too much on (at least when is large), Proposition 1 shows that estimates unbiasedly as soon as666The definition of actually used in this paper is slightly different for Efron() and Poisson() weights (see Table 2). We arbitrarily choosed the simplest possible expression making asymptotically equivalent to . The results of the paper also hold when .

In particular, all the examples of resampling weights given in Section 2.2 satisfy that does not depend on when is large, which leads to Proposition 2 below (see Table 2 for exact expressions of and ).

| Efr() | Rad() | Poi() | Rho() | Loo | |

|---|---|---|---|---|---|

Proposition 2.

Remark 5.

Remark 6.

Combined with the explicit expressions of for several resampling weights (Table 2), Proposition 2 helps to understand several known results.

-

•

In the maximum likelihood framework, Shibata Shi:1997 showed the asymptotical equivalence of two bootstrap penalization methods. The first penalty, denoted by , is Efron’s bootstrap penalty Efr:1983 , which is defined by (5) with Efr weights. The second penalty, denoted by , was proposed by Cavanaugh and Shumway Cav_Shu:1997 ; it transposes

into the maximum likelihood framework. In the least-squares regression framework (with histogram models), the proofs of Propositions 1 and 2 show that

for several resampling schemes, including Efron’s bootstrap (for which ). The concentration results of Section 8.10 show that this remains true without expectations.

-

•

With Efron () weights (and a bootstrap selection procedure close to RP, but with ), Shao Sha:1996 showed that leads to an inconsistent model selection procedure for identification. On the contrary, when and , Shao’s bootstrap selection procedure is model consistent. Proposition 2 shows that these assumptions on can be rewritten . Therefore, the rationale behind Shao’s result may mostly be that identification needs overpenalization within a factor tending to infinity with .

3.4.2 Concentration inequalities for resampling penalties

From (4), the ideal penalty can be written

Hence, is a U-statistics of order 2 conditionally on , which is sufficient to prove that resampling yields a consistent estimate of (Arcones and Giné Arc_Gin:1992 considered the bootstrap case; Hušková and Janssen Hus_Jan:1993 extended it to the exchangeable weighted bootstrap).

In the non-asymptotic framework, that is when the models can depend on , the following concentration inequality is needed.

Proposition 3.

Let , and be an exchangeable weight vector. Let be the model of histograms associated with some partition of and be defined by (7). Assume that two positive constants and exist such that for every ,

Let denote the event . Then, there exist constants and an event of probability at least on which

where and are defined by (13) and (14). The constant is absolute and may only depend on , and .

Proposition 3 is proved in Section 8.10.1. Note that the moment condition holds under the assumptions of Theorem 1 as well as the alternative assumptions of Section 3.3.2. It is here stated in its most general form.

Remark 7.

Since the factor should tend to infinity with for most reasonable models, Proposition 3 gives better bounds for resampling penalties than what could be obtained for ideal penalties with Proposition 10 in the same framework.

Although we do not know how tight are the bounds of Proposition 3, such a phenomenon is classical with bootstrap and can be understood from the asymptotic point of view through Edgeworth expansions Hal:1992 . In a non-asymptotic Gaussian framework, (Arl_Bla_Roq:2008:RC, , Section 2.3) shows the same property for resampling estimators, which concentrate at the rate instead of ( being the amount of data). Since plays the role of , the gain can reasonably be conjectured to be unimprovable without some more assumptions.

Let us emphasize that if resampling penalties estimate instead of , RP with cannot take into account the fact that may be far from its expectation.

3.4.3 Expectations of inverses

For any non-negative random variable , we define

This quantity appears in the explicit formulas for when is among the examples of resampling weights of Section 2.2 (see Lemma 17). Therefore, in order to prove Proposition 2, non-asymptotic bounds on are needed when has a binomial, hypergeometric or Poisson distribution.

Former results concerning can be found in papers by Lew 1976:Lew (for general ), by Jones and Zhigljavsky 2004:Jon_Zhi (for the Poisson case) and by Žnidarič 2005:Zni (for the binomial and Poisson case), but they are either asymptotic or not precise enough. Lemmas 4–6 solve this issue.

In the rest of the paper, for any , denotes the minimum of and and denotes the maximum of and .

Binomial case

Lemma 4.

For any and , denotes the binomial distribution with parameters , and . Then, if ,

| (18) | |||

| (19) |

Hypergeometric case

Recall that an hypergeometric random variable is defined by

Lemma 5.

Let such that and .

-

1.

General lower-bound:

-

2.

General upper-bound: let and .

(20) -

3.

“Rho” case: if ,

(21) -

4.

“Loo” case:

(22) -

5.

“Lpo” case: if ,

Poisson case

Lemma 6.

For every , denotes the Poisson distribution with parameter . Then,

Lemma 6 is proved in Section 8.11.3. It implies in particular that when , which can be derived from 2004:Jon_Zhi ; 2005:Zni .

4 Comparison of the weights

We investigate in this section how the loss of the final estimator may depend on the distribution of the exchangeable weight vector . First, we consider in Section 4.1 the most classical ones, that is Efr, Rad, Poi, Rho and Loo. Then, we discuss in Section 4.2 whether Theorem 1 can be extended to general exchangeable weights.

4.1 Comparison of the classical weights

According to Theorem 1, any resampling scheme among Efr, Rad, Poi, Rho and Loo leads to an asymptotically optimal procedure. Even from the non-asymptotic point of view, it is not quite clear to distinguish between these weights with the results of Section 3. Indeed, the resampling penalties are equal in expectation at first order (Proposition 2), and their deviations are negligible in front of their expectations (Proposition 3).

Therefore, differences between these weights can only come from second-order terms, either in the expectations or in the sizes of the deviations of resampling penalties. As a first step, we compare in this subsection second-order terms in the expectations of the penalties (that is, differences between second-order terms in (15) and (16)), for a fixed sample size. Asymptotic considerations can be found in the book by Barbe and Bertail (Bar_Ber:1995, , Chapter 2) where Edgeworth expansions are used to compare the accuracy of estimation with many exchangeable weights. The asymptotic results mentioned in Section 3.4.3 may also be useful.

Propositions 1 and 2 show that and have the same expectation, up to the small terms and . More precisely,

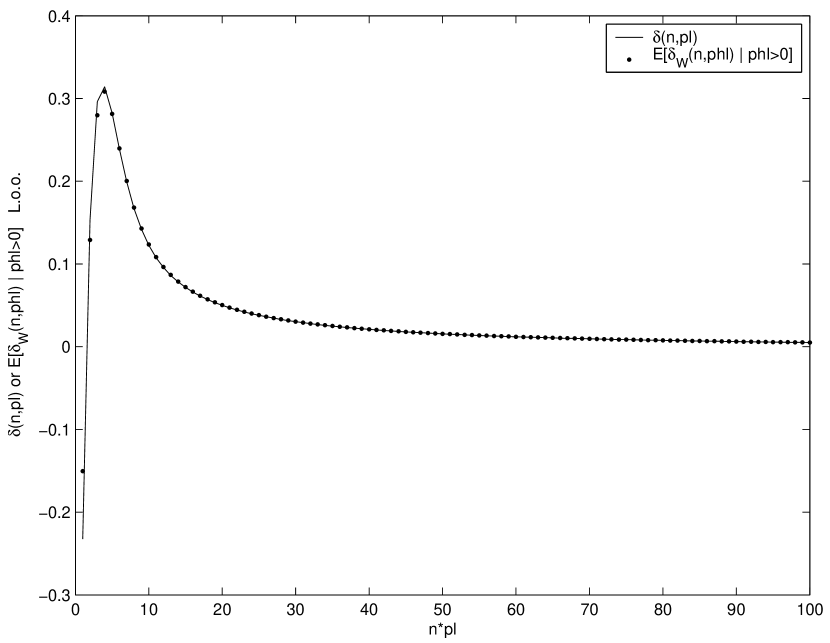

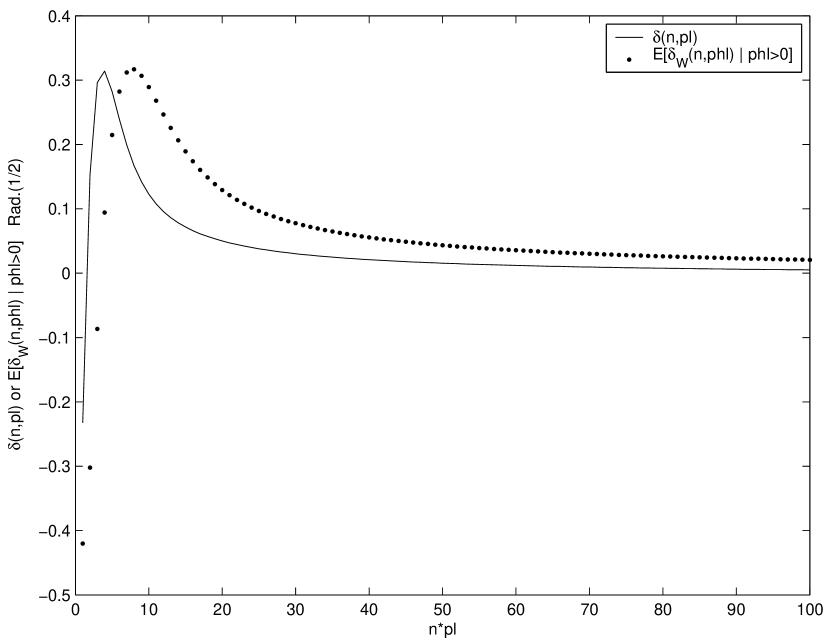

Using the explicit expressions of and , and have been computed numerically as a function of for several resampling schemes, with . The results are given on Figures 6–6 (with straight lines for and dots for ).

It follows that Loo weights are the most accurate ones, even when is small. On the contrary, Rho () and Rad tend to overestimate since (except when is small, where the inequality is reversed). It also seems that the bias of Rho () is a decreasing function of , as illustrated by Figures 6–6. Finally, Efr and Poi are strongly underestimating the ideal penalty, mostly because of the term in and .

This can be summed up as follows:

| (23) |

where “” means a comparatively large gap, but still negligible at first order. Hence, we can expect that the Loo penalty is the most efficient, closely followed by Rad and by Rho. However, from the non-asymptotic point of view, it turns out that smaller prediction loss is obtained by overpenalizing slightly (and sometimes strongly, see the simulations of Section 5 and the discussion of Section 6.3.2). Then, the ordering of (23) may also be the one of the prediction performances of RP, the best performances being obtained with Rad and Rho. This is confirmed by the simulation study of Section 5.

Another interesting point is that when is large enough. Then, provided that histograms with too small bins are removed from the collection, penLoo and penRho are almost equivalent, up to the choice of the factor . If a wise tuning of is possible, it remains to choose between Loo and Rho according to computational issues (see the discussion of Section 6.2).

4.2 Other exchangeable weights

5 Simulation study

As an illustration of the results of Section 3, the prediction performances of Procedure 1 (with several resampling schemes), Mallows’ and -fold cross-validation are compared on some simulated data.

5.1 Experimental setup

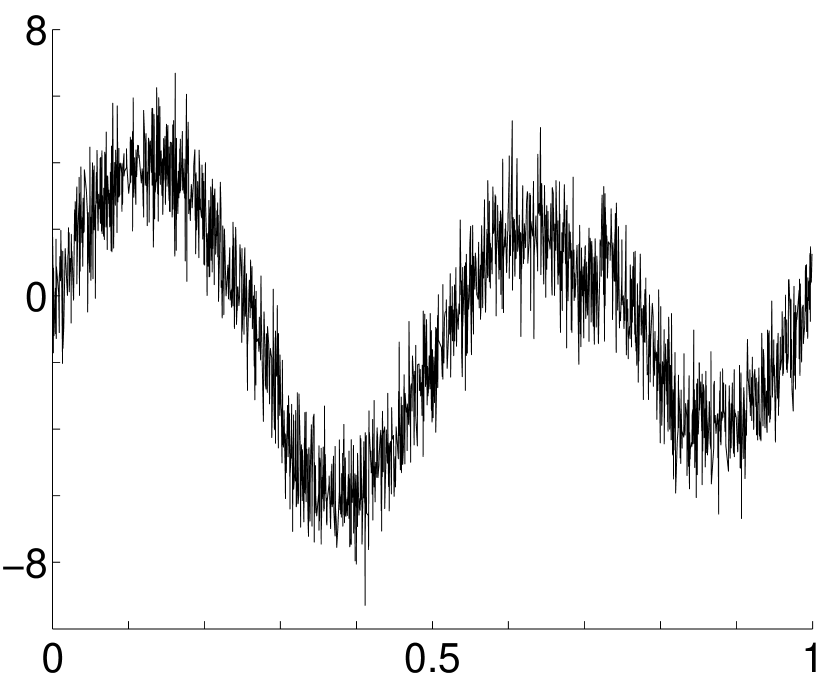

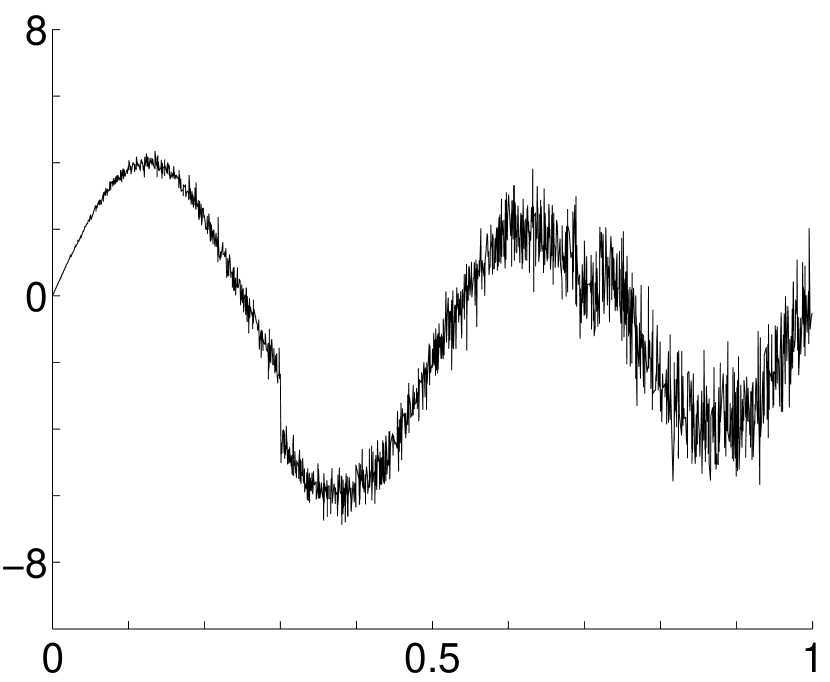

We consider four experiments, called S1, S2, HSd1 and HSd2. Data are generated according to

where are independent with uniform distribution over and are independent standard Gaussian variables independent of . The experiments differ from the regression function (smooth for S, see Figure 12; smooth with jumps for HS, see Figure 12), the noise type (homoscedastic for S1 and HSd1, heteroscedastic for S2 and HSd2) and the sample size (see Table 3). Instances of data sets are plotted on Figures 12–12.

The collections of histogram models also differ according to the experiments. Define

For every , let be the histogram model associated with the partition . Then, for each experiment, the collection of models is with different index sets :

-

S1

regular histograms with pieces, that is

-

S2

histograms regular on (resp. on ), with (resp. ) pieces, . The model of constant functions is added to , that is

-

HSd1

dyadic regular histograms with pieces, , that is

-

HSd2

dyadic histograms regular on (resp. on ) with bin sizes (resp. ), (dyadic version of S2). The model of constant functions is added to , that is

Note that the collections of models used in experiments S2 and HSd2 can adapt to and . Therefore, the oracle model is generally quite efficient so that the model selection problem is more challenging.

The following procedures777The code used for computing resampling penalties is available on the author’s webpage at http://www.di.ens.fr/~arlot/index.htm. are compared:

-

Mal

Mallows’ penalty: where is the classical variance estimator defined as

(24) where , is any model of dimension (only assumed to have a bias negligible in front of ) and is the Euclidean distance on . The non-asymptotic validity of this model selection procedure in homoscedastic regression has been assessed by Baraud Bar:2000 .

-

Expectation of the ideal penalty: , which witnesses what is a good performance in each experiment.

-

VFCV

-fold cross-validation, with (defined as in Arl:2008a ).

-

LOO

Leave-one-out (that is VFCV with ).

-

penEfr

Efron () penalty (7) with .

-

penRad

Rademacher () penalty (7) with .

-

penRho

Random hold-out () penalty (7) with .

-

penLoo

Leave-one-out penalty (7) with .

For each of these, the same penalties multiplied by are also considered (and they are denoted by a symbol added after the shortened names). This intends to test for overpenalization (the choice of the factor being arbitrary and certainly not optimal, see Section 6.3.2).

In each experiment, for each simulated data set, first the models with data points or less in one piece of their associated partition are removed. Then, the least-squares estimators are computed for each . Finally, is selected using each procedure and its true excess loss is computed as well as the excess loss of the oracle . data sets are simulated, thanks to which the model selection performance of each procedure is estimated through the two following benchmarks:

Basically, is the constant that should appear in an oracle inequality like (9), and corresponds to a pathwise oracle inequality like (8). Since and approximatively give the same rankings between procedures, Table 3 only reports ; the values of are reported in Arl:2008b:app .

| Experiment | S1 | S2 | HSd1 | HSd2 |

| HeaviSine | HeaviSine | |||

| 1 | 1 | |||

| (sample size) | 200 | 200 | 2048 | 2048 |

| regular | 2 bin sizes | dyadic, regular | dyadic, 2 bin sizes | |

| + | ||||

| Mal | ||||

| Mal+ | ||||

| 2-FCV | ||||

| 5-FCV | ||||

| 10-FCV | ||||

| 20-FCV | ||||

| LOO | ||||

| penRad | ||||

| penRho | ||||

| penLoo | ||||

| penEfr | ||||

| penRad+ | ||||

| penRho+ | ||||

| penLoo+ | ||||

| penEfr+ |

5.2 Results and comments

First, the above experiments show the interest of both Resampling Penalization (RP) and VFCV in several difficult frameworks, with relatively small sample sizes. Although RP and VFCV cannot compete with simple procedures such as Mallows’ from the computational point of view, they are much more efficient when the noise is heteroscedastic (S2 and HSd2). In these difficult frameworks, the prediction performances of RP and VFCV are comparable to those of . Note that in HSd2, penRad and penRho give smaller losses than any penalty proportional to the dimension of the models (see Section 7.1.2). Moreover, penRad and penRho perform slighlty worse than Mallows’ for the easiest problems (S1 and HSd1), which can be interpretated as the unavoidable price for robustness.

Second, in the four experiments, the best procedures always are the overpenalizing ones: many of them even beat the perfectly unbiased , showing the crucial need to overpenalize. This phenomenon disappears for small and large (Arl:2008b:app, , Experiments S0.1 and S1000), hence it is certainly due to the small signal-to-noise ratio. We would like to insist on the importance of the overpenalization phenomenon, which is seldom mentioned in theoretical papers because it vanishes in the asymptotic framework, and it is quite hard to find from theoretical results.

Let us now compare RP and VFCV. According to the four experiments of Table 3, RP with Rad or Rho resampling schemes clearly outperforms VFCV for any , even without overpenalizing. The only exception to this is HSd1 where -fold cross-validation yields a particularly good model selection performance.

This can be interpretated thanks to the non-asymptotic study of the performance of -fold cross-validation provided in Arl:2008a . In short, VFCV overpenalizes within a factor , while the -fold criterion has a variance decreasing with .

Then, when overpenalization is necessary (for instance in S1, S2 or HSd1), small values of can outperform the leave-one-out (). Nevertheless, RP with the right overpenalization level leads to a smaller prediction loss than VFCV, because RP provides a less variable model selection criterion than VFCV. The reason why penRad and penRho also perform slightly better without overpenalization is that they naturally overpenalize when (see Section 4).

Let us now consider the model selection performance of RP with several exchangeable resampling schemes. The two best ones are Rad and Rho in the four experiments, with or without overpenalization. Then, Loo performs slightly worse (but not always significantly) and Efr much worse. Looking carefully at the values of the penalties, it appears that Rad and Rho slightly overpenalize, Loo is exactly at the right level, and Efr underpenalizes (as well as Poi, which has performances quite similar to the ones of Efr, see Arl:2008b:app ). Note that this comparison can also be derived from theoretical computations (see Section 4). Since overpenalization is benefic in the four experiments of Table 3, this explains why penRad and penRho slightly outperform penLoo. In the case of Efron’s boostrap penalty, underpenalizing implies overfitting which explains the comparatively bad performances reported in Table 3.

We conclude this section with remarks concerning some particular points of the simulation study.

-

•

On the same data sets, Mallows’ and its overpenalized version Mal+ were performed with the true mean variance instead of (which would not be possible on a real data set). It yielded worse model selection performance for all experiments but S2, in which and . Therefore, overpenalization is crucial in experiment S2, more than the shape888The shape of a penalty is defined as the way depends on up to a linear transformation. of the penalty itself. Moreover, the overpenalization level being fixed, resampling penalties remain significantly better than Mallows’ . Hence, the performances of Mallows’ in Table 3 are not only due to a bad estimation of the mean noise-level (see also Section 7.1).

-

•

Eight additional experiments are reported in Arl:2008b:app , showing similar results with various , and (although the assumptions of Theorem 1 are not always satisfied).

-

•

Resampling penalties with a -fold subsampling scheme have also been studied in (Arl:2008a, , Section 4) on the same simulated data: exchangeable resampling schemes always give better model selection performance than non-exchangeable ones (significantly when is small), except for Efr and Poi which tend to underestimate the ideal penalty.

6 Practical implementation

This section tackles three main issues for using Procedure 1 in practice: how to compute the resampling penalty (7)? how to choose the weights ? how to choose the constant ?

6.1 Computational cost

An exact computation of resampling penalties with exchangeable weights (without using formula (50) for histograms) would be either impossible or computationally expensive. We suggest two possible ways to fix this problem.

First, one can use a classical Monte-Carlo approximation, that is draw a small number of independent weight vectors instead of considering each element of the support of . Practical Monte-Carlo methods for the boostrap are proposed for instance by Hall (Hal:1992, , Appendix II). Moreover, a non-asymptotic estimation of the accuracy of Monte-Carlo approximation can be obtained via McDiarmid’s inequality (see Arlot, Blanchard and Roquain (Arl_Bla_Roq:2008:RC, , Proposition 2.7) for a precise result using the same idea in another framework). This would provide a practical way of quantifying what is lost by making a Monte-Carlo approximation, and choose consequently (at least for Rad, Rho and Loo weights).

Second, it is possible to use non-exchangeable weight vectors such that the cardinality of the support of is much smaller than . A case-example is -fold subsampling: given a partition of and a uniform random variable over independent of the data, we define

The resulting resampling penalties —called -fold penalties— have been introduced and studied in Arl:2008a . They are computationally similar to VFCV while being more flexible, since the overpenalization factor is decoupled from the choice of ; hence, like resampling penalties, -fold penalties select an estimator with smaller prediction loss than the one selected by VFCV.

Both Monte-Carlo approximation of RP and -fold penalization have been tested on the simulated data of Section 5. The detailed results are given in Arl:2008b:app .

6.2 Choice of the weights

The influence of the weights has been investigated from the theoretical point of view in Section 4 with focus on second-order terms in expectation. However, deviations of around its expectation are likely to depend on the weight vector since the upper bound in (17) may not be tight. The simulation study of Section 5 allows to take into account both phenomena in the comparison between the resampling weights.

In terms of model selection efficiency, Table 3 shows that the best weights (for accuracy of prediction and for the variability999The variability of the accuracy is more an indicator of the stability of the performance of RP than of the variance of the resampling penalty. However, it remains an interesting measure, since a procedure performing always equally well can be preferred to a procedure with better mean efficiency but poor performances on a small probability event. of this accuracy) are Rho and Rad, whereas Loo perform slightly worse. On the contrary, from both accuracy and variability points of view, Efron’s bootstrap weights perform worse than Rho, Rad and Loo, mainly because they lead to underpenalization.

Note however that this comparison strongly depends on the precise definition101010However, it is quite unclear how to change in order to optimize each penalty in the general case. This is why has been chosen as “simple” as possible in Table 2. of , which makes all penalties unbiased at first order but possibly under or over-penalizing at second order. Then, different prediction performances may be observed on data which do not require overpenalization. Nevertheless, the computations of Section 4 show that Efron’s bootstrap weights have a real drawback which cannot be fixed only by changing .

When computing the penalties exactly, Loo weights are the only computationally tractable ones, while being almost as accurate as Rho and Rad. Hence, we suggest their use, enlarging the constant when needed (see Section 6.3.2 on overpenalization).

However, computing empirical risk minimizers (or the outputs of computationally more expensive algorithms) for each model is not always possible. In such a case, one should avoid using the Leave-one-out with a Monte-Carlo approximation, which would give a large importance to a small number of data points. Rho or Rad weights are much safer in this situation. Alternatively, one may consider the use of -fold penalties Arl:2008a as a good alternative when the computational power is limited.

Let us emphasize that this analysis and the subsequent advices should be considered with caution. First, the deviations of resampling penalties around their expectations should be understood much better, because they can be comparable or even larger than the second-order terms in expectations. Second, the optimal choice of for -fold cross-validation is known to be different between least-squares regression and binary classification (Arl:2008a, , Section 2.3). Such differences are expected to arise for choosing between exchangeable resampling weights.

Remark that the bias of the bootstrap penalty has already been noticed by Efron Efr:1983 ; Efr:1986 who proposed several ways to correct it, including a double bootstrap procedure and the .632 bootstrap. The novelty of the approach of this paper is to propose the use of other exchangeable resampling schemes instead of the boostrap so that the bias of resampling penalties no longer has to be corrected.

6.3 Choice of the constant C

6.3.1 Optimal constant for bias

From the asymptotic point of view, the optimal for prediction is generally the one for which estimates the ideal penalty unbiasedly (at least for collections of models of polynomial size). This is how is defined in the histogram framework and Theorem 1 implies that is asymptotically optimal for prediction. Hence111111See the proof of Theorem 1 in Arl:2008a to prove that asymptotic optimality requires as soon as there are enough models close to the oracle., is asymptotically equivalent to .

As showed by Arlot and Massart Arl_Mas:2008 , can also be estimated directly from data for general penalties, in particular for RP. Hence, the knowledge of is not necessary, which can be useful in the general prediction framework (see Section 7.2).

6.3.2 Overpenalization

A careful look at the proof of Theorem 1 shows that a similar oracle inequality holds for any , the leading constant remaining close to one when asymptotically. In other words, when the sample size is small, the optimal constant may not be exactly equal to . The simulations of Section 5 also support this fact: Overpenalization, that is, taking with , can improve the prediction performance of when is small, when is large or when is non-smooth.

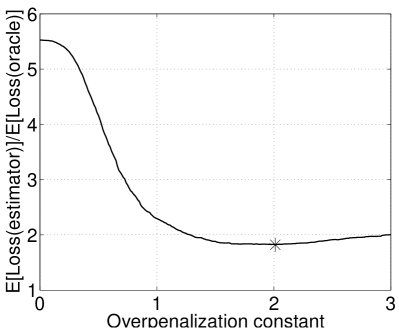

This problem would appear even if the “optimal” constant such that is non-asymptotically unbiased was known. On Figure 13, the estimated model selection performance of the penalty is plotted as a function of , for experiment S2 of Section 5. It appears that the optimal overpenalization constant for this particular problem. More generally, the drawback of using is that it does not take into account the deviations of around its expectation. To avoid the possible overfit induced by these deviations, the constant must be slightly enlarged. A major issue remains: How to estimate from data only, since it strongly depends on , on , on the smoothness of and on the number of models in ?

One can think of choosing by -fold cross-validation, but this would lead to a computationally intractable procedure. An alternative idea is to use resampling for building a simultaneous confidence region on instead of estimating only (see Arl_Bla_Roq:2008:RC on confidence regions built with general exchangeable resampling schemes). Then, the uncertainty on the estimation of can be taken into account for choosing a model, similarly to model selection procedures built upon relative bounds Aud:2004 ; Cat:2007 . Finally, the choice of the overpenalization factor would be replaced by the choice of a confidence level which should be made by the practicioner. See also (Arl:2007:phd, , Section 11.3.3) for a discussion on a data-driven choice of the overpenalization factor.

7 Discussion

7.1 Comparison with other procedures

In this article, the Resampling Penalization (RP) family of model selection procedures is defined and showed to satisfy some optimality properties under mild assumptions on the data (Theorems 1 and 2). In particular, RP is robust to the heteroscedasticity of the noise according to both theoretical and experimental results. The price for robustness is that the computational cost of RP is generally larger than simple procedures like Mallows’ , even with the suggestions of Section 6.1. The purpose of this subsection is to identify the “easy” problems, for which the computational cost of RP can be reduced by using -like penalties without enlarging the prediction loss too much.

7.1.1 Mallows’

Mallows’ penalty is equal to for a model of dimension , when the noise-level is constant. Non-asymptotic results about -like penalties can be found in Bar_Bir_Mas:1999 ; Bar:2000 ; Bar:2002 ; Bir_Mas:2006 . They imply that Mallows’ is asymptotically optimal in the homoscedastic framework, when the size of is polynomial in .

When the mean noise-level is unknown, it must be estimated. A classical estimator of is defined by (24). Baraud Bar:2000 ; Bar:2002 showed that the resulting data-driven model selection procedure satisfies a non-asymptotic oracle inequality with leading constant close to one.

Assume for the sake of simplicity that is even and let be a model such that each piece of the associated partition contains exactly two data points. Reordering the according to ,

so that

| (25) | |||

This should be compared with the result of Proposition 1:

| (26) | |||

Although both Mallows’ and the ideal penalty are in expectation the sum of a “variance” term (involving the ) and a “bias” term (involving the variations of through or ), they differ on at least two points.

First, when is smooth and is large, the “bias” term in (25) is negligible in front of the one of (26), which means that Mallows’ underpenalizes when the “bias” component of is large. Second, the “variance” component of , which is the main one in general, is distorted in Mallows’ : the part of the penalty corresponding to is multiplied by which is not close to 1 when the partition is not regular with respect to . This happens for instance in experiments S2 and HSd2 of Section 5. Therefore, there are at least three possibly “hard” problem classes:

-

•

heteroscedastic noise, with irregular histograms and uniform (for instance S2, HSd2 in Section 5, or Svar2 in Arl:2008b:app ),

-

•

heteroscedastic noise, with regular histograms and highly non-uniform on ,

-

•

regression function with jumps (such as HeaviSine121212However, in experiment HSd1, Mallows’ still behaves quite well compared to RP. We do not know whether the non-smoothness of can actually make Mallows’ fail.) or large non-smooth areas (such as Doppler in Arl:2008b:app ).

In either of these cases, one should avoid the use of -like penalties, and we suggest resampling penalties as an efficient alternative. As explained in Section 7.1.2 below, the first class of problems can make any penalty proportional to the dimension suboptimal.

7.1.2 Linear penalties

Mallows’ is simple because it is a linear function of the dimension of :

| (27) |

and is the only constant to determine. Depending on what is known on the mean variance level, the constant can be defined as

Refined versions of Mallows’ have also been proposed Bar_Bir_Mas:1999 ; Bar:2002 ; Bir_Mas:2006 but they are still linear or very close to linearity.

However, according to (11), the ideal penalty is not linear in general, even in expectation. Moreover, there exist some frameworks in which any penalty of the form (27) is suboptimal when data are heteroscedastic Arl:2008:shape , that is, it cannot satisfy any oracle inequality with leading constant smaller than some absolute constant . In other words, the optimal linear penalization procedure is suboptimal, where

As showed by Theorem 1, RP does not suffer from this drawback.

On the one hand, the optimal linear penalization procedure has a better model selection performance than RP for S1, S2 and HSd1, which is not surprising for the “easy” problems where Mallows’ is almost optimal (S1, HSd1). It is less intuitive for S2 where data are heteroscedastic. Considering that uses the knowledge of the true distribution , one can understand that it is sufficient to keep a good performance for “intermediate” problems.

On the other hand, in experiment HSd2, the optimal linear penalization has a model selection performance , which is worse than the one of RP (). Thus, the most difficult problem of Section 5 (with a large collection of models, heteroscedastic data and bias) gives an example where linear penalties are definitely not adapted, in addition to the ones of Arl:2008:shape .

7.1.3 Ad hoc procedures

One of the main advances with Theorems 1 and 2 is that RP is proved to work in the heteroscedastic framework contrary to Mallows’ . Nevertheless, in a framework such as the one of experiment S2, Mallows’ can be adapted to heteroscedasticity by splitting into several parts where is almost constant, and performing the histogram selection procedure with Mallows’ separately on each part of .

More generally, Efromovich and Pinsker Efr_Pin:1996 and Galtchouk and Pergamenschikov Gal_Per:2008 (among several others) defined estimators of that are minimax adaptive in the heteroscedastic framework, the latter by model selection. In the Gaussian regression framework, Gendre Gen:2008 proposed a model selection method for estimating simultaneously the regression function and the noise level.

All these procedures may perform slightly better than RP in terms of prediction loss. They are called “ad hoc” because they have been specially designed for the heteroscedastic framework (and a particular collection of estimators for Gal_Per:2008 ; Gen:2008 ). On the contrary, RP is a general-purpose device: It was neither built to be adaptive to heteroscedasticity nor to take advantage of a specific model, and RP has exactly the same definition in the general prediction framework (see Section 7.2).

When no information is available on the data or when no model selection procedure is known for using such information, we suggest the use of RP. Moreover, available information can be partial or wrong. Then, using an ad hoc procedure would be disastrous whereas a general device like RP would still work. In short, choose RP if you have no useful information or if you do not trust them.

7.1.4 Other model selection procedures by resampling

The most well-known resampling-based model selection procedure is cross-validation. For practical reasons, it is often used in its -fold version which can have some tricky behavior, in particular for choosing Yan:2007b ; Arl:2008a . This can also be showed in the simulation experiments of Section 5 (see Table 3): In HSd1, performs better than , a phenomenon explained in Arl:2008a by analyzing how the bias of the -fold criterion depends on .

-fold penalization, that is, RP with a -fold subsampling scheme, was proposed in Arl:2008a where it was showed to improve significantly the model selection performance of VFCV. In this paper and in Arl:2008b:app , RP with several exchangeable resampling schemes —generalizing the case— is proved to perform at least as well as -fold penalization and often better.

Several penalization procedures use the bootstrap for estimating the ideal penalty Efr:1983 ; Cav_Shu:1997 ; Shi:1997 . As noticed in Remark 6, the penalization procedures studied by Shibata Shi:1997 are quite close to RP, although they are restricted to bootstrap weights, which are the worst ones in the framework of the present paper (see Sections 4.1 and 6.2). Moreover, they do not consider useful to multiply the penalty by a factor possibly different from one, contrary to what is suggested in RP. The factor is crucial because it disconnects the choice of the weights from the overpenalization problem.

In order to select the correct model asymptotically with probability one, Shao Sha:1996 proposed to use RP with the out of bootstrap and provided a sufficient condition on to achieve model consistency. Thanks to the unified approach for all the exchangeable resampling weights provided in this paper, Shao’s condition can be rewritten as (see Remark 6), which corresponds to the known fact that model consistency requires overpenalization within a factor tending to infinity with Aer_Cla_Har:1999 . Hence, we conjecture that RP with a constant is model consistent for most exchangeable , which may improve Shao’s penalties since Efr() weights are probably not the best weights in terms of accuracy (see Section 4) and variability131313Taking into account all the data for computing the resampling penalty with Efr() weights is computationally costly when is large..

7.2 Resampling Penalization in the general prediction framework

As mentioned in Section 2.1, Resampling Penalization is a general-purpose method which is definitely not restricted to the histogram selection problem. The purpose of this subsection is to define properly RP in the general prediction framework and to discuss briefly what differences can be expected compared to the histogram selection framework.

7.2.1 Framework

Suppose we observe some data independent with common distribution . The goal is to predict given where is independent of the data. The quality of a predictor is measured by the prediction loss where and is a given contrast function. Typically, measures the discrepancy between and . The excess loss is defined as , even if is not well-defined. Classical examples are least-squares regression where and and binary supervised classification where and is the 0-1 contrast.

A general prediction algorithm is then defined as a function associating a predictor to any data sample. In order to simplify the presentation, algorithms are assumed to depend only on the empirical distribution as an input141414Otherwise, we can consider algorithms whose input is any weighted sample.. For instance, the empirical risk minimizer over a set of predictors is defined as , provided the minimum in exists and is unique.

Let us assume that a collection of algorithms is given. The goal is to select some data-dependent minimizing the prediction loss . The penalization method consists in selecting

where is a penalty function, possibly data-dependent. Since the goal is to minimize the prediction loss, the ideal penalty is

which cannot be used because it depends on the unknown distribution . When is not too large (for instance, when for some positive constants ), a natural strategy is to define as an estimator of with a bias as small as possible.

7.2.2 Definition of Resampling Penalization

As detailed in Section 2.2, the resampling heuristics can be used for estimating , leading to the following procedure.

Procedure 3 (Resampling Penalization).

-

1.

Replace by

-

2.

Choose a resampling scheme, that is the distribution of a weight vector .

-

3.

Choose a constant .

-

4.

Compute the following resampling penalty for each :

(28) where .

-

5.

Select .

As for the histogram selection problem, two possible problems have to be solved. First, may not be well-defined for a.e. even if . A way to define properly the resampling penalty for every such that is well-defined for every is suggested in (Arl:2007:phd, , Section 8.1). This assumption is satisfied by regressograms (hence, in the framework of the rest of the paper) for which the suggest of (Arl:2007:phd, , Section 8.1) yields exactly the penalty (7).

Second, the constant such that (28) estimates unbiasedly when is required in Procedure 3. For the histogram selection problem, the explicit expression of follows from Propositions 1 and 2. In general, the asymptotic theory of exchangeable bootstrap empirical processes (vdV_Wel:1996, , Theorem 3.6.13) suggests that if , which holds for the classical weights Efr, Rad, Poi and Rho; nevertheless, asymptotic control on the bias is not sufficient when the collection of algorithms is allowed to depend on the sample size , as in the histogram selection problem. Therefore, further theoretical investigations would be useful to compute the theoretical value of to be used in Procedure 3. From the practical point of view, the data-driven calibration algorithm of Arl_Mas:2008 can be used for choosing the constant in front of the resampling penalty.

7.2.3 Model selection properties of Resampling Penalization

The theoretical validity of Procedure 3 is only proved for histogram model selection in this paper, because precise non-asymptotic controls of the ideal penalty and its resampling counterpart are needed. To our knowledge, the only known result about model selection with Resampling Penalization was that RP with the classical bootstrap weights (Efr) is asymptotically optimal for selecting among maximum likelihood estimators in Shi:1997 , assuming that the distribution belongs to some parametric family of densities.

RP can be conjectured to enjoy adaptivity properties for a wide class of model selection problems for two main reasons. First, RP relies on the resampling idea which is known to be robust in a wide variety of frameworks; Theorems 1 and 2 have confirmed the robustness of RP to heteroscedasticity, whereas RP has not been designed specifically for least-squares regression with heteroscedastic data. Second, several of the key concentration inequalities used to prove Theorems 1 and 2 have been extended in (Arl_Mas:2008, , Propositions 8 and 10) to a general framework including bounded regression and binary classification.

As mentioned at the end of Section 7.2.1, Procedure 3 should be restricted to choosing among a number of algorithms at most polynomial in . Indeed, when is larger, estimating unbiasedly can yield strong overfitting Bir_Mas:2006 . Therefore, RP must be modified for large collections . We suggest to group algorithms according to some modelling complexity index , such as the dimension of if is the empirical risk minimizer over some vector space ; then, for every , define where ; finally, apply Procedure 3 to the collection , assuming that is at most polynomial in .

7.2.4 Related penalties for classification

In the classification framework, RP should be compared to several classical resampling-based penalization methods. First, RP with Efr weights was first introduced by Efron Efr:1983 and called bootstrap penalization; its main drawback is its bias (as for the histogram selection problem), which can be corrected in several ways, using for instance the double bootstrap penalization or the .632 bootstrap Efr:1983 . Nevertheless, the computational cost of the double bootstrap is heavy and the general validity of the .632 bootstrap is questionable because of its poor theoretical grounds.

Second, the global Rademacher complexities were introduced in order to obtain theoretically validated model selection procedures in classification Kol:2001 ; Bar_Bou_Lug:2002 . They are resampling estimates of