Improved Frechet bounds and model-free pricing of multi-asset options

Abstract

Improved bounds on the copula of a bivariate random vector are computed when partial information is available, such as the values of the copula on a given subset of , or the value of a functional of the copula, monotone with respect to the concordance order. These results are then used to compute model-free bounds on the prices of two-asset options which make use of extra information about the dependence structure, such as the price of another two-asset option.

Key words: copulas, Frechet-Hoeffding bounds, concordance order, basket options.

AMS 2010 subject classification: 60E15, 91G20

1 Introduction

A (two-dimensional) copula is a function with the following properties:

-

i.

Boundary conditions: and for all .

-

ii.

is -increasing, i.e. for every and , one has

(1)

The classical Frechet-Hoeffding bounds on the distribution function of a two-dimensional random vector, can be expressed in terms of the copula of this vector:

| (2) |

In the presence of additional information on the dependence between the components of the vector, these bounds can be narrowed. Nelsen et al. [9] compute the improved bounds when a measure of association such as Kendall’s or Spearman’s is given, and the Bertino’s family of copulas [1] yields best possible bounds when the values of the copula on the main diagonal are known. More generally, given a nonempty set of bivariate copulas , Nelsen et al. [10] introduce pointwise best-possible bounds of :

These bounds are in general not copulas but quasi-copulas, and a fortiori they do not necessarily belong to the set .

In the theoretical part of this paper (section 3), we first compute the improved Frechet bounds when the values of the copula on an arbitrary subset of are given, and provide a sufficient condition for each bound to be a copula, and therefore, be the best possible bound. This generalizes the findings of [10] on the improved Frechet bounds for copulas with given diagonal sections. Next, we compute the best-possible bounds when the value of a real-valued functional of the copula, monotone with respect to the concordance order and continuous with respect to pointwise convergence of copulas is given, extending the results of [9].

Since the work of Rapuch and Roncalli [11] it is known that the prices of most two-asset options, when the marginal laws of the two assets are fixed, become monotone functionals of the copula with respect to the concordance order. The classical Frechet-Hoeffding bounds therefore lead to model-free price estimates for such options [11, 4, 3].

In section 4, we obtain a new representation for the price of a two-asset option, allowing to use a quasi-copula. This representation enables us to compute (in section 5) the improved model-free estimates of the option’s value when the prices of all single-asset options on each of the two assets are known and some extra information about the dependence structure. This extra information may be, for example, the price of a different two-asset option (for example, zero-strike spread options are often quoted in the market), or the correlation of two assets. This is similar in spirit to a recent work by Kaas et al. [5] who compute worst-case bounds on the Value at Risk of a portfolio of two assets when the marginals and a measure of association are known.

2 Preliminaries

In this section, we recall several useful definitions and results and fix the notation for the rest of the paper. In the definition of quasi-copula [2], the -increasing property (1) is replaced by weaker assumptions:

Definition 1.

A (two-dimensional) quasi-copula is a function with the following properties:

-

i.

Boundary conditions: and for all .

-

ii.

is increasing in each argument.

-

iii.

Lipschitz property: for all .

We denote the set of all copulas on by and the set of all quasi-copulas by . The concordance order is the order on defined by if and only if . It is clear that all quasi-copulas satisfy the Frechet-Hoeffding bounds (2). Similarly, we say that pointwise if . The Lipschitz property implies that in this case the convergence is uniform in .

For a copula or a quasi-copula and a rectangle , we define .

A subset is called increasing if for all and either and or and . It is called decreasing if for all and either and or and . It is easy to see that for a decreasing set , the set is increasing. In the same spirit, if is a copula, the function is also a copula and if is a quasi-copula, is also a quasi-copula.

The following well-known result (see e.g. Theorem 3.2.3 in [8]), gives the best-possible bounds of a set of copulas taking a given value at a given point.

Proposition 1.

Let be a copula and suppose with . Then

| (3) |

where

are copulas satisfying .

Remark 1.

To close this section, we recall a well-known fact on distribution functions. Given a one-dimensional distribution function we define its generalized inverse by

with the convention . If the couple has copula then has the same law as , where are random variables with distribution function .

3 Constrained Frechet bounds

Let be a compact subset of and be a quasi-copula. We denote by the set of all copulas such that for all , and by the set of all quasi-copulas such that for all . Define

| (4) | ||||

| (5) |

The following theorem establishes that and are best-possible bounds of the set . This means that they are also bounds of the set , but not in general best possible. The second part of the theorem gives a sufficient condition under which or is a copula, and therefore a best possible bound of . As a by-product of the second part, we obtain an example of copula which coincides with a given quasi-copula on a given increasing or decreasing set.

Theorem 1.

-

i.

and are quasi-copulas satisfying

for every and

(6) for all .

-

ii.

If the set is increasing then is a copula; if the set is decreasing then is a copula.

The proof of this theorem can be found in the Appendix.

Example 1.

This example, similar to example 2.1 in [10] shows that if is increasing, may not always be a copula. Let and . Then , and , so that the -volume of the rectangle is equal to . Similarly, if is decreasing, is not always a copula.

Let be a mapping, continuous with respect to pointwise convergence of copulas and nondecreasing with respect to the concordance order on . We are interested in computing pointwise best possible bounds of the sets and . We denote

for .

For and , we define

For fixed , the mappings and are nondecreasing and continuous, and we define the corresponding inverse mappings by

for all such that the corresponding set over which the maximum or minimum is taken is nonempty.

Theorem 2.

Let . The bounds and are given by

| (7) | ||||

| (8) |

The proof of this theorem can be found in the Appendix.

Remark 2.

This result generalizes theorems 2 and 4 in [9], which treat the cases when is the Kendall’s and the Spearman’s . In these two cases, and are copulas. However, in general, this may not be the case. Let , , , and define

An easy computation shows that

that is, we obtain the copula of Equation (4) with and such that and . Then, example (1) shows that is not always a copula.

4 Copula based pricing of multi-asset options

We consider the problem of pricing a European-style option whose pay-off depends on the values of two random variables and . These random variables can represent the terminal values of two assets (in the context of equity options) or some other risk factors which influence the value of the option, such as the default dates of two defaultable bonds.

We assume that the law of and under the historical probability is unknown, or is very hard to estimate, so that all information comes from the prices of traded options on these assets.

Under the standard assumption of absence of arbitrage opportunities in the market, the option pricing theory implies that there exists a risk-neutral probability such that the option price is given by the discounted expectation of its pay-off under . In practice is not known, and only some incomplete information on it can be deduced from the prices of traded options on and .

We assume that these traded options include single-asset options allowing to reconstruct the cumulative distribution functions and of and . For example, if is the price of an asset at time and call options on this asset with prices , are available (where is the interest rate and is the strike price), the distribution function can be reconstructed as . Similarly, if is the default date of a defaultable bond, the distribution function may be reconstructed from the prices of credit default swaps on this bond with different maturities.

Let the discounted pay-off function of a two-asset option be denoted by . Its price then becomes a function of the copula of and :

| (9) |

It is known [7, 12] that for every 2-increasing function such that the integral in (9) exists, the mapping is nondecreasing with respect to the concordance order of copulas. Therefore, if the pay-off function is -increasing, and if we know that the copula of and satisfies for two copulas and , the option price satisfies . For example, if no additional information on the joint law of and is available, the standard Frechet bounds lead to

Since the support of is the diagonal and that of is the diagonal , these bounds are further simplified to

However, if and are quasi-copulas, this method no longer applies because the integral in (9) may not be well defined. The following result provides an alternative representation for which can be used for quasi-copulas, and establishes other useful properties of this mapping. We recall [6, Section 4.5] that for a 2-increasing function on which is left-continuous in both arguments, there exists a unique positive measure on such that

| (10) |

Proposition 2.

Assume that is 2-increasing, left-continuous in each of its arguments, and let the marginal laws of and satisfy

Then, and the mapping is well-defined for all , continuous with respect to pointwise convergence of copulas and satisfies

| (11) |

where is the positive measure on induced by .

The proof of this proposition can be found in the Appendix.

Remark 3.

Expression (11) can be alternatively written as

where is the survival copula defined by

and and are survival functions of and .

Table 1 gives several examples of 2-asset options whose pay-offs are 2-increasing (or 2-decreasing, meaning that is 2-increasing) continuous functions. These are mainly taken from [11]. For all these pay-offs, the integral with respect to in formula (11) reduces to a one-dimensional integral. Another important example is the function which is also 2-increasing, which means that for fixed marginal distributions, the linear correlation coefficient

is nondecreasing with respect to the concordance order of copulas. The corresponding measure is the Lebesgue measure on .

| Option type and |

increasing?

|

|

|---|---|---|

| Basket option, | if , if | |

| Call on the minimum |

|

|

| Put on the minimum |

|

|

| Call on the maximum |

|

|

| Put on the maximum |

|

|

| Worst-off call |

|

|

| Worst-off put |

|

|

| Best-off call |

|

|

| Best-off put |

|

5 Application: model-free bounds on option prices

In this section, we derive model-free bounds on the prices of two-asset options whose pay-off function satisfies the assumptions of Proposition 2 when extra information about the dependence of and is given. We give four examples corresponding to different kinds of extra information and different option pay-offs.

Example 2 (The case when prices of digital basket options are known).

As our first example, we consider an application to credit risk modeling assuming that and represent the times of default of two corporate bonds. In this context, an important problem is the pricing of the so called “first to default” option with pay-off at maturity given by or the “second to default” option with pay-off . The price of each of these options is directly related to the value of the copula of and at the point :

In view of the above, we concentrate on the “second to default” options. From the prices of these options with maturities , one can recover the values of the copula of and on the increasing set . Therefore, by Theorem 1, the copula of and satisfies

with

and the price of any 2-asset option whose pay-off function satisfies the assumption of Proposition 2 admits the bounds

Since, by Theorem 1, is a copula, the lower bound is sharp, while the upper bound may not necessarily be sharp.

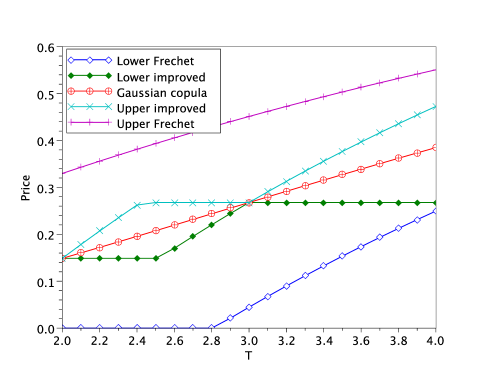

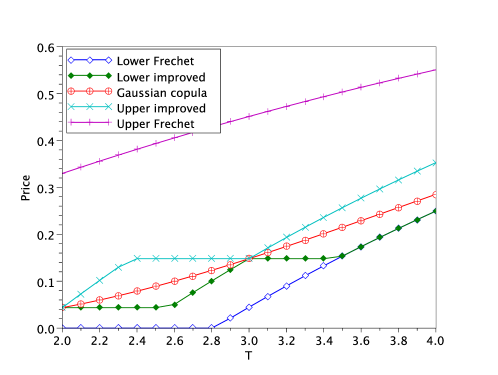

As an illustration, we have computed the upper and lower improved bounds for the prices of “second to default” options with different times to maturity. We assume that the marginal laws of and are exponential with parameters and respectively, and that the prices of the “second to default” options with and years to maturity are known. In this example, these two prices are computed assuming that and have Gaussian copula with correlation (the Gaussian copula is the industry standard). Figure 1 shows the prices of the “second to default” options as function of time to maturity for two different values of , along with the price in the “Gaussian copula” model and the standard Frechet bounds (without any information about dependence).

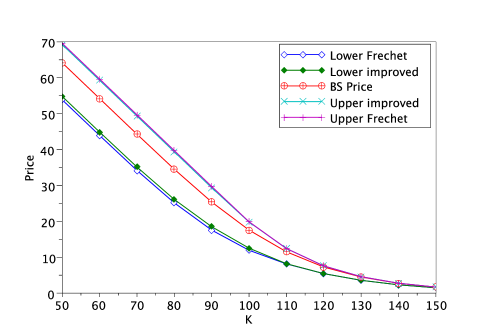

Example 3 (The case when prices of all options on the maximum of two assets are known).

The knowledge of prices of call or put options on the maximum or the minimum of and , for all strikes, allows to recover (by differentiation) the values of the distribution function for , or, equivalently, the values of the copula on the increasing set . Therefore, similarly to the previous example, the copula of and satisfies

where

| (12) | ||||

| (13) |

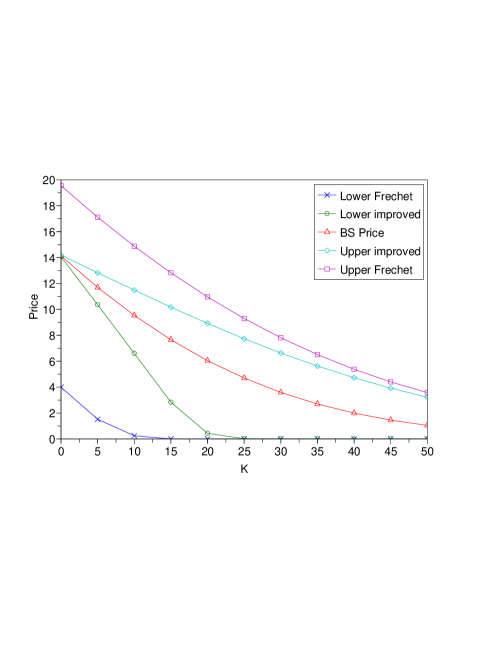

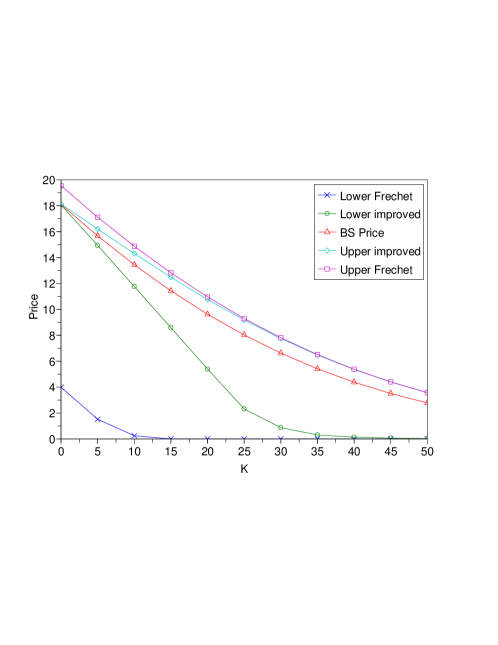

To illustrate this method, we have computed the improved upper and lower bounds for the spread option with pay-off at date given by . To fix the marginal laws of and , we assume that and , where , , and and are standard Brownian motions. We further assume that the prices of all options on the maximum of and are equal to the corresponding prices in a model where and are jointly Gaussian with correlation .

Figure 2 plots the improved bounds on the spread option price as function of the strike for two different values of the correlation , along with the Black-Scholes price and the standard Frechet bounds. For the numerical computation of the bounds, we have taken a discrete set of 400 strikes in (12) and (13) and used numerical integration to evaluate (11), which reduces to a one-dimensional integral in this case.

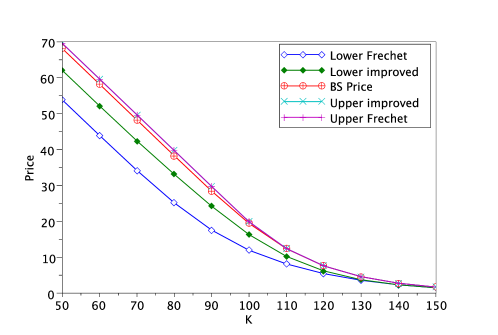

Example 4 (The case when a single option price is known).

Assume now that the extra information about the dependence structure of and is the expectation of a function which satisfies the assumptions of Proposition 2: . In this case, the price of a 2-asset option whose pay-off satisfies the assumptions of Proposition 2 admits the bounds with and given by Theorem 2. Although and are best-possible bounds of the set of copulas satisfying , if they are not copulas themselves, the bounds on the option price may not be best possible.

For the actual computation of and we reduce the expressions for and to one-dimensional integrals using the results in [8, section 3.2.3]:

As the first illustration of this approach, we have computed the improved bounds on the price of the call option on the maximum of two assets, with pay-off at date given by , assuming that the price of the zero-strike spread option, with pay-off , is known (these options are indeed often quoted in the market). The marginal laws of and are the same as in example 3, and we further assume that the price of the zero-strike spread option is equal to the corresponding price in a model where and are jointly Gaussian with correlation .

Figure 3 plots the improved bounds as function of the strike for two different values of the correlation , along with the Black-Scholes price and the standard Frechet bounds. Since we now have much less information on the dependence of and than in example 3, the improved bounds are not as narrow as in that example. Still, when the spread option price is close to one of its extreme values, such as, for example in the right graph of figure 3, where we have taken , the improved bounds lead to a considerable narrowing of the price interval. In the numerical example, and were evaluated by numerical integration, their inverses were then computed by bissection, and a further numerical integration was performed to evaluate the bounds.

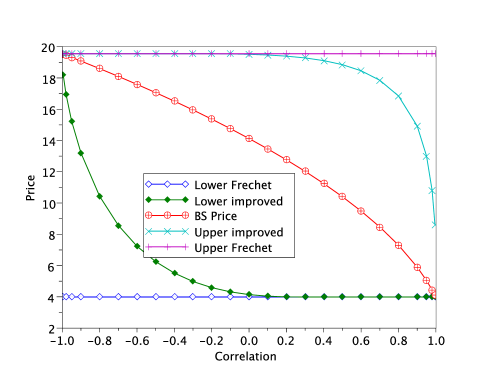

Example 5 (The case when the linear correlation of log-returns is known).

Very often, the option trader does not know the full two-dimensional distribution of and under but has a strong view about the risk-neutral correlation of log-returns

In this case, one can obtain bounds on the prices of two-asset options in the same way as in Example 4, using the function , which is -increasing. Figure 4 plots the bounds on the price of a zero-strike spread option with pay-off when the correlation of log-returns is known, for different correlation values. As we have already observed in Example 4, these bounds are most useful for extreme correlation scenarios, and yield little additional information when the correlation is close to .

Acknowledgement

This research is supported by the Chair Financial Risks of the Risk Foundation sponsored by Société Générale, the Chair Derivatives of the Future sponsored by the Fédération Bancaire Française, and the Chair Finance and Sustainable Development sponsored by EDF and Calyon.

The author would like to thank K. Jean-Alphonse for numerous discussions which helped to shape the paper and for doing preliminary simulations for this research during his internship at Ecole Polytechnique. Thanks are also due to the anonymous referee whose comments helped to improve the presentation of the paper.

References

- [1] G. A. Fredricks and R. B. Nelsen, The Bertino family of copulas, in Distributions with Given Marginals and Statistical Modelling, Kluwer, Dordrecht, 2002, pp. 81–92.

- [2] C. Genest, J. J. Q. Molina, J. A. R. Lallena, and C. Sempi, A characterization of quasi-copulas, Journal of Multivariate Analysis, 69 (1999), pp. 193–205.

- [3] D. Hobson, P. Laurence, and T.-H. Wang, Static-arbitrage optimal subreplicating strategies for basket options, Insurance: Mathematics and Economics, 37 (2005), pp. 553–572.

- [4] , Static-arbitrage upper bounds for the prices of basket options, Quantitative finance, 5 (2005), pp. 329–342.

- [5] R. Kaas, R. J. A. Laeven, and R. B. Nelsen, Worst VaR scenarios with given marginals and measures of association, Insurance: Mathematics and Economics, 44 (2009), pp. 146–158.

- [6] J. F. C. Kingman and S. J. Taylor, Introduction to Measure and Probability, Cambridge University Press, Cambridge, 1966.

- [7] A. Müller and M. Scarsini, Some remarks on the supermodular order, Journal of Multivariate Analysis, 73 (2000).

- [8] R. B. Nelsen, An Introduction to Copulas, Springer, New York, second ed., 2006.

- [9] R. B. Nelsen, J. J. Q. Molina, J. A. R. Lallena, and M. U. Flores, Bounds on bivariate distribution functions with given margins and measures of associations, Comm Statist Theory Methods, 30 (2001), pp. 1155–1162.

- [10] , Best-possible bounds on sets of bivariate distribution functions, Journal of Multivariate Analysis, 90 (2004), pp. 348–358.

- [11] G. Rapuch and T. Roncalli, Some remarks on two-asset options pricing and stochastic dependence of asset prices, tech. report, Groupe de Recherche Operationnelle, Credit Lyonnais, 2001.

- [12] A. H. Tchen, Inequalities for distributions with given margins, Ann. Appl. Probab., 8 (1980), pp. 814–827.

Appendix: the proofs

Proof of Theorem 1..

First, observe that can be obtained from by a simple transformation:

where the bar notation was introduced in section 2. It is therefore sufficient to prove only the statements involving .

Part i.

Let us first check that is a quasi-copula. The boundary conditions follow from the Frechet bounds for . The fact that is increasing in each argument is obvious, and the Lipschitz property follows because for a family of functions which are Lipschitz with constant , we have

which implies that is Lipschitz with the same constant. By proposition 1 and the remark after it, for all , and . Since is the upper bound of over , we have that .

Let us now check the property (6). Take . From the Frechet lower bound for , we get:

For every , using the Lipschitz property of and the fact that it is increasing in each argument, we get that

Therefore, the is attained for .

Part ii.

Let be an increasing set. By adding to this set the points and , we may with no loss of generality simplify the definition of :

Given that is a quasi-copula, we only need to prove property (1).

Since is Lipschitz continuous, for every , one can find a finite increasing set such that . Therefore, it is enough to prove property (1) for a set , where we suppose without loss of generality that and for .

The proof will be done by induction. For , property (1) is straightforward. Assume that it holds for and let , and . To simplify notation, we write , and . For convenience, we subdivide the domain onto four sets and as shown in Figure 5.

To prove that is 2-increasing, we must show that for every rectangle , . However, since is additive over rectangles, it is sufficient to consider only the cases , , and . By construction, on , the function only depends on the coordinate , and therefore, for every rectangle . Similarly, for because is constant on and for because only depends on the coordinate on . It remains to consider the case .

Let . We must show that

We consider separately three cases.

-

–

If and then by induction hypothesis.

-

–

Assume . Then, by the Lipschitz property of , necessarily , and therefore, by the Lipschitz property of , .

-

—

The remaining case, when and , is treated similarly to the second one.

∎

Proof of Theorem 2..

We give the proof for the bound . Since the proof is only based on Proposition 1 which holds in the same form both for copulas and for quasi-copulas, coincides with . The proof for lower bounds and is similar.

Assume . Then, since is increasing and continuous, and therefore, . On the other hand,

By definition of , for all , and therefore for every such that , . Therefore, .

Assume now that and let . Then , (by assumption of the theorem) and since is continuous, there exists such that . Since for all , this proves that . On the other hand, clearly (Frechet bound). ∎

Proof of Proposition 2..

Since is 2-increasing, is increasing in and , and therefore

for some , which implies .

Let be the law of . By Fubini’s theorem and (10) we then get

In the last integral, the integrand is positive and bounded from above by the function , which corresponds to the copula of complete dependence and is integrable by the first part of the proposition. Therefore, the dominated convergence theorem implies that is continuous with respect to pointwise convergence of copulas. ∎