Ergodic approximation of the distribution of a stationary diffusion : rate of convergence

Abstract

We extend to Lipschitz continuous functionals either of the true paths or of the Euler scheme with decreasing step of a wide class of Brownian ergodic diffusions, the Central Limit Theorems formally established for their marginal empirical measure of these processes (which is classical for the diffusions and more recent as concerns their discretization schemes). We illustrate our results by simulations in connection with barrier option pricing.

Keywords: stochastic differential equation; stationary process; steady regime; ergodic diffusion; Central Limit Theorem; Euler scheme.

AMS classification (2000): 60G10, 60J60, 65C05, 65D15, 60F05.

1 Introduction

In a recent paper ([22]), we investigated weighted empirical measures based on some Euler schemes with decreasing step in order to approximate recursively the distribution of a stationary Feller Markov process with invariant distribution . To be precise, let be such an Euler scheme, let denote its sequence of discretization times and let be a sequence of weights. On the one hand we showed under some Lyapunov-type mean-reverting assumptions on the coefficients of the and some conditions on the steps and on the weights that

| (1.1) |

for a broad class of functionals including bounded continuous functionals for the Skorokhod topology. On the other hand, in the marginal case, when , then the procedure converges to . When the Poisson equation related to the infinitesimal generator has a solution, this convergence is ruled by a Central Limit Theorem (): this has been extensively investigated in the literature (for continuous Markov processes, see [4], for the Euler scheme with decreasing step of Brownian diffusions, see [18, 21]). As concerns Lévy driven s, see [24].

Our aim in this paper is to extend some of these rate results to functionals of the path process and its associated Euler scheme with decreasing step, to study the rate of convergence to of and respectively. Here, we choose to assume that is an -valued process solution to

| (1.2) |

where is a -dimensional Brownian motion and and are Lipschitz continuous functions with values in and respectively, where denotes the set of -matrices. Under these assumptions, strong existence and uniqueness hold and is a Markov process whose semi-group is denoted by . We also assume that has a unique invariant distribution and we denote by , the distribution of when stationary.

Let us now focus on the discretization of . We are going to introduce some continuous-time Euler schemes with decreasing step: denoting by the increasing sequence of discretization times starting from , we assume that the step sequence defined by , , is nonincreasing and satisfies

| (1.3) |

First, we introduce the discrete time constant Euler scheme recursively defined at the discretization times by and

| (1.4) |

There are several ways to extend this definition into a continuous time process. The simplest one is the stepwise constant Euler scheme defined by

The stepwise constant Euler scheme is a right continuous left limited process (referred as càdlàg throughout the paper, following the French acronym). This scheme is easy to simulate provided one is able to compute the functions and at a reasonable cost. One could also introduce the linearly interpolated process built on but except the fact that it is a continuous process, it has no specific virtue in term of simulability or convergence rate.

The second possibility to extend the discrete time Euler scheme is what we will call the genuine Euler scheme, denoted from now on by . It is defined by interpolating the two part of the discrete time scheme in its own scale (time, Brownian motion). It is defined by

| (1.5) |

Such an approximation looks more accurate than the former one, especially in a functional setting, as it has been emphasized – in a constant step framework – in the literature on several problems related to the Monte Carlo estimation of ( continuous) functionals of a diffusion (with a finite horizon) (see [7], Chapter 5). This follows from the classical fact that the -convergence rate of this scheme for the sup norm is instead of for its stepwise constant counterpart (where stand for the step). On the other hand, the simulation of a functional of is deeply connected with the simulation of the Brownian bridge so that it is only possible for specific functionals (like running maxima, etc).

A convenient and synthetic form for the genuine Euler scheme is to write it as an Itô process satisfying the following pseudo-diffusion equation

| (1.6) |

where

| (1.7) |

Taking advantage of this notation for the stepwise constant Euler scheme, one can also note that

When necessary, we will adopt the more precise notation for a stepwise constant continuous-time Euler scheme to specify starting at at time with a nonincreasing step sequence satisfying (1.3).

Since we will deal with possibly càdlàg approximations of continuous processes we will introduce the spaces of -valued càdlàg functions on or , , endowed with the topology of the uniform convergence on compact sets, rather than the classical Skorokhod topology (see [6]). In fact, one must keep in mind that if is a continuous function and is a sequence of càdlàg functions, iff (with obvious notations). Furthermore, usual Skorokhod distance (so-called and topologies) on all satisfy

so that any functional which is Lipschitz with respect to such a distance will be Lipschitz continuous with respect to (hence measurable with respect to the Borel -field induced by the Skorokhod topology).

At this stage, we need to introduce further notations related to the long run behaviour of processes (or simply functions). Let denotes the Dirac mass at and denotes the -shift of .

We will see below that our aim is to elucidate the asymptotic - weak behaviour of the empirical measures as goes to infinity, where will be the diffusion itself or one of its (simulatable) Euler time discretizations. This suggests to introduce a time dicretization at times of the above time integral like we did to define the Euler scheme. This leads us to introduce, for any , the following abstract “Euler” empirical means

Then, for a functional defined on and ,

In the following, we will use this sequence of empirical measures for both stepwise constant and genuine Euler schemes. Compared to [22], this means that we assume that the sequence of weights satisfies for every .

Additional notations. will denote the canonical inner product and will denote Euclidean norm of a vector .

Let be an -valued matrix with rows and columns. will denote the transpose of , its trace and . If , one writes for .

2 Main results

2.1 Assumptions and background

We denote by the usual augmentation of by -negligible sets. Since and are Lipschitz continuous functions, Equation (1.2) admits a unique -adapted solution starting from . More generally, for every and every finite -measurable random variable , we can consider , unique strong solution to the :

| (2.8) |

where , , is the -shifted Brownian motion (independent of ). Note that and that can be also defined through the flow of (1.2) by setting

Throughout this paper, we consider a measurable functional . We will denote by the stopped functional defined on by

| (2.9) |

Let us introduce the assumptions on .

: is a bounded and Lipschitz continuous functional.

We set

It is classical background (see [15]) that, under the Lipschitz assumption on and , so that is in turn clearly Lipschitz continuous. Additional regularity properties (like differentiability) can be transfered from provided , and are themselves differentiable enough (see [15]). Furthermore, it follows from its very definition and the Markov property that

: There exists a bounded -function with bounded Lipschitz continuous derivatives such that

where denotes the infinitesimal generator of the diffusion (1.2) defined for every -function on by

REMARK 2.1.

In fact, we need in the sequel that satisfies a for the marginal occupation measures which follows (see [18, 24]) from Assumption combined with a Lyapunov stability assumption (such as introduced below). Namely, we have for a class of regular functions satisfying

| (2.10) |

and as soon as

| (2.11) |

where

and denotes the weak convergence of (real valued) random variables. For details on results in these directions, see [4] for the continuous case and [19, 21, 24] for the decreasing step Euler scheme.

Checking when Assumption is fulfilled is equivalent to solve the Poisson equation on . When has compact support, well-known results about the same equation in a bounded domain lead to Assumption when the diffusion is uniformly elliptic (see [16], Theorems III.1.1 and III.1.2). Such an assumption on is clearly unrealistic. In the general case, in [26], [27] and [28], the problem is solved under some ellipticity conditions in some Sobolev spaces and controls of the growth are given for and its first derivatives. Finally, when the diffusion is an Ornstein-Uhlenbeck process, one can refer to [18] where the problem is solved in .

Let us now introduce the Lyapunov-type stability assumptions on (1.2). Let denote the set of Essentially Quadratic functions, that is -functions such that

Note that since is continuous, attains its positive minimum so that, for any , there exists a real constant such that .

Let us come to the mean-reverting assumption itself. First, for any symmetric matrix , set where denote the eigenvalues of . Let and . We introduce the following mean-reverting assumption with intensity :

There exists a function such that:

where . The function is then called a Lyapunov function for the diffusion .

In Theorem 3 of [19], it is shown that this assumption leads to an marginal weak convergence result to the set of invariant distributions of the diffusion. When and the invariant distribution is unique, this result reads as follows.

PROPOSITION 2.1.

Let and such that holds. Then,

| (2.12) |

Let denote the unique invariant distribution of (1.2). Then, ,

for every continuous function satisfying as .

REMARK 2.2.

In the case , one checks for instance that for a given , Assumption is fulfilled for every if as and

and satisfies for every and .

As concerns the uniqueness of the invariant distribution , we need an additional assumption related to the transition . Namely, we assume that:

: is an invariant distribution for and the unique one for .

Then, is in particular the unique invariant distribution for . In fact, checking uniqueness of the invariant distribution for at a given time is a standard way to establish uniqueness for the whole semi-group . To this end, one may use the following two typical criterions:

Irreducibility based on ellipticity: for every , has a density the Lebesgue measure and , for every .

Asymptotic confluence: for every bounded Lipschitz continuous function , for every compact subset of ,

2.2 Main results

We are now in position to state our main results.

THEOREM 2.1.

Let . Assume and are Lipschitz continuous functions satisfying with an essentially quadratic Lyapunov function and parameters and . Assume furthermore that satisfies the growth assumption:

| (2.13) |

Assume that the uniqueness assumption holds. Finally, assume that the step sequence satisfies (1.3) and

| (2.14) |

Let be a functional satisfying and .

Genuine Euler scheme: Then

| (2.15) |

where

| (2.16) |

and , , (is -adapted).

Stepwise constant Euler scheme: furthermore, if there exists such that

| (2.17) |

then,

| (2.18) |

REMARK 2.3.

By a series of computations, we can obtain other expressions for . In particular, we check in the Appendix A that reads

| (2.19) |

where denotes the expectation under the stationary regime and is the covariance function defined by

| (2.20) |

This expression is not clearly positive but has the advantage to separate the “marginal part” that is represented by the last term from the “functional part” which corresponds to the first two ones.

For instance, when , being bounded and such that where is a bounded -function with bounded derivatives, then and one observes that the first two terms of (2.19) are equal to so that . This means that we retrieve the marginal given by (2.11) (under a slightly more condition on the step sequence which is adapted to the more general functionals we are dealing with, thus, more constraining than that of the original paper; see below for more detailed comments on the steps conditions).

If we now consider defined , satisfying the same assumptions as before, one can straightforwardly deduce from a simple change of variable that the limiting variance is still . In the appendix (Part B), we show that retrieving this limiting variance using (2.16) is possible but requires some non trivial computations. In particular, this calculus emphasizes the intricate nature of the structure of the functional variance.

Given the form of , it seems natural to introduce the (non-simulatable) sequence

which in fact appears naturally as a tool in the proof of the above theorem.

Finally, we also state the Central Limit Theorem for the stochastic process itself. This result can be viewed as a (partial) extension to functionals of Bhattacharya’s established in [4] for a class of ergodic Markov processes.

THEOREM 2.3.

Let . Assume and are Lipschitz continuous functions satisfying with an essentially quadratic Lyapunov function and parameters and . Assume holds. Let be a functional satisfying and . Then, for every ,

| (2.22) |

This means that our approach (averaging decreasing step schemes) induces no loss of weak rate of convergence with respect to that of the empirical mean of the process itself towards its steady regime. If we look at the problem from an algorithmic point of view, the situation becomes quite different. First, we will no longer discuss the recursive aspects as well as the possible storing problems induced by the use of decreasing steps: it has already been done in [22] and we showed that they can easily be encompassed in practice, especially for additive functionals or functions of running extrema (see simulations in Section 7).

Our aim here is to discuss the rate of convergence in terms of complexity. It is clear from its design that the complexity of the algorithm grows linearly with the number of iterations. Thus, if , , then so that the effective rate of convergence as a function of the complexity is essentially proportional to . However, the choice of is constrained by conditions (2.14) or (2.17) that are required for the control of the discretization error. These conditions imply that must be taken greater than 1/2 and lead to an “optimal” rate proportional to for every . This means that we are not able to recover the optimal rate of the marginal case that is proportional to and obtained for (see [19] for details). Indeed, in this functional framework, the weak discretization error is generally smaller and thus, is negligible compared to the long time error under a more constraining step condition (2.14) instead of in the marginal case).

The paper is organized as follows. In Sections 3, 4 and 5, we will focus on the proof of Theorem 2.1 and Theorem 2.3 about the rate of convergence of the two considered occupation measures of the genuine Euler scheme. Then, in Section 6, we will summarize the results of the previous sections and will give the main arguments of the proof of Theorems 2.1 and 2.3. Finally, Section 7 is devoted to numerical tests in a financial framework: the pricing of a barrier option when the underlying asset price dynamics is a stationary stochastic volatility model.

3 Preliminaries

As for the marginal rate of convergence (see [18]), the first idea is to find a good decomposition of the error (see Lemma 3.1). In particular, we have to exhibit a main martingale component. Here, since depends on the trajectory of the process between and , the idea is that the “good” filtration for the main martingale component is . That is why, in the main part of the proof of these theorems, we will introduce and study the sequence of random probabilities defined by:

where is a deterministic real number lying in .

To alleviate the notations, we will denote from now on, and , .

At this stage, the reader can observe on the one hand that for a bounded functional , is -adapted for every and on the other hand that is very close to the random measures of Theorem 2.1(b) by taking and exactly equal to its continuous time counterpart in Theorem 2.2 if one sets . (This fact will be made more precise in Section 6).

Hence, the main step of the proof of the above theorems will be to study the rate of convergence of the sequence to for which the main result is given in Section 6 (see Proposition 6.3). In this way, we state in this section a series of preliminary lemmas. In Lemma 3.1, we decompose the error between this new sequence and the target . In Lemma 3.2, we recall a series of results on the stability of diffusion processes and their genuine Euler scheme in finite horizon. Finally, in Lemma 3.3, we recall and extend results of [19] about the long-time behavior of the marginal Euler scheme.

For every , we define the -measurable random variable by

| (3.23) |

where . Please note that is -measurable.

LEMMA 3.1.

For every satisfying and , we have

where

is a -martingale decomposed as follows : with

and , and are -adapted sequences defined for every , by:

Proof.

With our newly defined notations, we have, for every ,

Now, for every , going twice backward through martingale increments, one checks that

Then, noting that , we introduce the approximation term between the genuine Euler scheme and the true diffusion so that

At this stage the Markov property applied to the original diffusion process yields

since . As a consequence, is a true -martingale increment and

On the other hand , so that

Finally, summing up all these terms yields

since . ∎

REMARK 3.4.

The term sums up the error resulting from the approximation of by its Euler scheme (with decreasing step) . The term is a residual approximation term as well: indeed, if we replace mutatis mutandis by , Itô’s formula implies that

so that the resulting term would be, instead of , .

LEMMA 3.2.

Let and . Assume that and are Lipschitz continuous functions and that there exists such that for a positive real constant . Then,

There exists a real constant , such that for every and every finite -measurable random vector

There exists a real constant such that, for every ,

There exists a real constant such that, for every ,

Let . Then, there exists such that, for every ,

Proof.

The proofs follow the lines of their classical counterpart for the constant step Euler scheme of a diffusion (see [7], Theorem B.1.4 p.276 and the remark that follows). In particular, as concerns , the only thing to be checked is that is the Euler scheme with decreasing step of where the step sequence is defined by

| (3.24) |

∎

LEMMA 3.3.

Let and such that holds and assume that and are Lipschitz continuous functions.

Let be a nonincreasing function such that . Let be a nonincreasing sequence of positive numbers such that . Then, ,

| (3.25) |

We have:

| (3.26) |

and

| (3.27) |

In particular, the families of empirical measures and are tight.

Assume . Then, , for every continuous function such that as ,

Proof.

First, note that

where . Consequently, the first statement is simply a rewriting with continuous time notations of Lemma 4 of [19]. As concerns the second one, using Lemma 3.2 with and the exponent p+a-1 yields for every and every :

As a consequence, considering the integrable, nonincreasing, nonnegative function leads to

owing to the previous statement.

and (3.26) follows.

Let us deal now with (3.27). Given (3.26), it is clear that (3.27) is equivalent to showing that for an increasing sequence such that , and ,

| (3.28) |

Setting for every , this suggests to introduce the martingale defined by and for every ,

where Set so that . Using that and the elementary inequality for , ,

where and is the nonincreasing function defined by on . Thus, we deduce from (3.25) that,

It follows from the Chow Theorem (see [10]) that converges toward a finite random variable which in turn implies by the Kronecker Lemma that

Then, (3.28) will follow from

| (3.29) |

In order to prove (3.29), we need to inspect two cases for :

Case . We decompose the increment into elementary increments, namely

Owing to the second order Taylor formula, we have for every :

Note that a similar development holds for . Now, one checks that the fact that implies that and that is a Lipschitz continuous function with Lipschitz constant . Consequently

where we used in the second inequality the standard control . Then, summing over and using that owing to , we deduce that

where . By , we can use Lemma 3.2 with and to obtain for every ,

| (3.30) |

Applying successively the above inequality with and and using the chain rule for conditional expectations show that,

for some real constant . As a consequence,

Let (note that since and ). Hence and by Lemma 3.2 and (3.25), one checks that

by the first part of the lemma. Then, one derives using a martingale argument based on (3.26), the Chow Theorem and the Kronecker Lemma that

Case . In that case, we just use that is bounded so that we just have to use (3.30) with (since ). This concludes the proof of .

The fact that , is but the statement of Proposition 2.1 with continuous time notations. Now, let us show that , for every continuous function such that ,

| (3.31) |

First, taking advantage of (3.27), standard weak convergence arguments based on uniform integrability show that it is enough to prove that, , (3.31) holds for every bounded continuous function . Then, using that weak convergence on can be characterized along a countable subset of Lipschitz bounded continuous functions , the problem amounts to showing that for every Lipschitz bounded continuous function

| (3.32) |

Owing to , our strategy here will be to show that almost any limiting distribution of the empirical measures is invariant since it leaves the transition operator invariant. As a first step, we first derive from a standard martingale argument that

| (3.33) |

Now, we remark that

| (3.34) | |||||

| (3.35) |

where denotes the genuine Euler scheme starting from with step sequence defined by (3.24). Since is bounded Lipschitz,

where in the second inequality, we used Lemma 3.2 with . Thus, since , it follows from (3.34) that, for every ,

Then, it follows from (3.33) and from the a.s. tightness of that, ,

Now, since and are bounded continuous, it follows that, , for every weak limit of the tight sequence , for every . This implies that is an invariant distribution for and one concludes the proof by . ∎

4 Rate of convergence for the martingale component

This section is devoted to the study of the rate of convergence of the martingale defined in Lemma 3.1. The main result of this section is Proposition 4.2 where we obtain a for this martingale. On the way to this result, the main difficulty is to study the asymptotic behavior of the previsible bracket of this sum of four dependent martingales. First, we decompose the martingale increment as follows:

where is a -adapted sequence defined for every by:

and . Keep in mind that . In the following lemma, we set

where, following the notation introduced in (2.8), denotes the unique solution to starting from .

LEMMA 4.4.

Assume and are Lipschitz continuous functions satisfying with an essentially quadratic Lyapunov function and parameters and . Let denote a functional satisfying and . Then,

| (4.36) |

and

| (4.37) |

where with

| and |

Proof.

We consider the -martingale defined by:

Let . Using Jensen’s inequality, we have

Using successively conditional Burkhölder-Davis-Gundy and Jensen inequalities and , we have

| (4.38) | |||||

Now, since is bounded and ,

| (4.39) | |||||

where By Lemma 3.2(i) applied with and with . it follows that for every ,

| (4.40) |

Then, we deduce from Lemma 3.3 applied with that

since . Finally, using the Chow theorem, it follows that is an convergent martingale and the result follows from the Kronecker lemma.

(ii) Set . We have so that

Thus, it is enough to show that

| (4.41) | ||||

| and | (4.42) |

Let us focus on (4.41). Set . Using conditional Hölder and Jensen inequalities, we obtain:

| (4.43) | ||||

| (4.44) |

Let us inspect successively the three terms involved in (4.44).

Now set . Still using Lemma 3.2, we show (like previously for (4.40)) that, for every and ,

| (4.45) |

On the other hand since and are bounded Lipschitz continuous functions,

Then, owing to the Markov property,

where denotes the Euler scheme of with step sequence as defined by (3.24). Now, using that for every ,

it follows from Lemma 3.2 that

| (4.46) |

and by Lemma 3.2,

| (4.47) |

so that, for every ,

| (4.48) |

Finally, we have

On the one hand and being both Lipschitz continuous and being bounded, we have for every ,

| (4.49) |

As a consequence, using Schwarz inequality and Assumption , it follows that

Owing to Lemma 3.2, it follows that

and by (4.46) and (4.47) that,

| (4.50) |

where we used in the last inequality that . On the other hand since

we deduce likewise from and Lemma 3.2 that

| (4.51) |

Thus, plugging the inequalities obtained in (4.45), (4.48), (4.50) and (4.51) into (4.44) and (4.43) yields for every ,

Since as and , it follows that , for every ,

Since , there exists such that . Hence, it follows from (3.27), that

Then, we deduce by a standard uniform integrability argument that

This completes the proof of (4.41). The proof of (4.42) is similar and the details are left to the reader. ∎

LEMMA 4.5.

Assume that and are Lipschitz continuous functions.

For every ,

| (4.52) |

with , .

If holds, is a continuous function on . As a consequence, if moreover , and hold for and ,

| (4.53) |

Proof.

Let be a bounded (or nonnegative) Borel functional defined on . Since pathwise uniqueness holds for (1.2) ( and being Lipschitz continuous), there exists a measurable function such that , for every , (see [13], Corollary 3.23). Then, using that is -measurable, that the Brownian motion is independent of and that, , one derives that

Using again the representation with function (or the fact that strong uniqueness implies weak uniqueness), one observes that the spatial process has the same distribution as where is the flow of (1.2) at tme . Consequently,

Similar arguments show that

Thus, it follows from the definition of and that

where

Note that the second expression clearly defines a functional on the canonical space. Now,

where . The result follows using that , that is a -martingale and that .

Let and set

Let be a convergent sequence of to . Owing to the standard identity and Schwarz’s inequality,

Let . Since and are bounded,

owing to Lemma 3.2. Thus,

and it follows easily that will be continuous if both () and are continuous. On the one hand and being Lipschitz continuous, elementary computations show that for ,

Now, since and are Lipschitz continuous functions, for every , there exists a real constant such that (see [15] or [29]),

The continuity of , , follows. On the other hand using (4.49),

This concludes the proof. ∎

PROPOSITION 4.2.

Suppose that assumptions of Theorem 2.1(a) hold. Then,

| (4.54) |

Proof.

By Lemma 4.5,

Then, we only need to prove a Lindeberg type condition (see [10], Corollary 3.1). To be precise, we will show that for every

First, a martingale argument similar to that of the beginning of the proof of Lemma 3.1, yields that

Second, using conditional Hölder and Chebyschev inequalities, we have for every

and thanks to (4.38) and (4.39), we deduce that

Thus, taking so that , we have for every , ,

by applying Lemma 3.3. ∎

5 Study of , and

In this section, we focus on the remainder terms of the decomposition of the error (see Lemma 3.1). Owing to Proposition 4.2, it is now enough to prove that

where denotes the convergence in probability. For , these properties are stated in Lemma 5.6 and 5.7. For , the result is obvious.

LEMMA 5.6.

Assume and are Lipschitz continuous functions such that with parameters , , and an essentially quadratic Lyapunov function satisfying . Let be Lipschitz continuous. If the step condition (2.14) holds then

Proof. Since is Lipschitz continuous, it follows from Lemma 3.2 (applied with ) that, for every ,

Consequently,

where in the second inequality, we used Lemma 3.2. Since and , we deduce that

| (5.55) |

Thus, owing to the Kronecker Lemma,

with

Now, as is nonincreasing, it follows from Lemma 3.3 that it is now enough to show that . We have

and

Using that the step sequence is nonincreasing, we deduce from Condition (2.14) that

| (5.56) |

LEMMA 5.7.

Assume and are Lipschitz continuous functions satisfying with an essentially quadratic Lyapunov function and parameters and . Let be a functional satisfying and . If the step condition (2.14) holds, then

Proof.

Owing to the Itô formula, we have:

Then, it follows from the definition of that

Since is bounded,

Then, it is now enough to show that

| (5.57) |

and that,

| (5.58) |

First, using that is a bounded -function with bounded Lipschitz continuous derivatives, that and are Lipschitz continuous functions, one checks that

Then, using that

it follows from Lemma 3.2 applied with , and , that,

By Asssumption , we deduce that

Now, since , , and by (5.56), we have

Then (5.57) follows from Lemma 3.3 and the Kronecker Lemma like in the proof of Lemma 5.6.

6 Proof of the main theorems

The first step for the proof of these theorems is now to state our main result about the sequence studied in the two previous sections:

PROPOSITION 6.3.

Proof.

Proof of Theorems 2.1 and 2.2. First, let denote a sequence of positive real numbers such that . Set . Since is a bounded functional, we have:

Thus, Theorem 2.2 follows taking . For Theorem 2.1(a), setting , and , we obtain that

Now,

and the fact that implies that,

By (2.14) and the Kronecker Lemma,

Applying this identity with yields the result.

Proof of Theorem 2.1. Owing to Theorem 2.1, it is now enough to show that

Since is a Lipschitz bounded functional, it follows from the definition of the previous occupation measures that

By Lemma 3.2 and Jensen’s inequality, for every ,

Thus, we deduce that

Let be a positive number such that (2.17) holds. Taking such that , we deduce from (2.17) and Lemma 3.3 that

We again deduce the result from Kronecker’s Lemma.

Proof of Theorem 2.3. We only give the main ideas of the proof of this result about the “perfect Euler scheme” , that is naturally simpler than that of the discretized processes. First, the reader can check that setting

one obtains a similar decomposition as that of Lemma 3.1 replacing by and by defined by

The main difference in this decomposition is that the term corresponding to is null. Then, since the assumption is only needed in the proof of the result about (see Lemma 5.6), we deduce that it is not necessary here. Then, the sequel of the proof works since the statements of Lemma 3.3 still hold if one replaces by . To be precise, the first statements of and can be directly derived from [25] (Chapter 1) and the second ones from an adaptation of the proof of this lemma.

7 Numerical Test on Barrier Options in the Heston model

As shown in [22], our algorithm can be successfully implemented for pricing path-dependent options in stochastic volatility models when the volatility process evolves in its stationary regime. Furthermore, such stationary versions of stochastic volatility models are more performing to take into account the behaviour of implicit volatility for short maturities. Then, even if the assumptions of our main theorems are usually not satisfied for the functionals involved in this context, we choose in this section to illustrate them by such an example. To be precise, we test numerically the asymptotic normality obtained in the main results on the computation of several Barrier options in a Heston stationary stochastic volatility model. The dynamics of the traded asset price process is given by:

where denotes the interest rate, is a standard two-dimensional Brownian motion, and , and are some nonnegative numbers. This model was introduced by Heston ([11]). The equation for has a unique (strong) pathwise continuous solution living in . If moreover, then, is a positive process (see [17]). In this case, the volatility process has a unique invariant probability with gamma distribution, namely with and . Thus, we assume that evolves in its stationary regime, that

Under this assumption, we showed in [22] that any option premium can be expressed as the expectation of a functional of a two-dimensional stationary stochastic process. Let us recall the idea: we will write as a functional of a stationary process. Elementary Itô calculus yields

| (7.61) |

Introducing the -dimensional ,

| (7.62) |

and using the fact that

we deduce that we can construct a (continuous) map from to such that . Now, we have built so that has a stationary regime. Denoting by the invariant distribution of , we obtain that

For further details we refer to [22]. Here, we are interested with an Up-and-Out barrier option whose discounted payoff is given by:

where . We now specify the discretization. First, the genuine Euler scheme of the so-called Heston volatility process (also known as the Cox-Ingersoll-Ross process) cannot be implemented since it does note preserve the positivity. Thus, we must replace it by a specific discretization scheme: we denote by the stepwise constant Euler scheme built as follows:

Note that convergence properties of this scheme have been studied in a constant step framework in [5] (see also [8], [1], and [2] for other specific discretization schemes).

Second, we denote by the continuous discretization scheme of defined by and

| (7.63) |

Note that we do not need to introduce the Euler of since its use is nothing but a theoretical way to justify why an algorithm for the approximation of the stationary regime can be adapted to this context. Finally, in order to compute the supremum of , let us recall the principle of the so-called Brownian Bridge method (transposed to this framework). Set

and let denote the Brownian Bridge on defined by , . For every , we have

Using the independence and the Gaussian properties of the Brownian motion, one deduces that, for every , the processes , are conditionally independent given the -field and that

where denotes a standard Brownian motion. Then, using the symmetry principle, one can show that, for every , for every and positive and

It follows that given , can be simulated by the method of inversion of the distribution function.

Let us now detail the algorithm.

From to . At each step between and , simulate recursively, and . Then, use the Brownian Bridge method to simulate given . Compute recursively . At time , compute

From to If , replace by . Store and . As in Step 1, from to , compute recursively , , and the maximum of . Then, at time ,

For the following choices of parameters,

| (7.64) |

we want now to obtain an approximation of the distribution of the (asymptotically normal) normalized error

First, we need to have an accurate approximation of the (risk-neutral) price. In this way, we choose to combine a very long simulation with a variance reduction method taking the corresponding Barrier option in the Black-Scholes model as a control variable. Indeed, on the one hand, it is well-known that the price of such Barrier option has a closed form in the Black-Scholes model (based on the Black-Scholes formula for European options) and on the other hand, this price can be approximated using the algorithm described above by simply replacing the stochastic volatility by a constant volatility denoted by . Note that the natural choice for is the long term volatility which is the mean of the stationary volatility process as well. Then, denoting by the genuine Euler discretization scheme of the Black-Scholes model (especially with the same trajectory for ) with constant volatility , we approximate the price of the option by

where denotes the (explicit) price of the up-and-out barrier option in the Black-Scholes model. Doing so with a simulation size , we get the following accurate approximation of the premium:

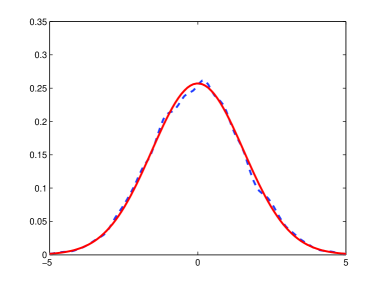

Then, setting , we proceed independent Monte Carlo simulations of . We denote by the empirical variance of the sample (which corresponds to an estimation of ). In Figure 1 are depicted the density of a centered Gaussian random variable with variance and the empirical density (smoothed by a convolution with a Gaussian kernel) defined by:

As a conclusion, this numerical experiment first illustrates that the occurs at a reasonable range (for numerical purpose) and also suggests that a local version holds true as well (“convergence of the density”). Another extension of our result could be, in the spirit of Bhattacharia’s result in [4] to establish an invariance principle of Donsker type.

Appendix

A. Proof of identity (2.19).

We have to deduce (2.19) from (2.16). First, we have (dropping x in ):

since one easily checks that . It follows that

Second, using the Markov property (or the fact that ) and the stationarity of the process, one observes that and have the same distribution under . In particular,

Since and , we obtain that

All we have to do now is to check that the three above terms correspond respectively to the three parts of (2.19). First, by Fubini’s Theorem,

Owing to the stationarity of the process under , we have

where is defined by (2.20). This yields

Second, setting

| (7.65) |

we have

Now, the fact that implies that we can make use of the stationarity property to obtain for every ,

With similar arguments, one checks that for every ,

It follows that

owing to the stationarity of the process. This concludes the proof.

B. Computation of when .

As mentioned in (2.3), when , the for marginal functions combined with a change of variable yields . Let us check this formula starting from (2.16). Following the notation introduced in (7.65), we have

In this case, and using that and commute, one checks that . This implies that . For the sake of simplicity we may assume w.l.g. . Then, on the one hand

On the other hand

so that

References

- [1] Alfonsi A. (2005). On the discretization schemes for the CIR (and Bessel squared) processes, Monte Carlo Methods Appl, 11, 355–384. 2186814

- [2] Andersen, Leif B. G., Efficient Simulation of the Heston Stochastic Volatility Model (January 23, 2007). Available at SSRN: http://ssrn.com/abstract=946405

- [3] Basak G.K., Bhattacharya R.N. (1992). Stability in Distribution for a Class of Singular Diffusions, Ann. Probab., 20(1):312–321.

- [4] Bhattacharya R.N. (1982). On the functional Central Limit Theorem and the law of the iterated logarithm for Markov processes, Z. Wahrsch. Verw. Gebiete., 60(2):185–201.

- [5] Berkaoui A., Bossy M., Diop A. (2008). Euler scheme for SDE’s with non-Lipschitz diffusion coefficient: strong convergence, ESAIM Probab. Stat., 12, 1–11. 2367990

- [6] Billingsley P. (1968) Convergence of Probability Measures, Wiley. 02333096

- [7] Bouleau N., Lépingle D. (1994). Numerical methods for stochastic processes, John Wiley & Sons, Inc., New York, 359 p. 1274043

- [8] Deelstra G., Delbaen F. (1998). Convergence of Discretized Stochastic (Interest Rate) Processes with Stochastic Drift Term, Appl. Stochastic Models Data Anal., 14, 77-84. 1641781

- [9] Duflo M. (1997). Random Iterative Models, Springer Verlag, Berlin. 1485774

- [10] Hall P., Heyde C. (1980). Martingale Limit Theory and its Application, Academic Press.

- [11] Heston S. (1993). A closed-form solution for options with stochastic volatility with applications to bond and currency options, Review of Financial Studies, 6:327-343.

- [12] Jacod J., Shiryaev A. N. (1987). Limit Theorems for Stochastic Processes, Springer. 1943877

- [13] Karatzas I., Shreve S. (1991), Brownian Motion and Stochastic Calculus, Springer. 1121940

- [14] Kloeden P., Platen E. (1992) Numerical solution of stochastic differential equations. Applications of Mathematics (New York), 23. Springer-Verlag, Berlin, 1992. 632 pp. 3-540-54062-8

- [15] Kunita H. (1982). Stochastic differential equations and stochastic flows of diffeomorphisms. Cours d’école d’été de Saint-Flour, LN-1097, Springer-Verlag, 1982.

- [16] Ladyzhenskaya, O. A., Ural’tseva, N. N. (1968). Linear and quasilinear elliptic equations. Academic Press, New York-London:495 p. 244627

- [17] Lamberton D. and Lapeyre B. (1996). Introduction to Stochastic Calculus Applied to Finance, Chapman and Hall/CRC, New York. 1422250

- [18] Lamberton D. and Pagès G. (2002). Recursive computation of the invariant distribution of a diffusion. Bernoulli 8:367-405. 1913112

- [19] Lamberton D. and Pagès G. (2003). Recursive computation of the invariant distribution of a diffusion: The case of a weakly mean reverting drift. Stoch. Dynamics 4:435-451. 2030742

- [20] Lemaire V. (2007). An adaptive scheme for the approximation of dissipative systems. Stochastic Process. Appl. 117:1491-1518. 2353037

- [21] Lemaire V. (2005). Estimation numérique de la mesure invariante d’un processus de diffusion, PhD Thesis, Université de Marne-La Vallée.

- [22] Pagès G., Panloup F. (2009). Approximation of the distribution of a stationary Markov process with application to option pricing. Bernoulli, 15(1):146–177. 2546802

- [23] Panloup F. (2008). Recursive computation of the invariant measure of a SDE driven by a Lévy process. Ann. Appl. Probab. 18:379-426. 2398761

- [24] Panloup F. (2008). Computation of the invariant measure of a Lévy driven SDE: Rate of convergence, Stochastic Process. Appl., 118(8):1351–1384. 2427043

- [25] Panloup F. (2006). Approximation du régime stationnaire d’une EDS avec sauts, PhD Thesis, Université Paris VI.

- [26] Pardoux E., Veretennikov A. (2001). On Poisson equation and diffusion approximation I, Ann. Probab., 29(3):1061–1085. 1872736

- [27] Pardoux E., Veretennikov A. (2003). On Poisson equation and diffusion appoximation II, Ann. Probab, 31(3):1166–1192. 1988467

- [28] Pardoux E., Veretennikov A. (2006). On the Poisson equation and diffusion approximation III, Ann. Probab, 33(3):1111–1133. 2135314

- [29] Protter P. (2005) Stochastic integration and differential equations. Second edition. Version 2.1. Corrected third printing. Stochastic Modelling and Applied Probability, 21. Springer-Verlag, Berlin:419 pp. 3-540-00313-4

- [30] Talay D. (1990). Second order discretization schemes of stochastic differential systems for the computation of the invariant law. Stoch. Stoch. Rep., 29(1):13-36.